intermediate financial accounting i operational assets: utilization and disposition

TRANSCRIPT

Intermediate Financial Accounting I

Operational Assets: Utilization and Disposition

Operational Assets: Utilization and Disposition 2

Objectives of the Chapter

A. To learn depreciation methods for financial reporting purposes.

B. To study income tax depreciation including Accelerated Cost Recovery System (ACRS) and modified ACRS.

C. To discuss the accounting issues related to asset impairments.

Operational Assets: Utilization and Disposition 3

A. Depreciation (For Financial Reporting Purposes)

1. Time-based methodsa. Straight-Line.b. Sum-of-the-Years’-Digits (SYD).c. Declining-Balance.

2. Activity-based method Unit-of-Production.

3. Special methodsa. Group Depreciation.b. Composite Depreciation.c. Retirement and Replacement Methods.

Operational Assets: Utilization and Disposition 4

iGAAP: Depreciation

iGAAP, as in US GAAP, perceives depreciation as a cost allocation of an asset over the asset’s life.

iGAAP, as in US GAAP, allows depreciation methods such as straight line, diminishing-balance, and unit-of-production.

IFRS requires component depreciation. GAAP permits component deprecation but is rarely applied.

Operational Assets: Utilization and Disposition 5

For Financial Reporting Purposes

1. Time-Based Methods Depreciation Methods based on the

passage of time:a. Straight-Line Method.

b. Sum-of-the-Years’-Digits (SYD).

c. Declining-Balance.

b and c are called the accelerated depreciation methods (or the decreasing charge methods).

Operational Assets: Utilization and Disposition 6

A.1a. Straight-Line Method Cost is allocated evenly through the life of the P.P.E. Example 1: Machine costing $10,000 was purchased on

1/1/x1. The estimated residual value of the machine is $2,000 and the estimated life of the machine is 4 years.Depreciation Expense per year:($10,000 - 2,000)/ 4 = $2,000

12/31/x1 Depreciation Expenses 2,000Accumulated Depreciation

2,000

Operational Assets: Utilization and Disposition 7

1a. Straight-Line Method (Partial Year Depreciation)

Example 2 :Using the information in example 1, except that the machine was purchased on 3/11/x1. Companies normally compute depre. on the basis of nearest full month. Depreciation Expense of year x1 ==> [($10,000-2,000)/4] x (10/12) = $1,667

Year Depr. Exp Acc. Depr.x1 1667 (10 months) 1,667x2 2000 (12 months) 3,667x3 2000 (12 months) 5,667x4 2000 12 months) 7,667x5 333 (2 months) 8,000

Operational Assets: Utilization and Disposition 8

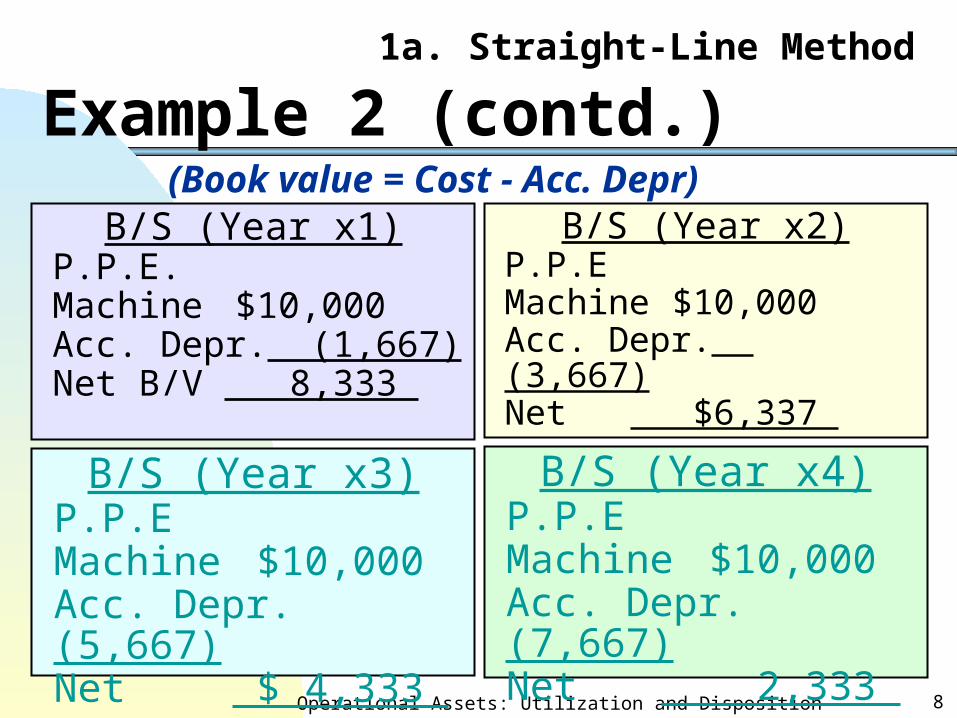

1a. Straight-Line Method

Example 2 (contd.)

B/S (Year x1)P.P.E. Machine $10,000 Acc. Depr. (1,667)Net B/V 8,333

B/S (Year x2)P.P.EMachine $10,000 Acc. Depr. (3,667)Net $6,337

B/S (Year x3)P.P.EMachine $10,000 Acc. Depr. (5,667)Net $ 4,333

B/S (Year x4)P.P.EMachine $10,000 Acc. Depr. (7,667)Net 2,333

(Book value = Cost - Acc. Depr)

Operational Assets: Utilization and Disposition 9

1b. Sum-of-the-Years’-Digits (SYD)

Example 1: Machine costing $10,000 was purchased on 1/1/x1 with an estimated residual value of $2,000 and an estimated life of 4 years.

Depr. **Book ValueYear *Depr. Base Fraction Expense at the end x1 $8,000 4/10 $3,200 6,800 x2 $8,000 3/10 $2,400 4,400 x3 $8,000 2/10 $1,600 2,800 x4 $8,000 1/10 $800 2,000

* Depr. Base= Cost - Residual Value** Book Value= Cost - Acc. Depreciation

Operational Assets: Utilization and Disposition 10

1b. S-Y-D (contd.)

Example 2: (Partial Year)

Same information as in example 1 on page 8 except that the machine was purchased on 2/21/x1 rather than on 1/1/x1.

The depr. period of Year x1 = 10 months

Operational Assets: Utilization and Disposition 11

1b. S-Y-D

Example 2 (contd.) Annual Depr.

By S-Y-D Depr. Year Method Months Computation Exp 1 x1 $3,200 10 10/12x3200= $2,667

2 x2 $2,400 12 2/12x3200+10/12x2400= $2,533

3 x3 $1,600 12 2/12x2400+10/12x1600= $1,733

4 x4 $800 12 2/12x1600+10/12x800= $934

5 x5 - 2 2/12x800= $133

Operational Assets: Utilization and Disposition 12

1c. Declining-Balance Method

Depreciation Exp.= constant rate book value at the beginning of the period Residual value is not considered in the

computation. Assets cannot be depreciated below the

residual value. The constant rate is expressed as a

function of a straight-line annual depreciation rate.

Operational Assets: Utilization and Disposition 13

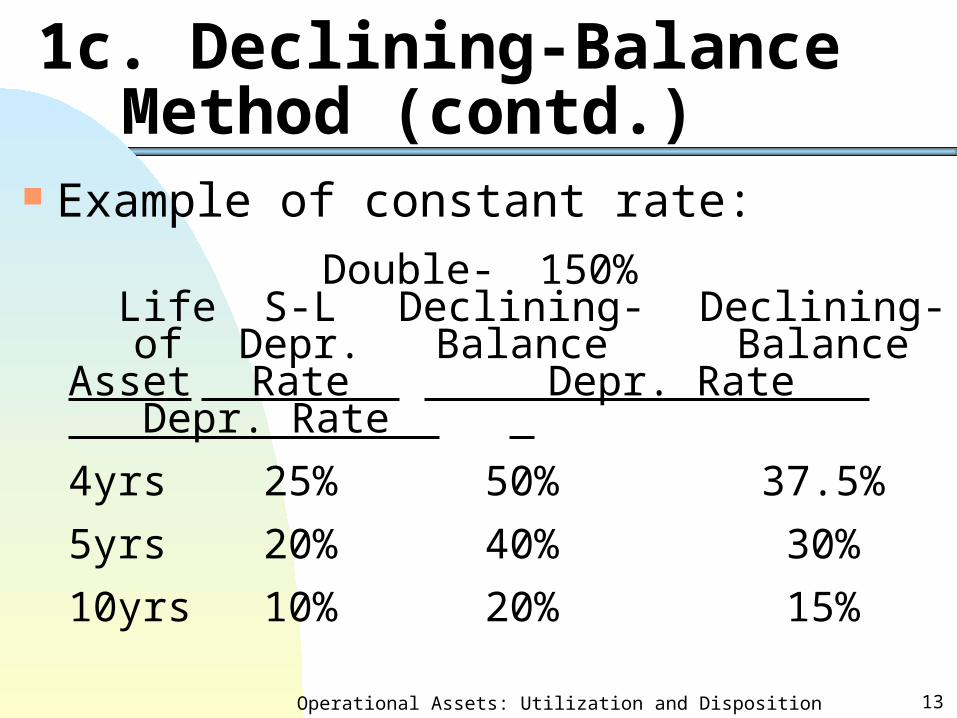

1c. Declining-Balance Method (contd.)

