pnb home laon report

DESCRIPTION

punjab national bank home loan reportTRANSCRIPT

A

PROJECT REPORT ON

“MARKETING OF BANKING ASSESTS HOME LOANS”

SUBMITTED TO

SAVITRIBAI PHULE UNIVERSITY OF PUNE

IN PARTIAL FULFILLMENT OF TWO YEAR FULL TIME

MASTER OF BUSINESS ADMINISTRATION

SUBMITTED BY

AKASH GUPTA

(BATCH -2014-2016)

UNDER THE GUIDANCE OF

PROF.SHRADHA SHINDE

ASM's Institute of Business Management and Research (IBMR)

Block C, MIDC,Chinchwad,

Pune, Maharashtra 411019

ACKNOWLEDGEMENT

I gratefully acknowledge the help and co-operation of the entire

Department of Punjab National Bank (Retail Assests Branch) at the outset; I

would like to thank Mr. Sandeep Sharma for giving me an opportunity to learn at

Punjab National Bank – Retail Assests.

I would like to thank my guide Prof. Shradha Shinde Mam for his

valuable guidance in making my project successful. I also wish to thank the IBMR

staff whose contribution cannot be overemphasized. With all their encouragement

and well wishes, my project proved to be fruitful.

Date:

Place: Pune-411019. (Akash Gupta)

DECLARATION

I hereby declare that the Project Report entitled “Investment in working capital

market analysis” written and submitted by me to the University of Pune in partial

fulfillment of the requirements for the award of degree of Master of Business

Administration under the guidance of Prof. Shradha Shinde is original work and

the conclusions drawn therein are based on the material collected by me.

Date:

Place: CHINCHWAD, (Akash Gupta)

SL NO CONTENTS PAGE NO1 EXECUTIVE SUMMARY2 BANKS IN INDIA3 COMPANY PROFILE4 PRODUCTS AND SERVICES5 OBJECTIVES OF STUDY6 REVIEW OF LITREATURE7 RESEARCH METHODOLY8 DATA ANALYSIS 9 ACTIVITY CHARTS10 INTERPRETATIONS11 CONCLUSIONS & SWOT ANALYSIS12 LIMITATIONS12 BIBLOGRAPHY

EXECUTIVE SUMMARY

The major participants of the Indian financial system are the commercial banks, the financial

institutions (FIs), encompassing term-lending institutions, investment institutions, specialized

financial institutions and the state-level development banks, Non-Bank Financial Companies

(NBFCs) and other market intermediaries such as the stock brokers and money-lenders. The

commercial banks and certain variants of NBFCs are among the oldest of the market

participants. The FIs, on the other hand, are relatively new entities in the financial market place.

Bank of Hindustan, set up in 1870, was the earliest Indian Bank . Banking in India on

modern lines started with the establishment of three presidency banks under Presidency Bank's

act 1876 i.e. Bank of Calcutta, Bank of Bombay and Bank of Madras. In 1921, all presidency

banks were amalgamated to form the Imperial Bank of India. Imperial bank carried out limited

central banking functions also prior to establishment of RBI. It engaged in all types of

commercial banking business except dealing in foreign exchange.

Reserve Bank of India Act was passed in 1934 & Reserve Bank of India (RBI) was

constituted as an apex bank without major government ownership. Banking Regulations Act was

passed in 1949. This regulation brought Reserve Bank of India under government control. Under

the act, RBI got wide ranging powers for supervision & control of banks. The Act also vested

licensing powers & the authority to conduct inspections in RBI

In 1955, RBI acquired control of the Imperial Bank of India, which was renamed as State Bank of India. In 1959, SBI took over control of eight private banks floated in the erstwhile princely states, making them as its 100% subsidiaries.

RBI was empowered in 1960, to force compulsory merger of weak banks with the strong ones. The total number of banks was thus reduced from 566 in 1951 to 85 in 1969. In July 1969, government nationalised 14 banks having deposits of Rs.50 crores & above. In 1980, government acquired 6 more banks with deposits of more than Rs.200 crores. Nationalisation of banks was to make them play the role of catalytic agents for economic growth. The Narsimham Committee report suggested wide ranging reforms for the banking sector in 1992 to introduce internationally accepted banking practices.

The amendment of Banking Regulation Act in 1993 saw the entry of new private sector banks.

Banking Segment in India functions under the umbrella of Reserve Bank of India - the regulatory, central bank. This segment broadly consists of:

Commercial; Banks

Co-operative Banks

Commercial Banks

The commercial banking structure in India consists of:

Scheduled Commercial Banks

Unscheduled Banks

Scheduled commercial Banks constitute those banks which have been included in the

Second Schedule of Reserve Bank of India(RBI) Act, 1934. RBI in turn includes only those

banks in this schedule which satisfy the criteria laid down vide section 42 (60 of the Act. Some

co-operative banks are scheduled commercial banks albeit not all co-operative banks are. Being a

part of the second schedule confers some benefits to the bank in terms of access to accomodation

by RBI during the times of liquidity constraints. At the same time, however, this status also

subjects the bank certain conditions and obligation towards the reserve regulations of RBI. This

sub sector can broadly be classified into:

1. Public sector

2. Private sector

3. Foreign banks.

CO-OPERATIVE BANKS

There are two main categories of the co-operative banks.

(a) Short term lending oriented co-operative Banks - within this category there are

three sub categories of banks viz state co-operative banks, District co-operative banks and

society.

(b) Long term lending oriented co-operative Banks - within the second category there

are land development banks at three levels state level, district level and village level.

The co-operative banking structure in India is divided into following main 5 categories:

1. Primary Urban Co-op Banks.

2. Primary Agricultural Credit Societies.

3. District Central Co-op Banks.

4, State Co-operative Banks.

5. Land Development Banks

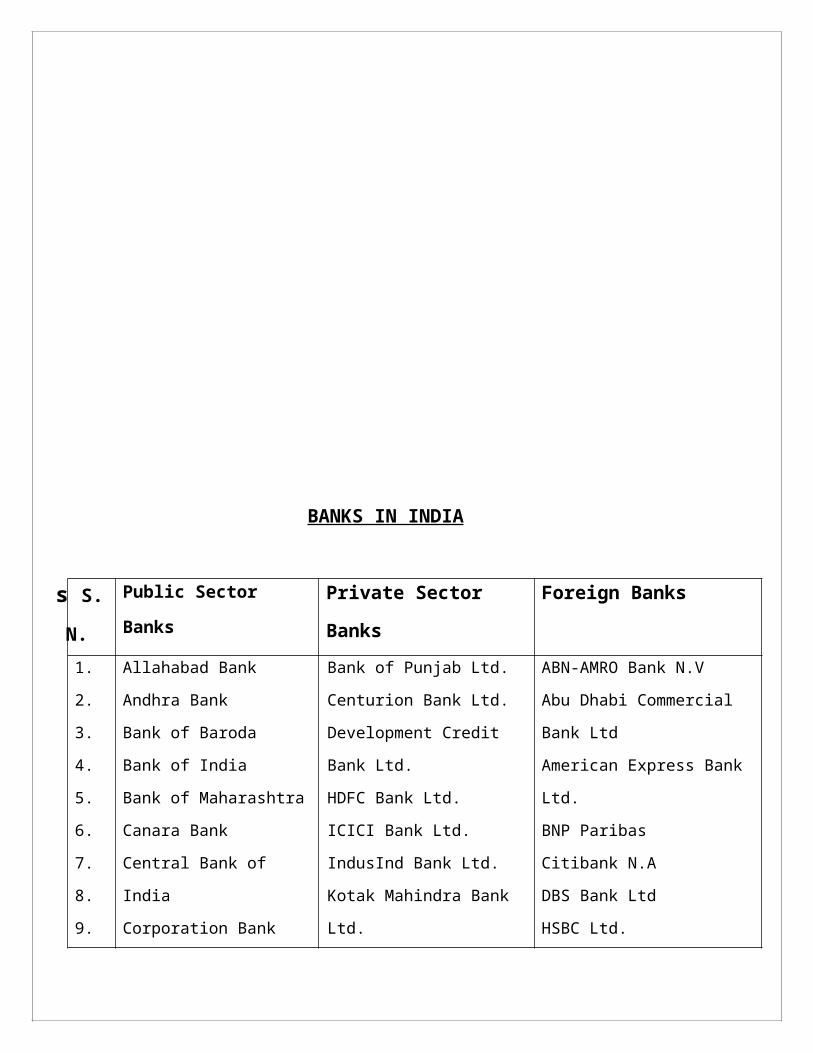

BANKS IN INDIA

s S. N. Public Sector Banks Private Sector

Banks

Foreign Banks

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

Allahabad Bank

Andhra Bank

Bank of Baroda

Bank of India

Bank of Maharashtra

Canara Bank

Central Bank of India

Corporation Bank

Dena Bank

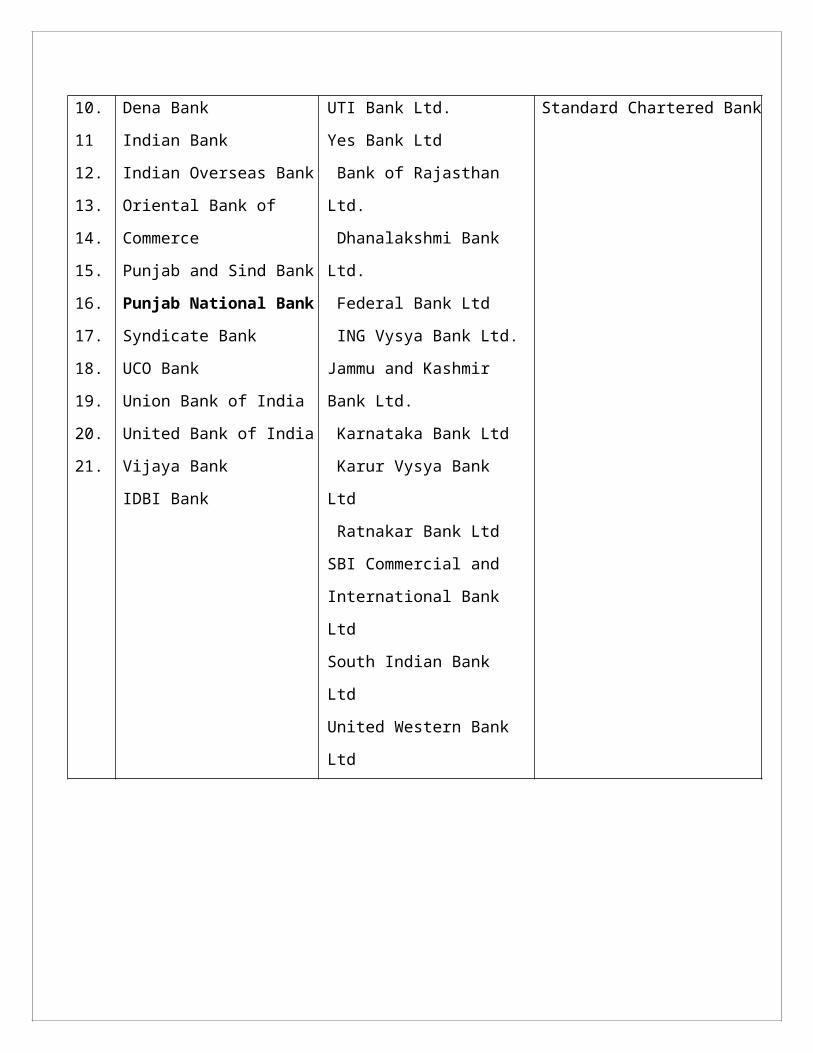

Indian Bank

Indian Overseas Bank

Oriental Bank of Commerce

Punjab and Sind Bank

Punjab National Bank

Syndicate Bank

UCO Bank

Union Bank of India

United Bank of India

Vijaya Bank

IDBI Bank

Bank of Punjab Ltd.

Centurion Bank Ltd.

Development Credit Bank Ltd.

HDFC Bank Ltd.

ICICI Bank Ltd.

