new venture internationalization, strategic change · pdf fileelsevier new venture...

TRANSCRIPT

ELSEVIER

NEW VENTURE

INTERNATIONALIZATION,

STRATEGIC CHANGE,

AND PERFORMANCE:

A FOLLOW-UP STUDY

PATRICIA PHILLIPS McDOUGALL Georgia Institute o f Technology

BENJAMIN M. OVIATT Georgia State University

Although many scholars, business experts, and government agencies enthu- EXECUTIVE siastically advise all firms, including new and small ventures, to internation- SUMMARY alize, such advice does not appear to be based on empirical evidence.

Few researchers have empirically examined the link between new venture performance and the internationalization of new ventures. At best, the evi- dence suggests that there is no significant relationship.

We used a sample of 62 U.S. new venture manufacturers in the computer and communications equipment industries during the late 1980s. These industries were purportedly globalizing and may have been leading other industries into increased international operations. We found that higher levels of internationalization (percentage of foreign sales to total venture sales) were associated with higher relative market share two years later. However, there was no significant direct relationship between percentage of international sales and subsequent return on investment (ROI). Perhaps international operations simply cost more than expected. Or perhaps, as MacMillan and Day (1987)found in their study of corporate ventures over a 4-year time period, increases in market share may be a prelude to higher ROI as scale benefits translate into higher profitability. However, the 2-year time period of our study may simply not be long enough for investments in higher market shares to produce improved profits.

During the 2-year study period, many of the ventures changed their level of internationalization. Of the 36 ventures who were domestic (no international sales) in the prior study, 10 expanded into international markets over the 2 years. Of the 26 originally international ventures (international sales of at least 5%), half increased their percentage of international sales, nine reduced it, and four stayed the same. Whereas the average change in international sales percentage of the ventures was only 2.9

Address correspondence to Patricia Phillips McDougall , School of Management, Georgia Institute of Technol- ogy, Atlanta, GA 30332-0520.

Journal of Business Venturing 11, 23-40 © 1996 Elsevier Science Inc. 655 Avenue of the Americas, New York. NY 10010

0883-9026/96/$15.00 SSDI 0898-6568(95)00081-I

24 P.P. MCDOUGALL AND B.M. OVIATT

percentage points, the large standard deviation of13. Opercentage points, and the leptokurtic distribution (9. 2) reflected the dramatic changes made by some of the ventures.

Using subgroup analysis we examined these changes in percentage of international sales in con- junction with changes in strategies and performance. Ventures that had increased international sales, relative to those that had not, exhibited more positive associations between the degree of strategic change and performance as measured in terms of both relative market share and ROI. Increased international sales in technology-based new ventures seems to require simultaneous strategic changes in order to positively impact venture performance.

This study is a follow-up to McDougall's (1989)finding that technology-based new ventures that had sales in foreign markets had significantly different strategies than similar ventures that soM their products only domestically. The current study enriches the previous findings by adding consideration of (1) changes in degree of internationalization, (2) changes in strategy, and (3) venture performance.

Although we found no performance penalty associated with increasing international sales alone, indiscriminant advice for new ventures to sell in foreign markets without other supporting strategic actions is inconsistent with our findings. Internationalization, alone, did not lead to increased profit- abili~.

Entrepreneurs of young technology-based firms who are considering internationalization should take heed of our results. Internationalization of sales does not appear to be a simple matter of applying established strategies and procedures developed for a domestic arena. Successful internationalization appears to require changes in the venture's strategy as well.

I N T R O D U C T I O N

Many scholars and business experts have been unrestrained in their recommendation that more firms should be competing in international markets (e.g., Ohmae 1990; Reich 1991). Government agencies have also enthusiastically encouraged firms, both new and established, to export as a means to improve profitability. One such government source cites the improve- ment in overall return on investment (ROI) as a principal reason for exporting, and further notes, " . . . the costs and risk of exporting can be less than those of selling domestically, and more important, profits can be higher" (U.S. Department of Commerce 1991, p. vii). The U.S. Small Business Administration is encouraging small- and medium-sized firms to export their products to other nations in order to survive, to take advantage of higher growth rates in other countries, to benefit from exchange rates for the dollar when they are favorable, and to improve the balance of trade, (Small Business in the American Economy 1988).

However, such advice does not appear to be based on empirical evidence, as few research- ers have empirically examined the link between new venture ~ performance and the internation- alization of new ventures. Moreover, that link may not be a direct one. With many markets becoming increasingly international, success would seem to require that new ventures (and established firms) change their strategies in order to adapt to new global realities. Yet the authors know of no published studies that have empirically and longitudinally examined the link between new venture performance, internationalization, and strategic change. Indeed, strategic change in new ventures is relatively unexplored in any aspect (McCarthy 1992). The purpose of this study is to fill that void.

This study is a follow-up to McDougall 's (1989) study, which compared the strategies and industry structures of domestic and internationalized new ventures in the computer and communications equipment industries. In the prior study, ventures were classified as "domes- tic" if they derived no sales revenue from foreign countries or "international" if sales in

Paralleling prior research (Biggadike 1979; Miller and Camp 1985) a firm was considered a new venture if it was 8 years old or less.

NEW VENTURE INTERNATIONALIZATION 25

foreign countries comprised 5 % or more of their total sales. Using a discriminant analysis, the strategy and industry structure profiles of the internationalized new ventures were found to be significantly different from their domestic counterparts. Venture strategy distinguished between the domestic and international ventures much more than industry structure did. Thus, this follow-up study did not consider industry structure further. Venture performance was not examined at all in the prior study.

Two closely related research questions will be addressed in this follow-up investigation:

Research Question 1: What is the impact of internationalization on new venture performance?

Research Question 2: As new ventures internationalize, are changes in their strategies necessary?

I M P A C T O F I N T E R N A T I O N A L I Z A T I O N ON ESTABLISHED-FIRM P E R F O R M A N C E

Many advantages associated with internationalization are well documented in the international business literature. However, it is important to note that many of these studies have focused on large, established multinational enterprises. The potential advantages for such firms include scale economies (Caves 1971; Hymer 1976), sales stabilization over time (Hirsch and Lev 1971; Rugman 1979), tax rate arbitrage (Lessard 1979), profitable transfers of innovation from one location to another (Bartlett and Ghoshal 1991), cheaper factors of production (Porter 1990), and improved operations from facing greater competition (Porter 1990). High firm growth has also been associated with a relatively high percentage of revenues coming from foreign sales (Feeser and Willard 1990). Moreover, becoming or increasing a firm's international presence may even be a requirement for survival in some markets (Ohmae 1990).

Yet internationalizing may be risky. Local firms nearly always enjoy certain advantages over their foreign competitors, such as greater knowledge of the culture and a superior network of local business partners. Thus, multinational corporations must have clearly offsetting competitive advantages to be successful in foreign markets (Buckley and Casson 1976; Dun- ning 1981, 1988; Hymer 1976).

