is coal to liquids fincially feasible in india

TRANSCRIPT

1

Is coal to liquids project financially feasible in

India?

2

TABLE OF CONTENT

Is coal to liquids project financially feasible in India? 1

Abstract 4

1. Introduction 6

2. Rationale for CTL in India 8

2.1. Growing crude oil prices vis-à-vis break-even CTL prices 8

2.2. Abundance of coal resources 8

2.3. Policy and fiscal support 9

2.4. Technology available for commercial scale CTL project 9

3. Case study of CTL project 10

3.1. Details of operations of SASOL 10

3.2. Financial analysis for SASOL 11

3.3. Capital cost estimates for CTL by world coal institute 15

4. CTL project conceptualization and financial analysis 16

4.1. Project conceptualisation 16

4.2. Financial analysis 18

4.3. Sensitivity to capital cost changes 21

4.4. Sensitivity to cost of production changes 21

4.5. Sensitivity on account of price of product changes 22

4.6. Sensitivity on account of carbon dioxide cost inclusion 22

5. Conclusion 24

6. Bibliography 25

6.1. Primary Sources 25

6.2. Secondary Source 26

TABLE OF TABLES

Table 1: SASOL’s CTL project summary ....................................................................................... 14

Table 2: CTL project conceptualization in India ............................................................................. 16

Table 3: Base case financial analysis for CTL project in India ....................................................... 19

Table 5: CCS Cost estimates ............................................................................................................ 23

3

TABLE OF FIGURES

Figure 1: Change in India’s primary energy mix (excluding bio-mass & waste) .............................. 6

Figure 2: Project price of crude oil vs. breakeven price of crude oil at which CTL is viable ........... 8

Figure 3: CTL product break-up of SASOL – 10 years average ..................................................... 10

Figure 4: SASOL’s CTL process at Secunda, South Africa ............................................................ 11

Figure 4: SASOL’s CTL product prices (average) vs global Brent prices ...................................... 12

Figure 6: SASOL’s CTL production cost structure ......................................................................... 13

Figure 6: Unconventional petroleum liquids capital investment ..................................................... 15

Figure 8: Benchmark gross refinery margin for Asian markets- Singapore Benchmark ................. 20

Figure 9: Changes in net revenue of Indian CTL project with capital cost changes ....................... 21

Figure 10: Changes in net revenue of Indian CTL project with changes in cost of production ...... 21

Figure 11: Changes in net revenue of Indian CTL project with product price changes .................. 22

Figure 12: Changes in net revenue of Indian CTL project with CCS cost ...................................... 22

4

Abstract

India needs to sustain it’s annual econmic growth rate around eight to ten percent which in turn is

dependent on availability of energy with lesser burden to economy. Liquid fuel availability could

be augumented through CTL technologies. This paper seeks to analyse the financial feasibility of

CTL projects in India by providing rationale of CTL projects followed by case study of successful

of CTL project in South Africa. Sensitivity of net revenue is presented with respect to changes in

capital costs, operating costs, product prices and application of carbon capture and sequestration.

Word Count: 2189

5

Abbreviations

BCOP Breakeven Crude Oil Price

bbl Barrel

BCF Billion cubic feet

bt Billion tons

CAGR Compounded Average Growth Rate

CCS Carbon Capture & Sequestration

CIL Coal India Limited

CMNA Coal Mines Nationalisation Act, 1973

CTL Coal to Liquids

DCL Direct Coal Liquefaction

DECC Department of Energy & Climate Change, Government of UK

DGH Directorate General of Hydrocarbons, Government of India

D&A Depreciation & Amortisation

FT Fisher-Tropsch

GDP Gross Domestic Product

GOI Government of India

ICL Indirect Coal Liquefaction

IEA International Energy Agency

INR Indian Rupee

ISP Indian Standard Procedure

MCL Mahanadi coalfields Limited

MDO Mine Developer and Operator

MoC Ministry of Coal. Government of India

MOPNG Ministry of Petroleum & Natural Gas, Government of India

Mtpa Million tons per annum

RBI Reserve Bank of India

6

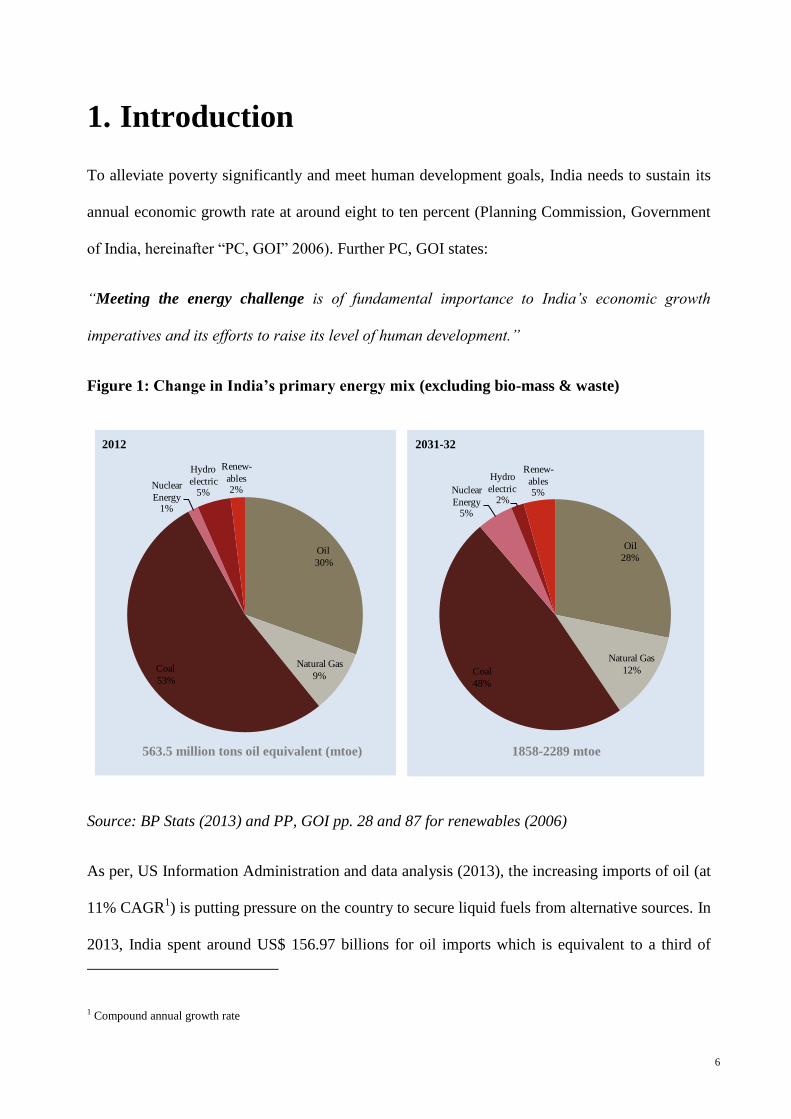

1. Introduction

To alleviate poverty significantly and meet human development goals, India needs to sustain its

annual economic growth rate at around eight to ten percent (Planning Commission, Government

of India, hereinafter “PC, GOI” 2006). Further PC, GOI states:

“Meeting the energy challenge is of fundamental importance to India’s economic growth

imperatives and its efforts to raise its level of human development.”

Figure 1: Change in India’s primary energy mix (excluding bio-mass & waste)

Source: BP Stats (2013) and PP, GOI pp. 28 and 87 for renewables (2006)

As per, US Information Administration and data analysis (2013), the increasing imports of oil (at

11% CAGR1) is putting pressure on the country to secure liquid fuels from alternative sources. In

2013, India spent around US$ 156.97 billions for oil imports which is equivalent to a third of

1 Compound annual growth rate

Oil

30%

Natural Gas

9%Coal

53%

Nuclear

Energy1%

Hydro

electric5%

Renew-

ables2%

2012

Oil

28%

Natural Gas

12%Coal

48%

Nuclear

Energy5%

Hydro

electric2%

Renew-

ables5%

2031-32

563.5 million tons oil equivalent (mtoe) 1858-2289 mtoe

7

India’s total import bill (Indian Express, 2013). Further as per EIA, India’s proven oil reserves

may exhaust in next 21 years with current production rate. So, India may look for producing

liquids fuels from coal by using Coal to Liquids (CTL) technologies.

This paper seeks to analyse the financial feasibility of CTL projects in India. The second chapter

provides the rationale for CTL projects. This is followed by case study on success of CTL project

in South Africa and then by financial feasibility of CTL project in India in fourth chapter. Fifth

chapter presents conclusion.

