honors college version of thesisthesis.honors.olemiss.edu/635/1/honors college... · airline...

TRANSCRIPT

DeltaAirLines:AFinancialAnalysisandCorrespondingRecommendationsfor

DeltaAirLines,Inc.

by

EmilyMarieBush

AthesissubmittedtothefacultyofTheUniversityofMississippiinpartialfulfillmentof

therequirementsoftheSallyMcDonnellBarksdaleHonorsCollege.

Oxford

May2016

Approvedby:

___________________________________Advisor:ProfessorVictoriaDickinson

ii

©2016

EmilyBush

ALLRIGHTSRESERVED

iii

ABSTRACT

DeltaAirLines:AFinancialAnalysisandCorrespondingRecommendationsfor

DeltaAirLines,Inc.

ThisalternativethesisprojectisafinancialanalysisofDeltaAirLines,Inc.

Utilizingthe10-KFinancialStatementsfrom2009to2013,alongwithsomecorrelating

outsideresources,afullbusinessandfinancialanalysiswascompleted.Startingwiththe

businessbackgroundandoperations,andthenworkingintoanalysisoftheFinancial

Statements,correspondingrecommendationswerecreatedfortax,auditandadvisory

planningstrategies..Thebulkoftheanalysisutilizedthe10-KdataprovidedbytheSEC,

onlyusingminimalotherresourcesforbackgroundresearch.

TheresearchfoundthatsincefilingChapter11bankruptcyDeltaAirLineshas

improvedsubstantially.Delta’slargestissuestoovercomeinthecomingyearsare

findingwaystocontinuegrowingwhilekeepingcostslow.Thecompanyhasalreadyhad

tofileforbankruptcyonceinthelastdecade;theydonotneedarepeat.Lookingatthe

currentfinancials,Deltaisontherighttrackforsuccessbutneedstoconsider

implementingstrongcontrolsforproperty,plant,equipment,andinventory.The

companyalsoneedstoensurethattaxesremainlow,seeingthatrightnowtheyhavea

largetaxbenefitduetocarryforwardlossesandothertaxcredits.Futuretaxexpenses

couldcauseanegativeimpactonnetincome,sothecompanyshouldseektax-planning

strategiestoensurefuturedeductions.Finallythecompanymaywanttoconsider

utilizingbettermethodsforflighttimesandonlinepayments,andincreasingthe

capacityoftheirfuelsegment.Theserecommendationsandcorrespondingfinancial

analysisisoutlinedthroughoutthecontentsofthepaper.

DeltaAirLines:AFinancialAnalysisand

CorrespondingRecommendationsfor

DeltaAirLines,Inc.

EmilyBush

Spring2015

DeltaAirLines

1

PREFACE

The Accountancy Alternative Thesis Course, ACCY 420, has allowedme to not

onlycompletemythesis,butalsolearnmoreaboutaccountingthaneverachievableina

classicalclassroomsetting.Firstsemester,thecoursegavestudentstheabilitytomeet

withvariousfirms,corporationsandpersonnelintheaccountingbusinessworldtogain

adeeperunderstandingofthethreemainservicelines,therecruitingprocess,andlife

asanaccountant.Thefirstsemesterpreppedmyclassmatesandmyselfforthemonths

andyearstocomeinpublicorevenprivateaccounting,andImostdefinitelyfeelIhave

the“insidescoop”comparedtosomeofmypeersnotinthecourse.

Secondsemestertookadifferentroutewiththefocuslyinginthecompletionof

thethesis.Theassignmentwastoselectanypubliclytraded,USdomiciledcompanyand

completeanindepthanalysisofitsbusinessfunctions,financialstatementsandthento

suggestcorrespondingrecommendationsbasedofftheanalysis.FormythesisIchose

Delta Air Lines because recreational companies are heavily concentrated in my

internship city of Phoenix, Arizona. Companies such asMesaAir Lines, Starwood and

professional sports teams are all key clients in that region. Choosing a company that

providessimilartravelandrecreationalservicesheavilyparalleledandpreparedmefor

theinternshipIwouldcompletethefollowingyear.

DeltaAirLines

2

Overall, the skills learned while completing this paper will translate into my

professional career. Before this course, I had no clue how to read actual financial

statements and only knew the premises of financial accounting. By completing this

course,Ihavegainedanindepthknowledgehowtoutilizecompany’s10-Ks,andhowto

completefinancial,auditandtaxworkforareallifecorporationratherthanjustabook

example.Thevalueofthecourseisbeyondwhatcanbedescribed,butthebenefitsare

suretopresentthemselvesinthecomingyears.

