lvmh strategic analysis

TRANSCRIPT

Khattab Al Qrarah Manas Ussenov Victoria Rosca Yousra Zaghdoud Bernichi 11.18.2014 1

LVMH Business review

Moët Hennessy • Louis Vuitton S.A.is a French multinational luxury goodsconglomerate, headquartered in Paris.

LVMH was formed by the 1987 merger of fashion house Louis Vuitton withMoët Hennessy (from the merger in 1971between the champagne producerMoët & Chandonand Hennessy, the cognac manufacturer.

2

LVMH Business review

Business Portfolio

• Wine and Spirits• Fashion &Leather Goods• Perfumes & Cosmetics• Watches & Jewelry• Selective Retailing• Media & Other Business

3

LVMH Facts

Chairman and CEO: Bernard Arnault

Revenue: 29.1 Billion Euros

Operational Profit: 6,021 Million Euros

Employees: 114,000 in over 70 countries

Distribution Channels : 3,384 Stores

60 Prestigious Brands

4

LVMH Revenue over category

5

LVMH Main Competitors

6

Timeline• 1743: M&C, established in Champagne Province (France). One of the first Champagne French brand, with exports

accounting for a large percentage of its sales by the 20th century

• 1968: Acquisition of Parfums Christian Dior

• 1971: Merger with Champagne Mercier

• 1971: Merger with Henessy & Cie (words second largest producer of cognac) -> Change name for Moët-Hennessy

• 1987: French government launched an area of privatization – Merger with Louis Vuitton, to avoid takeover from large international companies. Portofolio of uxury brands – Veuve Clicqot, Dom Pérignon, Canard Duchêne(wine), Christian Dior and Givenchy perfumes and cosmetics, Gearoges Delbard (grower or roses), Louis Vuitton, M&C, Hennessy

• 1987: Join ventures with Guinness PLC – distribution British cie

• 1988: Bernard Arnault – Owner of Chrstian Dior, Celine, and Christian Lacroix – purchase share of LVMH and join forces with Vuitton

• After a join venture with Guiness, Arnault became the LVMH’s largest shareholder, and ask for changes in the cie’smanagement

• 1988: Arnault acquire Givenchy

• 1989: Arnault became LVMH’s president

• 1990: Arnault became chairman

• 1990: Purchase interest on Loewe (Spanish brand) and all assets of Pommery (largest vineyard in Champagne region), increase of LVMH share in Guinness from 12% to 24% : LVMH became the world’s largest alcoholic beverage seller

• 1994: Arnault abandoned his quest to gain a controlling stake in Guinness, agreement to a stock swap

7

Timeline• Between 1990 and 1994, few small acquisitions

• Brought additional fashion and fragrance and diversified by purchasing 2 of France’s leading financial and business publications – Investir, La Tribune Desfosses, L’Agefi

• Expansion of the number of cie-owned retail stores where its LV, Loewe, Celine, CD, Givenchy can be found

• 1996: Arnault strongly believes that the brands should offer high quality customer service, acquisition of Duty Free Shopper (180 duty-free boutiques in Asia and various international airports)

• 1997: Acquisition of Sephora, French cosmetic retailer, and 30% interest in Douglas International, a German beauty-goods

• 1997: Acquisition of Château d’Yquem (Champagne)

• 1997: Purchase of 11% of Grand Metropolitan PLC – Britsh Food conglomerate ($1.5 bn wine and spririts sales)

• 1998: Retailing operations: La Belle Jardinière, Le Bon Marché

• 1998: Laflachère – France leading producer of hygiene beauty, and Marie-Jeanne Godard, a fine fragrance line

• 1999-2000: Boldest acquisition: TAH Heuer (watches), Ebel (watches), Chaumet (Jewelry), Zenith (Watches), Bliss, BeneFit, Hard Candy, Make Up For Ever, Fresh, Urban Decay (all make-up artists) Philips, de Pury & Luxembourg, L’Etude Tajan (all famous auction houses).

• Also these years, broadened the company’s media operations, thanks to a French radio network and magazines, New World wine produces in the US and Australia, retail outlets in the form of an Italian cosmetcs retailing chain,

• KRUG, producer of some of the wordl’t most expensive champagnes

• Emilio Pucci, Thomas Pink and Fendi acquisition

• 2001: Dona Karan International and La Samaritaine, the largest departement store in Paris

• Tried to acquire Gucci Group, but lost against the main competitor, PPR (today Kering)

8

LVMH Indutries

9

Luxury industry structureCharacteristics of luxury products

10

Global Market Size

Globaly growing market, sensitive to macro-events11

Growth by geographic markets

Important expected growth rate of the Asian Market12

Recent trendsGlobalization – over 40% of sales is from “luxury tourism”

13

Recent trendsGlobalization – plenty of untapped potential in emerging markets

14

Recent trendsConsolidation – individual brands are bought up by large luxury groups

15

Recent trendsConsolidation – large companies experience much higher margins

Brand recognition (esp. emerging markets) Economies of scale (eg. advertising) Optimal brand portfolio management

???

16

Recent trendsDiversification – apparel brands branch out to other luxury product categories, eg. jewelry, cosmetics, perfume, even restaurants

LVMH

17

5-forces model-Luxury industry

Rising popularity of middle-price brands

Consumers tend to trade down during economic crises

Counterfeit

Limited high skilled workersKey components and materials are

outsourcesHighly specialized “atelier d’art” with a narrow scope of expertiseCannot switch easily to another

supplier – risk a lower quality

Brand image and CRP programs build high brand loyalty

Scale economiesCapital requirement: very high

break-even pointExclusive access to suppliers &

distribution

Decreasing buyers concentrationIncerasing number of wealthy

househouldsTop-tier customers are usually early adopters and can drive consuption

No one single buyer can determine pricesIncreasing switching costs with loyalty

programs

Olipololy with the big 3Growing demand

High barrier for entry and high barrier to stay

Threat of Substitutes - Moderate

Threat of new entrants-Moderate to low

Rivalry among Existing competitorsHigh

Buyers’ Bargaining power - Low

Suppliers Bargaining PowerModerarte

18

Threat of new entrants

• Brand image and CRM programs build high brand loyalty

• Decreasing brand loyalty as a results of different needs in emerging markets

Traditional markets Emerging markets

• Craftmanship (artisanat)• Exclusivity• Innovation• Service• CRM• Heritage

• Extravagance• Status• Obvious brand logo-> Easily swith to other brands of similar status

19

Scale economies

Consolidation of luxury brands achieve high economies of scale – LVMH, PPR (Gucci), Prada Group, Richemont– Minimize risk through diversification in the company brand portfolio – More financing options e.g. IPO – Operating synergies e.g. advertising

High marketing & management costs – Distribution Fees:

– High rent to develop monobrand boutiques in prestigious shopping areas – e.g. South Korea’s Apgujeong; HK’s Tsim Sha Tsui Canton Road – To develop global presence, 400 stores are needed to cover the world!

– High salaries for craftsmen– High investment for promotional activities • • e.g. Chanel’s elaborate runway shows during Paris Fashion Week; Louis

Vuitton’s microfilm

20

Capital requirement

A very high break-even point • “...In the luxury sector, even the smaller brands have to

pretend they are powerful and rich, and by doing so they end up with a very high break-even.”

• “..For example, every brand must be present everywhere in the world.”

• “...If the Japanese tourist cannot find his Givenchy or Aquascutum store when he visits Milan or New York, he may well conclude that these brands are weak and he might decide to stop buying them in Japan.” (Abstract from “Luxury Brand Management: A world of Privilege”)

21

Exclusive Access to Suppliers & Distribution

• Many brands have acquired suppliers to protect competitive advantage and insulate against future rising supply costs

• E.g. LVMH acquired two watch dial manufacturers – Leman Cadran and ArteCadSA, French artisan shoemaker Delos Bottier & Cie and haute couture manufacturer Arnys.

Le Bon marché and desire to be present in the distribution

• More and more distribution access points are available to brands

• Contemporary areas like The Bund in Shanghai brings a multi- sensory experience to luxury

22

Potential retaliation from the existing companies

Small luxury brands do not have high barriers of distribution

– Pressure from powerful groups to prevent them from having access to multi-brand retailers

23

Threat of substitutes

• Price of substitues

• Quality if substitutes

• Switching costs to customers

24

Price of substitutes

• Rising popularity of middle price brands

• Consumers tend to “trade down” during economic crises

• Worldwide shipping of counterfeit goods from Turkey, China, North Africa, …

25

Quality of subsitutes

• Increased Internet accessibility of top luxury brand designs allow fast fashion brands to respond and copy trends within weeks after fashion shows

• e.g. Zara, Steve Madden

26

Switching cost to customer

• No monetary switching costs

• Loss of prestige if switch to high street or fast fashion brands

27

Buyers’ bargaining power

• Number of buyers relative to suppliers

• Level of dependence on a buyer

• Switching costs

• Possibility of buyer’s vertical integration

28

Number of buyers

Decreasing buyer concentration– Increasing number of buyers relative to suppliers

– Example: China’s emerging middle- class buyers

• Concept of “affordable luxuries” spreading in second-tier cities & satellite towns

– Increasing number of wealthy households

• Of the 1.6 million wealthy households, about 50 percent were not rich four years ago

29

Level of dependence on a buyer

• Luxury industry depends heavily on top-tier customers – Average spending by luxury consumers rose by

30% in 2009

– MOST driven by small groups of super- affluent top-tier consumers

• Top-tier customers eg. celebrities are usually early adopters and can drive consumption

• But not one single buyer can determine prices

30

Switching costs

• Buyers who develop an emotional attachment to the brand may have emotional switching costs

• Increasing switching costs with the introduction of customer loyalty programs

E.g. LV’s VIP clients receive free gifts

31

Possibility of backward integration

• Extremely low possibility

• Customers purchase luxury products for direct consumption

– No business reason for backward integration

• Size of luxury companies usually way out of a buyer’s purchasing power

32

Supplier’s bargaining power

• Number of suppliers relative to buyers

• Level of dependence on a supplier

• Effective substitues

• Switching costs (swith suppliers)

• Possibility of supplier’s vertical integration

33

Number of suppliers

• Limited high skilled workers

• Skills shortage – retiring craftsmen, not many youngsters willing to learn

• Couture-level embroiderers in France: ~10,000 in 1920, dropped to ~200 now

34

Level of dependence on a supplier

Some key components and materials are outsourced

– e.g. LV outsources its monogrammed leather

– Chanel ordered a large bunch of leathers from one supplier at one time in case they wouldn’t find a better one

35

Effective substitutes

Highly specialized “atelier d’arts” with a narrow scope of expertise

– E.g. Feather-maker Maison Lemarie , Costume jewellery and button-maker Desrues

– Very hard to replace

36

Switching costs

Cannot easily switch to another suppliers

– Past cooperating experience is important

– Risk a lower quality of products after switching to new suppliers

37

Possibility of forward integration

• Extremely low possibility

• Luxury companies, especially large groups, are much more powerful and wealthier than their manufacturers

38

Rivalry among existing competitors

• Competitive structure

• Demand condition

• Exit barriers

39

Market structure

Oligopoly– A few large luxury groups dominate

– Large number of small independent brands

– “Big Three”

• LVMH

• Richemont

• PPR Gucci

40

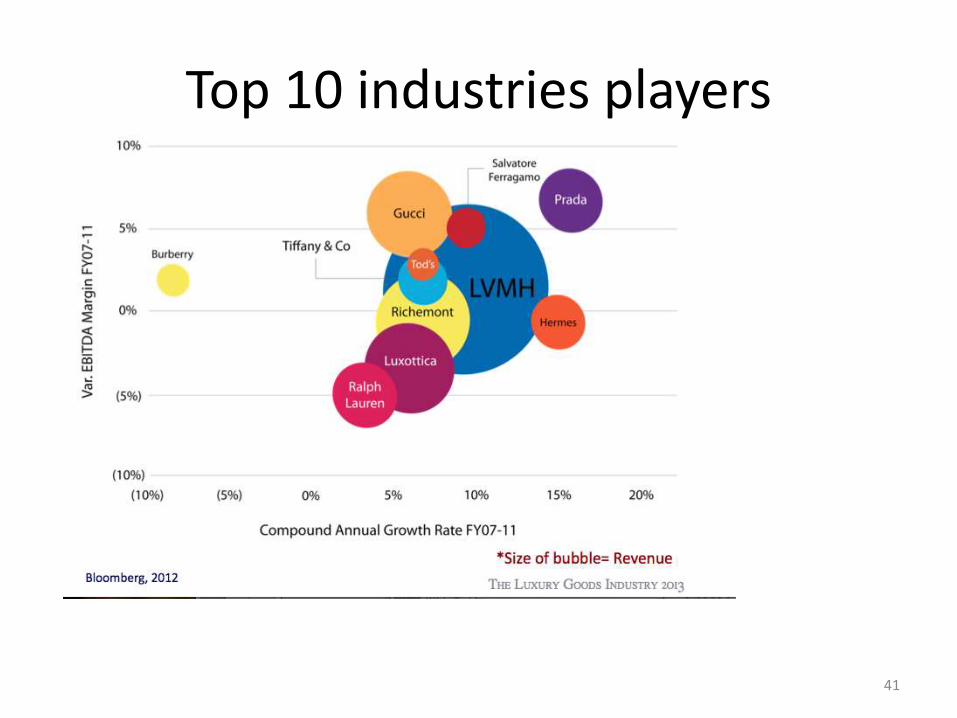

Top 10 industries players

41

Demand condition

• Demand will grow at a relatively high rate in the near future

42

Exit barriers

Emotional Barriers – Some brands may not break even but continue operating due to a small number of extremely loyal customers and critical acclaim – E.g. Christian Lacroix, never made a profit for the 22 years in operation

Specialized Assets – May be difficult to sell the highly specialized supply chain components – E.g. Chanel has 6 atelier d’arts under it

• Specialized machines no alternative purpose

43

5-forces model-LVMH

Many other products (Prada, Dior)Countefeit issues

Relatively lowLVMH purchase raw-materialssuppliers, which reduces loss

marking and establishes economiesof scales

e.g: recently bought Tanneries Roux

High entry barriersLVMH products, quality, serviceCost advantage due to the old

presence of the cie on the market

Targeted customers smaller in term of market size

2 types of customers : High-net income and middle-market customer

Not compatible: the first are quite loyal, and the second type more volatile

Olipololy with the big 3Growing demand

High barrier for entry and high barrier to stay

Wars of talents

Threat of Substitutes – Moderate to high

Threat of new entrants-Moderate to low

Rivalry among Existing competitorsHigh

Buyers’ Bargaining power - Low

Suppliers Bargaining PowerLow

44

Bargaining Power of Buyers

• Low.• Targeted customers are smaller in term of market size• 2 types of customers: fortunate (High Net worth individuals, seem not subject to the world economic cycles, and are a growing number (+9% per year) andmiddle-market customers - selectively trade-up to higher levels of quality, taste and aspiration)- Can potentially expand the market quite dramatically- Great opportunity but also a threats (more demanding, more selective,

showing less brand loyalty than the most fortunate ones.

-> Problem for the brand, because the 2 kinds of customers are not quite compatible, and this situation can lead to a difficult trade-off between satisfying a smaller number of loyal customers and a larger number of more volatile customers

45

Bargaining Power of Suppliers

• For LVMH, relatively low. Because the company often purchase raw materials from suppliers in basis of consignment. With this method, it reduces the loss marking and establishes economies of scale.

• e.g: LVMH has recently taken over les Tanneries Roux, a leather supplier. With this move to acquire key suppliers, it will reduce the bargaining power of suppliers in terms of leather products. By limiting the capability to plan suppliers contrary to each other. LVMH would be able to save costs on storage space and capable in making sure of the quality of products supplied.

46

Threats of new entrants

• Few new entrants threats which LVMH can focus on evaluate how much of a threat of new entrants are for LVMH

• New entrants made up mainly by new designers of new own brand in the industry, they are normally successful, and would be quickly acquired by the more famous brand of the industry to provide them facilities and needed infrastructure for growth.

• In return, if the new entrant remained independent, this would represent a threat to the company, by capturing volatile middle market customers. BUT these customers go after the established name and perception, which makes the threat of new entrants less significant.

• Also, the barriers to entry are high. Customer’s loyalty for LVMH among time, product service and quality are undeniable whereby a new entrant cannot be compatible for short period of time.

• LVMH has been functioning in the luxury products market for a century, giving them the complete cost advantage in business key development, which is absolute to new entrants by playing well in engaging their image in the market place to sustain their perception to cater not only customer’s need and wants but also the customers’ desires.

• New entrants find it difficult to survive and would easily be kicked out the market

47

Threats of substitute produtcs or services

• Relatively high.• Many other luxury products such as Prada, Dior, Chanel,

Hermes, Armani, …• Main competitors: PPr (now Kering, having Gucci, Yves

Saint Laurent, Boucheron, …) a,d Cie Financière Richemont(Cartier, Montblanc)

• Counterfeit issues: LVMH has to emphasis on the company core competency, uniqueness of product and service, and to attract and retain capable employees in order to have better value chain and distribution to reach the final users

• Louis Vuitton and their “ Toile Monogramme”, substitutes find it hard to earn in the market when the loyal customers are well-knowledge on the differences

48

Rivalry among existing competitors

• Relatively high• Oligopoly with 2 other main players: PPr (Kering) and Richemont.• BUT given the high margins and the customer’s perception about the price, the

competition is not on price, but on quality and image perception, as well as on the ability to attract the right designers with right abilities

• “Wars of Talent”, e.g, LVMH has the star designer Marc Jacobs for Louis Vuitton• The barriers to entry are very high. LVMH has built the intangible image and the

perception built around the brand.• Barriers to stay very hard to: continuous need to “feed” the image, to maintain the

perception but still to respond to customer’s need and changing expectations.• Trade-off between exclusivity, stylishness, extravagance and lasting image makes it

difficult to be for a long time in the business.• Hardly any barriers to exit given the high barriers to entry and to stay -> the

dynamics of the industry are: few big players and only the best• LVMH have to bear copycats as the high level of fakes as an open publicity and

competition from other brads, and there is only a limited group of customers who can afford to buy genuine product due to limited brands.

49

To sum up…

• The buyer power is reduces because buyers lack suitable alternatives

• To mitigate the power of suppliers, the companypurchase main raw materials suppliers in order to let the other players compete

• Creates higher entry barriers due to customer loyalty, to lower the treat of new entrants

• Establishes customer loyalty and hence less threat from substitutes

50

Competitve strategy of LVMH -Differentiation

• Unique products and services

• Price is not a problem: customers seek for uniqueness, prestige, brand image quality, and are glad pay a premium

• Customer service : importance to have controle on the retail channels for the highest level of customer service. The desire of Bernard Arnault to aquire retail points, in order to spread the luxury value not only on final product, but also during the purchase process and after sales

• Main competitors are not competing on prices, we can talk about a « high price parity »

• Integration of multiple points along the value chain

o Efficient order processing (e-commerce for all brands, LVMH e-commerce website)

o Very close relation with customers (mail, brochure, invitation for coktails, fashion shows, privates sales), espacially for main customers (loyalty programs, gifts)

o Customer service request are seriously taken into account: if a product is not available in a specific region, it will be ordered immedialty and receive as soon as possible

51

LVMH Strategy

Strategy-diversification into luxury goods

CORPORATE STRATEGY: business diversification, merger&aquisition

BUSINESS STRATEGY: focus on quality, Innovation, Marketing

52

Life cycle

LMVH position on the life cycle between

53

From 1999 to 2002

A slight decline in 2001, but the company has quickly caught in 2002

54

From 2009 to 2011

55

Value chain Analysis

Firm Infrastructure

HR Management

TechnologyDevelopment

Procurement

Primary Activities

Operations LogisticsMarketing

&SalesService

Combined shipping(Sea route, time saving)

•Decentralized System – various brands operate independently, with own creativity & brand image•Effective information technology• small nr of managers

Sup

po

rtA

ctiv

itie

s

•Product design, R&D process- carefully planned with the most modern and complete engineering technology•Production process - a creative process and perfectcombination of technology &handicraft

Control over thedistribution and sale of products among manybusiness units-Selective Retailing, MediaAdvertising inside desingteam-Distribution Channel100% exclusive

LVMH House

Premium serviceAfter saleLoyalty program

Cost Control & Resource Saving(common R&D group for variuosbusiness units + conductingdevelopment work => sharingresources and competences-most brands manufactured in country origin, few brands moved to low cost countries-strict control on quality

•Top designers•Special training for craftsmen•Emphasis on retining best talent and employees

A common supply chain management system

56

Sinergies of the Value Chain

• Interrelationships inside the firm – increase value & quality by exchanging practices and resources, knowledge sharing

Technology - exchange of technology via IntranetOperations - overlap among many businesses due to cost&resource savingSales & Marketing, Service- an obvious overlap, different businesses can lean on

each other for accessing the market given that target market is the same

• Relationships of activities within LVMH with customersand suppliers

- e-procurement- all businesses are trading in similar markets (high-end of the market,

premium price tag) => common practices in relation with customers

57

Resource-Based View of LVMH

• Competitive advantage => combination of tangible & intangible & organizational capabilities

• Tangible resources: - Physical Assets: numerous factories in France, Spain, Italy;

sophisticated machinery&equipment- Large financial capabilities- Technological resources: artistic creativity & an innovative

production process , trademarks, patents (LVMH Recherche)- Organizational resources: effective planning (carefully planned

production process, distribution ; effective control on distribution&sales

- Core assets of acquired brand are assessed and partly preserved

58

Resource-Based View of LVMH

• Intangible resources:- Well-known designers, high experience & capabilities craftsmen and other

employees, strong managerial skills- LVMH Recherche: innovation capabilities & scientific expertise- Reputation: image and brand names- Creative team and management of acquired firms are preserved- Knowledge is shared but at the same time the culture of company is maintained

• Organizational capabilities:- Great capability of the management of luxury brands: market analysis, product

development, advertising, promotion, retail management, customer service, quality assurance.

- capabilities are deployed across Louis Vuitton (accessories and leather goods); Hennessey (cognac); Moetet Chandon, Dom Perignon, Veuve Clicquot, and Krug (champagne); Celine, Givenchy, Kenzo, Dior, Guerlain, and Donna Karan (fashion clothing and perfumes); TAG Heuer and Chaumet (watches); Sephoraand La Samaritaine (retailing); and some 25 other branded businesses

59

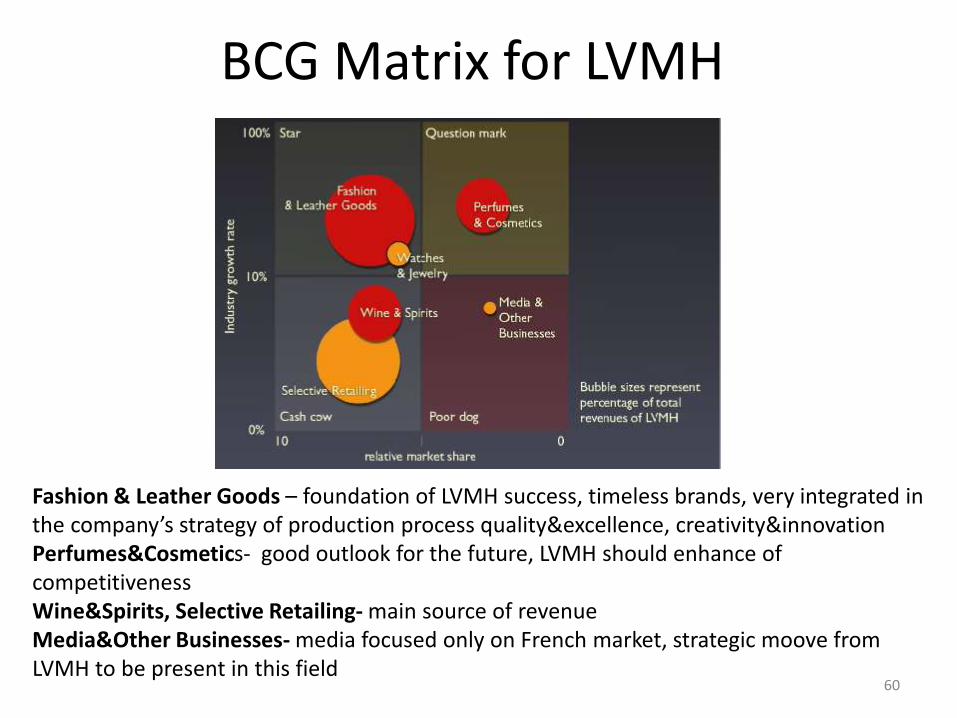

BCG Matrix for LVMH

Fashion & Leather Goods – foundation of LVMH success, timeless brands, very integrated in the company’s strategy of production process quality&excellence, creativity&innovationPerfumes&Cosmetics- good outlook for the future, LVMH should enhance of competitivenessWine&Spirits, Selective Retailing- main source of revenueMedia&Other Businesses- media focused only on French market, strategic moove fromLVMH to be present in this field

60

Innovation in

two types of innovation:

1. Product innovation

2. Process innovation

61

Product innovation in LVMH

• LVMH Recherche, founded in 1981 as a G.I.E. (Groupement d’Intérêt

Economique).

• Members: Parfums Christian Dior, Guerlain and Parfums Givenchy.

• Approximately 250 researchers (in Saint Jean de Braye).

• Areas of research: biologists, chemists, pharmacists, medical doctors,

ethno botanists, physicists

• Mission: develop innovative cosmetic approaches based on the latest

scientific discoveries.

• Collaborative studies with researchers in the major universities and

research centers (Ex. Cooperation with University of Orleon).

• The expertise and the know-how of its researchers in the fields of skin

biology, of formulation, as well as its discoveries of active ingredients

and evaluation methods of cosmetic products (skin care, make-up,

perfumes)

62

Process Innovation in LVMH

• The main core of the innovation creativity of the

designers.

• Giving complete freedom to designers by

decentralization of the department. Each brand

very much runs itself, headed by its own artistic

director

• Inventing product to see the creations on the

“street” on their costumers.

• Picking up right designers and ateliers , training

them for and maintaining them for a long time

• Specific testing of products comparing with

competitor’s products

Hand made Louis Vitton shoes

63

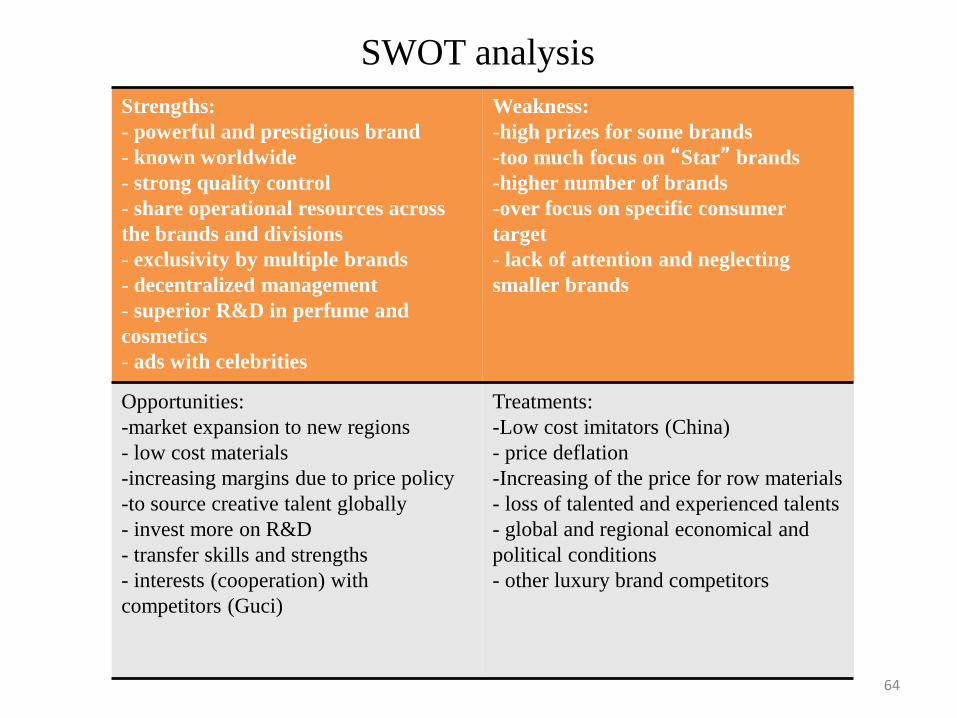

Strengths:

- powerful and prestigious brand

- known worldwide

- strong quality control

- share operational resources across

the brands and divisions

- exclusivity by multiple brands

- decentralized management

- superior R&D in perfume and

cosmetics

- ads with celebrities

Weakness:

-high prizes for some brands

-too much focus on “Star” brands

-higher number of brands

-over focus on specific consumer

target

- lack of attention and neglecting

smaller brands

Opportunities:

-market expansion to new regions

- low cost materials

-increasing margins due to price policy

-to source creative talent globally

- invest more on R&D

- transfer skills and strengths

- interests (cooperation) with

competitors (Guci)

Treatments:

-Low cost imitators (China)

- price deflation

-Increasing of the price for row materials

- loss of talented and experienced talents

- global and regional economical and

political conditions

- other luxury brand competitors

SWOT analysis

64

PESTEL analysis

Political:

-Establishing of Anti-Counterfeiting

Trade Agreement (ACTA)

-Political Issues for cheap labor in

Asia

-Good International relations for

trade

-Existing commerce infrastructure

-Being part of EU, allowing to make

easy trade with same currency within

the Europe

-Trade sanctions (Sanction against

Iran)

-Reluctance to trade with specific

regions (Middle east)

Economic:

- One the leader economies

LVMH’s impact on globalization

-Exchange rates: USA, EU, Asia

-Global economy: out of recession

-Inflation rate: low

-Interest rate: low

- large presence of workforce: more

people-lower wage, less people-

reduced production

Social:

-Workforce age: increase in

workforce population (baby boom

echo)

-Market age: baby boomers are

affluent

- religion: taboo for alcohol and

materialism

- trends: fashion and innovation

-Perception of prestigious items

Technological:

- High percentage of R&D

expenditure in France

-Good presence of online marketing

service

-Strong base Machinery and chemical

formulas

-Presence of social media

Legal:

-embargos: can lead for loss market

- labor low: inflexible but secure

- truth in advertising: EU bans

misleading ads.

- counterfeiting: reduces prestige

Environmental:

-Climate change: change in arable

lands (vineyards)

-Energy waste: effects on distribution

costs

-Carbon footprint: huge amount of

CO2 in wine production

-Quality of Water

-Reserve the natural resources

65

Conclusion

• LVMH is the one of the main actor of luxury goods retailing and luxury marketing

• Through numerous acquisitions, this company takes the biggest share in a notoriously fickle market.

• With an increasing revenue despite a global recession, and the fact that most LVMH products are high-priced and never go on sale is a testament to both tremendous quality and masterful marketing.

• Planning for the future, LVMH must be cognizant of the emerging BRICS nations, in addition, to the rising elite of China and Indie simply due to their population size.

• LVMH must also invest wisely in the emerging markets and attept to acquire PPE at low costs in order to help maintain a profitable bottom line.

• Paramount to all, LVMH must stay true to its core competency –selling the world’s premier luxury lifestyle

66