options parity

TRANSCRIPT

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 1/47

Computational Finance 1/47

Derivative SecuritiesForwards and Options

381 Computational Finance

Imperial College

London

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 2/47

Computational Finance 2/47

Topics Covered

Derivatives:

Forward Contracts, Options

Valuation techniques

Option Pricing Models

Binomial Option Pricing

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 3/47

Computational Finance 3/47

Introduction to Derivatives

securitywhose payoff is explicitly tied to value or price of other financial security

that determines value of derivative is called underlying security

derivatives

arise when individuals or companies wish to buy asset or commodity in

advance to insure against adverse market movements;effective tools for hedging risks ± designed to enable market participants to

eliminate risk.

business dealing with a good faces risk associated with price fluctuations.

control that risk through use of derivative securities.

Example:

farmer can fix price for crop even before planting, eliminating price risk

an exporter can fix a foreign exchange rate even before beginning to

manufacture product, eliminating foreign exchange risk.

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 4/47

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 5/47

Computational Finance 5/47

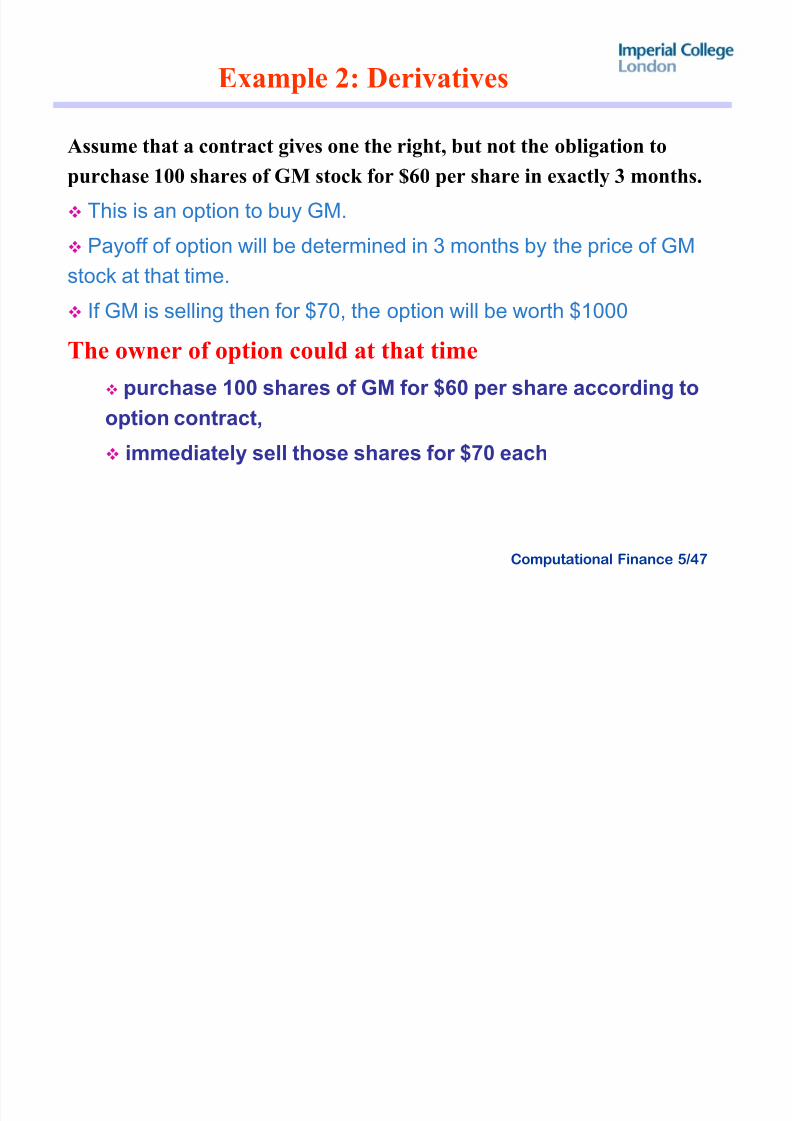

Example 2: Derivatives

Assume that a contract gives one the right, but not the obligation to

purchase 100 shares of GM stock for $60 per share in exactly 3 months.

This is an option to buy GM.

Payoff of option will be determined in 3 months by the price of GM

stock at that time. If GM is selling then for $70, the option will be worth $1000

The owner of option could at that time

purchase 100 shares of GM for $60 per share according to

option contract,

immediately sell those shares for $70 each

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 6/47

Computational Finance 6/47

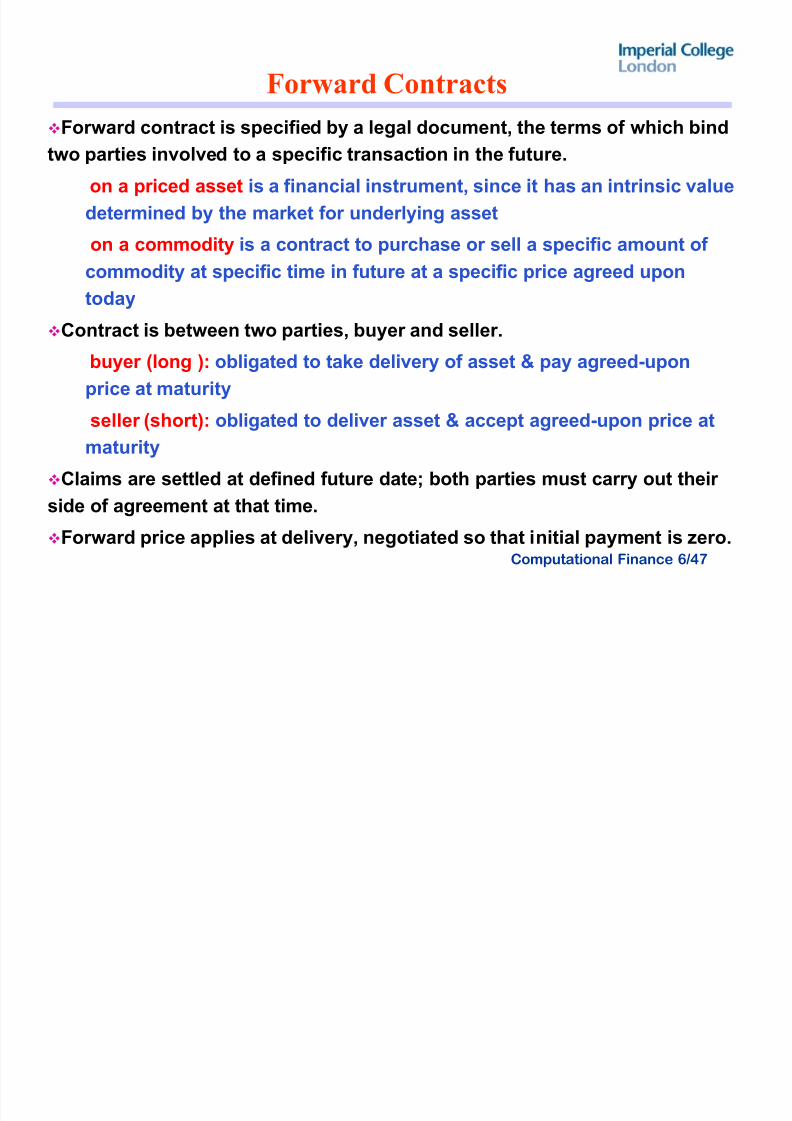

Forward Contracts

Forward contract is specified by a legal document, the terms of which bind

two parties involved to a specific transaction in the future.

on a priced asset is a financial instrument, since it has an intrinsic value

determined by the market for underlying asset

on a commodity is a contract to purchase or sell a specific amount of

commodity at specific time in future at a specific price agreed upontoday

Contract is between two parties, buyer and seller.

buyer (long ): obligated to take delivery of asset & pay agreed-upon

price at maturity

seller (short): obligated to deliver asset & accept agreed-upon price at

maturity

Claims are settled at defined future date; both parties must carry out their

side of agreement at that time.

Forward price applies at delivery, negotiated so that initial payment is zero.

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 7/47

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 8/47

Computational Finance 8/47

Standard Formulation: Discrete Compounding

Assumptions:

buy one unit commodity at price S 0 with no dividend payment

enter a forward contract to deliver at T one unit at price F

store until T with no cost, deliver to meet our obligation & obtain F

Cash flow sequence in two market operations is ( - S 0

, F ) fully

determined at t = 0 consistent with interest rate between t = 0 and T

For asset with zero storage cost, current spot price S 0 , forward price F

is calculated as

Buying the commodity at price S 0 = lending amount S 0 of cash for

which we will receive an amount F at time T since storage costless.

factor discount is where ),0(),0(0

T d F T d S v!

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 9/47

Computational Finance 9/47

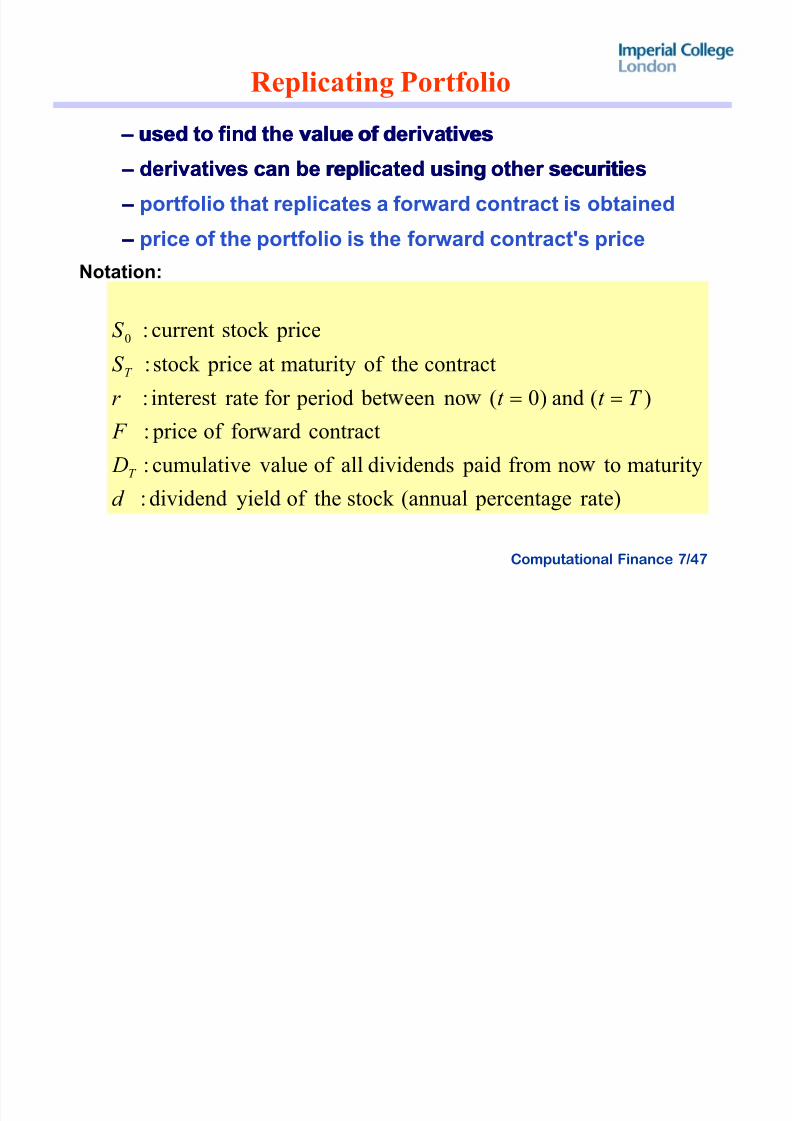

Arbitrage Portfolio

Assume that

borrow S 0 cash and buy one unit of the underlying asset

take one-unit short position (sell) in forward market

at T , deliver asset receiving cash amount F & repay our loan in amount

obtain positive profit of for zero net investment

Assume that

shorting one unit of underlying asset: borrow asset from s.o who plans to store

it during this period, then sell borrowed asset and replace borrowed asset at T

take one-unit long position (buy) in forward market

at T , receive from loan and pay F one-unit of asset and return

this to lender who made the short possible

profit is

),0(0

T d S F "