DeltaAirLines

3

**AnysectionsnotcitedcanbeassumedtohaveusedtheDeltaAirLines’10-KFinancial

StatementsandFootnotesfortheyears2009-2013locatedonSecuritiesandExchanges

Commission’sWebsite

DeltaAirLines

4

TABLEOFCONTENTS

Chapter1

CompanyHistory..…………………….……………………………………………………………………….….Page8

CompanyOperations..…………………………………………….……………………………..……..…….Page25

ValueChain..………………………………………………………………………………………………………..Page27

BusinessProcessesDiagram..………………..………………………………………………..…….…….Page28

BoardofDirectors..………………………………………..……………………………………..…………….Page29

Chapter2

MissionStatement..……………………………………………………………….……………………….….Page33

Goals..…………………………………………………………………………………..…………………………….Page34

BusinessStrategy..……………………………………………………………………………………………….Page37

AssessingDemandforProducts..…………………………………………………………………..…….Page38

AssessingSupplyofInputs..……………………………………………………………………………..….Page39

Competitors…………………………………………………………………………………………………..…….Page42

GeopoliticalRisks..…..………………………………………………………………..………………….…….Page44

Porter’sCompetitiveForces..……………….…………………………………………….…………...….Page46

SWOTAnalysis..……………………………………………………………………………………………….….Page47

DeltaAirLines

5

Chapter3

AssetComposition..………………………………………………………………………………………….….Page48

CompanyFinancing..……………………………………………………………..………………….……..….Page51

CashFlows..…………………………………………………………………………………………………….….Page57

Liquidity,SolvencyandEarningsperShare..…………………………………………………….….Page58

Chapter4

AccountsReceivable..…………………………………………………………………………..………….….Page61

Inventory..……………………………………………………………………………………………………………Page64

Property,PlantandEquipment..………………………………….…..…………………..………….….Page69

Chapter5

IntercorporateInvestments..…………………………….…………………………….……………...….Page73

Restructuring..……………………………………….……………………………………………….……….….Page79

ForeignCurrency..……………………………………………………….……………………………….….….Page82

ReturningWealthtoShareholders..……………………….………………………….…………….….Page86

Pensions..…………………………………………………………………………………………….…………..….Page87

DeltaAirLines

6

Chapter6

OperatingvNon-Operating..…………………………………………………………………………….….Page89

FinancialStatementAnalysis..……………………………..….……………………………………….….Page92

RNOADisaggregationAnalysis..……………………………………………………………………….….Page98

DecompositionofNon-OperatingReturn..……………………………..………….………….….Page102

Chapter7

LaggingMacroeconomicIndicators..…………………………………..……….…………………….Page106

LeadingMacroeconomicIndicators..……………………………….…………………………….….Page111

RevenueRecognitionPrinciples..………………………………………………….………….…….….Page115

Analysts’Forecasts..……………………………………………………..……………….……………….….Page117

EarningsManagement..……….……………………………………………………….……………….….Page119

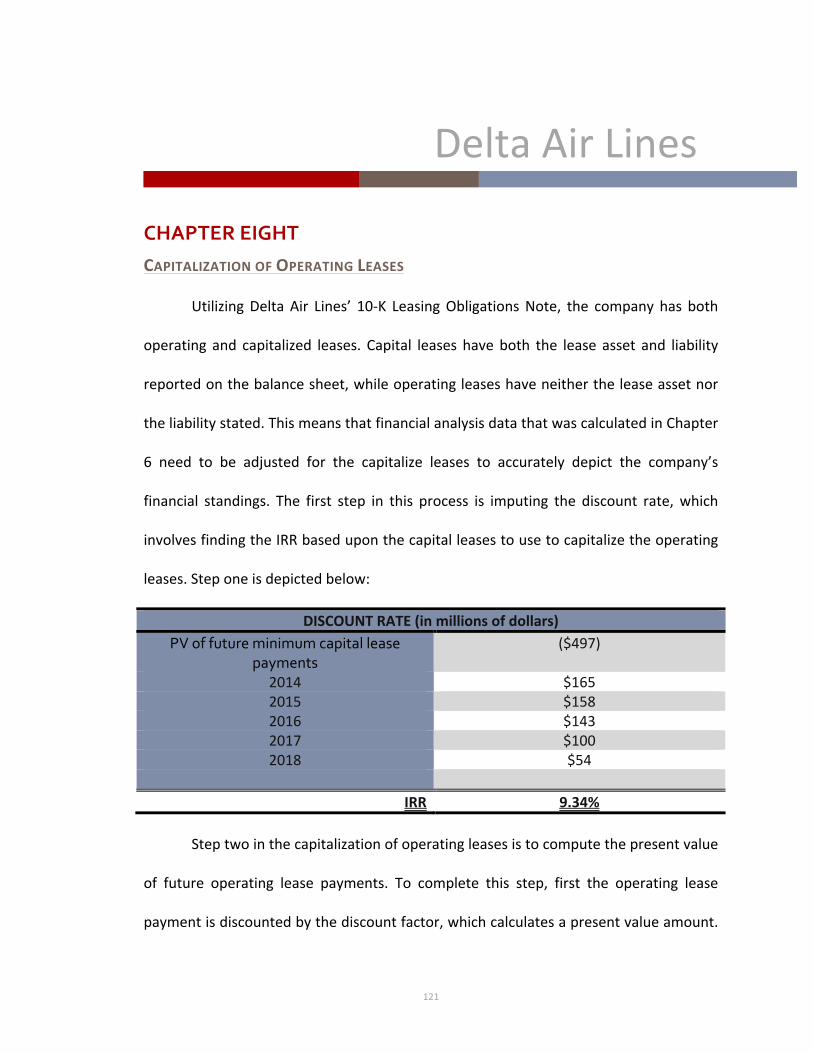

Chapter8

CapitalizationofOperatingLeases..……………………………………………………………….….Page121

Weighted-AverageCostofCapital..…………………………….………………………………….….Page124

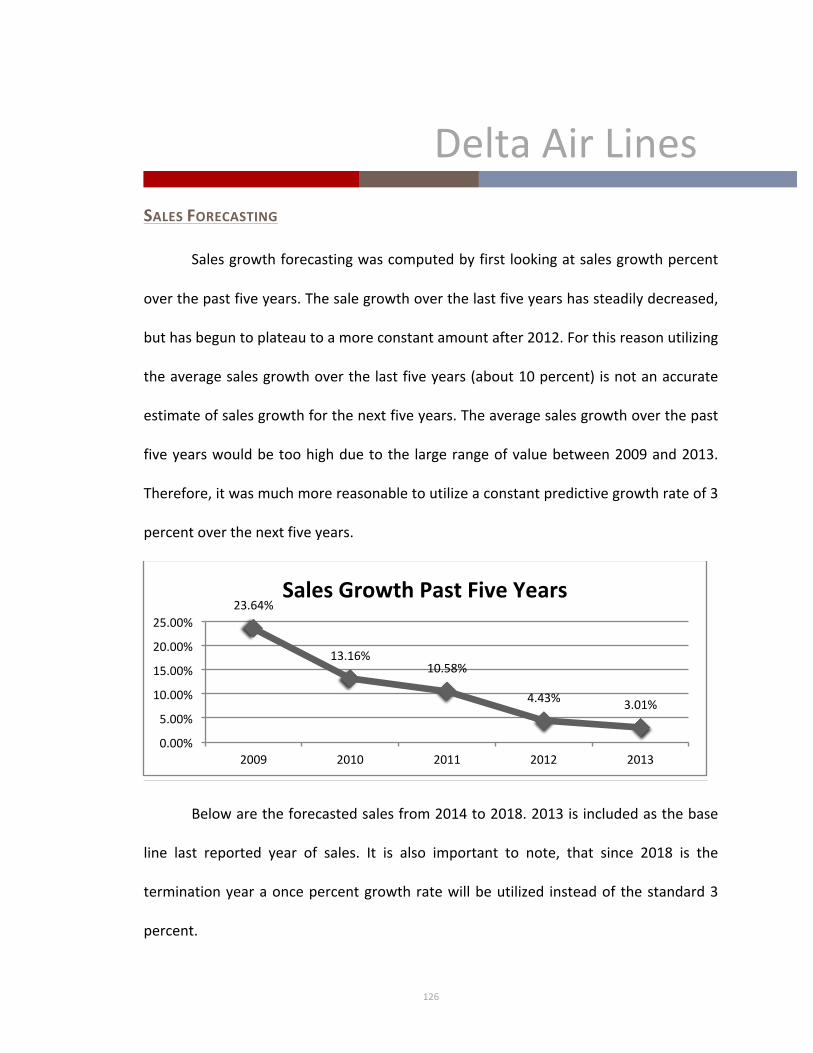

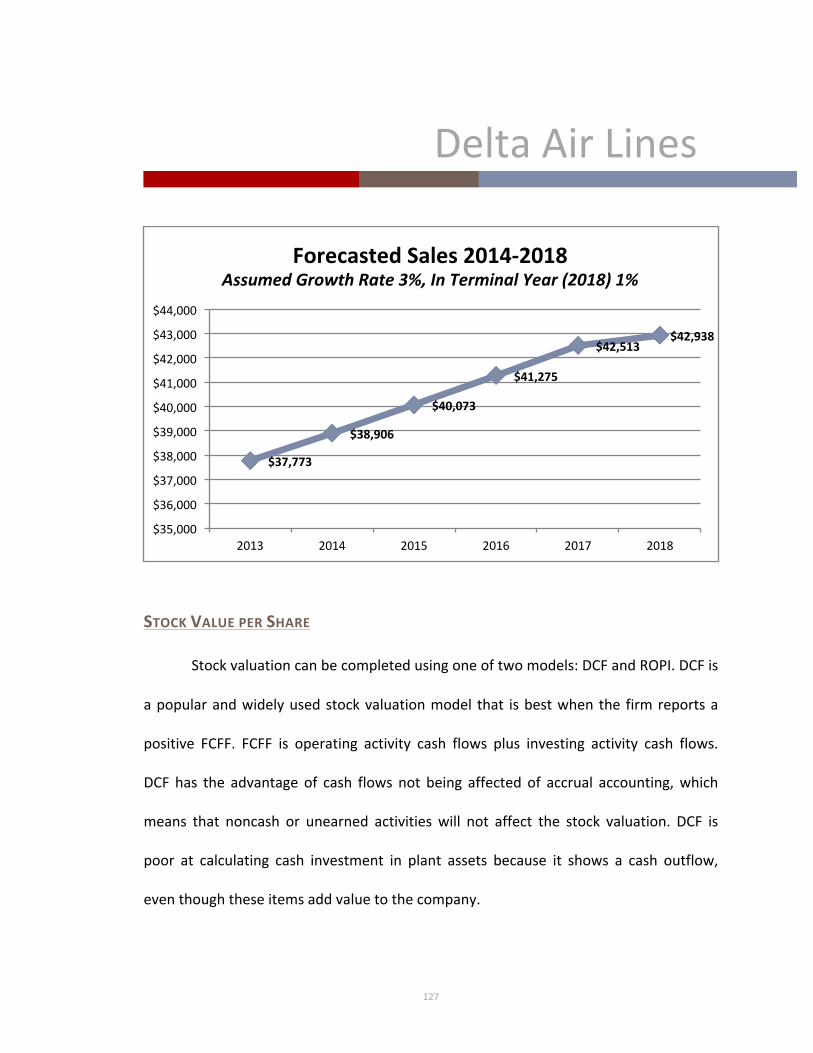

SalesForecasting..…………………..………………………………….………………………………….….Page126

StockValueperShare..…………………………………………………………….…………………….….Page127

DeltaAirLines

7

Chapter9

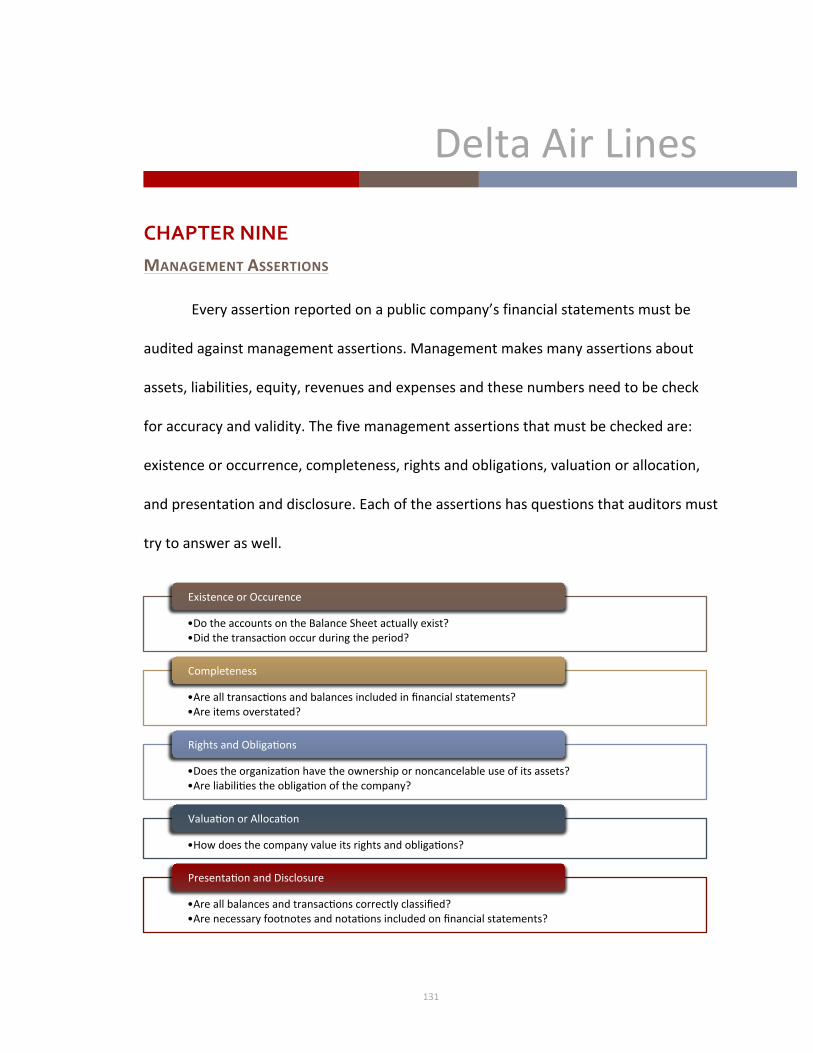

ManagementAssertions..……………………………………………………………..……………….….Page131

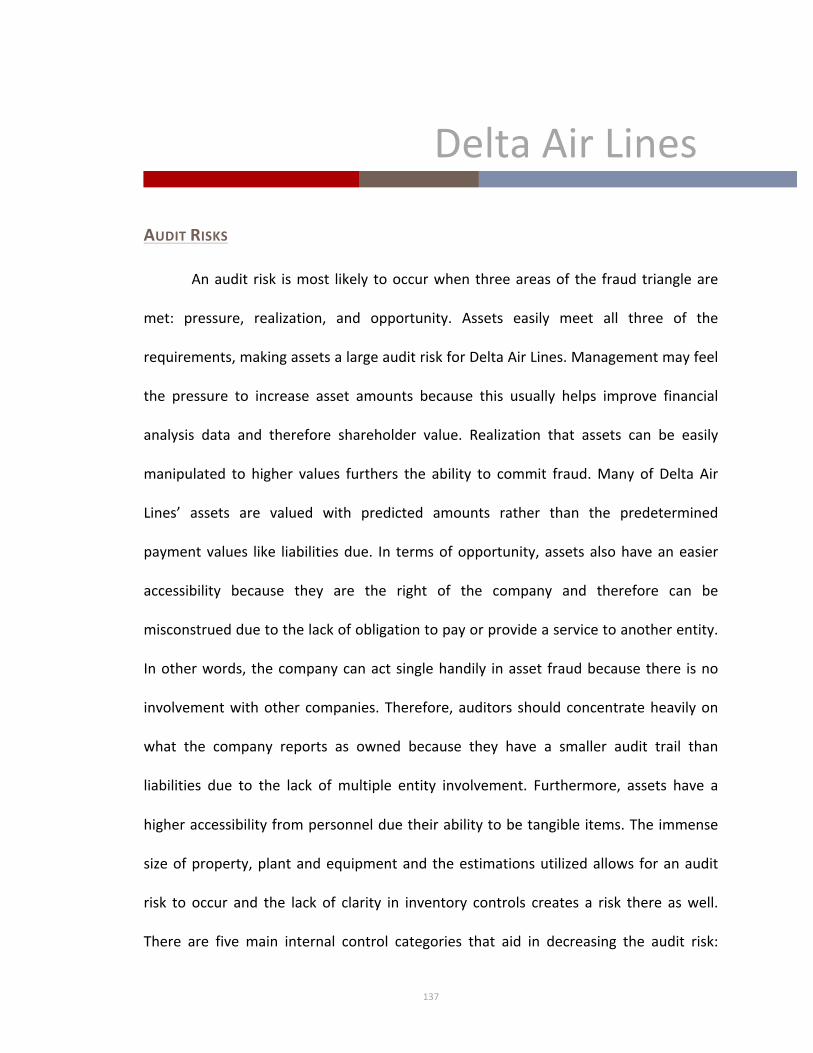

AuditRisks..…………………………………………………………………………….…………………….….Page137

ForeignTaxRates..…………………………………………………….………………………………….….Page141

TaxCredits..…………………………..………………….…………………………………….…………….….Page142

TaxRecommendation..…………………………………..……………………………….…………….….Page143

Chapter10

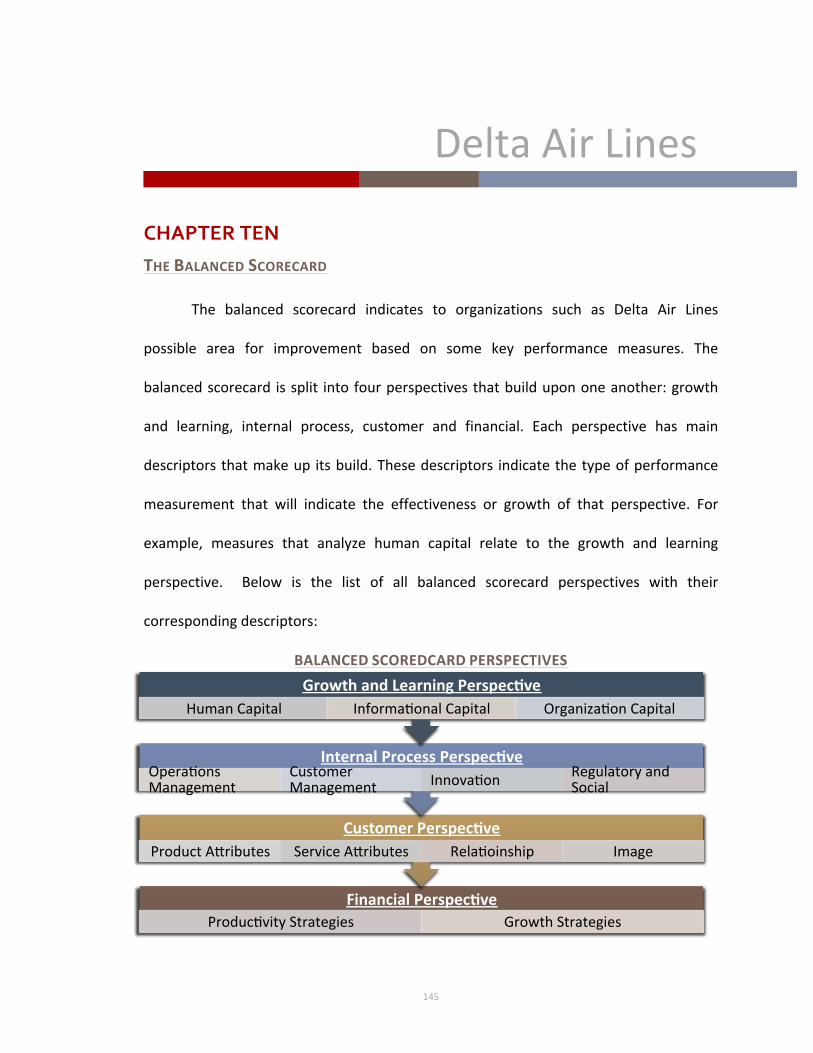

TheBalancedScoreCard..……….…………………………………….……………………………….….Page145

RecommendationOne..……….…………………….………………………………………………….….Page148

RecommendationTwo..……….…………………………….………………………………………….….Page149

RecommendationThree..……….……………………..…………………..………………………….….Page150

EffectofRecommendations..……….…………………………………………………………….….….Page152

WorksCited..……….…………..……………………………….……………………………………….….….Page154

DeltaAirLines

8

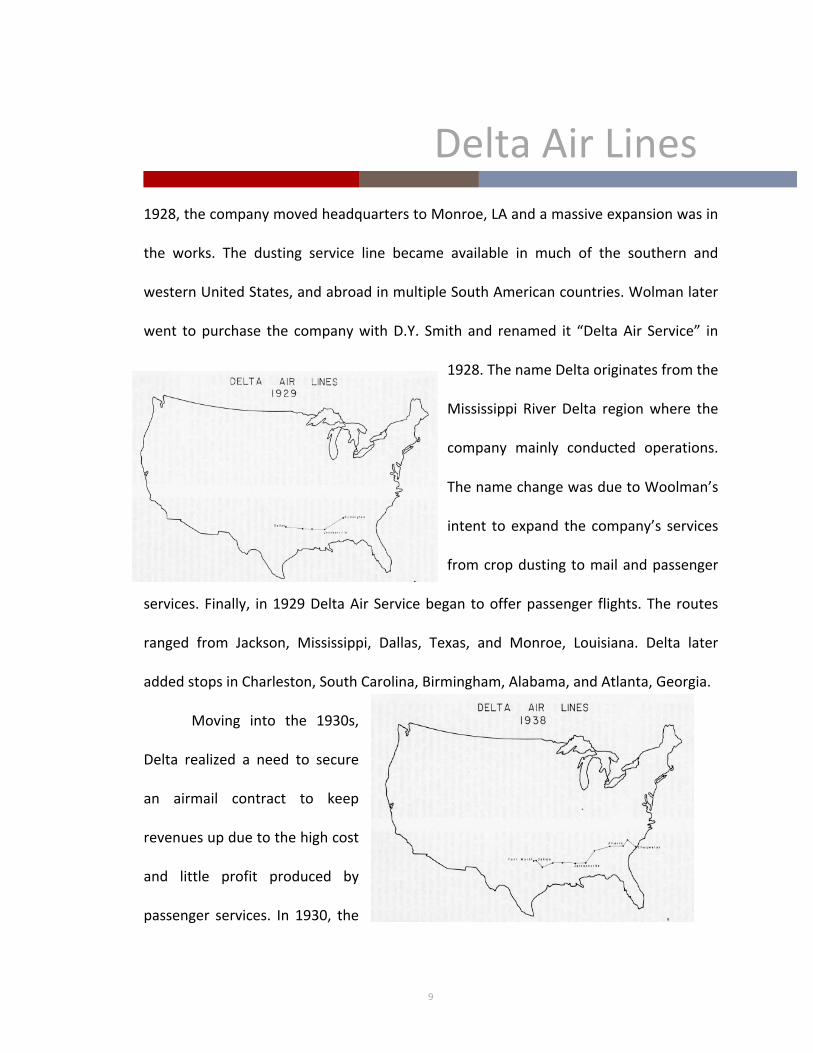

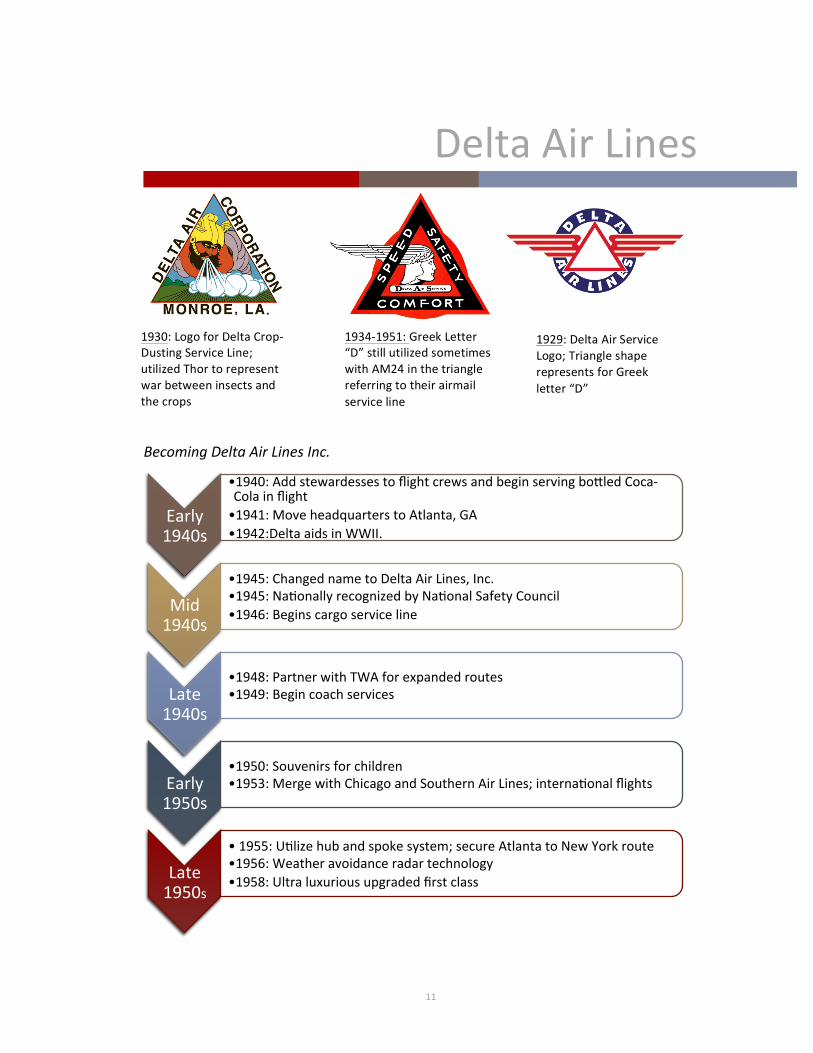

CHAPTERONECOMPANYHISTORYSources:DeltaAirlines.com,DeltaMuseum.org,Fairweather,Malcom.“TheHistoricalDevelopmentofDeltaAirLines.”ReferenceforBusiness.com

TheBeginnings

Huff Daland Dusters, later to become Delta Air Lines, originated on May 30,

1934,inMacon,Georgia.Ownedbyamilitaryaircraftcompany,HuffDaland,hopedto

aidfarmerswithkeepingtheiragriculturalproductsinsect-freebydustingthefieldswith

pesticides via plane. Collett Everman “C.E.”Woolman advisedHuffDaland during the

serviceline’screationandwasessentialtothecompany’sformation.Between1925and

1924• EstablishmentofHuffDalandDustersinMacon,GA

1920's

• 1925-1928:HeadquartersmovetoMonroe,LAandExpansionofcompany

• 1928:Renamedto"DeltaAirService"

• 1929:Deltabeginspassengerflights

1930

• "SpoilsConference"• Closepassengerserviceline• Companyrenamed"DeltaAirCorporajon"

1934

• AirMailActof1934

• ReceiveairmailcontractRoute24

• Reopenpassengerserviceline

1938

• CivilAeronaujcsAct• DeltaAirCorporajonfirsttorecievepermanentcerjficajoninUnitedStates

DeltaAirLines

9

1928,thecompanymovedheadquarterstoMonroe,LAandamassiveexpansionwasin

the works. The dusting service line became available in much of the southern and

westernUnitedStates,andabroadinmultipleSouthAmericancountries.Wolmanlater

went topurchase the companywithD.Y. Smith and renamed it “DeltaAir Service” in

1928.ThenameDeltaoriginatesfromthe

Mississippi River Delta regionwhere the

company mainly conducted operations.

ThenamechangewasduetoWoolman’s

intent toexpand the company’s services

fromcropdustingtomailandpassenger

services.Finally, in1929DeltaAirServicebegan toofferpassenger flights.The routes

ranged from Jackson, Mississippi, Dallas, Texas, and Monroe, Louisiana. Delta later

addedstopsinCharleston,SouthCarolina,Birmingham,Alabama,andAtlanta,Georgia.

Moving into the 1930s,

Delta realized a need to secure

an airmail contract to keep

revenuesupduetothehighcost

and little profit produced by

passenger services. In 1930, the

DeltaAirLines

10

United States Government decided to delegate airmail contracts to domestic air

carriers. Unfortunately, Delta lost the bid to American Airlines during this “Spoilers

Conference.”Due to the lackof income,Deltawas forced to shutdown itspassenger

servicestemporarilyonOctober1,1930.DuringthisperiodDeltaAirServicesalsowas

renamedtoDeltaAirCorporation.TheUnitedStatesGovernmentdeterminedthatthe

contractswereassignedunfairly and therefore they created theAirMailActof1934.

TheAirMailActof1934leftDeltaAirCorporationwithairmailRoute24,whichhandled

United States Postal Service Mail in the southeast region. The company began mail

service on July 4, 1934, and shortly after on August 5, 1934, Delta was able to

recommencetheirpassengerserviceline.Deltaalsoaddedin-flightmealsforpassenger

flights in1936.Finally,near theendof thedecadeairlinepassenger serviceswereon

the rise, and the government realized that it needed a regulatory power on air

transportationmuchlikefederalhighways.Soin1938,thegovernmentpassedtheCivil

Aeronautics Act that required airline companies to apply for “Certificates of

Conveniences and Necessity” for their routes. Delta Air Corporation became the first

airlineindustrytogainpermanentcertification.

DeltaAirLines

11

BecomingDeltaAirLinesInc.

Early1940s

• 1940:AddstewardessestoflightcrewsandbeginservingbomledCoca-Colainflight

• 1941:MoveheadquarterstoAtlanta,GA

• 1942:DeltaaidsinWWII.

Mid1940s

• 1945:ChangednametoDeltaAirLines,Inc.

