investor presentation - v1.hdfcbank.comtracking the india growth story private consumption •...

TRANSCRIPT

Investor Presentation

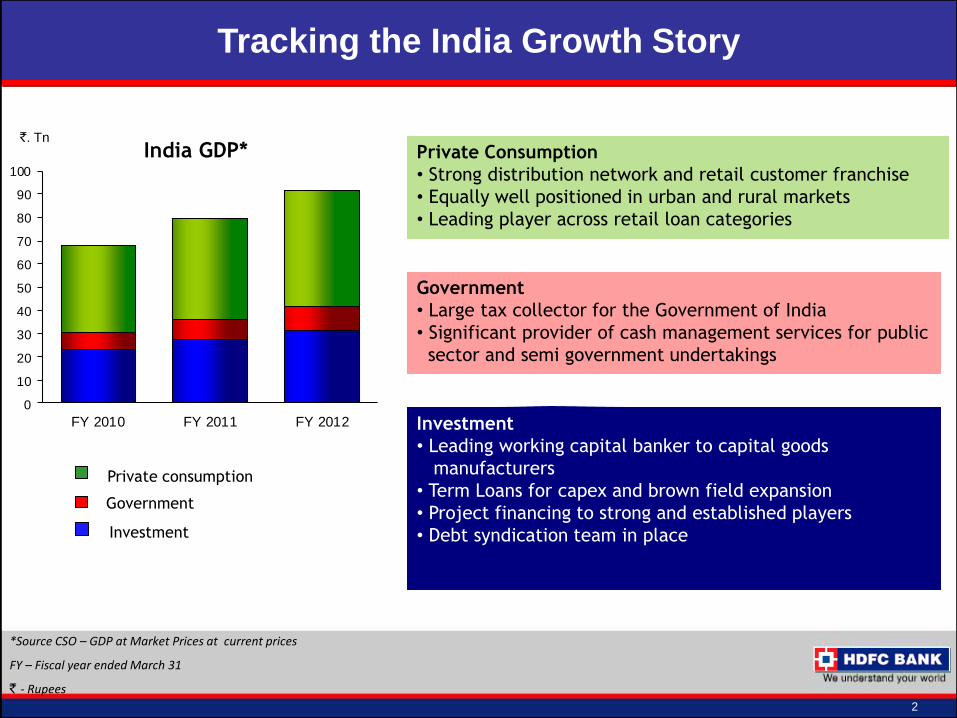

Tracking the India Growth Story

Meeting Diverse Customers’ Needs

Unique Franchise in the Indian Banking Sector

Key Business Initiatives

Financial Highlights

Value Proposition

1

Contents

Tracking the India Growth Story

Private Consumption

• Strong distribution network and retail customer franchise

• Equally well positioned in urban and rural markets

• Leading player across retail loan categories

Government

• Large tax collector for the Government of India

• Significant provider of cash management services for public

sector and semi government undertakings

Investment

• Leading working capital banker to capital goods

manufacturers

• Term Loans for capex and brown field expansion

• Project financing to strong and established players

• Debt syndication team in place

India GDP*

2

*Source CSO – GDP at Market Prices at current prices

FY – Fiscal year ended March 31

` - Rupees

`. Tn

Investment

Government

Private consumption

0

10

20

30

40

50

60

70

80

90

100

FY 2010 FY 2011 FY 2012

Tracking the India Growth Story

Meeting Diverse Customers’ Needs

Unique Franchise in the Indian Banking Sector

Key Business Initiatives

Financial Highlights

Value Proposition

3

Contents

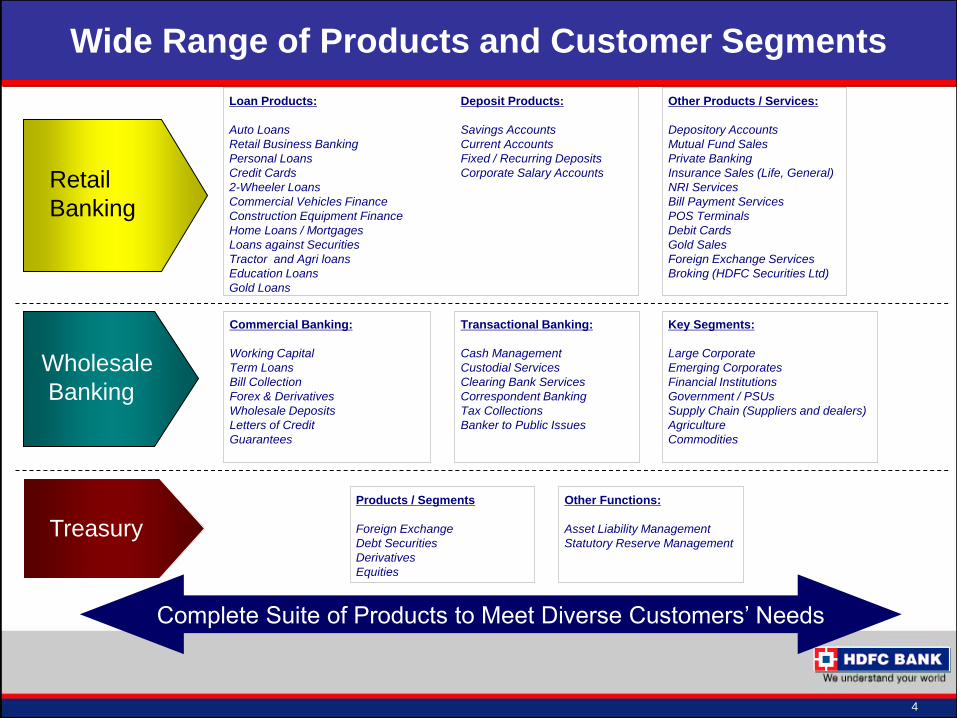

Wide Range of Products and Customer Segments

Loan Products:

Auto Loans

Retail Business Banking

Personal Loans

Credit Cards

2-Wheeler Loans

Commercial Vehicles Finance

Construction Equipment Finance

Home Loans / Mortgages

Loans against Securities

Tractor and Agri loans

Education Loans

Gold Loans

Other Products / Services:

Depository Accounts

Mutual Fund Sales

Private Banking

Insurance Sales (Life, General)

NRI Services

Bill Payment Services

POS Terminals

Debit Cards

Gold Sales

Foreign Exchange Services

Broking (HDFC Securities Ltd)

Deposit Products:

Savings Accounts

Current Accounts

Fixed / Recurring Deposits

Corporate Salary Accounts

Commercial Banking:

Working Capital

Term Loans

Bill Collection

Forex & Derivatives

Wholesale Deposits

Letters of Credit

Guarantees

Transactional Banking:

Cash Management

Custodial Services

Clearing Bank Services

Correspondent Banking

Tax Collections

Banker to Public Issues

Key Segments:

Large Corporate

Emerging Corporates

Financial Institutions

Government / PSUs

Supply Chain (Suppliers and dealers)

Agriculture

Commodities

Products / Segments

Foreign Exchange

Debt Securities

Derivatives

Equities

Other Functions:

Asset Liability Management

Statutory Reserve Management

Complete Suite of Products to Meet Diverse Customers’ Needs

Treasury

Wholesale

Banking

Retail

Banking

4

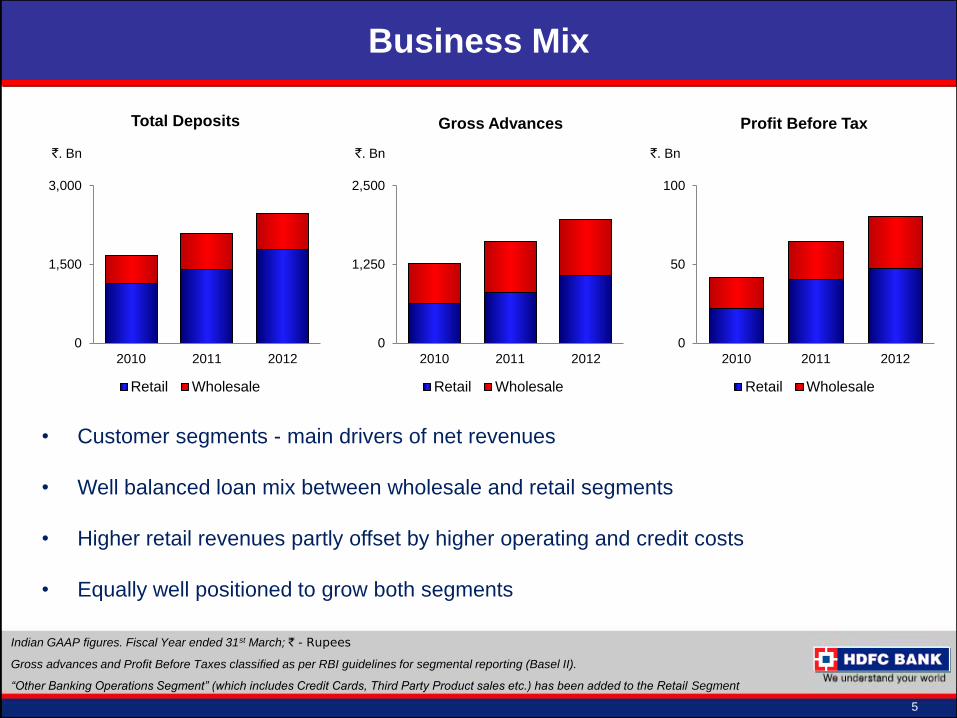

Total Deposits

Gross Advances

Profit Before Tax

5

Indian GAAP figures. Fiscal Year ended 31st March; ` - Rupees

Gross advances and Profit Before Taxes classified as per RBI guidelines for segmental reporting (Basel II).

“Other Banking Operations Segment” (which includes Credit Cards, Third Party Product sales etc.) has been added to the Retail Segment

Business Mix

• Customer segments - main drivers of net revenues

• Well balanced loan mix between wholesale and retail segments

• Higher retail revenues partly offset by higher operating and credit costs

• Equally well positioned to grow both segments

`. Bn

`. Bn

`. Bn

0

1,500

3,000

2010 2011 2012

Retail Wholesale

0

1,250

2,500

2010 2011 2012

Retail Wholesale

0

50

100

2010 2011 2012

Retail Wholesale

Tracking the India Growth Story

Meeting Diverse Customers’ Needs

Unique Franchise in the Indian Banking Sector

Key Business Initiatives

Financial Highlights

Value Proposition

6

Contents

7

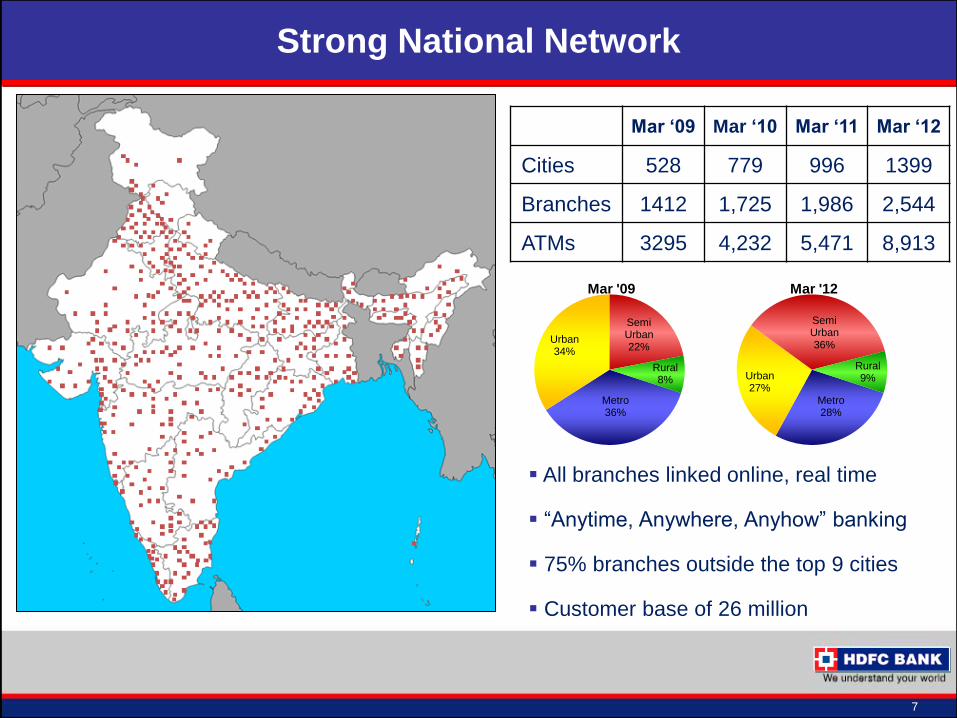

Strong National Network

All branches linked online, real time

“Anytime, Anywhere, Anyhow” banking

75% branches outside the top 9 cities

Customer base of 26 million

Branch classification

Mar ‘09 Mar ‘10 Mar ‘11 Mar ‘12

Cities 528 779 996 1399

Branches 1412 1,725 1,986 2,544

ATMs 3295 4,232 5,471 8,913

Metro 36%

Urban 34%

Semi Urban 22%

Rural 8%

Mar '09

Metro 28%

Urban 27%

Semi Urban 36%

Rural 9%

Mar '12

0

1500

3000

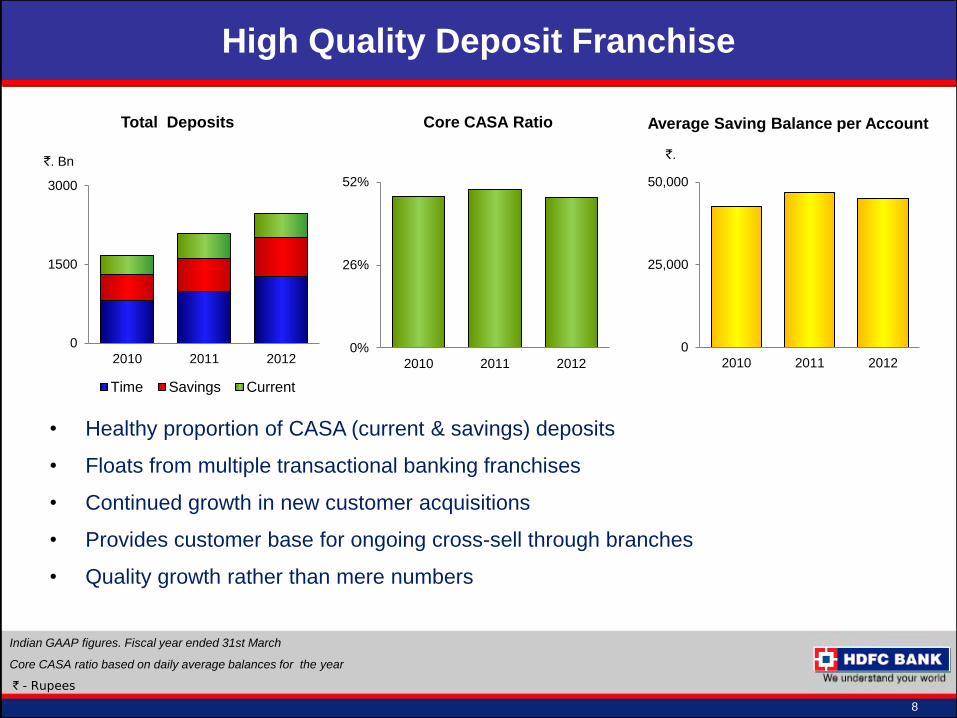

2010 2011 2012

Time Savings Current

Total Deposits

Core CASA Ratio

Average Saving Balance per Account

• Healthy proportion of CASA (current & savings) deposits

• Floats from multiple transactional banking franchises

• Continued growth in new customer acquisitions

• Provides customer base for ongoing cross-sell through branches

• Quality growth rather than mere numbers

`. Bn

Indian GAAP figures. Fiscal year ended 31st March

Core CASA ratio based on daily average balances for the year

` - Rupees

8

`.

