how to keep oi going in a decentralized structure to keep open innovation going in a decentralized...

TRANSCRIPT

How to Keep Open Innovation Going in a Decentralized Structure Spring ETN Meeting March 19, 2015

Joe Fox Director, Emerging & External Technologies Ashland Performance Materials

2

An Overview of Ashland Inc. • Over the past decade, Ashland has transformed itself from an oil company to

a global, diversified specialty chemical company

• Strengthened by the acquisition of Hercules in 2008 and International Specialty Products (ISP) in 2011

• Ashland’s total sales in 2014 were $6B.

• Three operating divisions:

3 An Overview of Ashland Inc. I represent

Performance Materials

4

• Business-to-Business focus

• Major product lines - Resins for composites - Intermediates & Solvents

• Composite resins are based on thermoset resin chemistry

- Unsaturated polyesters - Vinyl esters

• Key intermediates and solvents:

- Butanediol, THF, Butyrolactone, N-Methyl Pyrrolidone

Resins for Composites

Ashland Performance Materials (APM)

5

Material Substitution & Material Enhancement

• APM’s composites business looks for opportunities to substitute composites for more traditional materials of construction

- Metals • Steel • Aluminum

- Wood - Concrete

• We also look for opportunities to enhance the performance of traditional materials of construction

- Concrete + composites

Composite foundation walls

6

External Technology: Motivation & Approach

• Motivation: - Accelerate the development of new products, services and applications - Spur innovation - Supplement our internal resources with external resources

• Approach:

- Connect Ashland with other companies, universities, federal laboratories and other organizations that have already developed technology / products that we can use.

7

Ashland’s Partnering Strategy

• Performance Materials looks for both upstream and downstream partners in the value chain.

