kelvin leibold farm management field specialist phone 641-648-4850 e-mail [email protected] farm...

TRANSCRIPT

Kelvin LeiboldFarm Management Field Specialist

Phone 641-648-4850

E-mail [email protected]

Farm Finance for Women 101

Financial Terms

• Liquidity• Solvency• Profitability• Repayment Capacity• Financial Efficiency

http://www.extension.iastate.edu/Publications/FM1791.pdf

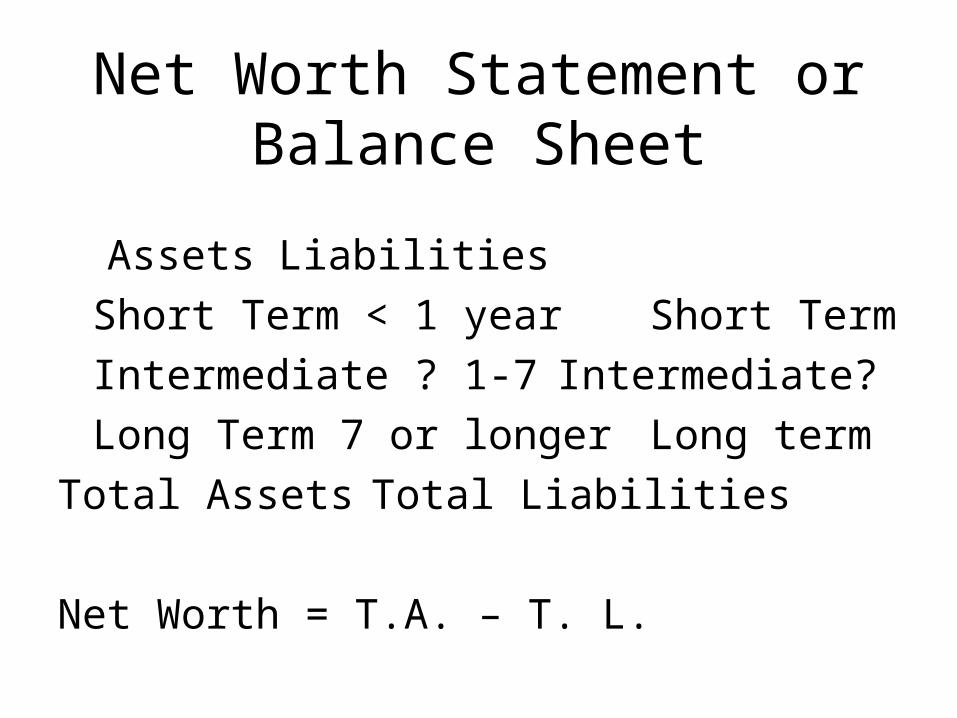

Net Worth Statement orBalance Sheet

Assets Liabilities

Short Term < 1 year Short Term

Intermediate ? 1-7Intermediate?

Long Term 7 or longer Long term

Total Assets Total Liabilities

Net Worth = T.A. – T. L.