),0(0

T d S

),0(0

T d S

F

F T d

S ),0(

0

),0(0

T d S

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 10/47

Computational Finance 10/47

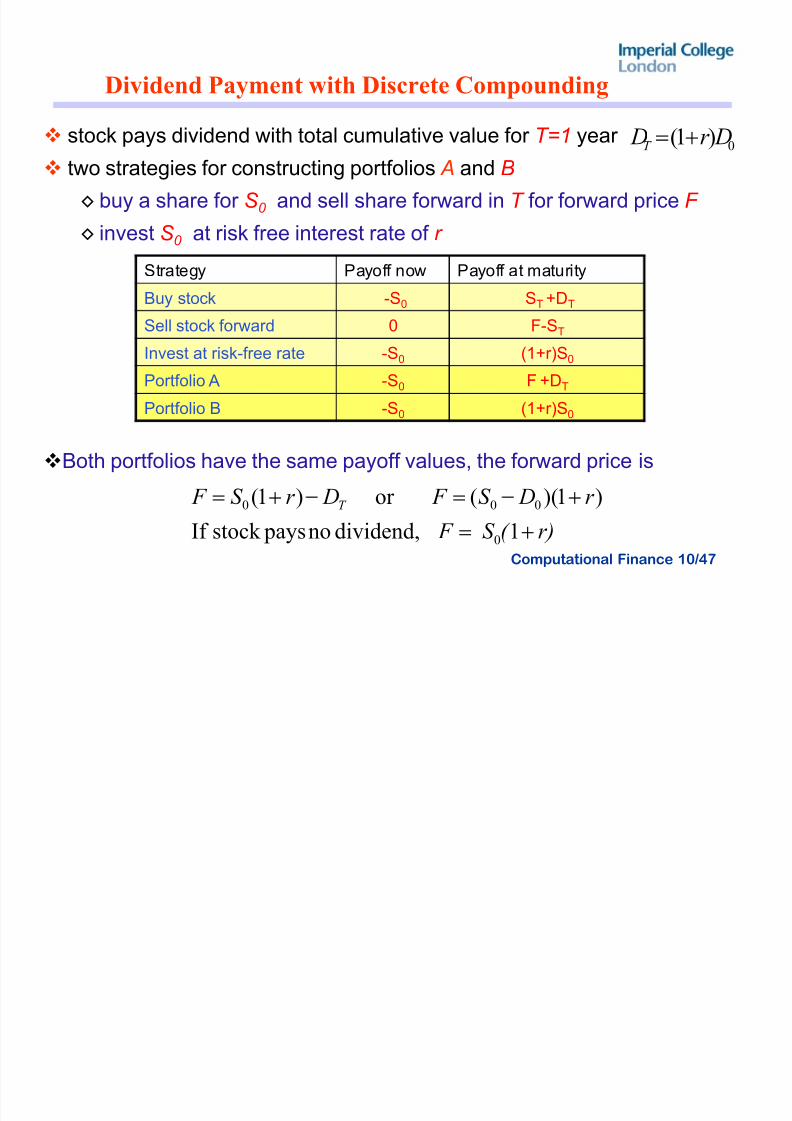

Dividend Payment with Discrete Compounding

stock pays dividend with total cumulative value for T=1 year two strategies for constructing portfolios A and B

¹ buy a share for S 0 and sell share forward in T for forward price F

¹ invest S 0 at risk free interest rate of r

Both portfolios have the same payoff values, the forward price is

Strategy Payoff now Payoff at maturityBuy stock -S0 ST +DT

Sell stock forward 0 F-ST

Invest at risk-free rate -S0 (1+r)S0

Portfolio A -S0 F +DT

PortfolioB

-S0 (1+r)S0

0)1( Dr DT !

r)( S F

r DS F Dr S F T

!

!!

1 dividend,no paysstock If

)1)((or )1(

0

000

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 11/47

Computational Finance 11/47

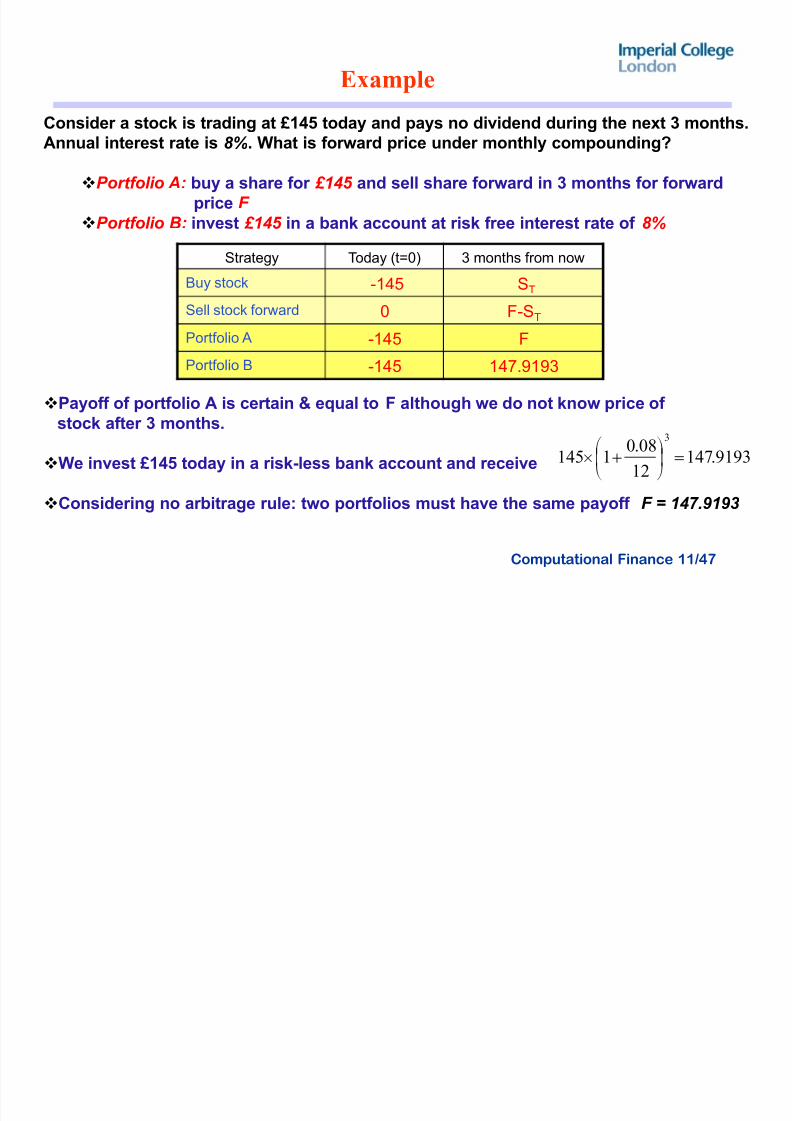

Example

Consider a stock is trading at £145 today and pays no dividend during the next 3 months.

Annual interest rate is 8%. What is forward price under monthly compounding?

Por tf olio A: buy a share for £145 and sell share forward in 3 months for forwardprice F

Por tf olio B: invest £145 in a bank account at risk free interest rate of 8%

Payoff of portfolio A is certain & equal to F although we do not know price of stock after 3 months.

We invest £145 today in a risk-less bank account and receive

Considering no arbitrage rule: two portfolios must have the same payoff F = 147.9193

Strategy Today (t=0) 3 months from now

Buy stock -145 ST

Sell stock forward 0 F-ST

Portfolio A -145 F

Portfolio B -145 147.9193

9193.14712

08.01145

3

!¹ º

¸©ª

¨v

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 12/47

Computational Finance 12/47

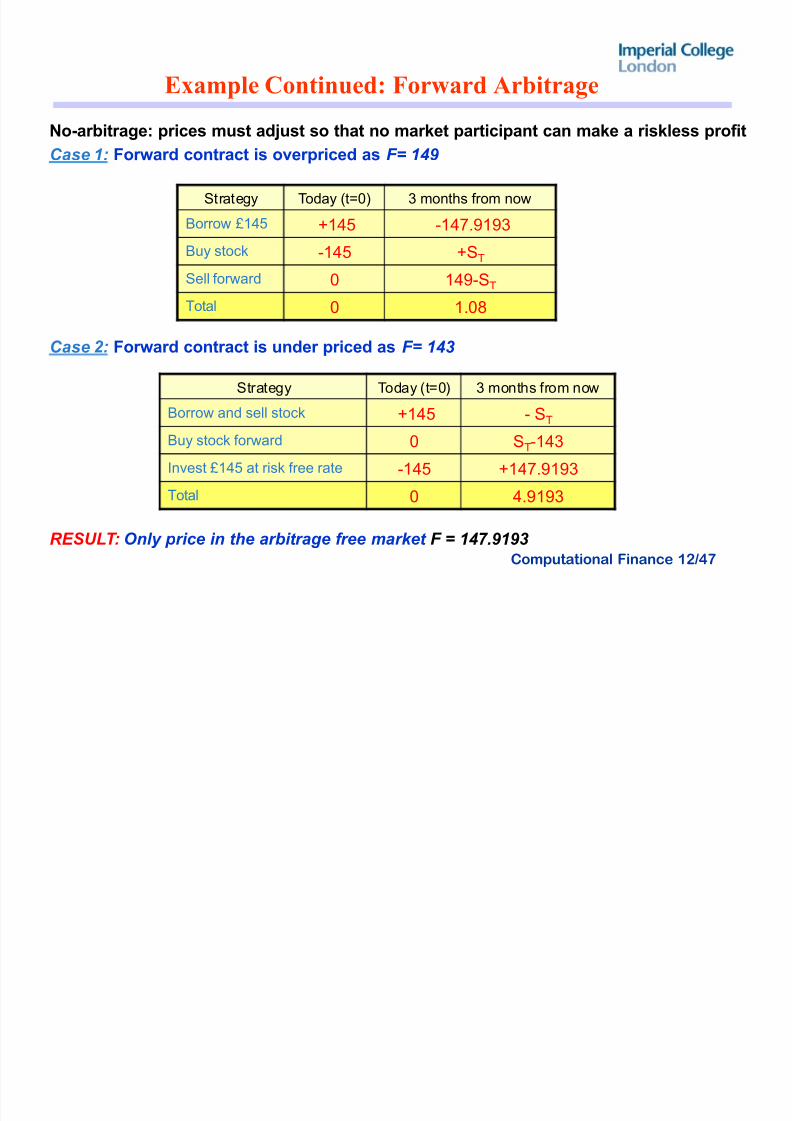

Example Continued: Forward Arbitrage

No-arbitrage: prices must adjust so that no market participant can make a riskless profitCase 1: Forward contract is overpriced as F = 149

Case 2: Forward contract is under priced as F = 143

RE SULT : Only pric e i n the arbi t r age f r ee mark et F = 147.9193

Strategy Today (t=0) 3 months from now

Borrow £145 +145 -147.9193

Buy stock -145 +ST

Sell forward 0 149-ST

Total 0 1.08

Strategy Today (t=0) 3 months from now

Borrow and sell stock +145 - ST

Buy stock forward 0 ST-143

Invest £145 at risk free rate -145 +147.9193

Total 0 4.9193

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 13/47

Computational Finance 13/47

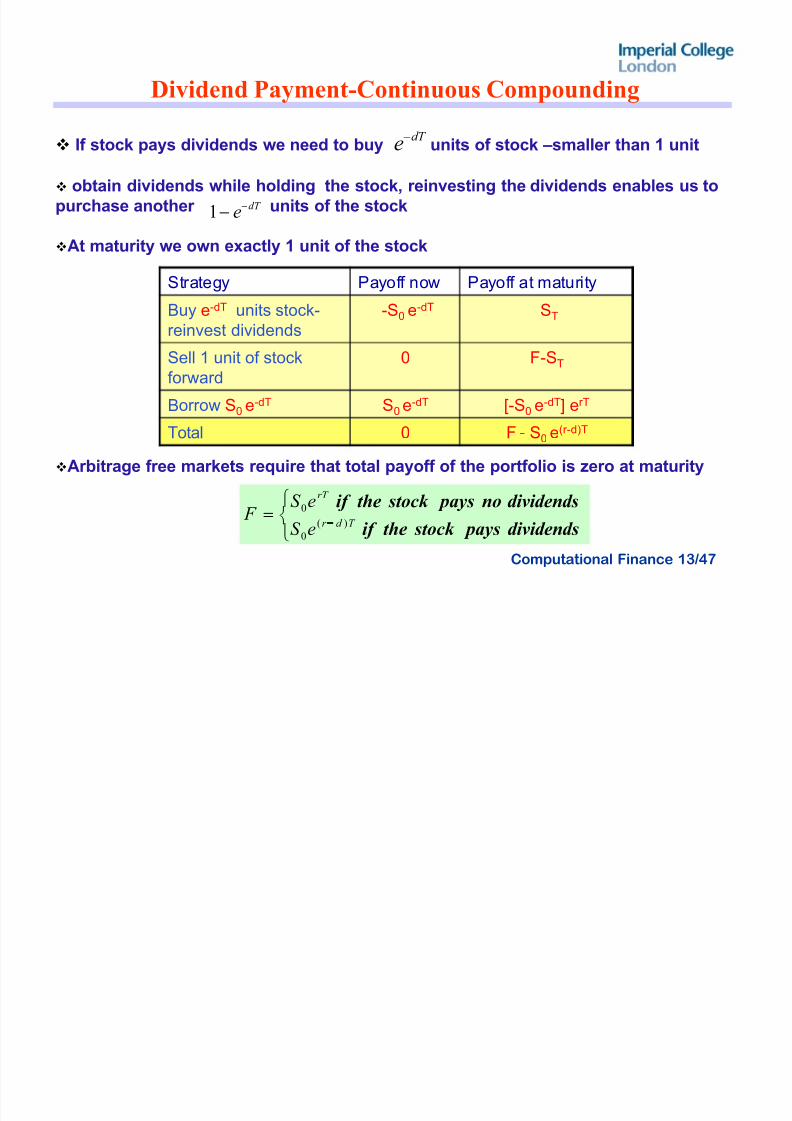

Dividend Payment-Continuous Compounding

If stock pays dividends we need to buy units of stock ±smaller than 1 unit

obtain dividends while holding the stock, reinvesting the dividends enables us topurchase another units of the stock

At maturity we own exactly 1 unit of the stock

Arbitrage free markets require that total payoff of the portfolio is zero at maturity

Strategy Payoff now Payoff at maturity

Buy e-dT units stock-reinvest dividends

-S0 e-dT ST

Sell 1 unit of stockforward

0 F-ST

Borrow S0e-dT S

0e-dT [-S

0e-dT] erT

Total 0 F - S0 e(r-d)T

°¯®

!dividends paysstock theif

dividendsno paysstock theif T d r

rT

eS

eS F

)(

0

0

dT e

dT e1

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 14/47

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 15/47

Computational Finance 15/47

Commodity Forwards

owner of commodities has to maintain their value,

requires storage (wheat, gold), feeding (live hogs), or

security (gold)

cost is called cost of carry expressed as an annual percentage rate q

It is treated as a negative dividend.

the valuation formula for commodity forwards is

obtained asT qr eS )(

0

!

