mawarid finance...

TRANSCRIPT

Mawarid Finance P.J.S.C.

for the year ended 31 December 2014Consolidated Financial Statements

Mawarid Finance P.J.S.C.Consolidated Financial Statementsfor the year ended 31 December 2014

Page

Directors' report 1-2

Independent auditors' report 3-4

Consolidated statement of financial position 5

Consolidated statement of profit or loss 6

Consolidated statement of profit or loss and other comprehensive income 7

Consolidated statement of changes in equity 8

Consolidated statement of cash flows 9

Notes to the consolidated financial statements 10-48

Mawarid Finance P.J.S.C.Consolidated statement of profit or loss for the year ended 31 December 2014

31 December 31 December 2014 2013

Note AED ’000 AED ’000

Income from financing and investing assets 27 26,975 27,384 Income from Islamic deposits and wakalah placements 28 3,776 2,602 Revenue from IT and security system services 29 95,946 59,228 Unrealised gain on revaluation of investment properties 14 22,411 6,098 Realised gain on sale of investment property 14 - 11,627 Gain/(loss) on investment carried at FVTPL (1,888) 6,241 Other income 30 11,855 13,117

Total revenue from operating activities 159,075 126,297

General and administrative expenses 31 (69,834) (57,519) Cost of sales relating to IT and security system services 29 (50,688) (35,410)

Total expenses from operating activities (120,522) (92,929)

Depositors’ share of profit (392) (814) Provision for impairment 12,838 -

Profit before associate's share of profit for the year 50,999 32,554

Share of profit from equity accounted investees 16 19,595 28,636

Profit for the year 70,594 61,190

Attributable to:Equity holders of the Parent 58,015 56,781 Non-controlling interest 12,579 4,409

70,594 61,190

The notes on pages 10 to 48 are an integral part of these consolidated financial statements.

The independent auditors' report on consolidated financial statements is set out on page 3-4.

6

Mawarid Finance P.J.S.C.Consolidated statement of profit or loss and other comprehensive incomefor the year ended 31 December 2014

31 December 31 December 2014 2013

AED ’000 AED ’000

Profit for the year 70,594 61,190

Other comprehensive income:

Items that will never be reclassified to profit or loss - -

Items that are or may be reclassified to profit or loss:Changes in fair value of available for sale investments 22,694 (4,715)

Total comprehensive income for the year 93,288 56,475

Total comprehensive income attributable to:

Equity holders of the Parent 80,778 52,066 Non-controlling interest 12,510 4,409

Total comprehensive income for the year 93,288 56,475

The notes on pages 10 to 48 are an integral part of these consolidated financial statements.

The independent auditors' report on consolidated financial statements is set out on page 3-4.

7

Mawarid Finance P.J.S.C.Consolidated statement of changes in equity for the year ended 31 December 2014

Investment Non-Share Treasury Statutory General revaluation Retained controlling

capital shares reserve reserve reserve earnings Total interest Total

AED ’000 AED ’000 AED ’000 AED ’000 AED ’000 AED ’000 AED ’000 AED ’000 AED ’000

Balance at 1 January 2014 1,000,000 (6,000) 20,870 20,870 (29,187) 19,514 1,026,067 26,283 1,052,350

Profit for the year - - - - - 58,015 58,015 12,579 70,594 Other comprehensive income:

- - - - 22,763 - 22,763 (69) 22,694

- - - - 22,763 58,015 80,778 12,510 93,288

- - 5,802 5,802 - (11,604) - - -

- - - - - - - 6,802 6,802

Transactions with owners of the Group

Dividend declared (note 32) - - - - - (49,700) (49,700) - (49,700)

Balance at 31 December 2014 1,000,000 (6,000) 26,672 26,672 (6,424) 16,225 1,057,145 45,595 1,102,740

Balance at 1 January 2013 1,000,000 (6,000) 15,481 14,903 (24,472) (22,655) 977,257 11,136 988,393

Profit for the year - - - - - 56,781 56,781 4,409 61,190 Other comprehensive income:

- - - - (4,715) - (4,715) - (4,715)

- - - - (4,715) 56,781 52,066 4,409 56,475

- - 5,389 5,967 - (11,356) - - -

- - - - - - - 10,738 10,738

- - - - - (3,256) (3,256) - (3,256)

Balance at 31 December 2013 1,000,000 (6,000) 20,870 20,870 (29,187) 19,514 1,026,067 26,283 1,052,350

. The notes on pages 10 to 48 are an integral part of these consolidated financial statements.

The independent auditors' report on consolidated financial statements is set out on page 3-4.

Movement upon further acquisition of subsidiary

Total comprehensive income for the year

Total comprehensive income for the year

Available to equity holders of the Parent

Changes in fair value of available for sale investments

Changes in fair value of available for sale investments

Non controlling interest arising on acquisition of subsidiary

Transfer to reserves

Transfer to reserves

Non controlling interest arising on acquisition of subsidiary

8

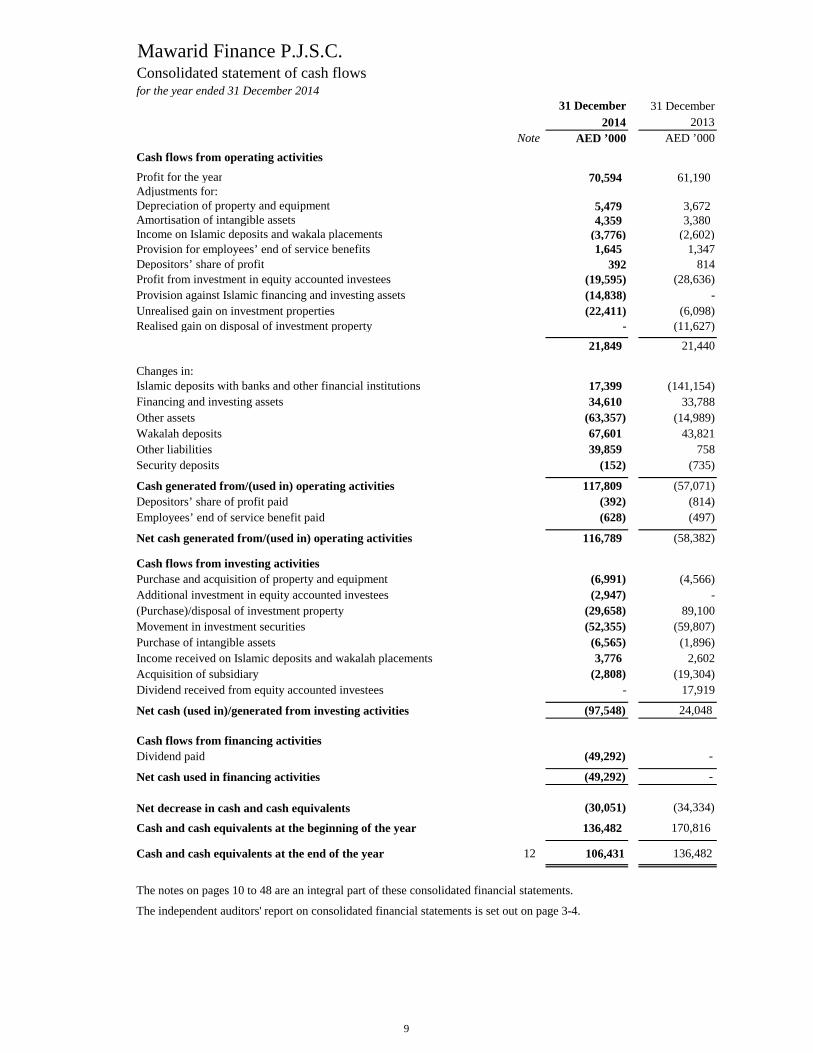

Mawarid Finance P.J.S.C.Consolidated statement of cash flows for the year ended 31 December 2014

31 December 31 December 2014 2013

Note AED ’000 AED ’000 Cash flows from operating activitiesProfit for the year 70,594 61,190 Adjustments for:Depreciation of property and equipment 5,479 3,672 Amortisation of intangible assets 4,359 3,380 Income on Islamic deposits and wakala placements (3,776) (2,602) Provision for employees’ end of service benefits 1,645 1,347 Depositors’ share of profit 392 814 Profit from investment in equity accounted investees (19,595) (28,636)Provision against Islamic financing and investing assets (14,838) - Unrealised gain on investment properties (22,411) (6,098)Realised gain on disposal of investment property - (11,627)