• Upstream partners - Biorenewable raw materials

• Downstream partners

- Fabricators - Channel-to-market

Consumer Fabricated Product

Formulated Materials

Intermediate Materials

Raw Material

Ashland plays here

Ashland looks for partners here

Ashland looks for partners here

8

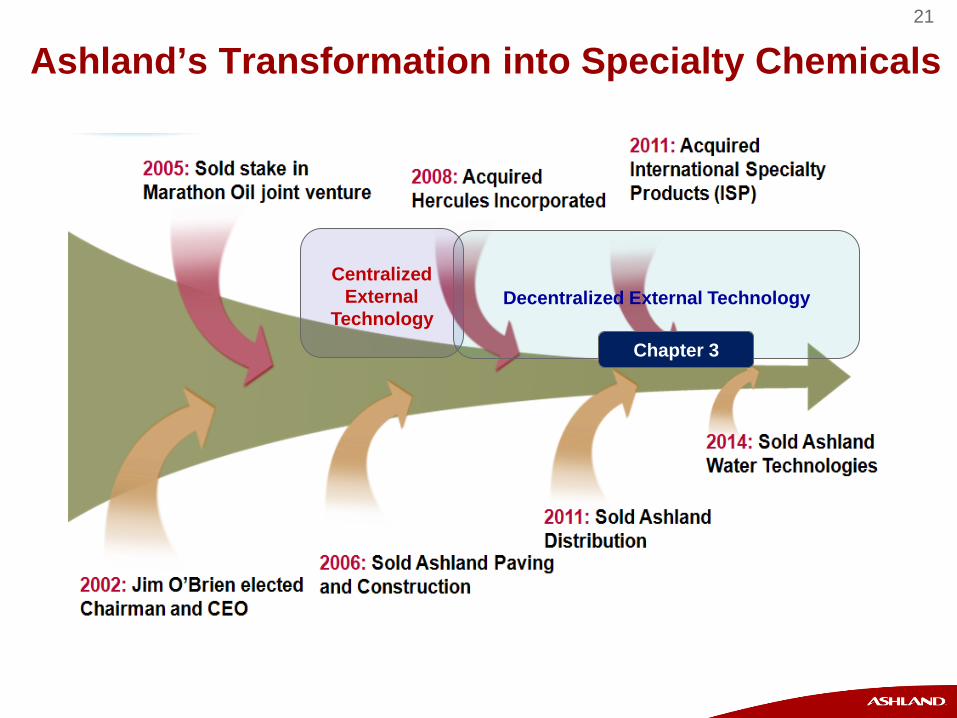

Ashland’s Transformation into Specialty Chemicals

9

Ashland’s Transformation into Specialty Chemicals

Centralized

External Technology

Decentralized External Technology

10

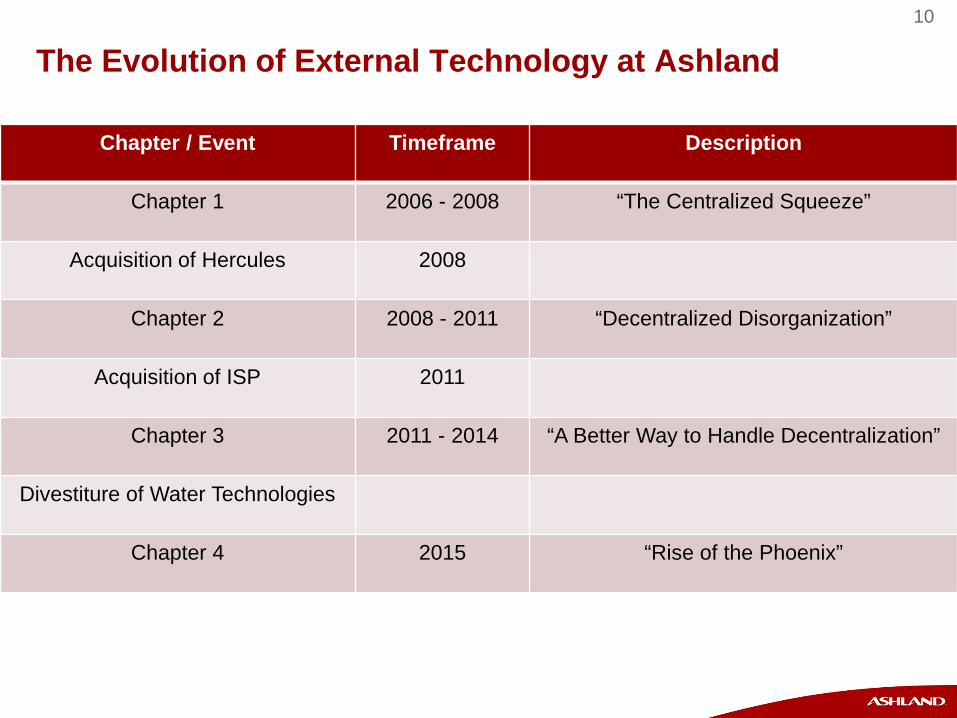

The Evolution of External Technology at Ashland

Chapter / Event Timeframe Description

Chapter 1 2006 - 2008 “The Centralized Squeeze”

Acquisition of Hercules 2008

Chapter 2 2008 - 2011 “Decentralized Disorganization”

Acquisition of ISP 2011

Chapter 3 2011 - 2014 “A Better Way to Handle Decentralization”

Divestiture of Water Technologies

Chapter 4 2015 “Rise of the Phoenix”

