hot topics in financial reporting - final - hugmnhugmn.org/downloads/techday2010/hot topics in...

TRANSCRIPT

Hot Topics in Financial ReportingMike MalwitzDirector, Product StrategyOracle CorpMarch 2010

© 2009 Oracle Corporation

Picture This…A World With

• Clear Regulatory Guidelines

• Global Accounting Standards

• Complete Corporate Transparency

• Fast, Easy Comparability of Financial Results

• Easy, Streamlined Corporate Reporting

© 2009 Oracle Corporation

Instead, we have…

© 2009 Oracle Corporation

Instead, we have…

SOXSOXSOXSOX

Auditing Auditing Auditing Auditing Standard #5Standard #5Standard #5Standard #5

IFRSIFRSIFRSIFRS

XBRLXBRLXBRLXBRL

GRCGRCGRCGRC

© 2009 Oracle Corporation

Agenda

• Hot Topics – What Are they?

• What is Oracle Doing to Address?

© 2009 Oracle Corporation6

AMERICAS • HIPAA• FDA CFR 21 Part 11• OMB Circular A-123• SEC & DoD Records Retention• USA PATRIOT Act• Gramm-Leach-Bliley Act• Federal Sentencing Guidelines • Foreign Corrupt Practices Act• Market Instruments 52 (Canada)

EMEA• EU Privacy Directives• UK Companies Law• Restriction of Hazardous

Substances (ROHS/WEE)

APAC• J-SOX, C-SOX, K-S0X,

C49 • CLERP 9: Audit Reform &

Corporate Disclosure Act (Australia)

• Stock Exchange of Thailand Code on Corporate Governance

GLOBAL• International Accounting Stds• Basel II (Global Banking)• OECD Guidelines on

Corporate Governance

Obama JintaoSarkozyGordon

Calls for Increased Regulatory Scrutiny

© 2009 Oracle Corporation

Global Momentum Towards IFRS

Source: IASB, Dec 2007

Countries seeking convergence with the IASB or pursuing adoption of IFRSs

Countries that require or permit IFRSs

© 2009 Oracle Corporation

US GAAP vs IFRS: What’s Different?IFRS is More “Principle Based” not “Rule Based”

IFRS: 250 PagesUS GAAP: 25,000 Pages

© 2009 Oracle Corporation

9

© 2009 Accenture All Rights Reserved.

US

D S

pen

t in

Millio

ns o

n IF

RS

Co

nv

ers

ion

Company RevenuesCompany Revenues

US

D S

pen

t in

Millio

ns o

n IF

RS

Co

nv

ers

ion

The amount of estimated spend on IFRS varies widely within each category of company size, with some companies in the same size category expecting to spend far more than their peers.

Accenture Survey InsightsInvestment Analysis

$23.2M$27.1M

$48.5M

$131.9M

$160.9M

$0.0

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

$140.0

$160.0

$180.0

$1 Billion to

$4.9 Billion US

$5 Billion to

$9.9 Billion US

$10 Billion to

$19.9 Billion US

$20 Billion to

$49.9 Billion US

$50 Billion US

or more

0.731%

0.200%

0.141%

0.103%

0.298%

0.000%

0.100%

0.200%

0.300%

0.400%

0.500%

0.600%

0.700%

0.800%

$1 Billion to

$4.9 Billion US

$5 Billion to

$9.9 Billion US

$10 Billion to

$19.9 Billion US

$20 Billion to

$49.9 Billion US

$50 Billion US

or more

Source: Accenture 2008 IFRS Survey Source: Accenture 2008 IFRS Survey

© 2009 Oracle Corporation

10

© 2009 Accenture All Rights Reserved.

More than 50 percent of the sample has assessed the impact of IFRS conversion on all systems as more than moderate or significant.

4.04

3.92

3.89

3.85

3.82

3.75

Average rating:

What is your assessment of the impact of IFRS conversion to the following systems?

