international bank for reconstruci1on...

TRANSCRIPT

RESTRICTED

Report No. PA-64a

Thds report b for offidil use only by the lank Gioup and specifafly authotized orpnizationsor penonL t nmay not be pubiished, quoted or cited without Bank Group authorization. TheBank Group does not accept teaponsibRity for the accuracy or completeness of the report.

INTERNATIONAL BANK FOR RECONSTRUCI1ON AND DEVELOPMENT

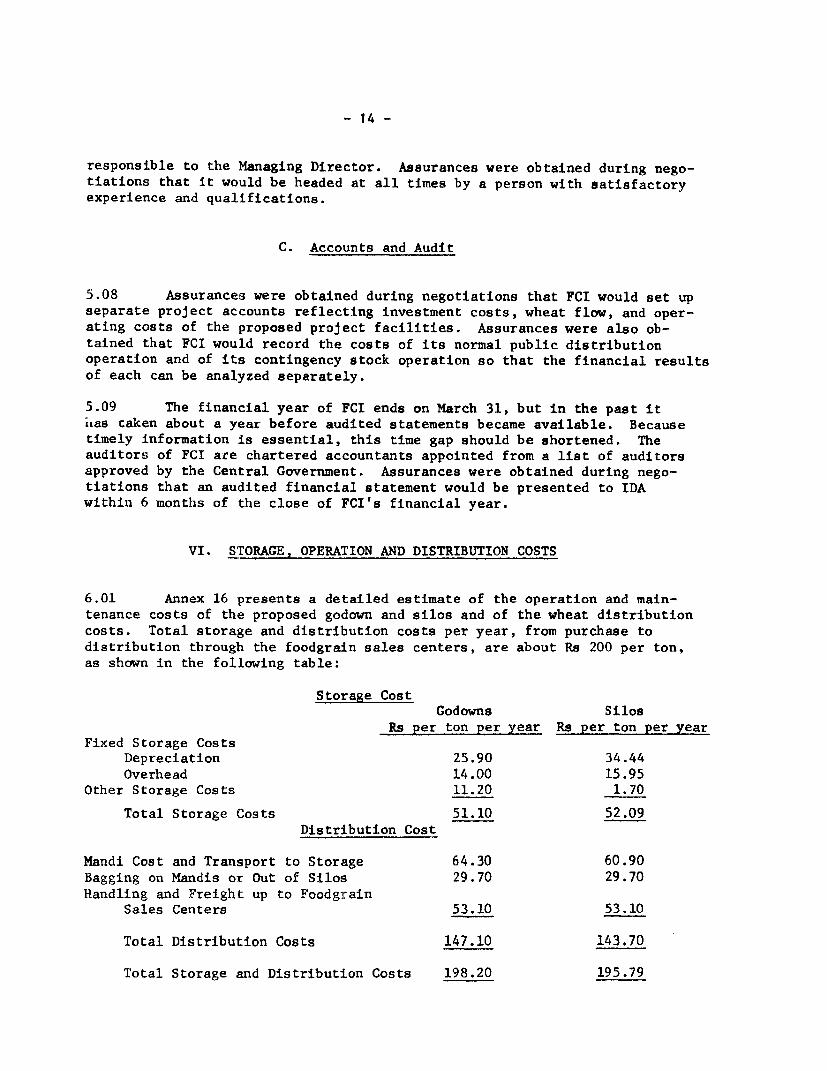

INTERNATIONAL DEVELOPMENT ASSOCIATION

APPRAISAL OF

A WHEAT STORAGE PROJE

INDIA

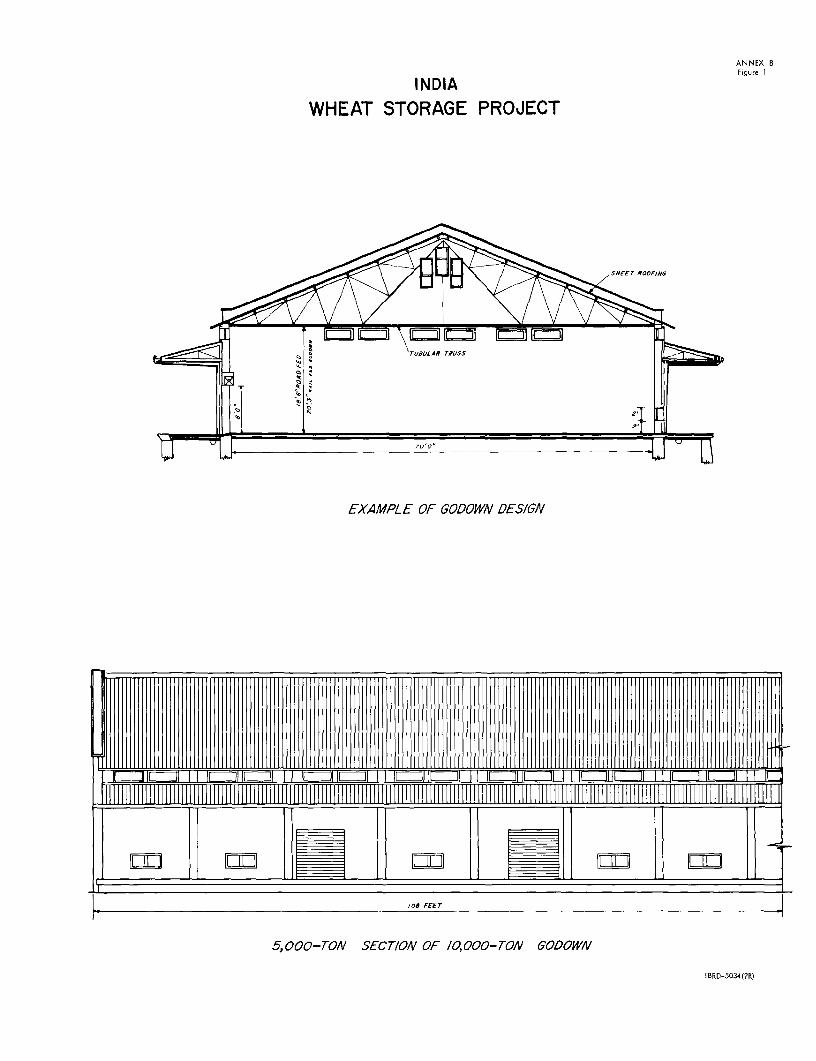

June 15, 1971

Agriculture Projects Department

Pub

lic D

iscl

osur

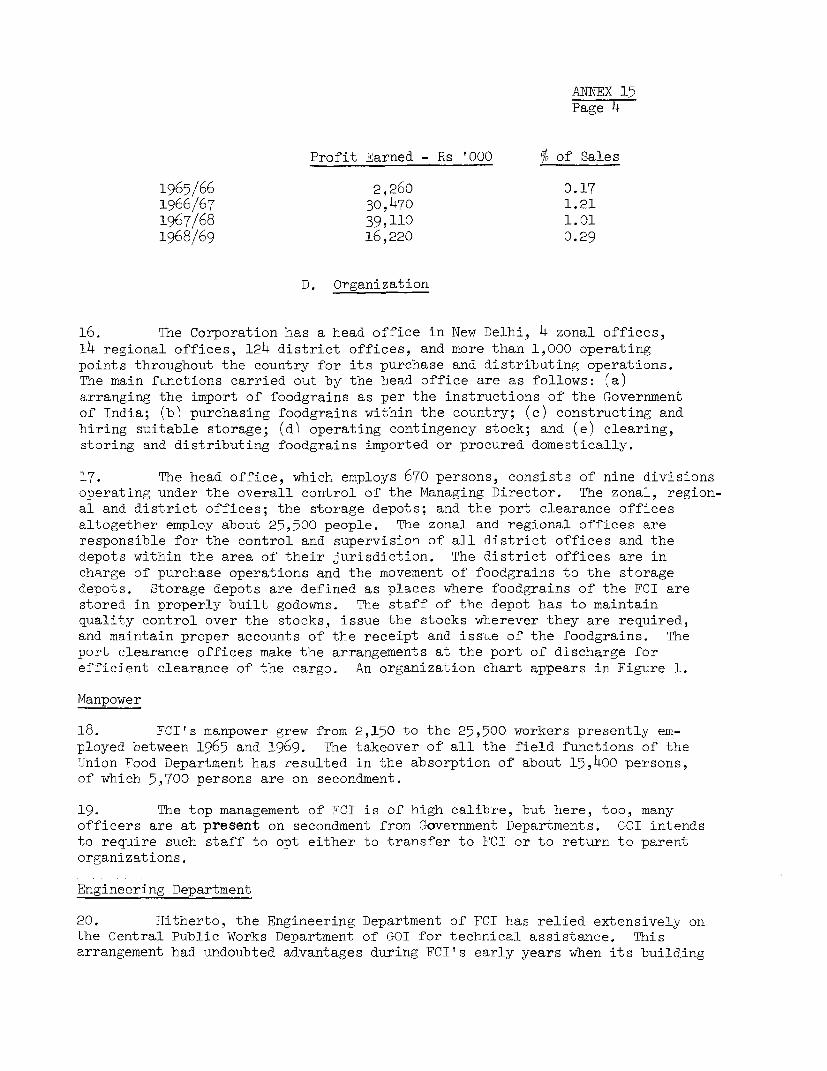

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY B2UIVALENTS

US$ 1.00 - Rupees (Rs) 7.50Rs1 = US$ 0.13Rs 1 million = US$ 133,333

WEIGHTS AND MEASURES

1 m ton = 1000 kg1 kg = 2.20 lb1 meter = 3.28 ft

ABBREVIATIONS

GOI = Government of IndiaFCI = Food Corporation of India

INDIA

WHEAT STORAGE PROJECT

TABLE OF CONTENTS

Page No.

SUMMARY AND CONCLUSIONS .............................- i

I. INTRODUCTION .................. . ........ 1 ...... 1

II. BACKGROUND ............................................ 1

A. Foodgrain Production Trends . .. 1B. Public Distribution of Foodgrains . . 4C. All-India Public Storage Requirements. 5

III. THE PROJECT AREA. 6

IV. THE PROJECT. 7

A. Project Description . . ...................... .. 7B. Technical Features .... 8

Site Selection.... 8Flat Storage (Godowns).... 8Silos.... 8Technical Training.... 9All-India Grain Storage and Distribution Study 9

C. Construction Schedule.... 9D. Cost Estimates ... 10E. Proposed Financing .... 11F. Procurement .... 11G. Disbursement . ... 12

V. ORGANIZATION AND MANAGEMENT .. 12

A. Operations of the Food Corporation of India 12B. Cost Control ... 13C. Accounts and Audit .14

VI. STORAGE, OPERATION AND DISTRIBUTION COSTS . .14

VII. BENEFITS AND JUSTIFICATION .15

A. Choice of Location .. 15B. Choice of Storage Method - Godown Versus Silo 16C. Economic Rate of Return .16

This report is based on the findings of an IDA mission in March/April 1970,composed of Messrs. L. Helmers, S. Reutlinger and Miss J. Noel (IDA); Messrs.R. Crofts and H. Heckman (IDA consultants); and L. Werin (Swedish Governmentconsultant).

-2-

Page No.

VIII. RECOMMENDATIONS ....................................... 18

ANNEXES

1. Gross Production of Foodgrains2. Net Production, Imports, Stock Changes and Consumption of Foodgrains3. Graph of Net Production and Consumption of Foodgrains4. Wholesale Price Index Numbers - Foodgrains and Manufactures5. Public Distribution of Foodgrains

Table 1 - Public Distribution, Local Procurement and ImportsTable 2 - Total Public Procurement and Public Distribution by

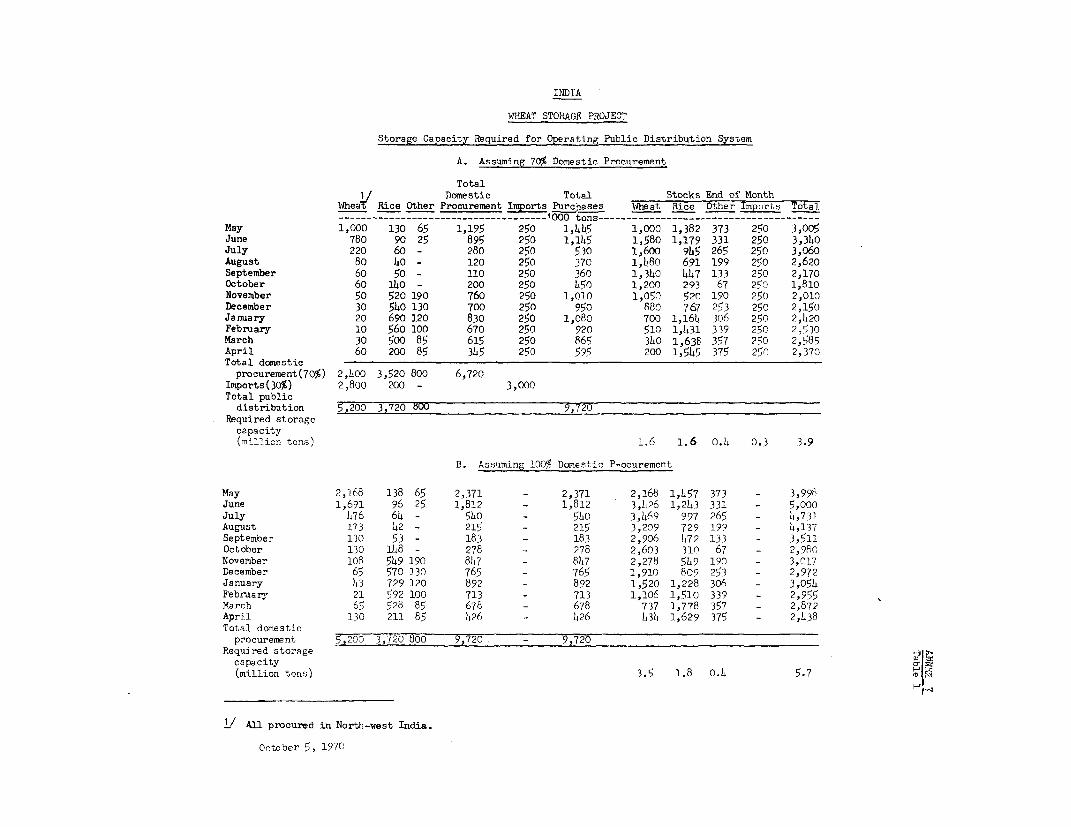

State and Main Foodgrains6. Total Public Storage Capacity and Stocks7. Analysis of Operational Storage Requirements

Table 1 - Storage Capacity Required for Operating Public Distri-bution System

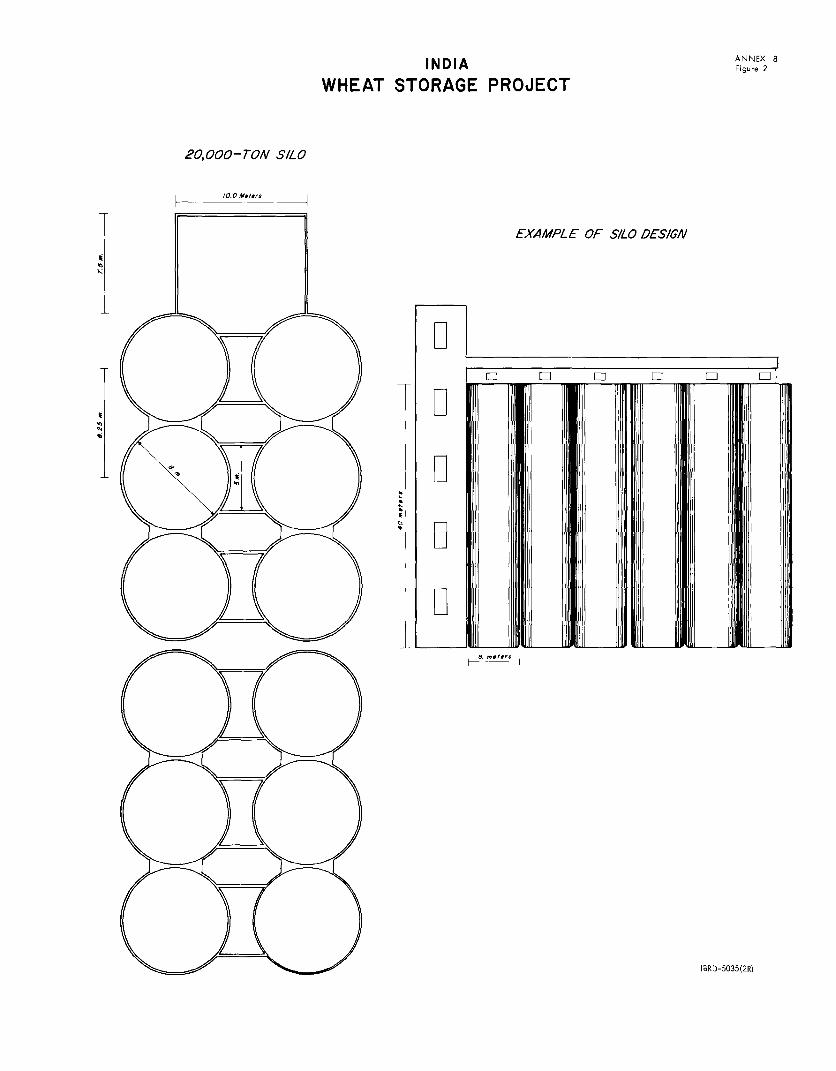

8. Technical Specifications for Godowns and SilosFigure 1 - Example of Godown DesignFigure 2 - Example of Silo Design

9. Tentative Location of Godowns and Silos10. Site Selection Criteria11. All-India Grain Storage and Distribution Study12. Time Schedule, Godown and Silo Construction13. Construction Costs of Godowns and Silos14. Estimated Schedule of Disbursements15. The Food Corporation of India