IndusInd Bank Ltd.

Kotak Mahindra Bank Ltd.

UTI Bank Ltd.

Yes Bank Ltd

Bank of Rajasthan Ltd.

Dhanalakshmi Bank Ltd.

Federal Bank Ltd

ING Vysya Bank Ltd.

Jammu and Kashmir Bank Ltd.

Karnataka Bank Ltd

Karur Vysya Bank Ltd

Ratnakar Bank Ltd

SBI Commercial and

International Bank Ltd

South Indian Bank Ltd

United Western Bank Ltd

ABN-AMRO Bank N.V

Abu Dhabi Commercial Bank Ltd

American Express Bank Ltd.

BNP Paribas

Citibank N.A

DBS Bank Ltd

HSBC Ltd.

Standard Chartered Bank

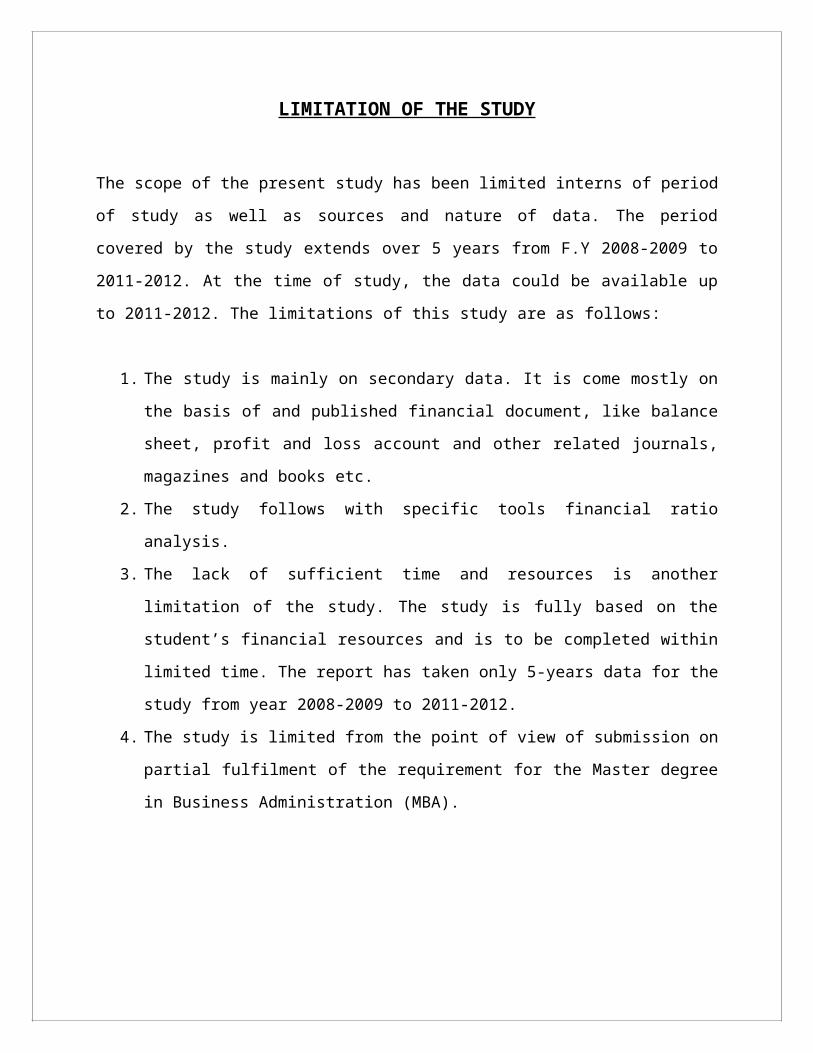

LIMITATION OF THE STUDY

The scope of the present study has been limited interns of period of study as well as sources and

nature of data. The period covered by the study extends over 5 years from F.Y 2008-2009 to

2011-2012. At the time of study, the data could be available up to 2011-2012. The limitations of

this study are as follows:

1. The study is mainly on secondary data. It is come mostly on the basis of and published

financial document, like balance sheet, profit and loss account and other related journals,

magazines and books etc.

2. The study follows with specific tools financial ratio analysis.

3. The lack of sufficient time and resources is another limitation of the study. The study is

fully based on the student’s financial resources and is to be completed within limited

time. The report has taken only 5-years data for the study from year 2008-2009 to 2011-

2012.

4. The study is limited from the point of view of submission on partial fulfilment of the

requirement for the Master degree in Business Administration (MBA).

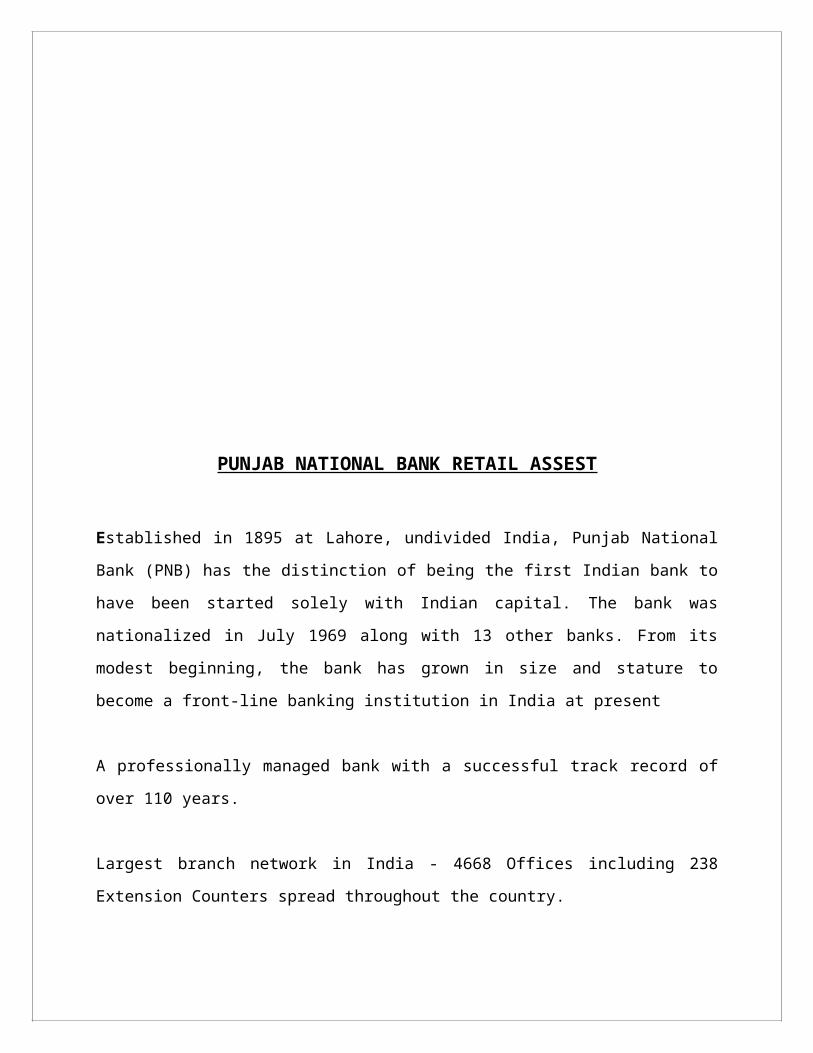

PUNJAB NATIONAL BANK RETAIL ASSEST

Established in 1895 at Lahore, undivided India, Punjab National Bank (PNB) has the distinction

of being the first Indian bank to have been started solely with Indian capital. The bank was

nationalized in July 1969 along with 13 other banks. From its modest beginning, the bank has

grown in size and stature to become a front-line banking institution in India at present

A professionally managed bank with a successful track record of over 110 years.

Largest branch network in India - 4668 Offices including 238 Extension Counters spread

throughout the country.

Strategic business area covers the large Indo-Genetic belt and the metropolitan centres.

Ranked as 248th biggest bank in the world by Bankers Almanac, London.

Strong correspondent banking relationships with more than 217 international banks of the world.

More than 50 renowned international banks maintain their Rupee Accounts with PNB.

Well equipped dealing rooms; 20 different foreign currency accounts are maintained at major

centres all over the globe.

Rupee drawing arrangements with M/s UAE Exchange Centre, UAE, M/s Al Fardan Exchange

Co. Doha, Qatar, M/s Bahrain Exchange Co, Kuwait, M/s Bahrain Finance Co, Bahrain, M/s

Thomas Cook Al Rostamani Exchange Co. Dubai, UAE, and M/s Musandam Exchange, Ruwi,

Sultanate of Oman.

With over 38 million satisfied customers and 4668 offices, PNB has continued to retain its

leadership position among the nationalized banks. The bank enjoys strong fundamentals, large

franchise value and good brand image. Besides being ranked as one of India's top service brands,

PNB has remained fully committed to its guiding principles of sound and prudent banking. Apart

from offering banking products, the bank has also entered the credit card & debit card business;

bullion business; life and non-life insurance business; Gold coins & asset management business,

etc.

Since its humble beginning in 1895 with the distinction of being the first Indian bank to have

been started with Indian capital, PNB has achieved significant growth in business which at the

end of March 2009 amounted to Rs 3, 64,463 crore. Today, with assets of more than Rs 2,

46,900 crore, PNB is ranked as the 3rd largest bank in the country (after SBI and ICICI Bank)

and has the 2nd largest network of branches (4668 including 238 extension counters and 3

overseas offices).During the FY 2008-09, with 39% share of low cost deposits, the bank

achieved a net profit of Rs 3,091 crore, maintaining its number ONE position amongst

nationalized banks. Bank has a strong capital base with capital adequacy ratio as per Basel II at

14.03% with Tier I and Tier II capital ratio at 8.98% and 5.05% respectively as on March’09. As

on March’09, the Bank has the Gross and Net NPA ratio of only 1.77% and 0.17% respectively.

During the FY 2008-09, its’ ratio of priority sector credit to adjusted net bank credit at 41.53% &

agriculture credit to adjusted net bank credit at 19.72% was also higher than the respective

national goals of 40% & 18%.

PNB has always looked at technology as a key facilitator to provide better customer service and

ensured that its ‘IT strategy’ follows the ‘Business strategy’ so as to arrive at “Best Fit”. The

bank has made rapid strides in this direction. Along with the achievement of 100% branch

computerization, one of the major achievements of the Bank is covering all the branches of the

Bank under Core Banking Solution (CBS), thus covering 100% of it’s business and providing

‘Anytime Anywhere’ banking facility to all customers including customers of more than 2000

rural branches. The bank has also been offering Internet banking services to the customers of

CBS branches like booking of tickets, payment of bills of utilities, purchase of airline tickets etc.

Towards developing a cost effective alternative channels of delivery, the bank with more than

2150 ATMs has the largest ATM network amongst Nationalised Banks.

With the help of advanced technology, the Bank has been a frontrunner in the industry so far as

the initiatives for Financial Inclusion is concerned. With it’s policy of inclusive growth in the

Indo-Gangetic belt, the Bank’s mission is “Banking for card based technology enabled Financial

Inclusion with the help of Business Correspondents/Business Facilitators (BC/BF) so as to reach

out to the last mile customer. The BC/BF will address the outreach issue while technology will

provide cost effective and transparent services. The Bank has started several innovative

initiatives for marginal groups like rickshaw pullers, vegetable vendors, diary farmers,

construction workers, etc. The Bank has already achieved 100% financial inclusion in 21,408

villages.

Backed by strong domestic performance, the bank is planning to realize its global aspirations. In

order to increase its international presence, the Bank continues its selective foray in international

markets with presence in Hong Kong, Dubai, Kazakhstan, UK, Shanghai, Singapore, Kabul and

Norway. A second branch in Hong Kong at Kowloon was opened in the first week of April’09.

Bank is also in the process of establishing its presence in China, Bhutan, DIFC Dubai, Canada

and Singapore. The bank also has a joint venture with Everest Bank Ltd. (EBL), Nepal. Under

the long term vision, Bank proposes to start its operation in Fiji Island, Australia and Indonesia.