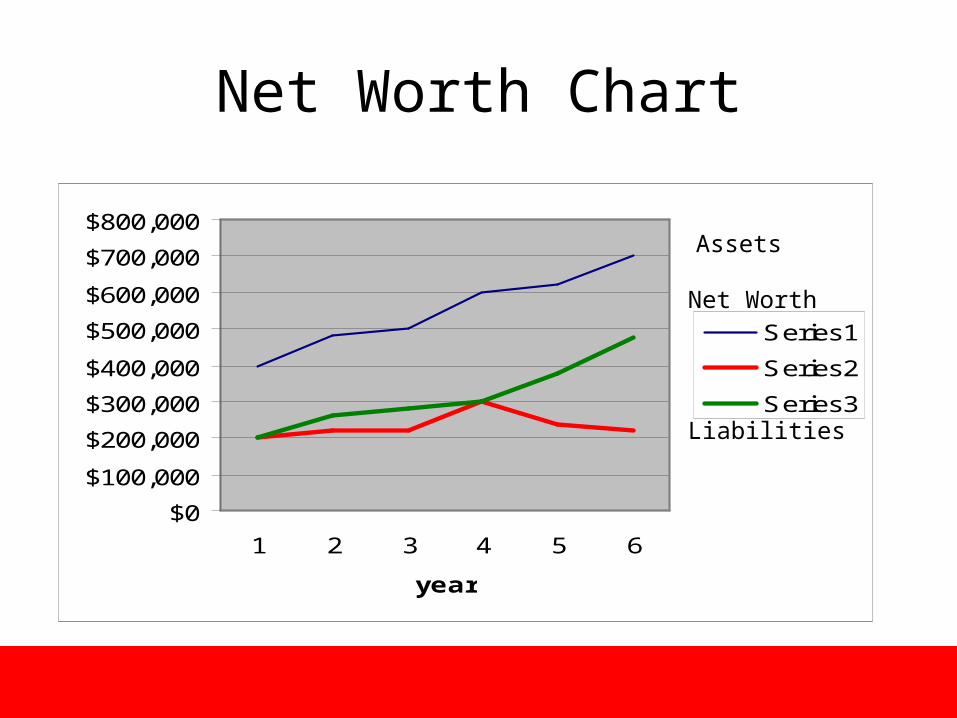

Net Worth Chart

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

1 2 3 4 5 6

year

Series1

Series2

Series3

Assets

Net Worth

Liabilities

Measuring Liquidity

• Working Capital• Current Ratio

This information comes from the balance sheet

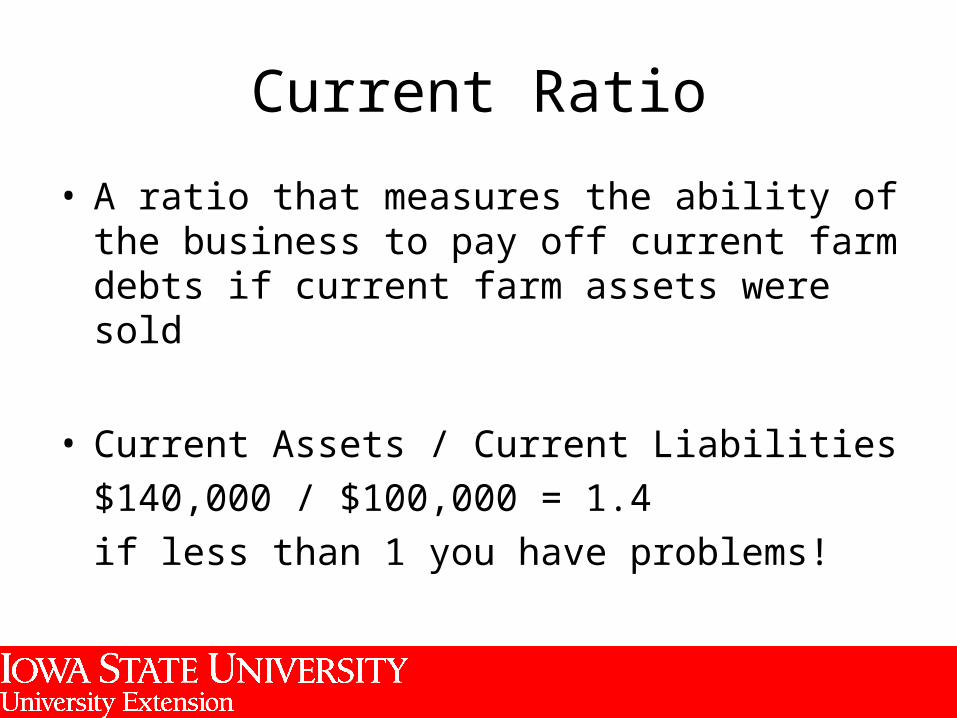

Current Ratio

• A ratio that measures the ability of the business to pay off current farm debts if current farm assets were sold

• Current Assets / Current Liabilities

$140,000 / $100,000 = 1.4

if less than 1 you have problems!

Working Capital

• The amount of operating capital available to the business in the short run to pay bills and support family living

• Current Assets – Current Liabilities = WC• $140,000 - $100,000 = $40,000

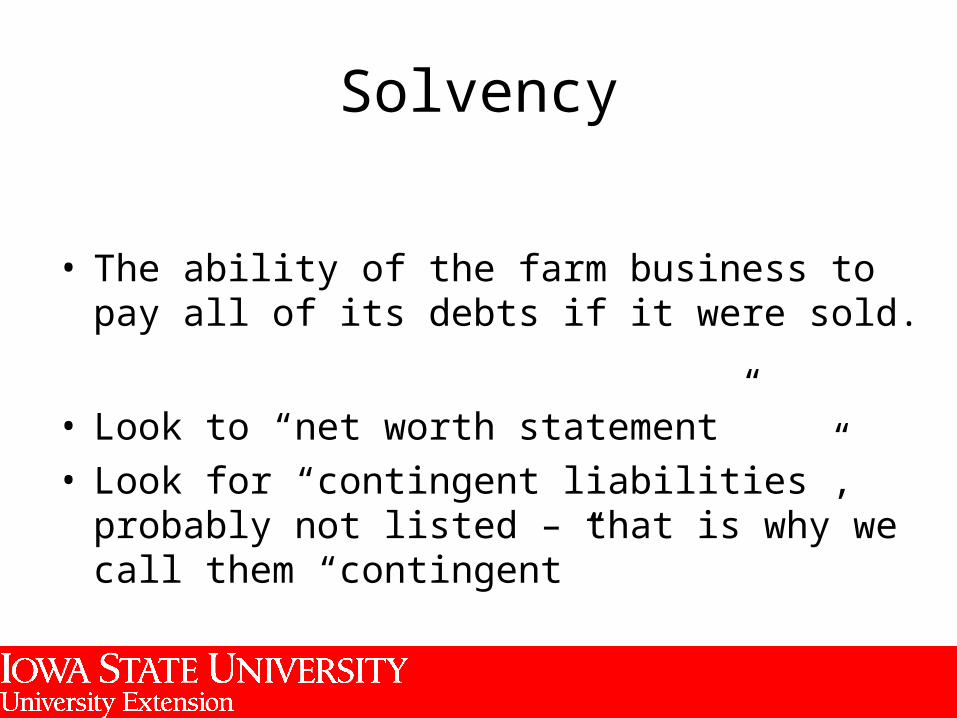

Solvency

• The ability of the farm business to pay all of its debts if it were sold.

• Look to “net worth statement”• Look for “contingent liabilities”, probably not listed –

that is why we call them “contingent”

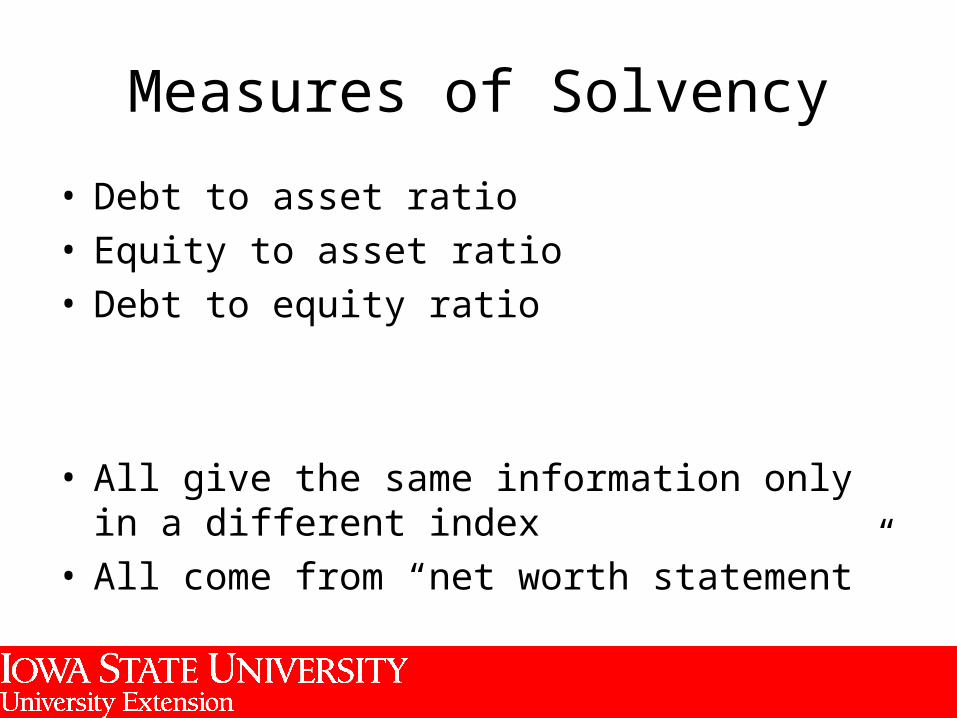

Measures of Solvency

• Debt to asset ratio• Equity to asset ratio• Debt to equity ratio

• All give the same information only in a different index

• All come from “net worth statement”

