hunting plc annual report & accounts 07

TRANSCRIPT

Excellence in Energy Services. . . for over 100 years

www.hunting.plc.uk

Contents

Chairman’s Statement _________________________________________________________ 2

Business Review _____________________________________________________________ 4

Board of Directors___________________________________________________________ 16

Report of the Directors ________________________________________________________ 18

Corporate Social Responsibility_________________________________________________ 24

The Remuneration Committee’s Report __________________________________________ 26

Corporate Governance ________________________________________________________ 34

Report of the Auditors _________________________________________________________ 39

Principal Accounting Policies __________________________________________________ 41

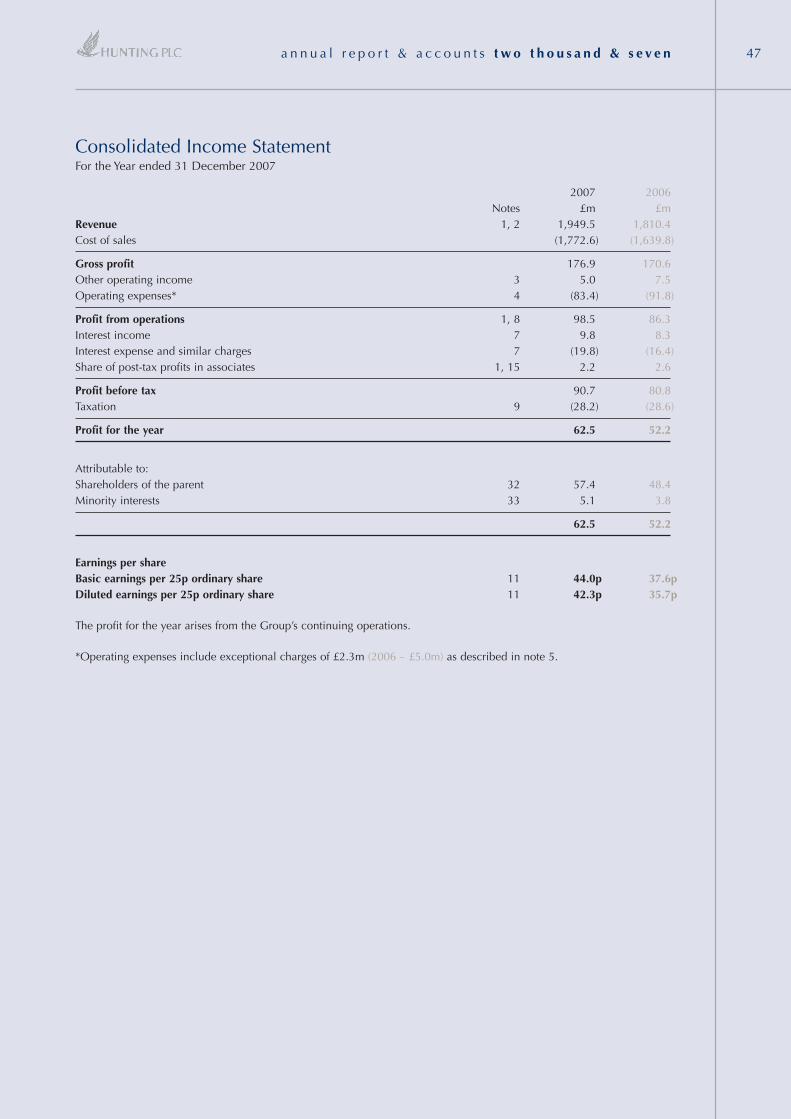

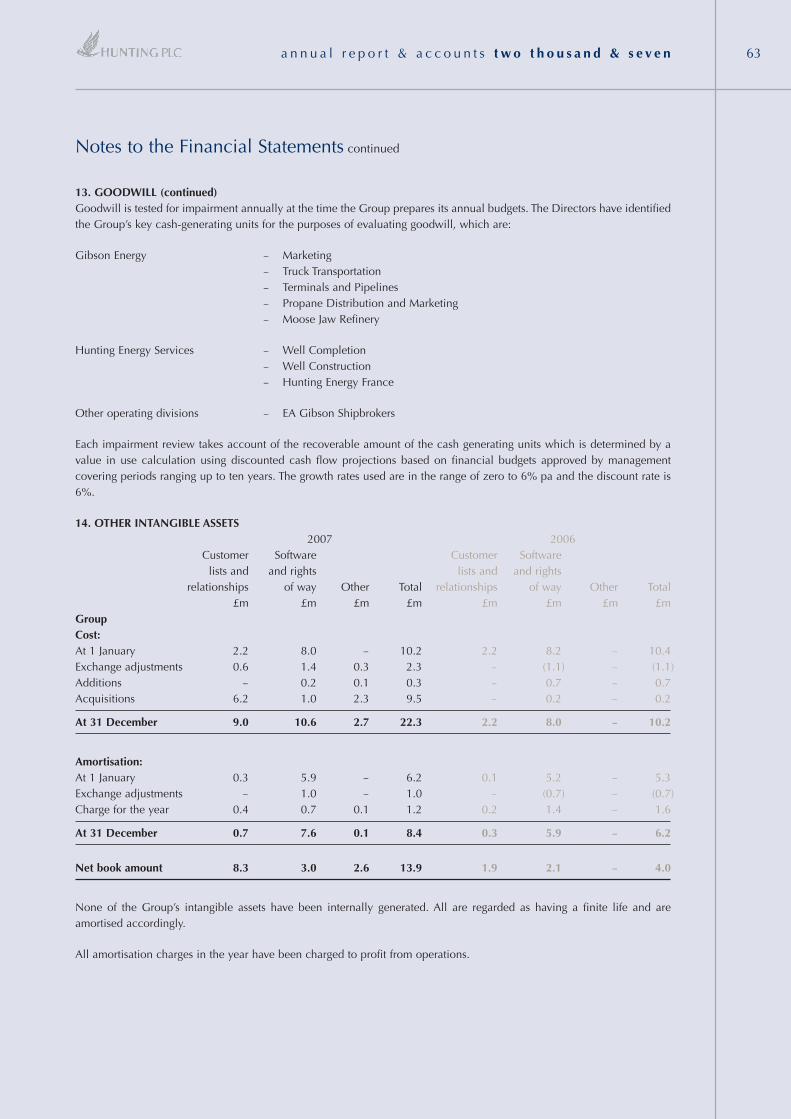

Consolidated Income Statement ________________________________________________ 47

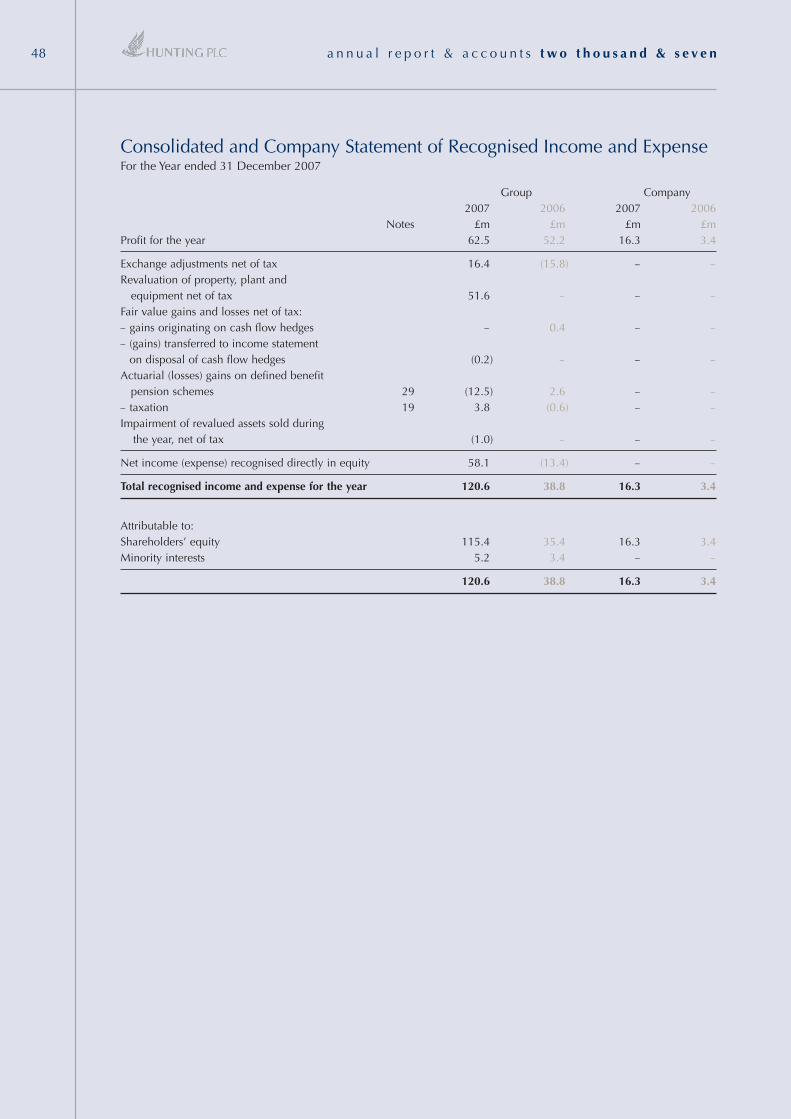

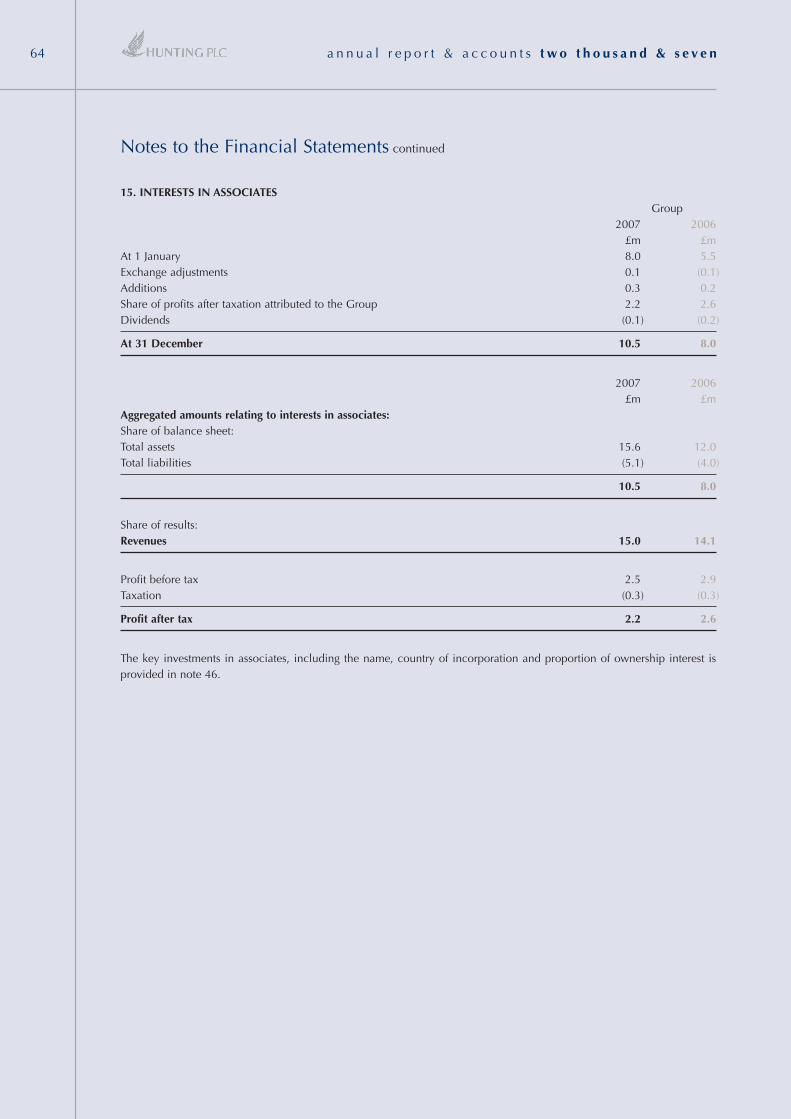

Consolidated and Company Statement of Recognised Income and Expense ___________ 48

