instructions and procedures - wells fargoretailservices.wellsfargo.com/instructions.pdf · these...

TRANSCRIPT

These Instructions and Procedures may be updated from time to time, and you are required to check the Online Resource Center located on our website at wellsfargo.com/retailservices on a monthly basis and as otherwise directed for any changes or updates. The current version of the Instructions and Procedures in effect is posted on the above referenced website. Your Agreement will be governed by the Instructions and Procedures posted at wellsfargo.com/retailservices as of the effective date of the posting.

Overview

These Instructions and Procedures: i. are effective as of the date specified above; ii. shall serve as a supplement to the Wells Fargo Retail Services General Dealer Agreement or other titled agreement

(hereinafter “Agreement”) by and between the Dealer (hereinafter “you,” “your,” or “Merchant”) and Wells Fargo Bank, N.A. (hereinafter “we,” “us,” “our,” or “Wells Fargo”); and

iii. are specifically incorporated into the terms of the Agreement. All capitalized terms used and not otherwise defined in Section 1 below or elsewhere in this Instructions and Procedures document shall have the meanings set forth in the Agreement.

These Instructions and Procedures are not an exhaustive list of your obligations under our Agreement but are designed to assist you in complying with our requirements, processes and procedures in connection with the Program. This document was designed for your complete review initially and contains features which allow you to search specific topics as you have questions about the Program. As such, certain key concepts are repeated in multiple sections of the document when the concept applies to more than one topic.

Instructions and ProceduresSupplement to The Wells Fargo Retail Services General Dealer Agreement

Effective March 13, 2018 – Updated with Version 6*Certain Programs may have customized portions of these Instructions and Procedures. Please contact Client Processing for more information.

Contact us

Unless otherwise noted in a particular section, if you have questions about the information contained in this Instructions and Procedures document contact our Client Processing Department.

Client Processing Department

1-800-551-5111Monday – Saturday, 8:00 a.m. – 10:00 p.m. Central Time

Sunday, 10:00 a.m. – 10:00 p.m. Central Time

Confidential: These Instructions and Procedures contain confidential information.Intended for use by the identified parties on the Agreement only. Not for consumer use.© 2018 Wells Fargo Bank, N.A. All rights reserved. [I and P Document V 6.0 03/2018]

Page 2Wells Fargo Bank, N.A. — Instructions and Procedures | Effective March 13, 2018

Transparency PrinciplesWells Fargo promotes full transparency and clear disclosure of all financing terms as described in the Credit Terms and Special Terms sections of these Instructions and Procedures. It is imperative that you understand the key features of the Credit Card Program (“Program”) and communicate them effectively to all consumers, applicants and Cardholders.

• The Program offers consumers the ability to finance purchases from you via the use of a Card and should be described as a Credit Card Program. Approved Cardholders will receive a Card in the mail within 14 calendar days of the credit decision.

• The Card accesses a revolving line of credit that can be used for future purchases for personal, family, or household use up to the available credit limit.

• The Program is not an in-house payment or billing plan from you. The Card is issued and serviced by Wells Fargo Bank, N.A.

• You will ensure that your employees who discuss the Program with consumers receive initial and ongoing training on the requirements of the Program. Please see Section 3 of this document regarding additional training requirements.

• The Credit Card Agreement must be furnished with the Consumer Credit Card Account Application to the consumer(s) at the time the consumer expresses an interest in applying for an Account. You should recommend that he/she read the Credit Card Agreement thoroughly.

• Before submitting the Consumer Credit Card Account Application for processing, the applicant(s) must agree to apply for an Account under the Program and sign an acknowledgement evidencing receipt of the Credit Card Agreement in accordance with your processing method.

The Card carries an Annual Percentage Rate (APR) based upon when it was opened and is not an interest- free credit card. However, special (promotional) terms may be offered. The No Interest if Paid in Full promotion (deferred interest) accrues the regular APR for Purchases on the Cardholder’s purchase balance during the promotional period. In order to avoid interest charges, the Cardholder must pay off the purchase balance before the end of the promotional period.

If the Cardholder only makes the minimum monthly payment each month, he/she will not pay off their purchase balance during the promotional period. He/she will either need to pay more than the minimum monthly payment each month or make a lump sum payment(s) before the end of the promotional period. It is very important that your employees understand and explain this and all credit terms described on your Price Sheet to Cardholders.

Cardholders should only be charged after their transaction is completed. A transaction is completed after you have performed all of your obligations to the Cardholder, including delivery of the goods and/or performance of any service.

You agree to have an expedited business process in place to promptly investigate and provide a full and complete response to Cardholder complaints and billing disputes received either directly from Cardholders or from us. If a Cardholder or consumer complains to you about Wells Fargo, you will provide the Cardholder or consumer’s contact information (name, address, and telephone number) and concerns to Wells Fargo through Client Processing for review and response.

You agree to establish and maintain a fair and uniform policy for exchange, cancellation and/or return of Products sold under a Card sale and to give credit upon each such return by issuance of a Credit Memo (never in cash).

Unless otherwise directed by us, Consumer Credit Card Account Applications must be sent into Wells Fargo for retention. If you are allowed to retain Consumer Credit Card Account Applications, you must retain for seven (7) years from the date of creation and store securely to prevent unauthorized access to confidential Cardholder information. You must also keep them in an orderly manner for quick retrieval when we request documents from you.

Wells Fargo reserves the right to monitor your adherence to your Agreement and our Instructions and Procedures. Merchants and Providers who violate these documents may be subject to chargebacks as well as to termination.

Page 3Wells Fargo Bank, N.A. — Instructions and Procedures | Effective March 13, 2018

Credit TermsIt is critical that you understand the credit terms offered in connection with the Program and clearly explain the requirements and differences to the consumer. Consumers will receive regular terms unless special terms are offered. This means that the APR for Purchases (also referred to as the regular rate) will be used to calculate interest on the purchase balance, and Regular Payment Terms will be required. The payment for balances with Regular Payment Terms will be the greater of: (1) $40.00; (2) 3.50% of the highest combined balance; or (3) the sum of interest charges for balance(s) on Regular Payment Terms, fees assessed during the current Billing Cycle, and 1% of the combined balance. All credit terms (including special terms) require monthly payments. Consumers may pay their outstanding Account balance in full at any time without a pre-payment penalty.

Special TermsBelow are descriptions of the types of special terms promotions that are currently available under the Program. Please refer to your Price Sheet and currently effective pricing communications for a list of the special terms available under your Program.

SPECIAL INTEREST TERMS Wells Fargo offers the following types of special interest terms. If one of these special interest terms applies to a purchase, the Invoice must contain the proper special interest terms disclosure (see Exhibit A).

• No Interest if Paid in Full. This special terms plan is also referred to within the industry as “Deferred Interest” plans. Key attributes of this plan include the following: › The Annual Percentage Rate (“APR”) for Purchases is

used to calculate interest on the purchase balance from the date of the original transaction and throughout the special terms (promotional) period. This amount is called the deferred interest charge.

› To avoid paying any interest, a Cardholder must pay off the entire purchase balance in full on or before the special terms end date.

› If the Cardholder does not pay off the purchase balance by the end of the special terms period, the deferred interest from the date of the original transaction will be added to the remaining balance, and the APR for Purchases will continue to apply until the purchase balance is paid in full.

If you have questions regarding the special terms available under your Program, please contact Wells Fargo Client Processing. The Client Processing Department is available Monday through Saturday 8:00 a.m. to 10:00 p.m. and Sunday 10:00 a.m. to 10:00 p.m. Central Time at 1-800-551-5111.

› Paying only the regular payment amount each month will not pay off the No Interest if Paid in Full purchase balance during the special terms period.

› Monthly payments must be made each month. The revolving account may not be paid ahead. However, the No Interest if Paid in Full purchase balance can be paid by larger monthly payments or by one large payment which we receive on or before the special terms end date.

› The special terms end date may be different than the Cardholder’s payment due date.

• Special Rate. This special terms plan is also referred to as “Reduced Rate” plans. Key attributes of this plan include the following: › The APR shown on the Invoice will be used to calculate

interest on the purchase balance from the date of the original transaction and will apply until the purchase balance is paid in full. Special Rate plans begin as low as 0.00% APR.

SPECIAL PAYMENT TERMSWells Fargo also offers the following types of payment terms. The Invoice must indicate which payment term applies to the purchase (see Exhibit A).