• 1945:NajonallyrecognizedbyNajonalSafetyCouncil• 1946:Beginscargoserviceline

Late1940s

• 1948:PartnerwithTWAforexpandedroutes

• 1949:Begincoachservices

Early1950s

• 1950:Souvenirsforchildren• 1953:MergewithChicagoandSouthernAirLines;internajonalflights

Late1950s

• 1955:Ujlizehubandspokesystem;secureAtlantatoNewYorkroute

• 1956:Weatheravoidanceradartechnology

• 1958:Ultraluxuriousupgradedfirstclass

1930:LogoforDeltaCrop-

DustingServiceLine;

utilizedThortorepresent

warbetweeninsectsand

thecrops

1929:DeltaAirService

Logo;Triangleshape

representsforGreek

letter“D”

1934-1951:GreekLetter

“D”stillutilizedsometimes

withAM24inthetriangle

referringtotheirairmail

serviceline

DeltaAirLines

12

The 1940s to 1950s era of

Delta Air Lines is marked by

the massive growth and

technology advancements

withinthecompany.The1940s

began with an essential

additiontotheDeltastaff,stewardesses.Theadditionofthestewardesseswasjustthe

beginningof services that illuminatedDelta’s extreme focuson customer satisfaction,

withbottledCoca-Colabeingofferedduringinflightbeverageservicethatyearaswell.

Justayearlater,DeltaAirCorporationHeadquartersrelocatedfromMonroe,Louisiana,

toAtlanta,Georgia,duetomassivegrowthinroutes.Whatoncebeganasflightshighly

saturatedinthe“deepsouth”hadmovedintoeasternstatesandthereforecausedthe

movetoAtlanta,acitythatcouldholdthecapacityoftheexpandingbusiness.AsWorld

War II began, Delta Air Corporation gave aid to the war effort and temporarily

terminatedcivilianservices.Thecompanymodifiedplanesformilitaryuse,trainedArmy

pilotsandmechanics,andrancargosupplyroutesthroughoutthewar.Throughoutthe

1940’sand1950’sDeltawasrecognizedforitssuperiorserviceandsafetystandardson

anationalplatform.WithWorldWarIIover,in1945DeltaAirCorporationreturnedto

its passenger services, but changed its name towhat it is known as today, Delta Air

DeltaAirLines

13

Lines, Inc. That year they received recognition from the National Safety Council for

achieving 300 million passenger miles and 10 years without any fatalities. By 1946,

Delta’sservicelinesevenfurtherexpandedwiththeadditionofcargoservices.Moving

intothelater1940sgrowthcontinuedwithpartnershipswithTWAthatallowedDeltato

expand its routes. The deal allowed Delta planes to be flown by TWA crews from

CincinnatitoDetroit,Columbus,DaytonorToledo.Inreturn,DeltaemployeesflewTWA

planes from Cincinnati to Atlanta, Miami and Dallas. This further allowed Delta to

increase its presence in the northernmarkets. Also during this time, Delta increased

plane cabin luxury by upgrading to in cabin pressurization and air conditioning, and

including seat trays. As the 1940’s came to an end expansion continued with the

commencementofCoachClassservicesonDeltaflights.

DeltaAirLinesgrowthandextensiveconcentrationonamenitiesandtechnology

continuedintothe1950’sera.Anewtarget-marketDeltabegantofocusonduringthis

period was children passengers. With the 1950 children’s souvenir of a Junior Pilot

Certificate foryoungboyandgirlpassengersand the1958souvenirof “kiddiewings”

pins,Deltaonceagainstrivedtomakeallpassengers’tripsenjoyable.In1953,amerger

between Delta Air Lines and Chicago and Southern Air Lines allowed the company’s

flightroutestoexpandexponentially.Themergercreatedanamechangefortwoyears

of“Delta-C&S,”butallowedDeltatoobtainitsfirstinternationalflightstotheCaribbean

DeltaAirLines

14

andCaracas.Themergercreatedthefifth largestairlinecompanyintheUnitedStates

and added 5,000 miles of new routes to Delta’s service lines. Throughout the mid

1950’s, Delta continued its development with the utilization of the hub and spoke

system beginning in 1955. The hub and spoke system is a technique that involves

droppingpassengersoffatairportterminalsor“hubs”andallowingthemtogetontoa

connecting flightora“spoke.”Thisallowedmorepassengers toutilize flightsand less

flights go under seated. By 1956, weather avoidance technology added to aircrafts

createdsafertripsforpassengersandcrews.Theupgradescontinuedin1958,withfirst

classflightsutilizingthreeinsteadoftwoflightattendants,playingboardingmusicand

offeringfreechampagneandsteaksin-flight.

1945-1953:FlyingDLogo1953-1955:Delta-C&SLogo;Logousedwhen

DeltamergedwithChicagoandSouthern

Airlinesthatcausedbriefnamechange

1955-1959:FlyingDLogousedbefore

themergerreturns

DeltaAirLines

15

TheJetEra

Asthe1950’scametoacloseDeltamoved intotheJetEra,becomingthefirst

airline to start a jet service in

1959.Thechangeleadstoanew

“widget” logo representing the

swept-wing look of jets. Of

course, Delta continuedwith its

customer satisfaction

innovationsby introducing in-flightmeals to coachpassengers. The1960sbeganwith

evenmoreexpansion,whenDeltafliesthefirstnon-stopflightfromAtlanta,Georgia,to

1959

• PurchaseofDouglasDC-8Jet• Firsttoofferjetservice• WidgetLogo

Early1960s

• 1961:AddsAtlantatoLosAngelesroute• 1962:SABRESystem

Late1960s

• 1966:C.E.Woolmandies;Terminatecropdusjngserviceline• 1967:MergeofDeltaandDelwareAirlinesInc.

Early1970s

• 1971:DeltaDashCargoService• 1972:NortheastAirlinesmergeswithDelta

• 1975:DeltaAirExpress

Late1970s

• 1976:PurchasedStonerLeasing• 1978:AirlineDeregulajonAct• 1979:EnergyCrisis;50YearAnniversary

DeltaAirLines

16

LosAngeles,California, in1961.In1961theyalsowerethefirstairservicewithflights

from California to Montego Bay and Caracas, and were recognized again with the

National Safety Award for 11 billion passengers without any fatalities. Technological

advancementfollowedin1962withthe initiationoftheSABREsystem,whichallowed

“instant” reservations through their “Deltamatic” system. Sadly, in 1966, original

founderofDeltaandcurrentCEOC.EWoolmanpassedaway.Withhispassing,thecrop-

dustingservicelineended.Unlikeotherairlinebusinesses,Delta’sCEO’spassingdidnot

hurt the company’s growth and income. Delta had a smooth transition from C.E.

Woolman to modern, collective management style, which aided in decreasing the

difficultiessomecompaniesfacewithmanagementchanges.

AseriesofmergersandpurchasesoccurredintheproceedingyearsforDeltaAir

Lines.DeltamergedwithDelawareAirlines (1967)andwithNortheastAirlines (1972),

and purchased Stoner

Leasing (1976). Delta

merger with Northeast

Airlines was especially

important because it

permitted more routes for

Delta in theNorthernUnited States regionswith direct flights toNew York andNew

DeltaAirLines

17

EnglandtoFlorida,Bermuda,Bahamas,andCanada.TheNortheastAirlinesmergeralso

broughtachangeincompanyroutepolicy.DeltadecreasedthenumberofsmallerNew

Englandroutesbygivingthoseroutestoanorthernregionalcompany,AirNewEngland.

Doing this allowed Delta to focus on the more profitable routes and longer haul

destinationflights.Duringthesameperiod,expansionwasalsohappeninginthecargo

service line. In 1971, Delta created Delta Dash Cargo, a service for small package

delivery.By1975,thecompanydecidedtocreateDeltaAirExpress,aguaranteedcargo

service.Deltaonceagainwasaleadinginnovatorbecomingthefirstairlinetoownanair

express service.Customeramenities continued to improveduring the1970’swith the

upgradesprovidingthefirstin-flightaudioentertainmentforpassengers.

In1978,theUnitedStatesGovernmentPassedtheAirlineDeregulationAct.The

act removed government control of airline routes, prices and entry into themarket.

Manyairlinecompaniesscurriedtograbasmanynewroutesaspossible,butDeltawas

more conservative. Delta

was cautious about the

change because they were

concernedthat itwould ruin

profitabilityof theirhuband

spoke systems, and also

DeltaAirLines

18

concerned that it would diminish flight services to small airport destinations. This

cautiousbehaviorwasvery typicalmanagement styleofDeltaduring the JetEra. The

company was technologically advanced and focused heavily on improving customer

satisfaction,but itwascarefulwith theirpurchasesbyonlybuyingaircrafts thatwere

proven to be durable and safe. This management policy, known as a “wait-and-see”

policy, savedDelta large amounts ofmoney in the 1970’s because they did not have

frivolousexpenses.AsDeltaChairmanduringthetimeperiod,W.T.Beebestated,“We

don’tsquanderoutmoneyongoofythingslikeadvertising.”Thisfurtherhighlightsthe

company’s culture of conservative spending on items that they could ensure were

value-added profitable activities. As the 1970’s drew to an end, Delta Air Lines

celebrated its 50thAnniversaryofpassenger services, andalso received recognition in

1979 for the first airline to board onemillion passengers in one city (Atlanta) in one

month and a Public Interest Award for their efforts in reducing jet noise. 1979 also

markedthebeginningofflightservicestoFrankfurt,WestGermany.Although1979was

ayearofsuccesses,itbeganasayearofturmoil.The1979EnergyCrisisoccurreddueto

the Iranian Revolution that caused an oil shortage worldwide. Due to the decreased

supplywiththedemandremainingconstant,pricesgrewexponentiallyandaffectedthe

airlineindustryforthebriefperiod.Duringthebeginningmonthsof1979,Delta,along

withotherairline service companies,was forced tocutbackon thenumberof flights

DeltaAirLines

19

duetotheoilshortage.DeltaAirLinesdroppedanaverageof18flightsadayandtheir

firstquarterearningswere61%lowerthantheywereinthefirstquarterof1978.This

subsidedexpansionofroutesforDelta,butluckilytheIranianRevolutionconcludedby

theendofthe1979allowingexpansiontocommenceonceagaininthe1980s.

1959-1965:SidewaysWidget,symbolizesspeed

ofwidgets

1962-mid1960’s:OvalWidgetLogo

1960’s-1970’s:UprightWidgettoLeftofCompany

name

DeltaAirLines

20

ExpansiontoanInternationalCarrier

The 1980’s to 1990’s for Delta Air Lines was marked by the extreme growth

domesticallyandinternationallyduetothetransition in internalmanagementstyle. In

thedecadesbefore,DeltaAir Lineshadbeenknown for their conservativeand“wait-

and-see”policies forbusinesspurchasesandventures,butduringthecomingdecades

Deltabeganutilizingaggressiveandriskystrategiesinhopesofexpandingthecompany

even more (ReferenceforBusiness.com). Throughtout the period, Delta continued to

developandinnovateincustomeramenitiesandaircrafttechnology.In1980,Deltawas

workingonacomputerreservationsystem(CRS)toeasetheboardingpassreservation

Early1980s

• 1980:DevelopmentofCRS

• 1981:Lauchesfrequentflyermileprogram

• 1983:Improveboardingprocessandreduceflyovernoise

1987

• WesternAirlinesmergeswithDelta

• RonaldW.AllennamedCEO

Early1990s

• Early1990'sRecessionandDropinOilPrices• 1991:PurchasePamAmAssets

Mid1990s

• 1994:Leadership7.5ProgramandRapidRedempjonFlyerProgram

• 1995:NamedAirlineofOlympicGames

Late1990s

• 1997:US-LajnAmericarouteexpansionsandnewaircrass

• 1998:FirstInternajonalCargoAlliance• 1999:AcquireASAHoldingsInc.

DeltaAirLines

21

process for consumers. That year, in-flight videoswere added as a customer amenity

andDeltacontinuedtoberankedNumberOnebytheDepartmentofTransportation.By

1981,customersatisfactionprojectscontinuedwiththedevelopmentofafrequentflyer

mileprogramlatertocalled“SkyMiles”in1995.Deltawantedtoimprovetheboarding

pass process further, so in 1983 the company upgraded to computer generated

boarding passes and automated advance seat selection. That year Delta also became

the first US aircraft line to meet new federal flyover noise standards. Continued

improvements and innovationswere a large part of the beginning of the 1980’s for

DeltaAirLines.In1987DeltaacquiredWesternAirlinestoaidintheexpansionofwest

coast routes. The merger caused Delta Air Lines to become the fifth largest aircraft

carrierworldwide. (DeltaMuseum.org). RonaldW. Allenwas named CEO that year as

well,whichfurtherconstructedtheaggressivebusinessstructureDeltabegantoutilize

duringthistimeperiod(ReferenceforBusiness.com).

Thelate1980sandearly1990swasaperiodofrecessionduetotheconflict in

the Middle East which caused oil shortages and increased oil prices throughout the

world.TheincreasingoilpricesanddecreasingcustomertrafficaffectedDeltaAirLines

bydiminishingprofitsduringtheearly1990speriod.Althoughaperiodoflittleincome,

Delta’sassertivebusinesspoliciespushedforthepurchaseofPamAmAssets in1991.

Thepurchasewas$1.7billionworthofassetsand$668millionworthofliabilities,italso

DeltaAirLines

22

openednumeroushubroutesforDeltaabroadanddomestically.ThepurchaseofPam

AmAssetsputDeltaatalossduetothehighcostofthetransactionandpooreconomic

conditions,endingwith$506millioninlossesin1991.Inordertodealwiththemultiple

years of losses, Delta created the Leadership 7.5 Program to get back on track. The

Leadership7.5Programwasacostcuttingschemetoreducecostsby7.5centsforevery

mile,perseattoreducecostby2billiondollarsinthenextthreeyears.TheLeadership

7.5 Program along with the Rapid Redemption Flyer Program, a program created to

encourage passengers to fly often and instantly reedeem miles for free tickets, the

companyfinallyreturnedtoapositiveprofitinthefourthquarterof1994.

In1995,Delta receivedahugepromotionalboostbybeingnamedtheOfficial

Airlineof the1996Olympics.Moving into theendof the century,Delta continued its

expansionwith growth ofUS-LatinAmerican routes and a purchase of an entire new

aircraftfleetin1997.In1998and1999respectively,Deltacreatedthefirstinternational

cargoallianceandacquiredASAHoldingsInc.Asthe20thcenturycametoaclose,Delta

AirLineshadgrowntoaninternationalandprestigeousaircraftcarrier.

1985-1991:SignatureServiceLogovisibleon

customeritems

1993-1995:FullCorporateLogo

DeltaAirLines

23

The21stCentury

Deltaenteredthe21

stCenturyasaleadingcompetitorintheAirlineIndustry.In

the age of technology Delta launched their Delta.com website in 2000, allowing the

companytointeractwithcustomerseasier.OnSeptember11,2001,terroistsstruckthe

UnitedStatesviaaircrafthijacking. In response, thecompanyshutdown for twodays

and had its first reported loss in six years. ButDelta bounced back from the horrible

eventbycontinuingtoimproveitssystems.In2003,theybecamealeaderinupgraded

check-insystemswithasystemthathadkioskboardingpasscheck-ins,expandedgate

Early2000s

• 2000:Delta.comWebsite

• 2001:Shutdowndueto9/11• 2003:Upgradedcheck-insystem

• 2004:75YearAnniversary

Late2000s

• 2005:OperajonClockwork;FileforBankruptcy• 2006:Overcomebankruptcyandhosjletakeover

• 2008:NorthwestAirlinesmerger

• 2009:Internajonalrouteexpansion

2010s

• 2010:2MillionDollarUpgrade

• Fortune'sMostAdmiredAirline2011,2013

• 2014:85yearsofPassengerService

1995-2000:FullCorporateLogo

DeltaAirLines

24

informationsystems,lobbyredesigns,bettersignagetoreducecongestionandcheck-in

capabilities on Delta.com. These improvements set Delta apart from its competitors.

2004 marked the 75 Year Anniversary of passenger service, but turmoil was on the

horizon. In 2005, Delta implemented “Operation Clockwork” which was the largest

scheduleing redesign in airline history. On September 24, 2005 Delta filed for

bankruptcy,butinNovemberhadthelargestexpansionofroutesincompany’shistory.

By 2006, Delta Air Lines had overcome its bankruptcy issue and avoided a hostile

takeoverbyUSAirways.In2008,thecompanymergedwithNorthwestAirlinesfurther

expanding the company’s routes and size. They also addedwi-fi to select flights that

year.Bytheendofthe2000s,DeltaAirLineswasundergoingaenormousinternational

routeexpansion. TheybecametheonlyUSAirlinetoservesixcontinentsandhasthe

largestpassenger loyaltyprogram,SkyMiles,with74millionmembers.DeltaAirLines

startedoffthisdecadewithatwomilliondollarupgradeofaircrafts-makingthemultra

luxurious. In both 2011 and 2013 Delta Air Lines was name Fortune’sMost Admired

Airline,provingitscustomers’lovefortheamenitiesandservicestheyprovide.Finallyin

2014thecompanycelebrate85yearsofpassengerservices.

2000-2007:HeritageLogo 2007-now:3DwidgetLogo

DeltaAirLines

25

COMPANYOPERATIONS

Delta Air Lines has twomain business segments according to Delta Air Lines’

SegmentReportingFootnoteofthe201310-KFinancialStatement.Deltastatedintheir

10-KDocumentsthattheydeterminedthesetwosegmentsbythegroupsinwhichthe

executive leadership team regularly discusses and reviews. Using this basis, Delta Air

Linesthereforearrivedattwooperatingsegmentsof:AirlinesandRefinery.TheAirline

Segment covers the passenger and cargo services that Delta offers domestically and

internationally,plus themaintaneanceand repairof thirdpartyaircraftsDelta serves.

