institutions and the internationalization of us venture ... · institutions and the...

TRANSCRIPT

Institutions and the internationalization of US

venture capital firms

Isin Guler1 andMauro F Guillen2

1Kenan-Flager Business School, University ofNorth Carolina, Chapel Hill, USA; 2The Wharton

School of the University of Pennsylvania,

Philadelphia, USA

Correspondence:I Guler, Kenan-Flager Business School,University of North Carolina, McCollBuilding CB3490, Chapel Hill, NC 27599,USA.Tel: þ1 919 962 0691;Fax: þ1 919 962 4266;E-mail: [email protected]

Received: 30 April 2008Revised: 12 February 2009Accepted: 21 February 2009Online publication date: 9 July 2009

AbstractIn recent years, venture capital firms have increasingly turned to foreigncountries in search of investment opportunities. The cross-border expansion of

venture capital firms presents an interesting case of internationalization,

because they are at variance with both conventional portfolio and directinvestment models. Given the specific nature of venture capital investing, a

new theoretical perspective is needed to understand foreign venture capital

investments. This paper contributes to international business research byexamining the features of the institutional environment that influence venture

capital firms’ foreign market entry decisions, and how their effect changes as

firms acquire experience. We report results on 216 American venture capital

firms potentially investing in 95 countries during the 1990–2002 period. Wefind that venture capital firms invest in host countries characterized by

technological, legal, financial, and political institutions that create innovative

opportunities, protect investors’ rights, facilitate exit, and guarantee regulatorystability, respectively. We also find that as firms gain more international

experience, they are more likely to overcome constraints related to these

institutions.Journal of International Business Studies (2010) 41, 185–205.

doi:10.1057/jibs.2009.35

Keywords: institutional context; venture capital; longitudinal (or time-series) researchdesign

INTRODUCTIONThe theory of foreign direct investment seeks to explain variousaspects associated with the control exercised by a firm over theproduction of a good or service in at least one location other thanits home country. As originally proposed by Hymer (1976) in thelate 1950s, the difference between direct and portfolio investmentlies precisely in the intention of the firm to exercise managerialcontrol over the foreign operation. In recent years, venture capitalfirms have increasingly turned to foreign countries in search ofinvestment opportunities. The cross-border expansion of venturecapital firms presents an interesting case of internationalization,because their foreign investments cannot be classified in astraightforward manner. In some respects, venture capital foreigninvestments appear to share some features of those characterized inthe literature as portfolio investments. First, the venture capitalfirm is a financial intermediary operating between the ultimateinvestor and the entrepreneur. Second, the venture capital firm’sultimate goal is not to produce a good or a service for profit, but to

Journal of International Business Studies (2010) 41, 185–205& 2010 Academy of International Business All rights reserved 0047-2506

www.jibs.net

obtain a capital gain with which to reward theultimate investor. Third, although the venturecapital firm may dispatch one or more directors tothe board, the managerial hierarchy of the foreignventure does not functionally report to the venturecapital firm. Moreover, venture capital firms typi-cally invest as part of a syndicate, and rarely aremajority investors.

Venture capital firms, however, behave as muchmore than pure financial intermediaries, given thatthey also provide the venture with organizational,managerial, industry, and even technologicalexpertise. Moreover, they exert much more fre-quent and extensive control over the investedcompany than the typical portfolio investor (Gompers& Lerner, 2000). Venture capital firms make capitalinvestments in ‘‘opportunities’’ that typically entailhigh risk, and a potential for high returns. Theseopportunities are not single resources or means ofproduction, but individual companies that consti-tute a unique ‘‘bundle of resources’’ (Penrose, 1959).Given the specific nature of venture capital invest-ing, one that is at variance with both conventionalportfolio and direct investment models, a newtheoretical perspective is needed to understandforeign venture capital investments.

Though still small, cross-border venture capitalactivity has risen quickly since the early 1990s.

VCs who once bragged about never driving more than half

an hour to visit a portfolio company are jetting to Australia

for optical engineers, Israel for security whizzes, India and

Kazakhstan for brute software coding, South Korea for

online gaming, and Japan for graphics chips. For growth

across the board, China is the place to go.1

According to one venture capitalist, ‘‘VCs inSilicon Valley used to pride themselves on beinglocal y That was well and good when the US wasthe mecca for technology.’’2 In many countriesaround the world, local practices and regulationsare being overhauled so as to make it easier forforeign venture capital firms to operate. Forinstance, a Chinese legislator and economic expertargued in an interview that ‘‘venture capital isnot conflicted with Socialism.’’3 Understanding thecross-border activities of venture capital firms is ofincreasing relevance as the world economy shiftstoward knowledge-intensive activities. The venturecapital industry has played an important role inspurring innovation and entrepreneurship in theUS. In recent years, US venture capital firms startedto look abroad for investment opportunities inother countries. This trend is important not only in

providing new opportunities for venture capitalfirms, but also in contributing to the developmentof local economies through entrepreneurship andinnovation.

In this paper we analyze the distinctive aspects offoreign venture capital investing by examining thereasons why venture capital firms decide to investin some foreign locations but not in others. Weadopt an institutional perspective focused on thecharacteristics of countries that make them moreattractive for US venture capital investors. Theconventional wisdom is that venture capital is anactivity difficult or nearly impossible to organizeeffectively and successfully across borders. Partici-pants in the industry emphasize the local nature ofdeal-making (Freeman, 2005). Research has docu-mented that venture capitalists tend to fundventures located relatively close to their domicileso as to facilitate monitoring and control (Sorenson& Stuart, 2001). Therefore it becomes relevant tostudy what institutions might help these organiza-tions overcome the difficulties of doing business inforeign environments.

We also examine changes in the choice of foreignmarket as the venture capital firm gains interna-tional experience. Research has demonstrated thatfirms adjust their foreign direct investment deci-sions as they accumulate knowledge about foreignmarkets (e.g., Barkema, Bell, & Pennings, 1996;Chang, 1995; Delios & Henisz, 2003; Guillen,2002). Firms are heterogeneous in their perceptionof institutional constraints and opportunities inforeign markets, and in their ability to cope withthem. We therefore examine whether and howventure capital firms’ international experiencemoderates the impact of country institutions onthe choice of foreign markets to enter.

By examining the foreign location choices ofventure capital firms, we strive to contribute to theinternational business literature by offering asystematic examination of the importance ofhost-country institutions on foreign market choiceof venture capital firms through a large-samplestudy. We argue that the decision of venture capitalfirms to invest in companies located in foreignmarkets is driven by institutions that foster theavailability of innovative and entrepreneurialopportunities, the ability to commercialize theseopportunities, and the extent to which the institu-tional infrastructure of each country enables theappropriation of returns. We also argue that firms’international experience moderates the effects ofinstitutions.

US venture capital internationalization Isin Guler and Mauro F Guillen

186

Journal of International Business Studies

THE VENTURE CAPITAL INDUSTRY IN THE USAND AROUND THE WORLD

The venture capital firm is a genuinely Americaninstitution. In 1946 a group of Boston academicsand financiers created American Research andDevelopment. A key innovation came about in1958, when one firm organized itself as a limitedpartnership, in which limited partners or investorsprovided funds to general partners or venturecapitalists to invest in entrepreneurial ventures.This organizational form enabled the venturecapitalist to be exempt from the prohibitions onowning more than 10% of the equity and servingon the board of directors of portfolio companies.The limited partnership became the dominant formof incorporation in the US. Nowadays the typicalventure capital firm has anywhere between twoand over 30 general partners. The amount of capitalunder management can range from 10 million toseveral billion dollars (Fenn, Liang, & Prowse,1997).

The venture capital industry has been one of themajor driving forces behind innovative activity andgrowth of high-technology industries in the USeconomy. Although venture capital outlays repre-sented only 3% of total corporate investmentbetween 1983 and 1992, they resulted in 8% ofall US industrial innovations (Kortum & Lerner,2000). As a result, venture capital has been asignificant driver of the US economy throughspurring entrepreneurial activity. As of 2005, ven-ture-capital-backed companies represented 9%of total US private sector employment and 16.6%of GDP (Venture Impact, 2007).

The success of the US venture capital industry infinancing innovation and contributing to growthhas encouraged venture capital activity in othercountries. Although private equity and venturecapital investment around the world are compara-tively smaller, many countries report large growthrates. For instance, during 2005 private equityinvestments grew by 45% in India, and 328% inChina (Global Private Equity, 2006). The earlyexperiments with venture capital in countries suchas Germany and Japan failed, in spite of govern-ment or corporate backing (Becker & Hellmann,2005; Kenney, Han, & Tanaka, 2002). Later devel-opments gave rise to venture capital activities thatdiffered in structure and operation from theirUS counterparts, always in response to uniqueinstitutional demands (Bottazzi, Da Rin, & Hell-mann, 2004). Some of the factors found to affectthe growth of venture capital activity include

appropriate structures and government policies toprotect investor returns (Becker & Hellmann, 2005;Jeng & Wells, 2000), the level of economic devel-opment, the availability of exit options (Black &Gilson, 1998; Kenney et al., 2002), and the qualityof the national system of innovation and levelsof entrepreneurship (Becker & Hellmann, 2005).4

A recent study of domestic investment decisionsin three countries shows that venture capitalists inrule-based economies base their decisions more onmarket characteristics, while those in relationship-based economies rely more on characteristics of thehuman capital (Zacharakis, McMullen, & Shepherd,2007). However, very little research has examinedthe internationalization decisions of venture capi-tal firms, or the patterns of cross-border investment(see Wright, Pruthi, & Lockett, 2005, for a review).