• Payment in Full/Equal Payments. The payment will be the amount required to pay the initial purchase balance shown on the Cardholder’s monthly billing statement in full during the special terms period.

• Custom Payments. The payment is a set dollar amount or a fraction (e.g., 1/30, 1/40, etc.) or percent (e.g., 2.00%, 3.00%, etc.) of the highest balance for the particular credit promotion. The payment will not change unless the balance increases above the previous high balance.

Page 4Wells Fargo Bank, N.A. — Instructions and Procedures | Effective March 13, 2018

Table of contentsOverview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Transparency Principles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Credit Terms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Special Terms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Section 1: Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Section 2: Fair and Responsible Lending Principles . . . . . 6

Section 3: Training . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Section 4: Advertising Credit . . . . . . . . . . . . . . . . . . . . . . . . . 7

Section 5: Offering Credit . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Section 6: New Cardholder Accounts (taking a Consumer Credit Card Account Application) . . . . . . . . 7

Section 7: Processing Consumer Credit Card Account Applications for New Cardholder Accounts . . . . . . . . . . . 9

Section 8: Receiving the Credit Decision and Communicating to the Applicant(s) . . . . . . . . . . . . . . . . . . 9

Section 9: Requesting a Credit Limit Increase . . . . . . . . . 10

Section 10: Obtaining an Authorization for a Purchase . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Section 11: Canceling an Authorization for a Purchase . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Section 12: Completing an Invoice . . . . . . . . . . . . . . . . . . . . 11

Section 13: Presenting an Invoice for Processing. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Section 14: Presenting a Credit on an Account . . . . . . . . 14

Section 15: Mailing in Completed Consumer Credit Card Account Applications and Important Terms of Your Credit Card Account Forms to Wells Fargo for Retention . . . . . . . . . . . . . . . . . . . 14

Section 16: Sending Documentation to Wells Fargo Upon Request . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Section 17: Retention of Program Materials . . . . . . . . . . . 15

Section 18: Destruction of Invoices and Credit Memos . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Section 19: Information Security . . . . . . . . . . . . . . . . . . . . . 16

Section 20: Passing Along the Costs of Financing . . . . . 17

Section 21: Sales Practices . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Section 22: Extended Product Warranties and Service Agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Section 23: Cardholder Payments . . . . . . . . . . . . . . . . . . . . 18

Section 24: Audits/Examinations of Book and Records . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Section 25: Notifying Us of Changes in Your Legal Name, Taxpayer Identification Number, Legal Ownership, Legal Entity Status, Number of Store Locations, Product Offerings, etc. . . . . . . . . . . . . 19

Section 26: Funding for Transactions . . . . . . . . . . . . . . . . . 19

Section 27: Wells Fargo’s Right to Reject or Revoke Acceptance of an Invoice . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Section 28: Cardholder Complaints and Billing Disputes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Section 29: Conducting Transactions in Languages other than English . . . . . . . . . . . . . . . . . . . . . . . .20

Section 30: Fraud . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20

Section 31: Power of Attorney . . . . . . . . . . . . . . . . . . . . . . . .20

Section 32: Internal Revenue Service 1099-K Reporting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Section 33: Americans with Disabilities Act — Effective Communication for Individuals with Disabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Section 34: Collection of Personal/Identification Information when Accepting a Card . . . . . . . . . . . . . . . . 22

Section 35: Sharing Cardholder Information for Marketing Purposes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Section 36: Consumer Credit Card Account Applications and Transactions Over the Telephone .. . .22

Section 37: Internet Shopping Cart Transactions . . . . . .22

Section 38: Kiosk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22

Section 39: Email Distribution of the Program Materials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22

Exhibit A . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .23

Page 5Wells Fargo Bank, N.A. — Instructions and Procedures | Effective March 13, 2018

Section 1: Definitions

Notwithstanding any provision in the Agreement to the contrary, the following definitions shall have their corresponding meanings when used within this Instructions and Procedures document.

i. “Account” is defined as a Cardholder’s credit card Account owned by us and utilized by the Cardholder for making purchases from you under the Program.

ii. “Account Number” is defined as a unique identification number assigned by us to an Account issued to a Cardholder.

iii. “Annual Percentage Rate (APR)” is defined as a measure of the cost of credit, expressed as a yearly rate.

iv. “Authorization” is defined as a reserve placed on a Cardholder’s credit limit by a Merchant.

v. “Card” is defined as a card with an Account Number issued to a Cardholder for use in connection with the Program.

vi. “Cardholder” is defined as a consumer customer that has applied for and has been approved for an Account.

vii. “Cardholder Account Information” is defined as any personal information about any applicant or co- applicant or any Cardholder received in connection with an Account or potential Account including that information found in, on or with a Consumer Credit Card Account Application for or through Card use, or is obtained from us, including but not limited to, the applicant and co-applicant’s name, address, Social Security number, date of birth, income information, Account Number, Account limits and Account balances and Account activity.

viii. “Credit Card Agreement” is defined as a written agreement between us and the Cardholder containing terms and conditions that govern the Account. Any changes to the Credit Card Agreement shall be solely made by Wells Fargo.

ix. “Consumer Credit Card Account Application” is defined as an application for an Account under the Program, in either written or electronic format, which may include but not be limited to any documents relating to a Consumer Credit Card Account Application that upon completion of and presentment to us represents such consumer’s desire to open an Account and their consent to undergo financial review. Such Consumer Credit Card Account Application shall include all documents containing the terms, conditions and disclosures governing such applications as provided for by Law, and shall be owned and governed by us.

x. “Credit Memo” is defined as evidence of a credit given for the cancellation and/or return of Products

regarding a previously presented Invoice, in paper or electronic form, or any other such adjustment or credit by you to an Account.

xi. “Initial Disclosures” are defined as a disclosure or set of disclosures that you shall provide to each Cardholder at the time of Account opening in a manner and method determined by us in accordance with these Instructions and Procedures. Such Initial Disclosures shall include, without limitation, the Truth in Lending disclosures and any other disclosures as determined by us in accordance with applicable Law.

xii. “Internet Processing System (IPS)” is defined as our proprietary Internet Processing System which may be used to electronically transmit Consumer Credit Card Account Applications, Invoices, and Credit Memos for processing.

xiii. “Invoice” is defined as evidence of a Card sale in paper or electronic form for Products purchased from you and shall include any and all other documents referred to in the Invoice.

xiv. “Law” or “Laws” is/are defined as all United States federal, state and local laws, regulations, rules, and ordinances, including but not limited to, the Fair Credit Reporting Act, the Truth in Lending Act, all applicable fair lending laws and regulations, the Federal Equal Credit Opportunity Act, as amended, and Section 5 of the Federal Trade Commission Act (FTC Act) — Unfair, Deceptive or Abusive Acts or Practices Regulation — and all state law counterparts of such, and all applicable regulations promulgated under these laws.

xv. “Price Sheet” is a document setting forth the credit term plans available under the Program and the discount rates on special interest terms and the administrative fees charged by us in connection with the Program.

xvi. “Products” are defined as any good, service, or merchandise that you offer, sell or provide that has not otherwise been prohibited under the Agreement or that requires our prior approval as may be noted in the Agreement.

xvii. “Program” is defined as the Card program that is contemplated by the Agreement for the purpose of arranging financing of your consumer customers’ purchases.

xviii. “Program Materials” are defined as any documents used in connection with the Program including documents that contain Cardholder Account Information which may include, but not be limited to, Consumer Credit Card Account Applications, Invoices and Credit Memos.

Page 6Wells Fargo Bank, N.A. — Instructions and Procedures | Effective March 13, 2018

Section 2: Fair and Responsible Lending Principles

Wells Fargo is committed to making financial services available to consumers on a fair and consistent basis. As a participant in this Program, we expect you to share this commitment both in words and actions. Wells Fargo’s vision is to satisfy our customer’s financial needs and help them succeed financially. Consistent with this vision, Wells Fargo is firmly committed to being a responsible provider of consumer credit in all of our markets.

Wells Fargo extends credit according to the following affirmative responsible lending practices:

• We provide our customers with the information they need to make fully informed decisions about our credit products and services.

• We price our credit products and services based on appropriate factors, including the risk and cost of extending credit, competition and marketplace strategy and conditions, and safety and soundness considerations.

