lawyer ceos and corporate innovation

TRANSCRIPT

Lawyer CEOs and Corporate Innovation*

Ronald Anderson

Fox School of Business

Temple University

Cheng “Jason” Jiang

Fox School of Business

Temple University

Barbara Su

Fox School of Business

Temple University

*We thank Claudia Custodio, Yi Liang, Kelvin Tan (discussant), and participants at the finance seminar of University

of Melbourne, Australian National University, Florida International University, and Asian Finance Association

Annual Meeting for helpful comments.

Lawyer CEOs and Corporate Innovation

Abstract

We examine whether CEOs with law education backgrounds (i.e., lawyer CEOs) exert a different

influence on firm innovation relative to other CEO types. CEOs with legal backgrounds arguably

enforce better compliance with governance, social and law norms than CEOs from other

backgrounds, leading to a more risk-averse approach to business activities and thereby impeding

corporate innovation. Consistent with this argument, we find that firms with lawyer CEOs are

associated with worse innovation outcomes, measured by patents and citations. This finding is

robust to alternative identification strategies, such as instrumental variable approach and coarsened

exact matching. Using a cross-sectional analysis, we further find that the negative association

between lawyer CEOs and corporate innovation is more pronounced when firm’s litigation risk is

higher. We also document the mechanism that lawyer CEOs spend less on R&D and capital

expenditures and are more likely to underinvest than non-lawyer CEOs. A rich set of robustness

tests are conducted to confirm the findings. To the best of our knowledge, we are the first to

document empirical evidence for the long-standing concern expressed by early studies (e.g., Hayes

and Abernathy 1980) that hiring CEOs with legal backgrounds decreases firms’ commitment to

innovation.

Keywords: lawyer CEO, innovation, risk taking

JEL Classification: G32, G38

3

1. Introduction

Chief executive officers (CEOs) influence and determine many strategic choices of firms,

including product innovation, resource allocation, and research and development budgets

(Bertrand and Schoar, 2003). Upper echelon theory (Hambrick and Mason, 1984) maintain that

strategic decisions partially derive from individuals’ traits and characteristics, suggesting that past

experience such as educational background influence firm investment decisions. Many firms

choose CEOs with legal education backgrounds (i.e., lawyer CEOs) to lead their organizations.

Past literature suggests that lawyer CEOs bring greater expertise to regulatory matters relative to

other CEO types. Jagolinzer et al. (2011), Kwak et al. (2012), Litov et al. (2013), Morse et al.

(2017), and Henderson (2017) find that executives and directors with legal expertise are

significantly less likely to experience corporate litigation than firms led by other CEOs, suggesting

that lawyer CEOs reduce firm risk through strong legal compliance.

Although lawyer CEOs appear to reduce litigation risk, many of the same traits leading to

better compliance potentially influence other aspects of firms’ operating and strategic decisions.

Legal education focuses on applying the principles and practices that society and governments

institute to regulate individuals’ and organizations’ behavior. Training in law focuses on the

downsides of engaging in particular actions. Business training conversely, focuses on activities

that grow and maximize shareholder wealth. Given the same operating or strategic decision, a

manager with legal training and a manager with business training potentially perceive the

associated risk factors in different ways. The manager with law education background arguably

pursues risk management through compliance and regulation. The manager with business

education background potentially sees risk management through the lens of shareholder wealth

4

maximization. These differing perspectives on risk suggest that CEOs with legal education

backgrounds may possess higher levels of risk aversion than CEOs with other backgrounds.

We examine the effect of lawyer CEOs on firm risk-taking. In particular, we investigate

the relationship between CEOs with legal education backgrounds and firm innovation relative to

CEOs without such educational backgrounds. Corporate innovation constitutes long-term, risky,

and unpredictable investments with a high probability of failure (Holmstrom, 1989). Innovation

however, determines a firm’s long-term success and represents an important driver of its economic

growth. Importantly, extant research indicates that CEOs with risk-taking traits (e.g., pilots

licenses, overconfidence, etc.) enhance firm innovation (Daellenback et al., 1999; Galasso and

Simcoe, 2011; Sunder et al., 2017). As previously noted, however, lawyer CEOs arguably exhibit

more risk aversion than other CEO types, suggesting that executives with legal education

backgrounds may detract from firm innovation.

Using a sample of 13,247 firm-years observations (representing 2,345 unique firms) from

year 2000 through 2008, we find that 9% of S&P 1500 firms employ lawyer CEOs. Our measures

of innovation outcomes are the number of patents that each firm files during the fiscal year and

eventually granted, and non-self patent citations, both of which are adjusted for truncation bias

(Hall et al., 2001, 2005; Amore et al., 2013; Fang et al., 2014; Sunder et al., 2017).

The primary analysis indicates that firms with lawyer CEOs experience worse innovation

outcomes than firms with non-lawyer CEOs. Specifically, in the first year after assuming control

of the firm, we find that lawyer-CEO firms report 9.5% fewer patents and 12.3% fewer patent

citations, respectively, relative to non-lawyer CEO firms. The analysis further confirms that in

subsequent years – second and third year after taking the leadership position – that the level of

innovation output in lawyer-CEO firms continues to significantly lag the innovation in non-lawyer

5

CEO firms. Firms with lawyer CEOs file 10.4% (12.1%) fewer patents and receive 13.6% (17.5%)

fewer patent citations in the second (third) year after the lawyer CEOs take the office. Our primary

results suggest that CEOs with legal education backgrounds, relative to non-legal education

backgrounds, impede corporate innovation.

In the empirical analysis, we control for numerous observable, including CEO’s risk-taking

incentives in compensation (vega and delta), CEO’s personal characteristics (e.g., tenure, age,

university choice, and business education) and firm characteristics (e.g., firm size, return on equity,

leverage, market-to-book) that could simultanenously affect firm’s decision to hire a lawyer CEO

and corporate innovation. Further, to ensure our results are not driven by other legal experts within

the firm such as General Counsels or directors with legal expertise, we control for the presence of

General Counsels in top management and the percentage of directors with a legal background. In

addition, we also include industry fixed effects, state fixed effects, and year fixed effects to reduce

the interference across the industries, states, and time.

However, we still cannot unambiguously infer that CEO’s legal training impedes firm

innovation. Firms may choose CEOs with this attribute for other reasons. Lawyer CEOs for

instance, could be chosen for their regulation and compliance acumen, future litigation events,

government relations, etc., indicating that our analysis suffers from a potential endogeneity

problem.

To strengthen the inference that we capture the effect of lawyer CEOs on firm innovation,

we use the following identification strategies. First, by using the coarsened exact matching (CEM)

approach, we match lawyer-CEO firms to non-lawyer CEO firms based on seven observable

characteristics that could affect a firm’s likelihood of hiring a lawyer CEO, which are firm’s prior

litigation experiences, size, market-to-book ratio, leverage, industry, state, and year. The data

6

balance is checked before and after the matching. The matched sample analysis provides results

similar to those from the main results of primary specification, suggesting that CEOs with law

backgrounds impede innovation relative to non-lawyer CEOs and that our results do not reflect

differences in firm characteristics that potentially influence firms to hire lawyer CEOs.

Second, we use an instrumental variable approach to investigate the relation between

lawyer CEOs and firm innovation. We employ two different instruments that drive the

appointment of lawyer CEOs but have no direct effects on firms’ patenting activity. Our first

instrument is adapted from Henderson et al. (2018). Based on the notion that firms having a larger

labor supply pool of potential CEO candidates with legal expertise are more likely to hire lawyer

CEOs, we instrument the presence of a lawyer CEO based on the percent of firms within a 100-

mile radius with a lawyer CEO. Our second instrument measures the lawyer density of the state

where the CEO attended college. The idea is that individuals who went to college in a place with

a higher density of lawyers are more likely to go to law schools and gain legal expertise. The

results of the two-stage least squares (2SLS) analysis from using only the first instrument and those

from using both instruments continue to hold, indicating that firms with lawyer CEOs achieve

fewer patents and receive fewer patent citations relative to non-lawyer CEO firms.

Third, to rule out the possibility of reverse causality that our findings of less innovation for

firms with lawyer CEOs are because less innovative firms are more likely to hire lawyer CEOs

afterwards, we conduct a temporal-based falsification test. We document that there is no sigifnicant

relationship between the past innovation outcome and hiring a lawyer CEO, confirming that lawyer

CEOs impede innovation, not that firms with less innovation tend to hire lawyer CEOs. This

addresses the concern that our results are driven by a certain type of firms’ inherent preference for

lawyer CEOs and reluctance for innovation.

7

We conduct a cross-sectional analysis to investigate if lawyer CEOs’ risk aversion is the

reason driving the negative association between lawyer CEO and corporate innovation. Our

analysis shows that the negative relationship between lawyer CEO and corporate innovation is

more pronounced for firms that face higher litigation risk, confirming that lawyer CEOs’ fear of

litigation risk and its associated costs provides a disincentive for them to promote innovative

activity. The results provide strong evidence of our assertation that lawyer CEOs exhibit more risk

aversion than other CEO types.

To shed light on the mechanisms through which lawyer CEOs impede corporate innovation,

we study the association between lawyer CEOs and firms’ investment policies. Our findings

suggest that lawyer CEOs spend less on R&D investments and capital expenditures and are more

likely to underinvest than non-lawyer CEOs, which leads to worse innovation outcomes.

Further, to rule out the alternative possibility that lawyer CEOs’ pursuit in filing lawsuits

distract them from committing to innovation, we show that lawyer CEOs are not more likely to

initiate lawsuits against other parties than non-lawyer CEOs. We confirm that lawyer CEOs are

associated with less innovation output because they are more risk-averse and choose to invest less

in innovative activities, instead of being distracted from innovative activities.

A rich set of robustness checks are conducted to assess the sensitivity of our main findings.

Given that the patent and citation data have non-negative values and are right-skewed with a large

proportion of the observations of zero, we perform additional tests using different models

including Tobit model and Poisson model, and find the similar results. In our main analysis, we

use truncation-adjusted patent and patent non-self citation counts following prior research (Hall et

al., 2001, 2005; Amore et al., 2013; Fang et al., 2014; Sunder et al., 2017). To additionally assess

8

the robustness of our results, we use alternative measures of innovation outcomes, such as the raw

number of patents and citation. The results continue to remain.

It is possible that legal expertise is highly useful for firms that operate in highly competitive

industries and receiving patent and citations is difficult for these firms. As another robustness

check, we control for product market competition using the measure proposed by Hoberg and

Phillips (2016) and continue to find the same results. Further, we include firm’s R&D and capital

expenditures as additional control variables and the results continue to hold.

To address the possibility that our results are driven by the industries and states with a high

presence of lawyer CEOs, we repeat our analysis after removing the companies in the utilities

industry and in Washington DC. We continue to see that lawyer CEOs impede innovation in the

subsample. We also reconduct our tests when removing the 2007-2009 financial crisis period and

continue to find similar results, suggesting that a firm’s financial streses during this period doesn’t

alter our analysis.

Our study contributes to the literature in at least three ways. First, we contribute to the

growing literature on whether executives or directors’ legal expertise influences firm behavior.

Henderson et al. (2018) find that firms with lawyers CEOs are associated with lower litigation

frequency and less severe litigation. Pham (2020) document higher stock market liquidity for firms

with lawyer CEOs versus for those with non-lawyer CEOs. Chen et al. (2021) show that lawyer

CEOs play an informative role in firms’ litigation loss contingency disclosure by providing

disclosures about a pending litigation case on a timelier basis compared to non-lawyer CEOs. To

the best of our knowledge, this paper is the first study to document empirical evidence for the long-

standing concern expressed by early studies (e.g., Hayes and Abernathy, 1980) that hiring CEOs

with legal backgrounds decreases firms’ commitment to innovation.

9

Second, we add to the existing literature that builds on Hambrick and Mason’s (1984)

“Upper Echelons Theory”, which suggests that individual managerial characteristics affect

corporate decisions and therefore outcomes. Consistent with this theory, Bertrand and Schoar

(2003) document that the personality traits, work experience, and education background of

individual manager explain a significant portion of the heterogeneity of corporate investment

behavior, financing policy, organizational strategy and performance. We add to this literature by

introducing the effect of CEOs’ law education background on corporate innovation.

Third, we contribute to the expanding literature on corporate innovation. Innovation

constitutes an important driver of economic growth, and prior research identifies a variety of

factors that affect corporate innovation such as analyst coverage (He and Tian, 2013), shareholder

type (Brav et al., 2018; Liu et al., 2019), and financial market development (Amore et al., 2013;

Cornaggia et al., 2015). We add to this line of research by documenting another important

determinant of corporate innovation and shedding light on the longstanding concern that lawyer

CEOs deter corporate innovation.

The remainder of this paper is organized as follows. Section 2 describes the research design.

Section 3 presents our empirical findings. Section 4 concludes.

2. Research Design

2.1 Data and Sample

Our sample is constructed from several databases. We obtain personal information about

CEOs and boards of directors from BoradEx, and we obtain executive compensation information

from ExecuComp. For the CEOs and boards of directors whose background information is not

covered by BoardEx or ExecuComp, we hand collect data from firms’ proxy statements and

10

Google. The accounting data of firm characteristics are from Compustat and stock return data are

from CRSP.

Following the innovation literature (e.g., Gu, Mao, and Tian, 2015; Mao and Zhang, 2018),

we collect the patent data from the National Bureau of Economic Research (NBER) U.S. Patent

Citations Data File, which contains patent applications filed prior to 2006. We then use

supplemental data from 2006 to 2010 provided by Kogan et al. (2017), which contains patents

filled till 2009 and granted till 2010.