Percentage of Respondents

4%

2%

2%

2%

2%

2%

9%

9%

9%

8%

5%

5%

27%

26%

24%

24%

27%

20%

27%

31%

32%

28%

27%

32%

32%

32%

33%

37%

38%

41%

0% 20% 40% 60% 80% 100%

Projects and fixed assets

Consolidation systems

Tax applications

General accounting ledgers

Revenue systems

Reporting and analytic systems

1 Not at all 2 3 Moderately 4 5 Significantly

2008 Accenture Survey on IFRSSystem Impacts

Source: Accenture 2008 IFRS Survey

© 2009 Oracle Corporation

Source: PricewaterhouseCoopers

Increasing Demand for Non-Financial Information

New metrics for valuation

Board-level focus on reputation, social responsibility and sustainability

Publishing of key non-financial information along side financial data

© 2009 Oracle Corporation

Corporate Governance and Sustainability are in Focus

• Standard & Poors Corporate Governance Scores

• FTSE/ISS Corporate Governance Indices

• Dow Jones Sustainability Indices

• Ethibel Sustainability Indices

© 2009 Oracle Corporation13

50% of Financial Reporting is OperationalDozens of Industry-specific Metrics in 10K Filings

How much of your financial reporting is made up of operational data—currently vs. two years ago vs. two years from now?

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

>10%

11-30%

31-50%

50%+

Two years from now

Currently

Two years ago

• 40% of respondents believe

operational data will make up

more than half of financial reporting,

compared with 25% today.

• The change from two years ago is

even more striking—only one in five

said operational data made up more

than half of financial reporting two

years ago.

© 2009 Oracle Corporation

PCAOB Auditing Standard #5http://www.pcaobus.orgThe “Final Word” Regarding Sarbanes-Oxley

© 2009 Oracle Corporation

Financial Process Continues to Incur Control Weaknesses CFOs struggle to improve governance of their financial processes

SEC FACT:

Auditing Standard No. 5 (AS5) directs auditors to focus on those areas that present the highest risk, such as the financial statement close process and controls designed to prevent fraud by management.

Source: SEC Approves PCAOB Auditing Standard No. 5, July 2007

Percentage of Internal Control

Weaknesses by Category

Personnel

Issues

17%

Financial

Close and

Controls

37%

Significant

Account

Level

40%

Other

6%

Source: Market Reactions to the Disclosure of Internal Control Weaknesses and to the

Characteristics of those Weaknesses Under Section 302 o the Sarbanes Oxley Act Of 2002, July 2007

© 2009 Oracle Corporation

“COSO 2” Enterprise Risk Management Framework

• What is it? “Gold Standard” for Internal Controls

— The four objectives categories - strategic, operations, reporting and compliance - are represented by the vertical columns.

— The eight components are represented by horizontal rows.

— The entity and its organizational units are depicted by the third dimension of the matrix.

