polish construction companies 2015: key players, growth ... · introduction dear sir/madam, we have...

TRANSCRIPT

Polish construction companies 2015: Key players, growth factors and industry development prospects

Table of contents

Introduction 5 Chapter 1. Financial analysis of the biggest construction companies 7 1.1. Ranking of the biggest construction companies by 2014 revenue 8 1.2. Ranking of the largest construction companies by 2014 operating margin 9 1.3. Ranking of the biggest construction companies by 2014 net profit 11 1.4. Debt of 15 biggest construction companies in 2014 2014 13 1.5. Capital expenditure to sales ratio of the largest companies in 2014 14 1.6. Revenue of the 15 largest construction companies by geography and by type in 2013 16 1.7. Market Capitalisation of the largest construction companies listed on Warsaw Stock Exchange at December 31, 2014 23 Chapter 2. Prospects for development of construction companies in Poland 27 2.1. Introduction 28 2.2. Key factors of the construction market development in Poland 30 2.3. Bankruptcies in the construction sector 32 2.4. Employment in the construction sector 34 2.5. Development outlook for construction segments in Poland 36 2.6. From the market perspective 52 2.7. Summary 54 Chapter 3. Profiles of the biggest construction companies in Poland 57 Bibliography 102 Contact 104

4

Introduction

Dear Sir/Madam,

We have the pleasure to present the third edition of the Polish construction companies 2015: Key players, growth factors and industry development prospects report, analysing the condition of the 15 largest construction companies operating on the Polish market based on their revenue, and describing their prospects for business development.

In 2014, a recovery was observed, accompanied with positive change in market outlook. Total revenue of the 15 largest companies increased by nearly PLN 2.5 billion, i.e. 9% vs. 2013. The growth correlated with an improved operating performance and net profit of the top fifteen. Capitalisation of the largest construction companies listed on the Warsaw Stock Exchange and included in the ranking was only slightly higher at the end of 2014 than in the previous year.

The reversal of the previously negative trend resulted mostly from the completion of unprofitable road construction contracts, which materially affected the performance of most companies in the past. The infrastructure segment continued to play a key role in construction and assembly related production, although railway, industrial and hydrotechnical construction was the main driver of the entire sector’s growth. Once tenders regarding contracts co-funded by the EU budget under the new financial perspective 2014-2020 are accepted, the increasing trend in the sector should be consitent.

The first part of our report is a financial analysis of companies in the construction sector in Poland, based on 15 entities that have managed to build the strongest position in the market. We analyse their revenue, operating margins, net profits, debt, and revenue structure by geography and by type.

The second part comprises a high-level analysis of the prospects for the industry’s short-term and medium-term development, including presentation of planned expenditure in each market segment, bankruptcy statistics and employment trends in the construction sector. This part of the report is concluded with a summary of the present condition and key growth factors for the sector from the viewpoint of the largest construction companies in Poland.

In the final part of the report we briefly examine the characteristics of the business activity of the 15 most important market players in 2014.

It includes crucial information concerning the scope of their activities, ownership structure and detailed financial data derived from their annual financial statements.

When preparing the report, we referred to commonly available financial data or information provided to us directly by the entities presented herein.

We hope that you will find the report Polish Construction Companies 2015: Key players, growth factors and industry development prospects useful and that it will give you better understanding of the current construction market position, indicating challenges and opportunities faced by construction companies in the years to come.

As always, we are open to your ideas and suggestions regarding any of the presented topics.