Our sample period is from 2000 to 2010. Our sample period starts in 2000 because 2000 is

the first year that BoardEx data are available. We end our sample in 2010 because this is the last

year that we have the patent data for. We exclude firm-years with negative book equities and

require the firm-years to have non-missing data for the regressions. After imposing these data

restrictions, our final sample consists of 13,247 firm-year observations, representing 2,382 unique

firms. In Section 3.5, we follow prior studies (e.g., Mao and Zhang, 2018) to conduct robustness

checks using alternative samples. We repeat our analysis after removing the companies in the

utilities industry and financial industry. We also remove the 2007-2009 financial crisis period from

our sample to confirm that our findings are not driven by the financial crisis period.

2.2 Model Specification and Variable Construction

We estimate the following baseline regression model to examine the association between

CEO’s law education background and corporate innovation:

Innovation = 𝛽0 + 𝜷𝟏LawyerCEO + 𝛽2CEOtenure + 𝛽3CEOage + 𝛽4CEOdelta

+ 𝛽5CEOvega + 𝛽6LawyerDirectorPct + 𝛽7Size + 𝛽8ROE + 𝛽9MB

+ 𝛽10Leverage + 𝛽11FirmAge + 𝛽12Ivy + 𝛽13MBA + 𝛽14GC

+ Industry Fixed Effects + Year Fixed Effects + State Fixed Effects + ε

(1)

Following prior research (e.g., Amore et al. 2013), we use patenting activities outcome as

11

the proxies for corporate innovation. Our first measure is innovation quantity, which is measured

by the total number of patent applications filed in a given year and eventually granted. There are

one to three years’ gap between patent application year and patent grant year (Hall et al. 2001,

2005), and the patent application year is closer to the actual timing of innovation activities than

the patent grant year. Therefore, we choose the patent application year instead of patent grant year.

Our second measure is innovation quality, which is the number of citations each patent receives in

subsequent years.

Prior research suggests that the raw number of patents and citations may have truncation

problems in the following ways (Hall et al. 2001, 2005; Fang et al. 2014). First, the patents appear

in the database only after they are granted but there is a lag between a patent’s application year

and grant year. Second, a patent can keep receiving citations over long periods of time, but we

only observe citations until the last year of the available patent data. We follow the existing

literature (Fang et al. 2014) to calculate truncation-adjusted patent counts by dividing raw patent

counts with the sum of application-grant lag distribution, and compute truncation-adjusted citation

counts by dividing raw citation counts with the fraction of predicted lifetime citations actually

observed during the lag interval. We also exclude self-citations to address the potential concern

that the results are driven by firms’ choice to cite their own patents.

The distributions of patent counts and non-self citations counts in our sample are both right-

skewed, with their median at zero. We winsorize these variables at the 1st and 99th percentile and

then use natural logarithm of one plus patent counts and non-self citations counts. Our first measure

of innovation is LogNPatentsAdj, calculated as the log value of the total number of patent

applications filed and eventually granted after adjusting for truncation bias. The second measure

is LogNCitesNonSelfAdj, calculated as the log value of the total number of non-self citations after

12

adjusting for truncation bias. Because innovation output such as patents and citations is the

outcome of a research and development process that take time (Amore et al. 2013), we follow

Cornaggia et al. (2015) to examine the impact of lawyer CEO on LogNPatentsAdj and

LogNCitesNonSelfAdj from year t+1 to t+3. In Section 3.5 of Robustness Check, we also use

several alternative measures of innovation outcomes to confirm the findings, such as the raw

counts of patents and citations that include self-citations.

Our key independent variable of interest is LawyerCEO, an indicator variable constructed

following Henderson et al. (2018). LawyerCEO is equal to one if the CEO holds an undergraduate

degree in law such as an LLB, or a graduate degree such as LLM, J.D., or Ph.D. in Jurisprudence.

β1 captures the estimate for the effects of lawyer CEO and corporate innovation. If lawyer CEOs’

risk aversion impedes firm innovation, we expect β1 to be significantly negative.

We include a variety of control variables. Specifically, we include CEO pay-performance

sensitivity (CEOdetla) and CEO pay-risk sensitivity (CEOvega) to account for the potential impact

of incentives embedded in CEO compensation as suggested by previous research (Coles et al.,

2006; Mao and Zhang, 2018; Chemmanur et al., 2019). We also control for other CEO

characteristics that may affect firm patenting activities including CEO’s tenure length

(CEOtenure), age (CEOage), education backgrounds such as whether the CEO has an MBA degree

(MBA) or has attended an Ivy League School (Ivy). Further, to ensure our results are not driven by

other legal experts within the firm such as GCs or directors with legal expertise, we control for the

presence of General Counsels in top management (GC) and the percentage of directors with a legal

background (LawyerDirectorPct). We also follow prior literature (e.g., Fang et al., 2014) to control

for firm characteristics such as firm size (Size), firm age (FirmAge), return on equity (ROE), market

to book value of total assets (MB) and leverage ratio (Leverage). We include industry fixed effects

13

to control for industry unobserved time-invariant heterogeneities and year fixed effects to control

for macroeconomic shocks that may affect all the sample firms in a given year. Our industry

classification in the regressions is based on the first two digits of the SIC code. We also include

state fixed effects to control for the heterogeneity in the legal environment complexity across states.

Following Pan et al. (2020), we cluster standard errors at the industry level to account for serial

correlation across all firms within an industry over time. All the continuous variables are

winsorized at the 1st and 99th percentiles to mitigate the influence of outliers. The definitions of all

variables can be found in Appendix A.

3. Findings

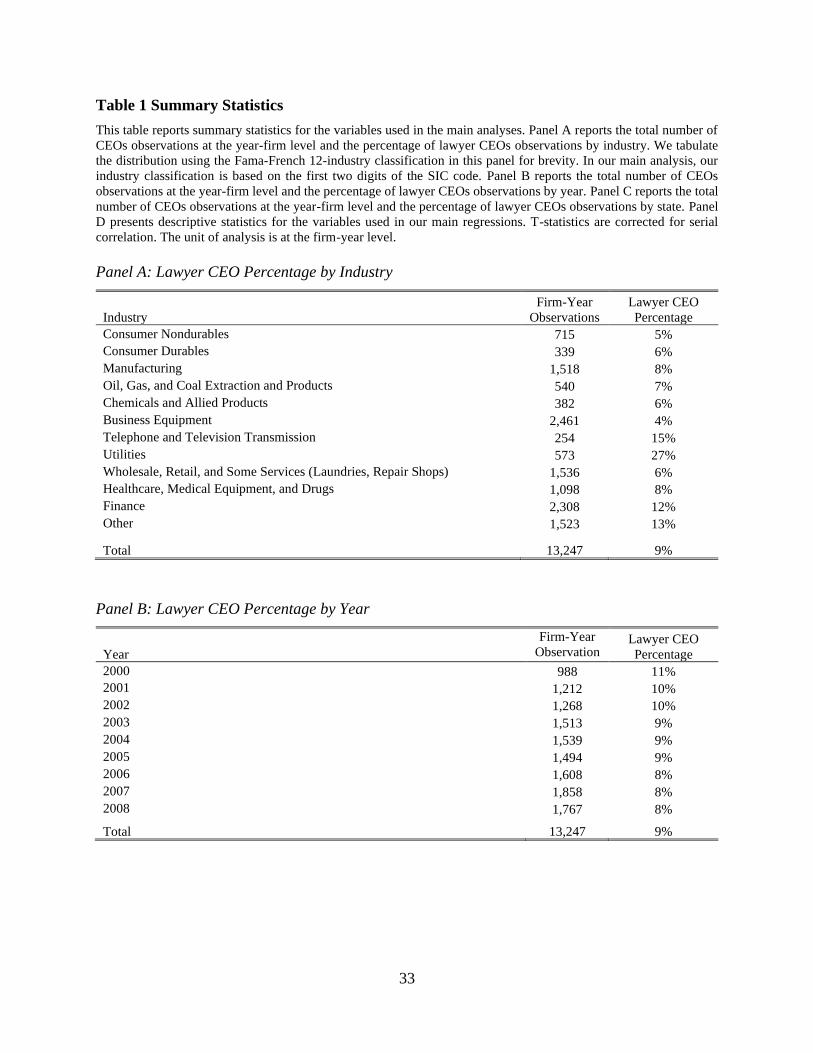

3.1 Descriptive Statistics

Table 1 reports summary statistics for our sample. To better understand our sample

composition, we present lawyer CEO distribution by industry in Panel A.2 The findings suggest

that, on average, 9% of firms in our sample have a lawyer CEO. This statistic is consistent with

Henderson et al. (2018).

The distribution of firms with lawyer CEOs is uneven across the states, industry, and time.

For example, 43% of firms in DC hire lawyer CEOs, while several states have 0% of firms with

lawyer CEOs. The utilities industry has the highest percentage of lawyer CEOs (26%) and the

business equipment industry has the lowest percentage of lawyer CEOs (4%). There exists a slight

downward trend in hiring lawyer CEOs. The average percentage drops from 11% in year 2000 to

8% in year 2008.

2 We tabulate the distribution using the Fama-French 12-industry classification in this panel for brevity, while our

industry classification is based on the first two digits of the SIC code in the main analysis.

14

Panel C of Table 1 shows the descriptive statistics for the main variables used in our

analysis. Consistent with prior research, the number of patents filed is right-skewed as the average

firm files 9.05 patents in t+1 and the median number of patents filed is zero. Therefore, we use the

natural log of patent counts and citation counts in the regressions. On average, 12% of the directors

have a law education background and 31% of the firms have general counsels in the top

management team. The distributions of the variables are largely consistent with our expectation.

Univariate t-test results show that firms with lawyer CEOs file fewer patents and receive fewer

citations than firms with non-lawyer CEOs one to three years after the lawyer CEOs take the office.

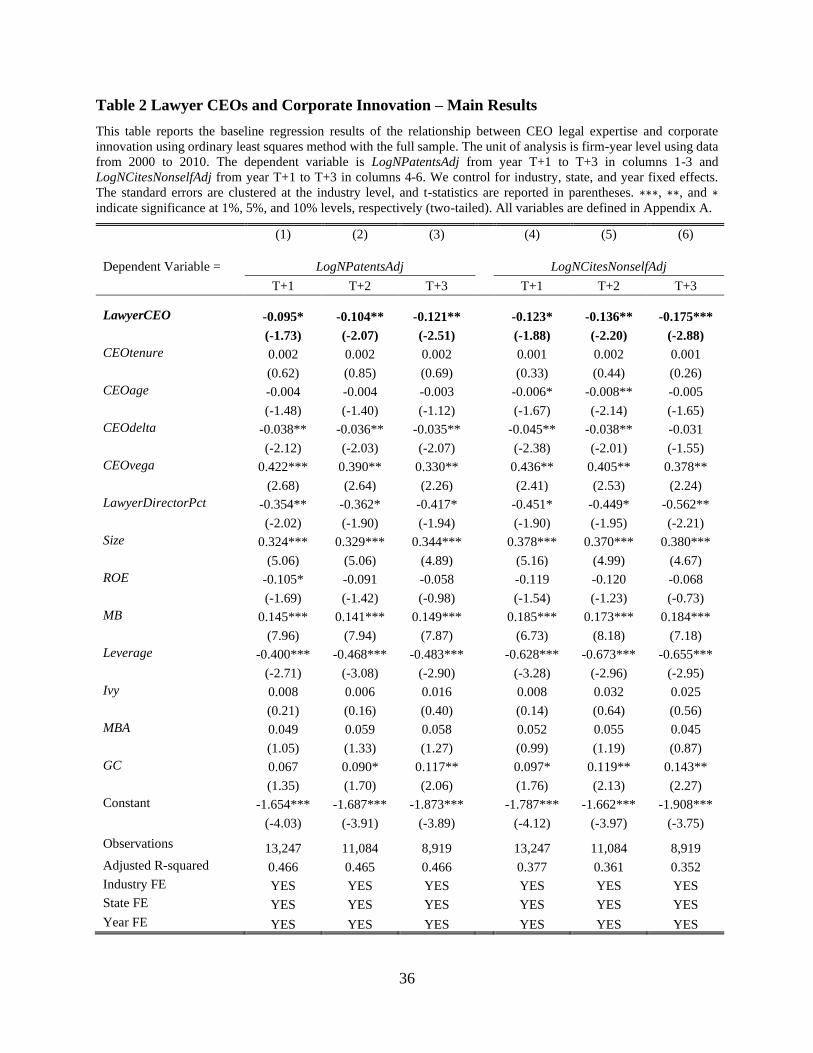

3.2 Main Analysis

We first study the association between lawyer CEOs and corporate innovation using the

baseline regressions including control variables and fixed effects. Table 2 presents the estimation

results of equation (1) using ordinary least squares regressions. In columns 1 to 3, we regress the

log value of the truncation-adjusted total number of patent applications filed and eventually

granted (LogNPatentsAdj) in year t+1 to t+3 on LawyerCEO, the control variables, and industry

and year fixed effects. We document a negative relationship between patent quantity and lawyer

CEOs. The coefficients on LawyerCEO are negative in columns 1 to 3, and are also economically

significant. For example, the coefficient on LawyerCEO -0.100 in column 1 suggests that firms

with lawyer CEOs file 9.5% fewer patents than firms with non-lawyer CEOs. The coefficients on

LawyerCEO in column 2 and 3 indicate that firms with lawyer CEOs file 10.4% and 12.1% fewer

patents in the second and third year after the lawyer CEOs take the office, compared with firms

with other types of CEOs.