© 2009 Oracle Corporation

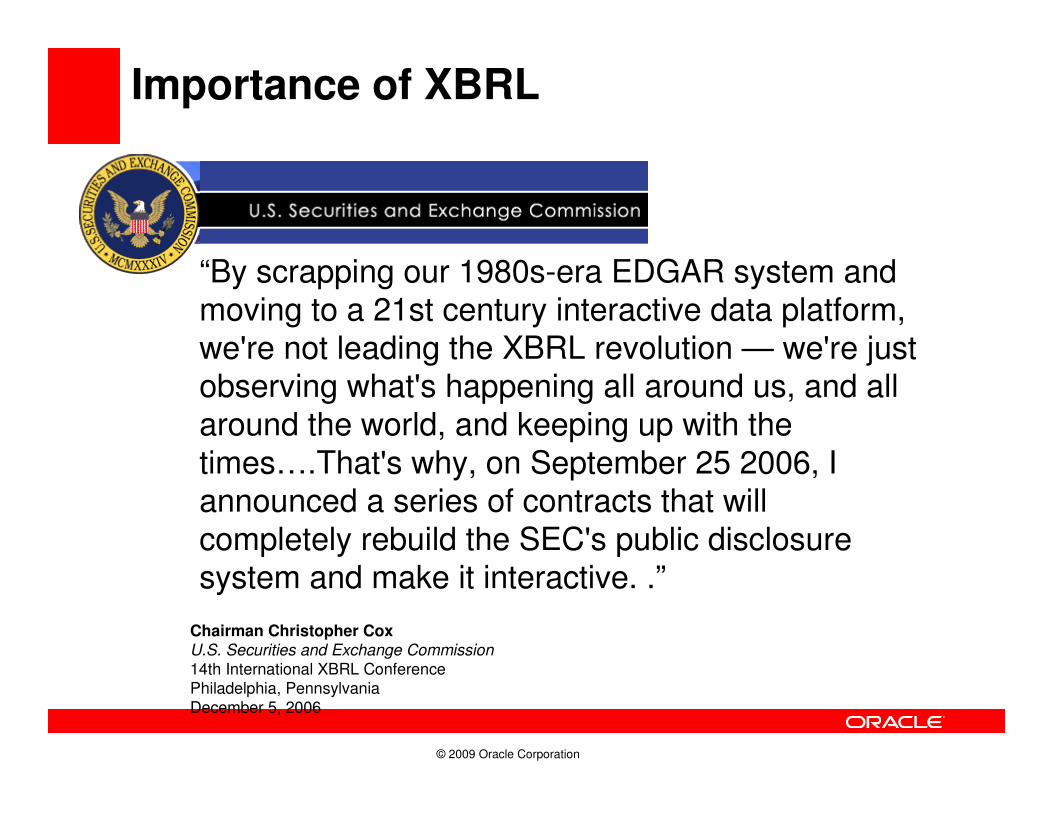

Importance of XBRL

Chairman Christopher CoxU.S. Securities and Exchange Commission

14th International XBRL ConferencePhiladelphia, PennsylvaniaDecember 5, 2006

“By scrapping our 1980s-era EDGAR system and moving to a 21st century interactive data platform, we're not leading the XBRL revolution — we're just observing what's happening all around us, and all around the world, and keeping up with the times….That's why, on September 25 2006, I announced a series of contracts that will completely rebuild the SEC's public disclosure system and make it interactive. .”

© 2009 Oracle Corporation

What is XBRL?

• eXtensible Business Reporting Language

• “Interactive Reporting”for investors and analysts

• Standardizes how to exchange financial information• Semantics

• Validation

• Dynamic extensibility

• Business rules

• Intended to replace current “Edgar” system

© 2009 Oracle Corporation

The SEC Rule Proposal Started Jun 2009

• Who? Public Companies on US Exchanges

• June 09 – Large accelerated filers with public float over $5Billion

• June 2010 – All large accelerated filers (public float over $700Million)

• June 2011 – The rest of public and foreign filers (IFRS)

• What? Addendum to 10K/Q

• Year 1 – Financial statements & notes and disclosures to the financial statements (block text)

• Year 2 - Financial statement & notes and disclosures to the financial statements (detail tagging)

XBRL: the “barcode”

for business reporting

© 2009 Oracle Corporation

Agenda

• Hot Topics – What Are they?

• What is Oracle Doing to Address?