21,849 21,440

Changes in:Islamic deposits with banks and other financial institutions 17,399 (141,154)Financing and investing assets 34,610 33,788 Other assets (63,357) (14,989)Wakalah deposits 67,601 43,821 Other liabilities 39,859 758 Security deposits (152) (735)

Cash generated from/(used in) operating activities 117,809 (57,071)Depositors’ share of profit paid (392) (814)Employees’ end of service benefit paid (628) (497)

Net cash generated from/(used in) operating activities 116,789 (58,382)

Cash flows from investing activitiesPurchase and acquisition of property and equipment (6,991) (4,566)Additional investment in equity accounted investees (2,947) - (Purchase)/disposal of investment property (29,658) 89,100 Movement in investment securities (52,355) (59,807)Purchase of intangible assets (6,565) (1,896)Income received on Islamic deposits and wakalah placements 3,776 2,602 Acquisition of subsidiary (2,808) (19,304)Dividend received from equity accounted investees - 17,919

Net cash (used in)/generated from investing activities (97,548) 24,048

Cash flows from financing activitiesDividend paid (49,292) -

Net cash used in financing activities (49,292) -

Net decrease in cash and cash equivalents (30,051) (34,334)

Cash and cash equivalents at the beginning of the year 136,482 170,816

Cash and cash equivalents at the end of the year 12 106,431 136,482

The notes on pages 10 to 48 are an integral part of these consolidated financial statements.

The independent auditors' report on consolidated financial statements is set out on page 3-4.

9

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

1 Establishment and operations

2 Basis of preparation

a) Statement of compliance

b) Basis of measurement

c) Functional and presentation currency

d) Use of estimates and judgments

3 Islamic shari'a definitionsThe following terms are used in the consolidated financial statements with the meaning specified:-

Shari'a

Ijarah

Mawarid Finance P.J.S.C. (the “Company”) was registered on 4 December 2006 as a Private Joint Stock Company inaccordance with the UAE Federal Law No 8 of 1984, as amended. The address of the Company’s registered office is P.O. Box212121, Dubai, United Arab Emirates ("UAE").

The Company is licensed by the Central Bank of the UAE as a finance company and is primarily engaged in Islamic Shari’acompliant financing and investment activities involving products such as Ijara, Forward Ijara, Murabaha, Musharaka andWakalah. The activities of the Company are conducted in accordance with Islamic Shari’a, which prohibits usury, and theprovisions of its Memorandum and Articles of Association.

The consolidated financial statements includes the results of the operations of the Company and its subsidiaries (collectivelyreferred to as “the Group”). Details of the Company’s subsidiaries are mentioned in note 24 of these consolidated financialstatements.

These consolidated financial statements have been prepared in United Arab Emirates Dirham (AED) rounded to nearestthousand, which is the Group’s functional and presentation currency.

These consolidated financial statements have been prepared in accordance with International Financial Reporting Standards(“IFRS”) and the requirements of UAE Federal Law No.8 of 1984 (as amended).

The consolidated financial statements have been prepared on the historical cost basis except for the following which aremeasured at fair value :i) available-for-sale investments ("AFS"); ii) financial assets at fair value through profit or loss ("FVTPL"); andii) investment properties.

Shari'a is the Islamic law which is essentially derived from the Quran and Sunnah that governs beliefs and conducts of human beings. The Group, incorporates the Shari'a rules and principles in its activities.

The preparation of the consolidated financial statements in conformity with IFRS requires management to make judgments,estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities,income and expenses. Actual results may differ from these estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised inthe period in which the estimate is revised and in any future period affected.

In particular, information about significant areas of estimation uncertainty and critical judgments in applying accountingpolicies that have the most significant effect on the amounts recognised in the consolidated financial statements are describedin note 5.

An agreement whereby the Group (the “Lessor”) leases an asset to its customer (the “Lessee”) (after purchasing/acquiring thespecified asset, either from a third party seller or from the customer, according to the customer’s request and based on hispromise to lease), against certain rental payments for specific lease term/periods, payable on fixed or variable rental basis.

10

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

3 Islamic shari'a definitions (continued)

Ijarah (continued)

Forward Ijarah

Murabaha

Mudaraba

Forward Ijarah (Ijarah Mausoofa Fiz Zimma) is an agreement whereby the Group (the “Lessor”) agrees to provide, on aspecified future date, a certain described asset on lease to its customer (the “Lessee”) upon its completion and delivery by thedeveloper, contractor or customer, from whom the Group has purchased the same, by way of Istisna.

A contract whereby the Group (the “Seller”) sells an asset to its customer (the “Purchaser”), on a deferred payment basis, after purchasing the asset and gaining possession thereof and title thereto, where the Seller has purchased and acquired that asset,based on a promise received from the Purchaser to buy the asset once purchased according to specific Murabaha terms andconditions. The Murabaha sale price comprises the cost of the asset and a preagreed profit amount. Murabaha profit isinternally accounted for on a time-apportioned basis over the period of the contract based on the principal amountoutstanding. The Murabaha sale price is paid by the Purchaser to the Seller on an installment basis over the period of theMurabaha as stated in the contract.

A contract between two parties whereby one party is a fund provider (the “Rab Al Mal”) who would provide a certain amountof funds (the “Mudaraba Capital”), to the other party (the “Mudarib”). Mudarib would then invest the Mudaraba Capital in aspecific enterprise or activity deploying its experience and expertise for a specific pre-agreed share in the resultant profit, ifany. The Rab Al Mal is not involved in the management of the Mudaraba activity. In principle Mudaraba profit is distributedon declaration/distribution by the Mudarib. However, since the Mudaraba profit is always reliably estimated it is internallyaccounted for on a time-apportioned basis over the Mudaraba tenure based on the Mudaraba Capital outstanding. TheMudarib would bear the loss in case of its default, negligence or violation of any of the terms and conditions of the Mudarabacontract; otherwise the loss would be borne by the Rab Al Mal, provided the Rab Al Mal receives satisfactory evidence thatsuch loss was due to force majeure and that the Mudarib neither was able to predict the same nor could have prevented thenegative consequences of the same on the Mudaraba. Under the Mudaraba contract the Group may act either as Mudarib or asRab Al Mal, as the case may be.

The Ijarah agreement specifies the leased asset, duration of the lease term, as well as, the basis for rental calculation and thetiming of rental payment. The Lessee undertakes under this agreement to renew the lease periods and pay the relevant rentalpayment amounts as per the agreed schedule and applicable formula throughout the lease term.

The Lessor retains the ownership of the asset throughout the lease term. At the end of the lease term, upon fulfillment of allthe obligations by the Lessee under the Ijarah agreement, the Lessor will sell the leased asset to the Lessee at nominal valuebased on a sale undertaking given by the Lessor.

Ijarah rentals accrue upon the commencement of the lease and continues throughout the lease term based on the outstandingfixed rental (which predominantly represent the cost of the leased asset).

The Forward Ijarah agreement specifies the description of the leased asset, duration of the lease term, and the basis for rentalcalculation and the timing of rental payment.

During the construction period, the Group pays to the developer/contractor one payment or multiple payments, Forward Ijarahprofit during the construction period will be accounted for on a time-apportioned basis over the construction period onaccount of rentals. These profit amounts are received either during the construction period as advance rental payment or withthe first or second rental payment after the commencement of the lease.

The lease rental under Forward Ijarah commences only upon the Lessee having received possession of the leased asset fromthe Lessor. The Lessee undertakes under the Forward Ijarah agreement to renew the lease periods and pay the relevant rentalpayment amounts as per the agreed schedule and applicable formula throughout the lease term.

The Lessor retains the ownership of the asset throughout the lease term. At the end of the lease term, upon fulfillment of allthe obligations by the Lessee under the Forward Ijarah agreement, the Lessor will sell the leased asset to the Lessee atnominal value based on a sale undertaking given by the Lessor.

11

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

3 Islamic shari'a definitions (continued)Wakalah

Musharaka

Sukuk

Amanat accounts

4 Changes in accounting policies

a)

i) Offsetting financial assets and financial liabilities (Amendment to IAS 32)

ii) Recoverable amount disclosures for non-financial assets (Amendments to IAS 36)

These amendments had no material impact on the disclosures in the Group's consolidated financial statements.

The Group acts as a trustee agent for clients escrow accounts for a fixed fee.

The amendments to IAS 32 clarify the requirements relating to offset of financial assets and financial liabilities. Specifically,the amendments clarify the meaning of 'currently has a legally enforceable right of set-off' and 'simultaneous realisation andsettlement'.