15

The signs of the coefficient estimates for the control variables are largely consistent with

our expectations. For example, firms with a larger size, higher market to book ratio, and lower

leverage file more patents. The coefficient on CEOvega is positive, consistent with prior literature

that vega in CEO compensation encourages risk taking (Coles et al., 2006, Mao and Zhang, 2018).

In columns 4 to 6, the dependent variables are the log value of truncation-adjusted non-self

citations recived from year t+1 to t+3, and the regression coefficients on LawyerCEO are

significantly negative. Using a similar calculation, firms with lawyer CEOs receive 12.3%, 13.6%,

and 17.5% fewer non-self citations than firms with non-lawyer CEOs in year t+1, t+2, and t+3.

Collectively, the results in Table 2 are consistent with our prediction that lawyer CEOs’

risk aversion discourages firms’ innovation. In addition, we also find the coefficients on

LawyerCEO and on MBA are significantly different, supporting our arguments earlier that legal

education and business training have different focuses.

16

3.3 Identification Strategies

Firms and CEOs associate by mutual choice, which raise concerns of potential endogeneity

issues. Lawyer CEOs could be chosen because of their regulation and compliance acumen, future

litigation events, government relations, etc. It is possible that certain firm characteristics are

simultaneously related with lawyer CEO appointment and firm patenting activities, and hence

statistically bias the estimation results. It is also possible that our findings of less innovation for

firms with lawyer CEOs are because less innovative firms are more likely to hire lawyer CEOs,

leading to reverse causality. To strengthen the inference that we capture the effect of lawyer CEOs

on firm innovation, we use a variety of identification strategies, including coarsened exact

matching, instrumental variable, and falsification tests.

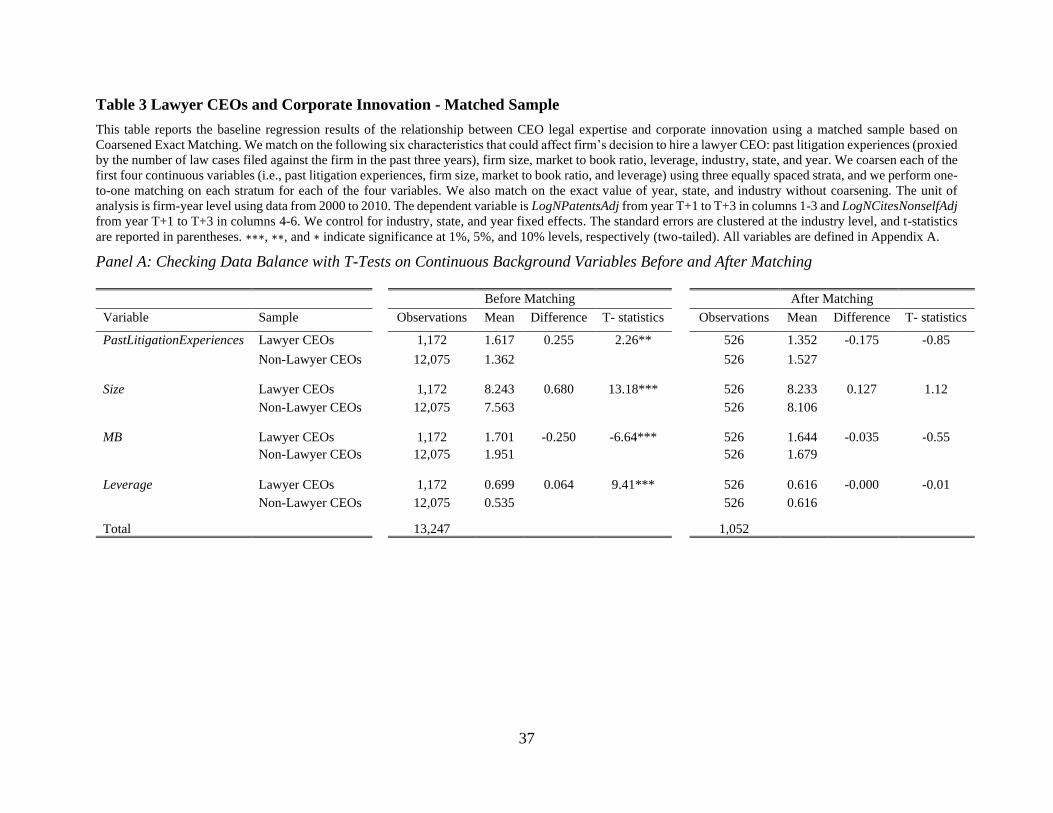

3.3.1 Coarsened Exact Matching

To address the possibility that certain firm characteristics are simultaneously associated

with lawyer CEO appointment and corporate innovation, we match firms with lawyer CEOs with

those with non-lawyer CEOs on observable firm characteristics that may affect firms’ decision to

hire lawyer CEOs using the Coarsened Exact Matching (CEM) method. Specifically, we match

these two groups of firms on the following seven dimensions of characteristics: firms’ past

litigation experience (proxied by the number of law cases filed against the firm in the past three

years), firm size, market to book ratio, leverage, industry, state, and year. We coarsen firm’s past

litigation experience, firm size, market to book ratio, and leverage using three equally-spaced strata,

and we perform one-to-one matching on each stratum for each of the variables. We also one-to-

one match on the exact value of year, state, and industry without coarsening.

17

The number of observations in the matched sample is significantly reduced in this analysis

because we use one-on-one matching. The t-tests results for data balance check before and after

matching are listed in the Panel A of Table 3. The results of t-tests show that the means of

background characteristics for firms with a lawyer CEO are significantly different from those with

a nonlawyer CEO before matching. However, the difference in the means of background

characteristics for firms with a lawyer CEO versus those with a nonlawyer CEO become

statistically insignificant after matching. This indicates that the data is balanced between two

groups and our matching is successful.

We present the baseline regression results using this matched sample in the Panel B of

Table 3. The regression coefficient on LawyerCEO continues to be negative and significant. Again,

this finding suggests that our inferences using the full sample are not affected by different firm

characteristics or industry membership between firms with lawyer CEOs and those without.

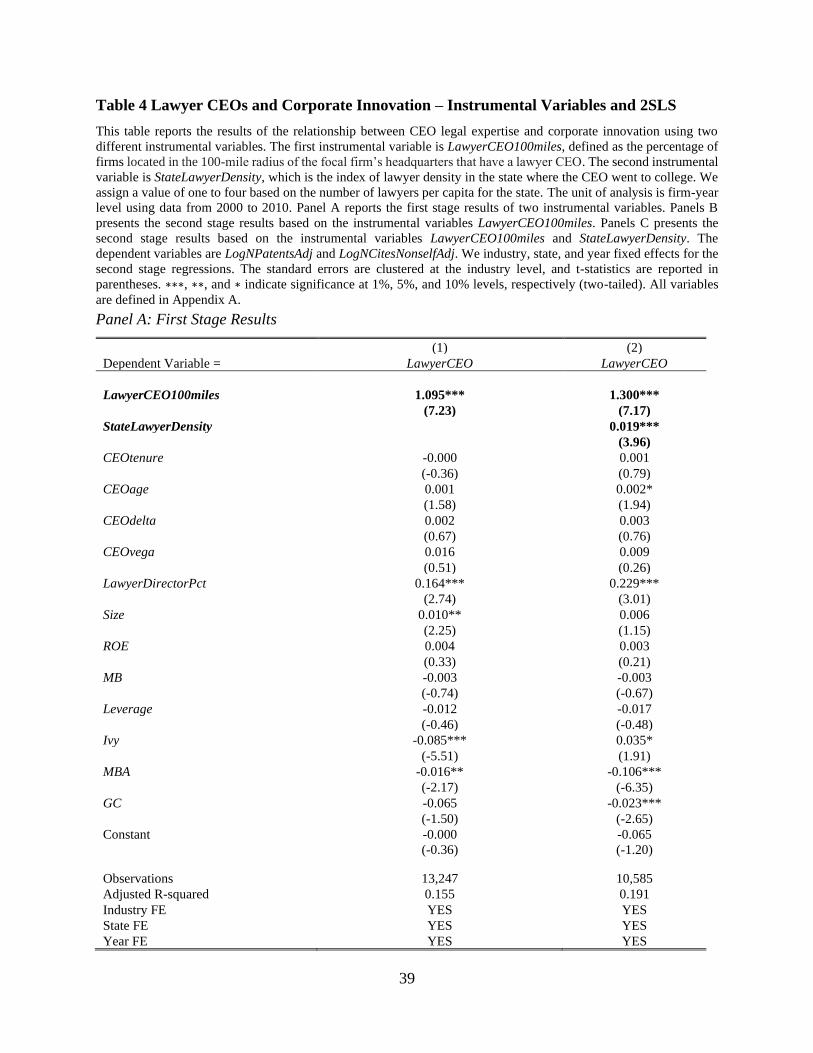

3.3.2 Instrumental Variable Analysis

It is possible that the CEO selection process is driven by a correlated omitted variable.

Since the coarsened exact matching approach only addresses endogeneity concerns related to CEO

selection on observable characteristics, we use an instrumental variable approach to further address

the potential endogeneity issues caused by unobservables. We use two different instruments that

drive the appointment of lawyer CEOs but have no direct effects on firms’ patenting activity.

Our first instrument, LawyerCEO100miles, is adopted from Henderson et al. (2018).

LawyerCEO100miles is calculated as the percentage of firms located in the 100-mile radius of the

focal firm’s headquarters that have a lawyer CEO.3 This instrumental variable captures the local

3 Following Heider and Ljungqvist (2015), we correct the historical firm headquarter locations provided in Compustat

using headquarter states reported in the SEC filings.

18

supply of prospective lawyer CEOs. The logic behind this instrument is that firms having a larger

labor pool of potential CEO candidates with legal expertise are more likely to hire lawyer CEOs,

indicating the relevance of the instrumental variable. On the other hand, the percentage of local

firms having lawyer CEOs has no direct effect on the focal firm’s innovation, which satisfies the

exclusion condition of an instrumental variable.

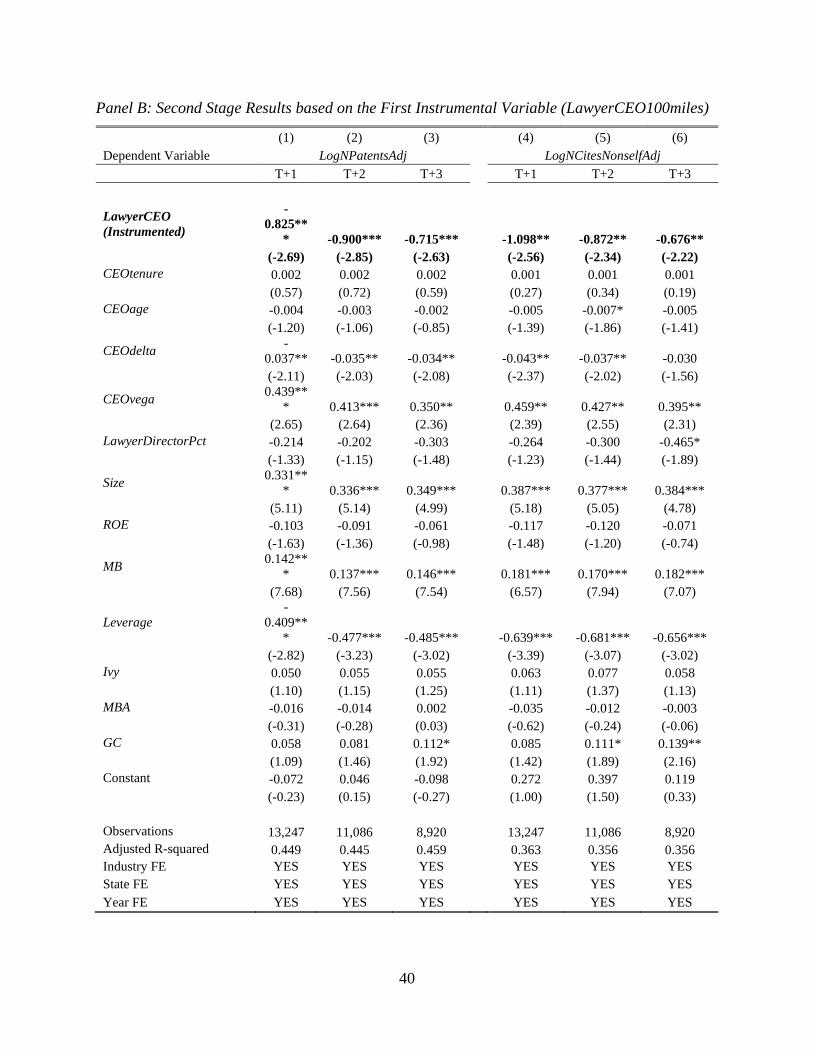

The results of the Two-Stage Least Squares (2SLS) analysis are presented in Table 4. In

column 1of Panel A, we regress LawyerCEO on the instrumental variable, LawyerCEO100miles,

along with other control variables for the first stage. The result shows that LawyerCEO100miles

is positively associated with a probability of hiring lawyer CEOs, which statistically confirms the

satisfaction of the relevance condition of an instrumental variable. This is consistent with our

expectation that a higher local supply of potential lawyer CEO candidates increases the chance of

a firm to hire a lawyer CEO. Panels B of Table 4 present the second stage results based on the

instrumental variable, LawyerCEO100miles. The regression coefficients on instrumented

LawyerCEO are significantly negative across all columns, confirming that laywer CEOs impede

corporate innovation.