8

2. Rationale for CTL in India

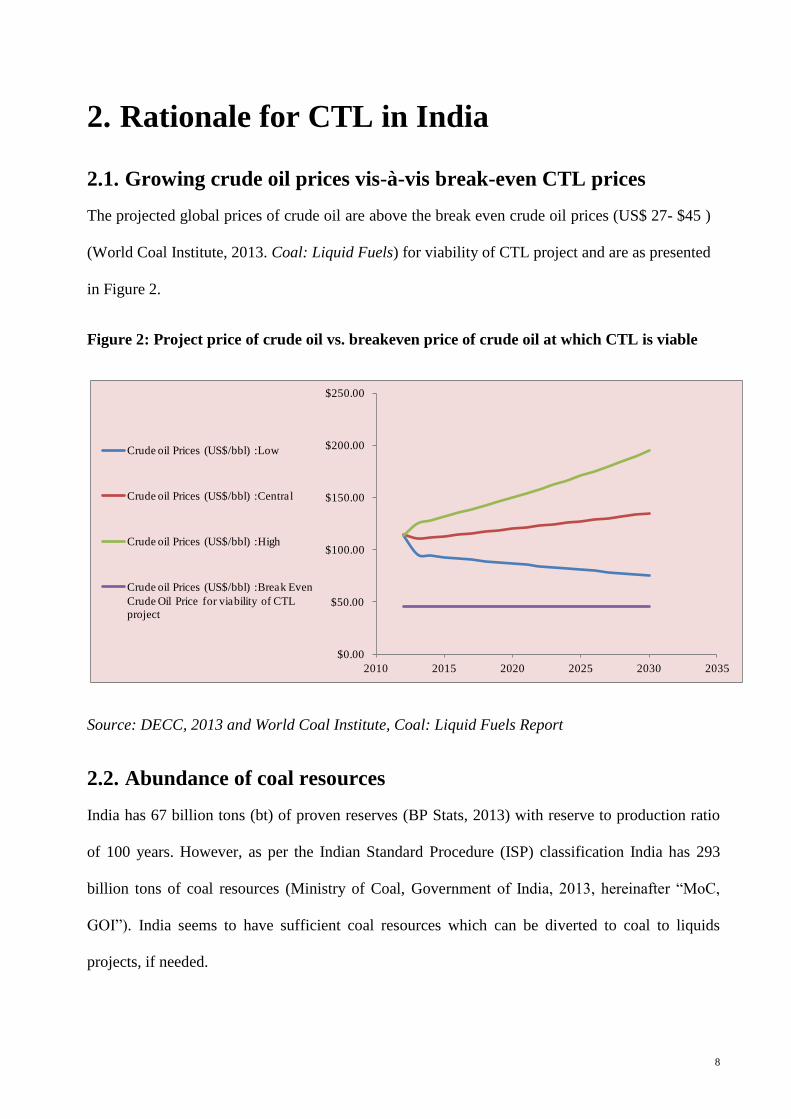

2.1. Growing crude oil prices vis-à-vis break-even CTL prices

The projected global prices of crude oil are above the break even crude oil prices (US$ 27- $45 )

(World Coal Institute, 2013. Coal: Liquid Fuels) for viability of CTL project and are as presented

in Figure 2.

Figure 2: Project price of crude oil vs. breakeven price of crude oil at which CTL is viable

Source: DECC, 2013 and World Coal Institute, Coal: Liquid Fuels Report

2.2. Abundance of coal resources

India has 67 billion tons (bt) of proven reserves (BP Stats, 2013) with reserve to production ratio

of 100 years. However, as per the Indian Standard Procedure (ISP) classification India has 293

billion tons of coal resources (Ministry of Coal, Government of India, 2013, hereinafter “MoC,

GOI”). India seems to have sufficient coal resources which can be diverted to coal to liquids

projects, if needed.

$0.00

$50.00

$100.00

$150.00

$200.00

$250.00

2010 2015 2020 2025 2030 2035

Crude oil Prices (US$/bbl) :Low

Crude oil Prices (US$/bbl) :Central

Crude oil Prices (US$/bbl) :High

Crude oil Prices (US$/bbl) :Break Even

Crude Oil Price for viability of CTL

project

9

2.3. Policy and fiscal support

Coal to liquids is recognised end-use for captive consumption of coal: The Section 3 (3)

(a) (iii) of amended Coal Mines Nationalisation Act, 1973 (CMNA) (MoC, GOI)

provides for captive mining by entities engaged in surface & underground coal

gasification and CTL in India from July 12, 2007 (PIB, GOI)

Foreign Direct Investment (FDI) of 100% in coal sector: Coal mining sector allows

100% of FDI in captive mining projects (Reserve Bank of India, 2012).

2.4. Technology available for commercial scale CTL project

There are two different CTL technologies - direct coal liquefaction (DCL) and indirect coal

liquefaction (ICL). In DCL technology, partially synthetic crude is produced from coal which is

further refined to produce synthetic diesel, gasoline, LPG etc. In ICL technologies, firstly coal is

gassified to produce synthetic gas, and then syngas is used to produce synthetic fuels. (Williams,

R.H. and Larson, E. D., 2003). It may be important to note that

1. As per Williams et al (2003, pp 103), ICL is a commercially proven technology.

2. Sasol Synfuels (Pty) Ltd (SASOL) in South Africa operates the only commercial CTL

projet based on ICL technology.

3. PC, GOI (2006, pp 63 and 105) recommends establishing CTL plant on SASOL’s

technology for domestic coal on commercial scale.

4. Further, Williams et al (2003, pp 117 ) indicate that the green house gas (GHG)

management may be an anciliary benefit of using ICL technologies.

Based on above facts, in favour of ICL technology, the paper analyses financial feasibility of a

typical CTL project in India based on ICL technology. However, to build-up assumptions

SASOL’s CTL operations in analysed and presented in next chapter.

10

3. Case study of CTL project

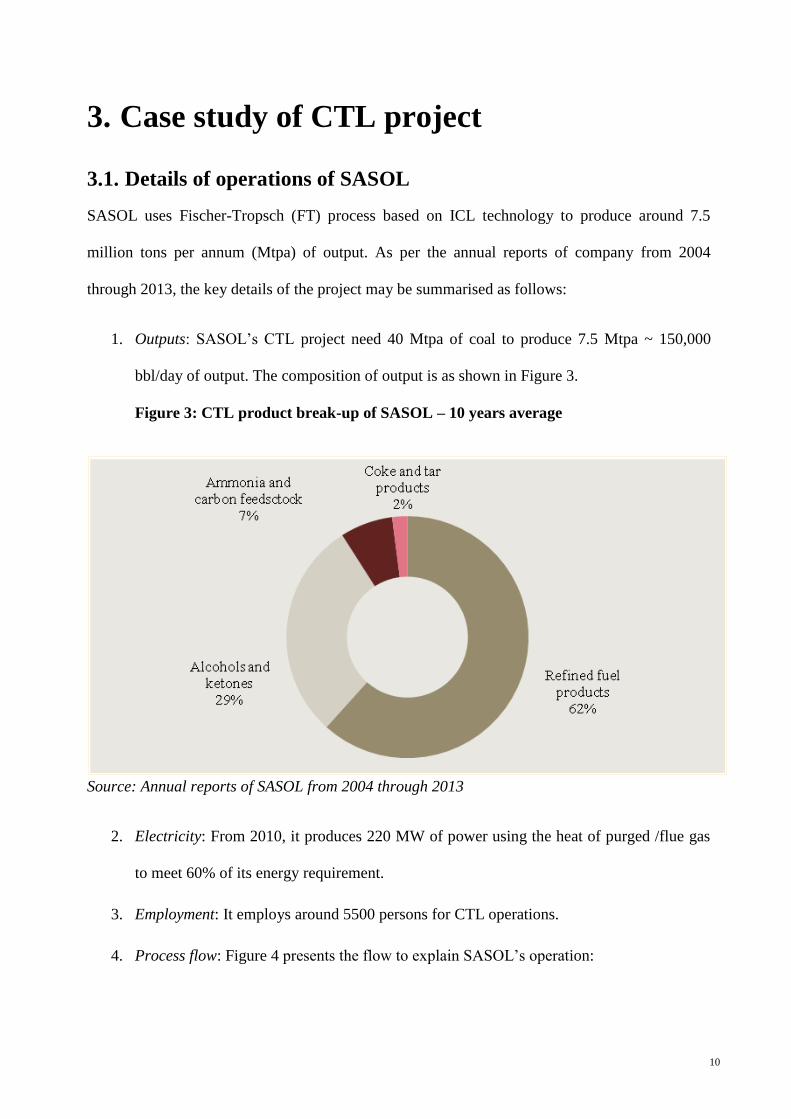

3.1. Details of operations of SASOL

SASOL uses Fischer-Tropsch (FT) process based on ICL technology to produce around 7.5

million tons per annum (Mtpa) of output. As per the annual reports of company from 2004

through 2013, the key details of the project may be summarised as follows:

1. Outputs: SASOL’s CTL project need 40 Mtpa of coal to produce 7.5 Mtpa ~ 150,000

bbl/day of output. The composition of output is as shown in Figure 3.

Figure 3: CTL product break-up of SASOL – 10 years average

Source: Annual reports of SASOL from 2004 through 2013

2. Electricity: From 2010, it produces 220 MW of power using the heat of purged /flue gas

to meet 60% of its energy requirement.