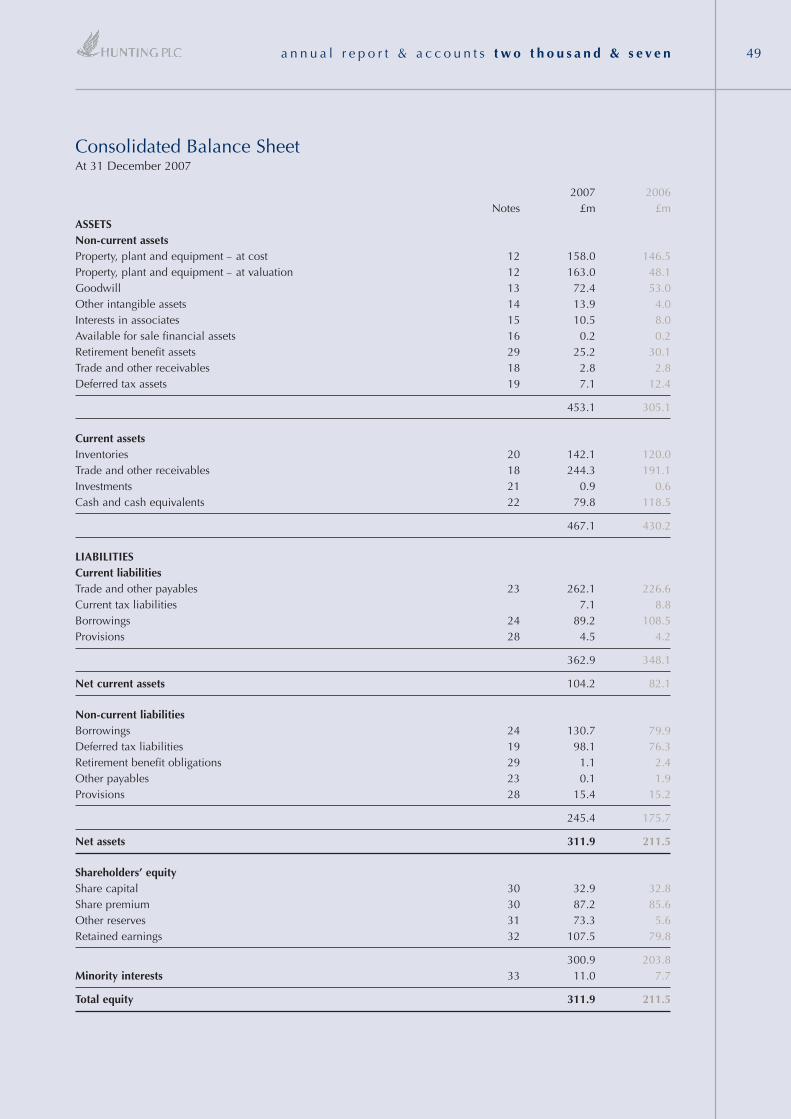

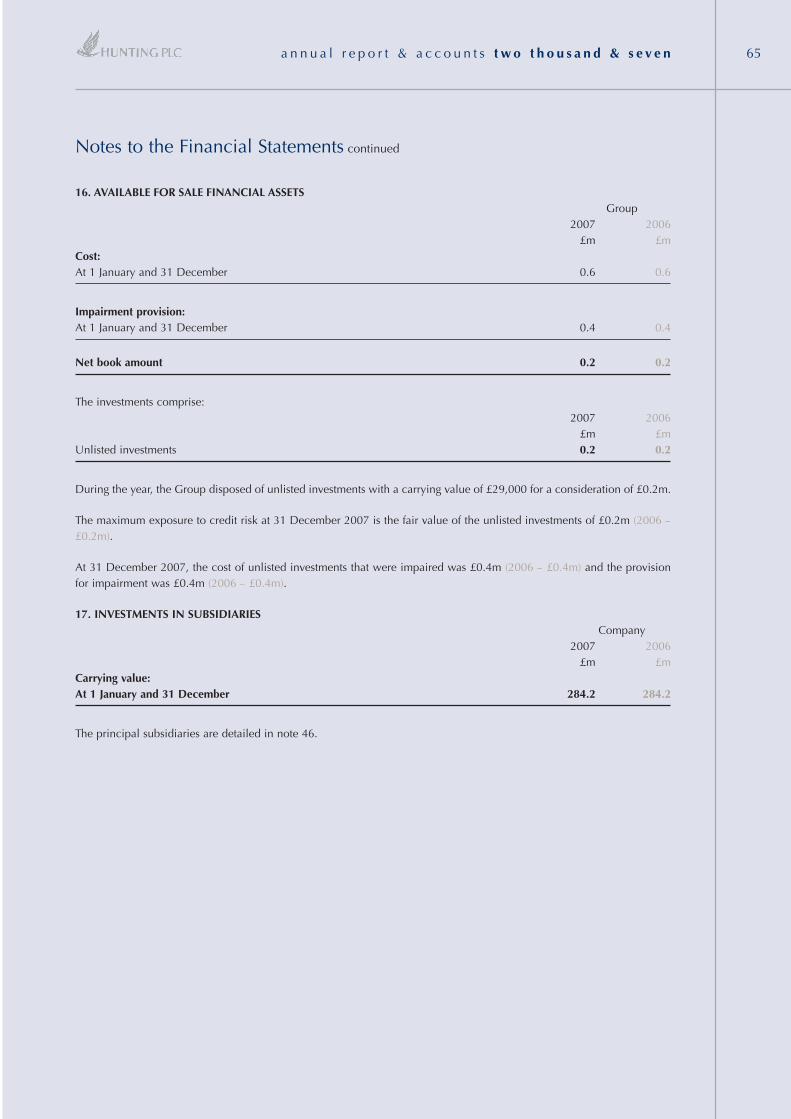

Consolidated Balance Sheet____________________________________________________ 49

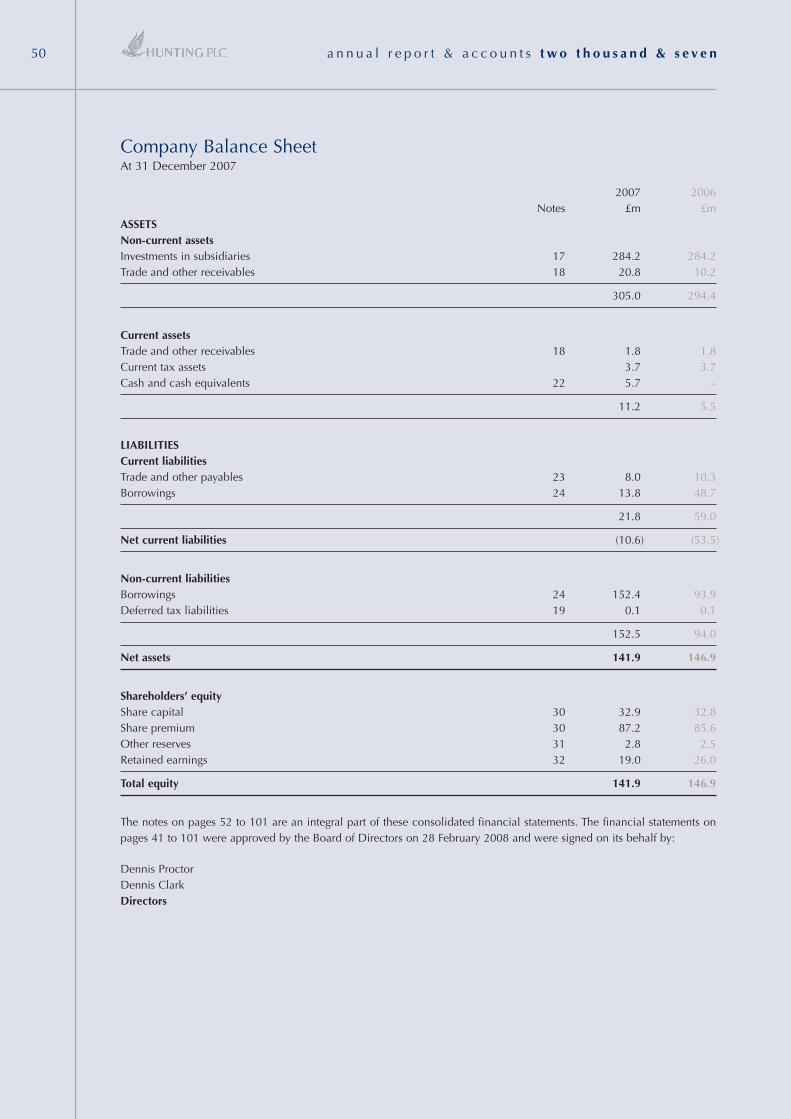

Company Balance Sheet_______________________________________________________ 50

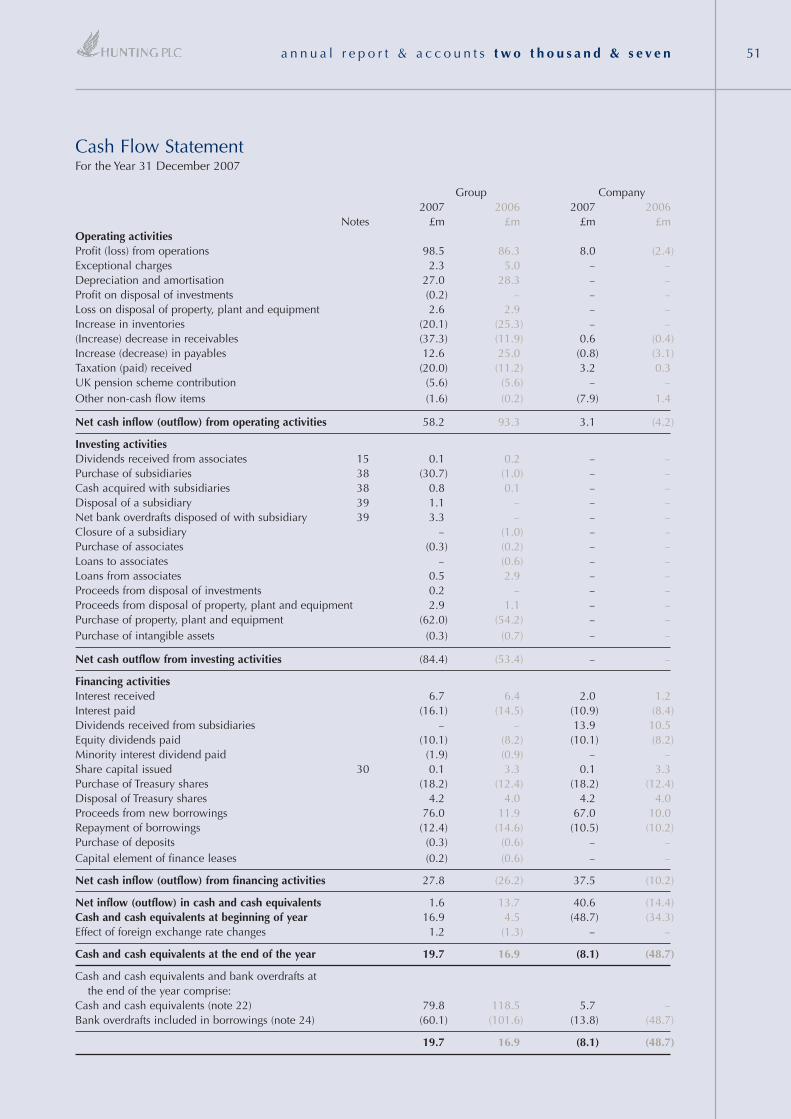

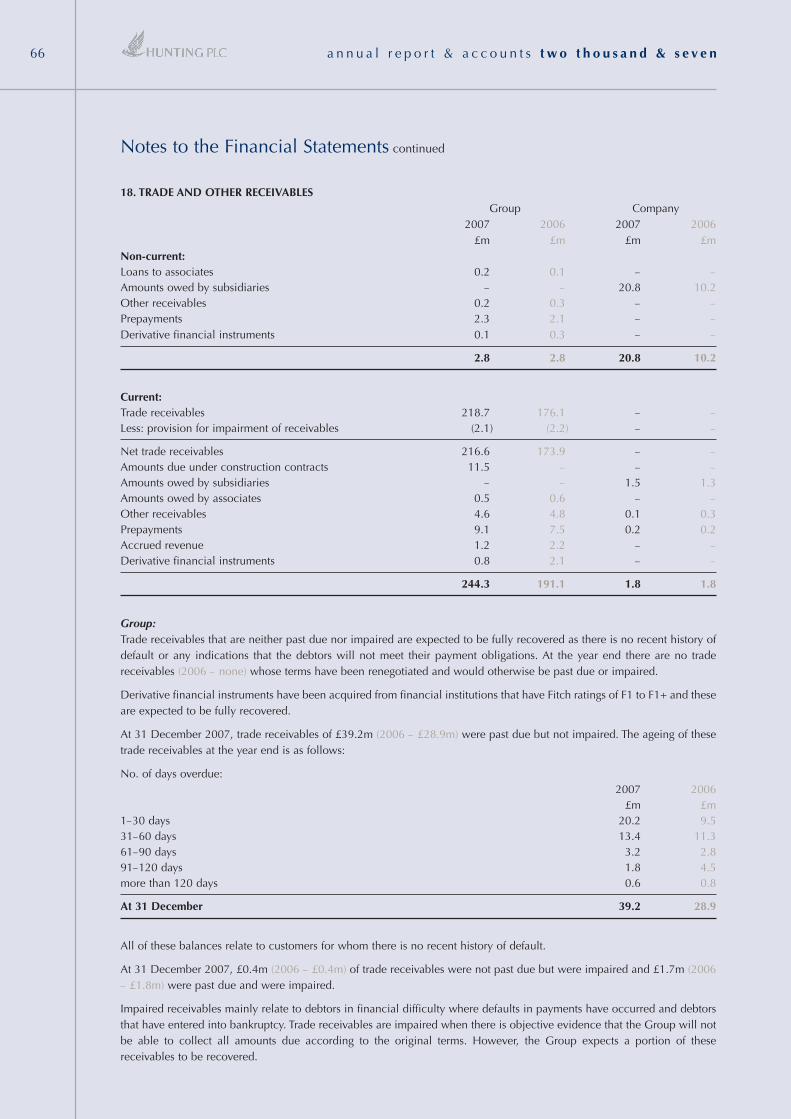

Cash Flow Statement__________________________________________________________ 51

Notes to the Financial Statements _______________________________________________ 52

Shareholder Information_______________________________________________________102

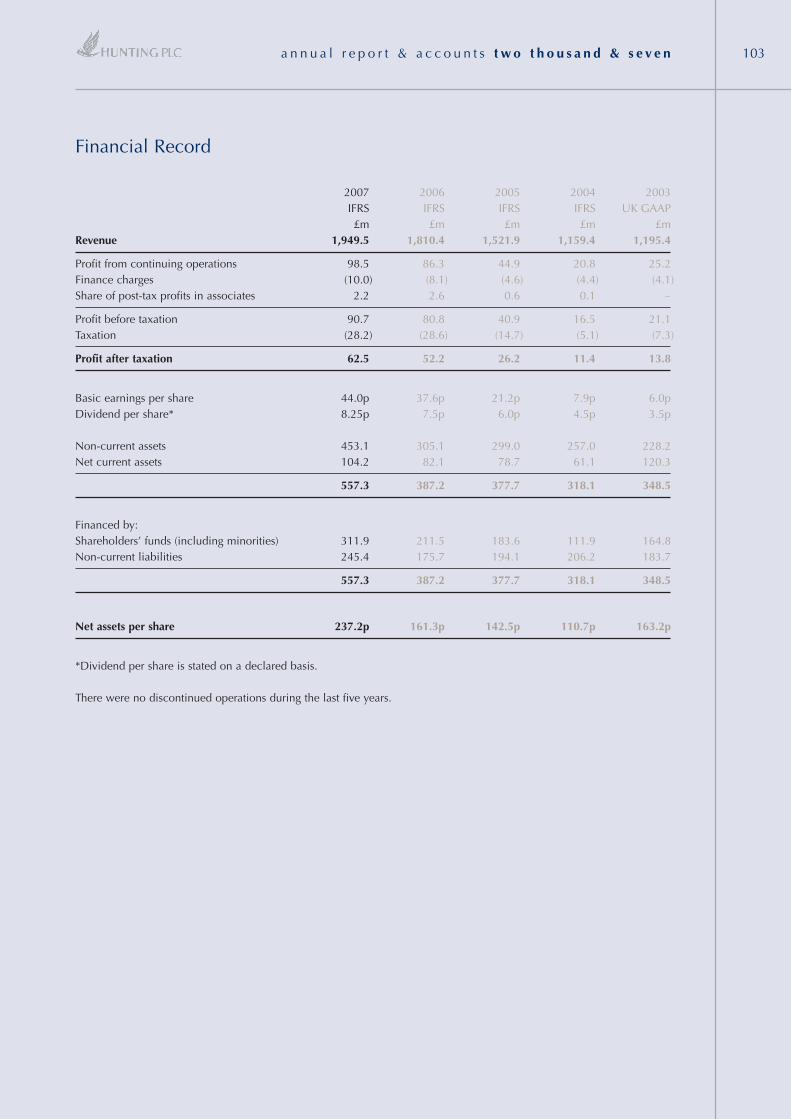

Financial Record _____________________________________________________________103