• We only approve Consumer Credit Card Account Applications where we believe the borrower has the ability to repay the credit according to its terms, using a method of assessment appropriate to the type of credit transaction.

• We provide timely responses to consumer questions and complaints, and take prompt corrective action if we have made an error.

Commitment to fair and responsible lending is good business and a basic responsibility of Wells Fargo, its Merchants participating in the Program, as well as all employees of both businesses. As a participant in the Program, you are required to adhere to these same principles in the manner in which you conduct your business.

✓ DO offer credit to all consumers fairly and consistently.

✓ DO advertise Products and services in a non- discriminatory manner that is designed to inform and attract a diverse customer base.

✓ DO ensure consumers have all disclosures and information to make an informed decision about the Products being purchased and with regard to utilizing the Program to finance the purchase.

✓ DO promptly respond to consumer questions and complaints and resolve all consumer issues in a fair and consistent manner.

Section 3: Training

We will make resources available to assist you with training your employees regarding the Program and compliance requirements associated with the Program.

You will designate one or more employees at the appropriate levels and departments within your business to be our primary point of contact for training purposes (“Training Contact(s)”). Your Training Contact(s) will, from time to time, help us with training related efforts in connection with the Program, including but not limited to, helping us coordinate the dissemination of training materials, exchanging information with us regarding your training process or materials, and we may also request that such Training Contact(s) attend required training offered by us in connection with the Program.

Your Training Contact(s) is required to attend on- boarding training facilitated or managed by our training team prior to using the Program.

You will maintain a training process to educate your employees on an ongoing basis regarding the provisions set forth in the Agreement, and/or these Instructions and Procedures, and acknowledge such training programs upon our request. In addition, Wells Fargo will conduct an annual review of any training materials and/or processes you may maintain related to the Program and your Training Contract(s) will assist us in the coordination and facilitation of such annual review. In the event you have not created your own independent training materials for the Program, we will provide you with standard pre-approved materials or work with you to create customized training materials to be used in connection with the Program.

You will promptly notify us in the event your Training Contact(s) leaves your place of employment or switches roles within your business. You will identify a replacement Training Contact for this role.

✓ DO designate and maintain experienced employee(s) as your Training Contact(s) to serve as our primary point of contact for training purposes regarding the Program.

✓ DO ensure all employees, who assist with the promotion of the Program, present Consumer Credit Card Account Applications, complete Invoices or submit transactions to us in connection with the Program, are properly trained on the requirements of the Program.

✓ DO conduct regular training of your employees regarding the requirements of the Program to ensure all employees, including new employees, receive consistent training and the most up to date information regarding the Program.

Page 7Wells Fargo Bank, N.A. — Instructions and Procedures | Effective March 13, 2018

Section 4: Advertising Credit

Specific credit advertising requirements are found in the Truth in Lending Act (TILA) and it’s implementing federal Regulation Z. Federal and State Unfair, Deceptive or Abusive Acts or Practices Laws require advertisements to fairly and accurately state the terms of the offer and not be false or misleading. These requirements apply to all persons and businesses that advertise consumer credit transactions. To help us comply with applicable Law, you are required to follow the Advertising Guides when creating advertisements which mention the Program (print ads, online, in-store signage, email or direct mail, broadcast, et al). The Advertising Guides are located on the Marketing tab of the Online Resource Center at wellsfargo.com/retailservices. All advertising which references our Program must comply with applicable Law and our Advertising Guides. From time to time we may request that you submit proposed advertising for our review prior to its publication.

✓ DO regularly check the Advertising Guides located on the Marketing tab of the Online Resource Center at wellsfargo.com/retailservices or as otherwise provided to you from time to time for updates to our advertising requirements.

✓ DO regularly check your existing advertising against the Advertising Guides and make any necessary updates. Note that different promotions (e.g., No Interest if Paid in Full vs. 0% APR) and different mediums (e.g., a print ad vs. your website) have different requirements. For example, APRs and other credit card terms may change from time to time.

✓ DO explore and utilize the Downloadable Web Banners available on the Marketing tab of the Online Resource Center at wellsfargo.com/retailservices.

Section 5: Offering Credit

• You will fairly and consistently offer all consumers the opportunity to apply for credit under the Program.

• You will ensure that your employees respond accurately and consistently to questions from consumers about the availability of financing and/or the ability to complete a Consumer Credit Card Account Application under the Program.

• Do not discourage any consumer from applying for credit in any way or for any reason.

• Do not attempt to determine a consumer’s credit worthiness before providing the consumer the opportunity to apply for credit under the Program.

You will not discriminate against any consumer for any reason including, but not limited to, any basis prohibited by Law. Under the Law, prohibited basis includes race, color,

religion, national origin, sex, marital status, age (provided the consumer has the capacity to contract), because all or part of the consumer’s income derives from any public assistance program, or because the consumer has in good faith exercised any right under the Consumer Credit Protection Act.

You will offer equal access to all current consumer financing promotions available to all consumer customers when purchasing like or similar Products of similar cost to the Cardholder.

✓ DO encourage all consumers to apply for an Account under the Program.

✓ DO submit all Consumer Credit Card Account Applications to us for processing and a credit decision.

✕ DON’T discourage any consumer from applying for an Account under the Program (e.g., through oral statements, delays, body language, etc.).

✕ DON’T charge any sort of application fee, processing fee or similar fee in connection with the taking or processing of a Consumer Credit Card Account Application.

✕ DON’T require optional protection plans or service plans as a condition of obtaining financing.

Section 6: New Cardholder Accounts (taking a Consumer Credit Card Account Application)

We will provide training materials which describe how to use the processing method applicable to your use of the Program. In addition to those training materials, follow these requirements when taking a Consumer Credit Card Account Application:

• Use only Consumer Credit Card Account Applications, Credit Card Agreements and related materials provided by us.

• Consumers must be provided a current version of the Credit Card Agreement (which includes the Initial Disclosures) at the time they apply. Do not make or use photocopies of paper applications.

• Applicants and co-applicants must be 18 years of age or older to apply. Applications for young consumers under the age of 21 must be in writing (electronic applications with the appropriate E-sign consent constitute “in writing”).

• Consumers may choose to apply individually or jointly. If they choose to apply jointly, both applicants must be available to agree to apply for an Account and to acknowledge receipt of the Credit Card Account Agreement in accordance with your processing method.

Page 8Wells Fargo Bank, N.A. — Instructions and Procedures | Effective March 13, 2018

• The applicants must provide all information requested on the Consumer Credit Card Account Application.

• The USA Patriot Act requires that we obtain each applicant’s full legal name, date of birth, taxpayer identification number (which for a consumer is his or her Social Security Number) and physical address. A post office box is not a sufficient physical address; however, it may be provided on the second line of the address field. Military addresses (APO/FPO) are acceptable.

• Each applicant is required to sign (either electronically or in physical form depending upon the process) acknowledging that they have read, agreed to, and are in receipt of, the terms of the Credit Card Agreement (which includes the Initial Disclosures and Arbitration Agreement) and the Privacy Notice. This acknowledgment could be located on the Consumer Credit Card Account Application, or other document depending upon your processing method.

• Applications may not be submitted for principals, officers, directors, managers or owners of your business.

• Married Wisconsin residents applying individually or jointly with someone other than their spouse are required to contact us immediately at 1-855-412-2787 between 8:00 a.m. and 6:00 p.m. Central Time to provide us with the name and address of their spouse. We are required by Law to inform the Wisconsin Applicant’s spouse that they have opened an Account with us.

• Net Annual Income is a required field. An applicant need not list income from alimony, child support, or separate maintenance payments unless he or she wishes to have it considered as a basis for repaying the obligation. An applicant may include income that he or she earns, owns, including funds regularly deposited into accounts he or she owns. If the applicant is age 21 or older, he or she may also include accessible income which is not earned or owned by him or her but is regularly accessed or used to pay his or her expenses.

• Each signature (whether physical or electronic) must be legally enforceable, which means that the consumer(s) is of sound mind and not under duress or undue influence at the time of signing (See Section 31 for additional information regarding use of a Power of Attorney).

• Provide the applicant(s) with a copy of the Credit Card Agreement (which includes the Initial Disclosures and Arbitration Agreement) and Privacy Notice in a form that they can keep prior to processing the Consumer Credit Card Account Application (Note: you only need to provide one Credit Card Agreement to joint applicants).

