lancaster colony corporation baird 2017 global...

TRANSCRIPT

Lancaster Colony Corporation

Baird 2017 Global Consumer, Technology & Services Conference

June 7, 2017

Presenters: Jay Gerlach, Chairman and Chief Executive OfficerDave Ciesinski, President and Chief Operating Officer

This presentation was prepared by Lancaster Colony Corporation for information purposes only and is not an offer

or solicitation with respect to the purchase or sale of Company securities. We desire to take advantage of the

“safe harbor” provisions of the Private Securities Litigation Reform Act of 1995 (the “PSLRA”). Any statements

concerning the Company’s future performance included in this presentation or made orally to the recipients of this

presentation are “forward–looking statements” within the meaning of the PSLRA and other applicable securities

laws. Such statements can be identified by the use of the forward-looking words “anticipate,” “estimate,”

“project,” “believe,” “intend,” “plan,” “expect,” “hope” or similar words. These statements discuss future

expectations; contain projections regarding future developments, operations or financial conditions; or state other

forward-looking information. Such statements are based upon assumptions and assessments made by us in light of

our experience and perception of historical trends, current conditions, expected future developments and other

factors we believe to be appropriate. These forward-looking statements involve various important risks,

uncertainties and other factors that could cause our actual results to differ materially from those expressed in the

forward-looking statements. Actual results may differ as a result of factors over which we have no, or limited,

control. Management believes these forward-looking statements to be reasonable; however, you should not place

undue reliance on such statements that are based on current expectations. For example, fluctuations in the market

price of material or freight costs or general economic conditions for domestic consumers, over which we have no

control, may significantly influence our financial results. Forward-looking statements speak only as of the date they

are made, and we undertake no obligation to update such forward-looking statements. More detailed statements

regarding significant events that could affect our financial results are included in our Annual Report on Form 10-K

and Quarterly Reports on Form 10-Q as filed with the Securities and Exchange Commission and available at

www.lancastercolony.com.