The empirical evidence concerning the financial benefits of firm internationalization is mixed. Numerous studies, using a variety of performance measures, have found the perfor- mance of multinational enterprises to be superior to that of domestic firms (e.g., Vernon 1971; Dunning 1973; Daniels and Bracker 1989; Grant, Jammine, and Thomas 1988), leading some scholars to conclude that the bulk of the evidence supports a positive relationship between firm internationalization and firm performance (Markides and Ittner 1994). On the other hand, studies have also reported a negative relationship (e.g., Michel and Shaked 1986; Kumar 1984; Collins 1990), and still others have reported an indeterminate relationship (e.g., Buhner 1987; Horst 1973). In general, the relationship between internationalization and performance among established firms is influenced by a complex web of firm strategies and industry conditions (Mitchell, Shaver, and Yeung 1992, 1993). Even the problems of internationalizing a small subsidiary can affect an entire corporation (Newbould, Buckley, and Thurwell 1978).

An additional body of research that has related internationalization and firm performance is the export management literature. A fairly large body of empirical research on export

26 P.P. MCDOUGALL AND B.M. OVIATT

performance appeared in the decade of the 1980s (Madsen 1987), and many of these studies used samples of smaller firms. Often these studies included a comparison of the performance of exporters and nonexporters or of exporters of differing levels of commitment (e.g., Tesar and Tarleton 1982). A number of these studies focused on marketing issues. For example, Keng and Jiuan (1989) found that exporters, when compared to nonexporters, emphasized the selection of distribution channels, marketing research, advertising and sales promotion, and product packaging. However, the findings relating to export market expansion strategies have been contradictory (Lee and Yang 1990). Numerous studies of small business have confirmed their reluctance to export (e.g., Karafakioglu 1986; Tesar and Tarleton 1982; O'Rourke 1985), have explored various ways that government policies might encourage small firms to internationalize (e.g., Blackman and Thompson 1987; Rossman 1984), and have shown that new small exporters report more problems than mature small exporters (Vozikis and Mescon 1985). Nevertheless, in their review of the export management literature, Aaby and Slater concluded that "given the quantity of published research on export practice, it is surprising that so few solid conclusions are available" (1989, p. 23). And as this literature has paid little attention to firm age, it provides few clues about the effect of internationalization on new ventures.

I M P A C T O F I N T E R N A T I O N A L I Z A T I O N O N N E W V E N T U R E P E R F O R M A N C E

Conventional theory suggests that internationalization occurs reluctantly in stages after a period of home market growth and maturation (Johanson and Vahlne 1977, 1990). Certainly, small new ventures would not be international, according to the theory. Some people have even transformed the stage theory of internationalization into a prescriptive version and proposed that firms should go international only incrementally (Bartlett and Ghoshal 1991).

Yet there is increasing evidence that the conventional stage theory of firm international- ization provides weak explanatory power for today's new ventures (Brush 1992; Welch and Loustarinen 1988; Turnbult 1987; McDougall, Shane, and Oviatt 1994). The numbers of international new ventures, firms that are international from inception, are reportedly increas- ing (McDougall, Shane, and Oviatt 1994; Oviatt and McDougall 1994). In some industries, internationalization is soon expected to be a requirement for participation for all firms, including newly formed ventures (Burrill and Almassy 1993).

Only a few empirical studies have investigated the relationship between internationaliza- tion and new venture performance. Brush (1992) found that venture age at the time of internationalization was not significantly related to either sales growth or employee growth, two common measures of new venture performance. That result is inconsistent with the prescriptive version of the stage theory. Tyebjee (1990) found that profitability among high technology new ventures that sold their products internationally was lower than ventures that only sold domestically, but the relationship was not statistically significant, and it was not a focus of his study. Thus, the relationship was not fully explored. Furthermore, both Brush's (1992) and Tyebjee's (1990) studies were cross-sectional. Perhaps, the true relation- ship is only revealed longitudinally because the benefits of internationalization are realized only after the venture's international position is established.

Earlier we explained that the relationship between internationalization and performance among established firms was complex. Among new ventures, however, the relationship may be simpler. The reason is that many new ventures that are international seem to be in high

NEW VENTURE INTERNATIONALIZATION 27

technology industries (McDougall, Shane, and Oviatt 1994) that may require some interna- tional sales as a condition of industry participation. The emergence of specialized global market niches and the high costs of R&D make early international sales necessary for technol- ogy-based firms (Lindqvist 1990). Sales to a domestic market alone would not support the required investments. Thus, in high technology markets, companies can no longer follow the stage theory of developing the domestic market first and then seeking out foreign markets (Seringhaus 1993). Moreover, new ventures that internationalize quickly seem to be highly focused firms with an intangible knowledge-based competitive advantage (Oviatt and McDou- gall 1994). Of course, the knowledge must be kept proprietary to the venture through patents, secrecy, or perhaps tacitness. Patented or secret knowledge that needs little local adaptation may be embedded in the technology of the product and transferred to multiple locations at a low marginal cost. Tacit knowledge is, of course, harder to transfer to additional locations even within one firm, but where it can be done competitors will find expropriation of the advantage extremely difficult. Thus, after a relatively short period to establish itself in foreign countries, the more international the new venture, the more profitable it is. In summary, it is possible that the relationship between international sales and performance is a simple one for technology-based new ventures:

HI: Technology-based new ventures with higher levels of international sales subsequently have higher levels of performance.

N E W V E N T U R E I N T E R N A T I O N A L I Z A T I O N , P E R F O R M A N C E , AND S T R A T E G I C C H A N G E

Perhaps that relationship is not so simple when it comes to changes in international sales. An essential element of the strategic choice perspective is that as a firm's environment changes, its strategies must also change to be congruent with its new circumstances (Child 1972). Otherwise, the organization is unlikely to be effective (Fry and Smith 1987). Certainly, international involvement is an important environmental contingency (Hambrick and Lei 1985; McDougall 1989; Porter 1980). For example, in addition to increased logistical costs, entrepreneurs and managers may need to learn something about foreign laws, language, culture, and competitors.

Organizational competencies that create competitive advantages in the international arena may be very different from those that create advantages domestically (Ghoshal 1987). Al- though the original study upon which this follow-up is based (McDougall 1989) did not consider firm performance, the strategies of purely domestic firms and those with international sales were found to be significantly different. Therefore, it is reasonable to assume that as ventures expand internationally they must make changes in their strategies to be congruent with their new environment. Thus, successful increases in venture internationalization may require broad strategic changes.

Indeed, the period while a venture is new or very young may be a critical time for strategic change. Institutionalized routines, structures, investments, and relationships charac- terize mature organizations and create age and size related inertia that inhibits strategic change (Freeman and Boeker 1984; Hannan and Freeman 1977, 1984; Tushman and Romanelli 1985). Therefore, the time of inception, or soon thereafter may be the best opportunity to set or to change a venture's strategy so that it is consistent with the needs of the international environment (McDougall, Shane, and Oviatt 1994).

28 P.P. MCDOUGALL AND B.M. OVIATT

In summary, perhaps strategic changes will be necessary for increased venture perfor- mance when technology-based new ventures increase their international presence. Exactly, what those strategic changes should be will inevitably depend on unique firm technologies, markets entered, and current strategies. At the current state of research on new venture internationalization any attempt to specify what those strategic changes should be would be speculative.

H2: Strategic change will be more positively related to performance among tech- nology-based new ventures that have increased their internationalization than among technology-based new ventures that have not increased their international- ization.

M E T H O D O L O G Y

Sample The follow-up sample of new ventures in this study was originally part of a database of 247 new ventures. In the original study, following a pilot test, surveys were mailed to the heads of new venture businesses in two related industry groups using addresses obtained from Dun and Bradstreet. As noted by Hambrick (1981), general managers are typically the most knowledgeable persons regarding their companies' strategies.