3. Employment: It employs around 5500 persons for CTL operations.

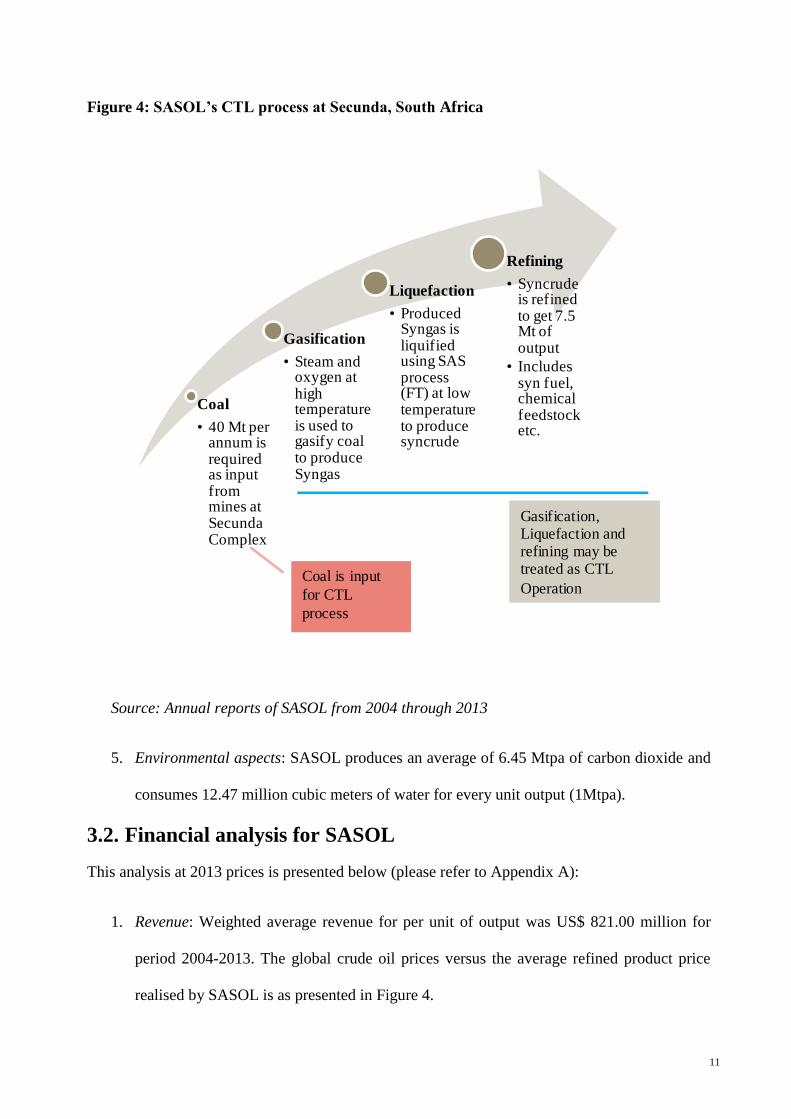

4. Process flow: Figure 4 presents the flow to explain SASOL’s operation:

11

Figure 4: SASOL’s CTL process at Secunda, South Africa

Source: Annual reports of SASOL from 2004 through 2013

5. Environmental aspects: SASOL produces an average of 6.45 Mtpa of carbon dioxide and

consumes 12.47 million cubic meters of water for every unit output (1Mtpa).

3.2. Financial analysis for SASOL

This analysis at 2013 prices is presented below (please refer to Appendix A):

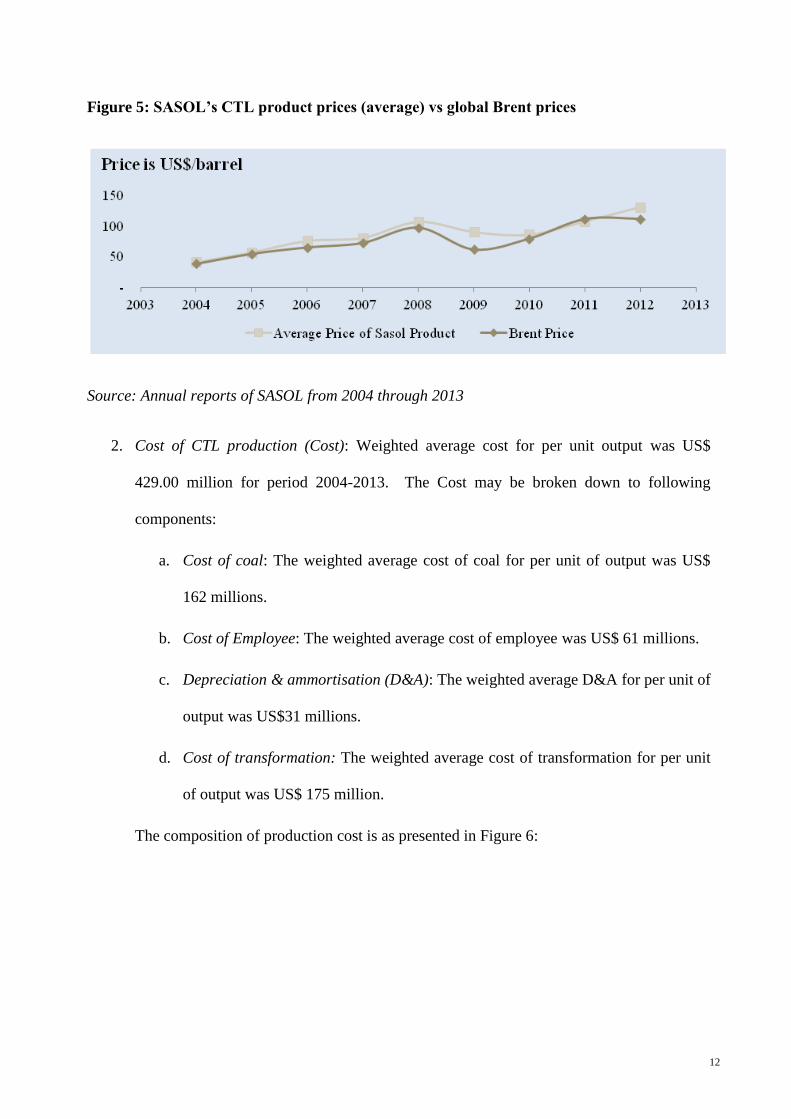

1. Revenue: Weighted average revenue for per unit of output was US$ 821.00 million for

period 2004-2013. The global crude oil prices versus the average refined product price

realised by SASOL is as presented in Figure 4.

Coal

• 40 Mt per annum is required as input from mines at Secunda Complex

Gasification

• Steam and oxygen at high temperature is used to gasify coal to produce Syngas

Liquefaction

• Produced Syngas is liquified using SAS process (FT) at low temperature to produce syncrude

Refining

• Syncrude is refined to get 7.5 Mt of output

• Includes syn fuel, chemical feedstock etc.

Gasification, Liquefaction and refining may be treated as CTL

Operation Coal is input

for CTL

process

12

Figure 5: SASOL’s CTL product prices (average) vs global Brent prices

Source: Annual reports of SASOL from 2004 through 2013

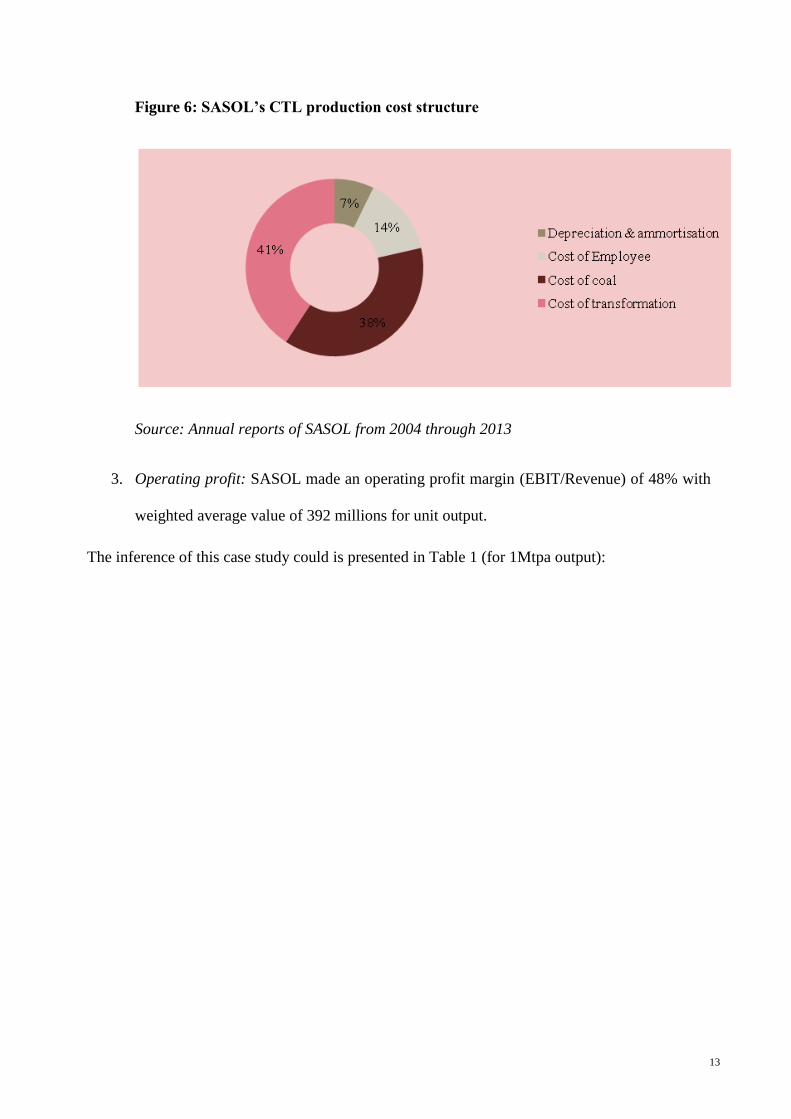

2. Cost of CTL production (Cost): Weighted average cost for per unit output was US$

429.00 million for period 2004-2013. The Cost may be broken down to following

components:

a. Cost of coal: The weighted average cost of coal for per unit of output was US$

162 millions.

b. Cost of Employee: The weighted average cost of employee was US$ 61 millions.

c. Depreciation & ammortisation (D&A): The weighted average D&A for per unit of

output was US$31 millions.

d. Cost of transformation: The weighted average cost of transformation for per unit

of output was US$ 175 million.

