mediobanca credit profile

TRANSCRIPT

MEDIOBANCA

CREDIT PROFILE

February 2022

AGENDA

1. MB Group profile

2. 1H22 Results

3. Funding & Treasury

3.1 Funding: structure & evolution

3.2 Treasury: structure & evolution

Annex

1. ESG profile

2. 12m figures as at June 21

3

CIB

42%

WM

11%

Consumer

25%

Other

22%

RWAs1

MEDIOBANCA AT A GLANCE

Revenues: €2.6bn

Net profit: €808m

ROTE adj: 9%

C/I ratio: 47%

Total assets: €83bn

Loan book: €48bn

TFA: €71bn

No. of staff: 4.9k

CETI : 16.3%, Tot. Cap: 18.9%

Moody’s rating 3 Baa1

S&P rating 3 : BBB

Fitch rating 3 : BBB

DPS21: €0.66

Payout FY22: 70%

Loan/funding ratio: 86%

Market cap.3: €9bn

Revenues (€m) Net profit (€m) ROTE adjusted2

2,525 2,513 2,628

1,459

June19 June20 June21 Dec21 (6M)

823

600

808

526

June 19 June 20 June21 Dec21 (6M)

10% 10%9%

11%

June19 June 20 June21 Dec21 (6M)

CIB

27%

WM

24%

Consumer

38%

Other

11%

Revenues1

MB Group profile Section 1

Key financial information (June21)

1) Figures referred to FY21 period (June-end 2021 annual period)

2) ROTE based on net profit adjusted calculated as GOP net of LLPs, minorities and taxes, with normalized tax rate (33% for Premier,

CIB, Consumer and HF; 25% for PB and AM; 4.16% for PI). Covid-related impact excluded for FY20

3) As at 10 February 2022

4

Capital intensive

NII driver

Anti-cyclical

Labour intensive

Fee driver

Cyclical

Capital light

Fee driver

Recurrent

EPS/DPS accretive

Revenue driver

Source of capital

AN INTEGRATED BUSINESS MODEL…

Principal Investing

HIGH SYNERGIC BUSINESS

HIGH RETURN BUSINESS

DIVERSIFICATION OPPORTUNITYREALLOCATION OPPORTUNITY

WealthManagement

Corporate & Inv.Banking

Consumer Banking

MB Group profile Section 1

5

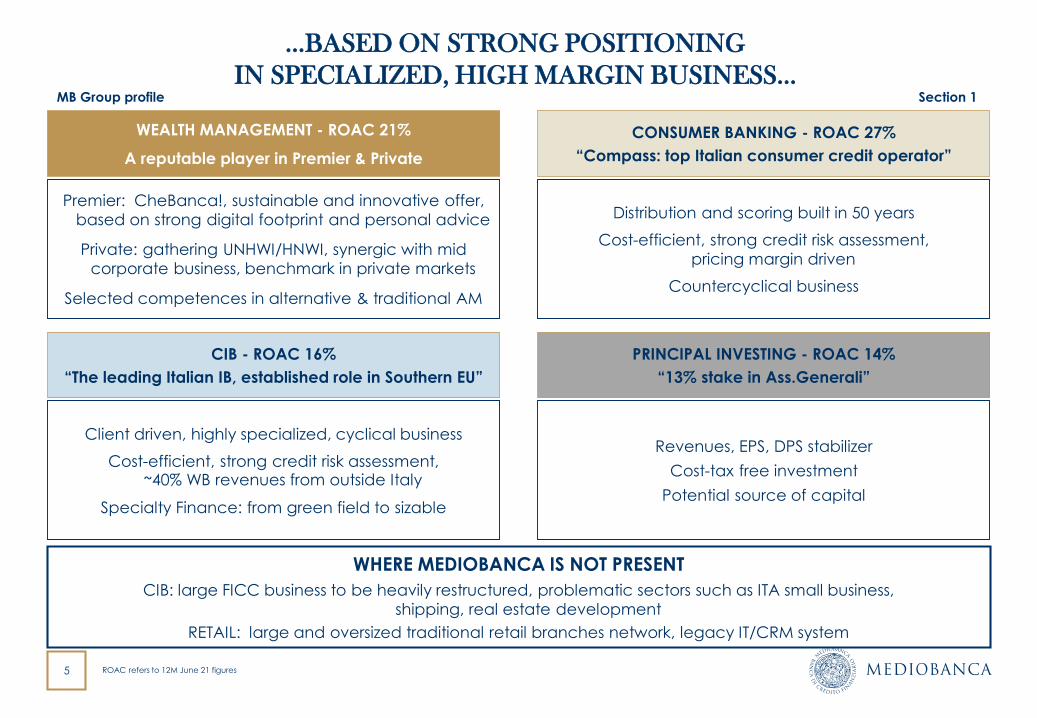

…BASED ON STRONG POSITIONING

IN SPECIALIZED, HIGH MARGIN BUSINESS…

Revenues, EPS, DPS stabilizer

Cost-tax free investment

Potential source of capital

Client driven, highly specialized, cyclical business

Cost-efficient, strong credit risk assessment, ~40% WB revenues from outside Italy

Specialty Finance: from green field to sizable

CIB - ROAC 16%

“The leading Italian IB, established role in Southern EU”

PRINCIPAL INVESTING - ROAC 14%

“13% stake in Ass.Generali”

Premier: CheBanca!, sustainable and innovative offer,

based on strong digital footprint and personal advice

Private: gathering UNHWI/HNWI, synergic with mid

corporate business, benchmark in private markets

Selected competences in alternative & traditional AM

Distribution and scoring built in 50 years

Cost-efficient, strong credit risk assessment,

pricing margin driven

Countercyclical business

CONSUMER BANKING - ROAC 27%

“Compass: top Italian consumer credit operator”

WEALTH MANAGEMENT - ROAC 21%

A reputable player in Premier & Private

WHERE MEDIOBANCA IS NOT PRESENT

CIB: large FICC business to be heavily restructured, problematic sectors such as ITA small business,

shipping, real estate development

RETAIL: large and oversized traditional retail branches network, legacy IT/CRM system

MB Group profile Section 1

ROAC refers to 12M June 21 figures

6

DIVERSIFIED AND STRONG QUALITY OF REVENUE-GENERATING ASSETS...

Fast growing TFA, with improving mix towards qualified AUM/AUA, while enlarging deposit base

Diversified loan book with very low risk profile

MB Group profile Section 1

Private

Banking

7%

Consumer

lending

26%

Leasing

3%

Large

corporate

34%

Specialty

Finance

7%Mortgages

22%

€50.8bn

6.8% 8.7%12.6%

10.1%

4.1% 3.8%

-20.0%-15.0%-10.0%-5.0%0.0%5.0%10.0%15.0%20.0%

0%

5%

10%

15%

20%

25%

MB

Sept21

EU avg.

Sept21

IT avg.

Sept21

Stage 2 loans% of loans1

2.9% 2.6%4.4%

67.1%

47.3%54.6%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

0%

2%

4%

6%

8%

10%

MB

Sept21

EU avg.

Sept21

IT avg.

Sept21

Stage 3 loans% of loans1

coveragecoverage

1) Source: EBA Risk Dashboard – Data as of Sept 2021- %of loans (histogram) and coverage ratio (dots). EBA data may differ from MB reported ratios as the EBA includes treasury balances that are excluded from the MB classification. Purchased or originated creditimpaired (POCI) are not included

3248

56 61 64 7179

June16 June17 June18 June19 June20 June21 Dec21

TFAs evolution (€bn)

Loan book (Dec21)

Deposits

€14.1bn

AUM/AUA

55%

Deposits

€27.2bn

AUM/AUA

66%

€32bn €79bn

June16 Dec21

45% corporate

55% retail

~80% domestic

~20% non-domestic

ESG/green loans: €2.9bn

7

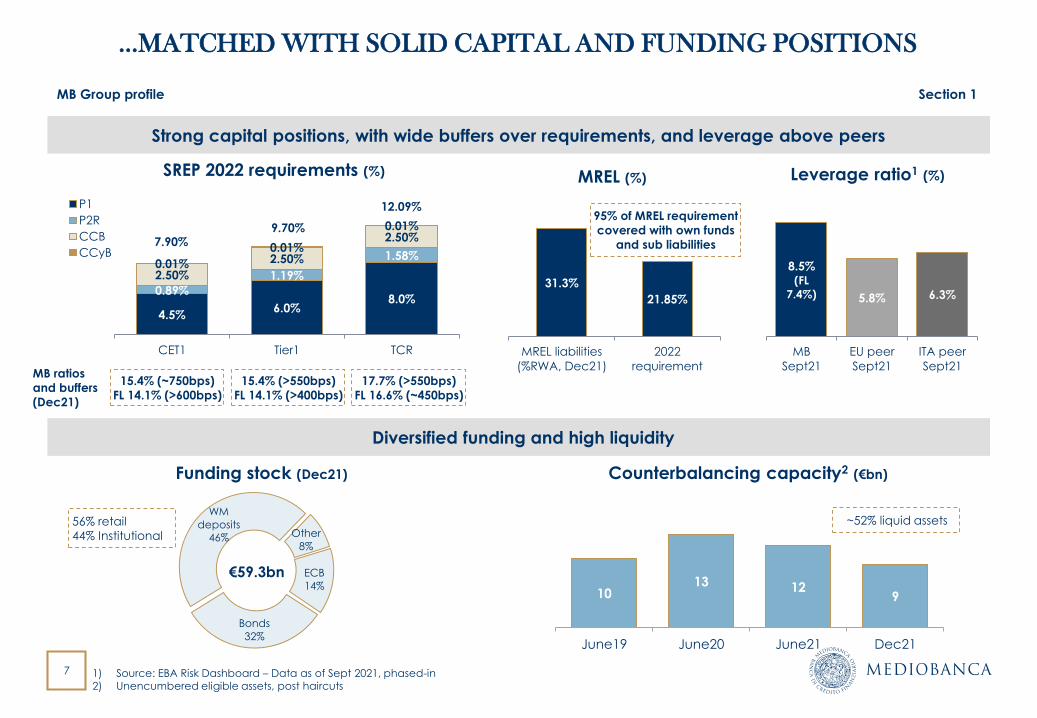

…MATCHED WITH SOLID CAPITAL AND FUNDING POSITIONS

Diversified funding and high liquidity

Strong capital positions, with wide buffers over requirements, and leverage above peers

