innovative approaches to investing in and funding ... · franchise gse rental programmes...

TRANSCRIPT

STRICTLY CONFIDENTIAL

CAPA Conference: MumbaiPeter Farthing, Macquarie Bank Limited

1 February 2018

Innovative Approaches to Investing in and Funding Infrastructure

Contents

STRICTLY CONFIDENTIAL

01 Macquarie’s Presence in Infrastructure and Aviation 2

02 Investing in Infrastructure Assets 9

03

Alternative Funding and Investing Strategies:

• Slots Financings

• Future Flow Securitisations

• Ground Support Equipment

15

STRICTLY CONFIDENTIAL

1Macquarie’s Presence in Aerospace and

Aviation

PAGE 3STRICTLY CONFIDENTIAL MACQUARIE

Macquarie Aviation/Aerospace highlights

Specialised airport and aviation financing, asset management, equipment trading/remarketing, & asset services

AIRPORT

INVESTMENT

+20 investments

in 14 years

Long term direct

investor manager

Value enhancing

operational focus

Airport and

terminal manager

Servicing ~ 144m

passengers per

annum

AIRPORT

SERVICES

Arlanda &

Stansted rail

Own / operate

Stansted Express

Own / operate

Arlanda Express

Baggage trolley

franchise

GSE RENTAL

PROGRAMMES

Specialised GSE

rental solutions

Tailored rental

arrangements

Broad coverage of

airside equipment

3-10 year rental

facilities

Maintenance &

Telematics options

CHECK-IN &

TICKETING

Key airport

ITC rental

Ticketing kiosk

rentals

Information

display rentals

Managed

technology services

POS technology

and retail fit-out

AIRCRAFT

LEASING

USD7bn aircraft

portfolio

+270 commercial

aircraft

+90 airline clients

worldwide

Experienced

management

Most modern

aircraft types

PAGE 4STRICTLY CONFIDENTIAL MACQUARIE

GroupsMacquarie India platform1

MacCap is a leading financial advisor in infrastructure and real estate transactions

ranking #3 by Bloomberg for announced M&A in CY2015 and #1 infrastructure advisor

in India. MacCap is also a leader in Private Capital Markets (PCM) transactions in India,

having advised on more than $US5b transactions in real estate and infrastructure

Macquarie Capital

MIRA managed funds are among the largest foreign infrastructure investors in India with $US1.3b

invested across 25 projects. MIRA managed funds are also collectively the largest investor in

Indian toll roads with with over 4,000 lane kilometres equity invested of ~$US465m2 across 15

assets

Macquarie Asset Management

Macquarie is a leading broking and research house in India and is with a market share of more

than 6%. Current research coverage of 101 stocks (over ranked top 8 equites broker in India

70% of overall market cap and over 85% of NIFTY Index). The Commodities and Financial

Markets division provides structured trade finance solutions across financing, physical supplies/

off-take, logistics and hedging

Commodities and Global Markets

1. Headcount as at 31 March 2017. 2 Includes investments exited in March 2017

795

staff

in

Gurgaon

103

staff in

Mumbai

Provides finance, technology, risk management and MAM operations services across all

Macquarie business groups, divisions and geographies. Operates as an extension of global

functional teams servicing respective functions globally with the FMG footprint being the highest

(40% of global FMG headcount)

Global Finance Services (GFS)

Macquarie is the biggest Infrastructure Investor in the World with US36.5b capital raised (Infrastructure

Investor 2017)

Macquarie has a long standing commitment to the Indian market, being based here since 2006 and with 900 staff across Delhi and Mumbai

Macquarie’s India Platform

PAGE 5STRICTLY CONFIDENTIAL MACQUARIE

A

B

A

B

C

D EF

G

H

K

J

A B

C

DE

G

A

F

ML

H

Delhi

Mumbai

Chennai

N

O

Airports Energy Roads Telecom

towers

MIRA IndiaUS$ 1.6b deployed in 44 assets across two funds

MB Power (Madhya Pradesh) Limited

1,200 MW coal based power plant in

Anuppur

Adhunik Power and Natural Resources

Limited

540 MW coal based power plant in

Jamshedpur

Ambuthirtha (Soham Renewable Energy)

22MW operational hydropower plant

Mannapitlu (Soham Renewable Energy)

15MW operational hydropower plant

Mahadevpura (Soham Renewable

Energy)

6MW hydropower plant

Mullibettu (Soham Renewable Energy)

10.5MW hydropower plant

Nekkilady (Soham Renewable Energy)

12.5MW hydropower plant, under

construction

Ind Barath Energy Utkal Limited

700 MW coal based thermal power plant

Stridor Portfolio Assets (Punjab)

31 MW across 2 solar assets

Stridor Portfolio Assets (Gujrat)

253 MW across 12 solar assets

Stridor Portfolio Assets (Madhya

Pradesh)

27 MW across 1 solar asset

Stridor Portfolio Assets (Tamil Nadu)

5 MW across 1 solar asset

Stridor Portfolio Assets (Orissa)

5.5 MW across 1 solar asset

Stridor Portfolio Assets (West Bengal)

5 MW across 1 solar asset

G

A

B

C

D

F

E

ATC Telecom Gurgaon (Head office)

India’s 2nd largest tower company by

tenancies

A

H

I

J

K

L

M

N

Indira Gandhi International

Airport (Delhi)

India’s largest airport by PAX

Rajiv Gandhi International Airport

(Hyderabad)

India’s sixth largest airport by PAX

A

B

Jaora – Nayagaon Road

128km long toll road, currently tolling

Kharar – Ludhiana Road

78km long HAM road, currently under

development

Belgaum – Dharwad Road

79km long toll road, currently tolling

Bhandara Road

80km long toll road, currently tolling

Durg Road

83km long toll road, currently tolling

Sambalpur – Baragarh Road

88km long toll road, currently tolling

A

B

C

D

E

Dhankuni – Kharagpur Road

111km toll road, currently tolling

Chennai Outer Ring Road

30km long annuity road, under construction

Ranastalam – Anandapuram

47km long HAM road, under construction

Jadcherla Expressways Private Limited

58km long toll road, currently tolling

Trichy Tollways Private Limited

94km long toll Road, currently tolling

Ahmedabad Mehsana Road

52km long toll road currently tolling

Vadodara Halol Road

32km long toll road currently tolling

Tada Nellore Road

111km long toll road currently tolling

Nandigama Viajayawada Road

49km long toll road currently tolling

H

I

K

J

L

M

N

O

I

J K

L

M

N

G

F

I

Divested in March 2017.