Example of constant rate:

Double- 150% Life S-L Declining- Declining- of Depr. Balance Balance Asset Rate Depr. Rate Depr. Rate

4yrs 25% 50% 37.5%

5yrs 20% 40% 30%

10yrs 10% 20% 15%

Operational Assets: Utilization and Disposition 14

1. Time-Based Methods

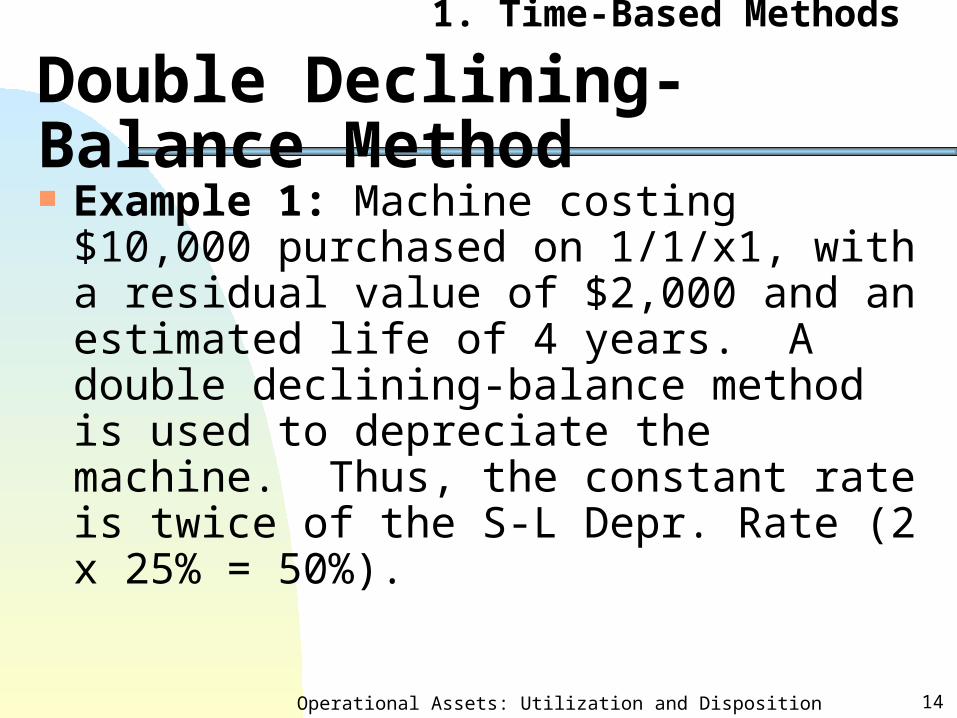

Double Declining-Balance Method Example 1: Machine costing $10,000

purchased on 1/1/x1, with a residual value of $2,000 and an estimated life of 4 years. A double declining-balance method is used to depreciate the machine. Thus, the constant rate is twice of the S-L Depr. Rate (2 x 25% = 50%).

Operational Assets: Utilization and Disposition 15

Double Declining-Balance Method

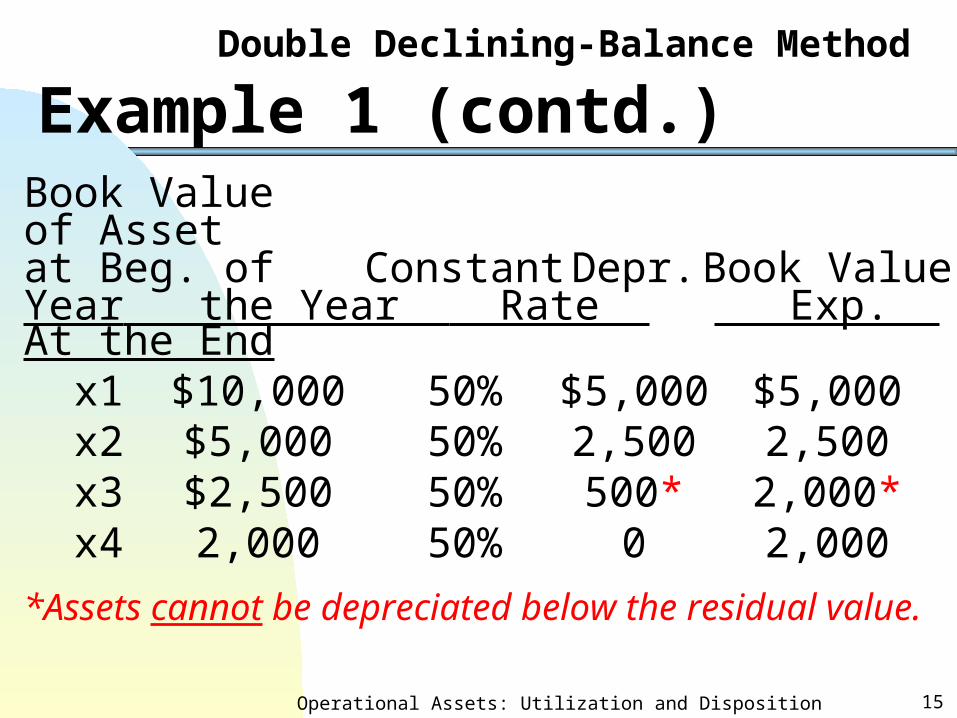

Example 1 (contd.)Book Value

of Assetat Beg. of Constant Depr. Book Value

Year the Year Rate Exp. At the End

x1 $10,000 50% $5,000 $5,000 x2 $5,000 50% 2,500 2,500 x3 $2,500 50% 500* 2,000* x4 2,000 50% 0 2,000

*Assets cannot be depreciated below the residual value.

Operational Assets: Utilization and Disposition 16

Double Declining-Balance Method

Example 2 (partial year) Use the same information as the

example on page 13, except that the machine was purchased on 3/10/x1.

The depreciation period of Year x1 = 10 months.

Two alternative treatments for the partial year depreciation of the declining-balance method are available as follows:

Operational Assets: Utilization and Disposition 17

Double Declining-Balance Method

Example 2 (contd.) - Alternative IAnnual Depr.

Using the Recognized D-D-B Months Computations Depr. Exp.

1 x1 $5,000 10 10/12x5000= $4,167

2 x2 $2,500 12 2/12x5000+10/12x2500= $2,916

3 x3 $500 12 2/12x2500+10/12x500= $834

4 x4 0 12 2/12x500= $835 x5 0 2 - -

Operational Assets: Utilization and Disposition 18

Double Declining-Balance Method

Example 2 (contd.) - Alternative II Book Book Value Value

Year at Beg. Rate Depr. Exp. At the End x1 $10,000 50% 10/12x(10,000 $5,833

x50%)= 4,167

x2 $5,833 50% 12/12x(5,833 2,916 x50%)= 2,917

x3 $2,916 50% 916 2,0001

x4 $2,000 50% 0 2,000

1.Assets cannot be depreciated below the residual value.

Operational Assets: Utilization and Disposition 19

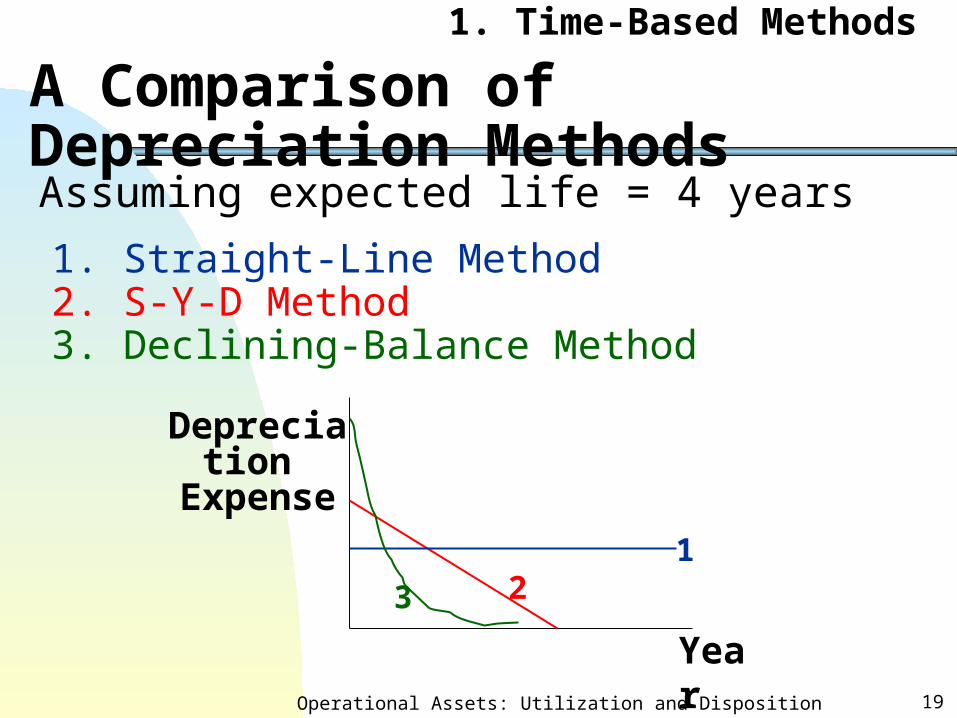

1. Time-Based Methods

A Comparison of Depreciation MethodsAssuming expected life = 4 years

1. Straight-Line Method2. S-Y-D Method3. Declining-Balance Method

Year

Depreciation Expense

123

Operational Assets: Utilization and Disposition 20

Changes In Depreciation Method (i.e., Change from D-D-B to S-L) Accounting treatment (SFAS No. 154: Accounting

Changes and Error Corrections, effective 1/1/2006):

Treated as an accounting estimate change that is achieved by change in accounting principle.