Bank continues with its goal to become a household brand

With global expertise. Amongst Top 1000 Banks in the World, ‘The Banker’ listed PNB at 250th

place. Further, PNB is at the 1166th position among 48 Indian firms making it to a list of the

world’s biggest companies compiled by the US magazine ‘Forbes’.

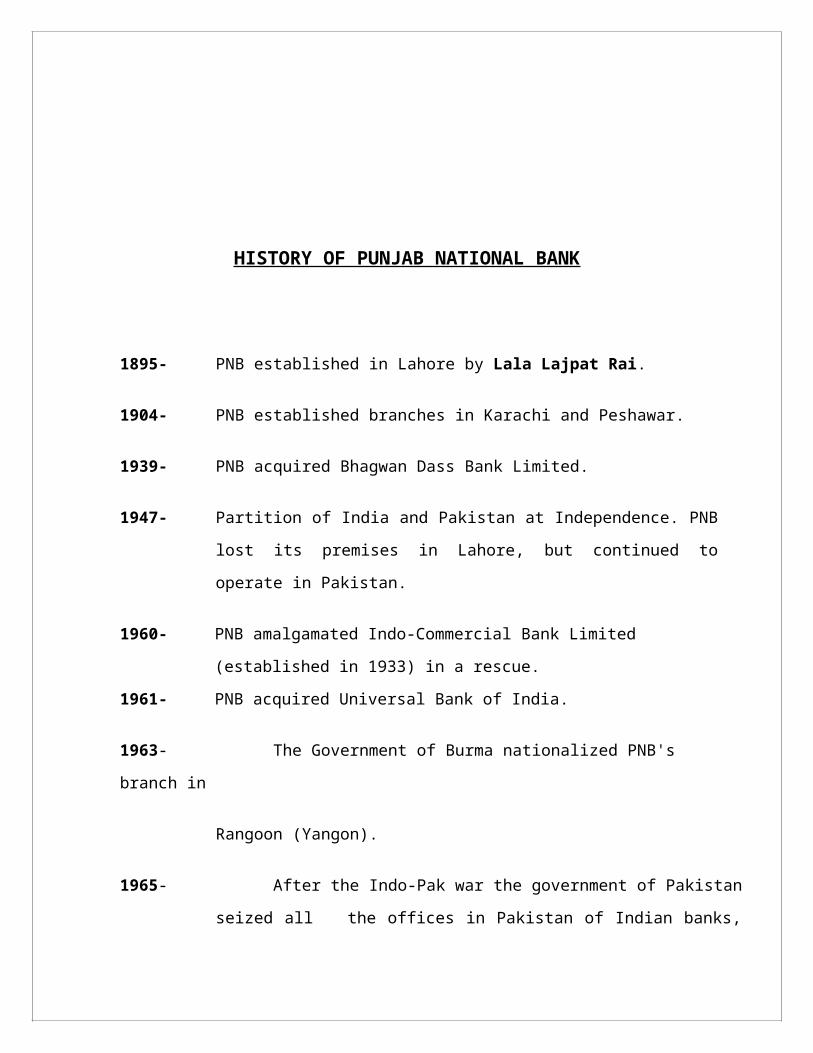

HISTORY OF PUNJAB NATIONAL BANK

1895- PNB established in Lahore by Lala Lajpat Rai.

1904- PNB established branches in Karachi and Peshawar.

1939- PNB acquired Bhagwan Dass Bank Limited.

1947- Partition of India and Pakistan at Independence. PNB lost its premises in

Lahore, but continued to operate in Pakistan.

1960- PNB amalgamated Indo-Commercial Bank Limited (established in 1933)

in a rescue.

1961- PNB acquired Universal Bank of India.

1963- The Government of Burma nationalized PNB's branch in

Rangoon (Yangon).

1965- After the Indo-Pak war the government of Pakistan seized all the offices in

Pakistan of Indian banks, including PNB's head office, which may have moved to

Karachi. PNB also had branches in East Pakistan (Bangladesh).

1969- The Government of India nationalized PNB and 13 other major banks on

19th July, 1969.

1978- PNB opened a branch in London.

1988- PNB acquired Hindustan Commercial Bank Limited in a rescue.

1993- PNB acquired New Bank of India, which the Government of India had

nationalized in 1980.

1998- PNB set up a representative office in Almaty, Kazakhstan.

2003- PNB took over Nedungadi Bank (established the bank in 1899), the oldest

private sector bank in Kerala. It was incorporated in 1913 and in 1965 had

acquired selected assets and deposits of the Coimbatore National Bank. At the

time of the merger with PNB, Nedungadi Bank's shares had zero value, with

the result that its shareholders received no payment for their shares.

VISION

"To be a Leading Global Bank with Pan India footprints and become a

household brand in the Indo-Gangetic Plains providing entire range of

financial products and services under one roof"

MISSION

"Banking for the unbanked

PERFORMANCE OF BANK

FINANCIAL PERFORMANCE OF PNB

AWARDS & RECOGNITION

Financial Performance of the Bank

Punjab National Bank continues to maintain its frontline position retained its NUMBER ONE

position among the nationalized banks in terms of number of branches, Deposit, Advances, total

Business, operating and net profit in the year 2008-09. The impressive operational and financial

performance has been brought about by Bank’s focus on customer based business with thrust on

SME, Agriculture, more inclusive approach to banking; better asset liability management;

improved margin management, thrust on recovery and increased efficiency in core operations of

the Bank. The performance highlights of the bank in terms of business and profit are shown

below:

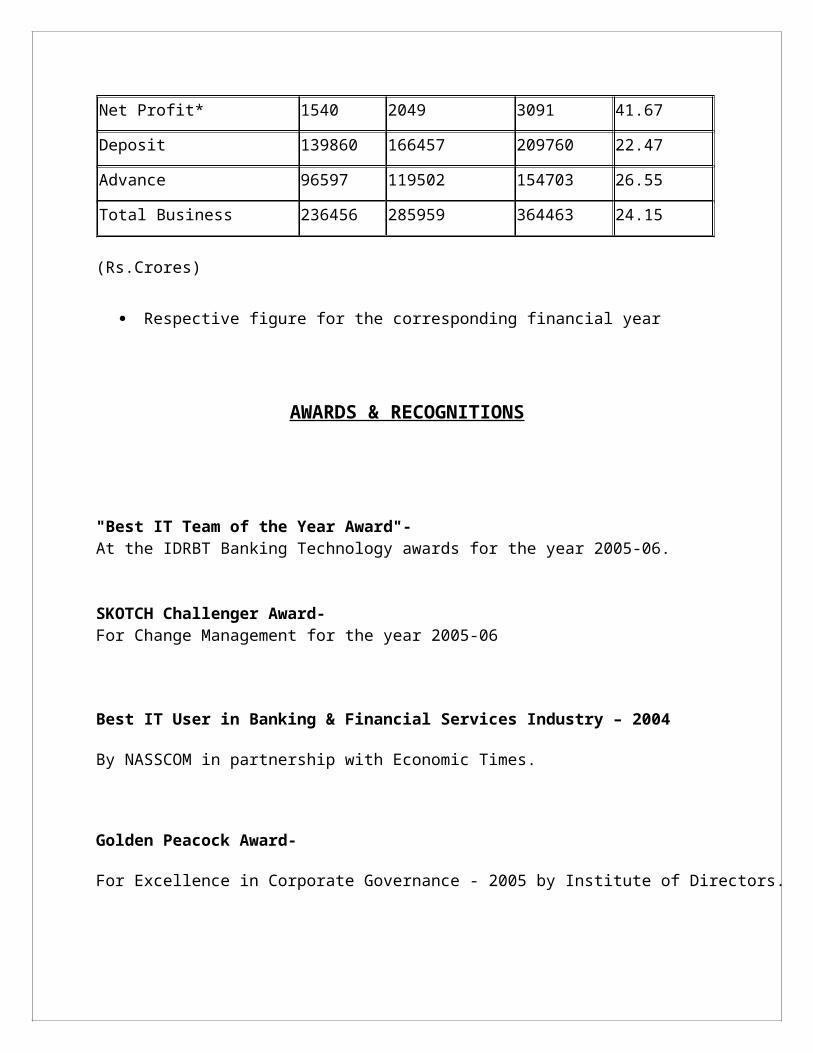

Parameters Mar'07 Mar'08 Mar'09 CRAR

Operating Profit* 3617 4006 5744 26.02

Net Profit* 1540 2049 3091 41.67

Deposit 139860 166457 209760 22.47

Advance 96597 119502 154703 26.55

Total Business 236456 285959 364463 24.15

(Rs.Crores)

Respective figure for the corresponding financial year

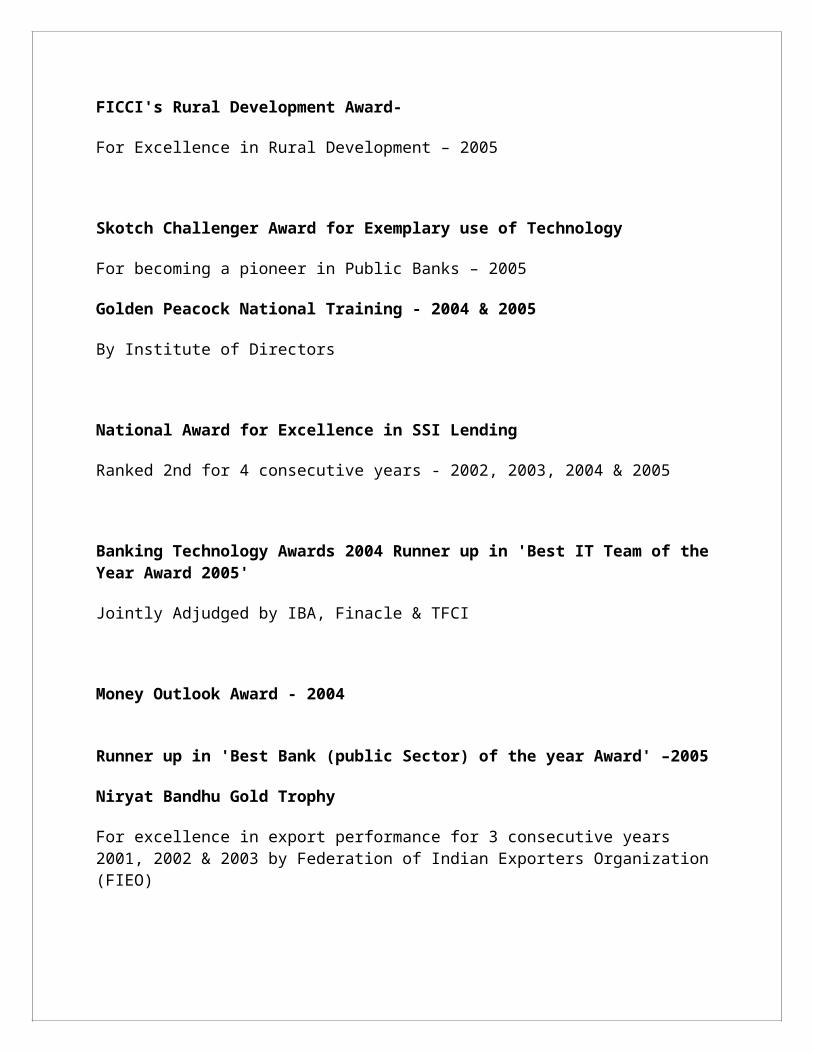

AWARDS & RECOGNITIONS

"Best IT Team of the Year Award"- At the IDRBT Banking Technology awards for the year 2005-06.

SKOTCH Challenger Award-For Change Management for the year 2005-06

Best IT User in Banking & Financial Services Industry – 2004

By NASSCOM in partnership with Economic Times.

Golden Peacock Award-

For Excellence in Corporate Governance - 2005 by Institute of Directors.