H u n t i n g P L C a n n u a l r e p o r t & a c c o u n t s

t w o t h o u s a n d & s e v e n 07

3 Cockspur Street, London SW1Y 5BQTel: 020 7321 0123 Fax: 020 7839 2072

www.hunting.plc.uk

HU

NT

ING

PLC

AN

NU

AL R

EPO

RT

AN

D A

CC

OU

NT

S 20

07

Excellence in Energy Services. . . for over 100 years

www.hunting.plc.uk

Contents

Chairman’s Statement _________________________________________________________ 2

Business Review _____________________________________________________________ 4

Board of Directors___________________________________________________________ 16

Report of the Directors ________________________________________________________ 18

Corporate Social Responsibility_________________________________________________ 24

The Remuneration Committee’s Report __________________________________________ 26

Corporate Governance ________________________________________________________ 34

Report of the Auditors _________________________________________________________ 39

Principal Accounting Policies __________________________________________________ 41

Consolidated Income Statement ________________________________________________ 47

Consolidated and Company Statement of Recognised Income and Expense ___________ 48

Consolidated Balance Sheet____________________________________________________ 49

Company Balance Sheet_______________________________________________________ 50

Cash Flow Statement__________________________________________________________ 51

Notes to the Financial Statements _______________________________________________ 52

Shareholder Information_______________________________________________________102

Financial Record _____________________________________________________________103

H u n t i n g P L C a n n u a l r e p o r t & a c c o u n t s

t w o t h o u s a n d & s e v e n 07

3 Cockspur Street, London SW1Y 5BQTel: 020 7321 0123 Fax: 020 7839 2072

www.hunting.plc.uk

HU

NT

ING

PLC

AN

NU

AL R

EPO

RT

AN

D A

CC

OU

NT

S 20

07

Professional Advisers

Solicitors

CMS Cameron McKenna LLP

Auditors

PricewaterhouseCoopers LLP

Brokers

Hoare Govett Limited

Merchant Bankers

Close Brothers Corporate Finance Limited

Insurance Brokers

Willis Limited

Pension Advisers & Actuary

Lane Clark & Peacock LLP

Registrars and Transfer Office

Equiniti Limited

Aspect House

Spencer Road, Lancing

West Sussex BN99 6DA

Telephone 0871 384 2030

Registered Office: 3 Cockspur Street, London SW1Y 5BQ

Registered Number: 974568 (Registered in England and Wales)

Telephone: 020 7321 0123 Facsimile: 020 7839 2072

Internet Web Site: www.hunting.plc.uk

Designed by Marshall Design, Godalming, Surrey.

Printed by Park Communications on paper manufactured from Elemental Chlorine Free (ECF) pulp sourced from sustainable forests.

Park Communications is certified to ISO 14001:2004 Environmental Management System and is a CarbonNeutral® company.

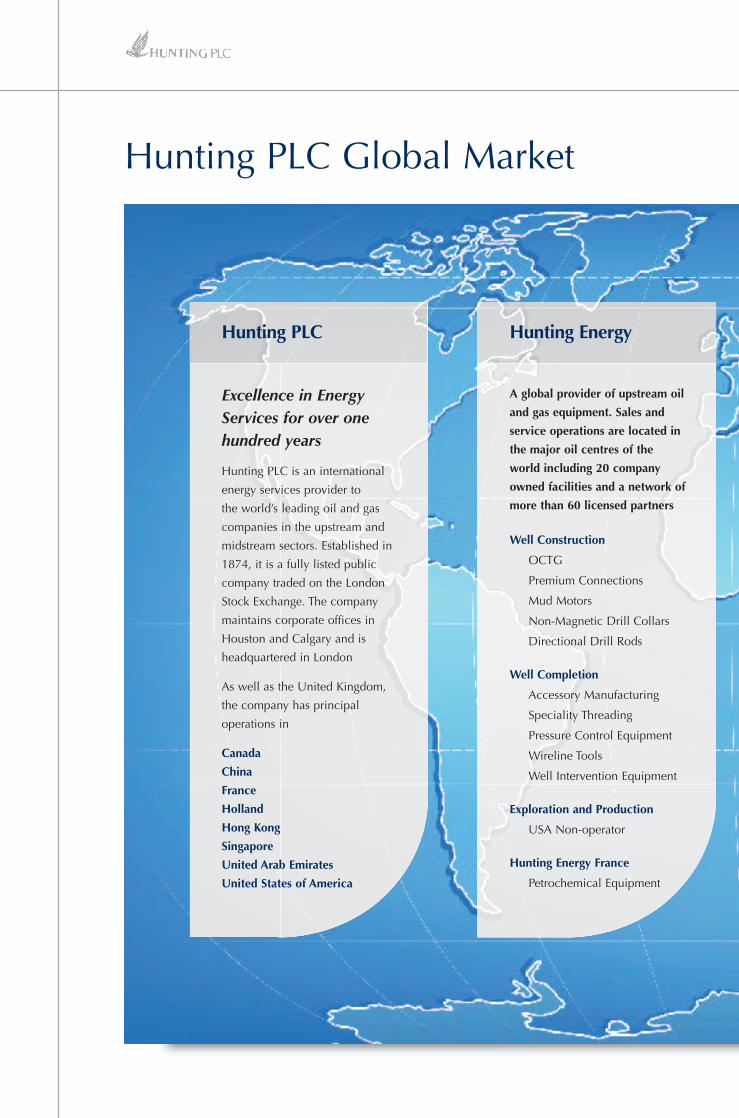

Hunting PLC Global Market www.hunting.plc.uk

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n

Excellence in EnergyServices for over onehundred years

Hunting PLC is an international

energy services provider to

the world’s leading oil and gas

companies in the upstream and

midstream sectors. Established in

1874, it is a fully listed public

company traded on the London

Stock Exchange. The company

maintains corporate offices in

Houston and Calgary and is

headquartered in London

As well as the United Kingdom,

the company has principal

operations in

Canada

China

France

Holland

Hong Kong

Singapore

United Arab Emirates

United States of America

Hunting PLC

A global provider of upstream oil

and gas equipment. Sales and

service operations are located in

the major oil centres of the

world including 20 company

owned facilities and a network of

more than 60 licensed partners

Well Construction

OCTG

Premium Connections

Mud Motors

Non-Magnetic Drill Collars

Directional Drill Rods

Well Completion

Accessory Manufacturing

Speciality Threading

Pressure Control Equipment

Wireline Tools

Well Intervention Equipment

Exploration and Production

USA Non-operator

Hunting Energy France

Petrochemical Equipment

Hunting Energy

Marketing

Crude Oil

Diluent

Natural Gas Liquids

Natural Gas

Truck Transportation

Crude Oil

Asphalt

Diluent

Natural Gas Liquids

Liquid Petroleum Gases

Carbon Dioxide

Industrial Chemicals

Terminals and Pipelines

Pipelines

Custom Terminals

Storage

Blending

Canada’s largest independent midstream energy company

playing a significant role in the country’s oil and gas industry

linking upstream producers with downstream refiners

Gibson Energy

Gibson Shipbrokers

Propane Marketing andDistribution

Retail Distribution

Wholesale Supply

Moose Jaw Refinery

Asphalt

Roofing Flux

Well Site Fluids

Light distillates

Crude Oil and Products

Specialised Tankers

LPG and LNG

Dry Cargo

Sale and Purchase

Offshore

Research 07

Professional Advisers

Solicitors

CMS Cameron McKenna LLP

Auditors

PricewaterhouseCoopers LLP

Brokers

Hoare Govett Limited

Merchant Bankers

Close Brothers Corporate Finance Limited

Insurance Brokers

Willis Limited

Pension Advisers & Actuary

Lane Clark & Peacock LLP

Registrars and Transfer Office

Equiniti Limited

Aspect House

Spencer Road, Lancing

West Sussex BN99 6DA

Telephone 0871 384 2030

Registered Office: 3 Cockspur Street, London SW1Y 5BQ

Registered Number: 974568 (Registered in England and Wales)

Telephone: 020 7321 0123 Facsimile: 020 7839 2072

Internet Web Site: www.hunting.plc.uk

Designed by Marshall Design, Godalming, Surrey.

Printed by Park Communications on paper manufactured from Elemental Chlorine Free (ECF) pulp sourced from sustainable forests.

Park Communications is certified to ISO 14001:2004 Environmental Management System and is a CarbonNeutral® company.

Hunting PLC Global Market www.hunting.plc.uk

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n

Excellence in EnergyServices for over onehundred years

Hunting PLC is an international

energy services provider to

the world’s leading oil and gas

companies in the upstream and

midstream sectors. Established in

1874, it is a fully listed public

company traded on the London

Stock Exchange. The company

maintains corporate offices in

Houston and Calgary and is

headquartered in London

As well as the United Kingdom,

the company has principal

operations in

Canada

China

France

Holland

Hong Kong

Singapore

United Arab Emirates

United States of America

Hunting PLC

A global provider of upstream oil

and gas equipment. Sales and

service operations are located in

the major oil centres of the

world including 20 company

owned facilities and a network of

more than 60 licensed partners

Well Construction

OCTG

Premium Connections

Mud Motors

Non-Magnetic Drill Collars

Directional Drill Rods

Well Completion

Accessory Manufacturing

Speciality Threading

Pressure Control Equipment

Wireline Tools

Well Intervention Equipment

Exploration and Production

USA Non-operator

Hunting Energy France

Petrochemical Equipment

Hunting Energy

Marketing

Crude Oil

Diluent

Natural Gas Liquids

Natural Gas

Truck Transportation

Crude Oil

Asphalt

Diluent

Natural Gas Liquids

Liquid Petroleum Gases

Carbon Dioxide

Industrial Chemicals

Terminals and Pipelines

Pipelines

Custom Terminals

Storage

Blending

Canada’s largest independent midstream energy company

playing a significant role in the country’s oil and gas industry

linking upstream producers with downstream refiners

Gibson Energy

Gibson Shipbrokers

Propane Marketing andDistribution

Retail Distribution

Wholesale Supply

Moose Jaw Refinery

Asphalt

Roofing Flux

Well Site Fluids

Light distillates

Crude Oil and Products

Specialised Tankers

LPG and LNG

Dry Cargo

Sale and Purchase

Offshore

Research 07

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n 1

Financial HighlightsDouble-digit growthonce again as the costand availability of energycontinues to dominatethe public arena.

Global oil servicescontinue to expanddriven by unrelentingenergy demand fromrapid industrialisation ofthe developing world andweak supply gains inproducing regions.

The Company foreseesheightened oil and gasactivity and demand for its expertisecontinuing to be strong.

072007 2006

Revenue +8% £1,950m £1,810m

Profit from operations +14% £98.5m £86.3m

Profit before tax andexceptional items +8% £93.0m £85.8m

Profit before tax +12% £90.7m £80.8m

Basic earnings per share +17% 44.0p 37.6p

Dividend declared +10% 8.25p 7.5p

I am pleased to report the Company’sthird consecutive year of recordresults. Profit before taxation in 2007was £90.7m (2006 – £80.8m), a 12%increase.

The Company continues to be focusedon North America with increasingcontributions from the internationalarena. The energy markets we serveare volatile, but your Company hasperformed well, increasing its pre-taxprofits despite sterling (our reportingcurrency) strengthening significantlyagainst the US and Canadian dollarsin which we mainly trade.

Two significant international trendsfrom the last few years have comeincreasingly to the fore. Hydrocarbonresources have become harder to findand deliver to consumers. The world’soil and gas reserves, once mainly inthe hands of the major international oilcompanies, are now substantiallycontrolled by state-owned national oilcompanies. Both of these trends playto the Company’s strengths. Deeperand higher pressure reserves requiredisproportionately large quantities ofour highly engineered upstreamproducts, while national oil companiesoften require more from the oil serviceindustry than do the oil majors.

Gibson Energy, the Company’smidstream services operation wasonce again busy and successful in thevery active Western Canadian scene,producing similar results to last year.Even more attention is being paid bythe company to the increasingproportion of hydrocarbon productionderiving from conventional heavy oiland from the huge Athabasca tarsands reserves. The key performers in2007 were the Truck Transportationoperation (with the largest crude oilfleet in Western Canada) and theTerminals and Pipelines operation.Although the Marketing Divisionfound that very high oil price levelsand volatility impacted on some of itstrading opportunities, it remainedhighly profitable.

Hunting Energy Services concentrateson the upstream side of the oilindustry, providing sophisticatedequipment mainly for below-ground

applications. It produced profits morethan 36% above last year, thanks toexcellent markets and efficientproduction, especially in USManufacturing, in the North Sea andin South-East Asia.

Capital expenditure increasedsubstantially to meet continued highdemand and to replace equipmentwhich has been working flat-out forsome years. A number of smalleracquisitions were also made.

Basic earnings per share were 44.0p,an increase of 17% on the previousyear. We are recommending a finaldividend of 5.7p per share, giving atotal of 8.25p for the year, a 10%increase.

We intend to appoint a new FinanceDirector, Peter Rose CA, with effectfrom the Company’s Annual GeneralMeeting. Peter has been with us sinceJuly 1997, initially as Group FinancialController and also as CompanySecretary since August 2004.

The current Finance Director, DennisClark, has been in the post since theformation of Hunting PLC in 1989. Heoriginally joined the Group in 1972and has had a distinguished career,culminating in his active involvementin the remarkable growth of the pastfew years. I would like to extend mygratitude and that of the rest of theBoard and of his colleagues forDennis’s outstanding achievements.

This has been a fine year for yourCompany. Although the worldeconomic outlook is cloudier than inrecent years, it seems certain thathydrocarbon demand and the need forour products and services willcontinue to be strong. I expect theCompany to continue to perform well.

I thank our staff for their hard workand dedication during anothersuccessful year.

Richard HuntingChairman

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n2

07

Chairman’s Statement

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n 3

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n

At Canwest Propane, Western andDel’s Propane companies wereacquired for £4.1m. In addition, theacquisition of MP Energy in EasternCanada for £8.8m occurred in thesecond half of 2007, which increasedvolumes in wholesale distribution.

Hunting Energy Services invested£36.5m in capital expenditure during2007 of which £7.0m was forexploration and productionexpenditure. The balance of £29.5mincluded expenditure of £8.3m foradditional facilities in Casper, Wyomingand new tools and spare parts forPerformance mud motor equipment. Inthe US manufacturing facilities,spending on the oil country tubulargoods finishing facility in Houston, deepwater accessory manufacturing facilityin Houma, Louisiana and the expansionof the Lafayette, Louisiana facilitytotalled £3.0m for the year. Additionalequipment in Asia, Aberdeen andHolland totalled approximately £2.0m.Hunting Oryx was acquired in Octoberfor £8.6m. Hunting Oryx is a distributorof non-magnetic drill collars.

