investor presentation - jefferies · investor presentation . safe harbor statement ... •six...

TRANSCRIPT

1

August 2014

INVESTOR

PRESENTATION

Safe Harbor Statement

Statements contained in this presentation that are not

historical facts are forward-looking statements, which

involve risks and uncertainties that could cause actual

results to differ materially from those expressed in the

forward-looking statements. Such forward-looking

statements are made pursuant to the safe harbor

provisions of the Private Securities Litigation Reform Act

of 1995. Please refer to the Company’s Securities and

Exchange Commission filings for further information,

including its most recent reports on Form 10-K and its

quarterly reports on Form 10-Q.

2

Company Overview

• Olympic Steel founded in 1954

• Original service center business entailed

break bulk, warehousing and distribution

• Tubular & Pipe product segment founded

in 1914 (acquired in 2011)

• Growth initiatives included expansions into:

• Value-added processing

• Diversified product categories

• New geographies

• Nasdaq symbol: ZEUS

3

Experienced & Engaged Management

4

Years in

Steel Industry

Years with

ZEUS

Michael D. Siegal Chairman and Chief Executive Officer 40 40

David A. Wolfort President and Chief Operating Officer 40 30

Richard T. Marabito Chief Financial Officer 20 20

Esther M. Potash Chief Information Officer 16 16

Donald R. McNeeley, Ph.D. President and Chief Executive Officer, Chicago Tube & Iron 42 3

Raymond Walker President and Chief Operating Officer - Flat Rolled 45 28

Andrew Greiff President - Specialty Metals 29 5

Andy Markowitz President - Integrity Stainless 20 4

Richard A. Manson Vice President and Treasurer 18 18

John W. Brieck Vice President - Southern Region 38 15

Steve Mallory Vice President - Central Region 34 22

John J. Mooney Vice President - Eastern Region 25 25

Stephen Reyes Vice President, Sales and Marketing - Flat Rolled 31 15

Frank Ruane Vice President - Purchasing 29 16

Clayton Treska Vice President - New Business Development and Director - International Trade 52 30

John Howard Director - Operational Excellence 25 1

AVERAGE 32 18

18% of shares held by insiders

A Century of Service

5

Strategic Value Creation

• Satisfying contemporary market demands

(higher complexity processing, intricate

parts kits, enabling JIT logistics, etc.)

• Successfully transformed into best-in-class

manufacturing logistics company

• Harnessed technology and operational excellence

to enhance efficiencies and customer service

• Reduced cyclicality and increased skilled labor and

machine intensiveness of products and services

• Major capital investments and growth

projects completed in 2013, on time and

within budget

6

Strategic Direction

7

Break Bulk

Tempering

Specialized Processing

Sheet & Plate

Specialty Metals

Fabrication Highly Engineered

Tube & Pipe Products

Strategic Execution

• Enhancing Manufacturing Efficiencies

• Lowering costs and enhancing customer service

• National supply programs

• Six Sigma/Lean Monitoring

• Using operational metrics to track progress

• Growing Volume Will Lever New Capacity

• Increasing market share in chosen markets

• Further integrating with prime OEMs:

• More pre-assembly processing

• 4-hour delivery cycles

• Precision packed and stacked

• Becoming the metals outsourcer of choice for OEMs

8

Value-Added Services

Flat Products:

• Custom tempering

heavy gauge cut-to-

length capabilities

• Plate processing

• Precision machining

• Laser cutting

• O2 & plasma cutting

• Welding

• Painting

• Blanking

Tubular and Pipe

Products:

• Tubing fabrication

• Bending

• Valves

• Fittings

• Pressure parts

• Hydraulic tubing

• Stainless tubing

• Aluminum pipe

• Threading & grooving

9

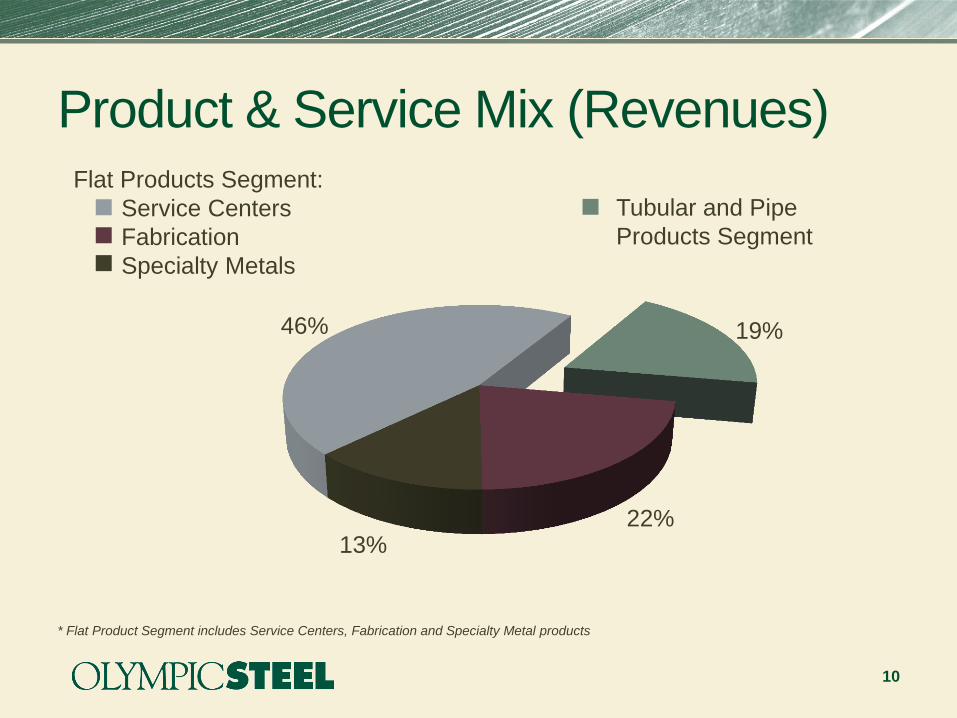

46% 19%

22% 13%

Product & Service Mix (Revenues)

10

* Flat Product Segment includes Service Centers, Fabrication and Specialty Metal products

Flat Products Segment:

Service Centers

Fabrication

Specialty Metals

Tubular and Pipe

Products Segment

Carbon Flat Products

• Olympic Steel’s core business

• 68% of consolidated sales

• Representing more than 3% of the U.S. carbon

flat rolled market and 5% of the plate market

• Three temper mills with heavy gauge

cut-to-length lines

• Increasing production to feed growing

fabrication business

• Satisfying OEMs that are outsourcing

more multi-stage metal processing

11

Tubular & Pipe Products

• Currently 19% of

consolidated sales

• Highly engineered and

labor intensive

• Less cyclical and higher margins vs.

