mcgraw-hill/irwin ©2001 the mcgraw-hill companies all rights reserved 12.0 chapter 12 cost of...

TRANSCRIPT

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.1

Chapter

12Cost of Capital

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.2

Key Concepts and Skills

Know how to determine a firm’s cost of equity capital

Know how to determine a firm’s cost of debtKnow how to determine a firm’s overall cost

of capitalUnderstand pitfalls of overall cost of capital

and how to manage them

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.3

Chapter Outline

12.1 The Cost of Capital: Some Preliminaries12.2 The Cost of Equity12.3 The Costs of Debt and Preferred Stock12.4 The Weighted Average Cost of Capital12.5 Divisional and Project Costs of Capital

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.4

12.1 The Cost of Capital: Some Preliminaries

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.5

Why Cost of Capital Is Important

We know that the return earned on assets depends on the risk of those assets

The return to an investor in a security, is the cost of that security to the issuing company

Our cost of capital is an indication of how the market views the risk of our assets

Knowing our cost of capital can also help us determine our required return for capital budgeting projects

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.6

Required Return

The required return is the same as the appropriate discount rate and is based on the risk of the cash flows

We need to know the required return for an investment before we can compute the NPV and make a decision about whether or not to take the investment The investment will have a positive NPV only if its return

exceeds the required returnWe need to earn at least the required return to

compensate our investors for the financing they have provided

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.7

Required Return

The cost of capital depends primarily on the “USE” of the funds, not the sourceThe riskier the investment or project – the higher the

cost of capital!

Note: The following terms are interchangeableRequired returnAppropriate discount rateCost of capital

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.8

12.2 The Cost of Equity

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.9

Cost of Equity

The cost of equity is the return required by equity investors given the risk of the cash flows from the firm

There are two major methods for determining the cost of equityDividend growth modelSML or CAPM

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.10

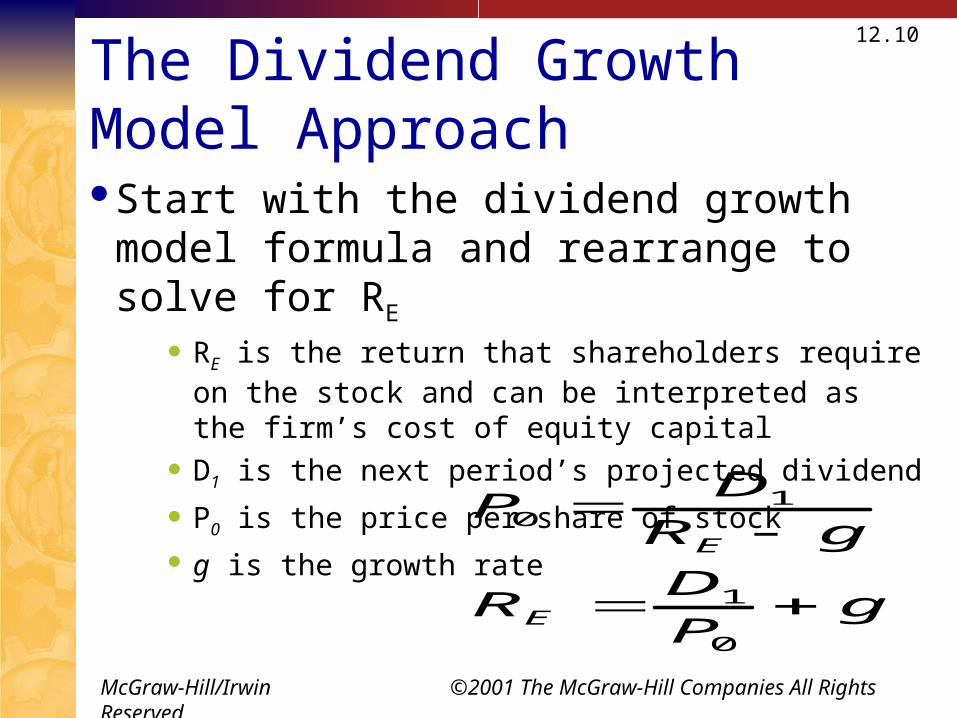

The Dividend Growth Model ApproachStart with the dividend growth model formula

and rearrange to solve for RE

RE is the return that shareholders require on the stock and can be interpreted as the firm’s cost of equity capital