11

Ashland’s Transformation into Specialty Chemicals

Centralized

External Technology

Decentralized External Technology

Chapter 1

12

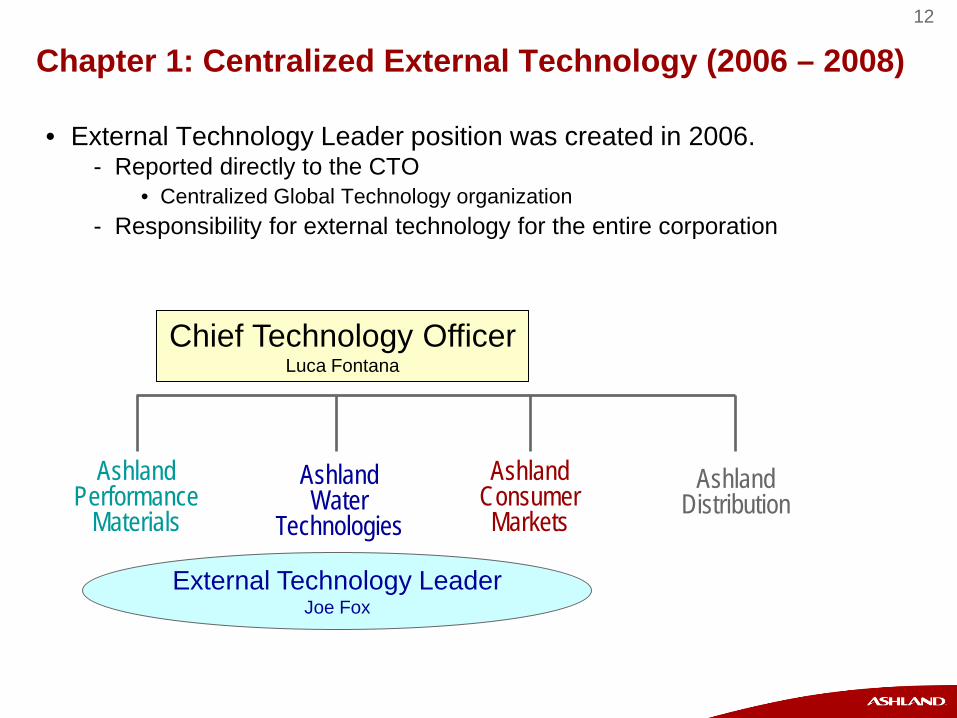

Chapter 1: Centralized External Technology (2006 – 2008)

• External Technology Leader position was created in 2006. - Reported directly to the CTO

• Centralized Global Technology organization - Responsibility for external technology for the entire corporation

Ashland Consumer Markets

Ashland Performance

Materials

Ashland Water

Technologies

Ashland Distribution

$3.9B $1.4B $0.5B $1.4B

Chief Technology Officer Luca Fontana

External Technology Leader Joe Fox

13 Centralized External Technology Function: Pros & Cons

• Pros: - Centralized function brought consistency

• Best practices for working with open innovation intermediaries - Corporate budget

• Ability to fund university programs that had the potential for multiple-division impact

- Global coordination • Tapped into European Technical Council formed by the CTO

• Cons: - Too much ground for one person to cover - Way too much ground for one person to cover

Chapter 1:

“The Centralized Squeeze”