• If available, the Consumer Internet Application (e.g., At Home Internet Application) is intended to be completed by a consumer when choosing to apply for a Credit Card Account using the consumer’s equipment. The Consumer

Internet Application is not intended to be completed on a Merchant’s computer, laptop, tablet, or other mobile device, because the Consumer must be able to print or save a copy of the Credit Card Agreement for their records.

• For your own protection against fraud, verify each applicant’s identity by asking for a state or federal form of unexpired photo ID such as a driver’s license, passport, military ID, tribal identification card, or similar document, or other acceptable identification method that allows you to form a reasonable belief that you know the identity of the applicant(s). Confirm that the signature(s) acknowledging receipt of the Credit Card Agreement matches the ID(s).

• Forward all completed Consumer Credit Card Account Applications to us for retention within 15 days of the credit decision pursuant to Section 15 “Mailing in Completed Consumer Credit Card Account Applications and Important Terms of your Credit Card Account Forms to Wells Fargo for Retention.”

✓ DO ensure that the consumer understands he or she is applying for a Card issued by Wells Fargo.

✓ DO only allow employees with a business need to know access to Cardholder Account Information (including during the processing of Consumer Credit Card Account Applications).

✓ DO verify that the applicant’s and co-applicant’s (if applicable) signature matches their ID.

✓ DO ensure that the applicant(s) receive a copy of the Credit Card Agreement, Initial Disclosures, and Privacy Notice in a form that they can keep prior to processing the Consumer Credit Card Account Application.

✕ DON’T take a Consumer Credit Card Account Application over the telephone for a consumer, unless otherwise permitted in your Agreement or Addendum. There are separate detailed Instructions and Procedures outlining this process, see Section 36.

✕ DON’T submit an application for consideration that has been denied by another lender.

✕ DON’T use another lender’s application and disclosures when submitting a Consumer Credit Card Account Application to us.

✕ DON’T use our Consumer Credit Card Account Application, Initial Disclosures, or Cardholder Account Information with any other lender’s credit program.

✕ DON’T increase the purchase price of any Product or add any application or other fee for financing.

Page 9Wells Fargo Bank, N.A. — Instructions and Procedures | Effective March 13, 2018

Section 7: Processing Consumer Credit Card Account Applications for New Cardholder Accounts You will submit the Consumer Credit Card Account Application information for a credit decision using a processing method reviewed and approved by Wells Fargo. We will provide training materials which describe how to use the processing method applicable to your use of the Program.Wells Fargo reserves the right to make changes to how Consumer Credit Card Account Application information is submitted and processed at any time.By submitting a Consumer Credit Card Account Application for processing you confirm the applicant has:

• agreed to apply for an Account under the Program and

• received and agreed to the current version of the Credit Card Agreement, Initial Disclosures, and other documentation provided to you by us for use with the Program.

Any and all information provided by the applicant(s) must be accurately entered into the processing system as written and/or provided by the applicant during the application process.

✓ DO ensure you are using the most recent version of the Consumer Credit Card Account Application and Credit Card Agreement.

✓ DO encourage applicants to submit only accurate information.

✓ DO accurately submit all information provided by the applicant(s) in connection with the Consumer Credit Card Account Application, including Net Annual Income amount(s).

✓ DO accurately respond to any system prompts you may receive when submitting a Consumer Credit Card Account Application.

✓ DO verify the identity of all applicants before submitting the Consumer Credit Card Account Application for processing. You are responsible for all transactions that we deem in our sole discretion to be fraudulent. See Section 30 for more information.

✕ DON’T use the Program to process Consumer Credit Card Account Applications which were not obtained or performed directly by your business or legal entity (e.g., you cannot broker or submit Consumer Credit Card Account Applications on behalf of another business).

✕ DON’T discourage any consumer from applying for an Account under the Program.

Section 8: Receiving the Credit Decision and Communicating to the Applicant(s)After submitting a completed Consumer Credit Card Account Application in accordance with Section 7, you generally will receive information as to whether the Consumer Credit Card Account Application is approved or denied within seconds. These credit decisions must be immediately communicated to the applicant(s). Consumer Credit Card Account Applications requiring review by the Credit team or Investigations team will require additional time and may result in us needing additional information from the applicant(s).

APPROVED APPLICATIONS An approved response may include the Cardholder’s name, Account Number, and credit limit granted. The Cardholder will receive his or her Card in the mail within 14 calendar days of the credit decision. The credit limit is available to use as soon as it is communicated to the new Cardholder.

PENDING APPLICATIONS Some applications may require review by Wells Fargo’s Credit or Investigations team. Reasons for a pending decision may include:

• a fraud alert on the consumer’s credit report;

• Consumer Credit Card Account Application information that does not match the information obtained from the credit bureau; or

• data entry errors.

TO HELP ELIMINATE PENDING DECISIONS

✓ DO review the Consumer Credit Card Account Application information prior to submitting it to make sure there are no misspellings or input errors. There should be no special characters, symbols or extra punctuation marks.

✓ DO ensure that all fields are entered completely and accurately when entering the Consumer Credit Card Account Application information into the designated application processing technology. You will receive a quicker response with a more accurate decision.

✓ DO confirm that all information is complete for the co-applicant if it is a joint application.

✕ DON’T enter the co-applicant’s name on the same line as the primary applicant, i.e., Doe, John/Jane.

✕ DON’T advise a consumer of a credit decision until received.

Page 10Wells Fargo Bank, N.A. — Instructions and Procedures | Effective March 13, 2018

If the applicant’s decision is still pending after 15 minutes, you may check the status of the application by calling our Client Processing Department at 1-800-551-5111, Option 1, or by checking the status of the decision on IPS if the IPS processing method was used to submit the Consumer Credit Card Account Application.

DECLINED APPLICATIONS

If the applicant is not approved for credit, he or she will receive a letter from Wells Fargo Bank, N.A. within 30 days of the credit decision. As required by Law, the letter outlines the reasons for the denial. Due to the privacy of our applicant’s personal financial information, we cannot provide you with the reason(s) for the turn down.

We suggest the following talking points when communicating to the consumer the application was not approved:

• Wells Fargo Bank, N.A. is unable to approve your application for credit.

• In the next 30 days you will receive a letter directly from Wells Fargo Bank, N.A. describing the reasons they did not approve your application.

• Would you like to discuss other payment options?

Section 9: Requesting a Credit Limit Increase

A credit limit increase can be requested if the credit limit granted is not enough to meet the Cardholder’s financing needs. This generally occurs in two scenarios: i) the credit line granted when the Consumer Credit Card Account Application was initially submitted for credit approval is insufficient to cover the Cardholder’s desired purchase(s), or ii) there is not enough available credit at the time a Cardholder wishes to make an additional purchase using the Card.

If the credit line granted when the Consumer Credit Card Account Application was initially submitted for credit approval is insufficient to cover the Cardholder’s desired purchase(s), ask the Cardholder if he or she has additional information the Cardholder would like to have considered and whether the Cardholder would like to request a credit limit increase. The Cardholder must affirmatively consent to requesting a credit limit increase before it can be submitted for processing.

When you ask for the Cardholder’s Net Annual Income in connection with the credit limit increase, the following disclosure must be read to the Cardholder by you or you must present the disclosure to the Cardholder to read prior to submitting a request for a credit limit increase (no exceptions):

“You need not list income from alimony, child support, or separate maintenance payments unless you wish it considered as a basis for repaying this obligation. You may include income that you earn or own, including funds regularly deposited into accounts you own. If you are age 21 or older, you may also include accessible income which is not earned or owned by you but is regularly accessed or used to pay your expenses.”

If a Cardholder wishes to use his or her Card for an add-on purchase but there is not enough available credit, ask the Cardholder if he or she would like to request a credit limit increase. The Cardholder must affirmatively consent to requesting a credit limit increase before it can be submitted for processing.

If the Cardholder requesting the credit limit increase is under the age of 21, the request must be submitted to us in writing. In addition, any co-borrower that is 21 years of age or older who assumed liability at the time of account opening must agree in writing to assume liability on the increase.

To request a credit limit increase contact Client Processing’s Interactive Voice Response (IVR) system at 1-800-551-5111 (Option 6) or sign on to the Online Resource Center, select the Internet Processing System tab, and submit an account inquiry. An option to submit a credit limit increase is located on the left-hand navigation bar.

✓ DO ensure the Cardholder consents to requesting a credit limit increase before submitting it for processing.