The composition of production cost is as presented in Figure 6:

13

Figure 6: SASOL’s CTL production cost structure

Source: Annual reports of SASOL from 2004 through 2013

3. Operating profit: SASOL made an operating profit margin (EBIT/Revenue) of 48% with

weighted average value of 392 millions for unit output.

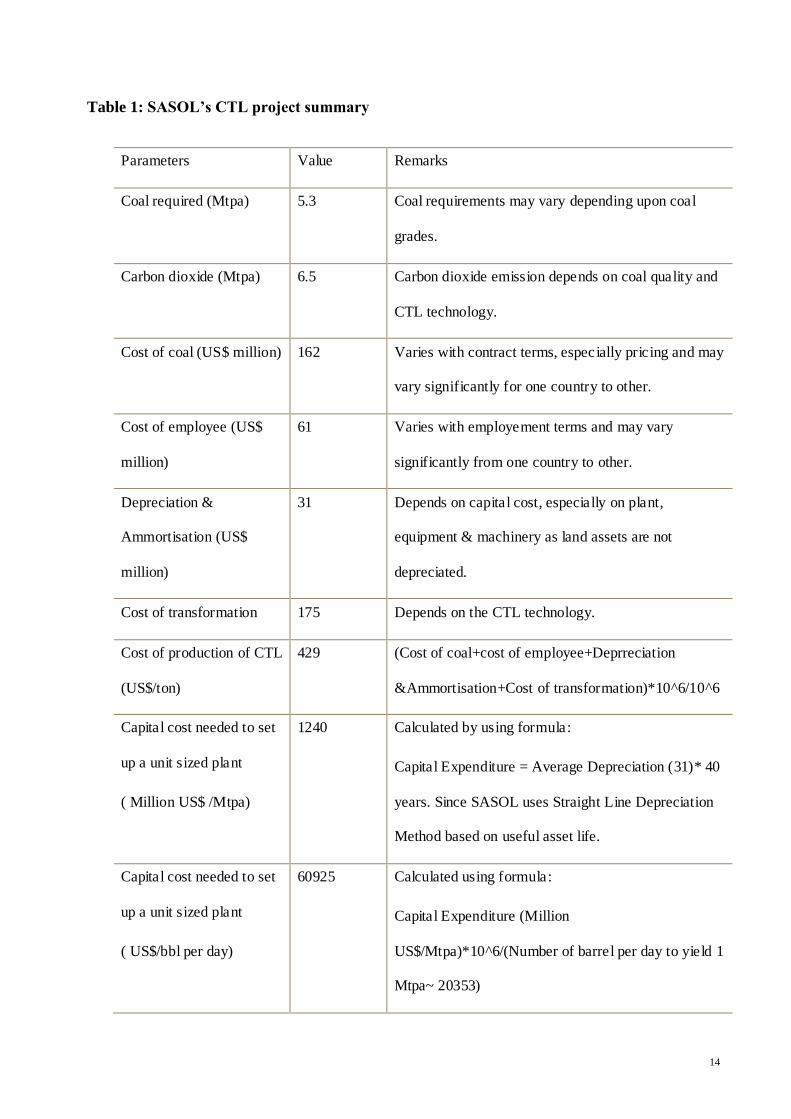

The inference of this case study could is presented in Table 1 (for 1Mtpa output):

14

Table 1: SASOL’s CTL project summary

Parameters Value Remarks

Coal required (Mtpa) 5.3 Coal requirements may vary depending upon coal

grades.

Carbon dioxide (Mtpa) 6.5 Carbon dioxide emission depends on coal quality and

CTL technology.

Cost of coal (US$ million) 162 Varies with contract terms, especially pricing and may

vary significantly for one country to other.

Cost of employee (US$

million)

61 Varies with employement terms and may vary

significantly from one country to other.

Depreciation &

Ammortisation (US$

million)

31 Depends on capital cost, especially on plant,

equipment & machinery as land assets are not

depreciated.

Cost of transformation 175 Depends on the CTL technology.

Cost of production of CTL

(US$/ton)

429 (Cost of coal+cost of employee+Deprreciation

&Ammortisation+Cost of transformation)*10^6/10^6

Capital cost needed to set

up a unit sized plant

( Million US$ /Mtpa)

1240 Calculated by using formula:

Capital Expenditure = Average Depreciation (31)* 40

years. Since SASOL uses Straight Line Depreciation

Method based on useful asset life.

Capital cost needed to set

up a unit sized plant

( US$/bbl per day)

60925 Calculated using formula:

Capital Expenditure (Million

US$/Mtpa)*10^6/(Number of barrel per day to yield 1

Mtpa~ 20353)

15

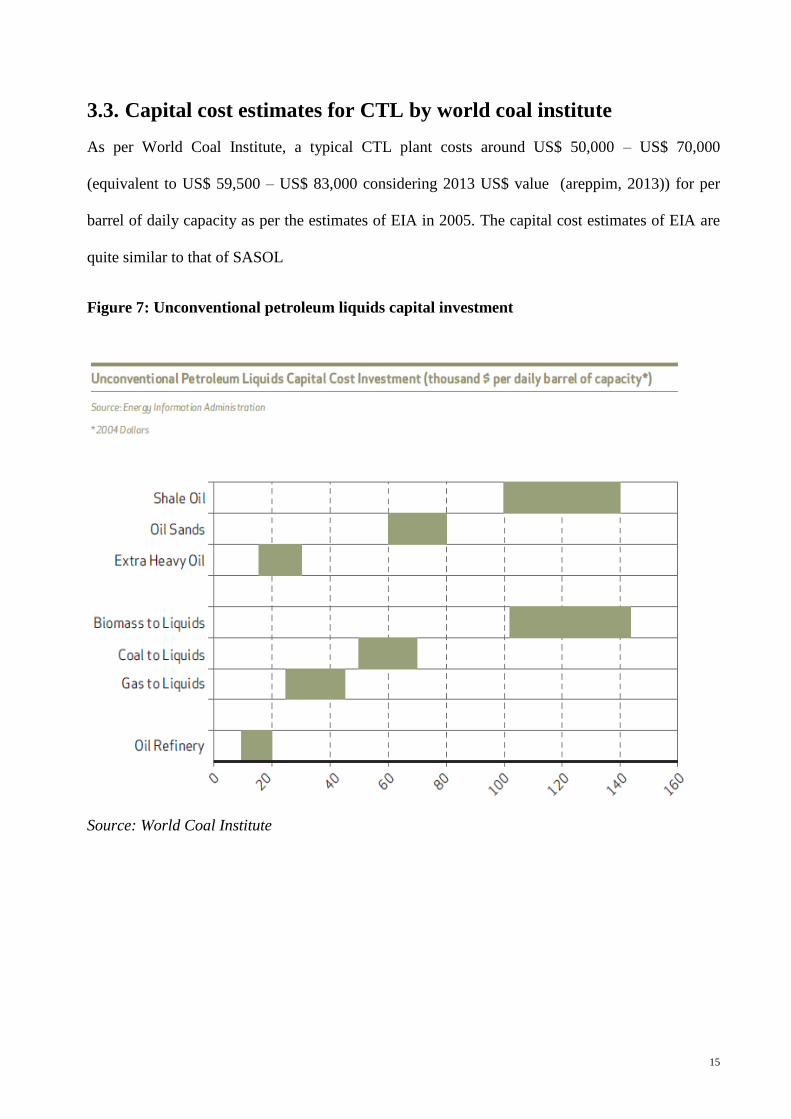

3.3. Capital cost estimates for CTL by world coal institute

As per World Coal Institute, a typical CTL plant costs around US$ 50,000 – US$ 70,000

(equivalent to US$ 59,500 – US$ 83,000 considering 2013 US$ value (areppim, 2013)) for per

barrel of daily capacity as per the estimates of EIA in 2005. The capital cost estimates of EIA are

