north america’s leading transit bus and motor coach ... · offer the industry’s widest range of...

TRANSCRIPT

0

Forward Looking Statements and Non-GAAP Measures are defined in APPENDIX B.

NFI Investor Update Q2 -2016North America’s leading Transit Bus and Motor Coach Manufacturer and Parts Distributor

August 11, 2016

1

NFI Investment Thesis

Leading Share in Diversified

Markets

� North Americas’ #1 heavy duty transit bus brand, #1 motor coach brand and #1 aftermarket parts and service supplier

� >70,000 vehicles (transit buses and motor coaches) currently in service with~50% share of Canadian and US installed base

Deep Relationships

with High Quality Customer Base

� Founded in the 1930’s, NFI and MCI have established relationships with well nearly all domestic transit authorities and specifically 24 out of 25 of the largest agencies operate New Flyer, NABI, Orion or MCI buses or motor coaches

� Strong reputation and long standing relationship with hundreds of motor coach operators in Canada and US operating MCI or SETRA motor coaches

BroadProduct Offering with Technology

Leadership

� Leading in-house engineering and new product development capability� Integrated aftermarket parts and services operation� Compliant with Buy-America and policies regarding Canadian content� Offer the industry’s widest range of green propulsion options: diesel, natural

gas, electric trolley, diesel-electric hybrid, and now battery-electric

Experienced Team poised for

Growth & Diversification

� Successful track record of positioning the business for growth and increased profitability

� Extensive LEAN transformation and OpEx experience with proven ability to complete accretive acquisitions and achieve synergies

Strong Financial metrics

� Proven financial performance and low leverage. � Strong/Predictable cash flow to support rapid deleveraging and dividends

+

2

Company Overview

• North America’s #1 Transit Bus & Motor Coach manufacturer and parts supplier with the leading installed base of ~50% of transit buses and motor coaches currently in service (~70,000 buses)

• Public company with combined growth and yield focus. Significant Shareholders: Marcopolo S.A. =18.6%, Management/Board =1.9%).

• Fully Diluted Market Cap: ~$C 2.6B. ~ 5,000 employees in Can/US

Q2-16 LTM Highlights:

Revenue: US $1.92 B

Adj EBITDA: US $229.3 M

Return on Sales: 11.9%

Net Debt: $573 M

Leverage: 2.21 (Converts treated as Equity)

ROIC: 14.0%

FCF: US $156.3 M

Payout Ratio: 22.0%

Bus Backlog:

Firm : 3,035 EUs, $1.6 B

Options : 6,975 EUs, $3.6 B

LTM Book to-Build Ratio: 159%

Common Share (TSX:NFI)

Shares Outstanding: 59.9M

60-day average Daily Volume: ~ 305K

Dividend = C$0.95/share (1), Yield: ~2.3%(3)

TSR(2): 2016 YTD = 48% 2015 =115%

(1) Effective May 12, 2016 the Dividend increased from C$0.70 to C$0.95 per share annually.(2) Total Shareholder’s Return (“TSR”) is calculated by the growth in capital assuming the dividends are reinvested each time they are paid.(3) Calculated using closing TSX market price as at August 5, 2016

Convertible Debt (TSX:NFI.DB.U)

Principal Outstanding: US $25.8 M

60-day average Daily Volume: ~US $280K

Coupon: 6.25%, Yield: ~ 2.0%(3)

Dec 18-15: NFI added to S&P/TSX Composite Index Mar 14-16: NFI added to S&P/TSX Equal Weight Industrials Index Mar 11-16: NFI Equity Options commenced trading on Montreal Exchange

3

NFI Business Strategy

1. Offer Canadian and US operators the best buses, ser vices and value in the industry� Migrate from selling buses to providing solutions and deliver best value and support for life of our products

focusing on lowest Total Cost of Ownership

� Provide complete offering: Bus (“Workhorses of the Fleet”) supported by Parts, Service and Valued Added services

� Lead the market in innovation, reliability and quality

� Excel at customer support, response and follow up with emphasis on aftermarket parts and services