INSTITUTIONS AND FOREIGN MARKET ENTRYBY VENTURE CAPITAL FIRMS

Venture capital firms depend on a number ofinstitutions in order to operate, including techno-logical institutions providing for entrepreneurialopportunities, legal institutions facilitating con-tracts between the firm and the entrepreneur,financial institutions making it possible to exitthe investment, and political institutions prevent-ing any harm to or curtailment of their propertyrights. Our main goal is to examine which of theseinstitutions increase the attractiveness of countriesfor venture capital firms located in the US, and theextent to which the effects of institutions aremoderated by firms’ international experience.

In examining the effect of host-country institu-tions on venture capital investment, we defineinstitutions as ‘‘multifaceted, durable social struc-tures, made up of symbolic elements, social activ-ities, and material resources’’ that ‘‘provideguidelines and resources for acting as well asprohibitions and constraints on action’’ (Scott,2001: 49–50). Several areas of recent institutionaltheory and research are relevant to the analysis ofthe host-country institutions that venture capitalfirms find attractive. First, institutions that supportinnovation and technology are important to ven-ture capital firms because such firms tend to focustheir attention on high-tech industries. The litera-ture on national systems of innovation offers aninstitutional framework for the comparative analy-sis of the characteristics, organization and perfor-mance of countries in the area of technology.This line of research draws on institutional analysis

US venture capital internationalization Isin Guler and Mauro F Guillen

187

Journal of International Business Studies

in economics, political science, sociology and/ororganizational studies (Furman, Porter, & Stern,2002; Nelson & Rosenberg, 1993; Patel & Pavitt,1994; Porter, 1990; Whitley, 1992). Second, therapidly growing literature on cross-national pat-terns of corporate governance and finance providesa framework for understanding the complex rela-tionship between legal systems, financial markets,and capitalist development in general, and thelegal protection of investors’ rights in particular(Guillen, 2000; La Porta, Lopez-de-Silanes, Shleifer,& Vishny, 1998), another issue that is of centralconcern to venture capital firms. Third, the litera-ture on political hazards uses institutional econom-ics and positive political theory to study theconditions that make for a stable political environ-ment (Henisz, 2000a, b; Henisz & Williamson,1999). This aspect is of cardinal importanceto venture capital firms, given that they need toensure that the investment returns will not beexpropriated. Based on these theoretical perspec-tives, let us turn to examining how technological,legal, financial, and political institutions affectforeign location choice by venture capital firms.

Institutions Supporting Knowledge andTechnology: National Systems of InnovationThe literature on national systems of innovationhas conceptualized and documented that coun-tries, and regions within countries, differ in termsof the inputs allocated to the creation of knowl-edge, technology and innovation, the quality ofthe institutions that help transform those inputs,and the resulting level of performance (Almeida &Kogut, 1999; Furman et al., 2002; Kogut & Zander,1993; Nelson & Rosenberg, 1993; Patel & Pavitt,1994; Porter, 1990; Romer, 1990). Although scienceand technology have become more global in natureover the last two decades, the country continues tobe a relevant unit of analysis. Globalization hasnot erased differences in effort or outcomes acrosscountries, resulting in persistent knowledge andtechnological gaps, for two reasons. First, manyof the institutional actors involved in the effort(i.e., governments, universities, trade associations)are distinctively national or subnational in char-acter (Nelson & Rosenberg, 1993). And second,knowledge and technology move more easilywithin than across national borders, as a largebody of empirical research has established(Guillen, 1994; Kogut & Chang, 1991; Patel &Pavitt, 1994).

Differences in national levels of innovation arelikely to influence the level of entrepreneurialactivity and, as a result, the attractiveness of thecountry to foreign venture capital investors. Entre-preneurs and firms tend to agglomerate in locationswith high levels of institutional support for innova-tion. For instance, prior work documents that newventures benefit from access to resources such ashuman capital, and from knowledge spillovers bylocating close to universities and other firms(Audretsch, Lehman, & Warning, 2005; Hall, Link,& Scott, 2003; Stuart & Sorenson, 2003a). Inparticular, geographic proximity facilitates spil-lovers, as inventors in universities and firmsbecome more aware of each other’s work, anddevelop new knowledge through more frequentface-to-face interaction (Adams & Jaffe, 1996;Jaffe, Tratjenberg, & Henderson, 1993). Researchshows that smaller and younger firms, that is, thosethat tend to be funded by venture capital, stand tobenefit the most from spillovers from local sourcesof knowledge (Alcacer & Chung, 2007). As a result,we expect venture capital firms as well as entrepre-neurs to locate in regions and countries character-ized by high innovative activity (Powell, Koput,Bowie, & Smith-Doerr, 2002). While prior workhas examined the regional agglomeration ofentrepreneurs and venture capital firms (Florida &Kenney, 1988; Kenney et al., 2002; Stuart &Sorenson, 2003a), the impact of national systemsof innovation on venture capital foreign invest-ment has not been addressed in the literature.

We argue that national systems of innovationinfluence the extent of profit-making opportunitiesand entrepreneurial activity in each market. Newventures choose among markets based on theexistence of institutions that support innovationand technological development (e.g., Audretschet al., 2005; Hall et al., 2003; Stuart & Sorenson,2003a). In turn, venture capital firms scan theenvironment for attractive opportunities, that is,new innovative ideas in which to invest, and oftenfind them in areas that have to do with theapplication of new knowledge or technology(Gompers & Lerner, 2000, 2001). Countries withvibrant institutions that support research andinnovation are likely to become more attractivefor venture capital firms looking to expand inter-nationally. Hence we predict:

Hypothesis 1: The rate of entry into a foreignmarket by venture capital firms increases with thelocal level of knowledge and technology.

US venture capital internationalization Isin Guler and Mauro F Guillen

188

Journal of International Business Studies

Institutions Supporting Venture CapitalTransactionsVenture capital involves a considerable ‘‘leap offaith,’’ given the nature of young entrepreneurialventures and the uncertainties about their success(Gompers & Lerner, 2001: 87). Hence the venturecapital firm uses certain monitoring and enforce-ment mechanisms to ensure that those runningthe invested company do so in a way consistentwith the interests of the investors, who tendto have a preference for an exit within a numberof years through an initial public offering (IPO).This chain of events is possible only in the presenceof appropriate legal, financial and political institu-tions. The most important legal institution iscorporate law, which specifies the rights andobligations of owners and managers. The existenceof large and active equity markets is required inorder to materialize the venture capitalist’s pre-ferred exit option, namely, the IPO. Finally, poli-tical institutions need to provide a dose of stabilityand predictability so as to placate investors’ fearsabout future changes in rules and regulations. Letus analyze each of these in turn.

Legal institutions: corporate law. Laws fulfill tworoles that facilitate economic activity and financialtransactions. First, they define legal personsthat transcend individuals, create negotiableinstruments, and establish how negotiations andtransactions can take place (Trevino, 1996). Second,the legal order defines and protects the legitimateinterests of the various parties. Weber (1978:328–329) observed that although ‘‘in most busi-ness transactions it never occurs to anyone even tothink of taking legal action, y economic exchangeis quite overwhelmingly guaranteed by the threatof legal coercion.’’ Firms and investors prefer tooperate in a context in which legal institutionsenable and protect them (Trevino, 1996).

Legal institutions are relevant to the growth ofventure capital activity. Recent research on thecontractual relationship between the entrepreneurand the venture capitalist highlights that the latterseeks to diversify its holdings by investing smallamounts in each venture. This allows the venturecapitalist to delegate control to the entrepreneurduring the normal course of operations, but toreassert its rights as owner if things take a turn forthe worse (Lerner & Schoar, 2005). The contractualarrangements typically used in venture capital dealswere first developed in the US (Gompers & Lerner,2000, 2001; Sahlman, 1990). The US, however,

provides a legal environment for venture capitalactivity that is not present in every country aroundthe world. Thus the transfer of the contractualarrangements to other countries may prove proble-matic (Bottazzi, Da Rin, & Hellmann, 2008; Kaplan,Martel, & Stromberg, 2007; Lerner & Schoar, 2005).

Comparative legal scholarship (Glendon, Gordon,& Osakwe, 1994; Reynolds & Flores, 1989) andmore recent economic analyses (La Porta et al.,1998; La Porta, Lopez-de-Silanes, & Shleifer, 1999)have documented that owners’ interests receivedifferent degrees of legal definition and protectiondepending on the legal system. This line of researchargues that owners’ or investors’ rights are definedand protected in varying ways and to differentdegrees depending on the legal tradition thatprovides the foundation for corporate law. Thetwo broad legal traditions that influence corporatelaw and investor protection are the English com-mon law tradition and the civil law tradition (LaPorta et al., 1998). The English common lawtradition, adopted by countries including the US,is shaped by the decisions of judges ruling onspecific issues more than other legal traditions. AsWeber (1978: 890) put it, ‘‘English legal thought isessentially an empirical art.’’ By contrast, the civillaw tradition encompasses French, German, andScandinavian families, and ‘‘uses statutes andcomprehensive codes as a primary means of order-ing legal material’’ (La Porta et al., 1998: 118).