MB Group profile Section 1

Bonds

32%

WM

deposits

46% Other

8%

ECB

14%€59.3bn

Funding stock (Dec21)

1) Source: EBA Risk Dashboard – Data as of Sept 2021, phased-in2) Unencumbered eligible assets, post haircuts

4.5%6.0%

8.0%0.89%

1.19%

1.58%

2.50%

2.50%

2.50%

0.01%

0.01%

0.01%

CET1 Tier1 TCR

P1

P2R

CCB

CCyB

15.4% (~750bps)

FL 14.1% (>600bps)

17.7% (>550bps)

FL 16.6% (~450bps)

SREP 2022 requirements (%)

7.90%

12.09%

MB ratios

and buffers

(Dec21)

95% of MREL requirement

covered with own funds

and sub liabilities

31.3%

21.85%

MREL liabilities

(%RWA, Dec21)

2022

requirement

MREL (%)

56% retail

44% Institutional

8.5%(FL

7.4%) 5.8% 6.3%

MB

Sept21

EU peer

Sept21

ITA peer

Sept21

Leverage ratio1 (%)

Counterbalancing capacity2 (€bn)

~52% liquid assets

1013 12

9

June19 June20 June21 Dec21

9.70%

15.4% (>550bps)

FL 14.1% (>400bps)

8

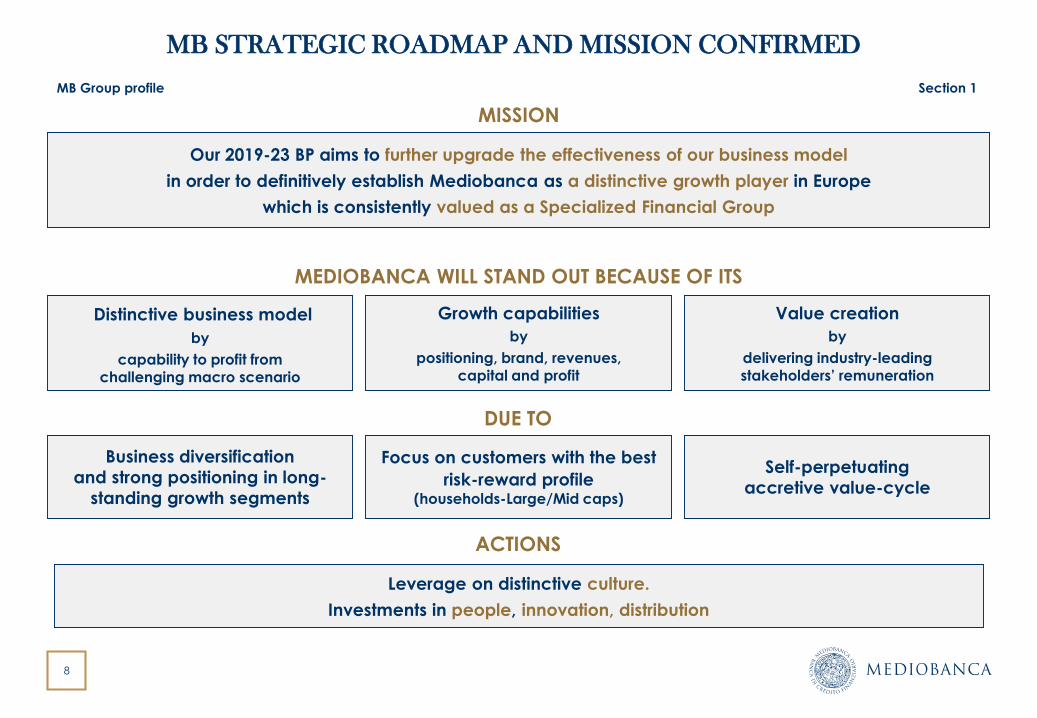

Our 2019-23 BP aims to further upgrade the effectiveness of our business model

in order to definitively establish Mediobanca as a distinctive growth player in Europe

which is consistently valued as a Specialized Financial Group

MB STRATEGIC ROADMAP AND MISSION CONFIRMED

Growth capabilities

by

positioning, brand, revenues, capital and profit

Value creation

by

delivering industry-leading stakeholders’ remuneration

Distinctive business model

by

capability to profit from challenging macro scenario

MEDIOBANCA WILL STAND OUT BECAUSE OF ITS

Focus on customers with the best

risk-reward profile(households-Large/Mid caps)

Self-perpetuating

accretive value-cycle

Business diversification

and strong positioning in long-

standing growth segments

DUE TO

ACTIONS

Leverage on distinctive culture.

Investments in people, innovation, distribution

MB Group profile Section 1

MISSION

9

WELL ON TRACK TO REACH BP23 TARGETS

TFAs up to €83bn(4YCAGR +8%)

✓

61 6471

83

FY19 FY20 FY21 FY23

BP

Ta

rge

t

(€bn)

Loans up to €51bn(4YCAGR +4%)

✓

44 47 48 51

0

10

20

30

40

50

60

FY19 FY20 FY21 FY23

BP

Ta

rge

t

(€bn)

Revenues up to €3bn(4YCAGR +4%)

✓

2.5 2.5 2.63.0

FY19 FY20 FY21 FY23

BP

Ta

rge

t

(€bn)

EPS1 up to €1.10ps(4YCAGR +4%)

(€)

0.93

0.68

0.91 0.931.10

FY19 FY20 FY21 FY21pf* FY22 FY23

ROTE adj. up to 11%(up 1pp)

10% 10%9%

11%

FY19 FY20 FY21 FY23

BP

Ta

rge

t

MB Group profile Section 1

BP

Ta

rge

t

1) FY19, FY20, FY21 calculated considering 887m shares. FY21 proforma calculated considering cancellation of up to 22.6m treasury shares approved in the 2021 AGM.

✓ ✓

AUM/AUA up to €59bn(4YCAGR +11%)

✓

39 4046

59

FY19 FY20 FY21 FY23

BP

Ta

rge

t

(€bn)

10

Targeting industry-leading performance

BP19/23 PLAN CONFIRMED, COVID IMPACT FULLY RECOVERED

Profitability growth

ROTE23 @11%

Earnings growth

+4% EPS CAGR1

Revenues growth

+4% CAGR1

Shareholders’ remuneration

70% cash payout

FY21and FY22

+

BB annually set

1) 4YCAGR 19/23, including treasury shares cancellation (subject to ECB authorization)2) Buyback purpose: cancellation, performance shares and M&A

Shift to capital-light fee business

Revenue growth in a challenging environment

Enhanced return to shareholders

CAPITAL MANAGEMENT POLICY

Capital invested in growth, organic and through M&A, cash DPS distribution, new buyback programmesset annually depending on M&A delivered and MB price

DPS21: €0.66, with 70% cash dividend payout

70% cash dividend payout confirmed also in FY22

Buybacks resumed in FY22: up to 22.6 million treasury shares cancellation + new up to 3% buyback programme2

MB Group profile Section 1

11

MB RIDING ESG MOMENTUM…

Agile and smart working platform project launched to foster work-life balance attractive to the younger generation

Employees: enhanced training programme and HR initiatives to foster engagement and satisfaction

Diversity: group self assessment project to develop new initiatives to address gender diversity and pay gap

MSCI: rating up from “BB” to “A”

CDP: rating up from “D” to “C”

S&P Global: included in the 2022 Sustainability Yearbook

BLOOMBERG: included also for 2022 in the Gender Equality Index

Employee empowerment,

diversity and inclusion

1. The S&P Europe 350 ESG Index is a broad-based, market-cap-weighted index that is designed to measure the performance of securities meeting sustainability criteria, while maintaining similar overall industry group weights as the S&P Europe 350.

2. MIB ESG index includes the top 40 Italian companies ranked according to ESG criteria in line with the UN Global Compact principles, and weighted on the basis of the free float market capitalization.

MB Group profile Section 1

RATING upgrade/confirmationNew Group investment policy

Application spectrum widened to ECM/DCM/Corporate Finance advisory to CIB clients (previously covering only lending and investing)

New Biodiversity Policy and ESG sensitive sectors Policy

MB included in ESG Market Indexes

Mediobanca included in the:

S&P Europe 350 ESG Index1 .

MIB ESG Index2.

The inclusion reflects the progression and improvement of Mediobanca’ssustainability strategy and ESG profile.

Remuneration policy: senior management STI scorecards

enhanced with quantitative ESG targets to support ESG/green product development

Governance enhanced by:

removal of requirement to have Group managers in the BoD,

increased minorities presence in the BoD with one seat reserved to Institutional Investors

Governance improvement

(2021 AGM)

In FY21 we have started several projects to respond to the new European ESG regulatory framework

Disclosure assessment to align in the near future with the requests of SASB

and TCFD

Enriched disclosure to come

12

… WITH GROWING COMMITMENT TO TACKLE CLIMATE CHANGE …

The Principles for Responsible Banking were launched at the United Nations’ General Assembly in September 2019 and have the aim of incentivizing banks to set objectives for sustainable growth and to measure the impact of their own activities on individuals and the planet.

This commitment is consistent with a

maximum temperature rise of well-below 2°C above pre-industrial levels by 2100 –equivalent to net-zero before 2065.

MB Group profile Section 1

Principles for Responsible Banking Net-Zero Banking Alliance

The Net-Zero Banking Alliance, established in April 2021, is the new climate commitment under UNEP FI.

This brings together over 80 banks, the majority of which are PRB signatories, which are committed to aligning their lending and investment portfolios with net-zero emissions by 2050, consistent with a maximum temperature rise of 1.5°C above pre-industrial levels by 2100.

The Mediobanca Group is:

signatory of the Principles for Responsible Banking (PRB) whose aim is to help steering the sector further in the direction of achieving the SDGs set by the UN,

member of the Net-Zero Banking Alliance (NZBA), initiative promoted by the United Nations with the objective of accelerating the sustainable transition of the international banking sector.