D1 is the next period’s projected dividend

P0 is the price per share of stock g is the growth rate

gP

DR

gR

DP

E

E

0

1

10

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.11

The Dividend Growth Model ApproachFor a publicly traded dividend paying

company:P0 and D0 can be observed in the marketg (the expected growth rate) must be estimatedD1 = D0 x (1 + g)

RE = D1 / P0 + g

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.12

Example: Estimating the Dividend Growth RateOne method for estimating the growth rate is to

use the historical averageCalculate the change in the dividend on a year-to-

year basis and then express the change as a %Year Dividend Percent Change1995 1.231996 1.301997 1.361998 1.431999 1.50

(1.30 – 1.23) / 1.23 = 5.7%

(1.36 – 1.30) / 1.30 = 4.6%

(1.43 – 1.36) / 1.36 = 5.1%

(1.50 – 1.43) / 1.43 = 4.9%

Average = (5.7 + 4.6 + 5.1 + 4.9) / 4 = 5.1%

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.13

Estimating the Dividend Growth RateA second method for estimating the growth

rate is to use analysts’ forecasts of future growth rates

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.14

Dividend Growth Model Example

Suppose that your company is expected to pay a dividend of $1.50 per share next year. There has been a steady growth in dividends of 5.1% per year and the market expects that to continue. The current price is $25. What is the cost of equity? RE = D1 / P0 + g

111.051.25

50.1ER

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.15

Advantages and Disadvantages of Dividend Growth ModelAdvantage – easy to understand and useDisadvantages

Only applicable to companies currently paying dividends Not applicable if dividends aren’t growing at a reasonably

constant rate Extremely sensitive to the estimated growth rate – an

increase in g of 1% increases the cost of equity by 1% Does not explicitly consider risk

No allowance for the degree of certainty or uncertainty surrounding the estimated growth rate in dividends

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.16

The Security Market Line (SML) ApproachFrom Previous ChapterUsing the SML, we can write the expected return on the

company’s equity, E(RE), as:

Risk-free rate, Rf

U.S. Treasury bill benchmark Systematic risk of asset, = Market Risk

Widely available on publicly traded companies Market risk premium, (E(RM ) – Rf )

Based on large common stocks

))(( fMEfE RRERR

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.17

Example - SML

Suppose your company has an equity beta of .58 and the current risk-free rate is 6.1%. If the expected market risk premium is 8.6%, what is your cost of equity capital?

RE = 6.1 + .58(8.6) = 11.1%Since we came up with similar numbers using both

the dividend growth model and the SML approach, we should feel pretty good about our estimate

))(( fMEfE RRERR

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.18

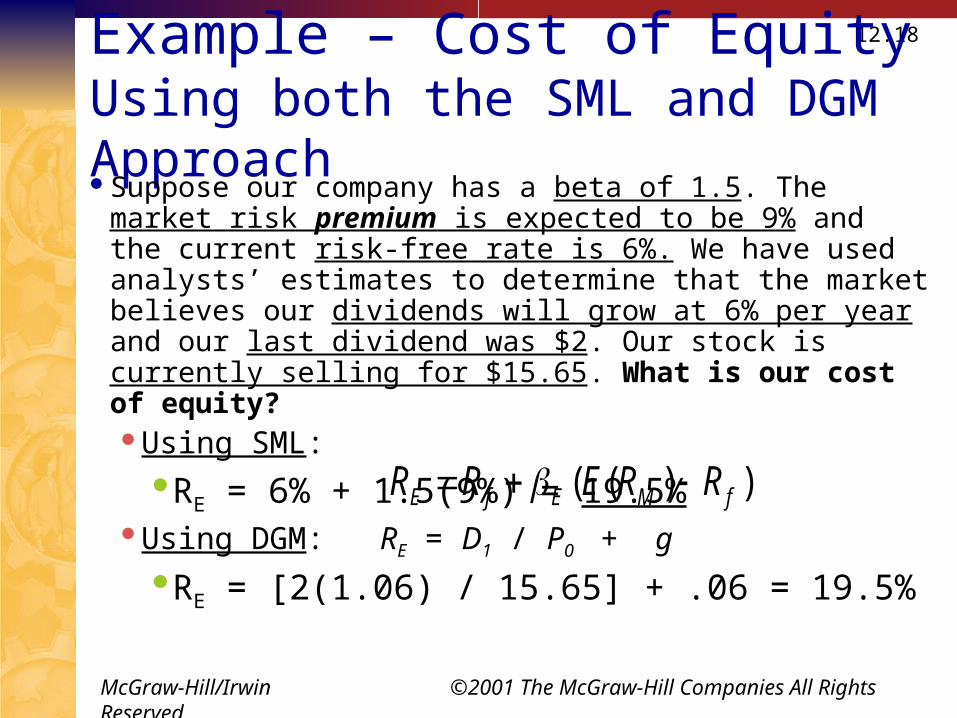

Example – Cost of EquityUsing both the SML and DGM ApproachSuppose our company has a beta of 1.5. The market risk