FICCI's Rural Development Award-

For Excellence in Rural Development – 2005

Skotch Challenger Award for Exemplary use of Technology

For becoming a pioneer in Public Banks – 2005

Golden Peacock National Training - 2004 & 2005

By Institute of Directors

National Award for Excellence in SSI Lending

Ranked 2nd for 4 consecutive years - 2002, 2003, 2004 & 2005

Banking Technology Awards 2004 Runner up in 'Best IT Team of the Year Award 2005'

Jointly Adjudged by IBA, Finacle & TFCI

Money Outlook Award - 2004

Runner up in 'Best Bank (public Sector) of the year Award' –2005

Niryat Bandhu Gold Trophy

For excellence in export performance for 3 consecutive years 2001, 2002 & 2003 by Federation of Indian Exporters Organization (FIEO)

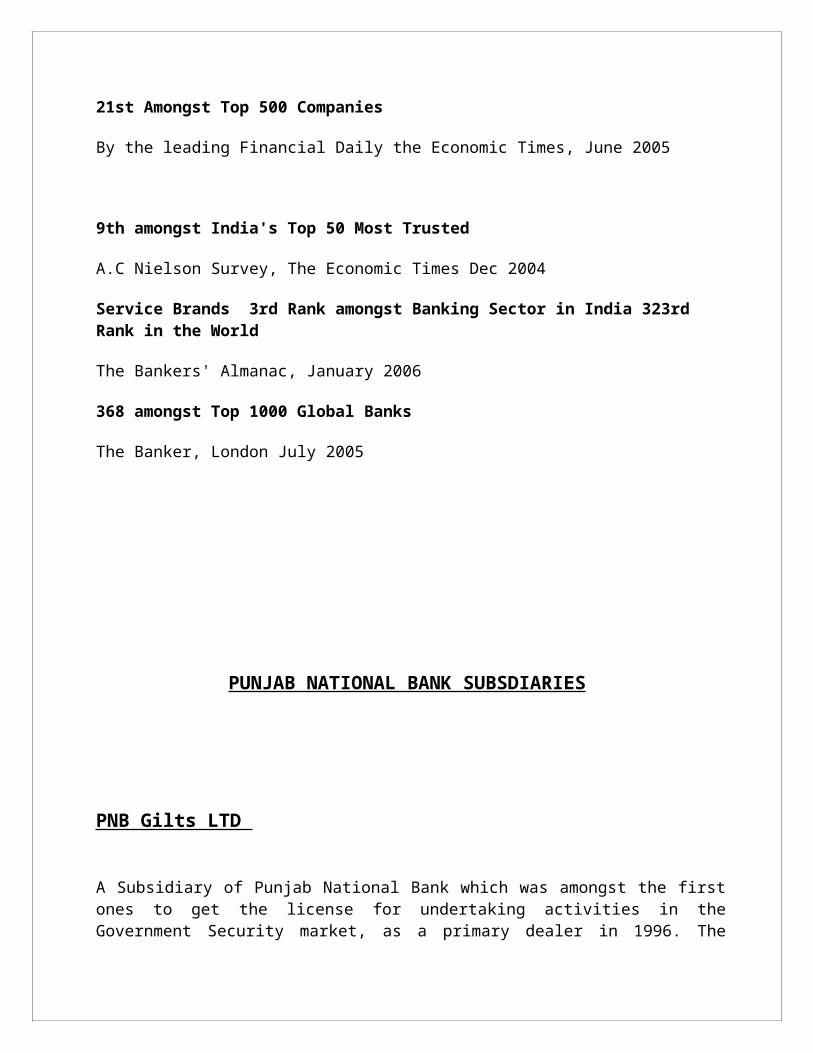

21st Amongst Top 500 Companies

By the leading Financial Daily the Economic Times, June 2005

9th amongst India's Top 50 Most Trusted

A.C Nielson Survey, The Economic Times Dec 2004

Service Brands 3rd Rank amongst Banking Sector in India 323rd Rank in the World

The Bankers' Almanac, January 2006

368 amongst Top 1000 Global Banks

The Banker, London July 2005

PUNJAB NATIONAL BANK SUBSDIARIES

PNB Gilts LTD

A Subsidiary of Punjab National Bank which was amongst the first ones to get the license for undertaking activities in the Government Security market, as a primary dealer in 1996. The company received ISO 9002 certification from British Standard Institution, making it as the first primary dealer in India to achieve this certification for its quality systems and procedures. This certificate has been granted to the company as a whole including its corporate and branch offices.

MISSION

BACKGROUND

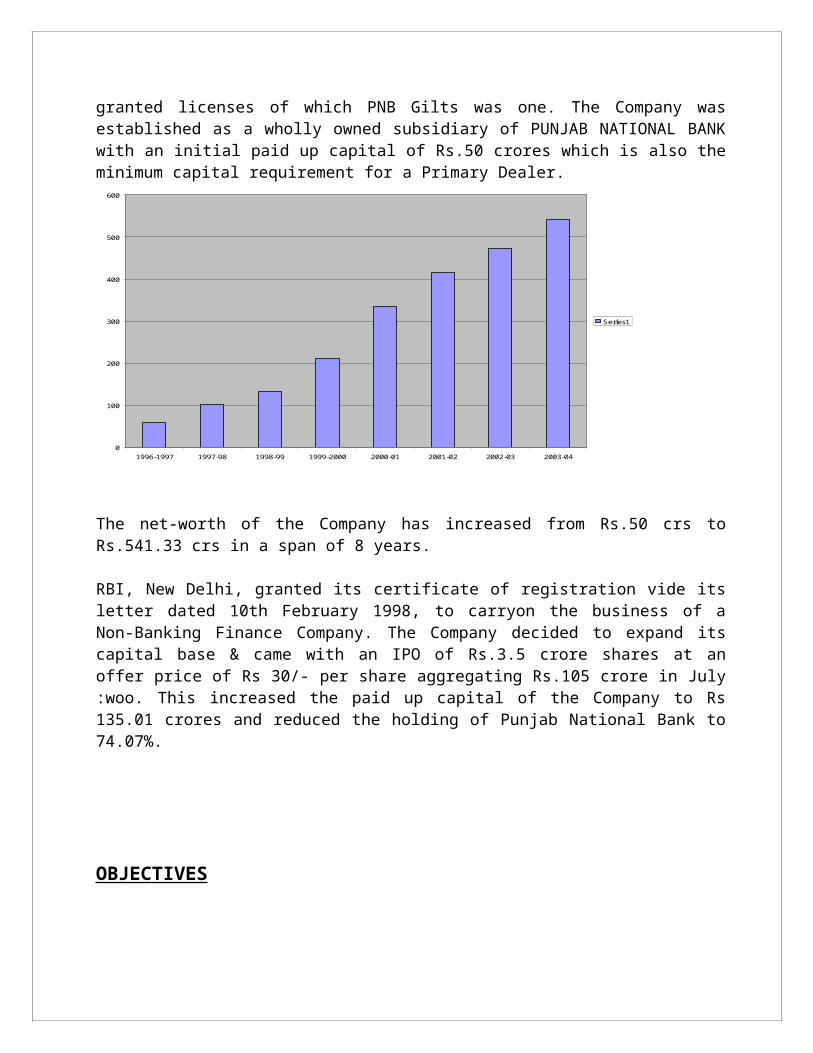

In the year 1996 Reserve Bank of India introduced the system of Primary Dealers with a view to strengthen the institutional infrastructure of Government Securities market. Six entities were granted licenses of which PNB Gilts was one. The Company was established as a wholly owned subsidiary of PUNJAB NATIONAL BANK with an initial paid up capital of Rs.50 crores which is also the minimum capital requirement for a Primary Dealer.

0

100

200

300

400

500

600

1996-1997 1997-98 1998-99 1999-2000 2000-01 2001-02 2002-03 2003-04

Series1

The net-worth of the Company has increased from Rs.50 crs to Rs.541.33 crs in a span of 8 years.

RBI, New Delhi, granted its certificate of registration vide its letter dated 10th February 1998, to carryon the business of a Non-Banking Finance Company. The Company decided to expand its capital base & came with an IPO of Rs.3.5 crore shares at an offer price of Rs 30/- per share aggregating Rs.105 crore in July :woo. This increased the paid up capital of the Company to Rs 135.01 crores and reduced the holding of Punjab National Bank to 74.07%.

OBJECTIVES

The objectives of the Company are in line with objectives laid down by RBI for the Primary Dealers:

Strengthen the infrastructure in the government securities market in order to make it vibrant, liquid and broad based.

Ensure the development of underwriting and market making capabilities for Government Securities.

Improve secondary market trading system, which would contribute to price discovery, enhance liquidity and turnover and encourage voluntary holding of Government securities amongst a wider investor base.

Become an effective conduit for conducting open market operations.

Besides the above, the Company has been pioneer in retailing of Government Securities contributing to a deep and broad-based market. The Marketing Department specifically caters to select segments viz. Provident Funds, Trusts, Regional Rural Banks, Co-operative Banks, Corporate & Individuals to create awareness and encourage healthy investment practices.

PRODUCTS & SERVICES

Being a primary dealer in the Government Securities Market the company undertakes more than 90% of its operations in Government Securities. The range of product and services offered by the company includes:

• Treasury Bills • Central Government Dated Securities• State Government Securities • PSU Bonds • Inter-Corporate Deposits • CSGL accounts • Money market instruments • Merchant Banking • Mutual Fund Distribution

In addition to the above, we also offer advisory services to our clients to manage the government securities portfolio.

The Company has well-defined systems and procedures. The Internal Control & Management systems are in place and are in accordance with the guidelines issued By the Regulatory Authorities.

The Company has a lean staff of 38 employees spread over the Country with 31 employees in the Head Office in New Delhi & rest in our branches at Mumbai, Chennai, Kolkata, Ahmedabad and Bangalore.

During the years the Company has emerged as a leading Primary Dealer in the country. We have to our credits ...

The first stand alone Primary Dealer to come with an IPO & get listed. The first PD to achieve ISO 9001:2000 certification. The first to obtain a PH rating from CRISIL for its short-term borrowing program. At present

the rating from CRISIL is for borrowing up to Rs 250 crore.

The company has achieved a turnover of Rs.116468 crores during 2003-2004, making it one of the largest debt traders in the country.

PUNJAB NATIONAL BANKHOUSING FINANCE LTD

INTRODUCTION

This is a wholly owned subsidiary of Punjab National Bank, is engaged in providing housing loans for purchase, construction and up gradation of a dwelling unit. The company offers Loans for construction or for purchase of house/flat from development authorities and also from private builders/ group housing societies as well as for renovation/ repairs .Company also provide finance for construction of residential projects. Loans to NRIs are also provided for purchase/ construction of house/ flat along with a resident/ non-resident co-borrower.

PRODUCTS AND SERVICES

• APNA GHAR YOJANA

• GHAR SUDHAR YOJANA

• LOAN AGAINST PROPERTY

• LOAN FOR COMMERCIAL PROPERTY

APNA GHAR YOJANA

We provide housing finance to individuals for construction or for acquisition/ purchase of house/flat from development authorities such as DDA/HUDA/PUDA/RHB etc. and also from private builders/groups housing societies. We consider enhancement in loan amount in the event of escalations in cost.