© 2009 Oracle Corporation

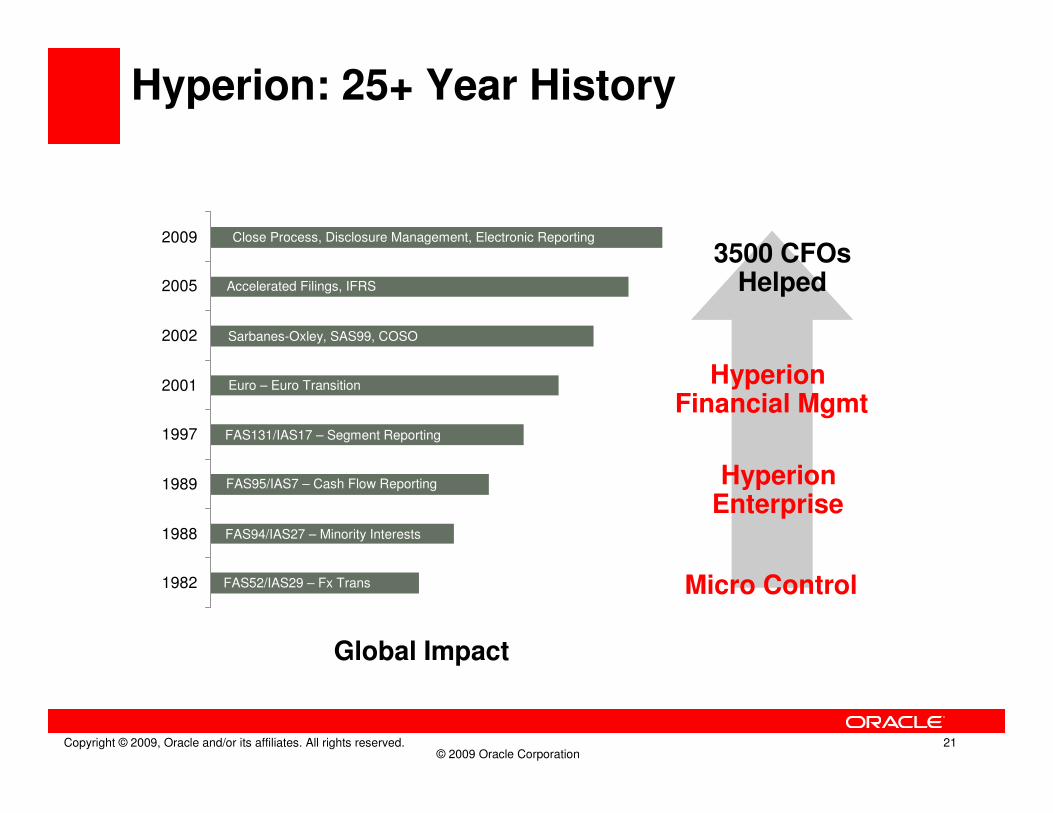

Hyperion: 25+ Year History

1982

1988

1989

1997

2001

2002

2005

2009 Close Process, Disclosure Management, Electronic Reporting

Accelerated Filings, IFRS

Sarbanes-Oxley, SAS99, COSO

Euro – Euro Transition

FAS131/IAS17 – Segment Reporting

FAS95/IAS7 – Cash Flow Reporting

FAS94/IAS27 – Minority Interests

FAS52/IAS29 – Fx Trans

Global Impact

Micro Control

Hyperion Enterprise

Hyperion Financial Mgmt

3500 CFOsHelped

Copyright © 2009, Oracle and/or its affiliates. All rights reserved. 21

© 2009 Oracle Corporation

Agenda

• Hot Topics – What Are they?

• What is Oracle Doing to Address?

• IFRS

• World Class Close

• Integrated GRC

• Sustainability Reporting

© 2009 Oracle Corporation

Agenda

• Hot Topics – What Are they?

• What is Oracle Doing to Address?

• IFRS

• World Class Close

• Integrated GRC

• Sustainability Reporting

© 2009 Oracle Corporation

First Time Adoption of IFRS – Retrospective Restatements, not a Cumulative Change

First-time Adoption of International Financial Reporting Standards (IFRS No.1):

Companies electing to adopt the financial reporting standards of the International Accounting Standards Board (IASB) are required to retrospectively apply the international standards that exist as of the company’s adoption of IFRS, to all periods presented as if they had always been in effect.

Net Income Trend

0

20

40

60

80

100

120

140

160

2010 2011 2012 2013 2014

Years

$(0

00,0

00)

USGAAP

IFRS

Difference

© 2009 Oracle Corporation

Impact on US CompaniesStart early for transition period with multi-GAAP

2009: Limited group of large US firms are permitted to use IFRS on an optional basis for fiscal periods ending on or after Dec 15, 2009

2011: SEC evaluates achievement of roadmap milestones and decides whether to adopt a mandatory approach for IFRS

2014: Large accelerate filers begin filing in IFRS

2015: Accelerated filers to begin filing in IFRS

2016: Non-accelerated filers begin filing in IFRS

Source: SEC Announcement, Aug 2008

© 2009 Oracle Corporation

Impact on US CompaniesStart early for transition period with multi-GAAP

2009: Limited group of large US firms are permitted to use IFRS on an optional basis for fiscal periods ending on or after Dec 15, 2009

2011: SEC evaluates achievement of roadmap milestones and decides whether to adopt a mandatory approach for IFRS

2014: Large accelerated filers begin filing in IFRS

2015: Accelerated filers to begin filing in IFRS

2016: Non-accelerated filers begin filing in IFRS

Source: SEC Announcement, Aug 2008

Transition Date?SEC may require 2 years of comparatives. Start Now!