PAGE 6STRICTLY CONFIDENTIAL MACQUARIE

GMR Airports Limited has key ownership stakes in:

• 64% stake in Delhi Airport Ltd

• 63% stake in GMR Hyderabad Airport.

Case Study: Delhi/Hyderabad Airports

Macquarie Asia Infrastructure Fund invested US$200m into GMR Airports Limited

Investment details

• Convertible preference share investment

• Convertible to equity 4 years from investment.

Rationale:

• vital operating airports critical to India's aviation

sector

• regulated assets

• Good asset quality

Key Concerns:

Regulatory regime at the time of investment –the regulator had just been formed and DIAL was hybrid till, GHIAL was single till. Since then, GHIAL is now hybrid till.

Real estate monetization - pricing and schedule of Delhi Airport land

Restriction on land usage at Delhi Airport –being restricted to only Airport related activities Thus a large number of hotels constructed at Delhi Airport

PAGE 7STRICTLY CONFIDENTIAL MACQUARIE

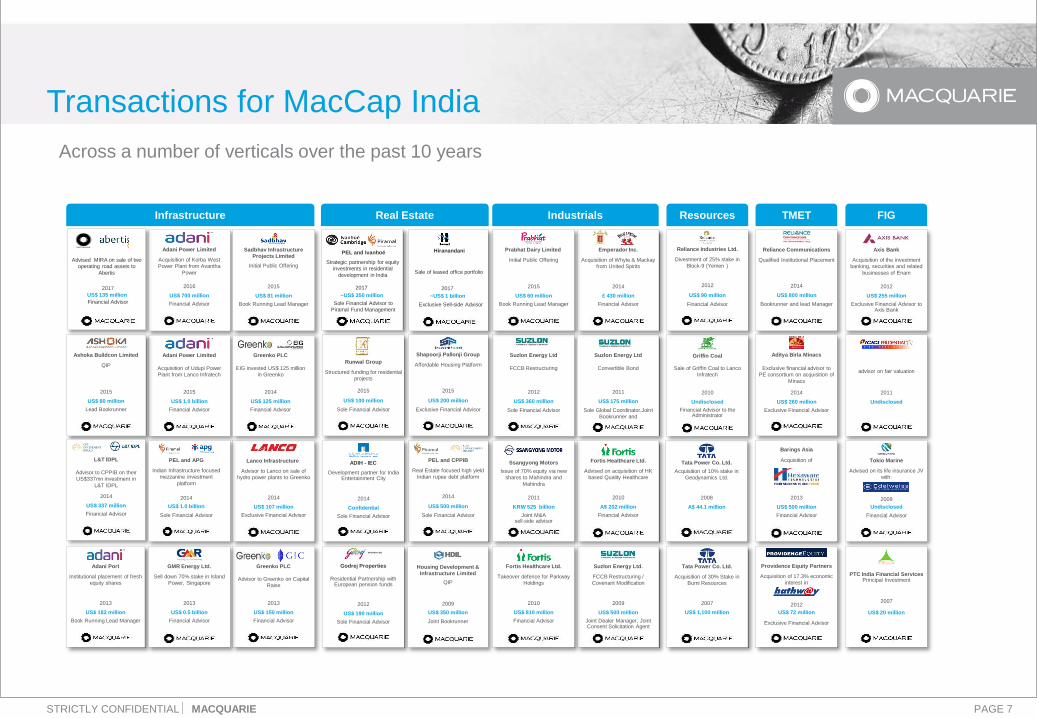

Resources

Tata Power Co. Ltd.

Acquisition of 10% stake in

Geodynamics Ltd.

A$ 44.1 million

2008

Tata Power Co. Ltd.

Acquisition of 30% Stake in

Bumi Resources

US$ 1,100 million

2007

Sale of Griffin Coal to Lanco

Infratech

Undisclosed

2010

Griffin Coal

Financial Advisor to the Administrator

Divestment of 25% stake in

Block-9 (Yemen )

US$ 90 million

Financial Advisor

Reliance Industries Ltd.

2012

Transactions for MacCap India

Real Estate

Residential Partnership with European pension funds

2012

US$ 190 million

Godrej Properties

Sole Financial Advisor

QIP

US$ 350 million

Housing Development &

Infrastructure Limited

Joint Bookrunner

2009

FIG

US$ 255 million

Exclusive Financial Advisor to Axis Bank

2012

Acquisition of the investment

banking, securities and related

businesses of Enam

Axis Bank

PTC India Financial ServicesPrincipal Investment

US$ 20 million

2007

advisor on fair valuation

Undisclosed

2011

Undisclosed

Financial Advisor

Tokio Marine

2009

Advised on its life insurance JV

with:

FCCB Restructuring

US$ 360 million

Sole Financial Advisor

Suzlon Energy Ltd

2012

Convertible Bond

US$ 175 million

Sole Global Coordinator,Joint

Bookrunner and

Lead Manager

Suzlon Energy Ltd

2011

Suzlon Energy Ltd.