ELIGIBILITY:

a) Individuals in permanent service or having their own business (Resident or non -resident). b) Age of the applicant should not be more than 60 years in case of service class and 65 years in case of businessman or self employed;

LOAN AMOUNT:

a) Minimum loan amount would be Rs.50,000/- and maximum loan amount depends entirely on the repayment capacity of the borrower(s). b) Actual loan eligibility shall be on the basis of repayment capacity as determined be PNBHFL taking into account income, age, qualification and occupation. c) Income of borrower(s) j co-borrower(s) shall be clubbed together for calculation of loan eligibility / the level of finance in case of joint application

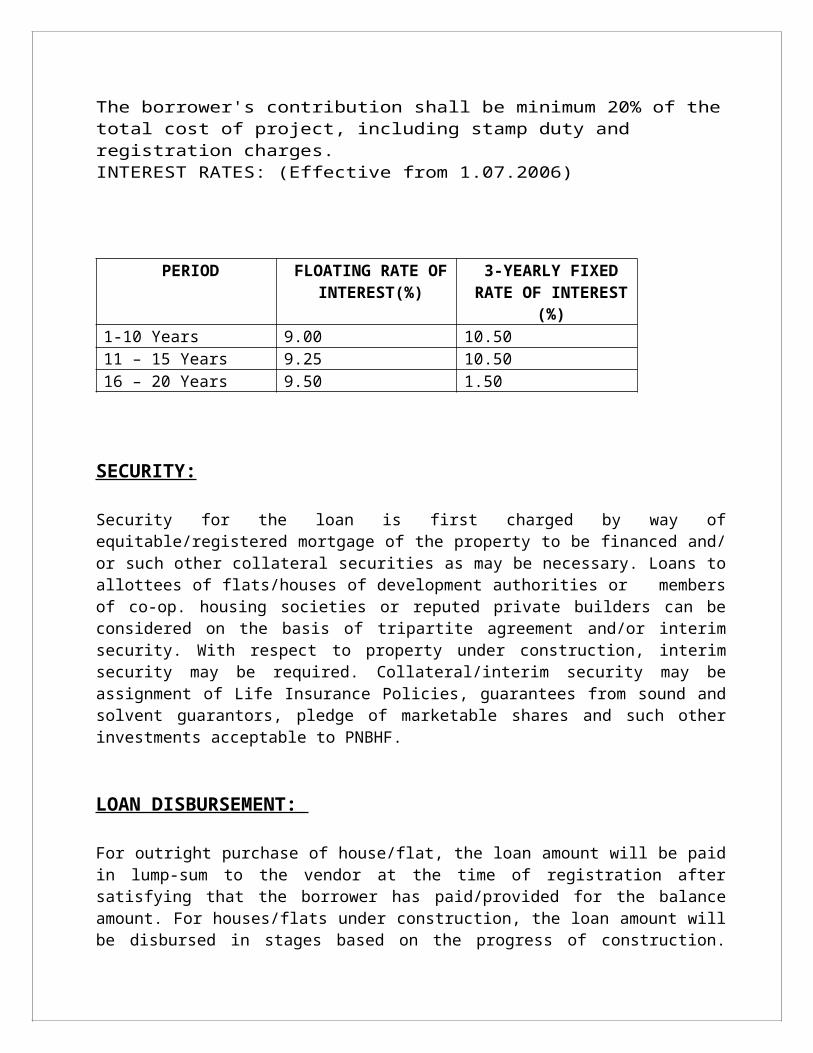

MARGIN: The borrower's contribution shall be minimum 20% of the total cost of project, including stamp duty and registration charges. INTEREST RATES: (Effective from 1.07.2006)

PERIOD FLOATING RATE OF INTEREST(%)

3-YEARLY FIXED RATE OF INTEREST

(%)1-10 Years 9.00 10.5011 – 15 Years 9.25 10.5016 – 20 Years 9.50 1.50

SECURITY:

Security for the loan is first charged by way of equitable/registered mortgage of the property to be financed and/ or such other collateral securities as may be necessary. Loans to allottees of flats/houses of development authorities or members of co-op. housing societies or reputed private builders can be considered on the basis of tripartite agreement and/or interim security. With respect to property under construction, interim security may be required. Collateral/interim security may be assignment of Life Insurance Policies, guarantees from sound and solvent guarantors, pledge of marketable shares and such other investments acceptable to PNBHF.

LOAN DISBURSEMENT:

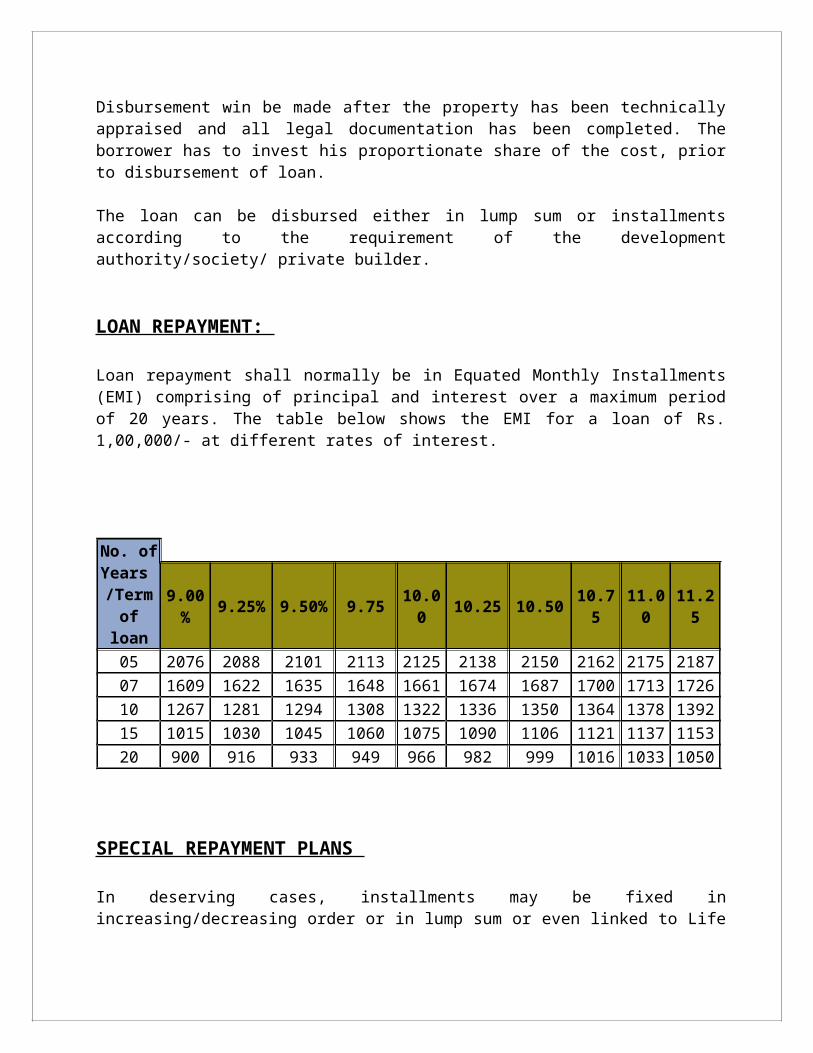

For outright purchase of house/flat, the loan amount will be paid in lump-sum to the vendor at the time of registration after satisfying that the borrower has paid/provided for the balance amount. For houses/flats under construction, the loan amount will be disbursed in stages based on the progress of construction. Disbursement win be made after the property has been technically appraised and all legal documentation has been completed. The borrower has to invest his proportionate share of the cost, prior to disbursement of loan.

The loan can be disbursed either in lump sum or installments according to the requirement of the development authority/society/ private builder.

LOAN REPAYMENT:

Loan repayment shall normally be in Equated Monthly Installments (EMI) comprising of principal and interest over a maximum period of 20 years. The table below shows the EMI for a loan of Rs. 1,00,000/- at different rates of interest.

No. of Years / 9.00% 9.25% 9.50% 9.75 10.00 10.25 10.50 10.75 11.00 11.25

Term of 05 2076 2088 2101 2113 2125 2138 2150 2162 2175 218707 1609 1622 1635 1648 1661 1674 1687 1700 1713 172610 1267 1281 1294 1308 1322 1336 1350 1364 1378 139215 1015 1030 1045 1060 1075 1090 1106 1121 1137 115320 900 916 933 949 966 982 999 1016 1033 1050

SPECIAL REPAYMENT PLANS

In deserving cases, installments may be fixed in increasing/decreasing order or in lump sum or even linked to Life Insurance Policies, under PNB Housing Finances special repayment plans like: • Graduated repayment plan • Decreasing repayment plan • LIC linked repayment plan • Balance payment facility

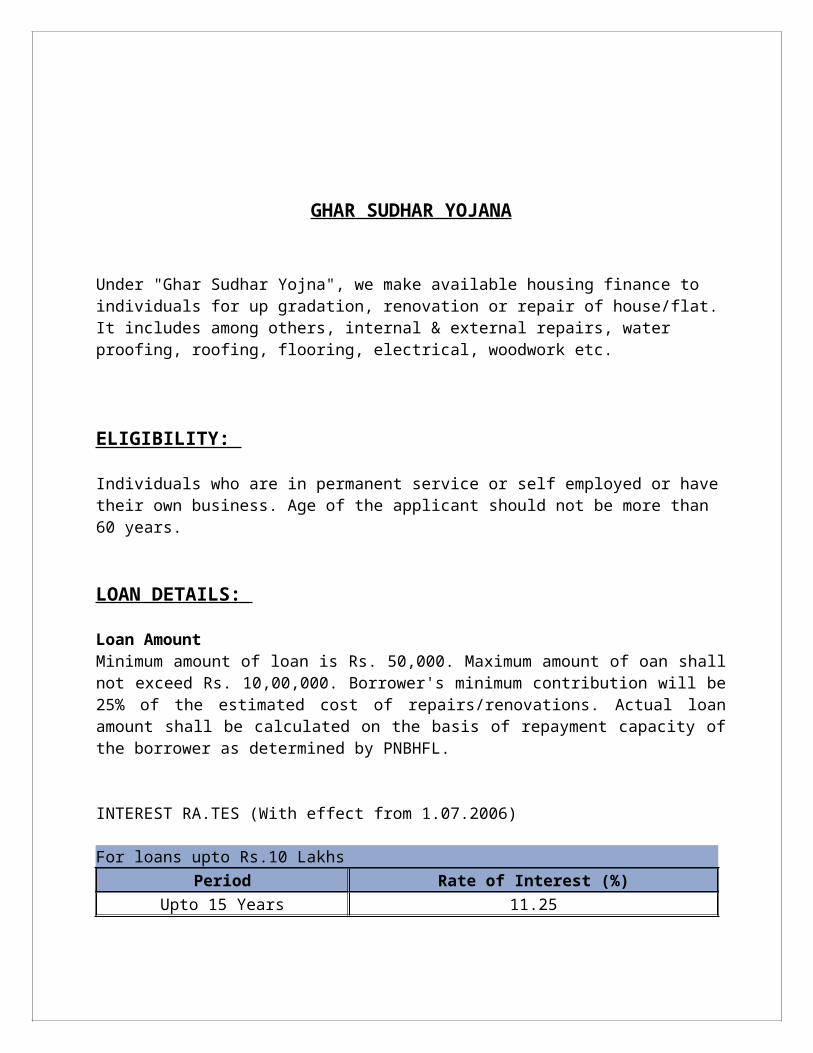

GHAR SUDHAR YOJANA

Under "Ghar Sudhar Yojna", we make available housing finance to individuals for up gradation, renovation or repair of house/flat. It includes among others, internal & external repairs, water proofing, roofing, flooring, electrical, woodwork etc.

ELIGIBILITY:

Individuals who are in permanent service or self employed or have their own business. Age of the applicant should not be more than 60 years.

LOAN DETAILS:

Loan Amount Minimum amount of loan is Rs. 50,000. Maximum amount of oan shall not exceed Rs. 10,00,000. Borrower's minimum contribution will be 25% of the estimated cost of repairs/renovations. Actual loan amount shall be calculated on the basis of repayment capacity of the borrower as determined by PNBHFL.