Health, Safety and the Environment

Gibson Energy’s lost time incidentrecord was 26% below the AlbertaProvincial average in 2007. Gibsonwas also recognised for itscommitment to Health, Safety and theEnvironment as a recipient of the 2007Certificate of Recognition (COR), anindustry health and safety standard,with a score at the 90% level. Gibsonand its affiliates received the following

awards related to Health, Safety andEnvironment of their employees andcommunity in which they operate.

1. Work Safe Alberta 2006 BestPerformer Award.

2. Leader status in the EnviroVista,Environmental Leadership Program,awarded to Gibson’s “BulkPetroleum Storage and TransfersFacility” in Hardisty by the Ministerfor Alberta Environment.

3. Chemical Shipper’s Safety Award –awarded to the Moose Jaw Refineryby the Canadian Pacific Railway fordemonstrating excellence intransportation safety.

4. CNR Safe Handling – awarded tothe Moose Jaw Refinery andGibson’s Edmonton Terminal by theCanadian National Railway as partof the “Partners in Responsible CareGold Award”.

Hunting Energy Services’ USmanufacturing operations incurred atotal of twenty-six recordableaccidents which reduced by 20% from2006. Approximately 50% of theincidents were by inexperiencedworkers with less than one year’semployment at Hunting. Hunting’sincident rate of 2.69 remains farbelow the Bureau of Labour Statisticsindustry average of approximately 7.5.

The European facilities’ accidentstatistics were once again below thelevel of the industry average inengineering and manufacturing.

Therefore, the Company applied fortheir sixth consecutive National SafetyAward by the British Safety Counciland retained the Five Star rating forthe tenth consecutive year.

No environmental issues occurred inthe year and all of Hunting EnergyServices’ primary manufacturingfacilities are ISO 14001 EnvironmentalManagement System certified.

Our goals remain simply put – noaccidents, no harm to people and nodamage to the environment.

Outlook

Oil accounts for more than 95% oftransportation energy, andtransportation is an economicnecessity. There are no easy energysubstitutes. In addition, the soaring oiluse throughout the developing worldwill challenge the oil and gasindustry’s ability to meet futuredemand. Some experts’ view of anannual 4% average depletion rate forexisting fields is often rebutted with alevel of 8%, thus posing a furtherobstacle to supply growth. At currentcommodity price levels, oil and gasproducers are once again increasingtheir investment to boost reserves andproduction capabilities. The 11%investment growth will placeadditional pressure on the existing and over stretched manpowerresources, but will continue to provide excellent growth opportunities for the oil serviceindustry.

5

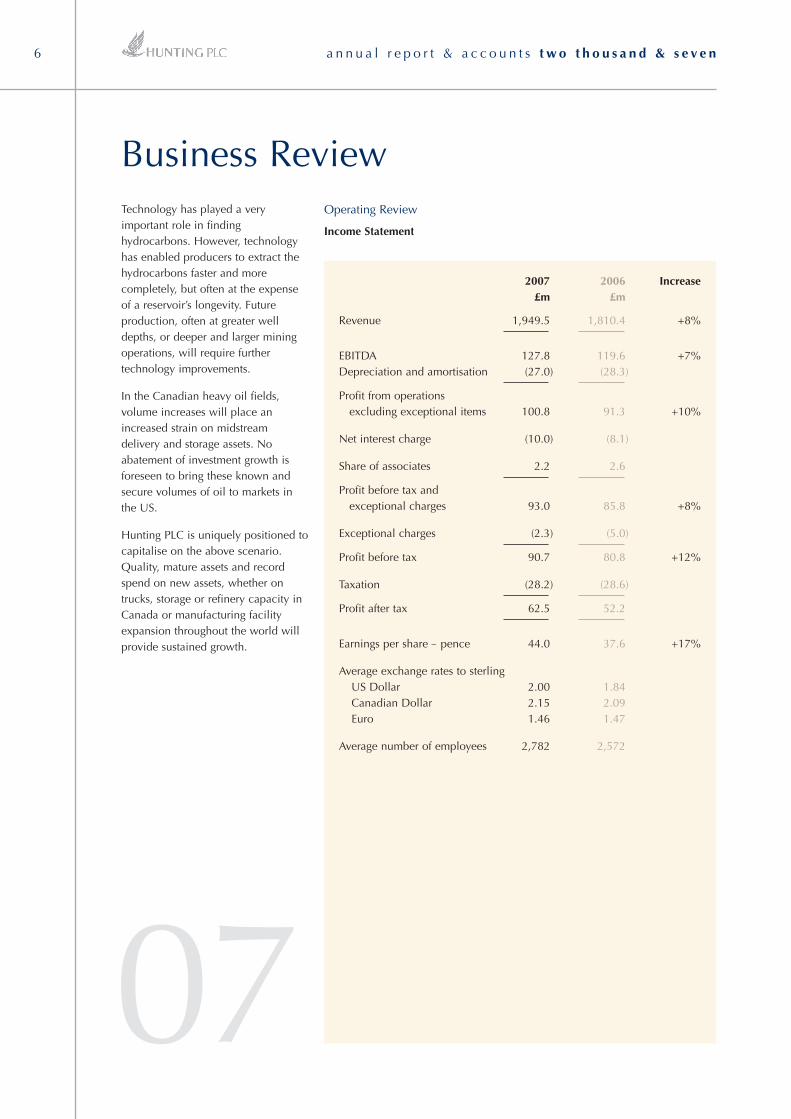

Technology has played a veryimportant role in findinghydrocarbons. However, technologyhas enabled producers to extract thehydrocarbons faster and morecompletely, but often at the expenseof a reservoir’s longevity. Futureproduction, often at greater welldepths, or deeper and larger miningoperations, will require furthertechnology improvements.

In the Canadian heavy oil fields,volume increases will place anincreased strain on midstreamdelivery and storage assets. Noabatement of investment growth isforeseen to bring these known andsecure volumes of oil to markets inthe US.

Hunting PLC is uniquely positioned tocapitalise on the above scenario.Quality, mature assets and recordspend on new assets, whether ontrucks, storage or refinery capacity inCanada or manufacturing facilityexpansion throughout the world willprovide sustained growth.

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n6

2007 2006 Increase£m £m

Revenue 1,949.5 1,810.4 +8%

EBITDA 127.8 119.6 +7%Depreciation and amortisation (27.0) (28.3)

Profit from operationsexcluding exceptional items 100.8 91.3 +10%

Net interest charge (10.0) (8.1)

Share of associates 2.2 2.6

Profit before tax andexceptional charges 93.0 85.8 +8%

Exceptional charges (2.3) (5.0)

Profit before tax 90.7 80.8 +12%

Taxation (28.2) (28.6)

Profit after tax 62.5 52.2

Earnings per share – pence 44.0 37.6 +17%

Average exchange rates to sterlingUS Dollar 2.00 1.84Canadian Dollar 2.15 2.09Euro 1.46 1.47

Average number of employees 2,782 2,572

Operating Review

Income Statement

Business Review

07

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n 7

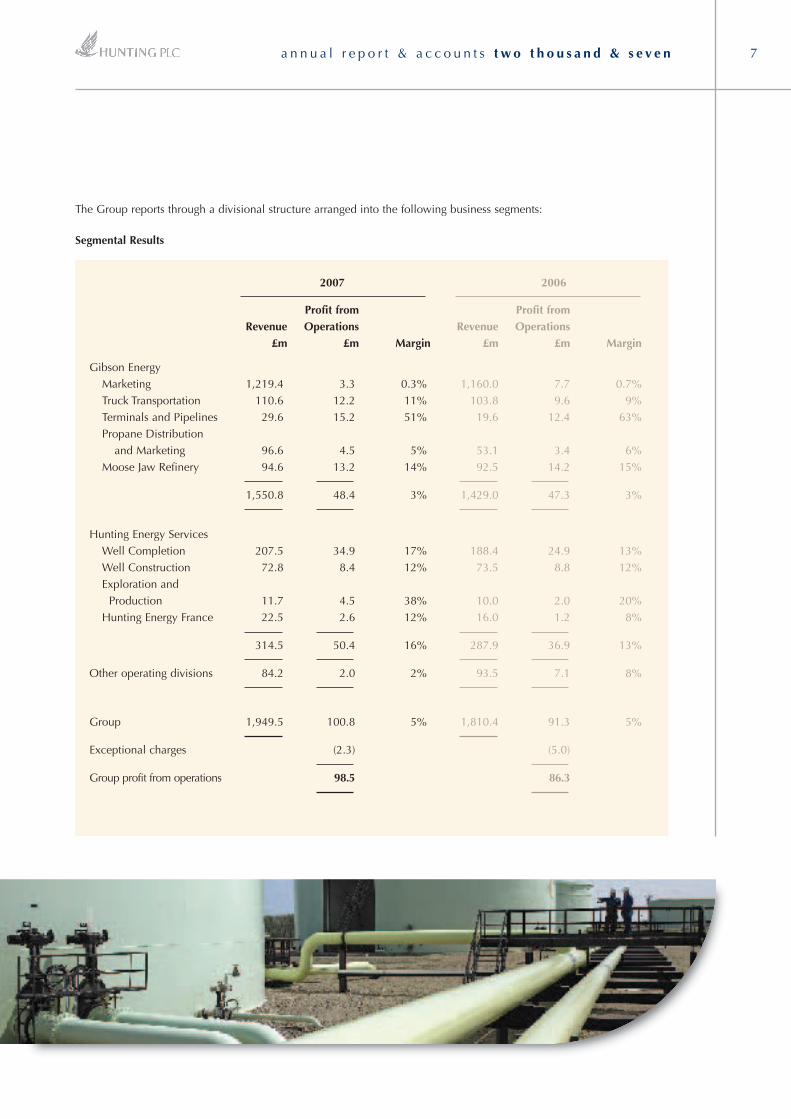

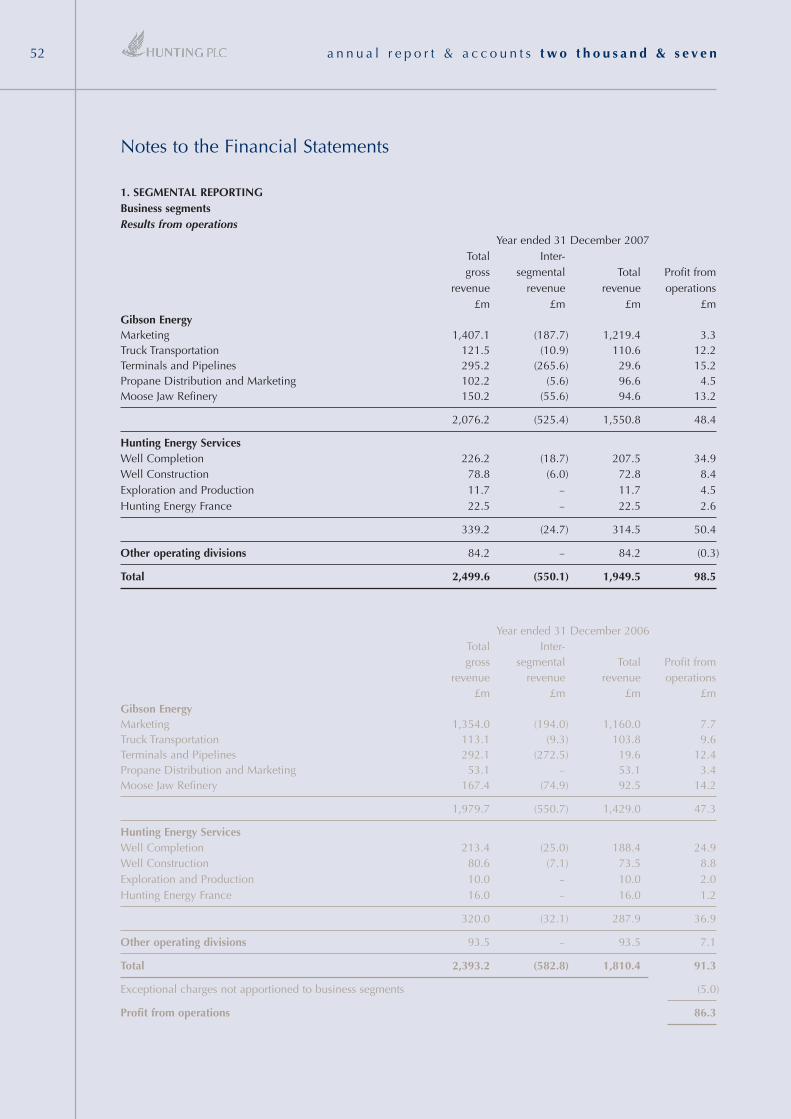

The Group reports through a divisional structure arranged into the following business segments:

Segmental Results

2007 2006

Profit from Profit fromRevenue Operations Revenue Operations

£m £m Margin £m £m Margin

Gibson EnergyMarketing 1,219.4 3.3 0.3% 1,160.0 7.7 0.7%Truck Transportation 110.6 12.2 11% 103.8 9.6 9%Terminals and Pipelines 29.6 15.2 51% 19.6 12.4 63%Propane Distribution

and Marketing 96.6 4.5 5% 53.1 3.4 6%Moose Jaw Refinery 94.6 13.2 14% 92.5 14.2 15%

1,550.8 48.4 3% 1,429.0 47.3 3%

Hunting Energy ServicesWell Completion 207.5 34.9 17% 188.4 24.9 13%Well Construction 72.8 8.4 12% 73.5 8.8 12%Exploration and

Production 11.7 4.5 38% 10.0 2.0 20%Hunting Energy France 22.5 2.6 12% 16.0 1.2 8%

314.5 50.4 16% 287.9 36.9 13%

Other operating divisions 84.2 2.0 2% 93.5 7.1 8%

Group 1,949.5 100.8 5% 1,810.4 91.3 5%

Exceptional charges (2.3) (5.0)

Group profit from operations 98.5 86.3

end the year at levels near 2006. As aresult, year on year operating profitsfor Gibson Energy were £48.4m (2006– £47.3m).

Marketing activities comprise thebuying, selling and blending of crudeoil, diluent, natural gas and well sitefluids across North America. The pricerisk on volumes purchased andinventories is managed throughpublicly traded commodityinstruments. Gibson remains one ofCanada’s largest independent crudeoil marketing companies dealing withall of the major, intermediate andsmaller Canadian producingcompanies and income trusts. It isfocused on the physical buying andselling of hydrocarbon productsutilising proprietary risk managementtechniques and strong customerrelationships to minimise risk andoptimise profitability. Marketingaccounted for 6.8% of Gibson’s profit from operations. While tradingmargins from marketing were robustduring most of the year, volatilemovement in differentials had animpact in the fourth quarter. Inaddition, extraordinary gains from theSuncor oil sands coker fire in 2006were not repeated, as diluent was notin historical short supply. Blendingvolumes, however, at the elevencustom terminals were nearexpectations, but margins were lowerthan in 2006. Further, the EdmontonNorth terminal began the yearpositively with good results throughmid-year, but suffered negatively fromwide differentials and lower inventoryvalues in October and December.