Method: Prospective method. The accounting for depreciation method

change is an example of revising US GAAP to converge to iGAAP.

Operational Assets: Utilization and Disposition 21

1. Time-Based Methods

Changes In Depreciation Estimate Accounting treatment: no retroactive

effect and make no adjustment for the past years’ misstatement. Spread the remaining undepreciated balance (i.e., the book value) less the revised (new) residual value over the revised (new) estimate of the remaining life of the assets.

Operational Assets: Utilization and Disposition 22

Example: (S-L Depr. Method)

Machine costing $10,000 acquired on 1/1/x1.

EstimatesEstimates

on 1/1/x1 on 1/1/x3

Residual value $2,000 $1,000

Life 4 years 5 years

Operational Assets: Utilization and Disposition 23

Example: (Contd.)

Year Depr. Exp Acc. Depr Book Valuex1 $2,0001 2,000 8,000x2 $2,0002 4,000 6,000x3 $1,667 5,666.7 4,333.3x4 $1,667 7,333.4 2,666.6x5 $1,667 9,000.1 1,000

1. (10,000-2,000)/4 = $2,0002. (6,000-1,000)/(5-2) =1666.7

Operational Assets: Utilization and Disposition 24

For Financial Reporting Purposes

2. Activity-Based Method Depreciation based on the usage of

assets. Depreciation bases -- hours of usage or production units.

Method:

Units-of-Production Method: depreciation based on the usage of the asset

Operational Assets: Utilization and Disposition 25

2. Activity-Based Method

Example Machine costing $10,000 was purchased

on 5/20/20x1 with an estimated residual value of $2,000 and an estimated service hours of 8,000 hours.

Depreciation expense per hour= ($10,000 - 2,000)/8,000 hours= $1 per hour

Operational Assets: Utilization and Disposition 26

2. Activity-Based Method

Example (contd.) During 20x1, the machine was used for 1,000

hours, the depreciation expense of 20x1: $1 x 1,000 = $1,000

J. E.12/31/x1 Depreciation Expense 1,000

Accumulated Depreciation 1,000

Operational Assets: Utilization and Disposition 27

For Financial Reporting Purposes

3. Special Methodsa. Group Depreciation (Group-Rate

Method).

b. Composite Depreciation (Composite-Rate Method).

c. Retirement and Replacement Methods (used by special Industries--public utilities and railroads).

Operational Assets: Utilization and Disposition 28

3a.&b. Group and Composite Methods

One depreciation rate is applied to multiple assets (i.e., telephone poles, switch boards, etc).

Group Method: Used when assets have similar economic lives and other attributes.

Composite Method: Used when assets are physically dissimilar (i.e., a group of heterogeneous assets).

Operational Assets: Utilization and Disposition 29

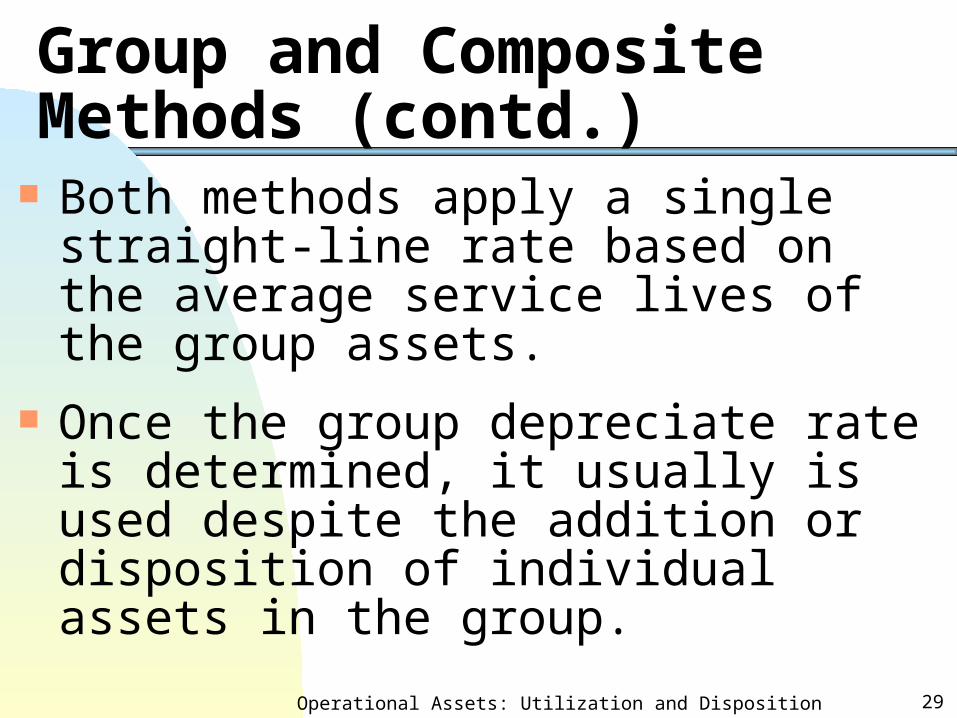

Group and Composite Methods (contd.)

Both methods apply a single straight-line rate based on the average service lives of the group assets.

Once the group depreciate rate is determined, it usually is used despite the addition or disposition of individual assets in the group.

Operational Assets: Utilization and Disposition 30

Group and Composite Methods (contd.)

When these methods are applied:

1. No partial year depreciation regardless of when these assets were purchased.

2. No gain or loss can be recognized in disposition of group assets except for the disposition of last piece(s) of assets in the group.

3. Cannot depreciate the remaining assets to below their residual value.

Operational Assets: Utilization and Disposition 31

Examples (Group Method)

Five machines were purchased on 3/5/x1 at $10,000 each. All machines were expected to last 4 years with a residual value of $2,000 each.

Depreciation expense per year= ($50,000-10,000)/4= $10,000

Group annual depreciation rate= $10,000/$50,000 = 20% (of cost)

Operational Assets: Utilization and Disposition 32

3a. Group Method

Example I Use the information on page 29 (assuming no early

retirement or new purchase within 4 years), the following J.E. would be recorded at the end of year:

12/31/x1 Depr. Exp 10,000Acc. Depr. 10,000

12/31/x2 Depr. Exp 10,000Acc. Depr. 10,000

12/13/x3 Depr. Exp 10,000Acc. Depr. 10,000

12/31/x4 Depr. Exp 10,000Acc. Depr. 10,000

Operational Assets: Utilization and Disposition 33

3a. Group Method

Example I (contd.) Five machines were sold (disposed) on

3/5/x5 for $1,500 each.

J.E. (The Retirement of 5 machines)

3/5/x5 Cash 7,500Acc. Depr. 40,000Loss on Disposal 2,500Machine 50,000

Operational Assets: Utilization and Disposition 34

3a. Group Method

Example II Use information on page 29 and assume one

machine was sold for $6,000 on 3/10/x3. Two were sold for $5,000 each on 8/9/x4 and the last two were discarded on 9/20/x5.

12/31/x1 (Recording the group depreciation expenses for Year x1)Depreciation Expenses 10,000

Accumulated Depreciation10,000

($50,000 x 20% = $10,000)(Total Cost) x (Group Rate)

Operational Assets: Utilization and Disposition 35

3a. Group Method

Example II (contd.)12/31/x2 (Group Depreciation Expenses for Year x2)Depreciation Expenses 10,000

Accumulated Depreciation10,000

($50,000 x 20% = $10,000)

3/10/x3 (the disposal of the first machine)Cash 6,000 Accumulated Depreciation 4,000a

Machine 10,000a. No gain or loss can be recognized.

Operational Assets: Utilization and Disposition 36

3a. Group Method

Example II (contd.)12/31/x3 (Group Depreciation Expenses for Year x3)Depreciation Expenses 8,000

Accumulated Depreciation8,000

[($50,000 - $10,000) x 20% = $8,000]

Cost for the Group rateremaining 4 machines

Machine 50,000 10,000 40,000

Operational Assets: Utilization and Disposition 37

3a. Group Method

Example II (contd.)8/9/x4 (Sold 2 machines for $5,000 each)Cash 10,000 Accumulated Depreciation 10,000a

Machine 20,000a. No gain or loss can be recognized

12/31/x4 (Depreciation Expenses for Year x4)Depreciation Expenses 2,000b

Accumulated Depreciation 2,000 [($50,000 - $10,000 - 20,000) x 20% = $4,000]

Cost for the remaining 2 machines Group rateb. See explanations on page 36.