FCCB Restructuring /

Covenant Modification

US$ 500 million

Joint Dealer Manager, Joint Consent Solicitation Agent

2009

Industrials

Fortis Healthcare Ltd.

Advised on acquisition of HK

based Quality Healthcare

A$ 202 million

Financial Advisor

2010

Fortis Healthcare Ltd.

Takeover defence for Parkway

Holdings

US$ 810 million

Financial Advisor

2010

Acquisition of Whyte & Mackay

from United Spirits

£ 430 million

Financial Advisor

Emperador Inc.

2014

Infrastructure

US$ 107 million

Exclusive Financial Advisor

2014

Advisor to Lanco on sale of

hydro power plants to Greenko

Lanco Infrastructure

US$ 182 million

Book Running Lead Manager

2013

Institutional placement of fresh

equity shares

Adani Port

US$ 150 million

Financial Advisor

2013

Advisor to Greenko on Capital

Raise

Greenko PLC

US$ 0.5 billion

Financial Advisor

2013

Sell down 70% stake in Island

Power, Singapore

GMR Energy Ltd.

US$ 700 million

Financial Advisor

2016

Acquisition of Korba West

Power Plant from Avantha

Power

Adani Power Limited

US$ 1.0 billion

Financial Advisor

2015

Acquisition of Udupi Power

Plant from Lanco Infratech

Adani Power Limited

US$ 80 million

Lead Bookrunner

2015

QIP

Ashoka Buildcon Limited

US$ 337 million

Financial Advisor

2014

Advisor to CPPIB on their

US$337mn investment in

L&T IDPL

L&T IDPL

Indian Infrastructure focused

mezzanine investment

platform

US$ 1.0 billion

Sole Financial Advisor

PEL and APG

2014

US$ 125 million

Financial Advisor

2014

EIG invested US$ 125 million

in Greenko

Greenko PLC

Real Estate focused high yield

Indian rupee debt platform

US$ 500 million

Sole Financial Advisor

PEL and CPPIB

2014

Structured funding for residential

projects

US$ 100 million

Sole Financial Advisor

Runwal Group

2015

US$ 60 million

Book Running Lead Manager

2015

Initial Public Offering

Prabhat Dairy Limited

US$ 81 million

Book Running Lead Manager

2015

Initial Public Offering

Sadbhav Infrastructure

Projects Limited

Development partner for India Entertainment City

2014

Confidential

ADIH - IEC

Sole Financial Advisor

Issue of 70% equity via new

shares to Mahindra and

Mahindra

KRW 525 billion

Joint M&A sell-side advisor

2011

Ssangyong Motors

TMET

Bookrunner and lead Manager

Reliance Communications

Qualified Institutional Placement

2014

US$ 800 million

US$ 72 million

Exclusive Financial Advisor

Providence Equity Partners

2012

Acquisition of 17.3% economic

interest in

Exclusive Financial Advisor

Aditya Birla Minacs

Exclusive financial advisor to

PE consortium on acquisition of

Minacs

2014

US$ 260 million

US$ 500 million

Financial Advisor

2013

Acquisition of

Barings Asia

Strategic partnership for equity

investments in residential

development in India

Sole Financial Advisor to

Piramal Fund Management

2017

PEL and Ivanhoé

~US$ 350 million

Advised MIRA on sale of two

operating road assets to

Abertis

US$ 135 million

2017

Financial Advisor

Sale of leased office portfolio

Exclusive Sell-side Advisor

2017

Hiranandani

~US$ 1 billion

Affordable Housing Platform

US$ 200 million

Exclusive Financial Advisor

Shapoorji Pallonji Group

2015

Across a number of verticals over the past 10 years

PAGE 8STRICTLY CONFIDENTIAL MACQUARIE

International Capital Markets Expertise Virgin Atlantic: First European Slots Deal

Transaction Overview

• £252m senior secured note

• Secured over take-off and landing Slots at Heathrow

• Bond instruments privately rated by Moodys’ –

investment grade

• A1 and A2 senior tranches offering different returns and

amortisation profile to accommodate investor demand

• 15 year maturity (AWL 10 years (A1 tranche) and 12

years (A2 tranche))

• Notes placed with blue-chip long term institutional

investors at attractive rates including:

• Pension Funds

• Insurance Groups – Life and General; and

• Specialist Debt Funds

• Macquarie’s role:

• devised structure and advised Virgin Atlantic Airways;

and

• acted as sole arranger and distributor of the bonds

Virgin Atlantic on the transaction

“As a business we challenge ourselves to think differently. We are

always looking for new opportunities to strengthen our position so

that we can invest more for our customers

This is an innovative financing arrangement. It represents not only a

significant milestone for Virgin Atlantic as our maiden capital

markets transaction, but is also the first time an airline has

successfully accessed the value of its London Heathrow slot

portfolio in this way.”

Macquarie successfully helped Virgin Atlantic to unlock the value of their Slots – a European first

Virgin Atlantic’s CFO

“This was a ground-breaking deal which was both innovative and

challenging. Full credit to the Macquarie team for seeing this through

from inception to closing, we are delighted with the terms of this

offering”