WheretheRefinerySegment,anewservice lineforDelta, focusesontherefiningand

productionof jet fuel.Deltapurchased the refinery fromPhillips66andhasacquired

deals, mostly with BP, to supply crude oil for Delta to refine. The main goal of the

Refinery Segment is to provide jet fuel to Delta Aircrafts for a cheaper amount than

outsourcing,butalsotoselljetfueltothirdpartiesforextraincome.Delta’s10-Kstated

thatbecausetheRefinerySegment’smaingoal is toprovidearesourcefortheAirline

Segment,thatmanyoperatinggainsandlossesarerealtedtoportionsinbothbusiness

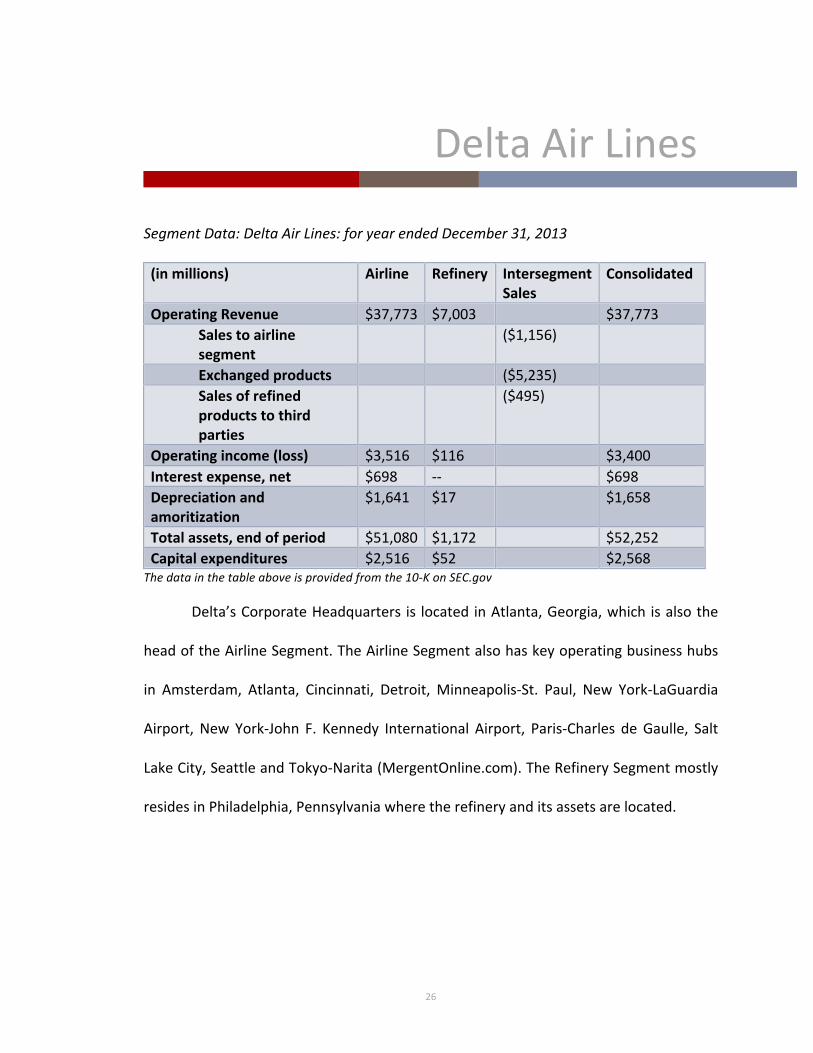

segments.ThetablebelowhighlightsthesegmenteddatabybusinessprocessforDelta

AirLinesfortheyearendof2013.

DeltaAirLines

26

SegmentData:DeltaAirLines:foryearendedDecember31,2013(inmillions) Airline Refinery Intersegment

SalesConsolidated

OperatingRevenue $37,773 $7,003 $37,773

Salestoairlinesegment

($1,156)

Exchangedproducts ($5,235)

Salesofrefinedproductstothirdparties

($495)

Operatingincome(loss) $3,516 $116 $3,400

Interestexpense,net $698 -- $698

Depreciationandamoritization

$1,641 $17 $1,658

Totalassets,endofperiod $51,080 $1,172 $52,252

Capitalexpenditures $2,516 $52 $2,568

Thedatainthetableaboveisprovidedfromthe10-KonSEC.gov

Delta’sCorporateHeadquarters is locatedinAtlanta,Georgia,which isalsothe

headoftheAirlineSegment.TheAirlineSegmentalsohaskeyoperatingbusinesshubs

in Amsterdam, Atlanta, Cincinnati, Detroit,Minneapolis-St. Paul, New York-LaGuardia

Airport, New York-John F. Kennedy International Airport, Paris-Charles deGaulle, Salt

LakeCity,SeattleandTokyo-Narita(MergentOnline.com).TheRefinerySegmentmostly

residesinPhiladelphia,Pennsylvaniawheretherefineryanditsassetsarelocated.

DeltaAirLines

27

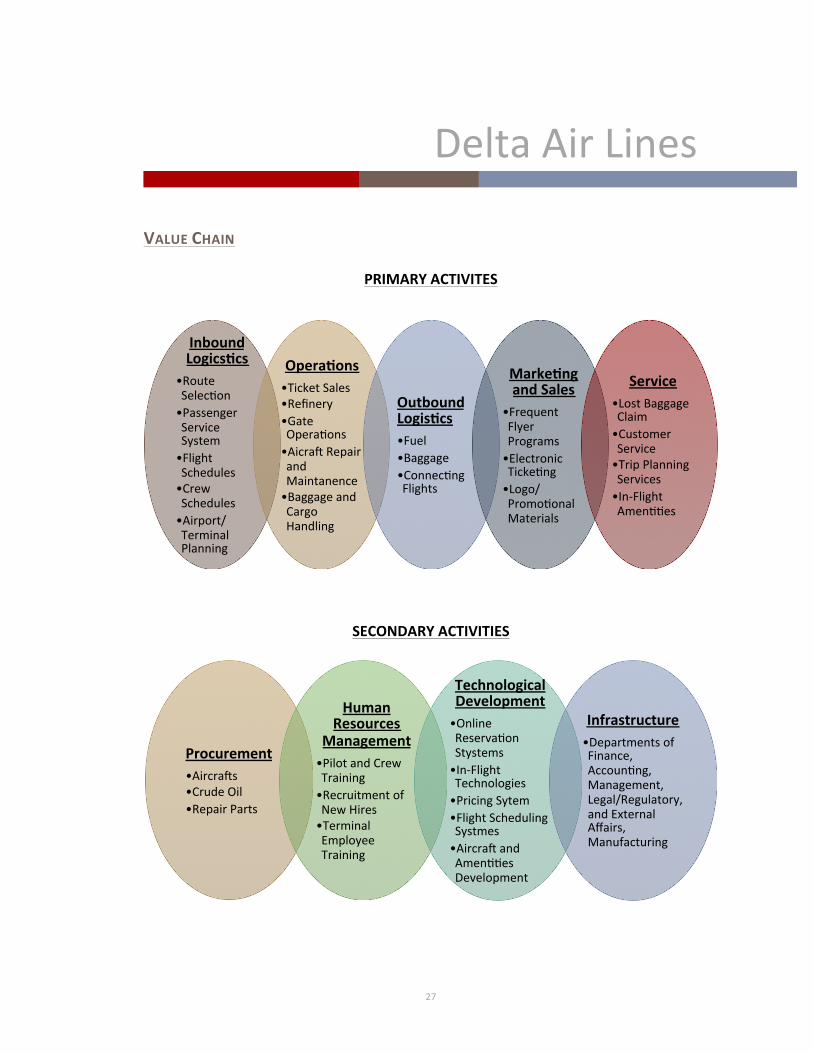

VALUECHAIN

PRIMARYACTIVITES

SECONDARYACTIVITIES

InboundLogicsXcs

• RouteSelecjon

• PassengerServiceSystem

• FlightSchedules

• CrewSchedules

• Airport/TerminalPlanning

OperaXons• TicketSales• Refinery• GateOperajons

• AicrasRepairandMaintanence

• BaggageandCargoHandling

OutboundLogisXcs• Fuel• Baggage• ConnecjngFlights

MarkeXngandSales

• FrequentFlyerPrograms

• ElectronicTickejng

• Logo/PromojonalMaterials

Service• LostBaggageClaim

• CustomerService

• TripPlanningServices

• In-FlightAmenjjes

Procurement• Aircrass• CrudeOil• RepairParts

HumanResources

Management• PilotandCrewTraining

• RecruitmentofNewHires

• TerminalEmployeeTraining

TechnologicalDevelopment• OnlineReservajonStystems

• In-FlightTechnologies

• PricingSytem

• FlightSchedulingSystmes

• AircrasandAmenjjesDevelopment

Infrastructure• DepartmentsofFinance,Accounjng,Management,Legal/Regulatory,andExternalAffairs,Manufacturing

DeltaAirLines

28

BUSINESSPROCESSESDIAGRAM

PointswheretheOperatingValueChainActivitiesTakePlaceinBPMNModel:

• Cargo/TicketRequestàdeliveringcargoorpassengertodesireddestination

• AircraftRepairRequestàfixingaircraftsforthirdparties

• RefinedOilOrderàprovidejetfuelforDeltaplanesandthirdparties

DeltaAirLines

29

BOARDOFDIRECTORS

Delta Board of Directors currently consists of sixteenmembers, although one

doesnothavevotingpower.TheBoardmeetsfourtimesayearregularly,butwillmeet

extra times for special situations. According to Delta Air Lines Website, “The Board

believes sound corporate governance practices provide an important framework in

assistingtheBoardtodischargeitsresponsibilities.Accordingly,theBoardhasadopted

corporate governance principles relating to its functions, structure, and operations”

(DeltaAirLines.com).

Name Position Age TotalPay Tenure BackgroundDanielA.Carp

Non-

Executive

Chairman

66 $412,854 8 CurrentDirectorofNorfolkSouthern

CompanyandTexasInstrumentsInc.;

FormerCEOofKodak

RoyJ.

Bostock

Non-

Executive

Vice-

Chairman

74 $276,394 7 CurrentDirectorofNortheastAirlines

CorporationandChairmanofthe

PartnershipforaDrug-FreeAmerica;

FormerCEOofMcManusGroup

(communicationservices)andDirector

ofB/Com3(advertising)

Richard

H.

Anderson

Director 60 $14,375,902 8 CurrentCEOofDeltaAirLinesInc.;

FormerCEOofNortheastAirlines

EdwardH.

Bastian

Director 57 $8,845,206 17 CurrentPresidentofDeltaAirLines

Inc.;FormerCFOofDeltaAirLinesInc.

andCEOofNortheastAirlines

JohnS.

Brinzo

Director 73 $234,956 8 CurrentDirectorofAKSteelHolding

CorporationandBoardofTrusteesfor

KentStateEndowmentFoundation;

FormerCEOofCliffsNatural

Resources

DavidG.

DeWalt

Director 51 $224,555 4 CurrentBoardofDirectorofFive9Inc.

andCEOofFIreEyeInc.(security

company);formerEMCsoftware

groupemployee,BoardofDirectorof

JiveSoftwareInc.andPolycomInc.

William

H.Easter

Director 65 $220,389 3 CurrentDirectorofConchoResources

Inc.andBoardofMemorialHermann

HospitalSystem;Hasa30yearcareer

innaturalgasmarketing,

transportationandrefiningfrom

ConocoPhillips,FormerCEOofDCP

Midstream

DeltaAirLines

30

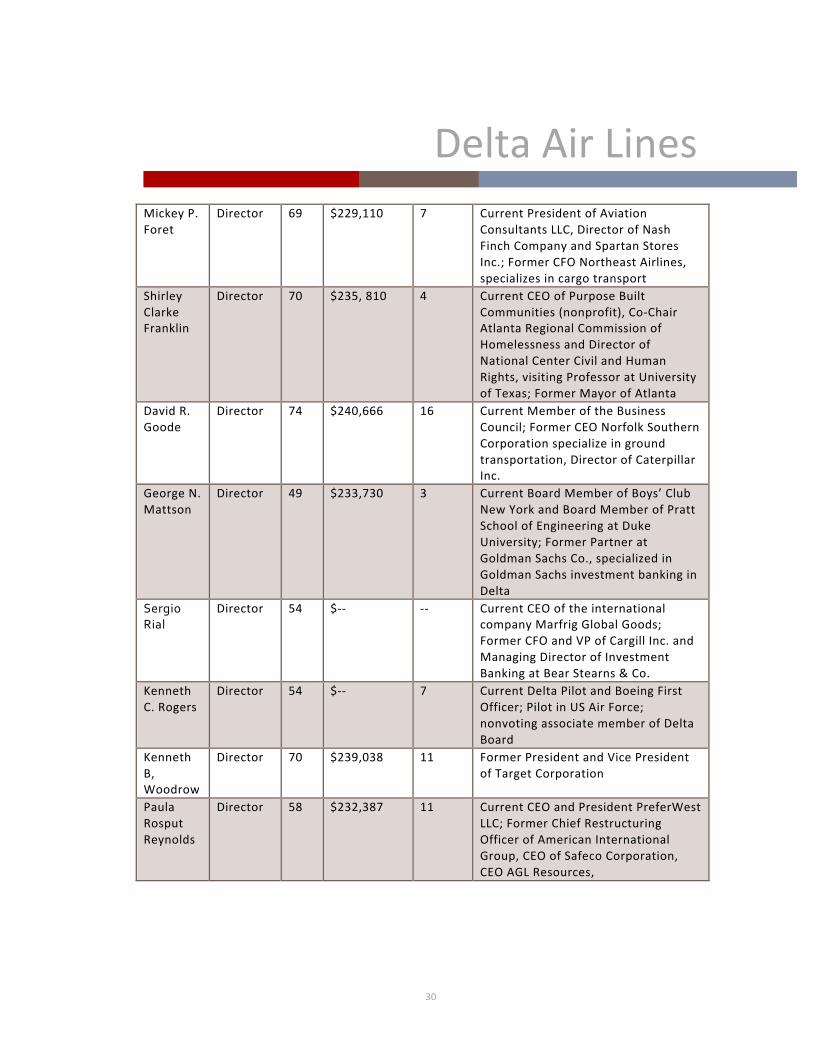

MickeyP.

Foret

Director 69 $229,110 7 CurrentPresidentofAviation

ConsultantsLLC,DirectorofNash

FinchCompanyandSpartanStores

Inc.;FormerCFONortheastAirlines,

specializesincargotransport

Shirley

Clarke

Franklin

Director 70 $235,810 4 CurrentCEOofPurposeBuilt

Communities(nonprofit),Co-Chair

AtlantaRegionalCommissionof

HomelessnessandDirectorof

NationalCenterCivilandHuman

Rights,visitingProfessoratUniversity

ofTexas;FormerMayorofAtlanta

DavidR.

Goode

Director 74 $240,666 16 CurrentMemberoftheBusiness

Council;FormerCEONorfolkSouthern

Corporationspecializeinground

transportation,DirectorofCaterpillar

Inc.

GeorgeN.

Mattson

Director 49 $233,730 3 CurrentBoardMemberofBoys’Club

NewYorkandBoardMemberofPratt

SchoolofEngineeringatDuke

University;FormerPartnerat

GoldmanSachsCo.,specializedin

GoldmanSachsinvestmentbankingin

Delta

SergioRial

Director 54 $-- -- CurrentCEOoftheinternational

companyMarfrigGlobalGoods;

FormerCFOandVPofCargillInc.and

ManagingDirectorofInvestment

BankingatBearStearns&Co.

Kenneth

C.Rogers

Director 54 $-- 7 CurrentDeltaPilotandBoeingFirst

Officer;PilotinUSAirForce;

nonvotingassociatememberofDelta

Board

Kenneth

B,

Woodrow

Director 70 $239,038 11 FormerPresidentandVicePresident

ofTargetCorporation

Paula

Rosput

Reynolds

Director 58 $232,387 11 CurrentCEOandPresidentPreferWest

LLC;FormerChiefRestructuring

OfficerofAmericanInternational

Group,CEOofSafecoCorporation,

CEOAGLResources,

DeltaAirLines

31

FrancisS.Blake

Director 65 $-- 1 CurrentDirectoroftheGeorgia

Aquarium,CEOandFormerDirectorof

HomeDepot,specializesinreal

estate,construction,creditservices,

strategicbusinessdevelopment,

growth,internationalandcallcenters

atHomeDepot;Formerexecutiveat

GeneralElectrichandledinternational

acquisitions.

DATAFROMTHETABLEISFROMMERGENT.COM(POSITION,WAGESANDTENURES)ANDDELTAAIRLINES.COM(NAMES,AGEANDBACKGROUND)

LookingatthetableoftheBoardofDirectorsforDeltaAirLines, Ibelievethey

didagreatjobatdiversifyingtheexpertiseofpersonnelontheirBoardofDirectors.The

company represents the supplier side of the company through themultipleDirectors

whomhaveexperience in theoil refineryandaircraft industries.Thecustomerside is

represented through the Directors with Communications and Relations backgrounds

such as, Roy J. Bostock and international customer affairs being represented through

Sergio Rial and Francis S. Blake’s backgrounds. I do believe that international affairs

could be more widely represented because the only strong representation is Rial’s

connection with South America. Delta has numerous business processes ongoing in

Europe, so it would beneficial to have European representation. Financially speaking,

Delta Air Lines’ Board of Directors contains numerous officers who used to work in

financial services or as CFO’s such as, Rial or Mattson. The technical aspects of the

company such as the refining process (understood by Easter) and the automated

programmingusedtoschedule,bookandmanageflightsandthecompany(background

DeltaAirLines

32

fits DeWalt) are clearly covered onmultiple levels. The company‘swell-differentiated

board allows the company to have a better understanding of the outside forces that

couldpossiblehinderthecompany’sgrowth.But,theboard lacksclearpersonnelthat

have worked in United States Transportation Regulatory Offices, although a political

aspect is coveredwith the former AtlantaMayor, Shirley Franklin’s background. I did

enjoy that the company included a pilot on its Board of Directors. This allows the

company to stay up to date on pilot codes, what its employees really want, and

understandinghowtheaircraftswork.OverallIbelievethatDelta’sBoardofDirectorsis

well diversified but could improve through the additionormemberswithUSAirways

Regulatory/backgroundsandinternationalexperience.

