mercatus tax lecture

DESCRIPTION

TRANSCRIPT

Principles of Tax Reform

Dr. Jason J. FichtnerSenior Research Fellow

Mercatus CenterMercatus CenterApril 19, 2011

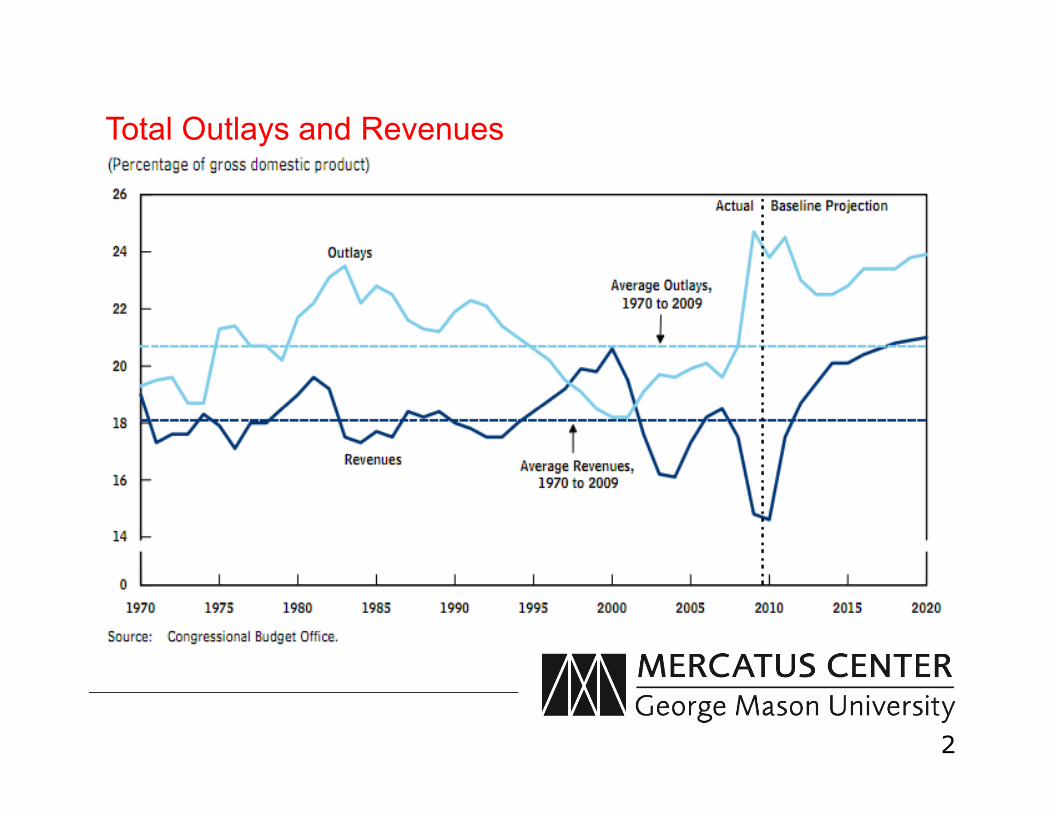

Total Outlays and Revenues

2

Congressional Budget Office - Budget Surplus/Deficit

Source: Congressional Budget Office

3

Federal Revenues by Fiscal Year

Source: CBO

4

Taxes – What you don’t know can cost you

$$$

5

How do we evaluate tax policy?� Why is tax policy important?

� What are the main tools used to evaluate tax policy?

� Estimates of Macroeconomic Effects

� Revenue Tables

� Tax Distribution Tables

� How do we evaluate tax policies?

� Efficiency, Simplicity (Complexity), Equity (Fairness)

� What is Fairness?

� Horizontal versus Vertical Equity� Horizontal versus Vertical Equity

� Generational Equity

� Point of Payment versus Incidence

� Direct vs. Indirect Taxes

� Importance of Marginal Rates vs. Effective Rates

� Inclusive Rate vs. Exclusive Rate (23% NRST vs. 30%)

� What is the tax base? Wider base and lower rates more efficient

� Social policy – tax expenditures versus government programs

� Taxes distort behavior

� Only PEOPLE can pay taxes!!!

6

What is a Distribution Table?