© 2009 Oracle Corporation

All Stages: Apply Policy and Control Management

Determine impact on accounting in

subsystems

Determine impact on accounting in

subsystems

Configure accounting rules

and set up ledgers

Configure accounting rules

and set up ledgers

Process and report using dual accounting

Process and report using dual accounting

Milestone 3Transactions Recorded

in Multiple GAAPs

Stage 3

Record Transactions

in both GAAPS

Stage 3

Record Transactions

in both GAAPS

Milestone 1Completed Preliminary

Study

Stage 1

Study Impact & Determine Strategy

Stage 1

Study Impact & Determine Strategy

Perform Preliminary Study

Perform Preliminary Study

Assess ImpactAssess Impact

Determine Strategy

Determine Strategy

Determine changes to

business model

Determine changes to

business model

Transform operations using

IFRS results

Transform operations using

IFRS results

Report IFRS results, increase

shareholder value

Report IFRS results, increase

shareholder value

Stage 4

Transform Your Business & Win with

IFRS

Stage 4

Transform Your Business & Win with

IFRS

Milestone 4Business Model

Optimized

IFRS Action PlanAchieve “early mover” advantage

Collect GAAP Financial Results

Collect GAAP Financial Results

Adjust and Consolidate

Under GAAP & IFRS

Adjust and Consolidate

Under GAAP & IFRS

Report, Reconcile and Audit ResultsReport, Reconcile and Audit Results

Milestone 2IFRS Reports Produced

Stage 2

Enable Top End Reports

Stage 2

Enable Top End Reports

© 2009 Oracle Corporation

DOCUMENT ATTACHMENTS

CORE CONSOLIDATION FEATURES

FLEXIBLE REPORTING

CUSTOM DIMENSIONS

GAAP IFRS

Flexible Rules Engine

Journal Entries and Audit

Enables tracking of GAAP vs. IFRS adjustments

Multiple reporting standards in a single solution

Creates “Electronic Binder” of all adjustments

Easy to reconcile and trend GAAP vs. IFRS results

Oracle Enterprise Performance Management Enable Top End IFRS Reporting

© 2009 Oracle Corporation

IFRS Adjustments: Different Accounts, Different Systems

- Load differences from ERP Systems

- Enter differences not in ERP Systems

- Pensions

- Tax Reserves

- Share Option Expense

- Etc

- Inventory

- Fixed Assets

- Billing/Revenue

- Fernbach, Etc…

FORM 10-Q/K

- Reconciliations

- Trend Reports

- Filings, Press Releases

- Etc…

© 2009 Oracle Corporation

What’s Required for IFRS

HFM Enterprise

•No Commingling of Accounts

•Workflow Controls

•Data Validations

•Data Audit Trails

•Supporting Documentation

•Disclosure Controls

•Multi-Dimensional Trend Reports

•Partial Ownership Accounting

•Journals Module

•Basic Consolidation Functionality(Intercompany, FX etc.)

Copyright © 2009, Oracle and/or its affiliates. All rights reserved. 30

© 2009 Oracle Corporation

Agenda

• Hot Topics – What Are they?

• What is Oracle Doing to Address?

• IFRS

• World Class Close

• Integrated GRC

• Sustainability Reporting

© 2009 Oracle CorporationCopyright © 2009, Oracle and/or its affiliates. All rights reserved. 32

Close Sub Ledgers into GL (i.e. AR, AP, FA, etc.)

Perform Reconciliations

• Bank Reconciliations

• Standard Account Recon

• Sub Ledger Recon

Post Accruals

Deliver self service reporting to the organization for performance discussions and plan realignment

Automate external reporting gathering disclosures and financial information

Automate and deliver Edgar & XBRL filings, Statutory filings, Tax, etc.

Gather and validate complete data sets to support all financial reporting needs (i.e. Legal Entity, Segment, Management, Tax, Sustainability Metrics, etc.)

Automate consolidated financial reporting leveraging multiple hierarchies and calculations (i.e. CTA, FASB, KPI’s, FX, Retained Earnings, Topside Entries etc.)

Close Process and Key Activities

© 2009 Oracle CorporationCopyright © 2009, Oracle and/or its affiliates. All rights reserved. 33

Workflow and Task Management Issues

• Lack of visibility to tasks across financial systems, departments, regions, etc.

• Manual spreadsheets are used to manage the financial close calendar

• ‘Hope’ and email are core to the process

• Account reconciliations are managed manually

• Task management is fragmented and manual

© 2009 Oracle CorporationCopyright © 2009, Oracle and/or its affiliates. All rights reserved. 34

Document Management and Creation Issues

• Management and creation of critical documents is manual (Debt Covenants, 10Q/K, Board Package and Presentation, etc.)