Each of the new venture manufacturers in the study was in some facet of the information processing industry; more specifically, computer-related or communications-related equip- ment manufacturing. Thus, these ventures were technology-based new ventures. A total of seven different, but closely related SIC codes were represented in the sample. Second- respondent data showed acceptable levels of interrater reliability, with average correlations of 0.58 on the 26 competitive strategy methods. A detailed description of the original data gathering procedure and sample characteristics may be found in McDougall and Robinson (1990), and the competitive strategy methods can be seen in the Appendix of this article.

Two years after the original data were gathered, heads of each of the 247 firms previously sampled were mailed a follow-up questionnaire with a cover letter asking for their participation in a longitudinal research project. Respondents were ensured confidentially. A second mailing was sent to nonrespondents 3 weeks later.

Forty-three surveys (17%) were returned with no forwarding addresses. Although an attempt was made to locate these ventures by calling the telephone information operator in the city in which the venture had been located 2 years previously, none of the firms could be reached in this manner. Of the 204 delivered questionnaires, 85 were returned for a response rate of 42 %. Four of the returned questionnaires had notes indicating the new venture was no longer in business.

The loss of 43 ventures for lack of a deliverable address 2 years later did not surprise us. Whereas some ventures may have moved and the forwarding order expired, others proba- bly were no longer in business or had been acquired by other firms. Financial constraints prevented us from obtaining new addresses or confirming the failure of the nonrespondent firms through Dun and Bradstreet.

As previously noted, the "new venture" definition in the original data paralleled prior research (Biggadike 1979) and classified a firm as a "new venture" if it was 8 years old or less. Thus, ventures in this sample that were 8 years old in the original sample were 10 years old in the follow-up sample. Miller and Camp (1985) classified firms of this age as adolescent firms. Only two of the ventures in this follow-up study were adolescents. We

NEW VENTURE INTERNATIONALIZATION 29

have retained them in the sample, because the purpose of this study was to conduct a follow-up of the new ventures previously studied.

In the first study comparing internationalized and domestic new ventures, ventures were classified as either "domestic" or "international" using a polar extreme approach (Hair et al. 1979). Domestic ventures were those with no sales to foreign countries, whereas international sales comprised 5 % or more of total sales of the international ventures. The technique excluded ventures whose international sales were between 0% and 5 % of total venture sales. Of the 90 domestic ventures and 98 international ventures in the first study, 36 of the domestic ventures and 26 of the international ventures provided sufficient follow-up data and are included in this study. Statistical tests on time-period-one (time~)data between the respondent and nonrespondent ventures indicated that the ventures did not differ significantly on age, sales, or number of employees. A binomial test of survivor bias showed that the proportional split between domestic and international ventures did not significantly differ from time~ to time2 (ct < 0.05). Our inability to contact 43 of the original ventures is worth further comment. Some of them may have failed or moved, as noted earlier. Given the industry segments in which these ventures are operating, it is likely that some of these ventures may have been acquired. Acquisition is a positive result, often the goal of the founder, that indicates the venture has achieved significant value. Although an acquired firm is technically no longer in business, acquisition should not be considered a failure as it is sometimes regarded in the study of established firms. Thus, the test for survivor bias says little about either the interna- tional or the domestic ventures' propensity to fail.

Measures

Internationalization

All ventures in the study were headquartered in the U.S. Internationalization was measured as the percentage of a sales in foreign countries to total venture sales. Internationalization was measured in the same manner in both the original study (time0 and 2 years later in the follow-up study (time2).

Strategic Change Strategic change in this study is focused at the business level and described the content of the venture's strategy as noted in McDougall (1989). It is operationalized as the sum total of changes in a venture's competitive strategy methods. Each of the 26 competitive strategy methods examined in the study captures some dimension of the venture's overall strategy, and combined, they represent the venture's strategy. The competitive strategy methods are presented in the Appendix. The use of competitive strategy methods to operationalize strategy has been used extensively in strategic management research (e.g., Dess and Davis 1984; Robinson and Pearce 1988). Whereas the operationalization of strategy in the original study entailed a factor-analytic procedure to reduce the 26 competitive strategy methods to 10 strategy factors, factor analysis was inappropriate for the follow-up study given the smaller sample size (Lawley and Maxwell 1971; Nunnally 1978).

The original and the follow-up surveys included exactly the same 26 competitive strategy methods, each scored by the respondents from 1 through 7. The absolute difference between a venture's response on the original survey and the follow-up survey was computed for each of the 26 items. For example, for a venture scoring "3" on the original survey on concern

30 P.P. MCDOUGALL AND B.M. OVIATT

for lowest cost per unit and "5" on the follow-up survey, the absolute difference would be two. Likewise, if that same venture had indicated a "1" in the follow-up the absolute difference would also be two. The higher the score, the more change the venture had made in its overall strategy. The individual absolute difference scores for each of the 26 strategy variables were summed for the strategic change score. Absolute differences in the ratings of the competitive strategy methods were used without regard to the direction of change, because there is a lack of theory that indicates emphasizing or deemphasizing any of the methods is always associated with performance differences or with differences in the degree of internationaliza- tion. Strategic change scores ranged from 16 to 65, with a standard deviation of 9.6.

Performance Our research questions and hypotheses are concerned with the relationship among changes in venture strategy, venture internationalization, and venture performance. In other words, we did not restrict our interest to the performance of the ventures' foreign operations, because it is likely that an effort to initiate international sales or to increase international sales has strong side-effects on domestic operations (Newbould, Buckley, and Thurwell 1978). That is especially true of the ventures in the present study. They are all relatively small and focused on a product segment, and, on average, the ones that are international derive 18 % of their sales from foreign markets (calculated from Table 1).

Measuring the performance of organizations is always a complex problem (Lentz 1981), but is especially thorny for new ventures. There are no commonly accepted lists of perfor- mance variables or methods by which new ventures are evaluated (Biggadike 1979; Brush and VanderWerf 1992). Strong profitability may or may not be an important objective for a new venture, which is trying to establish a foothold in a market. Thus, as suggested by Venkatraman and Ramanujam (1986), multiple measures of the concept were used in this research. Return on investment has been a commonly accepted measure of new venture performance (e.g., Biggadike 1979; Tsai, MacMillan, and Low 1991), although market share gain has been proposed as the best measure (Tsai, MacMillan, and Low 1991). Thus, both ROI (i.e., profit after tax divided by total investment) and relative market share (i.e., venture market share divided by the market share of its largest competitor) were the performance variables used. Objective measures of these variables were provided by the respondents.

