key banc conference investor presentation

TRANSCRIPT

MOVING THE WORLD AT WORK

Oshkosh Corporation (NYSE:OSK)

KeyBanc Capital Markets Industrial, Automotive & Transportation ConferenceMay 28, 2015

MOVING THE WORLD AT WORK

Forward-Looking Statements

2May 28, 2015Oshkosh Corporation Investor Presentation

This presentation contains statements that the Company believes to be “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical fact, including, without limitation, statements regarding the Company’s future financial position, business strategy, targets, projected sales, costs, earnings, capital expenditures, debt levels and cash flows, and plans and objectives of management for future operations, are forward-looking statements. When used in this press release, words such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe,” “should,” “project” or “plan” or the negative thereof or variations thereon or similar terminology are generally intended to identify forward-looking statements. These forward-looking statements are not guarantees of future performance and are subject to risks, uncertainties, assumptions and other factors, some of which are beyond the Company’s control, which could cause actual results to differ materially from those expressed or implied by such forward-looking statements. These factors include the cyclical nature of the Company’s access equipment, commercial and fire & emergencymarkets, which are particularly impacted by the strength of U.S. and European economies; the strength of the U.S. dollar and its impact on Company exports, translation of foreign sales and purchased materials; the expected level and timing of DoD and international defense customer procurement of products and services and funding thereof; risks related to reductions in government expenditures in light of U.S. defense budget pressures, sequestration and an uncertain DoD tactical wheeled vehicle strategy, including the Company’s ability to successfully manage the cost reductions required as a result of lower customer orders in the defense segment; the Company’s ability to win a U.S. Joint Light Tactical Vehicle production contract award and international defense contract awards; the Company’s ability to increase prices to raise margins or offset higher input costs; increasing commodity and other raw material costs, particularly in a sustained economic recovery; risks related to facilities expansion, consolidation and alignment, including the amounts of related costs and charges and that anticipated cost savings may not be achieved; global economic uncertainty, which could lead to additional impairment charges related to many of the Company’s intangible assets and/or a slower recovery in the Company’s cyclical businesses than Company or equity market expectations; projected adoption rates of work at height machinery in emerging markets; risks related to the collectability of receivables, particularly for those businesses with exposure to construction markets; the cost of any warranty campaigns related to the Company’s products; risks related to production or shipment delays arising from quality or production issues; risks associated with international operations and sales, including compliance with the Foreign Corrupt Practices Act; the Company’s ability to comply with complex laws and regulations applicable to U.S. government contractors; the impact of severe weather or natural disasters that may affect the Company, its suppliers or its customers; cyber security risks and costs of defending against, mitigating and responding to a data security breach; and risks related to the Company’s ability to successfully execute on its strategic road map and meet its long-term financial goals. Additional information concerning these and other factors is contained in the Company’s filings with the Securities and Exchange Commission, including the Form 8-K filed April 28, 2015. All forward-looking statements speak only as of April 28, 2015. The Company assumes no obligation, and disclaims any obligation, to update information contained in this presentation. Investors should be aware that the Company may not update such information until the Company’s next quarterly earnings conference call, if at all.