Operational Assets: Utilization and Disposition 38

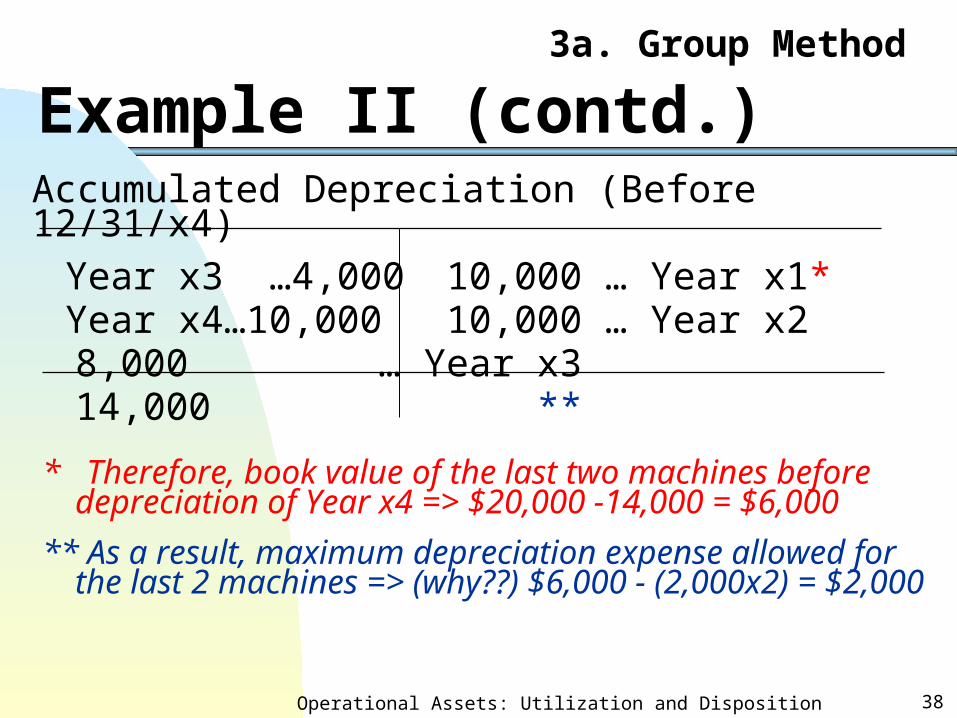

3a. Group Method

Example II (contd.)Accumulated Depreciation (Before 12/31/x4)

Year x3 …4,000 10,000 … Year x1* Year x4…10,000 10,000 … Year x2

8,000 … Year x314,000 **

* Therefore, book value of the last two machines before depreciation of Year x4 => $20,000 -14,000 = $6,000

** As a result, maximum depreciation expense allowed for the last 2 machines => (why??) $6,000 - (2,000x2) = $2,000

Operational Assets: Utilization and Disposition 39

3a. Group Method

Example II (contd.)9/20/x5 (Discard the Last Two Machines)Accumulated Depreciation (Before 12/31/x5)x3 ... 4,000 10,000 … x1x4 ... 10,000 10,000 … x2

8,000 … x32,000 … x4

16,000

Accumulated Depreciation 16,000Loss on Disposal 4,000

Machine 20,000

Operational Assets: Utilization and Disposition 40

3a. Group Method

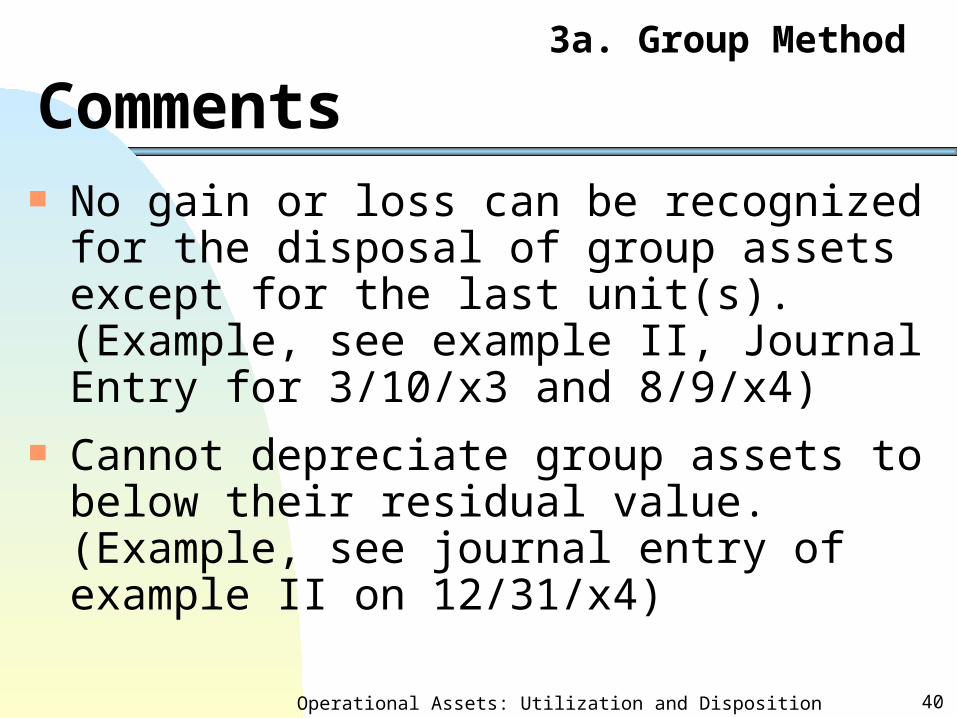

Comments No gain or loss can be recognized for

the disposal of group assets except for the last unit(s). (Example, see example II, Journal Entry for 3/10/x3 and 8/9/x4)

Cannot depreciate group assets to below their residual value. (Example, see journal entry of example II on 12/31/x4)

Operational Assets: Utilization and Disposition 41

3a. Group Method

Comments (contd.) If a similar asset were purchased and

added to the group, a new group depreciation rate may be computed as follows:

(Book value of the old in the group + cost of the new asset - estimated residual value of the group) / (weighted average lives of the assets in the group) (see example III)

Operational Assets: Utilization and Disposition 42

3a. Group Method

Example III (calculating new group depr. rate) Use the example on page 29. Additional

information is as follows:One machine was sold on 4/10/x3 for $7,000. A similar new machine was acquired on 8/19/x4 for $12,000 with an expected life of 4 years and $2,000 residual value. Two machines were sold on 9/10/x4 for $5,000 each. The last three machines were sold on 10/5/x5 for $1,000, $2,000 and $1,500, respectively.

Operational Assets: Utilization and Disposition 43

3a. Group Method

Example III (contd.)Journal Entries:

3/5/x1 (Purchasing of 5 machines on 3/5/x1)Machine 50,000

Cash 50,000

12/31/x1 (Recording Depr. Exp. for Year x1)Depreciation Expense 10,000

Accumulated Depreciation 10,000

12/31/x2 (Depreciation Expenses of Year x2)Depreciation Expense 10,000

Accumulated Depreciation 10,000

Operational Assets: Utilization and Disposition 44

3a. Group Method

Example III (contd.)4/10/x3 Cash 7,000Accumulated Depreciation 3,000

Machine 10,000

12/31/x3 Depreciation Expense 8,000

Accumulated Depreciation 8,000

8/19/x4Machine 12,000

Cash 12,000

Operational Assets: Utilization and Disposition 45

3a. Group Method

Example III (contd.)-New Group Depreciation RateDepreciation Expense = [($15,000+$12,000)1 - ($2,000x4+2,000)2]/1.6 years3

= $10,625

New Group Depreciation Rate= $10,625 / ($40,000 + 12,000)4

= 20.43%

1. Book Value of the remaining 4 machines.2. Residual value of 4 remaining machines and the new

one.3. The W-A lives of remaining machines and the new one

=>[(4-3) x 4 + 4] / 5 = 1.6 (years)4. Total cost of 4 remaining machines and the new one.

Operational Assets: Utilization and Disposition 46

3a. Group Method

Example III (contd.)Journal Entries:9/10/x4Cash 10,000Accumulated Depreciation 10,000

Machine 20,000

12/31/x4Depreciation Expense1 6,538

Accumulated Depreciation 6,538

1. (62,000 -30,000) x 20.43% = $6,538

Operational Assets: Utilization and Disposition 47

3a. Group Method

Example III (contd.)10/5/x5 sold the last 3 machines (update the

depreciation expenses for Year x5 because the group is not fully depreciated to the residual value of $6,000)

Depreciation Expenses 4,4621

Accumulated Depreciation 4,462

Cash 4,500Accumulated Depreciation 26,000Loss on Disposal 1,500

Machine 32,000

1. See explanation on next page.

Operational Assets: Utilization and Disposition 48

3a. Group Method

Example III (contd.)Machine

3/x1 50,000 10,000 … 4/x38/x4 12,000 20,000 … 9/x3

32,000

Accumulated Depreciation4/x3… 3,000 10,000 … 12/x19/x4 …10,000 10,000 … 12/x2

8,000 … 12/x3 6,538 … 12/x4

21,538

Operational Assets: Utilization and Disposition 49

3a. Group Method

Example III (contd.)* Book value of the last 3 machines on 10/5/x5 before the adjusting entry= $32,000 - 21,538 = 10,462