The change has no impact on the disclosures or the amounts recognised in the Group's consolidated financial statements.

The Group has adopted the following new standards and amendments to standards, including any consequential amendmentsto other standards, with a date of initial application of 1 January 2014.

The amendments to IAS 36 remove the requirement to disclose the recoverable amount of a cash-generating unit (CGU) towhich goodwill or other intangible assets with indefinite useful lives had been allocated when there has been no impairmentor reversal of impairment of the related CGU. Furthermore, the amendment introduce additional disclosure requirementapplicable to when the recoverable amount of an asset or a CGU is measured at fair value less cost of disposal. These newdisclosures include the fair value hierarchy, key assumptions and valuation techniques used which are in line with thedisclosure required by IFRS 13 Fair Value Measurement.

These comprise asset backed, Sharia’a compliant trust certificates.

An agreement between two parties whereby one party is a fund provider (the “Muwakkil”) who provides a certain amount ofmoney (the “Wakala Capital”) to an agent (the “Wakeel”), who invests the Wakala Capital in a Sharia’a compliant mannerand according to the feasibility study/investment plan submitted to the Muwakkil by the Wakeel. The Wakeel is entitled to afixed fee (the “Wakala Fee”) as a lump sum amount or a percentage of the Wakala Capital. The Wakeel may be granted anyexcess over and above a certain pre-agreed rate of return as a performance incentive. In principle, wakala profit is distributedon declaration/distribution by the Wakeel. However, since the Wakala profit is always reliably estimated it is internallyaccounted for on a time-apportioned basis over the Wakala tenure based on the Wakala Capital outstanding. The Wakeelwould bear the loss in case of its default, negligence or violation of any of the terms and conditions of the Wakala Agreement;otherwise the loss would be borne by the Muwakkil, provided the Muwakkil receives satisfactory evidence that such loss wasdue to force majeure and that the Wakeel neither was able to predict the same nor could have prevented the negativeconsequences of the same on the Wakala. Under the Wakala agreement the Group may act either as Muwakkil or as Wakeel,as the case may be.

An agreement between the Group and its customer, whereby both parties contribute towards the capital of the Musharaka (the“Musharaka Capital”). The Musharaka Capital may be contributed in cash or in kind, as valued at the time of entering into theMusharaka. The subject of the Musharaka may be a certain investment enterprise, whether existing or new, or the ownershipof a certain property either permanently or according to a diminishing arrangement ending up with the acquisition by thecustomer of the full ownership. The profit is shared according to a pre-agreed profit distribution ratio as stipulated under theMusharaka agreement. In principle Musharaka profit is distributed on declaration/distribution by the managing partner.However, since the Musharaka profit is always reliably estimated, it is internally accounted for on a time-apportioned basisover the Musharaka tenure based on the Musharaka Capital outstanding. Whereas the loss, if any, is shared in proportion totheir capital contribution ratios, provided in the absence of the managing partner’s negligence, breach or default, the Groupreceives satisfactory evidence that such loss was due to force majeure and that the managing partner neither was able topredict the same nor could have prevented the negative consequences of the same on the Musharaka.

12

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

4 Changes in accounting policies (continued)

iii) IFRIC 21-Levies

iv) Investment entities (Amendment to IFRS 10, IFRS 12, and IAS 27)

5 Significant accounting policies

a) Basis of consolidation

i) Business combinations

ii) Non-controlling interests("NCI")

The amendments to IFRS 10, define an investment entity and require a reporting entity that meets the definition of aninvestment entity not to consolidate its subsidiaries but instead to measure its subsidiaries at fair value through profit or lossin its consolidated and separate financial statements.

Consequential amendments have been made to IFRS 12 and IAS 27 to introduce new disclosure requirements for investmententities.

The consideration transferred does not include amounts related to the settlement of pre-existing relationships. Such amountsare generally recognised in consolidated statement of profit or loss.

Any contingent consideration payable is measured at fair value at the acquisition date. If the contingent consideration isclassified as equity, then it is not remeasured and settlement is accounted for within equity. Otherwise, subsequent changes inthe fair value of the contingent consideration are recognised in consolidated statement of profit or loss.

If share-based payment awards (replacement awards) are required to be exchanged for awards held by the acquiree’semployees (acquiree’s awards) and relate to past services, then all or a portion of the amount of the acquirer’s replacementawards is included in measuring the consideration transferred in the business combination. This determination is based on themarket-based value of the replacement awards compared with the market-based value of the acquiree’s awards and the extentto which the replacement awards relate to pre-combination service.

NCI are measured at their proportionate share of the acquiree’s identifiable net assets at the acquisition date. Changes in the Group’s interest in a subsidiary that do not result in a loss of control are accounted for as equity transactions.

The application of this Interpretation had no material impact on the disclosures or on the amounts recognised in the Group'sconsolidated financial statements.

Since the Company is not an investment entity (assessed based on the criteria set out in IFRS 10 as at 1 January 2014), theapplication of the amendments had no impact on the disclosures or the amounts recognised in the Group's consolidatedfinancial statements.

Business combinations are accounted for using the acquisition method as at the acquisition date – i.e. when control istransferred to the Group. The consideration transferred in the acquisition is generally measured at fair value, as are theidentifiable net assets acquired. Any goodwill that arises is tested annually for impairment. Any gain on a bargain purchase isrecognised in consolidated statement of profit or loss immediately. Transaction costs are expensed as incurred, except if theyare related to the issue of debt or equity securities.

IFRIC 21 defines a levy as an outflow from an entity imposed by a government in accordance with legislation. It confirmsthat an entity recognises a liability for a levy when - and only when - the triggering event specified in the legislation occurs.The Interpretation provides guidance on how different levy arrangements should be accounted for, in particular, it clarifiesthat neither economic compulsion nor the going concern basis of the financial statements preparation implies that an entityhas a present obligation to pay a levy that will be triggered by operating in a future period.

Except for changes in accounting policy mentioned in note 3 above, the Company has consistently applied the followingaccounting policies to all periods presented in these financial statements:-

13

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

5 Significant accounting policies (continued)

a) Basis of consolidation (continued)

iii) Subsidiaries

iv) Loss of control

v) Interest in equity accounted investee

vi) Transactions eliminated on consolidation

b) Foreign currencies

Foreign currency transactions

Non-monetary assets and liabilities that are measured at fair value in a foreign currency are translated into the functionalcurrency at the spot exchange rate at the date on which the fair value is determined. Non-monetary items that are measuredbased on historical cost in a foreign currency are translated using the spot exchange rate at the date of the transaction.

Foreign currency differences arising on translation are generally recognised in profit or loss. However, foreign currencydifferences arising from the translation of non-monetary available for sale equity instruments are recognised in consolidatedstatement of profit or loss and OCI.

Associate is an entity in which the Group has significant influence, but no control or joint control, over the financial andoperating policies. A joint venture is an arrangement in which the Group has joint control, whereby the Company has rights tonet assets of the arrangement, rather than rights to its assets and obligations for its liabilities.

The Group's interest in equity accounted investee comprise of interest in associates and joint ventures.

Interests in associates and the joint venture are accounted for using the equity method. They are recognised initially at cost,which includes transaction costs. Subsequent to initial recognition, the consolidated financial statements include theCompany's share of profit or loss and OCI of equity accounted investee, until the date on which significant influence or jointcontrol ceases.

The Group has evaluated the impact of the new definition of control and concludes that it sill retains control over itssubsidiaries and therefore results of subsidiaries should be consolidated in the consolidated financial statement.

An impairment loss in respect of equity accounted investee is measured by comparing the recoverable amount of theinvestment with its carrying amount. An impairment loss is recognised in consolidated statement of profit or loss, and isreversed if there has been a favorable change in the estimates used to determine the recoverable amount.

Subsidiaries’ are investees controlled by the Group. The Group ‘controls’ an investee if it is exposed to, or has rights to,variable returns from its involvement with the investee and has the ability to affect those returns through its power over theinvestee. The financial statements of subsidiaries are included in the consolidated financial statements from the date on whichcontrol commences until the date when control ceases.

When the Group loses control over a subsidiary, it derecognises the assets and liabilities of the subsidiary, and any related NCI and other components of equity. Any resulting gain or loss is recognised in profit or loss. Any interest retained in the former subsidiary is measured at fair value when control is lost.