Example of Basic Distribution Table -

Average Tax Change

Present Law Proposed Law

$ (millions) Percent Percent Percent

Less than $10,000 -20 -0.2 7.1 7.0 -300

Income CategoryChange in Federal Taxes

Effective Tax Rate

$

10,000 to 20,000 -365 -1.0 8.1 8.0 -400

20,000 to 30,000 -1,300 -1.5 15.2 15.0 -500

30,000 to 40,000 -2,150 -1.9 17.6 17.3 -750

40,000 to 50,000 -2,750 -2.1 19.3 18.9 -1,100

50,000 to 75,000 -7,200 -2.3 21.2 20.7 -1,500

75,000 to 100,000 -6,600 -2.4 23.9 23.2 -2,000

100,000 to 200,000 -8,100 -2.2 26.2 25.5 -3,500

200,000 and over -13,500 -3.1 29.2 27.6 -5,000

Total, all taxpayers -$41,985 -2.4% 22.2% 21.5% -$650

7

Why Are Distribution Tables Important to

Tax Policy Debates

Graphics: (1) Wall Street Journal, 10/05/00 & (2) New York Times, 1/14/03

8

How Inclusion/Omission of Data Can Lead to Different Perceptions of

Fairness

Slide 1

9

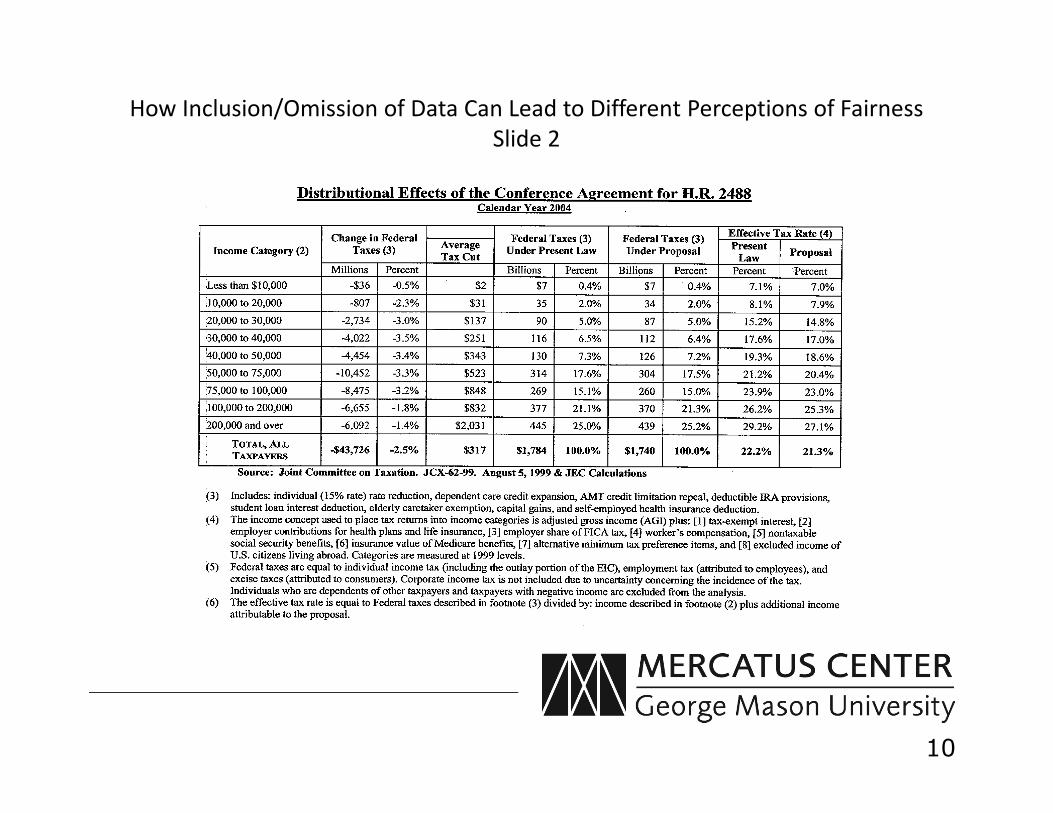

How Inclusion/Omission of Data Can Lead to Different Perceptions of Fairness

Slide 2

10

How Inclusion/Omission of Data Can Lead to Different Perceptions of Fairness

Slide 3

11

Distribution of Tax Burden

Percentage of Federal Personal Income Tax Paid by Different

58.72%

69.94%

86.34% 97.30%100 %

90 %

80 %

60 %

70 %

50 %

Source: Department of the Treasury, Internal Revenue Service

12

Top1%

Top5%

Top10%

Top25%

Top50%

Bottom50%

38.02%

2.70%

20 %

40 %

50 %

30 %

10 %

Percentage of Federal Personal Income Tax Paid by Ranked AGI Percentiles

Percentiles Ranked by AGI

Adjusted Gross Income Threshold on Percentiles

Percentage of Federal Personal Income Tax

PaidPercentage of Federal

Adjusted Gross Income

Top 1% $380,354 38.02% 20.00%

Top 5% $159,619 58.72% 34.73%

13

Top 10% $113,799 69.94% 45.77%

Top 25% $67,280 86.34% 67.38%

Top 50% $33,048 97.30% 87.25%

Bottom 50% < $33,048 2.70% 12.75%

Source: IRS (Tax Year 2008)

Distribution of Tax BurdenTax Shares by AGI: 2000 and 2005

84.0%

67.3%

56.5%

86.0%

70.3%

59.7%

50%

60%

70%

80%

90%

100%

Tax Year 2000

Tax Year 2005