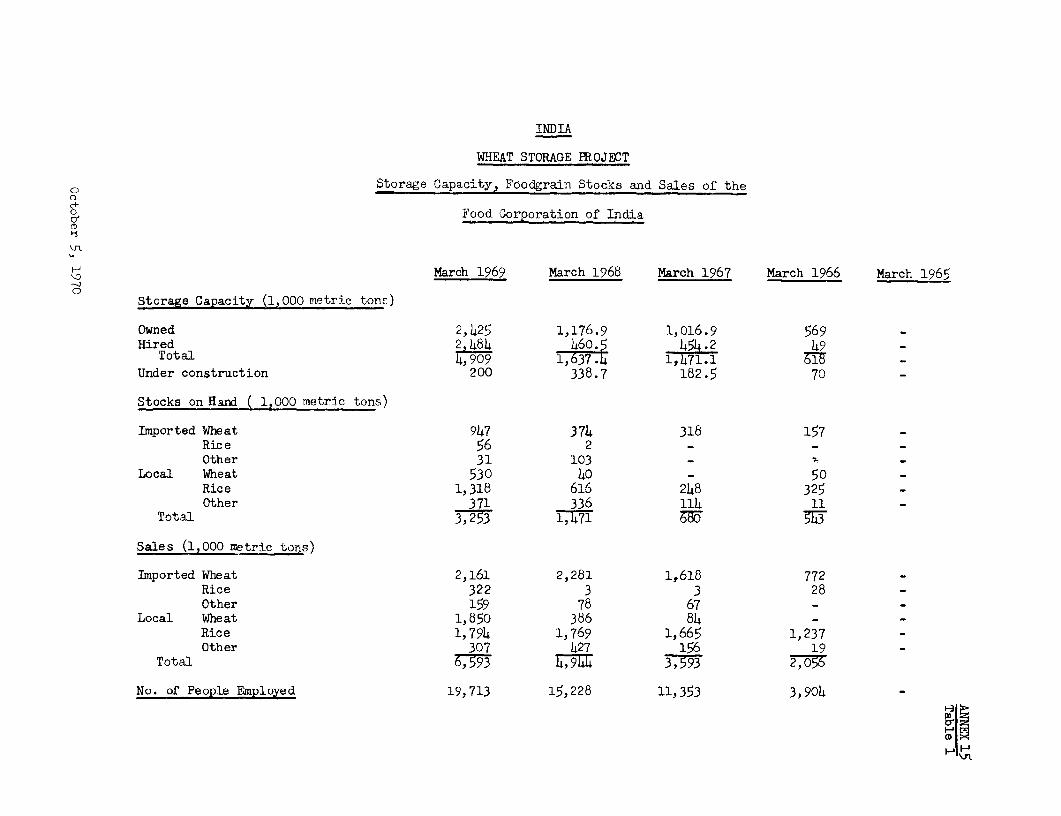

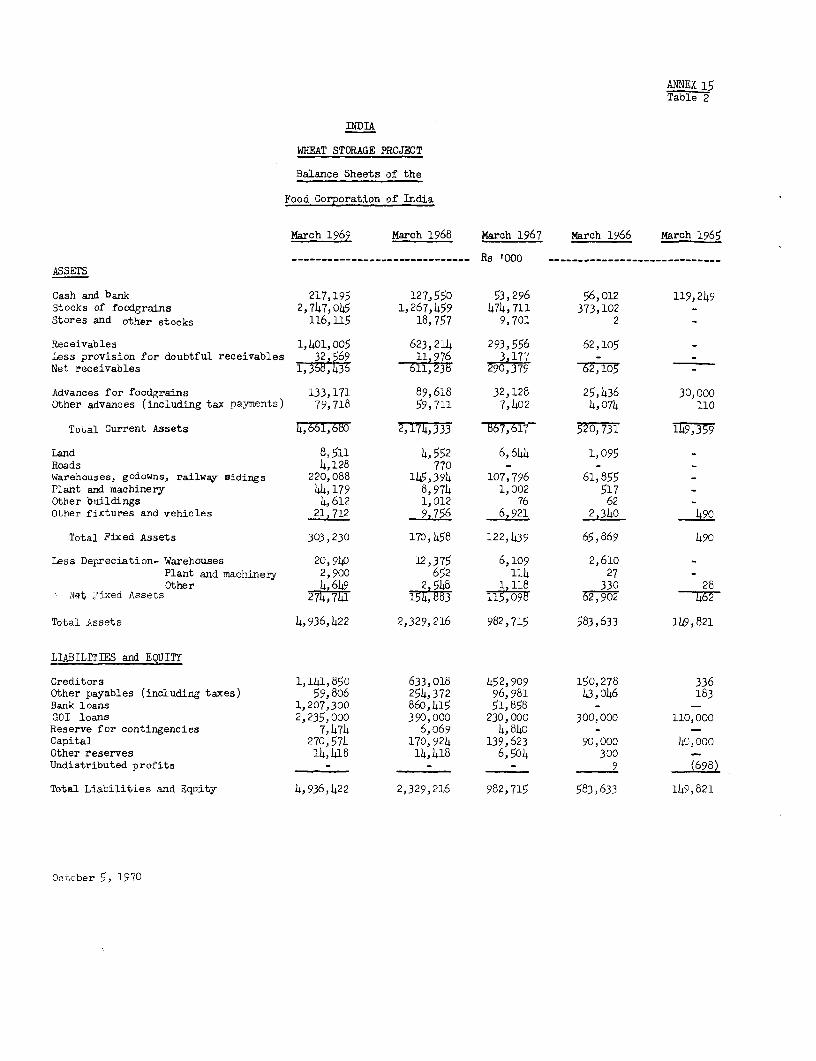

Table 1 - Storage Capacity, Foodgrain Stocks and Sales of theFood Corporation of India

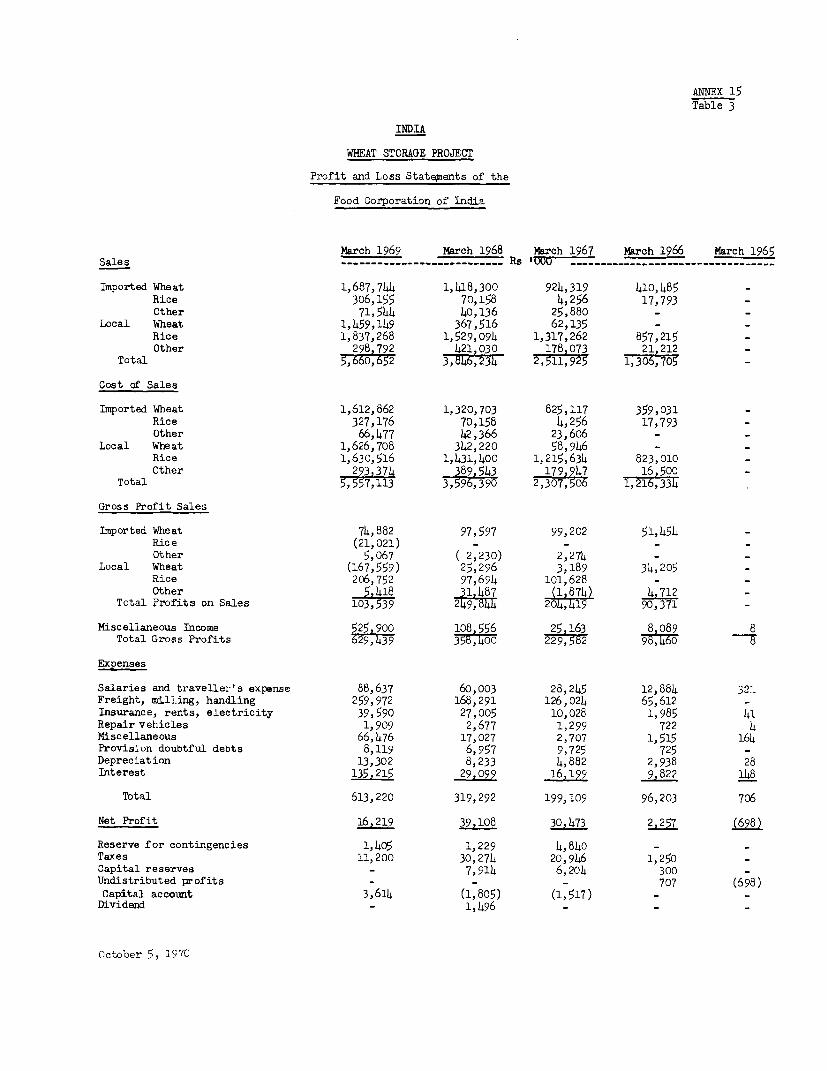

Table 2 - Balance Sheets of the Food Corporation of IndiaTable 3 - Profit and Loss Statements of the Food Corporation of

IndiaFigure 1 - Organization Chart of the Food Corporation of India

16. Storage and Distribution Cost17. Analysis of Godown Storage Versus Silo Storage18. Grain Storage Losses19. Incremental Return Analysis of Godown Storage Versus Silo Storage20. Economic Rate of Return of Proposed Facilities21. Economic Rate of Return of Facilities Used for Contingency Stock Opera-

tionsTable 1 - Benefits of Domestic SalesTable 2 - Import Price Savings

MAP - Location of Proposed Storage Facilities

INDIA

WHEAT STORAGE PROJECT

SUMMARY AND CONCLUSIONS

i. This report contains the appraisal of a wheat storage project which

would be the first Bank Group project for grain storage facilities in India.The total project cost is US$15.9 million. The Swedish Government hasoffered to contribute US$5.0 million and the proposed IDA credit would also

be for US$5.0 million. Although IDA and the Swedish Government would finance

different components, the Association would supervise the execution of the

entire project.

ii. Total foodgrain production in India is at present about 94 million

tons, of which about 35 million tons is marketed. Publicly owned storagecapacity (owned by Central and State Governments) total 5.0 million tons.

Privately owned storage capacity is not known. Estimates of grain losses

range between 7% and 12% of total production. However, as production in-creases, particularly of wheat, losses on the incremental production will be

much greater unless storage capacity expands equivalently.

iii. The project would help meet urgent storage needs resulting from

recent sharp increases in wheat production in North-west India and providethe basis for developing a more effective system for grain storage and dis-tribution throughout India. The project consists of (a) planning, designing,

constructing, and equipping 10 silos of 20,000 tons each and 10 flat storageunits of 10,000 tons each, providing a total capacity of 300,000 tons; (b)training silo personnel; and (c) conducting a study of India's foodgrain

storage and distribution.

iv. The proposed project storage facilities would be managed by theFood Corporation of India (FCI), which at present owns about 2.8 million tons

of storage capacity. Consultants would help FCI prepare the silo designs(FCI has acceptable designs for the flat storage units) and the tender docu-ments and wouldi supervise construction. The FCI, a public corporation, was

established in 1965 to operate storage facilities in connection with the Gov-

ernment's support price program and to undertake the interstate public dis-tribution of foodgrains. The Government is also considering having a 5-mil-lion-ton contingency stock operation in anticipation of the time when Indiabecomes self-sufficient in foodgrains. This stock would be used to meetshortfalls in marketable production during bad harvest years and would beoperated by FCI.

v. The IDA credit would help finance the construction of godowns,electrical and mechanical. equipment and the costs of consultants, trainingand the All India Grain Storage Study. The SIDA credit would help financethe construction of silos. Electrical and mechanical eqtuipment would be

procured under international competitive bidding and constitute the majorforeign exchange component of the project, about US$3.0 million allowingfor contingencies, representing about 19% of total project cost and 60%of the IDA credit.

- ii -

vi. As a result of the proJect, wheat losses during storage for oper-ational purposes would be reduced equivalent to a net saving in foreignexchange of about JS$3.0 million per annum. The economic rate of return ofthe project is estimated at 25%.

vii. The project is suitable for an IDA credit and a Swedish Govern-ment credit, each in the amount of US$5 million, on standard terms. Thecredits, totaling US$10 million, would cover the foreign exchange compon-ent of project costs and about 50% of local costs. The borrower would bethe Government of India. The IDA and Swedish Government credits would beonlent to FCI for 19 years, including 4 years' grace, at 7% interest. Theseare the normal terms for lending to state enterprises in India.

INDIA

WHEAT STORAGE PROJECT

I. INTRODUCTION

1.01 The Government of India (GOI) has requested IDA and Swedish Gov-ment financing for the establishment of modern grain storage and handlingfacilities to meet India's rapidly increasing storage requirements. Theproject would help meet the most urgent needs in North-west India broughtabout by the increase in wheat production. Ten flat storage units of10,000-ton capacity each and 10 silos of 20,000-ton capacity each would beconstructed, and there would be provision for training silo operators.A study would also be conducted to investigate ways of further improvingand expanding India's storage and handling facilities.

1.02 The total estimated cost of the project is US$15.9 millionequivalent. The proposed IDA credit would be for US$5 million. The Swed-ish Government would also contribute US$5 million on the same terms andconditions as IDA. GOT would supplement the IDA and SIDA funds with US$5.9million of its own funds and lend a total of US$15.9 million to the FoodCorporation of India, a public body charged with the interstate public dis-tribution of foodgrain, which would operate the facilities.

1.03 In June 1969, a Bank identification mission visited India todiscuss preparation of the project. FCI prepared the project and submittedits report to IDA in August 1969. This report is based on the findings ofan IDA appraisal mission in March/April 1970, composed of Messrs. L.Helmers, S. Reutlinger and Miss J. Noel (IDA); Messrs. R. Crofts andH. Heckman (IDA consultants); and L. Werin (Swedish Government consultant).

1.04 The total of past Bank Group lending for India's agricultureis nearly US$310 million as of June 30, 1971. Until 1969, most Bank Grouplending was for irrigation projects and the Bank Group is continuing tofinance such projects. Emphasis is now also being given to direct on-farminvestments and ancillary services. In the past financial year, there havebeen four Agricultural projects, three of which were for agricultural credit(Andra Pradesh, US$24.4 million, 226-IN; Haryana, US$25.0 million, 249-IN;Tamil Nadu, US$35.0 million, 250-IN). The other was for agricultural aviation(US$6.0 million, 230-IN).

II. BACKGROUND

A. Foodgrain Production Trends

2.01 The population of India, currently estimated at 550 million, hasbeen growing at an annual rate of about 2.5% during the last decade. The

- 2 -

growth of gross national product (GNP) over this period was about 3.5% perannum, or only about 1% per capita annually. This disappointing perform--ance was due mainly to the low average growth of agriculture, the largestsector, which grew at only 3% per annum. Agriculture produces nearlyhalf of GNP, employs about 70%.1 of the labor force and generates over halfthe foreign exchange earnings from the export of goods. Within the agri-cultural sector, the growth rate of foodgrains (75%U of the total croppedarea) was especially poor; at just under 2.5%, the rate of increase washardly equal to the rate of population growth during most of the lastdecade.

2.02 Foodgrain production and consumption statistics for the period1950 to 1969 are presented in Annexes 1 and 2 and a graphical presentationis in Annex 3. Net production 1/ of foodgrains grew from about 53 milliontons in 1950 to about 82 million tons in 1969, while net consumption offoodgrains grew from about 56 million tons to about 86 million tons duringthe same period. From 1950 to 1963, the average annual growth for foodgrainprices (especially those of wheat) lagged behind those of manufactured goods.It was not until 1964/65 that the price index for foodgrains rose above thatfor manufactures. Annex 4, showing the wholesale price indexes for food-grains and manufacture for the past 20 years, presents this price develop-ment. The policy of low agricultural prices weakened incentives to agricul-tural producers.

2.03 A new agricultural strategy was adopted in 1966 based on theconcentration of development efforts in priority areas. New high-yieldingvarieties of wheat and rice were imported; research was concentrated oncross-breeding between the imported and indigenous stock; and a major effortwas made to increase the availability and encourage the use of inputs, notablywater and fertilizer, along with improved seeds. The bad crop years of 1966and 1967 increased foodgrain prices relative to manufactured goods. TheGovernment had also instituted in 1965 a price support program that kept food-grain prices at the new higher level. The program's exact effect on food-grain production cannot be ascertained, but since its introduction, foodgrainproduction growth has increased from 2.3% to 2.9% per annum nationally and,in the North-west zone, wheat production has increased from just under 4% toabout 15% per annum.

2.04 India's net wheat production increased dramatically from 10.8million tons in 1965 to 16.4 million tons in 1969. This increase was notdue solely to good weather. Hligh producer prices (Annex 4) and the suc-cessful adaptation to Indian conditions of the high-yielding seed varietiesimported from Mexico provided the requisite economic inducements. Farmersin the wheat belt (especially in Punjab and Haryana) responded to the new

1/ According to GOT statistics, net production differs from gross produc-tion by the amount provided for feed, seed requirements and wastage,which is estimated at about 12.5% of the gross production of all food-grains. In 1969, gross production was about 94 million tons.

- 3 -

opportunities by using more fertilizer and by utilizing credit and theirown savings for on-farm investment, especially in tubewells and mechaniza-tion.

2.05 The increase in wheat production in North-west India has resultedin a substantial relaxation in zoning restrictions. Up to 1967, eachstate was considered a single zone from which foodgrains could not be ex-ported through private trade to other zones. The objective of this systemwas to facilitate the procurement of foodgrains by Government in the surplusstates and permit their resale in deficit states at controlled prices. Freetrade of wheat is now allowed in all of India, except in Bombay and Calcutta,and price differentials of wheat between zones have returned to normal. Withthe exception of seven states, zonal restrictions still apply to rice.