Intra-group balances and transactions, and any unrealised income and expenses (except for foreign currency transaction gains or losses) arising from intra-group transactions, are eliminated in preparing the consolidated financial statements. Unrealised losses are eliminated in the same way as unrealised gains, but only to the extent that there is no evidence of impairment.

Transactions in foreign currencies are translated into the respective functional currency of Group entities at the spot exchangerates at the date of the transactions.

Monetary assets and liabilities denominated in foreign currencies at the reporting date are translated into the functionalcurrency at the spot exchange rate at that date. The foreign currency gain or loss on monetary items is the difference betweenthe amortised cost in the functional currency at the beginning of the year, adjusted for effective profit and payments during the year, and the amortised cost in the foreign currency translated at the spot exchange rate at the end of the year.

14

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

5 Significant accounting policies (continued)

c) Revenue recognitionIjarah

Murabaha

Mudaraba

Musharaka

Income on deposit and wakalah placement

Dividend income

Commission income

IT related income:-

Rendering of services

Sale of goods

Contracts in progress

Income or losses on Mudaraba financing are recognised on an accrual basis using effective profit rate method if they can bereliably estimated. Otherwise, income is recognised on distribution by the Mudarib, whereas losses are charged to income ontheir declaration by the Mudarib.

Income is accounted for on the basis of the reducing balance on a time-apportioned basis using effective profit rate methodthat reflects the effective yield on the asset.

Income earned on deposits and Wakalah placements is recognised on a time proportion basis using effective profit ratemethod.

Dividends on equity instruments are recognised in the consolidated statement of profit or loss when the Group's right toreceive the dividends is established.

Commission income is recognised when the related services are rendered.

Revenue is recognized based on percentage of completion method. Percentage of completion is determined based on pre-defined tasks in the contract.

When the outcome of a transaction involving the rendering of services cannot be estimated reliably, revenue is recognized tothe extent of expenses incurred that are likely to be recovered. These expenses are recognized as expenses in the period inwhich they are incurred. When it is probable that total expenses associated with a transaction involving the rendering ofservices will exceed total revenue, the expected loss is recognized as an expense immediately.

Revenue from contracts for maintenance are recognised on straight line basis over the term of the contract.

Revenue is recognised when the significant risks and rewards of ownership have been transferred to the customer, recovery ofthe consideration is probable, the associated costs and possible return of goods can be estimated reliably, there is nocontinuing management involvement with the goods, and the amount of revenue can be measured reliably. Revenue ismeasured net of returns, trade discounts and volume rebates.

The timing of the transfer of risks and rewards varies depending on the individual terms of the sales agreement.

Contracts in progress represents the gross amount expected to be collected from customers for contract work performed todate. It is measured at costs incurred plus profits recognised to date less progress billings and recognised losses.

In the statement of financial position, contracts in progress for which costs incurred plus recognised profits exceed progressbillings and recognised losses are presented as trade and other receivables. Contracts for which progress billings andrecognised losses exceed costs incurred plus recognised profits are presented as deferred revenue. Advances received fromcustomers are presented as deferred revenue.

Ijarah income is recognised on a time-apportioned basis over the lease term based on the principal amount outstanding usingeffective profit rate method.

Murabaha income is recognised on a time-proportion basis over the period of the contract based on the principal amountsoutstanding using effective profit rate method.

15

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

5 Significant accounting policies (continued)

c) Revenue recognition (continued)

Allocation of profit

Investment properties rental income

Contract revenue

d)

i) Recognition and measurement

ii) Subsequent expenditure

iii) Depreciation

YearsOffice building 25Furniture and fixtures 4Office and IT equipment 3-5Motor vehicles 5

The estimated useful lives of significant items of property and equipment are as follows:

Depreciation methods, useful lives and residual values are reassessed at the reporting date and adjusted if appropriate. Gainsand losses on disposals are determined by comparing proceeds with the carrying amount. These are included in theconsolidated statement of profit or loss.

Property and equipment

Items of property and equipment are measured at cost less accumulated depreciation and any accumulated impairment losses.Cost includes expenditures that are directly attributable to the acquisition of the asset.

Subsequent expenditure is capitalised only when it is probable that the future economic benefits of the expenditure will flowto the Group. On going repairs and maintenance are expensed as incurred.

Depreciation is calculated to write off the cost of items of property and equipment less their estimated residual values usingthe straight line method over their useful lives, and is generally recognised in consolidated statement of profit or loss. Land isnot depreciated.

Allocation of profit between the depositors and the shareholders is calculated according to the Group's standard proceduresand is approved by the Company's Shari'a Supervisory Board.

Rental income from investment properties is recognised as revenue on a straight line basis over the term of the lease. Lease incentives granted are recognised as an integral part of the total rental income, over the term of the lease.

Revenue from contracts include complex custom designed security systems and the customers of the Group can specify majorstructural elements of the security systems. Revenue associated with these contracts is recognized by reference to the stage ofcompletion of the transaction at the end of the reporting period using the percentage of completion method as measured bythe proportion that contract costs incurred to date bear to total estimated costs of the transaction. Only costs that reflectservices performed to date are included in costs incurred to date and only costs that reflect services performed or to beperformed are included in the estimated total cost of the transaction.

When the outcome of a transaction involving the rendering of services cannot be estimated reliably, revenue is recognized tothe extent of expenses incurred that are likely to be recovered. These expenses are recognized as expenses in the period inwhich they are incurred. When it is probable that total expenses associated with a transaction involving the rendering ofservices will exceed total revenue, the expected loss is recognized as an expense immediately.

Gross amounts due from customers on a transaction involving the rendering of services, which are included in trade and otherreceivables, are stated at cost plus attributable profits less any losses incurred or foreseen in bringing contracts to completionand progress billings. For a transaction involving the rendering of services where progress billings exceed the revenuerecognized, the excess is included in trade and other payables as gross amounts due to customers on a transaction involvingthe rendering of service.

16

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

5 Significant accounting policies (continued)e)i) Goodwill

ii) Research and development

iii) Intangible assets

f)

g)

h) Non-derivative financial instrument

Financial assets and financial liabilitiesi) Recognition

ii) Measurement

iii) ClassificationFinancial assets

Financing and investing assets (also refer note 5j); available for sale (also refer note 5k(ii); and

The Group initially recognises financing and investing assets, wakalah placements, other receivables and payables on the date on which they are originated. All other financial instruments (including regular-way purchases and sales of financial assets) are recognised on the trade date, which is the date on which the Group becomes a party to the contractual provisions of the instrument.

A financial asset or financial liability is measured initially at fair value plus, for an item not at fair value through profit orloss, transaction costs that are directly attributable to its acquisition or issue.

The Group classifies its financial assets into one of the following categories:-

Intangible asset acquired in a business combination is identified and recognised separately from goodwill where it satisfies thedefinition of an intangible asset and fair value can be measured reliably. The cost of such intangible asset is its fair value atthe acquisition date.

Subsequent to initial recognition, intangible asset acquired is reported at cost less accumulated amortisation and accumulatedimpairment losses, on the same basis as intangible assets acquired separately. The intangible asset is amortised over a periodof five years, except for licenses which ha infinite useful life, where no amortisation is being charged.

Investment propertyInvestment property is property held either to earn rental income or for capital appreciation or for both, but not for sale in theordinary course of business, use in the production or supply of goods or services or for administrative purposes. Investmentproperty is measured at cost on initial recognition and subsequently at fair value with any change therein recognised in theconsolidated statement of profit or loss. The Group determines fair value on the basis of valuation provided by an independentvaluer who holds a recognised and relevant professional qualification and has recent experience in the location and categoryof the investment property being valued.

Intangible assets and goodwill

Goodwill arising on acquisition of subsidiaries is measured at cost less accumulated losses.

Expenditure on research activities is recognised in consolidated statement of profit or loss as incurred.

Development expenditure is capitalised only if the expenditure can be measured reliably, the product or process is technicallyand commercially feasible, future economic benefits are probable and the Group intends to and has sufficient resources tocomplete development and to use or sell the asset. Otherwise, it is recognised in consolidated statement of profit or loss asincurred. Subsequent to initial recognition, development expenditure is measured at cost less accumulated amortisation andany accumulated impairment losses.

Subsequent to the initial recognition, financial assets at fair value through profit or loss and available-for-sale investments arestated at their fair value. All other financial instruments are measured at amortised cost less impairment loss, if any.

InventoriesInventories are measured at the lower of cost and net realisable value. The cost of inventories is based on the weightedaverage principle.

at fair value through profit or loss, consisting of held for trading or designated at fair value through profit or loss (also refernote 5k(i).