English, French, and German corporate lawsdiffused widely throughout the world followingpatterns of imperial, military, economic, or culturalinfluence. The former British colonies – includingthe US, Canada, Australia, Ireland, Singapore, andmany others in Africa and South Asia – adoptedEnglish common law. French law spread not only tothe francophone colonies in the Middle East,Africa, Indo-China, Oceania, and the Caribbeanbut also to the Netherlands, Portugal, Spain, Italy,and their respective colonies. The German legaltradition shaped corporate laws in Austria, Switzer-land, Greece, Hungary, the Balkans, Japan, Korea,Taiwan, and China, among other countries. Lastly,the former socialist countries constitute a separatecategory because their legal systems, though inmany cases influenced by either French or Germanlaw, have been in flux since 1989 and have largelyfailed to provide a sound basis for effectivecorporate governance (Schneper & Guillen, 2004;Spicer, McDermott, & Kogut, 2000).

Comparative analyses of corporate legal tradi-tions reveal that the English common law tradition

US venture capital internationalization Isin Guler and Mauro F Guillen

189

Journal of International Business Studies

tends to provide stronger protection of investors’rights than the civil law tradition against potentialagency problems with management (La Porta et al.,1998). La Porta and his colleagues (1998) comparedcountries along the legal rules pertaining to therights of investors, and found that countries thathave adopted the English common law traditionprovided significantly better voting rights forshareholders as well as more legal rules thatprotected minority shareholders. The underlyingreasons for different levels of investor protectionbetween the two legal traditions were argued to bein the historical origins of each tradition. Specifi-cally, French civil law was developed after theFrench Revolution and emphasized state powerover property rights, whereas common law devel-oped as a response to the needs of aristocratsand merchants (La Porta, Lopez-de-Silanes, &Shleifer, 2008). Research has also demonstratedthat enforcement of owner protections and dis-pute-resolution time differs greatly across coun-tries, and that there were significant differencesin enforcement and dispute-resolution timebetween English common-law countries andothers (Djankov, La Porta, Lopez-de-Silanes, &Shleifer, 2003). These differences were attributedto the flexibility of decision-making undercommon law, as courts rely on broader standardsrather than specific rules (La Porta et al., 1998).

Based on this evidence and analysis, we arguethat venture capitalists prefer to operate in coun-tries with a legal system that protects the rights ofthe investor. In the case of venture capital firms, thereasons for this preference are twofold. First, incountries with poor investor protection againstagency risk, investors tend to protect themselvesby increasing their ownership concentration, andexerting more control over management (Jensen &Meckling, 1976; La Porta et al., 1998; Shleifer &Vishny, 1986). The available cross-national microevidence on venture capital contracts indicates thatprivate equity investors in general, and venturecapitalists in particular, respond to legal regimesoffering poor protection by relying to a muchgreater extent on common stock and debt asopposed to convertible preferred stock (Bottazziet al., 2008; Lerner & Schoar, 2005), by increasingthe size of their stakes (Lerner & Schoar, 2005), andby maximizing their presence on the venture’sboard of directors (Lerner & Schoar, 2005). Takentogether, this set of results parallels the finding thatlegal tradition affects patterns of corporate owner-ship in general (La Porta et al., 1999). In essence,

when investing in common-law countries, inves-tors are generally more comfortable with lowerlevels of control, given that they can more easilyachieve minority shareholder protection throughcontractual provisions such as convertible preferredequity, anti-dilution clauses, automatic conversion,and supermajority rules (Lerner & Schoar, 2005). Itshould be noted, however, that some empiricalstudies (e.g., Kaplan et al., 2007) found legal effectsto disappear when venture capital firm-specificcharacteristics are taken into account. However,these studies do not examine whether venturecapitalists systematically avoid funding otherwiseattractive ventures just because they are located in acountry with poor investor protection, examininginstead the actual investments that have alreadytaken place under each legal system. We argue thatventure capital firms are likely to systematicallyprefer countries with an English common lawtradition, because the need to increase equity stakesin countries with poor protection of investor rightsconstrains the ability of the venture capital firm todistribute capital among a larger number of ven-tures, and to diversify portfolio risk (Bottazzi et al.,2008; Lerner & Schoar, 2005).

The second reason for attractiveness of countrieswith better ownership protection has to do withentrepreneurs seeking capital. Entrepreneurs’appetite for venture capital funding may also belower when investors’ rights are not well protected,because of the additional equity stake demandedby the venture capitalist. Entrepreneurs withthe best entrepreneurial opportunities may preferto fund their ventures through alternative means,such as debt financing. As a result, venturecapitalists’ access to high-quality investmentopportunities may be more limited in countriesoffering poor investor protection. Therefore weformulate:

Hypothesis 2: The rate of entry into a foreignmarket by venture capital firms increases to theextent that the local legal system protectsinvestors’ rights.

Financial institutions: equity markets. Financialmarkets are part of the institutional infrastructureenabling organizational founding and growth (e.g.,Stuart & Sorenson, 2003b). The stock market iscertainly important for venture capital firms.Venture capitalists do not indefinitely hold on tothe equity in the entrepreneurial venture but ratherseek to realize capital gains (and distribute them,

US venture capital internationalization Isin Guler and Mauro F Guillen

190

Journal of International Business Studies

net of management fees, to the limited partners),typically through IPOs, which historically representthe majority of venture returns (Freeman, 2005;Gompers & Lerner, 2000). Hence the size anddynamism of the equity market in the country inwhich the venture is located promise betterprospects for a successful exit, thus increasingthe attractiveness of investments (Black & Gilson,1998; Leachman, Kumar, & Orleck, 2002).5 Asventure capitalists exit investments successfully,they can help investors recycle capital towardsnew opportunities and attract new funds (Black &Gilson, 1998). Thus a thriving local equity markethelps attract, reallocate, and reward investors’capital.

Countries differ massively in terms of the size oftheir equity market. One useful and widelyaccepted indicator of equity market size is totalstock market capitalization as a percentage of GDP(e.g., Kunt & Levine, 2004; La Porta et al., 2008;Rajan & Zingales, 2003). As of 2007, this measureranged from as low as 15 in Poland, 26 in India,27 in Brazil, 35 in Germany, 37 in China, 44 inIsrael or 46 in South Korea, to 68 in France, 106in the US and 119 in the United Kingdom, to namebut a few examples (World Bank, 2008). Giventhe importance of the size of the local stockmarket for the attraction of capital to venturecapital firms and for the realization of capital gains,we formulate:

Hypothesis 3: The rate of entry into a foreignmarket by venture capital firms increases with thesize of the local stock exchange.

Political institutions: policy stability. Political insti-tutions are a key determinant of the attractivenessof a location from the vantage point of an outsider.Firms benefit from the regular and predictableimplementation of public policy (Guthrie, 1997;Trevino, 1996). The venture capital firm – likeother types of firm – would generally prefer toinvest in countries with low political hazards.The reason is that the existence of investmentopportunities related to knowledge and techno-logy, the presence of appropriate legal institutionsprotecting investors’ rights, and the availabilityof financial channels to realize capital gains donot preclude the possibility that policymakersmight be tempted to change laws, rules orregulations concerning those three aspects inorder to appropriate investors’ returns in full or inpart. As institutional theorists argue, laws, rules and

regulations are seldom completely objective orunambiguous (Scott, 2001: 169–170). The extentto which laws, rules and regulations can potentiallybe changed or reinterpreted creates uncertainty forthe regulated.

Henisz (2000a, b) proposes to conceptualize poli-tical hazards as a structural attribute of countriesthat may change over time. Countries differ interms of the number of ‘‘political constraints.’’ Asthat number grows, so does ‘‘a government’s abilityto credibly commit not to interfere with privateproperty rights,’’ an argument first advanced asrelevant to the study of capital investment byNorth and Thomas (1973) (see also North, 1990).The constraints increase with the number ofindependent branches of government with vetopower (executive, higher legislature, lower legisla-ture, judiciary, local administration), and thedegree to which veto points are controlled bydifferent parties (i.e., when the various branchesof government are not aligned). Firms, includingventure capital firms, should anticipate littlechange in relevant regulations or property rightsprotections, or in their interpretation, to the extentthat policymaking is subject to institutional con-straints, thus providing for a more stable politicalenvironment for investment. Empirical evidenceconfirms that firms prefer to do business incountries in which rules and regulations concern-ing property rights are not likely to change as aresult of unilateral actions on the part of thegovernment. For instance, research has found thatpolicy stability exerts a significant influence onlong-term capital investments (e.g., Henisz, 2002),investor participation in infrastructure projects(Henisz, 2002; Henisz & Zelner, 2001), plantlocation decisions (Henisz & Delios, 2001), andthe sequencing and mode of cross-border invest-ments (e.g., Guillen, 2003). Thus we formulate:

Hypothesis 4: The rate of entry into a foreignmarket by venture capital firms increases with thelocal level of policy stability.