INTEREST RA.TES (With effect from 1.07.2006)

For loans upto Rs.10 LakhsPeriod Rate of Interest (%)

Upto 15 Years 11.25

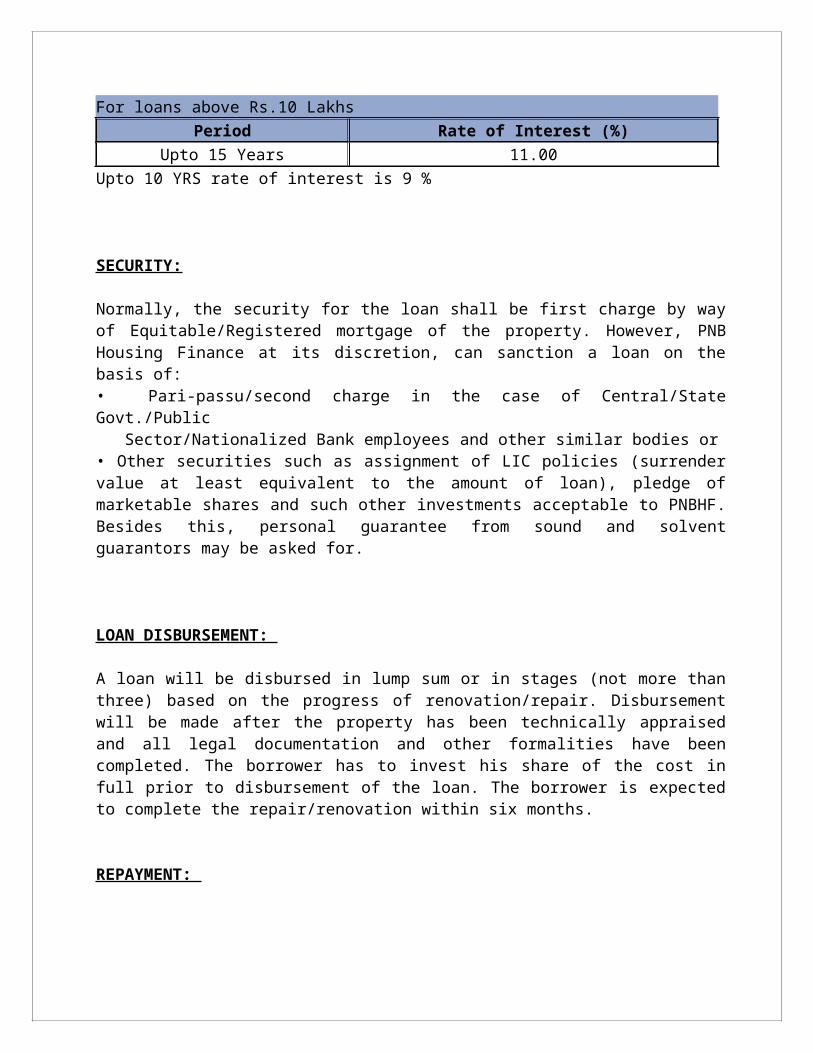

For loans above Rs.10 Lakhs

Period Rate of Interest (%)Upto 15 Years 11.00

Upto 10 YRS rate of interest is 9 %

SECURITY:

Normally, the security for the loan shall be first charge by way of Equitable/Registered mortgage of the property. However, PNB Housing Finance at its discretion, can sanction a loan on the basis of: • Pari-passu/second charge in the case of Central/State Govt./Public Sector/Nationalized Bank employees and other similar bodies or • Other securities such as assignment of LIC policies (surrender value at least equivalent to the amount of loan), pledge of marketable shares and such other investments acceptable to PNBHF. Besides this, personal guarantee from sound and solvent guarantors may be asked for.

LOAN DISBURSEMENT:

A loan will be disbursed in lump sum or in stages (not more than three) based on the progress of renovation/repair. Disbursement will be made after the property has been technically appraised and all legal documentation and other formalities have been completed. The borrower has to invest his share of the cost in full prior to disbursement of the loan. The borrower is expected to complete the repair/renovation within six months.

REPAYMENT:

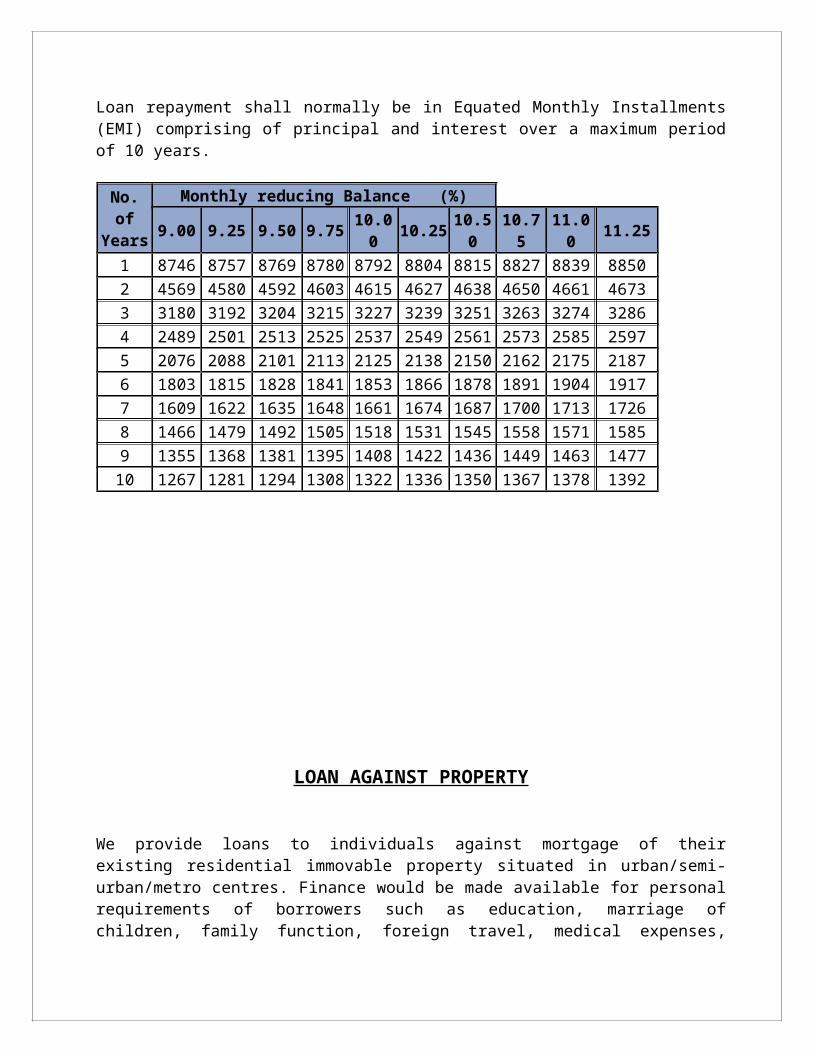

Loan repayment shall normally be in Equated Monthly Installments (EMI) comprising of principal and interest over a maximum period of 10 years.

No. of Years

Monthly reducing Balance (%)9.00 9.25 9.50 9.75 10.00 10.25 10.50 10.75 11.00 11.25

1 8746 8757 8769 8780 8792 8804 8815 8827 8839 88502 4569 4580 4592 4603 4615 4627 4638 4650 4661 46733 3180 3192 3204 3215 3227 3239 3251 3263 3274 32864 2489 2501 2513 2525 2537 2549 2561 2573 2585 25975 2076 2088 2101 2113 2125 2138 2150 2162 2175 21876 1803 1815 1828 1841 1853 1866 1878 1891 1904 19177 1609 1622 1635 1648 1661 1674 1687 1700 1713 17268 1466 1479 1492 1505 1518 1531 1545 1558 1571 15859 1355 1368 1381 1395 1408 1422 1436 1449 1463 1477

10 1267 1281 1294 1308 1322 1336 1350 1367 1378 1392

LOAN AGAINST PROPERTY

We provide loans to individuals against mortgage of their existing residential immovable property situated in urban/semi-urban/metro centres. Finance would be made available for personal requirements of borrowers such as education, marriage of children, family function, foreign travel, medical expenses, furnishing the house, buying a computer or other consumer durables, etc. by mortgaging their existing immovable property.

ELIGIBILITY:

Any individual having regular source of income can apply for the loan. Age of the applicant should not be more than 55 years.

LOAN AMOUNT:

Minimum loan amount would be Rs. 50,0001-. Maximum Loan Amount would be 50 % of the market value of the property as certified by PNBHF's approved valuer OR actual loan eligibility as determined on the basis of repayment capacity of the borrower, whichever is less. In case other earning family members are offered as co-borrowers, their income can also be clubbed with that of the borrower for computation of eligible loan amount.

INTEREST RATES: (With effect from 1.07.2006)

Interest rate for individuals will be 11.50% and for builders (floating rate) will be 12.00%

SECURITY:

We shall require Equitable I Registered Mortgage of property against which loan is being sought. Guarantee of one/ two persons will be required as per existing guidelines of the company.

LOAN DISBURSEMENT The loan would be disbursed directly to the borrower in lump sum through his bank account. Disbursement will be made after the property has been technically and legally appraised and legal documentation has been completed.

LOAN REPAYMENT

The loan would be repaid by way of Equated Monthly Installments (EMIs) consisting of principal and interest within a maximum period of 15 years. Repayment will commence in the month subsequent to the month in which loan has been disbursed.

LOAN FOR C0MMERCIAL PROPERTY

We provide loans to individuals against mortgage of their existing residential immovable property situated in urban/semi-urban/metro centers. Finance would be made available for personal requirements of borrowers such as education, marriage of children, family function, foreign travel, medical expenses, furnishing the house, buying a computer or other consumer durables, etc. by mortgaging their existing immovable property.

ELIGIBILITY:

Any individual having regular source of income can apply for the loan. Age of the applicant should not be more than 55 years.

LOAN AMOUNT:

Minimum loan amount would be Rs. 50,000/-. Maximum Loan Amount would be 50 % of the market value of the property as certified by PNBHF's approved value OR actual loan eligibility as determined on the basis of repayment capacity of the borrower, whichever is less. In case other earning family members are offered as co-borrowers, their income can also be clubbed with that of the borrower for computation of eligible loan amount.

INTEREST RATE: (With effect from 1.07.2006)

Interest rate both for individuals and builders will be 12.00%.

SECURITY:

We shall require Equitable/Registered Mortgage of property against which loan is being sought. Guarantee of one/ twu persons "vill be required as per existing guidelines of the company.

LOAN DISBURSEMENT

The loan would be disbursed directly to the borrower in lump sum through his bank account. Disbursement will be made after the property has been technically and legally appraised and legal documentation has been completed.

LOAN REPAYMENT: The loan would be repaid by way of Equated Monthly Installments (EMIs) consisting of principal and interest within a maximum period of 10 years. Repayment will commence in the month subsequent to the month in which loan has been disbursed.

PNB HOME LOAN

ELIGIBILITY

DOCUMENTATION

EXTENT OF LOAN

RATE OF INTEREST

REPAYMENT & SECURITY

FEATURES & CONDITIONS OF PNB HOME LOAN

PNB HOME LOAN

Punjab National Bank provides its customers with various Home loan policies and features at

highly competitive rates. They know the needs of the Indian customers that they have to deal

with, on a regular basis, and provide the policies accordingly. The PNB Home Loan cater mainly

to the requirement of the middle class individuals of India, as Pnb itself is one of the leading

public –sector banks of the nation.

The PNB Home loans are very easily available, and have an even easier process of repayment

that is given over a prearranged time period. This period of time is determined, when the PNB

Home loans are being finalized and along with the loans, the buyers get the opportunity of

having a life insurance covered against him. The basic grounds on which the PNB Home loans

are provided are:

Extending, repairing, modification and even renovating of an already existing building or

flat.

Purchase or building of a new house or flat.

The basic interest of the PNB Home loans may be around 9.5%, and the time period may vary

from a minimum of 5 years to a maximum of 25 years. However there is a certain limitation of

the loan amount that an individual may take from the bank. The maximum amount of the loan

amount sanctioned under PNB Home loans is need based. It generally takes around 7 days to

process the PNB Home loans, from the day it has been finalized with the bank.

Apart from all these details, the PNB Home loans also enable us to choose between fixed and

floating rates that may be applicable from time to time, and keep varying from one time period to

another. As far as the eligibility is concerned, a person between the age group of 18 to 60 years

may be qualified to apply for the PNB Home loans. Along with this, it has also to be noted that

the annual income of the individual, who is applying for the loan, must be greater than or equal

to 1.2 Lac INR.

Eligibility

Age of the applicant must be less than 60 years.

Existing home loan borrower can also apply provided their loan account is regular and no

IR irregularity persist.