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 16/47

Computational Finance 16/47

Options

Holder of forward contract is obliged to trade at maturity of contractUnless the position is closed before maturity, the holder must take possession of

the commodity, currency or whatever is the subject of the contract, regardless of

whether the price of the underlying asset has risen or fallen.

An option gives holder a right to trade in the future at a previously agreed pricebut takes away the obligations. If stock falls, we do not have to buy it after all.

An option is a privilege sold by one party to another that offers the buyer the right

to buy or sell a security at an agreed-upon price during a certain period of time or

on a specific date.Option holder Option holder has the right to chose to purchase a stock at a sethas the right to chose to purchase a stock at a set--price within a certain periodprice within a certain period

Option writer Option writer has the obligation to fulfil the choice of the holder:has the obligation to fulfil the choice of the holder:

deliver the asset (for deliver the asset (for call optioncall option ) OR buy the asset (for ) OR buy the asset (for put optionput option ))

receives the premiumreceives the premium

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 17/47

Computational Finance 17/47

Example: R eal life

You have seen a sale on a TV for £120 in a newspaper. You go to shop to purchase it at theadvertised price. Unfortunately at that time the TV is already out-of stock. But the manager gives you

a rain-check entitling you to buy the same TV for the advertised price of £120 anytime within the next

2 months.

You have just received a call option:

± gives you the right, but not the obligation, to buy the TV in the future

± at the guaranteed strike price of £120

± until the expiration date of 2 months

Scenario 1: A few weeks later you go to exercise your rain check -

± TV is now in stock and priced at £150. Since you have a rain check the store manager

agrees to issue the rain check and

sells you TV at £120. SAVED £30

± TV is now in stock but on sale for £100. Your rain check is worthless since you can buy TV at the reducedprice. You can let your option expire worthless ± have no obligation to exercise it.

Scenario 2: Your friend phoned you and told you that he needs a new TV. You mentioned your rain

check and agreed to sell it to him for £10.

± ± the option premium is £10, the same strike price of £120 and expiration date of 2 months.

± your friend is taking risk: TV might be cheaper than £120 (rain check is worthless lose £10)

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 18/47

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 19/47

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 20/47

Computational Finance 20/47

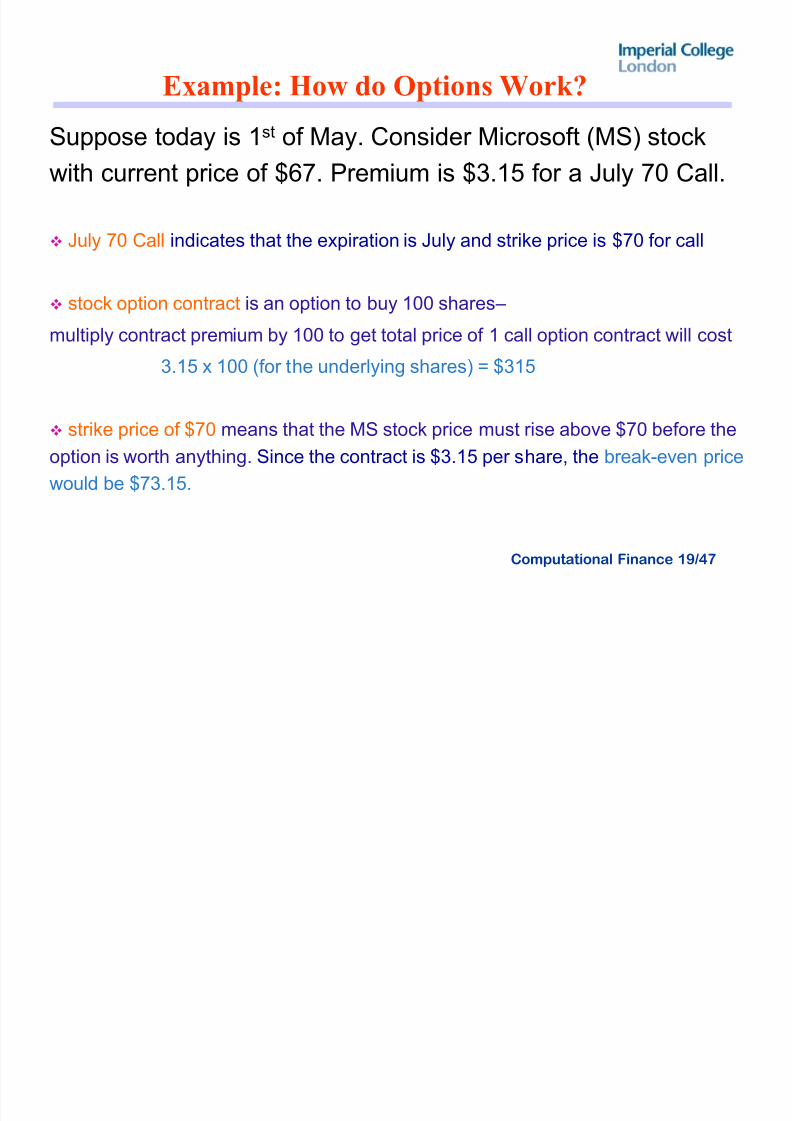

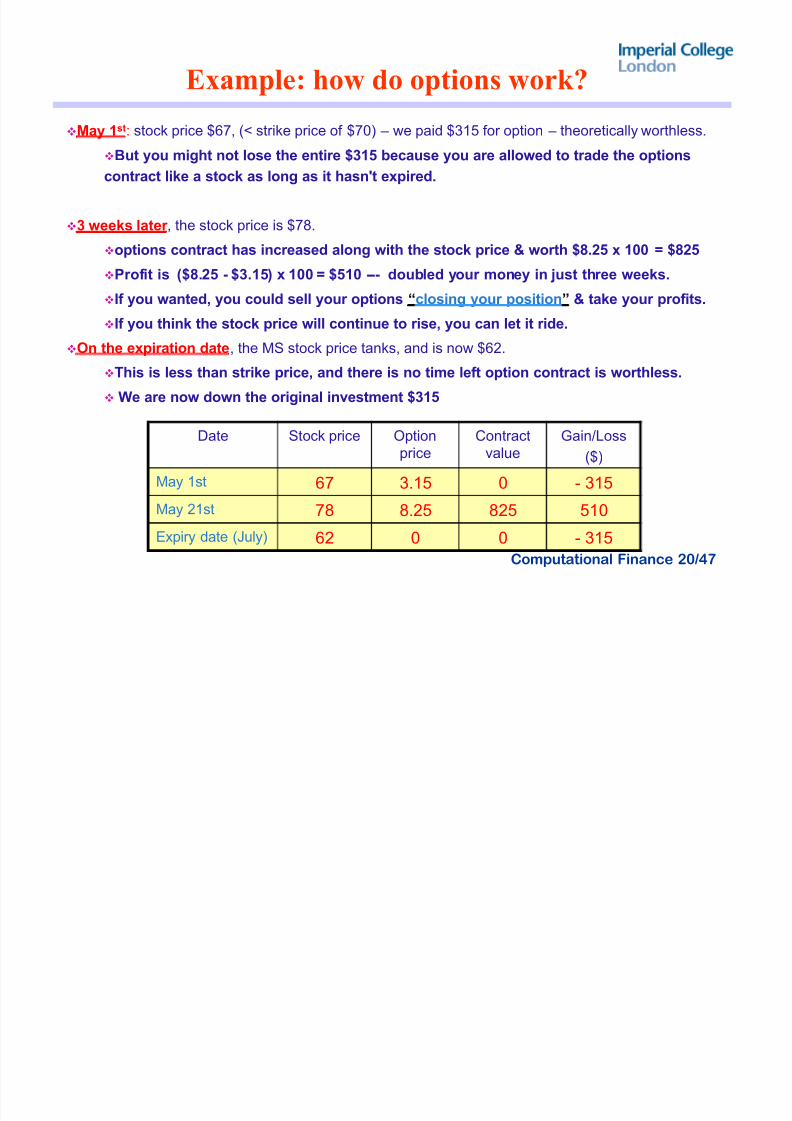

Example: how do options work?

May 1st: stock price $67, (< strike price of $70) ± we paid $315 for option ± theoretically worthless.

But you might not lose the entire $315 because you are allowed to trade the options

contract like a stock as long as it hasn't expired.

3 weeks later , the stock price is $78.

options contract has increased along with the stock price & worth $8.25 x 100 = $825

Profit is ($8.25 - $3.15) x 100 = $510 --- doubled your money in just three weeks.If you wanted, you could sell your options ³closing your position´ & take your profits.

If you think the stock price will continue to rise, you can let it ride.

On the expiration date, the MS stock price tanks, and is now $62.

This is less than strike price, and there is no time left option contract is worthless.

We are now down the original investment $315

Date Stock price Optionprice

Contractvalue

Gain/Loss

($)

May 1st 67 3.15 0 - 315

May 21st 78 8.25 825 510

Expiry date (July) 62 0 0 - 315

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 21/47

Computational Finance 21/47

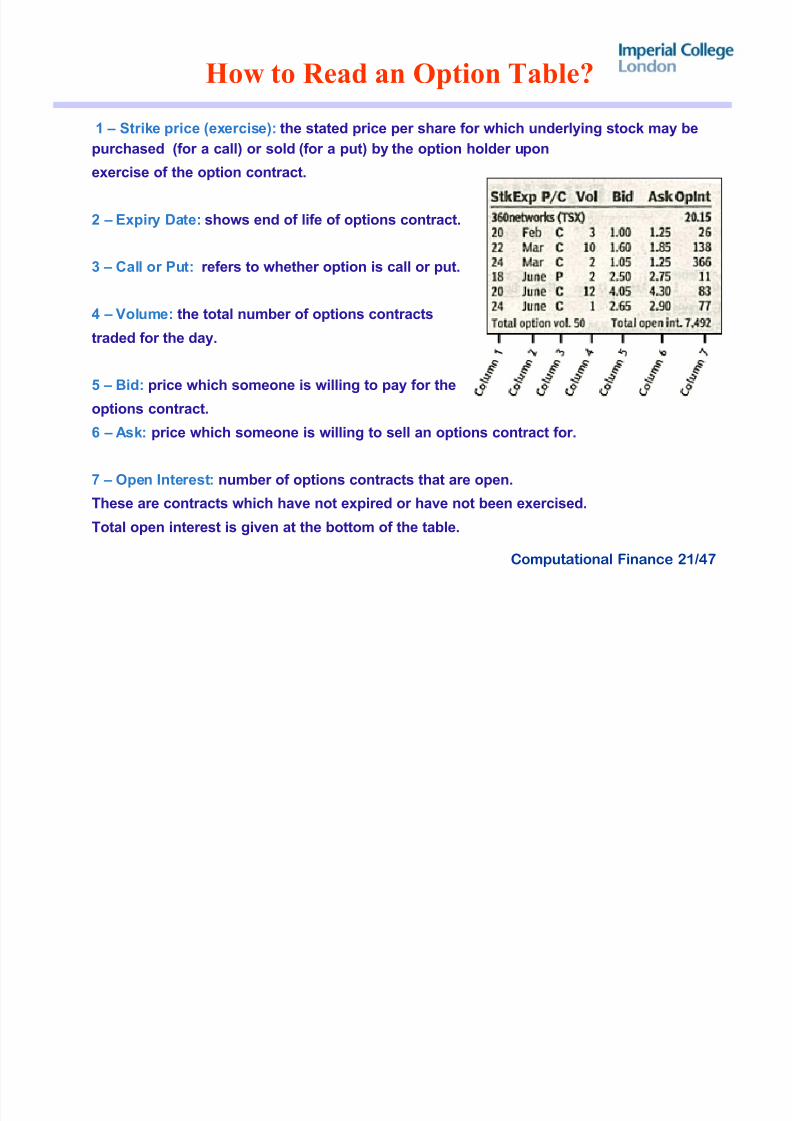

How to R ead an Option Table?