Going ahead MB will work:

to comply with the requirements of both PRB and NZBA (significative targets setting, reporting alignment etc.),

to reduce Scope 1 and Scope 2 emissions ,as well as for FY21, neutralizing “non-reducible” greenhouse gas emissions.

MB Group

commitmentNovember 2021June 2021

United Nations Environment Programme Finance Initiative (UNEP FI) is a partnership between UNEP and the global financial sector to mobilize private sector finance for sustainable development.

UNEP FI supports global finance sector principles to catalyze integration of sustainability into financial market practice. The frameworks UNEP FI has established or co-created

include: Principles for Responsible Banking (PRB), Principles for Sustainable Insurance (PSI).

Principles for Responsible Investment (PRI)

13

… DELIVERING BP ESG TARGETS

Procedure adopted to reach targets for equal opportunities, including specification in

head-hunter mandates

1) CSI: Customer Satisfaction Index; NPS: Net Promoter Score2) Premier: clients with wealth between €50k and €5m 3) Underlying 94% from renewables (BPTarget23: lifted to 94%), CO2 down 15% (BPTarget23: revised to down 27%); hybrid cars:

28% (BPTarget23: @90% of MB fleet)

Employee competences enhanced with training hours up 71% (BPTarget23: 25%).

AM: ESG criteria included in >98% of investment evaluation (BPTarget23: 100% of new

investments)

€140m investments in outstanding Italian SMEs (BPtarget23: €700m)

% of ESG qualified funds (under SFDR, Articles 8&9) out of total funds in Premier clients’

portfolio: 33%

Target review

Considering:

The new SFDR disclosure

requirement

The likely Premier target being

beaten (ESG qualified products

in clients’ portfolio: +30% by

FY23) due to increased ESG

product penetration and

significant TFA growth.

We have revised this target as

follows:

% of ESG qualified funds (ex SFDR

art. 8&9) to reach 40% of total funds

in Premier clients’ portfolio

ESG products’ (under SFDR Articles

8&9) penetration in clients’ portfolio

at @33%

ESG bond issue: target achieved (BPtarget23: €500m)

Procurement exp. assessed with CSR criteria: target achieved (BPtarget23: 40%)

Customer satisfaction: CheBanca! CSI¹ in Premier segment² @81, NPS¹ @43 ; Compass CSI¹

@88, NPS¹ @62

€7.3m in FY21 for social/environmental proj. (BPtarget: €4m per year)

MB Social Impact Fund: AUM up 43% (BPtarget23: up 20%)

Energy target: achieved with carbon neutrality (Scope 1 & 2)3

CheBanca! green mortgages up >5X vs FY20 (BPtarget: up 50%)

RAM: target achieved with the launch of Stable Climate Global Equities Fund

FY21 non-financial performanceSeveral targets already met, EU ESG regulation kicking in

SFDR driving AM world

disclosure

MB Group profile Section 1

AGENDA

1. MB Group profile

2. 1H22 Results

3. Funding & Treasury

3.1 Funding: structure & evolution

3.2 Treasury: structure & evolution

Annex

1. ESG profile

2. 12m figures as at June 21

15

RECORD HALF-YEAR RESULTS

CHARACTERIZED BY GROWTH, QUALITY AND SUSTAINABILITY

€1.5bn revenues (up 12%¹), record fees (up 16%1), NII back to growth (up 2%1)

Best-ever asset quality indicators

€526m net profit (up 28%1), 11% ROTE

Accelerating performance in 2Q despite Omicron

Robust growth and capital management² materially increased per share values

6m EPS adj. at €0.59 (up 17%1), TBVPS at €11.3 (up 7%1)

CET13 optimizing (at 15.4%), with 70% cash payout and new 3% buyback2 accrued

Revenues and profit generating capacity definitively increased

also due to digital enhancement with new state of the art investment App in Premier

and launch of Pagolight/BNPL in Consumer Finance

Significant non-financial ESG achievements

Mediobanca has joined the Net-Zero Banking Alliance

1) % changes related to YoY trend (6MDec21 vs 6MDec20)2) n. 22.6 millions of treasury shares from old buyback programme deleted in Dec21. Oct21AGM approved a new buyback

programme relative to max n. 25.9 millions shares (3% capital) to be bought within 12 months for staff performance sharesschemes, M&A and cancellation

3) CET1 Phase-in. CET1 FL @14.1% (without Danish Compromise ~120 bps and with IFRS 9 fully phased ~10 bps)

1H22/2Q22 - Group results Section 2

16

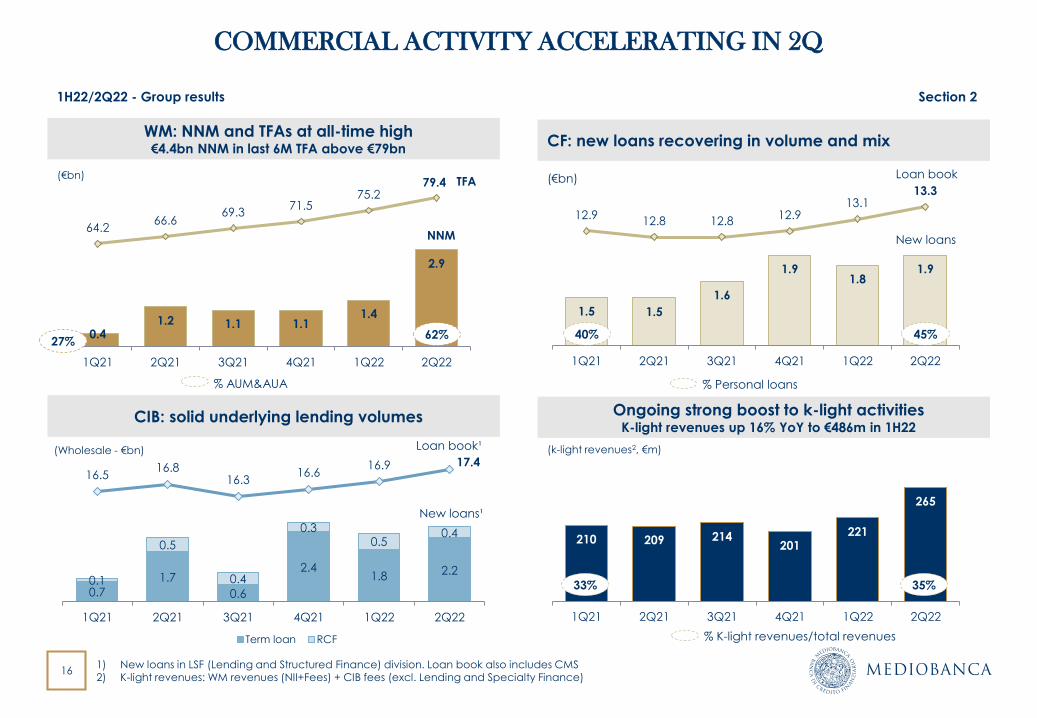

CF: new loans recovering in volume and mix

COMMERCIAL ACTIVITY ACCELERATING IN 2Q

WM: NNM and TFAs at all-time high€4.4bn NNM in last 6M TFA above €79bn

CIB: solid underlying lending volumes Ongoing strong boost to k-light activitiesK-light revenues up 16% YoY to €486m in 1H22

1) New loans in LSF (Lending and Structured Finance) division. Loan book also includes CMS2) K-light revenues: WM revenues (NII+Fees) + CIB fees (excl. Lending and Specialty Finance)

0.7

1.7

0.6

2.41.8 2.2

0.1

0.5

0.4

0.30.5

0.4

16.516.8

16.316.6

16.9 17.4

12

13

14

15

16

17

18

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1Q21 2Q21 3Q21 4Q21 1Q22 2Q22

Term loan RCF

(Wholesale - €bn) Loan book¹

New loans¹

1.5 1.5

1.6

1.91.8

1.9

12.912.8 12.8

12.913.1

13.3

11

12

12

13

13

14

1

1

1

2

2

2

2

2

1Q21 2Q21 3Q21 4Q21 1Q22 2Q22

40% 45%

% Personal loans

Loan book

New loans

0.41.2 1.1 1.1

1.4

2.9

64.266.6

69.371.5

75.279.4

30

35

40

45

50

55

60

65

70

75

80

0

1

1

2

2

3

3

4

4

5

1Q21 2Q21 3Q21 4Q21 1Q22 2Q22

(€bn)

27%62%

% AUM&AUA

TFA

NNM

(€bn)

1H22/2Q22 - Group results Section 2

210 209 214201

221

265

100120140160180200220240260280

1Q21 2Q21 3Q21 4Q21 1Q22 2Q22

(k-light revenues2, €m)

33% 35%

% K-light revenues/total revenues

17

1,3251,301

1,459

62

10 26

70 (10)

Revenues

6M-Dec19

Revenues

6M-Dec20

WM CF CIB PI HF Revenues

6M-Dec21

REVENUES UP 12% YoY, ACCELERATING IN 2QBENEFITING FROM RESTORED/INCREASED REVENUE-GENERATING CAPABILITIES IN ALL SEGMENTS

Group revenues by division (YoY, €m, 6M)

+2%1

+57%1

+20%1

+12% YoY

+7%1

1) YoY % change

156 162 163 172 192

2Q21

Dec20

3Q21

Mar21

4Q21

June21

1Q22

Sept21

2Q22

Dec21

WM: +11%

256 249 238 257 268

2Q21

Dec20

3Q21

Mar21

4Q21

June21

1Q22

Sept21

2Q22

Dec21

CF : + 4%

182 173 161185

206

2Q21

Dec20

3Q21

Mar21

4Q21

June21

1Q22

Sept21

2Q22

Dec21

1H22/2Q22 - Group results Section 2

CIB: +12%

Divisional revenues by Q (€m, 3M)