DeltaAirLines

33

CHAPTERTWO

MISSIONSTATEMENT

"We—Delta'semployees,customers,andcommunitypartners—togetherformaforce

forpositivelocalandglobalchange,dedicatedtobetteringstandardsoflivingandthe

environmentwhereweandourcustomersliveandwork.WeareDelta'sForcefor

GlobalGood"(Farfan).

The mission statement highlights Delta Air Lines’ purpose of organization,

business statement and values of the organization. We see that the purpose of the

organizationisto“formaforceofpositiveandglobalchange”.Thebusinessstatement,

or how theorganizationwillmeet its purpose is seen in the statement of, “bettering

standards of living and the environment where and our customers live and work.”

Finallythebusinessvaluesinabitambiguousbutitisportrayedinthestatement,“We

areDelta’s Force forGlobalGood.” Themission statementwould be better if it gave

more specific values that arenecessary for creatinga force for global good.Although

DeltacoveritscorevalueslaterinitsCoreResponsibilityReport.Thereportstatesthe

CoreValuesofDelta:

DeltaAirLines

34

AndtheFivePillarstoGlobalGoodcontinuetohighlightDeltaAirLines’Valuesintheir

CoreResponsibilityReport:

GOALS

Delta’s2013CorporateResponsibilityReportstatesthecompany’sgoalsfor2013and

whethertheywerecompletedsuccessfullyornotandalsoindicatesfuturegoalsfor

2014:

Honesty• Alwaystellthetruth

Integrity• Alwayskeepyourdeals

Respect• Don'thurtanyone

Perseverance• Tryharderthanourcompejtors

• Nevergiveup

ServantLeadership• Careforourcustomers,communityandeachother

SupporXngGlobalDiversity

ExpandingGlobal

HealthandWelllness

PromoXngArtsandCulture

AdvancingEducaXon

Improvingthe

Environment

DeltaAirLines

35

ENVIRONMENTALGOALS

SUPPLYCHAINGOALS

2013Goals• NojcesofViolajons• Aciheved• Non-Compliance/PermitExceedences

• DidNotMeetGoal

• Spills• DidNotMeet

• Achieve1.5%fuelefficienctimprovement

• InProgress• ReduceGreenhouseGassEmissionsbelow2012

• MetwithuseofCarbonOffsets

2014Goals• Achieve1.5%FuelEfficencyImprovement

• ReduceElectricityConsumpjonatSelectedAtlantaFacilijesby10%

• SetandArchieveaWaterReducjonGoalforAtlantaTechOps

• MeetEnvironmentalGoalsforNojcesofVioltaions(2),Non-Compliance/PermitExceedences(4),andSpills(69)

• ReduceGreenhouseGasEmissionsbelow2013Levels

2013Goals• AchievesettargetsinpercentagespendthroughMBE,WBEandSBE

• Achieved

2014Goals• AchievesettargetsinpercentagespendthroughMBE,WBE,andSBE

• ConjnuetosupportallNMSDCandWBENClocalandregionalorganizajonsandefforts

• Focusonfurthermaturajonof2ndjersupplierdiversityreporjng,and2ndjergoalofincreasingMWBEby10%overall

• FocusonethicsandcomplianceforSCMstaff,suppliersandenjrecorporajon

DeltaAirLines

36

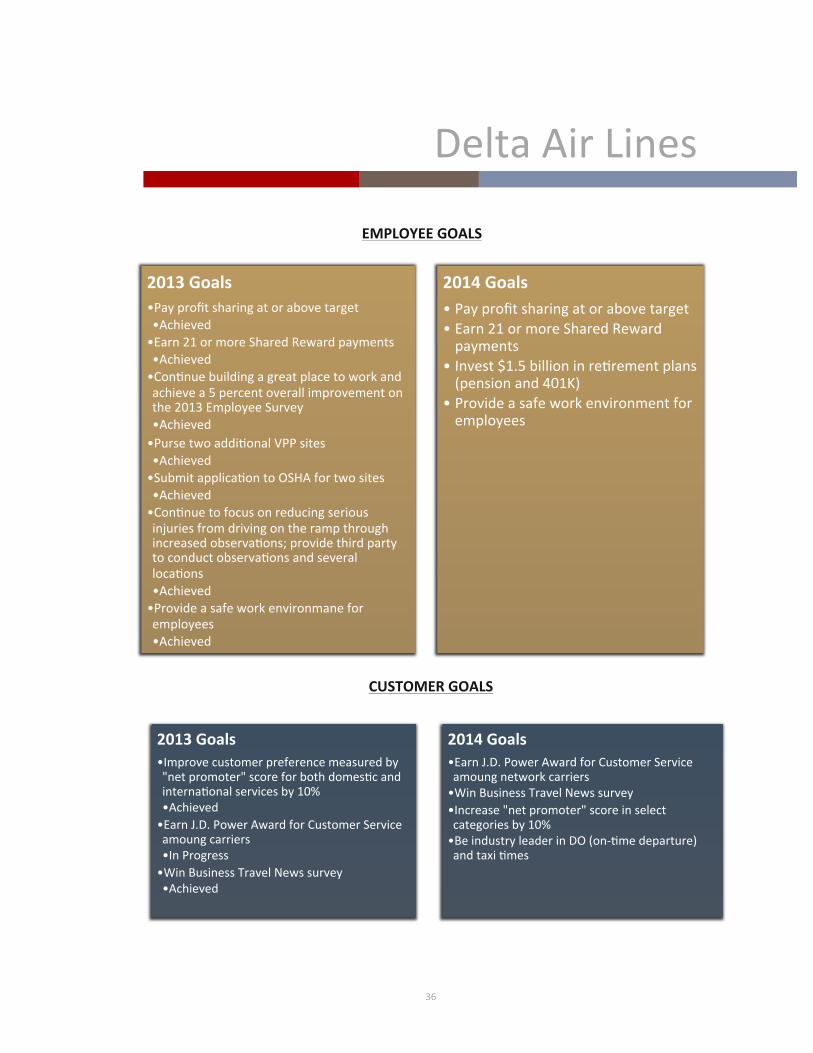

EMPLOYEEGOALS

CUSTOMERGOALS

2013Goals• Payprofitsharingatorabovetarget• Achieved• Earn21ormoreSharedRewardpayments

• Achieved• Conjnuebuildingagreatplacetoworkandachievea5percentoverallimprovementonthe2013EmployeeSurvey

• Achieved• PursetwoaddijonalVPPsites• Achieved• SubmitapplicajontoOSHAfortwosites

• Achieved• Conjnuetofocusonreducingseriousinjuriesfromdrivingontherampthroughincreasedobservajons;providethirdpartytoconductobservajonsandseveral

locajons

• Achieved• Provideasafeworkenvironmanefor

employees

• Achieved

2014Goals• Payprofitsharingatorabovetarget• Earn21ormoreSharedRewardpayments

• Invest$1.5billioninrejrementplans(pensionand401K)

• Provideasafeworkenvironmentforemployees

2013Goals• Improvecustomerpreferencemeasuredby"netpromoter"scoreforbothdomesjcandinternajonalservicesby10%

• Achieved• EarnJ.D.PowerAwardforCustomerServiceamoungcarriers

• InProgress• WinBusinessTravelNewssurvey

• Achieved

2014Goals• EarnJ.D.PowerAwardforCustomerServiceamoungnetworkcarriers

• WinBusinessTravelNewssurvey

• Increase"netpromoter"scoreinselectcategoriesby10%

• BeindustryleaderinDO(on-jmedeparture)andtaxijmes

DeltaAirLines

37

FINANCIALGOALS

BUSINESSSTRATEGY

Source:DeltaAirLinesCorporateResponsibilityReport

Airline corporations tend to fall into two categories of cost leadersor product

differentiators.DeltaAirLines isclearlyaproductdifferentiatorduetotheirextensive

focusoncustomerrelationsandamenities.Deltahasbuiltitsbusinessutilizingthebelief

thatDeltaisa“family”andcustomersareapartofthataswell.Customersatisfaction

built through the utilization of the most innovative and efficient technology and

luxurious amenities haveputDelta at the forefront of highquality commercial airline

services. Delta attempts to offer its passengers the best amenities possible while

keeping prices low and comparable to other airline providers. As seen through their

goalsateachbusinessprocesslevel,Deltahasafocusonmakingtheircustomersmore

comfortable, theiremployeeshappierand theworldabetterplace. This same idea is

outlinedintheirmissionstatementandnotsurprisinglyeffectsthestrategicpositionof

2013Goals• Produceatleast$300MillionofvaluethroughtheMonroeTrainerRefinery

• InProgress• Deliverprojectedreturnfrom$1Billionancillaryandseatrelatedrevenue

• Achieved

2014Goals• Quarterlydividendsofapproximately$200Millionayear

• Produceatleast$300MilliionofvaluethroughtheMonroeTrainerRefinery

• Improveancillaryrevenueto$670Millionandimprovedigitalchannelcustomersajsfacjontoindustry-leadinglevels

DeltaAirLines

38

thecompany.Ratherthanbeingacostisthebottomlinecompany,Deltaputsthefocus

onqualityandsatisfaction,differentiatingthemselvesfrommanyoftheircompetitors.

ASSESSINGDEMANDFORPRODUCTS

SOURCE:FLIGHTFOX.COM,CHRISSCHLICK

Air travel services are normal goods because as demand rises the cost of the

goodalsorises.Whenlookingattheairline industry,thiscanbeseeninthepricingof

passengertickets.Ticketpricesintheairlineindustrychangeconstantlyduetodemand

andseatavailability.Dependingonfactorssuchasthetimeofdaytheflightis,theday

of the week, and when to flight is booked can affect the quoted ticket price for a

passenger’s seat.When demand rises, the airlines raise prices accordingly, but when

demand falls for certain flights the company will lower the cost of passenger seats

temporarily.Priceslevelsareonaflight-by-flightbasis.Inthesubclassofnormalgoods,

passengerairlineserviceswouldbeconsideredaluxurygood.Airlineservicesareleisure

goods and when the economy is doing poorly the average family’s income spent on

leisure activities decreases significantly. Because consumers can dowithout air travel

duringtougheconomictimes,theservicewouldmost likelyfall intheluxurycategory.

Overallairservicecompaniesprofitssoarduringgoodeconomictimesduetoincrease

leisure travel, the only exceptionwould be business travel,whichwould still become

more limited by employers during economic downturns. On the other hand, the

DeltaAirLines

39

refinery segment of the Delta would also be a normal good, but instead of being

classifiedasaluxuryitemitwouldfallunderthenecessitycategorybecauseoftheneed

forjetfueltoprovidetheservicetocustomers.

ASSESSINGSUPPLYOFINPUTS

SOURCES:DELTAAIRLINES.COM,BOEING.COM

The biggest input in the airline industry is gasoline and aircrafts. Since Delta

Airlineshas takenaway the supplierportionof thegasoline supply chaindue to their

refinerysegment,Delta’s inputsareheavilyfocusedontheiraircraftfleet.Theseinput

costs include airplanes, parts and innovative technology upgrades. According to

DeltaAirLines.comthecompanyspentmoneyinthefollowingthreemaincategorieslast

year:Aircraft,GroundSupportEquipmentandSimulators.

Aircrafts GroundSupportEquipment Simulators

Aircraft&Engine

Parts

Insurance(Corporate) Supplies

AirportServices Mail&Postage Technology-Hardware

Beverages Marketing Technology-Phones&

Pagers

Cargo Meetings&Events Technology-Software

Environmental

Services

MRO(Mtc.Repair&Overhaul) Tooling

Equipment Paper&PrintedProducts Transportation

Facilities

Maintenance

PassengerExpenses(IROPs) Travel&Expenses

Food ProfessionalServices Uniforms

Fuel Safety&Security

DeltaAirLines

40

Focusing on the biggest

investment of inputs in the Airline

Industry,theaircraftsareprovidedby

two companies: Boeing and Airbus.

Boeing and Airbus are for the most

parttheonlytwocommercialaircraft

manufacturers with substantial

market shares. The small amount of

competition in the aircraft

manufacturing allows manufacturers

to build long-term contracts with

airlines and leaves air service

corporations such as Delta with little choice in manufacturer. Delta currently has an

aircraft fleetof764planeswith583ofthoseownedand181 leased.Themajorityare

Boeing aircraftmodelswith a few Airbus planes aswell. Looking at Boeing’swebsite

mostofthe700lineplanesthatDeltapurchaseshaveastickerpricebetween$330and

$380 million, further highlighting the extensive investment airline service providers

mustplace in theircompanies. Thetablebelowshowstheaircrafts inDelta’scurrent

Aircraft Owned Leased TotalB717–200 - 45 45

B737–700 10 - 10

B737–800 73 - 73

B737–900ER 17 10 27

B747–400 4 9 13

B757–200 92 35 127

B757–300 16 - 16

B767–300 11 5 16

B767–300ER 51 7 58

B767–400ER 21 - 21

B777–200ER 8 - 8

B777–200LR 10 - 10

A319–100 55 2 57

A320–200 50 19 69

A330–200 11 - 11

A330–300 21 - 21

MD–88 76 41 117

MD–90 57 8 65

Total 583 181 764

DeltaAirLines

41

fleetwith“B”aircraftsstandingforBoeingproducedplanes,“A”forAirbus,and“MD”

forMcDonald-Douglass(nowownedbyBoeing)planes.

Althoughanaircraftfleetisalargeinitialinvestment,theplaneslastmanyyears

allowingairplanecompaniestoutilizetheassettoitsfulldepreciation.Theplaneitself

may stay structurally throughout its years of use but the consumer amenities are

updatedtoprovidemorecomfortableandenjoyableflights.Airlinepurchasesareoften

very volatile and will be postponed depending on the current state of economy and

demandfor flights. Ifcustomersarecurrentlyunwillingtospendonair transportation

companies, suchasDelta,willpostponeaircraftpurchases.Therefore the relationship

betweenaircraftinputsandconsumerdemandisdirectandhasahighcorrelation.

Delta’svaluescontinuetoshineevenwiththeirchoiceinsuppliers.Thecompany

createdaplantowardssupplierdiversitybyutilizingsuppliersthatareowned,operated

and controlled by one of the following minority groups:Women, African Americans,

AsianAmerican,HispanicAmerican,NativeAmericans,DisabledVeterans,Gay,Lesbian,

andBisexual&Transgender. Delta’sgoal is tobuild relationshipswithmorequalified

anddiverse suppliersand theyencourage theirother suppliers todo soaswell. They

alsohopethat theprogramwillaid in thegrowthof jobs, theUSEconomy,andDelta

stockholder’sreturn.

DeltaAirLines

42

COMPETITORSSOURCE:IBISWORLD.COM

DOMESTICMARKETSHAREBYCOMPANY

INTERNATIONALMARKETSHAREBYCOMPANY

Delta has competitors on both the domestic and international level. Although

thereamultiple competitive forces that rivalDeltaAir Lines the twomain companies

thatcompetedirectlywithDeltaAirLinesonboththedomesticandinternationalfield

areAmericanAirlinesGroupInc.andUnitedContinentalHoldingsInc.WhileDeltaisnot

the leader in thedomesticor internationalmarkets, itdoesholda substantialmarket

share with 18.0 percent and 21.1 percent of the domestic and international market

share,respectively.

DeltaAirLines

43

UnitedContinentalHoldingsInc.

DomesticMarketShare:16.9percent

InternationalMarketShare:26.2percent

United ContinentalHoldings Inc. is the parent company ofUnitedAirlines and

Continental Airlines. They are headquartered in Chicago, IL and the two subsidiaries

merged in2010.Thecompanyhasabout5,600 flightsadayandservesdomesticand

international locations. The company serves international locations through its Star

Alliancenetworkandemploys80,500staffearning$38.8billionworldwide.

AmericanAirlinesGroupInc.

DomesticMarketShare:19.9percent

InternationalMarketShare:23.1percent

AmericanAirlinesGroupInc.istheparentcompanyofAmericanAirlinesandUS

Airways.AmericanAirlinesisheadquarteredinFortWorth,TXandthetwosubsidiaries

merged in 2013. The merger was not easy with the Department of Justice forcing

Americantogiveup landingspotsatmultipleairports inorder for themerger to take

place. The companyhas about 6,700 flights a day to 339destinations in 54 countries

around theworld. In2011,AmericanAirlines filed forChapter11Bankruptcywhen it

had$29.6billionindebt.Themergerbetweenthetwocompaniesearned$41.2billion

DeltaAirLines

44

in 2014, making it the highest revenue airline service. The company employs over

100,000worldwide.

DIRECTCOMPETITORCOMPARISON

DatainTableProvidedbyYahoo!FinanceDAL:DETLAAIRLINES,AAL:AMERICANAIRLINES,UAL:UNITEDCONTINENTALHOLDINGS

GEOPOLITICALRISKSSource:IBISWorld.com

1. OilPrices

OilPricesarevolatileandthereforehaveamajor impactonthecostof

transportationincludingtheairlineindustry.Luckily,Deltahascreatedarefinery

segment decreasing some of the middleman costs of refining crude oil. Still,

crudeoilpriceschangedailyandthereforeaffectthecostofflyingtheirplanes.

