loxley-opp day q2'12 20 aug v3€¢the 400 ton per day integrated municipal solid waste...

TRANSCRIPT

Opportunity DayQ2’2012

LOXLEY PUBLIC COMPANY LIMITED

August 20, 2012

"Inspired Choice for Customers, Business Partners and Investors"

August 20, 2012

1. Business and Revenue Structure

2. Financial Highlights Q2’2012 and Overview Y2012

3. Order Backlog and Project Highlights

2

•Established in 1939

•Loxley Group : about 30 activecompanies

•Listed company in SET100

•Last 5-year revenues : THB10,000-14,000 million/Year

“LOXLEY”

3

ICT & Project

Trading Business

Joint Venture Business

Service Business

Conglomerate Business

Diversification can generate a business

balance

73 Years experience

with

Jewel InvestmentsStrong and stable

Loxley’s

LOXLEY’s Key Drivers

4

with

Respect customers and business partners

Network

Synergy

Loxley’s Group

Strong Financial Leverage

Matching source and use of fund

Strong and stable contributions from

“JV”Loxley’s

Key Drivers

ICT & Project (Project Base) Trading

CO. & Subsidiaries

Technology

Service

Associates

Business and Organization Structure

ICT Project

5

MVNO

Loxley Global (LPC 51%)

Loxley Gtech(LPC 18%)

25% 40% 50% 40% 30% 45% 51%

33%

Start COD :

Dec 2011

PCC

ICT & Project

Trading Business

Business Overview

Transmission Line 3G NetworkElectronic Toll

Collection

Cable Submarine Network

Broadcast

Power Substation

6

Project Business

Joint Venture Business

Service BusinessLocomotive

Dipping Sonar System

Security Solution Services

Revenue Structure (2007-2011)