Institutions and firm experience. In the precedingarguments we have assumed that firms areuniformly affected by the presence of certaininstitutions in the host market. However, firmsare heterogeneous in their strategic approach toforeign market entry because of differences in theirprevious expansion experiences (e.g., Barkemaet al., 1996; Chang, 1995; Delios & Henisz, 2003;Guillen, 2002). In general, prior experience leads to

US venture capital internationalization Isin Guler and Mauro F Guillen

191

Journal of International Business Studies

learning in two ways. First, experience allows firmsto perfect their capabilities through repetition.Second, experiential learning leads firms to adjusttheir strategies as they obtain new information andupdate their assessments and calculations (Zollo &Winter, 2002). Companies acquire knowledge fromexperience, record it in their memory, and updatetheir strategies (Cyert & March, 1963; Levitt &March, 1988; March & Olsen, 1984). Thus pastexperience can change the firm’s subsequentstrategy as well as its attitudes towards risk-taking.

As firms accumulate international experience,they develop a capability for foreign marketentry and for surmounting whatever obstaclesand constraints exist in the different host countries.In other words, experience may enable firms toovercome the liability of foreignness if it leads toan upgrading of capabilities. The learning of acapability for market entry takes place in a varietyof ways, including the development of standardoperating procedures for entry that can be used ina wide variety of markets (Delios & Henisz, 2003;Guillen, 2002), or the more efficient use of thescarce managerial skills that are required to manageinternational operations (Kindleberger, 1969). Forinstance, by the 1980s the largest American multi-national enterprises had developed internal depart-ments charged with providing top managementwith ongoing analysis, assessment, and strategyformulation in the area of country risk (Kobrin,1987). Our argument is that firms will be deterredfrom entering a foreign market with an idiosyn-cratic mix of institutions unless they develop acapability to assess the institutional peculiaritiesand arrange their operations in a way thatsurmounts them.

Prior work on the venture capital industry alsodocuments the significance of firm experience forinvestment practices. For instance, Sorenson andStuart (2001) argue that prior investment experi-ence may increase the geographic reach of venturecapital firms’ subsequent investments, as experi-ence reduces the costs of monitoring. Lerner (1994)finds that venture capital firms’ investment experi-ence influences their syndication practices. Thesestudies, however, typically focus on venture capitalfirms’ domestic investment experience, whichimproves firms’ capabilities to evaluate, manageand monitor investments in the home country(e.g., Black & Gilson, 1998; Lerner, 1994; Sorenson& Stuart, 2001). In contrast, we argue that thedecision to invest in new institutional environ-ments is affected by the extent of venture capital

firms’ international investment experience. Inter-national investment experience provides venturecapital firms with skills to evaluate and monitorinvestment opportunities, write contracts, and leadinvestments toward successful liquidity eventsunder different institutional constraints. In short,we expect prior international experience to helpfirms negotiate the idiosyncratic institutionalconditions surrounding investments in foreignmarkets.

Hypothesis 5: The effects of the local level ofknowledge and technology, investor legal protec-tions, stock market size, and policy stability onthe rate of foreign market entry will weaken asthe venture capital firm’s international experi-ence increases.

RESEARCH SETTING, DATA, AND METHODSWe test the effects of institutions on the inter-nationalization of US venture capital firms withsystematic data on their foreign investment activ-ities between 1990 and 2002. The US venturecapital industry grew significantly during thisperiod, in terms of both capital available forinvestment and the number and amount of actualinvestments. Activity in the US and abroad peakedin the year 2000, which lies within our period ofobservation. We compiled the venture capitalinvestment data from the VentureXpert databaseprovided by Venture Economics,6 which collectsinformation through an annual survey of over1000 private equity partnerships in the US. Thisdatabase has been used extensively in venturecapital research (Barry, Muscarella, Peavy, &Vetsuypens, 1990; Gompers & Lerner, 2000; Meg-ginson & Weiss, 1991; Sahlman, 1990; Shane &Stuart, 2001). Although it tends to oversampleinvestments in Californian companies, most ofthe concerns about VentureXpert’s quality have todo with issues surrounding capital disbursedand valuations (Kaplan et al., 2007), which arenot the focus of this paper.

Given that our analysis focuses on the foreigninvestments of venture capital firms, we observedthe entire population of 1010 US-domiciled firmsbetween 1990 and 2002. Each of these firms had apresence in the venture capital industry, althoughsome of them also engaged in other forms of later-stage private equity.7 In order to capture causalrelationships between the dependent variable andthe independent variables, we used a one-year lag.We therefore empirically examined investments

US venture capital internationalization Isin Guler and Mauro F Guillen

192

Journal of International Business Studies

over the 12-year period between 1991 and 2002.As of the end of 2002, 216 of the 1010 venturecapital firms made 1714 rounds of investment in920 ventures located in 40 different foreign coun-tries. The largest investors were Warburg Pincus,Advent International Corporation, and Japan/America Ventures. We excluded from all analyses17 investments in companies that had gone publicbefore the US venture capital firm invested.

Estimation Method and Dependent VariableWe analyzed the rate of a venture capital firmentering a new country with a hazard rate model(Allison, 1995; Tuma & Hannan, 1984). The hazardfunction is

hðtÞ ¼ limDt!0

Pr tpTot þ DtjTXtf gDt

ð1Þ

and specifies the instantaneous rate at which entryoccurs at time t, given that the event has not yetoccurred (Allison, 1995; Kalbfleisch & Prentice,2002). We modeled the hazard rate of entering anew country with the piecewise exponential modelas implemented in Stata (Sorensen, 1999). Piece-wise exponential models are semi-parametric mod-els, where the baseline hazard rate is allowed tovary in an unconstrained way at each predefinedtime period. The benefit of this approach is theability to model the time dependence withoutthe more restrictive assumptions of parametricmodels. In order to estimate the hazard rate ineach time period, we divided the data into yearlyspells (Hannan & Freeman, 1989), and treated theobservations as censored unless an event (entry)occurred. The time-varying independent variableswere updated in each spell. The models wereestimated using maximum likelihood estimationas implemented in Stata. For each year j, the hazardfor each i is assumed to have the form

log hiðtÞ ¼ aj þ bxj for aj�1ptoaj ð2Þ

Because there are multiple observations for eachventure capital firm and country, observations inthe sample may not be independent. We thereforecalculated robust standard errors clustered oneach country–firm pair (Rogers, 1993; Wooldridge,2002). We also implemented alternative models byclustering on firms or countries only, and theresults did not change.

We estimated our models using a sample of firm-country-year observations. Each US venture capitalfirm may choose to enter a foreign country during a

given year. The dependent variable (event) equals 1if firm i entered country j during year t. Afterexcluding US venture capital firms that neverinvested abroad in this period, we have completedata for 137,605 firm-country-year observations.Results including firms that never invested arequalitatively similar to those reported below. Ourempirical analysis focuses on investment countsand not on the size of the investment, because onecan observe the latter only if an investment actuallytakes place. Focusing on the amount investedwould unavoidably introduce a selection bias intothe analysis of the impact of institutions, as wewould have to include in our analysis only actualentries, and we would not have been able toexamine the impact of institutions on the like-lihood of entry in the first place.

The 216 venture capital firms in the populationwere active for an average of 7 years between 1991and 2002. We obtained reasonably complete back-ground information on 95 countries (see Appendixfor a list), although for some of them the indepen-dent variables were not available for each and everyyear. The final sample for analysis consists of137,605 firm-country-year combinations.8

Independent VariablesWe follow the existing literature in measuring host-country institutions supporting innovation andtechnology (hereafter referred to as technologicalinstitutions) with outcome measures of the level ofinnovative activity in each country (Furman et al.,2002; Guler, Guillen, & MacPherson, 2002; Kumar-esan & Miyazaki, 1999; Niosi, 2002). We use twoseparate indicators to measure the level of innova-tive activity in country j: the number of US patentsgranted to establishments in country j during yeart�1, and the number of scientific and technicalarticles authored by residents of country j duringyear t�1. Patents and articles are widely usedempirical indicators of the performance of nationalsystems of innovation (Furman et al., 2002; Guleret al., 2002; Kumaresan & Miyazaki, 1999; Niosi,2002), although they do not capture the full extentof innovative activity (Nelson & Rosenberg, 1993).They are especially well suited to a study of thefactors that attract US venture capital firms toforeign environments because they are the resultof both the level of inputs and the productivity ofthe system. It is also important to note that the USPatent and Trademark Office and the Institute ofScientific Information are sources of informationon knowledge, technology and innovation routinely

US venture capital internationalization Isin Guler and Mauro F Guillen

193

Journal of International Business Studies

used by US venture capital firms. Our field inter-views revealed that venture capitalists and industryexperts use patents and scientific articles as indica-tors of innovative activity in foreign countries, or tolegitimize their decisions. Either way, countrieswith greater counts of patents and articles willbe more attractive to the venture capital firm. Weobtained the patent data from the NBER database(Hall, Jaffe, & Trajtenberg, 2001), and the publica-tion data directly from the Institute of ScientificInformation’s Science Citation Index (whichincludes journals in several languages).