• Gathering and managing commentary is manual

• Adjustment of financial data is manual

• MS Word documents sent to 3rd party who reformats and files with EDGAR (error prone)

• MS Word files are converted to XBRL by 3rd parties or manually (error prone)

© 2009 Oracle CorporationCopyright © 2009, Oracle and/or its affiliates. All rights reserved. 35

Oracle World Class Financial Close Architecture

Financial

Consolidation

Data

Assurance Disclosure

Management

XBRL/SEC

Financial andMgmt. Reporting

ERP:

Oracle, SAP,

Legacy, Other

Tax

Filing

Financial Close Management

CFO Dashboard

Tax

Calculations

Transactions Reporting

Governance, Risk & Compliance

© 2009 Oracle CorporationCopyright © 2009, Oracle and/or its affiliates. All rights reserved. 36

Streamline the Extended Close Process

• Close Process Analysis,

Trending and Improvement

• Process Monitoring

• Financial Calendar

• Single Task List

• Automated workflow

• Ensure Compliance

• Email and calendaring

(e.g. Outlook)

• Account Reconciliations

© 2009 Oracle CorporationCopyright © 2009, Oracle and/or its affiliates. All rights reserved. 37

TASK MANAGEMENT

PROCESS MONITORING

ACCOUNT RECONCILIATIONS

ACTIVE CALENDAR

Active integration with EPM and ERP systems

Executive Dashboard Views

Centralized web based task management and collaboration

Automation through matching capabilities and integration with all sources

Financial Close ManagementStreamline the Extended Close Process

© 2009 Oracle CorporationCopyright © 2009, Oracle and/or its affiliates. All rights reserved. 38

Disclosure Management

• Covers the entire process of taking a company’s consolidated results and transforming them into specifically stylized statutory filings

• Document creation process manages the entire distributed development of the statutory report

• Simple end user experience leverages user’s preferred document application -Microsoft Word

• Built-in, extensive XBRL reporting capabilities including full instance document creation and validation

• Supports multiple output formats

© 2009 Oracle CorporationCopyright © 2009, Oracle and/or its affiliates. All rights reserved. 39

• Output will support various regulatory authorities

• USGAAP - SEC

• IFRS - European Exchanges, Asia

• The following output formats are supported for the main document:

• Word

• XBRL

• HTML

• XHTML (in-line XBRL)

• EDGAR

XBRL: Just another output format

© 2009 Oracle Corporation

Agenda

• Hot Topics – What Are they?

• What is Oracle Doing to Address?

• IFRS

• World Class Close

• Integrated GRC

• Sustainability Reporting

© 2009 Oracle Corporation

The Inter-related Disciplines of Financial Governance Only Oracle Offers All Three

Enterprise Performance Management

Enterprise Resource Planning

Governance, Risk, and

Compliance

© 2009 Oracle Corporation

GRC DOCUMENTATION REPOSITORY

Oracle Governance, Risk, and Compliance SuiteManage changes to policies and controls