Farm Debt to Asset Ratio

• The percentage of total assets financed by debt

Total Farm Debt / Total Farm Assets X 100

$400,000 / $1,000,000 X 100 = 40%

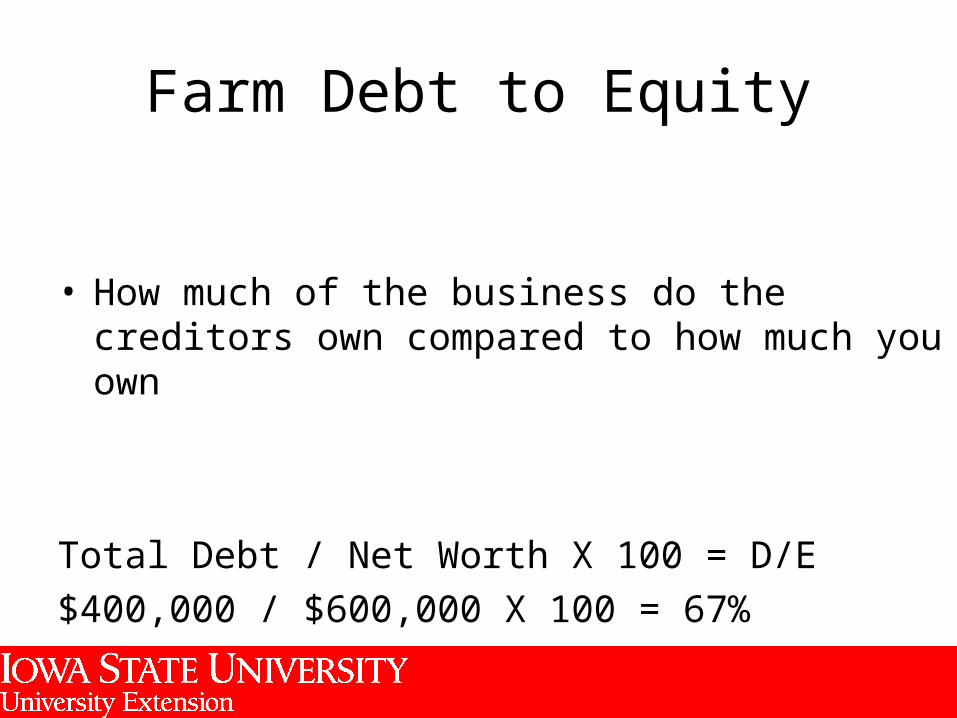

Farm Debt to Equity

• How much of the business do the creditors own compared to how much you own

Total Debt / Net Worth X 100 = D/E

$400,000 / $600,000 X 100 = 67%

Liquidity

• The ability of the farm or business to meet financial obligations as they come due with assets or income from the business including family living expenses.

• Look to “cash flow” and current ratio on “net worth statement”