While it is useful to measure the number ofpatents filed domestically rather than those filed inthe US, we chose the latter measure for threereasons. First, data on local patent filings are notavailable for many of the countries included in ouranalysis; using them would bias our sample towardcountries with a highly developed intellectualproperty protection regime. Second, differences inpatent laws limit the comparability of such figuresacross countries (Maskus, 2000). Third, for USventure capital firms, patents filed in the US arelikely to be a more relevant and visible indicator ofinnovative activity than patents filed elsewhere,since this information is more easily availableand comparable across ventures. We normalizedpatents and publications by the GDP of eachcountry j during year t�1.

We used various sources to calculate the indica-tors of supporting institutions. In order to capturethe effect of legal institutions, we used La Portaet al.’s (1998) classification of countries accordingto legal tradition. Following the existing literature,this classification takes into account several char-acteristics of the legal system in each country,including its history, underlying legal theories,and institutional development (Glendon et al.,1994; La Porta et al., 1998; Reynolds & Flores,1989; Zweigert & Kotz, 1998). La Porta and hiscolleagues classified countries into five legal tradi-tions: English, French, German, Scandinavian, andformerly socialist. French, German, and Scandina-vian legal families all belong to the civil lawtradition. Since prior work suggests that countrieswith a legal system based on English common lawprovided better investor protection (e.g., La Portaet al., 1998), we use a dummy variable that takesthe value of 1 for countries with English legaltradition, and 0 otherwise. In our sample, 30countries were classified under the English com-mon law category (see Appendix). In results notreported, we also added dummies for the other legal

families, as well as a dummy variable indicatingwhether English is the official or the most widelyspoken language. The results were similar.

We measured local stock market size with totalmarket capitalization as a percentage of GDP(World Bank, 2008). We also considered stockmarket turnover ratio and changes in the numberof listed companies as further indicators of theavailability of exit options. Capitalization hasthe additional advantage that it is correlated withthe two ways in which venture capitalists obtaintheir returns, namely helping ventures go publicand finding an acquirer. While a larger capitalmarket facilitates IPOs, it also increases availabilityof funds, which enables acquisition activity. Wemeasured political institutions (policy stability)with the political constraints index, which capturesthe limitations on policymakers to unilaterallychange the existing policy regime (Henisz, 2000b).This indicator ranges between 0 (most hazardous)and 1 (most constrained, i.e., stable). The politicalconstraint index is historically highly correlatedwith the risk indexes included in the InternationalCountry Risk Guide (ICRG, 1996) (Marshall &Jaggers, 2000). We measured each venture capitalfirm’s international experience with the cumulativenumber of ventures funded by the venture capitalfirm outside the US as of year t�1.

Control Variables

Firm-level control variables. We controlled for threeattributes of each venture capital firm in the homemarket:

(1) the domestic experience of the venture capitalfirm, measured as the cumulative number ofventures funded by the venture capital firm inthe US as of year t�1;

(2) the prior performance of the venture capitalfirm, measured as the cumulative number ofsuccessful exits (measured as the number ofIPOs) that the venture capital firm had achievedas of year t�1;

(3) the centrality score of the venture capital firm inthe domestic syndication network, measured withBonacich’s (1987) eigenvector centrality measure,calculated for years t�3, t�2, and t�1 (Guler &Guillen, 2010; Podolny, 2001, 2005).

The centrality score ranges between 0 (for isolatedfirms) and 1 (for firms that syndicate with otherhigh-status actors). These measures account for sizeand social status of the venture capital firm, as well

US venture capital internationalization Isin Guler and Mauro F Guillen

194

Journal of International Business Studies

as unobserved firm heterogeneity in skills andcapabilities (Bottazzi et al., 2008; Gompers &Lerner, 2000: 236; Hochberg, Ljungqvist, & Lu,2007; Kaplan et al., 2007). We also controlled forthe number of ventures funded by the venturecapital firm in foreign countries as of year t�1, andthe number of countries that the venture capitalfirm had entered until the end of year t�1, in orderto control both for unobserved firm heterogeneityin general, and for the propensity to invest abroadin particular.

Country-level and time control variables. Weincluded a time-varying control for the size of theeconomy, measured as GDP in constant 1995 US

dollars (World Bank, 2008), and for other sources ofunobserved cross-national heterogeneity in the firststage of our estimation procedure (see below). Inaddition, we controlled for the cumulative numberof ventures that US venture capital firms hadfunded in country j as of year t�1. This measureaccounts for unobserved cross-national differencesin taxes and other incentives (Jeng & Wells, 2000).We also included 12 ‘‘time pieces,’’ each of whichspans the period of a year.

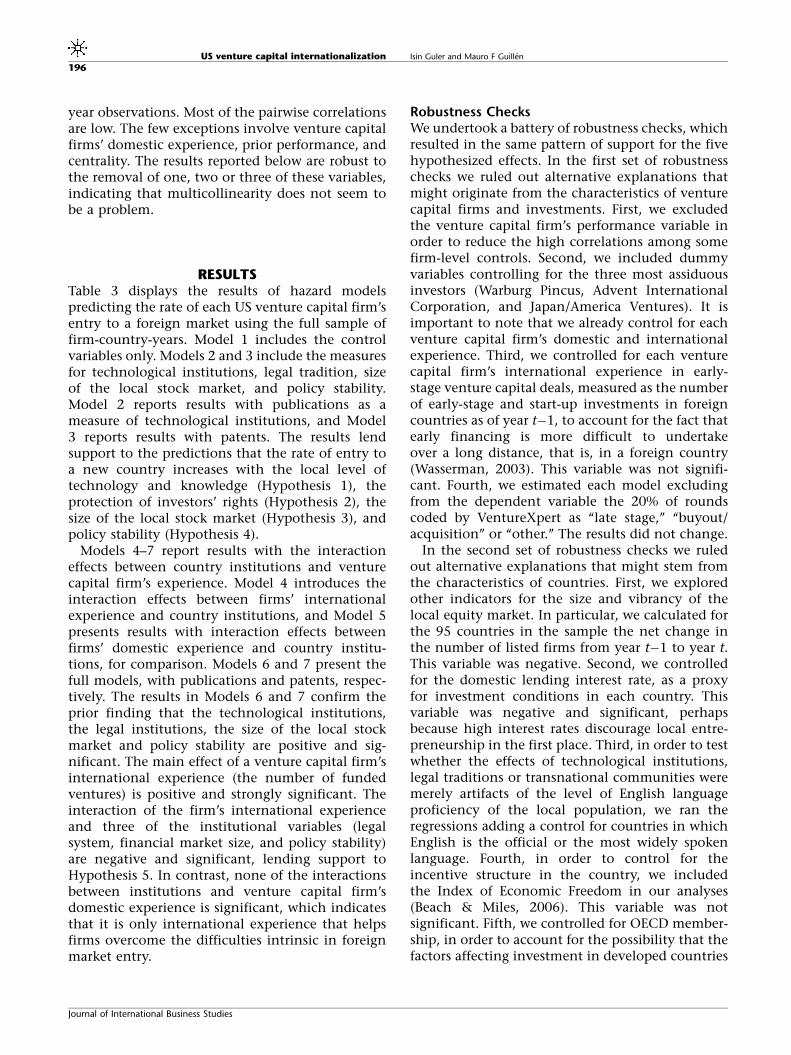

Descriptive StatisticsTables 1 and 2 display the sample descriptivestatistics and the correlations, which are based onthe sample of 137,605 venture capital firm-country-

Table 1 Descriptive statistics (N¼137,605 firm-country-years)

Variable Mean Std. dev. Min. Max.