Documents Needed

1. Proof of identity

2. Proof of income

3. Proof of residence

4. Bank statement or Pass Book where salary or income is credited.

5. Education Certificate

6. Photos

7. Salary slip & form 16

8. Income tax return last 3 years along with balance sheets.

9. Assets liabilities statements.

10. Documents of property.

11. Estimate of construction.

12. Guarantor

Freehold and Leasehold Property

1. The loan can be granted both for freehold and leasehold property.

2. In case of leasehold, loan can be granted on the basis of power of attorney basis from original

allotee where DDA/PUDA/HUDA permit conversion of leasehold into freehold property

otherwise advance is not permitted against plot purchased on Power of Attorney basis.

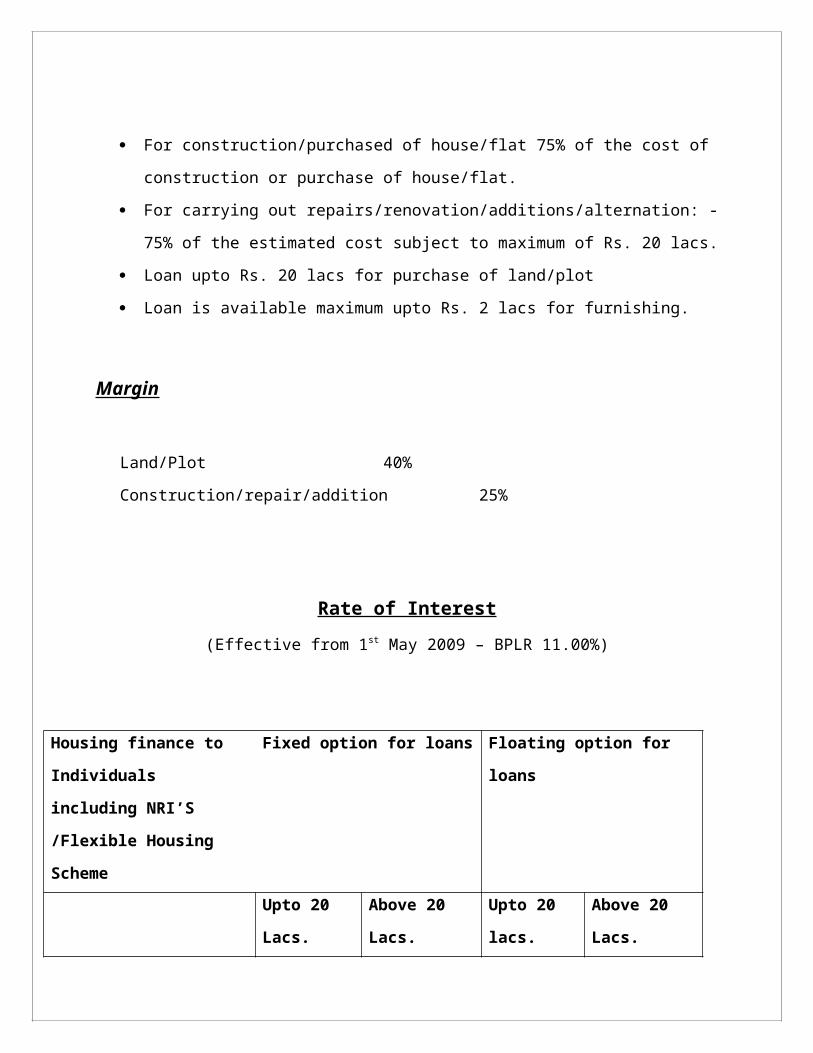

Extent of loan

For construction/purchased of house/flat 75% of the cost of construction or purchase of

house/flat.

For carrying out repairs/renovation/additions/alternation: - 75% of the estimated cost

subject to maximum of Rs. 20 lacs.

Loan upto Rs. 20 lacs for purchase of land/plot

Loan is available maximum upto Rs. 2 lacs for furnishing.

Margin

Land/Plot 40%

Construction/repair/addition 25%

Rate of Interest

(Effective from 1st May 2009 – BPLR 11.00%)

Housing finance to

Individuals including

NRI’S /Flexible Housing

Fixed option for loans Floating option for loans

Scheme

Upto 20

Lacs.

Above 20 Lacs. Upto 20 lacs. Above 20 Lacs.

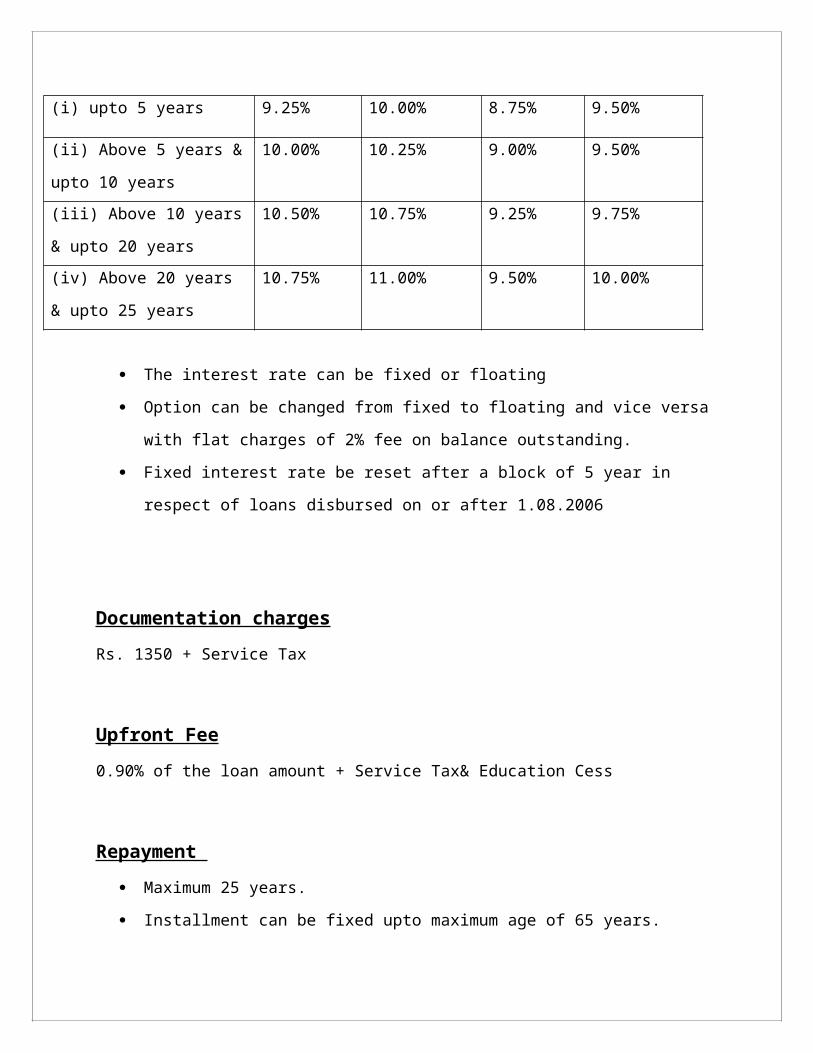

(i) upto 5 years 9.25% 10.00% 8.75% 9.50%

(ii) Above 5 years & upto 10

years

10.00% 10.25% 9.00% 9.50%

(iii) Above 10 years & upto

20 years

10.50% 10.75% 9.25% 9.75%

(iv) Above 20 years & upto 25

years

10.75% 11.00% 9.50% 10.00%

The interest rate can be fixed or floating

Option can be changed from fixed to floating and vice versa with flat charges of 2% fee

on balance outstanding.

Fixed interest rate be reset after a block of 5 year in respect of loans disbursed on or after

1.08.2006

Documentation charges

Rs. 1350 + Service Tax

Upfront Fee

0.90% of the loan amount + Service Tax& Education Cess

Repayment

Maximum 25 years.

Installment can be fixed upto maximum age of 65 years.

The income of spouse and earning children can be taken into account provided they are

made co-borrower.

Father/Mother can also be made co-borrower in cases property is in single name of his

/her son and also clubbing of their income is permitted for determining eligibility criteria.

Minimum 24 advance cheque should be obtained as and when, 6 cheques remain, fresh

lot to be obtained out of 24, 23 cheques should be of the amount equal to the balance.

Loan is to be repaid in EMI within a period of 25 years or before the borrower attains the

age of 65 years.

Security

Equitable/Registered mortgage of immovable property.

Tripartite agreement be executed amongst Housing Board/ Dev Authority / Coop

Society / Builder the borrower and the bank where mortgage cannot be created

immediately.

Equitable mortgage of other immovable property or pledge of NSC etc. upto 125% of

loan amount if property is being purchased from 1st P/A holder and where there is delay

in the execution of Tripartite agreement.

Verification of security is required once in 2 years.

Features

Loan can be sanctioned by branch/hub near to the present place of work/posting

/residence of the borrower.

Loan can be sanctioned even if property is in the name of wife/parents provided that the

owner is made co-borrower.

Loan can be granted for 2nd house in the same city.

Loan can be granted for purchase of house for rental purpose

For take over, permission of higher authority is not required.

Important Conditions : Loan cannot be granted

For construction in Un-authorized colonies.

If property is to be used for commercial purpose.

Without approved Map.

RESEARCHMETHODOLOGY

INTRODUCTION

The procedure adopted for conducting the research requires a lot of attention as it has direct bearing on accuracy, reliability and adequacy of results obtained. It is due to this reason that research methodology, which we used at the time of conducting the research, needs to be elaborated upon. Research Methodology is a way to systematically study & solve the research problems. If a researcher wants to claim his study as a good study, he must clearly state the methodology adopted in conducting the research so that it may be judged by the reader whether the methodology of work done is sound or not.

The research method here includes:-

1. Meaning of research 2. Research problem 3. Research design 4. Sampling design 5. Data coIlection method 6. Data analysis and interpretation 7. Recommendations

Meaning of Research

Research is defined as "a scientific & systematic search for pertinent information on a specific topic. Research is an art of scientific investigation. Research is a systematized effort to gain new knowledge. It is a careful investigation or inquiry especially through search for new facts in any branch of knowledge. Research is an academic activity and this term should be used in a technical sense. Research corn prices defining and redefining problems, formulating hypothesis or suggested solutions; making deductions and reaching conclusions to determine whether they fit the formulating hypothesis. Research is thus, an original contribution to the existing stock of knowledge making for this advancement. The search for knowledge through objective and systematic method of finding solution to a problem is research.

Research ProblemThe first step while conducting research is careful definition of research problem.

Research design A research design is the arrangement of conditions for collection and analysis of data in a manner that aims to combine relevance to the research purpose with economy in procedure. Research design is the conceptual structure within which research is conducted. It constitutes the blue print for the collection measurement and analysis of data. Research design includes an outline of what the researcher will do from writing the hypothesis and its operational implications to the final analysis of data.

A research design is a framework for the study and used as a guide in collecting and analyzing the data. It is a strategy specifying which approach will be used for gathering and analyzing the data. It also includes the time and cost budget since most studies are done under these two constraints.

Research design can be categorized as:

• Exploratory research • Descriptive • Diagnostic research • Experimental research

Sampling Design

Sampling is necessary because it is almost impossible to examine the entire parent population (i.e. the entire universe) various factors such as time available, cost, purpose of study etc make it necessary for the researchers to choose a sample. It should neither be too small nor too big. It should be manageable. Data Collection Method

After the sample has been taken the type of information to be sought was decided upon, the next step is to collect the data. As the data collected is to be the base of what we plan to find out, the relevant care should be taken that the errors in methods of collection of data involved are minimized. The factors of availability of time, cost and human involvement come to effect the reliability of the data collected. Broadly there are two types of data:

• Primary data • Secondary data

Secondary data means the statistics not gathered for the immediate study at hand but for some other data. It is the data collected by some one for purposes other than solving the problem being investigated. On the other hand primary data are generated in a study specifically designed to accommodate the data needs of the problem at hand.

ANALYSIS AND INTERPRETATION OF DATA AND RECOMMENDATIONS

The data collected in the aforesaid manner have been tabulated in condensed form to draw the meaningful result. The different techniques are adopted to analyze a data.