During this time, the ETN was an invaluable source of best practices

14

Ashland’s Transformation into Specialty Chemicals

Centralized

External Technology

Decentralized External Technology

Chapter 2

15 The Acquisition of Hercules (2008)

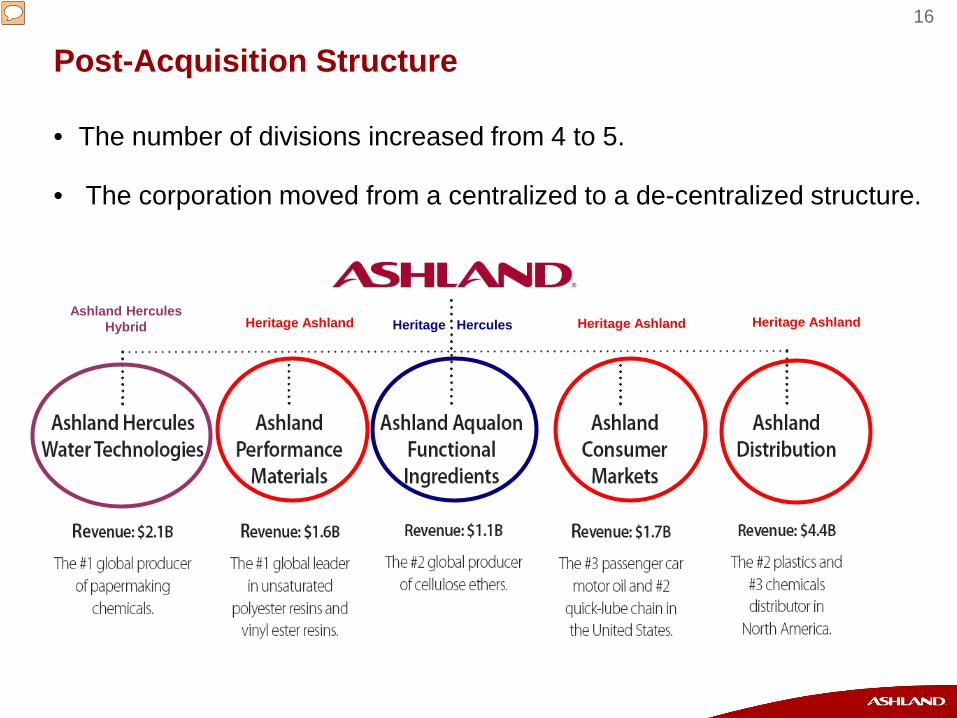

• In late 2008, Ashland acquired Hercules and strengthened its position as a specialty chemicals company.

• The corporation moved from 4 divisions to 5 divisions.

• At the same time, the corporation moved from a centralized to a de-centralized structure.

Ashland Consumer Markets

Ashland Performance

Materials

Ashland Water

Technologies

Ashland Distribution

$3.9B $1.4B $0.5B $1.4B

Pre-acquisition Structure

16

Post-Acquisition Structure

• The number of divisions increased from 4 to 5.

• The corporation moved from a centralized to a de-centralized structure.

Heritage Ashland Heritage Ashland Heritage Ashland Heritage Hercules Ashland Hercules

Hybrid

External Technology at Ashland Moving from a Centralized to a De-Centralized Framework

IRI External Technology Network Spring Meeting February 24, 2011

Joe Fox Director of Emerging & External Technologies Ashland Performance Materials

18

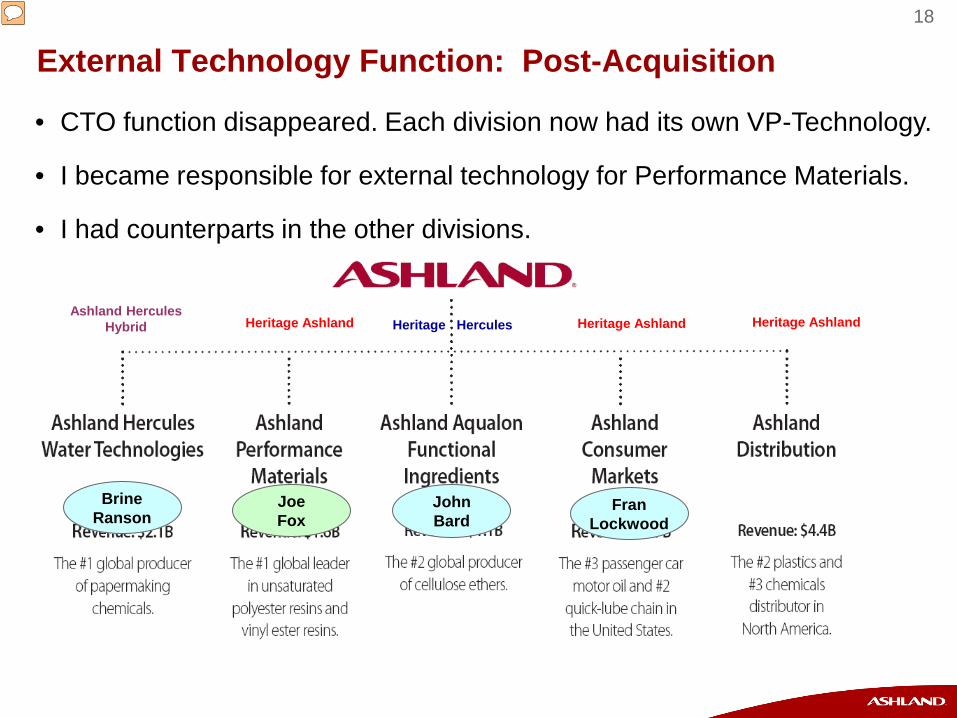

External Technology Function: Post-Acquisition

• CTO function disappeared. Each division now had its own VP-Technology.

• I became responsible for external technology for Performance Materials.

• I had counterparts in the other divisions.