A N A L Y S I S A N D R E S U L T S

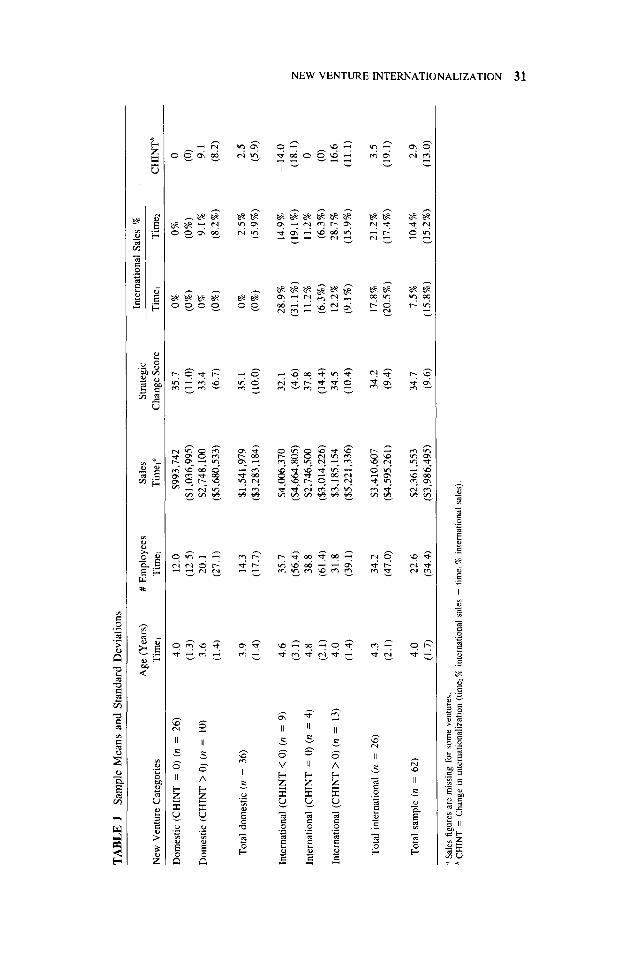

Sample characteristics of the 62 new ventures in this study are reported in Table 1. The categorization of the ventures as "domestic" and "international" is reflective of the venture's level of international sales in the original study (i.e., time0, whereas further breakdowns within these two categories indicate the change in international sales that occurred over the 2-year-period.

The level of international sales at time~ for the ventures that participated in the follow-up ranged from 0 to 100%, with one venture having 100% of its sales in foreign markets and the other ventures having between 0 and 60% in foreign markets. Fifty-eight percent of the ventures had no international sales at time~, whereas 18% reported international sales of 15% or more.

Two years later, the level of international sales ranged from 0 to 60%. Ten of the original 36 domestic ventures had become international to some degree. Of the 26 originally international ventures, half increased their percentage of international sales, nine reduced

TA

BL

E

1 S

ampl

e M

ean

s an

d S

tand

ard

Dev

iati

ons

Age

(Y

ears

) N

ew V

entu

re C

ateg

orie

s T

ime~

#

Em

ploy

ees

Tim

e~

Sal

es

Tim

e1"

Stra

tegi

c C

hang

e Sc

ore

Inte

rnat

iona

l Sa

les

%

Tim

e ~

Tim

e2

CH

INT

b

Dom

esti

c (C

HIN

T =

0)

(n

= 26

)

Dom

esti

c (C

HIN

T >

0)

(n =

10

)

4.0

(1.3

) 3.

6 (1

.4)

12.0

(1

2.5)

20

.1

(27.

1)

Tot

al d

omes

tic

(n =

36

) 3.

9 14

.3

(1.4

) (1

7.7)

Inte

rnat

iona

l (C

HIN

T <

0)

(n =

9)

4.

6 (3

.1)

Inte

rnat

iona

l (C

HIN

T =

0)

(n

= 4)

4.

8 (2

.1)

Inte

rnat

iona

l (C

HIN

T >

0)

(n =

13

) 4.

0 (1

.4)

35.7

(5

6.4)

38

.8

(61.

4)

31.8

(3

9.1)

Tot

al i

nter

nati

onal

(n

= 26

) 4.

3 34

.2

(2.1

) (4

7.0)

Tot

al s

ampl

e (n

=

62)

4.0

22.6

(1

.7)

(34.

4)

$993

,742

35

.7

0%

0%

0 ($

1,03

6,99

5 )

(11.

0)

(0 %

) (0

% )

(0)

$2,7

48,1

00

33.4

0%

9.

1%

9.1

($5,

680,

533)

(6

.7)

(0%

) (8

.2%

) (8

.2)

$1,5

41,9

79

35.1

0%

2.

5%

2.5

$3,2

83,1

84)

(10.

0)

(0%

) (5

.9%

) (5

.9)

$4,0

06,3

70

32.1

28

.9%

14

.9%

--

14.

0 ($

4,66

4,80

5)

(4.6

) (3

1.1%

) (1

9.1%

) (1

8.1)

$2

,746

,500

37

.8

11.2

%

11.2

%

0 ($

3,01

4,22

6)

(14.

4)

(6.3

%)

(6.3

%)

(0)

$3,1

85,1

54

34.5

12

.2%

28

.7%

16

.6

($5,

221,

336)

(1

0.4)

(9

.1%

) (1

5.9%

) (1

1.1)

$3,4

10,6

07

34.2

17

.8%

21

.2%

3.

5 $4

,595

,261

) (9

.4)

(20.

5%)

(17.

4%)

(19.

1)

$2,3

61,5

53

34.7

7.

5%

10.4

%

2.9

($3,

986,

495)

(9

.6)

(15.

8%)

(15.

2%)

(13.

0)

" Sa

les

figu

res a

re m

issi

ng f

or s

ome

vent

ures

. ~'

CH

INT

= C

hang

e in

inte

rnat

iona

lizat

ion

(tim

e., %

inte

rnat

iona

l sal

es -

tim

e~ %

inte

rnat

iona

l sal

es).

z .<

z ,-4

,--]

Z

2-

,-4

5 Z

;>

t"

;>

,-d

32 P.P. MCDOUGALL AND B.M. OVIATT

TABLE 2 Correlation Matrix

Variable 1 2 3 4 5 6 7

1. Strategic change 1.00 2. International sales %

(at time1) -0.06 1.00 3. International sales %

(at time2) -0.02 0.63 a 1.00 4. ROI (time,,) -0.01 0.00 -0.03 5. Relative market

share (time2) 0.16 0.27 b 0.16 6. Age (time~) -0.10 -0.07 -0.11 7. Number of employees -0.13 0.15 0.24 a

1.00

0.06 1.00 -0.09 -0.03 1.00 -0.02 -0.16 0.2& 1.00

"p< .1. ~p < .05. Cp < .01. d p < .001.

it, and four stayed the same. Over the 2-year per iod, the percentage o f ventures having no

international sales had dropped f rom 58 to 45 %, and 31% of the ventures had international

sales o f 15 % or more . H o w e v e r , the mean change in international sales was an increase o f

only 2.9 percentage points. The large standard deviat ion o f 13.0 percentage points along

with the leptokurt ic distr ibution (9.2) suggests that changes in internat ional izat ion were domi-

nated by a small number o f dramatic moves .