2.06 No comparable breakthrough has yet been achieved in rice produc-tion. Net production of rice in 1969 was about 37 million tons (Annex 2).Some new strains have proved susceptible to virus and bacterial disease,while others have encountered consumer resistance because of differingpalatability. In many rice growing areas, the small size of holdings,coupled with tenancy and credit difficulties and the lack of irrigation anddrainage, have retarded the spread of new varieties.

2.07 For the last 20 years, India has had to import substantial quan-tities of foodgrains. During the period 1950-59, foodgrain imports amountedto an average of 2.6 million tons per annum, which increased to an averageof 5.0 million tons for the period 1960-65. The successive drought years,1966 and 1967, showed imports of more than 10 million tons and 8 milliontons, respectively. Because of the increase in wheat production, the food-grain consumption-production gap decreased to about 3.5 million tons foreach of the years, 1969 and 1970. The Government expected that India wouldbe self-sufficient in foodgrains in 1971 and the Fourth Five-Year Plan(1969-74) calls for halting food imports on concessional terms in 1971 andfor an increase in net production of total foodgrains from 82 million tonsin 1969 to 110 million tons by 1974. This overall target of a 5-1/2% growthrate over the next 5 years appears optimistic.

2.08 Progress towards the wheat target (21 million tons net prodluctionby 1974 as against 16.4 million tons in 1969) appears reasonable. Althoughyields on present varieties show signs of leveling off, there i.8 stillroom for continued improvement of irrigation facilities and the introduc-tion of newer, more fertilizer-responsive and disease-resistant varieties.Nothing so encouraging, however, can be perceived for the other foodgrains.The difficulties with rice (target, 46 million tons as against 36.8 milliontons in 1969) have been discussed (para 2.06), and, although newer, bettervarieties are becoming available, their rate of spread is likely to remainslow for some time. Finally, for other foodgrains (target, 43 million tonsas against 29.1 million tons in 1969), although some progress has been madein the production of hybrid seed, the limited market for coarse grains andpulses and their susceptibility to pests are likely to restrict their pro-duction.

- 4 -

2.09 It is difficult to predict when India will become self-sufficientin foodgrains because this depends on the attainment of targets for the ex-pansion of the irrigated areas and the success of rice research currentlyunderway. As it is not possible to predict what the results of this researchwill be, projections concerning the actual date of self-sufficiency aresubject to a high margin of error. It is, however, quite clear that storagerequirements will increase because domestic supplies procured during peakperiods will continue to replace imports distributed evenly over the year.

B. Public Distribution of Foodgrains

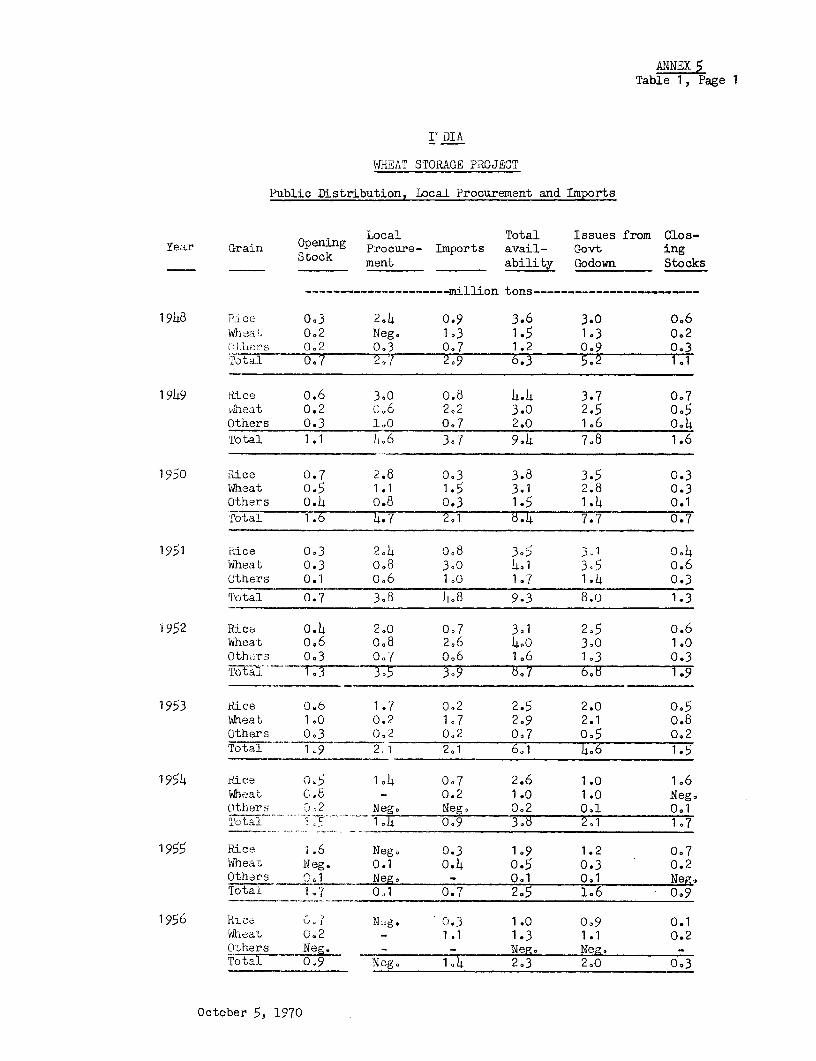

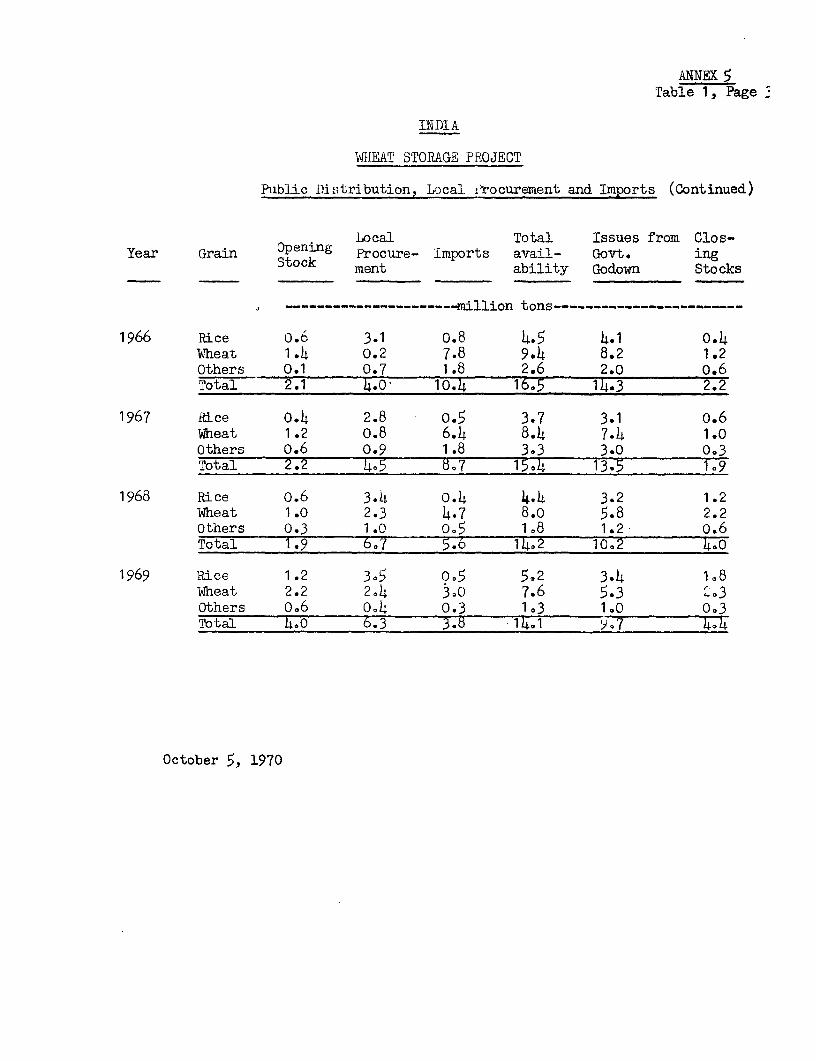

2.10 India's agriculture has always been subject to the vagaries ofthe weather, and large year-to-year fluctuations in foodgrain productionare common. There have been six distinct periods of famine since 1900.Under such conditions, the need for public distribution during periods ofshortfall is obvious. Since World War II and up to 1965, the responsibil-ity for public foodgrains procurement and distribution was shared betweenthe Food Department of the GOI, which was responsible for imports andtheir distribution to the states, and State Government agencies, whichwere handling local procurement and distribution within their respectivestates. Public distribution of foodgrains varied from as much as 1.6million tons in 1955 to 14 million tons in 1966. The background of thepresent situation in public distribution is outlined in Annex 5.

2.11 The new agricultural policy that evolved in the mid-1960's, withits emphasis on incentive and support prices to producers and the operationof a contingency stock (para 2.15) of foodgrains, necessitated the creationof a new, all-India executive agency. The Food Corporation of India (FCI)was therefore set up and began operations on January 1, 1965. FCI hasnow taken over all public distribution work of the Food Department and isresponsible for all interstate foodgrain movements. While the Food Depart-ment's task was mainly to take care of public distribution during periodsof serious shortfall, the FCI undertakes public distribution during normalyears as well. The function of the FCI is the procurement and storage offoodgrains and transport to its sales centers that supply the fair priceshops.

2.12 The fair price shops are owned by licensed private retailers.They were set up to provide foodgrains to the population during periods offamine, but they now also provide the lower quality foodgrains at controlledprices during normal years. In 1968, there were about 135,000 fair priceshops in India. Because the higher income consumers prefer to buy thebetter foodgrains on the open market, the system caters, during normalyears especially, to the lower income consumers. The total public distri-bution of foodgrains during normal years is now about 9.7 million tons.The rest of the marketable surplus (excess of net production over on-farmconsumption) in foodgrains, estimated at about 30% of total net production,or about 25 million tons, is distributed through private merchants.

2.13 While FCI's distribution price for rice covers the purchase priceand the direct storage and transport costs, such is not the case for wheat.

- 5 -

The difference between the price of domestically procured wheat and thecommon issue price at which FCI must sell does not allow sufficient margin

to show a profit or even break even (para 5.02). The deficit on locallyprocured wheat was covered in the past by the profits on imports, which werebought at a lower price but sold at the same issue price. Now, however, the

proportion of domestic purchases to imports is increasing, and, as a result,FCI incurred a deficit of Rs 230 million (US$30 million) in 1969/70, whichwas covered by the Government.

2.14 Government intends to pursue the public distribution policyuntil it is no longer necessary. It is willing to subsidize such distri-

bution because the high support prices promote an expansion of wheat pro-duction and because it considers the provision of low priced wheat to the

low income consumers essential. The program as it is now operating throughthe FCI and the fair price shops is relatively efficient and entails lessadministrative work than a system of direct rationing or money grants.

2.15 India has at present about 2 million tons of foodgrain contingencystocks that would be used when marked falls in foodgrain production occurduring a bad harvest year (para 2.16). Although grain production has in-

creased in the past few years, imports were available on concessionaryterms and most of the present contingency stocks have been built up fromimports. These stocks are at present stored mainly with the State Govern-ments. The Central Government has indicated that it intends to increasethe stock to about 5 million tons by the time India becomes self-sufficientand that FCI should then manage the operation.

C. All-India Public Storage Requirements

2.16 India's public storage requirements consist of facilities foroperational stocks and contingency stocks. Operational public stocks arethose that are stored following harvest (or import) and used to smoothpublic distribution of grains to consumers throughout the year. Contin-gency or emergency stocks are those that are placed in storage followinga surplus harvest (or import) and used to meet grain shortfalls in badharvest years, which may be 3 or 4 years later. Whereas foodgrains canbe stored in silos up to 3 years, foodgrains stored in flatstores must be

replaced every year or they deteriorate too much in quality. Thus, it isnot likely that the same foodgrains would remain stored for the entire con-tingency waiting period, making it impossible to earmark a certain physi-cal quantity of foodgrains as being contingency stocks. Operational stocksand contingency stocks are interchangeable, but it is the combined totalof the two that determines a country's storage requirement. Storage fa-

cilities containing contingency stocks at harvest time cannot be used tostore operational stocks at that time.

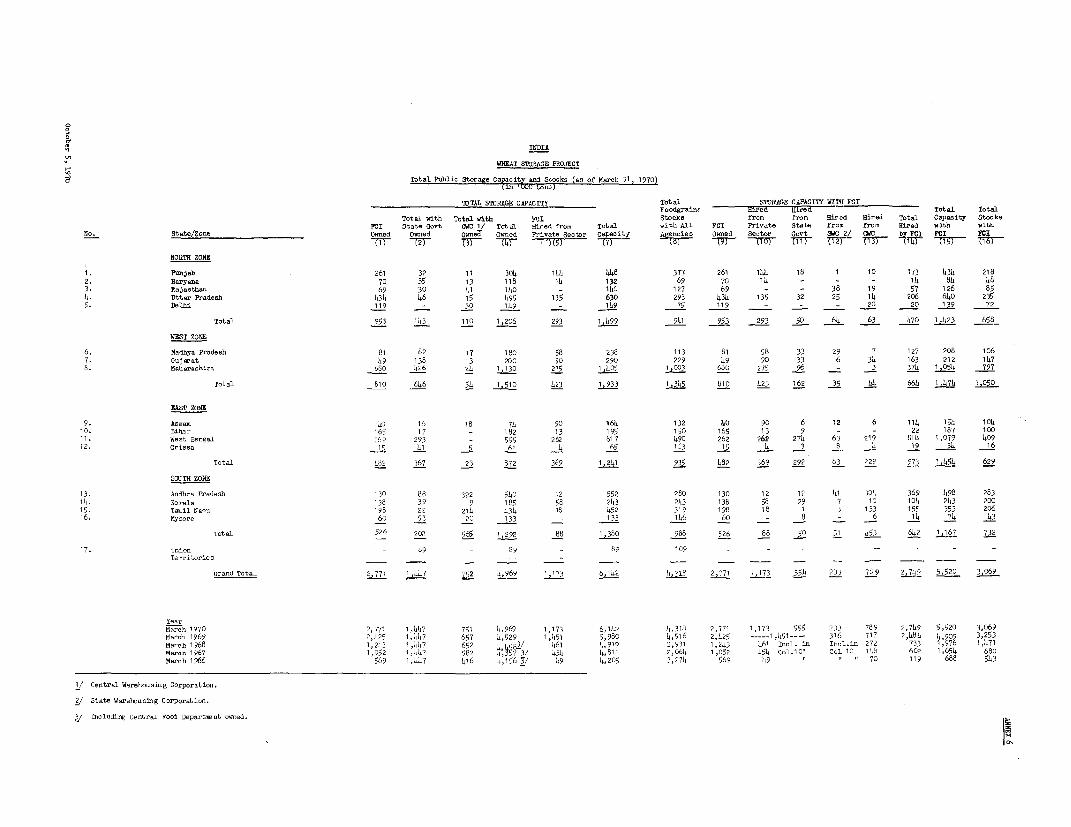

2.17 India has at present about 5.0 million tons of publicly ownedstorage facilities (Annex 6). The country's operational public storagereqtuirements are estimated to be about 3.9 million (Annex 7) and it hasa contingency stock of about 2.0 million tons. Its total public storagerequirement is therefore 5.9 million tons.

- 6 -

2.18 The deficit between available public facilities (5.0 milliontons) and reqtuired Public facilities (5.9 million tons) is covered byhiring storage capacity from the private sector. This, however, is alsoin short supply. Furthermore, a substantial part of the facilities (publicand private) appears to be located in the wrong areas and is of poor qual-ity, causing grain losses. Unfortunately, no exact data exist on theobsolescence of the existing facilities and no study has been made todetermine whether, in fact, the facilities are of the right type and lo-cated in the right areas (a study on this matter is proposed, as describedin para 4.11).

2.19 The UNDP/SF is at present investigating the best methods foron-farm storage. The project will end in 1972 and its findings should bevaluable in launching a national program for the improvement of on-farmstorage and handling procedures at a later stage.

2.20 When India becomes self-sufficient, the public distributionprogram may well be partly abolished. Probably at least as much storagecapacity would, however, still be necessary for the private trade. Thestorage capacity that would become available if public distribution wereabolished could be transferred to the private trade or the Central Ware-housing Corporation, a public organization whose main functions are toprovide improved storage facilities to the private trade and to issuenegotiable warehouse receipts. In the event that facilities financed byIDA were transferred, consultations with IDA would be required.

III. THE PROJECT AREA

3.01 The project would be located in the states of Punjab, Haryana,Rajasthan and Uttar Pradesh, which together constitute India's wheat belt.About 75% of India's wheat is produced in the area and nearly all publicprocurement takes place there. Such procurement in the area has grownfrom 400,000 tons in 1965, out of a net production of 8.3 million tons, to2.4 million tons in 1969, out of a net production of 14.0 million tons.Public procurement was expected to reach about 3.7 million tons in 1970.

3.02 Since farms have no adequate on-farm storage, the wheat has tobe delivered to the market, and about 85% of total wheat marketings takeplace during the post-harvest months of April to June. In 1969, therewere 1.2 million tons of public storage facilities in the project areawhere 1.6 million tons were required (Annex 7).

3.03 To accommodate the public procurement (para 3.01), additionalfacilities were hired from the private sector. These too, however, werein short supply, making it necessary to use buildings such as schools forstorage places. Some wheat was merely placed in heaps on the ground.

3.04 Losses during storage in these make-shift facilities were great;wheat stored in such manner was especially susceptible to substantial damagein the event of early monsoons. As a first-stage project, the Governmenthas asked IDA to finance 300,000 tons of storage facilities.