High Quality Deposit Franchise

0%

26%

52%

2010 2011 2012

0

25,000

50,000

2010 2011 2012

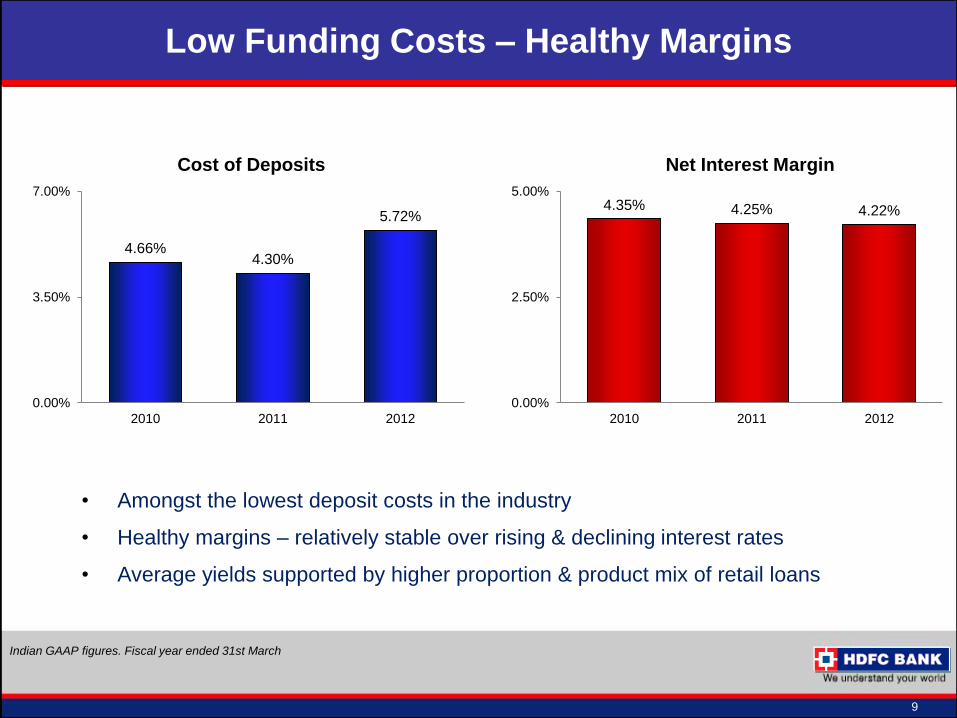

• Amongst the lowest deposit costs in the industry

• Healthy margins – relatively stable over rising & declining interest rates

• Average yields supported by higher proportion & product mix of retail loans

Indian GAAP figures. Fiscal year ended 31st March

9

Low Funding Costs – Healthy Margins

4.35% 4.25% 4.22%

0.00%

2.50%

5.00%

2010 2011 2012

Net Interest Margin

4.66% 4.30%

5.72%

0.00%

3.50%

7.00%

2010 2011 2012

Cost of Deposits

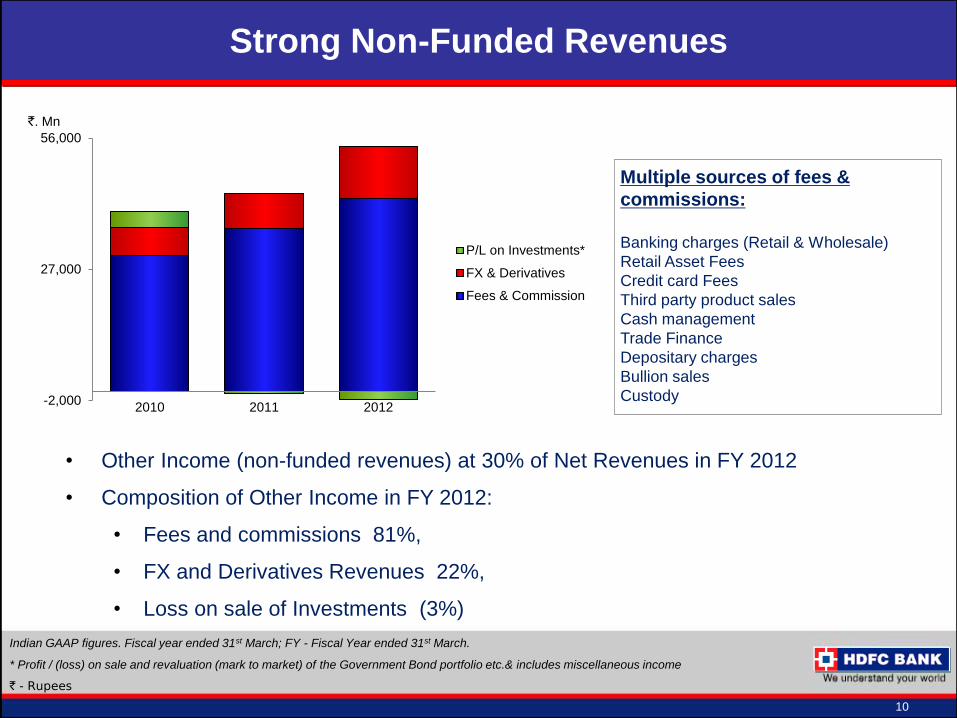

Indian GAAP figures. Fiscal year ended 31st March; FY - Fiscal Year ended 31st March.

* Profit / (loss) on sale and revaluation (mark to market) of the Government Bond portfolio etc.& includes miscellaneous income

` - Rupees

10

Strong Non-Funded Revenues

• Other Income (non-funded revenues) at 30% of Net Revenues in FY 2012

• Composition of Other Income in FY 2012:

• Fees and commissions 81%,

• FX and Derivatives Revenues 22%,

• Loss on sale of Investments (3%)

Multiple sources of fees &

commissions:

Banking charges (Retail & Wholesale)

Retail Asset Fees

Credit card Fees

Third party product sales

Cash management

Trade Finance

Depositary charges

Bullion sales

Custody

`. Mn

-2,000

27,000

56,000

2010 2011 2012

P/L on Investments*

FX & Derivatives

Fees & Commission

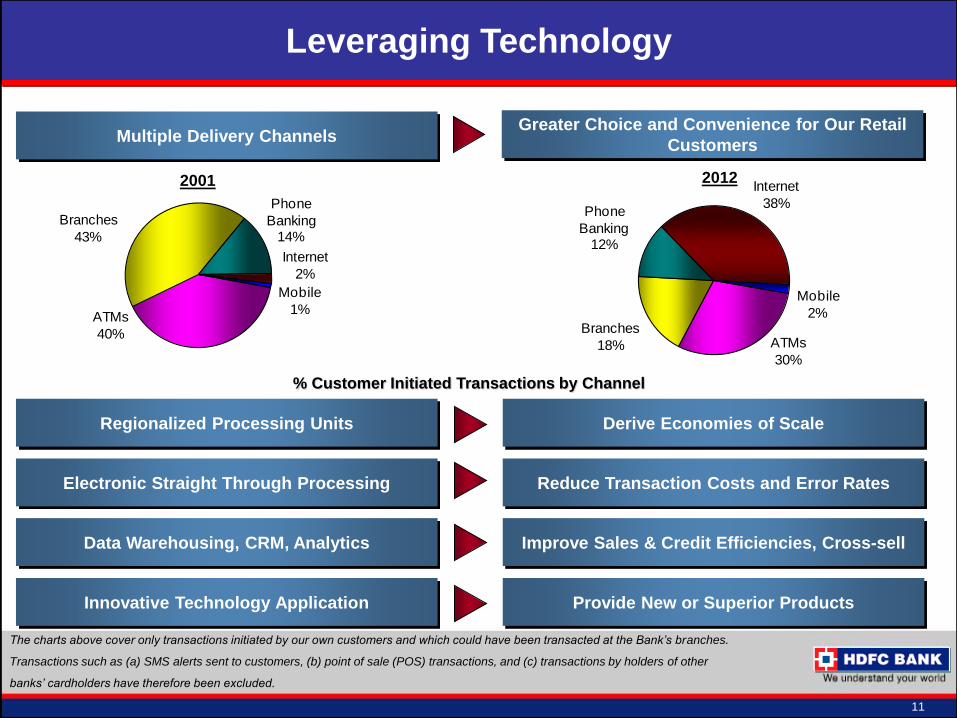

The charts above cover only transactions initiated by our own customers and which could have been transacted at the Bank‟s branches.