Residual Value of the last 3 machines = $2,000 x 3 = $6,000==> max. depreciation expenses for Year x5= 10,462 - 6,000 = $4,462

20.43% x $32,000 = $6,538 > $4,462 ==> Depreciation exp. for Year x5 = $4,462

Operational Assets: Utilization and Disposition 50

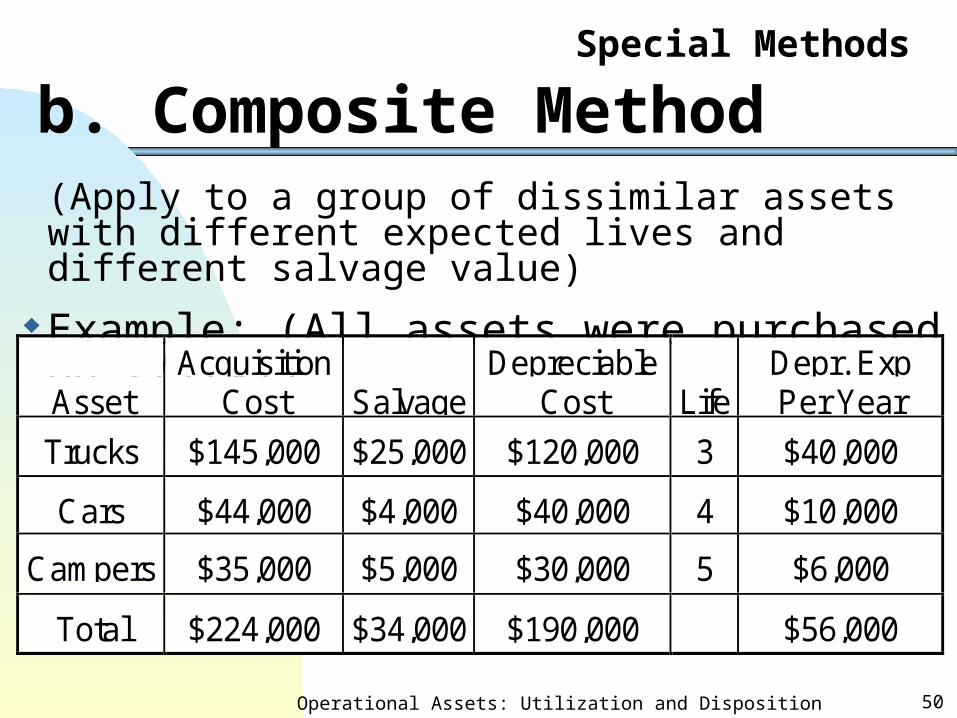

Special Methods

b. Composite Method(Apply to a group of dissimilar assets with different expected lives and different salvage value)

Example: (All assets were purchased on 2/1/x1)

AssetAcquisition

Cost SalvageDepreciable

Cost LifeDepr. ExpPer Year

Trucks $145,000 $25,000 $120,000 3 $40,000

Cars $44,000 $4,000 $40,000 4 $10,000

Campers $35,000 $5,000 $30,000 5 $6,000

Total $224,000 $34,000 $190,000 $56,000

Operational Assets: Utilization and Disposition 51

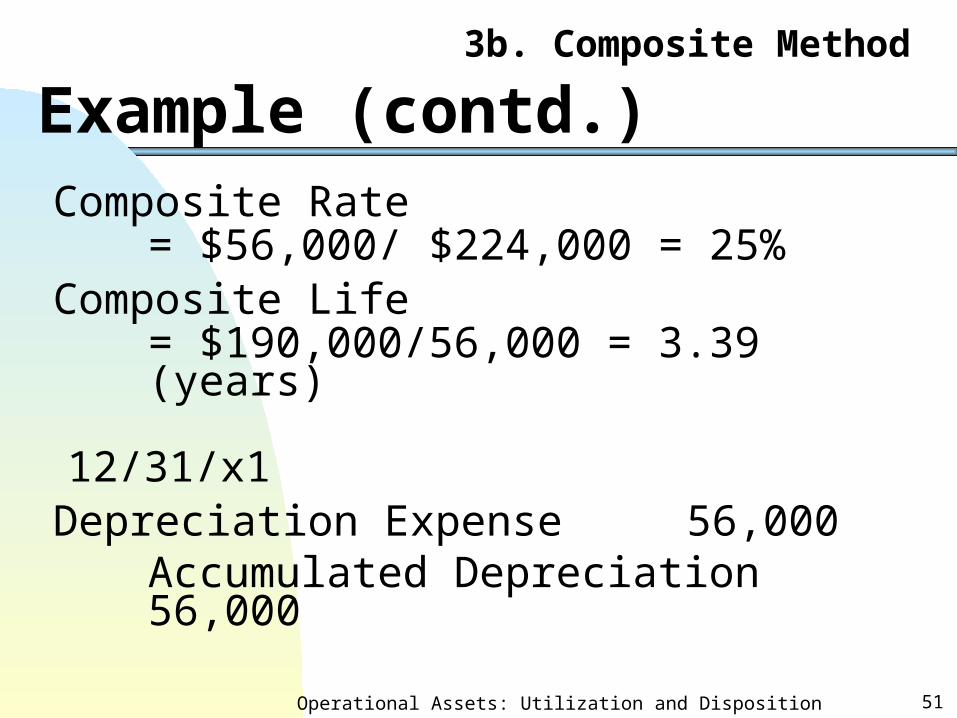

3b. Composite Method

Example (contd.)Composite Rate

= $56,000/ $224,000 = 25%Composite Life

= $190,000/56,000 = 3.39 (years)

12/31/x1Depreciation Expense 56,000

Accumulated Depreciation56,000

Operational Assets: Utilization and Disposition 52

3b. Composite Method

Comments Apply to a group of dissimilar assets. No

partial year depreciation. All rules that are applied to the group

depreciation method also are applied to the composite depreciation method.

No gain or loss can be recognized when composite assets are retired except for the last piece (pieces) of assets being disposed.

Operational Assets: Utilization and Disposition 53

3b. Composite Method

Comments (contd.) Cannot depreciate assets remained in

the group to below the residual value If a new asset is purchased, a new

composite rate may be calculated.

Operational Assets: Utilization and Disposition 54

3b. Composite Method

Retirement of Composite Assets(Similar accounting treatment as for the retirement of group assets -- no gain or loss can be recognized except for the disposal of the last asset(s) in the group).

i.e., Trunk 101 was sold on 3/8/x2 for $1,000. The cost for truck 101 is $8,000.

Operational Assets: Utilization and Disposition 55

Retirement of Composite Assets (contd.)3/8/x2Cash 1,000

Accumulated Depr. 7,000Truck 8,000

At the end of the year, the composite rate 25% would be applied to: ($224,000 - 8,000) = $216,000

$216,000 x 25% = $54,000

12/31/x2 Depreciation Exp. 54,000Accumulated Depr. 54,000

Operational Assets: Utilization and Disposition 56

Special Methods

c. Retirement and Replacement Methods Used by public utilities and railroad companies

which own many similar units of small value (i.e. poles, conductors, telephones,…). Retirement Method:

Charge the cost of the retired assets (less salvage) to depreciation expense.

Replacement Method:Charge the cost of newly purchased assets (less the salvage value of the replaced assets) to depreciation expense.

Operational Assets: Utilization and Disposition 57

3c. Retirement and Replacement Methods

Example

In 20x2, Greenway Co. purchased small tools costing $10,000. In 20x3, tools originally costing $3,000 were sold for $100 and replaced with new tools costing $4,000. Determine the depreciation expense for the small tools for the year of 20x3.

Under the retirement method: $2,900

Uner the replacement method:$3,900

Operational Assets: Utilization and Disposition 58

3c. Retirement and Replacement Methods

Example (cont.)

Journal entries (under the retirement method)

20x2 Small Tools 10,000 Cash 10,000 to record the acquisition of small tools

20x3 Small Tools 4,000 Cash 4,000

to record the additional small tool acquisition

Operational Assets: Utilization and Disposition 59

3c. Retirement and Replacement Methods

Example (cont.)

Journal entries (retirement method cont.)

20x3 Cash 100 Depreciation expense 2,900 Small tools 3,000 to record sale/depre. of small tools

Operational Assets: Utilization and Disposition 60

3c. Retirement and Replacement Methods

Example (cont.)

Journal entries (under the replacement method)

20x2 Small Tools 10,000 Cash 10,000 to record the acquisition of small tools

20x3 Small Tools 4,000 Cash 4,000

to record the additional small tool acquisition

Operational Assets: Utilization and Disposition 61

3c. Retirement and Replacement Methods

Example (cont.)

Journal entries (replacement method cont.)

20x3 Cash 100 Depreciation expense 3,900 Small tools 4,000 to record sale/depre. of small tools

Operational Assets: Utilization and Disposition 62

3c. Retirement and Replacement Methods

Comments

1. No depreciation expense recognized until assets are retired or replaced.

2. For railroad companies, these methods are rarely used after 1983 due to ICC required railroads to switch to traditional depreciation accounting (i.e., S-L method, SYD…).

Operational Assets: Utilization and Disposition 63

Disclosure of Depreciation (APB No. 12)1. Depreciation expense for the period.2. Balances of major classes of depreciable

assets at the balance sheet date.3. Accumulated depreciation, either by

major classes of depreciable assets or in total, at the balance sheet date.