-7-

3.05 The proposed project storage facilities would lessen the strainon rail transport during the post-harvest period; minimize the need forany later cross-hauling; provide tangible assurances to farmers of theGovernment's ability to sustain support price buying operations, itselfa significant factor in the maintenance of increased production; and takeadvantage of the favorable climatic conditions that exist in the area,which would minimize storage losses.

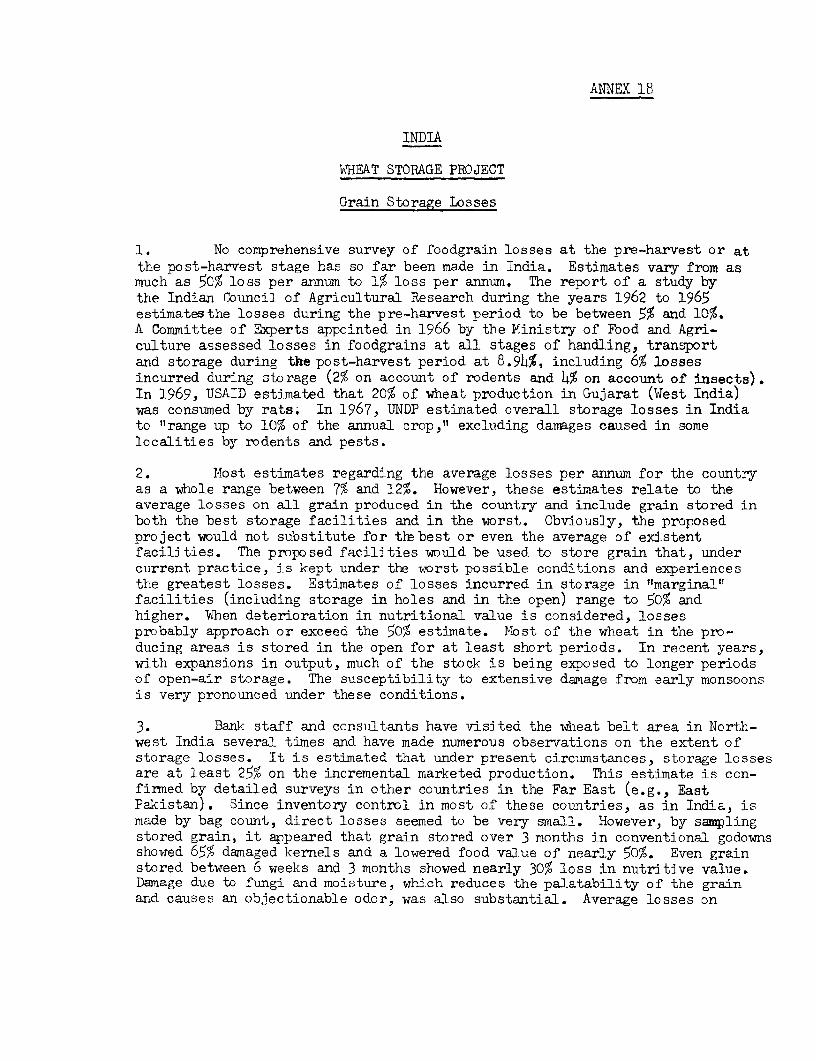

3.06 Most estimates regarding the storage losses per annum for thecountry as a whole range between 7% and 12%. However, these estimates relateto the average losses and include grain stored in both the best storagefacilities and in the worst. Obviously, the proposed facilities would notsubstitute for the best or even the average of existing facilities but wouldbe located in areas where, under current practice, grain is kept under theworst possible conditions and where the greatest losses occur. Estimates oflosses incurred in such marginal facilities (including storage in holes andin the open) range to 50% and higher. A conservative estimate is that about25% of the incremental wheat marketings in North-west India in 1969 were lost.The study referred to in paragraph 4.11 would include investigation of actualfoodgrain losses, since no such survey has so far been made in India.

IV. THE PROJECT

A. Project Description

4.01 The proposed project forms part of an ongoing program of food-grain storage facility construction for both operational and contingencystock purposes. The project would consist of (a) planning, designing,constructing and equipping 10 silos of 20,000 tons each and 10 godowns(flatetores) of 10,000 tons each in North-west India (i.e., the states ofPunjab, Haryana, Rajasthan and Uttar Pradesh); (b) training silo personnel;and (c) conducting a study on India's foodgrain storage and distribution.The proposed facilities would be used for wheat storage and would beconstructed in about 3 years.

4.02 FCI has prepared outline designs for the godowns and would engagelocal consultants for the detailed design of the silos. Technical speci-fications and preliminary designs are shown in Annex 8. The local consult-ants would also prepare necessary tender documents and assist FCI'sengineering department in supervising construction of silos and godowns(para 5.05). A well qualified consultant firm with substantial experiencein the slipform method of silo construction would be contracted by the localconsultants to help in the designing of the silos if the local firm couldnot show evidence of such experience. Provision would also be made for tech-nical training of silo operators (para 4.10).

4.03 The silo part of the project is intended to serve as a model forfurther construction of 8ilo8 but has been limited to 200,000 tons becausethat is the maximum that FCI believes it can handle efficiently in the next

three years. Since there is an acute shortage of storage facilities, anadditional 100,000 tons of godowns, which also have a satisfactory rate ofreturn (para 7.07), have been included in the project.

B. Technical Features

Site Selection

4.04 Locations for the project storage facilities are shown in Annex 9.

The facilities would be built only on sites having road and rail access, and,in the case of silos, located in areas capable of receiving grain in bulk.Based on consideration of the factors outlined in Annex 10, FCI has presenteda detailed justification for the selection of specific sites and agreementon sites has been reached during negotiations.

4.05 Nearly all of the selected sites are owned by FCI. Acquisitionof the remaining sites would not take longer than about 3 months because thesites are single-owner holdings and are located in rural areas. It wouldbe a condition of effectiveness of the proposed IDA and Swedish Governmentcredits that all the sites had been acquired by PCI.

Flat Storage (Godowns)

4.06 Standard designs would be used for the flat storage units, whichwould be of conventional brick construction. Internal dimensions of asub-unit would be approximately 22 m by 130 m. Each would provide 5,000 tonscapacity and be divided into four compartments. Sub-units would be placed

either end to end or side by side, depending on the configuration of the plotand road and rail access requirements, to provide 10,000-ton capacity per

site.

4.07 Godowns would be designed to receive grain in bags. Under cur-rent FCI operational practice, no mechanical equipment would be required.However, since there has been some difficulty in getting laborers tostack to the height necessary to make full utilization of the stores, acontingency provision has been made in the project for bag stackers.

Silos

4.08 Project silos would be designed to receive grain in bulk. Grainwould be sampled and weighed before being emptied into receiving pits tofacilitate purchase at the silo. Provision would be made for baggingbefore dispatch from silos, since this is likely to continue for sometime as the main method of wheat delivery.

4.09 Project silos would be made up of 12 round bins, each having an

inside diameter of about 8 m and a height of 40 m. Interstice spaces betweenthe bins would also be used for storage. Provision has been made for founda-tion piling at all silo sites, and bins would be built of reinforced concreteby the slipform method. The slipform method is the best and most economicalmethod of silo construction because less construction material and foundation

- 9 -

work is needed and greater strength of the silos is obtained. Mechanicalequipment would be installed for cleaning the grain, for distributing itinto and between bins, and for aerating stored grain. In addition, equipmentfor fumigation, temperature indicators and baggers would have to be obtainedfrom abroad.

Technical Training

4.10 To provide the necessary level of technical superintendence ofsilos, 15 trainees (the required number for 10 silos) would be sent abroadfor a period of 6 months to study grain handling in theory and practice inappropriate centers in either Europe or North America. In addition, theforemen and shift supervisors, as well as shift operators, mechanics andelectricians, would be given training in India. This personnel would assistduring the installation and test runs of the equipment. Consultants (para4.02) would make the training arrangements abroad and would be responsiblefor the placement of overseas trainees and for the training program. Overseastrainees would sign a contract obligating them to stay 2 years with the FCI.Consultants would also be responsible for the local training arrangements.Assurances were obtained during negotiations that all training arrangementswould be mutually satisfactory to the Government and IDA.

All-India Grain Storage and Distribution Study

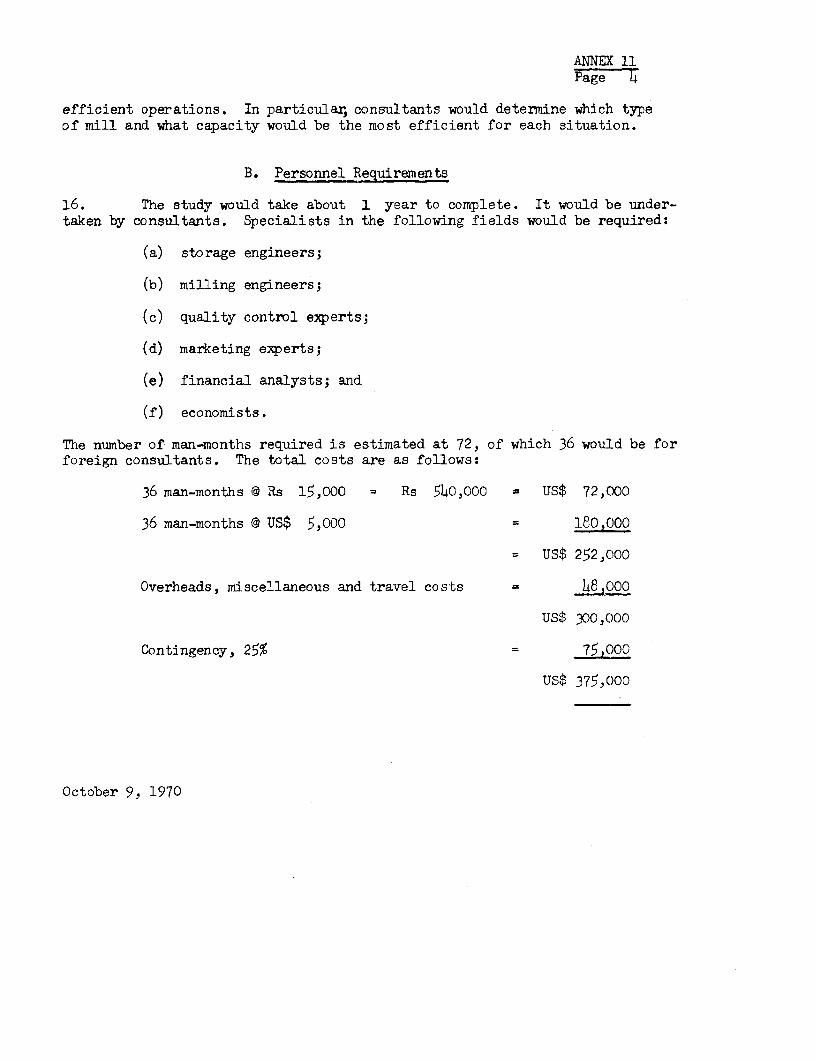

4.11 A nrovision has been made in the project for an All-India GrainStorage and Distribution Study. Assurances were obtained during negotiationsthat within six months of the date of the proposed credit agreements, India,Sweden and IDA would enter into discussions on the proposed study. Tentativeterms of reference (Annex 11), which will be discussed, cover the costs andbenefits of public distribution and contingency stock operations, a surveyof storage and rice processing facilities and grain losses, and the drawingup of programs for improvement of existing practices, rehabilitation ofexisting facilities and construction of new facilities. Government hasalready started carrying out several parts of the study which will be takeninto account during the discussions. It was also agreed during negotiationsthat the consultants who may be required to complete the study and theirterms of reference would be acceptable to IDA.

C. Construction Schedule

4.12 FCI already has considerable experience in the construction ofgodowns and there are many local contractors capable of undertaking thiswork. All godowns could probably be constructed in less than 1 year fromthe date of site selection. On the other hand, FCI has had little experi-ence with silo construction and there is, additionally, a lack of qualifiedcontractors and specialized building equipment. Silo construction wouldtake about 3 years. Annex 12 shows detailed construction time schedules.