Transactions such as (a) SMS alerts sent to customers, (b) point of sale (POS) transactions, and (c) transactions by holders of other

banks‟ cardholders have therefore been excluded.

% Customer Initiated Transactions by Channel

ATMs

40%

Branches

43%

Phone

Banking14%

Internet

2%

Mobile

1%

2001

Multiple Delivery Channels Greater Choice and Convenience for Our Retail

Customers

Regionalized Processing Units Derive Economies of Scale

Electronic Straight Through Processing Reduce Transaction Costs and Error Rates

Data Warehousing, CRM, Analytics Improve Sales & Credit Efficiencies, Cross-sell

Innovative Technology Application Provide New or Superior Products

2012

11

Leveraging Technology

ATMs

30%

Branches

18%

Phone

Banking12%

Internet

38%

Mobile

2%

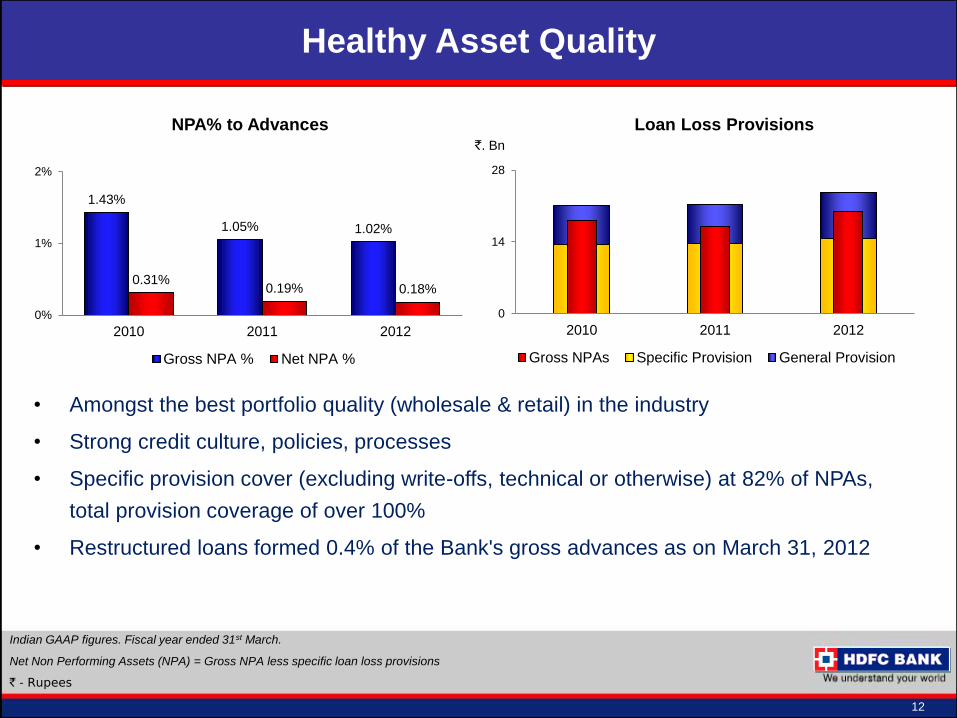

NPA% to Advances Loan Loss Provisions

`. Bn

• Amongst the best portfolio quality (wholesale & retail) in the industry

• Strong credit culture, policies, processes

• Specific provision cover (excluding write-offs, technical or otherwise) at 82% of NPAs,

total provision coverage of over 100%

• Restructured loans formed 0.4% of the Bank's gross advances as on March 31, 2012

Indian GAAP figures. Fiscal year ended 31st March.

Net Non Performing Assets (NPA) = Gross NPA less specific loan loss provisions

` - Rupees

12

Healthy Asset Quality

0

14

28

2010 2011 2012

Gross NPAs Specific Provision General Provision

1.43%

1.05% 1.02%

0.31% 0.19% 0.18%

0%

1%

2%

2010 2011 2012

Gross NPA % Net NPA %

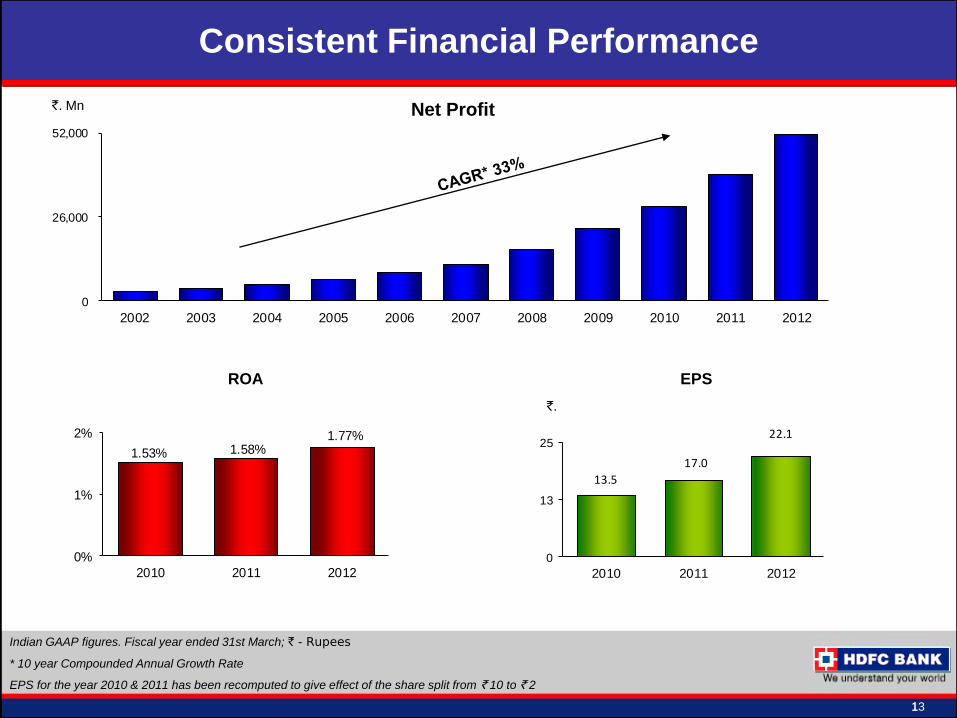

0

26,000

52,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Net Profit

13.5

17.0

22.1

0

13

25

2010 2011 2012

ROA

`. Mn

EPS

1.53% 1.58%1.77%

0%

1%

2%

2010 2011 2012

Indian GAAP figures. Fiscal year ended 31st March; ` - Rupees

* 10 year Compounded Annual Growth Rate

EPS for the year 2010 & 2011 has been recomputed to give effect of the share split from ` 10 to ` 2

1 13

Consistent Financial Performance

`.