Source: Department of the Treasury, Internal Revenue Service

3.9%

37.4%

3.1%

39.4%

0%

10%

20%

30%

40%

Bottom 50 percent Top 25 percent Top 10 percent Top 5 percent Top 1 percent

14

70.2

60

80

100

Distribution of Tax Burden: Current

Policy Baseline Law

Percent of

0.4 2.4

8.5

18.5

0

20

40

Lowest Quintile Second Quintile Third Quintile Fourth Quintile Highest Quintile

Source: President’s Advisory Panel On Tax Reform, Staff Presentation,

July 20, 2005 - Department of the Treasury, Office of Tax Analysis

Note: Estimates of 2006 law at 2004 income levels.

Percent of

federal

taxes paid

15

64.0

69.071.7

60

80

100

Flat Tax

Modified Flat Tax

Modified Flat Tax with top tax expenditures

Distribution of Tax Burden:

Flat Tax Proposals

Percent

0.73.7

10.5

21.0

0.32.6

9.2

18.7

0.3 2.1

8.1

17.6

0

20

40

Lowest Quintile Second Quintile Third Quintile Fourth Quintile Highest Quintile

Percent

of federal

taxes paid

Source: President’s Advisory Panel On Tax Reform, Staff Presentation,

July 20, 2005 - Department of the Treasury, Office of Tax Analysis

Note: Estimates of 2006 law at 2004 income levels. 16

Distributional analysis: National Sales

Tax with Prebate

70.2 69.3

40

60

80

100

Current law

Sales tax with prebate

Percent

0.4 2.4

8.5

18.5

-2.5

2.0

10.1

21.0

-20

0

20

40

Second Quintile Third Quintile Fourth Quintile Highest Quintile

Lowest Quintile

Percent

of federal

taxes paid

Source: President’s Advisory Panel On Tax Reform, Staff Presentation,

July 20, 2005 - Department of the Treasury, Office of Tax Analysis

Note: Estimates of 2006 law at 2004 income levels. 17

How the “Design” of Tax Policy Can Influence Results &

Bias Debate

� Different Measures of Income

�AGI v. FEI

� Variables to Include / Exclude

�Tax Cut Amount, Change in Effective Tax Rate, Change in

After-tax Income, Change in Taxes Paid, Tax Shares

18

After-tax Income, Change in Taxes Paid, Tax Shares

� Rates vs. Base

� Assumptions of Tax Incidence

� Tax Expenditures

� What’s the One Key Thing to Remember?