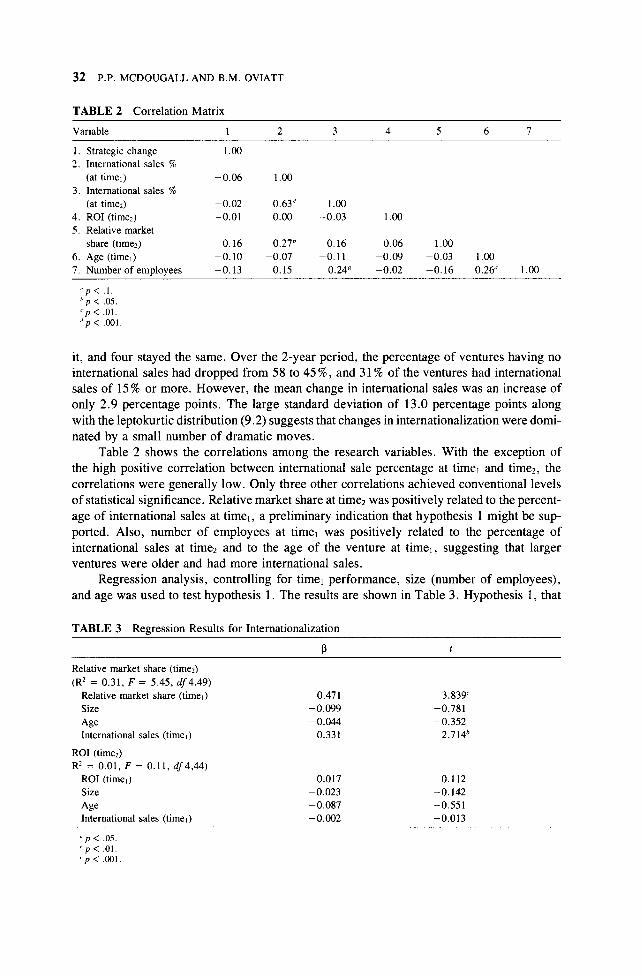

Table 2 shows the correla t ions among the research variables. With the except ion o f

the high posi t ive correlat ion be tween international sale percentage at times and time2, the

correlat ions were general ly low. Only three other correla t ions ach ieved convent ional levels

o f statistical significance. Relat ive market share at time2 was posi t ively related to the percent-

age o f international sales at timer, a pre l iminary indication that hypothesis 1 might be sup-

ported. Also, number o f employees at times was posi t ively related to the percentage o f

international sales at time2 and to the age o f the venture at times, suggesting that larger

ventures were older and had more international sales.

Regress ion analysis, control l ing for times per formance , size (number o f employees) ,

and age was used to test hypothesis 1. The results are shown in Table 3. Hypothesis 1, that

TABLE 3 Regression Results for Internationalization

13 t

Relative market share (time2) (R 2 = 0.31, F = 5.45, df4,49)

Relative market share (time~) 0.471 3.839 c Size -0.099 -0.781 Age -0.044 -0.352 International sales (time~) 0.331 2.714 b

ROI (timed R 2 = 0.01, F = 0.11, df4,44)

ROI (timel) 0.017 0.112 Size -0.023 -0.142 Age -0.087 -0.551 International sales (time~) -0.002 -0.013

Up < .05. b p < .01. ' p < . 0 0 1 .

NEW VENTURE INTERNATIONALIZATION 33

performance at time2 would be higher for ventures with higher internationalization at time1, was supported for relative market share. However, the hypothesis was not supported for ROI.

Although these new ventures were unable to translate their international sales into higher profitability over the two years, they did show significantly higher levels of relative market share over the period. Perhaps, as MacMillan and Day (1987) found in their study of corporate ventures over a 4-year time period, higher levels and increases in market share may be a prelude to higher ROI as scale benefits translate into higher profitability. The 2-year time period may simply not be long enough for investments in higher market shares to produce improved profits. An alternative explanation for the absence of a higher ROI among the more internationalized new ventures is that the costs of doing business abroad and competing against indigenous rivals was greater than they expected.

Subgroup analysis was used to test the second hypothesis, that is, to determine whether internationalization moderates the strength of the relationship between strategic change and new venture performance. For hypothesis 2, the ventures were sorted into two groups. One group was those ventures that had not increased their internationalization (i.e., domestics that had remained domestic or internationals that had not increased their international sales percentages). The other group included ventures that had a positive change in internationaliza- tion, either by expanding into international markets for the first time or by further penetration of international markets.

Partial correlations, controlling for time1 performance, age, and size (number of employ- ees), were computed within each subgroup to assess the strength of the relationship between strategic change and performance. A modified version of the Fisher Z transformation statistic, advocated by Schmidt, Hunter, and Pearlman (1981) was then used to determine whether these coefficients differed significantly between ventures that had increased their international sales and ventures that had not.

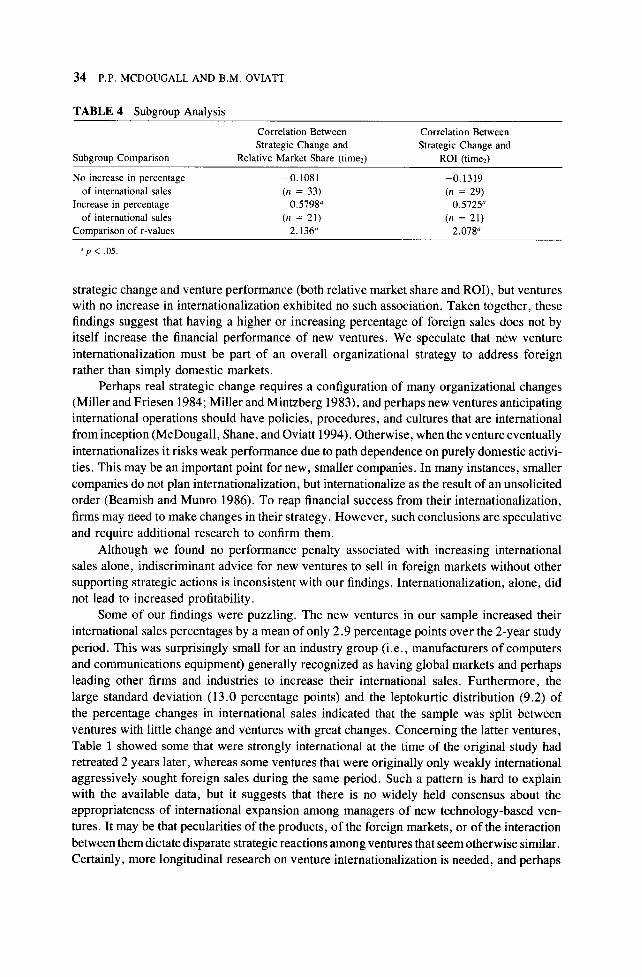

Table 4 shows the results of the subgroup analyses. Ventures with an increase in interna- tionalization had significantly higher correlations between strategic change and both relative market share and ROI. In addition, the partial correlation coefficients between strategic change and the performance measures were significantly positive, suggesting that changes in a strategy may be necessary for a venture to be successful with initial international sales or with increases in international sales. For ventures showing no increase in international presence, the partial correlation coefficients are both negative, although not statistically sig- nificant. Thus, hypothesis 2 is supported. 2

C O N C L U S I O N S

Two closely related major findings emerged from this research. First, although early interna- tionalization by new ventures in certain technology-based industries was associated with higher relative market share in subsequent years, there was no significant direct association between internationalization and ROI. Second, new ventures that increased their international- ization over the 2 years of the study exhibited significantly positive associations between

2As might be expected, no single configuration of competitive strategy methods was consistently associated with increased internationalization and superior new venture performance in our sample. Furthermore, small sample size prevented us from identifying clusters of international ventures with competitive strategy methods that were significantly higher in performance. Thus, the reduction in the number of respondents from the first round of data collection to the second round prohibited this study from explaining fully the strategic changes needed for successful new venture internationalization. Researchers investigating these questions in the future will need to take special care in maintaining their relationships over time with respondents in order to avoid this unfortunate problem.