- 10 -

D. Cost Estimates

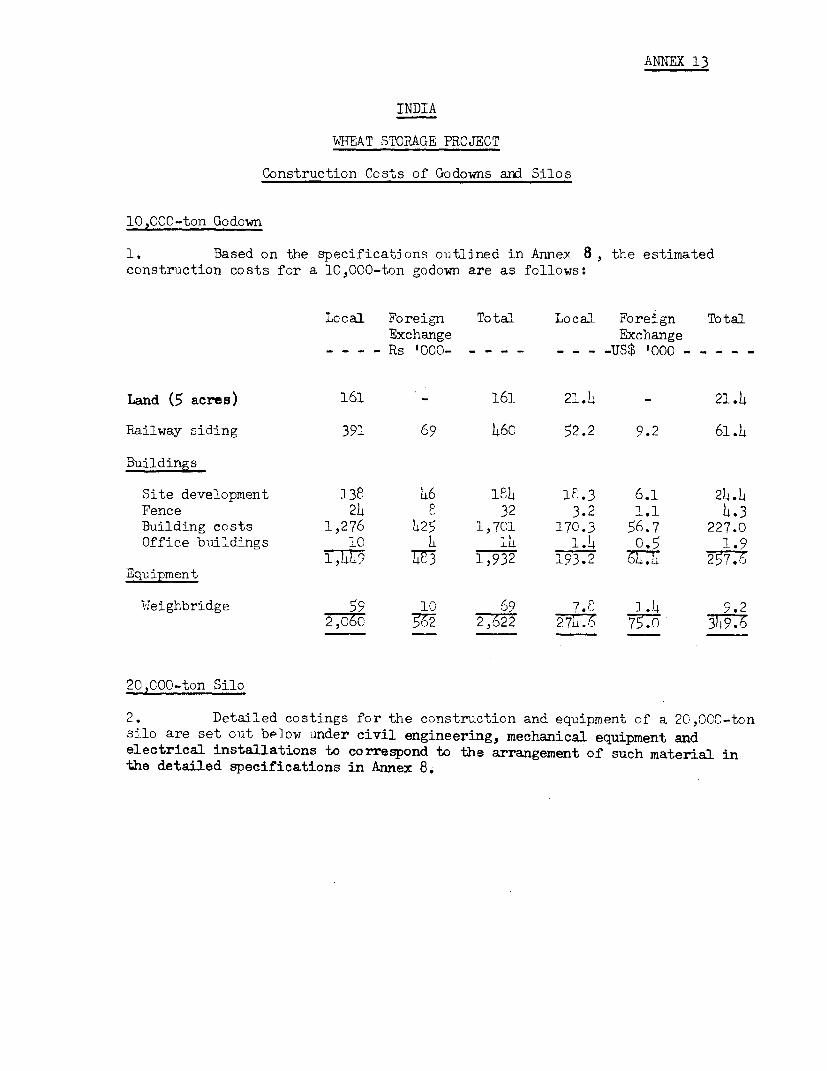

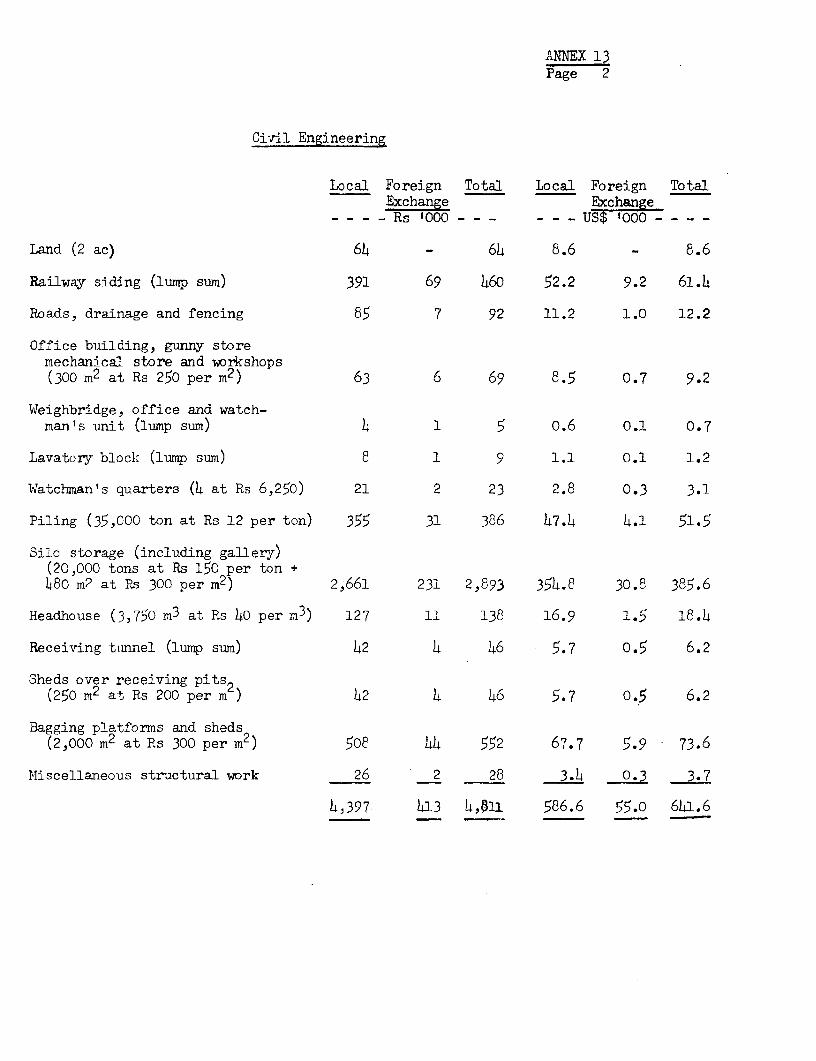

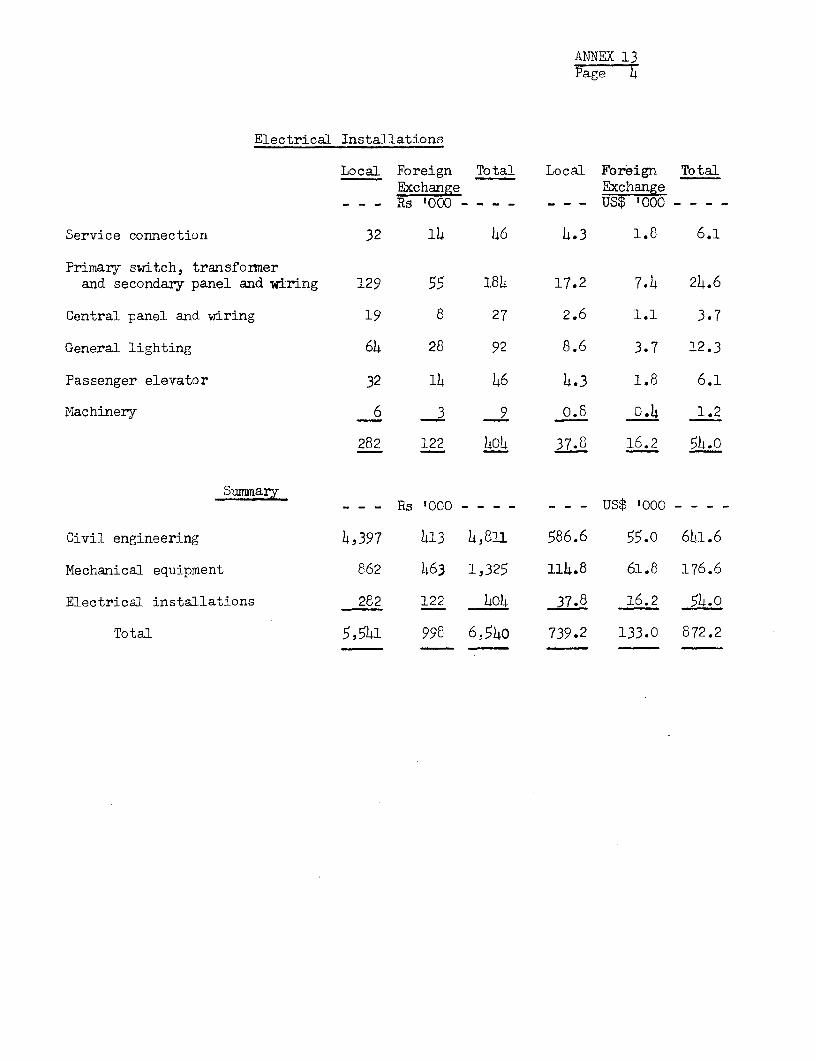

4.13 Total cost of the project is estimated at Rs 119.3 million(US$15.9 million). The foreign exchange component of Rs 22.1 million(US$3.0 million) represents about 19% of total costs and includes specialsilo equipment, the cost of foreign consultants, the training of keysilo operators abroad and the foreign exchange costs of the materialsproduced in India and used for project construction. The following tablepresents a summary of the estimates (see Annex 13 for details).

Rs (thousands) US$ (thousands) ForeignItem Local Foreign Total Local Foreign Total Exchange

Land 1,610 - 1,610 214 - 214 -Railway Sidings 3,910 690 4,600 522 92 614 15Buildings 14,490 4,830 19,320 1,932 644 2,576 25Mechanical Equipment 590 100 690 78 14 92 15

20,600 5,620 26,220 2,746 750 3,496 21SilosLand 644 - 644 86 - 86 -Railway Sidings 3,910 690 4,600 522 92 614 15Buildings 39,431 3,432 42,863 5,258 456 5,714 8Mechanical Equipment 8,611 4,637 13,248 1,148 618 1,766 35Electrical Equipment 2,834 1,214 4,048 378 162 540 30

55,430 9,973 65,403 7,392 1,328 8,720 15Consultants andSupervision CostsConsultants 350 350 700 47 47 94 50Supervision ofContractors 400 - 400 53 - 53 -

750 350 1,100 100 47 147 32

Training 75 425 500 10 57 67 85

Storage Study 900 1,350 2,250 120 180 300 60

Sub-total 77,755 17,718 95,473 10,368 2,362 12,730 19

,.ontingencies, 25%Physical (15%) 11,664 2,657 14,321 1,555 354 1,910Price (10%) 7,775 1,772 9,547 1,037 236 1,273 19

Total Project Cost 97,194 22,147 119,341 12,960 2,952 15,912 19

4.14 The 25% contingency includes a provision for price escalation overthe 3-year construction period of about 10% of total cost; the remainder rep-resents a contingency against unforeseen equipment requirements, constructiondifficulties, and acts of nature. Estimates for imported equipment items are

- 11 -

based on current manufacturers' prices, while costs of land, railway sidings,buildings and locally produced equipment have been based on figures suppliedby FCI and verified during appraisal.

E. Proposed Financing

4.15 The following table represents the proposed financing of projectcosts:

Rs '000 US$'000 X

IDA Funds 37,500 5,000 31.4Swedish Government Funds 37,500 5,000 31.4GOI Funds 44,341 5,912 37.2

119,341 15,912 100.0

4.16 The Swedish Government and IDA would together provide a totalcredit of US$10 million, representing about 63X of project cost. GOIwould supplement Swedish Government and IDA funds with its own funds andonlend the total to FCI. Because of the small proportion of foreign costof the project, the IDA credit would finance local cost expenditure. Thecredits would cover the foreign exchange component of project costs andabout 50% of local costs. The borrower would be GOI and the onlending toFCI would be for 19 years, including 4 years' grace, to be repaid at 7%interest. These are the normal terms for lending to state enterprises.

P. Procurement

4.17 Contracts for the civil works for the silos would be financedby the Swedish Government and would be let by FCI, assisted by the engineer-ing consultants, on the basis of local competitive bidding. The civil worksfor the godowns would be financed by IDA. Since the godowna are scatteredover a wide area, contracts would not be suitable for international biddingand would be let on the basis of local tender. Experience in godown construc-tion is widespread throughout India and local construction cost is low. Pre-

qualification of prospective bidders for both the silos and the godowns wouldbe made to ensure that the works would be carried out by capable contractors.These would be divided into two categories - one for the construction of thesilos and the other for the construction of the godowns. In the case of theconstruction of the silos, contractors would have to show evidence of experi-

ence in the slipform method of construction or their association with firmsthat had done such work. Bidding for the silos as well as the godowns wouldbe by individual site, and bids might be made for any number. Separate bidswould be invited for the mechanical and electrical works and the civil works.Mechanical and electrical equipment, to be financed by IDA, would be procuredunder international bidding and, for purposes of bid evaluation, a 15% pref-erence or the import duty, whichever is less, would be allowed in favor ofdomestic equipment supplies.

- 12 -

4.18 Tenders would be evaluated by the technical staff of FCI, assistedby the consultant to determine conformity with tender invitations. Success-ful tenders would be subject to IDA approval. During negotiations, assuran-ces were obtained that procedures outlined in paragraph 4.17 and in thisparagraph would be followed.

G. Disbursement

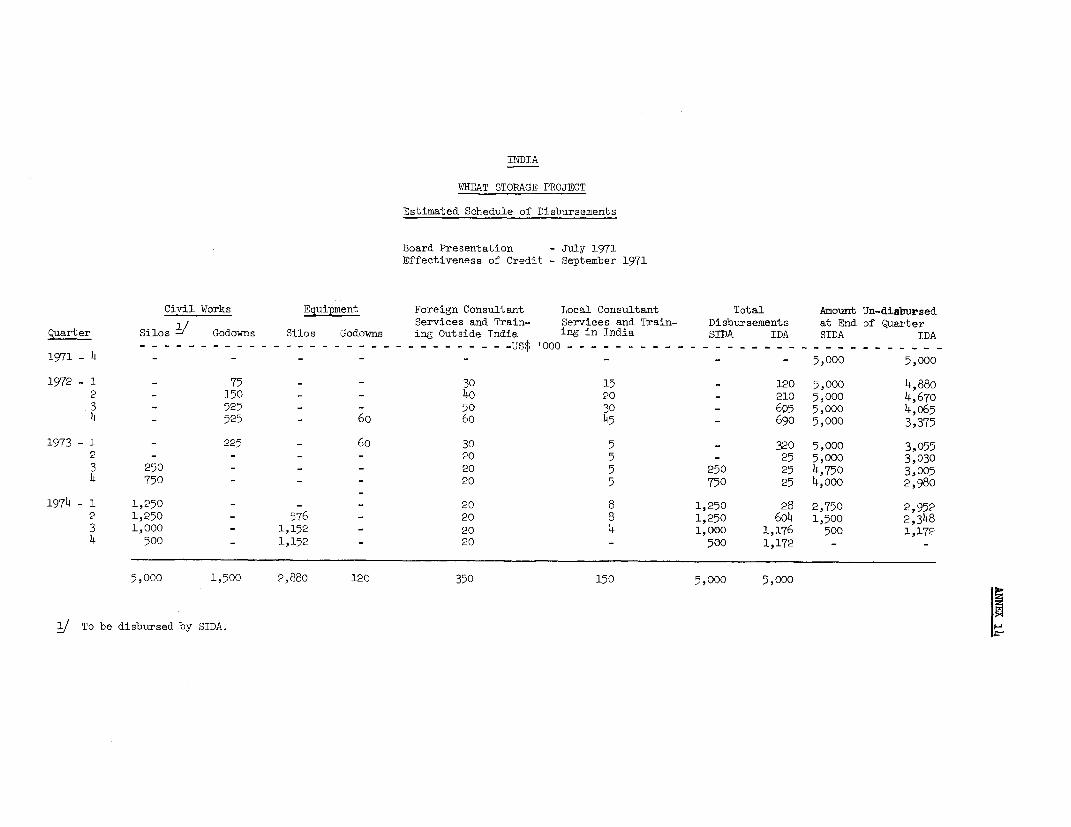

4.19 The Swedish Government credit would be disbursed against the costof civil works for the construction of silos, covering up to 80% of thesecosts, making full allowance for contingencies. In the event that the totalamount of the Swedish credit is not required for this work, it would be dis-bursed against other components. The IDA credit would be disbursed against:

(a) 100% of the cost of mechanical and electrical equipment;

(b) 100% of foreign expenditures for engineering and otherconsulting services acquired outside India and of thecost of training outside India;

(c) 50% of local expenditures for consulting services inIndia and the cost of training in India; and

(d) 37% of the total cost of civil works for the constructionof godowns.

4.20 Disbursements would take place when FCI presents evidence ofpayment. A detailed disbursement schedule is presented in Annex 14.

V. ORGANIZATION AND MANAGEMENT

A. Operations of the Food Corporation of India

5.01 The project would be managed entirely by the FCI. The Corporation'soperations are discussed in detail in Annex 15, which also presents FCI'sbalance sheets, its profits and loss statements and its organization chart.The FCI distributed about 6.6 million tons of foodgrains in 1969 (4.0 millionprocured locally and 2.6 million imported), which represents nearly 70% ofall foodgrain distributed publicly (9.7 million tons). The states accountfor the remaining 30%. FCI employs some 25,000 people and owns storage fa-cilities w-ith a capacity of about 2.8 million tons. Its net profits in1968/69 were negligible, 0.3% of sales.

5.02 The main reason for FCI's low profits is that, under the Govern-s,ent's price support policy, it must buy domestically produced wheat atRs 760 per ton and sell it at Rs 780 per ton. The margin of Rs 20 per ton isnot sufficient to cover storage and distribution costs, which are about

- 13 -

Rs 200 per ton (para 6.01) for domestically procured wheat. FCI makes aprofit on imported wheat and locally procured rice and other foodgrains(para 2.13).

5.03 FCI is financed by 4-year GOI loans (Rs 2.2 billion as of March1969) at an interest rate of 5.75%; bank overdrafts (Rs 1.2 billion as ofMarch 1969), guaranteed by the GOI at an interest rate of 7%; and equitycapital held entirely by GOI (Rs 285 million as of March 1969). Any deficitsin FCI's operations are covered by the Government (para 2.13). The Govern-ment has opted for this financing plan instead of making the funds availableat a zero interest rate because it wants FCI to operate eventually as an un-subsidized corporation.

5.04 The management of the FCI is good and, on the whole, it is a rea-sonably well-run operation. An inventory of all stocks is made available toheadquarters on a semi-monthly basis within 2 weeks after the date that in-ventories have been taken. Pest and insect control can be improved. Thestudy proposed in paragraph 4.11 would investigate ways and means to improvequality control.

5.05 Because FCI's engineering department lacks experience, especiallyin silo design and construction, local engineering consultants would be en-gaged to assist it. These consultants would have to show evidence of experi-ence in the slipform method of silo construction or their association withfirms that had done such work. Proposals for consultancy services (includingevidence of association with firms with adequate qualifications) would be ob-tained from the local firms and appointments made on the basis of evidence ofprevious pertinent training and experience, with the approval of IDA. Theappointment of the engineering consultants would be a condition of effective-ness of the proposed credit.

B. Cost Control

5.06 FCI operates under the limitations set by the buying and sellingprices fixed annually by Government, and its performance cannot, therefore,be judged on the basis of its profit record. FCI has constantly attemptedto explore the possibilities of effecting cost reductions, but the majorfactors in costing are not susceptible to unilateral reductions on its part.Taxes, market charges, railway freight, bag prices, administration charges ofState Governments and interest charges on capital invested represent theseitems, which are fixed by other bodies. FCI's efforts at economy can, there-fore, be directed only internally at control of purchase, storage and hand-ling charges; storage and transit losses; and transport charges by ensuringmore efficient methods. FCI has a Planning and Research Department but theposition of Head of the Department is vacant. Assurances were obtained duringnegotiations that within six months of the signing of the proposed credit, aHead with satisfactory experience and qualification would be appointed.

5.07 There is also a Cost Control Unit in PCI that reviews, on the basisof the accounting data, the various cost categories. The Unit is directly

- 14 -

responsible to the Managing Director. Assurances were obtained during nego-tiations that it would be headed at all times by a person with satisfactoryexperience and qualifications.

C. Accounts and Audit

5.08 Assurances were obtained during negotiations that FCI would set upseparate project accounts reflecting investment costs, wheat flow, and oper-ating costs of the proposed project facilities. Assurances were also ob-tained that FCI would record the costs of its normal public distributionoperation and of its contingency stock operation so that the financial resultsof each can be analyzed separately.

5.09 The financial year of FCI ends on March 31, but in the past itiUas caken about a year before audited statements became available. Becausetimely information is essential, this time gap should be shortened. Theauditors of FCI are chartered accountants appointed from a list of auditorsapproved by the Central Government. Assurances were obtained during nego-tiations that an audited financial statement would be presented to IDAwithin 6 months of the close of FCI's financial year.

VI. STORAGE, OPERATION AND DISTRIBUTION COSTS

6.01 Annex 16 presents a detailed estimate of the operation and main-tenance costs of the proposed godown and silos and of the wheat distributioncosts. Total storage and distribution costs per year, from purchase todistribution through the foodgrain sales centers, are about Rs 200 per ton,as shown in the following table:

Storage CostGodowns Silos

Rs per ton per year Rs per ton per yearFixed Storage Costs

Depreciation 25.90 34.44Overhead 14.00 15.95

Other Storage Costs 11.20 1.70

Total Storage Costs 51.10 52.09Distribution Cost

Mandi Cost and Transport to Storage 64.30 60.90Bagging on Mandis or Out of Silos 29.70 29.70Handling and Freight up to Foodgrain

Sales Centers 53.10 53.10

Total Distribution Costs 147.10 143.70

Total Storage and Distribution Costs 198.20 195.79

- 15 -

6.02 Except for the silos, these costs are based on FCI records. Theyinclude the actual out-of-pocket expenses and depreciation charges incurredby FCI, but not the grain losses, since FCI sells the grain per bag, in-cluding the moisture uptake, which compensates for the loss in nutritionalvalue during the storage period. Silo costs are estimated to be about thesame as those for the godowns but would be lower in the future (para 7.05).

6.03 The total cost (excluding distribution costs) incurred by FCI forthe storage of about 300,000 tons of wheat for a year amounts to about Rs15 million, or about Rs 4.30 per ton per month. Going rates for privatestorage are about Rs 5 to Rs 6 per ton per month, but, even at that price,there is not sufficient space available for rent. Since FCI's totalstorage and distribution costs are only partly covered by its margin onsales, the financing of these costs would be provided through regularbudgetary allocations from the Central Government.

6.04 The proposed project would enable FCI to procure, store and dis-tribute an additional 300,000 tons of domestic wheat. Under present procure-ment and issue prices (para 5.02), FCI would incur a deficit of about RS 180per ton, or about Rs 54 million (US$7.2 million), on this wheat. Since suchprices are fixed by Central Government after discussion with the State Gov-ernments, it is impossible to predict FCI's future deficits. The CentralGovernment has confirmed that the cost of the subsidy would be borne by thebudget of the Government of India.

VII. BENEFITS AND JUSTIFICATION

A. Choice of Location

7.01 Location of the proposed facilities in North-west India has defi-nite advantages over location in the main consuming areas. These includeclimatological factors and the avoidance of railroad bottlenecks (85% of thewheat is procured in the 3 months following the harvest). The better climatein North-west India keeps foodgrain losses there lower than in the mainconsuming centers such as Bombay, Madras or Calcutta. The railroad bottle-necks occur in the broad-gauge system, which handles the bulk of the wheatbelt's production and which connects this area with the rest of India exceptthe western part. The latter is served by a meter-gauge system that hassome unused capacity. Location in the wheat belt or along the meter-gaugewould help reduce the bottlenecks in the broad-gauge system.