✓ DO round the new credit limit requested to the next higher hundred dollar increment (e.g., a credit limit request of $2,685.00, should be rounded to a credit limit request of $2,700.00).

✓ DO allow 15 minutes to receive a response prior to calling Client Processing for a status update.

✓ DO verify the Cardholder’s identity and date of birth prior to requesting a credit limit increase.

✓ DO submit the request in writing if the Cardholder is under the age of 21.

Page 11Wells Fargo Bank, N.A. — Instructions and Procedures | Effective March 13, 2018

Section 10: Obtaining an Authorization for a Purchase

An Authorization reserves a portion of a Cardholder’s credit line for a purchase from your business and is used when the funding of a transaction will not occur on the same day as the commitment to purchase. An Authorization will not place the transaction on the Account for funding nor begin a Cardholder’s promotional terms or monthly billing.

We recommend you obtain an Authorization for all transactions in which you are not funding the transaction on the same day as the Cardholder commits to financing a purchase using the Card. Authorizations should only be obtained when there is a commitment to buy on the part of the Cardholder. The Authorization should be in an amount equal to the dollar amount which the Cardholder has committed to purchase and finance.

The Agreement addresses the length of time an Authorization is valid in the section entitled “Sales Transactions.” The section also describes the circumstances under which we may change pending Authorizations.

An Authorization may be obtained through your usual method of processing.

Section 11: Canceling an Authorization for a Purchase

If a Cardholder cancels the transaction or changes are made to a Cardholder’s initial Authorization, you must cancel your original Authorization number. To cancel an Authorization, contact Client Processing at 1-800-551-5111, Monday through Saturday from 8:00 a.m. to 10:00 p.m. or Sunday from 10:00 a.m. to 10:00 p.m. Central Time. If the Authorization was obtained via the Online Resource Center (ORC), you may cancel the Authorization by logging into the ORC and selecting the Internet Processing System tab > Cancel an Authorization.

Section 12: Completing an Invoice

An Invoice must be completed for each Card purchase. A Cardholder must open an Account or present a valid Account Number at the time of sale. Unless already known, you must confirm the Cardholder’s identity prior to completing an Invoice for an Account. Invoices submitted to Wells Fargo are to be used for personal, family, or household use only.

You must use a Wells Fargo approved Invoice for all sales transactions. Only Cardholders who are authorized on the Account may make purchases. If it is a joint Account, either Cardholder can use the Account and only one of the Cardholders is required to sign the Invoice. Any

documentation you provide to the Cardholder in connection with the transaction must not conflict with the Wells Fargo approved Invoice.

We offer a separate training piece for complete details on how to complete a manual Invoice. The Wells Fargo approved Invoice evidencing the Card transaction must include at a minimum the following information:

• Merchant name and address;

• Cardholder name;

• Description of the Products and services being purchased (the description of a purchase may be provided in another document referenced in the Invoice). › If a model number is used it should be preceded by

the word “model” and if a description is on a separate invoice, please note “See attached Invoice # (include number).”

• Net amount of sale (amount to be charged on the Card). › The net amount of sale is the amount Wells Fargo will

place on the Cardholder’s Account.

• Wells Fargo approved credit terms (e.g., special financing terms);For example: If the Cardholder is making a purchase with No Interest if Paid in Full within 12 months with regular monthly payments special terms, the Invoice must properly disclose the following: › No Interest if Paid in Full within 12 months with regular

monthly payments. If the purchase balance is not paid in full within 12 months, interest will be charged to your Account from the purchase date at a rate of XX.XX% (Note: insert proper APR for XX.XX%).

› See Exhibit A for a list of example special terms descriptions. See your Price Sheet, or currently effective pricing communications for a list of which special terms plans are available under your Program.

• Last four digits of the Account Number.

• The Wells Fargo purchase money security interest language: “This transaction is under your Credit Card Agreement with Wells Fargo Bank, N.A. (the “Bank”). You give the Bank a purchase money security interest in goods purchased in this transaction.”

• Cardholder signature and date.

A Cardholder must be given and be able to retain an exact or like copy containing all required attributes of the Invoice as listed above for their records.

✓ DO verify Cardholder identity prior to completing an Invoice for repeat purchases.

✓ DO provide a complete and detailed description of the Products and Services being purchased.

Page 12Wells Fargo Bank, N.A. — Instructions and Procedures | Effective March 13, 2018

✓ DO use a Wells Fargo approved Invoice and ensure all fields are legible.

✓ DO ensure complete and accurate special terms disclosures are provided on the Invoice.

✓ DO ensure the amount reflected on the Invoice is what is charged to the Cardholder’s Account.

✓ DO ensure the Cardholder signs the Invoice.

✓ DO follow the separate Instructions and Procedures for Shopping Cart a transaction, which is also referenced in Section 37.

✕ DON’T charge Cardholder’s additional fees for financing or require additional optional services as a condition of utilizing credit transactions.

✕ DON’T list financing terms on any other documentation that you provide to the Cardholder.

✕ DON’T use the Program for commercial or business transactions (e.g., for rental properties, business supplies, or inventory, etc.).

SPECIAL TERMS AND APR DISCLOSURE REQUIRED WITH NO INTEREST IF PAID IN FULL SPECIAL TERMS (“TEMPORARY RATE EXCEPTION”)

When a consumer agrees to “No Interest if Paid in Full” special terms, we are required by Law before the start of the special terms period, to provide the consumer in writing the length of the special terms period and the APR that will apply to any remaining balance after the expiration of the special terms period. This “Temporary Rate Exception” disclosure is provided on our IPS Invoices, Invoices approved by Wells Fargo, our manual Invoices, Invoice and Notice of Right to Cancel, and on sales slips printed from an Omni 3750 processing unit if used in support of our Program. You must ensure this “Temporary Rate Exception” disclosure is provided to all consumers utilizing a “No Interest if Paid in Full” special terms promotion.

✓ DO ensure the “Temporary Rate Exception” disclosure is provided to all consumers utilizing a “No Interest if Paid in Full” special terms promotion.

INVOICE AND NOTICE OF RIGHT TO CANCEL

In addition to the information set forth in the above paragraphs for Invoices, our approved Invoice and Notice of Right to Cancel must also be used in certain circumstances. In accordance with state and federal law, our processes for sales made to consumers outside of your normal business location (e.g., consumer home, fair, trade show, expo, etc.), require you to provide consumers with Invoice and Notice of Right to Cancel. Our Invoice and Notice of Right to Cancel

provides Cardholders the right to cancel their purchases within a specific time frame (Please reference the training document attached on the front of each Invoice and Notice of Right to Cancel and our separate training guide located on the Online Resource Center for successfully completing an Invoice and Notice of Right to Cancel). You must notify the Cardholder of the right and honor a cancellation including any rights a Cardholder may exercise after the Product is delivered and any service or work is completed. Our funding of an Invoice does not impact a Cardholder’s right of cancellation.

You must complete all fields on the top of the Invoice and Notice of Right to Cancel. The remainder of this section provides instructions on completing the Invoice and Notice of Right to Cancel section. We recommend you wait until after the Invoice and Notice of Right to Cancel period expires before installing goods or completing services. If you elect not to wait until after the Invoice and Notice of Right to Cancel period expires, you will still need to honor any Cardholder’s cancellation of the sale during the cancellation period.

COMPLETING THE INVOICE AND NOTICE OF RIGHT TO CANCEL

• Date of transaction: › Enter the date the buyer (Cardholder) signed the Invoice

(same date as in the line above the signature). This date does not count as one of the ‘Midnight of’ business days.

• Seller (Merchant) name and address: › Enter the full company name and physical street

address, including city, state and zip code.

• ‘Midnight of’ date: › Specify a date that is at least 3 business days from the

date listed on the ‘Date of Transaction’ line.

Cardholders should only sign their name in the Invoice and Notice of Right to Cancel section if they want to cancel the transaction. Edits or changes are not accepted on any part of the Invoice and Notice of Right to Cancel section, including and in particular to any of the dates. Errors found in the Invoice and Notice of Right to Cancel section will require a new Invoice and Notice of Right to Cancel form to be completed and signed by the consumer with a new “Midnight of” date.

You must provide the yellow copies of the Invoice and Notice of Right to Cancel to the consumer. If there are two consumers included in the transaction, then all four yellow copies of the Invoice and Notice of Right to Cancel must be provided so each consumer receives two copies.