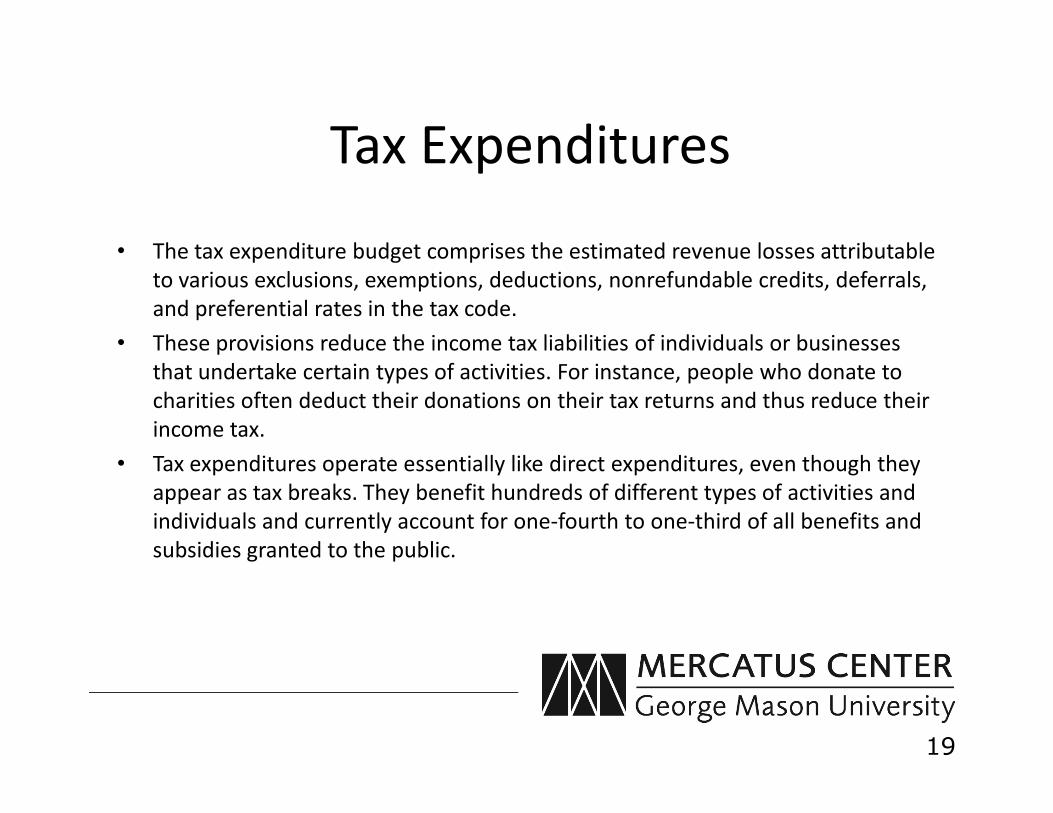

Tax Expenditures

• The tax expenditure budget comprises the estimated revenue losses attributable

to various exclusions, exemptions, deductions, nonrefundable credits, deferrals,

and preferential rates in the tax code.

• These provisions reduce the income tax liabilities of individuals or businesses

that undertake certain types of activities. For instance, people who donate to

charities often deduct their donations on their tax returns and thus reduce their charities often deduct their donations on their tax returns and thus reduce their

income tax.

• Tax expenditures operate essentially like direct expenditures, even though they

appear as tax breaks. They benefit hundreds of different types of activities and

individuals and currently account for one-fourth to one-third of all benefits and

subsidies granted to the public.

19

Tax Expenditures

• The Congressional Budget Act of 1974 requires that the budget include estimates

for tax expenditures, but only for those provisions that affect the federal income

taxes of individuals and corporations. The government could, but does not,

formulate tax expenditure budgets for Social Security and other taxes.

• Both the Office of Tax Analysis in the Treasury Department and the congressional

Joint Committee on Taxation (JCT) estimate tax expenditures; the items that each Joint Committee on Taxation (JCT) estimate tax expenditures; the items that each

includes and the estimated values are generally similar but do not always match.

• The Office of Management and Budget (OMB) publishes the Treasury’s estimates

in its Analytical Perspectives volume that accompanies each year’s publication of

the Budget of the U.S. Government. Each year JCT issues estimates covering the

current and four subsequent fiscal years.

