interim performance presentation - beranda · interim performance presentation ... notes: • fy...

TRANSCRIPT

1

1

15-May-07 5:46 PM Unique id: 036458 Documentum: GARL-Pegasus-Main.ppt

Interim Performance PresentationQ1 2007 : quarter ended 31st March 2007

15th May 2007

2

2

SECTION 1 Executive Summary 3

SECTION 2 Financial Highlights 5

SECTION 3 Operational Highlights 11

SECTION 4 Sales Highlights 16

SECTION 5 Growth Strategy 21

SECTION 6 Key Developments 26

Table of Contents

Section 1Executive Summary

4

4

Executive Summary

EBITDA US$ 88mn

Average CPO Price (FOB Belawan)

Net income

US$ 546/ton

Interim Dividend

Equity Placement

Palm Products Production 412,000 ton

43%

12%

46%

US$ 219mn 63%

S$0.02

325.3mn shares S$ 800mn

�

Q1 2007 vs. Q1 2006

Section 2Financial Highlights

6

6

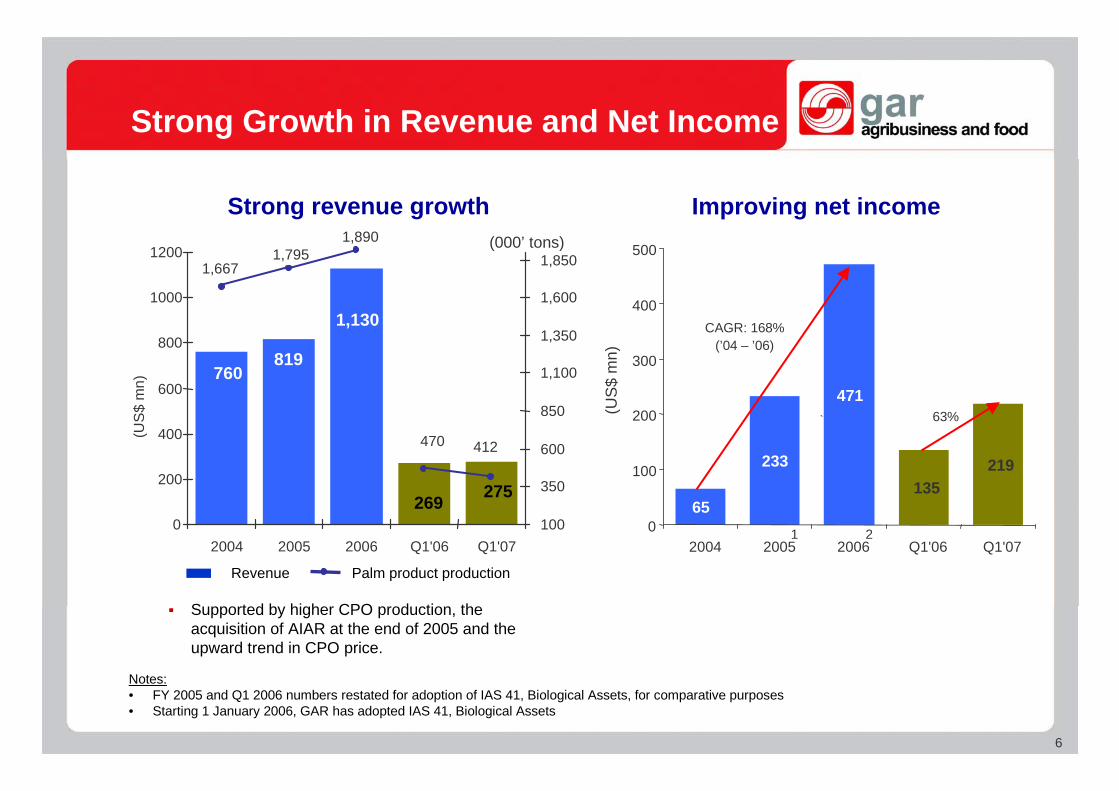

Strong revenue growth

Strong Growth in Revenue and Net Income

Supported by higher CPO production, theacquisition of AIAR at the end of 2005 and theupward trend in CPO price.