Page 13Wells Fargo Bank, N.A. — Instructions and Procedures | Effective March 13, 2018

✓ DO complete all fields in the Invoice and Notice of Right to Cancel, including the section which discloses any special interest and payment terms.

✓ DO ensure you have calculated the correct “Midnight of” date for the state where the sale is taking place.

✓ DO have the Cardholder initial any changes to the top portion, “sections A & B” on the example, of the Invoice and Notice of Right to Cancel.

✕ DON’T make any changes to the dates in the Invoice and Notice of Right to Cancel portion, “section C” on the example, of the Invoice and Notice of Right to Cancel.

– The three business days must not include Sundays or federal holidays.

– Please always refer to the instructions on the current version of the Invoice and Notice of Right to Cancel form or the Online Resource Center (ORC) for updated instructions on how to complete the Invoice and Notice of Right to Cancel form.

Section 13: Presenting an Invoice for Processing

You will submit Invoices for payment using a method approved by Wells Fargo. Wells Fargo reserves the right to make changes to how Invoices are submitted and/or processed at any time. Invoices must be presented with the terms and amount financed agreed upon by the Cardholder in writing on the Invoice.

Invoices may only be presented to us after the transaction is completed to the Cardholder’s satisfaction. Invoices must be presented to Wells Fargo electronically within three calendar days of the transaction completion date. You have up to 15 calendar days from the transaction completion date to present the Invoice for manual funding.

By submitting an Invoice for payment you confirm:

1. the Cardholder has agreed to the terms and conditions of the Invoice;

2. the Cardholder has signed and dated (if required) the Invoice;

3. the Cardholder has been notified of and given the appropriate right to cancel under applicable Law (if it applies to the transaction); and

4. the service has been completed and/or the Product(s) have been received by the Cardholder.

If your current processing technology is unavailable for an extended period of time, please notify our Client Processing Department at 1-800-551-5111, Monday through Saturday from 8:00 a.m. to 10:00 p.m. and Sunday from 10:00 a.m. to 10:00 p.m. Central Time.

✓ DO verify the Cardholder’s identity when completing an Invoice for a sale.

✓ DO retain the completed Invoice in accordance with Section 17 Retention of Program Materials.

✕ DON’T submit the Invoice for payment until the services have been provided and/or the Product has been received by the Cardholder unless otherwise expressly allowed in your Agreement.

✕ DON’T submit Invoices that you know or suspect to be fraudulent or not authorized by the Cardholder.

✕ DON’T present Invoices for cash advances. No cash can be given to a Cardholder by you in connection with any Card transaction.

✕ DON’T submit Invoices on behalf of other Merchants or businesses.

✕ DON’T submit, sell or assign any part of a transaction to another creditor (e.g., No split ticket transactions with another creditor).

A03/19/2018Bob Q. Buyer

Home Improvement Co. 100 Improvement Lane, Anytown, USA 1234503/22/2018

03/19/2018

1 2 3 4 111222

1800 001 2 3 4 5 6 7 8 9 0 1 2 3 4 5

Bob Q Buyer123 Main StreetAnytown, USA 12345

111-222-3333

Home Improvement Co.

US1234567890 Home ImprovementJohn Seller

4 7 0 5 0 0 1 2 3 4 5 6 7 8 9 0 111222333444

100 Improvement Lane

Windows

B

C

Anytown, USA 12345

111-222-4444 [email protected]

12

(This date must match, or be after, the signature date above.)

EXAMPLE

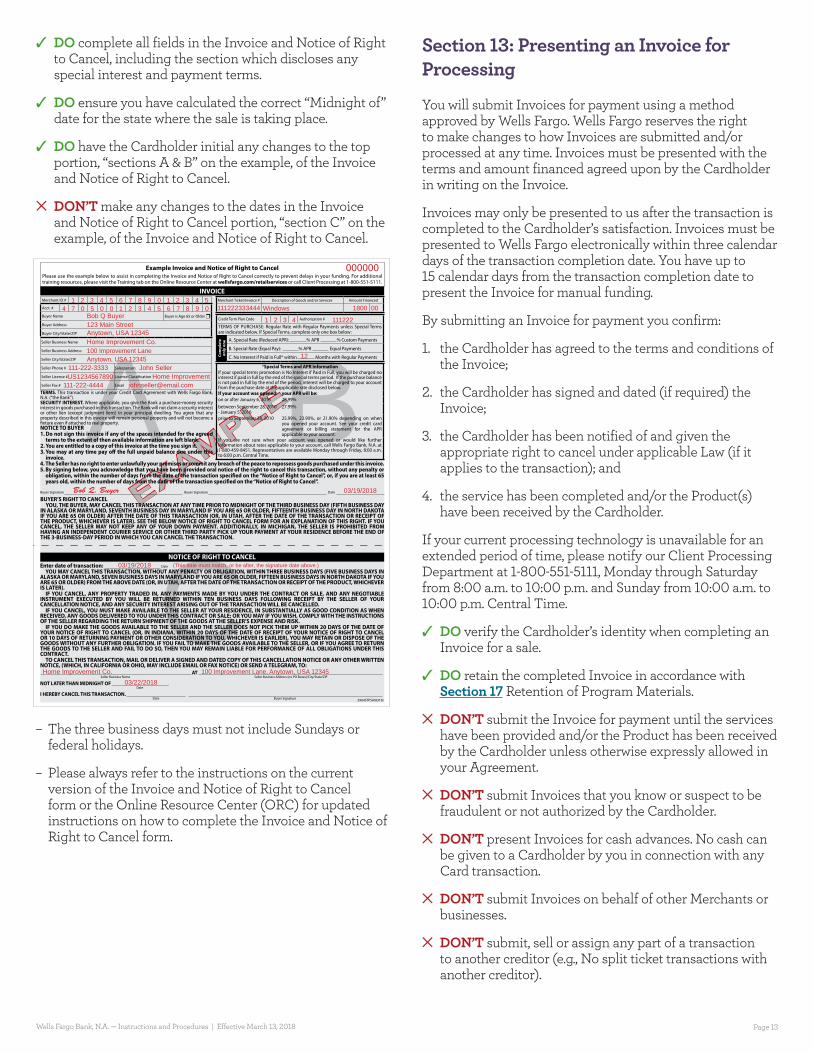

Example Invoice and Notice of Right to CancelPlease use the example below to assist in completing the Invoice and Notice of Right to Cancel correctly to prevent delays in your funding. For additional training resources, please visit the Training tab on the Online Resource Center at wellsfargo.com/retailservices or call Client Processing at 1-800-551-5111.

2964STPSA(0318)

000000

TERMS. This transaction is under your Credit Card Agreement with Wells Fargo Bank, N.A. (“the Bank”).SECURITY INTEREST. Where applicable, you give the Bank a purchase-money security interest in goods purchased in this transaction. The Bank will not claim a security interest or other lien (except judgment liens) in your principal dwelling. You agree that any property described in this invoice will remain personal property and will not become a fixture even if attached to real property.

Merchant ID #

Acct. #

Buyer Name Buyer is Age 65 or Older r

Buyer Address

Buyer City/State/ZIP

Seller Business Name

Seller Business Address

Seller City/State/ZIP

Seller Phone # Salesperson

Seller License # License Classification

Seller Fax # Email

NOTICE TO BUYER1. Do not sign this invoice if any of the spaces intended for the agreed

terms to the extent of then available information are left blank.2. You are entitled to a copy of this invoice at the time you sign it.3. You may at any time pay off the full unpaid balance due under this

invoice.4. The Seller has no right to enter unlawfully your premises or commit any breach of the peace to repossess goods purchased under this invoice.5. By signing below, you acknowledge that you have been provided oral notice of the right to cancel this transaction, without any penalty or

obligation, within the number of days from the date of the transaction specified on the “Notice of Right to Cancel”, or, if you are at least 65 years old, within the number of days from the date of the transaction specified on the “Notice of Right to Cancel”.

Merchant Ticket/Invoice # Description of Goods and/or Services Amount Financed

*Special Terms and APR InformationIf your special terms promotion is No Interest if Paid in Full, you will be charged no interest if paid in full by the end of the special terms period. If the purchase balance is not paid in full by the end of the period, interest will be charged to your account from the purchase date at the applicable rate disclosed below.If your account was opened: your APR will be:on or after January 6, 2016 28.99%between September 28, 2010 - January 5, 2016

27.99%

prior to September 28, 2010 25.99%, 23.90%, or 21.90% depending on when you opened your account. See your credit card agreement or billing statement for the APR applicable to your account.