Deltahasno control over thepriceof crudeoil and trendsonly foreshadowa

DAL AAL UAL IndustryMarkeyCap 39.90B 36.11B 26.01B 2.50B

Employees 79,655 111,852 80,500 59.71K

QtrlyRevGrowth .06 .63 0.00 .25

Revenue 40.36B 39.86B 39.90B 14.75B

GrossMargin .20 .27 .28 .21

EBITDA 4.70B 5.67B 4.48B 1.52B

OperatingMargin .07 .11 .07 .09

NetIncome 659M 284M 1.13B N/A

EPS .78 .51 2.93 .51

P/E 62.00 98.32 24.05 63.05

P/S 1.01 .95 .68 1.01

DeltaAirLines

45

continued rise in its average price in the future. The estimated barrel price is

2015was$56.70perbarrel,butinrealityitroseto$72.60perbarrelthatyear.

2. InternationalTravel

Since the recession it has become safer and cheaper for international

travel.ThelargestnumberofvisitorscamefromCanadaandMexicototheUSin

2014. The concern is the safety of US passengers flying internationally to

sometimesconflictingnations.Theotherconcernisforeignpassengerstraveling

totheUS.WithrecentoutbreakssuchasEbola, internationaltravelregulations

aretakingnewmeaningtogivethehealthandsecurityoftheUSincheck.

3. TerrorismandConflict

Increasedsecurityneedsduetoconflictabroadandterroristattacksand

attempts such as 9/11. 9/11 took a hard hit on the airline industry, causing a

complete restructuring of the security regulations and rules. Flying into

conflictingnationsbringsworriesofsafetyforpassengersandaircrafts.

DeltaAirLines

46

PORTER’SCOMPETITIVEFORCES

ReferenceforModel:Investopedia.comandAirlineIndustryAnalysis

Porter'sFiveForcesModel

RivalryAmoungExisXngFirms

• Highlycompejtvebetweenbrands

• Thereforemustdifferenjateservicesto

amractamarketsegmentofconsumers

• HIGHTHREAT

DeterminantsofSupplierPower

• Aircrassonlyhavetwoprimarysuppliers:Boeing

andAirbus

• Standardizedproductwithlimledifferientajon

• Airlinecompaniescannoteasilyswitchsuppliersduetohighcostandlong-termcontracts

• Unionscontrollaborsupply

• MILDTHREAT

ThreatofNewEntrants

• Largeamountofinvestmenttoenterindustry

• Difficulttobuildcustomerloyaltyandtrustdueto

consumerswanjngtobuyjcketsfromairlineswithproven

safetyandreliability

• Lowswitchingcostsbetweenbrands

• Needforaviajonexperienceandlicesnsestoenter

• Governmentregulajonsonindustry

• LOWTHREAT

DeterminantsofBuyerPower

• Buyergroupsincludepassengersandtravelagents

• Passengers-focusonjmeandcostofflight

• Travelagents-middlemanbetweenpassengersandairlines

• Lowswitchingcostbetweenbrandswithsameservicebeingprovidedwithdifferenjajonlayinginthecostoramenijes

• LOWTHREAT

ThreatofSubsXtuteProducts

• Threatincludesothersourcesoftransportajonsuchascar,train,busor

boat

• Airlinesprovidedshortesttraveljme

• Othertransportajonsmaybeopjmalopjonsforshorttravelorlow

monetarycosts

• MILDTHREAT

DeltaAirLines

47

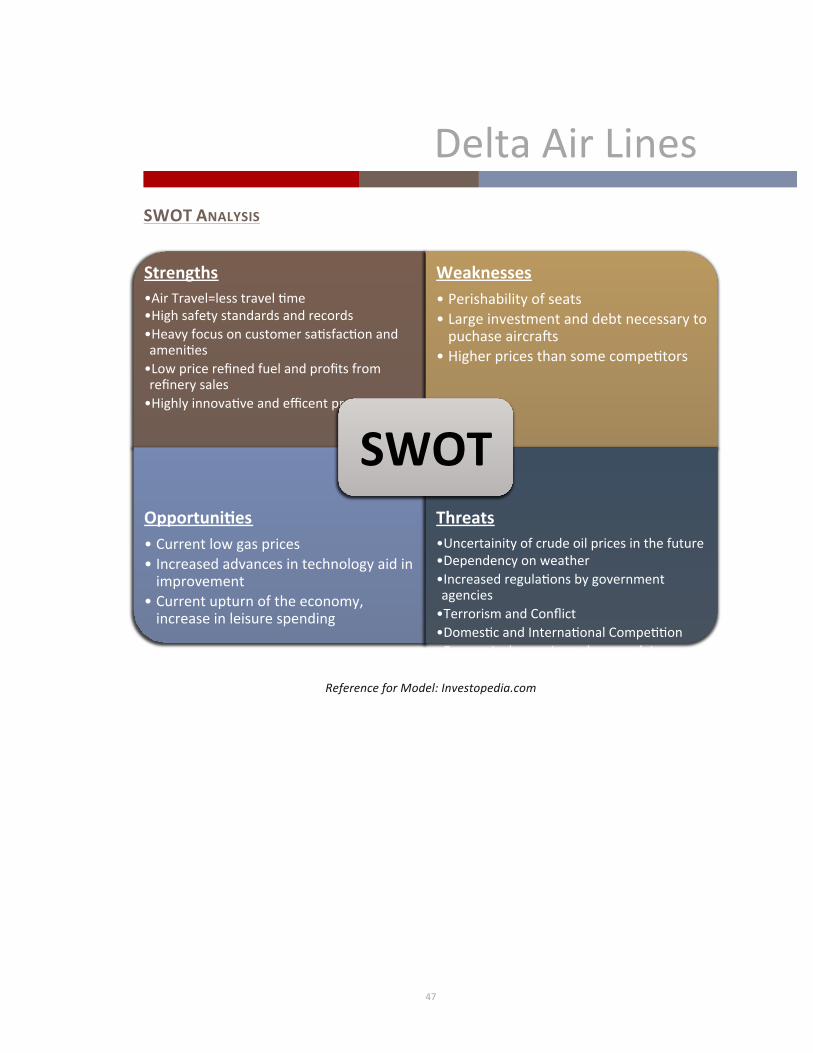

SWOTANALYSIS

ReferenceforModel:Investopedia.com

Strengths• AirTravel=lesstraveljme

• Highsafetystandardsandrecords• Heavyfocusoncustomersajsfacjonandamenijes

• Lowpricerefinedfuelandprofitsfromrefinerysales

• Highlyinnovajveandefficentprocesses

Weaknesses• Perishabilityofseats• Largeinvestmentanddebtnecessarytopuchaseaircrass

• Higherpricesthansomecompejtors

OpportuniXes• Currentlowgasprices• Increasedadvancesintechnologyaidinimprovement

• Currentupturnoftheeconomy,increaseinleisurespending

Threats• Uncertainityofcrudeoilpricesinthefuture• Dependencyonweather• Increasedregulajonsbygovernmentagencies

• TerrorismandConflict

• DomesjcandInternajonalCompejjon

• Economicdepressions,decreaseleisurespending

SWOT

DeltaAirLines

48

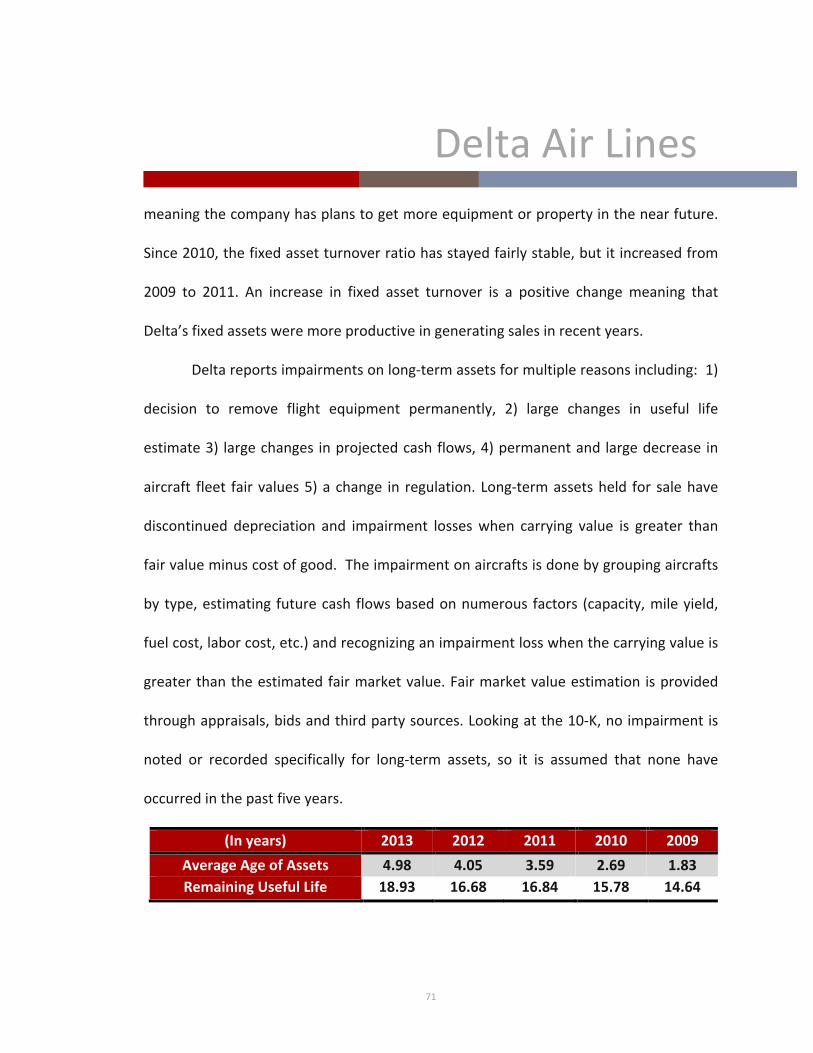

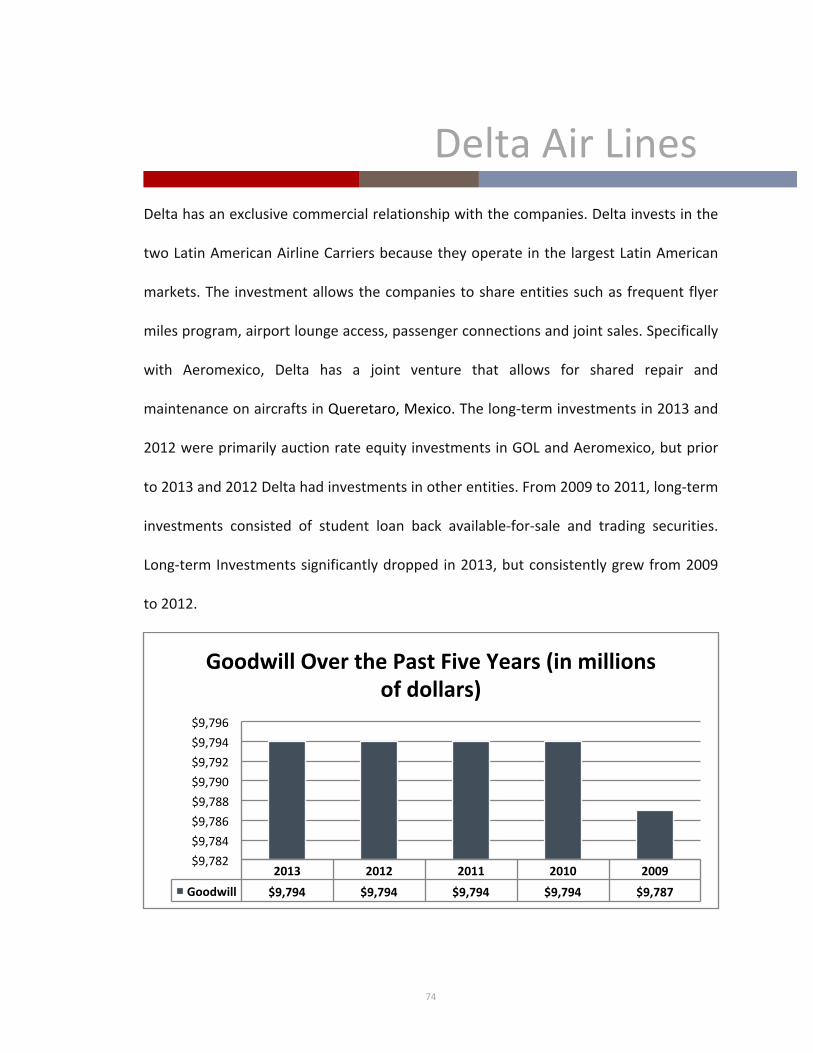

CHAPTERTHREEASSETCOMPOSITION

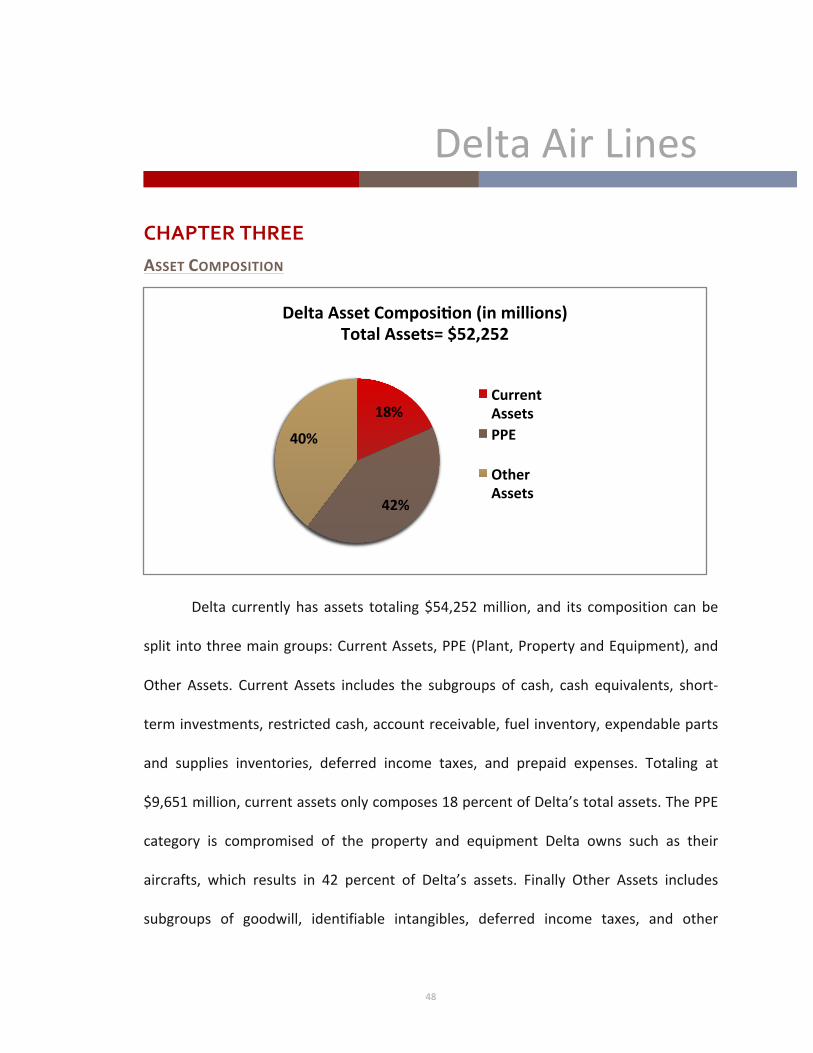

Delta currently has assets totaling$54,252million, and its composition canbe

split intothreemaingroups:CurrentAssets,PPE(Plant,PropertyandEquipment),and

Other Assets. Current Assets includes the subgroups of cash, cash equivalents, short-

terminvestments,restrictedcash,accountreceivable,fuelinventory,expendableparts

and supplies inventories, deferred income taxes, and prepaid expenses. Totaling at

$9,651million,currentassetsonlycomposes18percentofDelta’stotalassets.ThePPE

category is compromised of the property and equipment Delta owns such as their

aircrafts, which results in 42 percent of Delta’s assets. Finally Other Assets includes

subgroups of goodwill, identifiable intangibles, deferred income taxes, and other

18%

42%

40%

DeltaAssetComposiXon(inmillions)TotalAssets=$52,252

CurrentAssetsPPE

OtherAssets

DeltaAirLines

49

noncurrentassets.Thesealsotakealargeportionoftheassetcompositionat40%.The

companydoeshavequiteabitof goodwill and intangibleassetswith$14,362million

creatingapproximately27percentofthetotalassetcomposition.

The company makes some valuations utilizing fair market value but must

estimate for others. According to the companies 10-K they do make estimations on

certainvaluesofassetsandotherentities,butcomplywithGAAPpolicies.Forgoodwill

andintangiblesthe10-KstatesthatDeltautilizesafairmarketvalueimpairmenttoset

the value of intangible assets. Items in PPE are recorded utilizing impairments,

depreciationandpredictorsforfuturecashflowstodeterminethecarryingvalueofthe

property, plant or equipment item. Fair market value assets included cash, cash

equivalents, long-term investments, restricted cash, and hedge derivatives The main

entitiesDeltaAirLinesestimatesthatmaynotbeprecisewithactualvalueaccordingto

their10-KistheFrequentFlyerProgram,PassengerTicketSalesEarningMileageCredits,

Sale of Mileage Credits, Breakage, Goodwill, Intangibles, Long-Lived Assets (PPE),

Income Tax Valuation Allowances, Defined Benefit Pension Plans, Weighted-Average

Discount Rate, Expected Long-Term Rate of Return, and Funding. Items that are

estimated that involve customer contact (Frequent Flyer Program, Passenger Ticket

SalesEarningMileageCredits,SaleofMileageCredits)aremorelikelytobesensitiveto

change because the external environment affects them, which is outside of Delta’s

DeltaAirLines

50

control. Plus customers tend to be more unstable and volatile than entities such as

taxation,depreciationoflong-termassetsandsetpensionplans.