17

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

5 Significant accounting policies (continued)

h) Non-derivative financial instrument (continued)

Financial assets and financial liabilities (continued)

Financial liabilities

iv) DerecognitionFinancial assets

Financial liabilities

v) Offsetting

vi) Amortised cost measurement

Income and expenses are presented on a net basis only when permitted under IFRS, or for gains and losses arising from agroup of similar transactions such as in the Group’s trading activity.

The Group derecognises a financial liability when its contractual obligations are discharged or cancelled, or expire.

Financial assets and financial liabilities are offset and the net amount presented in the consolidated statement of financialposition when, and only when, the Group has a legal right to set off the amounts and it intends either to settle them on a netbasis or to realise the asset and settle the liability simultaneously.

The ‘amortised cost’ of a financial asset or financial liability is the amount at which the financial asset or financial liability ismeasured at initial recognition, minus principal repayments, plus or minus the cumulative amortisation using the effectiveprofit method of any difference between the initial amount recognised and the maturity amount, minus any reduction forimpairment.

In transactions in which the Group neither retains nor transfers substantially all of the risks and rewards of ownership of afinancial asset and it retains control over the asset, the Group continues to recognise the asset to the extent of its continuinginvolvement, determined by the extent to which it is exposed to changes in the value of the transferred asset.

In certain transactions, the Group retains the obligation to service the transferred financial asset for a fee. The transferredasset is derecognised if it meets the derecognition criteria. An asset or liability is recognised for the servicing contract if theservicing fee is more than adequate (asset) or is less than adequate (liability) for performing the servicing.

The Group classifies its financial liabilities, other than financial guarantees and loan commitments, as measured at amortisedcost or fair value through profit or loss.

The Group derecognises a financial asset when the contractual rights to the cash flows from the financial asset expire, or ittransfers the rights to receive the contractual cash flows in a transaction in which substantially all of the risks and rewards ofownership of the financial asset are transferred or in which the Group neither transfers nor retains substantially all of the risksand rewards of ownership and it does not retain control of the financial asset.

On derecognition of a financial asset, the difference between the carrying amount of the asset (or the carrying amountallocated to the portion of the asset derecognised) and the sum of the consideration received (including any new assetobtained less any new liability assumed) and any cumulative gain or loss that had been recognised in consolidated OCI isrecognised in consolidated profit or loss. Any profit in transferred financial assets that qualify for derecognition that is createdor retained by the Group is recognised as a separate asset or liability.

The Group enters into transactions whereby it transfers assets recognised on its consolidated statement of financial position,but retains either all or substantially all of the risks and rewards of the transferred assets or a portion of them. In such cases,the transferred assets are not derecognised. Examples of such transactions are securities lending and sale and repurchasetransactions.

When assets are sold to a third party with a concurrent total rate of return swap on the transferred assets, the transaction isaccounted for as a secured financing transaction similar to sale and repurchase transactions because the Group retains all orsubstantially all of the risks and rewards of ownership of such assets.

18

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

5 Significant accounting policies (continued)

h) Non-derivative financial instrument (continued)

vii) Fair value measurement

viii)

Portfolios of financial assets and financial liabilities that are exposed to market risk and credit risk that are managed by theGroup on the basis of the net exposure to either market or credit risk are measured on the basis of a price that would bereceived to sell a net long position (or paid to transfer a net short position) for a particular risk exposure. Those portfolio-level adjustments are allocated to the individual assets and liabilities on the basis of the relative risk adjustment of each of theindividual instruments in the portfolio.

The fair value of a demand deposit is not less than the amount payable on demand, discounted from the first date on which theamount could be required to be paid.

The Group recognises transfers between levels of the fair value hierarchy as of the end of the reporting period during whichthe change has occurred.

Identification and measurement of impairment

At each reporting date, the Group assesses whether there is objective evidence that financial assets not carried at fair valuethrough profit or loss are impaired. A financial asset or a group of financial assets is impaired when objective evidencedemonstrates that a loss event has occurred after the initial recognition of the asset(s) and that the loss event has an impact onthe future cash flows of the asset(s) that can be estimated reliably.

'Fair value' is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction betweenmarket participants at the measurement date in the principal or, in its absence, the most advantageous market to which theGroup has access at that date. The fair value of a liability reflects its non-performance risk.

When available, the Group measures the fair value of an instrument using the quoted price in an active market for thatinstrument. A market is regarded as active if transactions for the asset or liability take place with sufficient frequency andvolume to provide pricing information on an ongoing basis.

If there is no quoted price in an active market, then the Group uses valuation techniques that maximize the use of relevantobservable inputs and minimize the use of unobservable inputs. The chosen valuation technique incorporates all of the factorsthat market participants would take into account in pricing a transaction.

The best evidence of the fair value of a financial instrument at initial recognition is normally the transaction price - i.e. the fairvalue of the consideration given or received. If the Group determines that the fair value at initial recognition differs from thetransaction price and the fair value is evidenced neither by a quoted price in an active market for an identical asset or liabilitynor based on a valuation technique that uses only data from observable markets, then the financial instrument is initiallymeasured at fair value, adjusted to defer the difference between the fair value at initial recognition and the transaction price.Subsequently, that difference is recognised in the consolidated statement of profit or loss on an appropriate basis over the lifeof the instrument but no later than when the valuation is wholly supported by observable market data or the transaction isclosed out.

If an asset or a liability measured at fair value has a bid price and an ask price, then the Group measures assets and longpositions at a bid price and liabilities and short positions at an ask price.

In addition, for an investment in an equity security, a significant or prolonged decline in its fair value below its cost isobjective evidence of impairment. However, in specific circumstances a smaller decline or a shorter period may beappropriate.

The Group considers evidence of impairment for financing and investing assets at both a specific asset and a collective level.All individually significant financing and investing assets are assessed for specific impairment. Those found not to bespecifically impaired are then collectively assessed for any impairment that has been incurred but not yet identified. Financingand investing assets that are not individually significant are collectively assessed for impairment by grouping togetherfinancing and investing assets with similar risk characteristics.

19

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

5 Significant accounting policies (continued)

h) Non-derivative financial instrument (continued)viii)

If the expected restructuring will not result in derecognition of the existing asset, then the estimated cash flows arising fromthe modified financial asset are included in the measurement of the existing asset based on their expected timing and amountsdiscounted at the original effective profit rate of the existing financial asset.If the expected restructuring will result in derecognition of the existing asset, then the expected fair value of the new asset istreated as the final cash flow from the existing financial asset at the time of its derecognition. This amount is discounted fromthe expected date of derecognition to the reporting date using the original effective profit rate of the existing financial asset.

Impairment losses are recognised in consolidated statement of profit or loss and reflected in an allowance account againstfinancing and investing assets. Profit on the impaired assets continues to be recognised through the unwinding of the discount.If an event occurring after the impairment was recognised causes the amount of impairment loss to decrease, then the decreasein impairment loss is reversed through consolidated statement of profit or loss.

Impairment losses on available-for-sale investment securities are recognised by reclassifying the losses accumulated in theinvestment revaluation reserve in equity to consolidated statement of profit or loss. The cumulative loss that is reclassifiedfrom equity to consolidated statement of profit or loss is the difference between the acquisition cost, net of any principalrepayment and amortisation, and the current fair value, less any impairment loss recognised previously in consolidatedstatement of profit or loss. Changes in impairment attributable to application of the effective profit method are reflected as acomponent of profit income.

If, in a subsequent period, the fair value of an impaired available-for-sale debt security increases and the increase can berelated objectively to an event occurring after the impairment loss was recognised, then the impairment loss is reversedthrough consolidated statement of profit or loss; otherwise, any increase in fair value is recognised through consolidatedstatement of OCI. Any subsequent recovery in the fair value of an impaired available-for-sale equity security is alwaysrecognised in consolidated statement of OCI.

In assessing collective impairment, the Group uses statistical modeling of historical trends of the probability of default, thetiming of recoveries and the amount of loss incurred, and makes an adjustment if current economic and credit conditions aresuch that the actual losses are likely to be greater or lesser than is suggested by historical trends. Default rates, loss rates andthe expected timing of future recoveries are regularly benchmarked against actual outcomes to ensure that they remainappropriate.

Impairment losses on assets measured at amortised cost are calculated as the difference between the carrying amount and thepresent value of estimated future cash flows discounted at the asset’s original effective profit rate.