Tracking the India Growth Story

Meeting Diverse Customers’ Needs

Unique Franchise in the Indian Banking Sector

Key Business Initiatives

Financial Highlights

Value Proposition

14

Contents

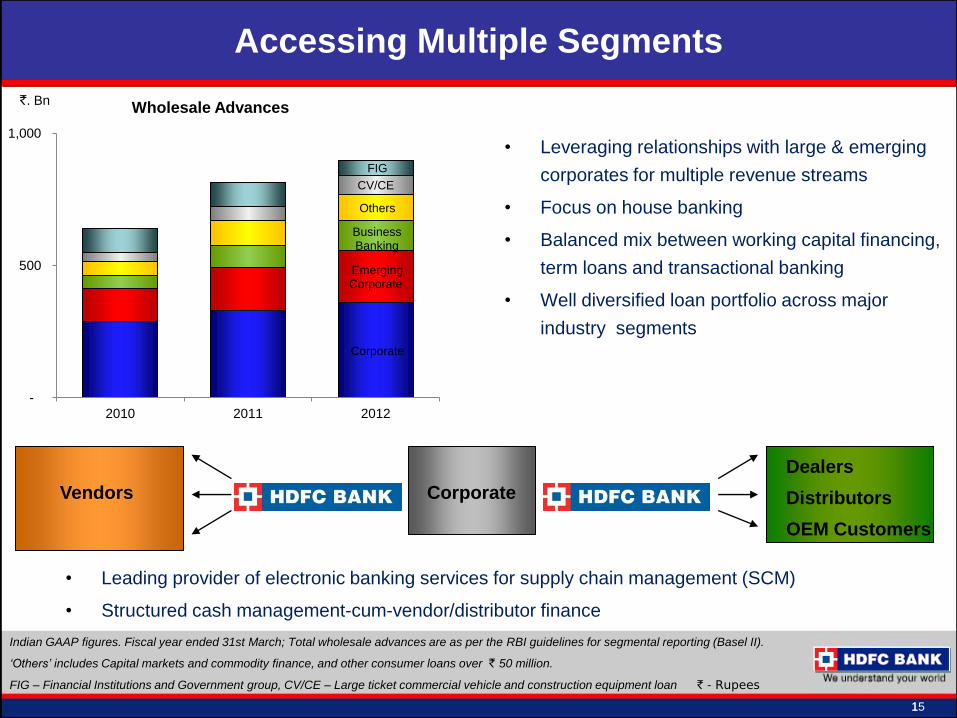

• Leading provider of electronic banking services for supply chain management (SCM)

• Structured cash management-cum-vendor/distributor finance

Corporate

Dealers

Distributors

OEM Customers

Vendors

`. Bn

Wholesale Advances

Indian GAAP figures. Fiscal year ended 31st March; Total wholesale advances are as per the RBI guidelines for segmental reporting (Basel II).

„Others‟ includes Capital markets and commodity finance, and other consumer loans over ` 50 million.

FIG – Financial Institutions and Government group, CV/CE – Large ticket commercial vehicle and construction equipment loan ` - Rupees

1 15

Accessing Multiple Segments

• Leveraging relationships with large & emerging

corporates for multiple revenue streams

• Focus on house banking

• Balanced mix between working capital financing,

term loans and transactional banking

• Well diversified loan portfolio across major

industry segments

Corporate

Emerging Corporate

Business Banking

Others

CV/CE

FIG

-

500

1,000

2010 2011 2012

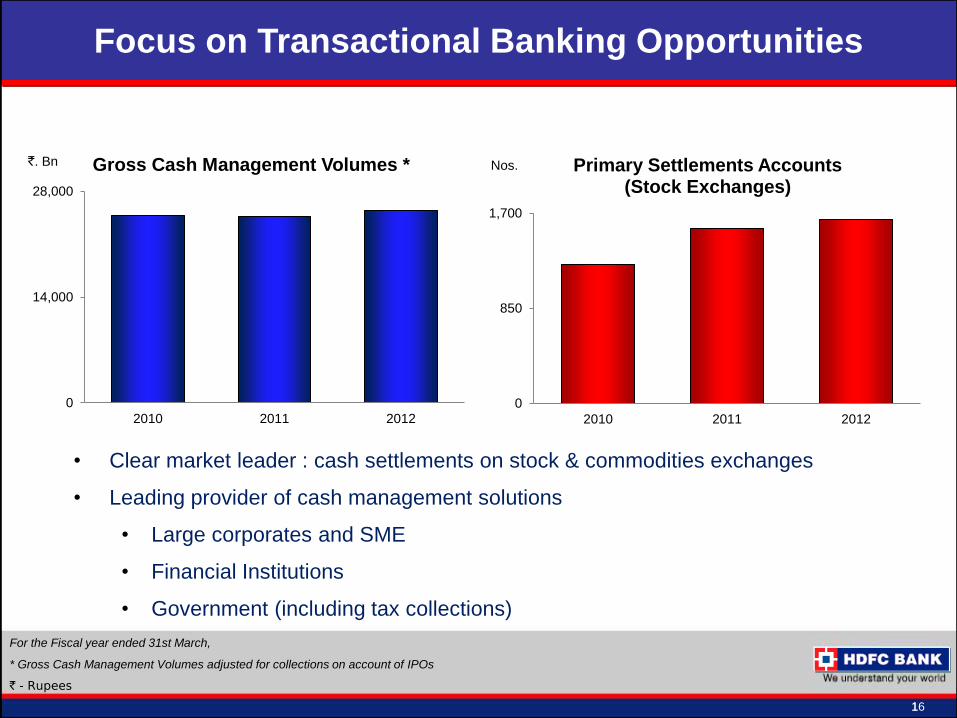

0

850

1,700

2010 2011 2012

Primary Settlements Accounts (Stock Exchanges)

0

14,000

28,000

2010 2011 2012

Gross Cash Management Volumes * Nos.

• Clear market leader : cash settlements on stock & commodities exchanges

• Leading provider of cash management solutions

• Large corporates and SME

• Financial Institutions

• Government (including tax collections)

For the Fiscal year ended 31st March,

* Gross Cash Management Volumes adjusted for collections on account of IPOs

` - Rupees

`. Bn

1 16

Focus on Transactional Banking Opportunities

0

6,000

12,000

2010 2011 2012

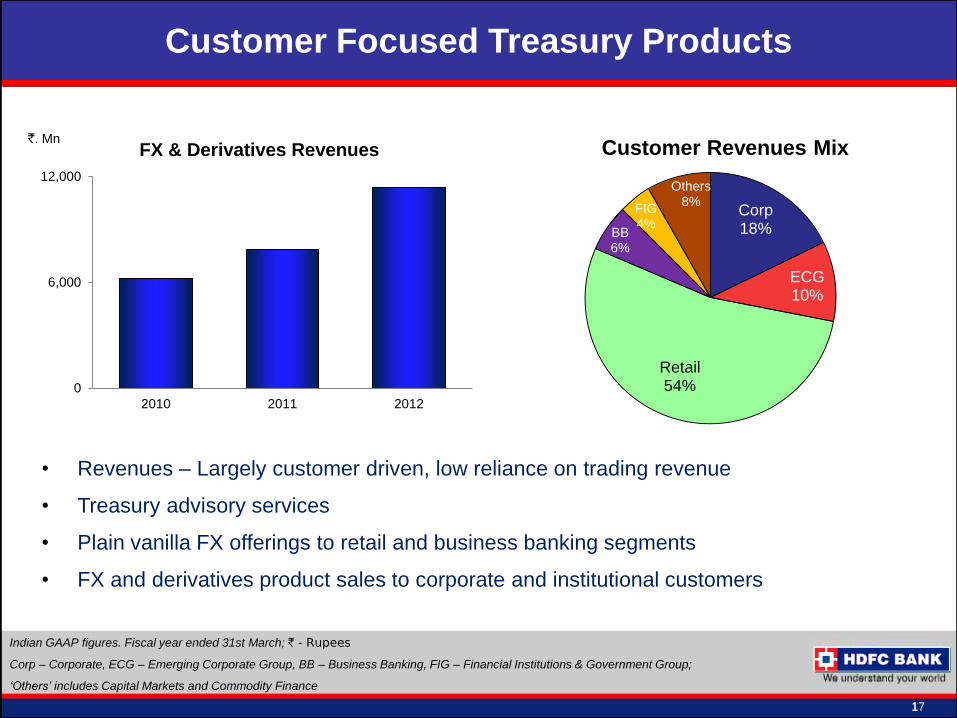

FX & Derivatives Revenues

• Revenues – Largely customer driven, low reliance on trading revenue

• Treasury advisory services

• Plain vanilla FX offerings to retail and business banking segments

• FX and derivatives product sales to corporate and institutional customers

Indian GAAP figures. Fiscal year ended 31st March; ` - Rupees

Corp – Corporate, ECG – Emerging Corporate Group, BB – Business Banking, FIG – Financial Institutions & Government Group;

„Others‟ includes Capital Markets and Commodity Finance

`. Mn

1 17

Customer Focused Treasury Products

Corp 18%

ECG 10%

Retail 54%

BB 6%

FIG 4%

Others 8%

Customer Revenues Mix

• Well diversified product mix

• Balancing volumes and market

share with margins and risk

• Home Loans* (Mortgage) offering

– origination (loan sanctions) now

around ` 8 Bn per month

• Loan losses within product pricing

parameters

`. Bn

Retail loans are net of loans sold and include loan assignments. Retail loans are classified as per RBI guidelines for segmental reporting (Basel II).