quite similar to that of SASOL

Figure 7: Unconventional petroleum liquids capital investment

Source: World Coal Institute

16

4. CTL project conceptualization and

financial analysis

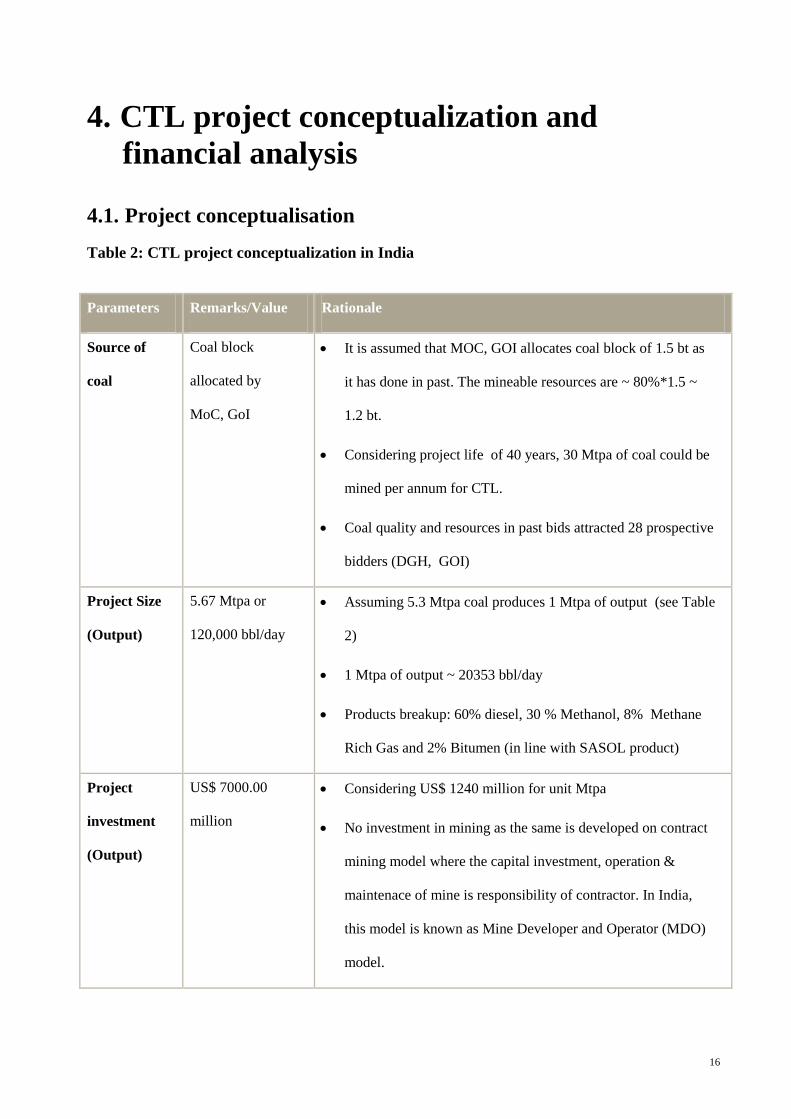

4.1. Project conceptualisation

Table 2: CTL project conceptualization in India

Parameters Remarks/Value Rationale

Source of

coal

Coal block

allocated by

MoC, GoI

It is assumed that MOC, GOI allocates coal block of 1.5 bt as

it has done in past. The mineable resources are ~ 80%*1.5 ~

1.2 bt.

Considering project life of 40 years, 30 Mtpa of coal could be

mined per annum for CTL.

Coal quality and resources in past bids attracted 28 prospective

bidders (DGH, GOI)

Project Size

(Output)

5.67 Mtpa or

120,000 bbl/day

Assuming 5.3 Mtpa coal produces 1 Mtpa of output (see Table

2)

1 Mtpa of output ~ 20353 bbl/day

Products breakup: 60% diesel, 30 % Methanol, 8% Methane

Rich Gas and 2% Bitumen (in line with SASOL product)

Project

investment

(Output)

US$ 7000.00

million

Considering US$ 1240 million for unit Mtpa

No investment in mining as the same is developed on contract

mining model where the capital investment, operation &

maintenace of mine is responsibility of contractor. In India,

this model is known as Mine Developer and Operator (MDO)

model.

17

Parameters Remarks/Value Rationale

Revenue per

annum

US$ 4571.82 Average price of all products is US$ 115.45/bbl (=60%*Price

of Diesel+30%*Price of Methanol+8%*Price of Methane Rich

gas+2%*Price of Bitumen).

Price of Diesel: US$ 142.99/bbl (Ministry of Petroleum &

Natural Gas (MOPNG) 2013; 2006-2013 average)

Price of Methanol: US$ 51.25/bbl (Methanex, 2013; 2006-

2013 average)

Price of Methane Rich gas: US$ 121.87/bbl (MOPNG, 2013;

2006-2013 average; price assumed to be price of LPG)

Price of Bitument: US$ 226.64/bbl (MOPNG, 2013; 2006-

2013 average)

Operating

Cost per

annum

US$ 1666.15

millions

Cost of Transformation = US$ 992.25 million, (5.67*175, 175

is transformation cost considering commercial model of

SASOL (see Table 2)

Cost of Coal: US$ 593.90 million, Present prices are around

US$ 19.80/ton (MCL, 2013 and RBI @ Exchange Rate 1

US$= INR62.40 ) for 4300 to 4600 kcal/kg grade.

Cost of Employee: US$ 80.00 million, Considering 5000

persons with average salary of INR 1 million2 (CIL, 2013)

each.

2 This is about 40% more than the average salary offered to a Coal India Limited (CIL) employee. This is calculated by dividing

annual average total cost (of CIL is last three financial years – 2011, 2012 and 2013) for salaries, wages & employee benefits with

total number of employees of CIL.

18

Parameters Remarks/Value Rationale

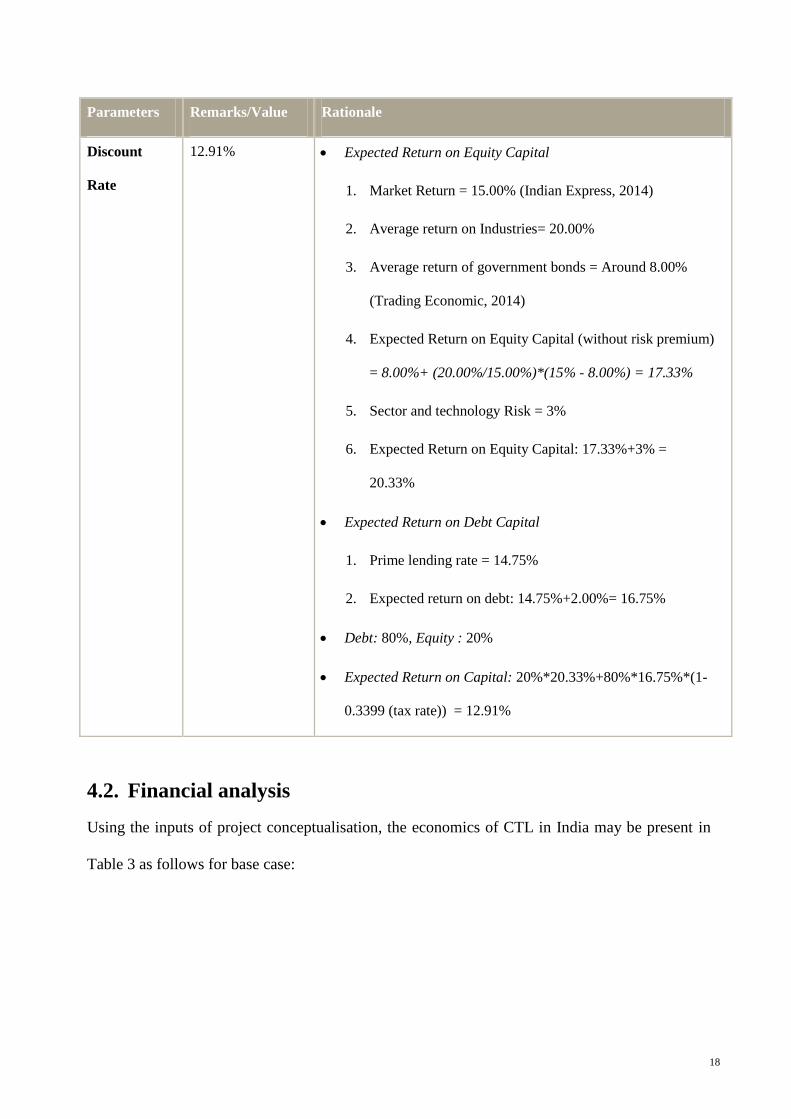

Discount

Rate

12.91% Expected Return on Equity Capital

1. Market Return = 15.00% (Indian Express, 2014)

2. Average return on Industries= 20.00%

3. Average return of government bonds = Around 8.00%

(Trading Economic, 2014)

4. Expected Return on Equity Capital (without risk premium)

= 8.00%+ (20.00%/15.00%)*(15% - 8.00%) = 17.33%

5. Sector and technology Risk = 3%

6. Expected Return on Equity Capital: 17.33%+3% =

20.33%

Expected Return on Debt Capital

1. Prime lending rate = 14.75%

2. Expected return on debt: 14.75%+2.00%= 16.75%

Debt: 80%, Equity : 20%

Expected Return on Capital: 20%*20.33%+80%*16.75%*(1-

0.3399 (tax rate)) = 12.91%

4.2. Financial analysis

Using the inputs of project conceptualisation, the economics of CTL in India may be present in

Table 3 as follows for base case:

19

Table 3: Base case financial analysis for CTL project in India

1. Break-even Crude Oil Price( BCOP): It is the price of crude oil above which the CTL

project is viable. It is given by following relation:

BCOP = Average cost of refined product – average refinery margin

The average refinery margin for Asian market is captured at bechmark gross refinery

margin (GRM) in Singapore. The trend is shown in Figure 8. The average GRM is US$

3.00 per barrel since 1992. However, Indian refineries have displayed GRM of around

US$10-$11 per barrel as well (DNA, 2013).