STRICTLY CONFIDENTIAL

2Investing in Infrastructure Assets

PAGE 10STRICTLY CONFIDENTIAL MACQUARIE

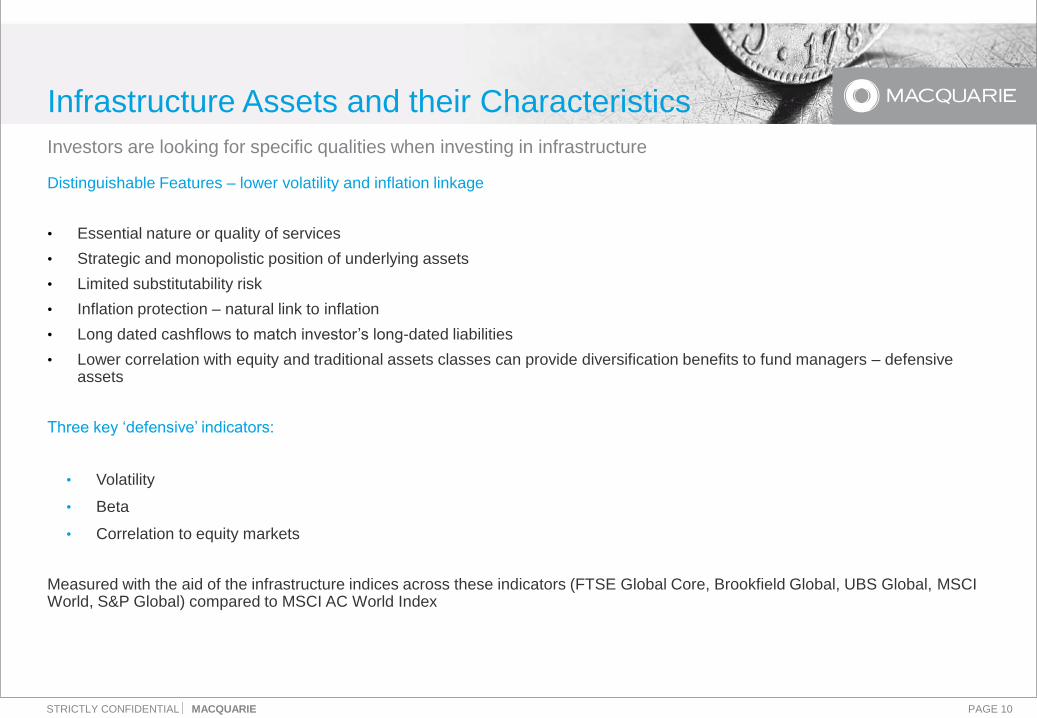

Infrastructure Assets and their Characteristics

Distinguishable Features – lower volatility and inflation linkage

• Essential nature or quality of services

• Strategic and monopolistic position of underlying assets

• Limited substitutability risk

• Inflation protection – natural link to inflation

• Long dated cashflows to match investor’s long-dated liabilities

• Lower correlation with equity and traditional assets classes can provide diversification benefits to fund managers – defensive assets

Three key ‘defensive’ indicators:

• Volatility

• Beta

• Correlation to equity markets

Measured with the aid of the infrastructure indices across these indicators (FTSE Global Core, Brookfield Global, UBS Global, MSCI World, S&P Global) compared to MSCI AC World Index

Investors are looking for specific qualities when investing in infrastructure

PAGE 11STRICTLY CONFIDENTIAL MACQUARIE

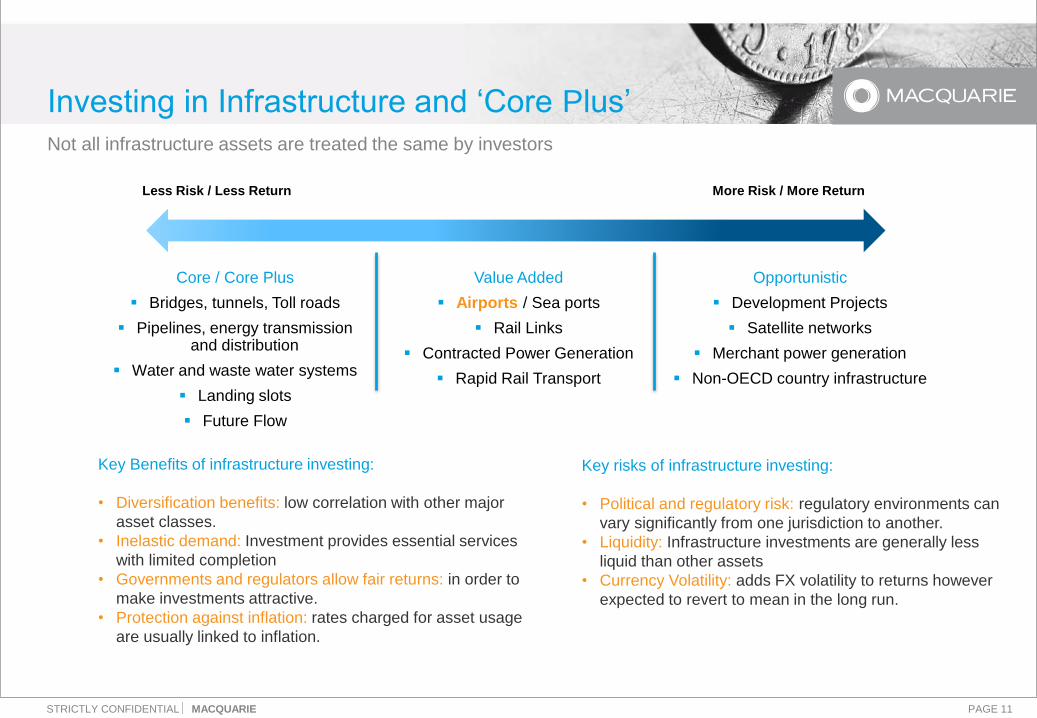

Investing in Infrastructure and ‘Core Plus’

Not all infrastructure assets are treated the same by investors

Less Risk / Less Return

Core / Core Plus

▪ Bridges, tunnels, Toll roads

▪ Pipelines, energy transmission and distribution

▪ Water and waste water systems

▪ Landing slots

▪ Future Flow

More Risk / More Return

Value Added

▪ Airports / Sea ports

▪ Rail Links

▪ Contracted Power Generation

▪ Rapid Rail Transport

Opportunistic

▪ Development Projects

▪ Satellite networks

▪ Merchant power generation

▪ Non-OECD country infrastructure

Key Benefits of infrastructure investing:

• Diversification benefits: low correlation with other major

asset classes.

