listed structured products brochure

TRANSCRIPT

Listed structured products

PRECISION TOOLS FOR PROFESSIONAL INVESTORS

2 Introduction4 Trackers6 Accelerated Trackers8 Reverse Trackers

10 Bonus Trackers12 Discount Trackers14 Capital Protected16 Key points18 Conclusion20 Glossary

Contents

2 L O N D O N S T O C K E X C H A N G E 3L I S T E D S T R U C T U R E D P R O D U C T S

Buying a structured product without the flexibility to sell it hasbeen likened to driving a car without any brakes - if the marketturns against you, or circumstances change, you can be leftspeeding downhill with little control.

The London Stock Exchange'slisted structured productsplatform seeks to change theway structured products aretraded by providing a primaryand a secondary market for bothbespoke and standardisedinstruments, giving investorsthe option of applying thebrakes at any time - or evenchanging vehicles.

The platform combines theflexibility of the OTC market withthe transparency of anon-exchange platform. Listedstructured products are issuedand marketed directly byinvestment banks, which haveutmost flexibility in terms of theunderlying instrument and

structure of the product. Therelative ease of issuing listedstructured products means theycan be brought to market within48 hours and the minimum sizerequired for a bespoke product iscomparatively low.

Added to this flexibility is thecontinuous two-way pricing whichissuers provide via the LondonStock Exchange, providingtransparent pricing and enablingadvisors to mark-to-market atany time.

There are virtually no restrictionson the types of structuredproducts that the issuing bankscan create, and investors have thefreedom to choose the type ofunderlying, the expiry profile and

risk structure. Additionally, theinstruments are very efficientin terms of pricing - issuing bankscompete directly on price andwithout a distributor acting asintermediary, there are noembedded fees and marketingcosts are minimal.

Already we have seen severalstructures based on manyunderlyings, some of which aredetailed in the following pages.For further information,contact Oliver Hesketh at theLondon Stock Exchange:[email protected],or one of the issuing banks directly.

TaxThe structure of a product is flexible, so canoften be constructed to achieve particularobjectives. Please contact the issuingbanks directly to discuss applicable taxregimes (see opposite).

Structured products are generally eligiblefor inclusion in SIPPs and, depending onstructure, may be eligible for ISAs. Pleasecontact the issuing banks directly forspecific information.

There is no stamp-duty or SDRT payable onstructured products which are cash-settled.

DrKW

Goldman Sachs

SG

UBM

Contact name

Shahzad Sadique

Mark Valentine

David Lake

Francesca Bosi

Contact number

020 7475 6344

020 7774 1551

020 7762 5021

+39 02 8862 8079

RegulationListed structured products are securitisedderivatives which are treated as derivativesfor the purpose of Conduct of Business.

A firm distributing these products must givea two-way risk warning, in the form of ageneric warrants/derivatives warning notice,a tailored risk warning or a copy of thelisting particulars (available on the LondonStock Exchange website,www.londonstockexchange.com/structuredproducts).

“ The platform combinesflexibility and transparency”

Issuing Banks

5L I S T E D S T R U C T U R E D P R O D U C T S4 L O N D O N S T O C K E X C H A N G E

Trackers give investors a cost efficient means to tradean asset (such as a currency or commodity) or todiversify their exposure across an index. As with allsecuritised derivatives, trackers are stamp duty free.

These instruments are typically long-dated or indeedundated with an indefinite lifespan.

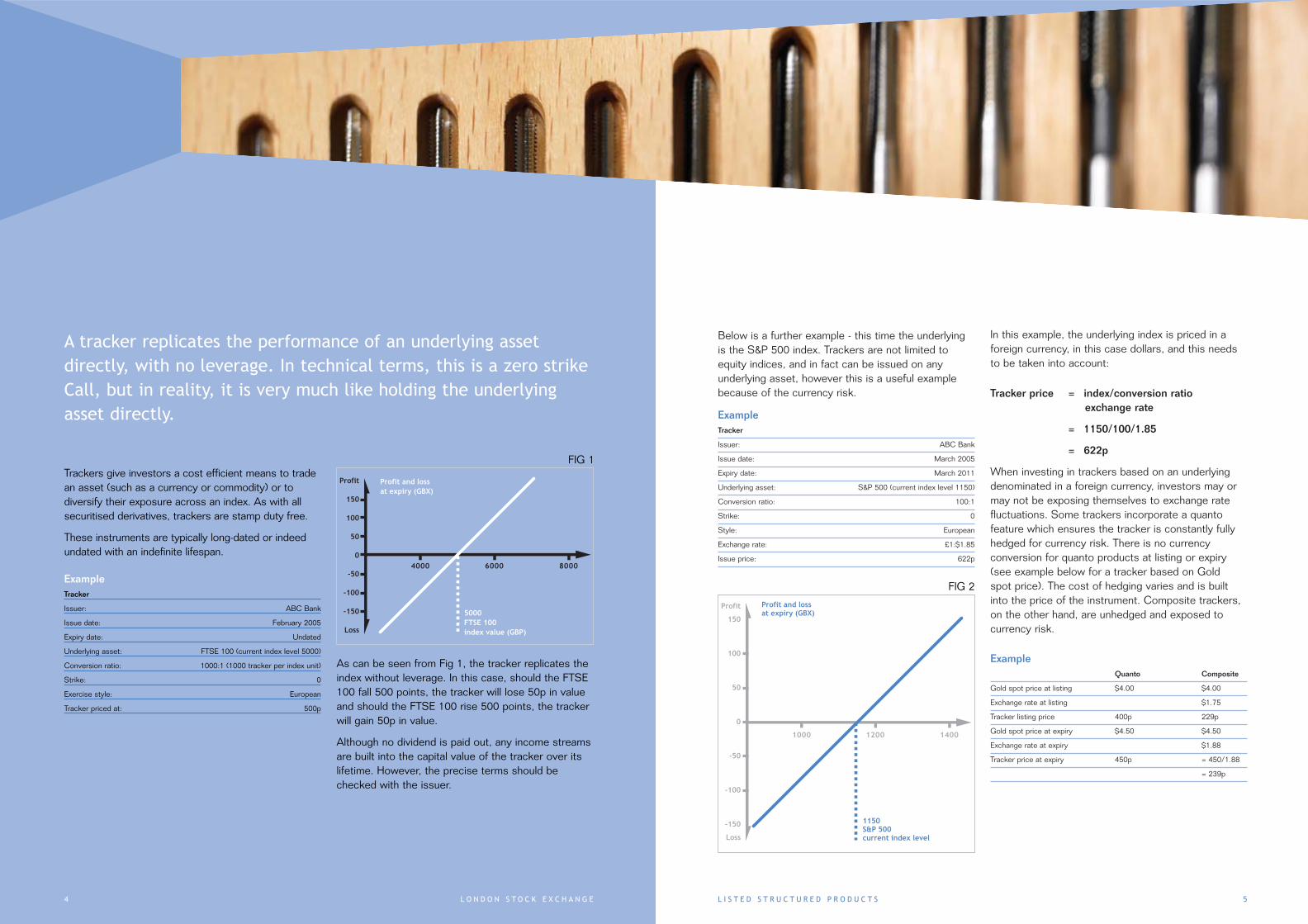

A tracker replicates the performance of an underlying assetdirectly, with no leverage. In technical terms, this is a zero strikeCall, but in reality, it is very much like holding the underlyingasset directly.

4000 6000 8000

Profit

150

100

50

0

-50

-100

-150

Loss

Profit and lossat expiry (GBX)

5000FTSE 100index value (GBP)

ExampleTracker

Issuer: ABC Bank

Issue date: March 2005

Expiry date: March 2011

Underlying asset: S&P 500 (current index level 1150)

Conversion ratio: 100:1

Strike: 0

Style: European

Exchange rate: £1:$1.85

Issue price: 622p

Below is a further example - this time the underlyingis the S&P 500 index. Trackers are not limited toequity indices, and in fact can be issued on anyunderlying asset, however this is a useful examplebecause of the currency risk.

1000 1200 1400

Profit

150

100

50

0

-50

-100

-150

Loss

Profit and lossat expiry (GBX)

1150S&P 500current index level

ExampleQuanto Composite

Gold spot price at listing $4.00 $4.00

Exchange rate at listing $1.75

Tracker listing price 400p 229p

Gold spot price at expiry $4.50 $4.50

Exchange rate at expiry $1.88

Tracker price at expiry 450p = 450/1.88

= 239p

Tracker price = index/conversion ratioexchange rate

= 1150/100/1.85

= 622p

When investing in trackers based on an underlyingdenominated in a foreign currency, investors may ormay not be exposing themselves to exchange ratefluctuations. Some trackers incorporate a quantofeature which ensures the tracker is constantly fullyhedged for currency risk. There is no currencyconversion for quanto products at listing or expiry(see example below for a tracker based on Goldspot price). The cost of hedging varies and is builtinto the price of the instrument. Composite trackers,on the other hand, are unhedged and exposed tocurrency risk.

As can be seen from Fig 1, the tracker replicates theindex without leverage. In this case, should the FTSE100 fall 500 points, the tracker will lose 50p in valueand should the FTSE 100 rise 500 points, the trackerwill gain 50p in value.

Although no dividend is paid out, any income streamsare built into the capital value of the tracker over itslifetime. However, the precise terms should bechecked with the issuer.

FIG 1

FIG 2

In this example, the underlying index is priced in aforeign currency, in this case dollars, and this needsto be taken into account:

ExampleTracker

Issuer: ABC Bank

Issue date: February 2005

Expiry date: Undated

Underlying asset: FTSE 100 (current index level 5000)

Conversion ratio: 1000:1 (1000 tracker per index unit)

Strike: 0

Exercise style: European

Tracker priced at: 500p

16001000 1200 1400

Profit

30

20

10

0

-10

-20

-30

Loss

Profit and lossat expiry (GBX)

1195.45 GBPUnderlying priceat issue

L O N D O N S T O C K E X C H A N G E 7L I S T E D S T R U C T U R E D P R O D U C T S

At maturity

On expiry, the holder of the accelerated tracker hasthe right to:

1. If the final underlying asset priceis greater than or equal to the initialunderlying asset price:

Initial price + (initial price x [participationlevel x change in underlying])

2. Otherwise:

Initial price + (initial price x change in underlying)

This means that should the index have risen 10% invalue at maturity, then the investor will receivea 21% profit.

In this case, £121 in cash(100 + (100 x [210% x 10%])).

The investor does not have to worry about thecurrency risk associated with the underlying assetbeing priced in Yen as this product is Quanto andcurrency risk is hedged out on the investors’ behalfby the issuing bank.

Despite the accelerated upside, the investor facesno additional downside risk (excluding foregoingany income). Should the index have fallen 10% atmaturity, the investor will realise a loss of -10%.

Accelerated Trackers are growth orientated structured products.These instruments give additional upside performance whilstmaintaining a 1:1 relationship on the downside in return forsurrendering income streams related to the underlying asset.

ExampleAccelerated Tracker

Issuer: ABC Bank

Issue date: March 2005

Expiry date: March 2006

Participation: 210%

Underlying asset: TOPIX Index

Underlying price: 1195.45

Instrument price: £100, Quanto

In the example above, the two dotted lines representthe pay-out profiles of the plain tracker and at-the-money Call option which form the components. Thesolid line represents the profit and loss profile of theaccelerated tracker.

6

FIG 3

9L I S T E D S T R U C T U R E D P R O D U C T S8 L O N D O N S T O C K E X C H A N G E

Reverse trackers are very similar to standard trackers but have aninverse relationship with the underlying asset – should the price ofthe underlying asset fall, the price of the reverse tracker will rise.

310 320 330 340

Profit15

10

5

0

-5

-10

-15Loss

Profit and lossat expiry (GBX)

325pLloyds TSB plc

Figure 4 shows the inverse relationship the reversetracker has with the price of Lloyds TSB plc - if theshare price falls 10p, then the reverse tracker pricewould rise 10p and vice versa.

The price is simply calculated as follows:

Price = strike - underlying= 800 - 475= 325p

In effect, this is a Put option, but so deeply in-the-money as to have a linear price relationship with theunderlying. However, should the underlying assetprice increase dramatically towards the strike, thelinear relationship will break down and the instrumentwill increasingly take on the characteristics of astandard Put option.

As with all trackers, no dividends are paid, but anyincome streams are built into the capital value of thetracker over its lifetime - check the pricingsupplement for details specific to each product.

ExampleReverse Tracker

Issuer: ABC Bank

Issue date: February 2005

Expiry date: February 2010

Underlying asset: Lloyd’s TSB plc (current Lloyd’s price 475p)

Conversion ratio: 1:1

Strike: 800p

Exercise style: European

Issue price: 325p

FIG 4

10 L O N D O N S T O C K E X C H A N G E 11

These instruments have slightly more complex structures whichare comparable to fixed term life products or insurance bonds. However, they are continuously priced throughout their lifetimeand investors do not face early redemption penalties.

ExampleBonus Tracker

Issuer: ABC Bank

Issue date: Jan 2005

Expiry date: Jan 2010

Bonus Level: 6000

Barrier Level: 3000

Underlying asset: FTSE 100

Conversion ratio: 1000:1

Issue price: 500p

5000FTSE index value(GBP)

50003000 7000

Profit300

200

100

0

-100

-200

-300Loss

Profit and lossat expiry (GBX)

L I S T E D S T R U C T U R E D P R O D U C T S

In addition, bonus trackers can be issued as muchshorter-dated instruments where required.

A bonus tracker is a combination productincorporating:- a zero strike Call (or standard tracker)- a barrier option (down-and-out Put)

The standard tracker simply replicates theperformance of an underlying with no leverage,and expires at the value of the instrument or index itis tracking.

A down-and-out Put is a type of option called abarrier option which ceases to exist when theunderlying asset reaches a predetermined level(in our next example, 3000) and is therefore cheaperthan a standard option.

Opposite is an example of a FTSE 100 bonus trackerwith a bonus level of 6000 (which translates to 600pdue to the conversion ratio of 1000:1) and a barrierlevel of 3000. This product is the combination of azero strike Call (or tracker) and a Put option with astrike of 6000 and a knock-out level of 3000.

This means that should the FTSE 100 fall below 3000at any point during the five year life of this product,the Put component will ‘knock-out’ leaving theproduct as a simple tracker. However, if the FTSE100 doesn’t fall below the barrier level of 3000, thePut option will remain, guaranteeing a minimumpayout level of 6000 (i.e. 600p) at expiry regardlessof where the FTSE 100 index is at expiry.

At maturityOn expiry the FTSE 100 index closes at 4000 havingnever fallen below 3000 during the five year lifespanof the product. The zero strike Call (or tracker) has avalue of 400p while the Put has a value of 200p(strike price - final index level) giving a total returnof 600p.

If, on the other hand, the FTSE 100 had fallen below3000 at any point during its lifetime, the Put optionwould have ‘knocked out’ and the total return wouldsimply be that of the zero strike Call (or plain tracker)of 400p.

Should the closing level of the FTSE 100 be above6000 at expiry (e.g.7050), the total return would bethat of the zero strike Call (or tracker) of 705p. Thisis the case even if the barrier level has previouslybeen hit.

FIG 5

13L I S T E D S T R U C T U R E D P R O D U C T S12 L O N D O N S T O C K E X C H A N G E

A discount tracker is a combination productincorporating:- a zero strike Call (or tracker)- writing a Call option

The tracker simply replicates the performance of anindex, with no leverage, and will simply expire at thevalue of the index or underlying it is tracking.

This is akin to covered call writing where the optionswriting income translates to a discount on theunderlying asset. Selling the Call option means thatthe investor benefits from the premium, hence thediscount. Upside is capped however, as any rise invalue of the underlying asset above the strike price iscancelled out by the liability created in selling the Calloption (Call option strike price = cap level).

At maturityShould the value of M&S increase by 25% to 500p,the discount tracker would reach the cap limit of430p (a 19.4% rise in value).

Should the value of M&S increase by 7% to 428p,the value of the discount tracker will be 428p (an18.9% rise in value).

Should the value of M&S fall by 20% to 320p, thevalue of the discount tracker would also fall to 320p(but because of the discount purchase price, thiswould represent only an 11.1% fall in value).

In short, additional downside protection is purchasedat the expense of limiting upside exposure above acertain level. As with all trackers, no income is paidout but, according to the terms of each product, isbuilt into the capital value.

Discount trackers also have the unusualcharacteristic of appreciating in value as time passes,all other factors remaining constant. Should theunderlying asset remain static over the lifetime of thediscount tracker (i.e. a 0% return), the discounttracker will expire, in the example above, with a 10%gain for the investor.

Discount trackers allow investors to buy into the performance ofan asset at a discount to the actual underlying price. However,the potential gain is limited to a pre-defined level (the cap level).

300 400 500 600

Profit150

100

50

0

-50

-100

-150Loss

Profit and lossat expiry (GBX)

360p Discount tracker- price at launch

400p Marks & Spencer- price at launch

ExampleDiscount Tracker

Issuer: ABC Bank

Issue date: February 2005

Expiry date: February 2006

Cap: 430p

Underlying asset: Marks & Spencer (M&S)

Conversion ratio: 1

Underlying price: 400p

Product price: 360p (10% discount)

In the example above, the two dotted lines representthe profit and loss expiry profiles of the tracker andthe short Call option. The solid line represents theprofit and loss profile of the discount tracker.

FIG 6

15L I S T E D S T R U C T U R E D P R O D U C T S14 L O N D O N S T O C K E X C H A N G E

At maturityOn expiry, the holder of the capital protectedinstrument has the right to:

1. If the final underlying asset priceis greater than or equal to the initialunderlying asset price:

Initial price + (change in underlying/conversionratio x participation)

2. Otherwise:

The higher of:a) Initial price/conversion ratio x protection levelb) Final price/conversion ratio

In this case, regardless of whether the index falls tozero by the time the product expires, the investor isguaranteed to receive the initial price of the productwhen launched. So a fall of -100% equates to a0% return.

Should the index rise over four years, then theinvestor fully partakes in any capital appreciation.A 15% rise in the FTSE100 will result in a 15% risein the value of the product. However, it should beremembered that the income attributable to theunderlying asset has been given up in order toachieve this payout profile.

Capital protected products allow investors to gain exposure tofinancial assets whilst protecting the capital invested, in returnfor surrendering any income related to the underlying asset.

52004600 4800 5000

Profit

30

20

10

0

-10

-20

-30

Loss

Profit and lossat expiry (GBX)

Underlying priceat issue 5000

As can be seen from the above chart, the investorfaces no downside risk over the three year lifetimeof the product but takes part in 100% of anyupside performance.

This achieved by purchasing a zero coupon bond andusing the discount from nominal value to invest in aCall option. The zero coupon bond matures at par,thereby guaranteeing the investor’s capital, whilst theCall option maintains the upside exposure required.

The degree to which there is participation in theperformance of the financial asset and protectionover capital invested vary from product to product.This will largely depend on the maturity profile,forward interest rates plus the yield and volatilityof the underling asset (ignoring any FXconsiderations).

ExampleCapital Protected

Issuer: ABC Bank

Issue date: March 2005

Expiry date: March 2008

Participation: 100%

Protection level: 100%

Underlying asset: FTSE 100

Underlying price: 5000

Conversion ratio: 1000:1

Instrument price: 500p

FIG 7

L I S T E D S T R U C T U R E D P R O D U C T SL O N D O N S T O C K E X C H A N G E

Terms can varyfrom issuer to issuerDespite trading on exchange,these are not standardised,exchange defined contracts. Thespecifications of each product areat the discretion of the issuingbank and it is incumbent on theinvestor to check the detailsbefore trading. Term sheets arepublished and easily accessible forall issues.

Currency risk managementThere will be an inherent currencyrisk in structured products wherethe underlying is denominated ina foreign currency. This may be anoverseas equity index or dollarexposure through a commodityproduct. Certain products containan in built dynamic currency hedge,thereby eliminating this risk. Suchproducts are termed Quanto.

Automatic exerciseIt is a key feature of this marketthat should a product be held toexpiry, no special instructions arerequired to exercise. Any moniesdue to the investor will beautomatically credited throughCREST back to the broker.

1716

This brochure is intended to give examplesof some of the key types of structuredproducts throughout Europe and the UK -it is certainly not an exhaustive list of allstructures available. Although productprofiles can vary substantially, there are afew key factors investors should be awareof when looking to invest in listedstructured products.

Key points

19L I S T E D S T R U C T U R E D P R O D U C T S18 L O N D O N S T O C K E X C H A N G E

ConclusionStructured products, listed and tradedon the London Stock Exchange, representthe latest innovation in this rapidlygrowing asset class. They carry a numberof features that make them anattractive proposition:

FlexibilityThis is a bespoke market whereissuers will liaise with client inproducing tailored products as wellas proposing interesting tradingideas through issuance. The easewith which securitised derivativesissuance takes place means thatthere can be as little as 48 hoursbetween conception and issuanceof some products.

Access & liquidityAll those who currently access UKequity markets automatically haveaccess to the London StockExchange structured productsplatform. It is a single access pointoffering electronic and telephoneexecution, no central counterpartyand T+3 CREST settlement. Allissuers are obliged to maintaincontinuous prices throughout thelifetime of the products andadhere to standard market makerobligations (minimum size,maximum spread).

Diversity & CompetitivenessThe platform already has fourproviders with more in thepipeline. All issuers are majorinvestment banks with a globalreach allowing them to access ahuge variety of assets and priceproducts competitively. All havesignificant pan-Europeanexperience in issuing suchproducts despite the relative youthof the UK securitised derivativesmarket. The single platform meansthat those looking for bespokeproduct can easily put it out totender and compare productsand prices.

Information provisionNot only are real time pricesdisseminated by the London StockExchange, but a dedicated sectionof the website carries details of allproducts and issuers.

Information:www.londonstockexchange.com/structuredproducts

Enquiries:[email protected]

2 120 L O N D O N S T O C K E X C H A N G E L I S T E D S T R U C T U R E D P R O D U C T S

Accelerated trackerAn instrument which tracks anunderlying asset, providing gearedupside exposure with only 1:1downside exposure (from theinitial price of the underlying).The additional upside is offeredin return for surrenderingincome streams.

Barrier levelThis is the underlying price/levelwhich, if breached, will cause abarrier option to ‘knock out’(cease to exist) or ‘knock in’(come into existence).

Barrier optionThis is a generic term applied toany type of option thatincorporates a barrier level, i.e. anunderlying price which, if reached,causes the option to ‘knock out’and expire worthless immediatelyor ‘knock in’ (come intoexistence).

Bonus levelRepresents the amount that aninvestor is guaranteed to receiveshould the specific terms of aparticular financial instrumentbe met.

Bonus trackerA financial instrument that directlytracks the price of the underlyingasset, though guarantees a certainpayout on expiry should theunderlying asset price stay withina certain range. As a result, theseare often known as range traders(see page 10).

Cap levelThe cap level represents themaximum price achievable with adiscount certificate. Potentialupside exposure is sacrificed infavour of the ability to purchasethe underlying asset at a discountto the market price.

Capital protectedAn instrument which tracks anunderlying asset at a fixedparticipation rate, whilst protectingthe capital invested at a setpercentage.

CompositeA composite instrument isunhedged for currency risk (seepage 5).

Conversion ratio/parityThis ratio indicates the numberof warrants that must be held andexercised in buying or selling asingle unit of the asset, e.g.one share.

GlossaryDiscount trackerA financial instrument that givesdirect exposure to an underlyingasset at a discount to marketvalue but with limited upsideexposure (see page 12).

Down-and-out PutA type of barrier option. This Putoption will automatically cease toexist should a pre-defined pricelevel below the existing price levelbe reached in the underlyingasset.

ExerciseThe process of using the right tobuy or sell the underlying at thespecified price.

Exercise/Redemption valueThis is the value on exercise,whether it be early, automatic oron expiry, of any financialinstrument.

HedgeA hedge is typically accomplishedby making offsetting transactionsthat will largely eliminate one ormore types of risk.

In-the-Money (ITM)For a Call option, this is where thestrike price is less than the priceof the underlying. For a Put option,this is where the strike price isgreater than the price of theunderlying.

Knock out/inThis term is used to describe theaction of any financial instrumentthat, when the underlying pricereaches a pre-defined level,automatically expires/comes intoexistence. In the case of expiry,the terms of the instrument canvary such that it can expireworthless or with someredemption value.

Leverage(d)Term used to indicate that thepercentage price movementsare greater in a financialinstrument versus those of theunderlying asset.

LongA long position is when someonebuys (holds) a warrant or holds theunderlying asset. Contrasts withshort position.

MarginThe amount of cash that must beheld on account to cover positionswhen trading other types ofderivatives such as spread betsor CFDs.

QuantoAn instrument described as‘quanto’ incorporates a featurewhich ensures the tracker is fullyhedged for currency risk (seepage 5).

Reverse trackerA financial instrument that has adirect but inverse relationship withthe underlying asset price. Alsoknown as bear certificate (seepage 8).

ShortA term used to describe a positionwhich involves the sale of anasset without first holding theunderlying asset. Contrasts withlong position.

Stop lossThe price level of an underlyingasset at which automatic exerciseof a financial instrument will occur,thereby closing out the position.

Strike priceThe price at which the investormay buy or sell the underlyingduring (if American style) or at theend (if European style) of theexpiry period. Also referred to as‘expiry price and exercise price’. Itis normally fixed when the productis issued.

TrackerA financial instrument that directlytracks the price of the underlyingasset.

Can also be referred to as bull orbenchmark certificates (see page 4).

UnderlyingThe asset on which the product isbased and from which it derives itsvalue. The underlying may be asecurity (such as shares), a shareindex (e.g. FTSE 100), acommodity or a currency. Someproducts are based on a ‘basket’of underlyings, which gives aninvestor exposure to theperformance of more than onesecurity.

London Stock Exchange plc10 Paternoster SquareLondon EC4M 7LSTelephone +44 (0)20 7797 1000

www.londonstockexchange.com

Trackers and other structured products are not suitable for all investors and you should not deal inthem unless you understand their nature and the extent of your exposure to risk. Since this disclaimercannot cover all the risks and other significant aspects of these products, you should consult anappropriately qualified financial advisor if you are in any doubt. Information in this document isprovided for information only on an “AS IS” basis. It does not constitute professional, financial orinvestment advice and must not be used as a basis for making investment decisions and is in no wayintended, directly or indirectly, as an attempt to market or sell any type of financial instrument.

SEC/STR/MAS/030