Safe Harbor Statement

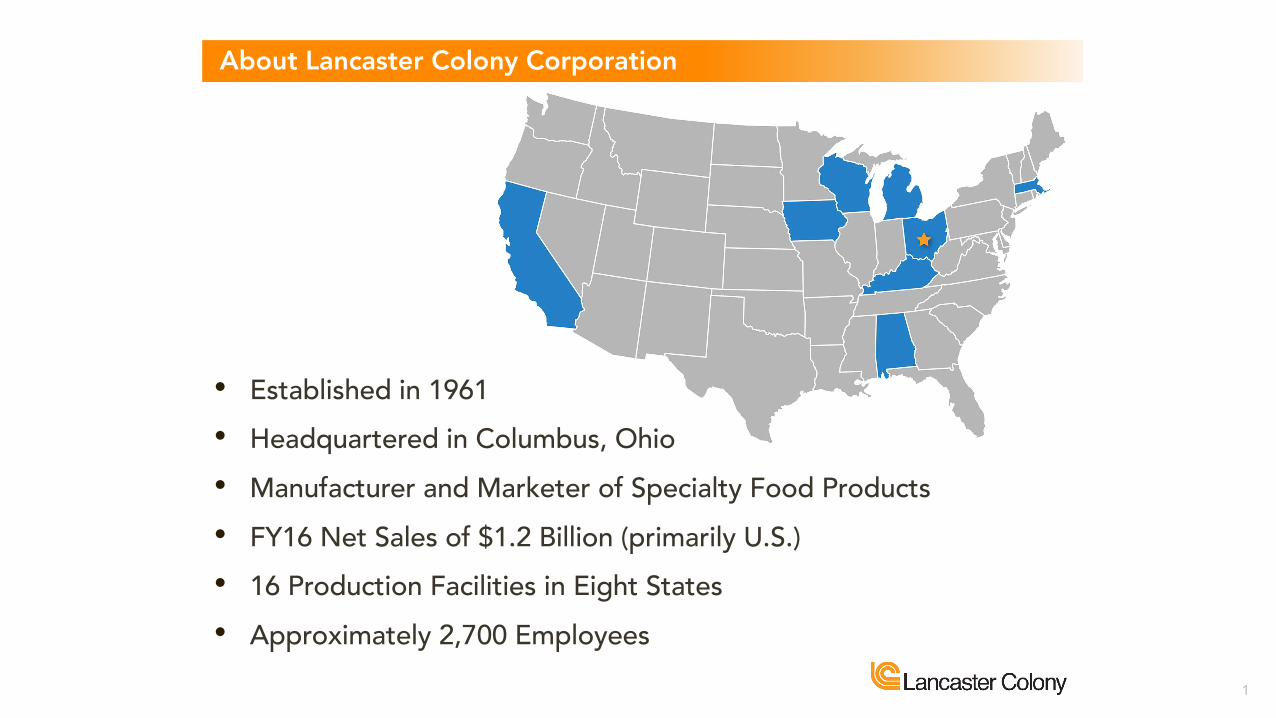

• Established in 1961• Headquartered in Columbus, Ohio• Manufacturer and Marketer of Specialty Food Products• FY16 Net Sales of $1.2 Billion (primarily U.S.)• 16 Production Facilities in Eight States• Approximately 2,700 Employees

About Lancaster Colony Corporation

1

• Leading Market Share Position in Six Retail Food Categories• Supplier to 18 of the Top 25 National Restaurant Chains• Long History of Sustained Organic Sales Growth • Strong Cash Flows• One of 14 U.S. Companies to have Increased Regular Cash

Dividend for 54 Consecutive Years

Company Highlights

2

Foodservice 48%Retail 52%

Based on approximated net sales for the 12 months ending June 30, 2016

Frozen20%

Produce & Deli19%

Grocery13% Industrial

2%

NationalAccounts

36%

Branded10%

Specialty Foods - Product Mix

3

Produce& Deli37%

Frozen39%

Grocery24%

Retail Sales Mix

Based on approximated net sales for the 12 months ending June 30, 2016

Note: Olive Garden SM dressings are produced and sold to retailers under a licensing agreement with Darden Restaurants. 4

Marzetti25.1%

All Others20.2%

Bolthouse12.3%

Litehouse21.0%

Marie’s21.4%

52 weeks ending 7/10/16, Source: IRI, Total U.S. Multi-Outlet

Refrigerated Dressing Market Share

5

Marzetti82.5%

All Others1.1%

Litehouse10.6%

Jimmy’s2.3%

Private Label3.5%

Produce Dip Market Share

52 weeks ending 7/10/16, Source: IRI, Total U.S. Multi-Outlet6

Pepperidge Farm15.3%New York Bakery

40.1%

Cole’s10.7%

Private Label28.6%

All Others5.3%

Frozen Garlic Bread Market Share

52 weeks ending 7/10/16, Source: IRI, Total U.S. Multi-Outlet7

All Others12.5%

Private Label6.3%

Rhodes30.0%

Sister Schubert’s51.2%

52 weeks ending 7/10/16, Source: IRI, Total U.S. Multi-Outlet

Frozen Roll Market Share

8

Mrs. Cubbison’s /Fresh Gourmet

27.7%

All Others6.2%

Private Label19.2%

Marzetti, Cardini’s,New York Bakery,Chatham Village

36.7%

Rothbury Farms10.2%

52 weeks ending 7/10/16, Source: IRI, Total U.S. Multi-Outlet

Crouton Market Share

9

Joseph’s14.2%

All Others38.6%

Toufayan14.1%

Tumaros6.9%

Flatout22.4%

Mission3.8%

52 weeks ending 7/10/16, Source: IRI, Total U.S. Multi-Outlet

Flatbread/Healthy Wraps/Pita Bread Market Share

10

National Accounts75%

Branded21%

Industrial4%

Foodservice Sales

Based on approximated net sales for the 12 months ending June 30, 2016 12

Dressings

Foodservice Products

Pasta

BreadsSauces

11

Lancaster Colony Corporation

Dave CiesinskiPresident and Chief Operating Officer

13

$1,200

$600

20161980 1990 2000

$ in Millions

$1,191.1Compound Annual Growth Rate – 12%

$5.2

1971 2010

Specialty Foods Net Sales

Net sales information is presented as originally reported in Lancaster Colony's Annual Report for the fiscal yearsending June 30. Therefore, certain years may not reflect adjustments for subsequent accounting changes.

*Compound Annual Growth Rate calculated from fiscal year 1972 through fiscal year 2016. 14

Sister Schubert’s®

Marzetti®

Portfolio of Strong Brands

$ Sales: 63.3MMRef. Dressing

$ Share: 16.0%

Marzetti® Simply Dressed® Olive GardenSM

$ Sales: 128.5MMDips

$ Share: 82.5%$ Sales: 36.0MM$ Share: 9.1%

$ Sales: 57.9MM$ Share: 3.3%

New York Brand® Bakery

$ Sales: 209.6MM$ Share: 40.1%

$ Sales: 109.7MM$ Share: 51.2%

Flatout®

$ Sales: 53.7MM$ Share: 22.4%

*Retailer sales and market share data for the 52 weeks ended 7/10/16. Source: IRI, Total U.S. Multi-Outlet

Note: Olive GardenSM dressings are produced and sold to retailers under a licensing agreement with Darden Restaurants.15

Consumers More Diverse

Demographic Changes Impacting the Food Industry

Millennials - Largest Cohort/Slow to Launch

Trends are Shifting

Resulting in a Disruptive Change in Food

16

Demographic Changes Impacting the Food Industry

…Now traffic heavily favors the store perimeter

High Foot Traffic Category

Low Foot Traffic Category

Layout of Typical Grocery Store

Prod

uce Frozen

Food

Bee

r / W

ineDry

Grocery

Meat Dairy+6%

+5% +3%

+5%+1%+1%+4%

*Branded Specialty Bakery Products & Deli Prep

Source: IRI. (Annualized changes for the three-year period ended 4/16/17).

Total Category $ Sales Growth Rate

(Unit sales declining) (Unit sales declining)

17

Large Food Co’s

Demographic Changes Impacting the Food Industry

Retail Food Industry (Yesterday)

Private Label Co’s

18

Organic/Natural Co’s

Large Food Co’s

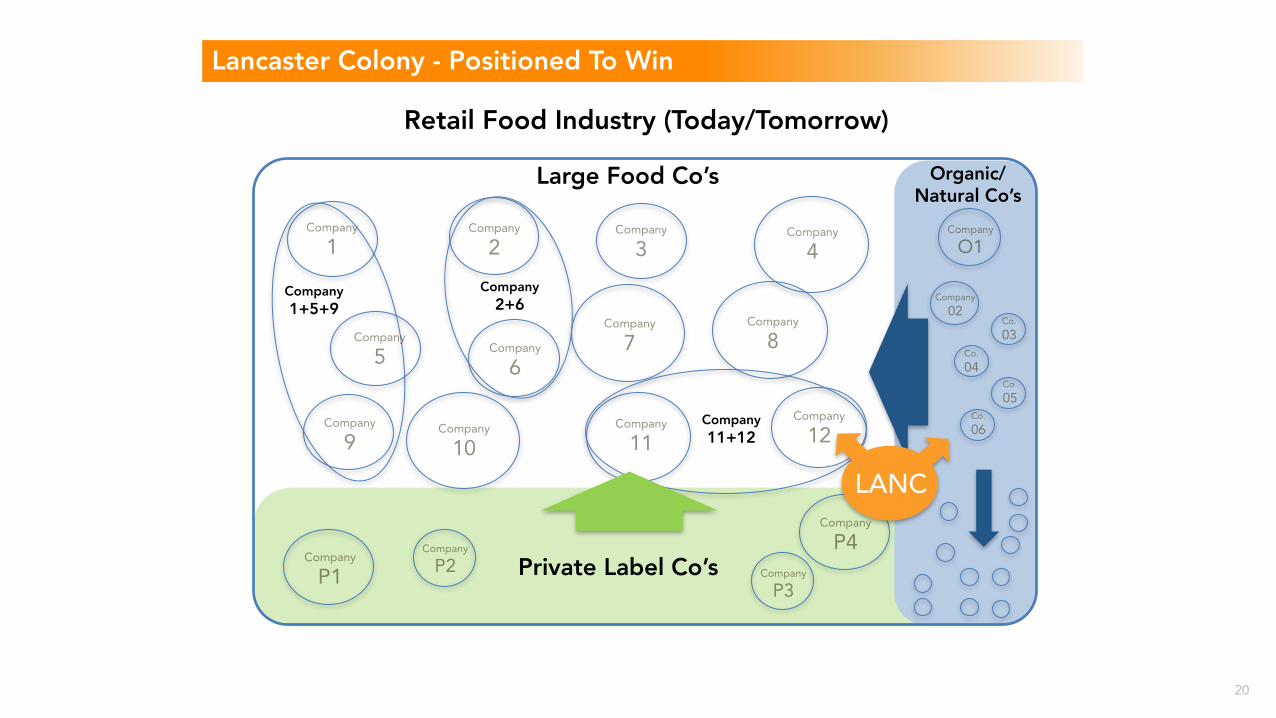

Demographic Changes Impacting the Food Industry

Retail Food Industry (Today/Tomorrow)

Company1+5+9

Company2+6

Company11+12

Private Label Co’s

19

Organic/Natural Co’s

Lancaster Colony - Positioned To Win

Retail Food Industry (Today/Tomorrow)

Private Label Co’s

LANC

Organic/Natural Co’s

Large Food Co’s

Company1+5+9

Company2+6

Company11+12

20

Growth – Portfolio Segmentation

Some Brands/Categories are Well Positioned for Strong Top-Line

Growth

Some Brands/Categories are Well Positioned for Strong OI and

Cash Flow

Growth BusinessesFocus, Invest, Grow

Foundation BusinessesSupport, Invest, Sustain

1st Choice is where we’ll play….Portfolio Segmentation

• Produce Dressings/ Dips• Fresh Dips• Branded Specialty

Bakery

• Frozen Bakery• Dry Grocery• Other Categories

Note: Olive GardenSM dressings are produced and sold to retailers under a licensing agreement with Darden Restaurants. 21

Growth – Three Imperatives

Accelerate Base Business Growth

Simplify OurSupply Chain

Expand Core w/ Focused M&A

Time

Gro

wth

+

+

2016 2021

=

Lancaster Colony

2nd Choice is how we’ll win…Focus on Three Imperatives

22

Growth – Three Imperatives

Accelerate Base Business Growth

Simplify Our Supply Chain

Expand Core w/ Focused M&A

Time

Gro

wth

+

+

2016 2021

=

Lancaster Colony

Accelerate Base Business Growth

2. Renovate Existing Products/Brands

3. Win at the Shelf

Operating Priorities

1. Launch New Innovation Platforms

23

Growth – Three Imperatives

Accelerate Base Business Growth

Simplify OurSupply Chain

Expand Core w/ Focused M&A

Time

Gro

wth

+

+

2016 2021

=

Lancaster Colony

Simplify Our Supply Chain

Operating Priorities

2. Integrated Business Planning

3. Optimize Supply Chain Capabilities

1. Lean Six Sigma/ Operational Excellence

24

Growth – Three Imperatives

Accelerate Base Business Growth

Simplify OurSupply Chain

Expand Core w/ Focused M&A

Time

Gro

wth

+

+

2016 2021

=

Lancaster Colony

Expand Core with Focused M&A

Operating Priorities

2. Focus on Branded Retail

1. Drive Profitable Growth

25

Net sales information is presented as originally reported in Lancaster Colony's Annual Report for the fiscal yearsending June 30. Therefore, certain years may not reflect adjustments for subsequent accounting changes.

*Compound Annual Growth Rate calculated from fiscal year 1972 through fiscal year 2016.

$1,200

$600

20161980 1990 2000

Net Sales $ in Millions

Compound Annual Growth Rate12%*

$5.2

1971 2010

Successful Track Record of Growth through Acquisitions

1969

1997

19781989

2000

2015

2003

26

Lancaster Colony Corporation

“The Better Food Company”“Better People, that Make Better Products, in a Better Corporate Culture,

that Work in Unison to Make the World a Little Bit Better Place”

27

Lancaster Colony Corporation

BAIRDJune 2017 Global Consumer,Technology & Services Conference