Heritage Ashland Heritage Ashland Heritage Ashland Heritage Hercules Ashland Hercules

Hybrid

Brine Ranson

Joe Fox

John Bard

Fran Lockwood

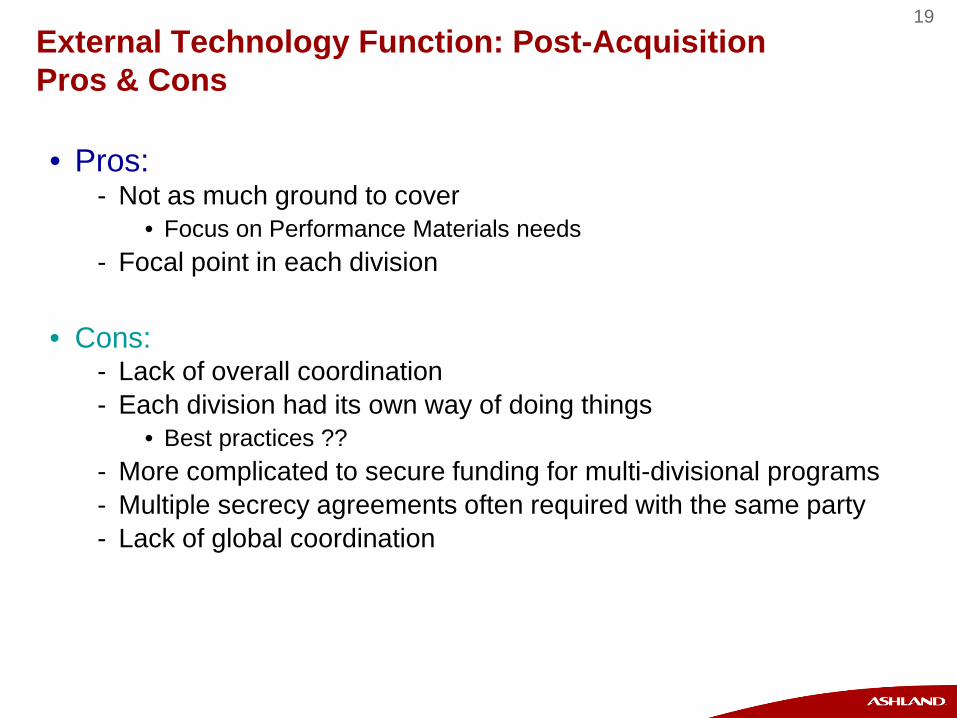

19 External Technology Function: Post-Acquisition Pros & Cons

• Pros: - Not as much ground to cover

• Focus on Performance Materials needs - Focal point in each division

• Cons:

- Lack of overall coordination - Each division had its own way of doing things

• Best practices ?? - More complicated to secure funding for multi-divisional programs - Multiple secrecy agreements often required with the same party - Lack of global coordination