Truck Transportation operates a fleetof 1,180 trailers and 660 tractors thatmove in excess of 93 million barrelsof oil equivalent per year acrossWestern Canada and theNorthwestern United States. TruckTransportation accounted for 25.2% of Gibson’s profit from operations – a27% profit improvement over 2006. Itis the largest crude oil truck hauler inWestern Canada. The large scale of its

The Company’s technologyinvestments will further its earningsgrowth from well cost savings tocompletion and productionimprovements. Its market sharestrength in Truck Transportation inCanada; proprietary tubularconnections; global manufacturingcapacity; and crude oil tankerbrokering will provide further marginenhancement. The respectivesynergistic assets of Gibson Energyand Hunting Energy will continue tomaximise profit from each barrel ofcrude oil and each operator purchaseorder. Hunting’s five yearcompounded annual growth rate of41% is exceptional. With a strongbalance sheet, a tested strategy and2,782 dedicated employees, HuntingPLC will continue delivering excellentvalue to its shareholders.

Gibson Energy

For Canada, crude oil remained thedominant commodity for increasedactivity in 2007, while natural gaswell completions experienced a 25%decline. 2007 was a year of extremevolatility for crude oil price marketswhich experienced a large year onyear gain in West Texas intermediateposting from US$54.35 to US$91.74/barrel. This was offset by an evenlarger increase in heavy/sourdifferentials for Canadian crude oilfrom the $16/barrel range to over$40/barrel at year end. This factorcombined with the reversal in futurecontracts from contango (increasingfuture prices) to backwardation(decreasing future prices) has madetrading unpredictable. Accordinglyprovisions were recorded in the fourthquarter from mark to marketderivatives which are regularly placedto protect physical volumes tradedinto the future. The extraordinarilywide differential for the heavy oilprices in December actually devaluedinventories as West Texas intermediateprices increased. This movementcaused the results for Moose JawRefinery and the Marketing group to

fleet operations allows Gibson to carry out logistically complex andhigh margin jobs regardless of thevolume or destination. A strong focuson health, safety and environmentalperformance is maintained, given thefact that these combined units travelapproximately 143,000 miles per day.

Terminals and Pipelines operationsincorporate an infrastructure of over270 miles of pipelines and eleventerminals with a storage capacityexceeding 2.3 million barrels. Theseassets provide tariff based pipelineservices and fee based storage andterminaling services for crude oil anddiluent products. The custom terminalscapture the spreads between high andlow quality crude oil through itsblending, terminaling andtransportation service offerings. Thisdivision accounted for 31.4% ofGibson Energy’s profit fromoperations, a 23% year on yearimprovement. Volumes from Suncor’sFort McMurray operations steadilyincreased throughout the year as didoverall heavy crude volumes. TheHardisty Terminal Frac Plant iscapable of processing approximately5,000 barrels per day of NGL intobutane, propane and other by-products.

Propane Distribution and Marketingincludes the operations of CanwestPropane Limited, the second largestCanadian retail distributor of propane,utilising a fleet of over 200 fullyequipped delivery and service trucksand operating through forty-eightstrategically located branch officesand storage facilities across WesternCanada and the Northwest US.Volumes almost doubled in 2007 to480 million litres and represented9.3% of Gibson’s operating profits – a32% increase.

Moose Jaw Refinery processesapproximately 3.9 million barrels ofheavy crude each year into A Gradeasphaltic and lighter distillate productsincluding road asphalt, roofing flux

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n8

Business Review

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n

and well site fluids. These productsare shipped via rail cars and trucksfrom Moose Jaw Refinery to marketsin the US and Western Canada. Thefacility produced 1,400 barrels perday for the paving industry, 3,500barrels per day for roofing flux in thehousing industry, 1,700 barrels perday for well site fluids in theexploration and production industry,and 3,900 barrels per day for TOPSutilised in heavy oil blendingthroughout the year.

Hunting Energy Services

Hunting Energy Services recordedprofit from operations of £50.4mversus £36.9m in 2006 – a 37%increase. At the year end, there were1,476 employees under four businessplatforms; Well Construction, WellCompletion, Exploration andProduction and Hunting EnergyFrance. Well Construction and WellCompletion, through generic growthof its global footprint, an expansion ofits product offerings and newtechnology, benefited from theexcellent market conditions. Hunting’sExploration and Production andHunting Energy France both had yearon year improvements from highermargins and exploration successes.

The Well Construction platformprovides products and services usedby customers for the drilling phase ofoil and gas wells along with associatedequipment used by the undergroundconstruction industry fortelecommunication infrastructurebuild out. The oil and gas activity is

focused on drilling depths of 10,000feet and deeper, typically in hightemperature, high pressureapplications. The trenchless businessfocuses on supplying drill rods andancillary tools to manufacturers anddealers for underground utilityinstallations. Technology is the keyasset to the products within thisdivision, including premiumconnections for oil country tubulargoods, mud motors and non-magneticdrill collars. These products areprocessed and/or manufactured atHunting Energy’s 15 facilitiesstrategically located throughout theworld. These facilities operated on a sixday, 24 hour basis throughout most ofthe year.

The Well Completion platformprovides products and services usedby customers for the completion andintervention phases of oil and gaswells. Its customer base includes themajor oil and gas operators as well asthe major OEM service companies.This platform reported record revenueand profits driven by newertechnologies, additional capacity andhigher margins. Expansion of thewireline/slickline division includedHouston and Southeast Asia andproprietary products such as ClearRun have been expanded into NorthAmerica.

The 43 patented products within theWell Construction and WellCompletion divisions are key toHunting Energy’s success. Theseunique technologies enable oil andgas operators to:

1. Complete wells faster with highspeed mud motors.

2. Make-up tubulars faster withredundant sealing for high pressureapplications.

3. Have connections capable ofextreme yield strength for thedeepest of well completions.

4. Use environmentally safe threadcompounds for threaded productson tubulars and accessories.

5. Intervene in existing wells through aunique and easy to repair “clam”blow out preventor for wirelineapplications.

These and many others will loweroperator costs and provide pricingleverage.

Hunting Energy France comprises theGroup’s French based businesseswhich provide petrochemicalequipment to the French andinternational energy and associatedindustries. The 2007 result was asignificant increase over 2006following a strong level of activity.Interpec in particular benefited from astrong order back log for China andthe Middle East.

Roforge commissioned a buildingextension in July which improvesmanufacturing efficiency and willprovide for future growth of thecompany.

Setmat and Larco jointly havesuccessfully secured orders for themetering of bio fuel truck loadingterminals.

9

liquefied natural and petroleum gasand other related services.

Despite a weaker US dollar tosterling exchange rate, Gibson’srevenues remained strong.

Challenging trading conditions forTankers were offset by improvedresults from Gas and SpecialisedTankers and in particular by thestrong performance of the Dry Cargo and Sale & PurchaseDepartments which achievedincreases of over 70% and 40%respectively.

Further expansion is expected duringthe year in the Far East to takeadvantage of identified opportunities.

Field Aviation Canada modifies,repairs and overhauls regional aircraftfor international customers fromCanadian facilities in Toronto andCalgary.

The Toronto Modification Center hada number of excellent projects thatwere successfully completed duringthe year, including US Customs andAustralian Coastwatch aircraft.However, delays in the delivery ofthree Swedish Coast Guard aircraftaffected results. Customer acceptanceof these aircraft is now in progresswith departure planned for April2008. Production capability for thenext 18 months is already presoldwith strong profits expected for 2008and 2009.

The Calgary Maintenance, Repair andOverhaul Facility made its highestprofit for many years, even thoughthe strength of the Canadian versusthe US dollar increased competitionfor commercial heavy maintenancework in North America. Themanufacturing facility wasreorganised in the year to address theexpected growth over the coming twoyears. Current production deliveriesextend into 2009.

Exploration and Production includesthe Group’s oil and gas explorationand production activities in theSouthern US and offshore Gulf ofMexico. The Group takes minoritynon-operating equity holdings andcurrently participates in over seventyoil and gas production facilities.

Markedly higher prices for oil andstable prices for natural gas, inconjunction with increasedproduction levels, contributed to asuccessful year for the Texas basedExploration and Production division.On a Net Equivalent Barrel (“NEB”)basis, production was up 20%compared to 2006 as a result ofsuccessful drilling in the shallowwaters of the Gulf of Mexico andonshore Texas and Louisiana. Thecompany participated in the drillingof 16 wells with 8 successes – 5 gas,1 oil and gas, 2 oil. Full year outputof 457,000 NEB was enhancedprimarily by higher natural gasproduction as a result of new wells.Profit from operations increased125% as compared to 2006. Year-end reserves of oil and gas on anSEC basis were 2.2m NEB comparedwith 2.3m NEB at the end of theprevious year.

Hunting Specialized Products is a USbased business supplying productsand services for the trenchlessrehabilitation of pipelines.

Revenues increased over 11% on theprevious year as a result of therecently launched structuralrehabilitation products; PolySprayand HydraWrap.

Investment in product and servicedevelopment was maintained tosupport the product development.

Other Operating Divisions

E. A. Gibson Shipbrokers is aninternational London based shipbrokerengaged in the transportation of crudeoil and other petroleum products,

Performance Measures

A number of performance measuresare used to compare thedevelopment, underlying businessperformance and position of theGroup and its business segments.These are used collectively andperiodically reviewed to ensurethey remain appropriate andmeaningful monitors of the Group’sperformance.

• Earnings before interest, tax,depreciation and amortisation(“EBITDA”).

• Profit before taxation (“PBT”).

• Return on capital employed(“ROCE”) – measures the profitbefore interest expressed as apercentage of the capitalemployed. Capital employed is theaverage of the aggregate of totalequity and the net debt at the startand end of the financial period.Also used as a benchmark fortarget acquisitions or capitalexpenditure proposals.

• Earnings per share (“EPS”).

• Free cash flow.

• Health and Safety arrangementswithin the Group are monitoredthrough regular reporting to theBoard.

Each of these performancemeasures are commented uponwithin the tables contained in theAnnual Report.

Indicators of future Groupperformance closely monitored bymanagement include:

• Drilling rig activity.

• Oil and gas commodity prices.

• Order book/backlog.

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n10

Business Review

effective rate of 31.1% (2006 –

35.4%). The lower rate than in

previous years is primarily a result of

a significant reduction in Canadian

Federal Tax effective December 2007.

Balance Sheet

Net Assets

Net assets at 31 December 2007

increased by 47% and include the

result of a property revaluation which

added £66.2m to property, plant and

equipment at the year end and the

retained result for the year of £62.5m.

Capital expenditure and acquisitions

together with high commodity prices

contributed to the 25% increase in

total assets year on year.

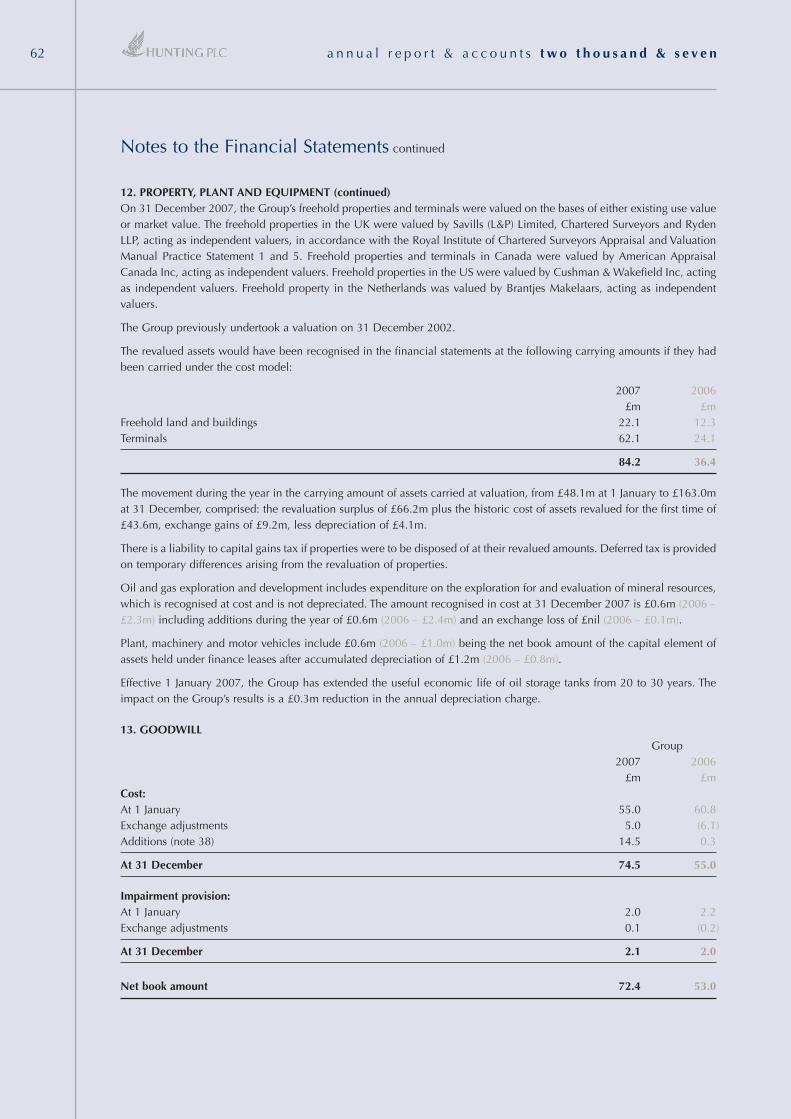

Property Revaluation

Group properties were revalued at

31 December 2007 giving rise to

an uplift of £66.2m in Group property

values. The resultant after tax increase

to the Group revaluation reserve was

£51.0m. The increase is principally

due to the strong economic conditions

driving property values in Alberta,

Canada.

Net Debt

Net debt increased to £139.2m

(2006 – £69.3m). Gearing increased

from 33% at the end of 2006 to

45% at 31 December 2007.

Finance Director’s ReviewResults Overview

Another strong year with revenuesand margins at record levels.

Revenue was £1,949.5m (2006 –£1,810.4m) with profit fromoperations up 14% at £98.5m (2006– £86.3m). This was achieved, eventhough both the US and Canadiandollars weakened against sterling.