1 ± Strike price (exercise): the stated price per share for which underlying stock may be

purchased (for a call) or sold (for a put) by the option holder upon

exercise of the option contract.

2 ± Expiry Date: shows end of life of options contract.

3 ± Call or Put: refers to whether option is call or put.

4 ± Volume: the total number of options contracts

traded for the day.

5 ± Bid: price which someone is willing to pay for the

options contract.

6 ± Ask: price which someone is willing to sell an options contract for.

7 ± Open Interest: number of options contracts that are open.

These are contracts which have not expired or have not been exercised.

Total open interest is given at the bottom of the table.

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 22/47

Computational Finance 22/47

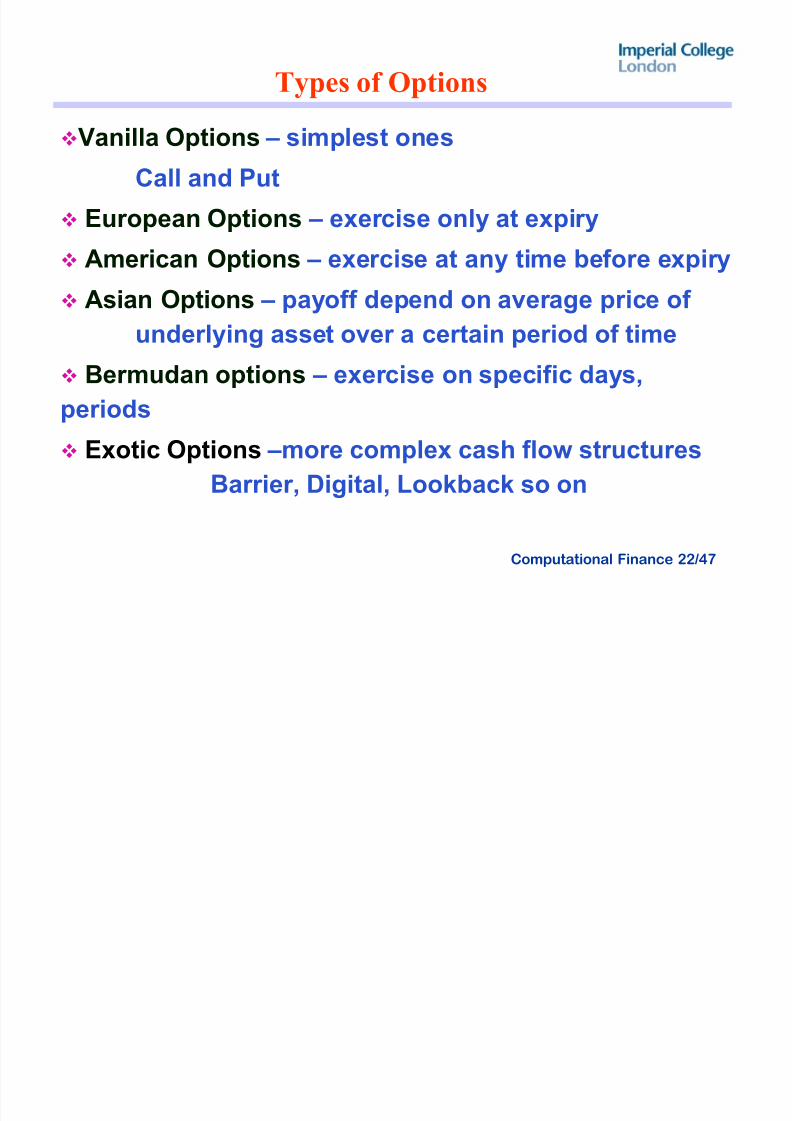

Types of Options

Vanilla Options ± simplest onesCall and Put

European Options ± exercise only at expiry

American Options ± exercise at any time before expiry

Asian Options ± payoff depend on average price of

underlying asset over a certain period of time

Bermudan options ± exercise on specific days,

periods Exotic Options ±more complex cash flow structures

Barrier, Digital, Lookback so on

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 23/47

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 24/47

Computational Finance 24/47

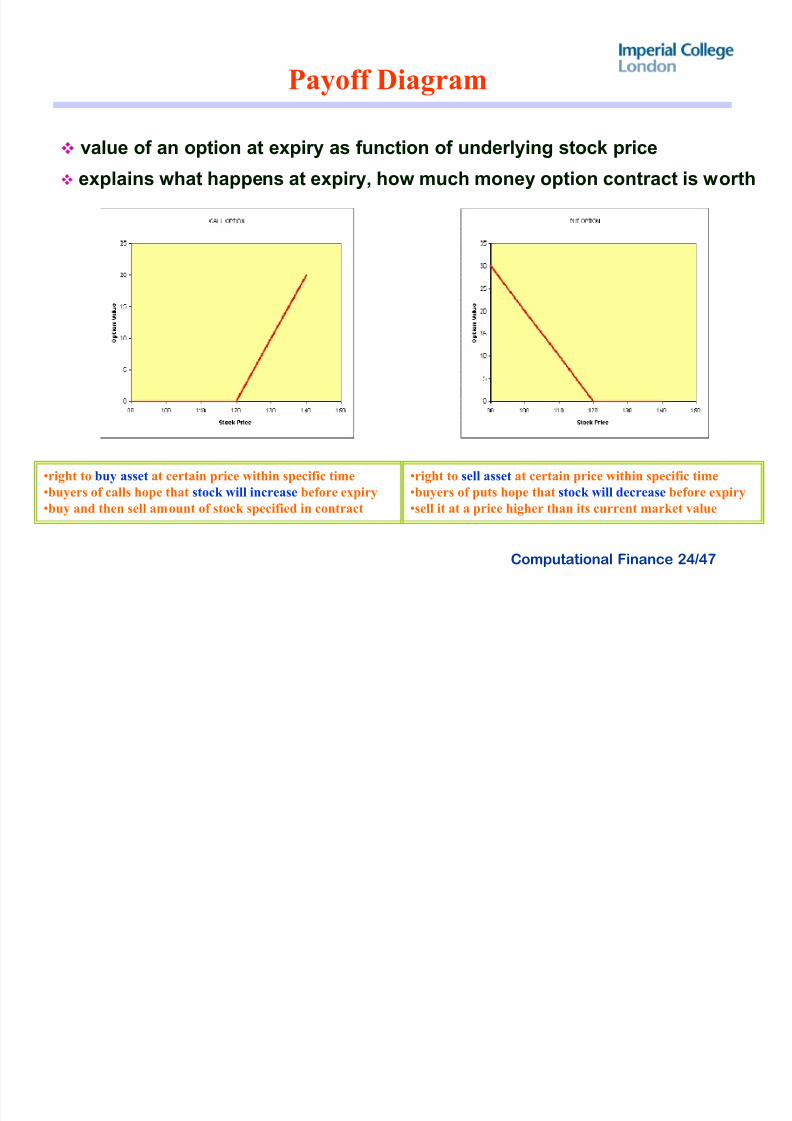

Payoff Diagram

value of an option at expiry as function of underlying stock price

explains what happens at expiry, how much money option contract is worth

�right to buy asset at certain price within specific time

�buyers of calls hope that stock will increase before expiry

�buy and then sell amount of stock specified in contract

�right to sell asset at certain price within specific time

�buyers of puts hope that stock will decrease before expiry

�sell it at a price higher than its current market value

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 25/47

Computational Finance 25/47

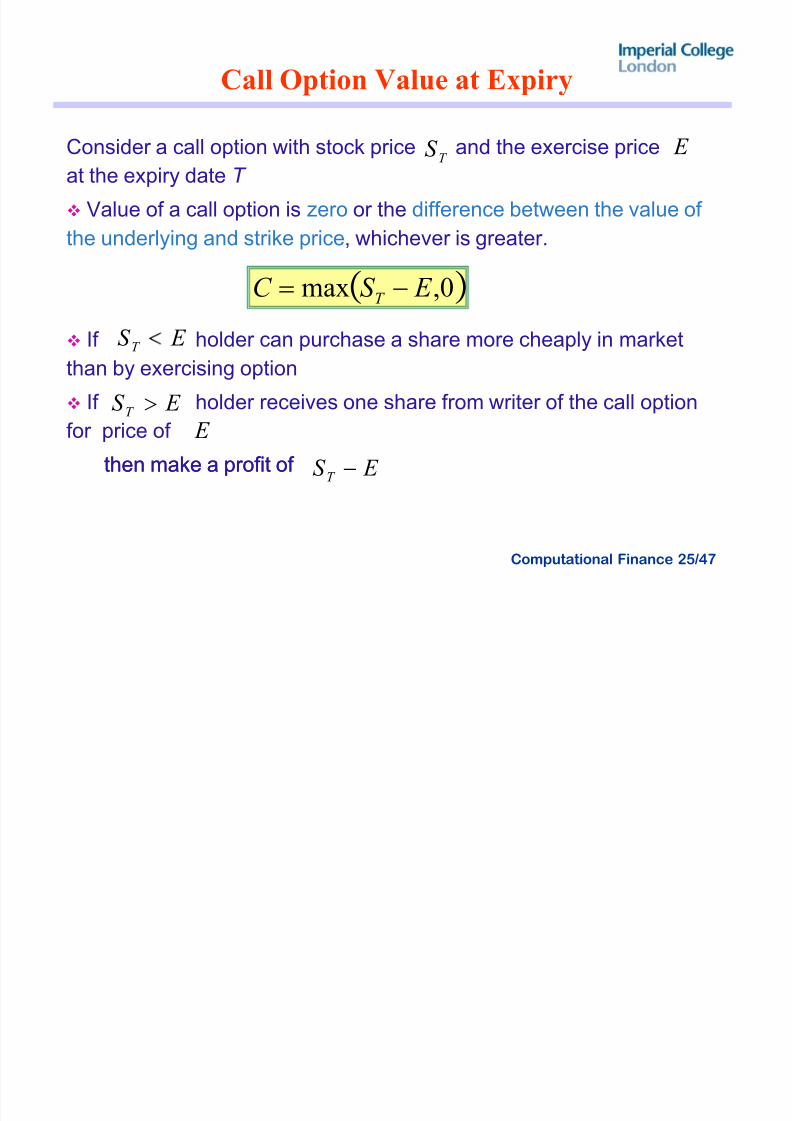

Call Option Value at Expiry

Consider a call option with stock price and the exercise priceat the expiry date T

Value of a call option is zero or the difference between the value of

the underlying and strike price, whichever is greater.

If holder can purchase a share more cheaply in market

than by exercising option

If holder receives one share from writer of the call option

for price of

then make a profit of then make a profit of

T S E

0,max E S C T !

E S T

E S T

" E

E S T

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 26/47

Computational Finance 26/47

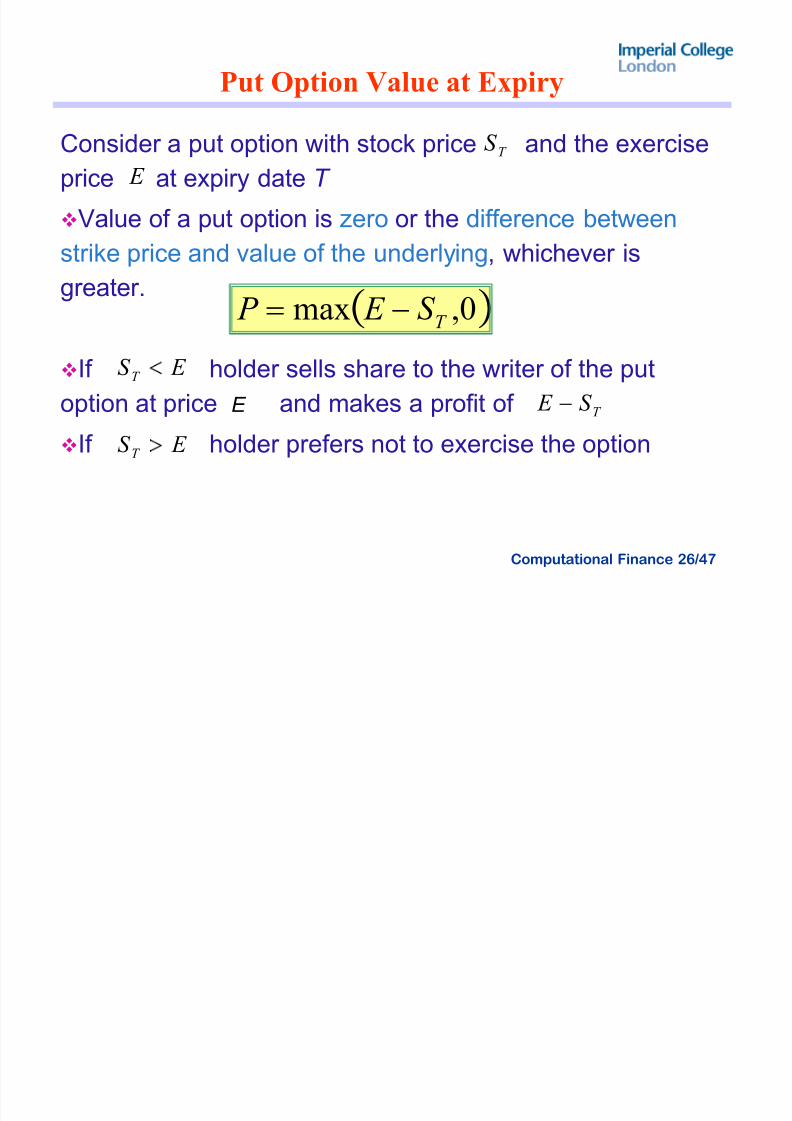

Put Option Value at Expiry

Consider a put option with stock price and the exerciseprice at expiry date T

Value of a put option is zero or the difference between

strike price and value of the underlying, whichever is

greater.