2. Operate as a world class OEM using LEAN principles, a Quality Roadmap and a Safety Culture� Be recognized as an Employer of Choice with an industry leading safety culture

� Excel in engineering, supply chain, strategic sourcing and appropriate in-sourcing

� Continuous pursuit of eliminating waste and cost reduction to improve competiveness

� Operate as a responsible, sustainable and environmentally conscious business

3. Perform while seeking Diversification and Growth� Lead the North American transit bus and motor coach industries and deliver strong TSR to Shareholders

� Operate with an appropriate and flexible capital structure to grow the business

� Seek to diversify over long term to ensure longevity and sustainability: Product (type of bus) and/or Market (Public vs Private) and/or Geography (North America vs International).

+

Our Facilities, Processes & Products

Our Market Leading Positions in Bus/Coach/Parts

Our Business and Revenue Stream

Our Revenue, EBITDA and CashFlow

Optimize, Defend, Diversify & Grow

4

663.6

136.9

--

100.0

200.0

300.0

400.0

500.0

600.0

700.0

Aug-12 Aug-13 Aug-14 Aug-15 Aug-16

Tot

al R

etur

n

NFI Strategic Plan and Execution has delivered solid TSR

Total Shareholder Return (1)

S&P/TSX Composite

Investment

Source: FactSet, Company filings

1. Total shareholder return includes capital appreciation and dividends paid.2. Calculated using closing TSX market price as at August 7, 2016

� NFI's first acquisition enhanced part fabrication capability and capacity

� 19.9% equity investment in NFI by a leading global bus and coach bodymanufacturer

� NFI acquired Orion’s parts business from Daimler

� NFI acquired US manufacturer of heavy-duty transit buses and parts distributor

� NFI acquired North America’s leading manufacturer of motor coach and parts/service support

� Adopted Stakeholder Model.

� Commitment to Culture, People & LEAN operations

� Migrated Capital Structure from Income Deposit Security (yield only focus) Common Share (Growth and Yield)

Cultural & Structural Change

Strategic Acquisition's

5

#1 Market Share in Transit Bus

HD Transit Bus Share (2015 market is ~5,300 units)

Heavy-Duty: Xcelsior ® Medium-Duty: MiDi ®

� Launch in 2009 based on >20 years experience with low floor transit buses

� Offered in 35’, 40’, and 60’ lengths� Primary targets is metropolitan & urban fleets� Typical sale price of approx US $450K for 35’/40’ and

US $700K for 60’ articulated

� JV with Alexander Dennis (UK) to introduce MiDi® to North America in 2014

� 30’ and 35’ low-floor medium duty bus, tested to HD standards. Primary target is municipal/ & commercial shuttles

� Typical sale price of approx US $300K

Active Canada/US HD Transit Bus Coach Fleet ~85,000

19%

33%

45%

3%

Source: New Flyer Database & Management Estimates

Average Age of the HD Transit Fleet: US = 7.8 years, Canada = 7.3 yearsSource: APTA Public Transportation Factbook 2016

Orion Parts and NABI acquired by NFI in 2013

6

MetropolitanFleets

17 operators39% of installed fleet

Urban Fleets

200 operators45% of installed fleet

MunicipalFleets

900+ Operators16% of installed

fleet

Transit Bus Market Segments in Canada and US

Source: New Flyer Database & Management Estimates

Transit Market Segments and primary targets

24 of the 25 largest Transit Agencies operate NF supported transit buses

New market entrants focusing only on battery-electric buses:

7

#1 Market Share in Motor Coaches

Motor Coach Share: 2015 market is ~2,265 units

38%

29%

24%

9%

50% 1% 26% 23%

New Coach – Private New Coach – Public Pre-Owned Coac h

� Targets the mid-range to luxury segments

� J Model is the #1 selling coach in the N.A. private market

� NA Distributor of Daimler’s SETRA coaches

� Tour and charter operators

� Hotels and casinos

� Inter-city line-haul operators

� Contract carriers

� Targets the mid-range segment

� “Buy America” compliant

� D Model is the #1 selling coach of all time in N.A.