Our second instrument is StateLawyerDensity, which measures the lawyer density of the

state where the CEO attended college. We assign a value of one to four based on the number of

lawyers per capita for the state. If the CEO went to a non-US institution for college, we assign a

value of zero. This variable captures an individual’s likelihood to go to law school. The idea is that

individuals who went to a college in a state with a higher density of lawyers are more likely to go

to law schools. 4 In column 2 of Panel A in Table 4, the regression coefficient on

4 Lent et al. (2002) document that contextual factorsplay a role in collegue students’ career choice. We otain the data

for the number of lawyers per capita by state from Indiana Bar Association.

https://cdn.ymaws.com/www.inbar.org/resource/resmgr/Conclave/_Rural_Access_Highest_Per_Ca.pdf. This is the

earliest data for the number of lawyers per capita by state we are able to identify.

19

StateLawyerDensity is positively significant, which statistically prove the relevance condition that

those who went to a college located in a place with a higher density of lawyers have a higher

likelihood to pursue law education and gain legal expertise. Besides, the CEOs’ choice of college

had been made well before he or she became CEOs and therefore is unlikely to have a direct impact

on firm innovation, indicating that the exclusion condition of a instrumental variable is satisfied.

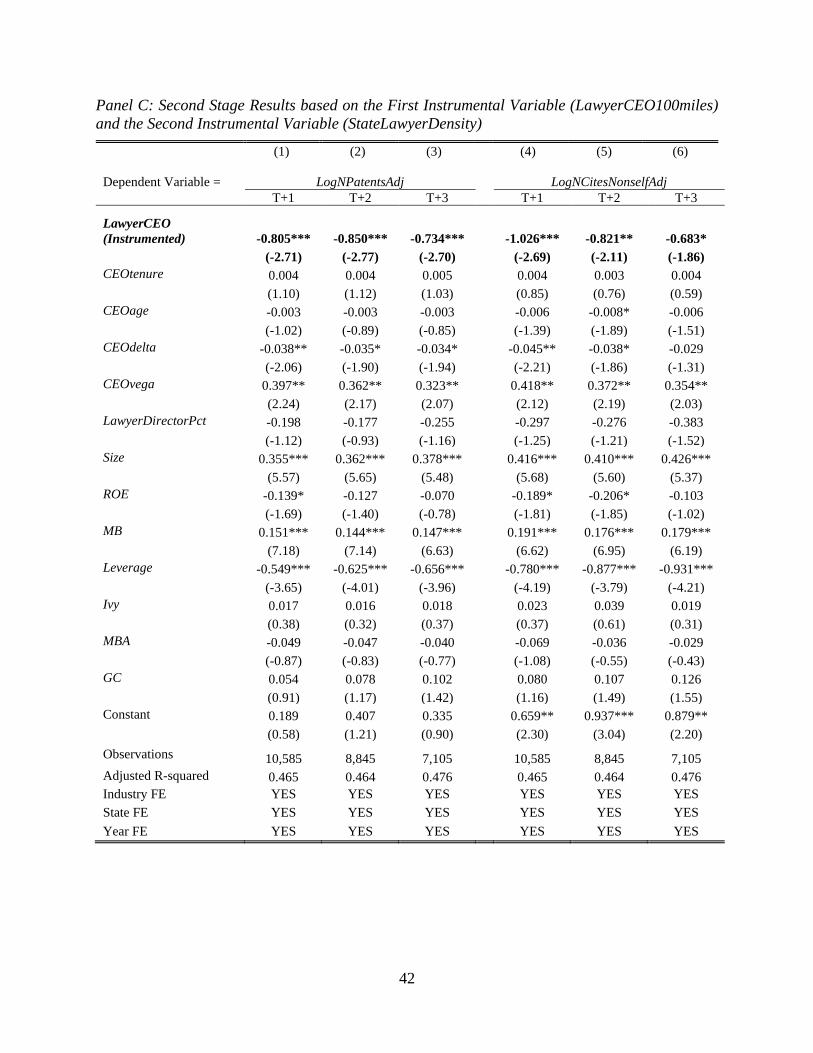

The second stage results of using both instrumental variables, LawyerCEO100miles and

StateLawyerDensity, are listed in the Panels C of Table 4. Again, the instrumented LawyerCEO

has significantly negative regression coefficients across all columns. The findings of both

instrumental variables provide us with more confidence that our results, lawyer CEOs impede

corporate innovation, are not biased by endogeneity.

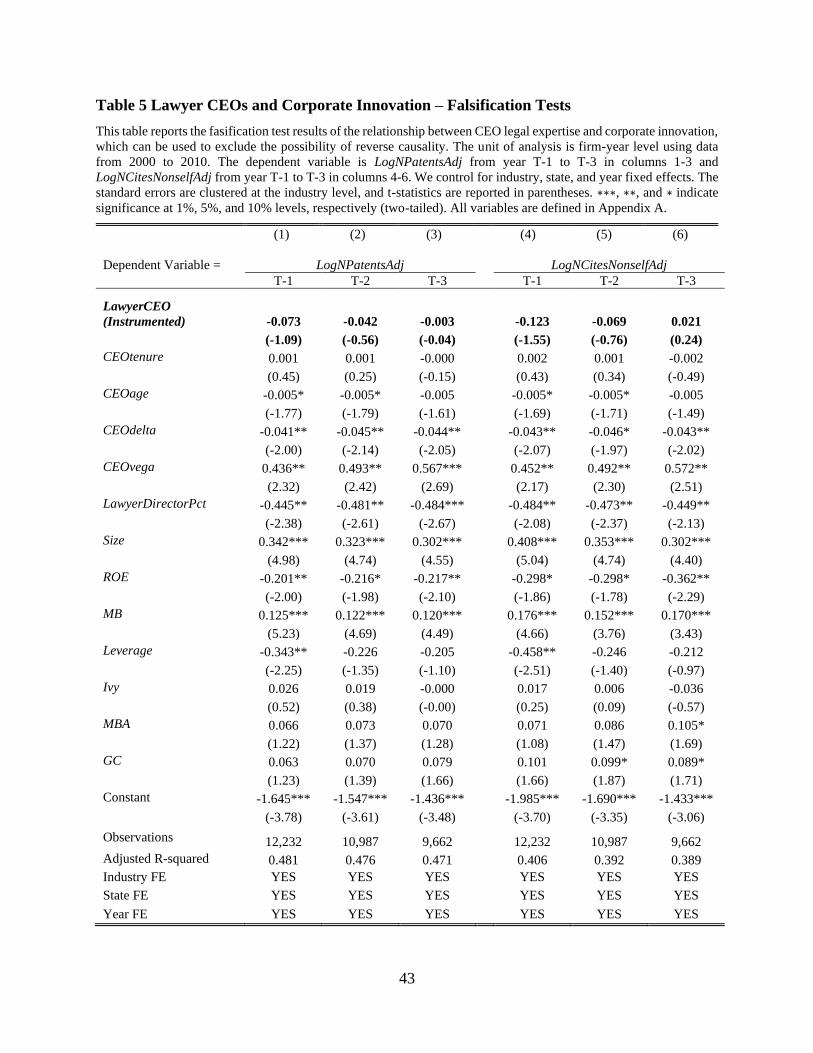

3.3.3 Falsification Test

To further rule out the reverse causality possibility that our findings of less innovation for

firms with lawyer CEOs are because less innovative firms are more likely to hire lawyer CEOs

afterwards, we conduct a temporal-based falsification test. We study patent outcomes in the past

three years relative to the year when a lawyer CEO takes the office. The results from Table 5 shows

that the findings documented in the previous sections do not hold when we examine the

relationship between lawyer CEO in year t and firm patenting activities in years t-1, t-2, and t-3,

suggesting that there is no significant relationship between the past innovation outcome and hiring

a lawyer CEO. Therefore, it is confirmed that lawyer CEOs impede innovation, not that firms with

less innovation tend to hire lawyer CEOs.

20

3.4 Supplemental Analysis

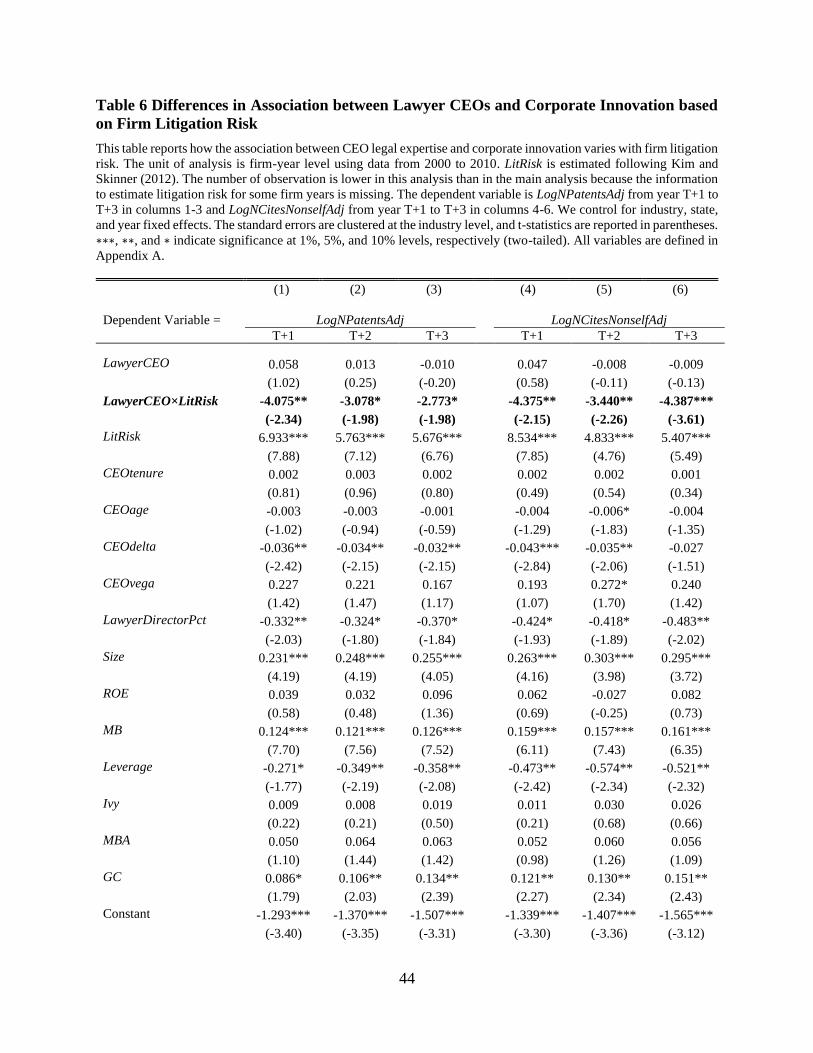

3.4.1 Cross-sectional Analysis Based on Firm Litigation Risk

After establishing a negative association between CEOs’ law backgrounds and corporate

innovation, we next examine if lawyer CEO’s risk aversion is the reason behind this negative

association. In particular, we investigate how this relationship varies with firm litigation risk.

Kempf and Spalt (2020) show that innovative firms are vulnerable to costly low-quality class

action litigation. Therefore, fear of litigation risk and its associated costs by lawyer CEOs provides

a disincentive for them to promote innovative activity.

We expect that the negative association between lawyer CEO and corporate innovation is

more pronounced for firms that face higher litigation risk. To test this prediction, we follow Kim

and Skinner (2012) to estimate firm litigation risk5 as the likelihood of being sued. The results of

this cross-sectional analysis are presented in Table 6. We document a negative coefficient on the

interaction term LawyerCEO×LitRisk, which suggests that when firm litigation risk is higher,

lawyer CEOs are less likely to engage in innovative activities due to their concerns over litigation

risk and costs. The results further confirm our expectation that lawyer CEOs impede innovation

because of their risk aversion.

5 Firm litigation risk is estimated following Kim and Skinner (2012). Specifically, we use the predicted values

estimated from the model: Suedt = 𝛾0 + 𝛾1FPSt-1 + 𝛾2Sizet-1 + 𝛾3SalesGrowtht-1 + 𝛾4Return t-1 + 𝛾5ReturnSkewness t-1

+ 𝛾6ReturnStd t-1 + 𝛾7Turnover t-1 + 𝜃, where Sued is an indicator variable that equals one if a class action lawsuit is

filed against the firm and zero otherwise. FPS is an indicator variable that equals one if the firm is in the biotech,

computer, electronic, or retail industry and zero otherwise. ReturnSkewness and ReturnStd represent the skewness and

standard deviation of monthly stock returns for a given year. Turnover is the trading volume scaled by the number of

shares outstanding.

21

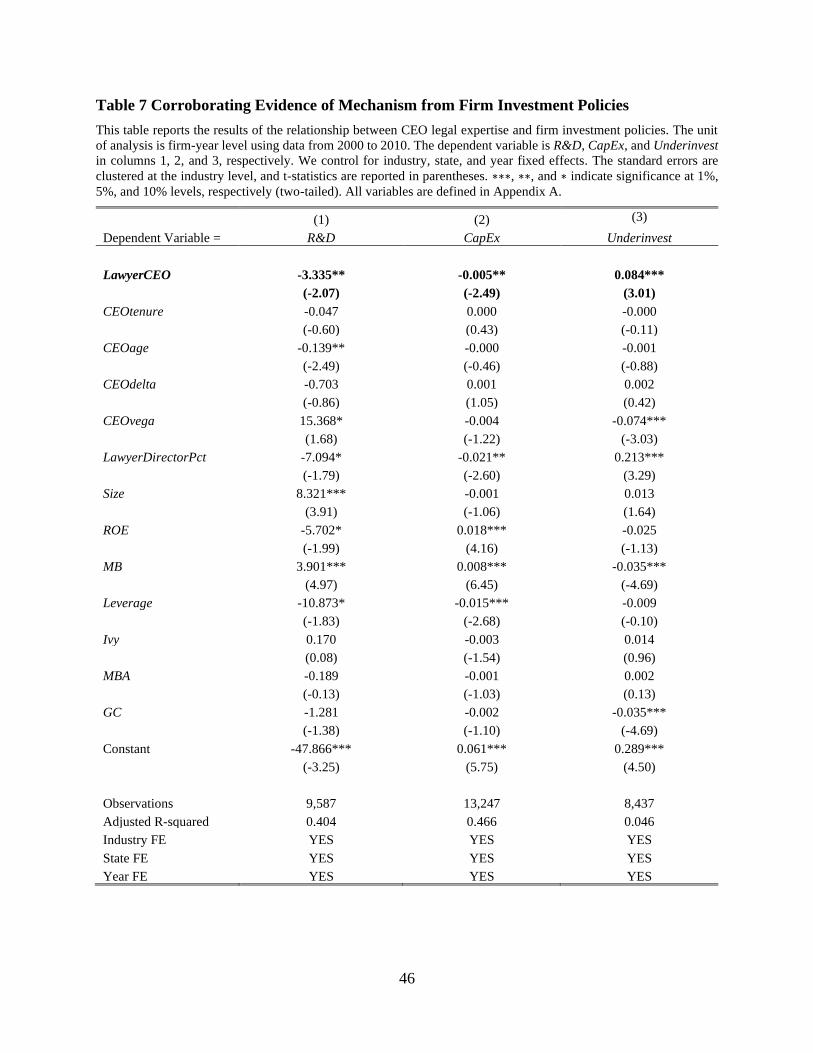

3.4.2 Corroborating Evidence of Mechanism from Firm Investment Policies

In the sections above, we provide evidence of a negative relation between CEOs’ legal

backgrounds and firm innovation, and we argue that the relation is the result of lawyer CEOs’ risk

aversion. In this section, we study the mechanism for this negative association by studying the

association between CEOs’ legal backgrounds and firm investment policies. Our proxies for

investment policies include research and development expenses scaled by lagged sales (R&D),

capital expenditures scaled by lagged total assets (Capex), and the likelihood of underinvestment

(UnderInvest). We construct the measure of underinvestment (UnderInvest) following Biddle et

al. (2019). Specifically, we regress the total investment in year t on the percentage change in sales

from year t-1 to t by industry-year. The total investment is the sum of capital expenditures, R&D

expenses and acquisitions minus sales of property, plant, and equipment, scaled by lagged total

assets. We then classify firms based on the residuals (i.e., deviations from predicted investments),

and firm-years in the bottom quartile are identified as under-investing and those in the top quartile

are identified as over-investing. The middle two quartiles are identified as the benchmark group.6

The results of the effect of lawyer CEOs on corporate investment policy are reported in

Table 7. Consistent with Henderson et al. (2018), our results in column 1 suggest that lawyer CEOs

spend less on R&D than non-lawyer CEOs. Column 2 shows a negative association between CEOs’

legal backgrounds and firm capital expenditures. Finally, in column 3, our result suggests that

lawyer CEOs are more likely to under-invest than non-lawyer CEOs. Collectively, the results in

this section provide strong evidence of our assertation that lawyer CEOs exhibit more risk aversion

6 The inferences remain unchanged if we include the top quartile as the the benchmark group. The number of

observations is lower than in the main tests because we follow Biddle et al. (2019) in requiring each regression to have

at least 20 observations when estimating deviations from predicted investments at the industry-year level.

22

than other CEO types and therefore are less likely to engage in innovation-related investment,

resulting in worse innovation outcomes.

3.4.3 Addressing Alternative Explanation

It is also possible that lawyer CEOs could be more likely to file lawsuits due to their legal

astuteness and their attention could be distracted away from innovation activities. Prior literature

suggests that attention is generally considered a resource in limited supply (e.g., Kahneman 1973).

If lawyer CEOs, in their zeal for initiating lawsuits against other parties, are distracted from

business operations and innovative activities, we may also observe firms with lawyer CEOs are

associated with less innovation output.

To ensure that our findings are not driven by this possibility, we analyze the impact of

lawyer CEOs on firms’ likelihood of filing lawsuits. We construct a variable, FileLawsuit, which

is an indicator variable that equals one if the firm files a lawsuit in a given year and zero otherwise.

The results are presented in Table 8. We do not find evidence that lawyer CEOs file more lawsuits,

suggesting that our main findings are not driven by this possibility of distraction. Therefore, we

confirm that lawyer CEOs impede innovation because they are more risk averse.

3.5 Robustness Tests

In order to assess the sensitivity of our main findings, we perform a rich set of additional

robustness tests in this section, including the estimation of different models, use of alternative

measures of variables, adding additional control variables, and subsample analysis.

23

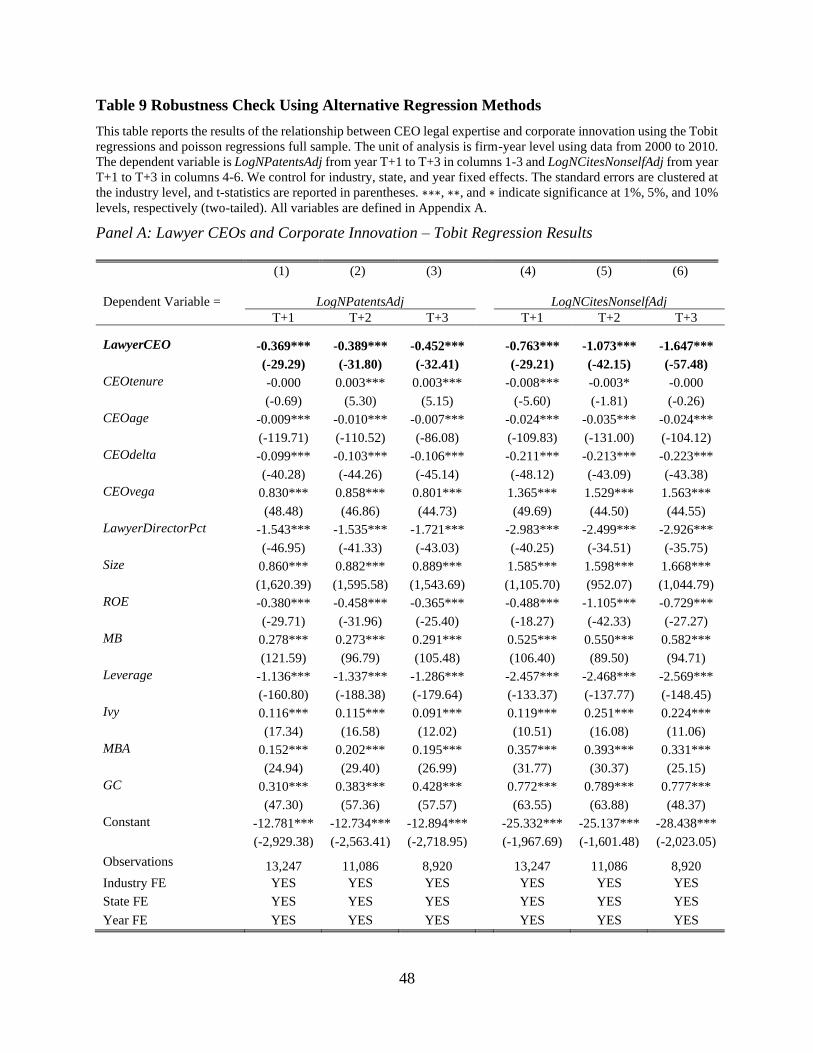

3.5.1 Tobit Model and Poisson Model

The patent and citation data have non-negative values. They are right-skewed with median

of zero, as a large proportion of the observations are zero. Alternative estimation methods dealing

with such data include Tobit model and Poisson model. The estimation results of Tobit regressions

are reported in the Panel A of Table 9 and those of Poisson regressions are reported in the Panel B

of Table 9. The coefficient estimates on LawyerCEO all negative and statistically significant for

all the regressions, suggesting that our main results are robust to alternative models.

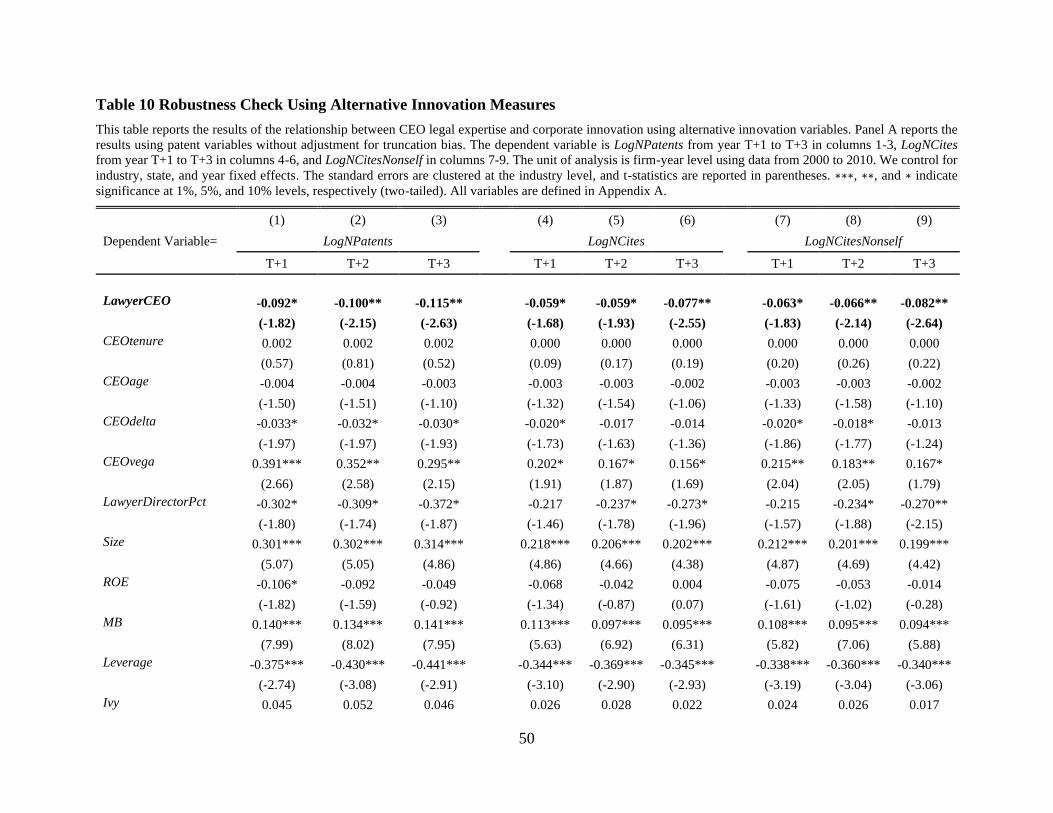

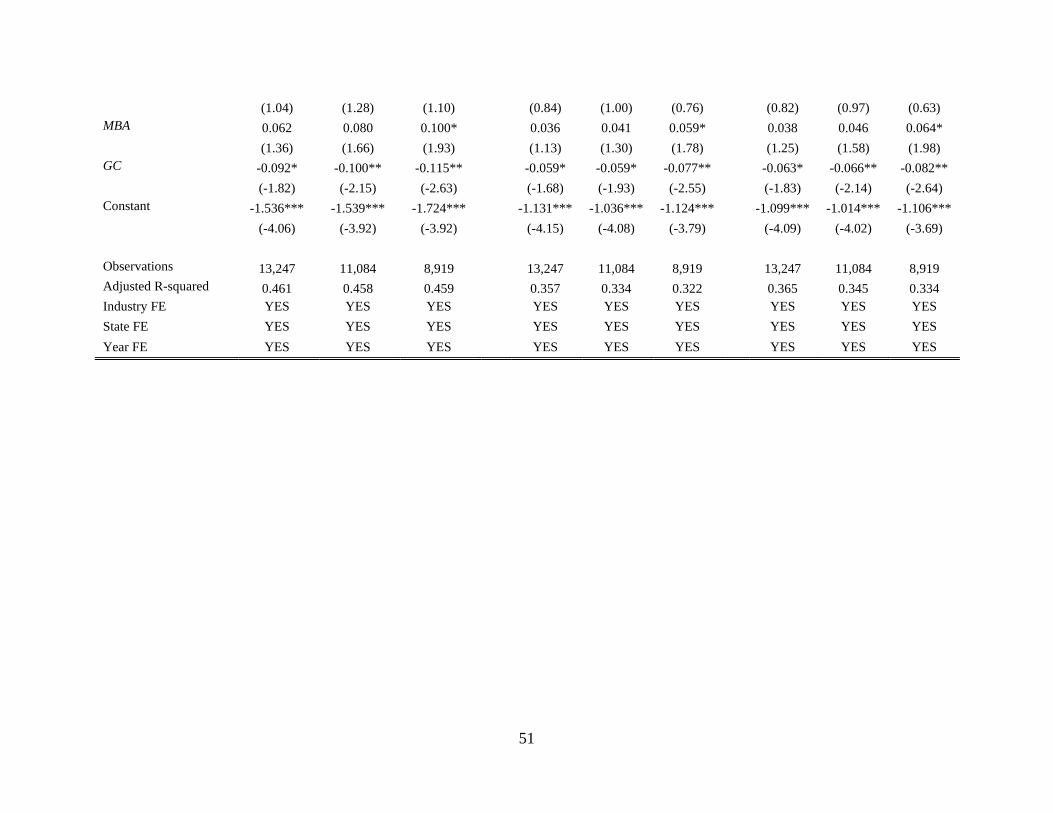

3.5.2 Alternative Measures of Innovation Outcomes

In addition to using the log value of the number of patents and non-self citations adjusted

for truncation bias as the dependent variable in the main specification, we also use several other

measures of innovation outcomes and present the results in Table 10. The results using the raw

number of patents and citations without truncation bias adjustment in columns 1 to 6 suggest that

our inferences remain the same. The findings in columns 7 to 9 show that our results are robust to

excluding firm’s self-citations. The evidence shows that our findings are robust to alternative

measures of innovation outcome variables.

3.5.3 Including Additional Control Variables

It is possible that legal expertise is highly useful for firms that operate in highly competitive

industries and receiving patent grants and citations may be difficult for these firms.7 As another

robustness check, we control for product market competition using the measure proposed by

7 We study patent applications but only patents that are granted appear in the database.

24

Hoberg and Phillips (2016) and continue to find the same results. Further, we include firm’s R&D

and capital expenditures as additional control variables and the results continue to hold.

3.5.4 Subsample Analysis

Panel A in Table 1 shows that firms in the utilities industry have the highest percentage of

lawyer CEO (i.e., 26%). To address the possibility that our results are driven by the utilities

industry with a high presence of lawyer CEOs, we repeat our analysis after removing the

companies in the utilities industry. We continue to see that lawyer CEOs impede innovation.

Further, if we follow the prior studies (e.g., Mao and Zhang, 2018) and only focus on non-financial

and non-utility firms, our results still hold.

Finally, we examine whether our results are driven by the 2007–08 financial crisis, during

which firms experienced reductions in corporate investments and had a greater likelihood of hiring

lawyer CEOs due to the financial stress. We remove the 2007-2009 financial crisis period from

our sample and continue to find similar results, suggesting that our results are not driven by the

financial crisis period. The robustness check results of Section 3.5.3 and 3.5.4 are not tabulated for

the purpose of brevity, and they are available upon request.

4. Conclusion

This study examines how CEOs’ law education background is associated with innovation

outcomes. We argue that training in law focuses on the downsides of engaging in particular actions

and may make lawyer CEOs prefer operating within the bounds of the law, and thereby exhibiting

a cautionary, conservative, risk-averse approach to business activities. Therefore, CEOs with legal

education backgrounds may possess higher levels of risk aversion than CEOs with other

25

educational backgrounds. On the other side, corporate innovation is a long-term, risky, and

unpredictable process that involves the exploration of new methods with a high probability of

failure (Holmstrom, 1989). Commitment to innovation carries a significant risk for managers, as

there are inherent uncertainties in innovative projects going from concept to realization of actual

profits. The arguments suggest that CEOs with legal backgrounds may detract from firm

innovation.

Using a sample of 13,247 firm-year observations (representing 2,345 unique firms) from

2000 to 2010, we find evidence supporting our prediction that firms with lawyer CEOs are

associated with fewer patents and citations, which measures the innovation quantity and quanlity

respectively.

To enhance our confidence in the references we draw from the tests, we use the several

identification strategies. First, we match firms with lawyer CEOs with those without using the one-

on-one coarsened exact matching based on the following firm characteristics: firms’ past litigation

experience (proxied by the number of law cases filed against the firm in the past three years), firm

size, market to book ratio, leverage, industry, state, and year. The data balance check shows that

the means of the above firm characteristics are statistically indifferent after the matching between

firms with lawyer CEOs and those without, indicating that our matching is successful. With the

matched sample, the number of observations are sharply reduced but our results still hold.

Second, we use two different instrumental variable with two-stage least squares regressions.

The first instrumental variable is the local labor supply of potential CEO candidates with legal

expertise, and the second instrument is the lawyer density of the state where the CEO attended

college. Both instrumental variables drive the appointment of lawyer CEOs but have no direct

26

effects on firms’ innovation outcomes. Our inferences remain unchanged using these alternative

identification strategies.

Third, falsification tests are conducted to rule out the possibility of reverse causality. We

find no association between the past innovation outcomes and the presence of lawyer CEO,

confirming that it is lawyer CEOs that impede innovation, instead of that firms tend to hire lawer

CEOs after they experience poor innovation outcomes.

Next, using cross-sectional analysis, we find that the negative association between CEOs’

law backgrounds and corporate innovation is more pronounced for firms with higher litigation risk.

When firm litigation risk is higher, lawyer CEOs are less likely to engage in innovative activities

due to their concerns over risk. Lawyer CEOs’ risk aversion is the reason that drives the negative

association between their law education backgrounds and corporate innovation.

To shed light on the mechanisms through which lawyer CEOs impede corporate innovation,

we study the association between CEOs’ legal backgrounds and firm’s investment policies. Our

findings suggest that lawyer CEOs spend less on R&D and capital expenditures and are more likely

to under-invest than non-lawyer CEOs. Further, to rule out the possibility that lawyer CEOs’

pursuit in filing lawsuits distract them from committing to innovation, we show that lawyer CEOs

are not more likely to initiate lawsuits against other parties than non-lawyer CEOs.

Our study makes the following contributions. First, we contribute to the growing literature

on whether executives or directors’ legal expertise affect firm policies by documenting the impact

of the legal background of the primary decision maker in the firm (i.e., CEO) on an important

outcome of corporate investment policy, i.e., patenting activity. Second, our study contributes to

the upper echelons theory literature by introducing the effect of CEOs’ law education background

27

on corporate innovation. Third, we add to the large literature on corporate innovation by providing

support for the longstanding concern that lawyer CEOs deter corporate innovation.

28

References

Akcigit, U., Celik, M. A., & Greenwood, J. (2016). Buy, keep, or sell: Economic growth and the

market for ideas. Econometrica, 84(3), 943–984.

Al Mamun, M. D., Balachandran, B., Duong, H. N., & Gul, F. A. (2020). Are corporate general

counsels in top management effective monitors? Evidence from stock price crash risk.

European Accounting Review, 1–33.

Amore, M. D., Schneider, C., & Žaldokas, A. (2013). Credit supply and corporate innovation.

Journal of Financial Economics, 109(3), 835–855.

Ben-David, I., Graham, J. R., & Harvey, C. R. (2013). Managerial miscalibration. The Quarterly

Journal of Economics, 128(4), 1547–1584.

Bertrand, M., & Schoar, A. (2003). Managing with style: The effect of managers on firm policies.

The Quarterly Journal of Economics, 118(4), 1169–1208.

Biddle, G. C., Hilary, G., & Verdi, R. S. (2009). How does financial reporting quality relate to

investment efficiency? Journal of Accounting and Economics, 48(2–3), 112–131.

Brav, A., Jiang, W., Ma, S., & Tian, X. (2018). How does hedge fund activism reshape corporate

innovation? Journal of Financial Economics, 130(2), 237–264.

Chemmanur, T. J., Kong, L., Krishnan, K. & Yu, Q. (2019). Top management human capital,

inventor mobility, and corporate innovation. Journal of Financial and Quantitative

Analysis, 54(6), 2383-2422.

Chen, F., Hou Y., Richardson, G., & Su, B. (2021) Lawyer CEOs and Strategic Disclosures of

Litigation Loss Contingencies. Working Paper.

Coles, J. L., Daniel, N. D., & Naveen, L. (2006). Managerial incentives and risk-taking. Journal

of Financial Economics, 79(2), 431–468.

Cornaggia, J., Mao, Y., Tian, X., & Wolfe, B. (2015). Does banking competition affect innovation?

Journal of Financial Economics, 115(1), 189–209.

Daellenbach, U. S., McCarthy, A. M., & Schoenecker, T. S. (1999). Commitment to innovation:

The impact of top management team characteristics. R&D Management, 29(3), 199–208.

Fang, V. W., Tian, X., & Tice, S. (2014). Does stock liquidity enhance or impede firm innovation?

The Journal of Finance, 69(5), 2085–2125.

Galasso, A., & Simcoe, T. S. (2011). CEO overconfidence and innovation. Management Science,

57(8), 1469–1484.

Hall, B. H., Jaffe, A. B., & Trajtenberg, M. (2001). The NBER patent citation data file: Lessons,

insights and methodological tools. National Bureau of Economic Research.

Hall, B. H., Jaffe, A., & Trajtenberg, M. (2005). Market value and patent citations. RAND Journal

of Economics, 36(1), 16–38.

29

Ham, C., & Koharki, K. (2016). The association between corporate general counsel and firm credit

risk. Journal of Accounting and Economics, 61(2–3), 274–293.

Hayes, R. H., & Abernathy, W. J. (1980). Managing our way to economic decline. Harvard Bus.

Rev.;(United States), 58(4).

He, J. J., & Tian, X. (2013). The dark side of analyst coverage: The case of innovation. Journal of

Financial Economics, 109(3), 856–878.

Heider, F., & Ljungqvist, A. (2015). As certain as debt and taxes: Estimating the tax sensitivity of

leverage from state tax changes. Journal of Financial Economics, 118(3), 684–712.

Henderson, M. T., Hutton, I., Jiang, D., & Pierson, M. (2017). Lawyer CEOs. Working Paper.

Hoberg, G., & Phillips, G. (2016). Text-based network industries and endogenous product

differentiation. Journal of Political Economy, 124(5), 1423–1465.

Holmstrom, B. (1989). Agency costs and innovation. Journal of Economic Behavior &

Organization, 12(3), 305–327.

Jagolinzer, A. D., Larcker, D. F., & Taylor, D. J. (2011). Corporate governance and the information

content of insider trades. Journal of Accounting Research, 49(5), 1249–1274.

Kempf, E., & Spalt, O. (2020). Attracting the Sharks: Corporate Innovation and Securities Class

Action Lawsuits. University of Chicago Working Paper.

Kim, I., & Skinner, D. J. (2012). Measuring securities litigation risk. Journal of Accounting and

Economics, 53(1–2), 290–310.

Kogan, L., Papanikolaou, D., Seru, A., & Stoffman, N. (2017). Technological innovation, resource

allocation, and growth. The Quarterly Journal of Economics, 132(2), 665–712.

Kwak, B., Ro, B. T., & Suk, I. (2012). The composition of top management with general counsel

and voluntary information disclosure. Journal of Accounting and Economics, 54(1), 19–

41.

Lent, R. W., Brown, S. D., Talleyrand, R., McPartland, E. B., Davis, T., Chopra, S. B., Alexander,

M. S., Suthakaran, V., & Chai, C.-M. (2002). Career choice barriers, supports, and coping

strategies: College students’ experiences. Journal of Vocational Behavior, 60(1), 61–72.

Litov, L. P., Sepe, S. M., & Whitehead, C. K. (2013). Lawyers and fools: Lawyer-directors in

public corporations. Geo. LJ, 102, 413.

Liu, Y., Shen, Y., Wang, J., & Wang, Q. (2019). Passive Institutional Investors and Corporate

Innovation. Baruch College Zicklin School of Business Research Paper, 2019–07, 02.

Mao, C. X., & Zhang, C. (2018). Managerial risk-taking incentive and firm innovation: Evidence

from FAS 123R. Journal of Financial and Quantitative Analysis, 53(2), 867 - 898.

Morse, A., Wang, W., & Wu, S. (2016). Executive lawyers: Gatekeepers or strategic officers? The

Journal of Law and Economics, 59(4), 847–888.

30

Pham, M. H. (2020). In law we trust: Lawyer CEOs and stock liquidity. Journal of Financial

Markets, 50, 100548.

Stein, J. C. (1988). Takeover threats and managerial myopia. Journal of Political Economy, 96(1),

61–80.

Sunder, J., Sunder, S. V., & Zhang, J. (2017). Pilot CEOs and corporate innovation. Journal of

Financial Economics, 123(1), 209–224.

31

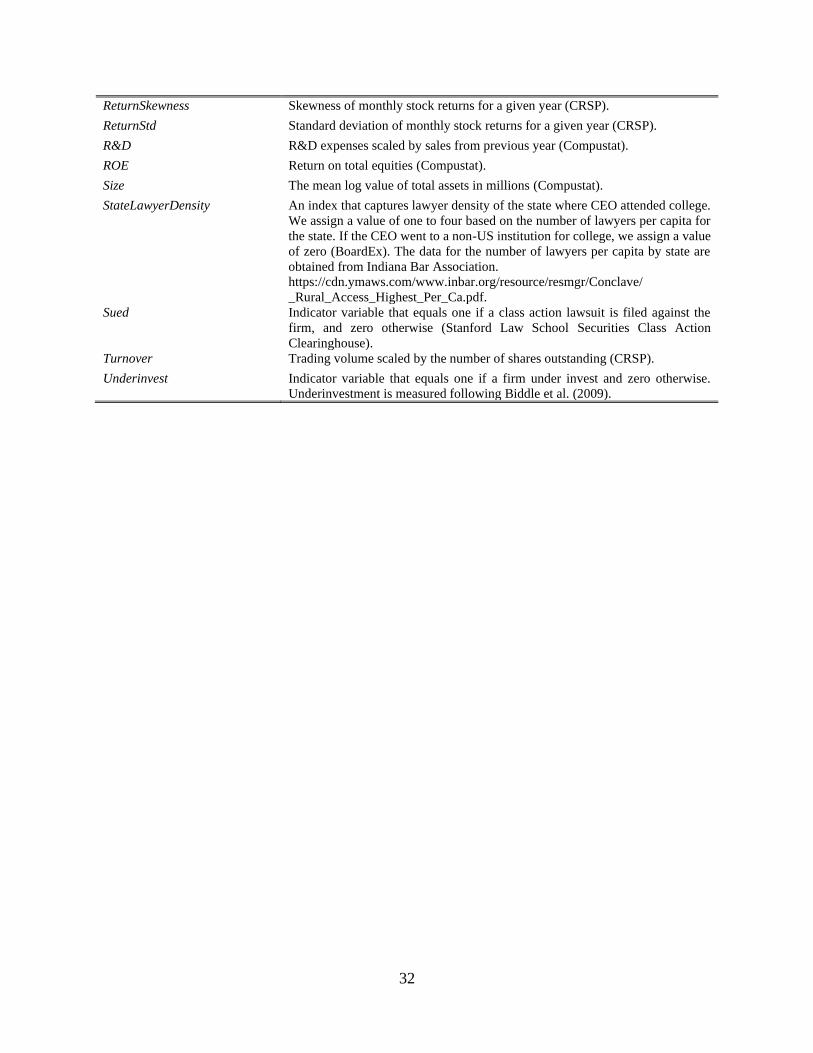

Appendix A Variable Definitions

Variable Definition

Capex Capital expenditures scaled by lagged total assets (Compustat).

CEOage CEO age (ExecuComp, BoardEx, or hand collected data).

CEOdelta The change in CEO’s wealth associated with a 1% change in the firm’s stock

price (ExecuComp).

CEOtenure CEO tenure defined as the number of years since the appointment year to the

year of measurement (ExecuComp, BoardEx, or hand collected data).

CEOvega The change in CEO stock option portfolio for a 1% change in stock volatility.

This variable includes vega from prior option grants and options granted in the

current year (ExecuComp).

FileLawsuit Indicator variable that equals 1 if the firm files a lawsuit in a given year and zero

otherwise (Audit Analytics Legal File)

FPS Indicator variable that equals one if the firm is in the biotech, computer,

electronic, or retail industry and zero otherwise.

GC Indicator variable that equals 1 if the general counsel is among the top five paid

executives, and 0 otherwise (ExecuComp).

Ivy Indicator variable that equals 1 if the CEO has a degree from an Ivy League

school, and 0 otherwise (BoardEx or hand collected data).

LawyerCEO Indicator variable that equals 1 if at least one of the CEOs possesses legal

expertise, and 0 otherwise. Following Henderson et al. (2018), we consider a

CEO to possess legal expertise if s/he holds an undergraduate degree in law such

as an LLB, or a graduate degree such as LLM, J.D., or Ph.D. in Jurisprudence

(ExecuComp, BoardEx, or hand collected data).

LawyerCEO100miles The percentage of firms located in the 100-mile radius of the focal firm’s

headquarters that have a lawyer CEO (ExecuComp, BoardEx, or hand collected

data).

LawyerDirectorPct The mean percentage of board of directors with legal expertise. We consider a

board member to possess legal expertise if s/he holds an undergraduate degree

in law such as an LLB, or a graduate degree such as LLM, J.D., or Ph.D. in

Jurisprudence (BoardEx or hand collected data).

Leverage Firm leverage (total liabilities scaled by total assets).

LitRisk Firm litigation risk is estimated following Kim and Skinner (2012). Specifically,

we use the predicted values estimated from the model below:

Suedt = 𝛾0 + 𝛾1FPSt-1 + 𝛾2Sizet-1 + 𝛾3SalesGrowtht-1 + 𝛾4Return t-1

+ 𝛾5ReturnSkewness t-1 + 𝛾6ReturnStd t-1 + 𝛾7Turnover t-1 + 𝜃

LogNCites Log value of the number of citations received (NBER and data provided by

Kogan et al., 2017).

LogNCitesNonself Log value of the number of non-self citations received (NBER and data provided

by Kogan et al., 2017).

LogNCitesNonselfAdj Log value of the number of non-self citation received adjusted for truncation

bias following Hall et al.,2001, 2005. (NBER and data provided by Kogan et al.,

2017).

LogNPatents Log value of the number of patents filed and eventually granted (NBER and data

provided by Kogan et al., 2017).

LogNPatentsAdj Log value of the number of patents filed and eventually granted, adjusted for

truncation bias following Hall et al.,2001, 2005 (NBER and data provided by

Kogan et al., 2017).

MB Market to book value of total assets (Compustat).

MBA Indicator variable that equals 1 if the CEO has an MBA degree, and 0 otherwise

(BoardEx or hand dcollected data).

PastLitigationExperiences The number of law cases filed against the firm in the past three years (Audit

Analytics Legal File)

Return Cumulative monthly stock returns for a given year (CRSP).

32

ReturnSkewness Skewness of monthly stock returns for a given year (CRSP).

ReturnStd Standard deviation of monthly stock returns for a given year (CRSP).

R&D R&D expenses scaled by sales from previous year (Compustat).

ROE Return on total equities (Compustat).

Size The mean log value of total assets in millions (Compustat).

StateLawyerDensity An index that captures lawyer density of the state where CEO attended college.

We assign a value of one to four based on the number of lawyers per capita for

the state. If the CEO went to a non-US institution for college, we assign a value

of zero (BoardEx). The data for the number of lawyers per capita by state are

obtained from Indiana Bar Association.

https://cdn.ymaws.com/www.inbar.org/resource/resmgr/Conclave/

_Rural_Access_Highest_Per_Ca.pdf.

Sued Indicator variable that equals one if a class action lawsuit is filed against the

firm, and zero otherwise (Stanford Law School Securities Class Action

Clearinghouse).

Turnover Trading volume scaled by the number of shares outstanding (CRSP).

Underinvest Indicator variable that equals one if a firm under invest and zero otherwise.

Underinvestment is measured following Biddle et al. (2009).

33

Table 1 Summary Statistics

This table reports summary statistics for the variables used in the main analyses. Panel A reports the total number of

CEOs observations at the year-firm level and the percentage of lawyer CEOs observations by industry. We tabulate

the distribution using the Fama-French 12-industry classification in this panel for brevity. In our main analysis, our

industry classification is based on the first two digits of the SIC code. Panel B reports the total number of CEOs

observations at the year-firm level and the percentage of lawyer CEOs observations by year. Panel C reports the total

number of CEOs observations at the year-firm level and the percentage of lawyer CEOs observations by state. Panel

D presents descriptive statistics for the variables used in our main regressions. T-statistics are corrected for serial

correlation. The unit of analysis is at the firm-year level.

Panel A: Lawyer CEO Percentage by Industry

Industry

Firm-Year

Observations

Lawyer CEO

Percentage

Consumer Nondurables 715 5%

Consumer Durables 339 6%

Manufacturing 1,518 8%

Oil, Gas, and Coal Extraction and Products 540 7%

Chemicals and Allied Products 382 6%

Business Equipment 2,461 4%

Telephone and Television Transmission 254 15%

Utilities 573 27%

Wholesale, Retail, and Some Services (Laundries, Repair Shops) 1,536 6%

Healthcare, Medical Equipment, and Drugs 1,098 8%

Finance 2,308 12%

Other 1,523 13%

Total 13,247 9%

Panel B: Lawyer CEO Percentage by Year

Year

Firm-Year

Observation

s

Lawyer CEO

Percentage

2000 988 11%

2001 1,212 10%

2002 1,268 10%

2003 1,513 9%

2004 1,539 9%

2005 1,494 9%

2006 1,608 8%

2007 1,858 8%

2008 1,767 8%

Total 13,247 9%

34

Panel C: Lawyer CEO Percentage by State

State

Firm-Year

Observations

Lawyer CEO

Percentage

State

Firm-Year

Observations

Lawyer CEO

Percentage

AK 9 0% MT 8 0%

AL 131 31% NC 253 8%

AR 94 14% ND 12 0%

AZ 151 18% NE 69 9%

CA 2208 5% NH 34 6%

CO 198 12% NJ 448 9%

CT 315 9% NM 4 0%

DC 49 43% NV 88 17%

DE 37 24% NY 1146 14%

FL 475 13% OH 588 10%

GA 393 6% OK 99 18%

HI 32 9% OR 139 1%

IA 93 2% PA 639 10%

ID 58 28% PR 2 0%

IL 732 7% RI 38 0%

IN 195 15% SC 77 19%

KS 51 2% SD 21 19%

KY 89 9% TN 279 4%

LA 98 6% TX 1174 7%

MA 584 6% UT 66 14%

MD 194 12% VA 329 13%

ME 18 0% VT 17 18%

MI 291 10% WA 219 6%

MN 410 4% WI 245 9%

MO 288 1% WV 20 0%

MS 40 8% Total 13,247 9%

35

Panel D: Descriptive Statistics

Full Sample

(N=13,247)

Lawyer

CEO

Non-Lawyer

CEO

Variable Mean Median

Standard

Deviation Minimum Maximum

Mean Mean Difference T-Statistics

LawyerCEO 0.09 0.00 0.28 0.00 1.00

NPatentsAdjt+1 9.12 0.00 35.80 0.00 269.44 7.50 9.28 -1.78 -1.67

NPatentsAdjt+2 8.60 0.00 32.96 0.00 244.31 6.64 8.79 -2.15 -2.05

NPatentsAdjt+3 8.27 0.00 31.08 0.00 228.56 5.87 8.50 -2.63 -2.51

NCitesNonSelfAdj t+1 49.19 0.00 217.24 0.00 1670.83 35.17 50.55 -15.38 -2.57

NCitesNonSelfAdj t+2 45.00 0.00 199.30 0.00 1518.70 29.22 46.54 -17.32 -2.98

NCitesNonSelfAdj t+3 45.14 0.00 199.67 0.00 1504.97 25.47 47.09 -21.62 -3.55

CEOtenure 4.83 3.00 5.58 0.00 29.00 5.19 4.79 0.40 2.47

CEOage 54.83 55.00 7.21 39.00 75.00 56.09 54.71 1.38 6.35

CEOdelta 0.72 0.19 1.76 0.00 13.13 1.01 0.69 0.32 4.66

CEOvega 0.14 0.05 0.25 0.00 1.52 0.18 0.14 0.04 4.76

LawyerDirectorPct 0.12 0.11 0.11 0.00 0.43 0.17 0.12 0.05 12.91

Size 7.62 7.48 1.70 4.20 12.52 8.24 7.56 0.68 13.08

ROE 0.12 0.13 0.25 -0.90 1.14 0.13 0.12 0.01 1.28

MB 1.93 1.50 1.23 0.79 7.61 1.70 1.95 -0.25 -7.39

Leverage 0.54 0.55 0.22 0.08 0.95 0.60 0.54 0.06 10.16

Ivy 0.15 0.00 0.36 0.00 1.00 0.23 0.14 0.09 7.35

MBA 0.34 0.00 0.47 0.00 1.00 0.14 0.36 -0.22 -20.11

GC 0.31 0.00 0.46 0.00 1.00 0.35 0.31 0.04 2.67

LawyerCEO100miles 0.08 0.08 0.07 0.00 0.33 0.14 0.08 0.06 25.64

StateLawyerDensity 2.45 2.00 1.14 1.00 4.00 2.61 2.43 0.18 4.86

36

Table 2 Lawyer CEOs and Corporate Innovation – Main Results

This table reports the baseline regression results of the relationship between CEO legal expertise and corporate

innovation using ordinary least squares method with the full sample. The unit of analysis is firm-year level using data

from 2000 to 2010. The dependent variable is LogNPatentsAdj from year T+1 to T+3 in columns 1-3 and

LogNCitesNonselfAdj from year T+1 to T+3 in columns 4-6. We control for industry, state, and year fixed effects.

The standard errors are clustered at the industry level, and t-statistics are reported in parentheses. ∗∗∗, ∗∗, and ∗

indicate significance at 1%, 5%, and 10% levels, respectively (two-tailed). All variables are defined in Appendix A.

(1) (2) (3) (4) (5) (6)

Dependent Variable = LogNPatentsAdj LogNCitesNonselfAdj

T+1 T+2 T+3 T+1 T+2 T+3

LawyerCEO -0.095* -0.104** -0.121**

-0.123* -0.136** -0.175***

(-1.73) (-2.07) (-2.51)

(-1.88) (-2.20) (-2.88)

CEOtenure 0.002 0.002 0.002

0.001 0.002 0.001

(0.62) (0.85) (0.69)

(0.33) (0.44) (0.26)

CEOage -0.004 -0.004 -0.003

-0.006* -0.008** -0.005

(-1.48) (-1.40) (-1.12)

(-1.67) (-2.14) (-1.65)

CEOdelta -0.038** -0.036** -0.035**

-0.045** -0.038** -0.031

(-2.12) (-2.03) (-2.07)

(-2.38) (-2.01) (-1.55)

CEOvega 0.422*** 0.390** 0.330**

0.436** 0.405** 0.378**

(2.68) (2.64) (2.26)

(2.41) (2.53) (2.24)

LawyerDirectorPct -0.354** -0.362* -0.417*

-0.451* -0.449* -0.562**

(-2.02) (-1.90) (-1.94)

(-1.90) (-1.95) (-2.21)

Size 0.324*** 0.329*** 0.344***

0.378*** 0.370*** 0.380***

(5.06) (5.06) (4.89)

(5.16) (4.99) (4.67)

ROE -0.105* -0.091 -0.058

-0.119 -0.120 -0.068

(-1.69) (-1.42) (-0.98)

(-1.54) (-1.23) (-0.73)

MB 0.145*** 0.141*** 0.149***

0.185*** 0.173*** 0.184***

(7.96) (7.94) (7.87)

(6.73) (8.18) (7.18)

Leverage -0.400*** -0.468*** -0.483***

-0.628*** -0.673*** -0.655***

(-2.71) (-3.08) (-2.90)

(-3.28) (-2.96) (-2.95)

Ivy 0.008 0.006 0.016

0.008 0.032 0.025

(0.21) (0.16) (0.40)

(0.14) (0.64) (0.56)

MBA 0.049 0.059 0.058

0.052 0.055 0.045

(1.05) (1.33) (1.27)

(0.99) (1.19) (0.87)

GC 0.067 0.090* 0.117**

0.097* 0.119** 0.143**

(1.35) (1.70) (2.06)

(1.76) (2.13) (2.27)

Constant -1.654*** -1.687*** -1.873***

-1.787*** -1.662*** -1.908***

(-4.03) (-3.91) (-3.89)

(-4.12) (-3.97) (-3.75)

Observations 13,247 11,084 8,919

13,247 11,084 8,919

Adjusted R-squared 0.466 0.465 0.466 0.377 0.361 0.352

Industry FE YES YES YES YES YES YES

State FE YES YES YES YES YES YES

Year FE YES YES YES YES YES YES

37

Table 3 Lawyer CEOs and Corporate Innovation - Matched Sample

This table reports the baseline regression results of the relationship between CEO legal expertise and corporate innovation using a matched sample based on

Coarsened Exact Matching. We match on the following six characteristics that could affect firm’s decision to hire a lawyer CEO: past litigation experiences (proxied

by the number of law cases filed against the firm in the past three years), firm size, market to book ratio, leverage, industry, state, and year. We coarsen each of the

first four continuous variables (i.e., past litigation experiences, firm size, market to book ratio, and leverage) using three equally spaced strata, and we perform one-

to-one matching on each stratum for each of the four variables. We also match on the exact value of year, state, and industry without coarsening. The unit of

analysis is firm-year level using data from 2000 to 2010. The dependent variable is LogNPatentsAdj from year T+1 to T+3 in columns 1-3 and LogNCitesNonselfAdj

from year T+1 to T+3 in columns 4-6. We control for industry, state, and year fixed effects. The standard errors are clustered at the industry level, and t-statistics

are reported in parentheses. ∗∗∗, ∗∗, and ∗ indicate significance at 1%, 5%, and 10% levels, respectively (two-tailed). All variables are defined in Appendix A.

Panel A: Checking Data Balance with T-Tests on Continuous Background Variables Before and After Matching

Before Matching After Matching

Variable Sample Observations Mean Difference T- statistics Observations Mean Difference T- statistics

PastLitigationExperiences Lawyer CEOs 1,172 1.617 0.255 2.26** 526 1.352 -0.175 -0.85

Non-Lawyer CEOs 12,075 1.362 526 1.527

Size Lawyer CEOs 1,172 8.243 0.680 13.18*** 526 8.233 0.127 1.12

Non-Lawyer CEOs 12,075 7.563 526 8.106

MB Lawyer CEOs 1,172 1.701 -0.250 -6.64*** 526 1.644 -0.035 -0.55

Non-Lawyer CEOs 12,075 1.951 526 1.679

Leverage Lawyer CEOs 1,172 0.699 0.064 9.41*** 526 0.616 -0.000 -0.01

Non-Lawyer CEOs 12,075 0.535 526 0.616

Total

13,247

1,052

38

Panel B: Baseline Regression Results using Matched Sample

(1) (2) (3) (4) (5) (6)

Dependent Variable = LogNPatentsAdj LogNCitesNonselfAdj

T+1 T+2 T+3 T+1 T+2 T+3

LawyerCEO -0.107** -0.145** -0.175**

-0.164** -0.252** -0.310***

(-2.28) (-2.46) (-2.73)

(-2.28) (-2.60) (-3.09)

CEOtenure 0.016** 0.019*** 0.028***

0.011 0.012 0.039**

(2.26) (2.80) (2.99)

(1.58) (0.96) (2.68)

CEOage -0.003 -0.002 -0.007

-0.002 -0.002 -0.020*

(-0.42) (-0.22) (-0.94)

(-0.22) (-0.27) (-1.76)

CEOdelta -0.049* -0.053** -0.055*

-0.049* -0.068** -0.058*

(-2.03) (-2.06) (-1.88)

(-1.97) (-2.38) (-1.75)

CEOvega 0.413 0.286** 0.376***

0.472 0.162 0.464***

(1.67) (2.07) (2.79)

(1.35) (0.79) (2.98)

LawyerDirectorPct -0.281 -0.153 -0.255

-0.284 0.330 -0.351

(-0.81) (-0.35) (-0.50)

(-0.60) (0.62) (-0.57)

Size 0.210** 0.209** 0.226**

0.288** 0.292** 0.291***

(2.70) (2.76) (2.66)

(2.49) (2.65) (2.80)

ROE 0.043 0.220* 0.139

0.181 0.148 0.304

(0.63) (1.82) (0.56)

(1.41) (0.72) (0.75)

MB 0.058 0.064 0.079*

0.040 0.177** 0.139**

(1.25) (1.12) (1.71)

(0.71) (2.31) (2.41)

Leverage 0.224 0.206 0.048

-0.053 -0.049 -0.055

(0.64) (0.46) (0.09)

(-0.11) (-0.10) (-0.10)

Ivy 0.012 0.064 0.057

-0.071 0.014 0.129

(0.21) (0.83) (0.66)

(-0.78) (0.11) (1.01)

MBA -0.066 0.007 -0.035

-0.113 0.043 -0.076

(-0.60) (0.07) (-0.37)

(-0.77) (0.37) (-0.60)

GC 0.018 -0.024 0.075

0.081 -0.002 0.083

(0.22) (-0.32) (0.76)

(1.05) (-0.03) (0.63)

Constant -1.202 -1.323* -1.155

-1.631* -1.954** -1.062

(-1.69) (-1.89) (-1.69)

(-1.88) (-2.63) (-1.47)

Observations 1,052 867 707

1,052 867 707

Adjusted R-squared 0.653 0.666 0.654 0.545 0.473 0.415

Industry FE YES YES YES YES YES YES

State FE YES YES YES YES YES YES

Year FE YES YES YES YES YES YES

39

Table 4 Lawyer CEOs and Corporate Innovation – Instrumental Variables and 2SLS

This table reports the results of the relationship between CEO legal expertise and corporate innovation using two

different instrumental variables. The first instrumental variable is LawyerCEO100miles, defined as the percentage of

firms located in the 100-mile radius of the focal firm’s headquarters that have a lawyer CEO. The second instrumental

variable is StateLawyerDensity, which is the index of lawyer density in the state where the CEO went to college. We

assign a value of one to four based on the number of lawyers per capita for the state. The unit of analysis is firm-year

level using data from 2000 to 2010. Panel A reports the first stage results of two instrumental variables. Panels B

presents the second stage results based on the instrumental variables LawyerCEO100miles. Panels C presents the

second stage results based on the instrumental variables LawyerCEO100miles and StateLawyerDensity. The

dependent variables are LogNPatentsAdj and LogNCitesNonselfAdj. We industry, state, and year fixed effects for the

second stage regressions. The standard errors are clustered at the industry level, and t-statistics are reported in

parentheses. ∗∗∗, ∗∗, and ∗ indicate significance at 1%, 5%, and 10% levels, respectively (two-tailed). All variables

are defined in Appendix A.

Panel A: First Stage Results

(1) (2)

Dependent Variable = LawyerCEO LawyerCEO

LawyerCEO100miles 1.095*** 1.300***

(7.23) (7.17)

StateLawyerDensity 0.019***

(3.96)

CEOtenure -0.000 0.001

(-0.36) (0.79)

CEOage 0.001 0.002*

(1.58) (1.94)

CEOdelta 0.002 0.003

(0.67) (0.76)

CEOvega 0.016 0.009

(0.51) (0.26)

LawyerDirectorPct 0.164*** 0.229***

(2.74) (3.01)

Size 0.010** 0.006

(2.25) (1.15)

ROE 0.004 0.003

(0.33) (0.21)

MB -0.003 -0.003

(-0.74) (-0.67)

Leverage -0.012 -0.017

(-0.46) (-0.48)

Ivy -0.085*** 0.035*

(-5.51) (1.91)

MBA -0.016** -0.106***

(-2.17) (-6.35)

GC -0.065 -0.023***

(-1.50) (-2.65)

Constant -0.000 -0.065

(-0.36) (-1.20)

Observations 13,247 10,585

Adjusted R-squared 0.155 0.191

Industry FE YES YES

State FE YES YES

Year FE YES YES

40

Panel B: Second Stage Results based on the First Instrumental Variable (LawyerCEO100miles)

(1) (2) (3) (4) (5) (6)

Dependent Variable LogNPatentsAdj LogNCitesNonselfAdj

T+1 T+2 T+3 T+1 T+2 T+3

LawyerCEO

(Instrumented)

-

0.825**

* -0.900*** -0.715***

-1.098** -0.872** -0.676**

(-2.69) (-2.85) (-2.63) (-2.56) (-2.34) (-2.22)

CEOtenure 0.002 0.002 0.002

0.001 0.001 0.001

(0.57) (0.72) (0.59)

(0.27) (0.34) (0.19)

CEOage -0.004 -0.003 -0.002

-0.005 -0.007* -0.005

(-1.20) (-1.06) (-0.85) (-1.39) (-1.86) (-1.41)

CEOdelta -

0.037** -0.035** -0.034**

-0.043** -0.037** -0.030

(-2.11) (-2.03) (-2.08)

(-2.37) (-2.02) (-1.56)

CEOvega 0.439**

* 0.413*** 0.350**

0.459** 0.427** 0.395**

(2.65) (2.64) (2.36) (2.39) (2.55) (2.31)

LawyerDirectorPct -0.214 -0.202 -0.303 -0.264 -0.300 -0.465*

(-1.33) (-1.15) (-1.48) (-1.23) (-1.44) (-1.89)

Size 0.331**

* 0.336*** 0.349***

0.387*** 0.377*** 0.384***

(5.11) (5.14) (4.99)

(5.18) (5.05) (4.78)

ROE -0.103 -0.091 -0.061 -0.117 -0.120 -0.071

(-1.63) (-1.36) (-0.98) (-1.48) (-1.20) (-0.74)

MB 0.142**

* 0.137*** 0.146***

0.181*** 0.170*** 0.182***

(7.68) (7.56) (7.54)

(6.57) (7.94) (7.07)

Leverage

-

0.409**

* -0.477*** -0.485***

-0.639*** -0.681*** -0.656***

(-2.82) (-3.23) (-3.02) (-3.39) (-3.07) (-3.02)

Ivy 0.050 0.055 0.055

0.063 0.077 0.058

(1.10) (1.15) (1.25)

(1.11) (1.37) (1.13)

MBA -0.016 -0.014 0.002 -0.035 -0.012 -0.003

(-0.31) (-0.28) (0.03) (-0.62) (-0.24) (-0.06)

GC 0.058 0.081 0.112* 0.085 0.111* 0.139**

(1.09) (1.46) (1.92) (1.42) (1.89) (2.16)

Constant -0.072 0.046 -0.098

0.272 0.397 0.119

(-0.23) (0.15) (-0.27)

(1.00) (1.50) (0.33)

Observations 13,247 11,086 8,920 13,247 11,086 8,920

Adjusted R-squared 0.449 0.445 0.459 0.363 0.356 0.356

Industry FE YES YES YES YES YES YES

State FE YES YES YES YES YES YES

Year FE YES YES YES YES YES YES

41

42

Panel C: Second Stage Results based on the First Instrumental Variable (LawyerCEO100miles)

and the Second Instrumental Variable (StateLawyerDensity)

(1) (2) (3) (4) (5) (6)

Dependent Variable = LogNPatentsAdj LogNCitesNonselfAdj

T+1 T+2 T+3 T+1 T+2 T+3

LawyerCEO

(Instrumented) -0.805*** -0.850*** -0.734***

-1.026*** -0.821** -0.683*

(-2.71) (-2.77) (-2.70)

(-2.69) (-2.11) (-1.86)

CEOtenure 0.004 0.004 0.005

0.004 0.003 0.004

(1.10) (1.12) (1.03)

(0.85) (0.76) (0.59)

CEOage -0.003 -0.003 -0.003

-0.006 -0.008* -0.006

(-1.02) (-0.89) (-0.85)

(-1.39) (-1.89) (-1.51)

CEOdelta -0.038** -0.035* -0.034*

-0.045** -0.038* -0.029

(-2.06) (-1.90) (-1.94)

(-2.21) (-1.86) (-1.31)

CEOvega 0.397** 0.362** 0.323**

0.418** 0.372** 0.354**

(2.24) (2.17) (2.07)

(2.12) (2.19) (2.03)