7.02 Establishing production-oriented storage facilities has thereforea definite advantage over placing them in the main consuming areas. Eighteenof the facilities would be located in the wheat belt; the remaining two wouldbe near consuming centers in the districts of Udaipur and AJmer in the stateof Haryana, which are served by the meter-gauge railroad. The location ofthe facilities is such that all would help reduce foodgrain losses and trans-port bottlenecks.

- 16 -

B. Choice of Storage Method - Godown Versus Silo

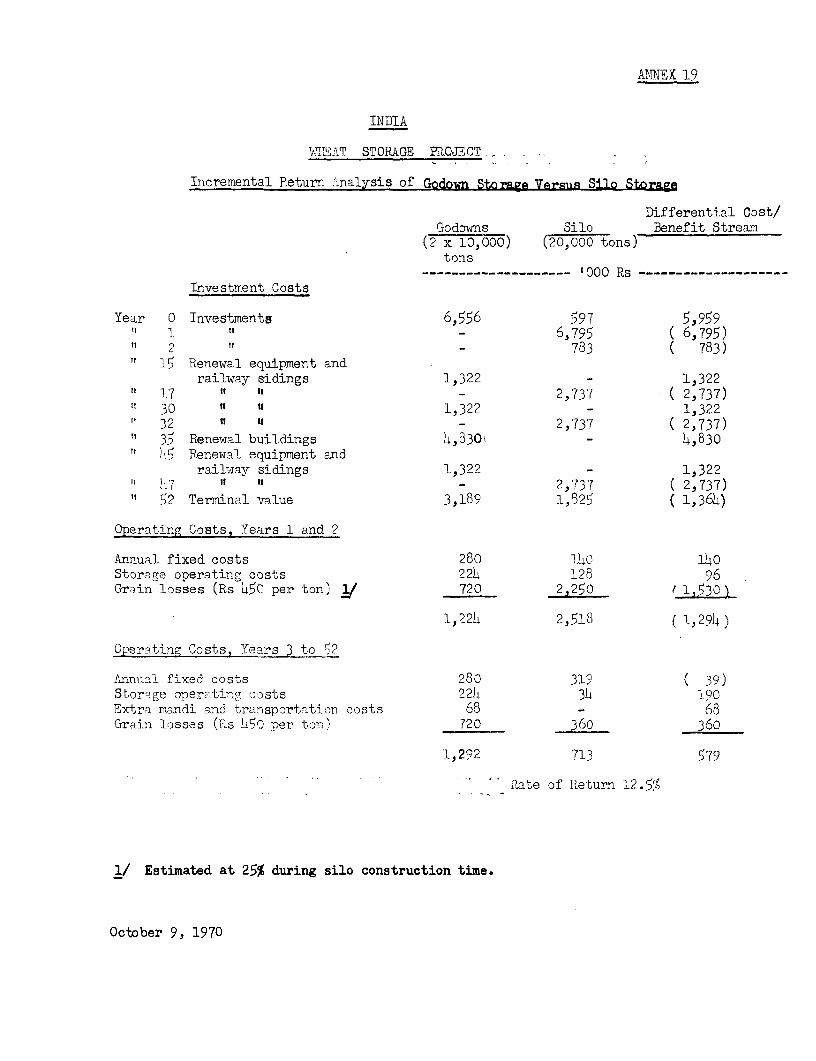

7.03 Godown construction cost, including contingencies, is about Rs 330per ton capacity while silo construction cost is about Rs 410 (Annex 16).On the other hand, operating costs are higher for godowns than for the silos,making the total fixed (including the capital recovery cost) and operatingcosts about the same. However, the main advantage of silos is that grainlosses are reduced substantially. A reduction in losses is, of course, abenefit to the economy. A detailed estimate of distributing and operatingcosts and losses for storage in godowns and silos for periods of up to 3years (the maximum period that the grain can be stored in silos withoutdeterioration) is presented in Annex 17.

7.04 The losses in North-west India under present conditions on the in-cremental marketed production, w!thout the project, are estimated to be atlca6c 25%. For tne wneat stored in the proposed project facilities, lossesare estimated to be about 8% for the godowns and 4% for the silos (assumingone turnover per annum). The losses under the project would be lower thanthose suffered in comparable facilities elsewhere in the world (for example,East Pakistan) because of the favorable climate for storage. Annex 18discusses grain storage losses in India.

7.05 Annex 19 analyzes the comparative advantages of silos and godowns.The incremental investment in a silo compared to a godown is compensated bythe silo's savings in operating costs and storage losses. The rate of returnon the incremental investment is about 12.5%. This rate of return computa-tion is based upon liberal cost estimates for the silos. Because the pro-posed method of silo construction (slipform construction) is new to India,it is expected that subsequent silos can be constructed at lower cost. Inaddition, further cost savings from handling grain in bulk, which is ex-pected to develop later but which has not been taken into account in thecalculation, can be realized from the silos. Thus, the rate of return onthe incremental inveistment quoted above should be considered a conservativeestimate. Silos are, therefore, the more economical storage facility.

7.06 As mentioned in paragraph 4.03, the silo program would be limitedto 200,000 tons. An additional 100,000 tons of godown storage has beenincluded in the proposed project to help meet the increasing need for space.The rate of return Is lower for the godowns than for the silos, but isnevertheless satisfactory (para. 7.07).

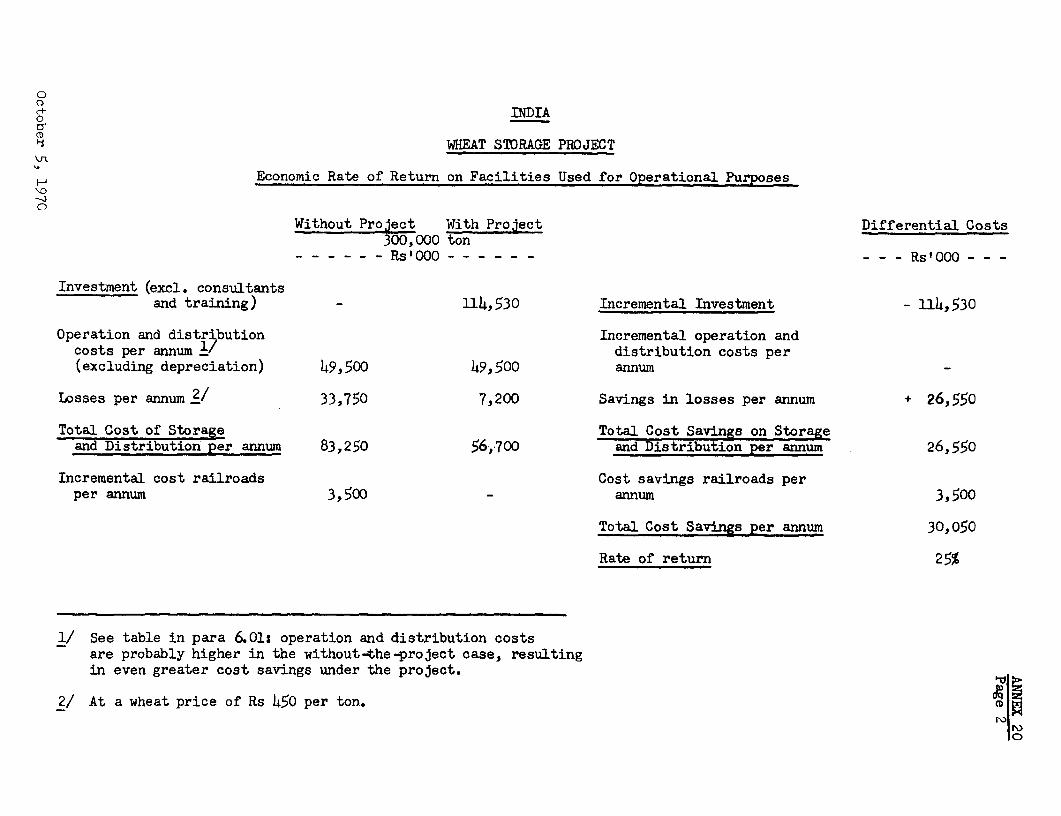

C. Economic Rate of Return

7.07 As wheat output continues to increase and the shortage of storagemounts, losses incurred on the incremental marketable production will becomegreater. A conservative estimate of such losses per annum, based on past ex-perience, is 25%. The main benefit of the proposed project is that theselosses would be reduced, as mentioned in paragraph 7.04. Annex 20 presentsa differential analysis of storage costs (including grain losses) with the

- 17 -

project versus the costs without the project. The overall rate of returnunder the project would be about 25%. The rate of return for the godownsis 20% and for the silos 28%.

7.08 A sensitivity analysis has also been made. If without-the-projectstorage losses were 15% per annum instead of 25% per annum (which is un-realistically low under the circumstances), the rate of return on the projectfacilities would be 15%. At a loss rate of 35% per annum, the rate of returnon the facilities would be about 40%.

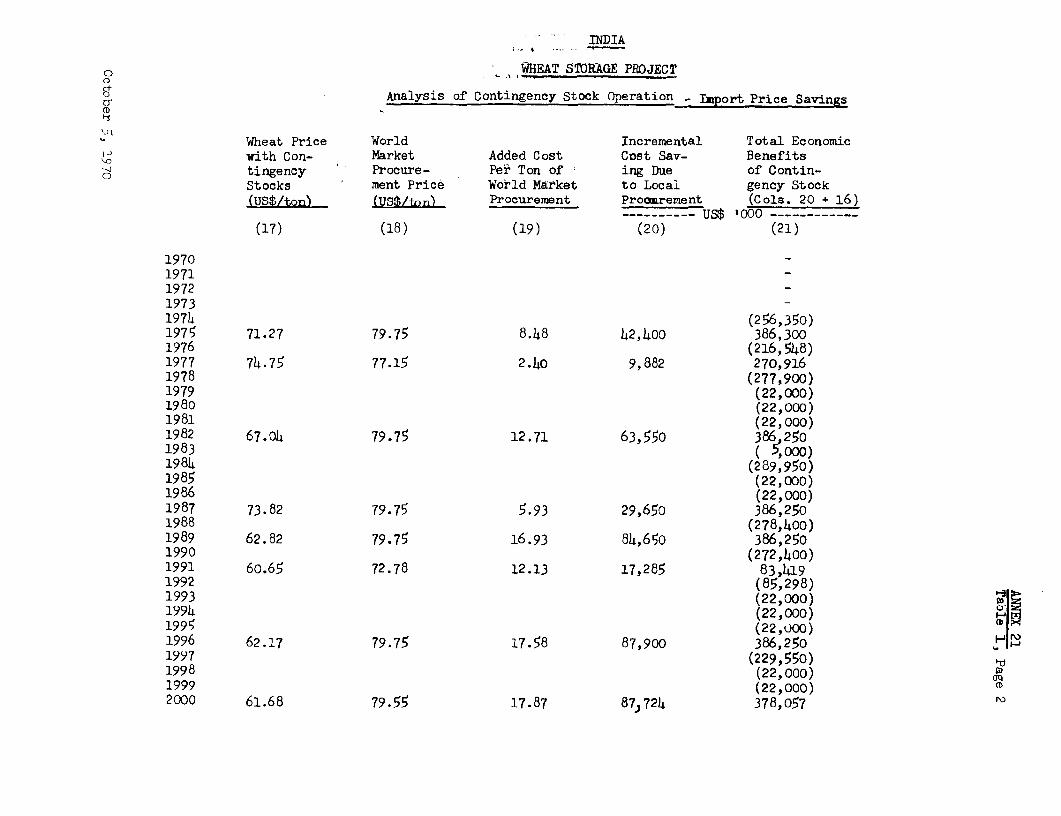

7.09 The proposed storage facilities would be used to store operationalstocks. However, since the proposed project forms part of India's storageconstruction program, which includes facilities for contingency stocks, anattempt has been made in Annex 21 to evaluate the benefits of a 5-million-toncontingency stock operation (para 2.15). The direct benefits of such anoperation are two-fold. First, they derive from the fact that a ton of graincan be bought cheaply when supply is abundant and sold at a higher price whensupply is scarce. This is the financial return that FCI would make and thathas been calculated to be about 2%. Second, without a contingency stockoperation, India would have to procure wheat in world markets if it wanted toprovide consumers with the same level of foodgrain consumption as would pre-vail under the contingency stock operation. This additional demand wouldraise world market prices to a level that would be subst,antially higher thanthe price level under the contingency stock operation. Because of the con-tingency stock operation, the Indian Government would, consequently, not haveto procure wheat at the higher world market prices. The rate of return onthe investment, based upon these two direct benefits and assuming that all ofthe facilities would be used for contingency storage, is between 5% and 10%,which is marginal.

7.10 In addition to the two direct benefits, there are indirect bene-fits from contingency stock operations. First, a substantial part ofthe contingency stock may be used to meet emergencies (e.g., floods mayisolate areas or transportation breakdowns may occur). The benefit of astock used for this purpose is difficult to evaluate. Second, withoutthe contingency stock operation, it may sometimes not be possible to obtainwheat on world markets, especially when there would be a substantial Indiandemand. Third, because of the contingency stock operation, farmer priceswould be stabilized and such stabilization tends to increase farmers' pro-duction. Since these indirect benefits cannot be evaluated, it is there-fore not possible to state whether the contingency stock operation is justi-fied. The analysis presented here, therefore, should not be considereda definitive comment on India's contingency program. The all-India storagestudy (para 4.11) would provide data necessary for a complete evaluation,analyze cost and benefits and recommend the most economical level of thecontingency stock operations.

7.11 As has been mentioned, the proposed facilities would be used foroperational purposes and, as such, would have a rate of return of at least25% (para 7.07). The proposed project would also result in substantial for-eign exchange savings. If the reduction in foodgrain losses is evaluated

- 18 -

at a world market price of US$65 per ton, the foreign exchange savings (afterdebt service) would be about US$3.0 million per annum.

7.12 The proposed project has high priority. It would serve an area inIndia where the progress of foodgrain production has been most impressiveand where an absolute shortage of adequate storage facilities exists. Pro-vision of such facilities is urgently needed, not only to prevent losses butalso to help India in her efforts to become self-sufficient in the shortestpossible time.

VIII. RECOMMENDATIONS

8.01 During negotiations, assurances were obtained on the following.u- r.cipal point6:

(a) suitable training arrangements, mutually satisfactoryto the Government and IDA, would be made for silopersonnel (para 4.10); and

(b) audited financial statements would be presented to IDAwithin 6 months of the close of FCI's financial year(para 5.09).

8.02 Conditions of effectiveness of the credit would be that:

(a) FCI had acquired all the sites for the storage facilities(para 4.05); and

(b) well-qualified engineering consultants had been appointedto assist the engineering department of FCI (para 5.05).

8.03 The Project is suitable for an IDA credit and a Swedish Governmentcredit, each in the amount of US$5 million.

June 25, 1971

ANNEX 1

INDIA

WHEAT STORAGE PROJECT

Gross Production of Foodgrains('000 tons)

Rice Wheat Other Cereals Pulses Total Foodgrains

1949/50 25,108 6,755 18,769 10,021 60,6531950/51 22,070 6,829 16,841 9,182 514,9221951/52 22,622 6,343 17,436 9,107 55,5081952/53 24,305 7,613 19,933 9,822 61,6731953/54 29,778 8,106 23,193 11,109 72,1861954/55 26,564 9,146 23,2614 11,632 70,6061955/56 28,674 8,869 19,986 11,687 69,2161956/57 30,230 9,504 20,469 12,134 72,3371957/58 26,539 8,oo5 21,864 10,096 66,50141958/59 32,038 9,957 23,1490' 13,202 78,6871959/60 31,687 10,322 22,872 11,818 76,6991960/61 34,574 10,997 23,743 12,704 82,0181961/62 35,663 12,072 23,216 11,755 82,7061962/63 33,217 10,776 214,630 11,528 80,1511963/64 36,998 9,853 23,718 10,073 80,6421964/65 39,034 12,290 25,234 12,438 88,9961965/66 30,655 10,424 21,151 9,800 72,0301966/67 30,438 11,393 24,053 -8,347 74,2311967/68 37,610 16,540 28,800 12,100 95,0501968/69 39,760 18,650 25,180 10,420 9h,010

Source:- Mir.istry of Food, Agriculture, Community Development andCooperation - Directorate of Economics and Statistics;Estimates of Area.and Production of Principa.l Crops inIndia. (1968-1969), New Delhi, 1969.

- Ihid: Bulletin on Food Statistics, New Delhi, 1969.- Government of India: Economic Survey - 1969-1?70, New Delhi, 1970.