Polish construction companies 2015: Key players, growth factors and industry development prospects 5

Chapter 1.Financial analysis of the largest construction companies

Polish construction companies 2015: Key players, growth factors and industry development prospects 7

No. Company name Revenue RevenueChange expressed in

PLNChange expressed

in %

1 Skanska Group 5 081 675 4 362 167 719 508 16.5%

2 Budimex Group 4 949 939 4 749 459 200 480 4.2%

3 Strabag Group** 3 133 492 3 298 754 -165 262 -5.0%

4 Polimex-Mostostal Group* 2 102 197 2 362 752 -260 555 -11.0%

5 Erbud Group 1 692 055 1 223 609 468 446 38.3%

6 Trakcja Group* 1 601 674 1 274 222 327 452 25.7%

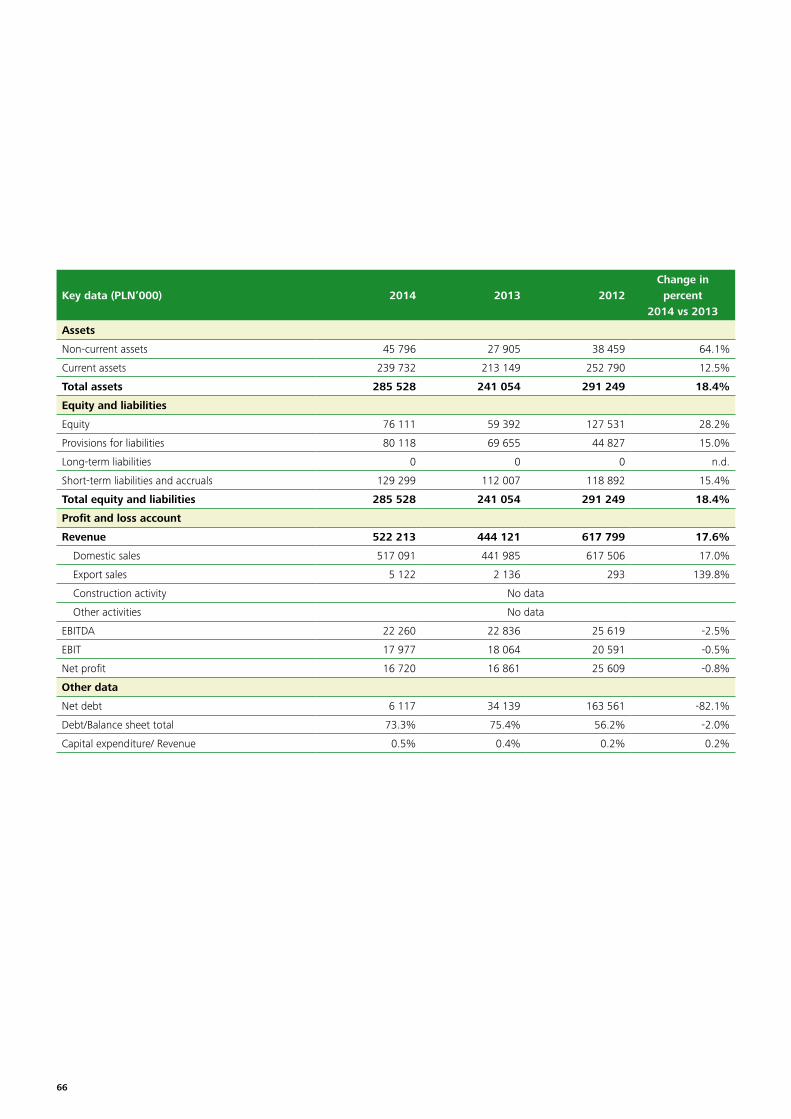

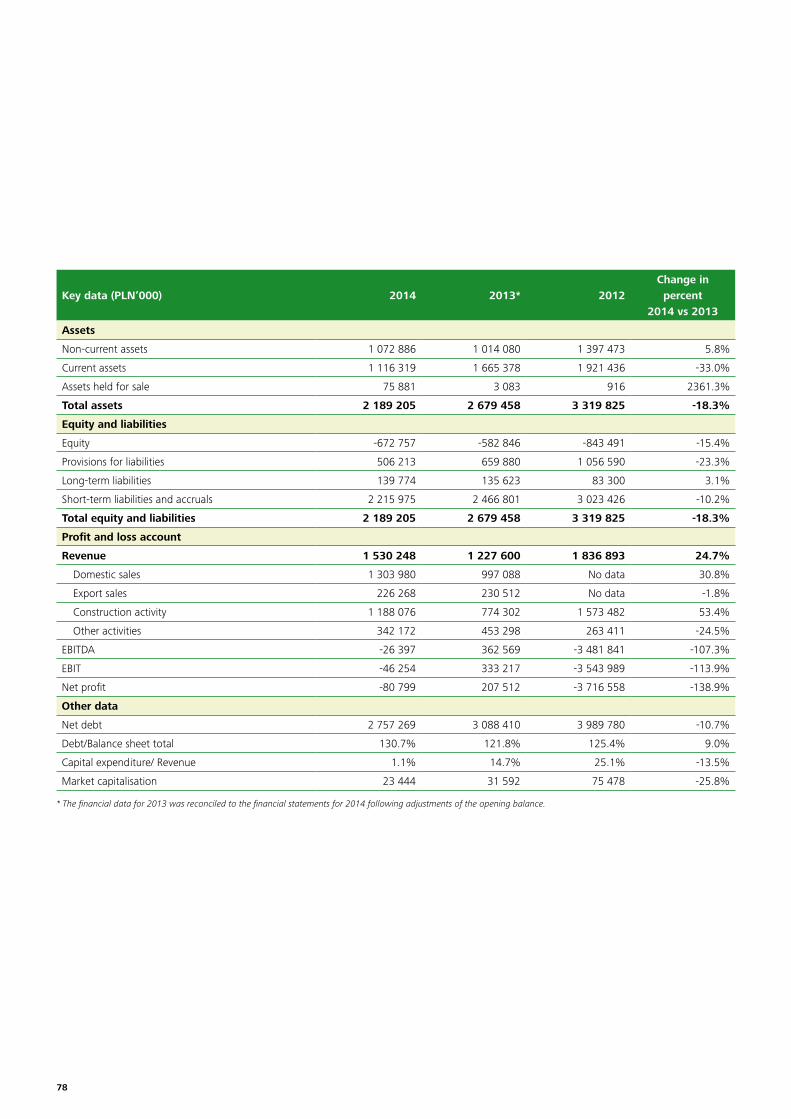

7 PBG Group* 1 530 248 1 227 600 302 648 24.7%

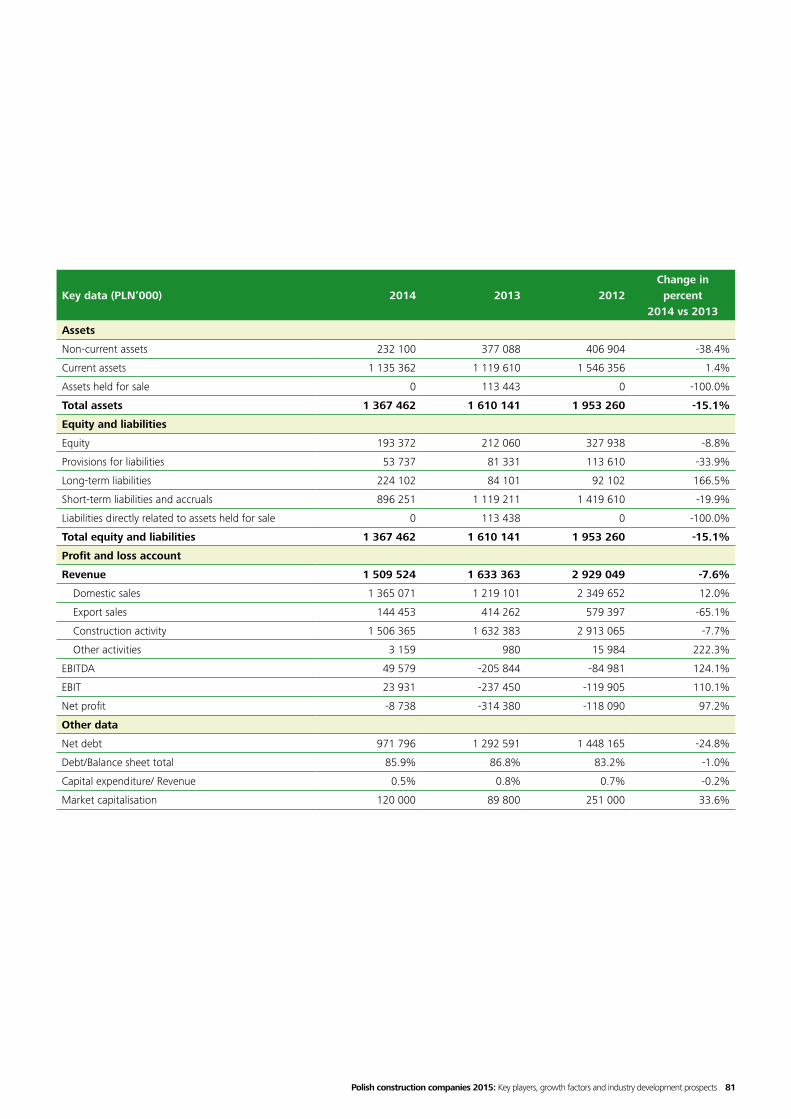

8 Mostostal Warszawa Group 1 509 524 1 633 363 -123 839 -7.6%

9 Elektrobudowa Group 1 108 316 905 553 202 763 22.4%

10 Unibep Group 1 079 703 920 548 159 156 17.3%

11 Warbud S.A.* 1 049 886 1 121 472 -71 586 -6.4%

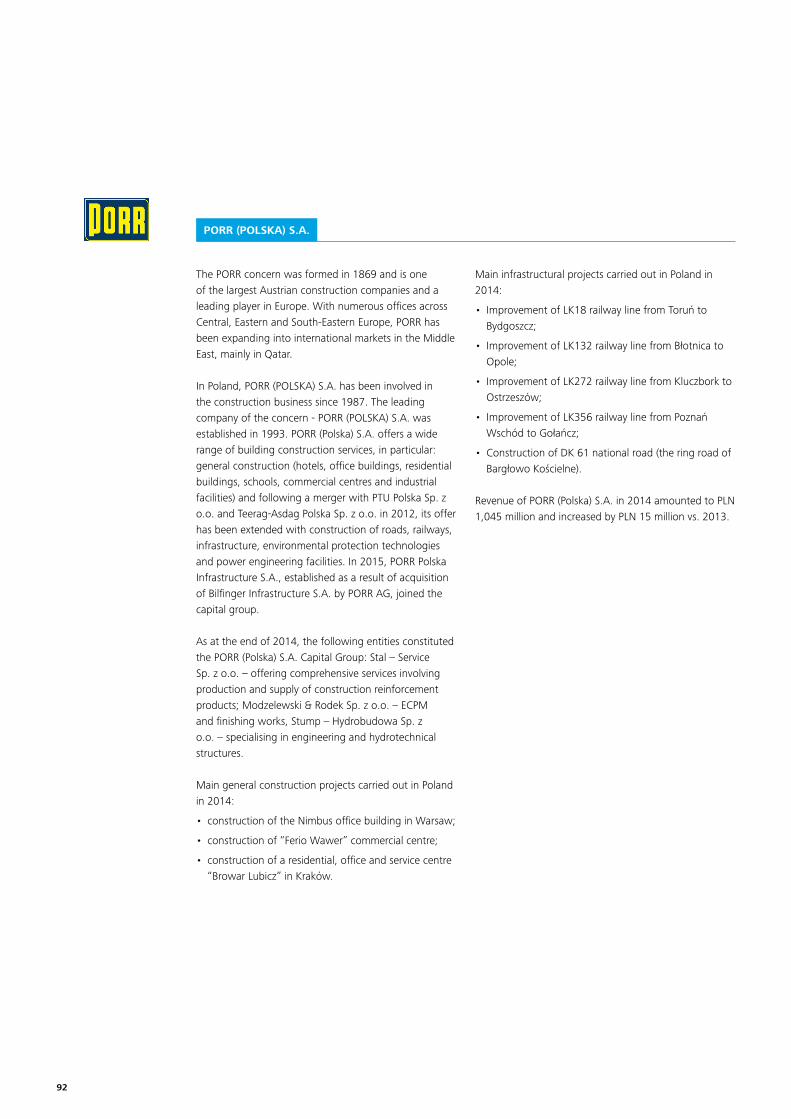

12 PORR (Polska) S.A. 1 045 019 1 030 076 14 943 1.5%

13 Mirbud Group 971 603 937 301 34 302 3.7%

14 Mostostal Zabrze Group 862 650 575 117 287 533 50.0%