3 4 P.P. M C D O U G A L L AND B.M. OVIATT

TABLE 4 Subgroup Analysis

Correlation Between Correlation Between

Strategic Change and Strategic Change and Subgroup Comparison Relative Market Share (times) ROI (time,_)

No increase in percentage - 0.1081 - 0.1319 of international sales (n = 33) (n = 29)

Increase in percentage 0.5798" 0.5725 a of international sales (n = 21) (n = 21)

Comparison of r-values 2.136" 2.078 a

"p < .05.

strategic change and venture performance (both relative market share and ROI), but ventures with no increase in internationalization exhibited no such association. Taken together, these findings suggest that having a higher or increasing percentage of foreign sales does not by itself increase the financial performance of new ventures. We speculate that new venture internationalization must be part of an overall organizational strategy to address foreign rather than simply domestic markets.

Perhaps real strategic change requires a configuration of many organizational changes (Miller and Friesen 1984; Miller and Mintzberg 1983), and perhaps new ventures anticipating international operations should have policies, procedures, and cultures that are international from inception (McDougall, Shane, and Oviatt 1994). Otherwise, when the venture eventually internationalizes it risks weak performance due to path dependence on purely domestic activi- ties. This may be an important point for new, smaller companies. In many instances, smaller companies do not plan internationalization, but internationalize as the result of an unsolicited order (Beamish and Munro 1986). To reap financial success from their internationalization, firms may need to make changes in their strategy. However, such conclusions are speculative and require additional research to confirm them.

Although we found no performance penalty associated with increasing international sales alone, indiscriminant advice for new ventures to sell in foreign markets without other supporting strategic actions is inconsistent with our findings. Internationalization, alone, did not lead to increased profitability.

Some of our findings were puzzling. The new ventures in our sample increased their international sales percentages by a mean of only 2.9 percentage points over the 2-year study period. This was surprisingly small for an industry group (i.e., manufacturers of computers and communications equipment) generally recognized as having global markets and perhaps leading other firms and industries to increase their international sales. Furthermore, the large standard deviation (13.0 percentage points) and the leptokurtic distribution (9.2) of the percentage changes in international sales indicated that the sample was split between ventures with little change and ventures with great changes. Concerning the latter ventures, Table 1 showed some that were strongly international at the time of the original study had retreated 2 years later, whereas some ventures that were originally only weakly international aggressively sought foreign sales during the same period. Such a pattern is hard to explain with the available data, but it suggests that there is no widely held consensus about the appropriateness of international expansion among managers of new technology-based ven- tures. It may be that pecularities of the products, of the foreign markets, or of the interaction between them dictate disparate strategic reactions among ventures that seem otherwise similar. Certainly, more longitudinal research on venture internationalization is needed, and perhaps

NEW VENTURE INTERNATIONALIZATION 35

long periods of study are needed to more fully explain the association between new venture internationalization and new venture performance.

Of course, there are important limitations to this empirical study. First, only small, technology-related, new ventures were included in the sample. Thus, generalization beyond this group is ill-advised. Second, the sample size was limited by the difficulty of obtaining responses from a large group of new venture entrepreneurs and by the further difficulty of obtaining responses from the same individuals 2 years later. Third, internationalization can occur through various modes of entry (i.e., exporting, licensing, alliances, joint ventures, direct investment, etc.), each requiring potentially different competencies and responsive changes in strategy. Finally, this study examined only the internationalization of outputs; that is, sales, and no attention was paid to the input and resource side of venture international- ization.

These limitations of our work suggest directions for future research. Ventures may need to alter their routines and strategies when they increase their use of foreign markets for major inputs and resources, just as our results suggest it is important when increasing international sales of outputs. However, we know of no studies on this topic, and since imports are so important for new ventures in many industries, research is needed on the association between venture strategy, venture performance, and the internationalization of inputs.

We were, unfortunately, unable to detect a consistent pattern of change among the competitive strategy methods that was clearly associated with venture internationalization. A primary reason was the small sample size available in this study, which is a significant problem for all longitudinal studies of this type. The whereabouts of 17% of the original sample (time,) was unknown 2 years later, and several more observations were unavoidably lost due to business failure and incomplete responses to the questionnaire at time2. To further limit the possibility of finding statistically significant associations, the mean change in interna- tionalization over the 2-year period was very small. Although a group of ventures in the sample made large changes in the percent of international sales, some in that group increased that percentage and some decreased it (see Table 1). Thus, with a small sample and inconsistent behavior on the part of ventures in the sample, we believe it was simply not possible for a statistically significant pattern of changes in the competitive strategy methods to emerge in this study.

This is disheartening for researchers hoping to find consistent patterns of change in strategy and international behavior over time among new ventures. Not only should the research period be longer than 2 years (as discussed earlier), but the sample size should also be relatively large in order to withstand inevitable losses of data over time and to detect any patterns in what may be rather disparate venture behaviors. These are difficult challenges for academic entrepreneurs.

Future research should also investigate the effect of mode of foreign entry on strategy change and venture performance. Modes that require fewer resource commitments, such as licensing and exporting through an agent, may require few strategic changes to increase a venture's international presence. Indeed, the export agent's strategy may be the critical vari- able, not the venture's strategy. 3 Perhaps venture strategy is more important in firms that have complex foreign alliances, joint ventures, and direct foreign investments. Again, we know of no published research on this topic.

Our findings are important primarily for academics. However, practicing entrepreneurs should take heed from our results. Internationalization of sales among high-technology new

3Thanks to an anonymous JBV reviewer for this suggestion.

36 P.P. MCDOUGALL AND B.M. OVIATT

ventures does not appear to be a simple matter of applying established strategies and proce- dures developed for a domestic arena. Successful internationalization appears to be accompa- nied by changes in venture strategy. At this time, however, no consistent pattern of strategic changes is clear from our research.

REFERENCES

Aaby, N., and Slater, S.F. 1989. Management influences on export performance: a review of the empirical literature 1978-88. International Marketing Review 6(4):7-26.

Bartlett, C.A., and Ghoshal, S, 1991. Managing Across Borders: The Transnational Solution. Boston: Harvard Business School Press.

Beamish, P.W., and Munro, H.J. 1986. Export performance of small and medium-sized Canadian manufacturers. Canadian Journal of Administrative Science 3(1):29-40.

Biggadike, R.E. 1979. The risky business of diversification. Harvard Business Review 57:103-111.

Blackman, R., and Thompson, J.H., 1987. The 1986 White House conference on small business. Journal of Small Business Management January:3-10.

Brush, C.G. 1992. Factors motivating small companies to internationalize: the effect of firm age. Doctoral dissertation, Boston University.

Brush, C.G., and VanderWerf, P.A. 1992. A comparison of methods and sources for obtaining estimates of new venture performance. Journal of Business Venturing 7(2): 157-170.

Buhner, R. 1987. Assessing international diversification of West German corporations. Strategic Man- agement Journal 8:25-37.

Buckley, P.J., and Casson, M. 1976. The Future of the Multinational Enterprise. New York: Holmes and Meier.

Burrill, G.S., and Almassy, S.E. 1993. Electronics "93 The New Global Reali~. : Ernst & Young's Fourth Annual Report on the Electronics Industry. San Francisco: Ernst & Young.