� Transit authorities

� Universities

� U.S. Federal Government

� Correctional facilities

� Trade-in option to support new coach sales

� Coaches are refurbished at MCI’s service centers and various 3rd parties

� Value customers in the private market

� Small private fleets

� MCIU sells approx 350 pre-owned units annually

Active Canada/US Motor Coach Fleet ~55,500 units

Netherlands & Macedonia

Canada & US

Turkey

Source: MCI Database & Management Estimates

Average Age of the Motor Coach Fleet: US and Canada = 9 yearsSource: ABA Motorcoach Census March 2015

8

Motor Coach Market in Canada and US

Market Segments and primary targets

Transit

12% of installed fleet

Fixed Route/Line Haul

34% of installed fleet

Tour & Charter

52% of installed fleet

Conversion

2% of installed fleet

Public Private Private Private

Source: MCI Database & Management Estimates

Private Market Segment Definitions

9

Annual Deliveries and Market Demand

Transit Bus EUs delivered in Can/US Motor Coaches delivered in Can/US

+

Public Bid Universe & Active Opportunities (EUs) 2 009-2016

NFI forecasted EU buys in next 5 years

Bids submittedby NFI and EUs awaiting selection

Operator RFPs Issued. EUs for Proposals in development

Source: MCI Database & Management Estimates

US Federal Funding for Transportation

935

1,05

0

1,50

0

1,86

4

2,05

1

1,27

2

1,73

1

1,93

8

1,58

3

1,44

2 2,00

3

2,16

4

2,25

7

2,02

3

1,81

1

1,65

6 2,19

1

2,43

7

2,45

1

4,79

7 5,34

7

5,81

6

6,23

6

5,38

8

5,00

9

4,72

3 5,21

2

4,33

3

4,04

7

5,06

5

5,28

4 6,03

2

5,93

3

5,15

4

5,10

9

5,01

0

5,12

8

5,37

3

0

1000

2000

3000

4000

5000

6000

7000

1,49

2

1,86

2

1,76

7

1,19

0

1,47

9

1,51

4

1,02

2

753

1,05

0

1,29

2

1,05

6

1,01

2

811

633

592

686

821

802

856

2,48

5 2,99

0

2,82

4

2,38

1

2,33

0

2,04

8

1,47

5

1,34

3

1,75

2

2,09

9

1,85

2

1,82

0

1,58

4

1,20

8

1,54

3

1,56

6

1,77

3

1,92

6

2,31

1

0

1000

2000

3000

4000

5000

6000

7000

TotalIndustry

Total Industry

10

Public Customers Book-to-Bill and Backlog

Book-to-Bill >100% for 13 of last 14 Quarters

Total Backlog (Firm and Options)

Note: US Customer deferred Order was removed from backlog IN 2013 following 5 years of inaction.

+

Includes MCI backlog

11

Most comprehensive Parts & Support Services in the industry

Aftermarket Parts Product Support Services

� Widest transit bus and motor coach product assortment and industry leading distribution network with shortest delivery times.

� Added value through Unique offerings (Kits, Mid-life upgrade programs, Vendor Managed Inventory, KanBan, etc).

� Publications: Wide range of customized parts, maintenance and operational documentation. New Flyer publications are the industry standard.

� Field Support: Product acceptance, field support, field engineering and warranty management.

� Training: Operator and maintenance training provided in connection with new bus sales or aftermarket support (On-the-job, Classroom, eLearning, etc.).

� New Flyer Connec t: On-board system that permits real-time monitoring of the bus driver and vehicle performance to help improve driver safety, driving efficiency, and reduce fuel use and maintenance costs

� MCI Service Centers: Nationwide footprint with service centers, distribution facilities and over 3,000 emergency response partners