If holder sells share to the writer of the put

option at price E and makes a profit of

If holder prefers not to exercise the option

T S E

0,max T S E P !

E S T

E S T

T

S E

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 27/47

Computational Finance 27/47

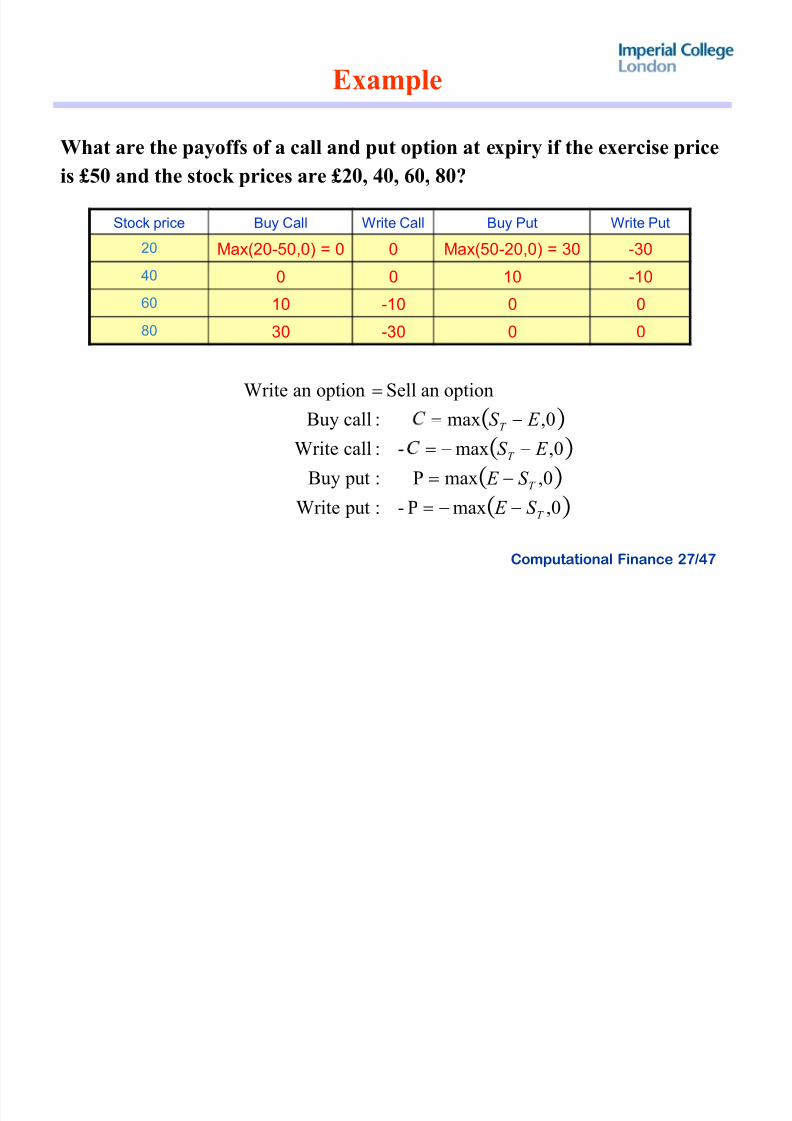

Example

Stock price Buy Call Write Call Buy Put Write Put

20 Max(20-50,0) = 0 0 Max(50-20,0) = 30 -30

40 0 0 10 -1060 10 -10 0 0

80 30 -30 0 0

What are the payoffs of a call and put option at expiry if the exercise price

is £50 and the stock prices are £20, 40, 60, 80?

0,maxP- : putWrite

0,maxP : putBuy

0,max- :callWrite0,max :callBuy

optionanSelloptionanWrite

T

T

T

T

S E

S E

E S

E S

!

!

!!

!

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 28/47

Computational Finance 28/47

Example

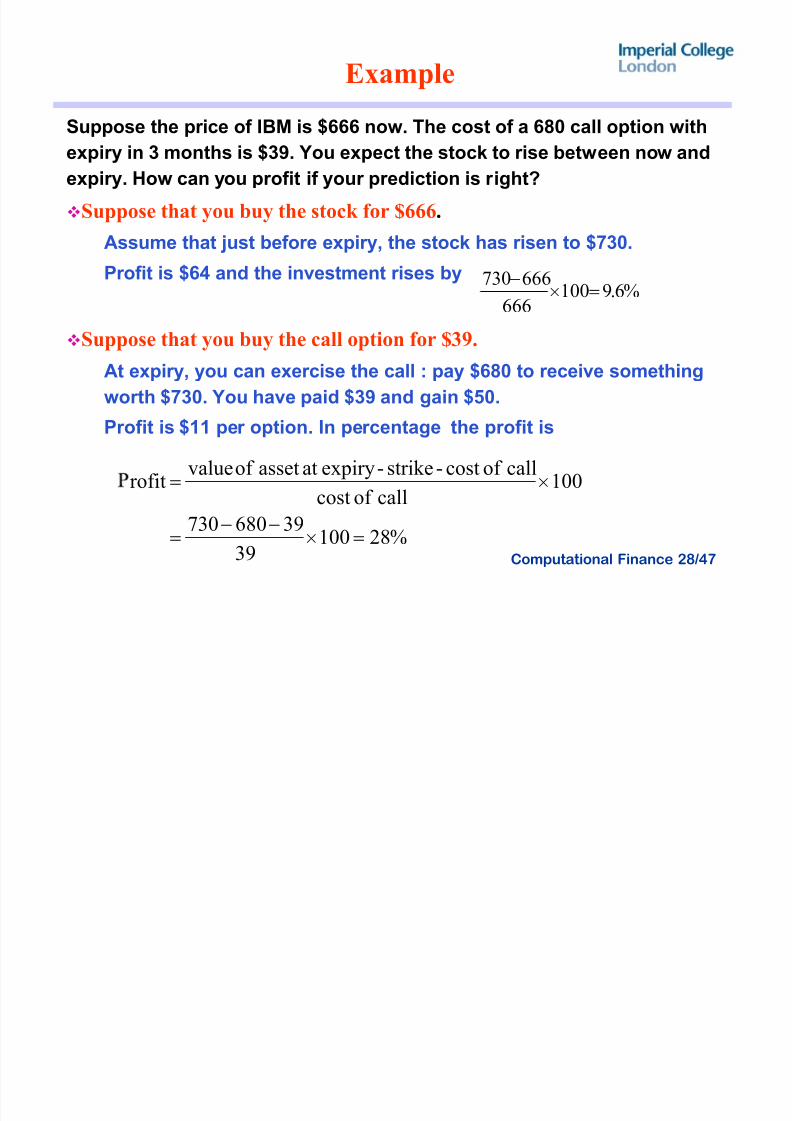

Suppose the price of IBM is $666 now. The cost of a 680 call option with

expiry in 3 months is $39. You expect the stock to rise between now and

expiry. How can you profit if your prediction is right?

Suppose that you buy the stock for $666.

Assume that just before expiry, the stock has risen to $730.

Profit is $64 and the investment rises by

Suppose that you buy the call option for $39.

At expiry, you can exercise the call : pay $680 to receive something

worth $730. You have paid $39 and gain $50.

Profit is $11 per option. In percentage the profit is

%6.9100666

666730 !v

%28100

39

39680730

100callof cost

callof cost-strike-expiryatassetof valuerofit

!v

!

v!

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 29/47

Computational Finance 29/47

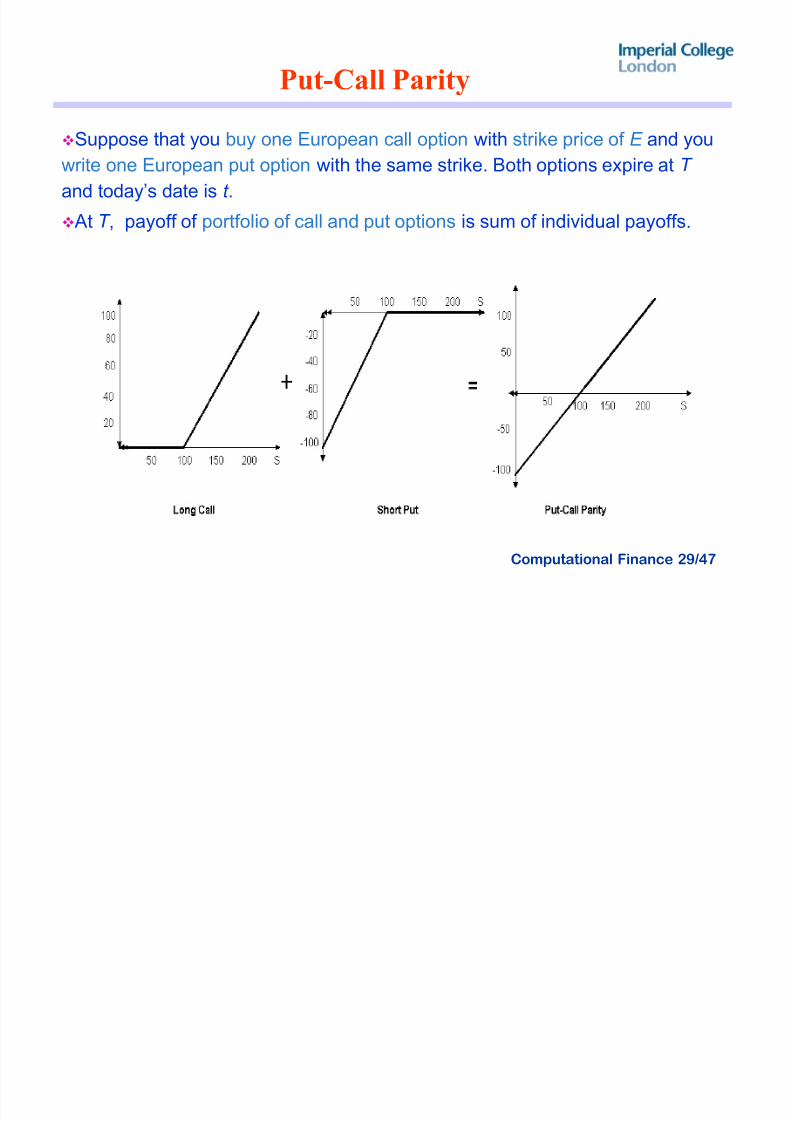

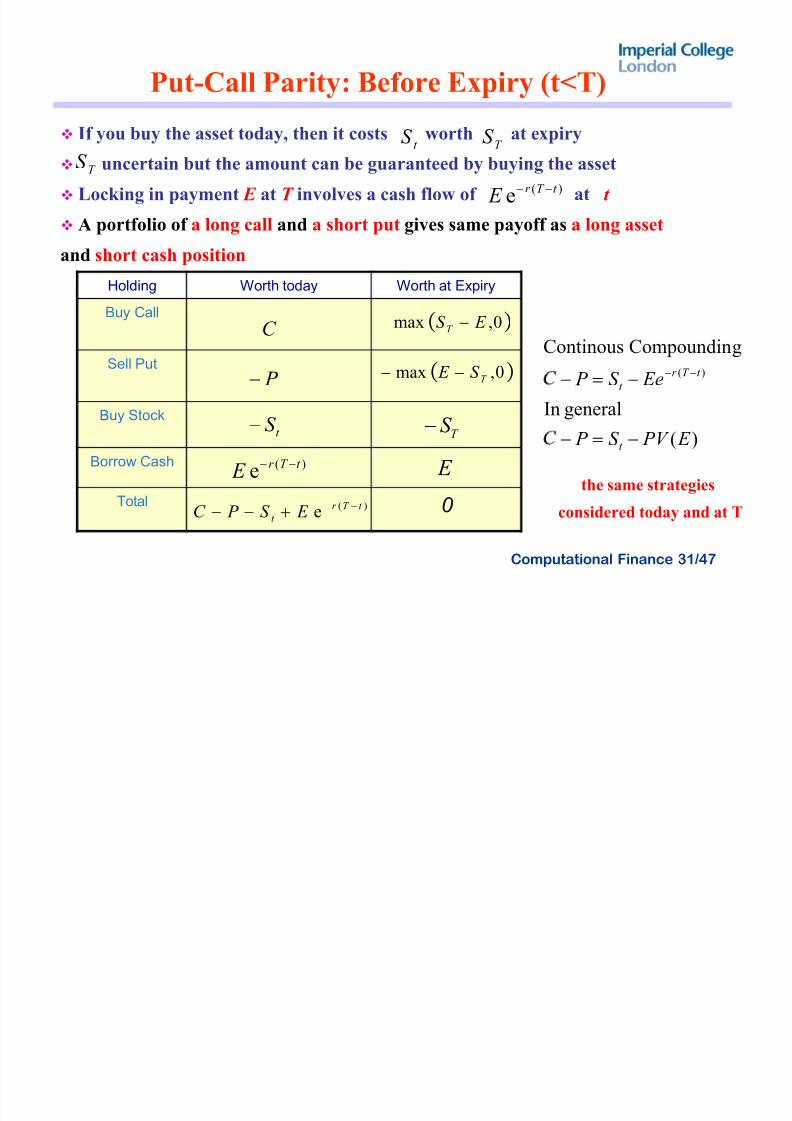

Put-Call Parity

Suppose that you buy one European call option with strike price of E and youwrite one European put option with the same strike. Both options expire at T

and today¶s date is t .