If the terms of a financial asset are renegotiated or modified or an existing financial asset is replaced with a new one due tofinancial difficulties of the borrower, then an assessment is made of whether the financial asset should be derecognised. If thecash flows of the renegotiated asset are substantially different, then the contractual rights to cash flows from the originalfinancial asset are deemed to have expired. In this case, the original financial asset is derecognised and the new financial assetis recognised at fair value. The impairment loss before an expected restructuring is measured as follows:-

The Group writes off a financing and investing asset or an investment debt security, either partially or in full, and any relatedallowance for impairment losses, when Group Credit determines that there is no realistic prospect of recovery.

Identification and measurement of impairment(continued)

20

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

5 Significant accounting policies (continued)

i)

j)

i)

ii)

iii)

k)

i)Investments in equity instruments are classified as financial assets at fair value through profit or loss, unless the Groupdesignates them as an investment that is not held for trading and are accordingly classified as available-for-sale investments.

Financial assets measured at FVTPL are initially recognised and subsequently measured at fair value, with any gains or lossesarising in re-measurement recognised in the consolidated statement of profit or loss. All transaction costs are charged toconsolidated statement of profit or loss.

Dividend income on investments in equity instruments at FVTPL is recognised in the consolidated statement of profit or losswhen Group’s right to receive is established.

Investment securities are initially measured at fair value plus, in the case of investment securities not at fair value throughprofit or loss, incremental direct transaction costs, and subsequently accounted for depending on their classification as eitherheld to maturity, fair value through profit or loss, or available-for-sale.

Financing and investing assetsFinancing and investing assets consist of Murabaha receivables, Mudaraba, Musharaka, Wakalah arrangements and Ijarahcontracts and they are measured at amortised cost less any amounts written off and allowance for impairment losses.

Allowance for impairment is made against financing and investing assets when their recovery is in doubt taking intoconsideration lAS 39 requirements for fair value measurement. Financing and investing assets are written off only when allpossible courses of action to achieve recovery have proved unsuccessful. Losses expected from future events are notrecognised. The Group writes off a loan or an investment debt security, either partially or in full, and any related allowancefor impairment losses, when Group Credit determines that there is no realistic prospect of recovery.

Individually assessed financing and investing assets

Cash and cash equivalentsCash and cash equivalents as referred to in the consolidated statement of cash flows comprises cash on hand, non-restrictedcurrent accounts with the Central Bank of U,A.E. and amounts due from/to other entities on demand or with an originalmaturity of three months or less.

Individually assessed financing and investing assets mainly represent corporate and commercial financing and investing assetswhich are assessed individually in order to determine whether there exists any objective evidence that they are impaired. Theyare classified as impaired as soon as there is doubt about the customer's ability to meet payment obligations to the Group inaccordance with the original contractual terms.

Impairment losses of collectively assessed financing and investing assets include mainly the allowances on financing andinvesting assets with common features which are assessed on a portfolio basis.

Collectively assessed financing and investing assets

Reversal of impairmentIf the amount of an impairment loss decreases in a subsequent period, and the decrease can be related objectively to an eventoccurring after the impairment was recognised, the excess is written back by reducing the impairment allowance accountaccordingly. The write-back is recognised in the consolidated statement of profit or loss in the period in which it occurs.

Fair value through profit or loss ("FVTPL")

Investment securities

21

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

5 Significant accounting policies (continued)

k)ii)

l) Impairment of non financial assets

m) Provisions

Warranty provision

Investment securities (continued)

For impairment testing, assets are grouped together into the smallest group of assets that generates cash inflows fromcontinuing use that is largely independent of the cash inflows of other assets or CGUs. Goodwill arising from a businesscombination is allocated to CGUs or groups of CGUs that are expected to benefit from the synergies of the combination.

A provision is recognised if, as a result of a past event, the Group has a present legal or constructive obligation that can beestimated reliably, and it is probable that an outflow of economic benefits will be required to settle the obligation. Provisionsare determined by discounting the expected future cash flows to reflect current market assessments of the time value of moneyand, where appropriate, the risks specific to the liability.

The ‘recoverable amount’ of an asset or CGU is the greater of its value in use and its fair value less costs to sell. ‘Value inuse’ is based on the estimated future cash flows, discounted to their present value using a pre-tax discount rate that reflectscurrent market assessments of the time value of money and the risks specific to the asset or CGU.

An impairment loss is recognised if the carrying amount of an asset or CGU exceeds its recoverable amount.

Impairment losses are recognised in consolidated statement of profit or loss. They are allocated first to reduce the carryingamount of any goodwill allocated to the CGU, and then to reduce the carrying amounts of the other assets in the CGU on a pro rata basis.

An impairment loss in respect of goodwill is not reversed. For other assets, an impairment loss is reversed only to the extentthat the asset’s carrying amount does not exceed the carrying amount that would have been determined, net of depreciation oramortisation, if no impairment loss had been recognised.

A provision for warranties is recognised when the underlying products or services are sold based on historical warranty dataand a weighing of possible outcome against their associated probabilities.

At each reporting date, the Group reviews the carrying amounts of its non-financial assets (other than investment propertiesand deferred tax assets) to determine whether there is any indication of impairment. If any such indication exists, then theasset’s recoverable amount is estimated. Goodwill is tested annually for impairment.

Available for sale‘Available-for-sale investments’ are non-derivative investments that are designated as available for- sale or are not classifiedas another category of financial assets. Available-for-sale investments comprise equity securities and debt securities.Unquoted equity securities whose fair value cannot be measured reliably are carried at cost. All other available-for-saleinvestments are measured at fair value after initial recognition.

Profit income is recognised in consolidated statement of profit or loss using the effective profit method. Dividend income isrecognised in consolidated statement of profit or loss when the Group becomes entitled to the dividend. Foreign exchangegains or losses on available-for-sale debt security investments are recognised in consolidated statement of profit or loss.Impairment losses are recognised in consolidated statement of profit or loss.

Other fair value changes, other than impairment losses, are recognised in OCI and presented in the fair value reserve withinequity. When the investment is sold, the gain or loss accumulated in equity is reclassified to profit or loss.

A non-derivative financial asset may be reclassified from the available-for-sale category to the financing and investing assetsand receivables category if it would otherwise have met the definition of financing and investing assets and receivables and ifthe Group has the intention and ability to hold that financial asset for the foreseeable future or until maturity.

22

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

5

n) Financial guarantees

o)

p)

q)

r)

Operating leasesLeases of assets under which the lessor effectively retains all the risks and rewards of ownership are classified as operatingleases. Payments made under operating leases are recognised in the consolidated statement of profit or loss on a straight-linebasis over the term of the lease.

Ordinary shares are classified as equity. Incremental costs directly attributable to the issue of ordinary shares and shareoptions are recognised as a deduction from equity, net of any tax effects.

Share capitalOrdinary shares

Forfeited incomeAccording to the Shari'a Supervisory Board of the Company, the Group is required to identify any income deemed to bederived from sources not acceptable under Shari'a regulations and to set aside such amount in a separate account used to payfor local social activities.

Staff terminal benefitsThe Group provides for staff terminal benefits based on estimation of the amount of future benefit that employees have earnedin return for their service until their retirement. This calculation is performed based on a projected unit credit method.

Significant accounting policies (continued)

Contributions to retirement pension for UAE nationals

The Group contributes to the pension scheme for UAE nationals under the UAE pension and social security law. This is adefined contribution pension plan and the Group’s contributions are charged to the consolidated statement of profit or loss inthe period to which they relate. In respect of this scheme, the Group has a legal and constructive obligation to pay the fixedcontributions as they fall due and no obligations exist to pay the future benefits.

‘Financial guarantees’ are contracts that require the Group to make specified payments to reimburse the holder for a loss thatit incurs because a specified debtor fails to make payment when it is due in accordance with the terms of a debt instrument.

Liabilities arising from financial guarantees are initially measured at fair value and the initial fair value is amortised over thelife of the guarantee. The liability is subsequently carried at the higher of this amortised amount and the present value of anyexpected payment to settle the liability when a payment under the contract has become probable. Financial guarantees areincluded within other liabilities.

23

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

5 Significant accounting policies (continued)

s) New standards and interpretations not yet adopted

IFRS 15 Revenue from Contracts with Customers (effective 1 January 2017)Financial instruments (2014) (effective 1 January 2018)

i) IFRS 15 Revenue from Contracts with Customers

ii)

6 Key accounting estimates and judgments

i) Impairment losses on financing and investing assets and other receivables

The Group makes estimates and assumptions that affect the reported amounts of assets and liabilities within the next financialyear and the resultant provisions and fair value. Estimates and judgments are continually evaluated and are based on historicalexperience and other factors, including expectations of future events that are believed to be reasonable under thecircumstances.