If you are not sure when your account was opened or would like further information about rates applicable to your account, call Wells Fargo Bank, N.A. at 1-800-459-8451. Representatives are available Monday through Friday, 8:00 a.m. to 6:00 p.m. Central Time.

Credit Term Plan Code Authorization #

TERMS OF PURCHASE: Regular Rate with Regular Payments unless Special Terms are indicated below. If Special Terms, complete only one box below:

Com

plet

e on

ly o

ne

A. Special Rate (Reduced APR): % APR % Custom Payments

B. Special Rate (Equal Pay): % APR Equal Payments

C. No Interest if Paid in Full* within Months with Regular Payments

INVOICE

Buyer Signature Buyer Signature Date

BUYER’S RIGHT TO CANCELYOU, THE BUYER, MAY CANCEL THIS TRANSACTION AT ANY TIME PRIOR TO MIDNIGHT OF THE THIRD BUSINESS DAY (FIFTH BUSINESS DAY

IN ALASKA OR MARYLAND, SEVENTH BUSINESS DAY IN MARYLAND IF YOU ARE 65 OR OLDER, FIFTEENTH BUSINESS DAY IN NORTH DAKOTA IF YOU ARE 65 OR OLDER) AFTER THE DATE OF THIS TRANSACTION (OR, IN UTAH, AFTER THE DATE OF THE TRANSACTION OR RECEIPT OF THE PRODUCT, WHICHEVER IS LATER). SEE THE BELOW NOTICE OF RIGHT TO CANCEL FORM FOR AN EXPLANATION OF THIS RIGHT. IF YOU CANCEL, THE SELLER MAY NOT KEEP ANY OF YOUR DOWN PAYMENT. ADDITIONALLY, IN MICHIGAN, THE SELLER IS PROHIBITED FROM HAVING AN INDEPENDENT COURIER SERVICE OR OTHER THIRD PARTY PICK UP YOUR PAYMENT AT YOUR RESIDENCE BEFORE THE END OF THE 3-BUSINESS-DAY PERIOD IN WHICH YOU CAN CANCEL THE TRANSACTION.

NOTICE OF RIGHT TO CANCELEnter date of transaction: Date

YOU MAY CANCEL THIS TRANSACTION, WITHOUT ANY PENALTY OR OBLIGATION, WITHIN THREE BUSINESS DAYS (FIVE BUSINESS DAYS IN ALASKA OR MARYLAND, SEVEN BUSINESS DAYS IN MARYLAND IF YOU ARE 65 OR OLDER, FIFTEEN BUSINESS DAYS IN NORTH DAKOTA IF YOU ARE 65 OR OLDER) FROM THE ABOVE DATE (OR, IN UTAH, AFTER THE DATE OF THE TRANSACTION OR RECEIPT OF THE PRODUCT, WHICHEVER IS LATER).

IF YOU CANCEL, ANY PROPERTY TRADED IN, ANY PAYMENTS MADE BY YOU UNDER THE CONTRACT OR SALE, AND ANY NEGOTIABLE INSTRUMENT EXECUTED BY YOU WILL BE RETURNED WITHIN TEN BUSINESS DAYS FOLLOWING RECEIPT BY THE SELLER OF YOUR CANCELLATION NOTICE, AND ANY SECURITY INTEREST ARISING OUT OF THE TRANSACTION WILL BE CANCELLED.

IF YOU CANCEL, YOU MUST MAKE AVAILABLE TO THE SELLER AT YOUR RESIDENCE, IN SUBSTANTIALLY AS GOOD CONDITION AS WHEN RECEIVED, ANY GOODS DELIVERED TO YOU UNDER THIS CONTRACT OR SALE; OR YOU MAY IF YOU WISH, COMPLY WITH THE INSTRUCTIONS OF THE SELLER REGARDING THE RETURN SHIPMENT OF THE GOODS AT THE SELLER’S EXPENSE AND RISK.

IF YOU DO MAKE THE GOODS AVAILABLE TO THE SELLER AND THE SELLER DOES NOT PICK THEM UP WITHIN 20 DAYS OF THE DATE OF YOUR NOTICE OF RIGHT TO CANCEL (OR, IN INDIANA, WITHIN 20 DAYS OF THE DATE OF RECEIPT OF YOUR NOTICE OF RIGHT TO CANCEL OR 10 DAYS OF RETURNING PAYMENT OR OTHER CONSIDERATION TO YOU, WHICHEVER IS EARLIER), YOU MAY RETAIN OR DISPOSE OF THE GOODS WITHOUT ANY FURTHER OBLIGATION. IF YOU FAIL TO MAKE THE GOODS AVAILABLE TO THE SELLER, OR IF YOU AGREE TO RETURN THE GOODS TO THE SELLER AND FAIL TO DO SO, THEN YOU MAY REMAIN LIABLE FOR PERFORMANCE OF ALL OBLIGATIONS UNDER THIS CONTRACT.

TO CANCEL THIS TRANSACTION, MAIL OR DELIVER A SIGNED AND DATED COPY OF THIS CANCELLATION NOTICE OR ANY OTHER WRITTEN NOTICE, (WHICH, IN CALIFORNIA OR OHIO, MAY INCLUDE EMAIL OR FAX NOTICE) OR SEND A TELEGRAM, TO: AT Seller Business Name Seller Business Address (no PO Boxes)/City/State/ZIP

NOT LATER THAN MIDNIGHT OF . Date

I HEREBY CANCEL THIS TRANSACTION. Date Buyer Signature

Page 14Wells Fargo Bank, N.A. — Instructions and Procedures | Effective March 13, 2018

Section 14: Presenting a Credit on an Account

You must electronically submit a credit to an Account any time a Cardholder returns or exchanges Products or you make an adjustment to an Account. The amount of the credit shall be for the full purchase price of the Products returned plus all related fees and taxes. The credit must be submitted within three calendar days of processing the return or adjustment. A Credit Memo must be created and provided to the Cardholder to evidence the return of Products or adjustment to the Account. A manual Credit Memo must be completed and faxed to our Funding Team at 1-877-226-1469 if you are unable to present the Credit Memo electronically.

The minimum required information you must provide on a manual Credit Memo is:

• Cardholder Account Information (e.g., Cardholder name, address, Account Number, etc.);

• 15-digit Merchant Number;

• Merchant name and address;

• Merchant employee’s signature and date;

• Description of returned Products;

• Note the original plan number used for the purchase; and

• Amount to be credited back to the Account.

If you are presenting the credit electronically, give the Cardholder a copy of the Credit Memo and retain the Credit Memo in accordance with the document retention requirements described in Section 17 of these Instructions and Procedures.

✓ DO submit a credit for the full purchase price of all Products returned plus all related fees and taxes within three calendar days of processing the return or adjustment.

✓ DO provide the Cardholder with a copy of the Credit Memo for their personal records.

✕ DON’T give cash refunds, store credit or gift cards for any return of Products or adjustments in connection with an Account.

✕ DON’T charge any restocking fees to an Account or subtract the restocking fee from the amount of the credit posted to an Account.

Section 15: Mailing in Completed Consumer Credit Card Account Applications and Important Terms of Your Credit Card Account Forms to Wells Fargo for Retention

When a consumer applies for an Account, the consumer may sign a Consumer Credit Card Account Application or another document (depending upon your processing method) to acknowledge receipt of the Initial Disclosures and our Credit Card Agreement. The following provisions apply to the mailing of Consumer Credit Card Account Applications to us for retention.

CONSUMER CREDIT CARD ACCOUNT APPLICATIONS

Keeping our mutual customer’s sensitive personal information secure is a top priority for both you and Wells Fargo. As a participant in the Program, you are obligated to safeguard Cardholder Account Information. To assist us both in maintaining this obligation, unless otherwise notified in writing, Wells Fargo requires that you submit both approved and turned down Consumer Credit Card Account Applications to Wells Fargo for retention. This enables us to protect Cardholder Account Information in a secure manner. In the event that the consumer is approved but does not finance a purchase, you are still required to mail the completed Consumer Credit Card Account Application to Wells Fargo for retention.

When having consumers complete the Consumer Credit Card Account Application, it is very important to have the consumer legibly complete his or her name, the last four digits of the Cardholder’s social security number and zip code.