15 Torpol Group 775 399 415 717 359 682 86.5%

Total 28 493 380 26 037 710 2 455 671 9.4%

Average 1 899 559 1 735 847 163 711 9.4%

Note: This analysis does not include the performance of foreign establishments of the construction companies operating in Poland, or that of SPV’s established within consortia in order to perform specified tasks, since this performance is included in consolidated performance of consortium members.

Source: Financial statements for the years 2014-2013

Table 1.1: Ranking of construction companies in Poland by revenue in 2014 (PLN’000)

1.1. Ranking of the largest construction companies by 2014 revenueIn 2014, the combined revenue of the 15 largest companies was PLN 28.5 billion which constitutes a growth of PLN 2.5 billion, i.e. 9.4% compared to 2013. In this year’s ranking, the Skanska Group came first with revenue of PLN 5.1 billion and 16.5% growth. The Budimex Group, controlled by Ferrovial of Spain, came second with revenue of PLN 4.9 billion and 4.2% growth, compared to 2013. Austrian Strabag was also in the top three, which was the only company that saw a revenue drop in 2014 (revenue decreased 5% to PLN 3.1 billion). Revenue was, however, sufficient to maintain its position from the previous year. Apart from the Skanska Group, the largest revenue growth by value was seen by the Erbud Group and Torpol Group, whose revenue increased by PLN 468 million and PLN 360 million, respectively. The Torpol Group also saw the largest revenue growth expressed as a percentage, while revenue generated by the Mostostal Zabrze Group increased by 50%. Thanks to the good performance, both groups debuted in this year’s ranking.

The Polimex- Mostostal Group reported the biggest year-on-year drop in revenue (PLN 261 million), but it has managed to maintain the fourth place that it occupied in the previous year. Apart from Polimex – Mostostal Group (an 11% drop in revenue), the largest revenue drop in excess of 5% was seen by the Mostostal Warszawa Group and Warbud S.A. (7.6% and 6.4% year-on-year, respectively).

Please note that in 2014, the number of companies that generated revenue growth was much bigger than in the previous year. Only four companies experienced a decrease in revenue. At the same time, the revenue of 11 companies increased.

Last year’s ranking was the opposite case.The average increase in revenue of 9% generated by the largest entities in the construction industry confirms the development of the construction market and reflects the growth seen in the industry in 2014.