Profit before tax recorded a 12%increase at £90.7m (2006 – £80.8m).If the 2007 results had been translatedusing 2006 rates the profit before taxwould have been £4.1m higher.

The results include a £2.3m exceptionalcharge relating to the disposal of ourformer Italian company, Aero Sekur.

Net Finance Costs

Net finance costs increased to £10.0m(2006 – £8.1m) following acquisitions,the increase in capital expenditure andhigher levels of working capital.Interest cover was 10 times.

Exchange Rates

Earnings Per Share

Basic earnings per share increased by17% from 37.6p in 2006 to 44.0p in2007. The average number of sharesused in calculating the earnings pershare in 2007 was 130.4m comparedto 128.9m in 2006.

Taxation

The tax charge for 2007 was £28.2m(2006 – £28.6m) which reflects an

2007 2006Average Year End Average Year End

US Dollar 2.00 1.99 1.84 1.96Canadian Dollar 2.15 1.96 2.09 2.28

Rates quoted to sterling

2007 2006£m £m

Total assets 920.2 735.3

Total liabilities (608.3) (523.8)

Net assets 311.9 211.5

Net debt 139.2 69.3

Gearing ratio 45% 33%

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n 11

07

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n12

Pensions

The Group continues to account forpensions in accordance with IAS 19and at the end of the year the netsurplus on the Group’s balance sheetwas £24.1m (2006 – £27.7m) ofwhich £25.2m (2006 – £30.1m)related to the UK defined benefitscheme which was closed to newentrants in 2002. An additional cashcontribution of £5.6m was paid to theUK defined benefit scheme in January2007 to fund the forecast cost on abuyout basis.

Liquidity, Resources and CapitalExpenditure

Cash Flow2007 2006

£m £m

Cash fromOperations 78.2 104.5

Tax Paid (20.0) (11.2)Replacement

CapitalExpenditure (31.4) (27.4)

Interest (9.4) (8.1)

Free Cash Flow 17.4 57.8

Acquisitions (30.8) (1.0)Growth Capital

Expenditure (30.6) (26.8)Dividends (10.1) (8.2)Foreign exchange (11.9) 10.3Other Movements (3.9) (4.4)

(Increase)Decrease inNet Debt (69.9) 27.7

Free cash flow, defined as profit fromoperations adjusted for workingcapital, tax, replacement capitalexpenditure and interest, generatedduring the year, was £17.4mcompared to £57.8m in 2006. Totalcapital expenditure was £62.0m(2006 – £54.2m) and included£23.7m in Gibson Energy and£36.5m (2006 – £31.3m) in HuntingEnergy Services which includes £7.0m(2006 – £10.2m) related to Explorationand Production. A further £30.2m wasspent on acquisitions in the year(£30.8m cash was paid during the year).

Liquidity and Funding

The Group has sufficient creditfacilities to meet its anticipatedfunding requirements over the shortand medium term. These facilities,which total £269.6m, includecommitted bank facilities of £172.5m,US$70m (£35.2m) Private PlacementNotes which mature in 2012 anduncommitted facilities of £61.9m. Thecommitted bank facilities include a£125m five year multi-currencyborrowing facility expiring inSeptember 2010.

The maturity profile of the Group’sundrawn credit facilities is shownwithin note 24 to the accounts.

Treasury Risk Management

The Group operates a centralisedTreasury service with policies andprocedures approved by the Board.These cover funding, bankingrelationships, foreign currency,interest rate exposures and cashmanagement. The policies and

procedures covering oil and gas priceexposure managed by Gibson Energyare approved by the Board.

Currency options are used to reducecurrency risk movements on theGroup’s results, by hedgingapproximately 50% of each year’sbudgeted Canadian and US Dollarearnings into Sterling. Currencyexposure on the balance sheet is,where practical, reduced by financingassets with borrowings in the samecurrency. Spot and forward foreignexchange contracts are used to coverthe net exposure of purchases andsales in non-domestic currencies.Price risk associated with sales,purchases and inventories of crude oiland petroleum products is managedthrough crude oil futures, swaps andoption contracts.

Interest expense is hedged by usinginterest rate swaps, interest rate caps,forward rate agreements and currencyswaps. At 31 December 2007, interestrate swaps and caps covered 44% ofnet borrowings.

Critical Accounting Policies

The Group accounts are preparedusing accounting policies inaccordance with IFRS. The principalaccounting polices are set out onpages 41 to 46.

The preparation of these accountsrequire the use of estimates,judgements and assumptions thataffect the reported amounts of assets,liabilities, revenue and expenses andthe disclosure of contingent assets

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n 13

and liabilities. Directors’ estimates arebased on historical experience,consultation with experts and othermethods that they believe arereasonable and appropriate.

Employee Benefits

The Group operates a defined benefitpension scheme in the UK, which wasclosed to new entrants with effect from31 December 2002, as well as anumber of smaller defined benefitschemes and defined contributionschemes within the Group. Thesedefined benefit schemes are accountedfor under IAS 19. The main actuarialassumptions used for the UK definedbenefit scheme are shown within note29 to the accounts and include:

Property Plant and Equipment

The Group’s property plant andequipment is subject to annual rates ofdepreciation intended to spread thecost of the assets over their estimatedservice life. These rates are regularlyreviewed. The rates currently in useare set out on page 42. The propertyrevaluation undertaken at the year endrelies on the judgements and estimatesmade by the Group’s qualifiedindependent property valuers.

Goodwill

The carrying value of goodwill heldon balance sheet is reviewed forimpairment at least annually. Thereview compares the carrying valuewith the estimated future cash flowsfrom the business unit to which the

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n14

goodwill relates. The cash flows arebased on management’s view offuture trading prospects. Any shortfallidentified is treated as an impairmentand written off.

Taxation

The effective tax rate for the full yearis 31.1% and is the combined ratearising from the regional mix ofGroup results. The rate also takes intoaccount the estimated futureutilisation of tax losses and theagreement with regional tax authoritiesof corporate tax computations.

Deferred Tax

A deferred tax asset and liability arerecorded within the financialstatements at 31 December 2007 of£7.1m and £98.1m respectively.These balances are derived fromassumptions which include the futureutilisation of trading losses andprovisions at assumed tax rates.

Share Based Payments

The estimated cost of grants ofequity instruments is spread evenlyover the vesting period. The actuarialassumptions used in determiningthe charge to income are set out innote 37.

Provisions

Provisions amounting to £19.9m areheld on balance sheet at the yearend. These are based on Directors’estimates of the future cost of currentobligations.

Primary Risks and UncertaintiesFacing the Business

The Group has an established riskmanagement monitoring and reviewprocess described in the CorporateGovernance report on pages 34 to 38.The process requires all businesses toidentify, evaluate and monitor risksand take steps to reduce, eliminate ormanage the risk. These risks arereviewed by the board three times a

year. In addition Risk Management isan agenda item at all Board meetings.

The primary risks and uncertaintiesfacing the business which could havea material adverse impact on theGroup include:

Commodity prices – Although notunder the control of the Company a material movement in commodity pricing could impactdemand for the Group’s products and services.

Effective control over subsidiaries –Group subsidiaries operate within aGroup framework with a degree ofautonomy vested in localmanagement. The operations ofsubsidiaries are subject to regularchecking by management togetherwith external and internal audit.

Health, Safety and Environmental(“HS&E”) – The adherence to GroupHS&E policy, local regulations andcompliance is discussed and reportedat all Board meetings. There is regularHS&E compliance reporting to theBoard.

Loss of key executives –Remuneration packages are regularlyreviewed to ensure key executivesand senior management are properlyremunerated.

Dennis ProctorChief Executive

Dennis ClarkFinance Director

Business Review

Assumption 2007 2006

Rate of inflation 3.5% 3.1%

Discountrate 5.7% 5.1%

Expected futurelifetime (yrs) 23.7 20.9

Expected future lifetime is the number ofyears a 65 year old male is expected tolive based on current mortality tables.

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n 15a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n 15

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n16

1. CHAIRMAN – RICHARD HUNTING ■Was elected an executive Director and Deputy Chairman on theformation of Hunting PLC in 1989 and has been Chairman of theBoard since 1991. Chairman of the Nominations Committee. Heis a non-executive director of Yule Catto & Co plc and of theRoyal Brompton & Harefield NHS Trust. Age 61

2. CHIEF EXECUTIVE – DENNIS PROCTOR ■Was appointed a Director in 2000 and Chief Executive in 2001.He was chief executive of Hunting Energy Services from March2000 after joining the Group in 1993. He is based in Houston,Texas and has held senior positions in the oil services industry inEurope, Iran and Canada as well as in the US. Age 55

3. FINANCE DIRECTOR – DENNIS CLARKWas appointed Finance Director of Hunting PLC in 1989 uponits formation. He is a non-executive director of Business PostGroup PLC. Age 64

4. EXECUTIVE DIRECTOR – TERRY GOMKEWas appointed a Director in 2000 and chief executive of GibsonEnergy in 1995. He began his Canadian Oil and Gas Industrycareer in 1974 and joined Gibson Energy in 1984. Currently heis a non-executive director and chairman of the AlbertaEconomic Development Authority. Age 55

5. NON-EXECUTIVE DIRECTOR – IAIN PATERSON ■■■Was appointed a non-executive Director in 2000 and ischairman of the Audit Committee and is the senior independentDirector. He is chairman of ITE Group plc and a non-executivedirector of ArmorGroup International plc and MOL Rt, theintegrated Hungarian energy company. He was internationaldirector at Enterprise Oil plc. Age 60

6. NON-EXECUTIVE DIRECTOR – GEORGE HELLAND ■■■Was appointed a non-executive Director in 2001 and ischairman of the Remuneration Committee. A U.S. citizen basedin Houston, Texas, he was Deputy Assistant Secretary in the U.S.Department of Energy from 1990 to 1993. He is a seniorassociate with Cambridge Energy Research Associates (CERA) ofCambridge, Massachusetts. Age 70

7. NON-EXECUTIVE DIRECTOR – HECTOR McFADYEN ■■■Was appointed a non-executive Director in 2002. A Canadiancitizen based in Calgary, Alberta with over 30 years experiencein the Canadian oil and gas industry. He was a senior executivewith Alberta Energy Company Ltd now EnCana Corporation andwas president of AEC Pipelines L.P. He is a director ofComputershare Trust Company of Canada and Harvest EnergyTrust. Age 64

Board of Directors

KEY:

■ AuditCommittee

■ NominationsCommittee

■ RemunerationCommittee

1 2

3 4

765

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n 17a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n 17

Board of Directors. From left to right: Richard Hunting, Dennis Clark, Dennis Proctor, George Helland,Hector McFadyen, Terry Gomke and Iain Paterson.

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n18

Report of the Directors

The Directors present their report, together with the audited financial statements for the year ended 31 December

2007.

Business Review and Principal ActivitiesThe Company is an industrial holding company, whose subsidiaries are primarily involved in international oil and

gas services. The Business Review, encompassing the Chief Executive’s Review and the Finance Director’s Review on

pages 4 to 14 together with the Chairman’s Statement on page 2, reports on the activities during the year ended

31 December 2007 and likely future developments. Details of the Company’s principal subsidiary and associated

undertakings are set out in note 46.

ResultsThe results of the Group are set out in the Consolidated Income Statement on page 47.

DividendsThe final dividend for 2006 of 5.2p per share (2005 – 4.0p) was paid on 2 July 2007 and on 21 November 2007 the

2007 interim dividend of 2.55p per Ordinary share was paid (2006 – 2.3p). The Directors recommend a final

Ordinary dividend of 5.7p per share (2006 – 5.2p) payable on 1 July 2008 to shareholders on the register at 30 May

2008.

DirectorsBrief biographies of the Directors are shown on page 16.

In accordance with the Articles of Association, Dennis Proctor and George Helland retire by rotation at the Annual

General Meeting and, being eligible, offer themselves for re-election. In addition, Richard Hunting offers himself for

re-election in accordance with the Combined Code on Corporate Governance.

No Director during the year had a material interest in any contract of significance to which either the Company or any

of its subsidiaries were a party. Directors’ interests in the shares of the Company are shown on pages 30 and 31. As at

31 December 2007, no Director of the Company had any beneficial interest in the shares of subsidiary companies.

Directors’ and Officers’ Liability InsuranceThe Company maintains insurance against certain liabilities which could arise from a negligent act or a breach of

duty by its Directors and officers in the discharge of their duties.

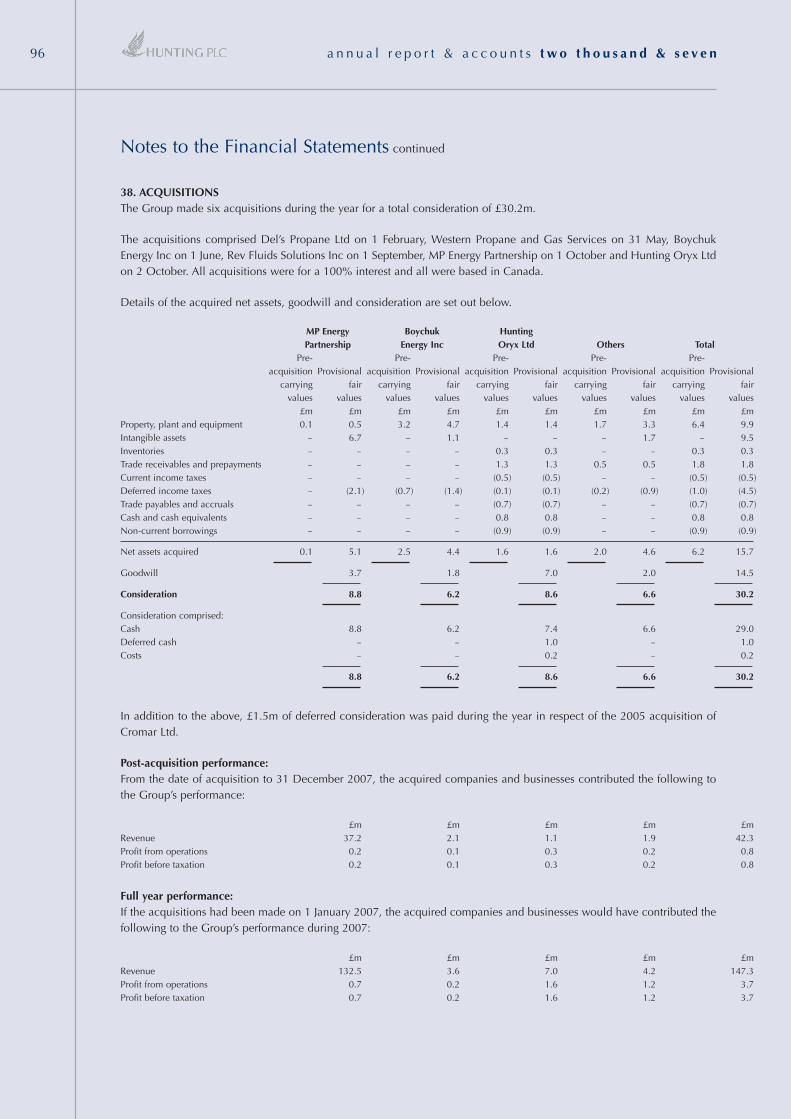

Principal AcquisitionsDuring 2007, the Group made the following six acquisitions, all of which were in Canada and all of which were for

a cash consideration only: Del’s Propane Ltd on 1 February for a consideration of £2.8m; Western Propane and Gas

Services on 31 May for £1.3m; Boychuk Energy Inc on 1 June for £6.2m; Rev Fluids Solutions Inc on 1 September

for £2.5m; MP Energy Partnership on 1 October for £8.8m and on 2 October, Hunting Oryx Ltd was acquired for

£8.6m, of which £1.0m is deferred. All the acquisitions were for 100% of the share capital except MP Energy

Partnership, which was an acquisition of its partnership units. Further details are provided in note 38 to the accounts.