Base Case Scenario

CTL plant technical details

Total product output (bbl/day) 120,000

CTL cost

Capital cost ($) $7,000,000,000

Interest rate 12.91%

Annual amortized capital cost ($) -$910,781,379

Annual operating cost ($) -$1,666,150,000

Average total cost ($/bbl) -$65.07

Cost at CTL plant mouth -$65

CTL Revenue

Price of product ($/bbl) 115.45

Total annual product outout (bbl) 39,600,000

Total annual average Revenue $4,571,820,000

CTL Net Revenue $1,994,888,621

20

Figure 8: Benchmark gross refinery margin for Asian markets- Singapore

Benchmark

Source: Refinery Margin, BP Statistical Review, 2013

BCOP for India = $65.00 – ($3.00-$11.00) ~ $54.00-$62

2. Analysis of the finding:

a. The CTL project seems to be feasible as per the conceptualised project details.

b. Average cost of CTL product is US$ 65.00 per barrel.

c. Net revenue per annum is US$ 1.99 billions.

d. Operating profit margin = 44%

21

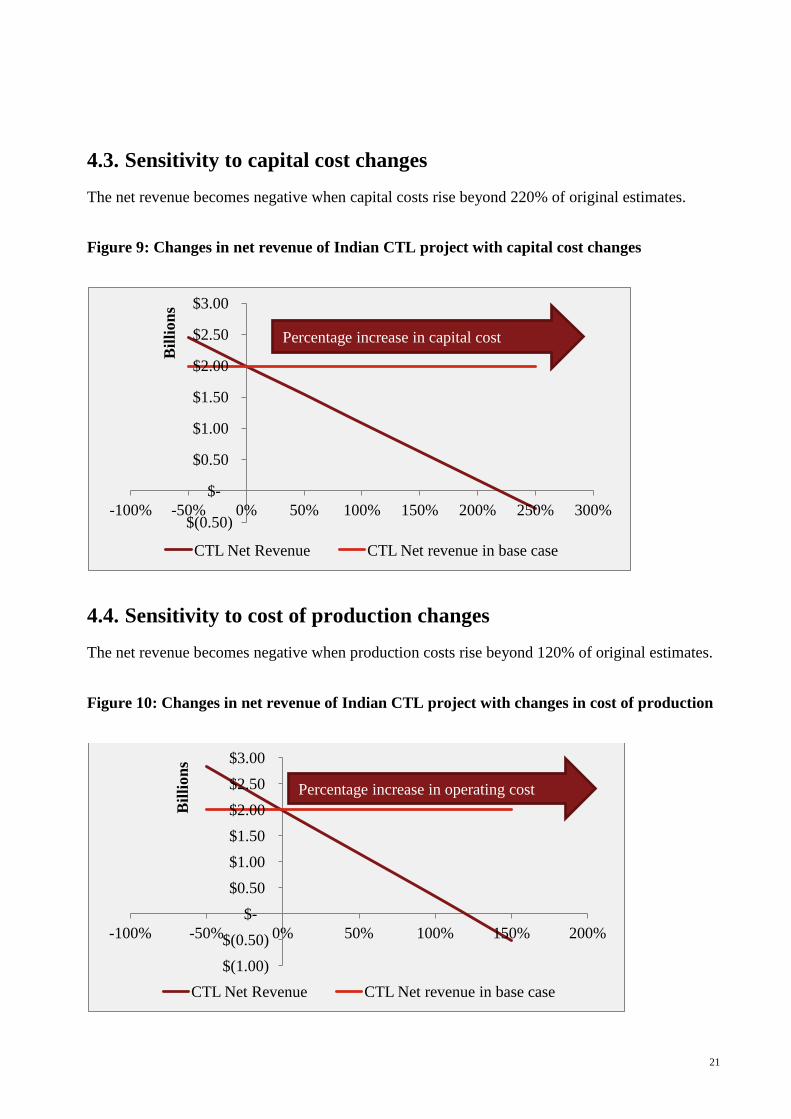

4.3. Sensitivity to capital cost changes

The net revenue becomes negative when capital costs rise beyond 220% of original estimates.

Figure 9: Changes in net revenue of Indian CTL project with capital cost changes

4.4. Sensitivity to cost of production changes

The net revenue becomes negative when production costs rise beyond 120% of original estimates.

Figure 10: Changes in net revenue of Indian CTL project with changes in cost of production

$(0.50)

$-

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

-100% -50% 0% 50% 100% 150% 200% 250% 300%

Bil

lion

s

CTL Net Revenue CTL Net revenue in base case

Percentage increase in capital cost

$(1.00)

$(0.50)

$-

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

-100% -50% 0% 50% 100% 150% 200%

Bil

lion

s

CTL Net Revenue CTL Net revenue in base case

Percentage increase in operating cost

22

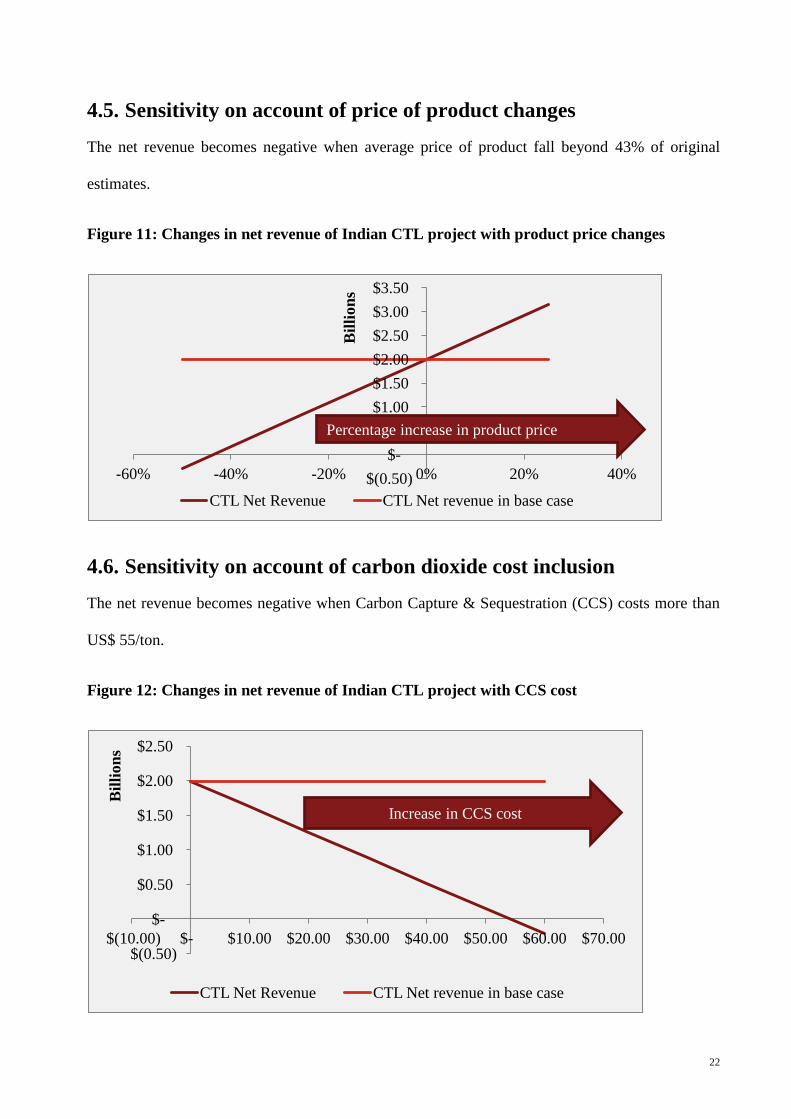

4.5. Sensitivity on account of price of product changes

The net revenue becomes negative when average price of product fall beyond 43% of original

estimates.

Figure 11: Changes in net revenue of Indian CTL project with product price changes

4.6. Sensitivity on account of carbon dioxide cost inclusion

The net revenue becomes negative when Carbon Capture & Sequestration (CCS) costs more than

US$ 55/ton.

Figure 12: Changes in net revenue of Indian CTL project with CCS cost

$(0.50)

$-

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

-60% -40% -20% 0% 20% 40%

Bil

lion

s

CTL Net Revenue CTL Net revenue in base case

Percentage increase in product price

$(0.50)

$-

$0.50

$1.00

$1.50

$2.00

$2.50

$(10.00) $- $10.00 $20.00 $30.00 $40.00 $50.00 $60.00 $70.00

Bil

lion

s

CTL Net Revenue CTL Net revenue in base case

Increase in CCS cost

23

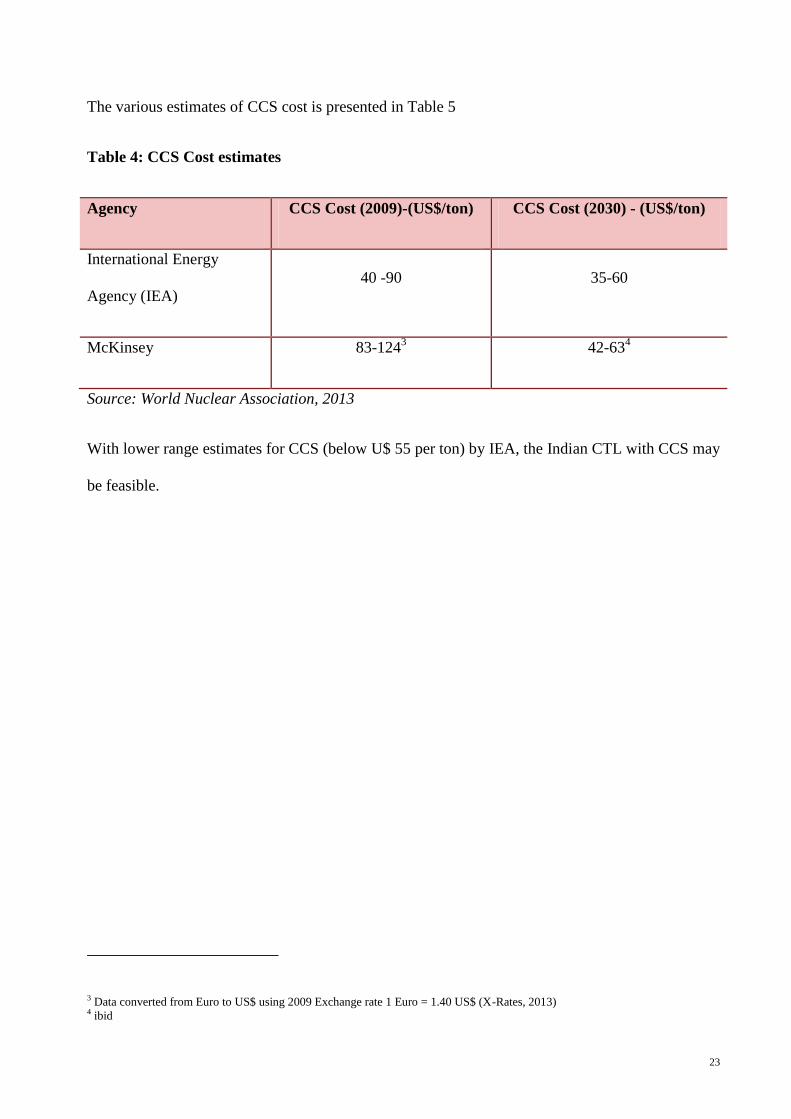

The various estimates of CCS cost is presented in Table 5

Table 4: CCS Cost estimates

Agency CCS Cost (2009)-(US$/ton) CCS Cost (2030) - (US$/ton)