8

No. Company nameOperating

margin 2014Operating

margin 2013

Change expressed in

PLN

Change expressed in %

1 Budimex Group 432 680 395 416 37 264 9%

2 Trakcja Group* 202 128 93 241 108 887 117%

3 Warbud S.A.* 136 033 116 516 19 517 17%

4 Strabag Group** 114 172 8 527 105 645 1239%

5 Mostostal Warszawa Group 103 927 -154 573 258 500 167%

6 Erbud Group 99 242 90 910 8 332 9%

7 PBG Group* 94 494 -26 952 121 446 451%

8 Mostostal Zabrze Group 73 791 45 725 28 066 61%

9 Elektrobudowa Group 73 218 63 147 10 071 16%

10 Mirbud Group 67 240 54 837 12 403 23%

11 Unibep Group 66 713 58 309 8 404 14%

12 Torpol Group 48 368 24 294 24 074 99%

13 Polimex-Mostostal Group* -201 623 24 673 -226 296 -917%

14 Skanska Group no data no data no data no data

15 PORR (Polska) S.A. no data no data no data no data

Average 100 799 61 082

Average operating margin (%) 5.86% 3.85%

Table 1.2: Operating margin of the 15 biggest companies in nominal terms (PLN’000)

For the Strabag Group companies, preparing profit and loss account by nature of expense, the operating margin reflects selling expenses and general and administrative costs (unlike that of the remaining companies).