18

NII BACK TO GROWTH, T-LTRO IMPACT SMOOTHED

NII at €734m in 1H22, clearly back to growth (up 2% YoY and6% HoH), with record 2Q helped by seasonality along withvolume growth and CoF reduction across all divisions; the CFcontribution was particularly positive, with loan book and NIIgrowing above expectations and up both QoQ and YoY

T-LTRO cliff smoothed and offset by ALM optimization: 50bpsremoval (from June22) spread over maturity (2.5Y); €10mimpact for 6M fully booked in 2Q

NII trend by division (€m, 3M)

Loan book by segment (€bn)

12.6 13.5 14.0 14.3 14.4 14.5 14.8

13.7 12.9 12.8 12.8 12.9 13.1 13.3

18.0 18.6 19.5 18.9 19.3 19.5 21.0

Pre-

Covid

(1)

Sept20 Dec20 Mar21 June21 Sept21 Dec21

WM CF CIB HF&Other

46.3 48.9

Quarterly NII trend (€m, 3M)

50.8

1) Pre-Covid: average between 1Q20 and 2Q20 for NII and Dec19 for loan book

48.1

358

375

+6+4

+12 (10)

+3+2

1Q22 CF Other

divisions

ALM optimiz TLTRO

smoothing

2Q22

Margin & CoF effect

Volume effect

237 226 223 216 214 226 236

69 68 69 72 72 74 73

68 72 77 70 68 68 72

Pre-

Covid (1)

1Q21 2Q21 3Q21 4Q21 1Q22 2Q22

CF WM CIB HF&Other

361 358 375363

€720m€695m

€734m+6%+2%

1H22/2Q22 - Group results Section 2

19

FEE INCOME: ROBUST HIGH-QUALITY GROWTH IN WM AND CIB

Fee income steadily on a growing path, posting new record in 2Q (€241m, up 19% QoQ), backed by WM and CIB performances:

WM: largest contributor (€117m in 2Q and €213m in 1H), impressive growth (up 33% YoY and 21% HoH), reflecting increase in management fees and in AUM/AUA, Bybrook consolidation, MB/Blackrock co-investments upfront fees (most in 1H22, €14m)

CIB: high-quality record fees (€102m in 2Q, €187m in 1H) recording material growth (up 9% YoY and 28% HoH) due to a strong performance in Advisory business

CF: broadly stable contribution

Fee income trend by division (€m, 3M)

34 33 33 24 31 32

76 85 87 8996

117

88 84 7769

85

102

1Q21 2Q21 3Q21 4Q21 1Q22 2Q22

CF WM CIB HF&Other

189 194 188173

203

CIB fees (€m, 3M)

1) Capmkt fees include ECM, DCM, CMS, Sales

(10) (12) (13) (15) (14) (15)

59 61 64 67 75 82

9 10 11 1116

1917 21 21 20

1922

1Q21 2Q21 3Q21 4Q21 1Q22 2Q22

Performance

Banking&other

Upfront/Advisory

Management

Passive

7685

8987

96

117

241

4127 35

2539

59

2629 21

17

13

1512

16 10

1317

1110 1212

14

16

17

1Q21 2Q21 3Q21 4Q21 1Q22 2Q22

Specialty fin

Lending

CapMkt¹

Advisory

88 8477

6985

102

€383m €362m

€443m

WM fees (€m, 3M)

+22%

+19%

1H22/2Q22 - Group results Section 2

20

COSTS UP 7% DRIVEN BY STRONG COMMERCIAL ACTIVITYBEST-IN-CLASS COST/INCOME RATIO CONFIRMED (@43%)

Group cost base and cost/income ratio (€m, %, 6M)

Group cost base increase by division (€m, 6M)

288 286 305

304 305 329

45% 45%

43%

20%

25%

30%

35%

40%

45%

0

100

200

300

400

500

600

700

800

900

1H20 1H21 1H22

Admin.expenses Labour cost

C/I ratio

591633+7%

+7%

+8%

Cost base up by €42m (up 7% YoY) driven by strong revenues/business activity and distribution platform enhancement while keeping

cost/income ratio under strict control @43%. Cost increase driven by:

€14m increase in revenues/business related costs including higher variable remuneration accrued (in line with positive revenues trend),

and other volume (mainly retail) related costs

€13m increase due to distribution enhancement mainly related to hiring, marketing, and branches opening

€10m related to further technology upgrades

14

13

10

5

42

Revenue/

business

related

Distribution

enhancement

Technology Other Total

32

13

42

WM CIB CF Other Total cost

increase

Group cost base increase breakdown (€m, 6M)

1H22/2Q22 - Group results Section 2

21

PRUDENT PROVISIONING FURTHER TIGHTENEDMACRO SCENARIO UNCHANGED, OVERLAYS NOT RELEASED, MORATORIA ENDED

Scenario June21 Scenario Dec21

20211 20221 20231 20211 20221 20231

IT GDP 4.5% 4.4% 1.5% +6.4% +4.7% +2.0%

EU GDP 4.0% 4.3% 2.2% +5.1% +4.4% +2.4%

IT UNEPL. Rate 9.8% 9.9% 9.5% 9.6% 9.1% 8.9%

IT 10Y yield 0.6% 1.2% 1.8% 0.7% 1.4% 2.4%

IFRS9 models did not incorporate Dec21 macro upgrade

Moratoria ended: <1% group loans, 83% expired; ~100% of residual positions classified in Stages 2-3, well covered

Extra provisioning: €10m for vintage positions in Leasing and €25m for MBCS portfolio, with a view to progressive de-risking

Overlay stock trend (€m)

1) IT and EU GDP annual % change as at end-December2) Decreased to €0.07bn at end-Jan. 2022

Granted Outstanding o/w Stage 2-3

MB Group 2.22 0.37 ~100%

Consumer 0.97 0.02 100%

Mortgages 0.63 0.10 100%

Leasing 0.62 0.242 100%

Moratoria as % of Group loans

5% <1%

Loans under moratoria (€bn, Dec21)

200 200

90 70

June21 Dec21

CF CIB Other

~€300m ~€290m

Macro scenario trend (MB internal baseline scenario)

1H22/2Q22 - Group results Section 2

Highlights

22

SOLID ASSET QUALITY TREND CONFIRMEDNPLs INCIDENCE DOWN AND COVERAGE RATIO UP

1) Figures in the graphs refer to the Customers Loan Book and may therefore differ from the EBA Dashboard. In particular, the EBA includes treasury balances in NPL and staging calculation (excluded from MB classification) and includes purchased NPLs (€0.4bn) in the NPL ratio (MB does not include gross purchased NPLs in NPL ratio, as does in stage 3 loans)

90% 89% 90%

0.68% 0.65% 0.63%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

50%

70%

90%

110%

Dec20 June21 Dec21

Gross Exposure/Loans Coverage

7.1% 7.6% 7.0%

9.4% 9.7% 10.2%

-10.0%

0.0%

10.0%

20.0%

-1%

4%

9%

14%

Dec20 June21 Dec21

Gross Exposure/Loans Coverage

Performing Loans – Stage 11

3.3% 3.2% 2.8%

63.1% 64.9% 66.9%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

0%

2%

4%

6%

8%

Dec20 June21 Dec21

Gross Exposure/Loans Coverage

➢ Stage 3 – Gross NPLs down to 2.8% of gross

loans (vs 3.2% in June21) as well as net NPLs.

Small ordinary NPL disposals in Consumer

Finance. Coverage ratio up to ~67%

➢ Stage 2 – Down in both absolute terms (by

3% HoH) and relative terms, mainly related

to CIB and mortgages. Coverage ratio at

~10%

➢ Performing loans – Coverage ratio 1.32% at

Group level, further strengthened in

Consumer Finance (up to 3.75%)

1.3% 1.2% 1.0%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

Dec20 June21 Dec21

Performing Loans – Stage 21

Gross NPLs – Stage 31 Net NPLs – Stage 31

(Net exposure/Loans)

Performing Loans coverage ratio

1.31% 1.36% 1.32%

3.35%3.62% 3.75%

Dec20 June21 Dec21

Group CF

1H22/2Q22 - Group results Section 2

23

…ACROSS DIVISIONS

Net NPLs (€m)

(“deteriorate”)

Leasing

Consumer Finance

(CF)

Corporate &

Investment Banking

(CIB)

Wealth

Management

(WM)

of which bad loans (€m)

(“sofferenze”)

NPL coverage NPLs as % of loans

Mediobanca

Group 609 560 487

Dec20 June21 Dec21

104 104 103

Dec20 June21 Dec21

296235

178

Dec20 June21 Dec21

111 116 123

Dec20 June21 Dec21

99 105 83

Dec20 June21 Dec21

83 72 63Dec20 June21 Dec21

0 0 0June20 Mar21 June21

11 9 9Dec20 June21 Dec21

49 43 38Dec20 June21 Dec21

23 20 16Dec20 June21 Dec21

63% 65% 67%

Dec20 June21 Dec21

55% 54% 53%

Dec20 June21 Dec21

72%76% 79%

Dec20 June21 Dec21

49% 49% 48%

Dec20 June21 Dec21

41% 40%51%

Dec20 June21 Dec21

3.3% 3.2% 2.8%

1.3% 1.2% 1.0%

Dec20 June21 Dec21

1.2% 1.2% 1.1%

0.5% 0.5% 0.5%

Dec20 June21 Dec21

7.4% 6.9% 5.8%

2.3% 1.8% 1.3%

Dec20 June21 Dec21

1.5% 1.6% 1.6%

0.8% 0.8% 0.8%

Dec20 June21 Dec21

8.9% 9.4% 9.4%

5.5% 5.9%4.9%

Dec20 June21 Dec21

-13%

-1%

+6%

-20%-20%

Net

Gross

-24%-7%

-11%

-13%

1H22/2Q22 - Group results Section 2

24

POSITIVE COR TREND ONGOING

Prudent approach: given the macro uncertainties and the new wave of the pandemic, the new macro scenario has not beenapplied to IFRS9 models

1H22 Group CoR at 55bps, with a slight increase in 2Q to 60bps due only to extra provisions to facilitate the downsizing of smallcredit buckets (Leasing /MBCS) (~40bps underlying COR in 1H):