20

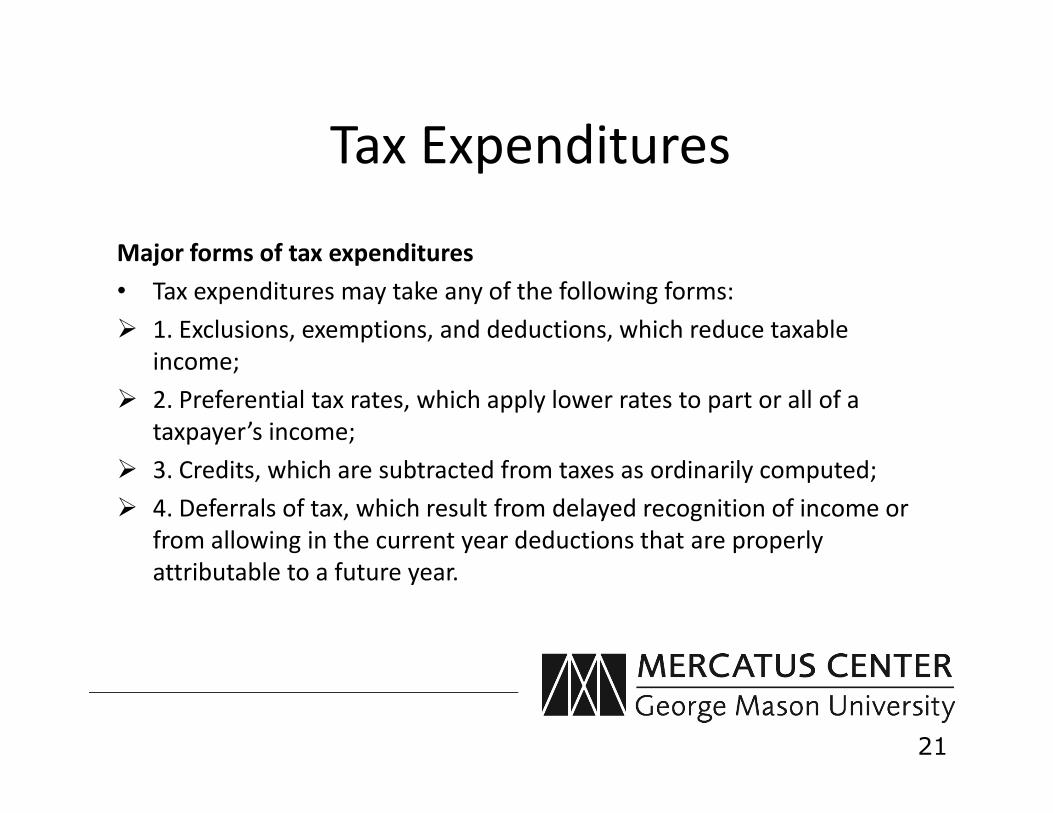

Tax Expenditures

Major forms of tax expenditures

• Tax expenditures may take any of the following forms:

� 1. Exclusions, exemptions, and deductions, which reduce taxable

income;

� 2. Preferential tax rates, which apply lower rates to part or all of a � 2. Preferential tax rates, which apply lower rates to part or all of a

taxpayer’s income;

� 3. Credits, which are subtracted from taxes as ordinarily computed;

� 4. Deferrals of tax, which result from delayed recognition of income or

from allowing in the current year deductions that are properly

attributable to a future year.

21

22http://www.whitehouse.gov/sites/default/files/omb/budget/fy2012/assets/spec.pdf

100

150

200

250

Co

un

t Count of Tax Expenditures, 1985-2009

23

0

50

Year

Source: Authors' calculations derived from the Joint Committee on Taxation annual pamphlets on tax expenditures, Estimates of Federal Tax

Expenditures for Fiscal Years (1985 - 2009), various years

1500

2000

2500

3000

3500

4000

To

tal

Am

ou

nt

(Bil

lio

ns

of

Do

lla

rs)

Combined Top 10 Individual & Top 10 Corporate Tax

Expenditures, 1975-2014(Nominal dollars)

24

0

500

1000

1500

1975-1979 1980-1984 1985-1989 1990-1994 1995-1999 2000-2004 2005-2009 2010-2014

To

tal

Am

ou

nt

(Bil

lio

ns

of

Do

lla

rs)

Years (Five Year Intervals)

Source: Authors' calculations derived from Tables 1-8 Section IV of the Joint Committee on Taxation, “Background Information On Tax Expenditure Analysis And

Historical Survey Of Tax Expenditure Estimates”, (JCX-15-11), February 28, 2011

Principles to Keep in Mind ->

Incentives Matter

�Perceived unfairness promotes system abuse

�High tax rates encourage avoidance and

evasion.evasion.

�Bad tax systems chase investors away

�Good tax systems attract investors and jobs

25

�Tax reform should fix the problem!

�Policy positions should be based on clearly articulated principles

�The validity of each decision should be checked against these principles

Principles to Keep in Mind ->

against these principles

�Long term solutions are superior to short term fixes

�The best results come from fixing everything at the same time.

�What’s the One Key Thing to Remember?

26

Any Questions???

27