* In arrangement with HDFC Ltd., Others‟ includes Tractor Loans, Loans to Self Help Group, Retail overdrafts, Loans against Securities, etc

Indian GAAP figures. Fiscal year ended 31st March; ` - Rupees

1 18

Retail Loans – Profitable Growth

Auto Loans

Business Banking

Commercial Vehicles

Personal Loans

Home Loans

Others

Credit Cards

Gold Loans

Two Wheelers

0

600

1,200

2010 2011 2012

0

35

70

2010 2011 2012

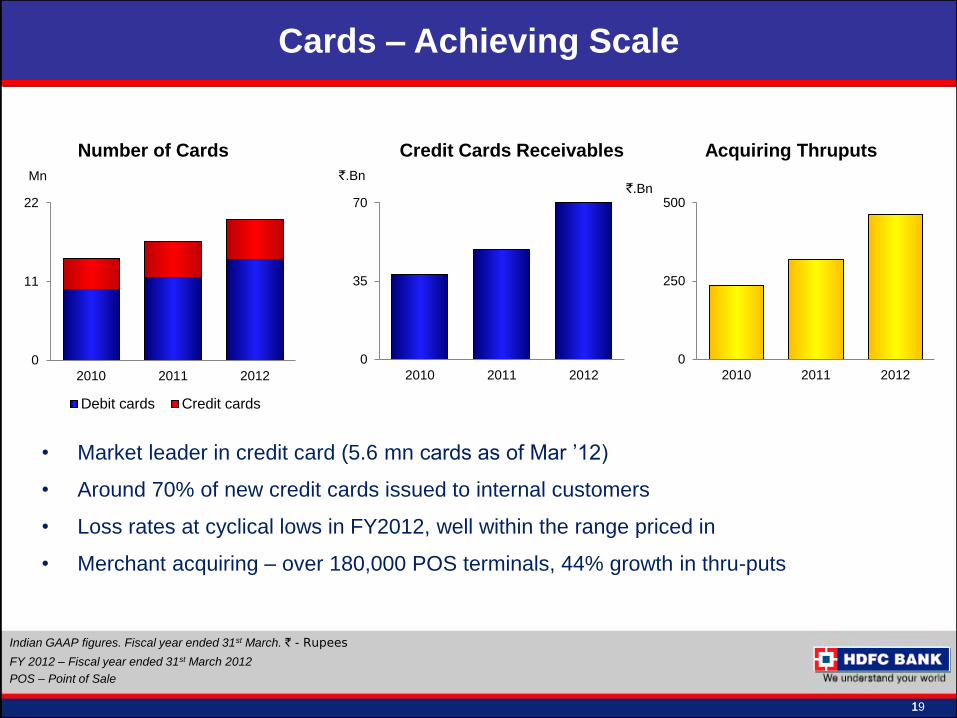

• Market leader in credit card (5.6 mn cards as of Mar ’12)

