ifrs convergence impact on the consolidated … · no. 1 convergence to ifrs •adoption of ifrs...

TRANSCRIPT

IFRS CONVERGENCE IMPACT ON THE CONSOLIDATED FINANCIAL STATEMENTS Monday May 1st 2017

No. 1

CONVERGENCE TO IFRS

• Adoption of IFRS streamlines SABIC’s worldwide financial reporting and enhances its consistency and transparency

• SABIC Group’s non-listed subsidiaries have early adopted IFRS by one year – this promotes further harmony and efficiency in SABIC Group’s accounting and reporting function

• IFRS provides a fresh perspective on certain of our operational matters enabling us to gain more efficiencies

• IFRS has impacted recognition, measurement and disclosure of key items like property, plant and equipment, intangible assets and employee benefit liabilities – although overall impact on net assets has not been significant for SABIC Group

IFRS impacts the way we view our business

• Business strategy, model and core operations

• Stringent risk management approach; and

• Cash flows and dividend policy

Applying IFRS will not change our:

• Streamline the presentation of financial statements of Saudi companies with increased comparability not only among Saudi companies, but also with global markets

• Provide greater transparency on business performances

• Support the Kingdom’s 2030 vision towards further maturity of Saudi capital market and its attractiveness to investors – both local and international

IFRS in Saudi Arabia will generally:

No. 2

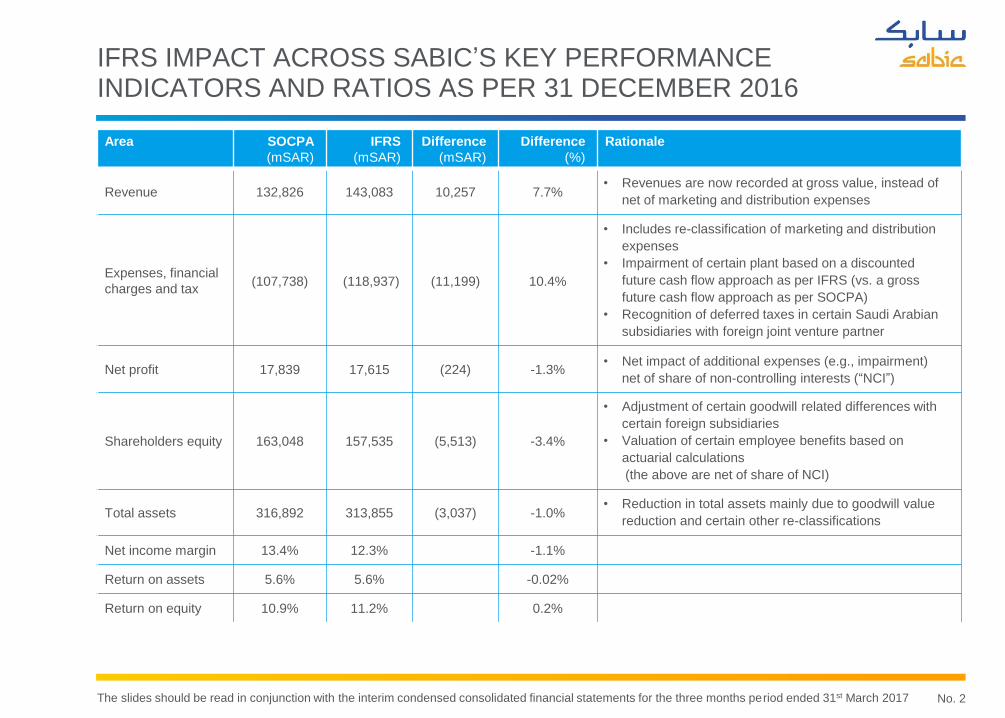

IFRS IMPACT ACROSS SABIC’S KEY PERFORMANCE INDICATORS AND RATIOS AS PER 31 DECEMBER 2016

Area SOCPA

(mSAR)

IFRS

(mSAR)

Difference

(mSAR)

Difference

(%)

Rationale

Revenue 132,826 143,083 10,257 7.7%• Revenues are now recorded at gross value, instead of

net of marketing and distribution expenses

Expenses, financial

charges and tax(107,738) (118,937) (11,199) 10.4%

• Includes re-classification of marketing and distribution

expenses

• Impairment of certain plant based on a discounted

future cash flow approach as per IFRS (vs. a gross

future cash flow approach as per SOCPA)

• Recognition of deferred taxes in certain Saudi Arabian

subsidiaries with foreign joint venture partner

Net profit 17,839 17,615 (224) -1.3%• Net impact of additional expenses (e.g., impairment)

net of share of non-controlling interests (“NCI”)

Shareholders equity 163,048 157,535 (5,513) -3.4%

• Adjustment of certain goodwill related differences with

certain foreign subsidiaries

• Valuation of certain employee benefits based on

actuarial calculations

(the above are net of share of NCI)

Total assets 316,892 313,855 (3,037) -1.0%• Reduction in total assets mainly due to goodwill value

reduction and certain other re-classifications

Net income margin 13.4% 12.3% -1.1%

Return on assets 5.6% 5.6% -0.02%

Return on equity 10.9% 11.2% 0.2%

The slides should be read in conjunction with the interim condensed consolidated financial statements for the three months period ended 31st March 2017

No. 3

IFRS IMPACT ON NET PROFIT FOR THE YEAR ENDED 2016

Under IFRS, end of service

benefits (“EOSB”), is calculated

using actuarial assumptions for

post-employment medical

benefits, continuous service

awards and other such benefits

Actuarial valuation

Impairment of a certain plant

based on a discounted future

cash flow approach as per IFRS

(vs. a gross future cash flow

approach as per SOCPA)

Impairment Accounting

This represents share of Non

controlling interest (NCI) in all

IFRS adjustments

NCI

17,615

NCI Net profit

under IFRS

(SAR’ mln)

-1.3%

-2.2%

Impairment

of PPE

-0.2%

Actuarial

valuation of

employee

benefits

Others, net

4.8%

17,839

-3.8%

Net profit

under

SOCPA

(SAR’ mln)

The slides should be read in conjunction with the interim condensed consolidated financial statements for the three months period ended 31st March 2017

No. 4

IFRS IMPACT ON SHAREHOLDERS EQUITY AS OF 31ST DEC2016

Under IFRS, end of service

benefits (“EOSB”), is calculated

using actuarial assumptions for

post-employment medical

benefits, continuous service

awards and other such benefits

Actuarial valuation

Impairment of a certain plant

based on a discounted future

cash flow approach as per IFRS

(vs. a gross future cash flow

approach as per SOCPA)

Impairment Accounting

Adjustment of certain goodwill

related differences with certain

foreign subsidiaries

Goodwill

Change in book value of PP&E

due to componentization as a

result of new components

having a different overall

average useful life

Componentization

-0.2%

0.2%0.3%

Reduction

in value of

goodwill

Impairment

of PP&E

Componen-

tisation

157,535

-3.4%

Others Equity

under IFRS

(SAR’mln)

-1.9%

Actuarial

valuation of

employee

benefits

-1.8%

Equity

under

SOCPA

(SAR’mln)

163,048

The slides should be read in conjunction with the interim condensed consolidated financial statements for the three months period ended 31st March 2017