premium is expected to be 9% and the current risk-free rate is 6%. We have used analysts’ estimates to determine that the market believes our dividends will grow at 6% per year and our last dividend was $2. Our stock is currently selling for $15.65. What is our cost of equity?Using SML:

RE = 6% + 1.5(9%) = 19.5%Using DGM: RE = D1 / P0 + g

RE = [2(1.06) / 15.65] + .06 = 19.5%

))(( fMEfE RRERR

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.19

The Cost of Equity Example 12.1

Review:The Cost of EquityExample 12.1Page 349

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.20

Advantages and Disadvantages of SMLAdvantages

Explicitly adjusts for systematic (Market) riskApplicable to all companies, as long as we can

compute beta Not restricted to just those companies with steady

dividend growth

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.21

Advantages and Disadvantages of SMLDisadvantages

Have to estimate the expected market risk premium, which does vary over time

Have to estimate beta, which also varies over time

We are relying on the past to predict the future, which is not always reliable If the estimates are poor, the resulting cost of equity

will be inaccurate

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.22

12.3 The Costs of Debt and Preferred Stock

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.23

Cost of Debt

In addition to ordinary equity, firms use debt and, to a lesser extent, preferred stock to finance their investments

The “cost of debt” is the required return on our company’s debtThe return that lenders require on the firm’s debtThe interest rate the firm must pay on new borrowing

We can observe these interest rates in the financial markets

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.24

Cost of DebtWe usually focus on the cost of long-term debt

or bondsIf the firm already has bonds outstanding, then

the required return is best estimated by computing the yield-to-maturity on the existing debt

The cost of debt is NOT the coupon rate –which indicates what the firm’s cost of debt was when the bonds were issued, not the cost of debt today. We must use the “yield” in today’s market: yield-to-

maturity

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.25

Cost of Debt

We can also use estimates of current rates based on the bond rating we expect when we issue new debtIf we expect the bonds to be rated AA:

Then we simply use the interest rate associated with newly issued AA-rated bonds

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.26

Cost of Debt ExampleSuppose we have a bond issue currently outstanding that

has 25 years left to maturity. The coupon rate is 9% and coupons are paid semiannually. The bond is currently selling for $908.72 per $1000 bond. What is the cost of debt?

Hint: Calculate the Yield-to-Maturity (YTM) N = 50; PMT = 45; FV = 1000; PV = -908.75;

I = 5%; YTM = 5(2) = 10%Pmt Computation: (1,000 x .09) / 2

(semiannually) = $45N Computation: 25 years x 2 (coupons are paid

semiannually or twice per year)

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.27

Cost of Debt Example 12.2 (Pg 350) Suppose the General Tool Company issued a 30-year, 7

percent bond eight years ago. The bond is currently selling for 96 percent of its face value, or $960. What is General Tool’s cost of debt?

N = 30 – 8 = 22; PMT = 1000 x .07 = 70;

FV = 1000; PV = -1000 x .96 = -960;

I = 7.37%; YTM = 7.37%

General Tool’s cost of debt, RD, is 7.37% (assuming annual coupons)

Note: since the bond is selling at $960 and the face value = $1,000, the bond is selling at a discount, therefore, the YTM of 7.37% is greater than the coupon rate of 7%

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.28

Cost of Debt

Question: Why is the coupon rate a bad estimate of a firm’s cost debt?

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.29

Cost of Debt

Answer: the coupon rate – indicates what the firm’s cost of debt was when the bonds were issued, not the cost of debt today.

We must use the firm’s cost of debt in today’s market.

Yield-to-maturity (YTM), estimates the firm’s cost of debt today.

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.30

Cost of Preferred Stock

Preferred stock has a fixed dividend paid every period forever

So a share of preferred stock is essentially a “Perpetuity”.