• Inelastic demand: Investment provides essential services

with limited completion

• Governments and regulators allow fair returns: in order to

make investments attractive.

• Protection against inflation: rates charged for asset usage

are usually linked to inflation.

Key risks of infrastructure investing:

• Political and regulatory risk: regulatory environments can

vary significantly from one jurisdiction to another.

• Liquidity: Infrastructure investments are generally less

liquid than other assets

• Currency Volatility: adds FX volatility to returns however

expected to revert to mean in the long run.

PAGE 12STRICTLY CONFIDENTIAL MACQUARIE

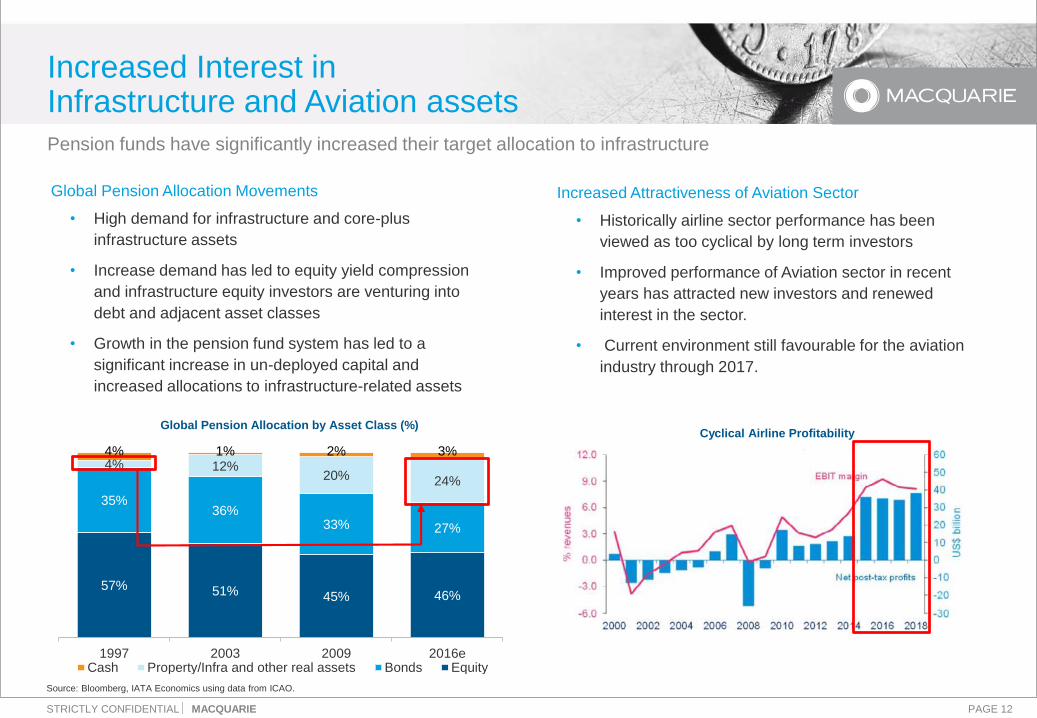

Increased Interest in Infrastructure and Aviation assets

Pension funds have significantly increased their target allocation to infrastructure

Global Pension Allocation Movements

• High demand for infrastructure and core-plus

infrastructure assets

• Increase demand has led to equity yield compression

and infrastructure equity investors are venturing into

debt and adjacent asset classes

• Growth in the pension fund system has led to a

significant increase in un-deployed capital and

increased allocations to infrastructure-related assets

Cyclical Airline Profitability

Increased Attractiveness of Aviation Sector

• Historically airline sector performance has been

viewed as too cyclical by long term investors

• Improved performance of Aviation sector in recent

years has attracted new investors and renewed

interest in the sector.

• Current environment still favourable for the aviation

industry through 2017.

Source: Bloomberg, IATA Economics using data from ICAO.

57% 51% 45% 46%

35%36%

33% 27%

4% 12%20% 24%

4% 1% 2% 3%

1997 2003 2009 2016eCash Property/Infra and other real assets Bonds Equity

Global Pension Allocation by Asset Class (%)

PAGE 13STRICTLY CONFIDENTIAL MACQUARIE

-

100

200

300

400

500

600

Dec-0

3

Dec-0

5

Dec-0

7

Dec-0

9

Dec-1

1

Dec-1

3

Dec-1

5

Fe

b-1

7

Global ‘dry powder’ equityacross alternative asset classes

Growth in the pension fund system has led to a significant increase in equity capital over the last 15 years

Private equity ($USbn) Real estate ($USbn)Infrastructure ($USbn)

-

50

100

150

200

250

300

Dec-0

3

Dec-0

5

Dec-0

7

Dec-0

9

Dec-1

1

Dec-1

3

Dec-1

5

Fe

b-1

7

Rest of World Asia Europe North America

161 billion as at Jan-18 532 billion as at Feb-17248 billion as at Feb-17

Source: Prequin, H2 2017

0

20

40

60

80

100

120

140

160

180

Dec-0

3

Dec-0

5

Dec-0

7

Dec-0

9

Dec-1

1

Dec-1

3

Dec-1

5

Dec-1

7

PAGE 14STRICTLY CONFIDENTIAL MACQUARIE

Demand is set to continue in the future

Source: Prequin, H2 2017, Prequin Investor Interviews, Dec 15 – June 17. Prequin Real Estate Online

Investment demand for 2017 and beyond

Expectations have been generally met or exceeded, meaning further demand in the future

Investor views of infrastructure performance

relative to expectations, 2015 - 2017

• Median IRRs have historically been around 10% since 2004

• 96% Investors deem performance to have met or exceeded expectationsStrategies targeted by Real Estate Investors

