investor & analyst update -...

TRANSCRIPT

1Q12 results and comments

INVESTOR & ANALYST UPDATE

11th May 2012

1

DISCLAIMER

The views expressed here contain information derived from publicly available sources that have not been independently verified. No

representation or warranty is made as to the accuracy, completeness or reliability of the information. Any forward looking information in this

presentation has been prepared on the basis of a number of assumptions which may prove to be incorrect. This presentation should not be

relied upon as a recommendation or forecast by Banpu Public Company Limited. Nothing in this release should be construed as either an

offer to sell or a solicitation of an offer to buy or sell shares in any jurisdiction.

2

1. Focus: long term coal market analysis

2. Coal operations

3. Coal marketing

4. Power business

5. Financial summary

Appendices

3

1. Focus: long term coal market analysis

4

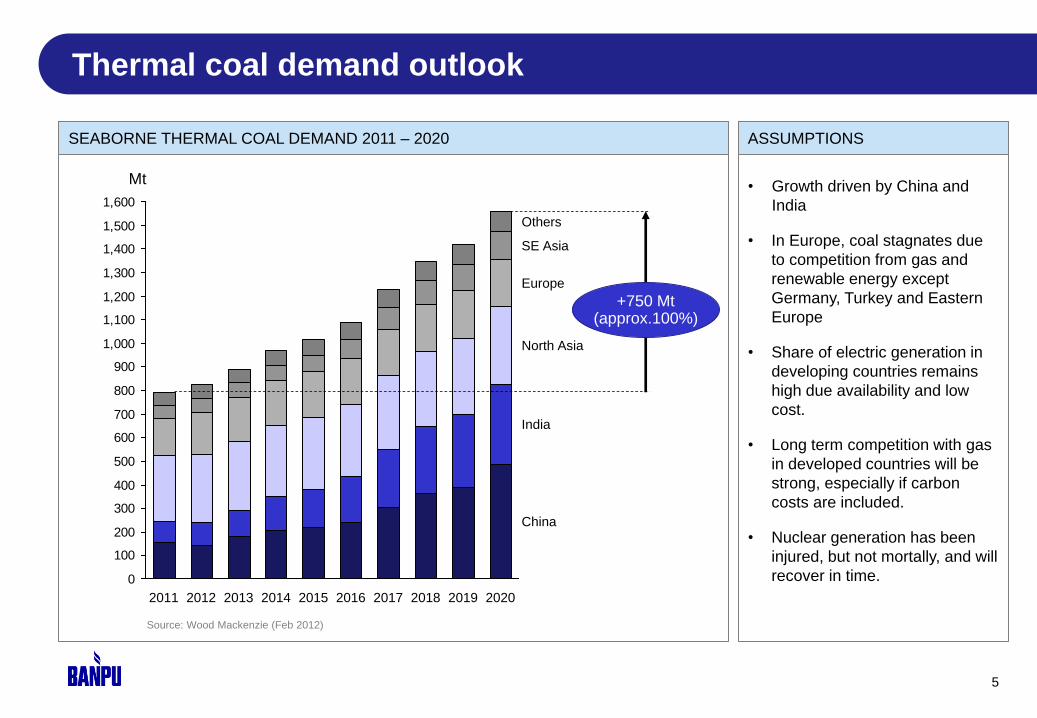

Thermal coal demand outlook

5

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

+750 Mt (approx.100%)

China

India

North Asia

Europe

SE Asia

Others

2020 2019 2018 2017 2016 2015 2014 2013 2012 2011

Source: Wood Mackenzie (Feb 2012)

Unit: Mt SEABORNE THERMAL COAL DEMAND 2011 – 2020 ASSUMPTIONS

• Growth driven by China and

India

• In Europe, coal stagnates due

to competition from gas and

renewable energy except

Germany, Turkey and Eastern

Europe

• Share of electric generation in

developing countries remains

high due availability and low

cost.

• Long term competition with gas

in developed countries will be

strong, especially if carbon

costs are included.

• Nuclear generation has been

injured, but not mortally, and will

recover in time.

Mt

6

Future dynamics (focus on Asia) IS

SU

ES

GOVT.

POLICY

DEMAND

ELASTICITY

NUCLEAR GAS FREIGHT ECONOMY

• Growth from

developing

countries

• EU debt

concern

• Exchange rate

• Credit issues

• China – coal price cap

• India - nuclear policy,

coal tax, environmental

policy

• Indonesian – Domestic

Market Obligation (DMO),

coal reference price, low

rank coal export ban?,

export tax?, foreign

ownership limit

• Australia – Mineral

Resource Rent Tax

(MRRT), Carbon tax

• South Africa – Mining law

and tax policy

• Development time lags

• Demand-side

management and

new technologies

• Japan – Target to

reduce energy

consumption by

7% by 2030

• China – Target to

reduce energy

intensity by 16%

and carbon

intensity by17%

by 2015 vs 2010

• Medium term

• Japan – closed,

approx.90 mtce*

or 26%, how

much will come

back?

• Taiwan –

capped?

• China and India –

diversification

and supply

security?

• Aftereffect from

Fukushima

incident

• Time lags if

recover

• US – low gas

price, availability

of domestic coal

• China –

development of

shale gas,

pipeline from

Russia and

Myanmar

• Gas price in Asia

link to oil price -

uncompetitive to

coal. Will this

delink for LNG?

• Time lags

• Low freight rates

now

• Will rise and

limit Columbia,

USA and some

South Africa

exports to Asia

• Short to medium

term

+ + +

- -

-

+ +

- - -

IMP

AC

T

+

Note: * mtce means million ton coal equivalent

7

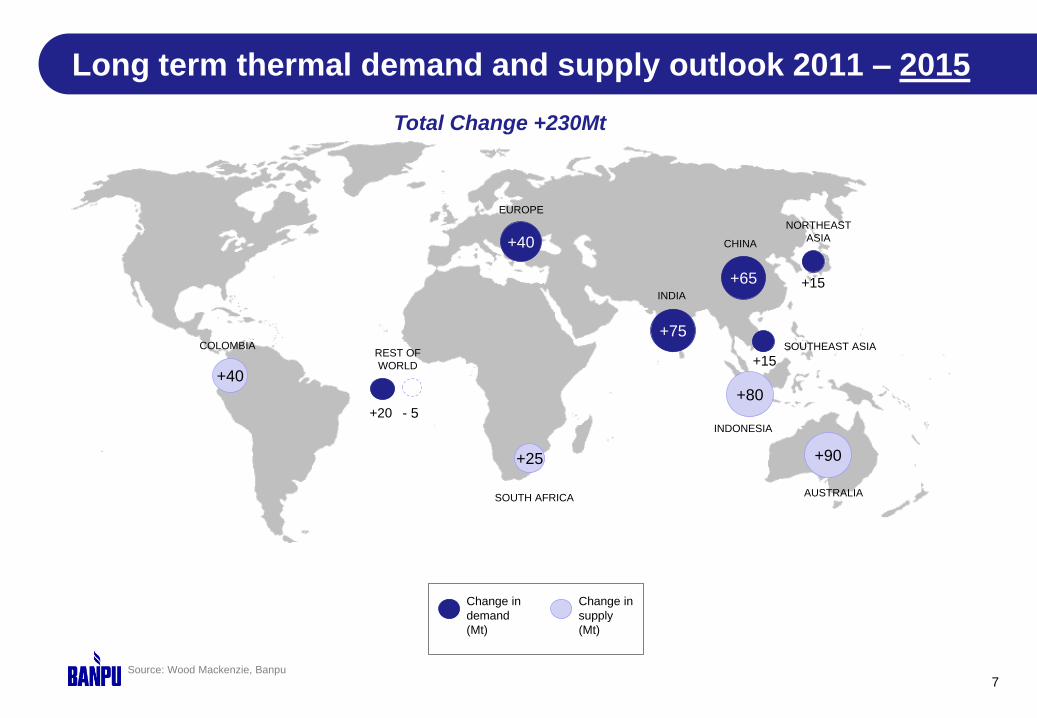

Long term thermal demand and supply outlook 2011 – 2015

Source: Wood Mackenzie, Banpu

Change in

supply

(Mt)

Change in

demand

(Mt)

+112 +75

+65 +15

+40

+20

+15 REST OF

WORLD

NORTHEAST

ASIA

SOUTHEAST ASIA

CHINA

INDIA

EUROPE

+90 +25

+40

+80 - 5

COLOMBIA

SOUTH AFRICA

INDONESIA

AUSTRALIA

Total Change +230Mt

+30

+320

+245

+45 NORTHEAST

ASIA

SOUTHEAST

ASIA +65

+45

8

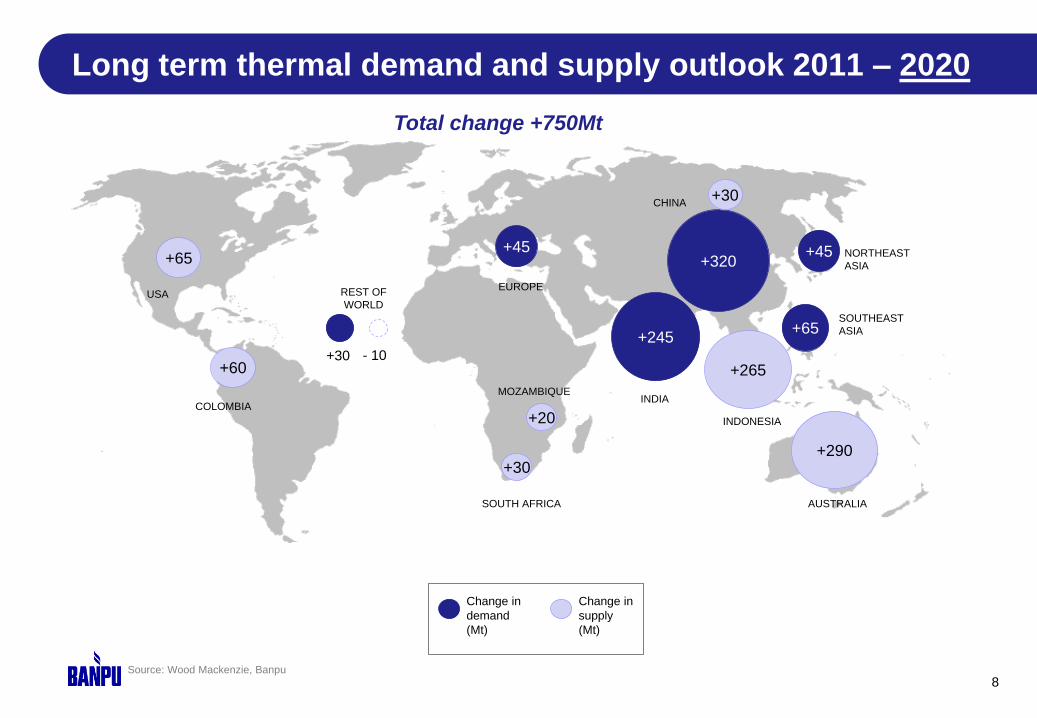

Long term thermal demand and supply outlook 2011 – 2020

Change in

supply

(Mt)

Change in

demand

(Mt)

REST OF

WORLD

INDIA

CHINA

EUROPE

+290

+265

+65

+20

+30

+30

+60 - 10

AUSTRALIA

INDONESIA

SOUTH AFRICA

MOZAMBIQUE

COLOMBIA

USA

Source: Wood Mackenzie, Banpu

Total change +750Mt

9

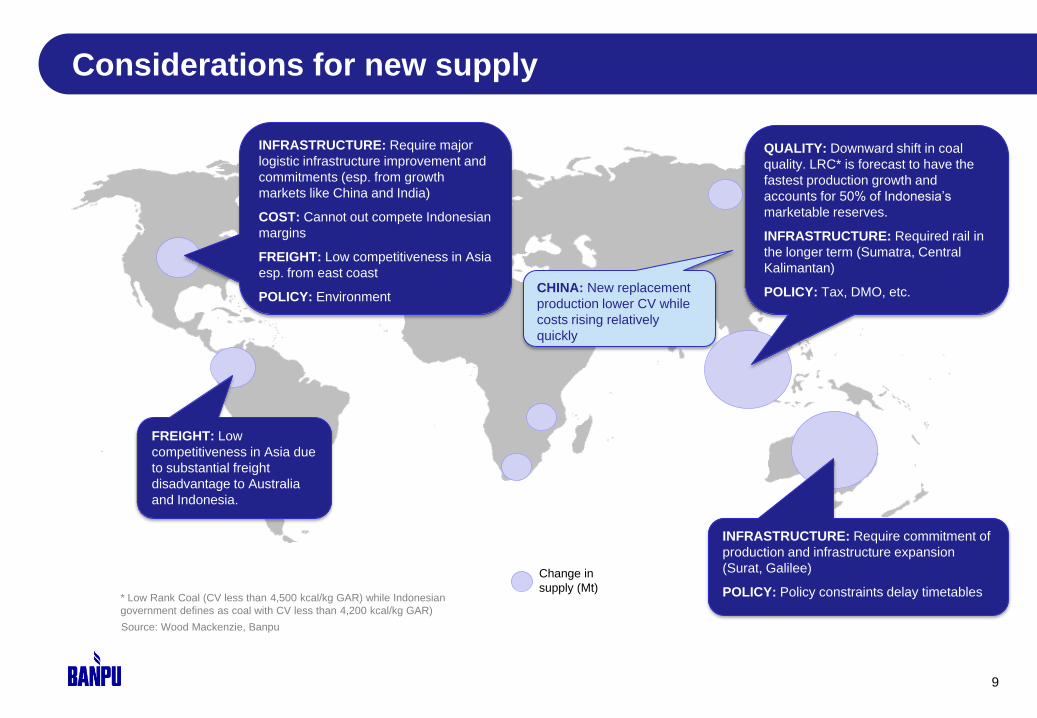

Considerations for new supply

Source: Wood Mackenzie, Banpu

Change in

supply (Mt)

QUALITY: Downward shift in coal

quality. LRC* is forecast to have the

fastest production growth and

accounts for 50% of Indonesia’s

marketable reserves.

INFRASTRUCTURE: Required rail in

the longer term (Sumatra, Central

Kalimantan)

POLICY: Tax, DMO, etc.

INFRASTRUCTURE: Require commitment of

production and infrastructure expansion

(Surat, Galilee)

POLICY: Policy constraints delay timetables

FREIGHT: Low

competitiveness in Asia due

to substantial freight

disadvantage to Australia

and Indonesia.

INFRASTRUCTURE: Require major

logistic infrastructure improvement and

commitments (esp. from growth

markets like China and India)

COST: Cannot out compete Indonesian

margins

FREIGHT: Low competitiveness in Asia

esp. from east coast

POLICY: Environment

* Low Rank Coal (CV less than 4,500 kcal/kg GAR) while Indonesian

government defines as coal with CV less than 4,200 kcal/kg GAR)

CHINA: New replacement

production lower CV while

costs rising relatively

quickly

10

More capacity is required to support growing demand

AUSTRALIA (40% of supply growth 2011 – 2020) INDONESIA (35% of supply growth 2011 – 2020)

0

50

100

150

200

250

Surat

Sydney

Galilee

Gunnedah

Others

Identified supply Required supply growth

Source: Wood Mackenzie, Banpu

Potential

0

50

100

150

200

250

Barito

E. Kali

Mahakam

Sumatra

Others

Identified supply Required supply growth

Source: Wood Mackenzie, Banpu

• Require additional supply for medium and long term need

• Rely on Sydney basin in the short term and Surat in the

longer term

• Surat and Galilee require new infrastructure

• Environmental sensitivities and challenges

• Off-Spec coal (high ash) becomes attractive

• Limited large scale project in pipeline

• More than half of identified supply is LRC

• Environmental and policy constraints

• Off-Spec coal (low CV or high sulphur) becomes attractive

Potential

Mt Mt

11

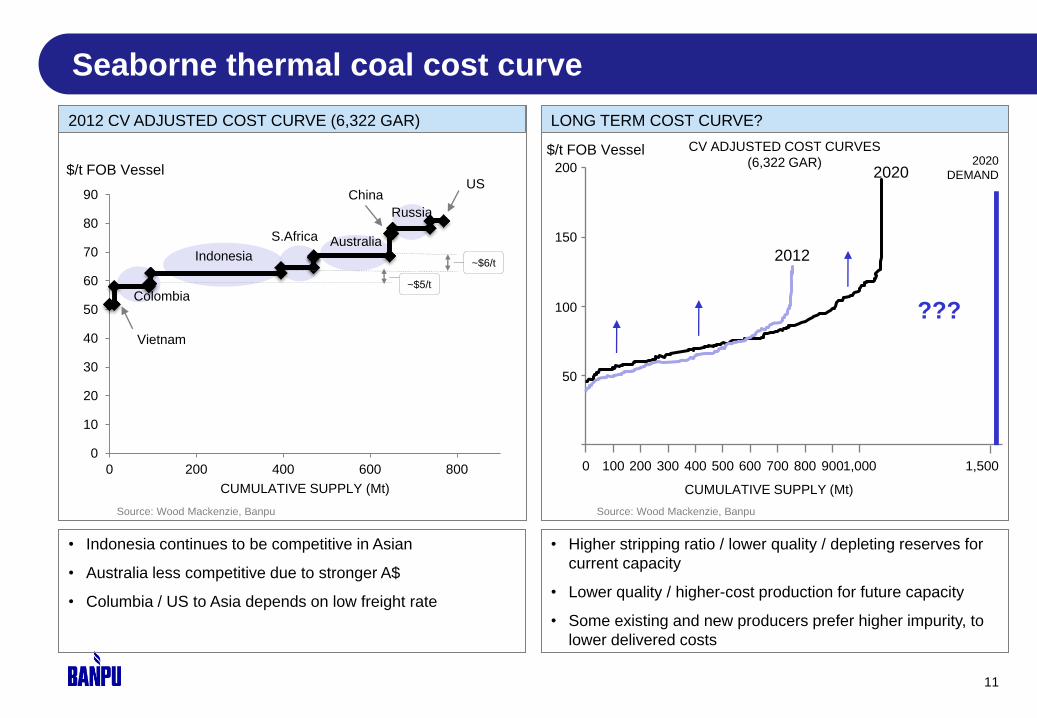

Seaborne thermal coal cost curve

2012 CV ADJUSTED COST CURVE (6,322 GAR) LONG TERM COST CURVE?

0

10

20

30

40

50

60

70

80

90

0 200 400 600 800

CUMULATIVE SUPPLY (Mt)

Vietnam

Indonesia

Colombia

S.Africa Australia

Russia

China US

Source: Wood Mackenzie, Banpu

• Higher stripping ratio / lower quality / depleting reserves for

current capacity

• Lower quality / higher-cost production for future capacity

• Some existing and new producers prefer higher impurity, to

lower delivered costs

• Indonesia continues to be competitive in Asian

• Australia less competitive due to stronger A$

• Columbia / US to Asia depends on low freight rate

CUMULATIVE SUPPLY (Mt)

0 100 200 300 400 500 600 700 800 900 1,000 1,500

50

100

150

200

2012

2020 2020

DEMAND

CV ADJUSTED COST CURVES

(6,322 GAR)

Source: Wood Mackenzie, Banpu

???

$/t FOB Vessel

$/t FOB Vessel

~$6/t

~$5/t

12

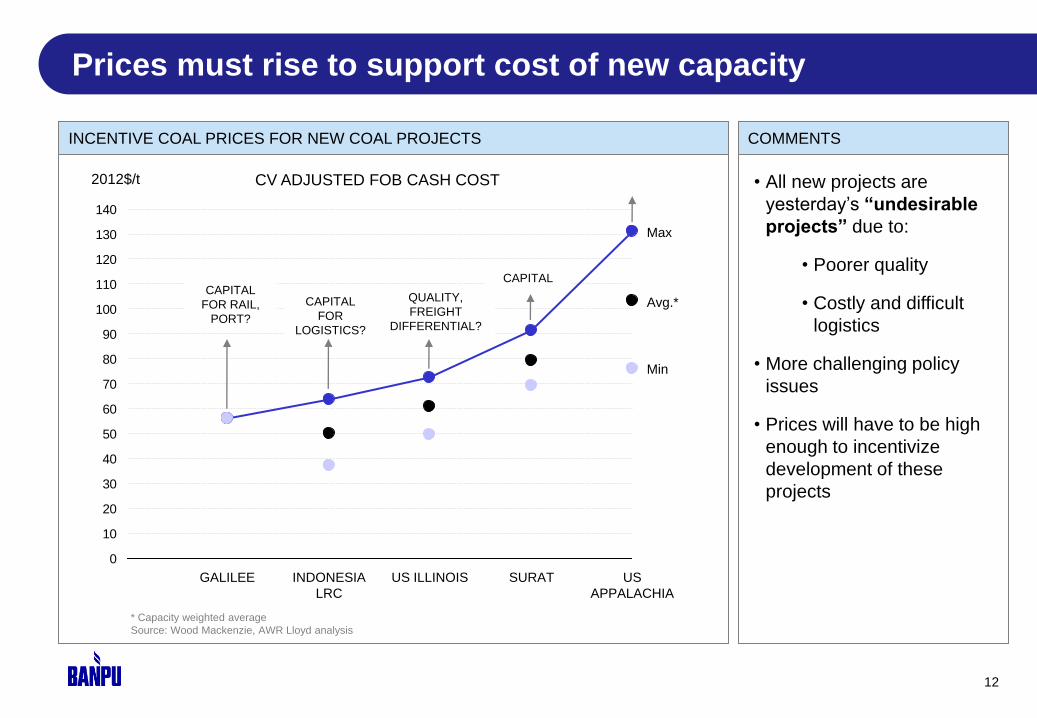

Prices must rise to support cost of new capacity

• All new projects are

yesterday’s “undesirable

projects” due to:

• Poorer quality

• Costly and difficult

logistics

• More challenging policy

issues

• Prices will have to be high

enough to incentivize

development of these

projects

ILLUSTRATIVE INCENTIVE PRICES FOR NEW COAL PROJECTS ($/t) INCENTIVE COAL PRICES FOR NEW COAL PROJECTS COMMENTS

* Capacity weighted average

Source: Wood Mackenzie, AWR Lloyd analysis

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

Min

Avg.*

Max

US

APPALACHIA

SURAT US ILLINOIS INDONESIA

LRC

GALILEE

CV ADJUSTED FOB CASH COST

CAPITAL

FOR RAIL,

PORT?

CAPITAL

FOR

LOGISTICS?

QUALITY,

FREIGHT

DIFFERENTIAL?

CAPITAL

2012$/t

13

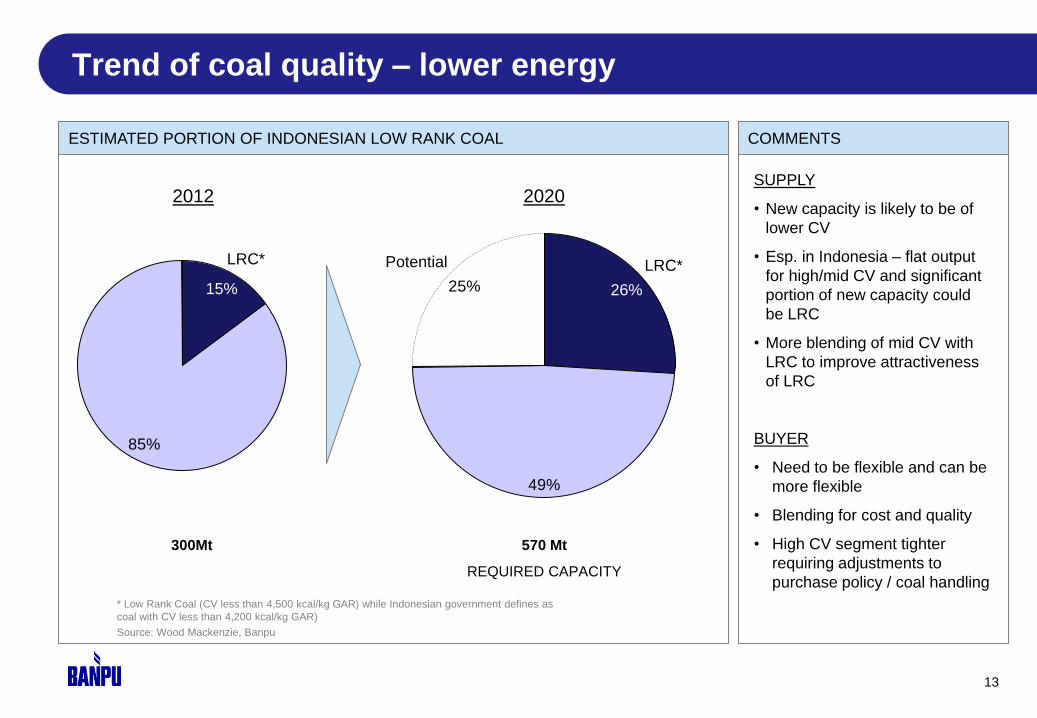

Trend of coal quality – lower energy

ESTIMATED PORTION OF INDONESIAN LOW RANK COAL COMMENTS

85%

LRC*

15% 25%

49%

Potential LRC*

26%

300Mt 570 Mt

REQUIRED CAPACITY

2012 2020

Source: Wood Mackenzie, Banpu

SUPPLY

• New capacity is likely to be of

lower CV

• Esp. in Indonesia – flat output

for high/mid CV and significant

portion of new capacity could

be LRC

• More blending of mid CV with

LRC to improve attractiveness

of LRC

BUYER

• Need to be flexible and can be

more flexible

• Blending for cost and quality

• High CV segment tighter

requiring adjustments to

purchase policy / coal handling

* Low Rank Coal (CV less than 4,500 kcal/kg GAR) while Indonesian government defines as

coal with CV less than 4,200 kcal/kg GAR)

14

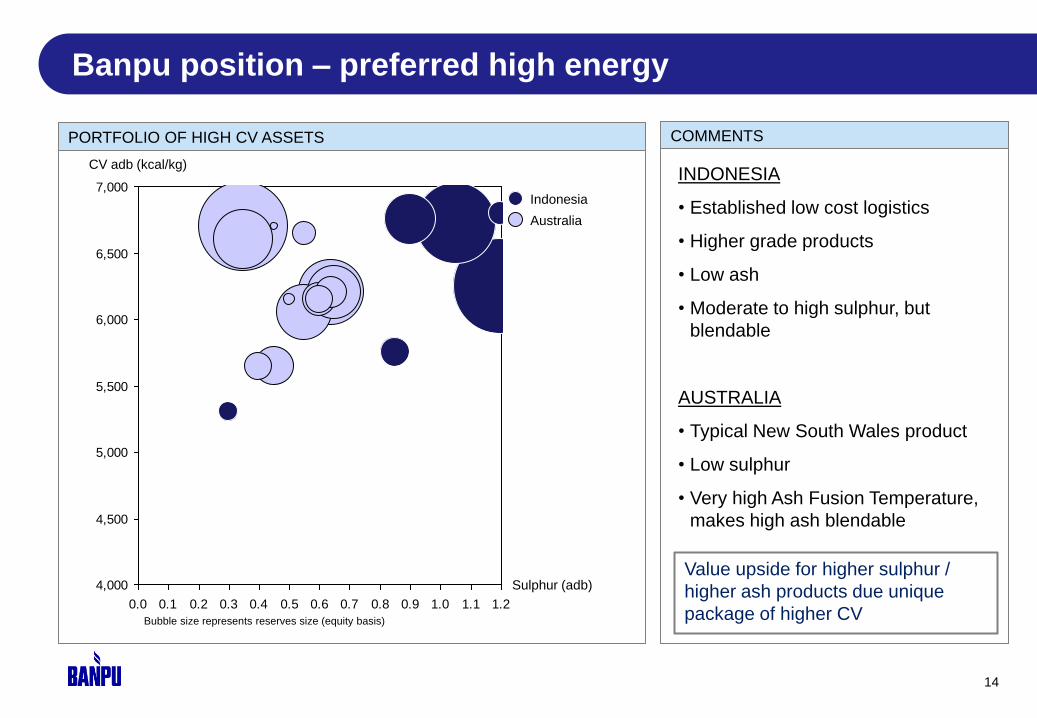

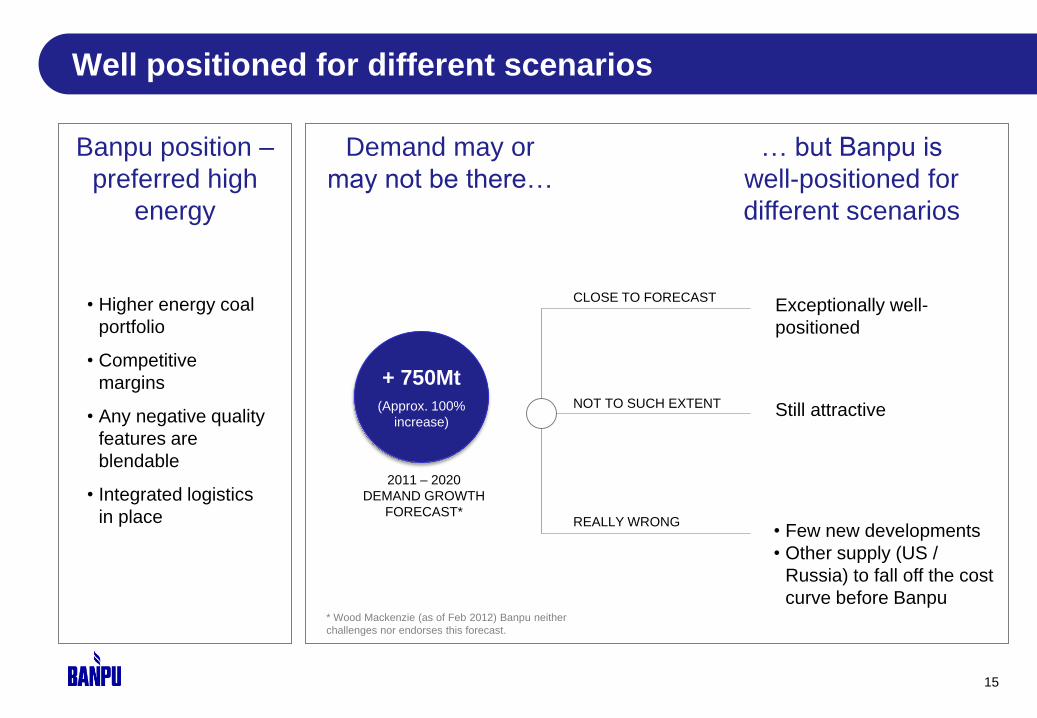

Banpu position – preferred high energy

PORTFOLIO OF HIGH CV ASSETS

4,000

4,500

5,000

5,500

6,000

6,500

7,000

0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0 1.1 1.2

Sulphur (adb)

CV adb (kcal/kg)

Australia

Indonesia

Bubble size represents reserves size (equity basis)

COMMENTS

INDONESIA

• Established low cost logistics

• Higher grade products

• Low ash

• Moderate to high sulphur, but

blendable

AUSTRALIA

• Typical New South Wales product

• Low sulphur

• Very high Ash Fusion Temperature,

makes high ash blendable

Value upside for higher sulphur /

higher ash products due unique

package of higher CV

15

Well positioned for different scenarios

• Higher energy coal

portfolio

• Competitive

margins

• Any negative quality

features are

blendable

• Integrated logistics

in place

Demand may or

may not be there…

… but Banpu is

well-positioned for

different scenarios

CLOSE TO FORECAST

NOT TO SUCH EXTENT

REALLY WRONG

Exceptionally well-

positioned

Still attractive

• Few new developments

• Other supply (US /

Russia) to fall off the cost

curve before Banpu

Banpu position –

preferred high

energy

* Wood Mackenzie (as of Feb 2012) Banpu neither

challenges nor endorses this forecast.

+ 750Mt

(Approx. 100%

increase)

2011 – 2020

DEMAND GROWTH

FORECAST*

2. Coal operations

16

2. Coal divisions

(a) Australia Coal

(b) Indonesia Coal

(c) China Coal

(d) Mongolia Coal

2. Coal operations

17

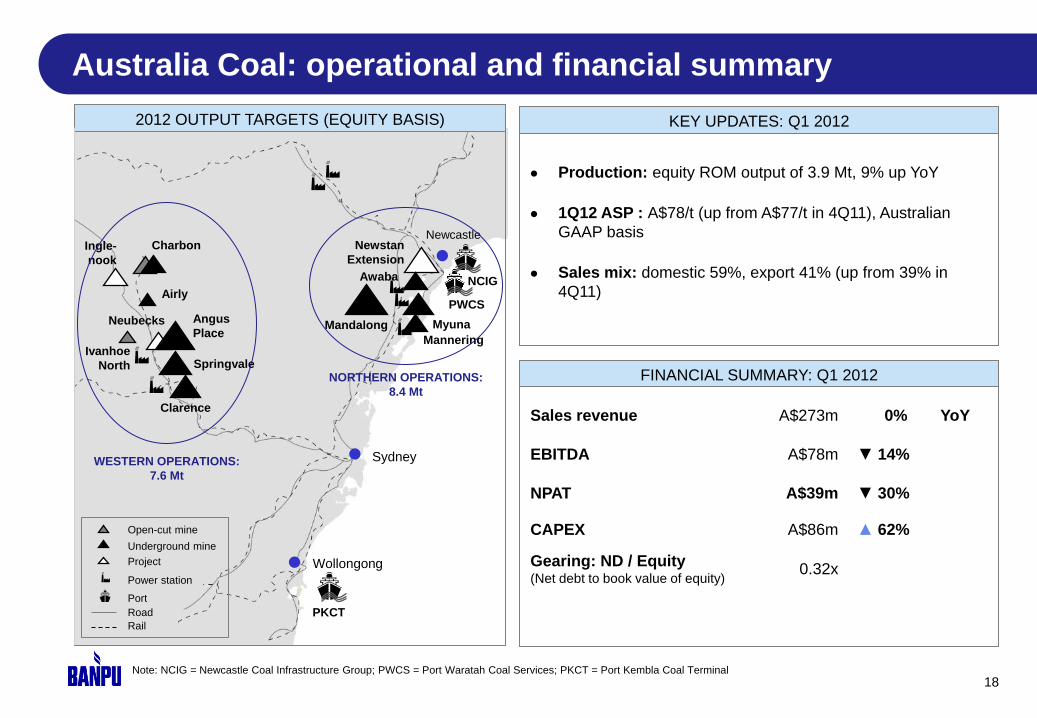

Australia Coal: operational and financial summary

18

Ivanhoe

North

Wollongong

PKCT

Charbon

Airly

Neubecks Angus

Place

Clarence

Springvale

Mandalong

Mannering

Myuna

Newstan

Extension

Awaba

Sydney

PWCS

Newcastle Ingle-

nook

Open-cut mine

Project

Underground mine

Port

Power station

Road

Rail

WESTERN OPERATIONS:

7.6 Mt

NORTHERN OPERATIONS:

8.4 Mt

2012 OUTPUT TARGETS (EQUITY BASIS)

NCIG

KEY UPDATES: Q1 2012

● Production: equity ROM output of 3.9 Mt, 9% up YoY

● 1Q12 ASP : A$78/t (up from A$77/t in 4Q11), Australian

GAAP basis

● Sales mix: domestic 59%, export 41% (up from 39% in

4Q11)

FINANCIAL SUMMARY: Q1 2012

Sales revenue A$273m 0% YoY

EBITDA A$78m ▼ 14%

NPAT A$39m ▼ 30%

CAPEX A$86m ▲ 62%

Gearing: ND / Equity (Net debt to book value of equity)

0.32x

Note: NCIG = Newcastle Coal Infrastructure Group; PWCS = Port Waratah Coal Services; PKCT = Port Kembla Coal Terminal

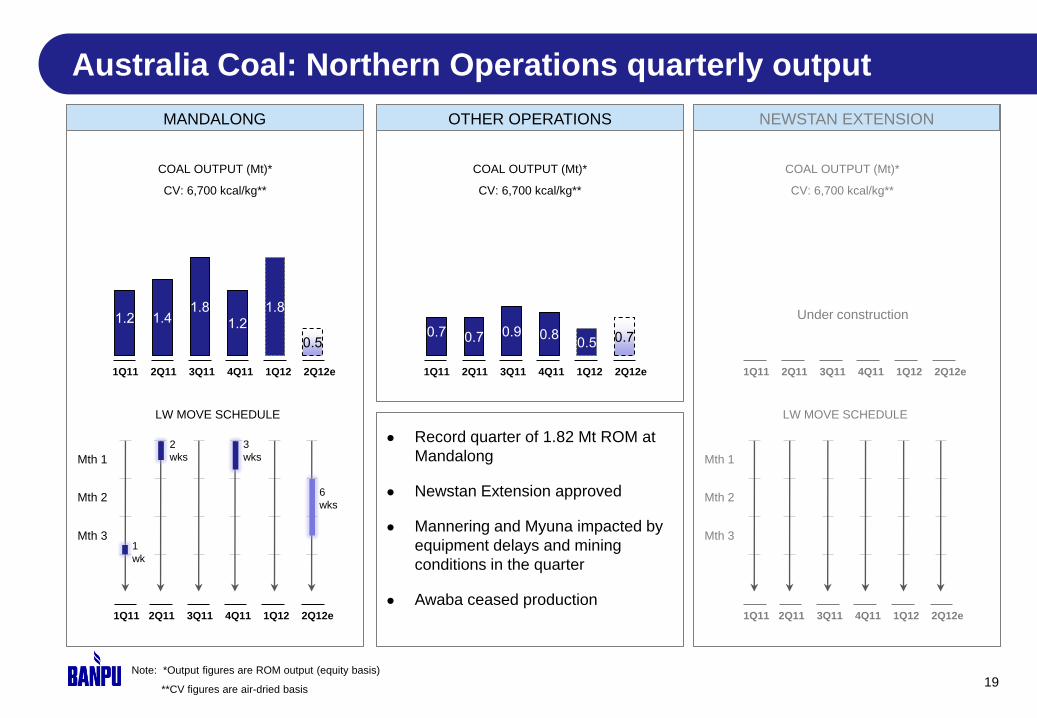

Australia Coal: Northern Operations quarterly output

19

OTHER OPERATIONS

● Record quarter of 1.82 Mt ROM at

Mandalong

● Newstan Extension approved

● Mannering and Myuna impacted by

equipment delays and mining

conditions in the quarter

● Awaba ceased production

MANDALONG

1.2 1.4 1.8

1.2

1.8

0.5

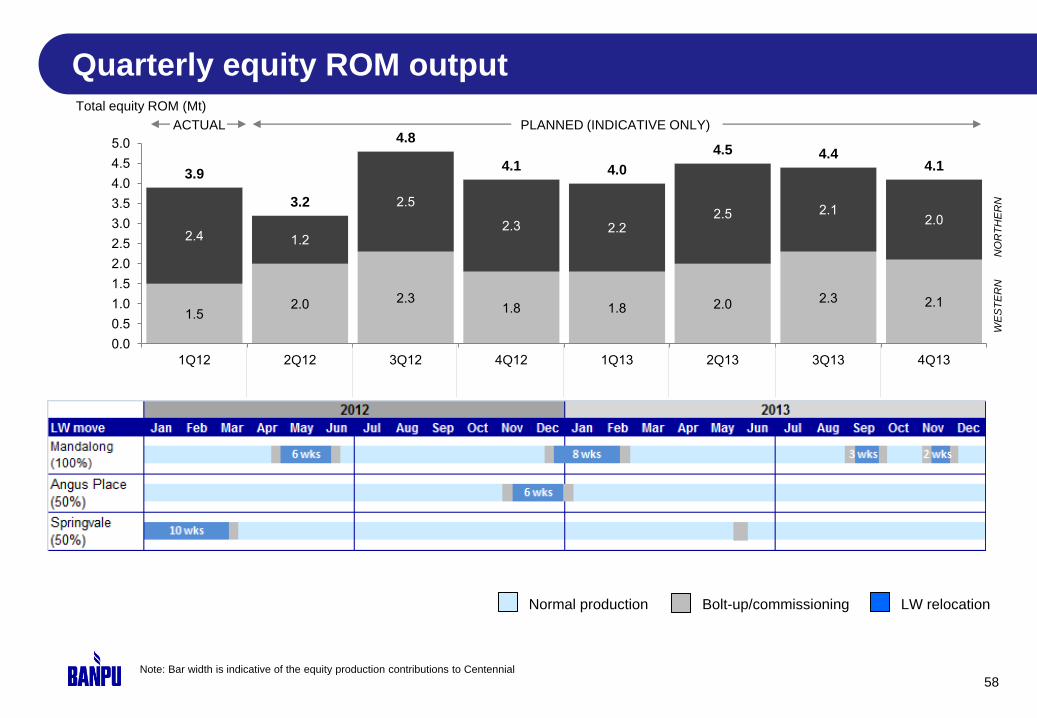

LW MOVE SCHEDULE

1

wk

2

wks

3

wks

6

wks

0.7 0.7 0.9 0.8 0.5 0.7

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12e

NEWSTAN EXTENSION

LW MOVE SCHEDULE

Mth 1

Mth 2

Mth 3

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12e

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12e

Under construction

Note: *Output figures are ROM output (equity basis)

**CV figures are air-dried basis

COAL OUTPUT (Mt)*

CV: 6,700 kcal/kg**

COAL OUTPUT (Mt)*

CV: 6,700 kcal/kg**

COAL OUTPUT (Mt)*

CV: 6,700 kcal/kg**

Mth 1

Mth 2

Mth 3

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12e

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12e

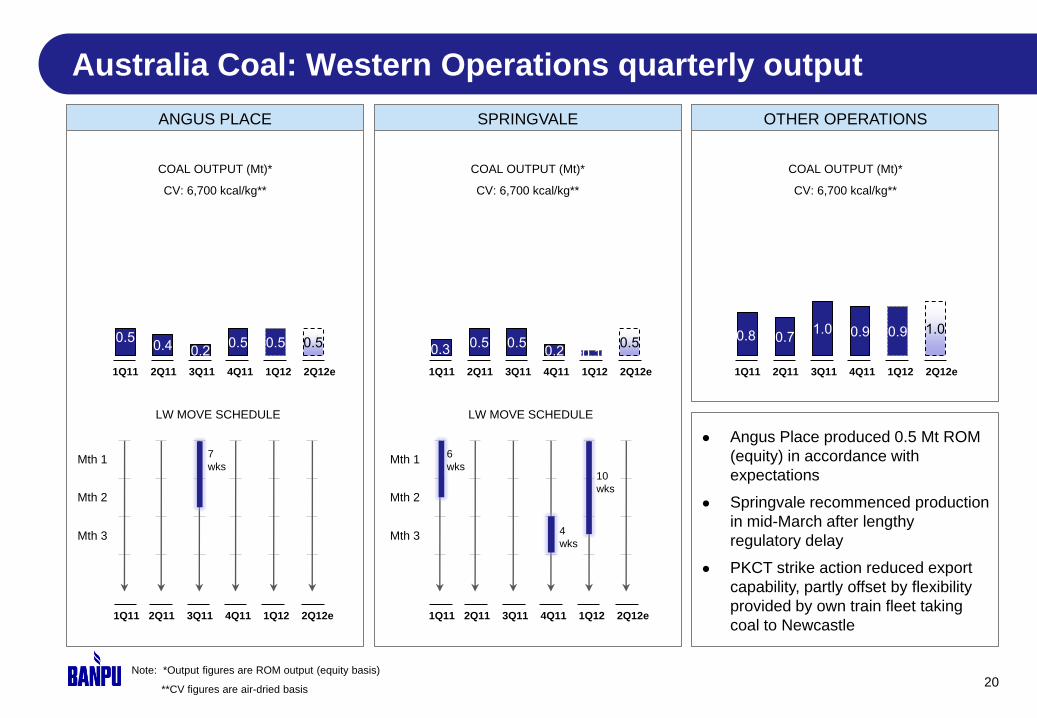

Australia Coal: Western Operations quarterly output

20

OTHER OPERATIONS

Note: *Output figures are ROM output (equity basis)

**CV figures are air-dried basis

● Angus Place produced 0.5 Mt ROM

(equity) in accordance with

expectations

● Springvale recommenced production

in mid-March after lengthy

regulatory delay

● PKCT strike action reduced export

capability, partly offset by flexibility

provided by own train fleet taking

coal to Newcastle

ANGUS PLACE SPRINGVALE

LW MOVE SCHEDULE

Mth 1

Mth 2

Mth 3

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12e

6

wks 10

wks

0.3 0.5 0.5

0.2 0.1 0.5

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12e

COAL OUTPUT (Mt)*

CV: 6,700 kcal/kg**

LW MOVE SCHEDULE

Mth 1

Mth 2

Mth 3

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12e

0.5 0.4 0.2

0.5 0.5 0.5

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12e

7

wks

4

wks

0.8 0.7 1.0 0.9 0.9 1.0

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12e

COAL OUTPUT (Mt)*

CV: 6,700 kcal/kg**

COAL OUTPUT (Mt)*

CV: 6,700 kcal/kg**

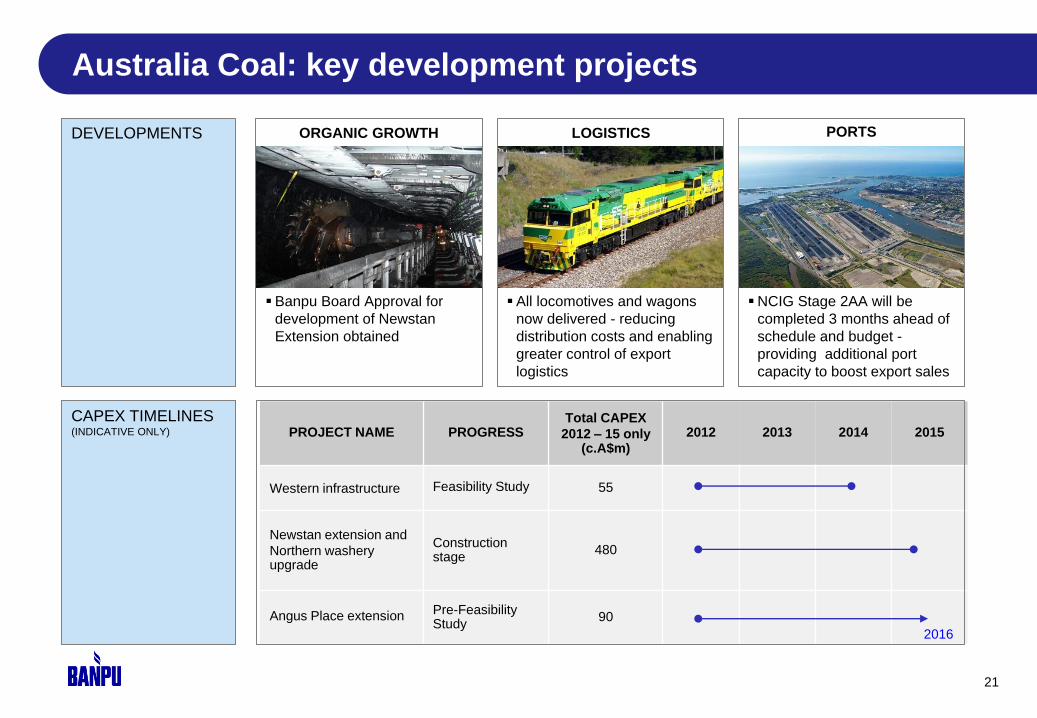

Australia Coal: key development projects

21

DEVELOPMENTS

CAPEX TIMELINES (INDICATIVE ONLY)

Banpu Board Approval for

development of Newstan

Extension obtained

All locomotives and wagons

now delivered - reducing

distribution costs and enabling

greater control of export

logistics

NCIG Stage 2AA will be

completed 3 months ahead of

schedule and budget -

providing additional port

capacity to boost export sales

ORGANIC GROWTH LOGISTICS PORTS

PROJECT NAME PROGRESS Total CAPEX

2012 – 15 only (c.A$m)

2012 2013 2014 2015

Western infrastructure Feasibility Study 55

Newstan extension and

Northern washery upgrade

Construction stage 480

Angus Place extension Pre-Feasibility Study 90

2016

2. Coal divisions

(a) Australia Coal

(b) Indonesia Coal

(c) China Coal

(d) Mongolia Coal

2. Coal operations

22

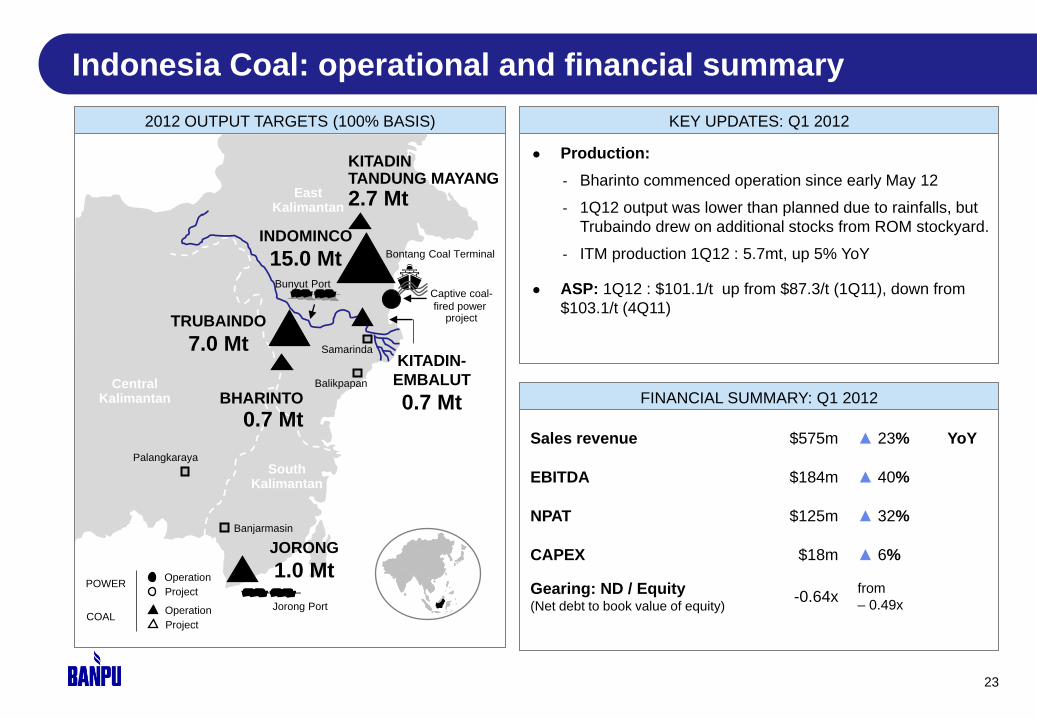

Indonesia Coal: operational and financial summary

23

East Kalimantan

Bunyut Port

Balikpapan

Palangkaraya

Banjarmasin

Central Kalimantan

South Kalimantan

KITADIN-

EMBALUT

0.7 Mt

INDOMINCO

15.0 Mt

TRUBAINDO

7.0 Mt

BHARINTO 0.7 Mt

JORONG

1.0 Mt

Samarinda

Jorong Port

Operation

Project

Operation

Project

POWER

COAL

Bontang Coal Terminal

Captive coal-

fired power project

KITADIN TANDUNG MAYANG

2.7 Mt

2012 OUTPUT TARGETS (100% BASIS) KEY UPDATES: Q1 2012

● Production:

- Bharinto commenced operation since early May 12

- 1Q12 output was lower than planned due to rainfalls, but

Trubaindo drew on additional stocks from ROM stockyard.

- ITM production 1Q12 : 5.7mt, up 5% YoY

● ASP: 1Q12 : $101.1/t up from $87.3/t (1Q11), down from

$103.1/t (4Q11)

FINANCIAL SUMMARY: Q1 2012

Sales revenue $575m ▲ 23% YoY

EBITDA $184m ▲ 40%

NPAT $125m ▲ 32%

CAPEX $18m ▲ 6%

Gearing: ND / Equity (Net debt to book value of equity)

-0.64x from

– 0.49x

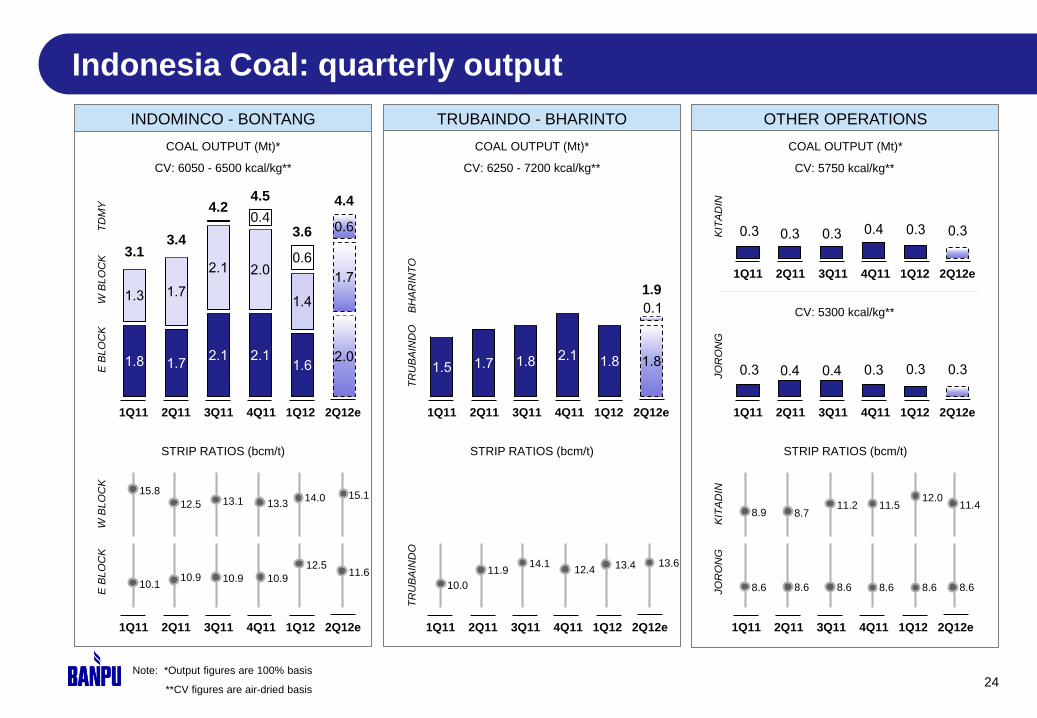

Indonesia Coal: quarterly output

24

TRUBAINDO - BHARINTO OTHER OPERATIONS INDOMINCO - BONTANG

COAL OUTPUT (Mt)*

CV: 6050 - 6500 kcal/kg**

COAL OUTPUT (Mt)*

CV: 6250 - 7200 kcal/kg**

COAL OUTPUT (Mt)*

CV: 5750 kcal/kg**

CV: 5300 kcal/kg**

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12e

E B

LO

CK

T

DM

Y

W B

LO

CK

TR

UB

AIN

DO

B

HA

RIN

TO

JO

RO

NG

K

ITA

DIN

STRIP RATIOS (bcm/t) STRIP RATIOS (bcm/t) STRIP RATIOS (bcm/t)

10.9

13.1

10.9

13.3

10.1

15.8

10.9

12.5

E B

LO

CK

W

BLO

CK

TR

UB

AIN

DO

8.6

11.5

8.6

8.9

8.6

8.7

8.6

11.2

JO

RO

NG

K

ITA

DIN

Note: *Output figures are 100% basis

**CV figures are air-dried basis

1.8 1.7 2.1 2.1

1.6 2.0

1.3 1.7

2.1 2.0

1.4

1.7

0.4

0.6

0.6

3.1 3.4

4.2 4.5

3.6

4.4

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12e

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12e

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12e

10.0

11.9 14.1

12.4

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12e

0.3 0.4 0.4 0.3 0.3 0.3

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12e

0.3 0.3 0.3 0.4 0.3 0.3

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12e

13.4 13.6

8.6

12.0

8.6

11.4

12.5

14.0

1.5 1.7 1.8 2.1 1.8 1.8

0.1

1.9

15.1

11.6

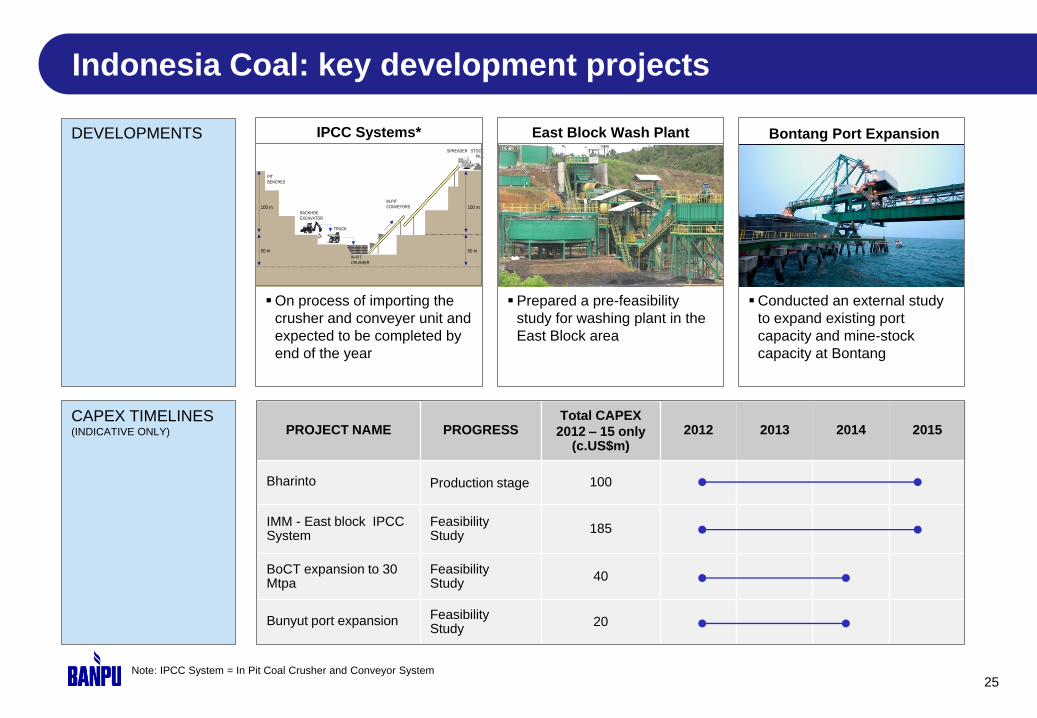

Indonesia Coal: key development projects

25

On process of importing the

crusher and conveyer unit and

expected to be completed by

end of the year

Conducted an external study

to expand existing port

capacity and mine-stock

capacity at Bontang

Prepared a pre-feasibility

study for washing plant in the

East Block area

IPCC Systems* Bontang Port Expansion East Block Wash Plant

Note: IPCC System = In Pit Coal Crusher and Conveyor System

100 m

50 m

PIT

BENCHES

BACKHOE

EXCAVATOR

TRUCK

IN-PIT

CRUSHER

IN-PIT

CONVEYORS

SPREADER STOCK

PILE

100 m

50 m

IPCC ILLUSTRATIONDEVELOPMENTS

CAPEX TIMELINES (INDICATIVE ONLY) PROJECT NAME PROGRESS

Total CAPEX

2012 – 15 only (c.US$m)

2012 2013 2014 2015

Bharinto Production stage 100

IMM - East block IPCC System

Feasibility Study 185

BoCT expansion to 30 Mtpa

Feasibility Study 40

Bunyut port expansion Feasibility Study 20

2. Coal divisions

(a) Australia Coal

(b) Indonesia Coal

(c) China Coal

(d) Mongolia Coal

2. Coal operations

26

27

CHINA COAL 2012 PRODUCTION TARGETS* OPERATIONAL UPDATES

GAOHE

● Six of eight required inspections passed at Gaohe in 1Q.

● Remaining inspections: Verification of Water and Soil

Conservation and Safety Facility Acceptance.

● Final acceptance inspection expected within Q2, then apply

for Production and Safety Licenses.

● Gaohe has finished the preliminary design of railway spur

about 8 km and worked on land acquisition.

● Gaohe began to build another 6 raw coal silos (Phase 2),

capacity of 10,000 tonnes each.

HEBI

● Hebi conducting 10 exploration drill holes in a new mining

area, to check geology and coal quality.

Gaohe

CV: 6500-8000 Kcal/kg**

Hebi

CV: 5300-6800 Kcal/kg**

Pre-production stage

2012 COAL OUTPUT (Mt ROM)

BEIJING

Hebi

(40%),

Henan

1.2 Mt

Gaohe

(45%),

Shanxi

3.8 Mt

Operation Project Operation Project

POWER

COAL

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12

0.6

1.0 0.9

0.5

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12

0.3 0.2

0.3 0.5

China Coal: operational and financial summary

Note: *Output figures are ROM output (equity basis)

**CV figures are air-dried basis

0.4 0.4 0.4 0.5

2. Coal divisions

(a) Australia Coal

(b) Indonesia Coal

(c) China Coal

(d) Mongolia Coal

2. Coal operations

28

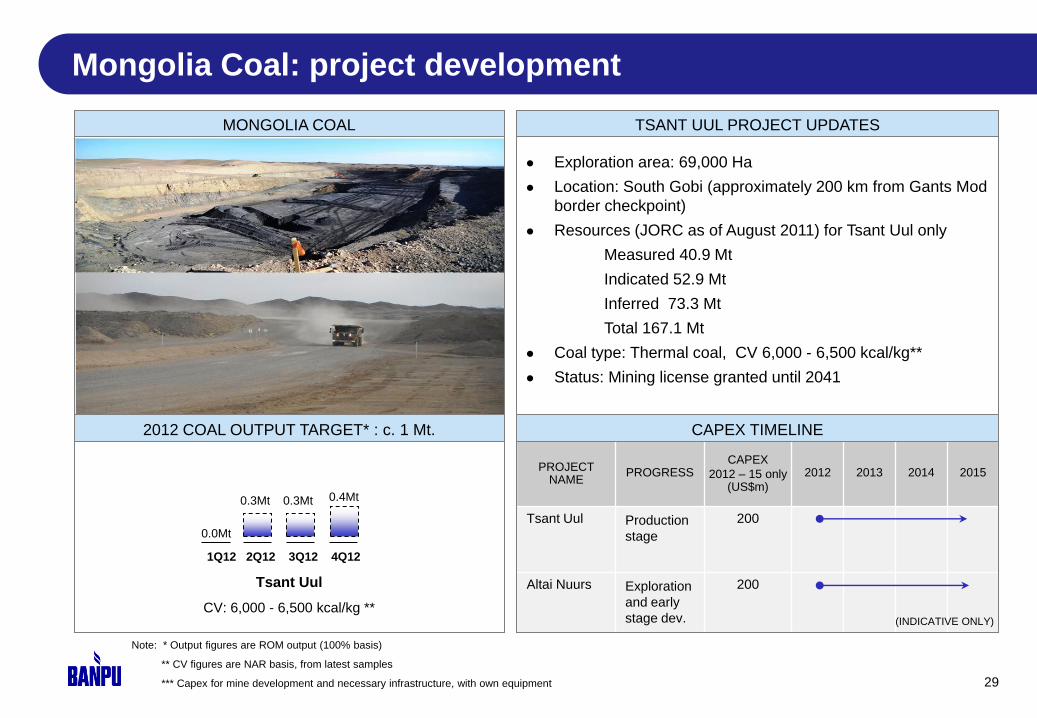

PROJECT NAME

PROGRESS CAPEX

2012 – 15 only (US$m)

2012 2013 2014 2015

Tsant Uul Production

stage

200

Altai Nuurs Exploration

and early

stage dev.

200

Mongolia Coal: project development

29

TSANT UUL PROJECT UPDATES

CAPEX TIMELINE

● Exploration area: 69,000 Ha

● Location: South Gobi (approximately 200 km from Gants Mod

border checkpoint)

● Resources (JORC as of August 2011) for Tsant Uul only

Measured 40.9 Mt

Indicated 52.9 Mt

Inferred 73.3 Mt

Total 167.1 Mt

● Coal type: Thermal coal, CV 6,000 - 6,500 kcal/kg**

● Status: Mining license granted until 2041

Tsant Uul

CV: 6,000 - 6,500 kcal/kg **

1Q12 2Q12 3Q12 4Q12

0.0Mt

0.3Mt 0.3Mt 0.4Mt

Note: * Output figures are ROM output (100% basis)

** CV figures are NAR basis, from latest samples

*** Capex for mine development and necessary infrastructure, with own equipment

2012 COAL OUTPUT TARGET* : c. 1 Mt.

MONGOLIA COAL

(INDICATIVE ONLY)

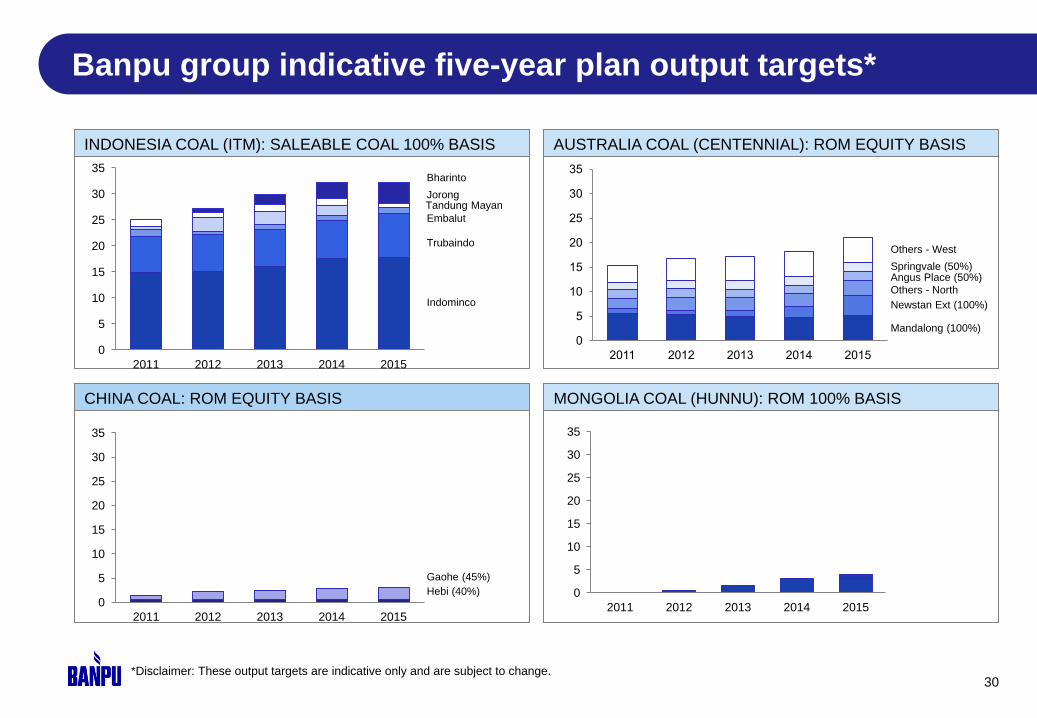

Banpu group indicative five-year plan output targets*

*Disclaimer: These output targets are indicative only and are subject to change.

INDONESIA COAL (ITM): SALEABLE COAL 100% BASIS AUSTRALIA COAL (CENTENNIAL): ROM EQUITY BASIS

0

5

10

15

20

25

30

35

2011 2012 2013 2014 2015

0

5

10

15

20

25

30

35

2011 2012 2013 2014 2015

30

0

5

10

15

20

25

30

35

2011 2012 2013 2014 2015

CHINA COAL: ROM EQUITY BASIS MONGOLIA COAL (HUNNU): ROM 100% BASIS

0

5

10

15

20

25

30

35

2011 2012 2013 2014 2015

Bharinto

Jorong

Embalut

Trubaindo

Indominco

Others - West

Springvale (50%) Angus Place (50%)

Others - North

Newstan Ext (100%)

Mandalong (100%)

Gaohe (45%)

Hebi (40%)

Tandung Mayan

2. Coal divisions

(a) Coal market

(b) Banpu coal sales

3. Coal marketing

31

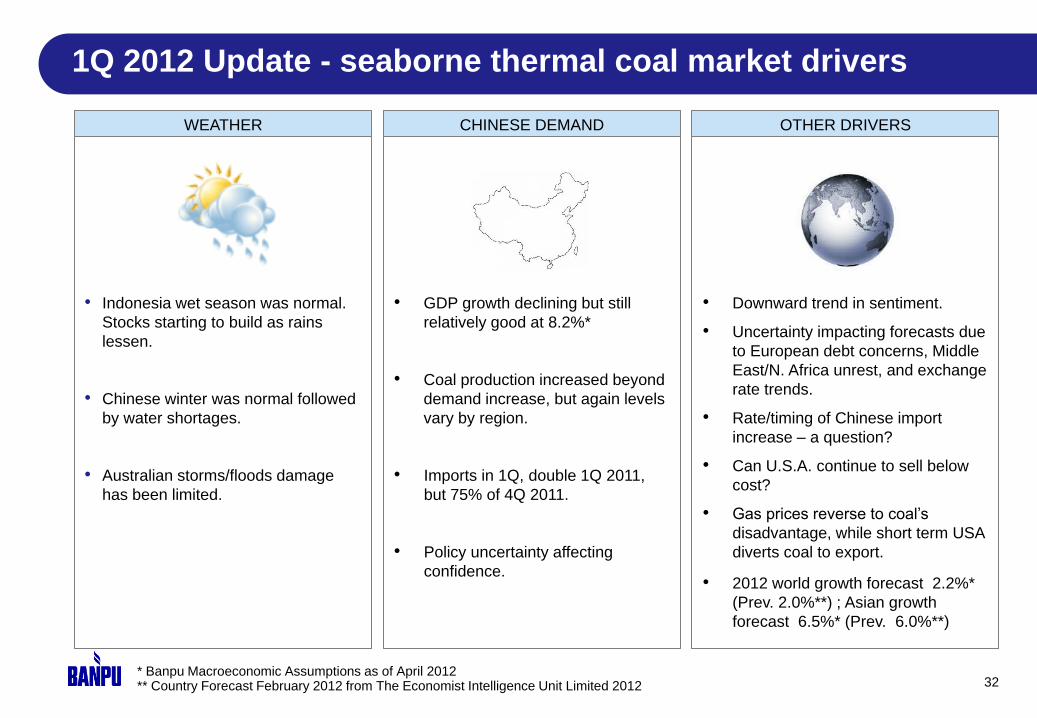

• Downward trend in sentiment.

• Uncertainty impacting forecasts due

to European debt concerns, Middle

East/N. Africa unrest, and exchange

rate trends.

• Rate/timing of Chinese import

increase – a question?

• Can U.S.A. continue to sell below

cost?

• Gas prices reverse to coal’s

disadvantage, while short term USA

diverts coal to export.

• 2012 world growth forecast 2.2%*

(Prev. 2.0%**) ; Asian growth

forecast 6.5%* (Prev. 6.0%**)

* Banpu Macroeconomic Assumptions as of April 2012 ** Country Forecast February 2012 from The Economist Intelligence Unit Limited 2012 32

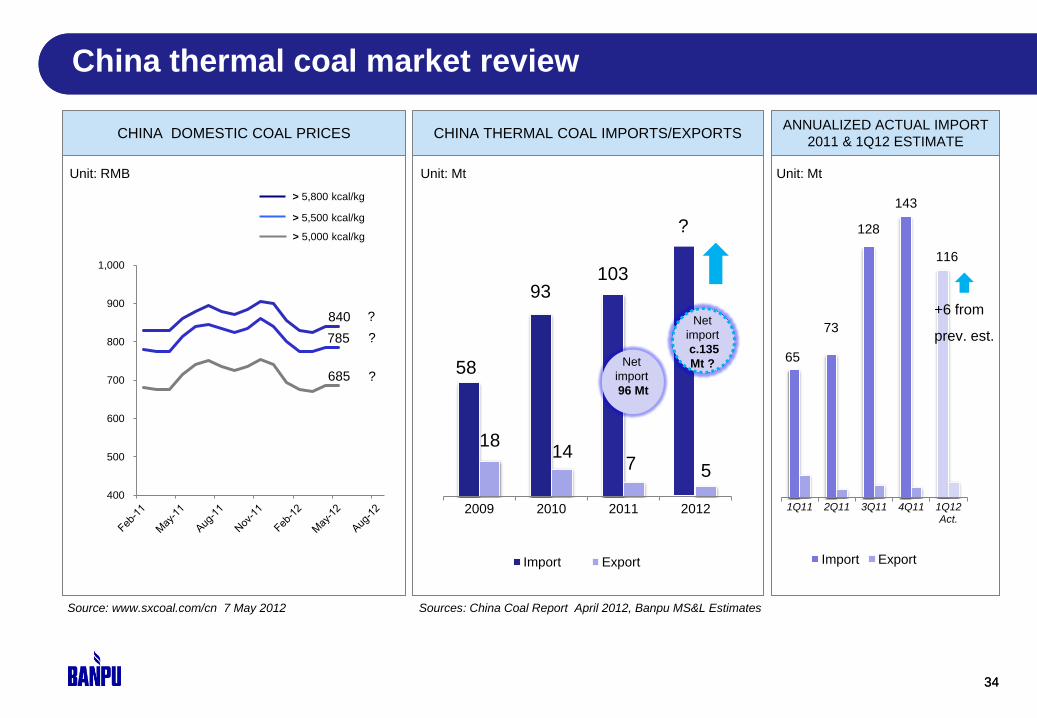

• Indonesia wet season was normal.

Stocks starting to build as rains

lessen.

• Chinese winter was normal followed

by water shortages.

• Australian storms/floods damage

has been limited.

• GDP growth declining but still

relatively good at 8.2%*

• Coal production increased beyond

demand increase, but again levels

vary by region.

• Imports in 1Q, double 1Q 2011,

but 75% of 4Q 2011.

• Policy uncertainty affecting

confidence.

WEATHER CHINESE DEMAND OTHER DRIVERS

1Q 2012 Update - seaborne thermal coal market drivers

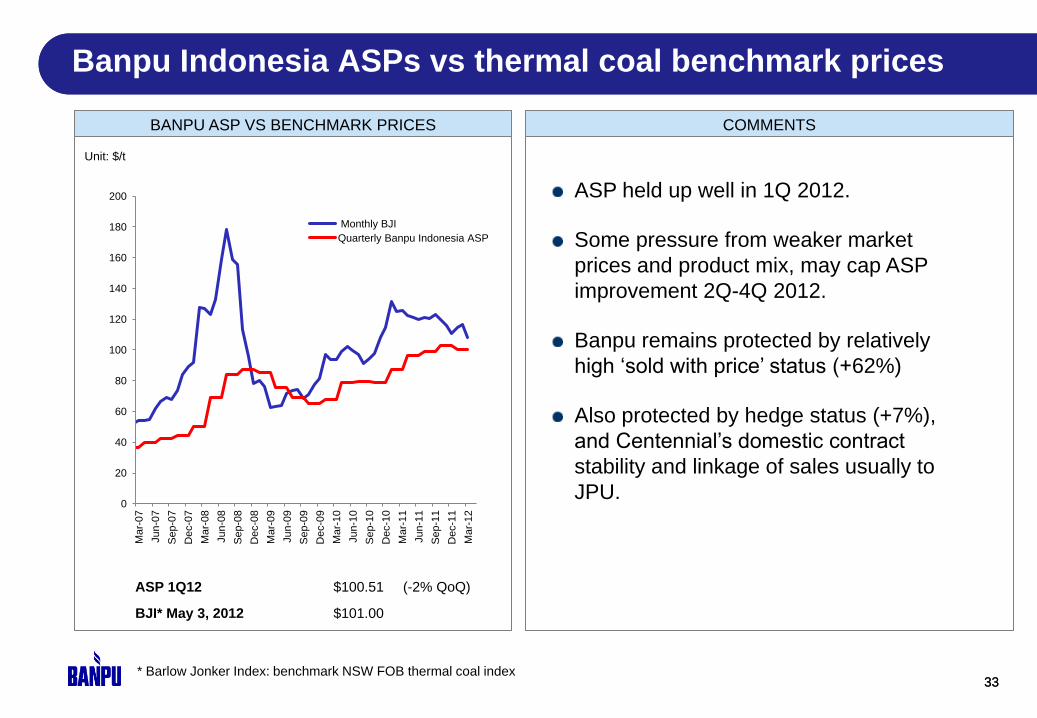

ASP 1Q12 $100.51 (-2% QoQ))

BJI* May 3, 2012 $101.00

33

Banpu average selling prices in 3Q10

ASP held up well in 1Q 2012.

Some pressure from weaker market

prices and product mix, may cap ASP

improvement 2Q-4Q 2012.

Banpu remains protected by relatively

high ‘sold with price’ status (+62%)

Also protected by hedge status (+7%),

and Centennial’s domestic contract

stability and linkage of sales usually to

JPU.

33

BANPU ASP VS BENCHMARK PRICES COMMENTS

0

20

40

60

80

100

120

140

160

180

200

Ma

r-0

7

Jun

-07

Sep

-07

Dec-0

7

Ma

r-0

8

Jun

-08

Sep

-08

Dec-0

8

Ma

r-0

9

Jun

-09

Sep

-09

Dec-0

9

Ma

r-1

0

Jun

-10

Sep

-10

Dec-1

0

Ma

r-1

1

Jun

-11

Sep

-11

Dec-1

1

Ma

r-1

2

Monthly BJI

Quarterly Banpu Indonesia ASP

Unit: $/t

Banpu Indonesia ASPs vs thermal coal benchmark prices

* Barlow Jonker Index: benchmark NSW FOB thermal coal index

400

500

600

700

800

900

1,000

785

65

73

128

143

116

1Q11 2Q11 3Q11 4Q11 1Q12 Act.

Import Export

58

93 103

18 14

7 5

2009 2010 2011 2012

Import Export

34

China thermal coal market review

Source: www.sxcoal.com/cn 7 May 2012

> 5,800 kcal/kg

> 5,500 kcal/kg

> 5,000 kcal/kg

Unit: RMB

Sources: China Coal Report April 2012, Banpu MS&L Estimates

Net

import

96 Mt

34

Net

import

c.135

Mt ?

CHINA DOMESTIC COAL PRICES CHINA THERMAL COAL IMPORTS/EXPORTS ANNUALIZED ACTUAL IMPORT

2011 & 1Q12 ESTIMATE

?

Unit: Mt Unit: Mt

840

685

China thermal coal market review

+6 from

prev. est.

?

?

?

2. Coal divisions

(a) Coal market

(b) Banpu coal sales

3. Coal marketing

35

36

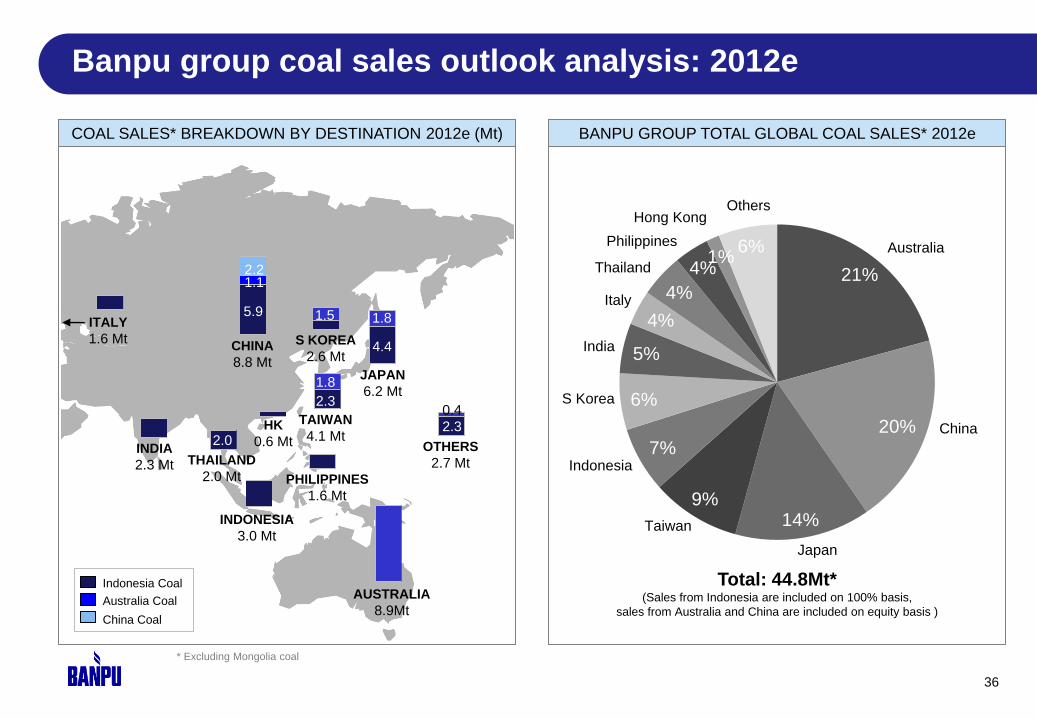

Banpu group coal sales outlook analysis: 2012e

Australia Coal

China Coal

Indonesia Coal

COAL SALES* BREAKDOWN BY DESTINATION 2012e (Mt) BANPU GROUP TOTAL GLOBAL COAL SALES* 2012e

Total: 44.8Mt* (Sales from Indonesia are included on 100% basis,

sales from Australia and China are included on equity basis )

JAPAN

6.2 Mt

PHILIPPINES

1.6 Mt

INDONESIA

3.0 Mt

THAILAND

2.0 Mt

INDIA

2.3 Mt

OTHERS

2.7 Mt

HK

0.6 Mt

S KOREA

2.6 Mt CHINA

8.8 Mt

TAIWAN

4.1 Mt

AUSTRALIA

8.9Mt

ITALY

1.6 Mt

2.2

1.8

4.4

1.8

5.9

2.0

1.5

1.1

2.3

0.4 2.3

21%

20%

14% 9%

7%

6%

5%

4%

4%

4% 1%

6% Australia

Japan

China

Taiwan

S Korea

Italy

Thailand

Philippines

Hong Kong

India

Indonesia

Others

* Excluding Mongolia coal

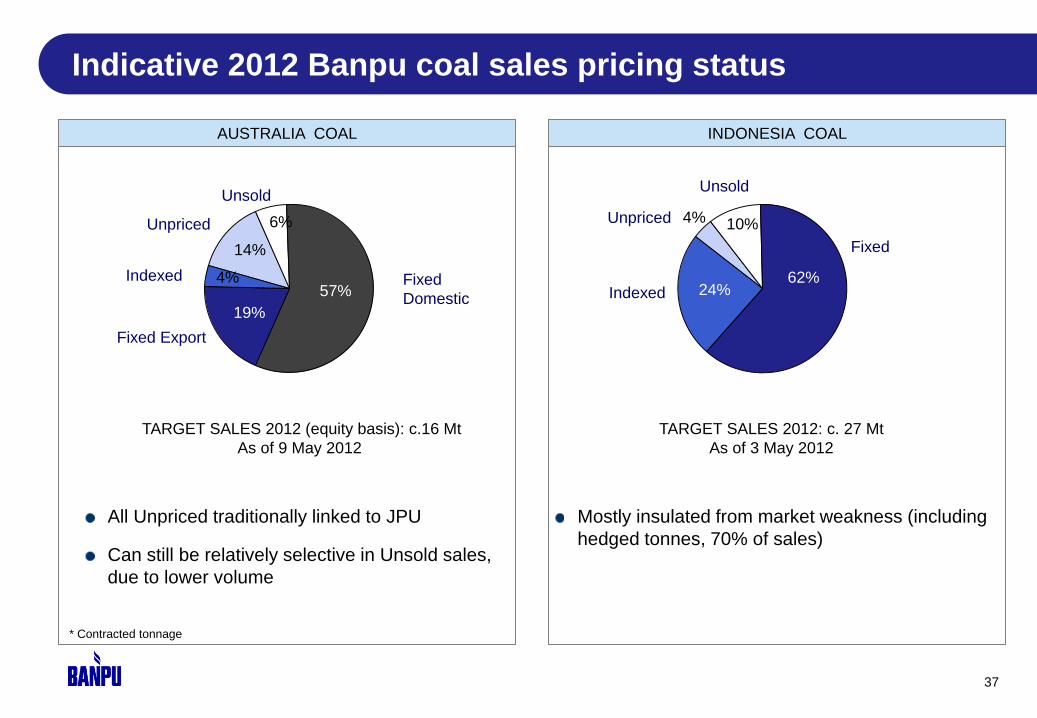

Indicative 2012 Banpu coal sales pricing status

37

TARGET SALES 2012 (equity basis): c.16 Mt

As of 9 May 2012

* Contracted tonnage

All Unpriced traditionally linked to JPU

Can still be relatively selective in Unsold sales,

due to lower volume

TARGET SALES 2012: c. 27 Mt

As of 3 May 2012

Mostly insulated from market weakness (including

hedged tonnes, 70% of sales)

Fixed

Indexed

Unpriced

Unsold

4% 10%

62% 24%

14%

6%

57%

19%

4% Indexed Fixed

Domestic

Unpriced

Unsold

Fixed Export

AUSTRALIA COAL INDONESIA COAL

4. Power business

38

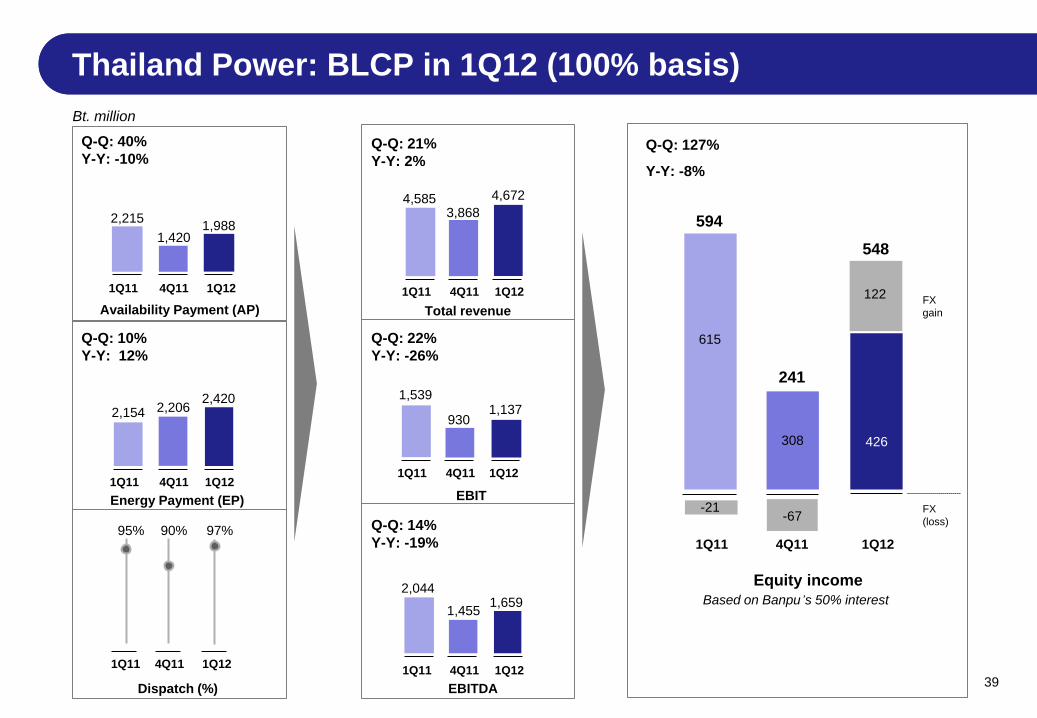

Bt. million

Q-Q: 40%

Y-Y: -10%

Q-Q: 10%

Y-Y: 12%

95% 90% 97%

2,215

1Q11 4Q11 1Q12

1Q11 4Q11 1Q12

Energy Payment (EP)

1Q11 4Q11 1Q12

Dispatch (%)

1,420 1,988

2,154 2,206 2,420

Availability Payment (AP)

Q-Q: 21%

Y-Y: 2%

Q-Q: 22%

Y-Y: -26%

Q-Q: 14%

Y-Y: -19%

1Q11 4Q11 1Q12

Total revenue

1Q11 4Q11 1Q12

EBIT

1Q11 4Q11 1Q12

EBITDA

4,585 3,868

4,672

1,539

930 1,137

2,044

1,455 1,659

39

Based on Banpu’s 50% interest

Q-Q: 127%

Y-Y: -8%

1Q11 4Q11 1Q12

Equity income

594

548

241

426 308

615

-67 FX

(loss)

-21

122 FX

gain

Thailand Power: BLCP in 1Q12 (100% basis)

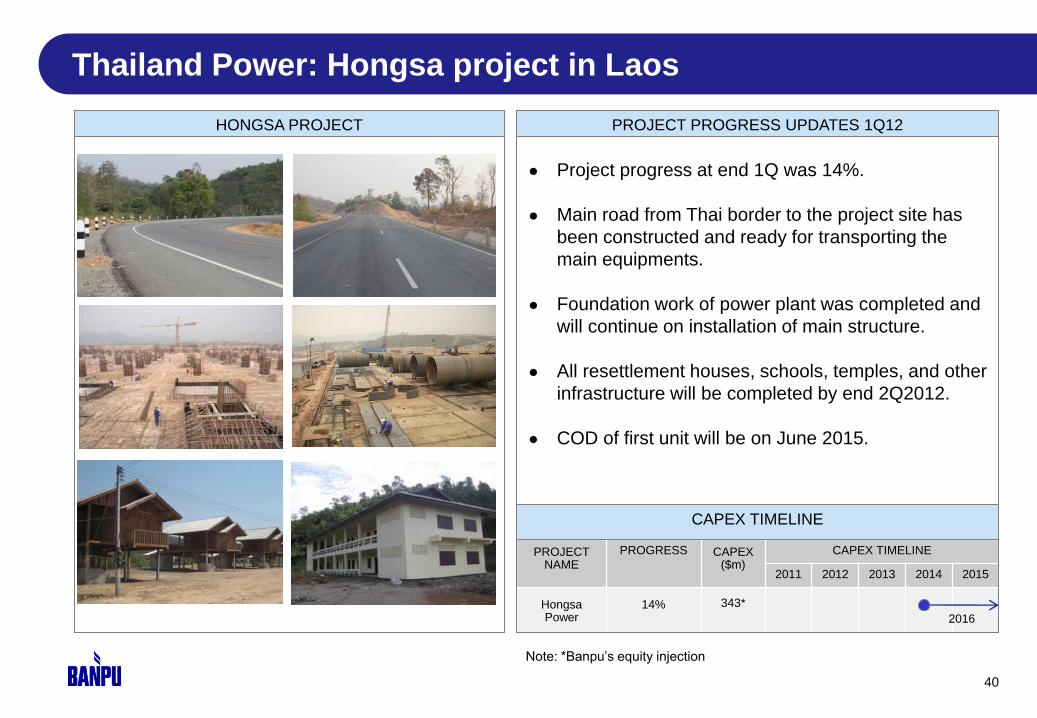

Thailand Power: Hongsa project in Laos

40

HONGSA PROJECT PROJECT PROGRESS UPDATES 1Q12

PROJECT NAME

PROGRESS CAPEX ($m)

CAPEX TIMELINE

2011 2012 2013 2014 2015

Hongsa Power

14% 343*

CAPEX TIMELINE

● Project progress at end 1Q was 14%.

● Main road from Thai border to the project site has

been constructed and ready for transporting the

main equipments.

● Foundation work of power plant was completed and

will continue on installation of main structure.

● All resettlement houses, schools, temples, and other

infrastructure will be completed by end 2Q2012.

● COD of first unit will be on June 2015.

Note: *Banpu’s equity injection

2016

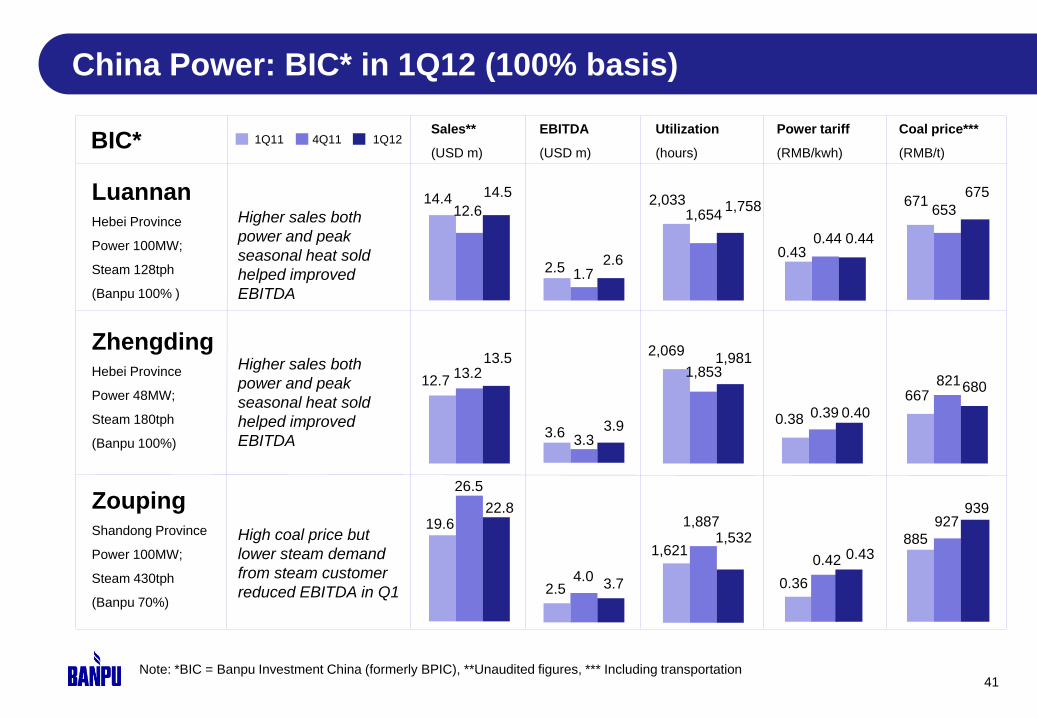

Note: *BIC = Banpu Investment China (formerly BPIC), **Unaudited figures, *** Including transportation

Luannan Hebei Province

Power 100MW;

Steam 128tph

(Banpu 100% )

China Power: BIC* in 1Q12 (100% basis)

41

Higher sales both

power and peak

seasonal heat sold

helped improved

EBITDA

Zhengding Hebei Province

Power 48MW;

Steam 180tph

(Banpu 100%)

Higher sales both

power and peak

seasonal heat sold

helped improved

EBITDA

Zouping Shandong Province

Power 100MW;

Steam 430tph

(Banpu 70%)

High coal price but

lower steam demand

from steam customer

reduced EBITDA in Q1

Sales**

(USD m)

EBITDA

(USD m)

Utilization

(hours)

Power tariff

(RMB/kwh)

Coal price***

(RMB/t)

2,069

1,853 1,981

0.38 0.39 0.40

12.7 13.2

13.5

3.6 3.3

3.9

667 821 680

19.6

26.5

22.8

2.5 4.0

3.7

1,621

1,887 1,532

0.36

885

927

939

0.43 0.44 0.44

671 653

675 2,033

1,654 1,758

14.4 12.6

14.5

2.5 1.7 2.6

0.42 0.43

BIC* 1Q11 4Q11 1Q12

5. Financial summary

42

Key external and corporate events

43

EX

TE

RN

AL

E

VE

NT

S

CO

RP

OR

AT

E E

VE

NT

S

Thai flood

crisis

Greece

referendum

Italy debt crisis?

Mahakam

Bridge

collapse

10 Nov

Banpu 3Q11

results

27 Oct

US$225M

private

placement

Downgrade 9

euro zone

nations

Ban

Iranian oil?

Completion of

Hunnu

acquisition

Announcement

of special Bt 3

dividend to be

paid on 10 Feb

BoT cuts

interest rate

to 3%

Greece passes

austerity plan

28 Dec

18 Jan

• Banpu 2011 results

• 2H11 Bt 9 dividend

to be paid on 30 Apr

• R&R upgrades

24 Feb

Indonesia

foreign

ownership

limit Aust Senate

passes MRRT

Banpu AGM 2012

Approved Annual Dividend 21

Baht/share (incl. special dividend 3

Baht/share)

Approved Bond issue

20,000 Mil Baht

11 May

Banpu 1Q12

results

4Q11

5 Apr

China’s

disappointing

Q1 GDP growth

Indonesia export

tax on minerals

May 12

European

elections sent

shockwave

Apr 12

Request for

contract review

DIR

EC

T

IND

IRE

CT

1Q12

Banpu group revenue analysis: coal operations

44

Indonesia Coal (ITM) Australia Coal (Centennial)

Note: ITM revenue is consolidated in Banpu income

statement.

Note: Centennial’s revenue is consolidated in Banpu

income statement.

SALES (Mt)

AVERAGE SELLING PRICE (US$/t)

REVENUE ($M)

SALES (Mt)

AVERAGE SELLING PRICE (A$/t)**

REVENUE (A$M)

468 502

678 733 578

1Q11 2Q11 3Q11 4Q11 1Q12

279 266 287 261 273

1Q11 2Q11 3Q11 4Q11 1Q12

NE

X*

AS

P

2.1 2.3 2.7 2.1 2.1

3.7 3.7 4.1 3.4 3.5

1Q11 2Q11 3Q11 4Q11 1Q12

Note: ‘$’ in this presentation denotes US dollar only, otherwise stated

*NEX = Newcastle Export Index (formerly Barlow Jonker Index or BJI)

It is relevant but not linked to China Coal’s ASP

**Australian GAAP

China Coal

Note: Hebi and Gaohe revenues are not consolidated in

Banpu income statement.

SALES (Mt)

AVERAGE SELLING PRICE (US$/t) excl. VAT

REVENUE ($M)

72 77 92 81 123

1Q11 2Q11 3Q11 4Q11 1Q12

0.3 0.4 0.4 0.4 0.5

1Q11 2Q11 3Q11 4Q11 1Q12

Domestic

Export

5.3 4.7 6.1 6.5

5.2

5.5 5.2

6.9 7.1 5.8

1Q11 2Q11 3Q11 4Q11 1Q12

125 118

122

110 110

87 97 98 103 101

1Q11 2Q11 3Q11 4Q11 1Q12

AS

P

75 73 70 77 78

1Q11 2Q11 3Q11 4Q11 1Q12

NE

X* 125

118 122

110 110

AS

P

90 91 96 92 107

1Q11 2Q11 3Q11 4Q11 1Q12

NE

X* 125

118 122

110 110

Equity basis Equity basis 100% basis

100% basis Equity basis 100% basis

Domestic

Export

Domestic

Export

45

Banpu consolidated sales revenues

14,606

23,306

18,385

8,145

7,858

8,352 1,427

1,489

1,573

1Q11 4Q11 1Q12

Bt. million

+17% Y –Y

Coal Indonesia

Power

+6% Q – Q

+10% Y - Y

-21% Q – Q

+26% Y - Y

Bt 24,178 M

Bt 32,653 M

Bt 28,310 M

USD

1,046 m USD

913 m

USD

791 m

Power

Coal Australia

Coal Indonesia

Note: USD exchange rate is the average exchange rate of the corresponding period, Revenue from other is included in Coal.

Coal Australia

+6% Q- Q

+3% Y - Y

*

* Under Thai GAAP, this is not included in the revenue.

Australian GAAP (AUD Million)

261 273

4Q11 1Q12

10 * Gain

from

forward

18

251 255

-13% Q – Q

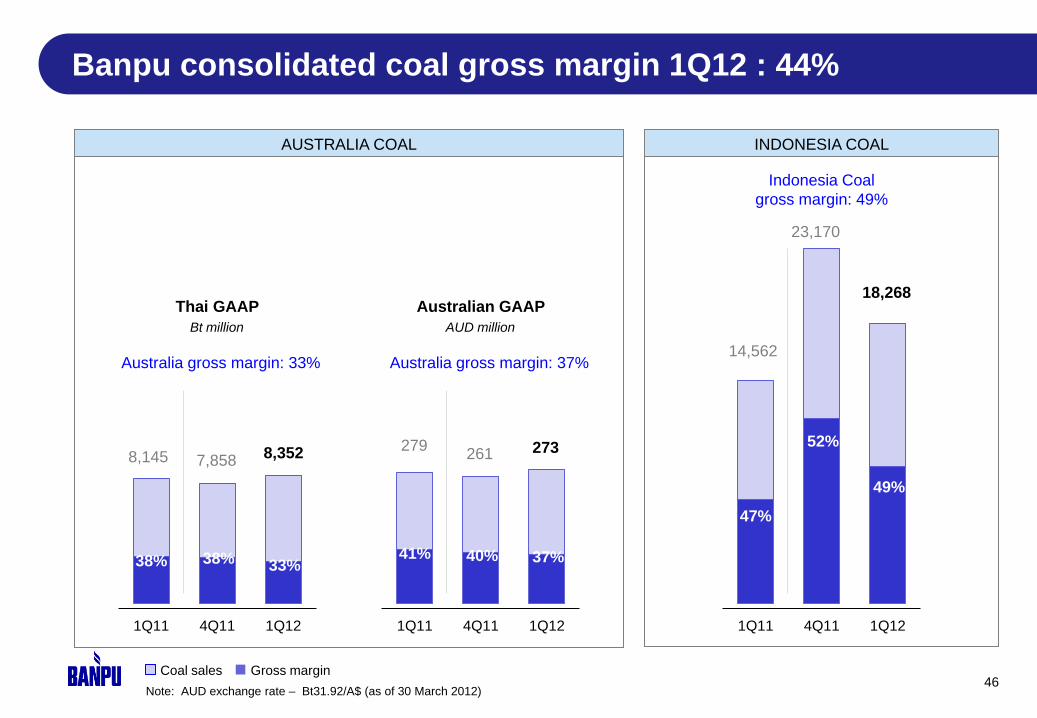

Banpu consolidated coal gross margin 1Q12 : 44%

46

Australia gross margin: 37%

Bt million

Australia gross margin: 33%

Thai GAAP

AUSTRALIA COAL

Australian GAAP

AUD million

1Q11 4Q11 1Q12

33% 38% 38%

8,145

8,352

7,858

1Q11 4Q11 1Q12

37% 40% 41%

279

273

261

Note: AUD exchange rate – Bt31.92/A$ (as of 30 March 2012)

INDONESIA COAL

Indonesia Coal

gross margin: 49%

1Q11 4Q11 1Q12

49%

52%

47%

18,268

23,170

14,562

Coal sales Gross margin

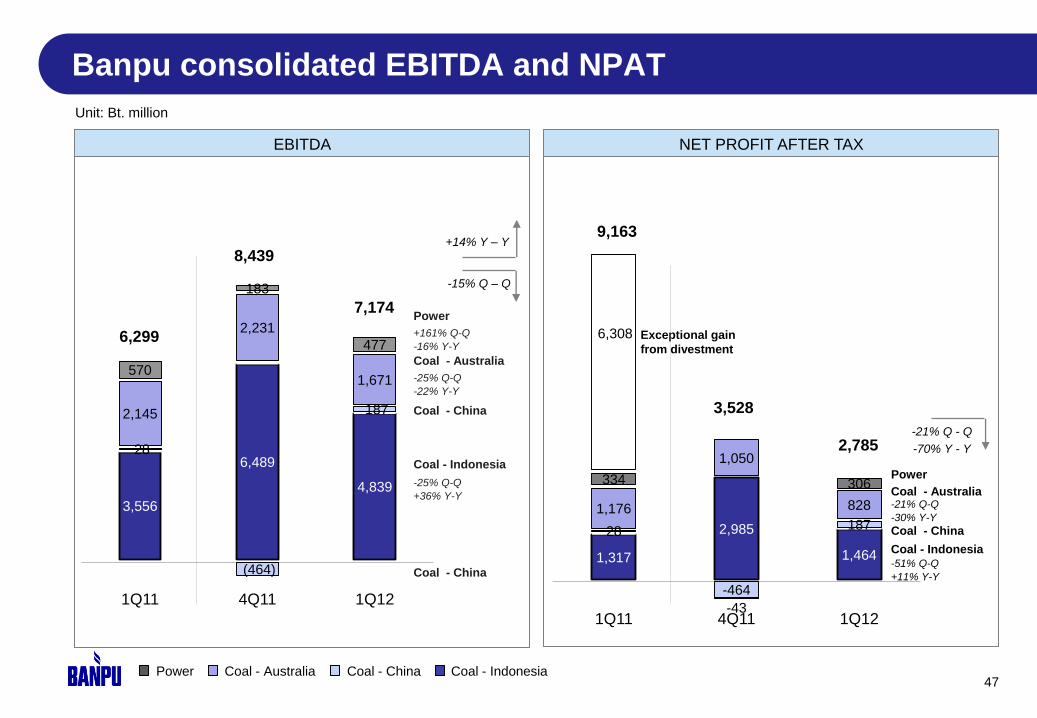

Banpu consolidated EBITDA and NPAT

47

Unit: Bt. million

1,317

2,985

1,464

28

-464

187 1,176

1,050

828

334

-43

306

6,308

1Q11 4Q11 1Q12

3,528

9,163

2,785

Coal - Indonesia

Exceptional gain

from divestment

-51% Q-Q

+11% Y-Y

Coal - Australia -21% Q-Q

-30% Y-Y 3,556

6,489

4,839

28

(464)

187 2,145

2,231

1,671 570

183

477

1Q11 4Q11 1Q12

6,299

8,439

7,174

Coal - Indonesia

Power

+161% Q-Q

-16% Y-Y

-25% Q-Q

+36% Y-Y

Coal - Australia

-25% Q-Q

-22% Y-Y

-15% Q – Q

Coal - China

Coal - China

-21% Q - Q

-70% Y - Y

Power

Power Coal - Australia Coal - China Coal - Indonesia

EBITDA NET PROFIT AFTER TAX

+14% Y – Y

Coal - China

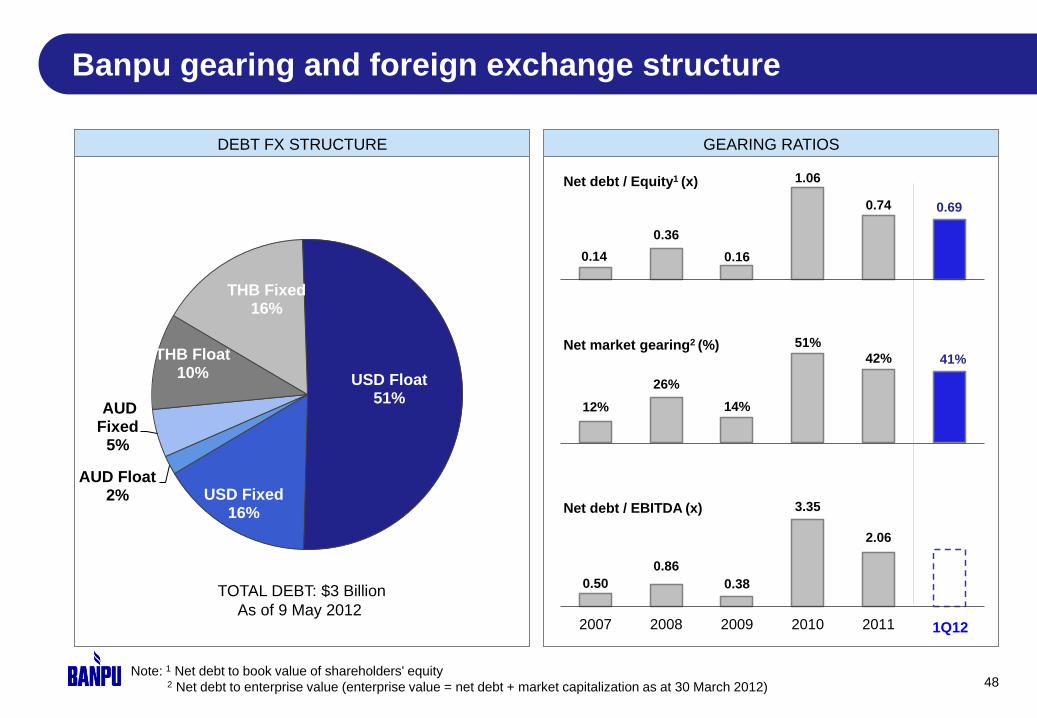

Banpu gearing and foreign exchange structure

48

DEBT FX STRUCTURE

USD Float 51%

USD Fixed 16%

AUD Float 2%

AUD Fixed

5%

THB Float 10%

THB Fixed 16%

GEARING RATIOS

0.14

0.36

0.16

1.06

0.74 0.69

2007 2008 2009 2010 2011 1Q12

Net debt / Equity1 (x)

Note: 1 Net debt to book value of shareholders' equity

2 Net debt to enterprise value (enterprise value = net debt + market capitalization as at 30 March 2012)

12%

26%

14%

51%

42% 41%

2007 2008 2009 2010 2011 1Q12

Net market gearing2 (%)

0.50

0.86

0.38

3.35

2.06

2007 2008 2009 2010 2011 1Q12

Net debt / EBITDA (x)

TOTAL DEBT: $3 Billion

As of 9 May 2012 1Q12

Appendices

49

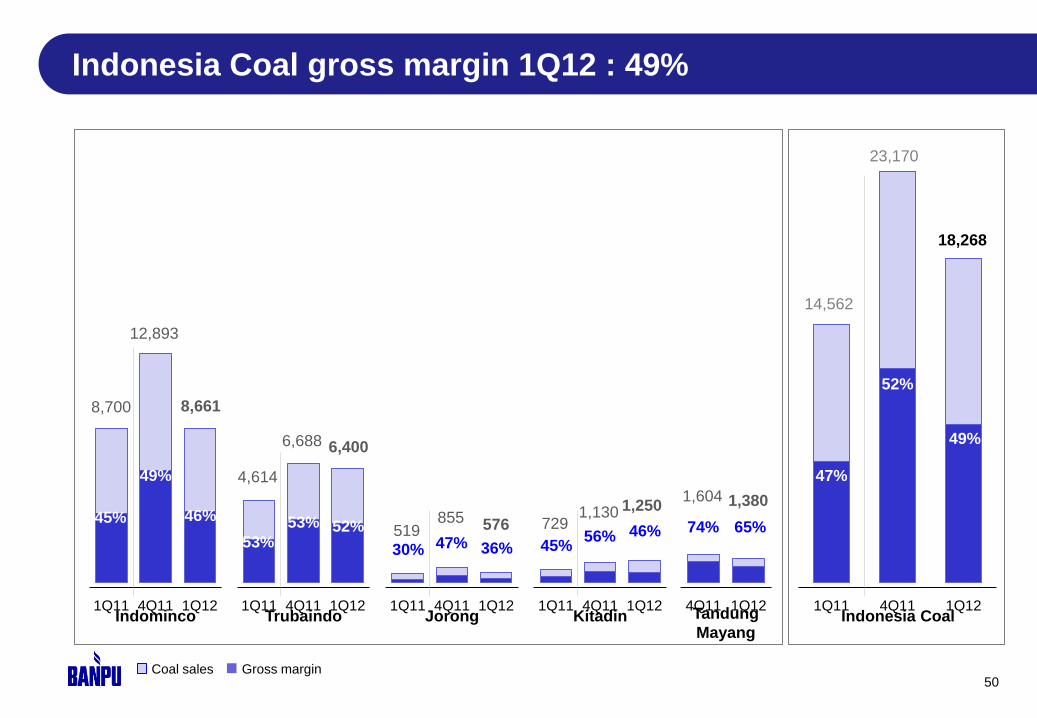

Indonesia Coal gross margin 1Q12 : 49%

50 Coal sales Gross margin

1Q11 4Q11 1Q12

49%

52%

47%

18,268

23,170

14,562

1Q11 4Q11 1Q12 Indonesia Coal Indominco

49%

45% 46%

8,700 8,661

12,893

1Q11 4Q11 1Q12

53%

53% 52%

4,614

6,400 6,688

Trubaindo 1Q11 4Q11 1Q12

53%

53% 52% 519

855

Jorong

576

30% 47% 36%

1Q11 4Q11 1Q12

53%

53% 52% 729

1,130 1,250

45% 56% 46%

Kitadin 4Q11 1Q12 Tandung

Mayang

1,604 1,380

74% 65%

51

50%

40%

Power & New energy

40%

45%

70%

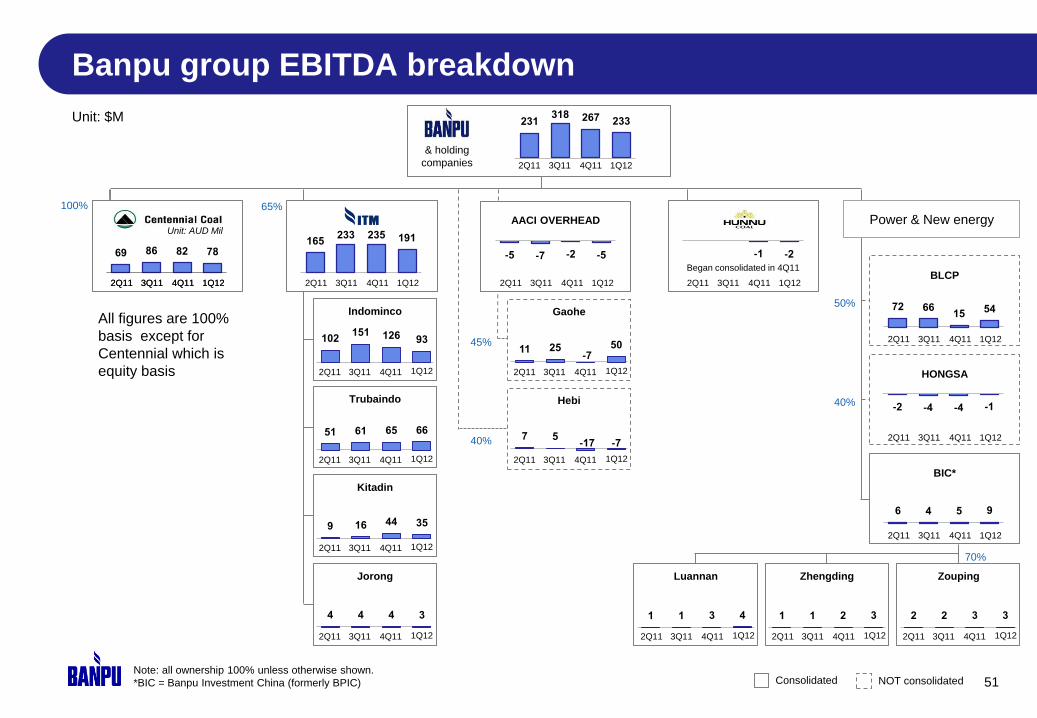

Note: all ownership 100% unless otherwise shown.

*BIC = Banpu Investment China (formerly BPIC)

Gaohe

Hebi

BLCP

HONGSA

BIC*

Zouping

2 2 3 3

Zhengding

1 1 2 3

Luannan

1 1 3 4

& holding

companies

65%

Indominco

Trubaindo

4Q11 Kitadin

Jorong

AACI OVERHEAD

-5 -7 -2 -5

Unit: $M

100%

69 86 82 78

Consolidated NOT consolidated

Banpu group EBITDA breakdown

2Q11 3Q11 4Q11 1Q12 2Q11 3Q11 4Q11 1Q12 2Q11 3Q11 4Q11 1Q12 2Q11 3Q11 4Q11 1Q12

2Q11 3Q11 4Q11 1Q12

2Q11 3Q11 4Q11 1Q12

2Q11 3Q11 4Q11 1Q12

2Q11 3Q11 4Q11 1Q12

2Q11 3Q11 4Q11 1Q12

2Q11 3Q11 4Q11 1Q12

2Q11 3Q11 4Q11 1Q12

2Q11 3Q11 4Q11 1Q12

2Q11 3Q11 4Q11 1Q12

2Q11 3Q11 4Q11 1Q12 2Q11 3Q11 4Q11 1Q12 2Q11 3Q11 4Q11 1Q12

2Q11 3Q11 4Q11 1Q12

165 233 235 191

102 151 126 93

51 61 65 66

9 16 44 35

4 4 4 3

11 25 -7

50

7 5 -17 -7

-1 -2

Began consolidated in 4Q11

72 66 15 54

-2 -4 -4 -1

6 4 5 9

Unit: AUD Mil

2Q11 3Q11 4Q11 1Q12

All figures are 100%

basis except for

Centennial which is

equity basis

231 318 267 233

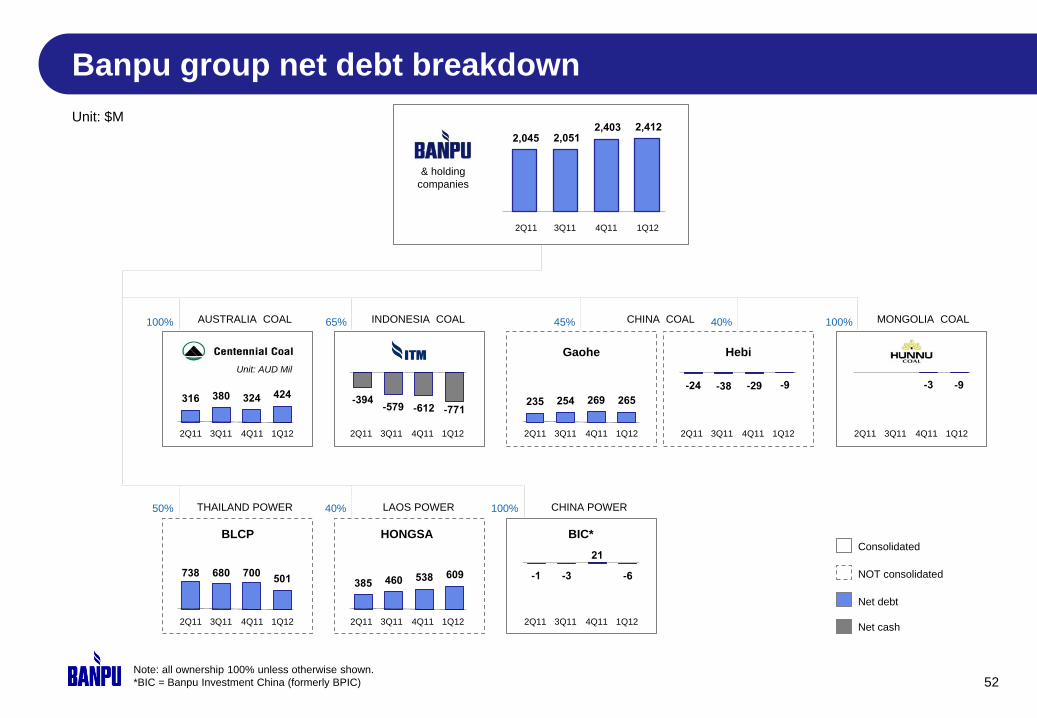

Banpu group net debt breakdown

52 Note: all ownership 100% unless otherwise shown.

*BIC = Banpu Investment China (formerly BPIC)

& holding

companies

2,045 2,051 2,403 2,412

2Q11 3Q11 4Q11 1Q12

2Q11 3Q11 4Q11 1Q12

AUSTRALIA COAL INDONESIA COAL CHINA COAL MONGOLIA COAL

THAILAND POWER LAOS POWER CHINA POWER

Gaohe Hebi

HONGSA BLCP BIC* Consolidated

NOT consolidated

100% 65% 45% 40% 100%

50% 40% 100%

Net debt

Net cash

2Q11 3Q11 4Q11 1Q12 2Q11 3Q11 4Q11 1Q12 2Q11 3Q11 4Q11 1Q12 2Q11 3Q11 4Q11 1Q12

2Q11 3Q11 4Q11 1Q12 2Q11 3Q11 4Q11 1Q12 2Q11 3Q11 4Q11 1Q12

316 380 324 424 -394

-579 -612 -771 235 254 269 265

-24 -38 -29 -9 -3 -9

738 680 700 501 385 460 538 609 -1 -3

21

-6

Unit: AUD Mil

Unit: $M

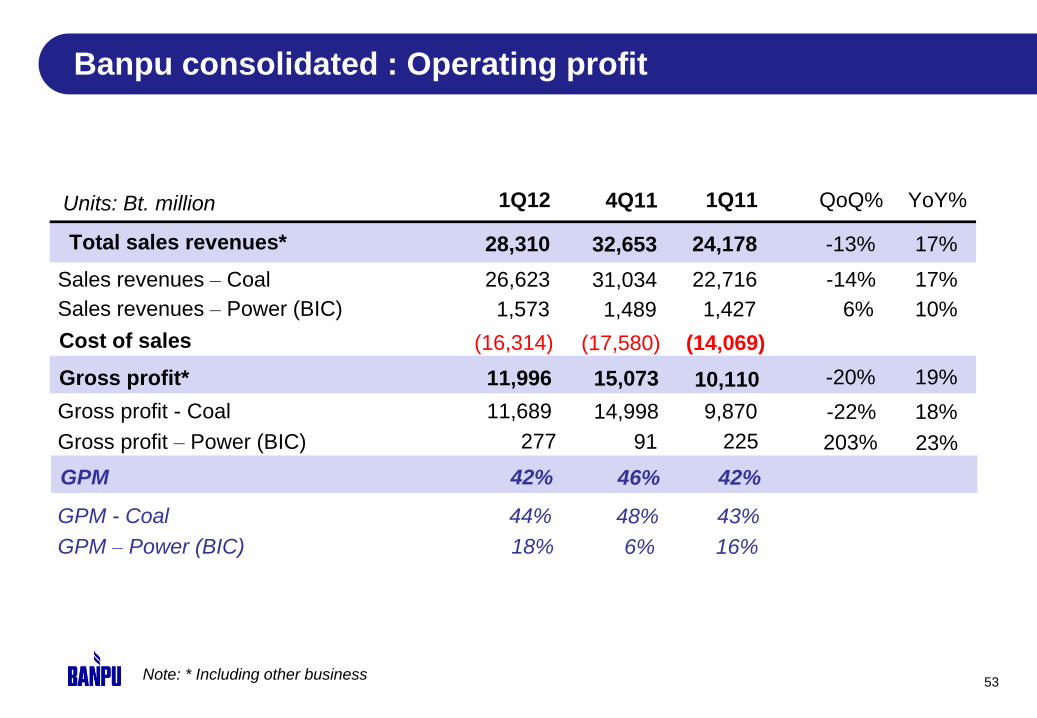

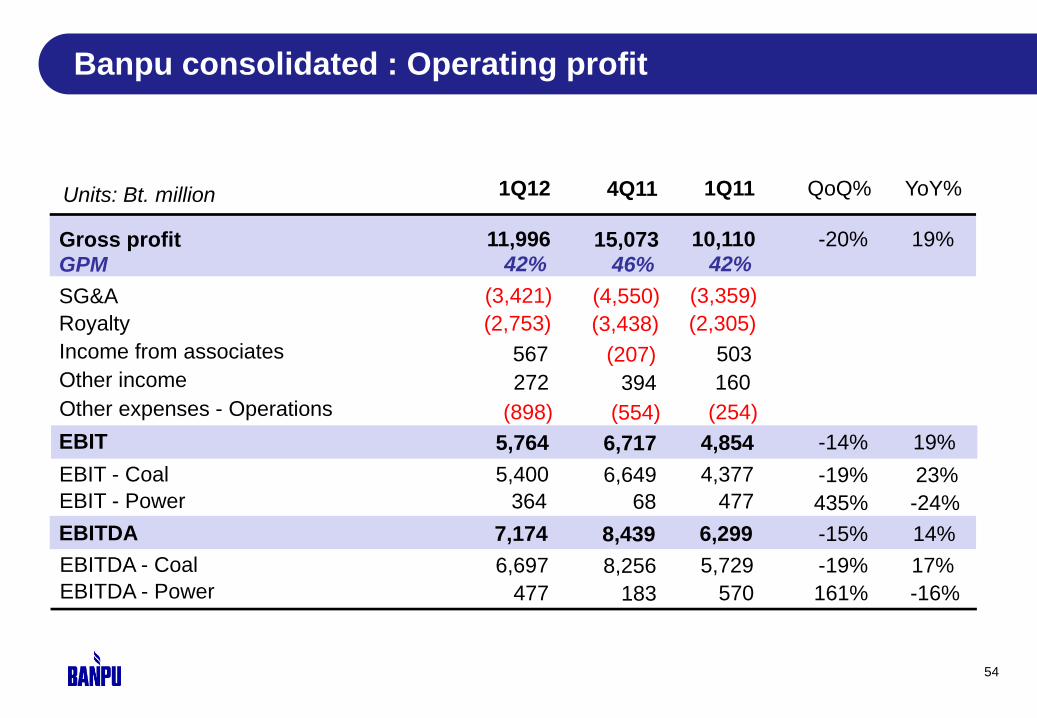

Banpu consolidated : Operating profit

Units: Bt. million

Sales revenues – Power (BIC) 1,573

Cost of sales (16,314)

Gross profit* 11,996 -20% 19%

GPM 42%

1Q12 QoQ% YoY%

28,310 -13% 17%

Note: * Including other business

Sales revenues – Coal

Total sales revenues*

26,623 -14% 17%

Gross profit - Coal 11,689 -22% 18%

Gross profit – Power (BIC) 277

GPM – Power (BIC) 18%

GPM - Coal 44%

6% 10%

203% 23%

53

1,489

(17,580)

15,073

46%

4Q11

32,653

31,034

14,998

91

6%

48%

1,427

(14,069)

10,110

42%

1Q11

24,178

22,716

9,870

225

16%

43%

Units: Bt. million

Gross profit 11,996 -20% 19%

GPM 42%

SG&A (3,421)

Royalty (2,753)

Other income 272

EBIT 5,764 -14% 19%

EBITDA 7,174 -15% 14%

1Q12 QoQ% YoY%

EBIT - Coal 5,400 -19% 23%

EBIT - Power 364

Income from associates 567

435% -24%

EBITDA - Coal 6,697 -19% 17%

EBITDA - Power 477 161% -16%

Other expenses - Operations (898)

Banpu consolidated : Operating profit

54

15,073

46%

(4,550)

(3,438)

394

6,717

8,439

4Q11

6,649

68

(207)

8,256

183

(554)

10,110

42%

(3,359)

(2,305)

160

4,854

6,299

1Q11

4,377

477

503

5,729

570

(254)

Banpu consolidated : Net profit

Units: Bt. million

EBIT

Interest expenses (824)

Financial expenses (88)

Income tax (core business) (1,724)

Minorities (1,193)

Net profit before extra items 1,934

Non-recurring items* 282

Net profit before FX 2,216 -73%

FX translations 569

Net profit 2,785 -70%

EPS (Bt/share) 10.25

Note: * Income from non-core assets and other non-operating expenses

YoY% 1Q12

-5%

-13%

-21%

QoQ%

-12%

5,764 -14% 19%

55

(817)

(117)

(1,897)

(1,691)

2,194

347

2,540

988

3,528

12.98

4Q11

6,717

(698)

(71)

(1,247)

(810)

2,027

8,058

8,144

1,019

9,163

33.72

1Q11

4,854

(1,941) Income tax (non- core business)

Centennial : Income Statement

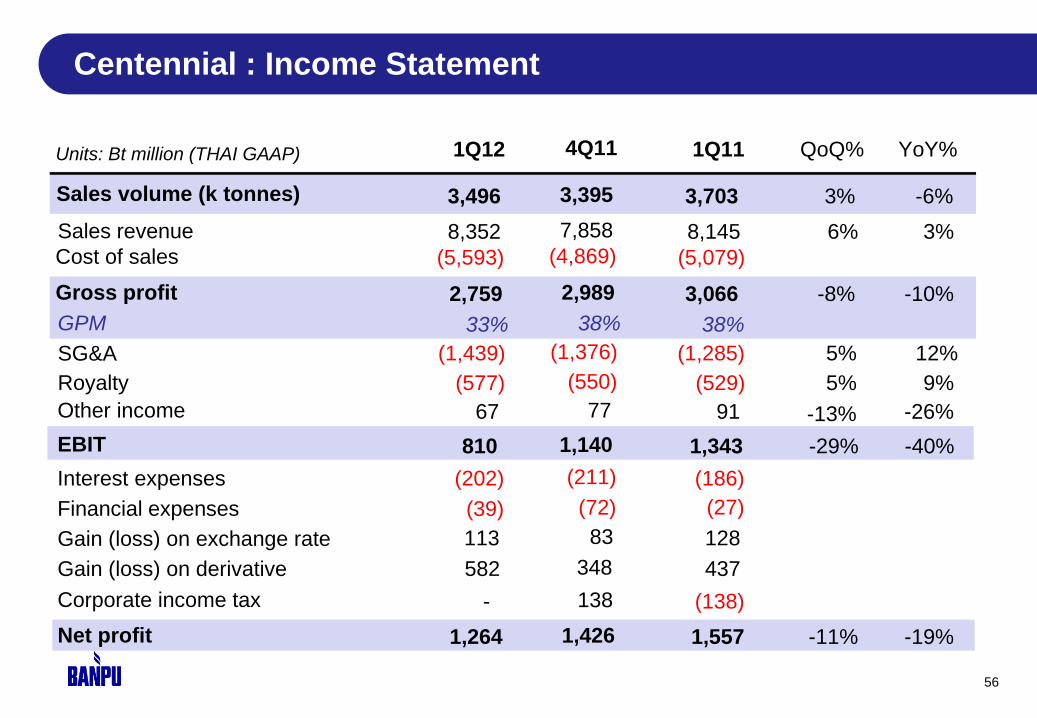

Units: Bt million (THAI GAAP) 1Q12 QoQ% 1Q11

56

Cost of sales (5,593)

Gross profit 2,759 -8%

(5,079)

3,066

GPM 33% 38%

Royalty (577)

SG&A (1,439) 5%

5% (529)

(1,285)

810 -29% EBIT 1,343

3,496 3%

Sales revenue

Sales volume (k tonnes)

8,352 6%

3,703

8,145

Other income 67 -13% 91

Interest expenses (202)

Financial expenses (39)

Gain (loss) on exchange rate 113

Corporate income tax -

Net profit 1,264 -11%

(186)

(27)

128

(138)

1,557

Gain (loss) on derivative 582 437

YoY%

-10%

12%

9%

-40%

-6%

3%

-26%

-19%

4Q11

(4,869)

2,989

38%

(550)

(1,376)

1,140

3,395

7,858

77

(211)

(72)

83

138

1,426

348

57

Banpu group coal sales 1Q12

COAL SALES BREAKDOWN BY DESTINATION 1Q12 (Mt) BANPU GROUP TOTAL GLOBAL COAL SALES 1Q12

Total: 9.8Mt (Sales from Indonesia are included on 100% basis,

sales from Australia and China are included on equity basis ) Australia Coal

China Coal

Indonesia Coal

21%

24%

14%

9%

7%

6%

6%

4% 3%

2% 2% 2%

Australia

Japan

China

Taiwan

S Korea

Italy

Thailand

Philippines

Hong Kong

India

Indonesia

Others

JAPAN

1.4 Mt

PHILIPPINES

0.4 Mt

THAILAND

0.6 Mt

INDIA

0.1 Mt

OTHERS

0.2 Mt

HK

0.2 Mt

S KOREA

0.7 Mt

CHINA

2.3 Mt

TAIWAN

0.9 Mt

AUSTRALIA

2.1 Mt

ITALY

0.3 Mt

0.5

0.9

1.8

INDONESIA

0.6 Mt

0.4 0.3

0.5

58

Quarterly equity ROM output

Normal production Bolt-up/commissioning LW relocation

Note: Bar width is indicative of the equity production contributions to Centennial

1.5 2.0 2.3

1.8 1.8 2.0 2.3 2.1

2.4 1.2

2.5

2.3 2.2 2.5 2.1

2.0

3.9

3.2

4.8

4.1 4.0

4.5 4.4 4.1

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13

Total equity ROM (Mt)

ACTUAL PLANNED (INDICATIVE ONLY)

WE

ST

ER

N

NO

RT

HE

RN