1 Patents/GDP 0.802 1.376 0.000 8.760

2 Number of publications/GDP 0.026 0.026 0.000 0.19

3 English legal system 0.343 0.475 0.000 1.000

4 Stock market capitalization (% GDP) 41.818 50.315 0.010 329.960

5 Policy stability 0.566 0.277 0.000 0.890

6 GDP (*10–12) 0.281 0.736 0.001 5.710

7 Foreign VC experience in country (no. of ventures) 4.582 15.074 0.000 157.000

8 VCF’s no. of countries entered 2.489 7.771 0.000 40.000

9 VCF centrality 0.038 0.049 0.000 0.230

10 VCF prior performance (no. of IPOs) 6.473 11.262 0.000 81.000

11 VCF’s international experience (no. of foreign ventures) 1.946 7.505 0.000 115.000

VCF’s domestic experience (no. of ventures) 24.418 38.504 0.000 363.000

Table 2 Correlations (N¼137,605 firm-country-years)

Variable 1 2 3 4 5 6 7 8 9 10 11 12

1 Patents/GDP 1.000

2 Number of publications/GDP 0.184 1.00

3 English legal system �0.015 �0.075 1.000

4 Stock market capitalization

(% GDP)

0.420 �0.051 0.161 1.000

5 Policy stability 0.371 0.076 0.036 0.239 1.000

6 GDP (*10–12) 0.515 �0.089 �0.137 0.166 0.191 1.000

7 Foreign VC experience in

country (no. of ventures)

0.553 0.084 0.119 0.317 0.168 0.495 1.000

8 VCF’s number of countries

entered

0.012 0.023 0.001 0.020 �0.006 0.000 0.053 1.000

9 VCF centrality 0.002 �0.001 0.003 �0.002 �0.004 0.003 �0.001 0.146 1.000

10 VCF prior performance

(no. of IPOs)

0.002 0.022 �0.004 0.015 0.004 �0.005 0.028 0.192 0.712 1.000

11 VCF’s international experience

(no. of foreign ventures)

0.010 0.020 0.001 0.016 �0.005 0.000 0.044 0.402 0.100 0.221 1.000

12 VCF’s domestic experience

(no. of ventures)

0.016 0.041 �0.001 0.032 �0.004 �0.003 0.078 0.268 0.705 0.879 0.271 1.000

US venture capital internationalization Isin Guler and Mauro F Guillen

195

Journal of International Business Studies

year observations. Most of the pairwise correlationsare low. The few exceptions involve venture capitalfirms’ domestic experience, prior performance, andcentrality. The results reported below are robust tothe removal of one, two or three of these variables,indicating that multicollinearity does not seem tobe a problem.

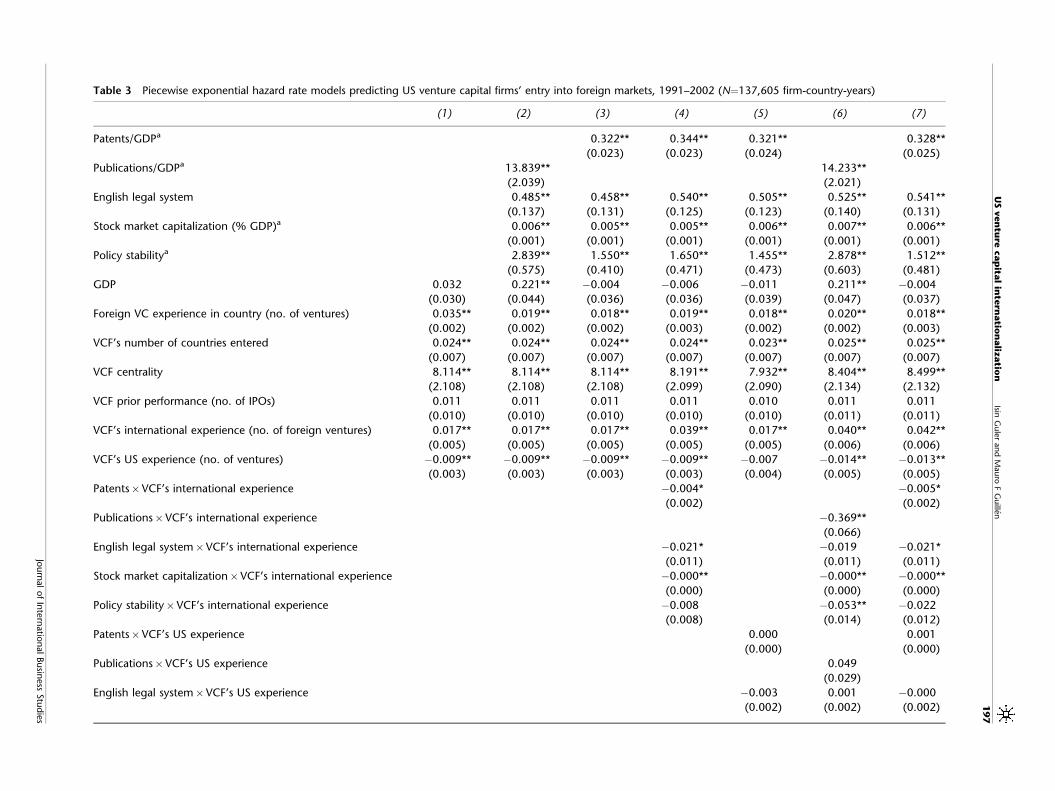

RESULTSTable 3 displays the results of hazard modelspredicting the rate of each US venture capital firm’sentry to a foreign market using the full sample offirm-country-years. Model 1 includes the controlvariables only. Models 2 and 3 include the measuresfor technological institutions, legal tradition, sizeof the local stock market, and policy stability.Model 2 reports results with publications as ameasure of technological institutions, and Model3 reports results with patents. The results lendsupport to the predictions that the rate of entry toa new country increases with the local level oftechnology and knowledge (Hypothesis 1), theprotection of investors’ rights (Hypothesis 2), thesize of the local stock market (Hypothesis 3), andpolicy stability (Hypothesis 4).

Models 4–7 report results with the interactioneffects between country institutions and venturecapital firm’s experience. Model 4 introduces theinteraction effects between firms’ internationalexperience and country institutions, and Model 5presents results with interaction effects betweenfirms’ domestic experience and country institu-tions, for comparison. Models 6 and 7 present thefull models, with publications and patents, respec-tively. The results in Models 6 and 7 confirm theprior finding that the technological institutions,the legal institutions, the size of the local stockmarket and policy stability are positive and sig-nificant. The main effect of a venture capital firm’sinternational experience (the number of fundedventures) is positive and strongly significant. Theinteraction of the firm’s international experienceand three of the institutional variables (legalsystem, financial market size, and policy stability)are negative and significant, lending support toHypothesis 5. In contrast, none of the interactionsbetween institutions and venture capital firm’sdomestic experience is significant, which indicatesthat it is only international experience that helpsfirms overcome the difficulties intrinsic in foreignmarket entry.

Robustness ChecksWe undertook a battery of robustness checks, whichresulted in the same pattern of support for the fivehypothesized effects. In the first set of robustnesschecks we ruled out alternative explanations thatmight originate from the characteristics of venturecapital firms and investments. First, we excludedthe venture capital firm’s performance variable inorder to reduce the high correlations among somefirm-level controls. Second, we included dummyvariables controlling for the three most assiduousinvestors (Warburg Pincus, Advent InternationalCorporation, and Japan/America Ventures). It isimportant to note that we already control for eachventure capital firm’s domestic and internationalexperience. Third, we controlled for each venturecapital firm’s international experience in early-stage venture capital deals, measured as the numberof early-stage and start-up investments in foreigncountries as of year t�1, to account for the fact thatearly financing is more difficult to undertakeover a long distance, that is, in a foreign country(Wasserman, 2003). This variable was not signifi-cant. Fourth, we estimated each model excludingfrom the dependent variable the 20% of roundscoded by VentureXpert as ‘‘late stage,’’ ‘‘buyout/acquisition’’ or ‘‘other.’’ The results did not change.

In the second set of robustness checks we ruledout alternative explanations that might stem fromthe characteristics of countries. First, we exploredother indicators for the size and vibrancy of thelocal equity market. In particular, we calculated forthe 95 countries in the sample the net change inthe number of listed firms from year t�1 to year t.This variable was negative. Second, we controlledfor the domestic lending interest rate, as a proxyfor investment conditions in each country. Thisvariable was negative and significant, perhapsbecause high interest rates discourage local entre-preneurship in the first place. Third, in order to testwhether the effects of technological institutions,legal traditions or transnational communities weremerely artifacts of the level of English languageproficiency of the local population, we ran theregressions adding a control for countries in whichEnglish is the official or the most widely spokenlanguage. Fourth, in order to control for theincentive structure in the country, we includedthe Index of Economic Freedom in our analyses(Beach & Miles, 2006). This variable was notsignificant. Fifth, we controlled for OECD member-ship, in order to account for the possibility that thefactors affecting investment in developed countries

US venture capital internationalization Isin Guler and Mauro F Guillen

196

Journal of International Business Studies

Table 3 Piecewise exponential hazard rate models predicting US venture capital firms’ entry into foreign markets, 1991–2002 (N¼137,605 firm-country-years)

(1) (2) (3) (4) (5) (6) (7)

Patents/GDPa 0.322** 0.344** 0.321** 0.328**

(0.023) (0.023) (0.024) (0.025)

Publications/GDPa 13.839** 14.233**

(2.039) (2.021)

English legal system 0.485** 0.458** 0.540** 0.505** 0.525** 0.541**

(0.137) (0.131) (0.125) (0.123) (0.140) (0.131)

Stock market capitalization (% GDP)a 0.006** 0.005** 0.005** 0.006** 0.007** 0.006**

(0.001) (0.001) (0.001) (0.001) (0.001) (0.001)

Policy stabilitya 2.839** 1.550** 1.650** 1.455** 2.878** 1.512**

(0.575) (0.410) (0.471) (0.473) (0.603) (0.481)

GDP 0.032 0.221** �0.004 �0.006 �0.011 0.211** �0.004

(0.030) (0.044) (0.036) (0.036) (0.039) (0.047) (0.037)

Foreign VC experience in country (no. of ventures) 0.035** 0.019** 0.018** 0.019** 0.018** 0.020** 0.018**

(0.002) (0.002) (0.002) (0.003) (0.002) (0.002) (0.003)