+

12

Manufacturing, Parts & Service Footprint

`

FL

AL

TX

CA

NDMN

IL IN OH

KY

WV

PA

NY

NJ

SK MB

ONQC

ABRenton, WA

NFI Service Center

Fresno, CANFI Parts Distribution

Ontario, CANFI Completion & Service Center

Crookston, MNNFI Bus Completion

St Cloud, MNNFI Bus Manufacture

Anniston, ALNFI Bus Manufacture

Elkhart, INTCB Part Fabrication

Hebron, KYNFI Parts Distribution

Delaware, OHNABI Parts Distribution

Brampton, ONNFI Parts Distribution

Arnprior, ONNFI Service Center

NFI - Winnipeg, MBParts Fabrication and Bus Shell Assembly

New Product DevelopmentParts Distribution

MCI - Winnipeg, MBParts Fabrication, MCI D Model Shell Assembly

Complete J Model manufactureNew Product Development

Montreal, PQMCI Service Center

Blackwood, NJMCI Service Center

East Brunswick, NJMCI Parts Distribution

Winter Garden, FLMCI Service Center

Dallas, TXMCI Service Center

Los Alamitos, CAMCI Service Center

Louisville, KYMCI Parts DistributionPembina, ND

MCI D Shell Completion

Des Plaines, ILMCI Service Center

Winnipeg, MBFrank Fair Fiberglass

Fabrication

+

13

Environmental Commitment: Green Propulsion Options

Natural GasClean Diesel Hybrid-Electric Battery-ElectricElectric-Trolley

+

Clean Diesel

Natural Gas

Electric Trolley

Hybrid Electric

All Electric

Xcelsior

MiDi

D Model

J Model

Additional propulsion options currently being evaluated for NFI MiDi and MCI J Model

14

Financial Performance

Sales ($M US)

Adj EBITDA ($M US)

Return on Invested Capital

ROIC = Net operating profit after taxAverage invested capital for the period

+

4164 57

90

159

20

31 50

61

70

0

50

100

150

200

250

2012 2013 2014 2015 2016 Q2 LTM

Bus Aftermarket

61

95107

151

229

746984

1,132 1,217

1,561119

215

319322

363

0

500

100 0

150 0

200 0

250 0

201 2 201 3 201 4 201 5 201 6 Q2 LTM

Bus Aftermarket

865

1,199

1,451 1,539

1,924

547.6 641.5 706.6 712.0957.9

6.2%

8.6%

8.5%

12.2%

14.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0

200

400

600

800

1000

1200

2012 2013 2014 2015 2016 Q2 LTM

Millio

ns

Average Invested Capital for the period Return on Invested Capital

17 16 14 14 15 1824

37

2027 26

35 3139 36

45

68

80

75 7163 62 60 62

72

95 99108 109 107

119

131142

151

188

229

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

$220

$240

2012 2013 2014 2015 2016

Adjusted EBITDA USD

Adjusted EBITDA LTM Adjusted EBITDA

Mil

lio

ns

Quarterly Adj EBITDA ($M US)

15

Cash Flow Performance

Free Cash Flow and Dividends ($M C)

2016 Q2 LTM Adjusted EBITDA to Free Cash Flow ($M)

229.3

20.3

39.2 11.1 2.5

156.3

35.6 191.9

-

50

100

150

200

250M

illio

ns

+

27.145.1

65.5

108.3

191.9

33.1 30.7 32.5 33.8 42.20.0

50.0

100.0

150.0

200.0

250.0

2012 2013 2014 2015 2016 Q2 LTM

Free Cash Flow Dividends

NFI Annual Dividend

Increased 35.7% from $.70/share to $.95/share

on May 12, 2016 (now paid quarterly)

16

Debt and Total Leverage

0

0.5

1

1.5

2

2.5

3

3.5

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

2010 2011 2012 2013 2014 2015 2016

Q2

IDS Debt Bachelor Bonds Senior Term Loan

Revolver Convertible Debenture Total leverage ratio

$26M Convertible Debenture issued in Jun-12 @ 6.25%. Convert price $US10/share

$343M Revolver facility used to manage working capital fluctuations ($91M outstanding)

$482M Senior secured term loan

Total Leverage Ratio does not include Convertible Debenture as debt.