Notes:• FY 2005 and Q1 2006 numbers restated for adoption of IAS 41, Biological Assets, for comparative purposes• Starting 1 January 2006, GAR has adopted IAS 41, Biological Assets

Improving net income

65

233

471

219135

0

100

200

300

400

500

2004 2005 2006 Q1'06 Q1'07

(US

$ m

n)

`

CAGR: 168%(’04 – ’06)

21

63%

CAGR: 22%(’04 – ’06)

(US

$ m

n)

(000’ tons)

275269

1,130

819760

412470

1,8901,795

1,667

0

200

400

600

800

1000

1200

2004 2005 2006 Q1'06 Q1'07100

350

600

850

1,100

1,350

1,600

1,850

Revenue Palm product production

7

7

Revenue 268.7 275.3 2.5%Gross profit 67.6 102.7 51.9%Gross profit Margin 25.1% 37.3% 48.6%Net gain from biological assets 178.1 164.9 (7.4%)Operating income 224.9 242.2 7.7%EBITDA 61.6 88.2 43.3%Tax (56.2) (62.3) 10.9%Net profit attributable to the equity holders 134.7 219.3 62.8%EPS (in US$ cents) 6.2 10.1 62.8%Interim dividend per share (in S$) - 0.02 n.m.

Financial Performance

Note:• Starting 1 January 2006, GAR has adopted IAS 41, Agriculture. Q1 2006 numbers restated for adoption of IAS 41, Agriculture, for comparative

purposes.

(in US$ mn) Q1 Q1 %2006 1 2007

increase/(decrease)

8

8

Revenue 184.6 203.6 10.3% 84.2 71.7 (14.7%)

Gross Profit 60.0 89.9 49.7% 7.5 12.8 69.5%

Gross Profit Margin 32.5% 44.1% 35.7% 8.9% 17.8% 100.0%

EBITDA 55.7 76.4 37.1% 5.9 11.8 102.1%

Profit Before Tax 213.7 291.3 36.3% 3.6 10.3 184.5%

Net Income 131.1 209.1 59.5% 3.6 10.2 186.6%

Q1 ~ 2007 Financial Performance

(in US$ mn) Indonesia Operation China OperationQ1 2006 Q1 2007 % increase/ Q1 2006 Q1 2007 % increase/

decrease decrease

9

9

Total Assets 2,985.4 3,303.3 10.6%Cash 130.4 62.7 (51.9%)Short Term Investment 3.7 10.3 180.3%

Total Liabilities 1,064.1 1,142.5 7.4%Interest Bearing Debt 477.4 514.6 7.8%

Total Equity 1,921.3 2,160.8 12.5%

Debt2/Equity Ratio (x) 0.25 0.24Net Debt/Equity Ratio (x) 0.18 0.20

Financial Position

Notes:• Starting 1 January 2006, GAR has adopted IAS 41, Biological Assets. Q1 2006 results are restated for adoption of IAS 41, Biological Assets, for

comparative purposes.• Interest bearing debt

(in US$ mn) FY Q1 %2006 1 2007

increase/(decrease)

Continuous growth in total assets with a low gearing ratio

10

10

Dividend

1.0

2.12.0

0.0

0.5

1.0

1.5

2.0

2.5

FY 05 FY 06 Q1 07

S$

Cen

ts P

er S

hare

Dividend Per Share

GAR has been increasing the dividend payout to shareholders and will always evaluatethe optimum utilization of its income

1

1 Equivalent to US$ 0.014/share for FY 2006 dividend

Section 3Operational Highlights

12

12

Planted Area 306,851 293,145 338,185 15.4%Nucleus 226,185 213,365 257,507 20.7%Plasma 80,666 79,780 80,678 1.1%

Mature Area 271,140 275,436 292,609 6.2%Nucleus 192,903 197,213 213,828 8.4%Plasma 78,237 78,223 78,781 0.7%

Land Bank 200,000 120,000 1,300,0001 983.3%

Operational Performance ~ Area

Note:• Include land acquisition in progress of approximately 1,100,000ha (plantable area) located in Kalimantan (100,000ha) and Papua (1,000,000ha)

(in ha) 31 Dec Q1 Q1 Q1’06 – Q1’072006 2006 2007 %increase/(decrease)

13

13

Operational Performance ~ Production

(000’Tons) (Ton/Ha)

Drought condition due to El Nino effect caused a decrease in productivity during Q12007

In April’07, the production started to recover, hence higher production is expected in thefollowing quarters.