ICT &

Project,

62%

Trading,

33%

Service,

6%

2011’s Revenue Structure

ICT Trading

Service

Annual Revenue

5,766 5,122 5,241 5,310

8,730

4,320 4,482 4,224 4,303 4,617

547 554 611 668 780

10,633 10,158 10,076 10,281

14,127

37%

THB’Million

7

ICT Trading

Service

JV

2007 2008 2009 2010 2011

ICT & Project Trading Service Total

Equity Profit from AssociatesTHB’Million

1,192 1,086

996 1,173 1,215

268 208

314 357 376

21,287

22,803

14,834

16,646

20,279

-

5,000

10,000

15,000

20,000

-

200

400

600

800

1,000

1,200

1,400

1,600

2007 2008 2009 2010 2011

Revenue

Equity profit

Profit

2011’s Equity Profit Structure

BP Castrol,51%

Blue Scope Steel, 37%

Oriental Post, 7%

Blue Scope Lysaght, 3%

Others, 2%

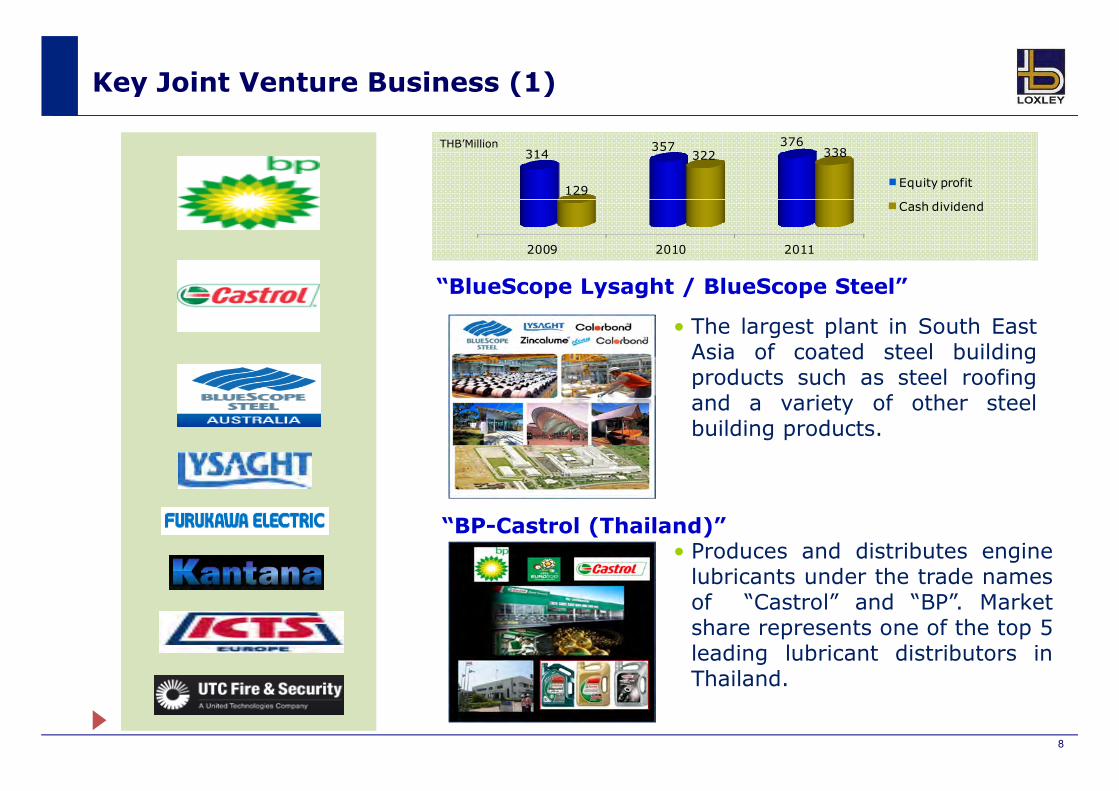

“BlueScope Lysaght / BlueScope Steel”

• The largest plant in South EastAsia of coated steel buildingproducts such as steel roofingand a variety of other steel

Key Joint Venture Business (1)

Equity profit

Cash dividend

THB’Million

2009 2010 2011

314357 376

129

322 338

8

and a variety of other steelbuilding products.

“BP-Castrol (Thailand)”• Produces and distributes enginelubricants under the trade namesof “Castrol” and “BP”. Marketshare represents one of the top 5leading lubricant distributors inThailand.

Background

• Manufacturing steel since 1915

• Headquartered in Melbourne, Australia

• World’s largest manufacturer of ZINCALUME steel with strong brands

Capacity

• Cold rolling facility of 400,000 tonnes

Key Joint Venture Business (2)

“BlueScope Lysaght / BlueScope Steel”

9

• Cold rolling facility of 400,000 tonnes

• Two metallic coating lines of 375,000 tonnes

• Painting operating of 90,000 tonnes

1. Business and Revenue Structure

2. Financial Highlights Q2’2012 and

Overview Y2012

3. Order Backlog and Project Highlights

10

Financial Highlights – 2Q12 and 1H12

THB Million 2Q11 1Q12 2Q12 1H11 1H12Sales 3,402 3,448 3,399 5,955 6,847

Costs 2,871 2,963 2,915 5,026 5,878

Gross profit 531 485 484 929 969

Selling & admin expenses 443 455 508 871 955

EBIT before Equity profit 112 83 (1) 109 83

Equity profit from associate 90 157 153 285 310

EBIT 202 240 152 394 393

“1H12, Continuing increase in sales but also increase in expenses due to business development activities”

11

EBIT 202 240 152 394 393

Finance cost 35 49 65 67 114

Income tax 44 30 18 55 48 Net Profit 111 165 67 254 232

Key Financial Ratio

% Gross Margin 16% 14% 14% 16% 14%

% SG&A/Sales 13% 13% 15% 15% 14%

% Net Margin 3% 5% 2% 4% 3%

Revenue

1Q12 VS 2Q12

• Slightly decreased due to a progressivedecline in 3G network installment

1H11 VS 1H12

• Significantly increased due to 2 megaprojects i.e. 3G and CSN

1%

15%

Revenue and EBIT – 2Q12 and 1H12

3,402 3,448 3,399

5,955

6,847

2Q11 1Q12 2Q12 1H11 1H12

Revenue

THB’Million

12

EBITEBIT

1Q12 VS 2Q12

• Decreased due to

– a drop in sales as 3G’s revenue wasunder target by 30% and,

– a hike in SG&A caused by new businessunit and new project developments

1H11 VS 1H12

• Slightly decreased as SG&A was up

36%

0.3%

2Q11 1Q12 2Q12 1H11 1H12

202 240

153

394 393

2Q11 1Q12 2Q12 1H11 1H12

THB’Million

Equity profit

2Q11 VS 2Q12

• Significantly increased due to the improvedperformances of BP Castrol and BlueScope Steel

• Associates’ ability to maintain the profit in bothQ1 and Q2 of 2012 of more than THB 150million.

1H11 VS 1H12

• Increased due to the improved performances of

70%

9%

Equity Profit and Net Profit – 2Q12 and 1H12

Equity Profit

90

157 153

285 310

2Q11 1Q12 2Q12 1H11 1H12

THB’Million

13

• Increased due to the improved performances ofBP Castrol and BlueScope Steel

• Also, L-Solar One commenced a full operationand its performance achieved target

Net profit

• Both quarterly and half yearly net profitdecreased as some parts of revenue recognitionwere inevitably postponed when there was aprogressive decline in 3G installment.