VCF’s number of countries entered 0.024** 0.024** 0.024** 0.024** 0.023** 0.025** 0.025**

(0.007) (0.007) (0.007) (0.007) (0.007) (0.007) (0.007)

VCF centrality 8.114** 8.114** 8.114** 8.191** 7.932** 8.404** 8.499**

(2.108) (2.108) (2.108) (2.099) (2.090) (2.134) (2.132)

VCF prior performance (no. of IPOs) 0.011 0.011 0.011 0.011 0.010 0.011 0.011

(0.010) (0.010) (0.010) (0.010) (0.010) (0.011) (0.011)

VCF’s international experience (no. of foreign ventures) 0.017** 0.017** 0.017** 0.039** 0.017** 0.040** 0.042**

(0.005) (0.005) (0.005) (0.005) (0.005) (0.006) (0.006)

VCF’s US experience (no. of ventures) �0.009** �0.009** �0.009** �0.009** �0.007 �0.014** �0.013**

(0.003) (0.003) (0.003) (0.003) (0.004) (0.005) (0.005)

Patents�VCF’s international experience �0.004* �0.005*

(0.002) (0.002)

Publications�VCF’s international experience �0.369**

(0.066)

English legal system�VCF’s international experience �0.021* �0.019 �0.021*

(0.011) (0.011) (0.011)

Stock market capitalization�VCF’s international experience �0.000** �0.000** �0.000**

(0.000) (0.000) (0.000)

Policy stability�VCF’s international experience �0.008 �0.053** �0.022

(0.008) (0.014) (0.012)

Patents�VCF’s US experience 0.000 0.001

(0.000) (0.000)

Publications�VCF’s US experience 0.049

(0.029)

English legal system�VCF’s US experience �0.003 0.001 �0.000

(0.002) (0.002) (0.002)

US

ven

ture

cap

ital

inte

rnatio

naliz

atio

nIsin

Gule

ran

dM

auro

FG

uille

n

19

7

Journ

al

of

Inte

rnatio

nalBusin

ess

Stu

die

s

Table 3 Continued

(1) (2) (3) (4) (5) (6) (7)

Stock market capitalization�VCF’s US experience �0.000* �0.000 �0.000

(0.000) (0.000) (0.000)

Policy stability�VCF’s US experience 0.005 0.024 0.013

(0.008) (0.012) (0.009)

1991 �14.192** �14.650** �14.710** �14.802** �14.696** �14.705** �14.799**

(0.432) (0.520) (0.500) (0.490) (0.496) (0.510) (0.490)

1992 �13.912** �14.376** �14.430** �14.528** �14.421** �14.429** �14.518**

(0.360) (0.451) (0.431) (0.416) (0.425) (0.436) (0.415)

1993 �14.961** �15.413** �15.384** �15.476** �15.381** �15.463** �15.463**

(0.389) (0.462) (0.442) (0.422) (0.430) (0.434) (0.416)

1994 �15.067** �15.682** �15.573** �15.687** �15.598** �15.763** �15.680**

(0.563) (0.619) (0.601) (0.606) (0.597) (0.620) (0.607)

1995 �14.204** �14.817** �14.676** �14.781** �14.696** �14.884** �14.767**

(0.278) (0.311) (0.294) (0.301) (0.297) (0.315) (0.303)

1996 �14.323** �14.944** �14.751** �14.858** �14.774** �15.010** �14.838**

(0.279) (0.347) (0.321) (0.322) (0.321) (0.342) (0.320)

1997 �14.239** �14.936** �14.682** �14.812** �14.714** �15.019** �14.788**

(0.219) (0.335) (0.297) (0.266) (0.265) (0.301) (0.262)

1998 �14.445** �15.125** �14.887** �15.030** �14.926** �15.211** �14.998**

(0.238) (0.290) (0.262) (0.264) (0.265) (0.287) (0.266)

1999 �13.727** �14.439** �14.405** �14.570** �14.452** �14.531** �14.532**

(0.164) (0.272) (0.245) (0.228) (0.224) (0.256) (0.229)

2000 �13.110** �13.960** �13.890** �14.078** �13.944** �14.067** �14.034**

(0.122) (0.210) (0.183) (0.183) (0.181) (0.207) (0.189)

2001 �14.793** �15.185** �15.139** �15.349** �15.207** �15.318** �15.302**

(0.282) (0.279) (0.268) (0.282) (0.282) (0.292) (0.289)

2002 �16.013** �15.958** �16.137** �16.350** �16.221** �16.105** �16.307**

(0.353) (0.322) (0.334) (0.335) (0.331) (0.329) (0.339)

Log likelihood �2651.3 �2536.6 �2483.4 �2461.3 �2480.6 �2512.2 �2458.6

aMean centered variable.Robust standard errors in parentheses.*po0.05; **po0.01.

US

ven

ture

cap

ital

inte

rnatio

naliz

atio

nIsin

Gule

ran

dM

auro

FG

uille

n

19

8

Journ

al

of

Inte

rnatio

nalBusin

ess

Stu

die

s

might be different from those in developingcountries, and our measures merely capture thelevel of development. While OECD membershipwas significant in predicting venture capital invest-ment, our results on predicted effects remainedsimilar. In these models we found robust supportfor the impact of country institutions on rate ofentry, as well as robust support for the interactioneffects between institutions and the venture capitalfirm’s international experience. The only excep-tions were the lack of significance in interactioneffects in some models between the size of thefinancial markets and international experience,and policy stability and international experience.

We also repeated the analyses with differentmodeling techniques. First, we estimated thehazard for a venture capital firm’s repeated invest-ments in a country with piecewise exponentialmodels with repeated events. In these models wecontrolled for the non-independence of repeatedevents by adding a gamma-distributed frailty termshared over venture capital firms, and by stratifyingon venture capital firms. We also added twovariables, VCF’s prior entries in the focal country,and duration since VCF’s entry into the country, inmodels with repeated events. While these twovariables were significant, they did not change thereported results. Second, we estimated the numberof investments that each US venture capital firmmade in each country using zero-inflated negativebinomial models. In these models we estimated thelikelihood of zero investments using country-levelvariables (number of patents, English legal systemdummy, stock market capitalization, policy stabi-lity, and GDP). Third, we repeated the analysis withnegative binomial models with firm fixed effects.Finally, we examined the rate of entry in a countrysample of country-years only (n¼812), in order tocheck whether our results were biased by usingfirm-country-years as the level of analysis. Theresults remained similar in each case, although thefixed effects models with interaction effects did notconverge.

The estimates reported in Table 3 are not onlyrobust to a variety of changes in the model’sspecification and to the inclusion of additionalcontrol variables, but also large in magnitude.Figure 1 reports the multiplier of the hazard rateof entry evaluated at different levels of each of thehypothesized variables, assuming different degreesof international experience and mean US experi-ence, according to Model 7 of Table 3. Wheninternational experience equals 0, the multiplier of

the hazard of entry increases approximately 22times as the patent variable increases from 0 to themaximum value observed in the data set, 6.5 timesas the stock market capitalization variable increasesfrom 0 to its maximum value, and five times as thepolicy stability variable increases from 0 to itsmaximum value. The multipliers are higher, thelower the international experience. At high levelsof patents, stock market capitalization, and policy

00

5

10

15

20

25

1 2 3 4Patents

5 6 7 8

No internationalexperience

Mean internationalexperience

Mean + 1sdinternationalexperience

00

1

2

3

4

5

6

0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9Policy stability

No internationalexperience

0 50 100 150 200 250 300Stock market capitalization

0

1

2

3

4

5

7

6

No internationalexperience

Mean internationalexperience

Mean + 1sdinternationalexperience

Figure 1 Multipliers of the hazard rate for significant hypoth-

esized variables evaluated at different levels of international

experience and mean US experience.

Source: Based on the estimates from Model 7 in Table 3.

US venture capital internationalization Isin Guler and Mauro F Guillen

199

Journal of International Business Studies

stability the mitigating effect of internationalexperience is greatest. Given that English legaltradition is a dummy variable, drawing a chartsimilar to those reported in Figure 1 is not possible.The moderating effect of international experienceis also sizeable for the English legal traditiondummy: for firms with no international experiencethe multiplier of English legal tradition (as opposedto any other) is almost twice as big as for firms witha level of international experience equal to themean plus one standard deviation.

DISCUSSION AND CONCLUSIONThis paper has offered a systematic analysis of therole of institutions in determining the attractive-ness of a foreign country to firms. It contributes tointernational business research by examining thefeatures of the institutional environment thatinfluence venture capital firms’ foreign marketentry decisions, and how their effect changes asfirms acquire experience. Firms pick and choose theenvironments in which they wish to operate,largely in terms of the nature and quality of theinstitutions present in them. Thus firms find iteasier to operate in environments in which theyhave access to the required institutional architec-ture or infrastructure. Our paper adds to thisliterature a finer-grained theoretical developmentof this idea, and robust empirical evidence in itsfavor. Moreover, we also argued and found that asthe firm accumulates international experience, theeffect of institutions becomes smaller in size, afinding we interpret as evidence that firms learn toovercome institutional constraints. This inter-pretation is all the more plausible becausedomestic experience, unlike international experi-ence, did not moderate the impact of institutionalvariables.