International Energy

Agency (IEA)

40 -90 35-60

McKinsey 83-1243 42-63

4

Source: World Nuclear Association, 2013

With lower range estimates for CCS (below U$ 55 per ton) by IEA, the Indian CTL with CCS may

be feasible.

3 Data converted from Euro to US$ using 2009 Exchange rate 1 Euro = 1.40 US$ (X-Rates, 2013) 4 ibid

24

5. Conclusion

The financial viability of CTL project in India is dependent on many factors including the reserve

& grade of coal, global prices of crude oil, CCS and structure & method of financing. With present

regulatory regime for coal block allocation for CTL projects, projected global crude oil prices,

CTL projects with ICL technologies is financially viable in India. Further, when CCS is added at

later stages, the viability of project may be ensured by suitable floor pricing.

25

6. Bibliography

6.1. Primary Sources

Coal India Limited, 2013. Company-wise manpower for the month of november-2013:

Performance, [e-document], Available at: <https://www.coalindia.in/Performance.aspx?tab=0>

[Accessed on 04 January 2014]

Mahanadi Coalfields Limited, 2014: Price of different grade of non-coking coal, Available at:

< http://www.mcl.gov.in/Business/Files/Coal_price.pdf> [Accessed 04 January 2014]

Ministry of Coal, Government of India, Department of Coal: Acts & Notifications Government

of India, 2013. [online], Available at: < http://coal.nic.in/acts.htm> [Accessed 01 January

2014]

Ministry of Finance, Government of India, 2012. Budget 2012-2013 Speech of Pranab

Mukherjee, Minister of Finance March 16, 2012 [e-document], Available at:

http://indiabudget.nic.in/budget2012-2013/ub2012-13/bs/bs.pdf> [Accessed 01 January2014].

Planning Commission, Government of India, 2006. Integrated Energy Policy: Report of Expert

Committee, pp Overview -viii, Available at: <

http://planningcommission.gov.in/reports/genrep/rep_intengy.pdf> [Accessed 31 December

2013]

26

Reserve bank of India, 2012. Foreign Investment in India - Sector Specific conditions, Circular

No. 137 [e-document], Available at:

http://rbidocs.rbi.org.in/rdocs/notification/PDFs/CAPFISS280612.pdf> [Accessed 01

January2014].

Sasol Limited , 2013. Annual Integrated reports, Form 20-F and Analysts Handbook [e-

documents], Available at:

<http://www.sasol.co.za/investor-centre/publications/integrated-report-1>

<http://www.sasol.co.za/investor-centre/publications/archive/integrated-report>

<http://www.sasol.co.za/investor-centre/publications/form-20-f>

<http://www.sasol.co.za/investor-centre/publications/archive/form-20-f-1>

<http://www.sasol.co.za/investor-centre/publications/interim-financial-results-and-analyst-

book>

<http://www.sasol.co.za/investor-centre/publications/archive/interim-financial-results-and-

analyst-book>

[Accessed 01 January2014].

6.2. Secondary Source

6.2.1. Articles

Areppim, 2013, Current to Real Dollars Converter (using GDP deflator), Available at: <

http://stats.areppim.com/calc/calc_usdlrxdeflator.php> [Accessed 03 January 2014].

27

British Petroleum, 2013. Refinery Margin, Historical Data: Statistical Review of World Energy

2013: [online], Available at: < http://www.bp.com/en/global/corporate/about-bp/energy-

economics/statistical-review-of-world-energy-2013/review-by-energy-type/oil/refinery-

margins.html> [Accessed 06 January 2013].

Methanex, 2014: Methanol Price, [online] Available at: <

http://www.methanex.com/products/methanolprice.html> [Accessed 04 January 2014]

Ministry of Petroleum & Natural Gas, 2013, Indian Petroleum & Natural Gas Statistics: 2012-13,

[e-document] Available at: <http://petroleum.nic.in/pngstat.pdf> [Accessed 04 January 2014]

Coal India Limited, 2013. Annual Report 2013, [e-document], pp 26 Available at: <

http://www.coalindia.in/Documents/Coal_India_AR_Mail_2012_-_2013_06082013.pdf>

[Accessed on 04 January 2014]

X-RATES. Monthly Average, 2009 [online], Available at: < http://www.x-

rates.com/average/?from=EUR&to=USD&amount=1.00&year=2009> [Accessed on 04 January

2014]

DNA India, 2013. Refining margins may have just peaked out [online], Available at: <

http://www.dnaindia.com/money/report-refining-margins-may-have-just-peaked-out-1797943>

[Accessed 06 January 2013].

28

Press Information Bureau, Government of India, 2013, Seven coal blocks identified for

underground coal gasification [online] Available at : <

http://pib.nic.in/newsite/erelease.aspx?relid=101118> [ Accessed 1 January 2014].

Reserve Bank of India, 2014: Exchange Rates, [online] Available at: <

http://www.rbi.org.in/home.aspx#> [Accessed 04 January 2014]

Sinha G., Roy, A., 2009, Coal to Liquids: Clean Fuel Technology: Petroview, DGH, Government

of India, Volume 2, No. 1, [e-document], Available at: <

http://www.dghindia.org/pdf/AprilPDF09.pdf> [Accessed 03 January 2014]

The Indian Express, 2013: Sensex valuations mean long-term return expectation of 15%: PWC,

[online] Available at: < http://www.indianexpress.com/news/sensex-valuations-mean-longterm-

return-expectation-of-15--pwc/1102320/> [Accessed 04 January 2014]

Trading Economics, 2013: INDIA GOVERNMENT BOND 10Y, [online] Available at:

<http://www.tradingeconomics.com/india/government-bond-yield> [Accessed 04 January 2014]

World Nuclear Association, 2013. "Clean Coal" Technologies, Carbon Capture & Sequestration,

[online], Available at: < http://www.world-nuclear.org/info/Energy-and-Environment/-Clean-

Coal--Technologies/> [Accessed on 04 January 2014]

29

Wiliams, R. H., Larson., E.D., 2003. A comparison of direct and indirect liquefaction technologies

for making fluid fuels from coal, Energy for Sustainable Development, Volume VII No.,

Bangalore, India

6.2.2. Online Knowledge Repositories

British Petroleum, 2013. Historical data workbook: Statistical Review of World Energy 2013:

[online], Available at: < http://www.bp.com/en/global/corporate/about-bp/energy-

economics/statistical-review-of-world-energy-2013.html> [Accessed 31 December 2013].

U.S. Energy information Administration, 2013. Independent Statistics & Analysis [online],

Available at: < http://www.eia.gov/countries/> [Accessed 27 December 2013]. (hereinafter “EIA”)

World Bank, 2013, Inflation, GDP Deflator (annual %), [online], Available at:

http://data.worldbank.org/indicator/NY.GDP.DEFL.KD.ZG> [Accessed 03 January2014].

30

Appendix A. - 10 year financial performance of Sasol

This analysis is based on the Annual reports, Form 20-F and Analyst Books (Reports) for SASOL for a period of 2004 through 2013 (10 years). The data was

further improved for meaningful comparison using following steps:

Step 1: numbers were converted to US$ using the exchange rate mentioned in respective reports.

Step 2: to compare with current prices, data were adjusted to inflation. Inflation figures for South Africa were taken from world bank (GDP Deflator, World

Bank, 2013)

The following method was used for adjusting to inflation:

1. Multiplication factor M for year 2013 (M2013)was 1

2. Multiplying factor for M for any year ‘n’ (n being less than 2013) was obtained by using formula:

Mn = M(n+1)/(1-Inflation for year ‘n’)

3. Multiplying factor (Mn) was multiplied to financial data of year n.

4. Multiplying factor for different year are as follows:

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

1.89 1.77 1.67 1.56 1.44 1.32 1.21 1.13 1.06 1.00

Also average calculations were done as follows:

1. Weighted average WA = ∑(P*R)/ ∑P, where P is either year wise sales (for revenue) or year wise production (for cost) calculation;

2. Weighted average revenue (cost) for per unit of output = WA/(∑P/n), where ∑P/n is average annual sales or production of output as the case may be.

31

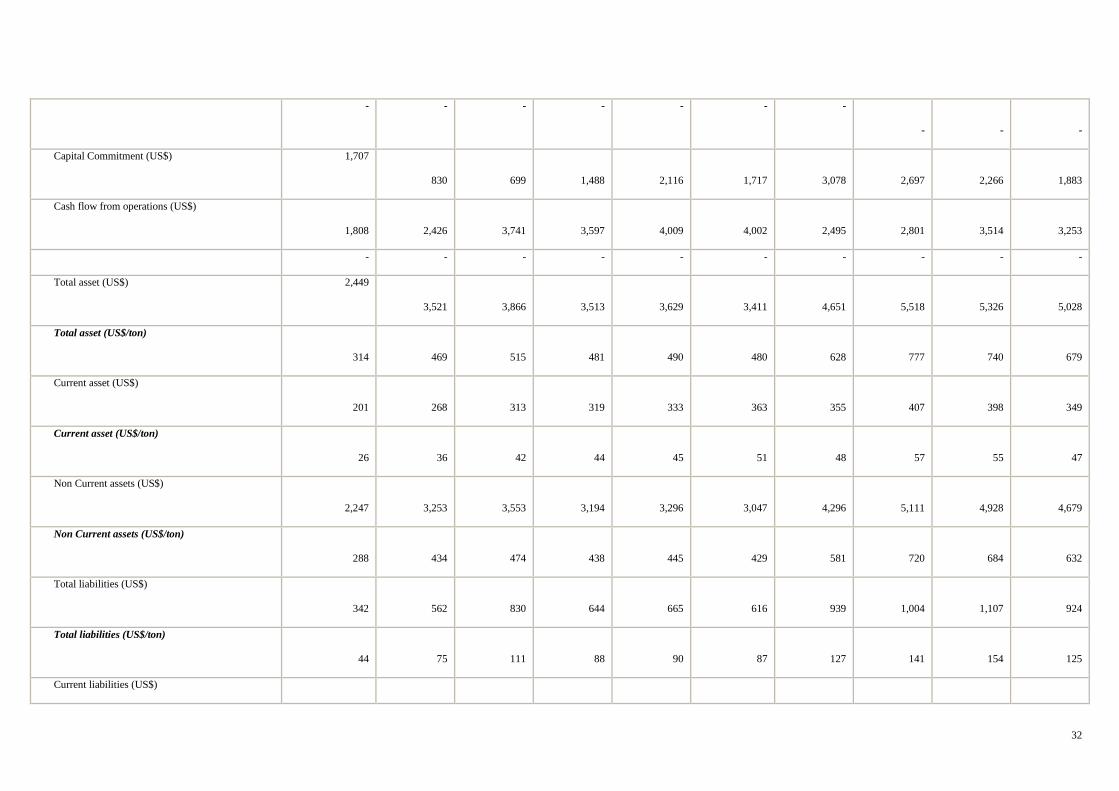

10 Years Performance of Sasol (prices are in US$)

2,004 2,005 2,006 2,007 2,008 2,009 2,010 2,011 2,012 2,013

Coal Sales to Secunda Plant (million tons) 40 39 40 40 40 39 39 38 38 40

Productions of CTLS from Secunda plant(million

tons)

8 8 8 7 7 7 7 7 7 7

Sales of CTL (million tons) 8 8 8 7 8 7 8 7 7 7

- - - - - - - - - -

10 9 9 9 8 7 6 6 6 5

Turnover (US$) 4,287 5,331 6,686 6,320 7,868 5,517 5,382 5,935 6,628 6,622

- - - - - - - - - -

Total operating costs (US$) 2,813 3,174 3,167 2,789 4,012 1,831 3,281 3,530 3,626 3,369

Cost of coal 1,106 1,261 1,204 1,124 1,292 1,072 1,105 1,227 1,284 1,256

Employee Cost 446 509 485 366 432 415 451 474 421 463

Cost of transformation 952 1,244 1,305 1,162 2,145 224 1,497 1,531 1,587 1,271

Depreciation & Ammortisation 309 160 172 137 143 119 229 299 335 379

- - - - - - - - - -

Operating profit (US$) 1,474 2,153 3,519 3,532 3,856 3,686 2,086 2,405 3,001 3,253

Addition to noncurrent asset (US$) 510 932 742 407 458 753 1,242 1,168 912 937

32

- - - - - - -

-

-

-

Capital Commitment (US$) 1,707

830

699

1,488

2,116

1,717

3,078

2,697

2,266

1,883

Cash flow from operations (US$)

1,808

2,426

3,741

3,597

4,009

4,002

2,495

2,801

3,514

3,253

- - - - - - - - - -

Total asset (US$) 2,449

3,521

3,866

3,513

3,629

3,411

4,651

5,518

5,326

5,028

Total asset (US$/ton)

314

469

515

481

490

480

628

777

740

679

Current asset (US$)

201

268

313

319

333

363

355

407

398

349

Current asset (US$/ton)

26

36

42

44

45

51

48

57

55

47

Non Current assets (US$)

2,247

3,253

3,553

3,194

3,296

3,047

4,296

5,111

4,928

4,679

Non Current assets (US$/ton)

288

434

474

438

445

429

581

720

684

632

Total liabilities (US$)

342

562

830

644

665

616

939

1,004

1,107

924

Total liabilities (US$/ton)

44

75

111

88

90

87

127

141

154

125

Current liabilities (US$)

33

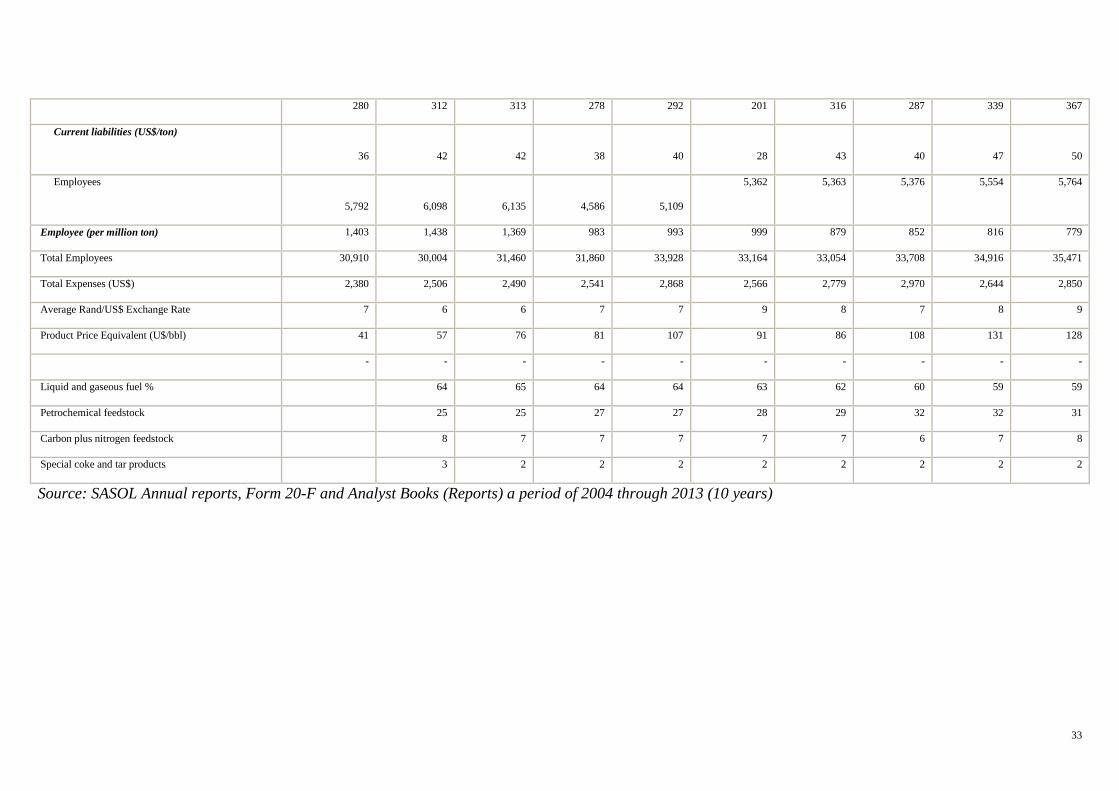

280 312 313 278 292 201 316 287 339 367

Current liabilities (US$/ton)

36

42

42

38

40

28

43

40

47

50

Employees

5,792

6,098

6,135

4,586

5,109

5,362 5,363 5,376 5,554 5,764

Employee (per million ton) 1,403 1,438 1,369 983 993 999 879 852 816 779

Total Employees 30,910 30,004 31,460 31,860 33,928 33,164 33,054 33,708 34,916 35,471

Total Expenses (US$) 2,380 2,506 2,490 2,541 2,868 2,566 2,779 2,970 2,644 2,850

Average Rand/US$ Exchange Rate 7 6 6 7 7 9 8 7 8 9

Product Price Equivalent (U$/bbl) 41 57 76 81 107 91 86 108 131 128

- - - - - - - - - -

Liquid and gaseous fuel % 64 65 64 64 63 62 60 59 59

Petrochemical feedstock 25 25 27 27 28 29 32 32 31

Carbon plus nitrogen feedstock 8 7 7 7 7 7 6 7 8

Special coke and tar products 3 2 2 2 2 2 2 2 2

Source: SASOL Annual reports, Form 20-F and Analyst Books (Reports) a period of 2004 through 2013 (10 years)