IFRS 15 establishes a comprehensive framework for determining whether, how much and when revenue is recognised. Itreplaces existing revenue recognition guidance, including IAS 18 Revenue, IAS 11 Construction Contracts and IFRIC 13Customer Loyalty Programmes.

IFRS 9 Financial Instruments

IFRS 9, published in July 2014, replaces the existing guidance in IAS 39 Financial Instruments: Recognition andMeasurement. IFRS 9 includes revised guidance on the classification and measurement of financial instruments, including anew expected credit loss model for calculating impairment on financial assets, and the new general hedge accountingrequirements. It also carries forward the guidance on recognition and derecognition of financial instruments from IAS 39.

A number of new standards, amendments to standards and interpretations are effective for annual periods beginning after 1January 2014 and have not been applied in preparing these consolidated financial statements. Those that may be relevant tothe Group are set out below. The Group does not plan to adopt these standards early.

IFRS 9

The Group reviews its portfolios of financing receivables and other receivable to assess impairment at least on a quarterlybasis. In determining whether an impairment loss should be recorded in the consolidated statement of profit or loss, theGroup makes judgments as to whether there is any observable data indicating that there is a measurable decrease in theestimated future cash flows from a portfolio within financing receivables and other receivable before the decrease can beidentified with an individual receivable in that portfolio.

This evidence may include observable data indicating that there has been an adverse change in the payment status ofcustomers in a group, or national or local economic conditions that correlate with defaults on assets in the Group.Management uses estimates based on historical loss. Experience for assets with credit risk characteristics and objectiveevidence of impairment similar to those in the portfolio when scheduling its future cash flows. The methodology andassumptions used for estimating both the amount and timing of future cash flows are reviewed regularly to reduce anydifferences between loss estimates and actual loss experience.

The key assumptions concerning the future, and other key sources of estimation uncertainty at the reporting date, that have asignificant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year,are discussed below:-

The Group has started the process of evaluating the potential effect of this standard but is awaiting finalisation of the limitedamendments before the evaluation can be completed. Given the nature of the Group’s operations, this standard is expected tohave a pervasive impact on the Group’s financial statements.

24

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

6 Key accounting estimates and judgments (continued)

ii) Valuation of financial instrument

iii) Classification of investments

iv) Useful life of property and equipment

v) Revenue recognition

The Group measures fair values using the fair value hierarchy, which reflects the significance of the inputs used in making themeasurements.

All other investments are classified as AFS investments.

The costs of items of property and equipment are depreciated on a systematic basis over the estimated useful lives of theassets. Management has determined the estimated useful lives of each asset and/ or category of assets based on the followingfactors:-

When the outcome of a transaction involving the rendering of service can be estimated reliably, revenue associated with thetransaction is recognised by reference to the stage of completion of the transaction activity at the end of the reporting period.In judging whether the outcome of a transaction involving the rendering of service can be estimated reliably, management hasconsidered the detailed criterion for determination of such outcome. For the purpose of estimating the stage of completion ofthe transaction, management has considered the forecasts for revenue and expenses, including cost estimates related to thetransaction.

Management considers the depreciation method utilised reflects the pattern in which the assets' future economic benefits areexpected to be consumed by the Group. Management has not made estimates of residual values for any items of property andequipment at the end of their useful lives as these have been deemed to be immaterial.

Valuation techniques include net present value and discounted cash flow models, comparison to similar instruments for whichmarket observable prices exist, and other valuation models. Assumptions and inputs used in valuation techniques include risk-free and benchmark profit rates, credit spreads in estimating discount rates, bond and equity prices, foreign currency exchangerates, equity and equity index prices and expected price volatilities and correlations. The objective of valuation techniques isto arrive at a fair value measurement that reflects the price that would be received to sell the asset or paid to transfer theliability in an orderly transaction between market participants at the measurement date.

Management decides on acquisition of an investment whether it should be classified as carried at FVTPL or AFS investments.

The Group classifies investments as FVTPL if they are acquired primarily for the purpose of making a short term profit by thedealers. Changes in fair values are reported as part of the consolidated statement of profit or loss.

The Group recognises transfers between levels of the fair value hierarchy at the end of the reporting period during which thechange has occurred.

expected usage of the assets;expected physical wear and tear, which depends on operational and environmental factors; andlegal or similar limits on the use of the assets.

25

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

6 Key accounting estimates and judgments (continued)

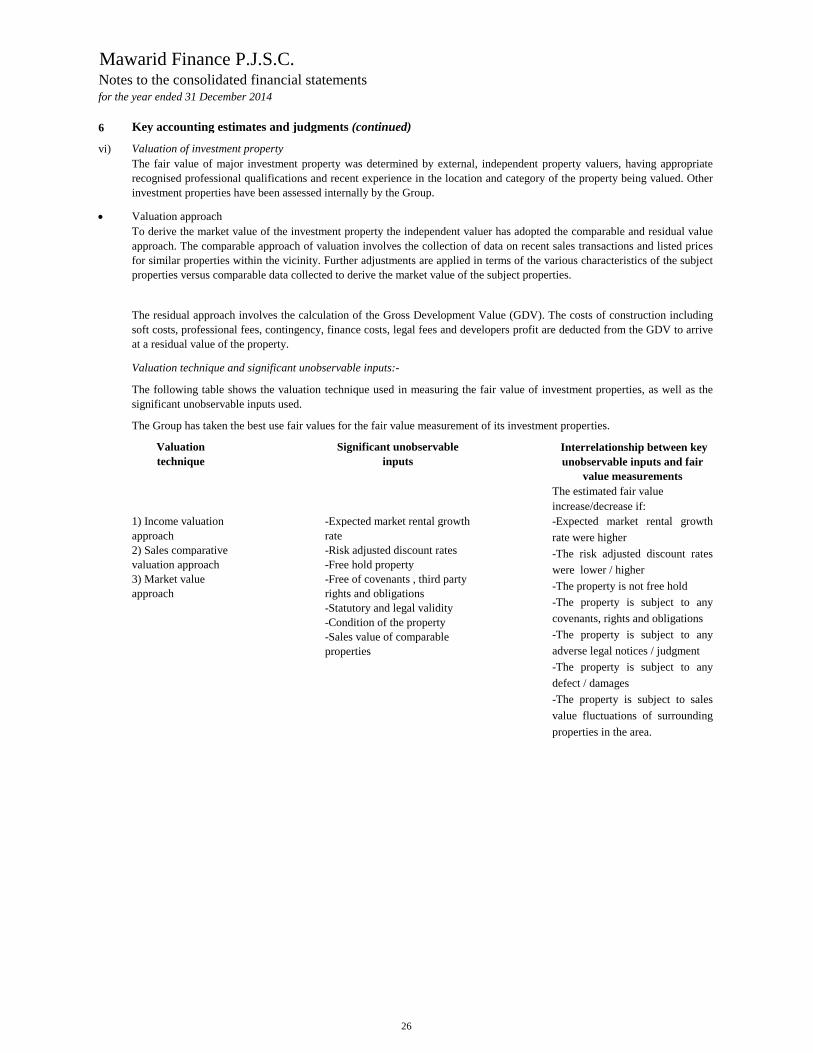

vi) Valuation of investment property

Valuation approach

Valuation technique and significant unobservable inputs:-

The estimated fair valueincrease/decrease if:

The fair value of major investment property was determined by external, independent property valuers, having appropriaterecognised professional qualifications and recent experience in the location and category of the property being valued. Otherinvestment properties have been assessed internally by the Group.

Significant unobservable inputs

-Expected market rental growth rate-Risk adjusted discount rates-Free hold property-Free of covenants , third party rights and obligations -Statutory and legal validity-Condition of the property -Sales value of comparable properties

Interrelationship between key unobservable inputs and fair

value measurements

-Expected market rental growthrate were higher-The risk adjusted discount rateswere lower / higher-The property is not free hold-The property is subject to anycovenants, rights and obligations -The property is subject to anyadverse legal notices / judgment-The property is subject to anydefect / damages-The property is subject to salesvalue fluctuations of surroundingproperties in the area.

The residual approach involves the calculation of the Gross Development Value (GDV). The costs of construction includingsoft costs, professional fees, contingency, finance costs, legal fees and developers profit are deducted from the GDV to arriveat a residual value of the property.