All the data and the material is arranged through internal resources and the last part of the project consist of the conclusions drawn from the report, a brief summary and recommendations and

giving the final touch to the reports by stating a conclusion.

COMPARATIVE CUSTOMER PREFERENCE ANALYSISIN HOME LOAN SECTOR

SCOPE OF THE STUDY

The present study was conducted by the researcher in Delhi covering some main and popular markets of Delhi because of constraints of time and money study could not be extended to other cities. As Delhi being a popular and among the good cities of India is a good market of financial products & also here customers of different classes like business segment, service segment, and professional segment are in excess. Since the report aims at finding the potential for financial products at Delhi itself taking into consideration certain limits and problems, the area was chosen on the basis of coverage of product no. of respondents.

DELHI MARKET SEGMENT The market of Delhi mainly comprises of the rural & urban people with population of around 15 million. The literacy rate is fairly high and there are around 65% males & 35% females.

This data clearly indicates the emergency of a middle class at Delhi. As is elsewhere, this class is the harbors of modern facilities. Apart from other contribution, it is this class for its money. These demands exhibits a vigilant customer & financial products have been on their toes to return them to pay the least if not attract the other ones.

Besides Delhi also boasts of a large financial market. It has an upcoming pharmacy distribution network & lots of Govt. institutions. There is increasing use of Cyber Cafe Internet & cable connection. The market size of the city is around 2 lacks, a significant chunk of which is occupied by the upcoming middle classes.

Besides, there is good number of industries.

Apart from this, there are many management and engineering conege's and universities. The much roaming growth of such institutions shows the presence of many high nets worth individual is Delhi.

For the purpose of the study the respondents were selected from all corners of Delhi mainly popular colonies and for gathering information about the trends, demands & brands available in financial products.

The data was collected through questionnaires. The question consisted of 10 questions along with the information regarding the occupation of the respondent. The number of respondents were kept to 100. The graphs of all the findings question wise are given below along with the tables of the data collected.

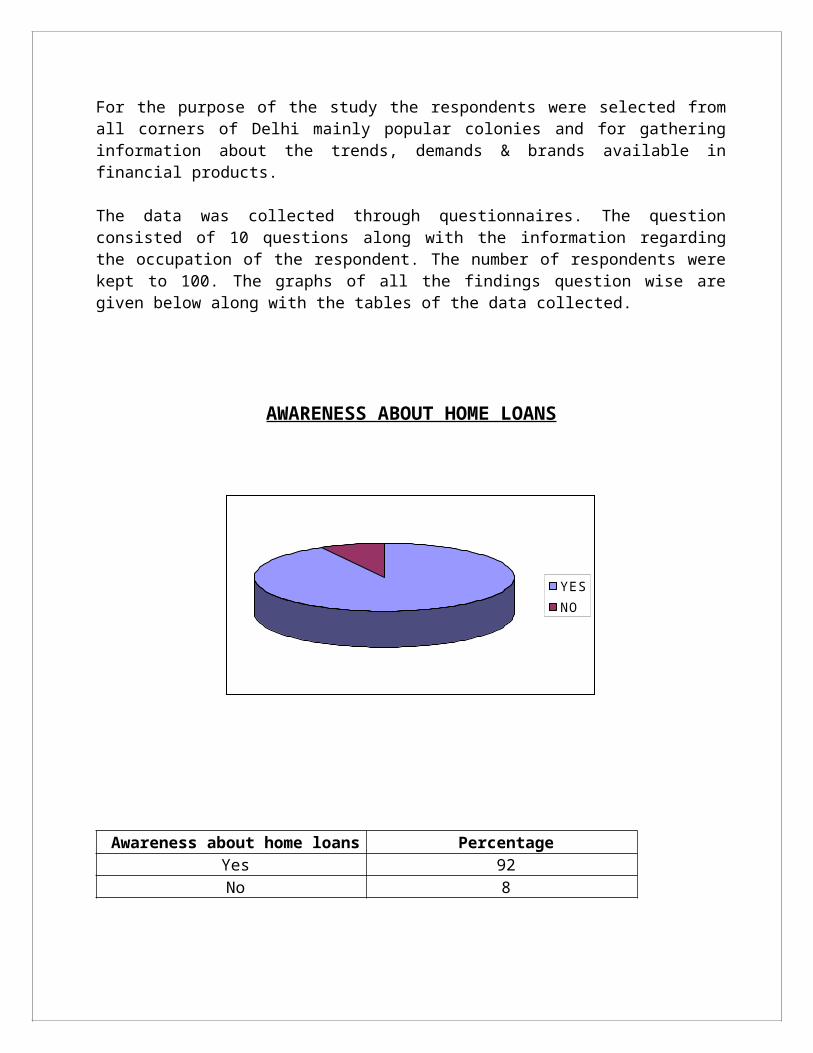

AWARENESS ABOUT HOME LOANS

YES

NO

Awareness about home loans PercentageYes 92No 8

INTERPRETATION

The above Pie chart depicts that 92% of total sample size is aware about the home loans and only 8% are unaware.

EASE OF GETTING HOME LOAN

EASE OF GETTING HOME LOAN

YES

NO

Ease Of Getting Home Loan PercentageYes 51No 49

INTERPRETATION

51% of the sample size finds easy to get the home loan while 49% finds it difficult The ratio is more or less same.

PREFERENCE OF TAKING HOME LOAN

PREFERENCE OF TAKING HOME LOAN

YES

NO

Preference of taking Home Loan PercentageYes 76No 24

INTERPRETATION

The above graph depicts that maximum percentage of the sample size prefers to go for home loan.

LOAN RECEIVED

LOAN RECEIVED

YES

NO

Loan Recieved PercentageYes 67No 33

INTERPRETATION

It has been found from the graph that 67% of the sample size has gone for the home loan.

BANK PREFERENCE

BANK PREFERENCE

ICICI

PNBHF

LICHF

HDFC

OTHERS

PREFERENCE OF BANK PERCENTAGEICICI 36PNBHF 18LICHF 10HDFC 35OTHERS 1

INTERPRETATION

The above graph depicts that only 18 % of the sample size has preferred to take home loan from PNB and maximum percentage of the sample size preferred to take home loan either from ICICI or HDFC and very few that is only one percent has the preference of other financial institutes.

PROVISION OF OPTIMAL/ECONOMICAL INTEREST RATE

PROVISION OF OPTIMAL/ECONOMICAL INTEREST RATE

ICICI

PNBHF

LICHF

HDFC

OTHERS

Provision Of Optimal/Economical Interest Rate

Percentage

ICICI 32PNBHF 24LICHF 13HDFC 27OTHERS 4

INTERPRETATION

The above graph shows that according to the 32 percentage of total sample size, ICICI provides the optimal/economical interest rate. The next preference is given to HDFC and PNBHFL has received the third preference for providing the optimal interest rate. And only 13 percent of the sample preferred LICHF.

SUITABLE EMI

SUITABLE EMI

ICICI

PNBHF

LICHF

HDFC

OTHERS

Preference of bank in case of suitability of EMI

Percentage

ICICI 32PNBHF 24LICHF 13HDFC 27OTHERS 4

INTERPRETATION

The above graph shows that according to the 32 percentage of total sample size, ICICI provides suitable EMI. The next preference is given to HDFC and PNBHFL has received the third preference for providing suitable EMI. And only 13 percent of the sample preferred LICHF.

LONG TERM PREFERENCE

LONG TERM PREFERENCE

ICICI

PNBHF

LICHF

HDFC

OTHERS

Long Term Preference PercentageICICI 27

PNBHF 24LICHF 25HDFC 20

OTHERS 4

INTERPRETATION

The above pie chart depicts that maximum number of people has preferred ICICI bank for long term loans and only 24 percent of sample size has given preference to PNBHF and only 4% has given preference to other financial institutes.

CUSTOMER FRIENDLINESS

CUSTOMER FRIENDLINESS

ICICI

PNBHF

LICHF

HDFC

OTHERS

Customer Friendliness PercentageICICI 26PNBHF 18LICHF 24HDFC 17OTHERS 15

INTERPRETATION

The above pie chart shows that maximum number of people finds ICICI more customer friendly than other banks.

PROMPT SERVICE

BANK PREFERENCE ACCORDING TO PROMPT SERVICE

ICICI

PNBHF

LICHF

HDFC

OTHERS

Prompt Service PercentageICICI 45PNBHF 13LICHF 23HDFC 14OTHERS 5

INTERPRETATION

ICICI bank has found to be quickest in sanctioning the loan among other financial institutes by maximum number of people.

POSITIVE ASPECT FOR SUCCESS OF PNBHF

Positive Aspect For Success Of PNBHF

Percentage

SALES PROMOTION & BRAND 25Customer Friendly Home Loan Schemes

35

Easy Sanctioning Of The Home Loans

10

Lower Interest Rates 15

SALES PROMO-TION & BRANDCUSTOMER FRIENDLY HOME LOAN SCHEMES

Lower Emi's 15

INTERPRETATION

The above graph depicts that customer friendly home loan schemes are the main aspect for the success of PNBHF.

LAGGING AREA

Lagging Area PercentageConfined Only In Urban Areas 12Non Effective Advertisements 78Delay In Processing 10

INTERPRETATION

Sales

1st Qtr 2nd Qtr 3rd Qtr 4th Qtr

The above Pie chart shows that Non effective Advertisement is the lagging area of PNBHFL in comparison to other home loan banks.

CONCLUSION ANDSWOT

ANALYSIS AND LIMITATIONS

SWOT ANALYSIS

STRENGTHS

• Brand name of Punjab National Bank (PNB) is established over the years.• Single window clearance - a single employee provides wide variety of

facilities to the borrower, minimizing the hassle of wastage of time. • Appraisal techniques are used. • Specialized software's are big assets. • There is no penalty for prepayment from borrowers own service.

WEAKNESSES

• High interest rates as compared to other housing finance institutions. • Top management takes large amount of time to approve high value seeking loan

borrowers. No publicity. • No marketing managers work, only through dsa's (direct sales agent).

• People are not aware of wide variety of schemes offered by the company; tend to think the company as only providing home loans.

• There is the shortage of staff at almost all branches which does not ensure easy addressable of the customers problems.

Delegation of authority and responsibility is not proper.

OPPORTUNITIES

• Special rates of interest are offered during exhibitions.• Special rates of interest can be introduced for employees of PSU'S & reputed national or

multinational companies'• Product life cycle is to be reviewed.• The growing category of the builders ensure that good, high value & qualitative projects,

providing them home loans with the new and innovative schemes can lead to over all development of the company.

THREATS

• The competition in market is very high due to the private players.• The rates of interest of other players are quite low. • Innovative schemes with horne loan from other players. • The processing process is quite slow which leads to low housing finance.

A fraud case involving 32 cases worth Rs.3 crores at the one branch of PNB Housing Finance Limited in year 2002 leads decreasing brand name.

LIMITATIONS OF THE STUDY

There are always present some limitations under which researcher has to work. Here following are some limitations under researcher had to work:

SAMPLE SIZE

The sample size surveyed was limited over 100 respondents which not may be fully representative of the universe. A large sample size could not be taken due to time & cost constraints.

NON - COVERAGE OF CERTAIN ASPECTS

There is wide range of perimeters affecting consumer behavior but only a few questions relating to those determinants have been endorsed in schedule.

TIME CONSTRAINT

We had limited time for conducting this survey report. In this short period of all the respondents had to be personally contacted for the purpose of survey & then their responses had to be analysed . So, some shortfalls may be present.

LIMITATIONS OF SAMPLING TECHNIQUES

Limitations & biasness of convenience & judgment sampling used in the present study to some extent.

MONEY

Available with the researcher also imposed a limitation on the comprehensive of this research.

BIBLIOGRAPHY

Books

Agrawal, N.K. (2003) Marketing Of Banking Products, Sterling

Publishers Pvt, Ltd, New Delhi

Agrawal, N.P (1983) Analysis of Financial Statements, National

Publishing House, New Delhi.

Websites:

www.pnb.com

www.indiainfoline.com

www.sribd.com