At T , payoff of portfolio of call and put options is sum of individual payoffs.

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 30/47

Computational Finance 30/47

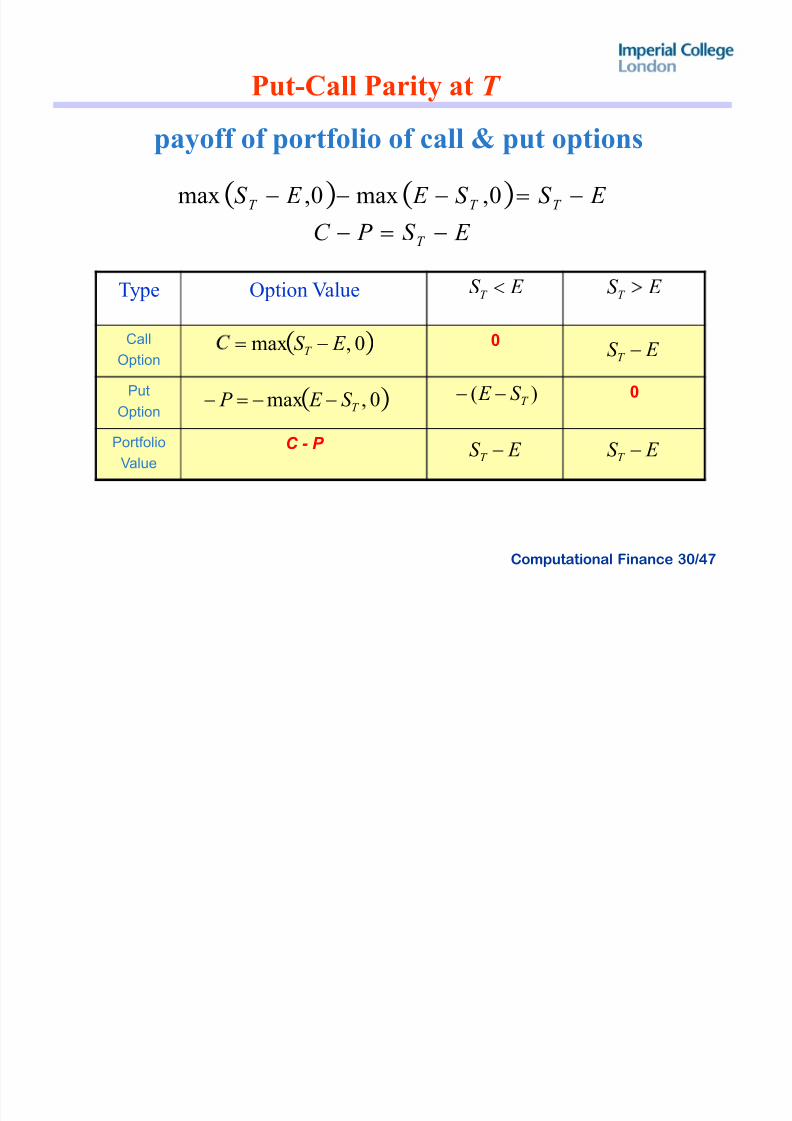

Put-Call Parity at T

Type Option Value

Call

Option

0

Put

Option

0

Portfolio

Value

C - P

0,max E S T !

E S T

0,max T S E P !

E S T

)( T S E

E S T

E S T E S T

E S P C

E S S E E S

T

T T T

!

! 0,max0,max

payoff of portfolio of call & put options

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 31/47

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 32/47

Computational Finance 32/47

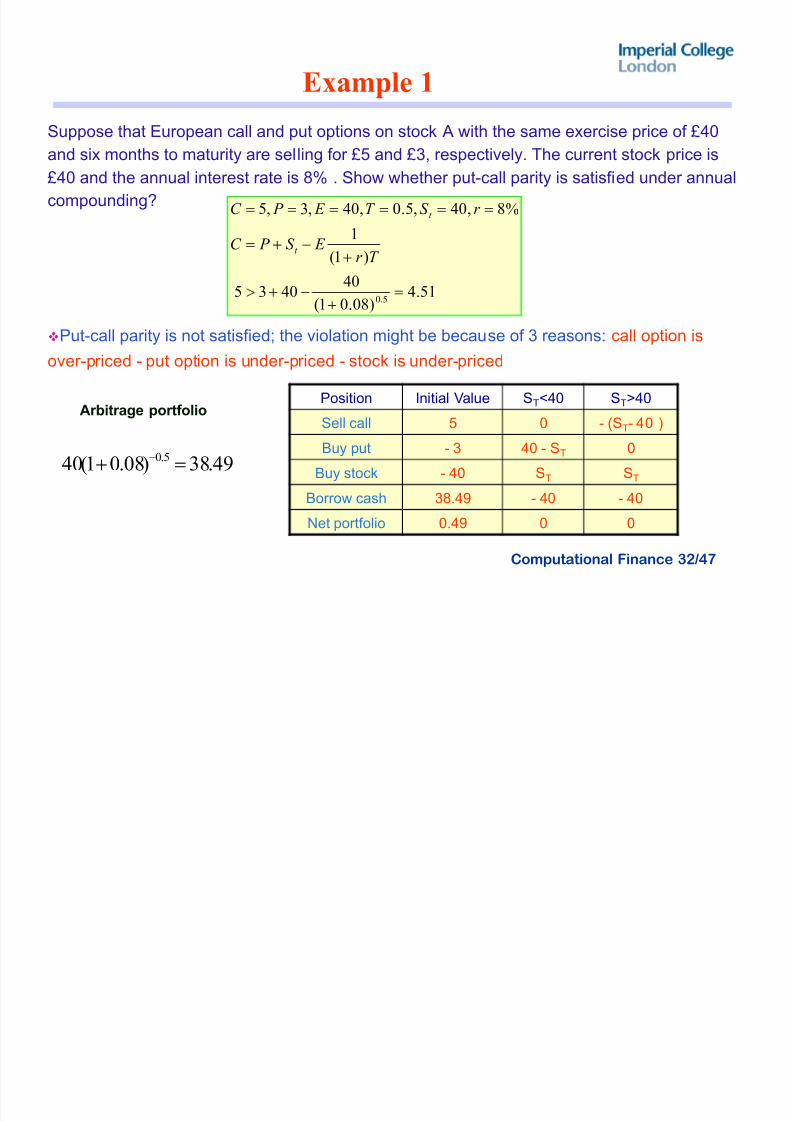

Example 1

Suppose that European call and put options on stock A with the same exercise price of £40

and six months to maturity are selling for £5 and £3, respectively. The current stock price is

£40 and the annual interest rate is 8% . Show whether put-call parity is satisfied under annual

compounding?

Put-call parity is not satisfied; the violation might be because of 3 reasons: call option is

over-priced - put option is under-priced - stock is under-priced

Arbitrage portfolio

51.4)08.01(

404035

)1(

1

%8,40,5.0,40,3,5

5.0!

"

!

!!!!!!

T r E S P C

r S T E P C

t

t

Position Initial Value ST<40 ST>40

Sell call 5 0 - (ST- 40 )

Buy put - 3 40 - ST 0

Buy stock - 40 ST ST

Borrow cash 38.49 - 40 - 40

Net portfolio 0.49 0 0

49.38)08.01(40 5.0 !

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 33/47

Computational Finance 33/47

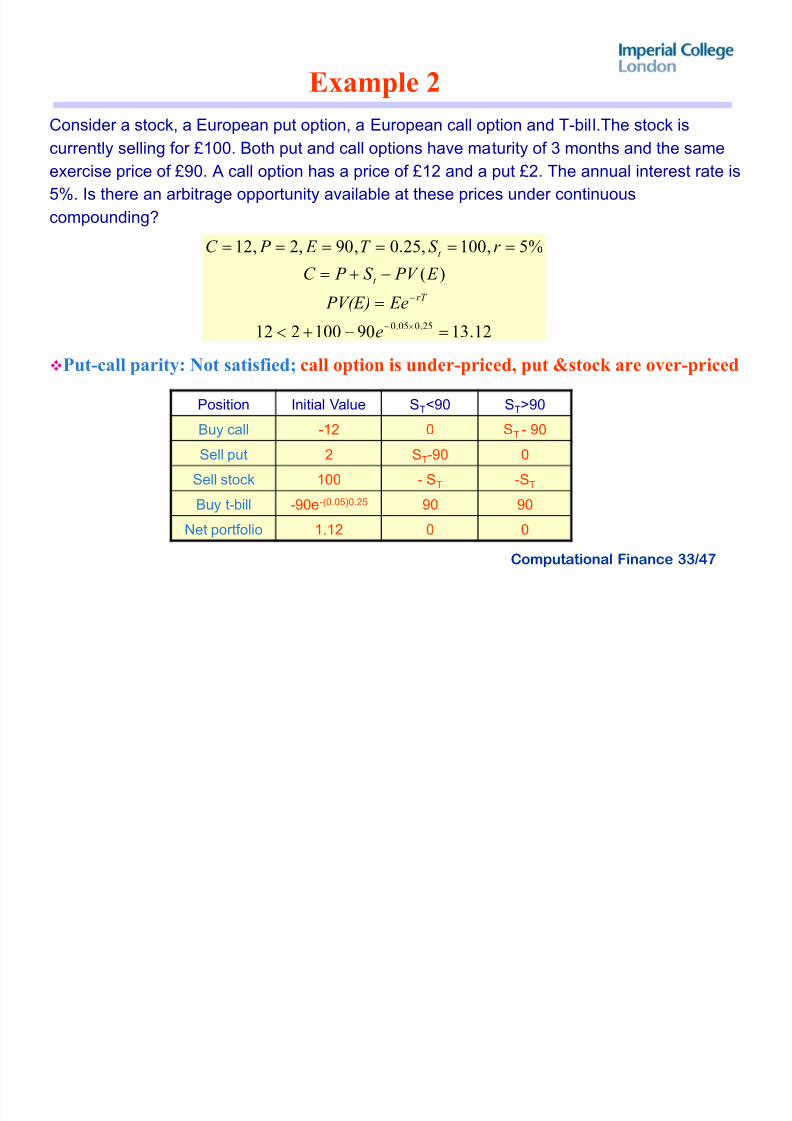

Example 2

Consider a stock, a European put option, a European call option and T-bill.The stock is

currently selling for £100. Both put and call options have maturity of 3 months and the sameexercise price of £90. A call option has a price of £12 and a put £2. The annual interest rate is

5%. Is there an arbitrage opportunity available at these prices under continuous

compounding?

Put-call parity: Not satisfied; call option is under-priced, put &stock are over-priced

12.1390100212

)(

%5,100,25.0,90,2,12

25.005.0 !

!

!