3,769 4,191 4,275 4,377

1,068 1,043

1,2031,463 1,595 1,624

394 337

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2003 2004 2005 2006 Q1'06 Q1'07

FFB Production ~ Nucleus FFB Production ~ Plasma

(000’Tons)

FFB Production Palm Products Production

1,176

257

337386

1,4791,367

1,553

7584

337315299

5.31 4.72

22.1321.4320.23

18.37

-

250

500

750

1,000

1,250

1,500

1,750

2,000

2003 2004 2005 2006 Q1'06 Q1'07-

4

8

12

16

20

24

CPO (Ton) PK (Ton) FFB Yield (Ton/Ha)

14

14

1,225

1,392

1,5541,624

1,348 1,380

1,5671,462

1,699

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Q1 2005 Q2 2005 Q3 2005 Q4 2005 Q1 2006 Q2 2006 Q3 2006 Q4 2006 Q1 2007

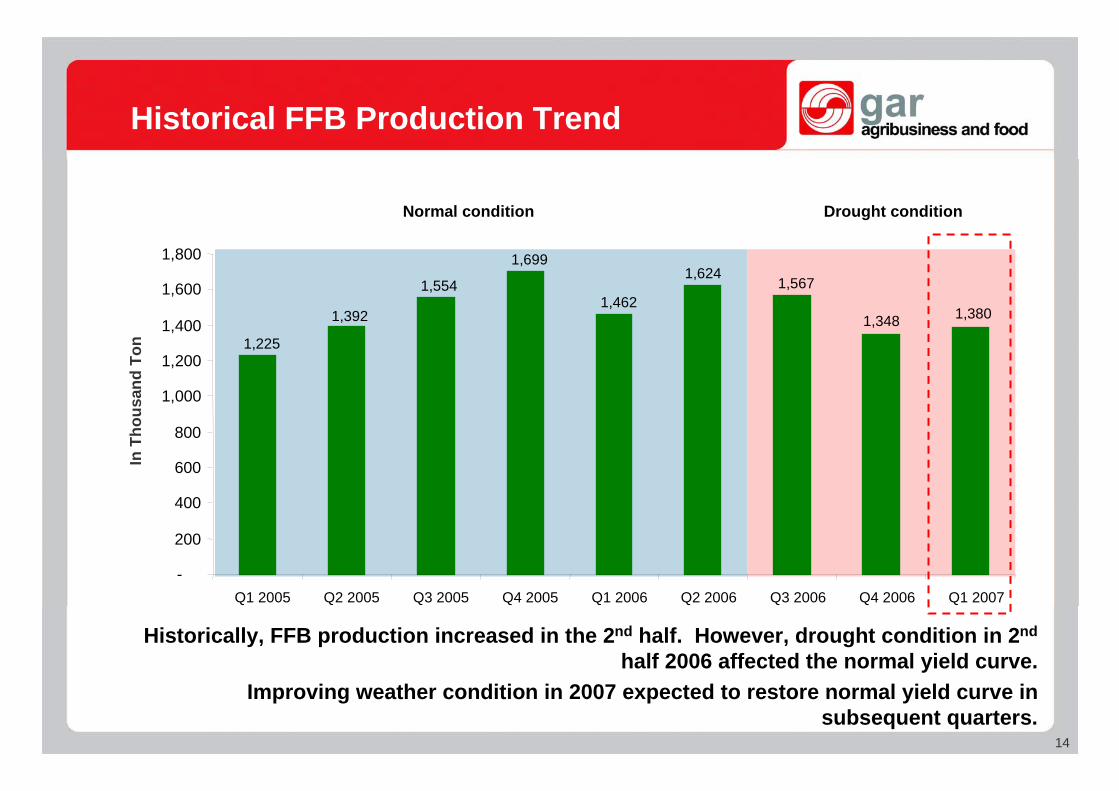

Historical FFB Production Trend

Normal condition Drought condition

In T

hous

and

Ton

Historically, FFB production increased in the 2nd half. However, drought condition in 2nd

half 2006 affected the normal yield curve.Improving weather condition in 2007 expected to restore normal yield curve in

subsequent quarters.

15

15

FFB Production (tons) 1,461,752 1,380,077 (5.6%)FFB Yield (ton/ha) 5.3 4.7 (11.1%)

Extraction RateOER 23.60% 23.62%KER 5.11% 5.24%

Palm Products Production (tons) 470,042 411,727 (12.4%)CPO (tons) 386,382 336,955 (12.8%)PK (tons) 83,660 74,772 (10.6%)

Utilization RateIndonesia Refinery 77.4% 69.2%China Refinery 57.7% 58.7%China Crushing 82.0% 54.0%

Soybean Processed (tons)Soybean Oil (tons) 37,006 24,534 (33.7%)Soybean Meal (tons) 166,023 110,135 (33.7%)

Operational Performance ~ Production

Q1 Q1 %2006 2007 increase/ (decrease)