DeltaAirLines(DAL)maindomesticandinternationalcompetitorsareAmerican

AirlinesGroup(AAL)andUnitedContinentalHoldings(UAL).Thethreeindustryleaders

allcontainprimarilythesamecompositionofassets,withvariancesbetweenthegroups

lyingintheamountofOtherAssets.OverallPPEisthehighestassetgroup,followedby

OtherAssetsandfinallyCurrentAssetsacrossall industrycompetitors. CurrentAssets

are usually low for airlines due to the large investment in PPE. PPE is essential to

functionof the companybecause theplanesandairport gatesneeded toprovide the

DAL AAL UAL

OtherAssets 20,747 8,696 10,063

PPE 21,854 19,259 18,047

CurrentAssets 9,651 14,323 8,702

0

10,000

20,000

30,000

40,000

50,000

60,000

Dollars(inm

illions)

IndustryComparisonsofAssetComposiXons(2013)

DeltaAirLines

51

serviceareclassifiedasPPE,wheremostretailcompaniesclassifywhattheyareselling

asinventory,acurrentasset.So,thisclassificationoftheserviceprovidedasalong-term

asset tends tohurtAirlineCompany’scurrentasset ratio,dueto itsexclusionof long-

termassetsinitscalculations.Thistrendofshort-termorcurrentassetsbeinglowand

long-termorPPEandotherassetsbeinghighcanbeseenthroughoutthepastfiveyears

atDeltaAirLinesandisdepicted inthegraphicbelow.Theairline industrymost likely

willnot seea change in this typeof compositionofassetsdue to the requirement to

place their product/service provided into the long-term category rather than a short-

termentity.

COMPANYFINANCING

2013 2012 2011 2010 2009

Long-TermAssets 42,601 36,278 35,770 35,881 35,798

Short-TermAssets 9,651 8,272 7,729 7,307 7,991

010,00020,00030,00040,00050,00060,000

Dollars(inmillions)

Short-TermandLong-TermAssetComparison

(INMILLIONSOF

DOLLARS)

2013 2012 2011 2010 2009

TOTALLIABILITIES 40,609 46,681 44,895 42,291 43,544

PIC 13,982 14,069 13,999 13,926 13,897

DeltaAirLines

52

Looking at Delta Air Lines financing, an adjustment was necessary when

comparing total liabilities with total equity to determinewhich primarily handles the

company’s financing.TotalStockholderEquitywouldnotbeappropriate touse in this

situationduetothedeficitinRetainedEarningsoccurringinmanyoftheyearsatDelta,

seemingly looking like therewasno income fromstock. Therefore, in this section the

comparisonof total liabilitieswaspairedwithPaid inCapital.Unsurprisingly,DeltaAir

Lines hadmuchhigher amounts of liabilities than stock income in the past five years

meaningthatthecompanyreliesheavilyonloansanddebttofinanceexpenditures.This

isriskybecauseitcanputthecompanyindebtandnegativelyaffectthesolvencyratios

duetothelargeamountsofliabilitiesandsmallamountsofequity.Largedebt-to-equity

ratiosmeanthecompanyismoreriskyduetotheincreasedloans.Onthenextpage,a

graphic showing the debt-to-equity ratios of Delta Air Lines over the past five years

comparedto itscompetitorsdepictstheenormousrangeofchange inDelta’sratio. In

2009,thecompanywasfacingextremelyhighriskdueto itshighdebt-to-equityratio.

Thislaterfellin2011and2012toanegativedebt-to-equityvalue.Anegativesolvency

ratiooften implies that the companyhasa largeportionof investment ingoodwill or

intangibles.Finallyin2013,Deltawasabletorestoreitsdebt-to-equityratiotoanormal

valueforairlineserviceindustryproviders.Furtherprovingthecompany’simprovement

inrecentyearsanddecreasedrisktoshareholders.

DeltaAirLines

53

2013 2012 2011 2010 2009

DAL 3.49 -21.91 -32.16 47.15 177.73

AAL -3.65 -2.76 -4.35 -7.36 -8.29

UAL 11.35 77.23 19.99 21.89 -7.65

-35-30-25-20-15-10-505

101520253035404550556065707580859095100105110115120125130135140145150155160165170175180

Deb

t-to-Equ

ityRa

Xon

Debt-to-Equity:5YearIndustryComparison

DeltaAirLines

54

ThefollowingisDeltaAirLines’compositionofbothcurrentandnoncurrentliabilities:

11%

29%

16%

14%

13%

5%4%

8%

CurrentLiabiliXesTotalCurrentLiabiliXes=$14,152

CurrentMaturijes

AirTrafficLiability

A/P

AccruedSalariesandBenefits

FrequentFlyerDeferredRevenue

TaxesPayable

FuelCardObligajon

OtherAccruedLiabilites

37%

47%

10%6%

NoncurrentLiabiliXesTotalNoncurrentLiabiliXes=$26,457

Long-termDebtandCapitalLeases

Pension

FrequentFlyerDeferredRevenue

DeferredIncomeTaxes

OtherNoncurrentLiabilijes

DeltaAirLines

55

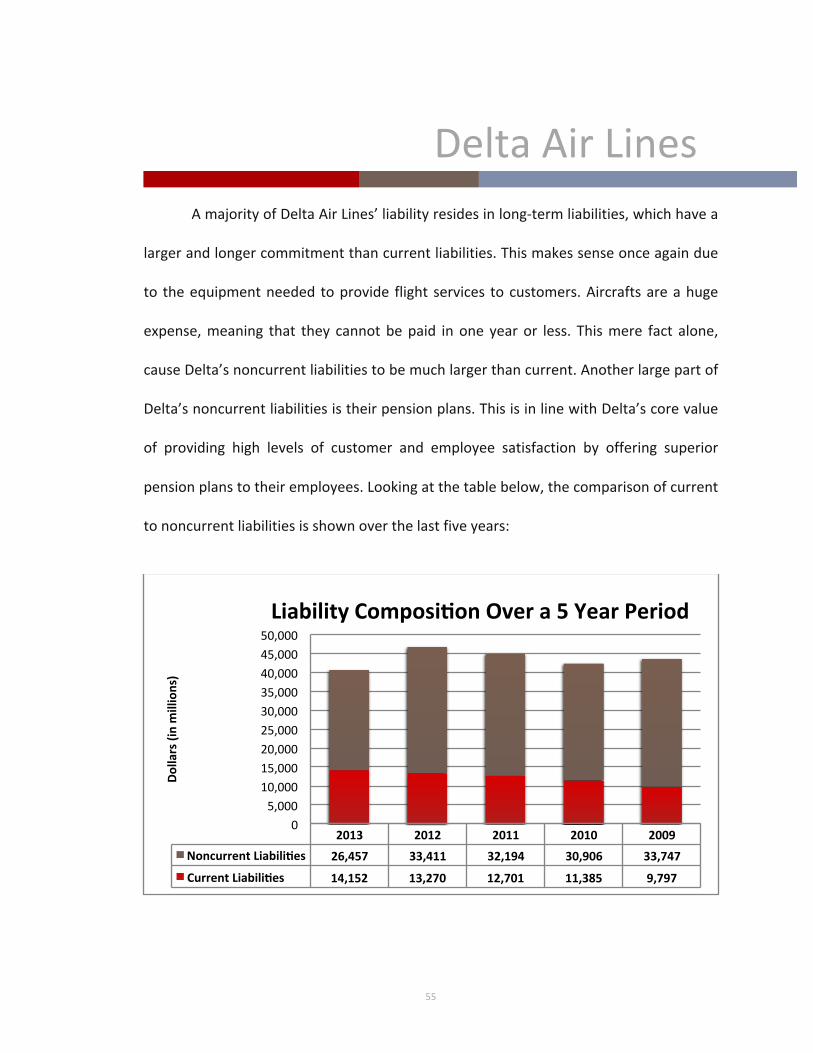

AmajorityofDeltaAirLines’liabilityresidesinlong-termliabilities,whichhavea

largerandlongercommitmentthancurrentliabilities.Thismakessenseonceagaindue

to theequipmentneeded toprovide flight services tocustomers.Aircraftsareahuge

expense,meaning that they cannotbepaid inone yearor less. Thismere fact alone,

causeDelta’snoncurrentliabilitiestobemuchlargerthancurrent.Anotherlargepartof

Delta’snoncurrentliabilitiesistheirpensionplans.ThisisinlinewithDelta’scorevalue

of providing high levels of customer and employee satisfaction by offering superior

pensionplanstotheiremployees.Lookingatthetablebelow,thecomparisonofcurrent

tononcurrentliabilitiesisshownoverthelastfiveyears:

2013 2012 2011 2010 2009

NoncurrentLiabiliXes 26,457 33,411 32,194 30,906 33,747

CurrentLiabiliXes 14,152 13,270 12,701 11,385 9,797

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Dollars(inmillions)

LiabilityComposiXonOvera5YearPeriod

DeltaAirLines

56

Over the past five years Delta has been increasing its current liabilities and

normally decreasing its liabilities except for 2012 and 2011. This could mean a few

differentthings.First,Deltacouldbepayingofftheirnoncurrentliabilitiesmakingthem

currentliabilities.Thiswouldbeapositivechangeforthecompanyandfurtherhighlight

therecentfinancialimprovementsthecompanyhasbeenmakingsincethebeginningof

the new decade. Second, Delta could bemakingmore transactions or contracts on a

short-termloanbasisratherthanalong-termholding.Thiscouldbeapositivechangeif

it isduetothefact thatDeltacanaffordandhastheassetstopayfortheamountof

purchasesonashort-termbasisratherthanneedingtoextendtolong-termcontracts.

DeltaAirLines

57

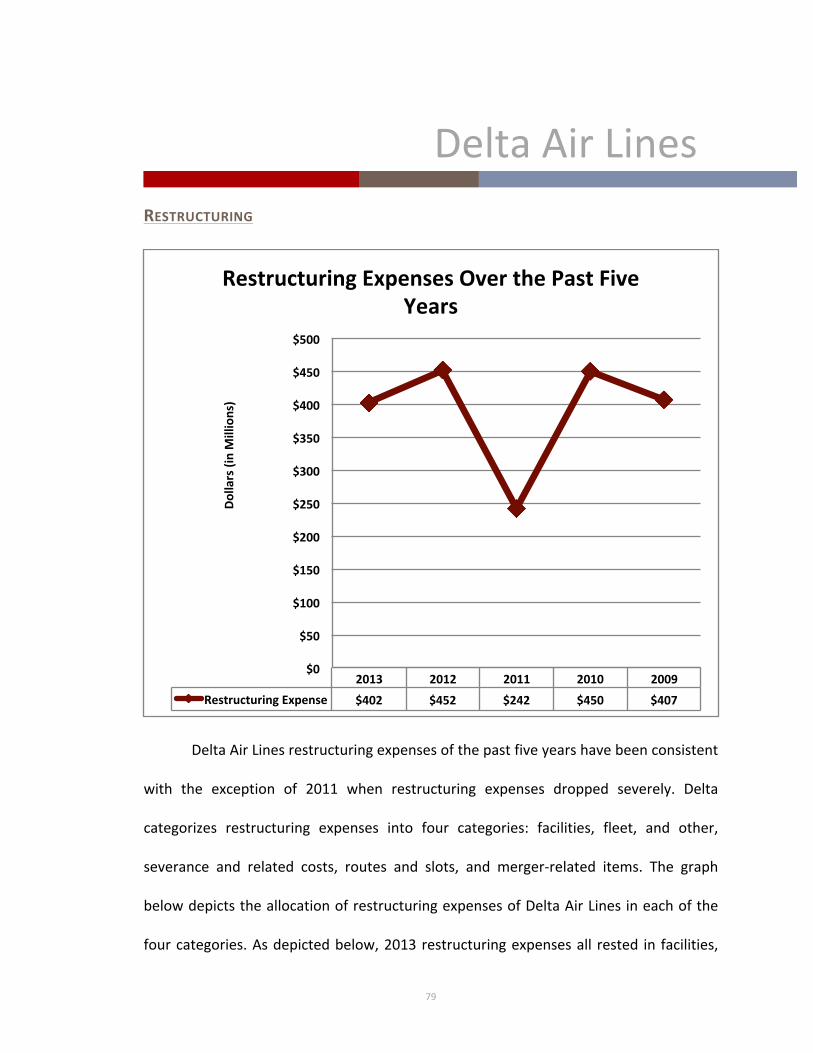

CASHFLOWS

The trend over the last five years in Delta Air Lines cash flows highlights the

company’seconomiclifecyclestage.Withoperatingactivitiesbeingpositivevaluesover

thepast five years, and financing and investing activities beingnegative integers, this

2013 2012 2011 2010 2009

OperaXng 4,504 2,476 2,834 2,832 1,379

InvesXng (2,756) (1,962) (907) (1,005) (951)

Financing (1,320) (755) (1,571) (2,521) (19)

CashIncrease 428 (241) (235) (1,715) 352

(3,000)

(2,000)

(1,000)

0

1,000

2,000

3,000

4,000

5,000

Dollars(inmillions)

DeltaAirLinesCashFlows5YearComparison

DeltaAirLines

58

indicates that the company is at themature stage of its life cycle. Themature cycle

indicatesthattheprofitswillbegintofallandsaleswillpeak.Duringthematuritystage

ofacompanyitisessentialfortheorganizationtoinnovateanddifferentiateitselffrom

itscompetitorsduetothehighsaturationof themarket. Inorder toavoid falling into

thedecliningstagethecompanymustfindawaytoincreaseprofitabilityandcontinue

to update the services and products it provides to customers to stay relevant and

coveted.

LIQUIDITY,SOLVENCYANDEARNINGSPERSHARE

(INMILLIONSOFDOLLARS) 2013 2012 2011 2010 2009CURRENTRATIO 0.68

0.62

0.61

0.64

0.82

DEBT-TO-EQUITY 3.49

(21.91)

(32.16)

47.15

177.73

TIMESINTERESTEARNED 5.00

2.26

1.85

1.63

(0.79)

EARNINGSPERSHARE 12.41

1.20

1.02

0.71

(1.50)

Liquidity:CurrentRatio

Thecurrentratiohasbeenslightlyimprovingsinceissubstantialfallafter2009.

Asdiscussedearlier the likelycauseofsucha lowcurrent ratio is that themajorityof

assets needed to provide air passenger services to customers are long-term and

thereforenotincludedintheratio.Thiscausesthenumeratortobeextremelysmallin

DeltaAirLines

59

comparison to the large amount of liabilities needed to pay for the long-termassets,

makingthecurrentratioconsistentlylessthanoneforDeltaAirLines.

Solvency:Debt-to-EquityandTimesInterestEarned

Debt-to-Equity has substantially improvedwith it going from extreme highs in

2009and2010,tonegativevaluesin2011and2012andfinallyanormalamountforthe

industryin2013.ThistypeofchangedepictsthatDeltahasmovedfromextremedebt,

toextreme investment in intangibleassets, to finallyabalanced relationshipbetween

theamountsofdebttheyhaveandtheamountofequitytheyarereceivingfromtheir

investors.

Times Interest Earned clearly shows the improvements of Delta Air Lines over

thepastfiveyears.Thetimesinterestsearnedvalueshavegrowneachyearsince2009,

withasignificant jumpfrom2012to2013.This impliesthatcompanycanpayback its

interest costs more times with their income. This shows that the riskiness of the

companyisfallingandthatthecompanyisbecomingmoresolvent.

EarningsperShare

EarningsperSharehavealsosignificantlyincreasedinthepastfiveyears,witha

large growth between 2012 and 2013. This number has been achieved in the recent

DeltaAirLines

60

years due to the large income growth with relatively same numbers of outstanding

shares; meaning the numerator had a drastic increase with a constant denominator.

ThisisagoodsignforDeltaAirLinesbecauseitimpliesthatthecompanyhasincreased

itsprofitsandthereforecanpaymoredividendstoitsshareholders.

DeltaAirLines

61

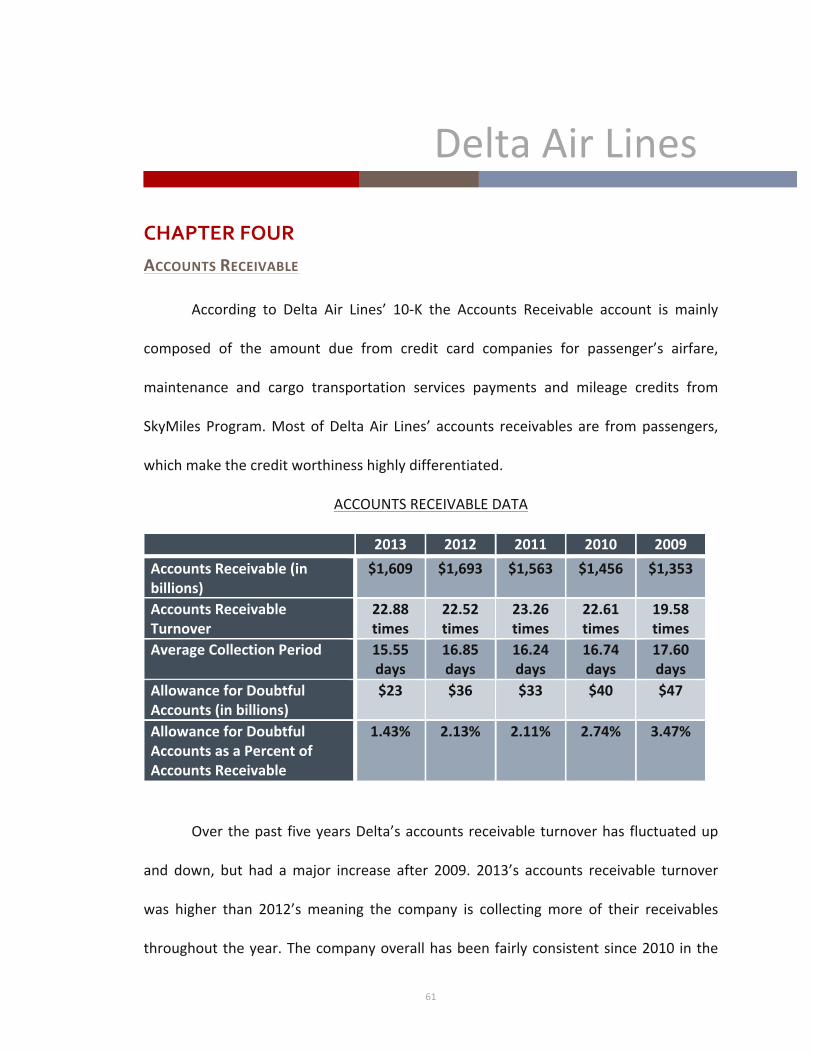

CHAPTERFOURACCOUNTSRECEIVABLE

According to Delta Air Lines’ 10-K the Accounts Receivable account is mainly

composed of the amount due from credit card companies for passenger’s airfare,

maintenance and cargo transportation services payments and mileage credits from

SkyMilesProgram.MostofDeltaAir Lines’ accounts receivables are frompassengers,

whichmakethecreditworthinesshighlydifferentiated.