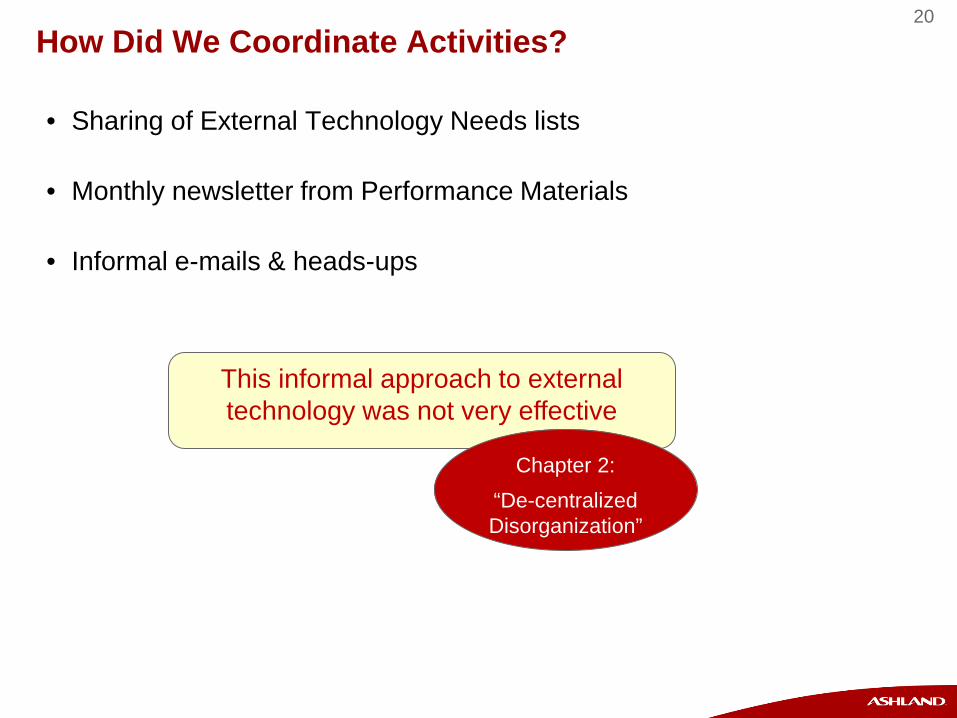

20 How Did We Coordinate Activities?

• Sharing of External Technology Needs lists

• Monthly newsletter from Performance Materials

• Informal e-mails & heads-ups

This informal approach to external

technology was not very effective

Chapter 2:

“De-centralized Disorganization”

21

Ashland’s Transformation into Specialty Chemicals

Centralized

External Technology

Decentralized External Technology

Chapter 3

22

The Evolution of External Technology at Ashland

Chapter / Event Timeframe Description

Chapter 1 2006 - 2008 “The Centralized Squeeze”

Acquisition of Hercules 2008

Chapter 2 2008 - 2011 “Decentralized Disorganization”

Acquisition of ISP 2011

Chapter 3 2011 - 2014 “A Better Way to Handle Decentralization”

Divestiture of Water Technologies

Chapter 4 2015 “Rise of the Phoenix”

23

The Acquisition of ISP

• In 2011, Ashland divested its Distribution business and quickly purchased International Specialty Products (ISP).

• This set of moves was consistent with the corporate strategy to move to specialty chemicals with higher margins.

• ISP was combined with the Aqualon division to form Ashland Specialty Ingredients (ASI).

- Global operations - Wilmington DE and Bridgewater NJ = key North American centers

24

Once again, ETN provided a very helpful perspective

25

Mike shared various organizational models for

Open Innovation & External Technology

26

27

28 Organizational Structures for External Technology

• Centralized Approach: Corporate group handles all the scouting and agreements for the entire corporation.

• Decentralized Approach: All activities occur separately within the divisions

• Most ETN members agreed that a centralized-decentralized hybrid model is the best organizational structure.

• This model was the genesis of Ashland’s External Technology Council.

Courtesy of Mike Cameron, Sherwin Williams

External Technology

Council

29

Getting Close to the Ideal State

• Centralized / De-Centralized Hybrid - Central group

• Best practices Templates for Legal agreements

• Budgets for cross-divisional programs & activities

- External Technology Leaders in each division • Full-time responsibility, not part-time

• Ashland did not form a corporate External Technology group, but we did create an External Technology Council to bring the divisions closer together on a less informal basis.

30 Ashland’s External Technology Council (ETC) • The External Technology Council (ETC) was formed in May 2011. It consisted

of a representative from each division.

• The Council met quarterly - In-person meetings

• R&D centers in Wilmington, Lexington & Dublin

- By Webex

• Topics of discussion: - Best practices - Technology needs lists - Networks - Issues - Special topics

• Accessing external technology through VCs • Open Innovation intermediaries

- Accessing technology from other Ashland divisions - Opportunities with potential inter-divisional impact

Meetings were patterned after ETN meetings

APM Joe Fox

ASI Sheila Murphy

AWT Darcy Culkin

Valvoline Dan Dotson

31 Ashland’s External Technology Council (ETC) • The External Technology Council (ETC) was formed in May 2011.

It consisted of a representative from each division.

• Members of the Council (besides Joe) began to attend ETN meetings.