STRICTLY CONFIDENTIAL

3Alternative Funding and Investing Strategies

PAGE 16STRICTLY CONFIDENTIAL MACQUARIE

Alternative Ways to Invest in Infrastructure

This has led to

• Increased demand for traditional infrastructure and ‘core plus’ infrastructure

• Investors moving into infrastructure debt and alternative asset strategies to gain analogous exposure to traditional

infrastructure assets such as airports

Three areas we are seeing new products and increasing demand from our infrastructure clients and investor

base:

Structured Capital Markets Products

• Landing Slot Rights as financing collateral to raise capital for airlines – private and public placements

• Future flow receivables securitisations used to fund future infrastructure projects – private and public

placements

Leasing Solutions

• Ground Support Equipment (“GSE”) leasing, servicing and pool solutions

Equity yields have compressed in infrastructure developed markets since 2012

PAGE 17STRICTLY CONFIDENTIAL MACQUARIE

Conventional Structural Enhancements can achieve a significant up-notch in the Bond Rating from the credit rating

Source: S&P, Bloomberg, Moodys.

Potential significant notch improvement from corporate rating

Structured Products: pricing benefits

S&P Rating Airport / Airline / Sovereign

Investment grade

AA

A+

A

A-

BBB+ easyJet PLC, Ryanair Holdings PLC

BBB Southwest Airlines Co.

BBB-Sovereign of India*, Deutsche Lufthansa AG, Qantas

Airways Ltd., Alaska Airlines Inc., WestJet Airlines Ltd.

Sub-investment grade

BB+ GMR Hyderabad Int Airport, Delta Air Lines Inc.

BB Delhi Int Airport Ltd, British Airways PLC

BB-

American Airlines Group Inc., JetBlue Airways Corp.,

United Airlines Inc., United Continental Holdings Inc.,

American Airlines Inc., Latam Airlines Group S.A., Spirit

Airlines Inc., Turk Hava Yollari A.O., US Airways Inc.

B+ Virgin Australia Holdings Ltd., Air Canada

B SAS AB, Avianca Holdings S.A.

B-

CCC Gol Linhas Aereas Inteligentes S.A.

This should translate to a material cost saving for the counterparty

Rating AA A BBB BB B CCC

Avg. Spread (bps) 146 180 257 443 661 1103

Delta from BB (bps) -297 -263 -186 - +218 +660

0

500

1000

1500

2000

2500

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

S&P Global Composite Credit Spreads By Rating Category (bps)

AA A BBB BB B

*Moody’s have recently upgraded India’s government bond rating to Baa2 (BBB) however

S&P have confirmed BBB-

PAGE 18STRICTLY CONFIDENTIAL MACQUARIE

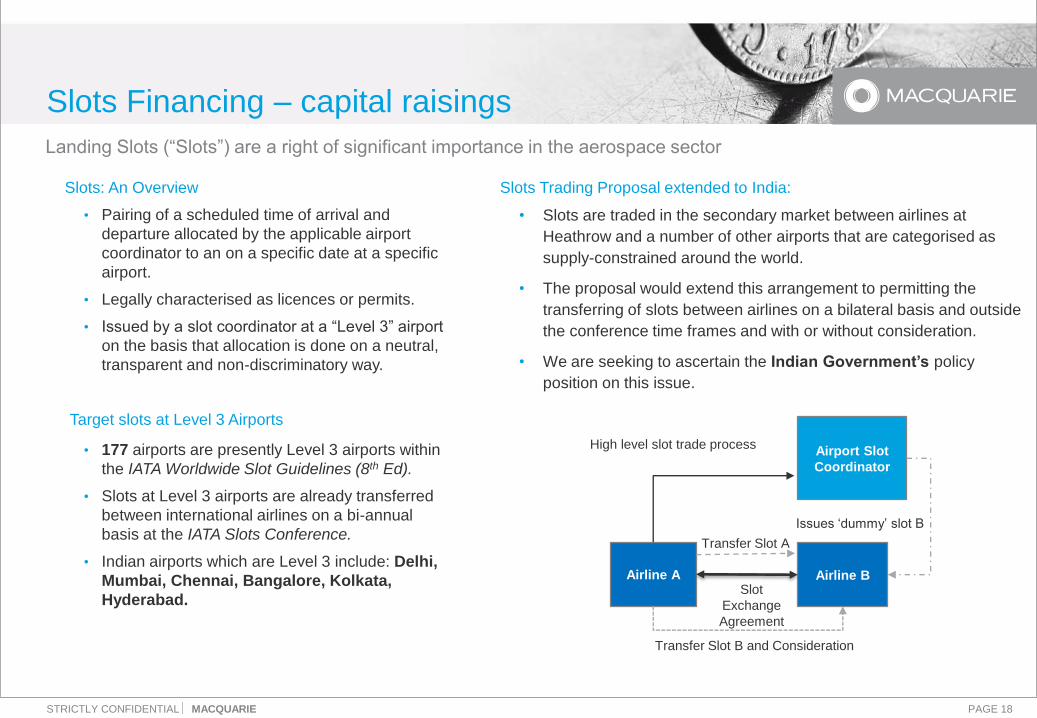

Slots Trading Proposal extended to India:

• Slots are traded in the secondary market between airlines at

Heathrow and a number of other airports that are categorised as

supply-constrained around the world.

• The proposal would extend this arrangement to permitting the

transferring of slots between airlines on a bilateral basis and outside

the conference time frames and with or without consideration.

• We are seeking to ascertain the Indian Government’s policy

position on this issue.

Slots Financing – capital raisings

Landing Slots (“Slots”) are a right of significant importance in the aerospace sector

Slots: An Overview

• Pairing of a scheduled time of arrival and

departure allocated by the applicable airport

coordinator to an on a specific date at a specific

airport.

• Legally characterised as licences or permits.

• Issued by a slot coordinator at a “Level 3” airport

on the basis that allocation is done on a neutral,

transparent and non-discriminatory way.