CF: CoR down to 133bps in 2Q22 at its lowest-ever level, on low default rates and sound asset quality

CIB: CoR at 27bps in 2Q22, reflecting €25m of extra provisioning for selected MBCS portfolios, only partly offset by writebacksrelated to repayments, upgrades and sector risk improvement

Leasing: additional €10m LLPs related to extra provisioning for residual moratoria and vintage NPLs

CoR trend (bps)

5839

85

141

6139

53 56 51 60

(15)

(52)

37

70

(38)(54)

3 58

2714

11 1327 18 17

13 6 12

11

197 185

223

361

248

196174 183

160133

1Q20 2Q20 3Q20 4Q20 1Q21 2Q21 3Q21 4Q21 1Q22 2Q22

Post-Covid

CF

Group

CIB

WM

Group 1H22

55bps

Group 2H21

54bps

Group 1H21

50bps

1H22/2Q22 - Group results Section 2

25

STRONG CAPITAL POSITION OPTIMIZINGORGANIC CAPITAL CREATION FINANCING GROWTH & SHAREHOLDER REMUNERATION

CET1 phased-in1 ratio trend (%,bps)

CET1 phased-in ratio down 90bps HoH to 15.4%, ow 70bps in 2Q, reflecting

+115bps organic capital generation (split equally between quarters) financing -30bps organic growth (loans up by €2.4bn at alower density, from 57% to 54%) and -80bps cash shareholders’ remuneration (70% cash payout)

-65bps full upfront-loading of buyback programme2 (in 2Q)

-20bps AG impact (mainly in 1Q, as in Q2 extra dividend was paid) to be reversed with AG dividend payment in May 2022

2022 SREP CET1 confirmed at 7.9%3

1) CET1 FL @14.1% (without Danish Compromise ~120 bps and with IFRS 9 fully phased ~10 bps).2) Buyback programme approved by ECB and started in Dec,21, for up to 25.9 million shares to be bought within 12 months for staff

performance shares schemes, M&A and cancellation3) SREP CET1 calculated as: 4.5% Pillar1 + 2.5% CCB + 56.25% P2R (1.58%)+ 0.01% CCyB.

16.3% 16.1% 16.1% 16.1% 16.3%

15.7%15.4% 15.4%

CET1

June21

Earnings 70% Dividend

Pay-out

AG RWA& other Bybrook CET1

Sept21

Earnings 70% Dividend

Pay-out

3% BB RWA CET1

Dec21

+55 +60-40 -20 -5 -10 -40

-65 -25

15.1% FL 15.0% FL 14.1% FL

1H22/2Q22 - Group results Section 2

RWA density

57.1%

RWA density

53.7%

RWA density

55.2%

AGENDA

1. MB Group profile

2. 1H22 Results

3. Funding & Treasury

3.1 Funding: structure & evolution

3.2 Treasury: structure & evolution

Annex

1. ESG profile

2. 12m figures as at June 21

27

FUNDING AT 59BN, HIGH LIQUIDITY

Comfortable funding & liquidity position, with CoF down 5bps vs

FY20/21 to ~60bps

Funding up 6% YoY and HoH to €59bn, with higher contribution

from WM deposits (up 11% YoY, up 8% HoH) and increased ECB

funding: TLTRO3 stock at ~€8.4bn (vs €8.8bn full capacity), after

additional €1bn drawn in 1Q22 and €2bn prolonged to Sept.24

TLTRO economic cliff smoothed: 50bps premium spread over the

residual maturity of 2.5Y

CBC at ~9bn, o/w ~52% liquid assets

NSFR: 110%; LCR:162%

Funding stock breakdown (€bn)

24.6 25.2 27.2

18.7 18.4 18.9

6.2 7.48.46.4 5.14.7

Dec20 June21 Dec21

WM deposits MB securities ECB Other

56.2 59.3+6%

HoH55.9

+6% YoY

Summary & recent trends Section 3

MB securities redemptions(€bn, CoF bps vs Euribor3M)

MB Group counterbalancing capacity (€bn)

CBC: ~€9bn

2.33.8

2.7

10.1

June22 June23 June24 > June23

90 175 165

Avg. CoF expiring bondsBps vs. Euribor3M

ABACO

2.6

HQLA -

Securities

1.5HQLA -

Cash

3.3

Non HQLA -

Securities

1.8

28

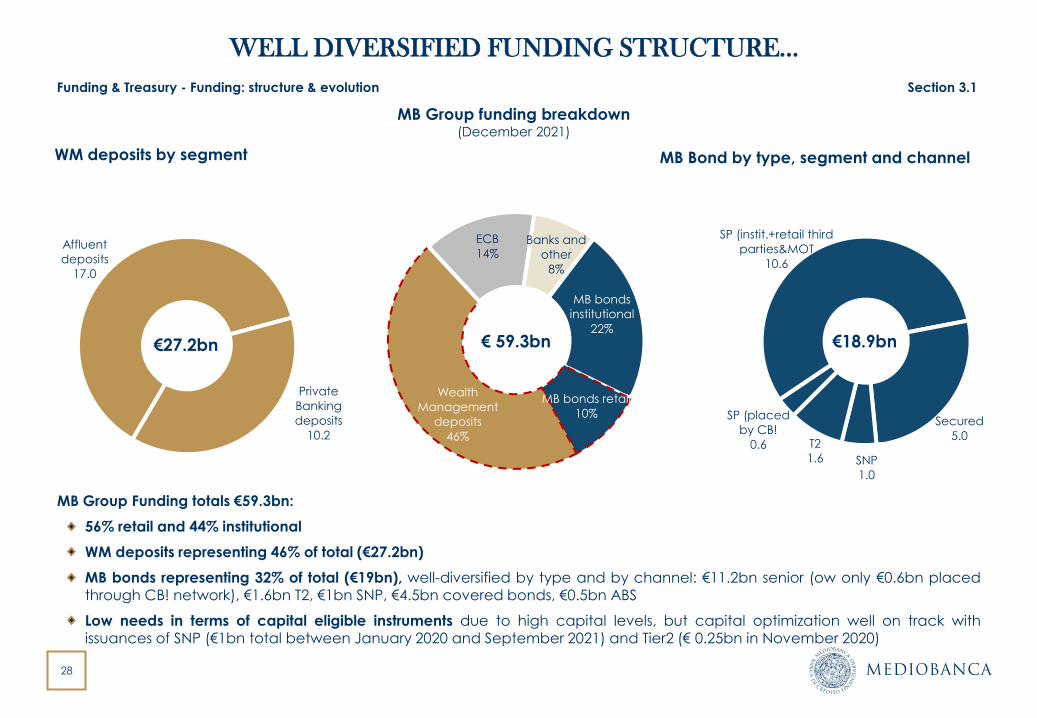

WELL DIVERSIFIED FUNDING STRUCTURE…

MB Group funding breakdown (December 2021)

MB Bond by type, segment and channel

MB Group Funding totals €59.3bn:

56% retail and 44% institutional

WM deposits representing 46% of total (€27.2bn)

MB bonds representing 32% of total (€19bn), well-diversified by type and by channel: €11.2bn senior (ow only €0.6bn placedthrough CB! network), €1.6bn T2, €1bn SNP, €4.5bn covered bonds, €0.5bn ABS

Low needs in terms of capital eligible instruments due to high capital levels, but capital optimization well on track withissuances of SNP (€1bn total between January 2020 and September 2021) and Tier2 (€ 0.25bn in November 2020)

WM deposits by segment

Funding & Treasury - Funding: structure & evolution Section 3.1

MB bonds

institutional

22%

MB bonds retail

10%

Wealth

Management

deposits

46%

ECB

14%Banks and

other

8%

Affluent

deposits

17.0

Private

Banking

deposits

10.2

SP (placed

by CB!

0.6

SP (instit.+retail third

parties&MOT

10.6

Secured

5.0

SNP

1.0

T2

1.6

€ 59.3bn €18.9bn€27.2bn

29

J-08 J-09 J-10 J-11 J-12 J-13 J-14 J-15 J-16 J-17 J-18 J-19 J-20 J-21 D-21

MB bonds Retail depositsPrivate banking deposits Banks & OtherECB

MB bond outstanding by investor

…DIVERSIFIED OVER THE LAST DECADE

MB Group funding trend (€bn)

WM deposit share increased due to CheBanca! and private banking arms’ growth

Bond funding diversified between retail and institutional investors, with institutional funding on a constant rising trend

ECB: reliance around 14% of Group Funding (~€8.4bn as of December 2021, 100% TLTRO3, with maximum drawable

amount of €8.8bn)

45

5659

55% 53%58% 60% 60% 62% 59% 56% 57%

52% 48% 47%37%

31% 30%

45% 47%42% 40% 40% 38% 41% 44% 43%

48% 52% 53%63%

69% 70%

J-08 J-09 J-10 J-11 J-12 J-13 J-14 J-15 J-16 J-17 J-18 J-19 J-20 J-21 D-21

Bonds to retail Bonds to institutionals

Funding: structure & evolution Section 3.1

30

…WITH LOW MREL NEEDS

MREL requirement for 2022 confirmed as one of thelowest in EU

21.84% RWA (19.34% + 2.5% CBR)

5.91% LRE (Leverage Ratio Exposure)

MREL own funds and eligible liabilities (~€15bn as ofDec21) @ 31.3% of RWAs with a surplus of 9.4% of RWAs

No subordination requirement for 2022: as of Dec21, CET1

and sub bonds (including SNP) totalling 21% of RWA, 95%of MREL requirement

SNP and T2 issuance of €500m in Jan 20 (SNP), €250m inNov 20 (T2) and €500m in Sept 21 to optimize capitalstructure in view of T2 expiring (€0.4bn expired in June 21and € 0.5bn due in Apr 23)

MREL liabilities vs 2022 MREL requirement

Funding & Treasury - Funding: structure & evolution Section 3.1

MREL

MREL Eligible

liabilities

31.12.2021

2022 MREL req. Subordination Stack

Own Funds

and Sub Liab

21%MREL Req

21.85% RWA

MREL Liabilities:

31.3%RWA

Sub stack

21%

MREL

Surplus

9.4%

95% of MREL Req

covered by Sub

Liab and Own

Funds

CET1:15.4%

Sub: 3.5%

Senior

bonds:

10.5%

SNP: 2.1%

31

RECENT PUBLIC OFFERS AMONG INSTITUTIONAL INVESTORS

MB public bonds placed to institutional investors since July 2019

Allocation by geography

1) Final maturity of Class A1, A2 and B Notes is October 2036. The WAL of Class A1 Notes is 2.27 years2) Referred to Class A1 Notes

Allocation by investor type

Funding & Treasury - Funding: structure & evolution Section 3.1

Italy

31%

Germany, AU

& CH

27%

France

19%BeNeLux

2%

UK & Ireland

9%

Iberia

7%

Nordics

3%

Others

2%

Banks &

Private Banks

32%

Asset

Managers

53%

CBs & OIs

11%

Insurance & PFs

3%

Others

1%

Issue date Bond type Tenor Amount (€m) Spread at issue Subscription rate

Jul-19 Covered long 7Y 750 MS+53bps ~2.3x

Jul-19 Senior Preferred 6Y 500 MS+137bps >2.7x

Nov-19 ABS n/a1 600 3mE+57bps2 >1.5x

Dec-19 Senior Preferred long 6Y 500 MS+103bps ~1.9x

Jan-20 Senior Non-Preferred long 5Y 500 MS+130bps >8.0x

Sep-20 Senior Preferred Green 7Y 500 MS+135bps >7.0x

Nov-20 Tier 2 10NC5 250 MS+280bps >9.0x

Jan-21 Covered 10Y 750 MS+13bps >2x

Sep-21 Senior Non-Preferred 7NC6 500 MS+100bps ~3x

Jan-21 Senior Preferred 7.5NC6.5 500 MS+90bps 1.8x

32

MEDIOBANCA INAUGURAL GREEN BOND

Mediobanca Inaugural Green 7-years € 500m Senior Preferred Issuance:

CSR targets are key elements of MB Strategic Business Plan 19-23 and the publication of the Green and Sustainable Bond Framework in June 2020 represents a key pillar of our ESG strategy

The inaugural green transaction has been focused towards the achievement of SDG 7 (Affordable Clean Energy), SDG 11(Sustainable Cities and Communities)and SDG 13 (Climate Action)

Total size of eligible green projects at the date of the issuance was € 528m, with residual maturity of 8.7 years

Breakdown of assets included in the green pool: 65% corporate loans, 26% retail mortgages, 9% consumer credit

Thanks to Mediobanca strategic ESG goals and ambitions, the transaction saw a meaningful participation from SRI investors, demonstrating a clear sign of appreciation for the newly established framework

In terms of pool evolution since the bond issuance (July 20 - June21): eligible assets financed increased by 38%, with Sustainable Mobility, Renewable Energy and Green Buildings as main green categories1

Transaction Highlights

Bond Type Senior Preferred Green

Pricing Date Sept 1st, 2020

Tenor 7 years

IPT Mid swap +165bps

Re-offer spread Mid swap +135bps

Amount € 500m

ISIN XS2227196404

Use of ProceedsRe-financing of eligible

Green Assets

NIP -8bps

Over-subscription ~7.0x

25%

15%

15%

14%

10%

10%

5% 6%

Allocation by Geography

France Ger&Austria

Italy UK

Nordics Iberia

Swiss Others

61%

25%

10%

3% 1%

Allocation by Investor Type

Funds Banks

CBs & OIs Insurance & PF

Others

1) Green Bond Report published in September 2021 and available here:https://www.mediobanca.com/en/investor-relations/financing-rating/green-and-sustainable-bond-framework.html

Funding & Treasury - Funding: structure & evolution Section 3.1

33

MEDIOBANCA SNP AND TIER2: RECENT ISSUANCES

Recent institutional Tier 2 and SNP issuances aimed at optimizing the capital structure, managing actively the evolution in regulatory and rating methodologies and increasing efficiency with callable structure

Market Feedback: all transactions priced inside FV. Both SNP issued with ca -5bps concession and T2 -35/40bps. Granular and well diversified order books, with significant distribution outside Italy

SNP (06/09/2021) Tier 2 (16/11/2020) SNP (16/01/2020)

ISIN XS2386287689 XS2262077675 XS2106861771

Issue Rating (M/S/F) Baa3/BBB-/BBB- Ba1/BB+/BB+ Baa3/BBB-/BBB-

Tenor (Y) 7 nc 6 10 nc 5 5

IPT Mid swap +125/130bps Mid swap +345bps Mid swap +160bps

Re-offer spread Mid swap +100bps Mid swap +280bps Mid swap +130bps

Amount € 500m € 250m € 500m

Coupon/Yield 0.75% / 0.75% 2.3% / 2.354% 1.125% / 1.157%

NIP -5bps -35/40bps -5bps

Over-subscription (final) ~3.2x ~9.0x ~8.0x

By Geography By Investor Type

23%

27%17%

14%

6%

6%5%

2% Italy

France

Germany & Austria

UK

Iberia

Swiss

Others

BeNeLux

72%

21%

3%3%

1% Fund Managers

Banks & PBs

Insurance & PFs

Central Banks & OIs

Others

Funding & Treasury - Funding: structure & evolution Section 3.1

34

MEDIOBANCA COVERED BONDS

Mediobanca €10bn Soft Bullet Covered Bond program, placed to investors:

UCITS and CRR Compliant, recently upgraded to AA Outlook Stable from Fitch;

The cover pool is composed by first lien Italian residential mortgage loans with an average size of €95k;

As of 31 December 2021, covered bonds outstanding amount is €4.5bn; 0.027% of the loans are in 90+ arrears;

In January 2021 Mediobanca issued the first Italian Covered Bond offering a negative yield.

Portfolio characteristics (31 December 2021)

Total Current Balance €6.142m

Average outstanding Balance €95k

No. of loans 64k

WA Seasoning 64.2 months

WA Remaining Term 229.8 months

No. of borrowers 64.3k

WA OLTV 65%

WA CLTV 55%

WA Margin (%) Variable loans 1.92

1) €250m tap launched in December 2015; 2) €250m tap launched in September 2018

Funding & Treasury - Funding: structure & evolution Section 3.1

ISIN Currency Outstanding amount (m) Rating (Fitch) Coupon Issue Date Maturity Date

IT0004966716 EUR 750 AA 3.625% Oct-13 Oct-23

IT0005142952 EUR 750 AA 1.375% Nov-151 Nov-25

IT0005315046 EUR 750 AA 1.25% Nov-17 Nov-29

IT0005339186 EUR 750 AA 1.125% Jul-182 Aug-24

IT0005378036 EUR 750 AA 0.50% Jul-19 Oct-26

IT0005433757 EUR 750 AA 0.01% Jan-21 Feb-31

50.3%48.0%

1.7%

Fixed rate

Floating rate

Floating rate

with Cap

4.1%

16.7%

32.1%

47.1%

0.1%

0-20

20-40

40-60

60-80

>80

CLTV distribution

Interest type

35

ABS (CONSUMER AND SALARY GUARANTEED LOANS)

Quarzo S.r.l. – Serie 2018 Quarzo CQS S.r.l. – Serie 2018

Quarzo 2018 is a securitization of consumer

loans originated to Italian borrowers by

Compass. The transaction factors in a 6-

months revolving period starting from Jan-

19. The issue was divided into three classes,

Class A1 offered to the market and Class

A2 and Class B retained by the Originator

Originator: Futuro S.p.A.

Collateral type: Italian Secured Consumer Loans

Total size of Class A: €598m

Announcement date: 20 March 2018

Settlement date: 27 March 2018

First payment date: 18 April 2018

Coupon: 1mE+37bps

Yield at issue: 1mE+37bps

Issue price: 100.00%

Listing: Irish Stock Exchange

ISIN (Class A): IT0005328312

Minimum denomination:

€100K + €1K

Mediobanca’s role:Sole Arranger & Joint Lead Manager

Quarzo CQS 2018 is a static cash

securitization of salary and pension

assignment loans originated to Italian

borrowers by Futuro S.p.a. The purchase of

the portfolio has been financed through

the issuance of a senior (Class A) and a

junior note. The Class A note has been

placed on the market

Mediobanca through its subsidiary Compass S.p.a. (Compass) has originated several structured finance transactions collateralized by consumer loans, the Quarzo S.r.l. series: the latest marketed ABS was priced in November 2019 and the current outstanding amount of the placed Class A1 notes of Quarzo series is ~€370m1

Starting from 2015, Mediobanca has placed on the market two salary guaranteed loans transactions originated by Compass’ subsidiary Futuro S.p.a. (incorporated in Compass in 2020), through the SPV Quarzo CQS S.r.l. The current Class A outstanding

amount for Serie 2018 is ~€96m1

Quarzo S.r.l. – Serie 2019

Quarzo 2019 is a securitization of consumer

loans originated to Italian borrowers by

Compass. The transaction factors in a 6-

months revolving period starting from Dec-

19. The issue was divided into three classes,

Class A1 offered to the market and Class

A2 and Class B retained by the Originator

Originator: Compass Banca S.p.A.

Collateral type: Italian Consumer Loans

Total size of Class A: €600m

Announcement date: 28 November 2018

Settlement date: 6 December 2018

First payment date: 15 January 2019

Coupon: 3mE+95bps

Yield at issue: 3mE+95bps

Issue price: 100.00%

Listing: Irish Stock Exchange

ISIN (Class A1): IT0005348989

Minimum denomination:

€100K + €1K

Mediobanca’s role:Sole Arranger & Joint Lead Manager

Originator: Compass Banca S.p.A.