The cost of preferred stock, RP, is thus:

RP = D / P0

Where D is the fixed dividend and P0 is the current price per share of the preferred stock

The cost of preferred stock is simply equal to the dividend yield on the preferred stock.

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.31

Cost of Preferred Stock - Example

Your company has preferred stock that has an annual dividend of $3. If the current price is $25, what is the cost of preferred stock?

RP = D / P0

RP = 3 / 25 = 12%

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.32

12.4 The Weighted Average Cost of Capital (WACC)

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.33

Weighted Average Cost of Capital

Now that we have the costs associated with the main sources of capital the firm employs: Equity and Debt: we need to determine the specific mix: The firms “Capital Structure”.

This mix or “average” is the required return on our assets, based on the market’s perception of the risk of those assets

Weights are determined by how much of each type of financing (equity or debt) that we use

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.34

Capital Structure WeightsCapital Structure Weight Calculations

wE = E/V = percent financed with equity wD = D/V = percent financed with debt

Where: E = “market value” of equity = # outstanding shares

times price per share D = “market value” of debt = # outstanding bonds times

bond price If there are multiple bond issues, we repeat this calculation

for each and then add up the results V = “market value” of the firm = D + E

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.35

Example – Capital Structure WeightsSuppose you have a market value of equity

equal to $500 million and a market value of debt = $475 million.What are the capital structure weights?

V = market value of the firm = 500 + 475 = 975 million wE = E/V = 500 / 975 = .5128 = 51.28%

wD = D/V = 475 / 975 = .4872 = 48.72%

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.36

Taxes and the WACCWe are always concerned with after-tax cash flows, so we

need to consider the effect of taxes on the various costs of capital

Interest expense reduces our tax liability This reduction in taxes reduces our cost of debt After-tax cost of debt = RD(1-TC)

Dividends are not tax deductible, so there is no tax impact on the cost of equity

WACC = (E/V) x RE + (D/V) x RD x (1-TC)WACC = wERE + wDRD(1-TC)

WACC = the overall return the firm must earn on its existing assets to maintain the value of the stock

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.37

Weighted Average Cost of Capital (WACC)WACC is the required return on any

investments by the firm that have essentially the same risk as existing operations

If we were evaluating the cash flows from a proposed expansion of our existing operations, WACC is the discount rate we would use i.e. in an NPV calculation

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.38

Extended Example – WACC - I

Equity Information 50 million shares $80 per share Beta = 1.15 Market risk premium = 9% Risk-free rate = 5%

Debt Information $1 billion in outstanding

debt (face value) Current quote = 110 Coupon rate = 9%,

semiannual coupons 15 years to maturity Tax rate = 40%

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.39

Extended Example – WACC - IIWhat is the cost of equity?

RE = 5 + 1.15(9) = 15.35%

What is the cost of debt? If the firm already has bonds o/s, then the required return

= yield-to-maturity on the existing debt N = 30; PV = -1100; PMT = 45; FV = 1000; I = 3.9268 RD = 3.927(2) = 7.854%

What is the “after-tax” cost of debt? RD(1-TC) = 7.854(1-.4) = 4.712%

))(( fMEfE RRERR

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.40

Extended Example – WACC - III

What are the capital structure weights? E = 50 million (80) = 4 billion D = 1 billion (1.10) = 1.1 billion V = 4 + 1.1 = 5.1 billion wE = E/V = 4 / 5.1 = .7843 wD = D/V = 1.1 / 5.1 = .2157

What is the WACC? WACC = wERE + wDRD(1-TC) WACC = .7843(.1535) + .2157(.04712) WACC = .1204 + .0102 WACC = .1306 or 13.06%

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.41

Table 12.1 – Page 355Summary of Capital Cost CalculationsKnow the information in this table.

McGraw-Hill/Irwin ©2001 The McGraw-Hill Companies All Rights Reserved

12.42

Chapter 12: Suggested Homework and Test Review Chapter Review and Self-Test Problems: 12.1 & 12.2, Page 359 Questions and Problems: 1, 2, 5, 7 abc, 10, and 24 (Pages 361, 362 and

364) Know: The formulas in Table 12.1 on page 355 Know how to calculate:

The Cost of Equity (Dividend growth and SML)The Cost of Debt (bonds - YTM)The Cost of Preferred StockThe Weighted Average Cost of Capital, WACCThe capital structure weights (debt and equity)

required for the WACC calculation Study the examples presented in this presentation Know chapter theories, concepts, and definitions