• Around 70% of new credit cards issued to internal customers

• Loss rates at cyclical lows in FY2012, well within the range priced in

• Merchant acquiring – over 180,000 POS terminals, 44% growth in thru-puts

Number of Cards Credit Cards Receivables Acquiring Thruputs

Indian GAAP figures. Fiscal year ended 31st March. ` - Rupees

FY 2012 – Fiscal year ended 31st March 2012

POS – Point of Sale

`.Bn `.Bn

Mn

1 19

Cards – Achieving Scale

0

11

22

2010 2011 2012

Debit cards Credit cards

0

250

500

2010 2011 2012

0

13

26

2010 2011 2012

Insurance Premium

Life General

0

600

1,200

2010 2011 2012

Mutual Fund Sales

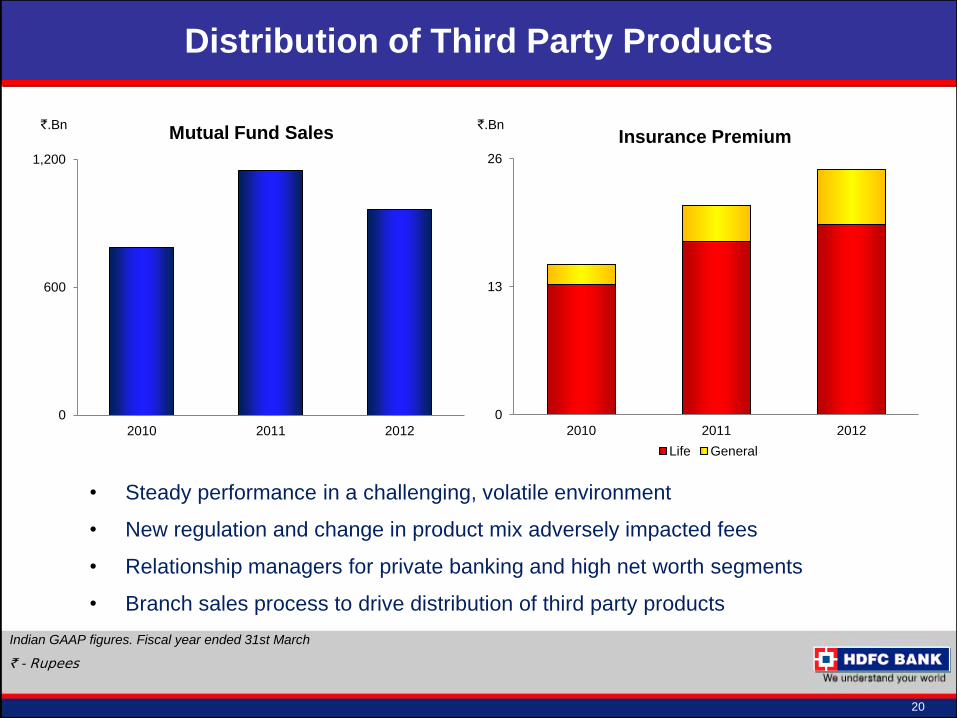

• Steady performance in a challenging, volatile environment

• New regulation and change in product mix adversely impacted fees

• Relationship managers for private banking and high net worth segments

• Branch sales process to drive distribution of third party products

Indian GAAP figures. Fiscal year ended 31st March

` - Rupees

20

Distribution of Third Party Products

`.Bn `.Bn

21

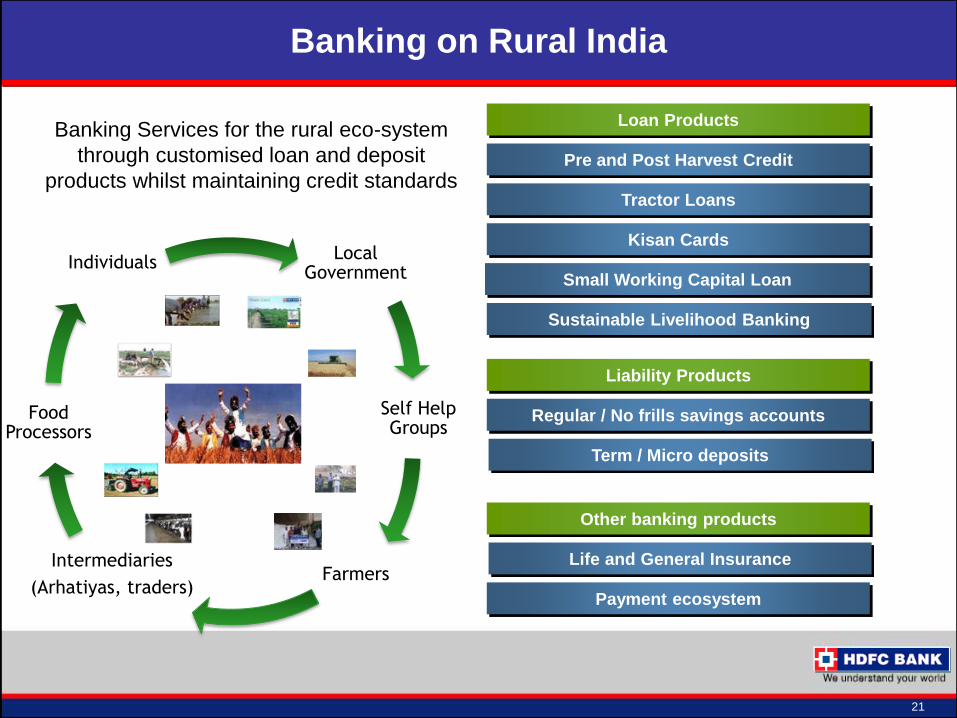

Banking on Rural India

Local Government

Self Help Groups

Farmers Intermediaries

(Arhatiyas, traders)

Food Processors

Individuals

Pre and Post Harvest Credit

Tractor Loans

Kisan Cards

Small Working Capital Loan

Regular / No frills savings accounts

Term / Micro deposits

Life and General Insurance

Payment ecosystem

Banking Services for the rural eco-system

through customised loan and deposit

products whilst maintaining credit standards

Other banking products

Liability Products

Sustainable Livelihood Banking

Loan Products

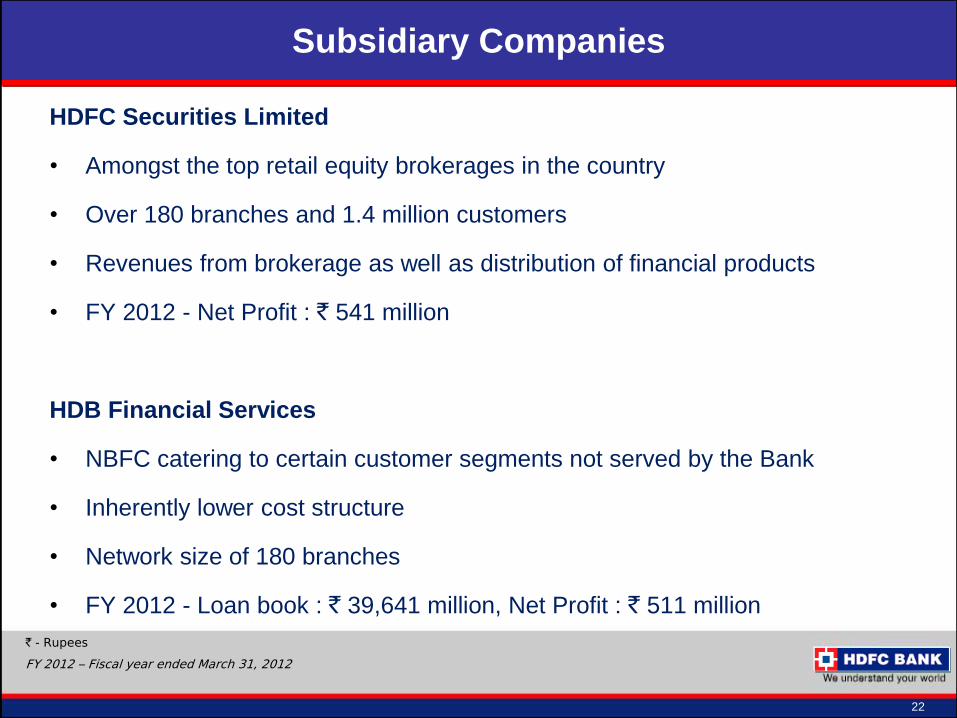

HDFC Securities Limited

• Amongst the top retail equity brokerages in the country

• Over 180 branches and 1.4 million customers

• Revenues from brokerage as well as distribution of financial products

• FY 2012 - Net Profit : ` 541 million

HDB Financial Services

• NBFC catering to certain customer segments not served by the Bank

• Inherently lower cost structure

• Network size of 180 branches

• FY 2012 - Loan book : ` 39,641 million, Net Profit : ` 511 million

22

Subsidiary Companies

` - Rupees

FY 2012 – Fiscal year ended March 31, 2012

Tracking the India Growth Story

Meeting Diverse Customers’ Needs

Unique Franchise in the Indian Banking Sector

Key Business Initiatives

Financial Highlights

Value Proposition

23

Contents

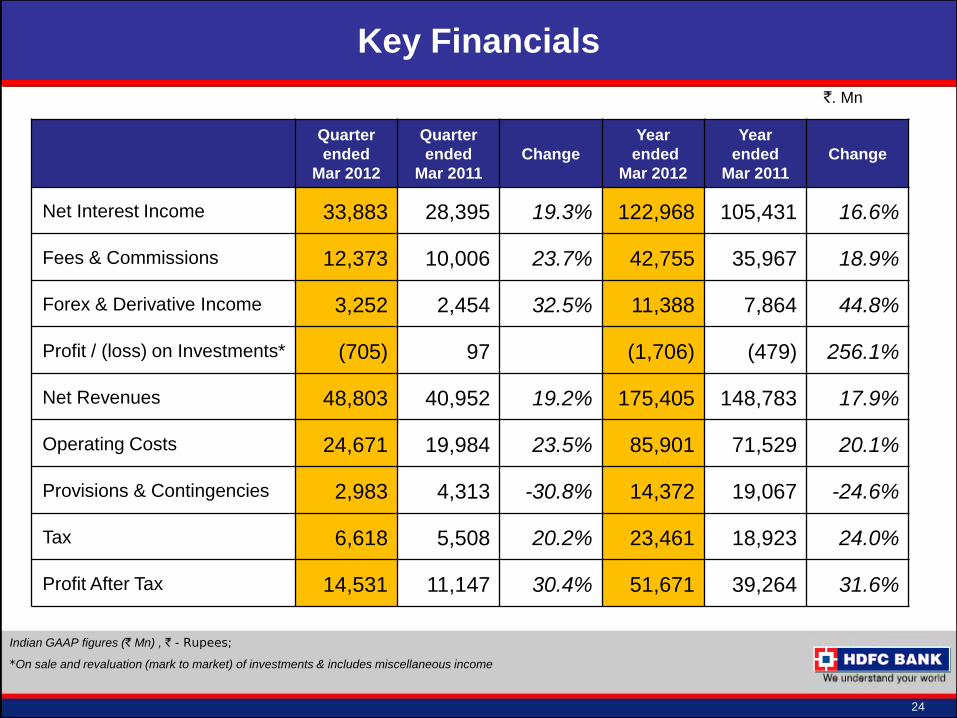

Indian GAAP figures (` Mn) , ` - Rupees;

*On sale and revaluation (mark to market) of investments & includes miscellaneous income