• The Council facilitated interactions between divisions and leveraged resources from the other divisions

- Lab tours during in-person meetings - Accessing technology from other Ashland divisions

• Inter-divisional internal webinar series - Opportunities with potential inter-divisional impact

• Mining / fracking • Biorefineries

APM ASI

AWT Valvoline

Chapter 3:

“A Better Way to Handle

Decentralization””

32

Ashland’s Transformation into Specialty Chemicals

Centralized

External Technology

Decentralized External Technology

Chapter 4

33

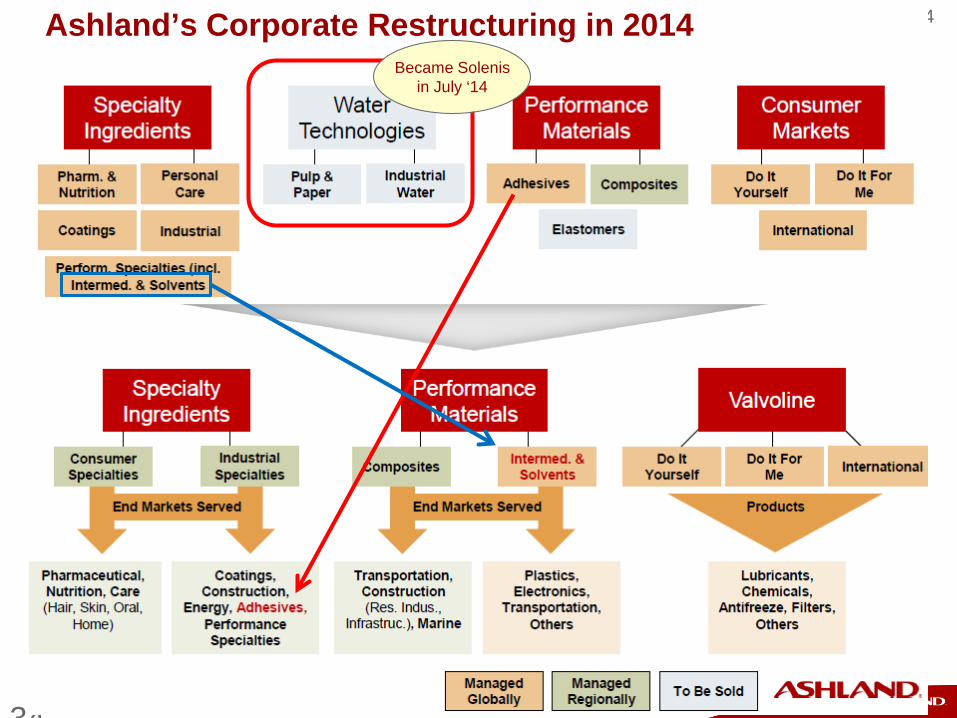

Divestiture of Water Technologies in 2014

• The Water Technologies Division was divested in July of 2014.

• The remaining three divisions were restructured and rightsized.

Adhesives & Resins for Composites

Water Treatment Chemicals

Functional Additives

Formulated Motor Oils

Water Technologies

Specialty Ingredients

Performance Materials

Consumer Markets

Became Solenis in July ‘14

34

34

Ashland’s Corporate Restructuring in 2014 Became Solenis

in July ‘14

35 Impact of the Corporate Restructuring on the ETC

• Three representatives “left” the Council - Water Technologies was being divested - The representatives from Valvoline and Specialty Ingredients decided to

take a voluntary separation program offered as part of the rightsizing

• The ETC was temporarily disbanded in February 2014 during the corporate restructuring

• In January 2015, the ETC was re-formed with new members from Valvoline and Specialty Ingredients

• Current members: - APM Joe Fox - ASI JJ Gulka, David Hood - Valvoline Jesse Dambacher

Chapter 4:

“Rise of the Phoenix””

36

Ashland’s Transformation into Specialty Chemicals

Centralized

External Technology

Decentralized External Technology

Chapter 1 Chapter 4 Chapter 3 Chapter 2

37 Lessons Learned

• The ETN has been a very valuable source of best practices and advice.

• In the absence of a corporate OI group, Ashland’s use of an informal External Technology Council has worked well in a decentralized structure.