Caves, R.E. 1971. International corporations: the industrial economics of foreign investment. Econom- ica 38(February): 1-27.

Child, J. 1972. Organizational structure, environment, and performance: the role of strategic choice. Sociology 6:2-12.

Collins, J.M. 1990. A market performance comparison of U.S. firms active in domestic, developed, and developing countries. Journal of International Business Studies 1:271-287.

Daniels, J.D., and Bracker, J. 1989. Profit performance: do foreign operations make a difference? Management International Review 29(1):46-56.

Dess, G.G., and Davis, P.S. 1984. Porter's (1980) generic strategies as determinants of strategic group membership and organizational performance. Academy of Management Journal 27(3):467-488.

Dunning, J.H. 1973. The determinants of international production. Oxford Economic Papers 25(Novem- ber):289-336.

Dunning, J.J. 1981. International Production and the Multinational Enterprise. London: George Allen and Unwin.

Freeman, J., and Boeker, W. 1984. The ecological analysis of business strategy. California Management Review 26(3):73-110.

Feeser, H.R., and Willard, G.E. 1990. Founding strategy and performance: a comparison of high- and low-growth, high-tech firms. Strategic Management Journal 11:87-98.

Fry, L.W., and Smith, D.A. 1987. Congruence, contingency, and theory building. Academy of Manage- ment Review 12:117-132.

Ghoshal, S. 1987. Global strategy: an organizing framework. Strategic Management Journal 8:425- 440.

Grant, A., Jammine, P., and Thomas, H. 1988. Diversity, diversification, and profitability among British manufacturing companies, 1972-1984. AcademyofManagementJourna131(4):771-801.

NEW VENTURE INTERNATIONALIZATION 37

Hambrick, D.C. 1981. Strategic awareness within top management teams. Strategic Management Journal 2:263-279.

Hambrick, D.C., and Lei, D. 1985. Toward an empirical prioritization of contingency variables for business strategy. Academy of Management Journal 28:763-788.

Hannan, M., and Freeman, J. 1977. The population ecology of organizations. American Journal of Sociology 32:929-964.

Hannan, M.T., and Freeman, J. 1984. Structural inertia and organizational change. American Sociologi- cal Review 49:149-164.

Hair, J., Anderson, R., Tatham, R., and Gradlowsky, R. 1979. Multivariate Data Analysis. Tulsa, OK: Petroleum Publishing Company.

Hirsch, S., and Lev, B. 1971. Sales stabilization through export diversification. Review of Economics and Statistics August:258-266.

Horst, T.E. 1973. Firm and industry determinants of the decision to invest abroad. Review of Economics and Statistics 54(August):258-266.

Hymer, S.H. 1976. The international operations of national firms: a study of direct foreign investment. Doctoral dissertation, MIT. Subsequently published by Cambridge, MA: MIT Press.

Johanson, J., and V ahlne, L. 1977. The internationalization process of the f i rm-A model of knowledge development and increasing foreign market commitment. Journal oflnternational Business Stud- ies 8(1):23-32.

Johanson, J., and Vahlne, J. 1990. The mechanism of internationalization. International Marketing Review 7(4): 11-24.

Karafakioglu, M. 1986. Export activities of Turkish manufacturers. International Marketing Review 3 (4): 34-43.

Keng, K.A., and Jiuan, T.S. 1989. Differences between small and medium sized exporting and nonex- porting firms: nature or nurture. International Marketing Review 6(4):27-40.

Kumar, M.S. 1984. Growth Acquisition and Investment: An Analysis of the Growth of Industrial Firms and Their Overseas Activities. Cambridge, U.K.: Cambridge University Press.

Lawley, D.N., and Maxwell, A.E. 1971. Factor analysis as a statistical method. New York: MacMillan.

Lee, C.S., and Yang, Y.S. 1990. Impact of export market expansion strategy on export performance. International Marketing Review 7(4):41-51.

Lessard, D. 1979. Transfer prices, taxes, and financial markets: implications of international financial transfers within the multinational corporation. International Business and Finance 1:101-135.

Lentz, R.T. 1981. Determinants of organizational performance: an interdisciplinary review. Strategic Management Journal 2:131-154.

Lindqvist, M.C. 1990. Critical success factors in the process of internationalization of small hi-tech firms. In Sue Birley, ed., Building European Ventures. New York: Elsevier.

Madsen, T.K. 1987. Empirical export performance studies: a review of conceptualizations and findings. In S.T. Cavusgil, ed., Advances in International Marketing, Vol. 2. Greenwich, CT: JAI Press, pp. 177-198.

Markides, C.C., and Ittner, C.D. 1994. Shareholder benefits from corporate international diversifica- tion: evidence from U.S. international acquisitions. Journal of International Business Studies 25(2):343-366.

McCarthy, A.M. 1992. The role of strategy, environment, resources, and strategic change in new venture performance. Unpublished dissertation. Purdue University.

McDougall, P.P. 1989. International versus domestic entrepreneurship: new venture strategic behavior and industry structure. Journal of Business Venturing 4:387--400.

McDougall, P.P. and Robinson, R.B. Jr. 1990. New venture strategies: an empirical identification of eight "archetypes" of competitive strategies for entry. Strategic Management Journal 11 (6):447- 468.

McDougall, P.P., Shane, S., and Oviatt, B.M., 1994. Explaining the formation of international new ventures: the limits of theories from international business research. Journal of Business Venturing 9(6) :469-487.

38 P.P. MCDOUGALL AND B.M. OVIATT

MacMillan, I.C., and Day, D.L. 1987. Corporate ventures into industrial markets: dynamics of aggres- sive entry. Journal of Business Venturing 2:29-39.

Michel, A., and Shaked, I. 1986. Multinational corporations vs. domestic corporations: financial performance and characteristics. Journal of International Business Studies 18(3):89-100.

Miller, A., and Camp, B. 1985. Exploring determinants of success in corporate ventures. Journal of Business Venturing 1:87-105.

Miller, D., and Mintzberg, H. 1983. The case for configuration. Beyond method. In Gareth Morgan, ed., Strategies for Social Research. Newbury Park, CA: Sage.

Miller, D., and Friesen, P.H. 1984. Organizations: A Quantum View. Englewood Cliffs, NJ: Prentice- Hall.

Mitchell, W., Shaver, J.M.. and Yeung, B. 1992. Getting there in a global industry: impacts on performance of changing international presence. Strategic Management Journal 13:419-432.

Mitchell, W., Shaver, J.M., and Yeung, B. 1993. Performance following changes of international presence in domestic and transition industries. Journal of International Business Studies 24(4): 647-669.

Newbould, G.D., Buckley, P.J., and Thurwell, J.C. 1978. Going International: The Experience of Smaller Companies Overseas. New York: Wiley.

Nunnally, J.C. 1978. Psychometric Theory. New York: McGraw-Hill. Ohmae, K. 1990. The Borderless World. USA: Harper Business.

O'Rourke, A.D, 1985. Differences in exporting practices, attitudes, and problems by size of firm. American Journal of Small Business 9(3):25-29.

Oviatt, B.M., and McDougall, P.P. 1994. Toward a theory of international new ventures. Journal of International Business Studies 25(1):45-64.