MOVING THE WORLD AT WORK

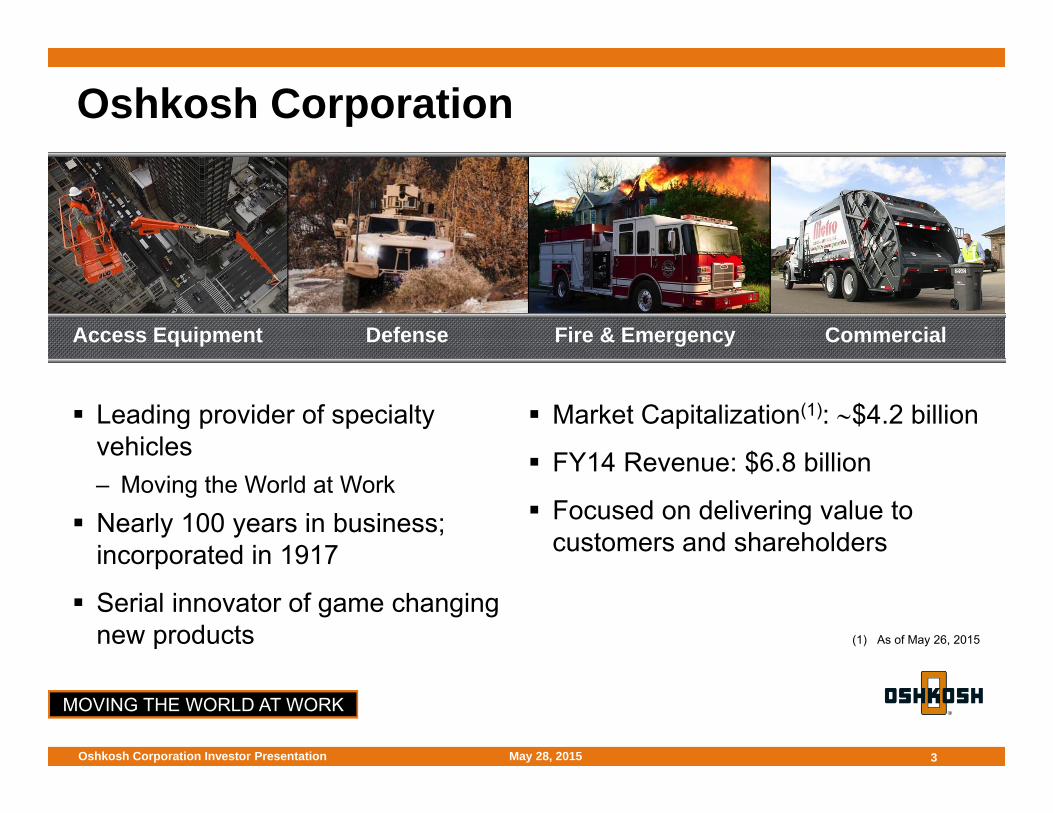

Oshkosh Corporation

Leading provider of specialty vehicles– Moving the World at Work

Nearly 100 years in business; incorporated in 1917

Serial innovator of game changing new products

Market Capitalization(1): $4.2 billion

FY14 Revenue: $6.8 billion

Focused on delivering value to customers and shareholders

3

(1) As of May 26, 2015

Access Equipment Defense Fire & Emergency Commercial

May 28, 2015Oshkosh Corporation Investor Presentation

MOVING THE WORLD AT WORK

Oshkosh Corporation Profile – FY14

Source: Oshkosh Corporation 2014 Annual Report

4Oshkosh Corporation Investor Presentation May 28, 2015

51%

25%

11%

13%

Revenue by Segment

Access Equipment Defense Fire & Emergency Commercial

77%

5%10%

8%

Revenue by Geography

United States Other NA EAME Rest of World

Non-Defense Segment Revenues and Operating Income Both Grew in FY14

─ Expected to Repeat Again in FY15

MOVING THE WORLD AT WORK

Confidence in FY15– Targeting to nearly double EPS from FY12 to FY15– Strong customer sentiment

Positive Outlook Beyond FY15– Additional market recovery opportunities in

non-defense segments– Significant upside opportunities in defense– MOVE to deliver margin expansion and growth

5

A Positive Outlook for OSK

May 28, 2015Oshkosh Corporation Investor Presentation

MOVING THE WORLD AT WORK

Basis for Positive Outlook

6May 28, 2015Oshkosh Corporation Investor Presentation

MOVING THE WORLD AT WORK

FY15 MOVE ScorecardFY15 Adjusted EPS Target Range

7

FY15 TargetInitiative

EPS ~ Double EPS by FY15 (1) EPS of $4.00 - $4.50

…Bottom Line Results for Shareholders

FY15 Estimate

$4.00 - $4.25*

(1) Compared with FY12 expectations as of September 2012 Analyst Day.(2) Net of investment costs and compared with consolidated FY11 operating income margins.

* Non-GAAP results. See Appendix for reconciliation to GAAP results.

May 28, 2015Oshkosh Corporation Investor Presentation

MOVING THE WORLD AT WORK

Solid Q2 FY15 Results Q2 adjusted EPS* of $0.81- In line with expectations- Significant defense sales decline- Foreign exchange and weather

headwinds- Double digit sales and operating

income growth in all non-defense segments

Positive rental company sentiment- Little oil & gas slowdown impact

Refinanced $250 million senior notes due 2020 Reduced interest rate by > 300

bps Targeting FY15 adjusted EPS*

estimate range of $4.00 to $4.25

Net Sales(billions)

Adjusted EPS*

8

$1.6 $1.7

$0.81 $0.80

$0.00

$0.25

$0.50

$0.75

$1.00

$0.0

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2

$1.4

$1.6

$1.8

FY15 FY14Net Sales Adjusted EPS*

* Non-GAAP results. See Appendix for reconciliation to GAAP results.

OSK Fiscal Q2 Performance

May 28, 2015Oshkosh Corporation Investor Presentation

MOVING THE WORLD AT WORK

Access Equipment –The Market Leader

MOVE delivered in FY14– Exciting new products– Strong incremental margins– Record revenues, operating

income and operating income margin

Expect continued growth in FY15– Moderate growth in North America

and Europe– Mixed outlook in other regions Strong new product launches

during the year

9

Reaching Out – Rising to Every Challenge

May 28, 2015Oshkosh Corporation Investor Presentation

MOVING THE WORLD AT WORK

Slow U.S. Construction Recovery is Continuing

10

Source: U.S. Census Bureau, May 19, 2015 Source: U.S. Census Bureau, May 1, 2015

U.S. Housing Starts - Current Annual Forecasts (millions)

Date 2014 2015 2016Global Insight Feb-15 1.00 1.18 1.33Moody's - Slower Recovery Apr-15 1.00 1.20 1.58Portland Cement Association Apr-15 1.00 1.18 1.34Average Analyst Estimate 1.00 1.19 1.42

U.S. Nonresidential Construction (yr/yr Growth) - Current Analyst EstimatesDate 2014 2015 2016

Portland Cement Association Apr-15 8.2% 8.8% 8.3%FMI Source Mar-15 6.0% 8.0% 7.0%Global Insight Mar-15 2.8% 2.2% 3.6%Moody's – Slower Recovery Apr-15 6.9% 7.7% 4.6%Construction Market Data Mar-15 3.9% 8.2% 8.6%McGraw-Hill Mar-15 13.5% 10.9% 13.0%Average Analyst Estimate 6.9% 7.6% 7.5%

Thousands $ MillionsU.S. Non-Residential SpendingHousing Starts

May 28, 2015Oshkosh Corporation Investor Presentation

450,000

500,000

550,000

600,000

650,000

Jan‐2010

Jul‐2

010

Jan‐2011

Jul‐2

011

Jan‐2012

Jul‐2

012

Jan‐2013

Jul‐2

013

Jan‐2014

Jul‐2

014

Jan‐2015

400

500

600

700

800

900

1,000

1,100

1,200

Jan‐2010

Jul‐2

010

Jan‐2011

Jul‐2

011

Jan‐2012

Jul‐2

012

Jan‐2013

Jul‐2

013

Jan‐2014

Jul‐2

014

Jan‐2015

MOVING THE WORLD AT WORK

Operating Income Margin Expansion Remains a Priority

Expect biggest impact from optimize cost and value innovation initiatives still to come

11

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

FY14 FY15E Target

(Ope

ratin

g In

com

e M

argi

n %

)

16%

17%

~ 15% 14.3%

ACCESS EQUIPMENT

May 28, 2015Oshkosh Corporation Investor Presentation

MOVING THE WORLD AT WORK

Defense –Reduced Cost Structure with Upside Opportunities

Believe FY15 will be trough year for both revenues and operating income

Submitted proposal for JLTV program in February– Expect decision on winning bidder

between July and September 2015 Canada MSVS program award

decision expected by June 2015

Continuing pursuit of sales of thousands of M-ATVs– International– Reset opportunities in U.S.

Generally favorable FY16 budget funding requests for our programs

12

Mission Proven – World-Class Performance

May 28, 2015Oshkosh Corporation Investor Presentation

MOVING THE WORLD AT WORK

Fire & Emergency –Operational Improvements Leading to Bright Future

Continuing to execute operational efficiency roadmap− More work to be done

Positive response to recent new product launches– Enforcer and Saber chassis– Revolutionary Ascendant™ two

axle aerial ladder vehicle

Modest market growth expectedin North America in FY15– Recently announced 3% price

increase Additional international success− ARFF orders in Asia, Australia

and Latin America

13

Recently Launched New Products Driving Customer Interest

May 28, 2015Oshkosh Corporation Investor Presentation

MOVING THE WORLD AT WORK

Operating Income Margin Expansion Remains a Priority

Margin expansion behind schedule, but improvement roadmap is solid

14

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

FY14 FY15E Target

(Ope

ratin

g In

com

e M

argi

n %

)

10%+

~ 4.25% 3.5%

FIRE & EMERGENCY

May 28, 2015Oshkosh Corporation Investor Presentation

MOVING THE WORLD AT WORK

Commercial –Progress Continues

Solid North American concrete mixer market recovery over last several years

− Driven by slowly improving housing market

− Strong U.S. dollar creating some drag for multinational concrete mixer customers

RCV market expected to grow in FY15

– Grew modestly in FY14

Split-bin and automated RCV models generating incremental demand

MOVE investments continue

15

North American Market Leader Split Body Rear Loaders

May 28, 2015Oshkosh Corporation Investor Presentation

MOVING THE WORLD AT WORK

Operating Income Margin Expansion Remains a Priority

Optimize cost initiatives continue Absorption benefits accelerate in market recovery

16

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

FY14 FY15E Target

(Ope

ratin

g In

com

e M

argi

n %

)

10%+

~ 6.5% 6.2%

COMMERCIAL

May 28, 2015Oshkosh Corporation Investor Presentation

MOVING THE WORLD AT WORK

Driving to FY15 MOVE Targets and Beyond

17May 28, 2015Oshkosh Corporation Investor Presentation

MOVING THE WORLD AT WORK

What to Expect from Oshkosh in FY15?

Deliver MOVE strategy– FY15 adjusted EPS* estimate

range of $4.00 - $4.25– Margin improvement in all non-

defense segments– Launch game changing new

products– Compete vigorously for business

around the world

Target defense contract awards

Maintain strong customer focus

Increase industry leading quality to higher level

Drive shareholder value

18

* Non-GAAP results. See Appendix for reconciliation to GAAP results.

May 28, 2015Oshkosh Corporation Investor Presentation

MOVING THE WORLD AT WORK

Expectations for FY15*

Additional expectations Corporate expenses of $140 - $145 million Tax rate of ~32% CapEx of ~$150 million Free cash flow** ~$200 million Assumes share count of ~79.5 million

Segment information

Revenues of $6.5 billion to $6.6 billion Adjusted operating income** of $510 million to $540 million Adjusted EPS** of $4.00 to $4.25

* As of April 28, 2015** Non-GAAP results. See Appendix for reconciliation to GAAP results.

19

Q3 Commentary Expect seasonally highest EPS; above prior year Defense segment results similar to Q2 Higher non-defense segment sales and operating

income compared to prior year Q3

Measure Access Equipment Defense Fire &

Emergency Commercial

Sales(billions) $3.7 - $3.8 ~$1.0 ~$0.80 ~$1.0

Operating Income Margin ~15.0% Slightly above

break even ~4.25% ~6.5%

May 28, 2015Oshkosh Corporation Investor Presentation

MOVING THE WORLD AT WORK

And Beyond FY15? Continued improvement

Execute effectively to deliver positive near-term outlook

Continue operating income margin expansion – Target 16 – 17% at Access Equipment– Initially target 10% at other segments

Prudent capital allocation– Target annual dividend increases– Begin building cash; deploy with

crocodile patience Sustain talent and process

improvement to outperform with Oshkosh Operating System

20

7.0% 7.5% ~ 8.0%

10.0%+

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2013 2014 2015E Target

OSK Consolidated Adjusted Operating Income Margin *

* Non-GAAP results. See Appendix for reconciliation to GAAP results.

May 28, 2015Oshkosh Corporation Investor Presentation

MOVING THE WORLD AT WORK

For informationcontact:

Patrick N. DavidsonVice President, Investor Relations(920) [email protected]

21

Jeffrey D. WattDirector, Investor Relations(920) [email protected]

May 28, 2015Oshkosh Corporation Investor Presentation 21

MOVING THE WORLD AT WORK

22

Appendix: Commonly Used AcronymsARFF Aircraft Rescue and Firefighting MECV Modernized Expanded Capability VehicleAWP Aerial Work Platform MRAP Mine Resistant Ambush ProtectedCapEx Capital Expenditures MSVS Medium Support Vehicle System (Canada)CNG Compressed Natural Gas NOL Net Operating LossDGE Diesel Gallon Equivalent NPD New Product DevelopmentDoD Department of Defense NRC National Rental CompanyEAME Europe, Africa & Middle East OH OverheadEMD Engineering & Manufacturing Development OI Operating IncomeEPS Diluted Earnings Per Share OOS Oshkosh Operating SystemFHTV Family of Heavy Tactical Vehicles OPEB Other Post-Employment BenefitsFMS Foreign Military Sales PLS Palletized Load SystemFMTV Family of Medium Tactical Vehicles PUC Pierce Ultimate ConfigurationGAAP U.S. Generally Accepted Accounting Principles R&D Research & DevelopmentHEMTT Heavy Expanded Mobility Tactical Truck RCV Refuse Collection VehicleHET Heavy Equipment Transporter RFP Request for ProposalHMMWV High Mobility Multi-Purpose Wheeled Vehicle ROW Rest of WorldIRC Independent Rental Company SMP Standard Military Pattern (Canadian MSVS)IT Information Technology TACOM Tank-automotive and Armaments CommandJLTV Joint Light Tactical Vehicle TDP Technical Data PackageJPO Joint Program Office TPV Tactical Protector VehicleJROC Joint Requirements Oversight Council TWV Tactical Wheeled VehicleJUONS Joint Urgent Operational Needs Statement UCA Undefinitized Contract ActionL-ATV Light Combat Tactical All-Terrain Vehicle UIK Underbody Improvement Kit (for M-ATV)LVSR Logistic Vehicle System Replacement UK United KingdomM-ATV MRAP All-Terrain Vehicle ZR Zero Radius

May 28, 2015Oshkosh Corporation Investor Presentation

MOVING THE WORLD AT WORK

May 28, 2015Oshkosh Corporation Investor Presentation 23

Appendix: Non-GAAP to GAAP Reconciliation

• The table below presents a reconciliation of the Company’s presented non-GAAP measures to the most directly comparable GAAP measures:

2015 2014

Adjusted earnings per share - diluted (non-GAAP) 0.81$ 0.80$ Reduction of valuation allowance on net operating loss carryforward - 0.14 Pension and OPEB curtailment, net of tax - (0.03) Debt extinguishment costs, net of tax (0.12) (0.08) Earnings per share - diluted (GAAP) 0.69$ 0.83$

Three Months EndedMarch 31,

MOVING THE WORLD AT WORK

May 28, 2015Oshkosh Corporation Investor Presentation 24

Appendix: Non-GAAP to GAAP Reconciliation

• The table below presents a reconciliation of the Company’s presented non-GAAP measures to the most directly comparable GAAP measures:

2013 2014 2015E

Consolidated operating income margins (non-GAAP) 7.0% 7.5% 8.0%Union contract ratification costs -0.1% - - Pension curtailment and settlement loss - -0.1% - OPEB curtailment gain - 0.2% - Tender offer and proxy contest costs -0.2% - - Impairment charge -0.1% - - Contract pricing adjustment for OPEB costs - -0.2% - Consolidated operating income margins (GAAP) 6.6% 7.4% 8.0%

Fiscal Year EndedSeptember 30,

MOVING THE WORLD AT WORK

May 28, 2015Oshkosh Corporation Investor Presentation 25

Appendix: Non-GAAP to GAAP Reconciliation

• The table below presents a reconciliation of the Company’s presented non-GAAP measures to the most directly comparable GAAP measures (in millions, except per share amounts):

Low High

Adjusted operating income (non-GAAP) 510.0$ 540.0$ OPEB curtailment gain 3.4 3.4 Operating income (GAAP) 513.4$ 543.4$

Adjusted earnings per share - diluted (non-GAAP) 4.00$ 4.25$ OPEB curtailment gain, net of tax 0.03 0.03 Debt extinguishment costs, net of tax (0.12) (0.12) Earnings per share - diluted (GAAP) 3.91$ 4.16$

Fiscal 2015Expectations

Net cash flows provided by operating activities 359.0$ Additions to property, plant and equipment (150.0) Net additions to equipment held for rental (9.0) Free cash flow 200.0$

Fiscal 2015 Expectations