24

Key Financials

`. Mn

Quarter

ended

Mar 2012

Quarter

ended

Mar 2011

Change

Year

ended

Mar 2012

Year

ended

Mar 2011

Change

Net Interest Income 33,883 28,395 19.3% 122,968 105,431 16.6%

Fees & Commissions 12,373 10,006 23.7% 42,755 35,967 18.9%

Forex & Derivative Income 3,252 2,454 32.5% 11,388 7,864 44.8%

Profit / (loss) on Investments* (705) 97 (1,706) (479) 256.1%

Net Revenues 48,803 40,952 19.2% 175,405 148,783 17.9%

Operating Costs 24,671 19,984 23.5% 85,901 71,529 20.1%

Provisions & Contingencies 2,983 4,313 -30.8% 14,372 19,067 -24.6%

Tax 6,618 5,508 20.2% 23,461 18,923 24.0%

Profit After Tax 14,531 11,147 30.4% 51,671 39,264 31.6%

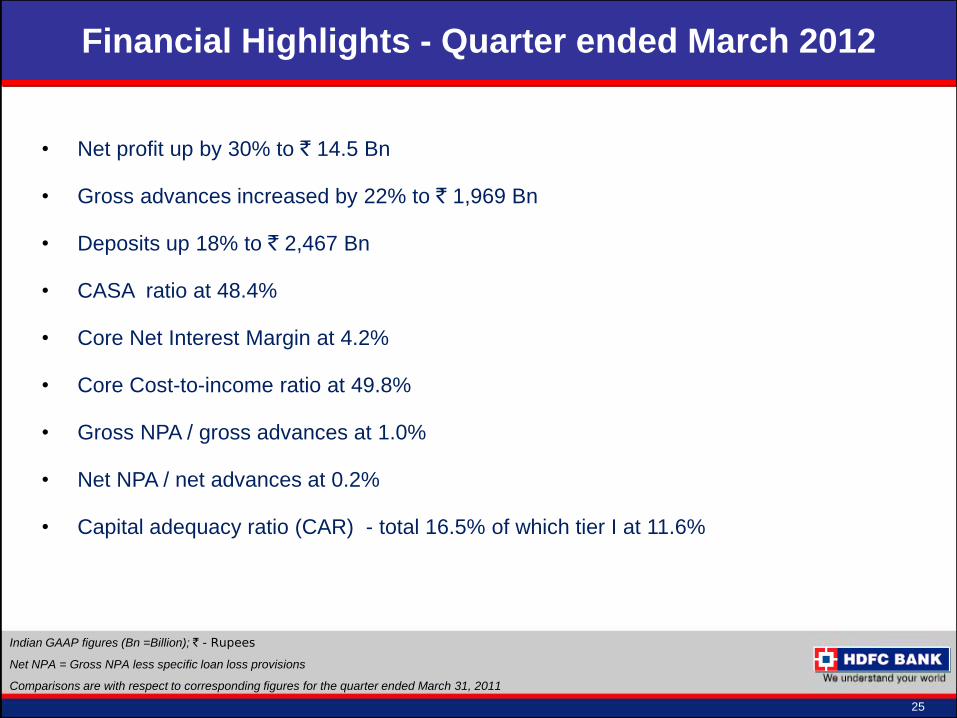

• Net profit up by 30% to ` 14.5 Bn

• Gross advances increased by 22% to ` 1,969 Bn

• Deposits up 18% to ` 2,467 Bn

• CASA ratio at 48.4%

• Core Net Interest Margin at 4.2%

• Core Cost-to-income ratio at 49.8%

• Gross NPA / gross advances at 1.0%

• Net NPA / net advances at 0.2%

• Capital adequacy ratio (CAR) - total 16.5% of which tier I at 11.6%

25

Indian GAAP figures (Bn =Billion); ` - Rupees

Net NPA = Gross NPA less specific loan loss provisions

Comparisons are with respect to corresponding figures for the quarter ended March 31, 2011

Financial Highlights - Quarter ended March 2012

Tracking the India Growth Story

Meeting Diverse Customers’ Needs

Unique Franchise in the Indian Banking Sector

Key Business Initiatives

Financial Highlights

Value Proposition

26

Contents

27

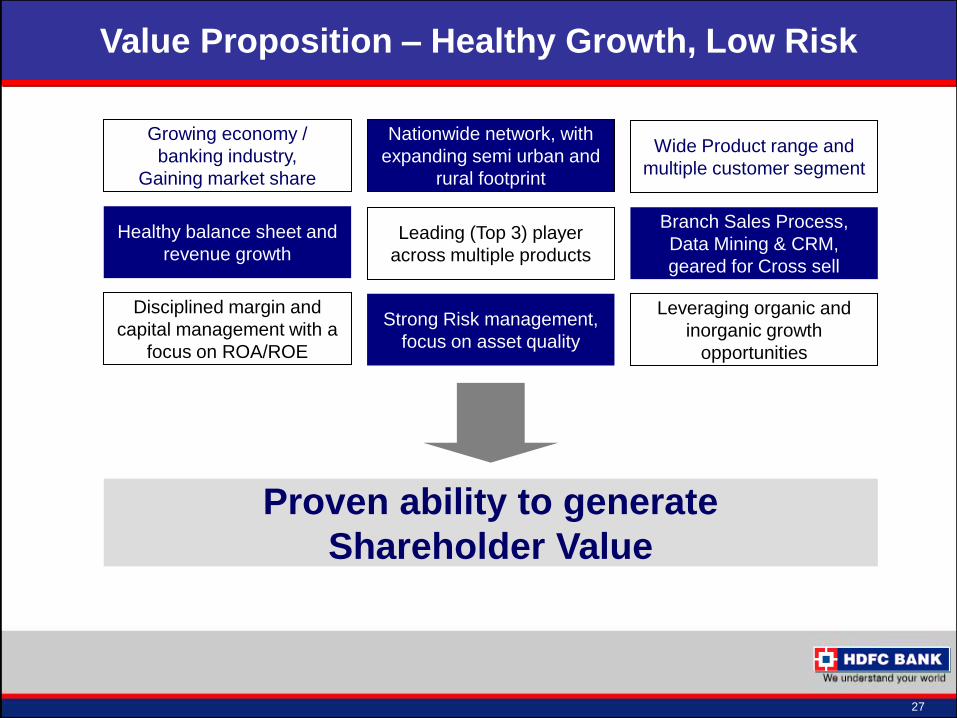

Value Proposition – Healthy Growth, Low Risk

Healthy balance sheet and

revenue growth

Leveraging organic and

inorganic growth

opportunities

Proven ability to generate

Shareholder Value

Branch Sales Process,

Data Mining & CRM,

geared for Cross sell

Strong Risk management,

focus on asset quality

Disciplined margin and

capital management with a

focus on ROA/ROE

Nationwide network, with

expanding semi urban and

rural footprint

Growing economy /

banking industry,

Gaining market share

Leading (Top 3) player

across multiple products

Wide Product range and

multiple customer segment

Certain statements are included in this release which contain words or phrases such as “will,” “aim,” “will likely

result,” “believe,” “expect,” “will continue,” “anticipate,” “estimate,” “intend,” “plan,” “contemplate,” “seek to,”

“future,” “objective,” “goal,” “project,” “should,” “will pursue” and similar expressions or variations of these

expressions that are “forward-looking statements.” Actual results may differ materially from those suggested by

the forward-looking statements due to certain risks or uncertainties associated with our expectations with respect

to, but not limited to, our ability to implement our strategy successfully, the market acceptance of and demand for

various banking services, future levels of our non-performing loans, our growth and expansion, the adequacy of

our allowance for credit and investment losses, technological changes, volatility in investment income, our ability

to market new products ,cash flow projections, our outcome of any legal, tax or regulatory proceedings in India

and in other jurisdictions we are or become a party to, the future impact of new accounting standards, our ability

to pay dividends, the impact of changes in banking regulations and other regulatory changes in India and other

jurisdictions on us, our ability to roll over our short-term funding sources and our exposure to market and

operational risks. By their nature, certain of the market risk disclosures are only estimates and could be materially

different from what may actually occur in the future. As a result, actual future gains, losses or impact on net

income could materially differ from those that have been estimated.

In addition, other factors that could cause actual results to differ materially from those estimated by the forward-

looking statements contained in this document include, but are not limited to: general economic and political

conditions in India and the other countries which have an impact on our business activities or investments; the

monetary and interest rate policies of the government of India; inflation, deflation, unanticipated turbulence in

interest rates, foreign exchange rates, equity prices or other rates or prices; the performance of the financial

markets in India and globally; changes in Indian and foreign laws and regulations, including tax, accounting and

banking regulations; changes in competition and the pricing environment in India; and regional or general

changes in asset valuations.