traditional carbon markets

• CT&I growth outpacing industry

• St. Paul facility expansion

• Integration into Ohio, Kentucky, Georgia

and Mexico flat rolled facilities

12

Fabrication

• Profit margins far exceed distribution

and pre-production processing

• Highly fragmented industry with attractive

bolt-on acquisition opportunities

• Three custom temper mills provide

highest-quality materials for proprietary

downstream fabrication jobs

13

Specialty Metals

• Currently 13% of consolidated sales

• Significantly higher revenue orders and

gross profits vs. distribution and

warehousing business

• Growing aluminum sales to auto sector

• Strong and growing presence in

stainless steel markets

• Food and beverage

• Appliances/White goods

• Medical, chemical and pharmaceutical vessels

• Transportation/Tankers

14

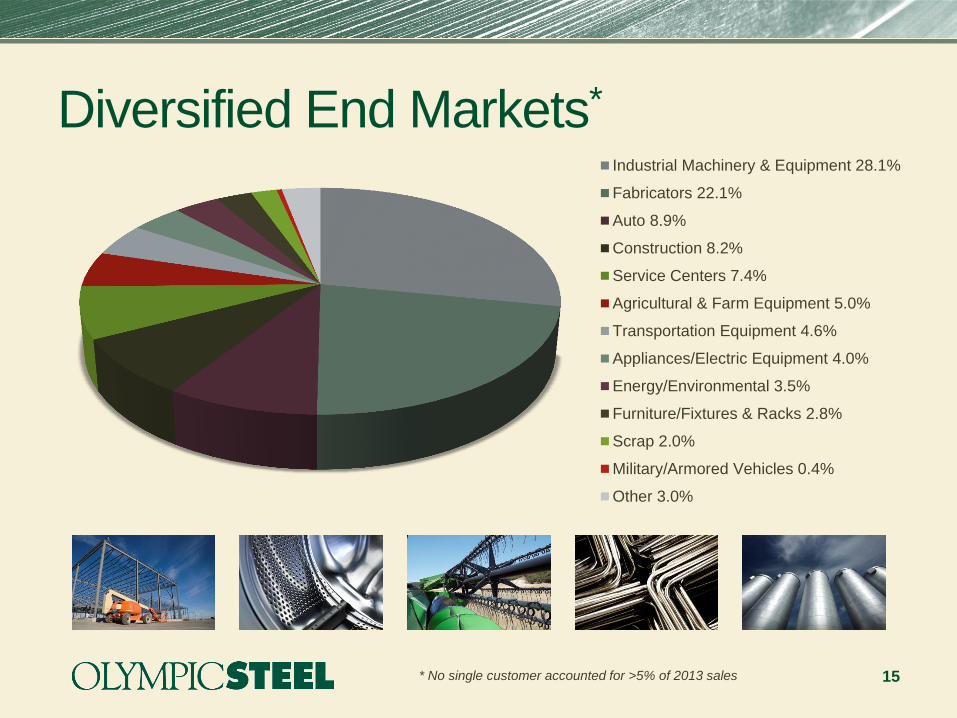

Diversified End Markets*

Industrial Machinery & Equipment 28.1%

Fabricators 22.1%

Auto 8.9%

Construction 8.2%

Service Centers 7.4%

Agricultural & Farm Equipment 5.0%

Transportation Equipment 4.6%

Appliances/Electric Equipment 4.0%

Energy/Environmental 3.5%

Furniture/Fixtures & Racks 2.8%

Scrap 2.0%

Military/Armored Vehicles 0.4%

Other 3.0%

15 * No single customer accounted for >5% of 2013 sales

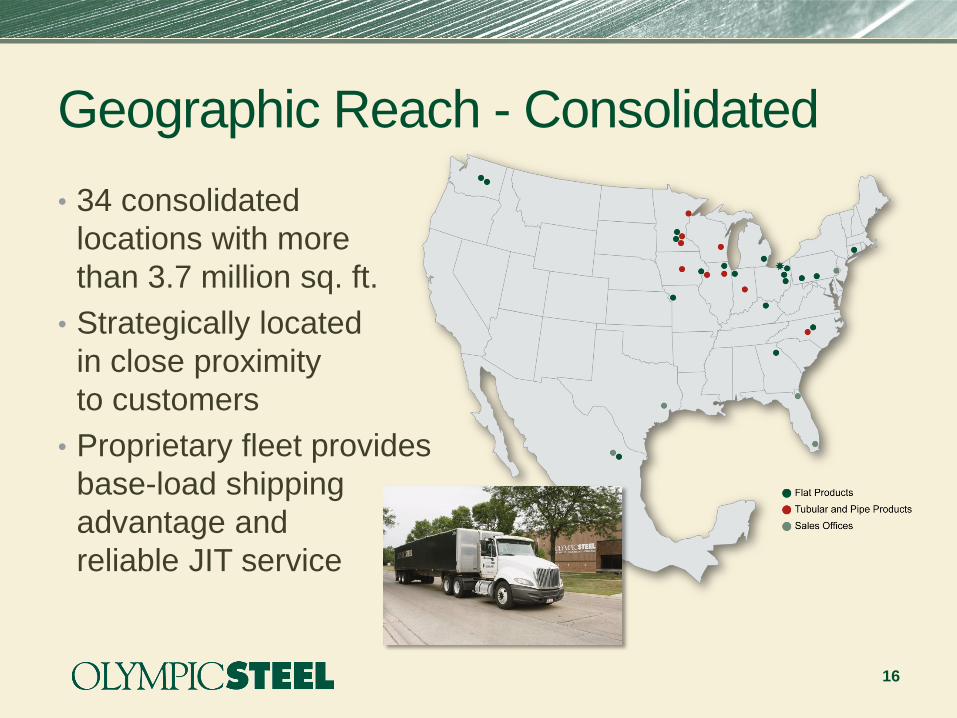

Geographic Reach - Consolidated

• 34 consolidated

locations with more

than 3.7 million sq. ft.