!!!!!!

v

e

E e PV ( E )

E PV S

P C

r S T E P C

rT

t

t

Position Initial Value ST<90 ST>90

Buy call -12 0 ST - 90

Sell put 2 ST-90 0

Sell stock 100 - ST -ST

Buy t-bill -90e-(0.05)0.25 90 90

Net portfolio 1.12 0 0

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 34/47

Computational Finance 34/47

Option Pricing Models

Approaches to option pricing problem based on different

assumptions about market, dynamics of stock price behaviour

Theories based on the arbitrage principle,

applied when dynamics of underlying stock take certain forms

The simplest of these theories is based on binomial model of

stock price fluctuations

widely used in practice since it is simple and easy to calculate

approximation to movement of real prices

generalizes one period ³up-down´ model to multi-period setting

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 35/47

Computational Finance 35/47

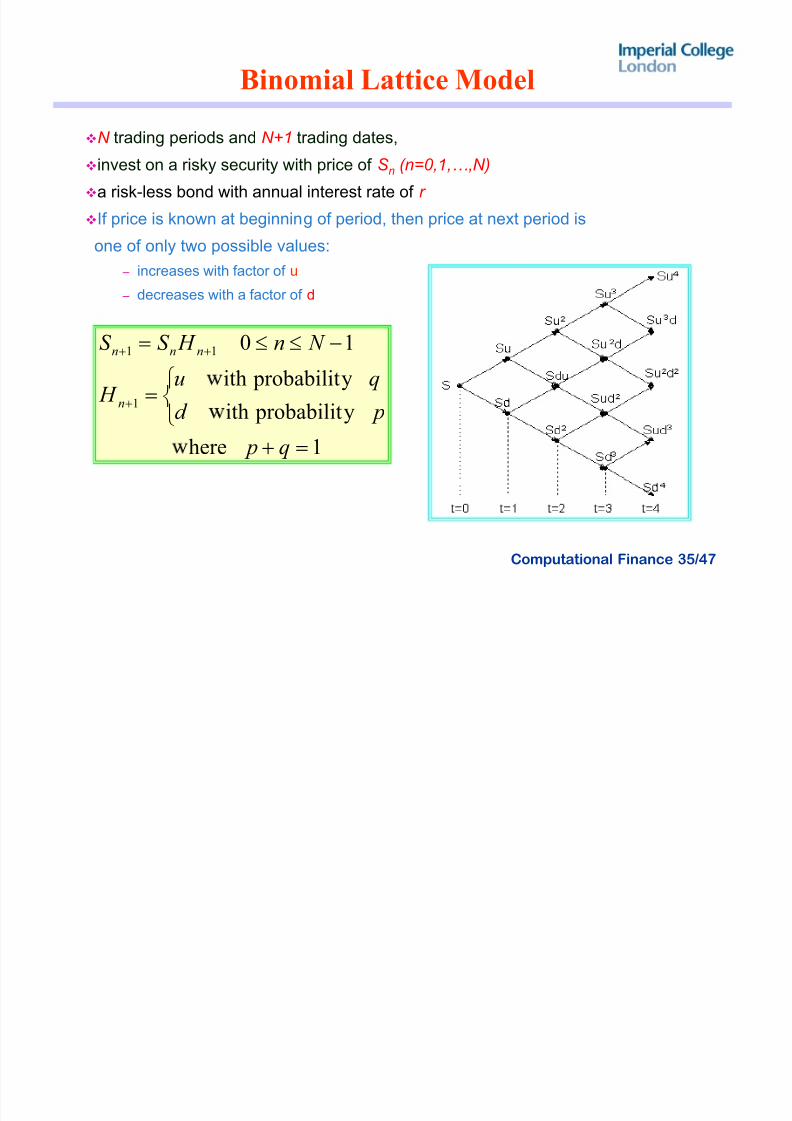

Binomial Lattice Model

N trading periods and N+1

trading dates,invest on a risky security with price of S n (n=0,1,«,N)

a risk-less bond with annual interest rate of r

If price is known at beginning of period, then price at next period is

one of only two possible values:

± increases with factor of u

± decreases with a factor of d

1 here y probabilitith

y probabilitith

10

1

11

!°

¯®

!

ee!

q p pd

qu H

N n H S S

n

nnn

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 36/47

Computational Finance 36/47

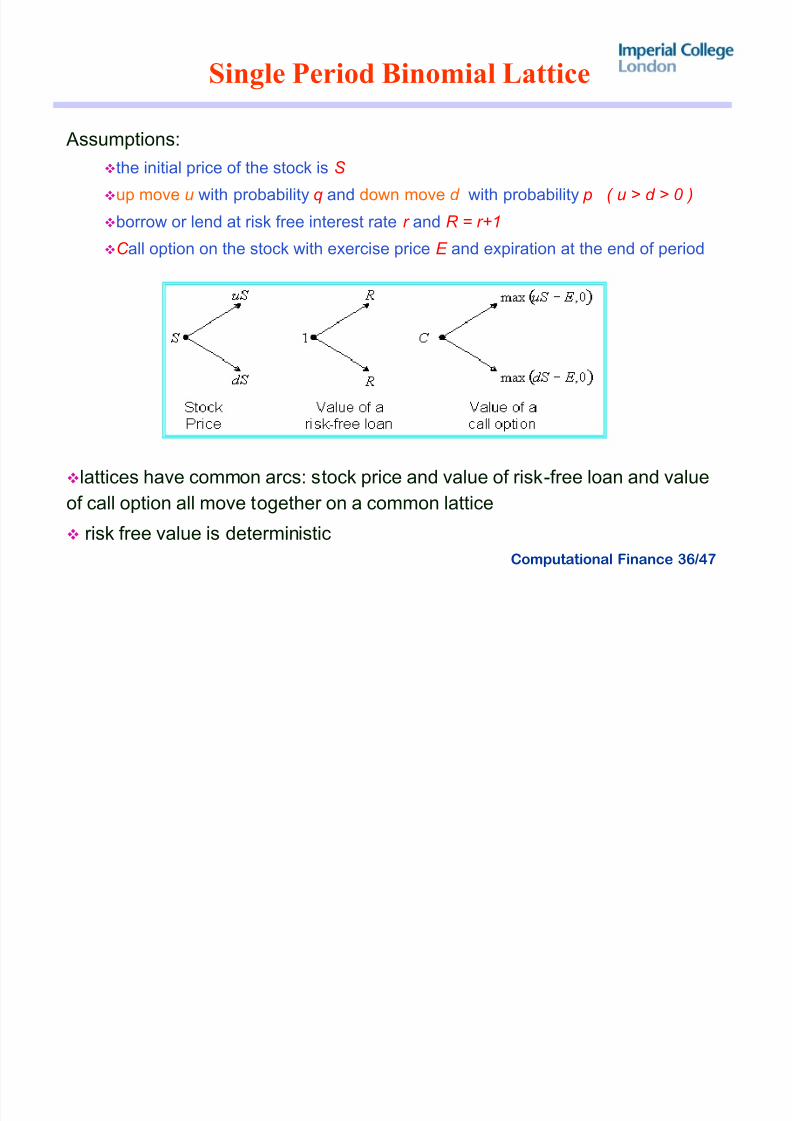

Single Period Binomial Lattice

Assumptions:the initial price of the stock is S

up move u with probability q and down move d with probability p ( u > d > 0 )

borrow or lend at risk free interest rate r and R = r +1

C all option on the stock with exercise price E and expiration at the end of period

lattices have common arcs: stock price and value of risk-free loan and value

of call option all move together on a common lattice

risk free value is deterministic

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 37/47

Computational Finance 37/47

R isk ±Neutral Probability

Based on discounting expected value of option using risk-free rate

For risk-neutral probabilities q and p= 1-q ( 0 < q, p < 1 ) value of one-period call

option on a stock governed by a binomial lattice is found by

taking expected value of option using the probability

discounting this value according to risk ± free rate

risk neutral formula holds for underlying stock

? A

d u

Ruq p pC qC

RC

d u

d RqC qqC

RC

C E R

C

d u

d u

T T

!!!

!!

!

)1( here 1

here)1(1

11

? Ad S qquS

R

S )1(1

!

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 38/47

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 39/47

Computational Finance 39/47

Parameters: Binomial Lattice Model

In order to specify the model completely, chose values of u , d and probabilities p, q

such a way that stochastic nature of stock is captured as much as possible

multiplicative in nature and u , d >0 - Stock price never becomes negative

Expected yearly growth rate

In deterministic process, exponential growth rate

Other parameters

Binomial model match when period of length is smaller and large number of steps is considered

¼½

»¬«

¹¹ º

¸©©ª

¨!

0

lnS

S E v T

vT T

T eS S S S v 0

0

ln !¹¹ º ¸©©

ª¨!

t t

T

ed eu

t

v

q

S

S

(( !!

(¹ º

¸

©ª

¨

!

¼½

»¬«

¹¹ º

¸©©ª

¨!

W W

W

W

,

,2

1

2

1

lnvar 0

2

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 40/47

Computational Finance 40/47

Multi-periodOption Pricing

Single period option pricing model can be extended to

multistage option pricing

Find the stock price evaluation through time periods

Find the option values at expiry using the payoff function.

To find option price, use either

Ri sk Neut ral Di scount ing M ethod Ri sk Neut ral Di scount ing M ethod

or or

R e pli c at ing P or tf oli o M ethod R e pli c at ing P or tf oli o M ethod

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 41/47

Computational Finance 41/47

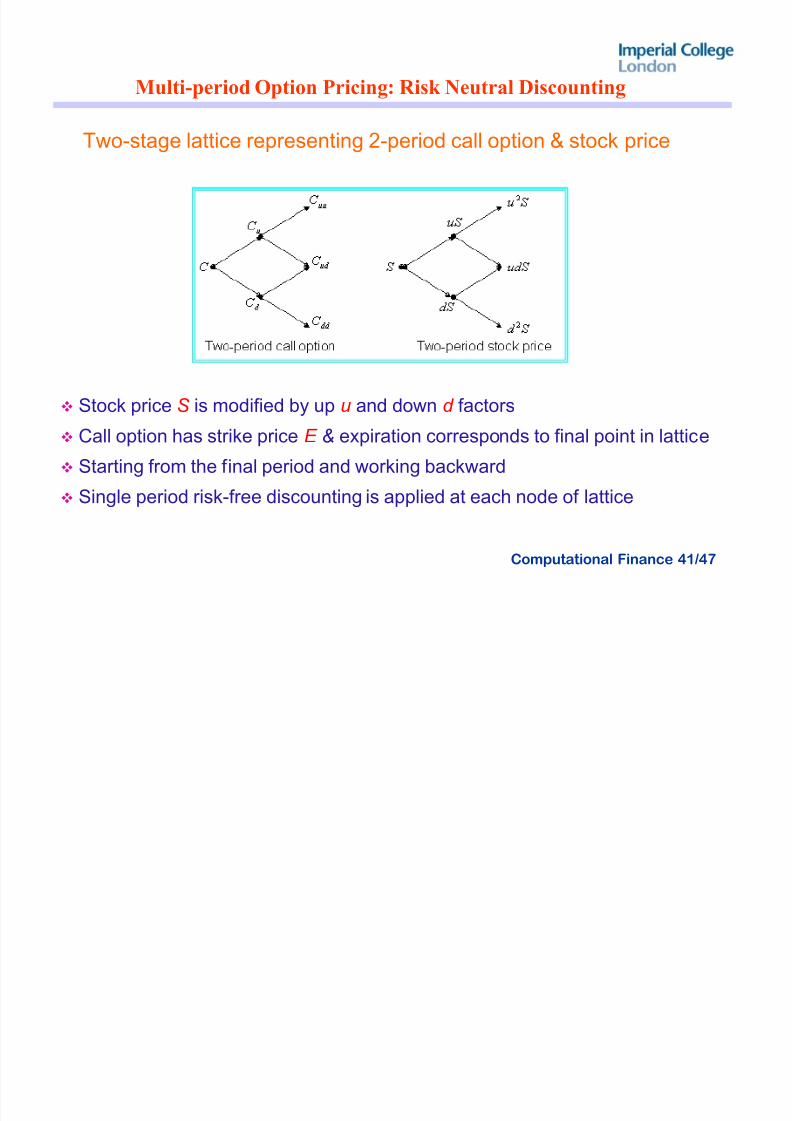

Multi-periodOption Pricing: R isk Neutral Discounting

Two-stage lattice representing 2-period call option & stock price

Stock price S is modified by up u and down d factors

Call option has strike price E & expiration corresponds to final point in lattice

Starting from the final period and working backward

Single period risk-free discounting is applied at each node of lattice

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 42/47

Computational Finance 42/47

Multi-periodOption Pricing : R isk Neutral Discounting

At time period 2, the option value

Risk neutral probability

0,max

0,max

0,max

2

2

E S d C

E udS C

E S uC

dd

ud

uu

!

!

!

? A

? A

? Ad u

dd ud d

ud uuu

C qqC R

C

C qqC R

C

C qqC R

C

)1(1

)1(1

)1(1

!

±±À

±±¿

¾

!

!

d u

Ruq p

d u

d Rq

!!