Net Profit

111

165

67

254 232

2Q11 1Q12 2Q12 1H11 1H12

THB’Million

Consolidated Balance Sheet•Cyclical incremental inworking capital both inassets and liabilities

oCommencement of 2 megaprojects

oPile-up A/Rs and inventories

oAdditional project financeand short-term loans

Temporary increase in D/E

4,502 4,405

1,6611,604

7,807 6,185

5,084 4,962

8,885 7,233

Assets Liabilities &Equity

Assets Liabilities &Equity

1H2012 Y2011

Financial Status – 2Q12 and 1H12

14

oTemporary increase in D/Eratio

1H2012 Y2011

Shareholders' equity Non current liabilities Current liabilities

Non current assets Current assets

1H2012 Y2011 Change

Current assets 8,885 7,233

Non current assets 5,084 4,962

Total assets 13,970 12,194 15%

Current liabilities 7,807 6,185

Non current liabilities 1,661 1,604

Total liabilities 9,468 7,789 22%

Shareholders' equity 4,502 4,405 2%

Current ratio 1.1 1.2

D/E ratio 2.1 1.8

BV per share (THB) 2.3 2.2

Return on Equity 6% 7%

THB Million Consolidated

4,648

1,838

ICT & Project

Trading

Core Business

•Current backlog 8,159 MB (45 % will be 2H12 revenue)

•New project (high potential)

1H12 Revenue 2H12 “Key Drivers”Expected growth

•“Strong Client Base” in consumer and chemical products

•Construction material group: “Roof work for station start”

•New Business “Food”: Full operation from 5 branches

Outlook Y2012

15

•Strong performance of key associates (BST & BP)

•Continuing income (Equity profit) from renewable business, “L Solar 1”

310

Service

Expected growth 10-1

2%

Expected

growth

35-4

0%Joint

venture

1H12 Equity profit

•New Business “Food”: Full operation from 5 branches

361 •Strong revenue base from “Contract with AOT”

•New customer base from “Airline and Cargo”

1. Business and Revenue Structure

2. Financial Highlights Q2’2012 and Overview Y2012

3. Order Backlog and Project Highlights

16

Order Backlog

Backlog Summary THB Million

Backlog - 31/12/11 9,797

New Backlog (Jan-Jun 2012) 2,277

Less Invoicing (Jan-Jun) 3,915

Current Backlog 8,159

Major Projects

NorthNortheast

“3G” “CSN” “NEdNet”

17

Central

South

Construction and installation of 3G “TOT”

5,600 MB.

May 2011- Dec 2012

Y2011-39%Y2012-61% or 3,400 MB

Design, Supply and Installation of Optical Fiber Cable 1,340 km.

2,527 MB.

Aug 2011 – Sept 2012

Y2011-17%Y2012-83% or 2,200 MB

Installation of Optical Fiber Cable-MOE

1,036 MB.

Jan 2012 – Sept 2013

Y2012-22%Y2013-78%

Type

Project Value

Project Period

ProjectStatus

New Backlog 1H12

Optical Installation for 3G Purple Line - Lysaght HW / SW Applications

659MB

384 301

NEW BACKLOG 2,277 MB.

MB MB

“Continuous awarded projects in the pipeline with 2,277 MB new backlog in 1H12”

18

ADM / ATM Geographic Application Substation

Replacement Radio Transmission 7 Networks

Water Installation & PipeWorks

Other Projects

286 158 120

115 93 184

MB MB MB

MB MB MB

High Potential Projects

•Concession for electricity dam construction in Laos

•2 projects of transmission line in Laos with capacity of 230-115 and 500 kV

Dam Construction Transmission Line

“High potential projects to stimulate further revenue 2H12 and 2013”

19

High Potential

13,000 MB.

construction in Laos

•Small and large dam with capacity of 3-10 MW and

50-60 MW

line in Laos with capacity of 230-115 and 500 kV

•On process to final deal

•Substation project for PEA and MEA, 115 kV and 115-24 kV

•Status-waiting for E-Auction

•The 400 ton per day integrated municipal solid waste management project

•On process to final deal

Substation Kompogas

Project Highlights-Online Lottery (1)

เดลนิิวส์ 14 สค. 55 Primary Data Center

Less than 8 seconds

Terminal

20

ขา่วหุ้น 16 สค. 55

โพสตท์เูดย ์ 14 สค. 55

• 6,700 terminals had been already installed through all provinces, testing process (3 times of Soft launch) was done.

• Current Status : On the process of Terminal, Software and Network review

Back up Data Center

Project Highlights-Online Lottery (2)

Lottery operated by GLO

• Purchase/round (2 round a month) 2,800-3,200 MB. or 70-80 million bets/round

• LGT’s revenue 0.75 Baht per bet, or revenue at 1,200-1,500 million/year

• Contract period : 5 years

Financial Forecast

21

906

1,362

1,607

2,025

2,829

Y2003 Y2004 Y2005 Y2006 Y2007

Purchase/Round

• Contract period : 5 years starting from the operation date (Able to extend for 3 years ( 3 times, 1 year/time)

Purchase/Round :THB Million

Thank you

22

Investor RelationsContact Person : Boonlert JaimunTel: 66 (0) 2348-8141 Fax: 66 (0) 2348-8614E-mail: [email protected]

Loxley Public Company Limited102 Na Ranong Road, KlongToeyBangkok 10110, Thailandwww.loxley.co.th