Porter, M.E. 1980. Competitive Strategy. New York: The Free Press. Porter, M.E. 1990. The Competitive Advantage of Nations. New York: The Free Press. Reich, R.B. 1991. The Work of Nations. New York: Alfred A. Knopf. Robinson, R.B., Jr., and Pearce, J.A., II. 1988. Planned patterns of strategic behavior and their

relationship to business-unit performance. Strategic Management Journal 9(1):43-60. Rossman, M.L. 1984. Export trading company legislation: U.S. response to Japanese foreign market

penetration. Journal of Small Business Management October:62-66. Rugman, A.M. 1979. International Diversification and the Multinational Enterprise. Lexington, MA:

Lexington Books. Schmidt, F.L., Hunter, J.E., and Pearlman, K. 1981. Task differences as moderators of aptitude test

validity in selection: a red herring. Journal of Applied Psychology 66:166-185. Seringhaus, F.H.R. 1993. Comparative marketing behavior of Canadian and Austrian high-tech export-

ers. Management International Review 33(3):247-269. Small Business in the American Economy. 1988. Washington, D.C.: U.S. Government Printing Office. Tesar, G., and Tarleton, J.S. 1982. Comparison of Wisconsin and Virginia small- and medium-sized

exporters: aggressive and passive exporters. In M.R. Czinkota and G. Tesar, eds., Export Management: An International Context. New York: Praeger, pp. 85-112.

Tsai, W.M., MacMillan, I.C., and Low, M.B. 1991. Effects of strategy and environment on corporate venture success in industrial markets. Journal of Business Venturing 6(1):9-28.

Tushman, M.L., and Romanelli, E. 1985. Organizational evolution: a metamorphosis model of conver- gence and reorientation. In L.L. Cummings and B.M. Staw, eds., Research in Organizational Behavior. Greenwich, CT: JAI Press, 7:171-222.

Turnbull, P.W. 1987. A challenge to the stages theory of internationalization process. In Philip J. Rosson and Stanley D. Reid, eds., Managing Export Entry and Expansion. New York: Praeger.

Tyebjee, T.T. 1990. The internationalization of high-tech ventures. Paper presented at 1990 Babson Entrepreneurship Conference, Wellesley, MA.

U.S. Department of Commerce. 1991. A Basic Guide to Exporting. Lincolnwood, IL: NTC Business Books.

Venkatraman, N., and Ramanujam, V. 1986. Measuring organizational performance in strategy re- search: a comparison of approaches. Academy of Management Review 11:801-814.

NEW VENTURE INTERNATIONALIZATION 39

Vernon, R. 1971. Sovereignty at Bay: The Multinational Spread of U. S. Enterprises. New York: Basic Books.

Vozikis, G.S., and Mescon, T.S. 1985. Small exporters and stages of development: an empirical study. American Journal of Small Business 9:49-64.

Welch, Lawrence S., and Loustarinen, R. 1988. Internationalization: evolution of a concept. Journal of General Management 14(2):34-55.

4 0 P.P. M C D O U G A L L A N D B.M. OVIATT

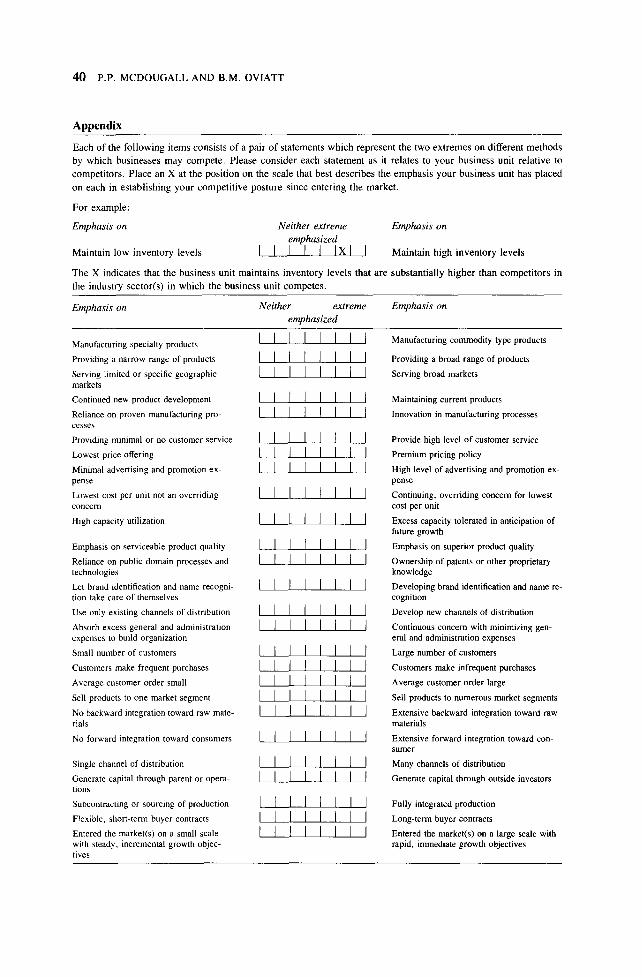

Appendix

Each of the fol lowing items consists o f a pair o f statements which represent the two extremes on different methods

by which businesses may compete . Please cons ider each statement as it relates to your business unit relative to

competi tors . Place an X at the posit ion on the scale that best describes the emphasis your business unit has placed

on each in establishing your competi t ive posture since entering the market .

For example:

Emphasis on Neither extreme emphasized

Maintain low inventory levels I I I r I I x l I

The X indicates that the business unit maintains inventory levels that are

the industry sector(s) in which the business unit competes .

Emphasis on

Maintain high inventory levels

substantial ly h igher than compet i tors in

Emphasis on Neither extreme Emphasis on emphasized

Manufacturing specialty products

Providing a narrow range of products

Serving limited or specific geographic markets

Continued new product development

Reliance on proven manufacturing pro- cesses

Providing minimal or no customer service

Lowest price offering

Minimal advertising and promotion ex- pense

Lowest cost per unit not an overridilag concern

High capacity utilization

Emphasis on serviceable product quality

Reliance on public domain processes and technologies

Let brand identification and name recogni- tion take care of themselves

Use only existing channels of distribution

Absorb excess general and administration expenses to build organization

Small number of customers

Customers make frequent purchases

Average customer order small

Sell products to one market segment

No backward integration toward raw mate- rials

No forward integration toward consumers

Single channel of distribution

Generate capital through parent or opera- tions

Sut~contracting or sourcing of production

Flexible, short-term buyer contracts

Entered the market(s) on a small scale with steady, incremental growth objec- tives

Manufacturing commodity type products

Providing a broad range of products

Serving broad markets

Maintaining current products

Innovation in manufacturing processes

Provide high level of customer service

Premium pricing policy

High level of advertising and promotion ex- pense

Continuing, overriding concern for lowest cost per unit

Excess capacity tolerated in anticipation of future growth

Emphasis on superior product quality

Ownership of patents or other proprietary knowledge

Developing brand identification and name re- cognition

Develop new channels of distribution

Continuous concern with minimizing gen- eral and administration expenses

Large number of customers

Customers make infrequent purchases

Average customer order large

Setl products to numerous market segments

Extensive backward integration toward raw materials

Extensive forward integration toward con- sumer

Many channels of distribution

Generate capital through outside investors

Fully integrated production

Long-term buyer contracts

Entered the market(s) on a large scale with rapid, immediate growth objectives