October 5, 1970

INDIA

C+ WWHET STORAGE PROJECT0

Net Production, Imports, Stock Changes and Consumption of Foodgrains

Net Production Net Imports Net Stock Changes Total Net Consumption

Xjheat Rice 2/2 2/ 2/o Wheat Rice Other- Total 'Wheat Rice Other-/ Total Wheat Rice Other- Total Wheat Rice Other- Total

----------------------------------------------------------------000 Ton-------------------------------------------------------

1950 5,938 23,200 23,933 53,071 1,429 359 371 2,159 -220 _354 -291 -865 7,587 23,913 24,595 56,0951951 6,003 20,393 21,661 48,057 3,063 761 977 4,801 +356 +70 +163 +589 8,710 21,084 22,475 52,2691952 5,575 20,903 22,092 48,570 2,551 734 641 3,926 +348 +218 +52 +618 7,778 21,419 22,681 51,878

1953 6,692 22,458 24,814 53,964 1,711 178 146 2,035 -168 -113 -202 -483 8,571 22,749 25,162 56,4821954 7,125 27,515 28,522 63,163 198 628 6 832 -778 +1,034 -54 +202 8,101 27,109 28,582 63,7931955 8,039 24,545 29,196 61,780 440 165 -92 513 +184 -868 -62 -746 8,295 25,578 29,166 63,0391956 7,796 26,495 26,273 60,564 1,104 287 -19 1,372 -50 -540 -12 -602 8,950 27,322 26,266 62,5381957 8,354 27,933 27,008 63,295 2,879 747 -6 3,620 +643 +145 +68 +856 10,590 28,535 26,934 66,0591958 7,036 24,522 26,633 58,191 2,709 396 105 3,210 -307 +8 +30 -269 10,052 24,910 26,708 61,6701959 8,752 29,603 30,496 68,851 3,543 295 13 3,851 +171 +380 -59 +492 12,124 29,518 30,568 72,2101960 9,073 29,279 28,760 67,112 4,376 699 43 5,119 +1,057 +351 -5 +1,403 12,392 29,627 28,809 70,8281961 9,666 31,946 30,154 71,766 3,090 384 12 3,486 -20 -121 -24 -165 12,776 32,451 30,190 75,4171962 10,611 32,953 28,804 72,368 3,249 390 -10 3,629 -42 -303 -10 -355 13,902 33,646 28,804 76,3521963 9,472 30,693 29,967 70,132 4,071 480 -15 4,536 +179 -201 - -22 13,364 31,374 29,952 74,6901964 8,661 34,186 27,715 70,562 5,621 642 -11 6,252 -1,297 +47 +7 1,243 15,579 34,781 27,697 78,o571965 10,803 36,067 31,001 77,872 6,572 780 87 7,439 +858 +89 +116 +1,063 16,517 36,758 30,972 84,2411966 9,163 28,325 25,538 63,026 7,827 776 1,708 10,311 -214 -107 +458 +137 17,204 29,208 26,788 73,2001967 10,014 28,125 26,814 64,952 6,400 448 1,810 8,659 -237 +201 -246 -282 16,651 28,372 28,870 73,8931968 14,562 34,981 34,097 83,640 4,766 443 467 5,676 +1,240 +518 +236 +1,994 18,088 34,906 34,328 87,322196 9(est.) 16,394 36,739 29,128 82,261 3,090 476 270 3,836 +144 +565 -242 +467 19,340 36,650 29,640 85,630

1/ According to GOI statistics, net production u-iffers from gross produaction (Annex 1) by theesmount provided for feed, seed requtreme-ts and \rastage,which i£ estimated at 12.5t- of the grossproduction of all foodgrains.

2/ Other = other cereals and pulses.

Source: Ministry of Food, Agriculture, Community Developrent and Cooperation, Directorateof Economics and Statistics Bulletin of Import Statistics - New Delhi, 1969.

INDIA: WHEAT STORAGE PROJECT ANNEX 3

NET PRODUCTION AND CONSUMPTION OF FOODGRAINS(MILLIONS OF TONS)

120 1 1 1 1 1 1 1 1 1 I 120

FOURTH PLAN'SNET PRODUCTION TARGET /

100 100

80 80

TOTAL CCONSUMP T10IO\N

TOTAL NET PRODUCTION

60 6~~~~~~~~~~~~~0

IFOURTH PLAN 'S NETr PRODUCTION TARGET_v

40 19516016 16 940

FOURTH PLA5NRS_. .. ~~~~~~~~~~ET PRODUCTION TARGET--,,_

20 *fi20

D W _/ASWF I~~~W EAT (PRODUCTION)

O 0 t I -J ll O1950 1955 1960 1965 1969 1974

IBoRD-5000(2R)

ANNEX 4

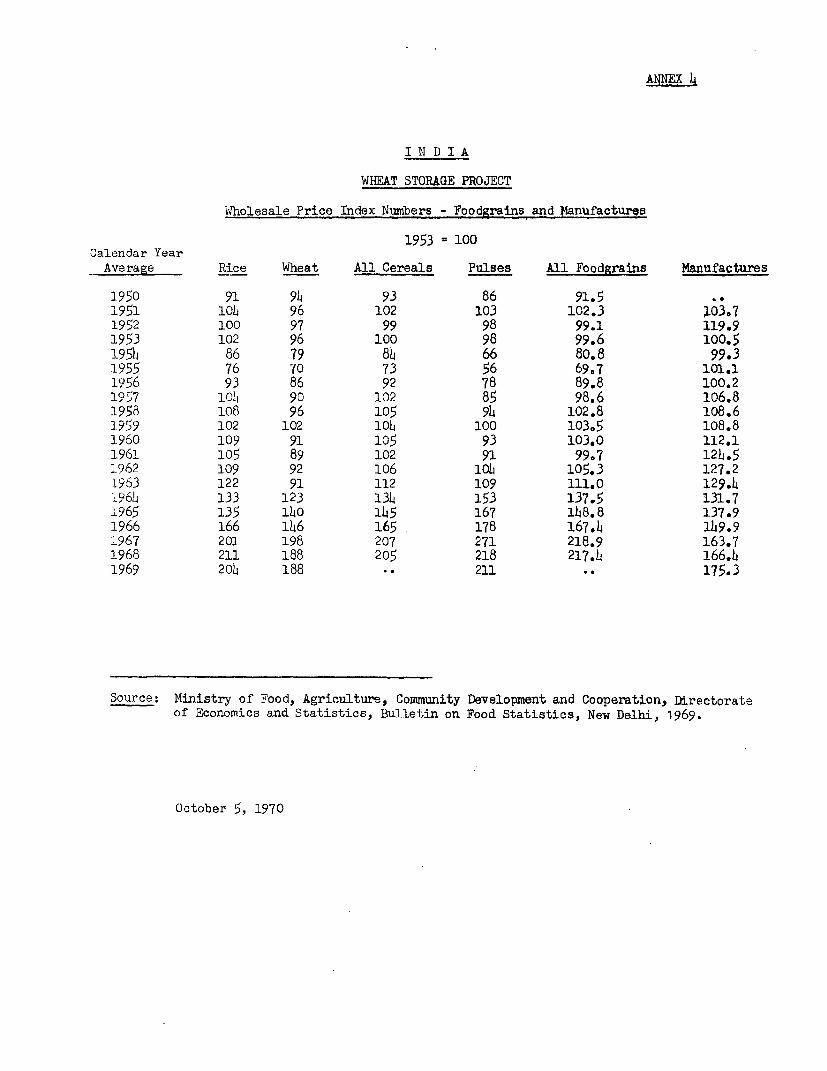

I N D IA

WHEAT STORAGE PROJECT

Wholesale Price Index Nuibers - Foodgrains and annufactures

1953 = 100Calendar Year

Average Rice Wheat All Cereals Pulses All Foodgrains Manufactures

1950 91 94 93 86 91.51951 lob 96 102 103 102.3 1Q3,71952 100 97 99 98 99.1 119.91953 102 96 100 98 99.6 100.5195h 86 79 84 66 80.8 99.31955 76 70 73 56 69.7 101.11956 93 86 92 78 89.8 100.2192'7 lo, 90 102 85 98.6 106.81958 108 96 105 9b 102.8 108.61959 102 102 10l 100 103.5 108.81960 109 91 105 93 103.0 112.11961 105 89 102 91 99.7 124.51962 109 92 106 lob 105.3 127.21t963 122 91 112 109 111.0 129.4196h 133 123 134 153 137.5 131.7

1965 135 140 145 167 148.8 137.91966 166 146 165 178 167.4 149.91967 201 198 207 271 218.9 163.71968 211 188 205 218 217.4 166.41969 204 188 . 211 175.3

Source: Ministry of Food, Agriculture, Community Development and Cooperation, Directorateof Economics and Statistics, Bulletin on Food Statistics, New Delhi, 1969.

October 5, 1970

INDIA

WHEAT STORAGE PROJECT

Public Distribution of Foodgrains

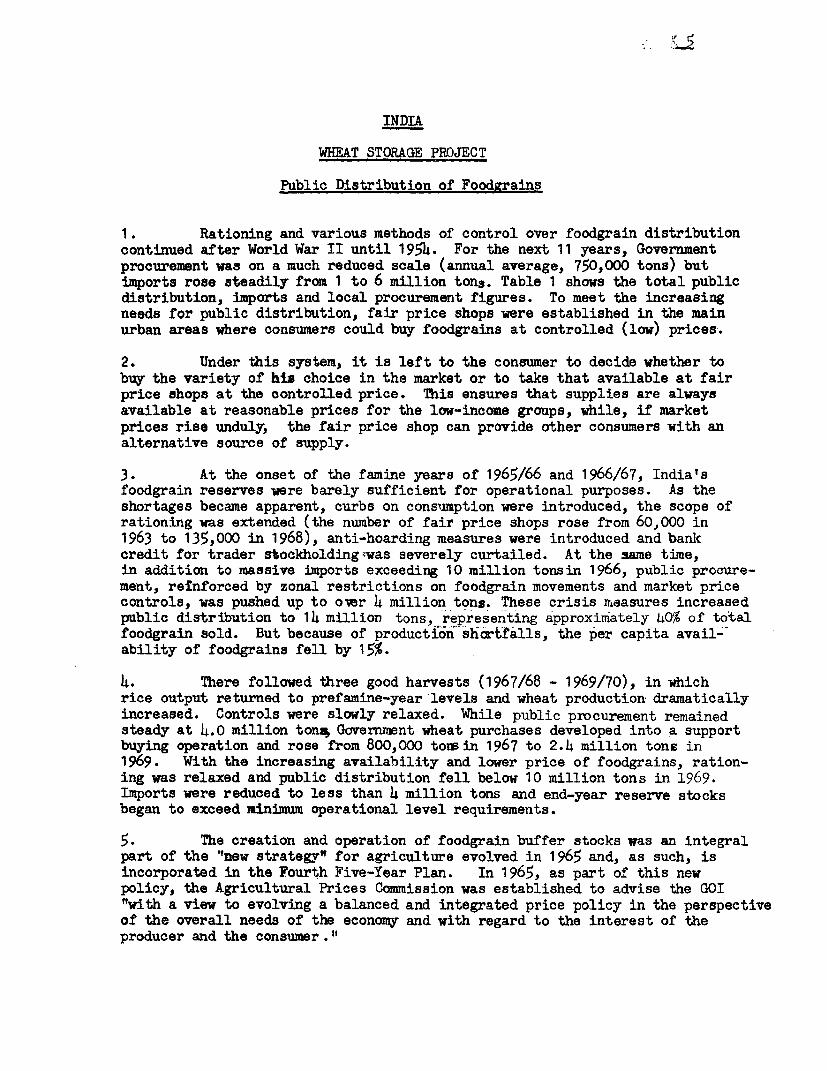

1. Rationing and various methods of control over foodgrain distributioncontinued after World War II until 1954. For the next 11 years, Governmentprocurement was on a much reduced scale (annual average, 750,000 tons) butimports rose steadily from 1 to 6 million tons. Table 1 shows the total publicdistribution, imports and local procurement figures. To meet the increasingneeds for public distribution, fair price shops were established in the mainurban areas where consumers could buy foodgrains at controlled (low) prices.

2. Under this system, it is left to the consumer to decide whether tobuy the variety of his choice in the market or to take that available at fairprice shops at the controlled price. This ensures that supplies are always

available at reasonable prices for the low-income groups, while, if marketprices rise unduly, the fair price shop can provide other consumers with analternative source of supply.

3. At the onset of the famine years of 1965/66 and 1966/67, India'sfoodgrain reserves were barely sufficient for operational purposes. As theshortages became apparent, curbs on consuimption were introduced, the scope ofrationing was extended (the number of fair price shops rose from 60,000 in1963 to 135,000 in 1968), anti-hoarding measures were introduced and bankcredit for trader stockholding;was severely curtailed. At the same time,in addition to massive imports exceeding 10 million tonsin 1966, public procure-ment, reTnforced by zonal restrictions on foodgrain movements and market pricecontrols, was pushed up to oxer 4 million tons. These crisis measures increasedpublic distribution to 14 million tons, representing approximately 40% of totalfoodgrain sold. But because of production shortfalls, the per capita avail-_ability of foodgrains fell by 15%.

4. There followed three good harvests (1967/68 - 1969/70), in whichrice output returned to prefamine-year levels and wheat production dramaticallyincreased. Controls were slowly relaxed. While public procurement remainedsteady at 4.0 million tonq Gcvernment wheat purchases developed into a supportbuying operation and rose from 800,000 tow in 1967 to 2.4 million tons in1969. With the increasing availabil-ity and lower price of foodgrains, ration-ing was relaxed and public distribution fell below 10 million tons in 1969.Imports were reduced to less than 4 million tons and end-year reserve stocksbegan to exceed minimum operational level requirements.

5. The creation and operation of foodgrain buffer stocks was an integralpart of the 'now strategy" for agriculture evolved in 1965 and, as such, isincorporated in the Fourth Five-Year Plan. In 1965, as part of this newpolicy, the Agricultural Prices Commission was established to advise the GOI"with a view to evolving a balanced and integrated price policy in the perspectiveof the overall needs of the economy and with regard to the interest of theproducer and the consumer."

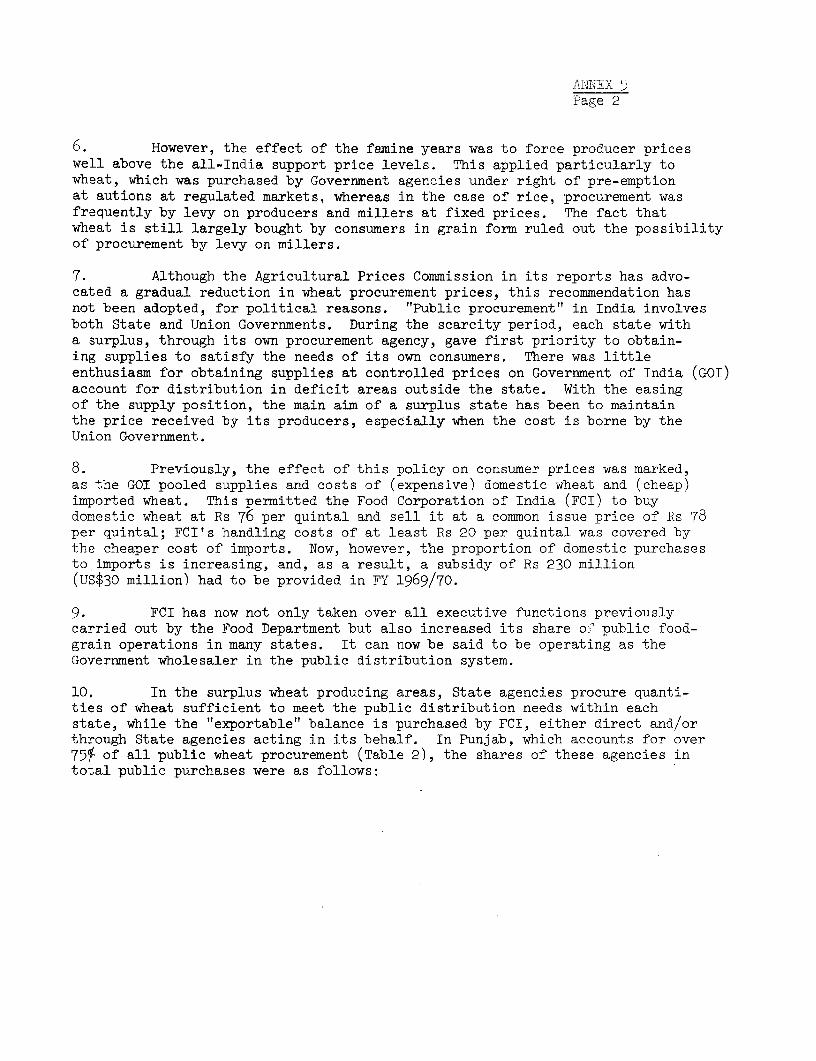

AI]NFX 5Page 2

6. However, the effect of the famine years was to force producer priceswell above the all-India support price levels. This applied particularly towheat, which was purchased by Government agencies under right of pre-emptionat autions at regulated markets, whereas in the case of rice, procurement wasfrequently by levy on producers and millers at fixed prices. The fact thatwheat is still largely bought by consumers in grain form ruled out the possibilityof procurement by levy on millers.

7. Although the Agricultural Prices Commission in its reports has advo-cated a gradual reduction in wheat procurement prices, this recommendation hasnot been adopted, for political reasons. "Public procurement" in India involvesboth State and Union Governments. During the scarcity period, each state witha surplus, through its own procurement agency, gave first priority to obtain-ing supplies to satisfy the needs of its own consumers. There was littleenthusiasm for obtaining supplies at controlled prices on Government of India (GOI)account for distribution in deficit areas outside the state. With the easingof the supply position, the main aim of a surplus state has been to maintainthe price received by its producers, especially when the cost is borne by theUnion Government.

8. Previously, the effect of this policy on consumer prices was marked,as the GOI pooled supplies and costs of (expensive) domestic wheat and (cheap)imported wheat. This permitted the Food Corporation of India (FCI) to buydomestic wheat at Rs 76 per quintal and sell it at a common issue price of Rs 78per quintal; FCI's handling costs of at least Rs 20 per quintal was covered bythe cheaper cost of imports. Now, however, the proportion of domestic purchasesto imports is increasing, and, as a result, a subsidy of Rs 230 million(US$30 million) had to be provided in FY 1969/70.

9. FCI has now not only taken over all executive functions previouslycarried out by the Food Department but also increased its share of public food-grain operations in many states. It can now be said to be operating as theGovernment wholesaler in the public distribution system.