4. A general description of the method or methods used with respect to major classes of depreciable assets.

Operational Assets: Utilization and Disposition 64

The Use of Alternative Depreciation Methods -- Statistics from a Survey of 600 Companies

Source: Accounting Trends and Techniques1

1.There are more than 600 responses because many companies use more than one method of depreciation.

Method 2010 2007 2001 1998 1991 1990

Straight Line 488 592 576 578 558 560

Declining balance 10 16 22 26 28 38

Sum of the years’ digits 3 5 7 10 8 11

An Accelerated method (not specified)

17 27 53 50 70 69

Units of production 16 23 34 39 50 50

Group/composite 1 9

Operational Assets: Utilization and Disposition 65

Miscellaneous Points Related To Depreciation Group method is applied to a group of

homogeneous assets with similar lives and attributes (may or may not have the same residual value).

Composite method is used when assets are physically dissimilar but are aggregated for convenience.

Hybrid of combination methods: GAAP allows any systematic and rational way to allocate costs. Steel industry uses a combination of straight-line and activity based method (a production variable method).

Operational Assets: Utilization and Disposition 66

Miscellaneous Points Related To Depreciation (contd.) Selection of a depreciation method is based

on the goal of the company. There is no cash flow involved in the

deprecation. The depreciation method change should not

have an impact on stock price based on the efficient market hypothesis.

This is supported by some research (Kaplan & Roll, 1972).

Partial year depreciation is computed on the basis of the nearest full month.

Operational Assets: Utilization and Disposition 67

For Income Tax Reporting Purposes

B. Income Tax Depreciation Tax Depreciation in different periods:

1.GAAP depreciation methods (i.e., S-L, SYD or DDB): Apply to assets acquired before 1981; cannot be depreciated to below the residual value. IRS published tables with estimated lives for depreciable assets .

2.ACRS: Accelerated Cost Recovery System applies to assets purchased between 1981 - 1986.

3.Modified ACRS: MACRS applies to assets purchased in 1987 or later.

Operational Assets: Utilization and Disposition 68

Tax Depreciation

ACRS & MACRS vs. GAAP ACRS and MACRS differ with GAAP

depreciation in the following aspects:a. a mandated tax life, which is generally

shorter than the economic life;b. cost recovery on an accelerated basis;c. an assigned salvage value of zero (i.e.,

salvage = $0);d. Assume assets acquired in the mid-year.

Operational Assets: Utilization and Disposition 69

Tax Depreciation

2. ACRS (Skip) Classify depreciable assets into five classes

(i.e., 3, 5 ,10, 15 and 18 year classes). Have a tax rate table for each class. Examples of classes:

3-year class: cars, light-duty trucks, equipment..

5-year class: office furniture, heavy duty truck..

10-year class: depreciable real estate..15-year class:18-year class: buildings.

Operational Assets: Utilization and Disposition 70

2. ACRS (contd.) (Skip)

Rate Table for ACRS:3-year 5-year 10-year 15-year25% 15% 18% 5%38% 22% 14% 10%37% 21% 12% 9%

21% 10% 8%21% 10%

9%9%9%9%9%

Operational Assets: Utilization and Disposition 71

Tax Depreciation

3. MACRS MACRS was enacted by Congress in

the Tax Reform Act of 1986. Assets are classified in 8 property classes instead of 5 classes as in ACRS. In addition, a specified GAAP depreciation method is used in computing the depreciation expense for all classes.

Operational Assets: Utilization and Disposition 72

MACRS Depreciation Methods

MACRS Depreciation Method Property Class Double-Declining Balance 3,5,7 or 10-year

property 150% Declining Balance 15 or 20-year

property Straight-Line 27.5 or 39 year

property

Operational Assets: Utilization and Disposition 73

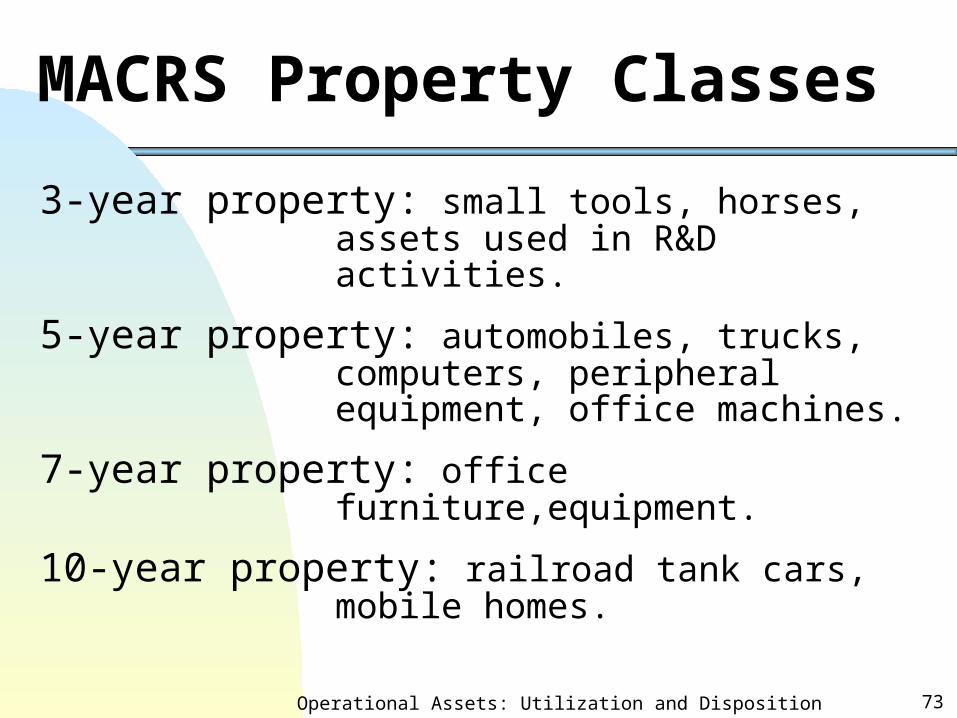

MACRS Property Classes

3-year property: small tools, horses, assets used in R&D activities.

5-year property: automobiles, trucks, computers, peripheral equipment, office machines.

7-year property: office furniture,equipment.

10-year property: railroad tank cars, mobile homes.

Operational Assets: Utilization and Disposition 74

MACRS Property Classes (contd.)

15-year property: roads, shrubbery, low-income housing, sewage treatment plants.

20-year property: certain real estate.

27.5 -year property: residential rental property.

39-year property: nonresidential real property.

Operational Assets: Utilization and Disposition 75

Principles Applied to MACRS

1. No residual value assigned (100% depreciation for tax purposes). All proceeds from the disposal of a fully depreciated asset are fully taxable.

2. Assume acquired in the mid-year (half-year convention).

3. When applying 150% declining balance(DB) method or DDB method, the depreciation method should be switched to S-L method if S-L method results in a higher depreciation expense than that of the DB method.

Operational Assets: Utilization and Disposition 76

MACRS

Example Cost= $200,000 (purchased on 10/2/x1). Expected life= 8 years. Salvage= $40,000. GAAP depr. method= Straight-Line. MACRS life = 5 years. MACRS method= Double-Declining

Balance Method. Disposal proceeds – 1/2/x9 = $22,000

Operational Assets: Utilization and Disposition 77

MACRS

Example (contd.) Year Depr. Exp Dep.% BookV x1 $200,00040%0.5 = 40,000 20%

160,000 x2 160,000 40% = 64,000 32% 96,000 x3 96,000 40% = 38,400 19.2% 57,600 x4 57,600 40% = 23,040 11.52% 34,560 x5 34,560/ 1.51 = 23,040 11.52% 11,520 x6 11,520 5.76% 0

1.DDB depr for year x5 is 34,560 40% = 13,824. The S-L method results in a higher depr. exp. (i.e., $23,040) than that of DDB in year x5. Thus, the depr. Method should be switched to the S-L method in x5.

Operational Assets: Utilization and Disposition 78

GAAP Depreciation and Gain/Loss at Disposal Annual GAAP depreciation

= ($200,000-40,000)/8 =$20,000 Accumulated GAAP depre. over 8 years

= $20,000x8= $160,000 Disposal loss for finanical reporting

= $22,000 - 40,000 = -18,000 Disposal gain for tax filing= $22,000 – 0 =22,000

Operational Assets: Utilization and Disposition 79

Gain/Loss at Disposal (contd.) Total expense recognized for tax filing = accumulated tax depreciation – disposal gain = $200,000 -22,000= $178,000

Total GAAP expense = accumulated GAAP depreciation + disposal loss = $160,000+18,000=178,000

Even though the net effects on income (i.e., $178,000 total expense) are the same, MACRS enables companies to defer income tax payments to later years.

Operational Assets: Utilization and Disposition 80

Table 11A-3 MACRS DEPR. RATES BY CLASS OF PROPERTY .