Please mail all approved and turned down Consumer Credit Card Account Applications within 15 calendar days of receiving the credit decision. The Consumer Credit Card Account Applications should be mailed to:

Wells Fargo Retail Services MAC F0003-030 800 Walnut Street Des Moines, IA 50309

Place the Consumer Credit Card Account Applications in a sealed envelope or other tamper- evident closed container and send them by first-class mail through the U.S. Postal Service or through another common carrier.

✓ DO ensure all Consumer Credit Card Account Applications are signed by the consumer prior to mailing them in for retention.

Page 15Wells Fargo Bank, N.A. — Instructions and Procedures | Effective March 13, 2018

✓ DO establish a standard business process to gather and mail all Consumer Credit Card Account Applications take out to the aforementioned address every 15 calendar days.

✓ DO mail in the Consumer Credit Card Account Application. The accompanying Credit Card Agreement should be given to the consumer for his or her records.

✓ DO keep other records like the Invoice or sales slip pursuant to the requirements of Section 17 Retention of Program Materials.

✕ DON’T wait until the Products are delivered or the services are completed to mail the Consumer Credit Card Account Applications to us.

✕ DON’T mail more than 200 Consumer Credit Card Account Applications in one shipment.

✕ DON’T mail any other documents except the Consumer Credit Card Account Application unless specifically requested by us.

Section 16: Sending Documentation to Wells Fargo Upon Request

From time to time we will request documentation from you in connection with an Account. It is very important that you promptly review the request, locate all requested documentation and send us all requested documentation in a timely manner. Unless other delivery instructions are provided, requested documents must be faxed to us at 1-888-245-8842, within seven calendar days of receiving the request. When faxing the requested documentation to us, include the request page as a cover page.

✓ DO fax all requested documentation included in the request form.

✕ DON’T mail the documents (e.g., Invoices or Credit Memos) that were requested. Unless other delivery instructions are provided, only fax them to 1-888-245-8842 to ensure prompt delivery to our Documentation team.

Section 17: Retention of Program Materials

In the course of completing transactions, you will be handling documents that contain Cardholder Account Information which may include, but not be limited to, Consumer Credit Card Account Applications, Invoices

and Credit Memos (collectively referred to in Section 1 as “Program Materials”). Unless otherwise directed by us, all Consumer Credit Card Account Applications must be sent into Wells Fargo for retention (see Section 15 above). Follow the guidelines below when retaining Program Materials you are allowed to retain.

Program Materials must be:

i. Retained for seven (7) years from the date of creation.

ii. Retained in a secure and orderly manner:

1. Secure: Physical access to Program Materials must be given only to employees who require access to perform certain functions of their job duties. All access to the physical location of Program Materials must be locked and secured. All Program Materials must be kept in a controlled area (e.g., an area with limited access by employees and no access by the public) to prevent unauthorized access.

2. Orderly: With the exception of Consumer Credit Card Account Applications which must be sent into Wells Fargo for retention, all other Program Materials must be filed in an orderly manner, allowing for quick retrieval should we request documents from you.

Important Reminders:

• Any documents referred to in the Invoice, (e.g., internal invoice), are considered part of the Invoice and should also be retained according to the guidelines above.

• Wells Fargo has the right to request any Program Materials in your possession and you must deliver such materials to us within seven calendar days of our request or such other timeline outlined in the request.

• Wells Fargo may request information regarding your filing procedures to ensure Program Materials are being retained in accordance with our Instructions and Procedures.

✓ DO ensure only authorized persons with a business need have access to Program Materials such as Consumer Credit Card Account Applications and Invoices which contain confidential Cardholder Account Information.

✓ DO retain all Program Materials in a locked file cabinet or other secure area to ensure confidentiality of sensitive consumer information.

✕ DON’T use a third-party vendor to retain or image Program Documents such as Consumer Credit Card Account Applications or Invoices in connection with the Program.

Page 16Wells Fargo Bank, N.A. — Instructions and Procedures | Effective March 13, 2018

Section 18: Destruction of Invoices and Credit MemosAfter the seven year retention period has expired on any Program Materials (as that term is defined in Section 1 above) you must destroy the Program Materials in a manner that renders the document unreadable and unidentifiable and that such data cannot be recreated. We require the use of an approved cross-cut shredder which renders the data contained in the document unreadable and unidentifiable. No document can be destroyed if we notify you that such record is subject to a Records Preservation Order (“RPO”). If we notify you that a document is subject to a RPO, you must retain the document in a secure and orderly manner until such time that we notify you the RPO is lifted. If the RPO is lifted and the document is past its seven year retention period, then you must destroy the document in accordance with the terms of this section.

✓ DO establish a standard business process to destroy Program Materials after the seven year retention period has expired.

✓ DO ensure the documents are destroyed in such a manner that renders the data contained in the document as unreadable and unidentifiable.

✕ DON’T destroy any document or other information that we have notified you is subject to a records preservation order (RPO) until such time as we notify you the RPO is lifted and the document is past its required seven year retention period.

Section 19: Information SecurityAs a participant in the Program you have a shared responsibility to adhere to strict information security standards to ensure the confidentiality of our mutual consumers’ sensitive personal information and Cardholder Account Information.

KEEPING CONSUMER INFORMATION SECURE

You will adhere to the highest standards of confidentiality in protecting the personal information, including nonpublic information, of any applicant, co-applicant, Cardholder (past or current), and/or any information obtained through the use of the Card. This includes, but is not limited to, all Cardholder Account Information.

KEEPING WELLS FARGO BANK, N.A. INFORMATION SECURE

You will regard all information provided to you by us, our representatives, and our affiliates as confidential. This includes, but is not limited to, analyses, forecasts, discount

rates and pricing information, and passwords for our internet sites and other technologies. This information constitutes our proprietary information and trade secrets which you are obligated to protect against any threat of compromise or disclosure.

WHO SHOULD HAVE ACCESS

Only your permanent employees with a business need should have access to Cardholder Account Information. You will not allow temporary employees, independent and sub-contractors, third-party management and/or marketing companies, and employees operating in capacity as a shared resource to have access to Cardholder Account Information or to any of our technology systems. For example, you will not allow third-party answering services, back room processors, after-hours processors, contract employees etc. to have access to Cardholder Account Information.

PROTECTING CARDHOLDER INFORMATION AGAINST BREACHES

Invoke appropriate information security measures to protect any Cardholder Account Information and confidential or proprietary Wells Fargo information against unauthorized access, accidental or unlawful destruction, tampering, copying, and/or anticipated threats or hazards. You will retain and store any information, in electronic and/or paper form, in a secure and orderly manner at all times.

WHAT TO DO IF AN INFORMATION SECURITY BREACH OCCURS

You must immediately notify us of any confirmed or suspected compromises or unauthorized access of any Cardholder Account Information or other confidential information of ours and implement appropriate actions to prevent further unauthorized access while information is in your possession or in transit to us. You will cooperate with us during our investigation, providing us, appropriate law enforcement agencies, and governmental regulatory authorities all pertinent information regarding the unauthorized access.

✓ DO immediately notify our Corporate Information Security Team at 1-877-494-9355 (24 hours a day, seven days a week) and notify our Client Processing Department at 1-800-551-5111 (Monday through Saturday from 8:00 a.m. to 10:00 p.m. and Sunday from 10:00 a.m. to 10:00 p.m. Central Time) of any confirmed or suspected compromise of any Cardholder Account Information or Confidential Wells Fargo information.

✓ DO ensure only permanent employees have access to Cardholder Account Information.

✓ DO retain Cardholder Account Information in a secure and orderly manner.

Page 17Wells Fargo Bank, N.A. — Instructions and Procedures | Effective March 13, 2018

✓ DO ensure only authorized employees have access to your secured storage location.

✕ DON’T disclose the existence of an Account or any Cardholder Account Information to any third-party or to any employee who does not have a business need to know.

✕ DON’T leave Cardholder Account Information in an area accessible by an unauthorized party.

✕ DON’T allow any unauthorized party to obtain Cardholder Account Information on your behalf.

✕ DON’T allow any unauthorized third-party, operating for their own interest, to utilize any aspect of or represent themselves as a party in relationship with the Card Program.

✕ DON’T allow any unauthorized third-party to image and/ or store information for you.

Section 20: Passing Along the Costs of Financing