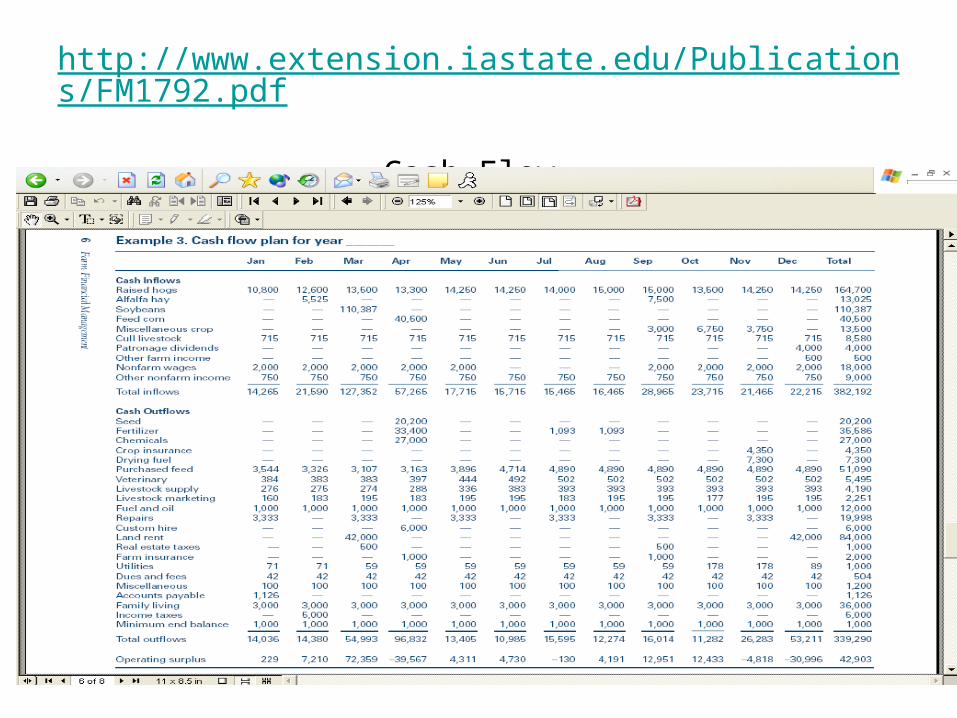

http://www.extension.iastate.edu/Publications/FM1792.pdfCash Flow

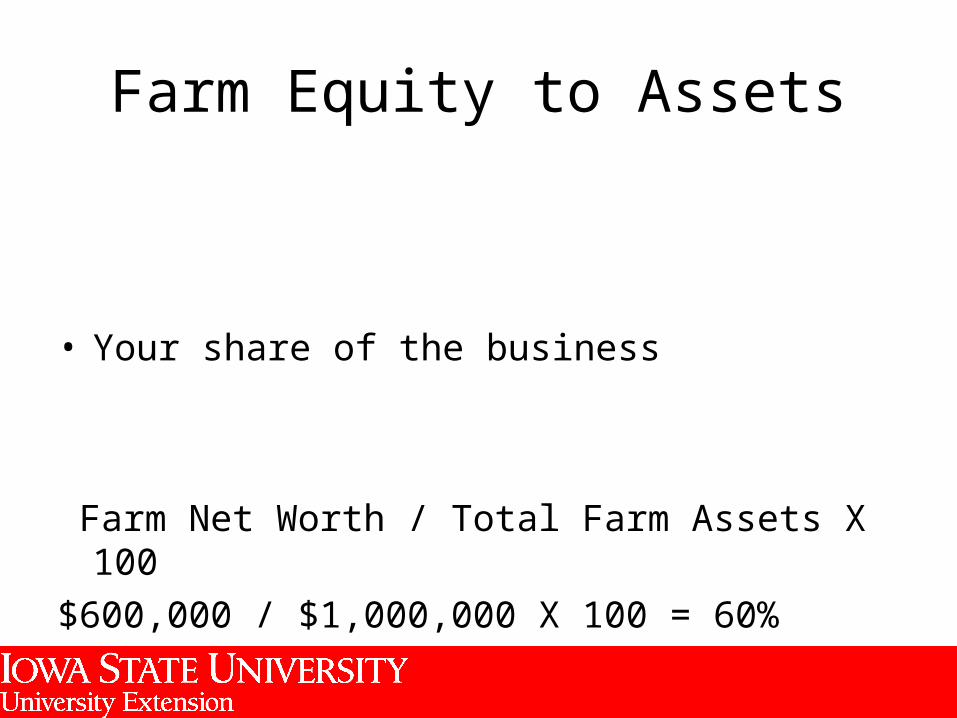

Farm Equity to Assets

• Your share of the business

Farm Net Worth / Total Farm Assets X 100

$600,000 / $1,000,000 X 100 = 60%

Return on Farm Equity

• Average interest rate earned by the money you have invested in the business

Change in Net worth / Ave. Net Worth X 100 =

$50,000 / [($600,000 + $650,000) / 2] X 100 = 8%

Profitability

• The difference between the cost of resources used and the value of the goods sold.

• Look to “income statement” and • Look at inventory change.

http://www.extension.iastate.edu/Publications/FM1816.pdf

Repayment Capacity

• Your ability to repay intermediate and long term debts on time

• Look at “current ratio” and “cash flow”

Financial Efficiency

• How well your business is able to use assets to generate income.

• Look to “income statement”

Rate of Return on Farm Assets

• Average interest rate being earned by the money invested in the business.

• Net Farm Income + interest expense – owner withdrawals / average assets X 100 = ROA

• Needs to be higher than the cost of borrowing money or “you got troubles”.

Repayment Capacity

• Profit available to repay term debt and replace capital assets

Measures of Financial Efficiency

• Asset Turnover Ratio• Operating Expense Ratio• Depreciation Ratio• Interest Expense Ratio• Net Farm Income from Operations Ratio

Asset Turnover Ratio

• How quickly does the business turn over the revenue or capital it requires.

Operating Expense Ratio

• The proportion of farm income that is used to pay operating expense excluding principal and interest

Depreciation Expense Ratio

• How fast the depreciable assets wear out and need to be replaced

• May be inversely correlated with repairs

Interest Expense Ratio

• Indicates how much of the farm income is used to pay for borrowing capital

Net Farm Income Ratio

• Shows the net farm income from the whole operation compared to the gross revenue of the farm operation not including unpaid labor or charge for management

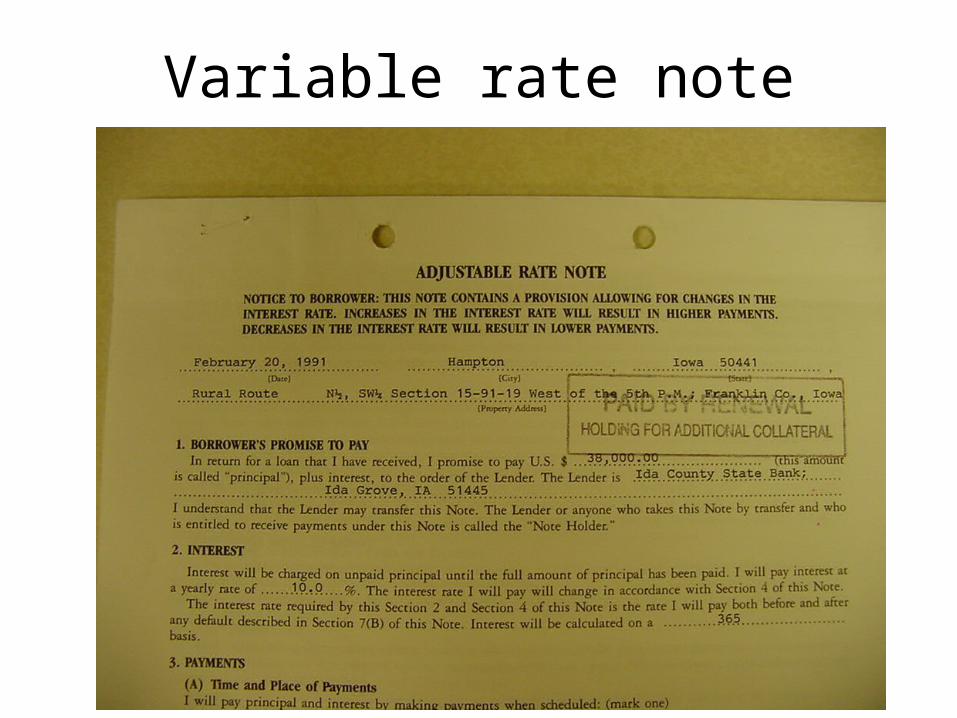

Variable rate note

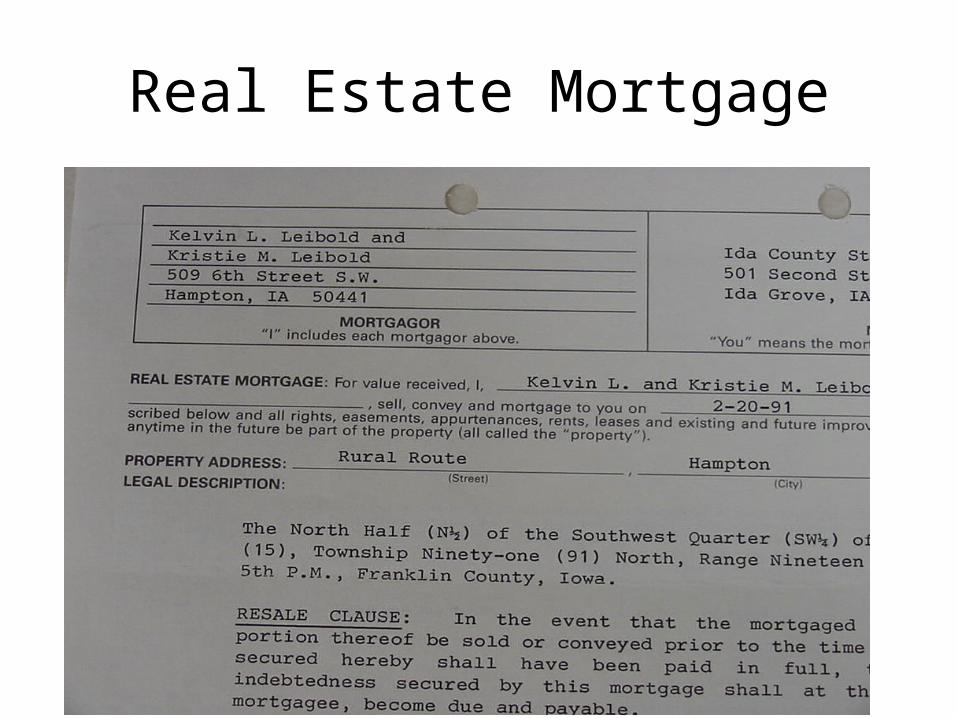

Real Estate Mortgage

Legal Description

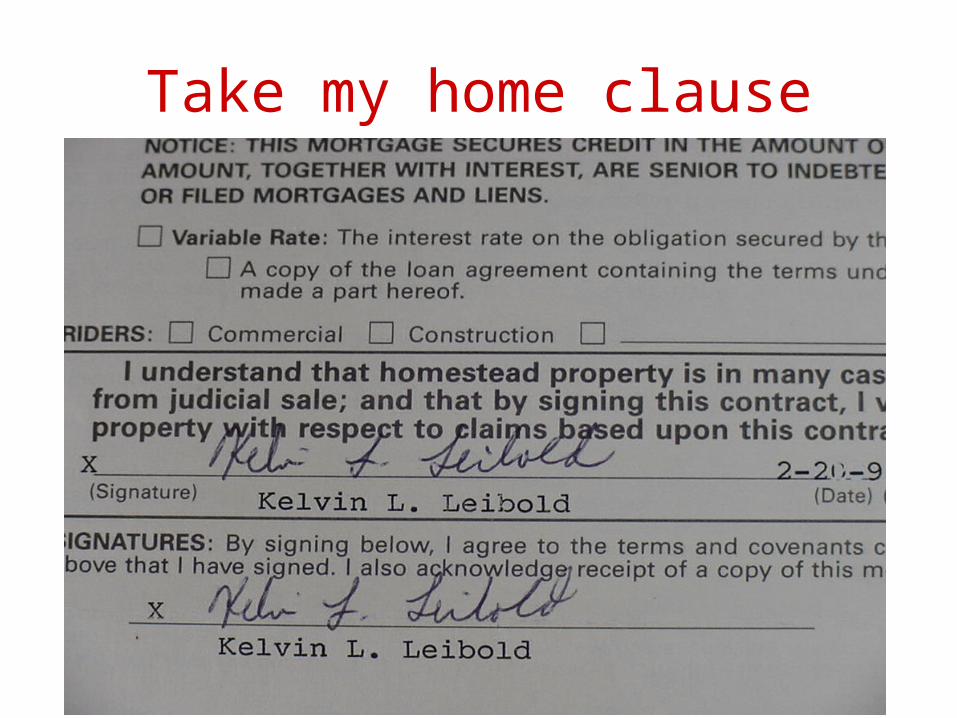

Take my home clause

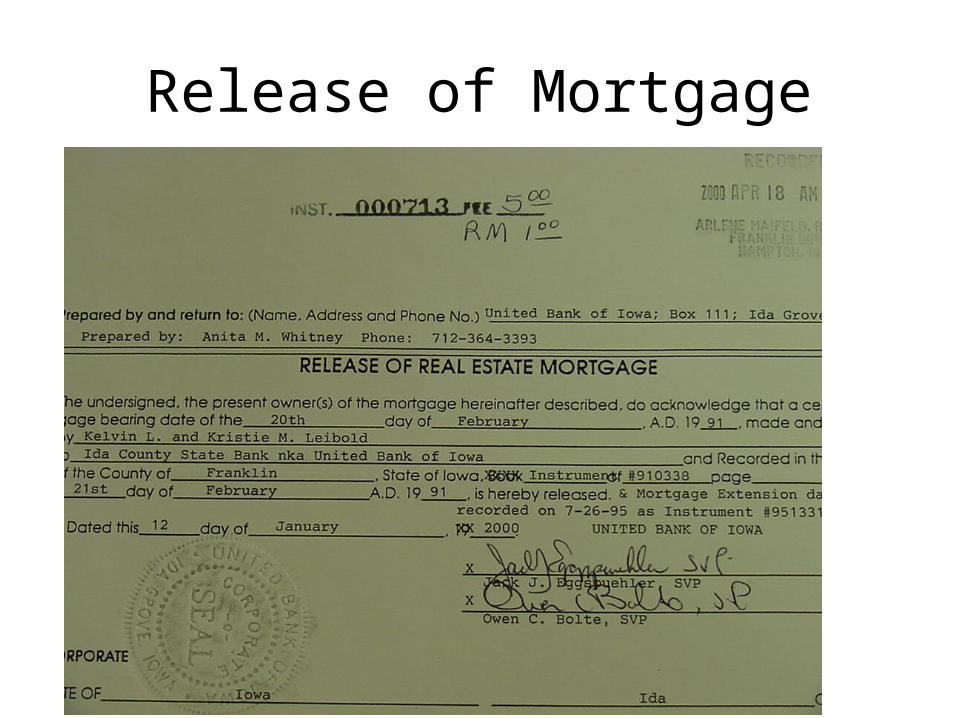

Release of Mortgage

EWG.ORG

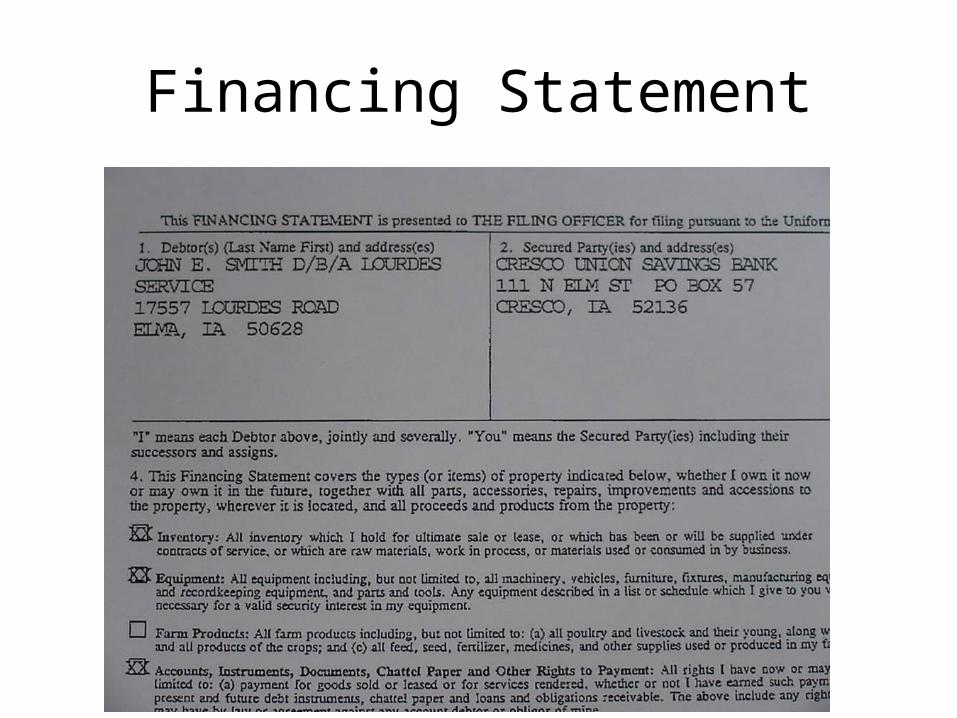

http://www.sos.state.ia.us/UCC_Search/

UCC RA9 Search

Financing Statement

Financing Statement

Estate Tax Planning

If the “pie” is a small pie ( $1.5 million in 2004) look at impact of inflation and legal costs

Don’t worry about Federal Estate Tax, focus on income tax issues, possible Iowa inheritance tax

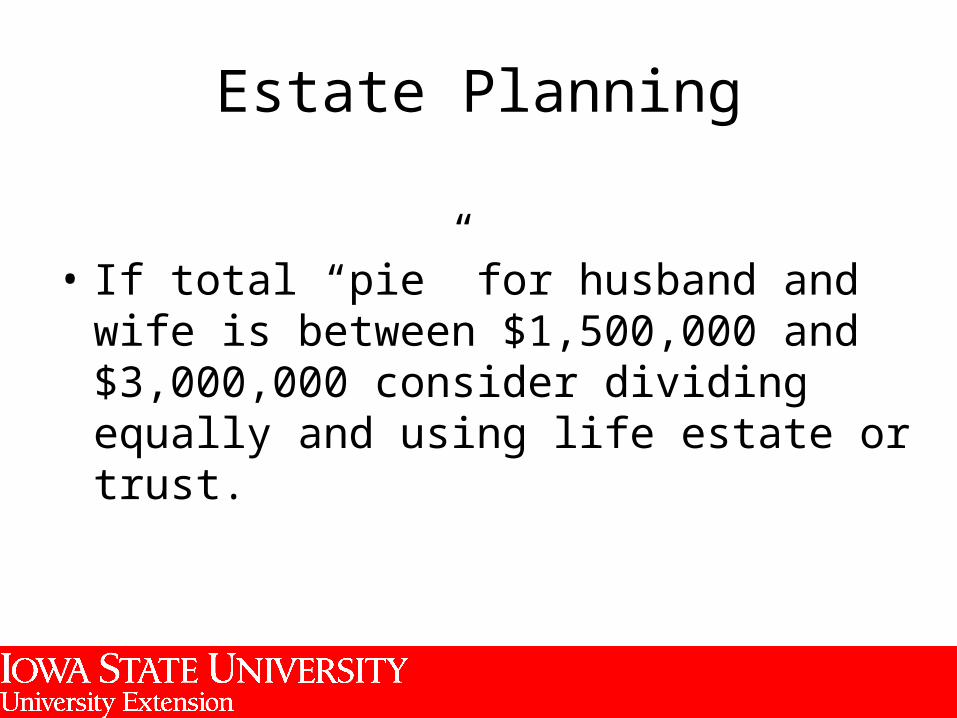

Estate Planning

• If total “pie” for husband and wife is between $1,500,000 and $3,000,000 consider dividing equally and using life estate or trust.

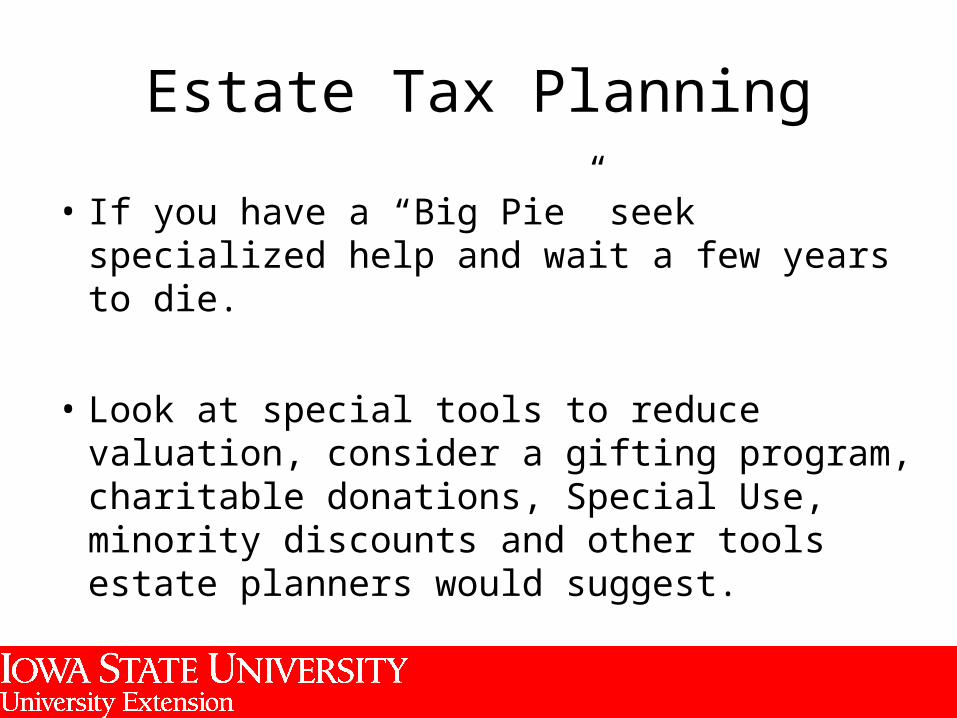

Estate Tax Planning

• If you have a “Big Pie” seek specialized help and wait a few years to die.

• Look at special tools to reduce valuation, consider a gifting program, charitable donations, Special Use, minority discounts and other tools estate planners would suggest.

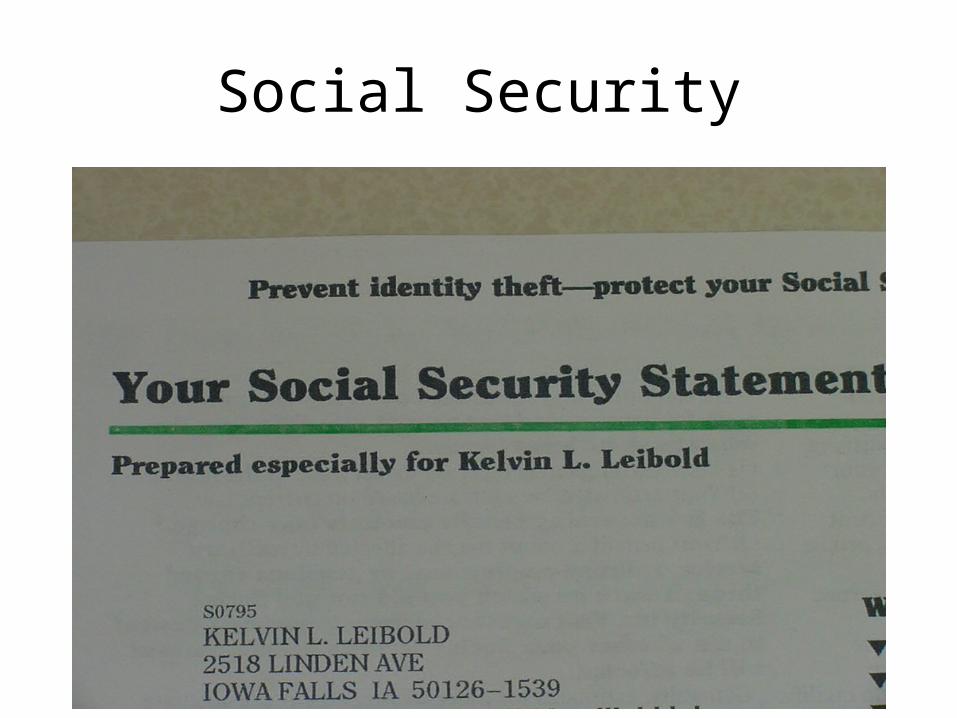

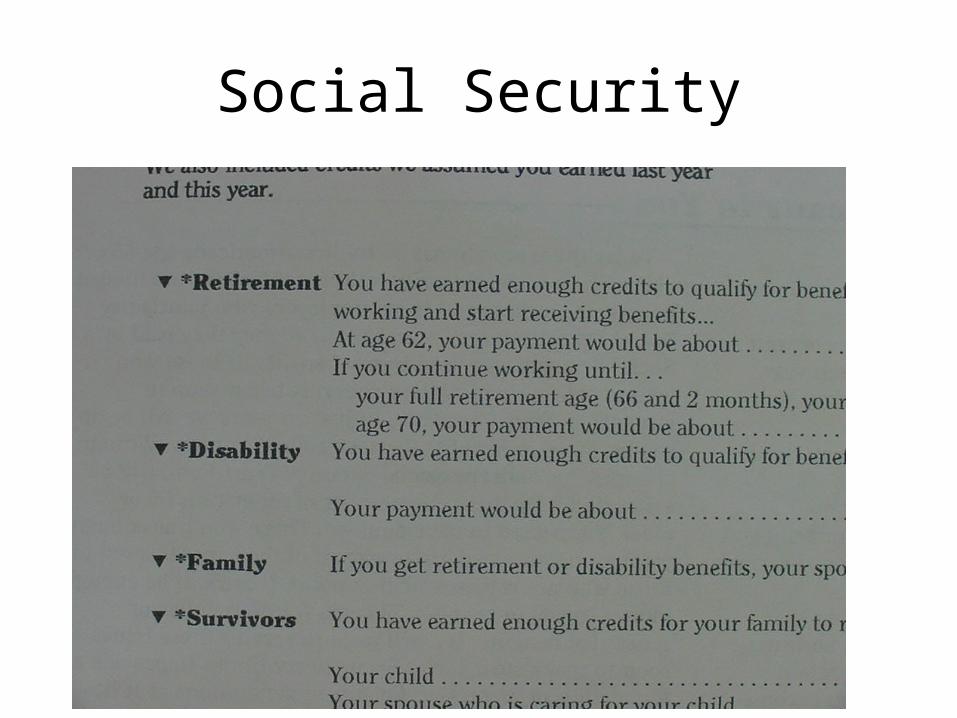

Social Security

Social Security

Social Security

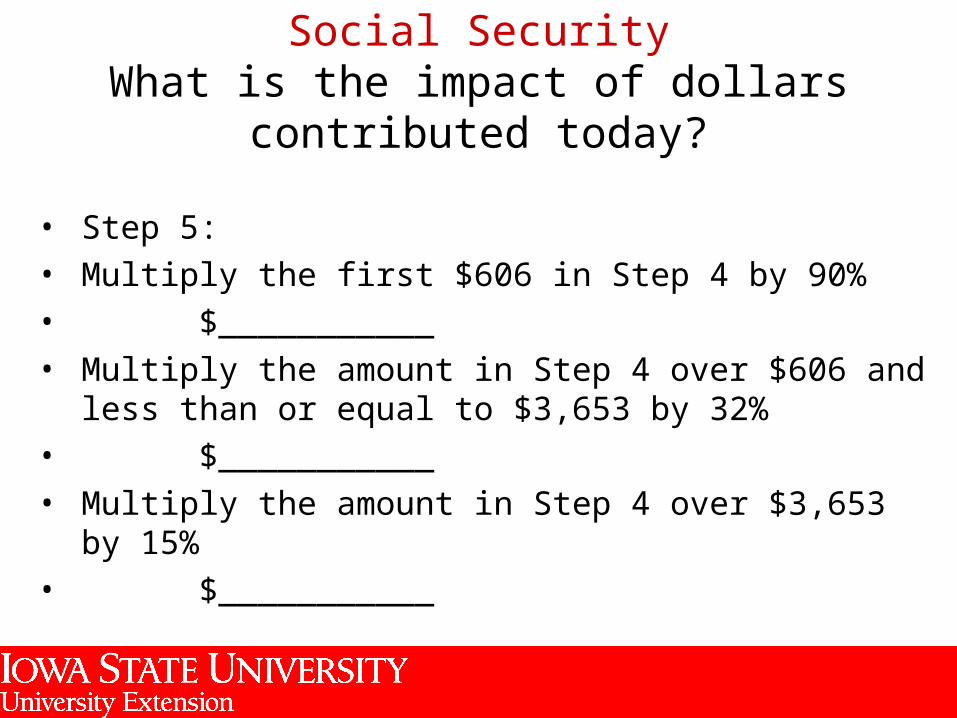

Social SecurityWhat is the impact of dollars contributed today?

• Step 5:• Multiply the first $606 in Step 4 by 90%• $___________• Multiply the amount in Step 4 over $606 and less

than or equal to $3,653 by 32%• $___________• Multiply the amount in Step 4 over $3,653 by 15%• $___________

Assume $7,075 / month of SE earnings

• $606 times 90% = $545 of AIME

• $3,653 times 32% = $1169 of AIME• so $4,259 / mo. Equals $1,714 of AIME

• $2,816 times 15% = $422 of AIME• so $7,075 / mo equals $2,136 of AIME

Normal Retirement Age

• 1937 and prior 65• 1938 65 and 2 months• 1939 65 and 4 months• 1940 65 and 6 months• 1941 65 and 8 months• 1942 65 and 10 months• 1943-54 66• 1955 66 and 2 months• 1956 66 and 4 months• 1957 66 and 6 months• 1958 66 and 8 months• 1959 66 and 10 months• 1960 and later 67• Note: Persons born on January 1 use the NRA for the previous year

Spousal Benefit• If your full retirement age is 67, the reduction for starting your:

• Retirement benefit at 62 is about 30 percent. The reduction for starting benefits at age • 63 is about 25 percent• 64 is about 20 percent• 65 is about 13.3 percent and • 66 is about 6.7 percent

• Benefits as a spouse at 62 is about 67.5 percent of the benefit your spouse would receive if his or her benefits started at full retirement age. The reduction for starting benefits as a spouse at age

• 63 is 65 percent• 64 is 62.5 percent• 65 is about 58.3 percent• 66 is about 51.5 percent• 67 is about 50 percent

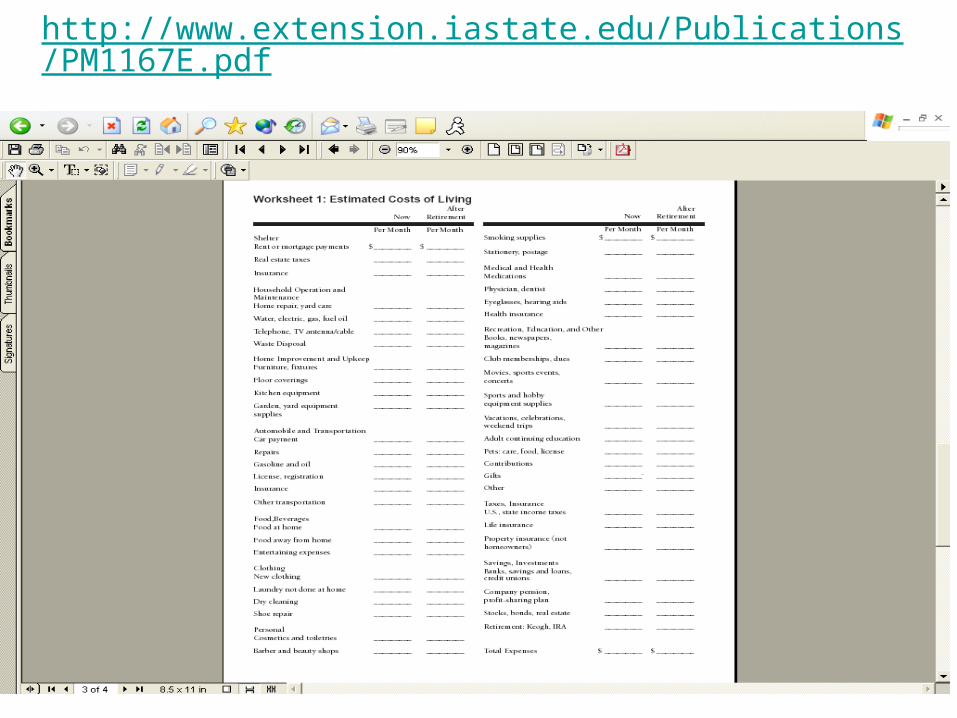

http://www.extension.iastate.edu/Publications/PM1167E.pdfEstimated Costs of Living

Retirement Income

Social Security

Farm property – rent or sale

Other Retirement Income

Other sources?

How Much Retirement Income?

Three phases of retirementa) Go Go Years – travel, entertainmentb) Slow down years – housing, c) Health Issue years – insurance, drugs, nursing

home

Kelvin’s Rule - plan for 100 % of current spending because of tax issues.

Questions???