Collateral type: Italian Consumer Loans

Total size of Class A: €600m

Announcement date: 7 November 2019

Settlement date: 25 November 2019

First payment date: 15 January 2020

Coupon: 3mE+70bps

Yield at issue: 3mE+57bps

Issue price: 100.30%

Listing: Irish Stock Exchange

ISIN (Class A1): IT0005389264

Minimum denomination:

€100K + €1K

Mediobanca’s role:Sole Arranger & Joint Lead Manager

Funding & Treasury - Funding: structure & evolution Section 3.1

1) As of 31 December 2021

AGENDA

1. MB Group profile

2. 1H22 Results

3. Funding & Treasury

3.1 Funding: structure & evolution

3.2 Treasury: structure & evolution

Annex

1. ESG profile

2. 12m figures as at June 21

37

Client&Other

2.5

Trading

book

0.3

Liquidity

3.4

BB govies

5.3

BB bonds

2.6

CAUTIOUS ASSET & LIABILITIES MANAGEMENT

MB Group net treasury assets* (€bn) MB Group treasury assets* breakdown (Dec21)

8.4

11.8 12.09.2 8.7 9.9

8.4 7.7 6.7 6.8 7.1 7.9

8.6

9.3 8.2

9.3

5.05.6

7.3

4.95.5 6.2 6.4

6.2

J-11 J-12 J-13 J-14 J-15 J-16 J-17 J-18 J-19 J-20 J-21 D-21

Banking book Liquidity and HFT

14.1

Total €14.1bn

Net treasury assets: €14.1bn; ~55% banking book govies and corporate bonds, ~45% liquidity/low risk client business

Fixed income banking book at €7.9bn, ~2/3 represented by Govies, 60% of which are Italian

High liquidity: €3.4bn, o/w €2.8bn cash and liquidity at ECB

* Sum of: financial asset/liabilities held for trading, treasury financial assets/liabilities, banking book securities, excluding banking book equities

Italy 60%

Germany 17%

Other 22% Corporate

15%

Financials

85%

Treasury: structure & evolution Section 3.2

38

LOW SOVEREIGN EXPOSURE AND DURATION OF IT GOVIES

Banking book government bonds…by geography

Italian govies exposure confirmed low at €3.2bn (or

43% of CET1 capital) out of €5.3bn, o/w ~40% classified

as HTC

IT govies avg duration 3Y

Low sensitivity of CET1 to rates:

+50bps rates = ~5bps neg. impact on CET1

7.1

5.6 5.44.6 4.7

5.4 5.35.1

3.32.7

2.2

3.3 3.5 3.2

June16 June17 June18 June19 June20 June21 Dec21

Total Govies IT Govies

Treasury: structure & evolution Section 3.2

€m 20222023-

2026

2027-

2030Beyond Total

Italy 533 2,036 418 200 3,186

Germany 267 655 - - 922

France 351 - - - 351

Spain 100 - - - 100

US 441 57 - - 499

Other - 214 - - 214

Total 1,691 2,963 418 200 5,273

…and maturities

Book value (€bn) % CET1

Total Govies (Dec21) 5.3 72%

Italy 3.2 43%

- HTC 1.3 18%

- HTCS 1.8 25%

Germany 0.9 13%

France 0.4 5%

US 0.5 7%

Other 0.3 4%

39

BBB

22%

BB

76%B and

below

2%

BANKING BOOK BOND PORTFOLIO

Italy

71%

Benelux

3%Fra/Ger

8% US/UK

6%

Other

11%

AAA/AA

14%

A

35%

BBB

10%BB

31%

B and

below

9%NR

0.4%

AAA

13%

AA

3% A

42%

BBB

8%BB

23%

B and

below

10%

NR

0.4%

€0.4bn €2.2bn

Non Financials (15%) Financials (85%) Total (Dec21)

€2.6bn

€0.4bn €2.2bn €2.6bnItaly

75%

Benelux

3%

Fra/Ger

6%US/UK

4%

Other

13%

BB corporate bond portfolio at €2.6bn (~85% Financials, ~15% Non Financials), well diversified in terms of geographies

Non Financials: ratings concentrated mainly in the BB/BBB areas (76%/22%)

Financials: investment grade representing 66%, 89% IG+BB rating

Treasury: structure & evolution Section 3.2

Italy

53%

Benelux

5% Fra/Ger

22%

US/UK

17%

Other

4%

AGENDA

1. MB Group profile

2. 1H22 Results

3. Funding & Treasury

3.1 Funding: structure & evolution

3.2 Treasury: structure & evolution

Annex

1. ESG profile

2. 12m figures as at June 21

41

ESG DEVELOPMENT: STRATEGY, REPORTING AND COMPLIANCE …FOUNDATION AND DEVELOPMENT OF GROUP SUSTAINABILITY

2016-2017

2017-2018

2018-2019

Group

Sustainability unit

Group

Sustainability

management

Committee

Group

Sustainability Policy

First Materiality

Matrix

First Group

sustainability

reporting

Directive on

responsible

investing

Multi-stakeholder

forum to update

materiality matrix

Signed up to UN

Global Compact

First Consolidated

Non-Financial

Statement

New Policy on

responsible

lending and

investing

Responses to

leading ESG Index

questionnaires

E-learning course

on Sustainability

and Human Rights

Second

Consolidated Non-

Financial

Statement

CSR objectives in

the 2019-23

Strategic Plan and

in the LTI for top

mngt.

BoD CSR

Committee

Revised Group

Sustainability Policy

Signed up to

Principles for

Responsible

Investing

Third Consolidated

Non-Financial

Statement

2019-2020 CSR objectives in

the STI for top

mngt.

Revised Group

ESG Policy

Assessment of

SASB1 requests

Signatory to PRB -

Principles for

Responsible

Banking

Assessment for

aligning to the

requests of TCFD2

Implementing a

plan to respond to

the new EU ESG

regulatory context

2020-2021

1) Sustainability Accounting Standards Board is a US non-profit organization whose mission is to develop and disseminate sustainability reporting standards that help

companies disclose material and useful information to investors in order to make decision

2) Task Force on Climate-related Financial Disclosures

Signatory to the

Net-Zero Banking

Alliance

2021-2022

ESG profile Annex 1

42

…RELYING ON A STRONG GOVERNANCE

BoD committees

Board of Directors

Risks Committee

Remunerations

Committee

AppointmentsCommittee

CEO

General Manager

Executive Committee

Management committees

Group Sustainabilitymanagement

Committee

MembersAlberto Nagel (CEO)Giovanna Giusti del Giardino (Head of Group Sustainability) Top management of the Group staff and business activities

CSR Committee

ChairmanAlberto Nagel (CEO)MembersVirginie BanetMaximo IbarraAngela GambaElisabetta Magistretti

Related parties Committee

CEO in charge of sustainability.

Corporate Social Responsibility

Committee (including the CEO

and 3 independent BoD

members) has responsibility for

prior analysis of sustainability

issues to be submitted to the

BoD.

The Group Sustainability

Management Committee

remains responsible for defining

policies and implement

practices within the Group

Green and Sustainable Bond

Committee is composed by

Group Treasury, ESG team, CIB

division and all relevant legal

entities that contribute to the

origination of the Eligible Assets Green and Sustainable Bond Committee

ESG profile Annex 1

43

OUR SUSTAINABLY PRIORITIES ARE REFLECTED …

ENVIRONMENT & CLIMATE CHANGE

BRIBERY & CORRUPTION

DIVERSITY & INCLUSION

HUMAN RIGHTS

The Group Policy, in line with the principal international standards and declarations, is sub-divided into four areas held to be

priorities: measures to tackle bribery and corruption, human rights, diversity and inclusion and environment and climate

change with the objective of driving improvement in the Group’s conduct and direct impact in all these areas.

We promote diversity as a value that forms the basis of personal growth and cultural and professional

enrichment

We are committed to conducting our business in accordance with the highest ethical standards and

we do not tolerate any form of corruption, whether active or passive

We believe that respect of human rights is a fundamental prerequisite to our own sustainability

We are sensitive to the need to protect the environment, and climate change, as the primary

resource of human well-being

ESG profile Annex 1

44

… IN OUR EVOLVING GROUP INVESTMENT POLICY…NEW ESG POLICY RELEASED IN JULY 2021 AND EFFECTIVE STARTING FROM OCTOBER THE 1ST

Group Policy on responsible lending and

investing

The policy applies to lending activities, investment of own funds and advisory

services on investments provided to clients by the Mediobanca Group, pursuing

an approach which is based on a combination of:

Negative screening through use of exclusion criteria, to identify companies

involved in specific activities which therefore cannot be taken into

consideration for lending, investment and advice processes

Positive screening based on precise inclusion criteria to identify companies that

are committed to ESG issues

Reviewed

in July 21

New Group ESG Policy

The new policy:

widen the application spectrum (covering ECM, DCM, Corporate finance

advisory to CIB clients)

articulate more precisely negative and positive screening for all business areas

include a policy to protect biodiversity as well as specific lists of exclusion

criteria for lending and principal investment applicable to ESG sensitive sectors

(mining, forestry and use of forested areas, production of agricultural goods,

the energy sectors, defence and arms, and infrastructure and transport,

excluded materials)

ESG profile Annex 1

45

Mediobanca SGR, RAM Active Investment and Cairn Capital are signatories to the Principles for Responsible Investment

(PRI) launched by the United Nations in 2006 set up to promote a sustainable and responsible approach to investment by

institutional investors

… AND IN OUR AM BUSINESS

Mediobanca SGR has adopted a Policy on

responsible investments, considering the

integration of environmental, social and

governance criteria within the investment

processes as a priority

RAM adopted a Policy for responsible

investing setting out the investment beliefs,

the guidelines, and the approach to

consider and incorporate ESG factors into

investment process and strategies and a

Policy on climate change, to tackle climate

change risks through investment decisions

and direct or collaborative engagements

Cairn Capital has adopted an ESG policy

based on negative, top-down screening to

exclude companies operating in certain

sectors, combined with a bottom-up

approach to evaluating investments based

on ESG criteria specific to each asset

Mediobanca Social Impact

is a fund for philanthropic purposes, which has been developed in partnership with some of the leading Italian charitable which

receive a recurring devolution

CMB - MonactionInternational ESG fund

which invests in international equities based on robust

environmental, social and governance criteria for its

sector

RAM Stable Climate Global Equities Fund

a fund set up with the aim ofaddressing the climate emergency by offering

investors an active strategy based on solid ESG

principles

Some ESG products

and services

ESG profile Annex 1

46

EU REGULATIONS PROGRESSIVELY INTEGRATED …

GOVERNANCE

Task-Force Steering Committee

DISCLOSUREPOLICIES ANDPROCEDURES

Group ESG policies and website disclosure

BUSINESS STRATEGY

ESG products and services

RISKMANAGEMENT

ESG risks integration in lending and

investment processes

IMPACT ON REAL ECONOMY

Business/impact oriented approach to the integration of ESG Regulation changes

Mediobanca has set up a dedicated task force transversal to the main Group functions and legal entities impacted by the new European regulations with the aim of complying by the required times and methods

The task force is governed by a dedicated Steering Committee whose members cover different business areas and are committed to integrate regulation evolution and translate it into a new way of making business

Regulation

Taxonomy

ECB Guide on climate

related and environmental

risks

Sustainablefinance

disclosureregulation

ESG profile Annex 1

47

… WITH STRONG COMMITMENT TO FURTHER ESG DEVELOPMENT

Starting from FY22 CEO and GM STI include quantitative ESG targets (qualitative were already present).