The following table shows the valuation technique used in measuring the fair value of investment properties, as well as thesignificant unobservable inputs used.

The Group has taken the best use fair values for the fair value measurement of its investment properties.

Valuation technique

1) Income valuation approach2) Sales comparative valuation approach3) Market value approach

To derive the market value of the investment property the independent valuer has adopted the comparable and residual valueapproach. The comparable approach of valuation involves the collection of data on recent sales transactions and listed pricesfor similar properties within the vicinity. Further adjustments are applied in terms of the various characteristics of the subjectproperties versus comparable data collected to derive the market value of the subject properties.

26

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

7 Financial risk management

i)ii)iii)iv)

Risk management framework

i) Credit risk

Formulating credit policies in consultation with business units, covering collateral requirements, credit assessment, riskgrading and reporting, documentary and legal procedures, and compliance with regulatory and statutory requirements.

Establishing the authorisation structure for the approval and renewal of credit facilities. Authorisation limits are allocated tobusiness unit Credit Officers. Larger facilities require approval by the Head of Group Credit, the Group Credit Committee orthe Board of directors.

The Group has exposure to the following risks from financial instruments and its operations:

Market risk; andOperational risk

This note presents information about the Group’s objectives, policies and processes for measuring and managing risk.

The Group’s board of directors has overall responsibility for the establishment and oversight of the Group’s risk managementframework. The board of directors has established the Group Asset and Liability Management Committee (ALCO), which isresponsible for developing and monitoring Group risk management policies.

The Group’s risk management policies are established to identify and analyse the risks faced by the Group, to set appropriaterisk limits and controls, and to monitor risks and adherence to limits. The risk management policies and systems are reviewedregularly to reflect changes in market conditions and the Group’s activities. The Group, through its training and managementstandards and procedures, aims to develop a disciplined and constructive control environment in which all employeesunderstand their roles and obligations.

Reviewing and assessing credit risk in accordance with authorisation structure, limits and discretionary powers prior tofacilities being committed to customers. Renewals and reviews of facilities are subject to the same review process.

Providing advice, guidance and specialist skills to business units to promote best practice throughout the Group in themanagement of credit risk.

The Group Audit Committee oversees how management monitors compliance with the Group’s risk management policies andprocedures, and reviews the adequacy of the risk management framework in relation to the risks faced by the Group. TheGroup Audit Committee is assisted in its oversight role by Internal Audit. Internal Audit undertakes both regular and ad hocreviews of risk management controls and procedures, the results of which are reported to the Group Audit Committee. Internalaudit has been outsourced to the third party.

Credit risk is the risk of financial loss to the Group if a customer or counterparty to a financial instrument fails to meet itscontractual obligations, and arises principally from the Group’s financing and investing assets to customers and other banks,and investment in debt securities and funds and receivable from customers. For risk management reporting purposes, theGroup considers and consolidates all elements of credit risk exposure (such as individual obligor default risk, country andsector risk).

Management of credit risk

The Board of directors has delegated responsibility for the oversight of credit risk to its Group Credit Committee. A separateGroup Credit department, reporting to the Group Credit Committee, is responsible for managing the Group’s credit risk,including the following:-

Credit risk;Liquidity risk;

27

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

7 Financial risk management (continued)

i) Credit risk (continued)

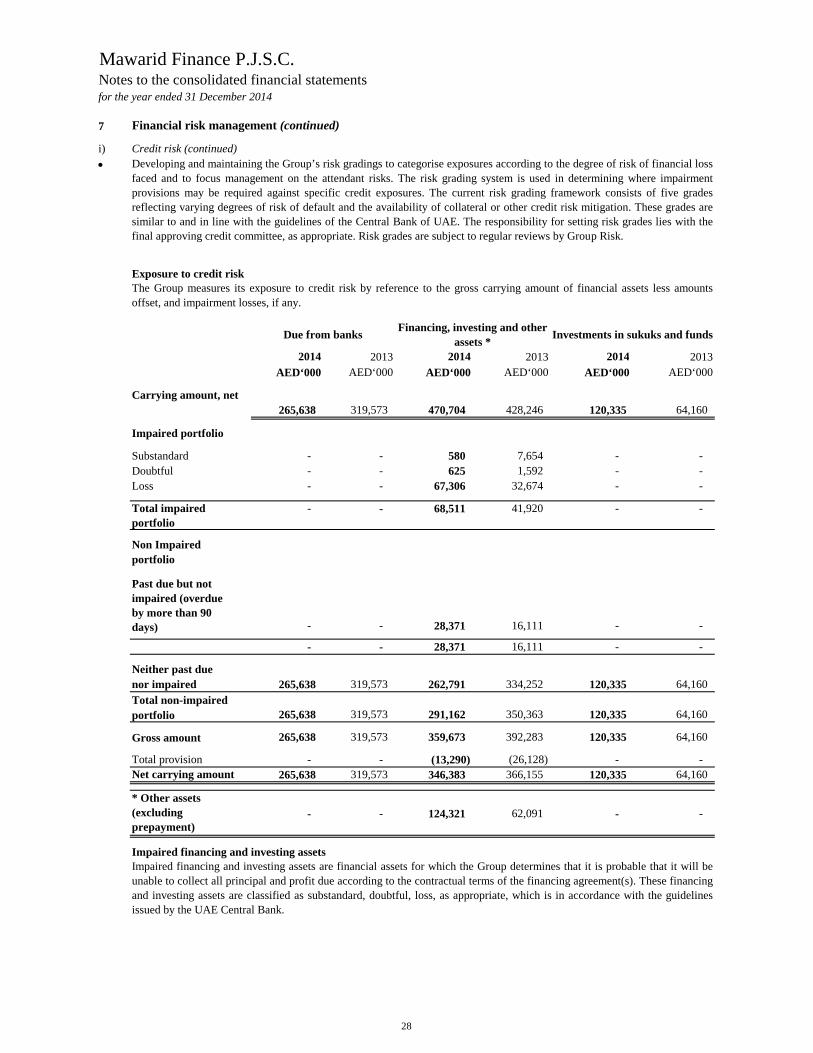

Exposure to credit risk

2014 2013 2014 2013 2014 2013AED‘000 AED‘000 AED‘000 AED‘000 AED‘000 AED‘000

265,638 319,573 470,704 428,246 120,335 64,160

Impaired portfolio

Substandard - - 580 7,654 - - Doubtful - - 625 1,592 - - Loss - - 67,306 32,674 - -

- - 68,511 41,920 - -

- - 28,371 16,111 - -

- - 28,371 16,111 - -

Neither past duenor impaired 265,638 319,573 262,791 334,252 120,335 64,160 Total non-impairedportfolio 265,638 319,573 291,162 350,363 120,335 64,160

Gross amount 265,638 319,573 359,673 392,283 120,335 64,160

Total provision - - (13,290) (26,128) - - Net carrying amount 265,638 319,573 346,383 366,155 120,335 64,160

- - 124,321 62,091 - -

Impaired financing and investing assets

* Other assets (excluding prepayment)

Financing, investing and other assets * Investments in sukuks and funds

Impaired financing and investing assets are financial assets for which the Group determines that it is probable that it will beunable to collect all principal and profit due according to the contractual terms of the financing agreement(s). These financingand investing assets are classified as substandard, doubtful, loss, as appropriate, which is in accordance with the guidelinesissued by the UAE Central Bank.

Carrying amount, net

Total impaired portfolio

Non Impaired portfolio

Past due but not impaired (overdue by more than 90 days)

Developing and maintaining the Group’s risk gradings to categorise exposures according to the degree of risk of financial lossfaced and to focus management on the attendant risks. The risk grading system is used in determining where impairmentprovisions may be required against specific credit exposures. The current risk grading framework consists of five gradesreflecting varying degrees of risk of default and the availability of collateral or other credit risk mitigation. These grades aresimilar to and in line with the guidelines of the Central Bank of UAE. The responsibility for setting risk grades lies with thefinal approving credit committee, as appropriate. Risk grades are subject to regular reviews by Group Risk.

Due from banks

The Group measures its exposure to credit risk by reference to the gross carrying amount of financial assets less amountsoffset, and impairment losses, if any.

28

Mawarid Finance P.J.S.C.Notes to the consolidated financial statements for the year ended 31 December 2014

7 Financial risk management (continued)

i) Credit risk (continued)Past due but not impaired financing and investing assets

Financing and investing assets with renegotiated terms

Allowances for impairment

Collateral

2014 2013AED‘000 AED‘000