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n 19

Report of the Directors continued

DisposalsOn 12 July 2007, the Group disposed of its interests in Aero Sekur SpA, its former Italian subsidiary, for a

consideration of £2.0m. Further details are provided in note 39 to the accounts.

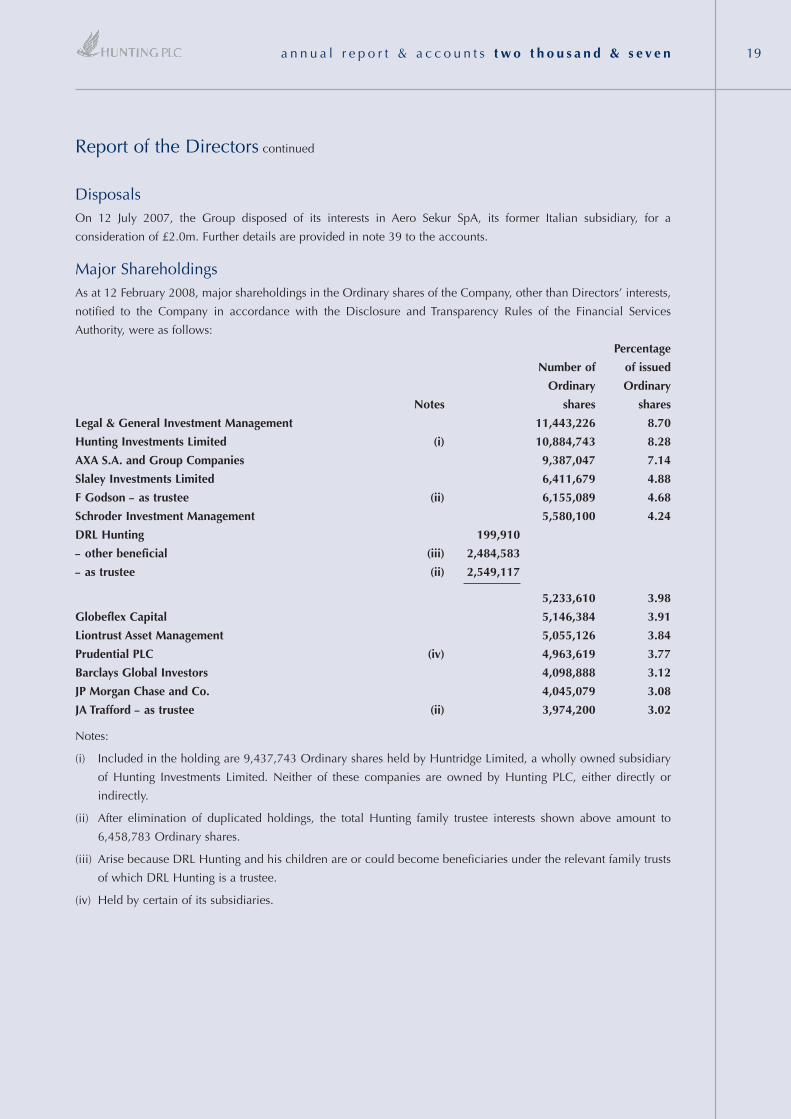

Major ShareholdingsAs at 12 February 2008, major shareholdings in the Ordinary shares of the Company, other than Directors’ interests,

notified to the Company in accordance with the Disclosure and Transparency Rules of the Financial Services

Authority, were as follows:

Percentage

Number of of issued

Ordinary Ordinary

Notes shares shares

Legal & General Investment Management 11,443,226 8.70

Hunting Investments Limited (i) 10,884,743 8.28

AXA S.A. and Group Companies 9,387,047 7.14

Slaley Investments Limited 6,411,679 4.88

F Godson – as trustee (ii) 6,155,089 4.68

Schroder Investment Management 5,580,100 4.24

DRL Hunting 199,910

– other beneficial (iii) 2,484,583

– as trustee (ii) 2,549,117

5,233,610 3.98

Globeflex Capital 5,146,384 3.91

Liontrust Asset Management 5,055,126 3.84

Prudential PLC (iv) 4,963,619 3.77

Barclays Global Investors 4,098,888 3.12

JP Morgan Chase and Co. 4,045,079 3.08

JA Trafford – as trustee (ii) 3,974,200 3.02

Notes:

(i) Included in the holding are 9,437,743 Ordinary shares held by Huntridge Limited, a wholly owned subsidiary

of Hunting Investments Limited. Neither of these companies are owned by Hunting PLC, either directly or

indirectly.

(ii) After elimination of duplicated holdings, the total Hunting family trustee interests shown above amount to

6,458,783 Ordinary shares.

(iii) Arise because DRL Hunting and his children are or could become beneficiaries under the relevant family trusts

of which DRL Hunting is a trustee.

(iv) Held by certain of its subsidiaries.

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n20

Corporate Social ResponsibilityDetails of the Group’s policies on employment, health, safety and the environment are contained within the Business

Review on page 5 and within the Corporate Social Responsibility Report on pages 24 and 25.

Research and DevelopmentGroup subsidiaries undertake, where appropriate, research and development to meet particular market and product

needs. The amount incurred and written off by the Group during the year was £0.7m (2006 – £1.0m).

Charitable and Political ContributionsDuring the year the Group donated £57,000 (2006 – £49,000) to UK charitable organisations and £213,000 (2006

– £137,000) to overseas charities. No UK political donations were made (2006 – £nil).

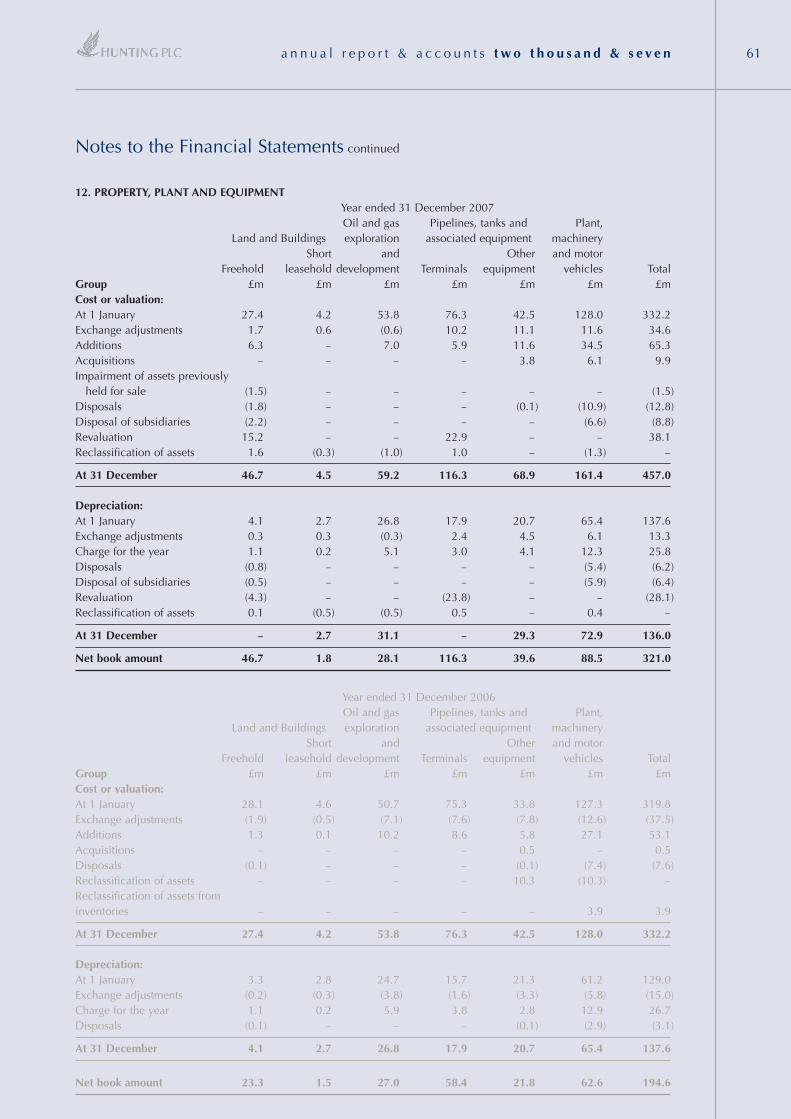

Property, Plant and EquipmentDetails of movements in property, plant and equipment are shown in note 12 to the financial statements.

Annual General Meeting The Annual General Meeting of the Company will be held on Wednesday 23 April 2008 at The Royal Automobile

Club, 89 Pall Mall, London SW1Y 5HS commencing at 10.30 a.m.

Further details of resolutions the Company is seeking for the allotment, issue and purchase of its Ordinary shares are

set out in the letter containing details of the Annual General Meeting which accompanies the Notice of the Annual

General Meeting to be held on 23 April 2008.

Powers of the Directors Subject to the Company’s Memorandum and Articles of Association, UK legislation and any directions prescribed by

ordinary resolution of the Company in general meeting, the business of the Company is managed by the Board. The

Directors have been authorised to allot and issue Ordinary shares and to make market purchases of the Company’s

Ordinary shares. These powers are exercised under authority of resolutions of the Company passed at its Annual

General Meeting.

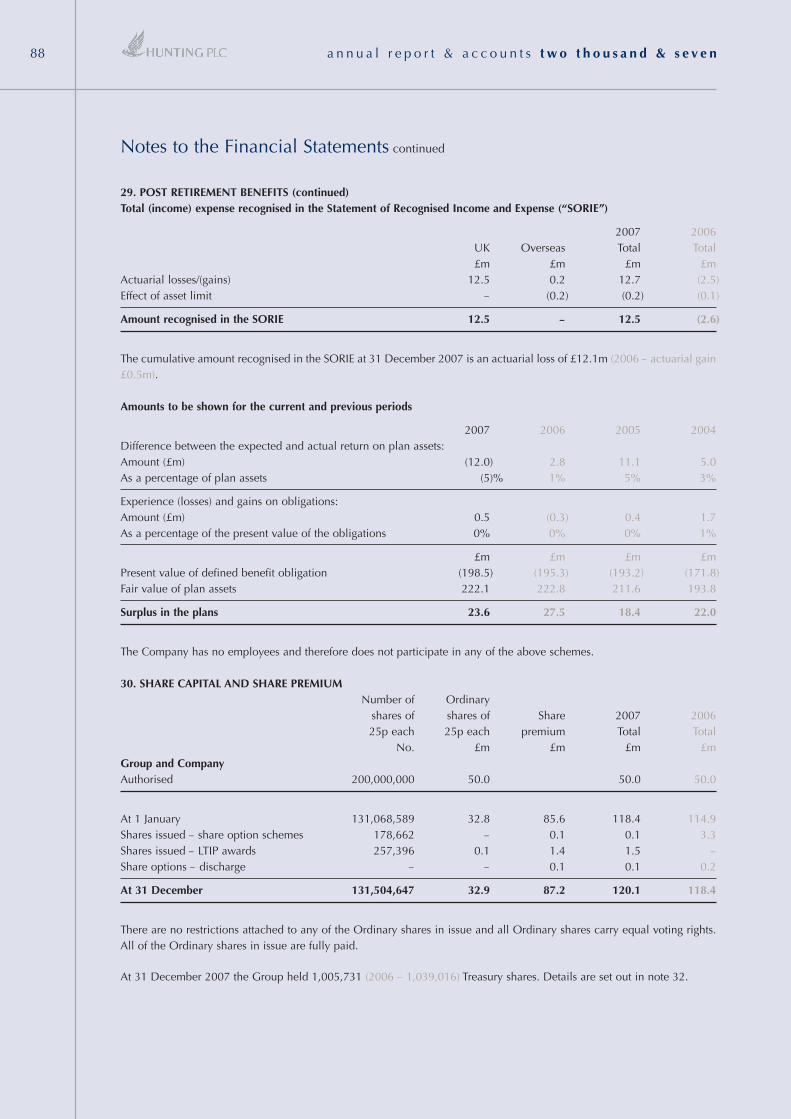

Share Capital The Company’s issued share capital comprises a single class of share capital which is divided into Ordinary shares

of 25 pence each. Details of the share capital of the Company are set out in note 30 to the financial statements. The

rights and obligations attaching to the Company’s Ordinary shares are set out in the Company’s Articles of

Association, copies of which can be obtained from Companies House in the UK or by writing to the Company

Secretary. Subject to applicable statutes, shares may be issued with such rights and restrictions as the Company may

by ordinary resolution decide, or (if there is no such resolution or so far as it does not make specific provision) as

the Board may decide. Holders of Ordinary shares are entitled to speak at general meetings of the Company, to

appoint one or more proxies and, if they are corporations, corporate representatives and to exercise voting rights.

Holders of Ordinary shares may receive a dividend and on a liquidation may share in the assets of the Company.

Holders of Ordinary shares are entitled to receive the Company’s annual report and accounts. Subject to meeting

certain thresholds, holders of the Ordinary shares may require a general meeting of the Company to be held or the

proposal of resolutions at Annual General Meetings.

Report of the Directors continued

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n 21

Report of the Directors continued

Authority to Allot Shares and Disapply Statutory Pre-Emption Rights The Directors will seek to renew their authorities to allot unissued shares and to disapply statutory pre-emption rights

at the Annual General Meeting to be held on 23 April 2008.

Purchase of Own Shares At the Annual General Meeting held on 25 April 2007, the Company was given authority to purchase up to

13,106,858 of its Ordinary shares until the date of its next Annual General Meeting. No purchases were made during

the year. The Directors will be seeking a new authority for the Company to purchase its Ordinary shares at the Annual

General Meeting to be held on 23 April 2008. Any shares purchased will be cancelled and the number of Ordinary

shares in issue reduced accordingly.