Our results highlight the importance of nationalsystems of innovation in attracting foreign venturecapital investment. Our theoretical and empiricalanalysis is in line with recent work in internationalbusiness research emphasizing that firms frequentlyexpand abroad in order to enhance and comple-ment their existing capabilities with new knowl-edge (Alcacer & Chung, 2007; Chung & Alcacer,2002). While this body of work has focused on theexpansion of firms operating in research-intensiveindustries through direct investment, especially inR&D activities (e.g., Florida, 1997; Kuemmerle,1999), the inclination of venture capital firms todo business in countries with a highly developedsystem of innovation and plentiful technology is

fully consistent with prior findings. Even thoughventure capital firms may not have the objective tointernalize the local sources of knowledge, theystill stand to benefit from identifying local entre-preneurial ventures that create and exploit suchknowledge.

Our paper contributes to the small but burgeon-ing literature on international venture capitalinvestments. As opposed to most research in thisarea, which compares the precedents of domesticventure capital industries (Becker & Hellmann,2005; Black & Gilson, 1998; Kenney et al., 2002),we focused on the cross-border investments ofUS venture capital firms, an understudied pheno-menon (Wright et al., 2005). We extend prior workin this area emphasizing the domestic supply ofventure capital (e.g., Maula & Makela, 2003), byinvestigating local demand for venture capital(through national systems of innovation), as wellas supporting institutions. We also point to theneed to treat the choice of international markets asan endogenous one in examining the practices ofventure capital firms in those markets.

In particular, we believe that our results on theimportance of legal institutions can help improveprevious work on cross-national differences incontracting. Prior research has focused on howventure capital firms adapt their practices to legalregimes with poor investor protection throughincreasing ownership stakes and maximizingtheir presence on the venture’s board of directors(Bottazzi et al., 2008; Kaplan et al., 2007; Lerner &Schoar, 2005). These studies, however, do notcorrect for the self-selection bias that may accruewhen venture capitalists systematically avoidfunding otherwise attractive ventures just becausethey are located in a country with poor investorprotection, thus resulting in an econometricunderestimation of the impact of legal institutions.Our theoretical argument was that venture capital-ists may avoid investing in countries with poorinvestor protection in the first place, since the needto increase ownership stakes for control purposeswould interfere with the logic of portfolio diversi-fication. Our empirical results provide modestevidence that legal institutions may influence theattractiveness of a country for venture capital firms.As such, it can be readily used to calculate thechances that a firm originating from a countrywith strong investor protections will fund a venturein a country with a legal regime not offering suchprotections, thus helping assess the true effectof legal tradition on investment by taking into

US venture capital internationalization Isin Guler and Mauro F Guillen

200

Journal of International Business Studies

account the information provided by the non-occurrence of investments, that is, by eliminatingthe self-selection bias.

While the implications of our research seem toparallel those stemming from studies on foreigndirect and portfolio investments, it is importantto emphasize that the specific institutions thatmake a country attractive to foreign venturecapitalists are not as relevant for the other typesof investment. A country’s technological andscientific knowledge stocks are relevant only for asmall proportion of foreign direct investmentdecisions – those having to do with the acquisitionof strategic assets. They tend not to be a considera-tion in the cases of the much more frequentefficiency- or market-seeking direct investments(Dunning, 1998). Similarly, international port-folio investors do not look for opportunitiesexclusively in the technology area, whereasventure capitalists overwhelmingly do (Gompers& Lerner, 2000). The legal protection of owners’rights is certainly critical to the portfolio investor,but of much less consequence to the direct investor,who tends to acquire a majority stake (Caves,1996). Similarly, the size and dynamism of theequity market is crucial for making decisionsabout portfolio investment, but much less impor-tant to the direct investor, whose foreign subsidi-aries are rarely floated, especially in the extractiveand manufacturing sectors. Finally, policy stabilityis relevant to the portfolio investor, but it affectsdirect investors seeking market access to a greaterextent than those seeking an input, increasedefficiency or strategic assets (Caves, 1996; Dunning,1993). Thus, while these institutions are pertinentto foreign venture capital investments, their rele-vance to direct or portfolio investments varies fromcase to case, reflecting the fact that, while venturecapital investing shares some features of directand portfolio investing, it exhibits key peculiaritiesas well.

Our empirical results also have implications forgovernments. We found that institutions have alarge impact on entry into new markets. The resultssuggest that the best way for a government toencourage foreign entry in general, and venturecapital investment from abroad in particular,is to introduce ‘‘horizontal’’ improvements in thescientific, financial, and political institutionalinfrastructures, that is, reforms that benefit allfirms and entrepreneurs as opposed to just achosen few. Hence governments would be wise tomake information about local opportunities

and institutional mechanisms as widely availableas possible.

The research reported in this paper is limited inseveral respects. First, we examined the interna-tional expansion only of US venture capital firms,ignoring the fact that European firms are moreinternationally oriented because of the small size oftheir individual home markets (Maula & Makela,2003). For instance, Hall and Tu (2003) reportthat venture capital funds located in smallercountries such as Switzerland and Greece made upa bigger proportion of cross-border investmentsthan those based in larger countries, while therecent increase of cross-border investments by UKventure capital funds reflected the maturity ofthe European venture capital industry. Even thoughthere may be differences in the propensity ofventure capital firms to invest abroad based oncharacteristics of their home countries, we believeour results on the importance of institutions andinternational investment experience on venturecapital firms’ international expansion to be general-izable. Second, the analysis in this paper did nottake into account the way in which venture capitalfirms undertake activities abroad, namely by estab-lishing a local office or by conducting businessdirectly from the home country. Third, we did nottake into account whether and how venture capitalfirms transferred their practices in their homecountry, or adapted them to accommodate theinstitutional and cultural differences (Ferner,Almond, & Colling, 2005; Kostova, 1999). Fourth,we did not explore whether venture capital firmsfind foreign countries more attractive dependingon the types of co-investors available for syndicat-ing or the presence of other home-country venturecapital firms. Last, we did not take into account theamount of capital invested by each venture capitalfirm, but the event of entry into a country.While this test would provide an importantsensitivity analysis, data limitations, as well asthe fact that amounts are observable only for actualand not potential investments, prevented us fromconducting this test. These limitations offeropportunities to continue integrating research onventure capital with the international businessliterature on technological and supporting institu-tions. Future work can also examine the roleof network connections across countries in indu-cing international investment, or the impactof institutions on venture capital practices oncethe foreign firm starts operating in the foreigncountry.

US venture capital internationalization Isin Guler and Mauro F Guillen

201

Journal of International Business Studies

ACKNOWLEDGEMENTSWe thank the Area Editor and two anonymousreviewers for valuable suggestions and comments.Funding from the Mack Center for TechnologicalInnovation at the Wharton School is greatly appre-ciated. Gary Dushnitsky, Vit Henisz, Steve Kobrin,Robert Salomon, Harry Sapienza, Adrian Tschoegl andseminar participants at the Academy of ManagementMeetings, the universities of Maryland, Michigan, andSouthern California, Harvard Business School and TheWharton School provided excellent comments andsuggestions on various versions of this draft.

NOTES1‘‘The Global Startup,’’ Forbes Global, 29 November

2004.2Erel Margalit, founder of Jerusalem Venture Part-

ners. See ‘‘The Global Startup,’’ Forbes Global, 29November 2004.

3Interviews with K.O. Chia, formerly a principal at aHong Kong VC firm, and Chen Siwei, NationalPeople’s Congress and Chinese Academy of Sciences.

4Other studies have focused on differences indecision-making (Manigart et al., 2000), or on thewillingness to invest abroad (Hall & Tu, 2003).

5Becker and Hellmann (2005) argue that, whilehaving an active capital market is important to venturecapital, it is not sufficient. In the 1970s and 1980sgovernment-supported experiments with establishinga domestic venture capital industry failed in Germany,

in spite of the existence of well-developed capitalmarkets (Becker & Hellmann, 2005).

6VentureXpert includes ‘‘standard US venture invest-ing’’ in portfolio companies, as long as the companyis domiciled in the US, at least one of the investorsis a venture capital firm, venture investment is aprimary investment, and it entails an equitytransaction.

7While the number of venture capital firms repre-sented in the sample may seem high, it shouldbe noted that not all firms are active during theentire period of observation. We checked thesensitivity of our results by excluding VC firms thatmade fewer than three investments in the US in eachyear. The results of the analyses with the reducedsample are qualitatively similar to the ones reportedhere.

8Our analyses of this loss of information did notreveal any significant biases in the sense that theyears for which information was not available forsome of the countries appeared to be random. Thecountries with more missing years of data on somevariables tended to be less developed than thecountries with more complete data. In the empiricalanalysis we control for the level of economic develop-ment, which did not alter the general pattern ofresults. We considered using multiple imputationtechniques, but the fact that we are not using ordinaryleast-squares estimation prevented us from imple-menting them in an appropriate way.

REFERENCESAdams, J. D., & Jaffe, A. B. 1996. Bounding the effects of R&D: