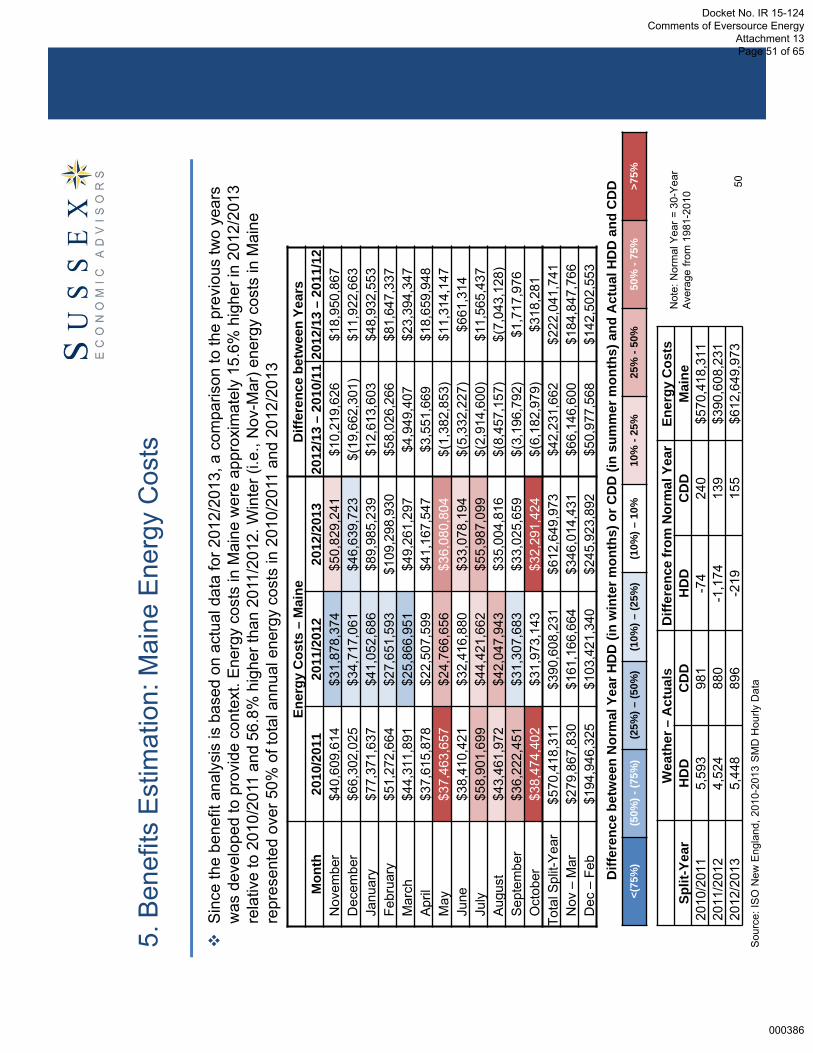

maine public utilities commission review of natural … investigation/eversource... · maine public...

TRANSCRIPT

Mai

ne P

ublic

Utili

ties

Com

miss

ion

Rev

iew

of N

atur

al G

as C

apac

ity O

ptio

ns

Febr

uary

26,

201

4

Suss

ex E

cono

mic

Adv

isor

s, L

LC (“

Suss

ex”)

has

relie

d up

on c

erta

in p

ublic

sou

rces

of i

nfor

mat

ion

cons

iste

nt w

ith s

tand

ard

cons

ultin

g pr

actic

es. S

usse

x m

akes

no

war

rant

ies

or g

uara

ntee

s re

gard

ing

the

accu

racy

of a

ny e

stim

ates

, pro

ject

ions

or a

naly

ses

cont

aine

d he

rein

. Tho

se re

view

ing

the

info

rmat

ion

cont

aine

d he

rein

wai

ve a

ny c

laim

aga

inst

Sus

sex,

its

partn

ers

and

empl

oyee

s.

Sus

sex

shal

l not

be

liabl

e to

any

par

ty re

view

ing

this

info

rmat

ion.

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 1 of 65

000336

Con

tent

s

1.In

trod

uctio

n

Legi

slat

ive

Bac

kgro

und

P

roje

ct O

bjec

tive

and

Rep

ort O

rgan

izat

ion

2.E

xecu

tive

Sum

mar

y

3.N

atur

al G

as M

arke

t Ove

rvie

w

4.N

atur

al G

as P

ipel

ine

Cap

acity

Opt

ions

5.C

ost /

Ben

efit

Ana

lysi

s

6.S

umm

ary

and

Con

clus

ions

1

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 2 of 65

000337

1. In

trodu

ctio

n: L

egis

lativ

e B

ackg

roun

d

B

ased

on

the

rece

ntly

ena

cted

H.P

. 112

8 –

L.D

. 155

9 (i.

e., A

n A

ct to

Red

uce

Ene

rgy

Cos

ts, I

ncre

ase

Ene

rgy

Effi

cien

cy, P

rom

ote

Ele

ctric

Sys

tem

Rel

iabi

lity

and

Pro

tect

th

e E

nviro

nmen

t), th

e M

aine

Pub

lic U

tiliti

es C

omm

issi

on (“

Mai

ne P

UC

”) h

as th

e ab

ility

to e

xecu

te c

ontra

cts

for n

atur

al g

as p

ipel

ine

capa

city

:3.

Par

ties

to a

n en

ergy

cos

t red

uctio

n co

ntra

ct. T

he c

omm

issi

on m

ay e

xecu

te, o

r dire

ct to

be

exec

uted

, an

ener

gy c

ost r

educ

tion

cont

ract

that

con

tain

s th

e fo

llow

ing

prov

isio

ns.

A. T

he c

omm

issi

on m

ay d

irect

one

or m

ore

trans

mis

sion

and

dis

tribu

tion

utili

ties,

gas

util

ities

or

natu

ral g

as p

ipel

ine

utili

ties

to b

e a

coun

terp

arty

to a

n en

ergy

cos

t red

uctio

n co

ntra

ct. I

n de

term

inin

g w

heth

er a

nd to

wha

t ext

ent t

o di

rect

a u

tility

to b

e a

coun

terp

arty

to a

con

tract

un

der t

his

subs

ectio

n, th

e co

mm

issi

on s

hall

cons

ider

the

antic

ipat

ed re

duct

ion

in th

e pr

ice

of

gas

or e

lect

ricity

, as

appl

icab

le, a

ccru

ing

to th

e cu

stom

ers

of th

e ut

ility

as

a re

sult

of th

e co

ntra

ct a

s de

term

ined

by

the

com

mis

sion

in a

n ad

judi

cato

ry p

roce

edin

g.A

ny e

cono

mic

loss

, inc

ludi

ng b

ut n

ot li

mite

d to

any

effe

cts

on th

e co

st o

f cap

ital r

esul

ting

from

an

ene

rgy

cost

redu

ctio

n co

ntra

ct fo

r a tr

ansm

issi

on a

nd d

istri

butio

n ut

ility

, a g

as u

tility

or a

na

tura

l gas

pip

elin

e ut

ility

, is

deem

ed to

be

prud

ent a

nd th

e co

mm

issi

on s

hall

allo

w fu

ll re

cove

ry th

roug

h th

e ut

ility

's ra

tes.

B. I

f the

com

mis

sion

con

clud

es th

at a

n en

ergy

cos

t red

uctio

n co

ntra

ct c

an b

e ac

hiev

ed w

ith th

e pa

rtici

patio

n of

oth

er e

ntiti

es, t

he c

omm

issi

on m

ay c

ontra

ct jo

intly

with

oth

er e

ntiti

es, i

nclu

ding

ot

her s

tate

age

ncie

s an

d in

stru

men

talit

ies,

gov

ernm

ents

in o

ther

sta

tes

and

natio

ns, u

tiliti

es

and

gene

rato

rs.

C. T

he c

omm

issi

on m

ay e

xecu

te a

n en

ergy

cos

t red

uctio

n co

ntra

ct a

s a

prin

cipa

l and

co

unte

rpar

ty.

2

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 3 of 65

000338

1. In

trodu

ctio

n: P

roje

ct O

bjec

tive

and

Rep

ort O

rgan

izat

ion

S

usse

x E

cono

mic

Adv

isor

s, L

LC (“

Sus

sex”

) was

reta

ined

by

the

Mai

ne P

UC

to

revi

ew th

e va

rious

nat

ural

gas

pip

elin

es s

ervi

ng N

ew E

ngla

nd, t

heir

rela

ted

open

sea

sons

for c

apac

ity, a

nd th

e po

tent

ial c

osts

and

ben

efits

of i

ncre

men

tal

natu

ral g

as d

eliv

erab

ility

into

New

Eng

land

. The

rem

aind

er o

f thi

s re

port

is

orga

nize

d as

follo

ws:

S

ectio

n 2

–Ex

ecut

ive

Sum

mar

y: P

rovi

des

an e

xecu

tive

sum

mar

y of

the

key

obse

rvat

ions

and

find

ings

S

ectio

n 3

–N

atur

al G

as M

arke

t Ove

rvie

w: P

rovi

des

an o

verv

iew

of t

he c

urre

nt n

atur

al

gas

mar

kets

in N

ew E

ngla

nd, w

ith a

par

ticul

ar fo

cus

on M

aine

; dis

cuss

es th

e re

gion

al

natu

ral g

as d

eman

d an

d su

pply

driv

ers;

and

revi

ews

natu

ral g

as p

rices

and

bas

is v

alue

s

Sec

tion

4 –

Nat

ural

Gas

Pip

elin

e C

apac

ity O

ptio

ns: I

dent

ifies

and

revi

ews

the

natu

ral

gas

pipe

line

capa

city

opt

ions

into

New

Eng

land

S

ectio

n 5

–C

ost /

Ben

efit

Ana

lysi

s: P

rovi

des

an e

stim

ate

of th

e co

sts

and

bene

fits

asso

ciat

ed w

ith in

crem

enta

l pip

elin

e ca

paci

ty in

to th

e N

ew E

ngla

nd re

gion

S

ectio

n 6

–Su

mm

ary

and

Con

clus

ions

: Sum

mar

izes

the

obse

rvat

ions

and

con

clus

ions

ba

sed

on th

e an

alys

es a

nd re

sear

ch p

rese

nted

her

ein

3

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 4 of 65

000339

Con

tent

s

1.In

trodu

ctio

n

2.Ex

ecut

ive

Sum

mar

y

3.N

atur

al G

as M

arke

t Ove

rvie

w

4.N

atur

al G

as P

ipel

ine

Cap

acity

Opt

ions

5.C

ost /

Ben

efit

Ana

lysi

s

6.S

umm

ary

and

Con

clus

ions

4

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 5 of 65

000340

2. E

xecu

tive

Sum

mar

y: N

atur

al G

as D

eman

d D

river

s

Th

ere

is s

igni

fican

t act

ivity

affe

ctin

g na

tura

l gas

dem

and

in th

e N

ew E

ngla

nd,

New

Yor

k C

ity a

nd A

tlant

ic C

anad

a re

gion

M

aine

: loc

al d

istri

butio

n co

mpa

nies

(“LD

Cs”

) hav

e si

gnifi

cant

nat

ural

gas

exp

ansi

on

plan

s

Con

nect

icut

Com

preh

ensi

ve E

nerg

y S

trate

gy (“

CT

CE

S”)

: pot

entia

l for

300

,000

new

na

tura

l gas

cus

tom

ers

over

the

next

sev

en to

ten

year

s

Mas

sach

uset

ts: D

epar

tmen

t of E

nerg

y R

esou

rces

(“D

OE

R”)

has

spo

nsor

ed a

stu

dy

rega

rdin

g po

tent

ial p

olic

y ch

ange

s as

soci

ated

with

LD

C e

xpan

sion

N

ew Y

ork

City

: no

perm

its fo

r No.

4 a

nd 6

fuel

oil

unle

ss e

mis

sion

s ar

e eq

uiva

lent

to N

o.

2 oi

l, w

hich

has

resu

lted

in s

igni

fican

t con

vers

ion

to n

atur

al g

as; C

on E

diso

n es

timat

ed

peak

day

gro

wth

of a

ppro

xim

atel

y 4%

A

tlant

ic C

anad

a: in

crea

sing

dem

and

for n

atur

al g

as fr

om th

e LD

C a

nd p

ower

gen

erat

ion

segm

ents

IS

O N

ew E

ngla

nd (“

ISO

-NE

”): i

ncre

asin

g re

lianc

e on

nat

ural

gas

, as

over

hal

f of t

he

gene

ratio

n in

the

inte

rcon

nect

ion

queu

e is

nat

ural

gas

-fire

d; n

early

10%

of I

SO

-NE

’s to

tal

gene

ratin

g ca

paci

ty is

sch

edul

ed to

be

retir

ed o

ver t

he n

ext t

hree

yea

rs

5

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 6 of 65

000341

2. E

xecu

tive

Sum

mar

y: N

atur

al G

as S

uppl

y D

river

s

E

aste

rn C

anad

a:

Dec

reas

ing

prod

uctio

n fro

m th

e S

able

Offs

hore

Ene

rgy

Pro

ject

(“S

OE

P”)

D

eep

Pan

uke

is o

n-lin

e an

d at

full

volu

me

(i.e.

, app

roxi

mat

ely

300

MM

cf/d

ay);

how

ever

, th

ere

are

unce

rtain

ties

rega

rdin

g su

stai

nabi

lity

and

dura

tion

of p

rodu

ctio

n

Li

quef

ied

Nat

ural

Gas

(“LN

G”):

M

assa

chus

etts

off-

shor

e fa

cilit

ies

have

not

rece

ived

any

car

goes

in th

e pa

st 3

yea

rs

Can

apor

t LN

G a

nd G

DF

SU

EZ

volu

mes

are

app

roxi

mat

ely

50%

of p

revi

ous

leve

ls

Alte

rnat

ive

mar

ket p

rices

for L

NG

are

cur

rent

ly m

ore

attra

ctiv

e th

an N

ew E

ngla

nd m

arke

t in

dex

pric

es

D

awn

Gas

Sup

ply

Hub

(“D

awn

Hub

”) / W

este

rn C

anad

a:

Tran

sCan

ada

Pip

elin

es L

imite

d (“

TCP

L”) M

ainl

ine,

the

prim

ary

pipe

line

deliv

erin

g C

anad

ian

natu

ral g

as s

uppl

ies

to N

ew E

ngla

nd, h

as re

ache

d a

toll

and

serv

ice

settl

emen

t with

the

maj

or e

aste

rn C

anad

ian

LDC

s. T

he s

ettle

men

t was

sub

mitt

ed fo

r re

view

by

the

Nat

iona

l Ene

rgy

Boa

rd (“

NE

B”)

in D

ecem

ber 2

013,

and

as

a re

sult,

the

tolls

for s

ervi

ce o

n th

e TC

PL

Mai

nlin

e w

ill b

e su

bjec

t to

the

resu

lts a

nd ti

min

g of

that

pr

ocee

ding

A

lgon

quin

Gas

Tra

nsm

issi

on (“

AG

T”) /

Ten

ness

ee G

as P

ipel

ine

(“TG

P”):

M

arce

llus

Sha

le g

as p

rodu

ctio

n co

ntin

ues

to g

row,

whi

ch h

as in

crea

sed

the

utili

zatio

n of

th

e A

GT

and

TGP

pipe

lines

and

has

resu

lted

in in

crea

sed

inte

rrup

tible

or n

on-fi

rm

serv

ice

rest

rictio

ns6

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 7 of 65

000342

2. E

xecu

tive

Sum

mar

y: R

esul

tant

Nat

ural

Gas

Pric

e S

igna

ls

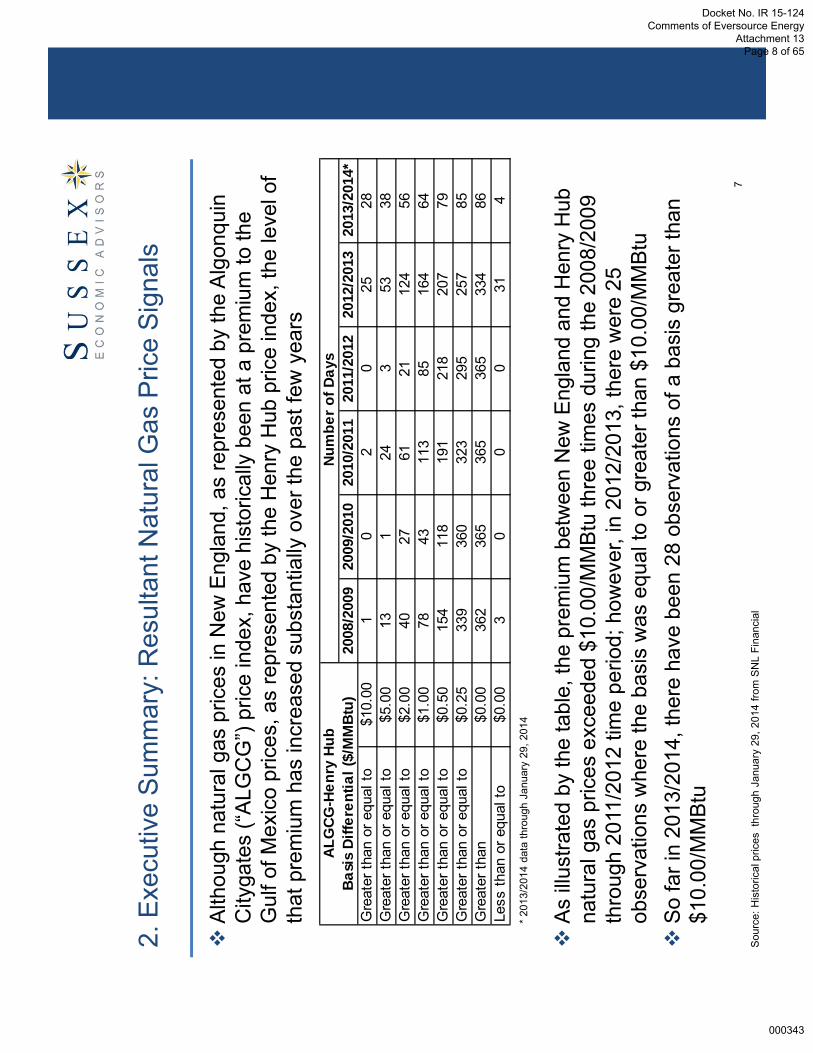

A

lthou

gh n

atur

al g

as p

rices

in N

ew E

ngla

nd, a

s re

pres

ente

d by

the

Alg

onqu

in

City

gate

s (“A

LGC

G”)

pric

e in

dex,

hav

e hi

stor

ical

ly b

een

at a

pre

miu

m to

the

Gul

f of M

exic

o pr

ices

, as

repr

esen

ted

by th

e H

enry

Hub

pric

e in

dex,

the

leve

l of

that

pre

miu

m h

as in

crea

sed

subs

tant

ially

ove

r the

pas

t few

yea

rs

A

s illu

stra

ted

by th

e ta

ble,

the

prem

ium

bet

wee

n N

ew E

ngla

nd a

nd H

enry

Hub

na

tura

l gas

pric

es e

xcee

ded

$10.

00/M

MB

tu th

ree

times

dur

ing

the

2008

/200

9 th

roug

h 20

11/2

012

time

perio

d; h

owev

er, i

n 20

12/2

013,

ther

e w

ere

25

obse

rvat

ions

whe

re th

e ba

sis

was

equ

al to

or g

reat

er th

an $

10.0

0/M

MB

tu

So

far i

n 20

13/2

014,

ther

e ha

ve b

een

28 o

bser

vatio

ns o

f a b

asis

gre

ater

than

$1

0.00

/MM

Btu

* 20

13/2

014

data

thro

ugh

Janu

ary

29, 2

014

Sou

rce:

His

toric

al p

rices

thr

ough

Jan

uary

29,

201

4 fro

m S

NL

Fina

ncia

l

2008

/200

920

09/2

010

2010

/201

120

11/2

012

2012

/201

320

13/2

014*

Gre

ater

than

or e

qual

to$1

0.00

10

20

2528

Gre

ater

than

or e

qual

to$5

.00

131

243

5338

Gre

ater

than

or e

qual

to$2

.00

4027

6121

124

56G

reat

er th

an o

r equ

al to

$1.0

078

4311

385

164

64G

reat

er th

an o

r equ

al to

$0.5

015

411

819

121

820

779

Gre

ater

than

or e

qual

to$0

.25

339

360

323

295

257

85G

reat

er th

an$0

.00

362

365

365

365

334

86Le

ss th

an o

r equ

al to

$0.0

03

00

031

4

ALG

CG-H

enry

Hub

Ba

sis

Diffe

rent

ial (

$/M

MBt

u)Nu

mbe

r of D

ays

7

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 8 of 65

000343

2. E

xecu

tive

Sum

mar

y: N

atur

al G

as P

ipel

ine

Cap

acity

Opt

ions

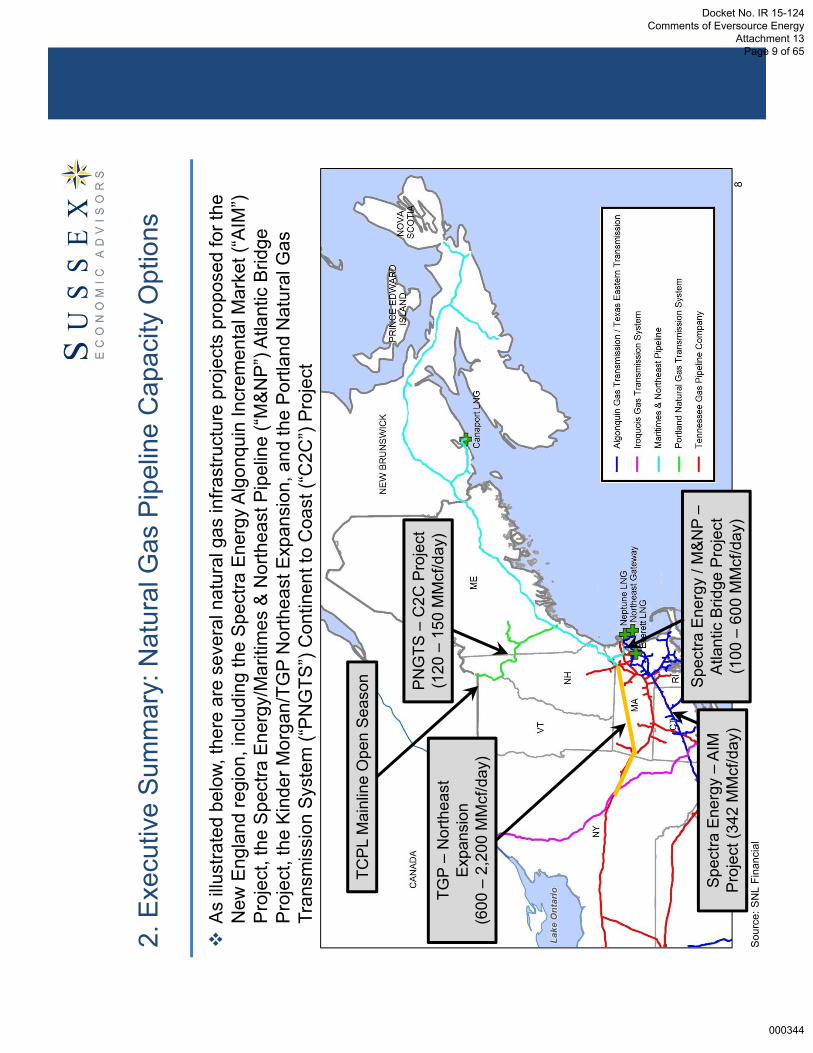

A

s ill

ustra

ted

belo

w, th

ere

are

seve

ral n

atur

al g

as in

frast

ruct

ure

proj

ects

pro

pose

d fo

r the

N

ew E

ngla

nd re

gion

, inc

ludi

ng th

e S

pect

ra E

nerg

y A

lgon

quin

Incr

emen

tal M

arke

t (“A

IM”)

Pro

ject

, the

Spe

ctra

Ene

rgy/

Mar

itim

es &

Nor

thea

st P

ipel

ine

(“M

&N

P”)

Atla

ntic

Brid

ge

Pro

ject

, the

Kin

der M

orga

n/TG

P N

orth

east

Exp

ansi

on, a

nd th

e P

ortla

nd N

atur

al G

as

Tran

smis

sion

Sys

tem

(“P

NG

TS”)

Con

tinen

t to

Coa

st (“

C2C

”) P

roje

ct

Spe

ctra

Ene

rgy

–AI

M

Pro

ject

(342

MM

cf/d

ay)

TGP

–N

orth

east

Ex

pans

ion

(600

–2,

200

MM

cf/d

ay)

PN

GTS

–C

2C P

roje

ct(1

20 –

150

MM

cf/d

ay)

Spe

ctra

Ene

rgy

/ M&

NP

–A

tlant

ic B

ridge

Pro

ject

(1

00 –

600

MM

cf/d

ay)

TCP

L M

ainl

ine

Ope

n S

easo

n

Sou

rce:

SN

L Fi

nanc

ial

8

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 9 of 65

000344

2. E

xecu

tive

Sum

mar

y: C

ost /

Ben

efit

Ana

lysi

s –

New

Eng

land

B

ased

on

the

rela

tions

hip

betw

een

natu

ral g

as p

rices

and

ele

ctric

ity lo

catio

nal

mar

gina

l pric

es (“

LMP

s”) i

n IS

O-N

E, S

usse

x ca

lcul

ated

the

pote

ntia

l red

uctio

n in

LM

Ps

as a

resu

lt of

a re

duct

ion

in w

hole

sale

nat

ural

gas

pric

es to

est

imat

e th

e po

tent

ial e

nerg

y co

st s

avin

gs to

ele

ctric

ity c

usto

mer

s fo

r the

201

2/20

13

split

-yea

r[1]

A

s illu

stra

ted

by th

e ta

bles

bel

ow, a

40%

redu

ctio

n in

the

New

Eng

land

nat

ural

ga

s ba

sis

(i.e.

, a lo

wer

ing

of th

e pr

emiu

m b

etw

een

New

Eng

land

and

Gul

f of

Mex

ico

natu

ral g

as p

rice

indi

ces)

wou

ld o

ffset

1,0

00,0

00 D

th/d

ay o

f inc

rem

enta

l pi

pelin

e ca

paci

ty, a

ssum

ing

a da

ily p

ipel

ine

char

ge a

s hi

gh a

s $2

.00/

Dth

Not

e: [1

] Spl

it-ye

ar is

def

ined

as

the

twel

ve-m

onth

per

iod

from

Nov

embe

r to

Oct

ober

Estim

ated

Ben

efits

Bas

is R

educ

tion

of:

Annu

al E

nerg

y C

ost S

avin

gs fo

r M

aine

Cus

tom

ers

($)

Annu

al E

nerg

y C

ost S

avin

gs fo

r IS

O-N

E C

usto

mer

s ($

)25

%$4

0,04

7,60

5$4

67,6

68,0

31

30%

$48,

057,

127

$561

,201

,637

35%

$56,

066,

648

$654

,735

,243

40%

$64,

076,

169

$748

,268

,849

45%

$72,

085,

690

$841

,802

,455

50%

$80,

095,

211

$935

,336

,062

55%

$88,

104,

732

$1,0

28,8

69,6

68

60%

$96,

114,

253

$1,1

22,4

03,2

74

65%

$104

,123

,774

$1,2

15,9

36,8

80

70%

$112

,133

,295

$1,3

09,4

70,4

86

75%

$120

,142

,816

$1,4

03,0

04,0

92

Cos

t Ass

umpt

ions

(1,0

00,0

00 D

th)

Rat

e($

/Dth

)C

apac

ity (D

th)

Annu

al C

ost

($)

$1.0

01,

000,

000

$365

,000

,000

$1.1

01,

000,

000

$401

,500

,000

$1.2

01,

000,

000

$438

,000

,000

$1.3

01,

000,

000

$474

,500

,000

$1.4

01,

000,

000

$511

,000

,000

$1.5

01,

000,

000

$547

,500

,000

$1.6

01,

000,

000

$584

,000

,000

$1.7

01,

000,

000

$620

,500

,000

$1.8

01,

000,

000

$657

,000

,000

$1.9

01,

000,

000

$693

,500

,000

$2.0

01,

000,

000

$730

,000

,000

9

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 10 of 65

000345

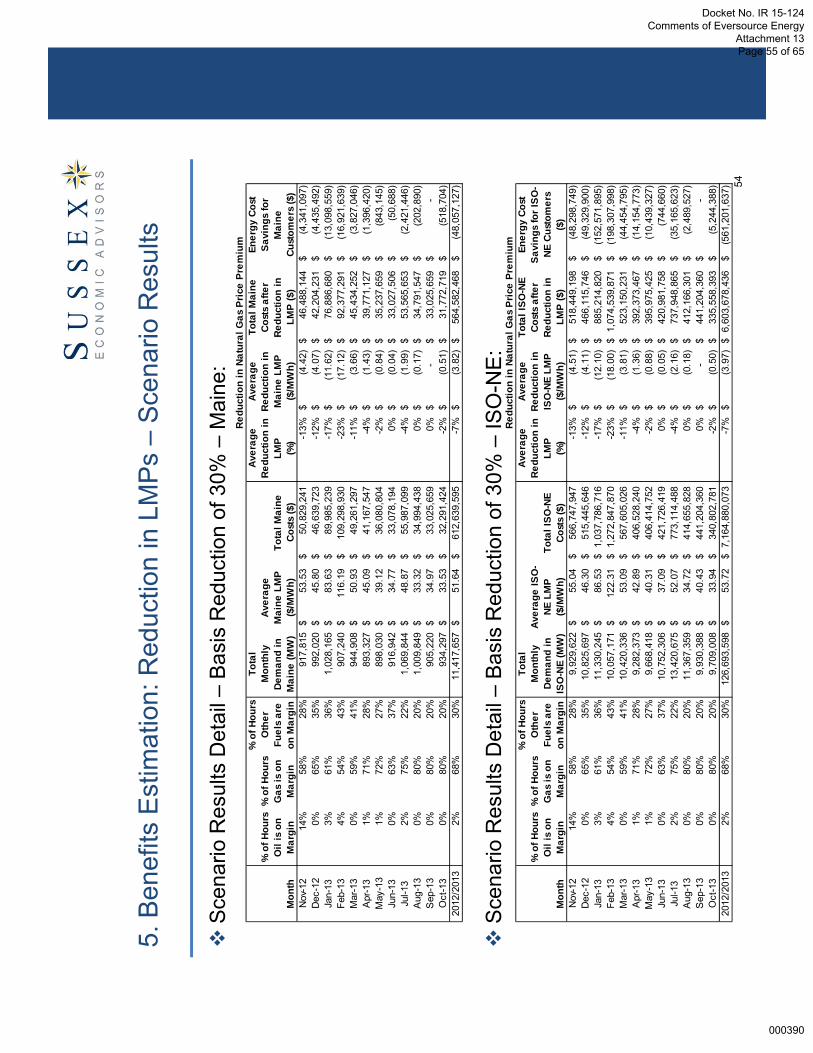

2. E

xecu

tive

Sum

mar

y: C

ost /

Ben

efit

Ana

lysi

s –

Mai

ne

A

cost

/ be

nefit

ana

lysi

s w

as a

lso

cond

ucte

d fo

r Mai

ne u

sing

an

appr

oach

si

mila

r to

the

ISO

-NE

ana

lysi

s di

scus

sed

earli

er a

nd u

nder

two

volu

me

scen

ario

s (i.

e., 5

0,00

0 D

th a

nd 2

00,0

00 D

th)

A

s in

dica

ted

in th

e ta

bles

bel

ow, t

he e

stim

ated

ann

ual b

enef

its to

Mai

ne u

nder

a

scen

ario

in w

hich

the

natu

ral g

as b

asis

is re

duce

d by

40%

is a

ppro

xim

atel

y $6

4 m

illion

, whi

ch w

ould

offs

et a

50,

000

Dth

/day

con

tract

ass

umin

g a

daily

rate

as

high

as

$2.0

0/D

th

How

ever

, the

est

imat

ed a

nnua

l ben

efits

to M

aine

of a

ppro

xim

atel

y $6

4 m

illion

w

ould

not

offs

et a

200

,000

Dth

/day

con

tract

at a

dai

ly ra

te o

f a $

1.00

/Dth

Estim

ated

Ben

efits

Bas

is

Red

uctio

n of

:

Annu

al E

nerg

y C

ost S

avin

gs fo

r M

aine

Cus

tom

ers

($)

25%

$40,

047,

605

30%

$48,

057,

127

35%

$56,

066,

648

40%

$64,

076,

169

45%

$72,

085,

690

50%

$80,

095,

211

55%

$88,

104,

732

60%

$96,

114,

253

65%

$104

,123

,774

70%

$112

,133

,295

75%

$120

,142

,816

Cos

t Ass

umpt

ions

(200

,000

Dth

)

Rat

e($

/Dth

)C

apac

ity (D

th)

Annu

al C

ost

($)

$1.0

020

0,00

0$7

3,00

0,00

0$1

.10

200,

000

$80,

300,

000

$1.2

020

0,00

0$8

7,60

0,00

0

$1.3

020

0,00

0$9

4,90

0,00

0

$1.4

020

0,00

0$1

02,2

00,0

00

$1.5

020

0,00

0$1

09,5

00,0

00

$1.6

020

0,00

0$1

16,8

00,0

00

$1.7

020

0,00

0$1

24,1

00,0

00

$1.8

020

0,00

0$1

31,4

00,0

00

$1.9

020

0,00

0$1

38,7

00,0

00

$2.0

020

0,00

0$1

46,0

00,0

00

Cos

t Ass

umpt

ions

(50,

000

Dth

)

Rat

e($

/Dth

)C

apac

ity (D

th)

Annu

al C

ost

($)

$1.0

050

,000

$18,

250,

000

$1.1

050

,000

$20,

075,

000

$1.2

050

,000

$21,

900,

000

$1.3

050

,000

$23,

725,

000

$1.4

050

,000

$25,

550,

000

$1.5

050

,000

$27,

375,

000

$1.6

050

,000

$29,

200,

000

$1.7

050

,000

$31,

025,

000

$1.8

050

,000

$32,

850,

000

$1.9

050

,000

$34,

675,

000

$2.0

050

,000

$36,

500,

000

10

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 11 of 65

000346

Con

tent

s

1.In

trodu

ctio

n

2.E

xecu

tive

Sum

mar

y

3.N

atur

al G

as M

arke

t Ove

rvie

w

Mar

ket C

onte

xt

Reg

iona

l Nat

ural

Gas

Dem

and

Driv

ers

N

atur

al G

as S

uppl

y D

river

s

Nat

ural

Gas

Pric

e an

d B

asis

Ana

lysi

s

4.N

atur

al G

as P

ipel

ine

Cap

acity

Opt

ions

5.C

ost /

Ben

efit

Ana

lysi

s

6.S

umm

ary

and

Con

clus

ions

11

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 12 of 65

000347

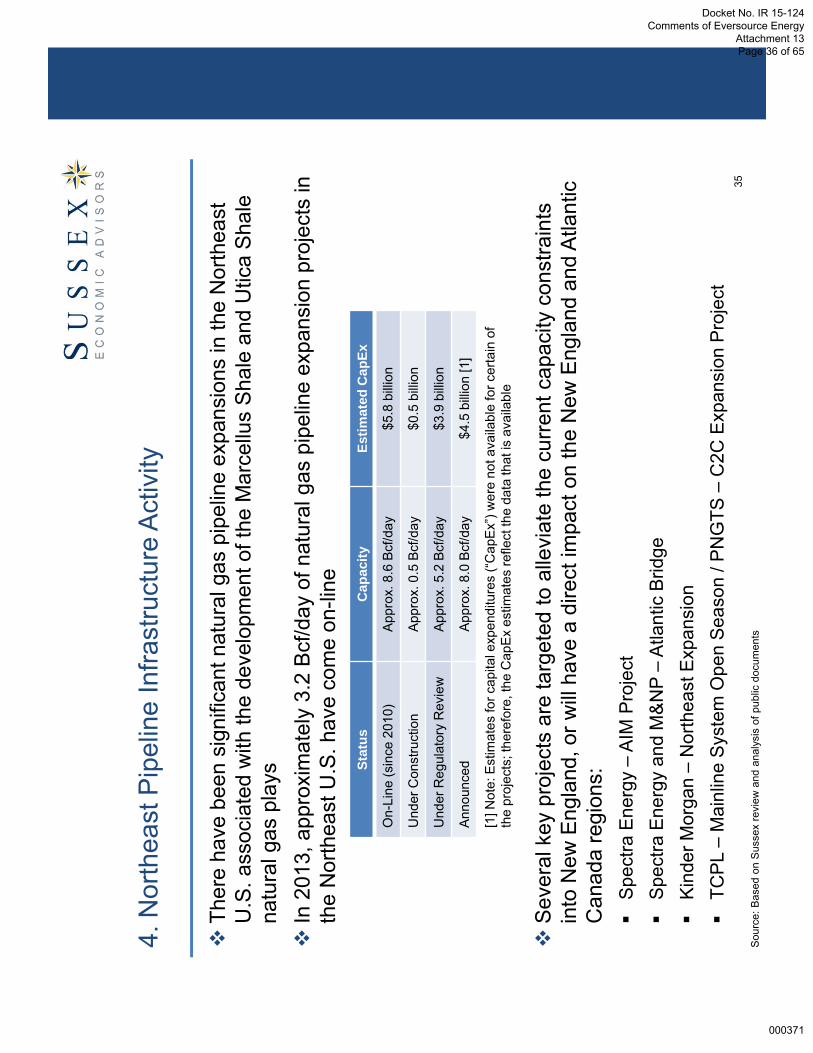

3. M

arke

t Con

text

: Nat

ural

Gas

Infra

stru

ctur

e –

New

Eng

land

Fi

ve in

ters

tate

nat

ural

gas

pip

elin

es s

erve

the

New

Eng

land

regi

on:

Sou

rces

: Com

pany

web

site

s; a

nd S

NL

Fina

ncia

l

Pipe

line

Ow

ner(

s)Pr

imar

y Su

pply

Sour

ces

Alg

onqu

in G

as T

rans

mis

sion

,LLC

(“

Alg

onqu

in” o

r “A

GT”

)S

pect

raEn

ergy

Par

tner

s, L

PG

ulfo

f Mex

ico,

App

alac

hian

B

asin

, Roc

kies

Bas

in, L

NG

Iroqu

ois

Gas

Tra

nsm

issi

on,L

.P.

(“Iro

quoi

s”)

Iroqu

ois

Gas

Tra

nsm

issi

on, L

.P.

Wes

tern

Can

adia

n S

edim

enta

ry

Bas

in (“

WC

SB

”)/ D

awn

Hub

Mar

itim

es&

Nor

thea

st P

ipel

ine

(“M

&N

P”)

(U.S

.)S

pect

ra E

nerg

y P

artn

ers,

LP

(77.

53%

); E

mer

a, In

c. (1

2.92

%);

Exx

onM

obil

Cor

p. (9

.55%

)

SO

EP

/ Dee

p P

anuk

e / L

NG

Por

tland

Nat

ural

Gas

Tra

nsm

issi

on

Sys

tem

(“P

NG

TS”)

Tran

sCan

ada

Pip

elin

es L

imite

d (6

1.71

%);

Gaz

Met

ro(3

8.29

%)

WC

SB

/ D

awn

Hub

Tenn

esse

eG

as P

ipel

ine

Com

pany

, L.

L.C

. (“T

enne

ssee

” or “

TGP

”)K

inde

r Mor

gan

Ene

rgy

Par

tner

s,

L.P.

Gul

f ofM

exic

o, A

ppal

achi

anB

asin

, Roc

kies

Bas

in, L

NG

12

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 13 of 65

000348

3. M

arke

t Con

text

: Nat

ural

Gas

Infra

stru

ctur

e –

New

Eng

land

(con

t.)

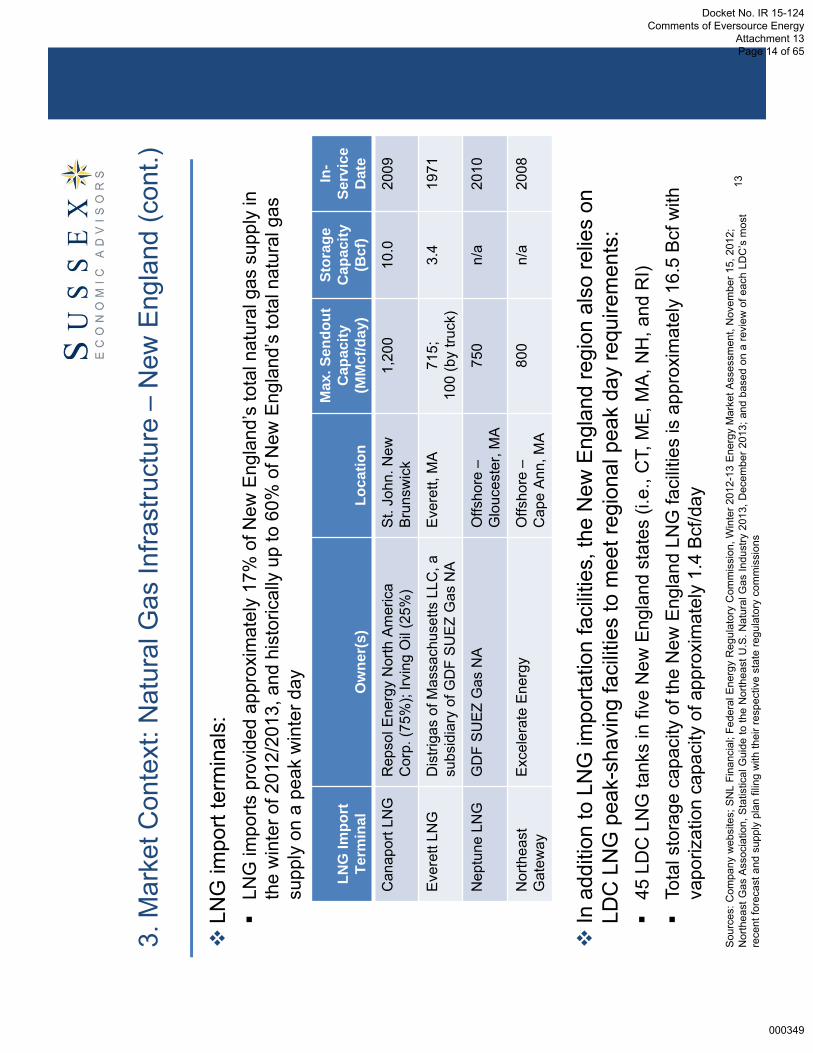

LN

G im

port

term

inal

s:

LNG

impo

rts p

rovi

ded

appr

oxim

atel

y 17

% o

f New

Eng

land

’s to

tal n

atur

al g

as s

uppl

y in

th

e w

inte

r of 2

012/

2013

, and

his

toric

ally

up

to 6

0% o

f New

Eng

land

’s to

tal n

atur

al g

as

supp

ly o

n a

peak

win

ter d

ay

In

add

ition

to L

NG

impo

rtatio

n fa

cilit

ies,

the

New

Eng

land

regi

on a

lso

relie

s on

LD

C L

NG

pea

k-sh

avin

g fa

cilit

ies

to m

eet r

egio

nal p

eak

day

requ

irem

ents

:

45 L

DC

LN

G ta

nks

in fi

ve N

ew E

ngla

nd s

tate

s (i.

e., C

T, M

E, M

A, N

H, a

nd R

I)

Tota

l sto

rage

cap

acity

of t

he N

ew E

ngla

nd L

NG

faci

litie

s is

app

roxi

mat

ely

16.5

Bcf

with

va

poriz

atio

n ca

paci

ty o

f app

roxi

mat

ely

1.4

Bcf

/day

Sou

rces

: Com

pany

web

site

s; S

NL

Fina

ncia

l; Fe

dera

l Ene

rgy

Reg

ulat

ory

Com

mis

sion

, Win

ter 2

012-

13 E

nerg

y M

arke

t Ass

essm

ent,

Nov

embe

r 15,

201

2;

Nor

thea

st G

as A

ssoc

iatio

n, S

tatis

tical

Gui

de to

the

Nor

thea

st U

.S. N

atur

al G

as In

dust

ry 2

013,

Dec

embe

r 201

3; a

nd b

ased

on

a re

view

of e

ach

LDC

’s m

ost

rece

nt fo

reca

st a

nd s

uppl

y pl

an fi

ling

with

thei

r res

pect

ive

stat

e re

gula

tory

com

mis

sion

s

LNG

Impo

rt

Term

inal

Ow

ner(

s)Lo

catio

n

Max

. Sen

dout

Cap

acity

(M

Mcf

/day

)

Stor

age

Cap

acity

(B

cf)

In-

Serv

ice

Dat

e

Can

apor

t LN

GR

epso

l Ene

rgy

Nor

thA

mer

ica

Cor

p. (7

5%);

Irvin

g O

il (2

5%)

St.

John

.New

B

runs

wic

k1,

200

10.0

2009

Eve

rett

LNG

Dis

triga

s of

Mas

sach

uset

tsLL

C, a

su

bsid

iary

of G

DF

SU

EZ

Gas

NA

Eve

rett,

MA

715;

10

0 (b

y tru

ck)

3.4

1971

Nep

tune

LN

GG

DF

SU

EZ

Gas

NA

Offs

hore

–G

louc

este

r, M

A75

0n/

a20

10

Nor

thea

stG

atew

ayE

xcel

erat

e E

nerg

yO

ffsho

re –

Cap

e A

nn, M

A80

0n/

a20

08

13

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 14 of 65

000349

3. M

arke

t Con

text

: Nat

ural

Gas

Infra

stru

ctur

e –

New

Eng

land

(con

t.)

Sou

rce:

SN

L Fi

nanc

ial

14

Th

ere

are

five

maj

or in

ters

tate

pip

elin

es a

nd fo

ur L

NG

impo

rt te

rmin

als

that

de

liver

nat

ural

gas

to N

ew E

ngla

nd

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 15 of 65

000350

3. M

arke

t Con

text

: Nat

ural

Gas

Infra

stru

ctur

e –

Mai

ne

Th

e M

aine

nat

ural

gas

mar

ket i

s pr

imar

ily s

erve

d by

M&

NP

and

PN

GTS

; in

addi

tion,

ther

e ar

e fo

ur L

DC

s th

at p

rovi

de d

istri

butio

n se

rvic

e

15S

ourc

e: S

NL

Fina

ncia

l

Not

es:

[1] T

he m

ap a

bove

sho

ws

the

serv

ice

terr

itorie

s fo

r the

Mai

ne L

DC

s pr

ior t

o th

e na

tura

l gas

pip

elin

e ex

pans

ions

to th

e ci

ty o

f A

ugus

ta, M

aine

by

Mai

ne N

atur

al G

as a

nd S

umm

it N

atur

al G

as in

late

201

3[2

] Mad

ison

Pap

er is

cur

rent

ly s

erve

d by

LN

G, a

nd is

exp

ecte

d to

be

serv

ed b

y S

umm

it N

atur

al G

as in

201

4

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 16 of 65

000351

O

ver t

he p

ast f

ive

split

-yea

rs (i

.e.,

2008

/200

9 to

201

2/20

13):

To

tal a

nnua

l dem

and

for n

atur

al g

as in

crea

sed

by

a co

mpo

und

annu

al g

row

th ra

te (“

CA

GR

”) o

f 2.3

%

from

731

.7 B

cf (i

.e.,

2,00

5 M

Mcf

/day

) to

801.

1 B

cf

(i.e.

, 2,1

95 M

Mcf

/day

)

W

inte

r nat

ural

gas

dem

and

incr

ease

d by

a C

AG

R

of 1

.0%

from

400

.0 B

cf (i

.e.,

2,64

9 M

Mcf

/day

) to

416.

0 B

cf (i

.e.,

2,75

5 M

Mcf

/day

)

S

umm

er n

atur

al g

as d

eman

d in

crea

sed

by a

C

AG

R o

f 3.8

% fr

om 3

31.7

Bcf

(i.e

., 1,

550

MM

cf/d

ay) t

o 38

5.1

Bcf

(i.e

., 1,

800

MM

cf/d

ay)

In

201

2/20

13, t

he p

ower

gen

erat

ion

segm

ent

acco

unte

d fo

r app

roxi

mat

ely

43%

of t

otal

na

tura

l gas

dem

and,

follo

wed

by

the

resi

dent

ial,

com

mer

cial

and

indu

stria

l se

gmen

ts w

ith 2

6%, 1

9% a

nd 1

2%,

resp

ectiv

ely

3. M

arke

t Con

text

: His

toric

al D

eman

d –

New

Eng

land

(exc

ludi

ng

Mai

ne)

Not

e: D

ata

for 2

013

for c

erta

in s

tate

s ba

sed

on S

usse

x es

timat

es (S

ourc

e: U

.S. E

nerg

y In

form

atio

n A

dmin

istra

tion,

Nat

ural

Gas

Con

sum

ptio

n by

End

Use

, re

leas

e da

te J

anua

ry 7

, 201

4)

0.0

20.0

40.0

60.0

80.0

100.

0

120.

0

Nov-2008

Feb-2009

May-2009

Aug-2009

Nov-2009

Feb-2010

May-2010

Aug-2010

Nov-2010

Feb-2011

May-2011

Aug-2011

Nov-2011

Feb-2012

May-2012

Aug-2012

Nov-2012

Feb-2013

May-2013

Aug-2013

Consumption (Bcf)

Res

iden

tial

Com

mer

cial

Indu

stria

lPo

wer

Gen

erat

ion

Res

iden

tial

205.

8 Bc

f26

%

Com

mer

cial

152.

2 Bc

f19

%In

dust

rial

93.6

Bcf

12%

Pow

er

Gen

erat

ion

349.

5 B

cf43

%

Tota

l 201

2/20

13 N

atur

al G

as D

eman

d =

801.

1 B

cf

16

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 17 of 65

000352

O

ver t

he p

ast f

ive

split

-yea

rs (i

.e.,

2008

/200

9 to

201

2/20

13):

To

tal a

nnua

l dem

and

for n

atur

al g

as d

ecre

ased

by

a C

AG

R o

f 3.4

% fr

om 6

9.2

Bcf

(i.e

., 19

0 M

Mcf

/day

) to

60.3

Bcf

(i.e

., 16

5 M

Mcf

/day

)

W

inte

r nat

ural

gas

dem

and

decr

ease

d by

a C

AG

R

of a

ppro

xim

atel

y 2.

0% fr

om 3

0.9

Bcf

(i.e

., 20

5 M

Mcf

/day

) to

28.6

Bcf

(i.e

., 18

9 M

Mcf

/day

)

S

umm

er n

atur

al g

as d

eman

d de

crea

sed

by a

C

AG

R o

f 4.6

% fr

om 3

8.3

Bcf

(i.e

., 17

9 M

Mcf

/day

) to

31.

7 B

cf (

i.e.,

148

MM

cf/d

ay)

W

hile

the

resi

dent

ial,

com

mer

cial

and

indu

stria

l se

gmen

ts a

ll ha

ve e

xper

ienc

ed in

crea

ses

in

cons

umpt

ion,

the

dem

and

for n

atur

al g

as b

y th

e po

wer

gen

erat

ion

segm

ent h

as d

eclin

ed fr

om 3

6.9

Bcf

(i.e

., 10

1 M

Mcf

/day

) to

20.0

Bcf

(i.e

., 55

M

Mcf

/day

), lik

ely

driv

en b

y hi

gher

gas

sup

ply

cost

s

In

201

2/20

13, t

he p

ower

gen

erat

ion

segm

ent

acco

unte

d fo

r app

roxi

mat

ely

33%

of M

aine

’s

tota

l nat

ural

gas

dem

and,

whi

le th

e in

dust

rial

segm

ent a

ccou

nted

for 5

2% o

f the

tota

l de

man

d

3. M

arke

t Con

text

: His

toric

al D

eman

d –

Mai

ne

Res

iden

tial

1.5

Bcf

3%

Com

mer

cial

7.4

Bcf

12%

Indu

stria

l31

.5 B

cf52

%

Pow

er

Gen

erat

ion

20.0

Bcf

33%

Tota

l 201

2/20

13 N

atur

al G

as D

eman

d =

60.3

Bcf

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Nov-2008

Feb-2009

May-2009

Aug-2009

Nov-2009

Feb-2010

May-2010

Aug-2010

Nov-2010

Feb-2011

May-2011

Aug-2011

Nov-2011

Feb-2012

May-2012

Aug-2012

Nov-2012

Feb-2013

May-2013

Aug-2013

Consumption (Bcf)

Res

iden

tial

Com

mer

cial

Indu

stria

lPo

wer

Gen

erat

ion

Not

e: D

ata

for J

anua

ry-A

pril

2013

for t

he re

side

ntia

l and

com

mer

cial

seg

men

ts b

ased

on

Sus

sex

estim

ates

(Sou

rce:

U.S

. Ene

rgy

Info

rmat

ion

Adm

inis

tratio

n,

Nat

ural

Gas

Con

sum

ptio

n by

End

Use

, rel

ease

dat

e Ja

nuar

y 7,

201

4)17

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 18 of 65

000353

3. N

atur

al G

as D

eman

d D

river

s: M

aine

Th

e fo

ur M

aine

LD

Cs

have

sig

nific

ant n

atur

al g

as in

frast

ruct

ure

deve

lopm

ent

and

expa

nsio

n pl

ans:

U

nitil

, whi

ch s

erve

s na

tura

l gas

cus

tom

ers

in M

aine

, New

Ham

pshi

re a

nd

Mas

sach

uset

ts, h

as p

lans

to in

crea

se it

s nu

mbe

r of c

usto

mer

s fro

m 7

4,00

0 to

92,

000

(i.e.

, an

appr

oxim

atel

y 25

% in

crea

se in

cus

tom

er b

ase)

by

2016

thro

ugh

addi

tions

and

co

nver

sion

s

Sum

mit

Nat

ural

Gas

(“S

umm

it”) i

s cu

rren

tly u

nder

taki

ng m

ultip

le p

roje

cts

to p

rovi

de

natu

ral g

as s

ervi

ce to

new

are

as w

ithin

Mai

ne•

The

$350

milli

on K

enne

bec

Valle

y P

roje

ct, w

hich

con

sist

s of

an

88-m

ile tr

ansm

issi

on p

ipel

ine

to

supp

ly n

atur

al g

as to

two

pape

r mills

, alo

ng w

ith 1

,600

mile

s of

dis

tribu

tion

pipe

line

to e

xpan

d S

umm

it’s

serv

ice

terr

itory

into

sev

ente

en c

omm

uniti

es in

the

Ken

nebe

c Va

lley

regi

on

•S

umm

it al

so re

ceiv

ed a

ppro

val f

or a

$42

milli

on p

roje

ct, w

hich

con

sist

s of

32

mile

s of

tran

smis

sion

lin

es a

nd 2

13 m

iles

of d

istri

butio

n lin

es, t

o pr

ovid

e na

tura

l gas

dis

tribu

tion

serv

ice

to th

e to

wns

of

Cum

berla

nd, F

alm

outh

and

Yar

mou

th

Th

e ne

w $

23 m

illio

n na

tura

l gas

pip

elin

e bu

ilt b

y M

aine

Nat

ural

Gas

from

an

inte

rcon

nect

w

ith M

&N

P in

Win

dsor

, Mai

ne to

Aug

usta

, Mai

ne c

omm

ence

d se

rvic

e in

Nov

embe

r 201

3

In la

te O

ctob

er 2

013,

Ban

gor N

atur

al G

as a

nnou

nced

pla

ns to

con

stru

ct a

five

-pha

se,

$7.5

mill

ion

natu

ral g

as p

ipel

ine

to L

inco

ln, M

aine

Sou

rces

: Uni

til, P

rese

ntat

ion

for S

econ

d Q

uarte

r 201

3 E

arni

ngs

Con

fere

nce

Cal

l, Ju

ly 2

4, 2

013;

Sum

mit

Nat

ural

Gas

, “G

as is

Tur

ned

On,

Sum

mit

Now

S

ervi

ng C

usto

mer

s”, J

anua

ry 6

, 201

4; B

ango

r Dai

ly N

ews,

“Fal

mou

th re

leas

es m

ap d

etai

ling

natu

ral g

as li

ne e

xpan

sion

”, D

ecem

ber 2

3, 2

013;

SN

L Fi

nanc

ial,

“Mai

ne N

atur

al G

as c

ompl

etes

1st

gas

pip

elin

e to

Aug

usta

, Mai

ne”,

Oct

ober

28,

201

3; a

nd S

NL

Fina

ncia

l, “R

epor

t: B

ango

r Nat

ural

pro

pose

s $7

.5M

pip

elin

e in

Mai

ne”,

Oct

ober

23,

201

318

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 19 of 65

000354

3. N

atur

al G

as D

eman

d D

river

s: C

onne

ctic

ut

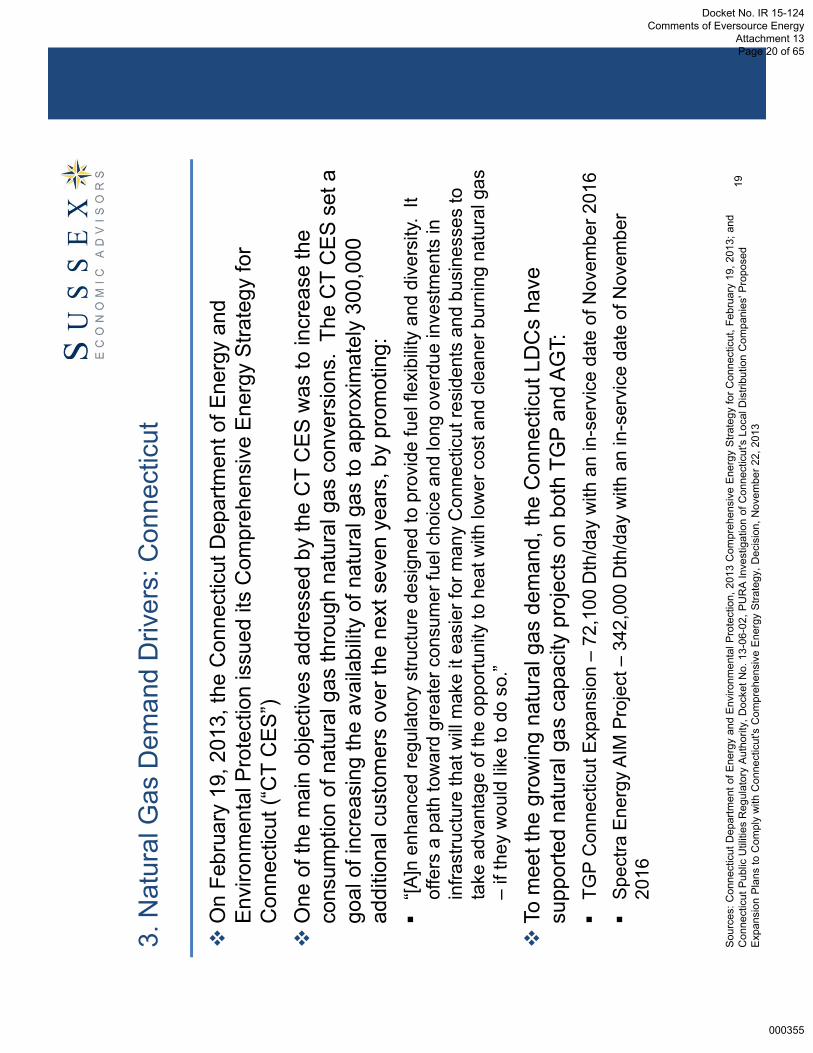

O

n Fe

brua

ry 1

9, 2

013,

the

Con

nect

icut

Dep

artm

ent o

f Ene

rgy

and

Env

ironm

enta

l Pro

tect

ion

issu

ed it

s C

ompr

ehen

sive

Ene

rgy

Stra

tegy

for

Con

nect

icut

(“C

T C

ES

”)

One

of t

he m

ain

obje

ctiv

es a

ddre

ssed

by

the

CT

CE

S w

as to

incr

ease

the

cons

umpt

ion

of n

atur

al g

as th

roug

h na

tura

l gas

con

vers

ions

. Th

e C

T C

ES

set

a

goal

of i

ncre

asin

g th

e av

aila

bilit

y of

nat

ural

gas

to a

ppro

xim

atel

y 30

0,00

0 ad

ditio

nal c

usto

mer

s ov

er th

e ne

xt s

even

yea

rs, b

y pr

omot

ing:

“[A

]n e

nhan

ced

regu

lato

ry s

truct

ure

desi

gned

to p

rovi

de fu

el fl

exib

ility

and

div

ersi

ty.

It of

fers

a p

ath

tow

ard

grea

ter c

onsu

mer

fuel

cho

ice

and

long

ove

rdue

inve

stm

ents

in

infra

stru

ctur

e th

at w

ill m

ake

it ea

sier

for m

any

Con

nect

icut

resi

dent

s an

d bu

sine

sses

to

take

adv

anta

ge o

f the

opp

ortu

nity

to h

eat w

ith lo

wer

cos

t and

cle

aner

bur

ning

nat

ural

gas

–

if th

ey w

ould

like

to d

o so

.”

To

mee

t the

gro

win

g na

tura

l gas

dem

and,

the

Con

nect

icut

LD

Cs

have

su

ppor

ted

natu

ral g

as c

apac

ity p

roje

cts

on b

oth

TGP

and

AG

T:

TGP

Con

nect

icut

Exp

ansi

on –

72,1

00 D

th/d

ay w

ith a

n in

-ser

vice

dat

e of

Nov

embe

r 201

6

Spe

ctra

Ene

rgy

AIM

Pro

ject

–34

2,00

0 D

th/d

ay w

ith a

n in

-ser

vice

dat

e of

Nov

embe

r 20

16

Sou

rces

: Con

nect

icut

Dep

artm

ent o

f Ene

rgy

and

Env

ironm

enta

l Pro

tect

ion,

201

3 C

ompr

ehen

sive

Ene

rgy

Stra

tegy

for C

onne

ctic

ut, F

ebru

ary

19, 2

013;

and

C

onne

ctic

ut P

ublic

Util

ities

Reg

ulat

ory

Aut

horit

y, D

ocke

t No.

13-

06-0

2, P

UR

A In

vest

igat

ion

of C

onne

ctic

ut's

Loc

al D

istri

butio

n C

ompa

nies

' Pro

pose

d E

xpan

sion

Pla

ns to

Com

ply

with

Con

nect

icut

's C

ompr

ehen

sive

Ene

rgy

Stra

tegy

, Dec

isio

n, N

ovem

ber 2

2, 2

013

19

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 20 of 65

000355

3. N

atur

al G

as D

eman

d D

river

s: M

assa

chus

etts

Th

e M

assa

chus

etts

DO

ER

has

spo

nsor

ed a

stu

dy to

ana

lyze

the

net e

cono

mic

an

d en

viro

nmen

tal b

enef

its o

f exp

andi

ng n

atur

al g

as d

istri

butio

n se

rvic

e to

mor

e M

assa

chus

etts

hou

seho

lds

and

busi

ness

es (“

the

Nat

ural

Gas

Stu

dy”)

Th

e pu

rpos

e of

the

Nat

ural

Gas

Stu

dy is

to d

evel

op a

n an

alyt

ical

fram

ewor

k,

findi

ngs,

and

reco

mm

enda

tions

rega

rdin

g na

tura

l gas

dis

tribu

tion

expa

nsio

n in

lig

ht o

f cha

ngin

g m

arke

t con

ditio

ns a

nd e

nviro

nmen

tal i

ssue

s

The

DO

ER

ant

icip

ates

that

the

outc

ome

of th

e N

atur

al G

as S

tudy

, alo

ng w

ith it

s re

new

able

ther

mal

exp

ansi

on s

tudy

, cou

ld re

sult

in n

ew a

ppro

ache

s w

ith

resp

ect t

o th

erm

al p

olic

ies

in M

assa

chus

etts

Th

e N

atur

al G

as S

tudy

will

eval

uate

the

bene

fits,

cos

ts, a

nd c

halle

nges

as

soci

ated

with

nat

ural

gas

LD

C e

xpan

sion

und

er a

rang

e of

pot

entia

l stra

tegy

op

tions

20

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 21 of 65

000356

3. N

atur

al G

as D

eman

d D

river

s: N

ew Y

ork

City

G

as c

onve

rsio

n re

ques

ts h

ave

incr

ease

d be

twee

n 20

10 a

nd 2

013

P

laN

YC

cal

ls fo

r the

elim

inat

ion

of th

e us

e of

No.

4 a

nd 6

hea

ting

oil

N

o pe

rmits

for n

ew N

o. 4

or 6

boi

lers

(unl

ess

emis

sion

s as

cle

an a

s N

o. 2

oil)

N

o ce

rtific

ate

of o

pera

tion

will

be

rene

wed

for

No.

6 b

oile

r as

of J

uly

2012

(unl

ess

emis

sion

s as

cle

an a

s N

o. 4

oil)

A

ll bo

ilers

mus

t use

No.

2 o

il, n

atur

al g

as o

r eq

uiva

lent

upo

n re

tirem

ent o

r by

2030

C

on E

diso

n is

fore

cast

ing

peak

usa

ge o

ver

the

next

five

yea

rs to

incr

ease

C

EC

ON

Y G

as: 3

.8%

ann

ually

O

&R

Gas

: 0.7

% a

nnua

lly

Pote

ntia

l Con

vers

ions

by

Fuel

Typ

eM

ulti-

Fam

ily a

nd C

omm

erci

al B

uild

ings

Year

Num

ber o

f Con

vers

ions

2010

73

2011

310

2012

855

Thro

ugh

Sep.

201

387

0

Num

ber o

f Con

vers

ions

–C

ECO

NY

Gas

Mul

ti-Fa

mily

and

Com

mer

cial

Bui

ldin

gs

Sou

rce:

Con

Edi

son,

Inve

stor

Pre

sent

atio

n at

the

Edi

son

Ele

ctric

Inst

itute

Fin

ance

Con

fere

nce,

Nov

embe

r 10-

12, 2

013

No.

2 O

il,

70%

No.

4 O

il,

12%

No.

6 O

il,

18%

21

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 22 of 65

000357

3. N

atur

al G

as D

eman

d D

river

s: M

ariti

mes

Can

ada

A

ccor

ding

to a

rece

nt N

ova

Sco

tia D

epar

tmen

t of E

nerg

y (“N

S D

OE

”) S

tudy

:

Nat

ural

Gas

Dem

and:

•M

ariti

mes

Can

ada

natu

ral g

as c

onsu

mpt

ion

will

incr

ease

from

app

roxi

mat

ely

62 B

cf in

201

2 (i.

e.,

170

MM

cf/d

ay) t

o ap

prox

imat

ely

70 B

cf b

y 20

20 (i

.e.,

192

MM

cf/d

ay),

larg

ely

driv

en b

y th

e po

wer

ge

nera

tion

segm

ent

•G

as-fi

red

gene

ratio

n in

Nov

a S

cotia

has

incr

ease

d fro

m 3

% o

f tot

al g

ener

atio

n in

200

6 to

ove

r 20%

in

201

2

N

atur

al G

as S

uppl

y:•

Mar

itim

es C

anad

a na

tura

l gas

sup

ply

is e

xpec

ted

to s

hift

from

a re

lianc

e on

offs

hore

nat

ural

gas

re

sour

ces

(i.e.

, SO

EP,

Dee

p P

anuk

e) to

ext

erna

l sou

rces

of n

atur

al g

as s

uppl

y (e

.g.,

LNG

, or

impo

rts fr

om th

e U

.S.)

•O

ne o

f the

focu

s ar

eas

of th

e N

S D

OE

Stu

dy w

as u

pstre

am c

apac

ity c

ontra

ctin

g, s

peci

fical

ly:

“[g]iv

en th

e ne

ed fo

r ext

erna

l sup

ply,

ICF

belie

ves

ther

e is

a s

trong

arg

umen

t for

Mar

itim

es C

anad

a co

nsum

ers

to c

ontra

ct fo

r firm

pip

elin

e ca

paci

ty o

n on

e of

the

prop

osed

pip

elin

e ex

pans

ions

into

N

ew E

ngla

nd th

at w

ould

allo

w s

hipp

ers

to b

uy g

as a

t one

of t

he M

arce

llus

basi

n hu

bs to

an

inte

rcon

nect

ion

with

M&

NP.

Thi

s w

ould

ens

ure

a re

liabl

e so

urce

of g

as a

s w

ell a

s av

oid

the

pric

e vo

latil

ity in

New

Eng

land

.”

Sou

rce:

Nov

a S

cotia

Dep

artm

ent o

f Ene

rgy,

The

Fut

ure

of N

atur

al G

as S

uppl

y fo

r Nov

a S

cotia

, pre

pare

d by

ICF

Con

sulti

ng C

anad

a, In

c., M

arch

28, 2

013

22

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 23 of 65

000358

3. N

atur

al G

as D

eman

d D

river

s: P

ower

Gen

erat

ion

Th

ere

are

appr

oxim

atel

y 35

0 ge

nera

ting

units

in th

e IS

O N

ew E

ngla

nd re

gion

–a

tota

l of

over

32,

000

MW

of g

ener

atin

g ca

paci

ty –

with

nat

ural

gas

-fire

d ge

nera

tors

repr

esen

ting

appr

oxim

atel

y 43

% o

f tot

al g

ener

atin

g ca

paci

ty a

nd 5

2% o

f tot

al e

lect

ric e

nerg

y pr

oduc

tion

in 2

012

S

ever

al k

ey g

ener

atin

g fa

cilit

ies,

whi

ch re

pres

ent n

early

10%

of t

he re

gion

’s to

tal c

apac

ity,

have

ann

ounc

ed p

lans

to re

tire

over

the

next

thre

e ye

ars:

S

alem

Har

bor (

750

MW

) –sc

hedu

led

to b

e re

tired

by

June

201

4; e

xpec

ted

to b

e re

plac

ed b

y a

new

ap

prox

imat

ely

700

MW

com

bine

d cy

cle

gas

turb

ine

faci

lity

Ve

rmon

t Yan

kee

(604

MW

) –ex

pect

ed to

be

deco

mm

issi

oned

in la

te 2

014;

sin

ce 2

007,

has

gen

erat

ed

appr

oxim

atel

y 4%

of t

he to

tal a

nnua

l ele

ctric

ity s

uppl

y in

New

Eng

land

B

rayt

on P

oint

(1,4

92 M

W) –

thre

e co

al-fi

red

units

and

sev

eral

oil-

fired

uni

ts s

ched

uled

to re

tire

by 2

017

N

orw

alk

Har

bor (

340

MW

) –oi

l-fire

d ge

nera

ting

faci

lity

sche

dule

d to

be

retir

ed b

y Ju

ne 2

017

A

s of

Jan

uary

1, 2

014,

ther

e ar

e 70

gen

erat

ion

proj

ects

in v

ario

us s

tage

s of

dev

elop

men

t in

the

ISO

New

Eng

land

regi

on to

talin

g 4,

980

MW

S

even

of t

he 7

0 pr

ojec

ts a

re d

ual f

uel (

i.e.,

natu

ral g

as a

nd o

il-fir

ed) g

ener

atio

n pr

ojec

ts lo

cate

d in

M

assa

chus

etts

and

Con

nect

icut

, for

a to

tal o

f 2,2

30 M

W, w

ith in

-ser

vice

dat

es b

etw

een

2014

and

201

7;

and

two

proj

ects

are

nat

ural

gas

com

bine

d-cy

cle

gene

ratio

n pr

ojec

ts, f

or a

tota

l of 5

03 M

W, w

ith in

-se

rvic

e da

tes

in 2

014

and

2017

S

tate

d di

ffere

ntly,

of t

he 4

,980

MW

of g

ener

atio

n be

ing

deve

lope

d, o

ver h

alf (

i.e.,

2,73

3 M

W) w

ill be

fu

eled

by

natu

ral g

asS

ourc

es: I

SO

New

Eng

land

, New

Eng

land

201

2-13

Reg

iona

l Pro

file

and

Mai

ne 2

012-

13 S

tate

Pro

file,

Feb

ruar

y 20

13; I

SO

New

Eng

land

, Sea

sona

l Cla

imed

C

apac

ity M

onth

ly R

epor

t, O

ctob

er 1

, 201

3; IS

O N

ew E

ngla

nd, S

tatu

s of

Non

-Pric

e R

etire

men

t Req

uest

s, D

ecem

ber 2

0, 2

013;

and

ISO

New

Eng

land

, In

terc

onne

ct R

eque

st Q

ueue

, Jan

uary

1, 2

014

23

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 13 Page 24 of 65

000359

3. N

atur

al G

as S

uppl

y D

river

s: A

tlant

ic C

anad

a

Sou

rces

: Can

ada-

Nov

a S

cotia

Offs

hore

Pet

role

um B

oard

, Sab

le M

onth

ly P

rodu

ctio

n R

epor

ts, a

s of

Jan

uary

21,

201

4; N

ova

Sco

tia D

epar

tmen

t of E

nerg

y,

The

Futu

re o

f Nat

ural

Gas

Sup

ply

for N

ova

Sco

tia, p

repa

red

by IC

F C

onsu

lting

Can

ada,

Inc.

, Mar

ch 2

8, 2

013;

and

The

Chr

onic

le H

eral

d, “D

eep

Pan

uke

back

in

full

swin

g”, D

ecem

ber 1

1, 2

013

S

able

Offs

hore

Ene

rgy

Pro

ject

:

Nat

ural

gas

pro

duct

ion

from

SO

EP

decl

ined

from

a p

eak

of n

early

600

MM

cf/d

ay in

Dec

embe

r 20

01 to

240

MM

cf/d

ay in

Aug

ust 2

012;

sin

ce S

epte

mbe

r 201

2, a

vera

ge d

aily

SO

EP

prod

uctio

n ha

s de

clin

ed to

app

roxi

mat

ely