Voting Rights and Restrictions on Transfer of Shares On a show of hands at a general meeting of the Company every holder of Ordinary shares present in person or by

proxy and entitled to vote has one vote and on a poll every member present in person or by proxy and entitled to

vote has one vote for every Ordinary share held. Further details regarding voting at the Annual General Meeting can

be found in the notes to the Notice of the Annual General Meeting. None of the Ordinary shares carry any special

rights with regard to control of the Company. Proxy appointments and voting instructions must be received by the

Company’s Registrars not later than 48 hours before a general meeting. A shareholder can lose his entitlement to vote

at a general meeting where that shareholder has been served with a disclosure notice and has failed to provide the

Company with information concerning interests in those shares.

The Directors may refuse to register a transfer of a certificated share which is not fully paid, provided that the refusal

does not prevent dealings in shares in the Company from taking place on an open and proper basis. The Directors

may also refuse to register a transfer of a certificated share unless the instrument of transfer: (i) is lodged, duly

stamped (if stampable), at the registered office of the Company or any other place decided by the Directors

accompanied by the certificate for the share to which it relates and/or such other evidence as the Directors may

reasonably require to show the right of the transferor to make the transfer; (ii) is in respect of only one class of shares;

(iii) is in favour of a person who is not a minor, bankrupt or a person of unsound mind; or (iv) is in favour of not more

than four transferees.

Transfers of uncertificated shares must be carried out using CREST and the Directors can refuse to register a transfer

of an uncertificated share in accordance with the regulations governing the operation of CREST.

The Directors may decide to suspend the registration of transfers, for up to 30 days a year, by closing the register of

shareholders. The Directors cannot suspend the registration of transfers of any uncertificated shares without obtaining

consent from CREST.

There are no restrictions on the transfer of Ordinary shares in the Company other than:

• certain restrictions may from time to time be imposed by laws and regulations (for example insider trading

laws);

• pursuant to the Company’s share dealing code whereby the Directors and certain employees of the Company

require approval to deal in the Company’s shares; and

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n22

• where a shareholder with at least a 0.25% interest in the Company’s certificated shares has been served with

a disclosure notice and has failed to provide the Company with information concerning interests in those

shares.

The Company is not aware of any agreements between shareholders that may result in restrictions on the transfer of

Ordinary shares or on voting rights.

Articles of Association The Company’s Articles of Association may only be amended by special resolution at a general meeting of the

shareholders. At the Annual General Meeting to be held on 23 April 2008, a resolution will be put to shareholders

proposing the adoption of new Articles of Association. A summary of the principal proposed changes can be found

in the Appendix to the Notice of Annual General Meeting.

Significant Agreements The Company is a party to certain funding agreements in which the counterparties can determine whether or not tocancel the agreements where there has been a change of control of the Company.

The service agreements of the executive Directors include provisions that provide for compensation for loss of officeor employment as a result of a change of control. Further details of the Directors’ service contracts can be found inthe Remuneration Committee’s Report on pages 28 and 29.

Appointment and Replacement of Directors Rules for the appointment and replacement of Directors are set out in the Company’s Articles of Association.Directors are appointed by the Company by ordinary resolution at a general meeting of holders of Ordinary sharesor by the Board on the recommendation of the Nomination Committee. The Company may also remove a Director.The Corporate Governance Report sets out further details of the requirements for re-election of Directors on page 34.In addition, further details of the workings of the Nomination Committee are set out on page 35.

Policy on Payment of CreditorsThe Company’s and Group’s policy is to pay all creditors in accordance with agreed terms of business. The Companyitself has no substantial trade payables. The total amount of Group trade payables falling due within one year at31 December 2007 represents 40 days worth (2006 – 33 days), as a proportion of the total amount invoiced bysuppliers during the year ended on that date.

Statement on Disclosure of Information to AuditorsIn accordance with Companies Act requirements all Directors in office as at the date of this report have confirmedso far as they are aware there is no relevant audit information of which the Company’s auditors are unaware andeach Director has taken all reasonable steps necessary in order to make himself aware of any relevant auditinformation and to establish that the Company’s auditors are aware of that information.

Going ConcernThe Directors, after making enquiries and on the basis of current financial projections and the facilities available,believe that the Company and the Group have adequate financial resources to continue in operation for theforeseeable future. For this reason, they continue to adopt the going concern basis in preparing the financialstatements.

Report of the Directors continued

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n 23

Report of the Directors continued

AuditorsPricewaterhouseCoopers LLP have indicated their willingness to continue in office as auditors. A resolution to reappoint

them as auditors to the Company will be proposed at the Annual General Meeting to be held on 23 April 2008.

By order of the BoardPeter RoseCompany Secretary

28 February 2008

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n24

IntroductionThis report describes the policies and procedures put in place by the board to ensure that the Company operates in

a safe and responsible manner and where practical takes steps to protect the environment.

The Company acknowledges and is committed to its corporate social responsibilities within the areas in which it

operates. Its contribution and involvement is determined by the regional custom and best practice in those locations

and is subject to regular monitoring and review by the board and divisional management.

Employment and TrainingThe Company recognises that its success and reputation is dependent upon the efforts and the integrity of its people.

It encourages and promotes an awareness of the financial and economic factors affecting the performance of the

Company through regular communication and consults with employees to the degree relevant to local conditions.

• As a responsible employer, full and fair consideration is given to applications for positions from disabled persons

and to their training and career advancement. Every effort is made to retain in employment those who become

disabled while employed by the Company.

• Appropriate training is provided to employees to suit their particular work environment within the Company.

• Communication with employees is undertaken through a variety of media including the bi-annual Hunting

Review magazine.

Health and SafetyThe Company is committed to achieving and maintaining the highest standards of safety for its employees,

customers, suppliers and the public. The Group operates a range of facilities and installations and each location has

in place a tailored health and safety programme designed to at a minimum comply with local regulatory

requirements. All subsidiaries target continuous improvement to their Health and Safety Standards. The Health and

Safety policies include:

• Regular review and audit of equipment, practices and procedures to assure compliance with prevailing standards

and legislation.

• Accreditation is sought and procedures are aligned with long standing company programmes to internationally

recognised Quality Assurance standards.

• Monitoring is a management task which is documented and reported at each board meeting.

• Appropriate training and education of all staff.

The Chief Executive, who is directly responsible for Health and Safety, presents a Health and Safety report at every

PLC board meeting.

EnvironmentThe Group’s environmental policy is to look for opportunities and adopt practices that create a safer and cleaner

environment. It is particularly sensitive to the challenges for the industry in which it operates. The Group has

programmes in place to monitor environmental impact from its operational activities and remains focused on

ensuring environmental consideration is at the forefront of its business practices.

Corporate Social Responsibility

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n 25

Corporate Social Responsibility continued

Key aspects of the environmental policies include:

• Policies, procedures and practices are in place so that any adverse effects on the environment are reduced to a

practicable minimum.

• The Group encourages the reduction of waste and emissions and promotes awareness of recycled materials and

use of renewable resources.

• Each operating unit develops and implements its own procedures and conducts structured reviews to ensure that

they are maintained and refined.

• Employees are encouraged to pay special regard to environmental concerns in the communities in which the

Group operates.

Regulatory EnvironmentThe Company is listed on the London Stock Exchange and is subject to regulation by the Financial Services Authority

in the United Kingdom as well as compliance with UK Company Law. With the aim of maintaining standards and to

comply with customer trading requirements a high proportion of our operating facilities are either ISO or API

registered or subject to other similar registrations or industry qualifications.

Business EthicsThe Group targets and encourages the highest standards of integrity and honesty in all business dealings. The

objective is to maintain and enhance the reputation of the Company and enforce ethical dealings with customers

and suppliers.

The Board has established “whistle blowing” procedures for any employee to raise in confidence any concerns they

may have about possible financial improprieties or other matters with either the Chairman of the Board or the senior

independent Director. Details of the procedure have been communicated to all employees.

Hunting in the CommunitySubsidiaries support a range of charitable and community projects in their local areas. Of particular note in 2007,

was the annual Hunting Art competition held in Houston, Texas, which raised in excess of US$100,000 for SIRE, a

local charity assisting disabled people.

Dennis Proctor

Chief Executive

28 February 2008

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n26

Remuneration CommitteeThe Remuneration Committee of the Board (“the Committee”), which met four times in 2007, comprises the non-executive Directors of the Company.

George Helland (chairman), Iain Paterson and Hector McFadyen all served throughout the year. The Committee isresponsible for determining in particular the remuneration of the Chairman and executive Directors, including thesetting of annual performance targets and participation in the executive share option plans.

During the year Hewitt Bacon & Woodrow, who were appointed by the Committee, provided advice and assistanceon Directors’ remuneration, executive incentive plans and share scheme matters. The Company also received adviceon various remuneration matters during the year from Buck Consultants Limited.

The Board determines fees payable to the non-executive Directors who do not participate in the Group’s share plansor receive any other benefits.

The constitution and operation of the Committee during the year has complied with the Combined Code’s guidanceon Directors’ remuneration, except for the recommended period of notice for executive Directors as referred tobelow.

Remuneration PolicyThe Company’s policy on remuneration aims to ensure that the individual rewards and incentives are competitiveand appropriate to attract, motivate and retain executives of high ability, experience and commitment.

The executive Directors’ remuneration packages consist of an annual salary, health cover, and where appropriate,car and fuel benefits, life and disability insurance, an annual performance linked cash bonus plan, pensioncontributions, participation in performance-linked share plans and a performance-linked long term incentive plan.Performance targets are established to achieve consistency with the interests of shareholders with an appropriatebalance between long and short-term goals.

Basic salaries are reviewed annually. In considering appropriate salary levels, the Committee takes into account theremuneration paid by comparable companies in terms of asset size, revenues, profits, the number of employees,market capitalisation and the complexity and international spread of the Group’s operations as well as applicablerates of inflation. The Company’s practice is to target basic salaries at the mid-market level in the appropriate marketfor the executive position. In determining executive salaries consideration is given to their experience and generalperformance level.

The Company operates an executive share option scheme to provide longer term incentives for executives andexecutive Directors. This reflects market practice, provides longer term focus and aligns the interests of executivesand shareholders. The award of options under the scheme are performance related and are principally aligned to thebasic salary of the Director. The right to exercise an option is subject to the growth performance of the Company’sbasic earnings per share (“BEPS”) over a three year period in comparison to that of comparator companies, whocomprise UK, US and Canadian oil and gas services companies. No shares are exercisable if the growth in BEPS doesnot exceed the rate of inflation by at least 3% per annum over the three year period. The number of sharesexercisable, expressed as a percentage, by a Director can range from nil if the Company’s performance is below themedian level, to 40% at the median level and up to 100% if the Company’s performance is between the median andupper quartile levels of the comparator group.

The Company’s Long Term Incentive Plan (“LTIP”) is intended to link key executives’ remuneration to the long-termsuccess and performance of the Group.

The Remuneration Committee’s Report

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n 27

The Remuneration Committee’s Report continued

The LTIP is a performance-linked plan with an incentive pool which for 2007 is calculated using the sum of theGroup’s after tax operating income after deducting a charge for the after tax cost of capital at a rate of 7% on averageshareholders’ funds. The incentive has two components, the first being 2% of the absolute value added, and thesecond being 5% of the incremental value added. These performance conditions align the interests of the executiveswith those of the Group and its shareholders and will only produce value to the participants if value is created forthe Group.

Awards are determined for each participant at the beginning of a three-year performance cycle and are settled at theend of each cycle either in shares or in cash. The award for each participant is calculated as a percentage of theincentive pool resulting from the performance of the business over the performance cycle as determined by theCommittee.

At 31 December 2007 the pool available for distribution has increased from £4,526,761 to £6,219,577 following anincrease in the pool of £1,692,816.

Following vesting, the amount payable under any single award may not exceed a certain multiple of the basic annualsalary of each participant as at the relevant award date. The maximum award levels under the LTIP rules as a multipleof base salaries are 3.5 times annual salary for the Chief Executive and 1.75 times annual salary for other executiveDirectors. As the pool was greater than these maximum levels, the awards were restricted to these multiples. Theamount of the pool awarded to all participants as a result of this restriction was £3,542,693.

In 2007 an annual performance-linked cash bonus scheme was in place for the executive Directors. The scheme,which is not pensionable, is designed to provide an incentive and reward for performance and reflects thecompetitive markets in which the Group conducts its business.

Dennis Proctor and Dennis Clark are eligible for a bonus under the scheme when 80% of the Group budgeted pretax profit is achieved. Below this level no bonus is payable. The amount payable under the scheme whenperformance achieves the budgeted profit before tax and return on capital targets, is 65% of base salary for DennisProctor and 50% of base salary for Dennis Clark. When actual results achieve 120% of these performance targetsDennis Proctor and Dennis Clark are entitled to a maximum cash bonus of 130% and 100% of base salaryrespectively. Terry Gomke has a similar scheme based on the same percentages as set out above for Dennis Clark.However his entitlement is based on the results of Gibson Energy.

Richard Hunting has no bonus entitlement and his remuneration and that of the non-executive Directors is whollynon-performance related.

The current balance between fixed and variable remuneration is approximately 28% deriving from salary andbenefits and 72% from variable incentives.

Bonus schemes are also in place for the majority of Group employees.

a n n u a l r e p o r t & a c c o u n t s t w o t h o u s a n d & s e v e n28

Performance graphThe graph below compares the total shareholder return for an investment in Hunting PLC Ordinary shares with the

return for the same investment in the FTSE Oil and Gas index commencing on 31 December 2002.

Total Shareholder Return vs FTSE Oil & Gas Index

In the opinion of the Directors the FTSE Oil and Gas Index is the most appropriate index against which the total

shareholder return of the Company should be compared, because this is the sector in which the Company is quoted.

Directors’ Service ContractsThe Company’s policy on executive Directors’ contracts is to comply with the guidance in the Combined Code. Thecontracts of Richard Hunting, Dennis Proctor and Dennis Clark are in compliance with that guidance. Terry Gomke’scontract pre-dates this policy and presently the Remuneration Committee does not consider it appropriate to seek toamend his contract which is in accordance with Canadian practice.

All the Directors’ Service Agreements contain standard provisions allowing the Company to terminate summarily forcause, such as gross misconduct.

Dennis Proctor entered into an Employment Agreement with Hunting Energy Services Inc, a wholly ownedsubsidiary of the Company, on 7 February 2001. This Agreement is governed by the laws of the State of Delaware,USA. Under the terms of the Agreement both Hunting Energy Services Inc and Dennis Proctor are required to giveone year’s notice of termination.