Target slots at Level 3 Airports

• 177 airports are presently Level 3 airports within

the IATA Worldwide Slot Guidelines (8th Ed).

• Slots at Level 3 airports are already transferred

between international airlines on a bi-annual

basis at the IATA Slots Conference.

• Indian airports which are Level 3 include: Delhi,

Mumbai, Chennai, Bangalore, Kolkata,

Hyderabad.

Airline A

Transfer Slot A

Airline B

Airport Slot

Coordinator

High level slot trade process

Transfer Slot B and Consideration

Slot

Exchange

Agreement

Issues ‘dummy’ slot B

PAGE 19STRICTLY CONFIDENTIAL MACQUARIE

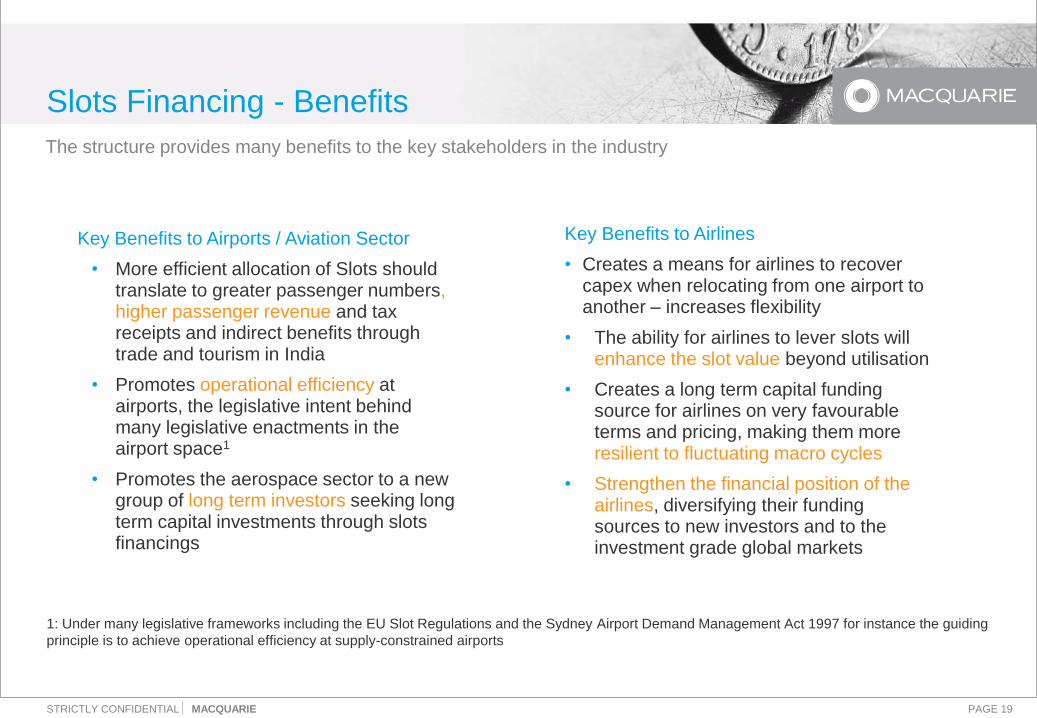

Key Benefits to Airports / Aviation Sector

• More efficient allocation of Slots should translate to greater passenger numbers, higher passenger revenue and tax receipts and indirect benefits through trade and tourism in India

• Promotes operational efficiency at airports, the legislative intent behind many legislative enactments in the airport space1

• Promotes the aerospace sector to a new group of long term investors seeking long term capital investments through slots financings

Slots Financing - Benefits

The structure provides many benefits to the key stakeholders in the industry

1: Under many legislative frameworks including the EU Slot Regulations and the Sydney Airport Demand Management Act 1997 for instance the guiding

principle is to achieve operational efficiency at supply-constrained airports

Key Benefits to Airlines

• Creates a means for airlines to recover capex when relocating from one airport to another – increases flexibility

• The ability for airlines to lever slots will enhance the slot value beyond utilisation

• Creates a long term capital funding source for airlines on very favourable terms and pricing, making them more resilient to fluctuating macro cycles

• Strengthen the financial position of the airlines, diversifying their funding sources to new investors and to the investment grade global markets

PAGE 20STRICTLY CONFIDENTIAL MACQUARIE

Future Flow Capital Raisings: Benefits

No. Feature Details Potential Benefit/s

1Pricing

• Structural enhancements could produce

significant saving over the term when

compared with existing capital raisings

• Saving in cost of debt over the bond term

• Long term interest rates are at historically low levels

2 Tenor of bonds

• Potential tenor of 10+ years for this

asset given the predictability and stability

of the future flows.

• Longer amortisation profiles

• potentially match projects migrating to revenue generating

3 Favourable terms

• We expect our investor base will permit

the flexible use of funds for general

corporate purposes

• Financial covenants will be focused on

debt service and leverage ratios

• Flexible use of funds to utilise on existing projects and

minimise negative carry on borrowed funds

• DSCR tolerance range: 4-8x

• Leverage Ratio tolerance range: 2-4x

4Amortisation

Profile

• Investor base less focused on

amortisation in short term seeking longer

maturity debt

• Repayment profile could be structured to suit the

counterparty with limited restraints

5Currency

Optionality

• Capital can be raised in USD and INR (or

a combination)

• Capital may be raised to match currency longer-dated actual

and anticipated liabilities

• US inflationary pressure and anticipated interest rate hikes in

next 12 months are likely to generate upward pressure on

USD over short to medium term

• Financing presents good opportunity to raise USD

Using future receivables to fund growth is a well-established funding technique for growth

PAGE 21STRICTLY CONFIDENTIAL MACQUARIE

Emerging Markets: Future Flow Deals

Transaction Description Ratings Information (Moody’s)