Re-covery 3-year 5-year 7-year 10-year

15-year 20-year Year (200% DB) (200% DB) (200% DB)

(200% DB) (150% DB) (150% DB) 1 33.33 20.00 14.29 10.00 5.00 3.750 2 44.45 32.00 24.49 18.00 9.50 7.219 3 14.81* 19.20 17.49 14.40 8.55 6.677 4 7.41 11.52* 12.49 11.52 7.70 6.177 5 11.52 8.93* 9.22 6.93 5.713 6 ……….. 5.76 8.92 7.37 6.23 5.285 7 8.93 6.55* 5.90*4.888 8 4.46 6.55 5.90 4.522 9 6.56 5.91 4.462*

* Switchover to straight-line depreciation.80

Operational Assets: Utilization and Disposition 81

Table 11A-3 (contd.) Re-covery 3-year 5-year 7-year 10-year 15-year 20-year

Year (200% DB) (200% DB) (200% DB) (200% DB) (150% DB) (150% DB) 10 6.55 5.90 4.46111 ……………………………… 3.28 5.91 4.46212 5.90 4.46113 5.91 4.46214 5.90 4.46115 5.91 4.46216 2.95 4.46117 4.46218 4.46119 4.46220 4.46121 2.231

81

Operational Assets: Utilization and Disposition 82

Tax Versus GAAP Depreciation

Purpose of tax depreciation: to raise revenue.

Purpose of GAAP depreciation: for financial reporting to fairly reflect the performance of a company.

With difference purposes, tax depreciation is different from GAAP depreciation.

Operational Assets: Utilization and Disposition 83

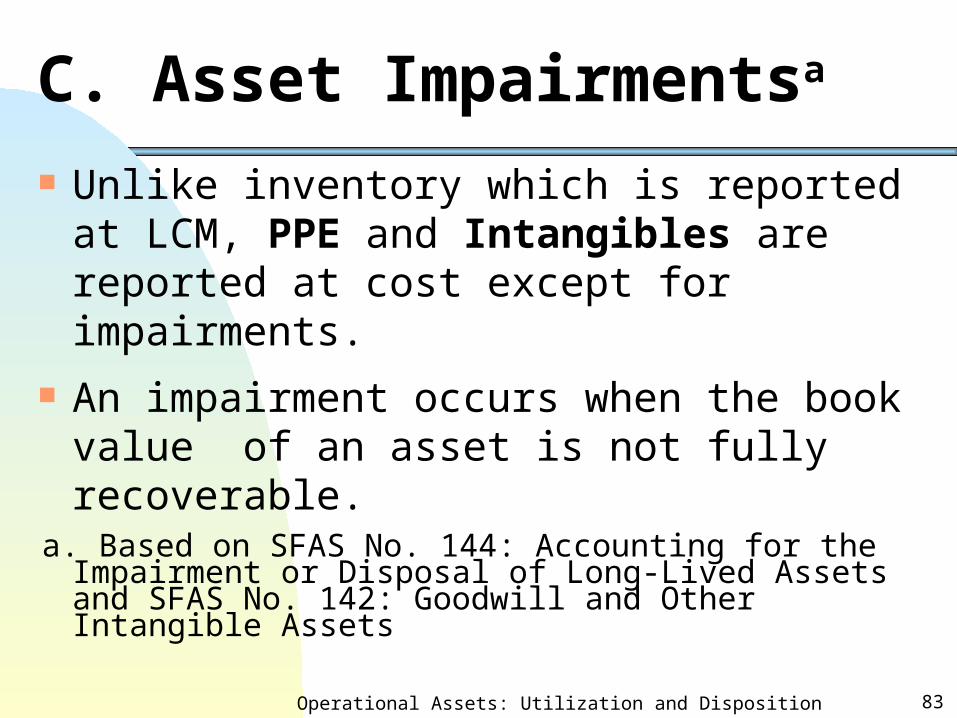

C. Asset Impairmentsa

Unlike inventory which is reported at LCM, PPE and Intangibles are reported at cost except for impairments.

An impairment occurs when the book value of an asset is not fully recoverable.

a. Based on SFAS No. 144: Accounting for the Impairment or Disposal of Long-Lived Assets and SFAS No. 142: Goodwill and Other Intangible Assets

Operational Assets: Utilization and Disposition 84

C. Asset Impairments (all intangibles related impairments (i.e., C1b and C1c) should be deferred until chapter 12 is discussed)

C.1: Operational Assets Held for Use

a. Tangible assets and intangible assets with finite life (i.e., patens, copyrights).

b. Intangible assets with indefinite life other than goodwill (i.e., trade names).

c. Goodwill C.2: Operational Assets Held for Sale C.3: Operational Assets Held to be

Disposed of other than by Sale

Operational Assets: Utilization and Disposition 85

C.1a Operational Assets Held for Use – Tangible Assets and Finite-Life Intangibles (Patents, etc) SFAS No. 144 (effective 2002) requires

test for impairment only when events or changes in circumstances indicate that the book value of this asset (or asset group) may not be recoverable.

For the purpose of this test, assets are grouped at the lowest level in which the cash flows of each group are independent.

Operational Assets: Utilization and Disposition 86

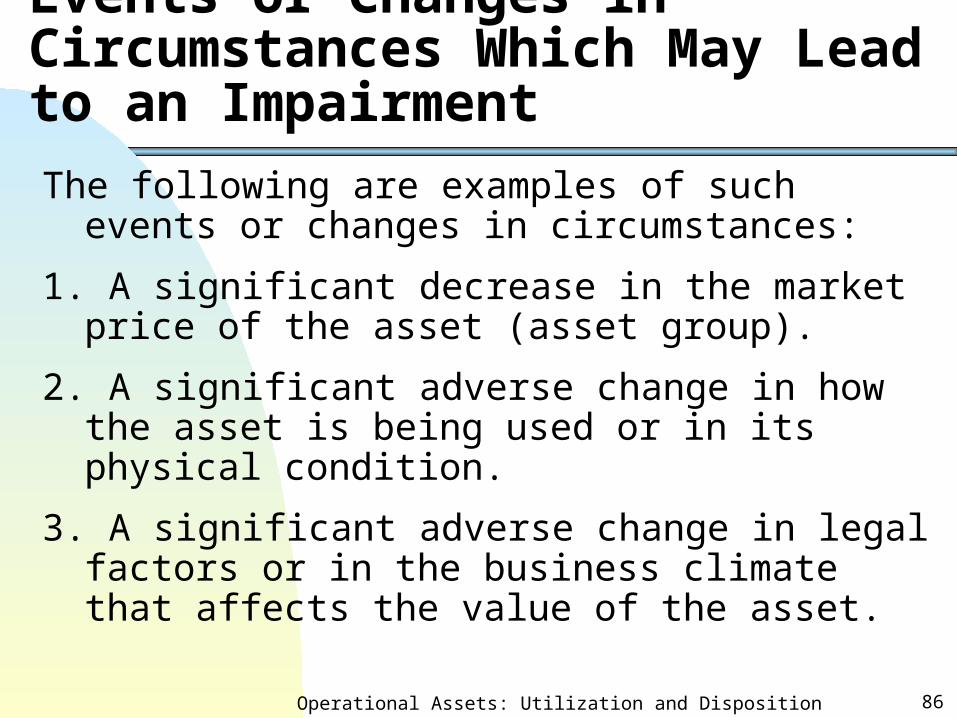

Events or Changes in Circumstances Which May Lead to an Impairment

The following are examples of such events or changes in circumstances:

1. A significant decrease in the market price of the asset (asset group).

2. A significant adverse change in how the asset is being used or in its physical condition.

3. A significant adverse change in legal factors or in the business climate that affects the value of the asset.

Operational Assets: Utilization and Disposition 87

Events or Changes in Circumstances Which May Lead to an Impairment (Cont.)

4. An accumulation of costs significantly in excess of the amount originally expected for the acquisition or construction of an asset.

5. A current-period loss combined with a history of losses or a projection of continuing losses associated with an asset.

6. A realization that the asset will be disposed of significantly before the end of its estimated life. (not in SFAS 121)

Operational Assets: Utilization and Disposition 88

The Accounting Treatment for Impairment (for Held for Use Tangible and finite-Life Intangibles)

Steps:

1. Conduct the Recoverability Test.

2. Compute the Impaired Amount.

Operational Assets: Utilization and Disposition 89

Step 1: Conduct the Recoverability Test Compare the book value (BV) of the

asset with the undiscounted expected future cash flows (EFCF) of the asset (asset group).

If BV > Undiscounted EFCF, the impairment has occurred and the impaired amount should be written off.

Operational Assets: Utilization and Disposition 90

Step 2: Compute The Impaired Amount

Impaired amount = Book value - fair value (if the fair value is available) or

Impaired amount = Book value – estimated fair value1

(if fair value is not available)

1. discounted present value of the future cash flows of the asset can be the estimated fair value

Operational Assets: Utilization and Disposition 91

Write Off the Impaired Amount

Recognition of Impairment Loss:

Loss on Impairment1 $$$$$

Accumulated Depre.$$$$$

1. Reported as part of income from continuing operations, not extraordinary losses.

Operational Assets: Utilization and Disposition 92

Impairment (contd.)

After the write off, the fair value (or the estimated fair value if fair value is not available) becomes the new cost base for depreciation.

No restoration of impaired loss is allowed for tangibles and finite-life intangibles assets held for use.