! 1 and

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 43/47

Computational Finance 43/47

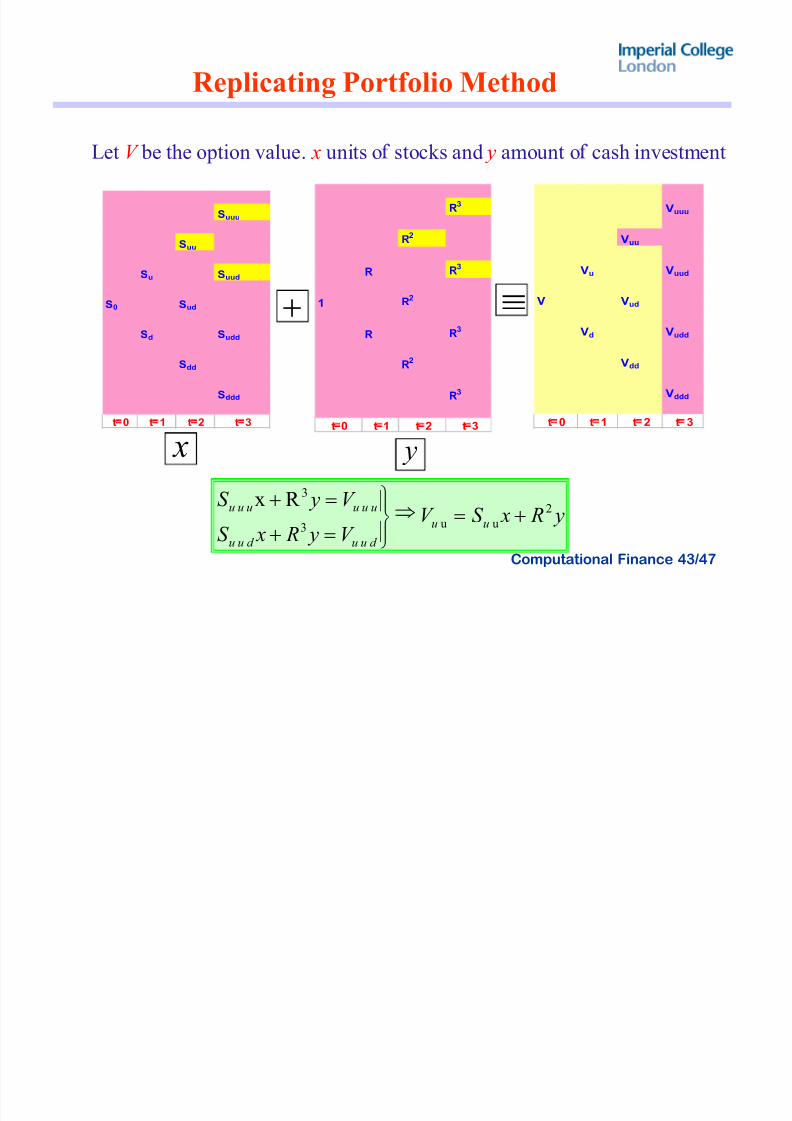

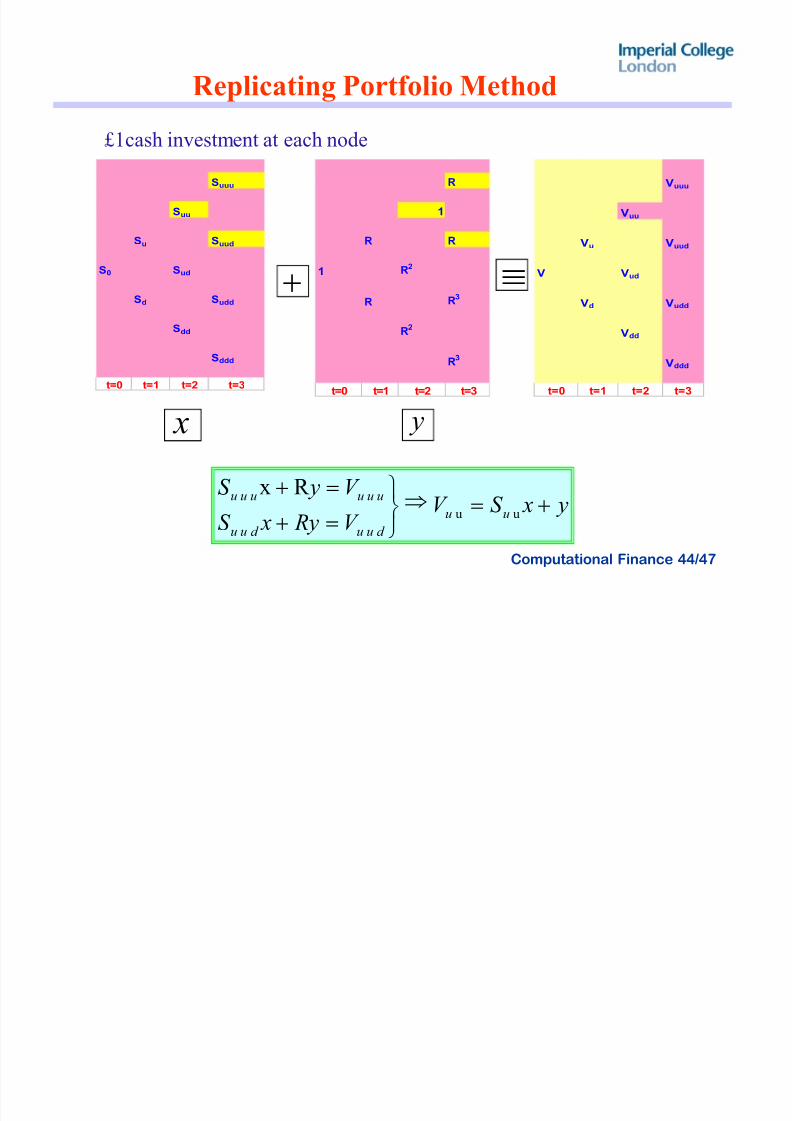

R eplicating Portfolio Method

Suuu

Suu

Su Suud

S0 Sud

Sd Sudd

Sdd

Sddd

t 0 t 1 t 2 t 3

R3

R2

R R3

1 R2

R R3

R2

R3

t 0 t 1 t 2 t 3

Vuuu

Vuu

Vu Vuud

V Vud

Vd Vudd

Vdd

Vddd

t 0 t 1 t 2 t 3

|

x y

y R xS V

V y R xS

V yS uu

d uud uu

uuuuuu 2

uu

3

3

R x!

±À

±¿¾

!

!

Let V be the option value. x units o stocks and y amount o cash investment

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 44/47

Computational Finance 44/47

R eplicating Portfolio Method

Suuu

Suu

Su Suud

S0 Sud

Sd Sudd

Sdd

Sddd

t=0 t=1 t=2 t=3

R

1

R R

1 R2

R R3

R2

R3

t=0 t=1 t=2 t=3

Vuuu

Vuu

Vu Vuud

V Vud

Vd Vudd

Vdd

Vddd

t=0 t=1 t=2 t=3

|

x y

y xS V V R y xS

V yS uu

d uud uu

uuuuuu!

À¿¾

!

!uu

R x

£1cash investment at each node

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 45/47

Computational Finance 45/47

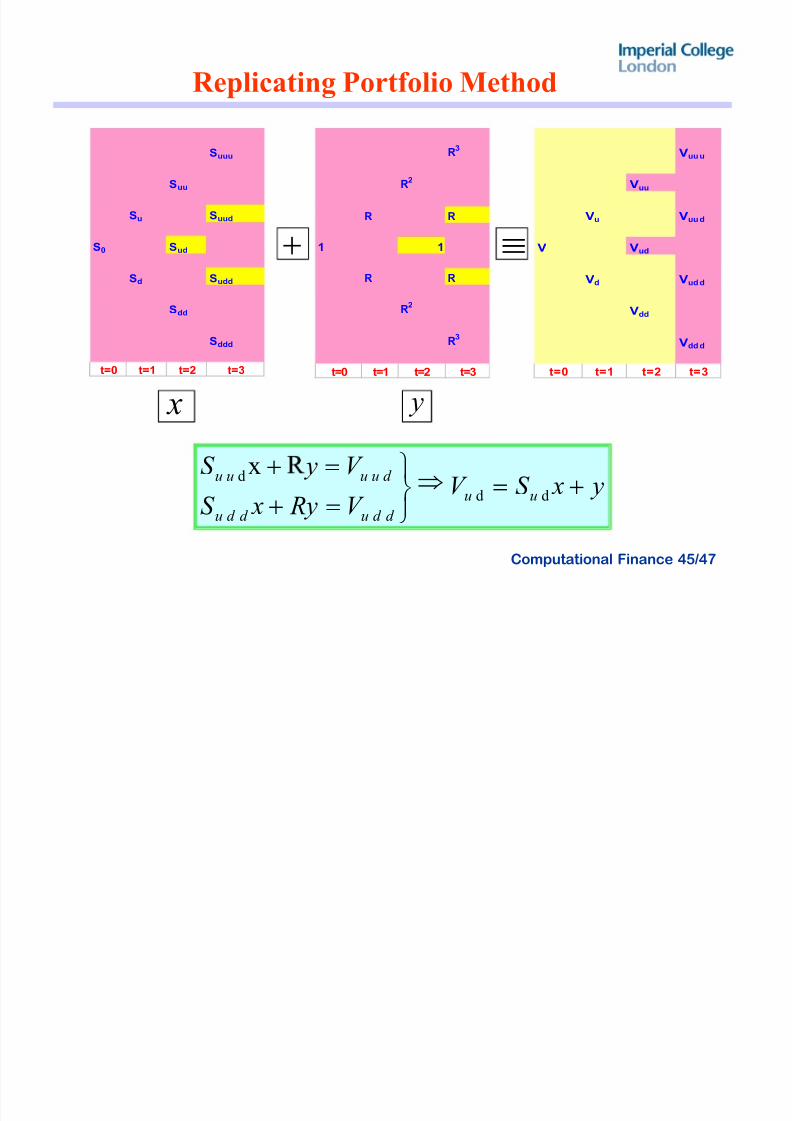

R eplicating Portfolio Method

|

x y

Suuu

Suu

Su Suud

S0 Sud

Sd

Sudd

Sdd

Sddd

t=0 t=1 t=2 t=3

R3

R2

R R

1 1

R R

R2

R3

t=0 t=1 t=2 t=3

Vuu u

Vuu

Vu Vuu d

V Vud

Vd

Vud d

Vdd

Vdd d

t=0 t=1 t=2 t= 3

y xS V V R y xS

V yS uu

d d ud d u

d uuuu!

À¿¾

!

!dd

d x

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 46/47

Computational Finance 46/47

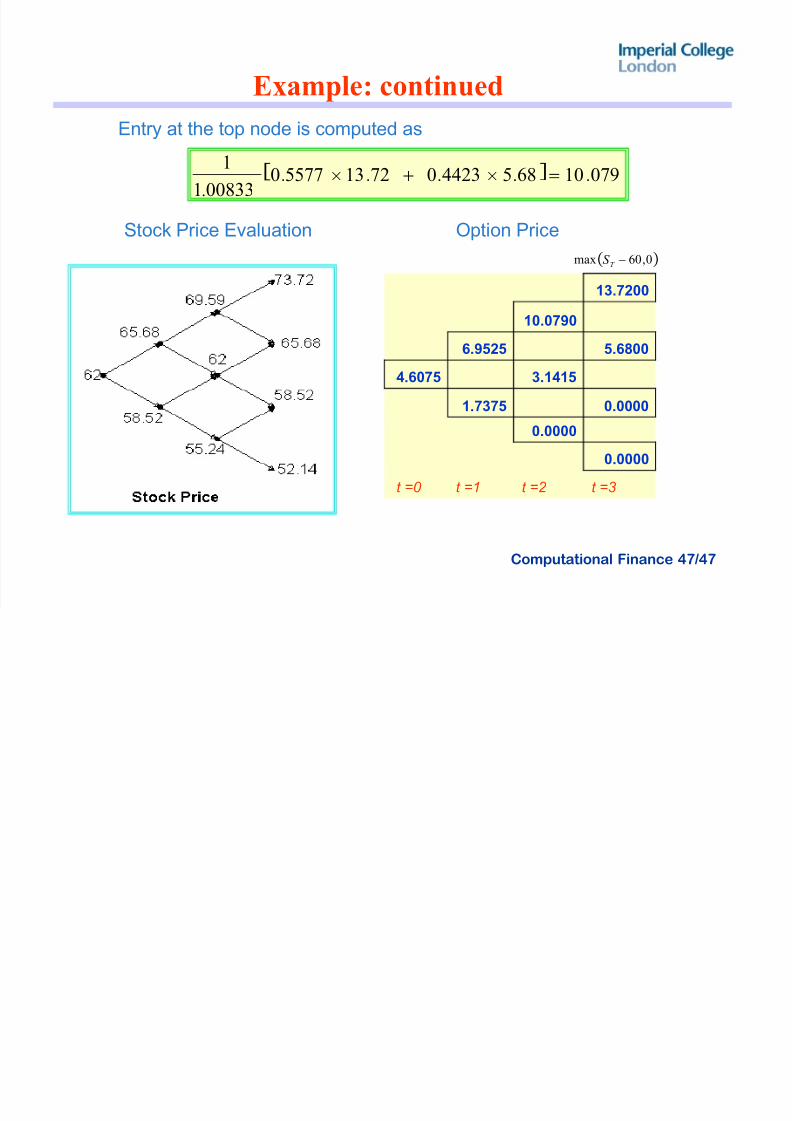

Example:Multi-period Binomial Lattice

Consider a stock with a volatility of The current price of the stock is £62 pays no

dividends. A call option on this stock has an expiration date 3 months from now and strike

price is £60. Current interest rate is 10% compounded monthly. Determine price of call

option by binomial lattice approach.

Time period length is 1 month Risk Neutral Probabilities

20.0!W

00833.112

1.01

94390.0

05943.1

121

!!

!!

!!

!

¡

(

R

ed

eu

t

t

t

W

W

4423.055770.01

5577.0

!!

!

!

p

d u

d Rq

8/7/2019 Options Parity

http://slidepdf.com/reader/full/options-parity 47/47

Computational Finance 47/47

Example: continued

Entry at the top node is computed as

Stock Price Evaluation Option Price

13.7200

10.0790

6.9525 5.6800

4.6075 3.1415

1.7375 0.0000

0.0000

0.0000

t =0 t =1 t =2 t =3

? A 0791068544230721355770008331

1.....

.

!vv

0,60max T S