Garanti Diversified Payment

Rights

• US$150m issued in 2003 by Garanti, a Turkish Bank, 5 year tenor

• Diversified payment receivables, generated through SWIFT

payments made into Turkey, payments receipted into a trust, P&I

paid and remainder swept to Turkey

• Covenant, DSCR of better than 6:1x

• Series A rated Aaa (Series B notes

Baa3)

• Garanti rated B3 (foreign currency)/Baa2

(local currency deposit)

• Turkey country rating of B3

KAL future ticket receivables

• JPY 40b issued in 2007 (and multiple times since) by Korean Air

(KAL)

• Securitised over future airline ticket receivables• Rated the notes A3

Eco Frontier Revenue Trust

• JPY 10b issued in 2011 by Ibaraki Prefecture Eco Frontier Revenue

Trust for 35 years

• Receivables generated by the Ibaraki Prefecture Environmental

Conservation Agency, generated through waste disposal

businesses in Japan

• SPV had a DSCR 2x at inception due to very reliable cash flows

• The waste disposal service is a mandatory service, covenants

include servicer replacement provisions (payment is independent of

servicer), cash reserves providing for 6 months of no income

• Notes rated A1

• Moody’s noted A2 or A3 would be more

applicable if the DSCR was between

1.5x and 1.8x

Brazilian Electric Power

Receivables Future Flow

• Various transactions issued by the Brazilian Government, long

dated

• Government charges companies royalty to generate and sell

electricity

• Can be longer dated than other funding sources

• Generally covenants at DSCR of 2.5x

• 2.0x-2.5x+ DSCR

• BrAAA (equal to the Brazilian sovereign

rating, as this is a domestic transaction)

PAGE 22STRICTLY CONFIDENTIAL MACQUARIE

GSE Fleet Procurement, Rental & Fleet Management

Macquarie finds the best solution that helps users focus on managing their core operations at competitive rates.

PRODUCT TYPES

We support a number of structures across the majority of GSE types

including:

• Multi asset, single or multi location rental and asset services.

• Dry Operating Rental

• GSE Pool Service incorporating additional costs and issues.

• Over a variety of tenors suited to the client.

WORKING ACROSS WHOLE GSE ECOSYSTEM:

REGULATOR

Economic and

social benefit

HANDLER

Market share and

Profitability

FLEET OWNER

Manageability

and ROI

KEY SERVICES

Profitability and

risk

SUPPLIERS

Sales volume and

profitability

AIRPORT

Capacity, cost

and efficiency

Ensuring key stakeholders are satisfied

PAGE 23STRICTLY CONFIDENTIAL MACQUARIE

This presentation is provided on a confidential basis to selected recipients only, and may not be reproduced in whole or in part or distributed or transmitted to

any other person, nor may any of its contents be disclosed to any other person, without Macquarie’s prior written consent. This presentation has been prepared

as a basis for further discussion. This is a sounding document only. Any offer or proposal in respect of the arrangements described in this presentation will be

subject to further subject to internal approvals and discretion and formal engagement. Furthermore, the arrangements described in this presentation, including,

without limitation, the proposed financing terms, are subject to Macquarie internal approvals and change and any subsequent offer or proposal in respect of

those arrangements, if made, may not be made on the basis of the arrangements or terms as described herein.

The name “Macquarie” in this document refers to Macquarie Group Limited ABN 94 122 169 279 and its affiliates.

This presentation is provided for general information purposes only, without taking into account any potential investors’ personal objectives, financial situation

or needs. It should not be relied upon by the recipient in considering the merits of any particular transaction. It does not constitute a prospectus or offering

memorandum and is not an offer to buy or sell, or a solicitation or recommendation to invest in or refrain from investing in, any securities or other investment

product or an invitation to be involved in or take any further part in the arrangements described in this presentation. Neither this presentation nor any other

documentation or information (or any part thereof) delivered or supplied in connection with this presentation shall be deemed to constitute an offer of or an

invitation to purchase or subscribe for any securities or any other investment product or to be involved in or take any further part in the arrangements described

in this presentation. Nothing in this presentation constitutes investment, legal, tax, accounting or other advice. The recipient should consider its own financial

situation, objectives and needs, and conduct its own independent investigation and assessment of the contents of this presentation, including obtaining

investment, legal, tax, accounting and such other advice as it considers necessary or appropriate. This presentation has been prepared on the basis of publicly

available information and information provided by the airline. Macquarie has relied upon and assumed, without independent verification, the accuracy and

completeness of all such information. It contains selected information and does not purport to be all-inclusive or to contain all of the information that may be

relevant to the arrangements described in this presentation. The recipient acknowledges that circumstances may change and that this presentation may

become outdated as a result. Macquarie is under no obligation to update or correct this presentation.

Macquarie, its related bodies corporate and other affiliates, and their respective directors, employees, consultants and agents (“Macquarie Group”) make no

representation or warranty as to the accuracy, completeness, timeliness or reliability of the contents of this presentation. To the maximum extent permitted by

law, no member of the Macquarie Group accepts any liability (including, without limitation, any liability arising from fault or negligence on the part of any of

them) for any loss whatsoever arising from the use of this presentation or its contents or otherwise arising in connection with it.

This presentation may contain forward-looking statements, forecasts, estimates and projections (“Forward Statements”). All statements other than statements

of historical facts included in this presentation, including, without limitation, those regarding the airline’s financial position, business strategy, plans and

objectives, are Forward Statements. Such Forward Statements involve known and unknown risks, uncertainties and other factors which may cause actual

future results and operations to vary materially from the Forward Statements. Such Forward Statements are based on numerous assumptions regarding the

airline’s present and future business strategies and the environment in which the airline will operate in the future. Further, certain Forward Statements are

based upon assumptions of future events which may not prove to be accurate.

Important Notice and Disclaimer