Section 4Sales Highlights

17

17

Business Performance

Indonesia Operation ~ By Products

Revenue contribution

China Operation ~ By Products

China Local26% Indonesia

Local40%

Indonesia Export

34%

Unbranded palm products

35%

Branded products

11% PK 3%

CPO51%

Others1%

Soybean meal40%

Branded products

9%

Unbranded palm products

15%

Soybean oil35%

PK2%

Branded products

11%

Soybeanoil9%

Others1%

Unbranded palm product

30%

Soybeanmeal10%

CPO37%

Revenue contribution ~ By Products

18

18

Indonesia OperationCPO 247,000 225,000 (8.7%)PK 37,000 23,000 (38.1%)Refined Products 217,000 206,000 (5.1%)

BrandedCooking Oil 21,000 18,000 (14.4%)Margarine 11,000 13,000 15.5%

Unbranded 176,000 160,000 (9.1%)

China OperationBranded Cooking Oil 10,000 7,000 (30.0%)Unbranded:

Soybean Oil 44,000 30,000 (31.8%)Soybean Meal 172,000 106,000 (38.4%)Palm oil based 9,000 15,000 66.7%

Sales Volume

Q1 Q1 %2006 2007 increase/ (decrease)

19

19

$100

$200

$300

$400

$500

$600

$700

$800

$900

Jan-06

Feb-06

Mar-06

Apr-06

May-06

Jun-06

Jul-06

Aug-06

Sep-06

Oct-06

Nov-06

Dec-06

Jan-07

Feb-07

Mar-07

Apr-07

May-07

CPO (CIF Rotterdam) Soybean Oil (Dutch, FOB ex mill)

CPO Price Trend

Sources : Oil World & Reuters

China lifted quotaimport on palm oil

El-Nino effect reduceproduction

India’s CPO importtax reduced

New demand from bio-dieselUS$/Ton

20

20

Bio-diesel Capacity

Local market isheated in 1-2 years

New capacity in 2007 is at 1.6 million ton

Company Plant locationSize

(tonnes) Completion

date Company CommentSize

(tonnes) Completion

dateLipid Tech Sdn. Bhd Port Klang, Selangor 12,000 Jun 2008 Darmex Oil 200,000 n.aGolden Hope Banting, Selangor 35,000 Completed Sumi Asih Group 2,000 tonslyr and increase gradually 200,000 2009Carotech Chemor, Perak 48,000 n.a. Sari Dumai Sejati Part of larger company 100,000 naCaratino (JV with MPOB) Pasir Gudang, Johor 60,000 Completed Indo Bio Fuels Focus on biodiesel conversion tech. 100,000 n.aGolden Hope (JV with MPOB) Carey Island, Selangor 60,000 1H2007 Asianagro Part of Raja Garuda Mas. 150,000 naGolden Hope Pasir Gudang, Johor 60,000 2007 Molindo Raya Ind'IIPT PNX Increase from current 30,000 to 40,000T 40,000 2007IJM Plantations Sandakan, Sabah 90,000 Q4 2007 Eterindo Wahanatama Producing 22,000 T, supply to Pertamina 200,000 2008/2009PPB Group Pasir Gudang, Johor 100,000 early 2007 PT Mopoli 1 of 4 plants to start in 2007 (Apindo) 150,000 2007SPC Biodiesel Lahad Datu, Sabah 100,000 end-2007 Sinar Mas Citic 1 of 4 plants to start in 2007 (Apindo) 100,000 2007Mission Biotechnologies Kuantan, Pahang 100,000 July 2007 PT Musimas 1 of 4 plants to start in 2007 (Apindo) 100,000 2007Global Bonanza Sdn Bhd Kuching, Sarawak 100,000 June 2007 PT Sumiasih 1 of 4 plants to start in 2007 (Apindo) 60,000 2007GS Palm Sdn Bhd Masai, Johor 100,000 Q3 2007 Energi Alternative Indonesia 300 ProducingAchi Jaya Plantations Segamat, Johor 100,000 end-2007 PT Rekayasa and Pertamina 5,000 2006Pacific Bio-Energy Sdn Bhd Lahad Datu, Sabah 100,000 n.a. Astra Agra Trial stage for in-house use 5,000 2007Kulim (jv with Cremer) Pasir Gudang, Johor 100,000 2007 Wahana Abadi Tirta A clean water management company 30,000 n.aKulim (jv with Cremer) Singapore 100,000 2007 Anugerah Inti Gemanusa 50,000 naEmpee Industries Bhd Kuantan, Pahang 100,000 n.a. Artha Trans Jaya 1,200 naTSH Resources Sabah 100,000 n.a. Wilmar Bioenergi 150,000 T in 2007 250,000 2008Zurex Lahad Datu, Sabah 200,000 Q1 2008 Makindo related Potential for litigation 100,000 naHimpunan Sari Sdn. Bhd Kemamam, Terengganu 200,000 June 2007 Government projects 4x6,000 tons and 4x3,000 tons 36,000 n.aTotal Malaysia 1,865,000 Total Indonesia 1,877,500