- Information sharing - Common approaches - Leveraged resources

• An even better structure would be a true centralized / decentralized hybrid. - Small corporate group for best practices & cross-divisional OI budget - Decentralized activities / scouting in the divisions

• Area for improvement: Coordination on a global basis

- The current ETC is still North American-centric

39

Backup

40

40

The Value Chain for Composites

End Users Fabricated Composite

Building Product

Fully-Formulated Resin

Resin

Intermediate

Raw Material

Ashland plays here.

Bio-based

Petroleum-based

Recycled

Ashland’s customers play here.

Examples:

Automotive OEMs Building Contractors

Wind Turbine Manufacturers

41

APM’s Partnering Strategy

• Performance Materials looks for both upstream and downstream partners in the value chain.

• Upstream partners - Biorenewable raw materials - Replacements for styrene

• Downstream partners - Fabricators - Channel-to-market

Consumer Fabricated Product

Formulated Materials

Intermediate Materials

Raw Material

Ashland plays here

Ashland looks for partners here

Ashland looks for partners here

Envirez resins (multiple partners) Styrene replacement (Tetramer+ Purac)

CIPS countertops (VT Industries) Composite Panels -- Foundations (FiberTech + Cornerstone) -- Exterior panels (Acell)

42 The “WFGM” Model

Want What external resources do we need to succeed in our mission?

Find

Get

Manage

What mechanisms will we use to find these resources?

What processes will we use to plan, structure & negotiate an agreement to access the resources?

What tools, metrics & management techniques will we use to implement the relationship?

External Technology Needs List

Networks

Companies, Universities, Federal Labs,

Open Innovation Intermediaries

Alliance Framework

Project Leadership

43 Lessons Learned

• Upstream and downstream partnerships make it easier to go from A to Z in the value chain and to create new opportunities for growth.

• IRI’s External Technology Network is an excellent source of best practices.

• The ideal organization for Ext Tech is a centralized / de-centralized hybrid. - Ashland’s approach = External Technology Council

• There needs to be a commitment to follow through on External Technology. - Budget + Dedicated resources - Commitment of technical, commercial and legal resources

• Multi-department and multi-university ERCs and I/UCRCs are a very effective networking tool on the academic front.

• Open Innovation intermediaries can be an effective tool for finding external technology

- Especially at small to medium-sized companies - Global reach

44

45

46

47

48

49

Ashland before the acquisition of

Hercules

50

External Technology

Council

Ashland after the acquisition of

Hercules

51 Ashland Performance Materials Needs List

• Composites - Bio-based resin building blocks

• For unsaturated polyester (UPE) and vinyl ester (VE) resins - Styrene replacement / reduction in UPE and VE resins - Resins with improved fire resistance

• Lower smoke and toxicity - Low density composites

• Natural fiber-based - Antifouling gel coats - New uses of composites

• Adhesives - Structural adhesives

• Higher heat resistance – for wood, composites • Improved impact resistance

- Pressure-sensitive adhesives • 100% solids • Emulsion-based psa’s with performance comparable to solvent-based

- Robust flexible packaging adhesives - Replacements for Bis Phenol A - Adhesives for low surface energy surfaces

• Pressure-sensitive adhesives • Structural adhesives

- Bio-based adhesives • Urethanes, acrylics

Contact: Joe Fox Director, Emerging & External Technologies 614-790-3686 [email protected]

Chapter 2

52

• Water Technologies - Disassembly of biomass - Formation of uniform, aqueous slurries of fibers - Non-woven sheet formation - Paper-like matrices with novel performance properties - Ampiphilic polymers & oligomers - Non-chemical methods for water treatment

• For corrosion inhibition, scale inhibition and biofilm inhibition - Sensors for system performance

• Scale, biofilm formation; corrosion

• Aqualon Functional Ingredients - Cost-effective sources of pure cellulose - Modification / etherification of cellulose - Rheological control of aqueous systems

• Valvoline

- Low wear, high thermal conductivity fluids - Low cost base oil feedstocks - Bio-based lubricants

Needs and Interests of Other Ashland Divisions

Chapter 2