ACCOUNTSRECEIVABLEDATA

2013 2012 2011 2010 2009

AccountsReceivable(inbillions)

$1,609 $1,693 $1,563 $1,456 $1,353

AccountsReceivableTurnover

22.88times

22.52times

23.26times

22.61times

19.58times

AverageCollectionPeriod 15.55days

16.85days

16.24days

16.74days

17.60days

AllowanceforDoubtfulAccounts(inbillions)

$23 $36 $33 $40 $47

AllowanceforDoubtfulAccountsasaPercentofAccountsReceivable

1.43% 2.13% 2.11% 2.74% 3.47%

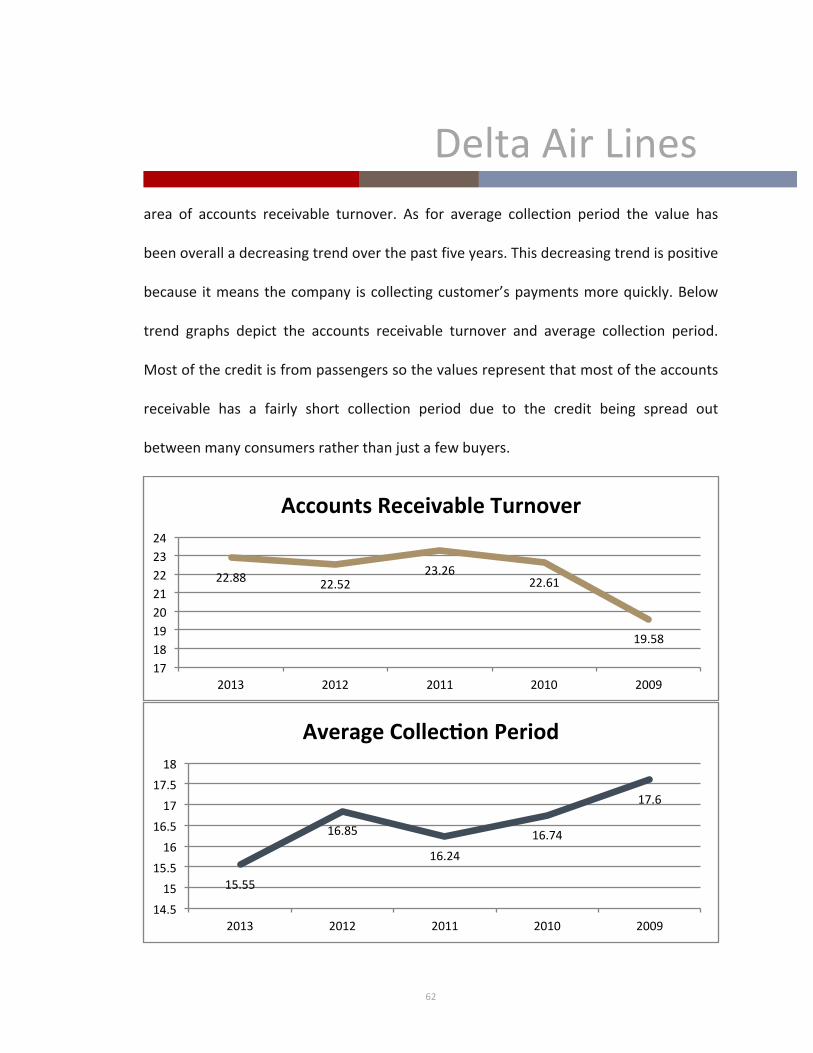

Overthepast fiveyearsDelta’saccountsreceivableturnoverhasfluctuatedup

and down, but had amajor increase after 2009. 2013’s accounts receivable turnover

was higher than 2012’smeaning the company is collectingmore of their receivables

throughouttheyear.Thecompanyoverallhasbeenfairlyconsistentsince2010inthe

DeltaAirLines

62

area of accounts receivable turnover. As for average collection period the value has

beenoveralladecreasingtrendoverthepastfiveyears.Thisdecreasingtrendispositive

because itmeansthecompany iscollectingcustomer’spaymentsmorequickly.Below

trend graphs depict the accounts receivable turnover and average collection period.

Mostofthecreditisfrompassengerssothevaluesrepresentthatmostoftheaccounts

receivable has a fairly short collection period due to the credit being spread out

betweenmanyconsumersratherthanjustafewbuyers.

22.8822.52

23.2622.61

19.58

17

18

19

20

21

22

23

24

2013 2012 2011 2010 2009

AccountsReceivableTurnover

15.55

16.85

16.24

16.74

17.6

14.5

15

15.5

16

16.5

17

17.5

18

2013 2012 2011 2010 2009

AverageCollecXonPeriod

DeltaAirLines

63

Thecompanyestimatestheirbaddebtsexpensebyusinghistoricalchargebacks,

write-offs, bankruptcies and other specific analyses, but the bad debts expense is

immaterial and therefore fairly irrelevant. But the bad debts expense data does

illuminate that the company is typically predicting less bad debts expense each year

over the past five years, meaning that the company is expecting to receivemore of

accountsreceivablepayments.Theeffectofalowbaddebtsexpensewouldbehigher

net incomebecause the companywouldhave less expense reportedon their income

statement.

AcompanysuchasDeltaAirLinesmaymanipulatetheiraccountsreceivable in

order to increasenet income.Theirbaddebtsexpense is immaterial,meaning itdoes

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

2013 2012 2011 2010 2009

BadDebtsExpenseasaPercentofA/R

DeltaAirLines

64

nothaveahugeeffectontheaccountsreceivable.However,thelowestimationcould

have been purposeful. By reporting less bad debts expense, Delta is decreasing the

amountofexpensesreportedontheincomestatementandconsequentlyincreasingnet

income.Thatbeingsaid,itmakessenseforDeltatohavefairlylowbaddebtsexpense

due to the large amount of accounts receivable being low amount consumer airfare

creditpurchases.Channel stuffingwouldbedifficult tomanipulatedue to the limit in

theamountofproduct(numberofseats)availabletoselltoconsumers.Inotherwords,

there is a limit in theamount the company can report as sales throughadistribution

channel.Meaning that channel stuffing ismost likely notwhereDeltaAir Lines could

manipulateaccountsreceivable. Finally,thereisapossibilityofthecompanyselling it

accountsreceivable.Thiswouldcauseartificiallyhighrevenueduetothe“collection”of

theaccountsreceivable,whichwouldcausenetincometoincrease.Thecompanycould

bemotivatedtomanipulateaccountsreceivablebecausestakeholderstendtoonlycare

about income.Havingabiggerbottomlinewouldmotivatecompaniestoperformthis

typeofmanipulation.

INVENTORY

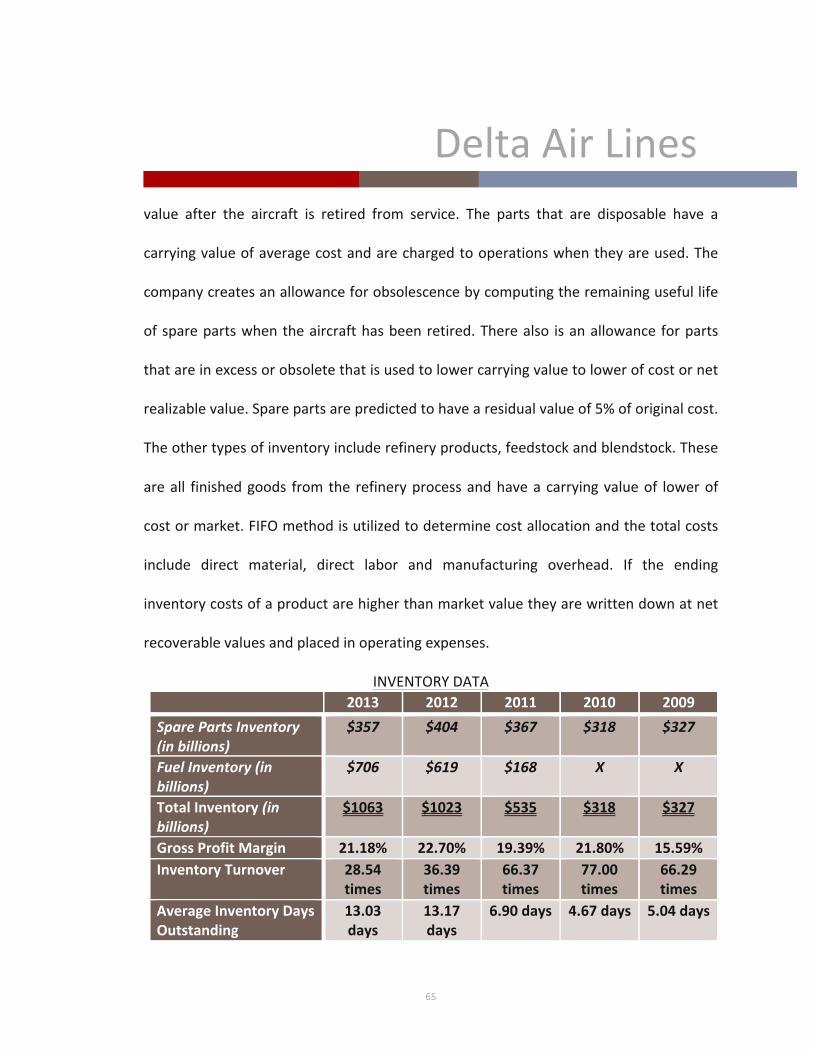

According to the 10-K, Delta Airlines’ types of inventory fall in two main

categories: Spare Parts and Refinery Items. Spare parts inventory includes disposable

partsrelatedtoflightequipmentthatcannotbereusedandthenflightpartsthathave

DeltaAirLines

65

value after the aircraft is retired from service. The parts that are disposable have a

carryingvalueofaveragecostandarechargedtooperationswhentheyareused.The

companycreatesanallowanceforobsolescencebycomputingtheremainingusefullife

ofsparepartswhentheaircrafthasbeenretired.Therealso isanallowanceforparts

thatareinexcessorobsoletethatisusedtolowercarryingvaluetolowerofcostornet

realizablevalue.Sparepartsarepredictedtohavearesidualvalueof5%oforiginalcost.

Theothertypesofinventoryincluderefineryproducts,feedstockandblendstock.These

areall finishedgoods fromthe refineryprocessandhaveacarryingvalueof lowerof

costormarket.FIFOmethodisutilizedtodeterminecostallocationandthetotalcosts

include direct material, direct labor and manufacturing overhead. If the ending

inventorycostsofaproductarehigherthanmarketvaluetheyarewrittendownatnet

recoverablevaluesandplacedinoperatingexpenses.

INVENTORYDATA

2013 2012 2011 2010 2009

SparePartsInventory(inbillions)

$357 $404 $367 $318 $327

FuelInventory(inbillions)

$706 $619 $168 X X

TotalInventory(inbillions)

$1063 $1023 $535 $318 $327

GrossProfitMargin 21.18% 22.70% 19.39% 21.80% 15.59%InventoryTurnover 28.54

times36.39times

66.37times

77.00times

66.29times

AverageInventoryDaysOutstanding

13.03days

13.17days

6.90days 4.67days 5.04days

DeltaAirLines

66

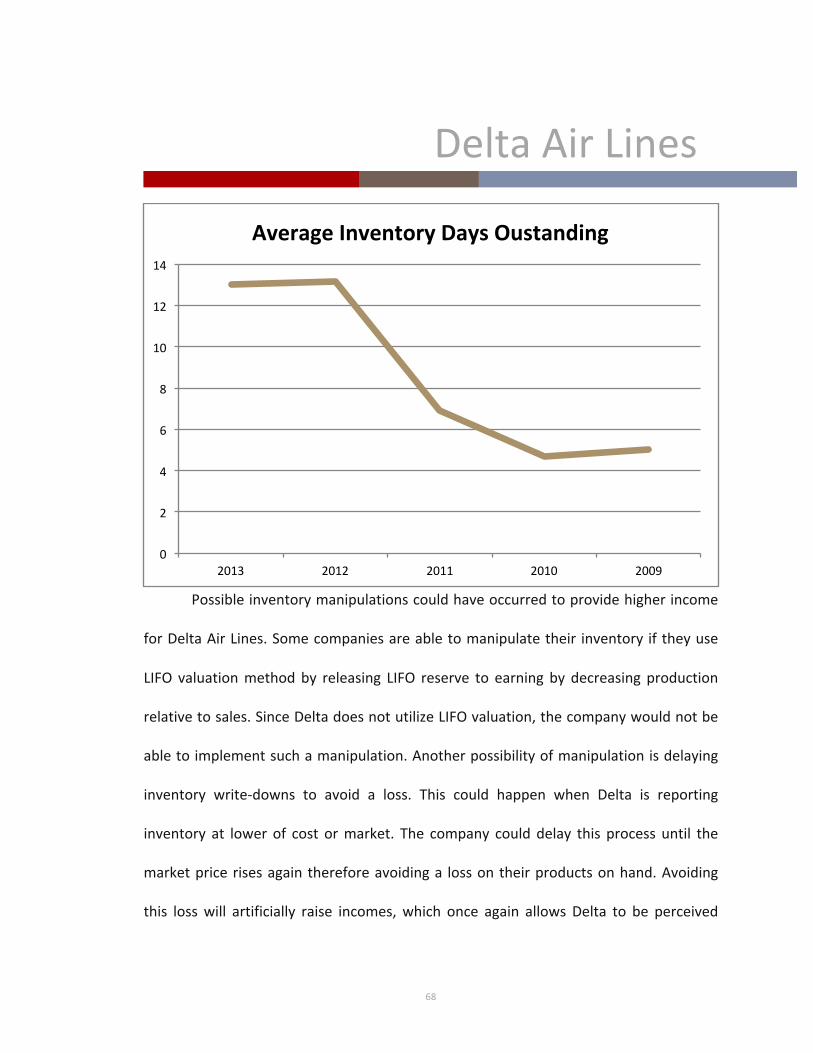

Thegrossprofitmarginoverthepastfiveyearsincreasedgreatlyafter2009,but

since thenhas stayed fairly stablewith a slight drop in 2010. The gross profitmargin

depicts theamounta company receives for a saleof aproductonce costshavebeen

deducted.Aconstantgrossprofitmarginprovidesthatcostsperunitandsalespriceper

unitarestayingrelativelystableaswell.Whenlookingatbothinventoryturnoverand

average inventorydaysoutstanding,adramaticchangeoccurs in2010andthereafter.

This is due to the implementation of the refinery segment for Delta Airlines. Delta

refinescrudeoiltojetfuelthattheyutilizeontheirownaircraftsandselltheexcessto

otherairlinecarriers.BecauseDeltausessomeofitsinventoryforitsownservices,the

inventory turnover decreased significantly and average inventory days outstanding

increaseddrasticallydue toan increase in theamountof inventoryonhandbut little

change in the amount of sales. Although a low inventory turnover and high average

inventorydaysoutstanding is typically anegativeattribute, thedata is abit distorted

duetoDelta’srefinerysegmentimplementation.

DeltaAirLines

67

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

2013 2012 2011 2010 2009

GrossProfitMargin

GrossProfitMargin

0

10

20

30

40

50

60

70

80

90

2013 2012 2011 2010 2009

InventoryTurnover

InventoryTurnover

DeltaAirLines

68

Possibleinventorymanipulationscouldhaveoccurredtoprovidehigherincome

forDeltaAirLines.Somecompaniesareabletomanipulatetheir inventory iftheyuse

LIFO valuationmethodby releasing LIFO reserve to earning by decreasing production

relativetosales.SinceDeltadoesnotutilizeLIFOvaluation,thecompanywouldnotbe

abletoimplementsuchamanipulation.Anotherpossibilityofmanipulationisdelaying

inventory write-downs to avoid a loss. This could happen when Delta is reporting

inventory at lower of cost ormarket. The company could delay this process until the

marketpricerisesagainthereforeavoidinga lossontheirproductsonhand.Avoiding

this losswill artificially raise incomes,which once again allows Delta to be perceived

0

2

4

6

8

10

12

14

2013 2012 2011 2010 2009

AverageInventoryDaysOustanding

DeltaAirLines