COMPLIANCE WORKFLOW

Single subledger transaction creates multiple accounting representations

APPLICATION CONTROLS MONITORING COMPLIANCE DASHBOARDS

Automate steps to audit IFRS compliance

Record changes to business process due to IFRS

Control changes to ERP applications

Monitor status of testing and exceptions

© 2009 Oracle Corporation43

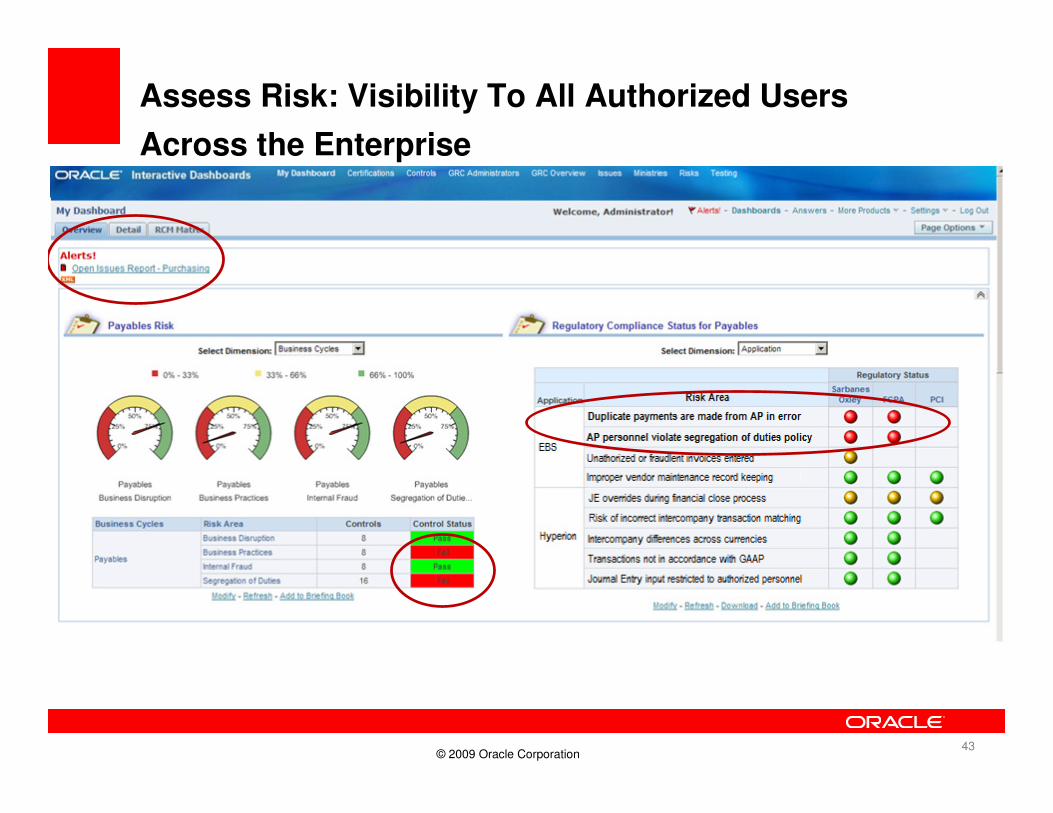

Assess Risk: Visibility To All Authorized Users

Across the Enterprise

© 2009 Oracle Corporation

Enterprise Risk Analysis Intelligence that brings together risk assessment and financial balances

• Consolidated view of financial balances from Hyperion Financial Management and risk rating from GRC Manager

• Intelligent scoping for testing

© 2009 Oracle Corporation

Drill Down to the Root of the IssueVisibility into financial balances

© 2009 Oracle Corporation

Drill Down to the Root of the IssueVisibility into risk indicators

© 2009 Oracle Corporation47

GRC: How Important Is It?CERTIFICATION PURSUANT TO SECTION 302 OF THE SARBANES-OXLEY ACT

I, Lawrence J. Ellison, certify that:1. I have reviewed this quarterly report on Form 10-Q of Oracle Corporation;2. Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the

statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report;

3. Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the registrant as of, and for, the periods presented in this report;

4. The registrant’s other certifying officer and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Exchange Act Rules 13a-15(e) and 15d-15(e)) and internal control over financial reporting (as defined in Exchange Act Rules 13a-15(f) and 15d-15(f)) for the registrant and we have:

a) designed such disclosure controls and procedures or caused such disclosure controls and procedures to be designed under our supervision, to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared;

b) designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed underour supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financialstatements for external purposes in accordance with generally accepted accounting principles;c) evaluated the effectiveness of the registrant’s disclosure controls and procedures and presented in this report our conclusions about the

effectiveness of the disclosure controls and procedures, as of the end of the period covered by this report based on such evaluation; andd) disclosed in this report any change in the registrant’s internal control over financial reporting that occurred during the registrant’s most recent fiscal

quarter that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting; and5. The registrant’s other certifying officer and I have disclosed, based on our most recent evaluation of internal control over financial reporting, to the

registrant’s auditors and the Finance and Audit Committee of the registrant’s board of directors (or persons performing the equivalent functions):a) all significant deficiencies and material weaknesses in the design or operation of internal control over financial reporting which are reasonably

likely to adversely affect the registrant’s ability to record, process, summarize and report financial information; andb) any fraud, whether or not material, that involves management or other employees who have a significant role in the registrant’s internal control

over financial reporting.

Date: December 22, 2008 By: /s/ LAWRENCE J. ELLISONLawrence J. Ellison, Chief Executive Officer and Director

© 2009 Oracle Corporation

Agenda

• Hot Topics – What Are they?

• What is Oracle Doing to Address?

• IFRS

• World Class Close

• Integrated GRC

• Sustainability Reporting

© 2009 Oracle Corporation

Coming Soon…

• Sustainability Reporting Starter Kit for HFM

• “GRI Metrics” Built In

© 2009 Oracle Corporation

Sustainability Reporting in Financial Management

© 2009 Oracle Corporation

Sustainability Reporting in Financial Management

© 2009 Oracle Corporation

Sustainability Reporting in Financial Management

© 2009 Oracle Corporation

Q & A

Copyright © 2009, Oracle and/or its affiliates. All rights reserved. 53

You can also email me at [email protected]