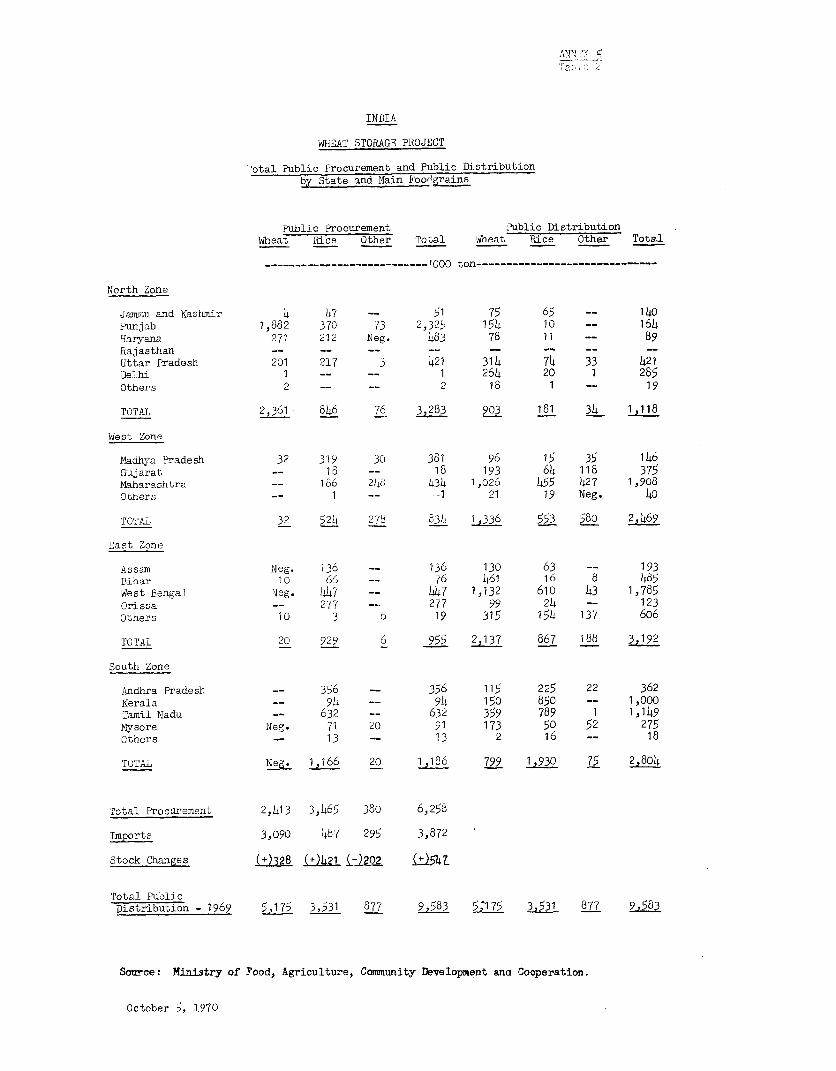

10. In the surplus wheat producing areas, State agencies procure quanti-ties of wheat sufficient to meet the public distribution needs within eachstate, while the "exportable" balance is purchased by FCI, either direct and/orthrough State agencies acting in its behalf. In Punjab, which accounts for over75% of all public wheat procurement (Table 2), the shares of these agencies intotal public purchases were as follows:

ANNEX 5Page 3

1969/70 1968/69Purchases Percentage Purchases Percentage

to End of Total to End of TotalJuly Purchases July Purchases'OOOT 'OOOT '

Procurement Agency

Punjab Civil SuppliesDepartment

(purchases for distributionwithin Punjab only) 307 17.o 309 24.0

FCI Interstate Distribution

Own purchases 734 40.0 498 38.5

Purchases +through agencyof Punjab CooperativeSupply and MarketingFederation 783 43.0 488 37.5

1,824 100.0 1,295 100.0

Purchases by the Punjab Civil Supplies Department remained at about the

same level, so that the residual purchase by or on behalf,of FRI increased withthe growth of the marketed surpluses.

11. Public sector buying agencies operate through the markets (mandis),using the traditional channels of buying and selling agents and public auction.The absence of standardized grading leads to visual assessment of each lot forprice differentials of only Rs 0.2r up or down on the basic purchase price ofRs 76 per quintal.

12. Harvesting of wheat in the surplus producing areas of North-west India(mainly Punjab, Haryana and Western Uttar Pradesh) takes place between mid-Apriland early July. Marketed surpluses have increased at an even faster rate thanproduction, as evidenced by the public procurement figures given below:

ANTNE X 5Page 4

Wheat 1.268/69 1967/68 1966 6

_________________- '000 tons)-----------

Production 20,000 18,650 16,567 11,528

Public procurement 3,700 2,386 2,262 815

Public procurement inpercentage of production 18.5 12.8 13.7 7.1

IEstimates.

At the same tine, the proportion of w1-eat marketings during the post-harvestmonths of April/June to annual marketings rose from about 65% to over 85%.This new marketing pattern was due to such factors as producers' fears thatGovernment agencies would not be able to sustain prices under pressure oflarger crops; doubts as to the storage capacity of the new varieties; thespread of mechanical threshers and irrigation, making possible increasedcropping intensity; and the shortage of on-farm storage.

October 5, 1970

ANNEX 5Table 1, Page 1

I' DIA

WHEAT STOiRAGE PROJECT

Public Distribution, Local Procurement and Imports

Op J Local Total Issues from Clos-Year Grain Openlng Procure- Imports avail- Govt ing

Stock ment ability Godown Stocks

--------------------imillion tons------------------------

1948 Rice 0.3 2.4 0.9 3.6 3.0 o.6

Wlh.a 0.2 Neg. 1,3 1.5 1,3 0,2Others 0.2 0.3 0.7 1.2 0.9 0.3Thtal °07 2.7 2.9 6.3 5.2 1.1

1949 Rice o.6 3.0 0.8 4.4 3.7 0.7heat 0.2 CO6 2.2 3.0 2.5 0.5Others 0.3 1.0 0.7 2.0 1.6 004

Total 1.1 Lt6 3.7 9.4 7.8 1.6

1950 Rice 0.7 2.8 0.3 3.8 3.5 0.3Wheat 0,5 1.1 1.5 3.1 2.8 0.3Others 0.4 0.8 0.3 1.5 1.4 0.1

Total 1.6 4.7 2.1 8.4 7.7 0.7

1951 Rtice 0.3 244 08 365 3.1 0.4Wheat 0.3 0O8 3.0 4.1 3.5 o.6Others 0.l oO6 1.0 1.7 144 0.3

Total 0.7 3.8 4.8 9.3 8.o 1.3

1952 Rice 0.4 2.0 0.7 3,1 2,5 o.6Wheat o.6 0,8 2.6 4.0 3,0 1.0Oth-t-r7 0.3 0O7 0,6 1.6 1,3 0.3

Total t 3a5 3,9 9,7 6.5 1.9

1953 Rice 0.6 1.7 0.2 2.5 2.0 0.5I*aeat 1.0 0.2 1.7 2.9 2.1 0.8Others 0.3 0.2 0.2 0,7 065 0,2Total 1,9 2.i 2,1 6.1 4.6 1.5

1954 Rice -. 1,4 0.7 2.6 1.0 1,6Wheat , 6 - 0.2 1.0 1.0 Neg.others ?.2 Neg. Neg. 0,2 0O1 01Total 114 0.9 3.5 2,1 1.7

1955 Rice 1.6 Neg. 0.3 109 1.2 0.7lWheat Neg. 0.1 0.4 0.5 0.3 0.2Othars 0.1 1 Neg. - 001 01 Neg,Total 1I.7 0,1 0.7 2,5 1.6 0.9

1956 R3ao N,g. 0.3 1.0 0.9 0.1Whlleat 0.2 - 1.1 1.3 1.1 0.2(Oters Neg. - Neg. Neg. -

Total 0.9 Neg. 1.4 2,3 2,0 0.3

October 5, 1970

ANNiX 5_e 1, Page 2

INDIA

WHEAT STORAGE PROJECT

Puolic Distribution, Local 'rocurement and Imports (Continued)

Local Total Issues from Clos-Year Grain Spockg Procure- Imports avail- Govt ingStack ment ability Codown Stocks

…-nmillion tons---------------------

1957 Rice 0.1 0.2 0.8 1.1 0.8 0.3Wheat 0.2 - 2.8 3.0 2.2 0.8Others - 0.1 - 0.1 Neg. 0.1Total 0.3 0.3 3.6 4.2 3.0 1T2

1958 ?ice 0.3 0.5 0.4 1.2 0.9 0.3Waheat 0.8 - 2.7 3,5 3.0 0.5Others 0.1 Neg. 0.1 0.2 0.1 0.1Total 1.2 0.5 3.2 t49 4.0 009

1959 Rice 0.3 1.5 0,3 2.1 1.4 0.7Wheat 0.5 0.3 3.5 4.3 3.6 0.7Others 0.1 Neg. Neg. 0.1 0.1 Neg.Total 0o9 1-, 3.7 6.5 5.1

1960 Rice 0.7 o.8 0.7 2.2 1.2 1.0Wheat 0.7 0.4 4,3 5.4 3.7 1.7Others Neg. Ne* _ 0.1 0.1 0.1 Neg.Total 1.'- 1.,' 5.-1 7.7 5.0 2.7

1961 Rice 1.0 0.5 0.4 1.9 1.0 0.9-Wheat 1.7 Neg. 3.0 4,7 3.0 1.7Others Neag. Neg. Neg. Neg. Neg. Neg.Total 2,7 0L5 3,4 6,6 4.0 2.6

1962 Rice o.9 0.5 0.4 1,8 1.2 o.6Wheat 1.7 Neg. 3.2 4.9 3.2 1.7Others Ney. Neg. - Neg. Neg. Neg,Total 2.6 005 3,6 6.7 4,4 2,3

1963 Rice o,6 0,7 0.5 1.8 1.4 0.4Wheat 1.7 Neg. 4.0 5.7 3.8 1.lOthers Neg. aeg, Neg. Neg. Neg.Total 2,3 0.7 o_ 7 5 5.2 2,3

1964 Rice 0.4 1,3 o.6 2,3 1.9 0,4Wheat 10° Neg. 5.6 7.5 6.9 o.6Others Neg. Neg. - Neg. Neg. Neg.Total T 103 9.5 Mo. 1.0

1965 Rica 0.4 2.9 0.8 4,1 3,5 o.6,dheat 01' 0. 4 6.6 7.6 6,2 1.4Others Ngeu. 007 0,1 oO8 0.7 0.1Tota 1 o 75 1225 10.L ; 2-1

October 5, 1970

ANNEX5Table 1, Page _

INDIA

WHEAT STORAGE PROJECT

Public iDistribution, Local R>rocurement and Imports (Continued)

Local Total Issues from Clos-Year Grain Opening Procure- Imports avail- Govt. ing

Stock ment ability Godown Stocks

--- n-illion tons----------------------

1966 Rice o.6 3.1 0.8 4.5 4.1 0.4Wheat 1.4 0.2 7.8 9.4 8.2 1.2Others 0.1 0.7 1.8 2.6 2.0 o.6Total 2.1 4.0 10.4 16,5 143 2.2

1967 Rice 0.4 2.8 0.5 3.7 3.1 o.6WJheat 1.2 0.8 6.4 8.4 7.4 1.0Others o.6 0.9 1.8 3,3 3.0 0.3Total 2.2 4,5 807 15.4 13.5 1.9

1968 Rice o.6 3.4 0.4 4.4 3.2 1.2Wheat 1.0 2.3 4.7 8.0 5.8 2.2Others 0.3 1.0 0.5 1.8 1.2 o.6Total 1.9 6.7 5.6 14.2 10.2 4.0

1969 Rice 1.2 3°5 0.5 5.2 3.4 1o8Wlheat 2.2 2.4 3.O 7.6 5.3 203Others o.6 04 0.3 1,3 1.0 0.3Total 4.0 6.3 3.8 14.1 ).7 474

October 5, 1970

AN 'T f:

INDIA

WHEAT STORAGE PROJECT

otal Public Procurement and Public Distributionby State and Main Foodgrains

Public Procurement Public DistributionWheat _ice Other To Dal Wheat Rice Other Total

--------------- ---------- '000 ton------------------------------

North Zone

Jammu and Kashmir 4 47 -- 51 75 65 -- 140Punjab 1,882 370 73 2,325 154 10 -- 164Haryana 271 212 Neg. 483 78 11 __ 89Rajasthan __ -- -- -- -- -_ --Uttar Pradesh 201 217 3 421 314 74 33 421Delhi 1 -- -- 1 264 20 1 285Others 2 -- -- 2 18 1 -- 19

TOTAL 2,361 846 76 3,283 903 181 34 1,118

West Zone

Madhya Pradesh 32 319 30 381 96 15 35 146Gujarat -- 18 -- 18 193 64 118 375Maharashtra -- 186 248 434 1,026 455 427 1,908Others -- 1 -- -1 21 19 Neg. 40

TOTAL 32 524 278 834 1,336 553 580 2,469

East Zone

Assam Neg. 136 -- 136 130 63 -- 193Bihar 10 66 -- 76 461 16 8 485West Bengal Neg. 447 -- 447 1,132 610 43 1,785Orissa -- 277 __ 277 99 24 -- 123Others 10 3 6 19 315 154 137 606

TOTAL 20 929 6 955 2,137 867 188 3,192

South Zone

Andhra Pradesh -- 356 356 115 225 22 362Kerala 94 -- 94 150 850 -- 1,000Tamil Nadu __ 632 __ 632 359 789 1 1,149Yiysore Neg. 71 20 91 173 50 52 275Others __ 13 -- 13 2 16 -- 18

TOTAL Neg 1,166 20 1,136 799 1,930 75 2,804

Total Procurement 2,413 3,465 380 6,258

Inports 3,090 487 29$ 3,872

Stock Changes (J)328 (J+)21 £-)202 Lt54?.

Total PublicDistribution - 1969 5,175 3,531 877 9,583 5, 175 3,531 877 9,583

Sonrce: Ministry of Food, Agriculture, Community Development ana Cooperation.

October 5, 1970

va5 ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~INDIA

WHEAT STORAGE PROJECT

Total Public Storage Ca02r4tcandS;oeks (as of March 31, 1970)

TDTaD STORAGE CAPACITY Total STORAGE CAPACITY WITT FCIFoodgrainc Hired Hired Total Total

Total with Total sith FGI Stocks from from Hired Hired Total Capacity StocksPCI State Govt CWC 1/ Total Hired frb,, Total- ith All FCI Private State from from Hired with with

Nc. Stats/Zone OGaed Osmed Omrea Owned Private Sector CaPacity Aguncies Owned Sector Govt SWC 2/ CNO b CI FCI FCI(2) 727(T5) (7) -79- 7--7) -MT) (11) 77 TT37' $F 7(177 T

!NORTH ZONS

1. Pomjab 261 32 11 3Q4 144 448 377 261 144 18 1 10 173 434 2182. Haryana 70 35 13 118 14 132 69 70 14 - - - 14 84 483. Rajacsthac 69 30 41 140 - 140 127 69 - - 38 19 57 126 854. Uttar Pradesh 034 46 15 495 135 630 293 434 135 32 25 14 206 640 2355. Delhi 119 30 149 - 149 75 119 - C - 90 20 139 72

Total 953 143 110 1,206 293 1,499 941 953 293 50 64 63 470 1,423 658

WEST ZONE

6. Madhya Pradesh 81 82 17 180 58 238 113 81 58 33 29 7 127 208 1067. Gujarat 49 138 13 200 90 290 229 49 90 33 6 34 163 212 1478. Mrhsrashtrr 680 426 24 1,130 275 1,405 1,003 680 275 96 - 3 374 1,054 797

Total 810 646 54 1,510 423 1,933 1.345 810 423 162 35 44 664 1 ,474 1 050

EAST ZONE

9. Asesm 40 16 18 74 90 164 132 bo 90 6 12 6 114 154 10410. Bihar 165 17 - 182 13 195 150 165 13 9 - - 22 187 10011. West BRngal 2G2 293 - 555 262 817 490 262 262 274 63 219 818 1,079 40912. Orissa 125 41 5 61 4 65 1 3 15 4 3 8 14 19 34 16

Total 482 367 23 872 369 1,241 935 482 369 292 63 229 973 '1,454 629

SOTh ZONE

13. Andhra Pradech 130 88 322 540 12 552 280 130 12 12 41 3°4 369 498 28314.E.Yeralo 138 39 9 185 58 243 243 138 58 29 7 10 104 243 20015. Tamil NHd, 198 22 214 434 18 452 319 198 18 1 3 133 155 353 2066. Yysore 60 53 20 133 - 133 146 60 _ - _ 6 14 74 43

octal 526 202 565 1,292 88 ,380 988 526 88 50 51 453 642 1,167 732

17. Union - 89 - 89 - 89 109 _ - - - --Territories _

Grand Total 2,771 1,447 252 4,969 1,173 6,142 4,31P 2,771 1,173 5514 333 _9 2,749 5,520 3,069

YearMarch 1970 2,771 1,447 751 4,969 1,171 6,142 4,318 2,771 1,173 555 233 789 2,719 5,520 3,069March 1969 2,4 25 1,447 657 4,529 1,451 5,980 4,516 2,125 ----- 1,451---- 316 717 2,484 4,909 3,253March 1968 1,243 1,447 652 3 .cg3/ 461 4,919 2,031 1,243 461 Incl. in I-cl.in 272 733 1,976 1,471March 1967 1,052 1582 52 15'7r 3 454 14811 2,064 1,052 454 001.1C" Ccl 10 148 602 1,654 680March 1966 569 1,447 416 4,156 !/ 49 4,205 3,274 569 49 " I' 70 119 688 543

4/ Central Wrrehonsing Corporation.

2/ State Warehousing Corporation.

3/ Includirg CentraL Food Departeerc or.ed.

INDIA

WHEAT STORAGE PROJECT

Analysis of Operational Storage Requirements