Under NFI Senior Credit Agreement Total Leverage must be maintained

below 4X Adj EBITDA Total Debt ($US M) Total Leverage Ratio

+

17

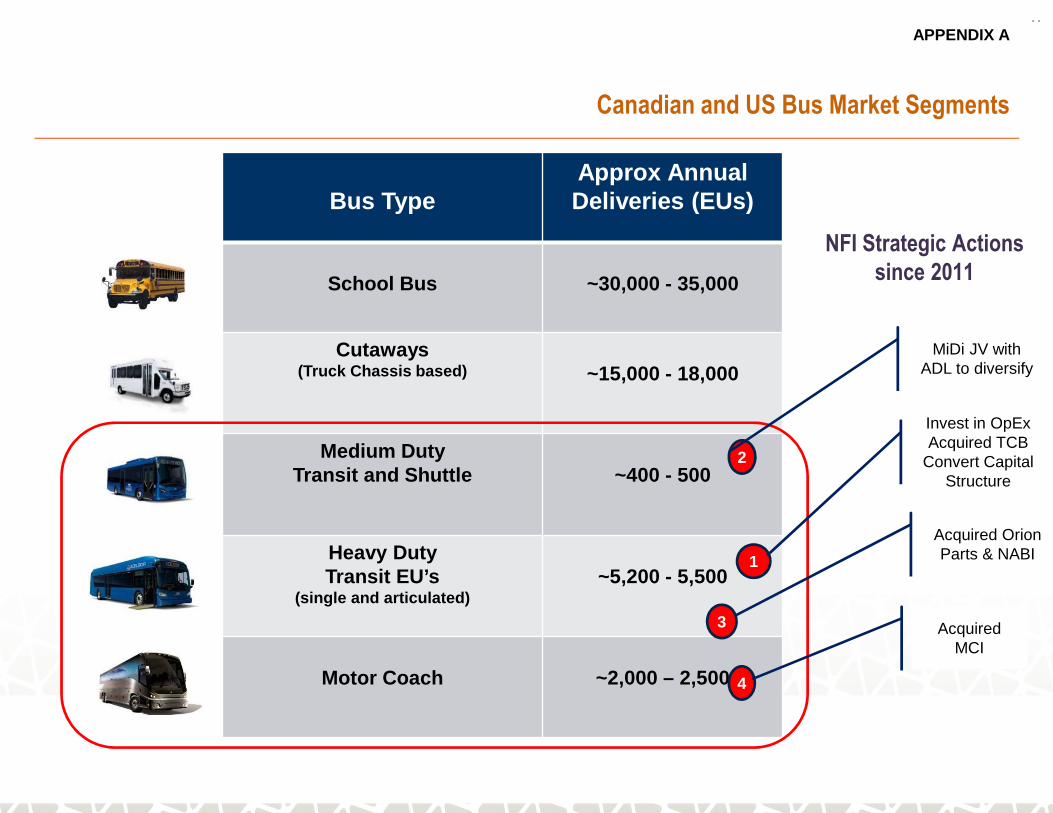

NFI Strategic Actionssince 2011

Bus TypeApprox Annual Deliveries (EUs)

School Bus ~30,000 - 35,000

Cutaways(Truck Chassis based) ~15,000 - 18,000

Medium DutyTransit and Shuttle ~400 - 500

Heavy DutyTransit EU’s

(single and articulated)~5,200 - 5,500

Motor Coach ~2,000 – 2,500

2

MiDi JV with ADL to diversify

1

Invest in OpEx Acquired TCB

Convert Capital Structure

3

Acquired Orion Parts & NABI

4

Acquired MCI

Canadian and US Bus Market Segments

APPENDIX A

18

FORWARD LOOKING STATEMENTS

This investor presentation contains forward-looking statements relating to expected future events, including the integration of the acquired business into New Flyer’s existing business and expected synergies, the

diversification and growth of the combined bus and aftermarket parts businesses. Although the forward-looking statements contained in this investor presentation are based upon what management believes to be

reasonable assumptions, investors cannot be assured that actual results will be consistent with these forward-looking statements, and the differences may be material. Actual results may differ materially from

management expectations as reflected in such forward-looking statements for a variety of reasons, including risks related the ability to implement the operational changes necessary to achieve the intended

synergies, acquisitions, joint ventures and other strategic relationships with third parties (including liabilities relating thereto), the covenants contained in the Company’s new senior credit facilities could impact the

ability of the Company to fund dividends, market and general economic conditions and economic conditions of and funding availability for customers to purchase buses and to purchase parts or services, customers

may not exercise options to purchase additional buses, the ability of customers to suspend or terminate contracts for convenience and the other risks and uncertainties discussed in the materials filed with the

Canadian securities regulatory authorities and available on SEDAR at www.sedar.com. Due to the potential impact of these factors, the Company disclaims any intention or obligation to update or revise any forward-

looking statements, whether as a result of new information, future events or otherwise, unless required by applicable law.