• Strategically located

in close proximity

to customers

• Proprietary fleet provides

base-load shipping

advantage and

reliable JIT service

16

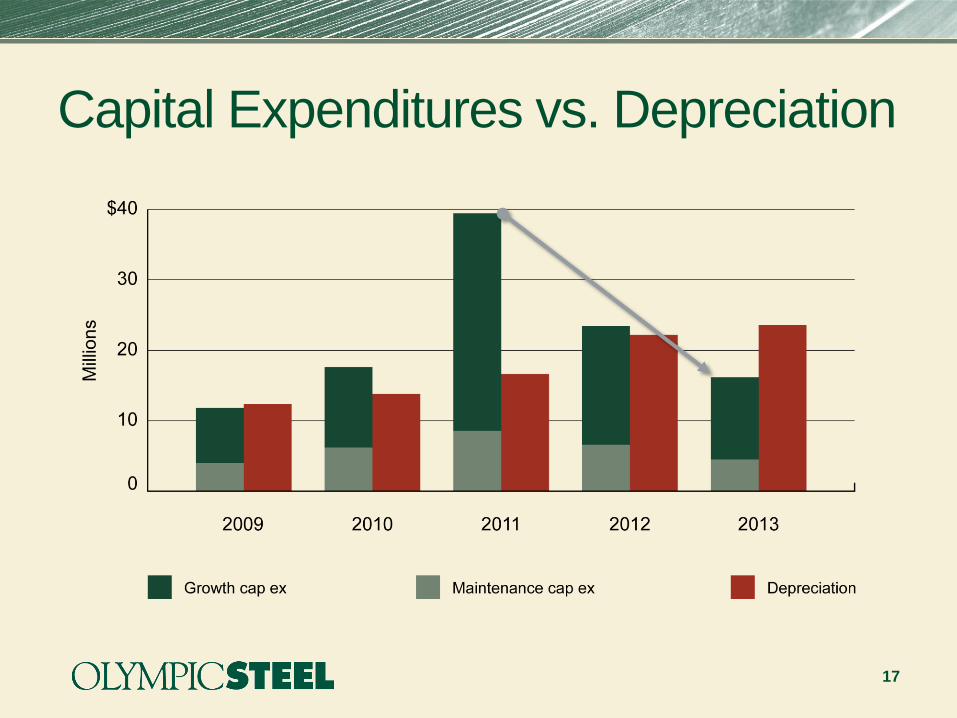

Capital Expenditures vs. Depreciation

17

Investment Highlights

• Concluded 5-year strategic expansion plan

• $143M cap ex (‘08-‘13) and $149M for the highly accretive

CT&I acquisition

• Poised for higher returns on investments

• Doubled normalized earnings capacity

• Ongoing debt reduction

• Cap ex < Depreciation is driving higher free cash flow

• Goal to reduce debt/EBITDA by 50%

• Low cost (<3%), flexible asset-based credit facility

• Opportunistic acquisitions

• Higher margin and less cyclical assets

18

19

INVESTOR Q&A

20

APPENDICES

Sales Mix Evolution by Product Group

21

2013 Carbon flat products ~68%

Hot Rolled 35.5% Plate 19.8%

Cold Rolled 6.4% Coated 6.0%

Tolling 0.3% Other 0.1%

Specialty Metals 12.8% Tube and Pipe 19.1%

2005 Carbon flat products ~95%

Hot Rolled 49.3% Plate 29.2%

Cold Rolled 8.3% Coated 7.3%

Tolling 0.9% Other 0.5%

Specialty Metals 4.5%

Fundamentals

22

$0

$500

$1,000

$1,500

2005 2006 2007 2008 2009 2010 2011 2012 2013

Revenue (in millions)

-$100

-$50

$0

$50

$100

$150

2005 2006 2007 2008 2009 2010 2011 2012 2013

Operating Income (in millions)

($6.00)

($4.00)

($2.00)

$0.00

$2.00

$4.00

$6.00

$8.00

2005 2006 2007 2008 2009 2010 2011 2012 2013

Earnings per Share

$0

$10

$20

$30

2005 2006 2007 2008 2009 2010 2011 2012 2013

Tangible BV per Share