For FY22 such targets include metrics related to ESG corporate loan book, ESG consumer loan new production

and ESG funds within clients’ portfolio.

DISTRIBUTION

CheBanca!: as at June 2021 €2.2bn (equal to almost 34% of the assets invested by clients in funds) was invested in funds ex SFDR art.8 and art.9.

MB Private Banking: as at June 2021 €127mln (equal to more than 20% of the assets invested by clients in funds) was invested in funds ex SFDR art.8 and art.9.

Procedure started to include ESG criteria in investment evaluation

RAM – as at June 2021 80% of the AUM was ex SFDR art.8 and art.9.

MB SGR - 3 ESG funds (ESG European Equity, ESG US Equity & Social Impact totaling €354mln as at June 2021) representing 15% of managed funds ex SFDR art.8.

ASSET MANAGEMENT

CORPORATE LOANS

Mediobanca has syndacated several ESG credit lines for domestic (including Enel, Inwit, Nexi) and international corporates (including Ramsay-GDS).

As at June 2021 CIB corporate loan book with green/ESG features totaled €1.5bn (10% of the total corporate loan book).

RETAIL LOANS

Consumer: new green production doubled YoY to €71mln. The green stock totaled €87mln as at June 2021.

Mortgages: green loon book totaled €159mln as at June

2021 (5X YoY).

ESG profile Annex 1

48

Transport &

infra

29%

Industrial goods

19%

Consumer

goods

19%

Telco&media

9%

Oil & gas

8%

Financials

6%Other

10%

CIB LOAN BOOK BY INDUSTRY

20%

9% 9%8% 7%

6%5%

3% 3% 3% 3% 3% 2% 2% 2% 2%

14%

WB loan book by sector (€16.6bn as at June21)

1. “Other” includes sectors with exposure each below 2%: Building Materials, Construction, Containers&Packaging, Services , Gaming, Healthcare,

Infrastructure, IT, Lodging&Leisure, Luxury, Metal, Paper, Restaurants&Catering, Retail non-Food, Transportation and other residual sectors

2. Investment grade (IG) including rating classes from AAA to BBB-, crossover including BB+ rating bucket

WB loans : €16.6bn, 34% of MB Group loans:

High quality portfolio with large-export oriented corporate clients and well diversified among sectors

Rating distribution: 60% IG, 13% crossover2

ESG loans: ~10% of total WB portfolio (€1.5bn)

Gas

17%

Pure

renewables

16%

Integrated

utilities

(Transportation

& Distribution)

43%

Oil

23%

Energy sector exposure by power source

(~€1bn as at June21)Energy exposure:

~€1bn, 7% WB loans and 2% MB Group loans

16% pure renewables

43% energy transportation & distribution

Just one exposure with coal generation (<7%, phasing-out)

No exposure to mining and coal mining sectors

ESG loans by sector

(€1.5bn as at June21)

ESG profile Annex 1

49

ESG

POLICY

INTERNATIONAL PRINCIPLES AND STANDARDS

SUSTAINABILITY

POLICY

17 UN Sustainable Development Goals (SDGs)

UN Principles for Responsible Banking (“PRB”)

UN Global Compact principles

In recent years the Mediobanca Group has signed up to the most important international principles and standards

Net Zero Banking Alliance

UN Principles for Responsible Investment (“PRI”)

NEW

ESG profile Annex 1

50

MEDIOBANCA – ESG INDEXES AND RATING1

Corporate rating: C (2^ decile)

Governance: 2

Environment: 2Social: 1

81 2 3 4 5 6 7 9 10lower risk higher risk

A B C+ C C- Dexcellent medium low

81 2 3 4 5 6 7 9 10high relative perf. (decile) low

S EG

Rating A

Mediobanca score: 4.9

Industry-adjusted score: 7.0

AAA AA A BBB BB Bexcellent medium low

CCC

Rating: 16/100 - low riskIndustry rank: 76/920

(Diversified Financials)

Subindustry rank 1/122(Investment Banking and Brokerage)

negligible low medium high severe

0-10 10-20 20-30 30-40 >40

ESG risk exposure: 41,9

ESG risk management: 64,4

low medium high

0-35 35-55 >55

low medium strong

0-35 35-55 >55

Rating C

A A- B B- C C-Leadership management awareness disclosure

D D-

Rating EE-

Outlook: positive

EEE

EEE-

EE+

Compliant

Non compliant

Negative

EE

EE-

E+

E

E-

F-

2021

Included in the index

Included in the index

(percentile rank: 77)

Environment: 2,0 Social: 3,8

Governance: 4,6

0 1 2 3 4 5weak strong

SE G

Environment: 59Sector average performance: 42

Social: 57Sector average performance: 42

Governance: 67Sector average performance: 44

weak limited robust advanced

0-29 30-49 50-59 60-100

Rating: 60/100 Rank in sector: 6/96

Rank in region: 161/1,624

Rank in Universe: 180/4,952

Performance leve:

ESG profile Annex 1

Not included in the index1

Score Mediobanca: 64Average score: 39

S&P Europe 350 ESGIncluded starting from April 2021

1) Updated as at 9 December 2021

Included in the 2022

Sustainability Yearbook

AGENDA

1. MB Group profile

2. 1Q22 Results

3. Funding & Treasury

3.1 Funding: structure & evolution

3.2 Treasury: structure & evolution

Annex

1. ESG profile

2. 12m figures as at June 21

52

MEDIOBANCA GROUP A&L

1) YoY=June21/June20; QoQ=June21/Mar212) CET1 Phase-in. CET1 FL @15.1% (without Danish Compromise 110 bps and with IFRS 9 fully phased 13bps)

12m figures as at June 21 Annex 2

€bn June21 Mar21 Dec20 Sept20 June20∆

QoQ1∆

YoY1

Funding 56.2 56.6 55.9 56.7 54.9 -1% +2%

Bonds 18.4 19.0 18.7 19.3 18.8 -3% -2%

Direct deposits (retail&PB) 25.2 25.2 24.6 24.2 23.8 +0% +6%

ECB 7.4 7.0 6.2 6.5 5.7 +7% +32%

Others 5.1 5.4 6.4 6.7 6.7 -6% -24%

Loans to customers 48.4 47.7 48.1 46.8 46.7 +2% +4%

CIB 19.3 18.9 19.5 18.6 18.6 +2% +3%

Wholesale 16.6 16.3 16.8 16.5 16.5 +2% +0%

Specialty Finance 2.7 2.5 2.7 2.1 2.1 +7% +28%

Consumer 12.9 12.8 12.8 12.9 13.0 +1% -1%

WM 14.4 14.3 14.0 13.5 13.2 +1% +9%

Mortgage 11.1 10.9 10.7 10.4 10.2 +2% +8%

Private banking 3.3 3.4 3.3 3.1 2.9 -1% +13%

Leasing 1.8 1.8 1.8 1.8 1.8 -1% -3%

Treasury and securities at FV 14.4 15.3 13.8 15.7 13.8 -6% +5%

RWAs 47.2 47.7 48.7 47.6 48.0 -1% -2%

Loans/Funding ratio 86% 84% 86% 83% 85%

CET1 ratio (%)2 16.3 16.3 16.2 16.2 16.1

TC ratio (%) 2 18.9 19.0 19.0 18.8 18.8

53

12M RESULTS BY DIVISION AS AT 30 JUNE 21

12m- June21 (€m)Wealth

ManagementConsumerBanking

CIBPrincipal Investing

Holding Functions

Group

Net interest income 281 879 287 (7) (47) 1,415

Net treasury income 10 - 93 31 58 197

Net fee and commission income 336 123 318 - 12 745

Equity-accounted companies - - - 272 - 272

Total income 627 1,002 698 295 22 2,628

Labour costs (241) (104) (165) (4) (121) (635)

Administrative expenses (231) (210) (141) (1) (39) (603)

Operating costs (472) (314) (307) (5) (160) (1,238)

Loan loss provisions (19) (258) 40 - (13) (249)

Provisions for other financial assets 2 - 2 52 (8) 48

Other income (losses) 4 (15) 1 - (74) (86)

Profit before tax 143 415 434 343 (232) 1,104

Income tax for the period (42) (136) (147) (34) 68 (292)

Minority interest - - (3) - (2) (4)

Net profit 100 279 285 309 (166) 808

Customer loans 14,405 12,943 19,292 - 1,774 48,414

RWAs 5,217 11,779 19,925 7,246 2,992 47,159

No. of staff 2,037 1,446 635 11 792 4,921

12m figures as at June 21 Annex 2

54

INVESTOR CONTACTS

Mediobanca Group

Investor Relations

Piazzetta Cuccia 1, 20121 Milan, Italy

Jessica Spina Tel. no. (0039) 02-8829.860

Luisa Demaria Tel. no. (0039) 02-8829.647

Matteo Carotta Tel. no. (0039) 02-8829.290

Marcella Malpangotto Tel. no. (0039) 02-8829.428

Email: [email protected]

http://www.mediobanca.com