FINANCIAL TERMS, DEFINITIONS AND CONDITIONS

References to “EBITDA” are to earnings before interest, income taxes, depreciation and amortization, fair value adjustment for total return swap and unrealized foreign exchange losses or gains on non-current

monetary items. References to “Adjusted EBITDA” are to EBITDA after adjusting for: the effects of certain non-recurring and/or non-operations related items that have impacted the business and are not expected to

recur, including non-recurring transitional costs relating to business acquisitions, product rationalization costs, impairment loss on equipment and intangible assets, realized investment tax credits (“ITCs”), equity

settled stock-based compensation, past service costs, fair value adjustment to MCI’s inventory and deferred revenue, proportion of the total return swap realized, loss on derecognition of long-term debt and costs

associated with assessing strategic and corporate initiatives. Return on Invested Capital “ROIC” is calculated by dividing Net Operating Profit After Tax by Average Invested Capital for the period. References to “Net

Operating Profit After Tax” are to Adjusted EBITDA less depreciation of plant and equipment and income taxes. References to “Invested Capital” are to shareholders’ equity plus long-term debt, obligations under

finance leases, other long-term liabilities, convertible debentures and derivative financial instrument liabilities less cash.

Management believes EBITDA, Adjusted EBITDA, ROIC and Free Cash Flow (as defined below) are useful measures in evaluating the performance of the Company. “Free Cash Flow” means net cash generated by

operating activities adjusted for changes in non-cash working capital items, interest paid, interest expense, income taxes paid, current income tax expense, effect of foreign currency rate on cash, past service costs,

defined benefit funding, non-recurring transitional costs relating to business acquisitions, costs associated with assessing strategic and corporate initiatives, product rationalization costs, defined benefit expense,

cash capital expenditures, realized ITCs, fair value adjustment to MCI’s inventory and deferred revenue, proportion of the total return swap realized and principal payments on capital leases. However, EBITDA,

Adjusted EBITDA, ROIC and Free Cash Flow are not recognized earnings measures and do not have standardized meanings prescribed by IFRS. Readers of this presentation are cautioned that EBITDA, and

Adjusted EBITDA should not be construed as an alternative to net earnings or loss determined in accordance with IFRS as an indicator of New Flyer's performance, and Free Cash Flow should not be construed as

an alternative to cash flows from operating, investing and financing activities determined in accordance with IFRS as a measure of liquidity and cash flows. A reconciliation of net earnings and cash flow to EBITDA

and Adjusted EBITDA, based on the Financial Statements, has been presented In Management’s Discussion and Analysis of Financial Condition under the heading “Reconciliation of Net Earnings to EBITDA and

Adjusted EBITDA” and “Reconciliation of Cash Flow to EBITDA and Adjusted EBITDA”, respectively. A reconciliation of Free Cash Flow to cash flows from operations is provided under the heading “Summary of

Free Cash Flow”.

New Flyer’s method of calculating EBITDA, Adjusted EBITDA, ROIC and Free Cash Flow may differ materially from the methods used by other issuers and, accordingly, may not be comparable to similarly titled

measures used by other issuers. Dividends paid from Free Cash Flow are not assured, and the actual amount of dividends received by holders of Shares will depend on, among other things, the Company's financial

performance, debt covenants and obligations, working capital requirements and future capital requirements, all of which are susceptible to a number of risks, as described in New Flyer’s public filings available on

SEDAR at www.sedar.com.

All figures are in U.S. dollars unless otherwise noted.

FORWARD LOOKING STATEMENTS, FINANCIAL TERMS, DEFINITIONS AND CONDITIONS

APPENDIX B

+