Operational Assets: Utilization and Disposition 93

iGAAP –Assets Impairments

iGAAP, as in US GAAP, allows reporting impairments on PPE.

iGAAP, as in GAAP, use fair value test to measure the impairments.

In determining the impairment loss, iGAAP compares the book value with the fair value (thus, iGAAP is more strict than US GAAP in this test).

Operational Assets: Utilization and Disposition 94

iGAAP – PPE Valuation and Impairment (contd.) iGAAP, unlike GAAP, permits write-ups

for subsequent recoveries of impairment losses back to the amount before the impairments (i.e., the reversals of impairment losses).

Operational Assets: Utilization and Disposition 95

Impairment (contd.)

Disclosure Requirements of impairment loss:

1. A description of the impaired asset or asset group.

2. The facts and circumstances leading to the impairment.

3.The amount of the loss.

4.The method used to determined the fair value.

Operational Assets: Utilization and Disposition 96

C.1.b. Intangibles with indefinite life Other than Goodwill – (Held-for-Use)

For indefinite life intangibles (i.e., trade names) held for use, impairment test should be conducted at least annually or more often if events or changes in circumstances indicate an impairment.

Test of Impairment: one-step test =>

Compare book value with the fair value.

Operational Assets: Utilization and Disposition 97

C.1.b. (contd.)

If book value > fair value, impairment loss exits and should be recognized.

The fair value becomes the new cost base.

A recovery of the impairment loss is prohibited.

Disclosure requirements are similar to those of tangible and finite-life intangibles.

Operational Assets: Utilization and Disposition 98

C.1.c. Impairment for Goodwill (SFAS 142) The cost of goodwill cannot be directly

associated with any specific identifiable right.

Also, goodwill cannot be separated from the company (or a reporting unit)a as a whole.

a. An operating segment of a company or a component of an operating segment for which discrete financial information is available and segment management regularly review the operating results of that component.

Operational Assets: Utilization and Disposition 99

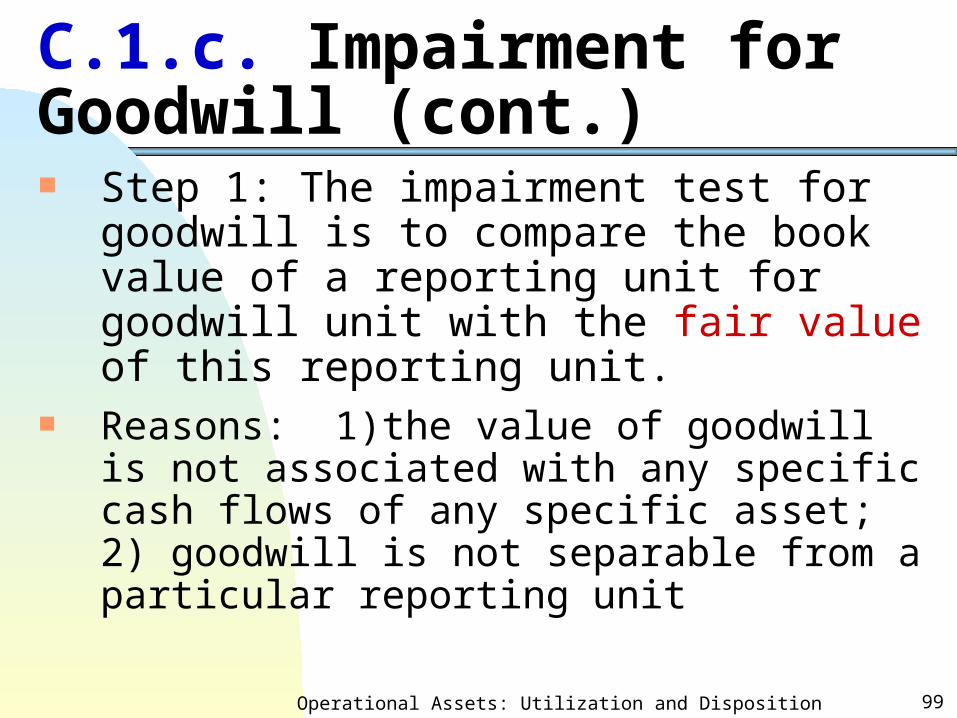

C.1.c. Impairment for Goodwill (cont.) Step 1: The impairment test for goodwill

is to compare the book value of a reporting unit for goodwill unit with the fair value of this reporting unit.

Reasons: 1)the value of goodwill is not associated with any specific cash flows of any specific asset; 2) goodwill is not separable from a particular reporting unit

Operational Assets: Utilization and Disposition 100

Impairment for Goodwill (cont.)

If book value exceeds the fair value for the reporting unit of the goodwill, an impairment loss exists.

The impairment test should be conducted at least annually or more often if impairment indicated.

Operational Assets: Utilization and Disposition 101

Impairment for Goodwill (cont.)

If goodwill is tested for impairment at the same time as other assets of the reported unit, the other assets must be tested first and adjusted for impairment (if any) prior to testing goodwill.

Operational Assets: Utilization and Disposition 102

Impairment for Goodwill (cont.)

Step 2: If goodwill impairment exits, the goodwill impairment loss equals:

Book value of goodwill – implied fair value of goodwilla

a The implied fair value of goodwill is calculated in the same way that goodwill is determined in a business combination.

Operational Assets: Utilization and Disposition 103

Impairment for Goodwill (cont.) Example of calculating implied goodwill of

a reporting unit:

Determination of Implied goodwill:

Fair value of the reporting unit $400 million

Fair value of the reporting unit's $330 million net assets (excluding goodwill)

Implied value of goodwill $ 70 million

Operational Assets: Utilization and Disposition 104

Impairment for Goodwill (cont.)

Determination of impairment loss:

Book value of goodwill $320 million

Implied fair value of goodwill 70 million

Impairment loss 250 million

Operational Assets: Utilization and Disposition 105

C.2 Impairment for Operational Assets to be Sold (SFAS 144) If the impaired asset is to be disposed

ofa by sale, the following principles apply: 1. An impairment test needs to be

conducted when an asset is considered as held for sale.

2. A one-step test: impairment exists when book value exceeds fair vale.

a. Assets which managers have actively committed to sell immediately in their present condition and for which sale is probable, including assets held for sale of discontinued operations.

Operational Assets: Utilization and Disposition 106

Impairment for Operational Assets to be Sold (cont.)

3. The impaired amount = book value - (fair value - disposal cost)a,b.

4. No depreciation after the write-down.

a. Fair value – disposal cost = the net realizable value

b. if the asset is unsold in the subsequent period, the restoration of the impairment loss is allowed when the fair value rebounded in the subsequent period.

Operational Assets: Utilization and Disposition 107

C.3 Impairment for Operational Assets to Be Disposed Other Than by Sale Examples of this type of assets: assets

to be abandoned, exchanged for a similar assets or distributed to owners in a spin-off.

SFAS 144 requires these assets to be treated as assets held for use until they are disposed of.

Operational Assets: Utilization and Disposition 108

Summary of Asset Impairment: Assets Held for Use

Asset Type When to Test Impair. Test

To be used: Tangible and Intangible (finite life))

Events indicate BV not recoverable

Two-Step:

1. BV > EFCF

2. BV - FV

Intangible(indefinite, excluding goodwill)

Goodwill

Annually or more often

Annually or more often

One-Step:

BV – FV

1.BV (reporting unit) > FV

2. BV of goodwill – implied FV

Operational Assets: Utilization and Disposition 109

Summary of Asset Impairment: Assets Held to Be Disposed ofAsset Type When to Test Impair. Test

To be sold(including assets of discontinued operations)

To be disposed of other than sale

When considered held for sale

Considered as held for use until disposal

One-Step: BV > (FV-disposal cost)

No depreciation after write-down

Depre. Life needs to be revised based on APB 20

Operational Assets: Utilization and Disposition 110

The Impact of SFAS 144 on the Disposal Loss of Discontinued operations SFAS 144 applied to assets for both

continuing and discontinued operations (Par. 41).

Therefore, the assets held for sale of the discontinued operations are also reported at the lower of book value or the (fair value - cost to sell), not at the net realizable value as prescribed in APB 30.

Operational Assets: Utilization and Disposition 111

The Impact of SFAS 144 on the Disposal Loss of Discontinued operations (contd.) Also, the future operating losses of the

discontinued operations are no longer recognized before they occur under SFAS 144.

Operational Assets: Utilization and Disposition 112

The Impact of SFAS 144 on the Disposal Loss of Discontinued operations (cont.) The impairment loss (disposal loss) of

the assets held for sale under the discontinued operations is reported as a component of the discontinued operations.

See Chapter 4 notes for detailed discussion of the reporting of the operating results and disposal results for discontinued operations.

Operational Assets: Utilization and Disposition 113

Impairment Losses and Earnings quality Similar to the write-down of inventory

and restructuring costs, impairment losses can have significant adverse impact on the current year's income number.

When fair value needs to be estimated, the estimation of fair value requires the forecast of future cash flows generated by the asset.

Operational Assets: Utilization and Disposition 114

Impairment Losses and Earnings quality (contd.) Companies can understate future

cash flows to understate the fair value and overstate the write-down amount.

By writing down large amounts of operational assets, companies are able to increase future earnings by lowering future depreciation, depletion or amortization.