Diesel Diesel(mn tonnes) Consumed for Transportation B5 B10

Malaysia 8.7 4.6 0.4 0.9 Indonesia 30.4 8.0 1.5 3.0 Total 39.1 12.6 1.9 3.9

Section 5Growth Strategy

22

22

Growth Strategy

Commitment to sound business strategies and continuous operationalexcellence will enable GAR to sustain growth and profitability

Food Industrial Bio-Fuel

Strong Plantation FoundationLargest in the world with 338,000 ha planted

ContinuedGrowth and Profitability

Future expansion of 1.3 mn ha land bank

23

23

Q1 2007 Growth Achievements and Targets

PlantationTarget planted area of 40,000 ha for FY 2007Achieved additional planted area of 31,000 ha during Q1 07

- 3,000 ha of new planting- 28,000 ha of acquired plantation

DownstreamCompleted new speciality fat factory in Ningbo, China with capacity of 44,000 ton/yearCompleted conversion of Surabaya and Medan refineries energy source from diesel to coal in April07New refinery in Tarjun, South Kalimantan with capacity of 300,000ton/year under constructionNew Cocoa Butter Substitute facility in Belawan, Indonesia with capacity of 30,000 ton/year underconstruction

Bio-dieselSigned a MOU with CNOOC and HK Energy to develop bio-diesel and bio-ethanol.Expected investment of US$ 5.5bn over 8 years.On May 3, 2007, signed a JV agreement with Fulcrum Biofuels LLC to establish a bio-diesel plant inDumai, Indonesia with USA as a market

24

24

Bio-diesel JV ~ Transaction Highlights

Parties : Blue Sky Golden Fulcrum Ltd (wholly owned subsidiary of GAR)~ (50%)

Fulcrum Biofuels LLC ~ (50%)

Purpose : To initially build and operate a bio-diesel plant in Dumai, Sumatra,Indonesia and market the bio-diesel in the US market

Capacity : 400,000MT per annum, expected to be fully operation in 2008

Cost : US$ 60m, include working capital

25

25

GAR Fulcrum

JV Co.

Biodiesel plant atDumai

End CustomersCalifornia, USA

50% 50%

Partnership to enter into growing US bio-diesel market

Strong synergies between GAR’s CPO supply advantage and Fulcrum’s Logistics andMarketing expertise

The JV will be entitled to the tax credit of approx. US$ 300/ton

Bio-diesel JV Structure

• 200,000 tons p.a. first 3yrs, then 100,000 tonsp.a. on year 4-5 at US$585/ton

• Additional 200,000 tonp.a. at floating price

• Logistics & marketing• Hedging & Risk

management• Guaranteed EBITDA/ton

of US$ 75/ton for200,000 ton p.a. for min.3 years

Section 6Key Developments

27

27

Equity Placement ~ Transaction Highlights

Deal type : Placement of new shares (Reg S only)

Placement price : S$ 2.4588 (7.22% discount to the closing price on 19th April2007)

Size of the deal : 325,300,000 new shares(representing 15% of pre-placement share capital)

S$ 800m or equivalent to US$ 530mn

Use of proceeds : To finance GAR’s capital expenditure and general corporatepurposes

Total institutional accounts : > 80

Placement date : 19th April 2007

Joint Bookrunner & : BNP Paribas (Singapore) Ltd, CIMB-GK Securities Pte. Ltd.Placement Agent and Oversea-Chinese Banking Corporation Limited

28

28

Equity Placement ~ Demand Analysis

Demand by investor type Demand by geography

Book of demand comprised mainly institutional investors with Long Funds dominating with63% contributionPrivate banking demand was mainly discretionarily managed portfoliosEurope and UK investors represented 63% buyers

Private bank13%

Hedge fund21%

Bank3%

Long fund63%

USA5% Others

3%

Singapore28%

HK1%

UK25%

Europe38%

29

29

Contact Us

Golden Agri-Resources Ltdc/o 3 Shenton Way#17-03 Shenton HouseSingapore 068805

Telephone : +65 62207720Facsimile : +65 62207020

Contact Person : Rafael B. Concepcion, Jr. ([email protected])Suwandy Chen ([email protected])

If you need further information, please contact: