investor presentation - burgan bank13_final.pdf · 2013-08-26 · q2'12 q3'12 q4'12...

TRANSCRIPT

1

INVESTOR

PRESENTATION 2nd Quarter 2013 |

Financial Performance

2

Agenda

Economic Overview

Results Overview

Performance Trends: 2nd Quarter 2013

Key Developments

Appendix: Financial & Other Achievements

3

Economic Overview

4

2

3

4

5

6

7

8

9

1986 1989 1992 1995 1998 2001 2004 2007 2010 2013 2016

Actual growth Trend growth-4

-3

-2

-1

0

1

2

3

4

5

1986 1989 1992 1995 1998 2001 2004 2007 2010 2013 2016

Actual growth Trend growth

No major changes… with low growth ahead,

debt and unemployment remaining high….

Global Macro: As expected, weak fundamentals with stabilization sustained by policy hence

the risk of excessive liquidity creating new bubbles but not helping growth…

Source: IMF 2013 Data base & Burgan Bank Economic Research.

Dotcom

bubble Gulf War

Financial

Crisis

Advanced - Real GDP growth (%) Developing - Real GDP growth (%)

Asian Fin.

Crisis

Dotcom bubble,

China WTO

accession

Lo

we

r g

row

th p

rosp

ec

ts..

Up

wa

rd g

row

th t

ren

d b

roke

n..

Gulf War

Financial

Crisis

MENAT average GDP growth (%)

Slo

we

r M

EN

AT

gro

wth

ex

pe

cte

d..

Growth as expected is subdued, generally below-potential.

Many EU countries are poorer today than five year ago,

social pressures are likely to rise.

MENAT growth as expected is slower, while there is an

urgent need to create jobs.

MENAT low growth combined with low employment growth

could create political tensions and delay much needed

reforms.

MENAT banking: Solvency, prudence and liquidity at good

levels, more growth ahead.

Key takeaways

Note: Trend Growth is the forecasted growth.

0

2

4

6

8

10

12

14

KU JOR TUR ALG IRAQ TUN LEB QA UAE BAH EGP MOR KSA

2000-2009

2011-2018

5

Results Overview

6

Revenue 12.8% 47.5%|29.5%(1)

2nd Quarter 2013: Key Highlights

STRONG GROWTH IN REVENUE SUPPORTED BY

IMPROVED NET INTEREST INCOME AND NON INTEREST

INCOME RESULTS

NIMS ADVANCED DESPITE LOW INTEREST RATES

ENVIRONMENTS

HIGHEST RETURN RATIOS & NET INCOME REACHING

KD23.8M WITH (34.8% GROWTH YOY) BEFORE

PRECAUTIONARY RESERVES OF KD11.5M

ENHANCED ASSET QUALITY; WITH IMPROVED NPA

RATIO AND BETTER COVERAGE RATIO

MAINTAINED GROWTH YOY & QOQ IN BALANCE

SHEET; SUPPORTED BY INTERNATIONAL OPERATIONS

PERFORMANCE

OPTIMIZING BALANCE SHEET WITH SOUND

LIQUIDITY LEVELS

Q2’12 Q2’13

NPA’s, net of

collaterals

4.0%

1.9%

Loan

Growth 20.4% 31.4%|10.0%(1)

Solid Business

Performance

with access &

exposure to high

growth markets

Healthy Balance

Sheet generating

resilient stream

of earnings

Asset Quality

in comfortable

levels with

effective risk

management

ROTE(2) 27.7% 31.9%|32.8%(1)

NIM % 2.6% 2.91%|2.93%(1)

Deposit

Growth 26.6% 29.6%|16.8%(1)

Liquidity

Ratio 36.2% 34.0%|37.6%(1)

NPA’s

Coverage(3) 120% 246%

NPA’s Ratio 9.2% 4.2%

(1)Excl. BBT contribution including cost impact of new sub-debt in Q2’13.

(2)Excl. additional precautionary reserves.

(3)Total Provisions(General + Specific) to NPA’s net of collateral.

7

Performance Trends –

2nd Quarter 2013

8

13.6 15.2

9.2

15.6 12.3

4.0 2.5 10.8

5.0 11.5 17.6 17.7

20.0 20.6

23.8

Q2'12 Q3'12 Q4'12 Q1'13 Q2'13

4.5 6.4

2.9 2.3 5.9

4.0 2.5 10.8

5.0

11.5 8.5 8.9

13.7

7.3

17.4

Q2'12 Q3'12 Q4'12 Q1'13 Q2'13

Net Profit | KD million(1)

Cost of Credit | KD million(1) Revenue | KD million(1)

Strong Financial and Operating Performance…

Key Indicators(1)

Burgan Bank Group Q2 12 Q2 13

Revenue Growth (YoY) 12.8% 47.5%|29.5%(2)

Operating Profit Growth (YoY) 8.2% 41.2%|40.9%(2)

Cost to Income Ratio 39.1% 41.7%|33.7%(2)

Jaws Ratio (YoY) (8.0%) (9.8%)|14.9%(2)

Loans to Cust. Deposits 81.9% 83.1%|77.1%(2)

Liquidity Ratio(3) 36.2% 34.0%|37.6%%(2)

NPA Ratio 9.2% 4.2%

NPA net of Collateral Ratio 4.0% 1.9%

ROE | ROE ex. Additional Provisions 12.7%|16.6% 10.0%|20.0%

ROTE | ROTE ex. Additional Provisions 21.0%|27.7% 15.6%|31.9%

48.1

48.2 51.2

48.1

62.3 7.9

8.7

56.0

71.0

Q2'12 Q3'12 Q4'12 Q1'13 Q2'13

BBT contribution after allocation of subdebt cost in KD million.

(1)Figures are reported after consolidation adjustments,

(2)Excl. BBT contribution in Q2’13

(3)Liquid assets comprises of Cash & Cash eq., Treasury bills & bonds and Due from Banks & OFIs.

Additional Provisions

2,697 3,484

Gross Loans in KD million. Additional Provisions

3,498 2,894 3,536

∆ 47.5%| 29.5%(2)

∆ 34.8%

9

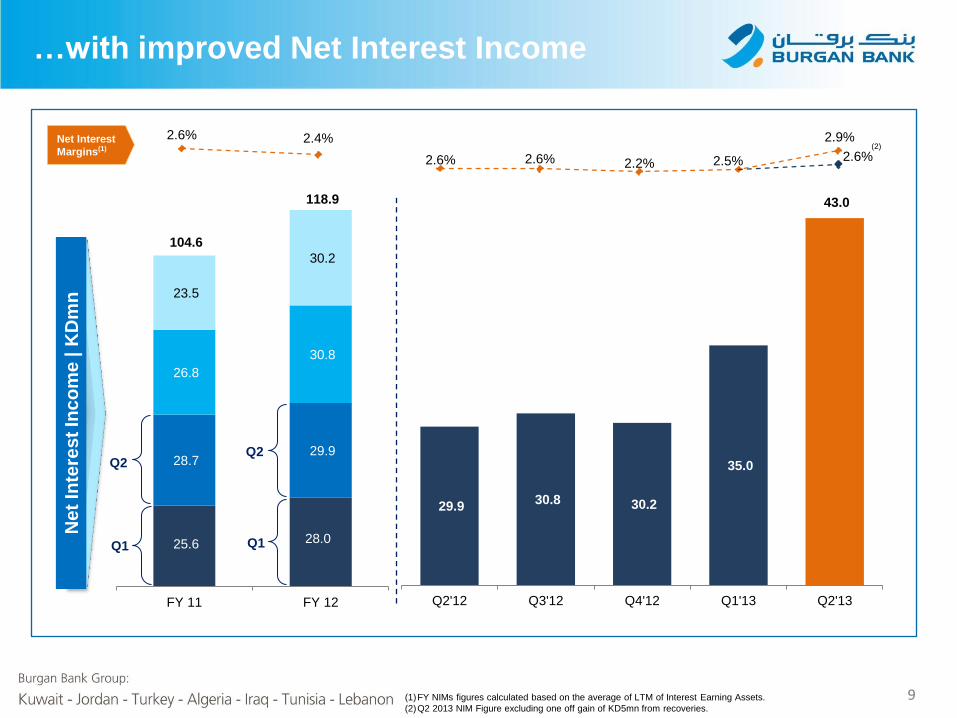

…with improved Net Interest Income

29.9 30.8 30.2

35.0

43.0

Q2'12 Q3'12 Q4'12 Q1'13 Q2'13

25.6 28.0

28.7 29.9

26.8

30.8

23.5

30.2

104.6

118.9

FY 11 FY 12

Q2 Q2

Q1 Q1

2.6% 2.4% Net Interest

Margins(1)

2.6% 2.6% 2.2% 2.5%

Ne

t In

tere

st

Inc

om

e | K

Dm

n

(2) 2.9%

2.6%

(1)FY NIMs figures calculated based on the average of LTM of Interest Earning Assets.

(2)Q2 2013 NIM Figure excluding one off gain of KD5mn from recoveries.

10

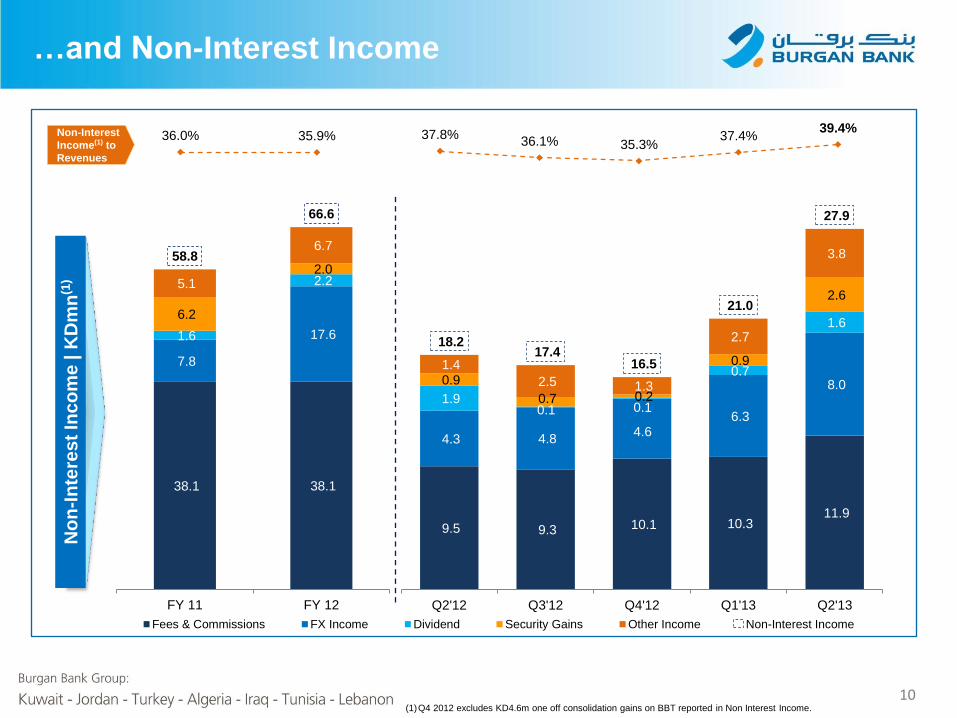

…and Non-Interest Income

9.5 9.3 10.1 10.3 11.9

4.3 4.8 4.6

6.3

8.0 1.9

0.1 0.1

0.7

1.6

0.9

0.7 0.2

0.9

2.6

1.4

2.5 1.3

2.7

3.8

18.2 17.4

16.5

21.0

27.9

Q2'12 Q3'12 Q4'12 Q1'13 Q2'13

38.1 38.1

7.8

17.6 1.6

2.2

6.2

2.0 5.1

6.7 58.8

66.6

FY 11 FY 12

36.0% 35.9% 37.8% 36.1% 35.3%

37.4% 39.4%

No

n-I

nte

res

t In

co

me

| K

Dm

n(1

)

Fees & Commissions FX Income Dividend Security Gains Other Income Non-Interest Income

Non-Interest

Income(1) to

Revenues

(1)Q4 2012 excludes KD4.6m one off consolidation gains on BBT reported in Non Interest Income.

11

Strengthen/Diversify Balance Sheet

2,135 2,211 2,218 2,298 2,407

1,029 1,119

1,677 1,670

1,694 3,164

3,330

3,895 3,968

4,101

Q2'12 Q3'12 Q4'12 Q1'13 Q2'13

1,867 2,029 2,054 2,048 2,055

725

755

1,331 1,318 1,351 2,592

2,783

3,384 3,366 3,406

Q2'12 Q3'12 Q4'12 Q1'13 Q2'13

28.0%

27.1%

39.3% 39.1%

39.7%

Cu

sto

me

r L

oa

ns

| K

Dm

n

Cu

sto

me

r D

ep

os

its

| K

Dm

n

81.9% 83.6%

86.9% 84.8%

83.1%

32.5%

41.3%

International

Contribution

Loans to

Deposits

Kuwait International Customer Loans Kuwait International Customer Deposits

Customer loans and Customers deposits figures after consolidation adjustments.

12

…and effectively managed risk position

9.2% 8.8%

5.6% 5.6%

4.2%

Q2'12 Q3'12 Q4'12 Q1'13 Q2'13

NPA’s to Gross Facilities NPA’s net of collateral to Gross Facilities

4.0%

3.7%

1.8% 1.8% 1.9%

Q2'12 Q3'12 Q4'12 Q1'13 Q2'13

NPL KPIs

Indicators Q2’12 Q1’13 Q2’13

Gross Loans 2,697 3,484 3,536

NPL’s 254 258 188

NPL Ratio 9.4% 7.4% 5.3%

NPL, net of

collateral 2.8% 2.1% 2.1%

NPL Coverage, net

of collateral 139% 165% 175%

Non Performing Assets (KD million) and Coverage Ratio

349 341 267 277

206 153 143

86 90 92

184 188 194 202 226

120% 131% 226% 226%

246%

53% 55% 73% 73%

110%

Q2'12 Q3'12 Q4'12 Q1'13 Q2'13

NPA NPA net of collateral Total provisions Coverage net of collateral Coverage Ratio

Indicators Q2’12 Q1’13 Q2’13

Gross Loans 2,697 3,484 3,536

NPL’s 254 258 188

NPL Ratio 9.4% 7.4% 5.3%

NPL, net of

collateral 2.8% 2.1% 2.1%

NPL Coverage 41.2% 45.8% 69.1%

NPL Coverage, net

of collateral 139% 165% 175%

13

13.5 16.1

9.2

17.5 13.6

3.5 7.9

4.0

17.0 16.1 17.1 17.5 17.6

13.6 15.2

9.2

15.6 12.3

4.0 2.5 10.8

5.0 11.5 17.6 17.7

20.0 20.6

23.8

2011 Quarterly Net Profits 2012 Quarterly Net Profits 2013 Quarterly Net Profits

ROE(1) ROTE(1)

12.7% 13.8%

7.9%

13.4% 10.0%

3.9% 2.4%

9.9%

4.5% 10.0%

16.6% 16.2% 17.8% 17.9%

20.0%

Q2'12 Q3'12 Q4'12 Q1'13 Q2'13

21.0% 22.4%

12.5%

21.5%

15.6%

6.8% 4.0%

16.1%

7.5% 16.3%

27.7% 26.4%

28.6% 29.0% 31.9%

Q2'12 Q3'12 Q4'12 Q1'13 Q2'13

… with stable shareholder returns

(1) Quarterly ROE & ROTE are Annualized.

Quarterly Net Profit | KD million

Additional Provisions

Q2’11 Q2’12 Q3’11 Q3’12 Q4’11 Q4’12 Q1’12 Q1’13 Q2’12 Q2’13

Additional Provisions Additional Provisions

14

Burgan Bank –

By Country

15 (1)Reported contribution excluding consolidated adjustments, with Sub Debt cost allocated to subsidiaries.

Net Profit contribution to BB Share; Q2 2013 Turkey Non Meaningful.

Burgan Bank Contribution Summary Q2’13(1)

49.3%

55.3%

45.7%

58.1%

60.1%

59.4%

8.9%

17.9%

17.9%

15.3%

15.0%

13.7%

25.9%

16.1%

14.5%

7.2%

7.1%

6.2%

0.2%

11.8%

9.8%

16.2%

11.5%

7.7%

6.7%

6.9%

7.8%

1.4%

6.9%

8.3%

3.8%

3.3%

1.9%

0.2%

2.2%

Net Profit^

OperatingProfit

Revenue

CustomerDeposits

CustomerLoans

Total Assets

Kuwait Jordan Algeria Turkey Iraq Tunisia

Diversification Benefits Burgan Balance

Sheet & P&L…

16

1,867

504

195

31 5

2,055

513

243

555

47 7

Kuwait Jordan Algeria Turkey Iraq Tunisia

Q2'12 Q2'13

2,135

569

224 167 67

2,407

633

298 404 324

78

Kuwait Jordan Algeria Turkey Iraq Tunisia

Q2'12 Q2'13

24

34

11 13 8

11 9 3 5 1 2

1 1

1

12

14

10

…with stable performance from all the

subsidiaries

Revenue | KD million Operating Profit | KD million

Net Loans(1) | KD million Customer Deposits(1) | KD million

Kuwait

Q2’13

Jordan Algeria Turkey Iraq Tunisia

Q2’12

Sub Debt Cost. Sub Debt Cost.

(1)Figures are reported before consolidation adjustments.

16

25

7 8 6 7

2 3 0.3 1.7

1 1

1

8 9

2

Kuwait

Q2’13

Jordan Algeria Turkey Iraq Tunisia

Q2’12

17

Key Developments

18

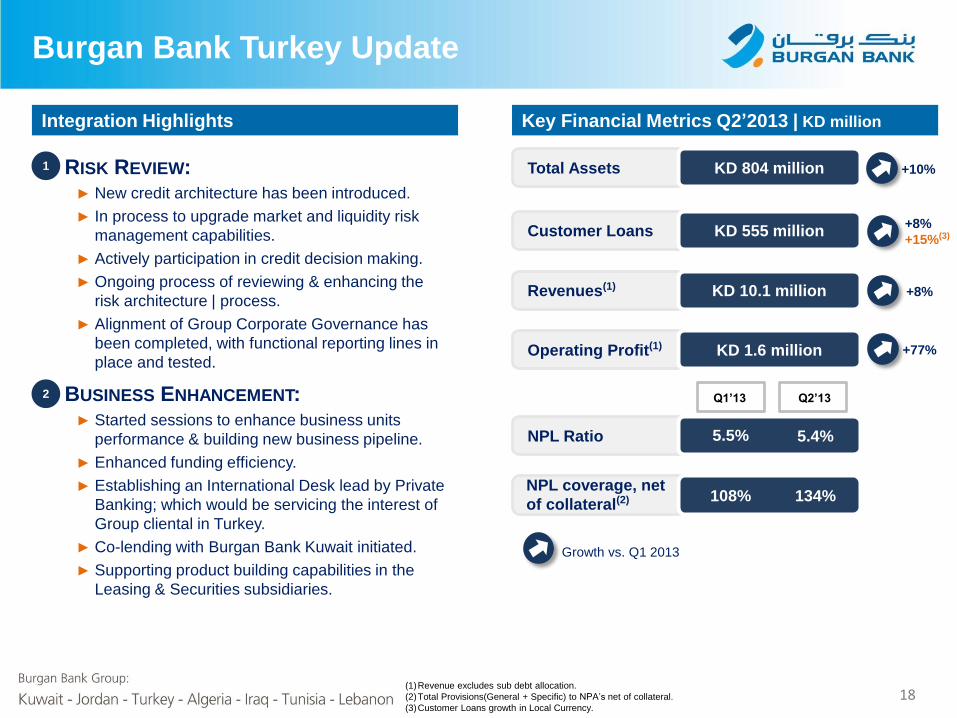

Burgan Bank Turkey Update

Integration Highlights

(1)Revenue excludes sub debt allocation.

(2)Total Provisions(General + Specific) to NPA’s net of collateral.

(3)Customer Loans growth in Local Currency.

RISK REVIEW: ► New credit architecture has been introduced.

► In process to upgrade market and liquidity risk

management capabilities.

► Actively participation in credit decision making.

► Ongoing process of reviewing & enhancing the

risk architecture | process.

► Alignment of Group Corporate Governance has

been completed, with functional reporting lines in

place and tested.

BUSINESS ENHANCEMENT: ► Started sessions to enhance business units

performance & building new business pipeline.

► Enhanced funding efficiency.

► Establishing an International Desk lead by Private

Banking; which would be servicing the interest of

Group cliental in Turkey.

► Co-lending with Burgan Bank Kuwait initiated.

► Supporting product building capabilities in the

Leasing & Securities subsidiaries.

1

2

Key Financial Metrics Q2’2013 | KD million

Total Assets KD 804 million

Customer Loans KD 555 million

Revenues(1) KD 10.1 million

Operating Profit(1) KD 1.6 million

Growth vs. Q1 2013

+10%

NPL Ratio 5.4%

NPL coverage, net

of collateral(2)

+8%

+15%(3)

+8%

+77%

Q1’13 Q2’13

5.5%

134% 108%

19

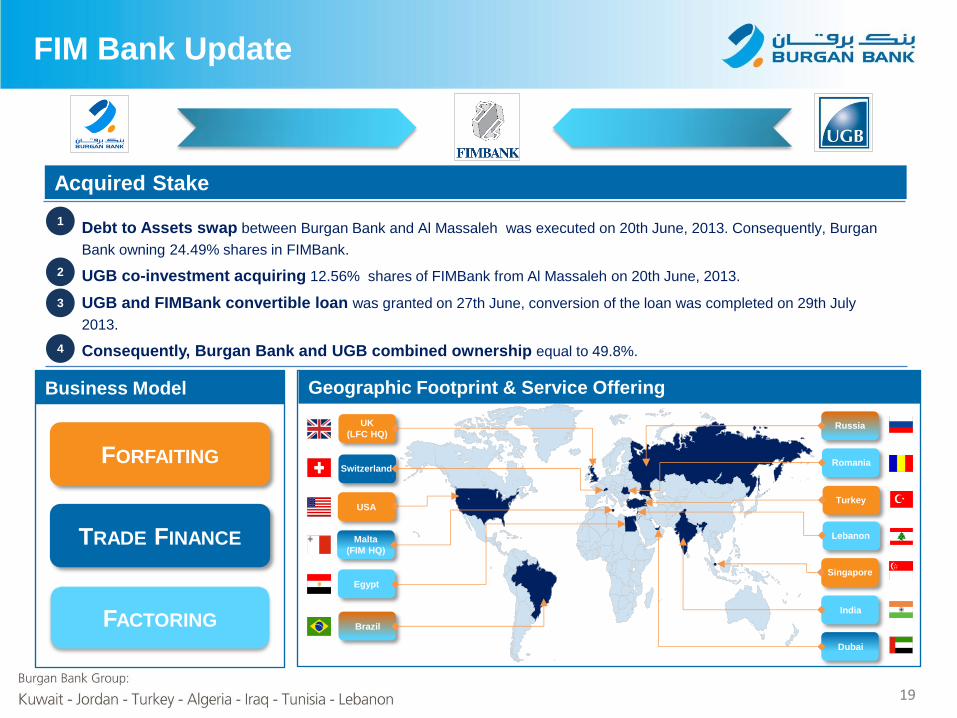

FIM Bank Update

Acquired Stake

Debt to Assets swap between Burgan Bank and Al Massaleh was executed on 20th June, 2013. Consequently, Burgan

Bank owning 24.49% shares in FIMBank.

UGB co-investment acquiring 12.56% shares of FIMBank from Al Massaleh on 20th June, 2013.

UGB and FIMBank convertible loan was granted on 27th June, conversion of the loan was completed on 29th July

2013.

Consequently, Burgan Bank and UGB combined ownership equal to 49.8%.

1

2

3

4

Business Model

FORFAITING

TRADE FINANCE

FACTORING

Geographic Footprint & Service Offering

UK

(LFC HQ)

Brazil

Russia

Egypt

Romania

Lebanon

India

USA Turkey

Singapore

Malta

(FIM HQ)

Dubai

Switzerland

20

FIM Bank Capabilities & Opportunities

FIM Bank

Capabilities &

Opportunities

Global

Network &

Presence

Diversification of

Risk

Unique

Business Model

EU

Operating

License

Successful

Product

Portfolio

Structured Trade

& Loan

Syndication

Factoring &

Fortaiting

Best in Class

21

Performance vs. Peers

22

Customer Deposits Growth | KD million Customer Loans Growth | KD million

ROTE(1)(2) | % Revenues Growth | %

2.1%

3.0%

7.1%

22.6%

31.4% 1

2

3

4

5

1

2

3

4

5

(6.3%)

7.7%

9.6%

26.7%

47.5% 1

2

3

4

5

1

2

3

4

5

Local Peers – Q2 2013 Ranking

(1)Burgan Bank ROTE exclude additional precautionary reserves.

(2)Annualized ROTE based on Open Equity.

5.2%

5.6%

8.1%

11.7%

31.9%

(3.4%)

(0.5%)

13.9%

29.6%

39.7%

23

Customer Deposits Growth | KD million Customer Loans Growth | KD million

ROTE(1)(2) | % Revenues Growth | %

2.0%

3.3%

9.7%

17.7%

22.6%

26.3%

31.4%

39.2%

Regional Peers – Q2 2013 Ranking

(1)Burgan Bank ROTE exclude additional precautionary reserves.

(2)Annualized ROTE based on Open Equity.

1

2

3

4

5

6

8

7

6.1%

14.2%

14.3%

15.6%

17.3%

29.6%

32.7%

39.7%

11.7%

13.7%

15.3%

15.8%

16.7%

18.3%

25.4%

31.9%

0.0%

2.2%

13.2%

16.8%

26.7%

33.6%

47.5%

51.4%

1

2

3

4

5

6

8

7

1

2

3

4

5

6

8

7

1

2

3

4

5

6

8

7

24

Conclusion

25

… In Summary

BUSINESS

PERFORMANCE

Solid Operating Performance with access &

exposure to high growth markets delivering resilient

underlying earnings

LIQUIDITY & CAPITAL Healthy Balance Sheet maintained growth YoY &

QoQ supported by International operations

performance with CAR at 17.6% & Tier 1 at 11.4%

ASSET QUALITY In Comfortable Levels, NPA ratio improved supported

by asset growth, better coverage and major declines in

NPA’s from Kuwait

REGAINING SPEED OF GROWTH RESULTING IN HIGH RETURNS &

SOLID OPERATING PERFORMANCE

26

Thank You

27

Appendix

28

Q3 2012 Q1 2013 Q4 2012 Q2 2013

Best Banking

CEO Kuwait 2013

Global Banking &

Finance Review

Best Banking

Group MENA

2013

Global Banking &

Finance Review

External Recognitions….

All awards mentioned above are the results of “peers & customers voting” process

organized by the publications.

Best Private Bank

in Kuwait Capital

Finance

International

Quality

Recognition

Award

JP Morgan Chase

Bank of the year

Tunisia

InterContinental

Finance Magazine

Deal of the Year

“ET Deal”

Acquisition

International

Best Bank in

Jordan for 2012

Global Banking &

Finance Review

Best Private

Banking offering

in Jordan 2012

Global Banking &

Finance Review

Best Co-branded

credit card in

Jordan 2012

Global Banking &

Finance Review

Best Bank in Iraq

2012

EMEA Finance

Best Banking

Group In Kuwait

World Finance

2013

Best Employee

Development in

GCC

World Finance

2013

Best Domestic

Retail Bank of Year

Asian Banking &

Finance Magazine

2013

29

Total Share Returns Analysis

Source: Bloomberg.

Share Price Performance vs. Peers

80

90

100

110

120

130

140

150

160

Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Apr-13 Jul-13

NBK CBoK ABK GBK BB