Source: Financial statements for the years 2014-2013

1.2. Ranking of the largest construction companies by 2014 operating marginThe operating margin earned by the biggest construction companies, expressed as the operating revenue less costs of sales (excluding other operating revenue and expenses), indicates that the revenue increase in 2014 was accompanied by a growth in the profit of core operations. The average operating margin of the largest companies increased by nearly PLN 40 million, with a profit on core operations for the largest companies increased by nearly PLN 40 million in 2014 (compared to a PLN 117 million increase in 2013). As in the preceding year, the Budimex Group recorded the biggest operating margin and earned a profit on sales of PLN 433 million. The Trakcja Group came second with an operating margin of PLN 202 million, i.e. more than double the previous year. Warbud S.A. took third place, having generated an operating margin of PLN 136 million (more than PLN 66 million lower than the Trakcja

Group). Only one entity in the ranking, the Polimex-Mostostal Group, incurred an operating loss (PLN 202 million) in 2014.

Polish construction companies 2015: Key players, growth factors and industry development prospects 9

12.96% 12.62%

8.74% 8.55%

6.92% 6.88%6.61% 6.24% 6.18% 6.18% 5.87%

3.64%

-9.59%

5.86%

10.39%

7.32%8.33% 7.95%

5.85%

-9.46%

6.97%

5.84%6.33%

-2.20%

7.43%

0.26%1.04%

b.d. b.d.

3.85%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

-15.00%

Averag

e

Strab

ag G

roup

**

Budim

ex G

roup

Torp

ol Gro

up

Trakc

ja Gro

up*

Elektr

obud

owa G

roup

Mos

tosta

l Zab

rze G

roup

Unibep

Gro

up

Mirb

ud G

roup

Erbud

Gro

up

Mos

tosta

l War

szawa G

roup

PBG G

roup

*

Polim

ex-M

osto

stal G

roup

*

Skan

ska G

roup

2014 2013

Chart 1.2: Operating margin of the largest construction companies (in percent)

Source: Financial statements for the years 2014-2013

Furthermore, 13 ranked companies have managed to improve their operating margin and in only one case it is worse than for the preceding 12 months. The Mostostal Warszawa Group saw the biggest growth (in excess of PLN 258 million), while the Polimex-Mostostal Group saw the biggest decrease (in excess of PLN 226 million). The ranking indicates that ten of thirteen entities that disclosed their data have generated a profit on sales both in 2013 and in 2014.

The average operating margin was positive and amounted to 5.86% in 2014, indicating a growth in excess of 2 p.p. vs. 2013. Warbud S.A. had the best result with an operating margin of 12.96%.

The Trakcja Group was second with an operating margin of 12.62%, followed by the Budimex Group with the positive ratio of 8.74%. The Polimex-Mostostal Group occupied the opposite end of the scale with the operating margin of minus 9.59%.

In summary: in 2014, along with a growth in revenue, profitability of operations of the largest companies further improved, although not as rapidly as in the previous year (an increase by 5.69 p.p.) when the number of unprofitable contracts performed by companies was significantly limited.

10

Table 1.3: Net profit of the 15 biggest companies in nominal terms (PLN’000)

Source: Financial statements for the years 2014-2013

No. Company nameNet profit

2014Net profit

2013Change expressed

in PLNChange

expressed in %

1 Budimex Group 193 938 301 300 -107 362 -36%

2 Strabag Group** 148 330 74 351 73 979 99%

3 Trakcja Group* 50 391 29 995 20 396 68%

4 Warbud S.A.* 48 416 32 555 15 861 49%

5 Erbud Group 27 892 18 079 9 813 54%

6 Elektrobudowa Group 27 015 17 585 9 430 54%

7 Torpol Group 25 009 4 790 20 219 422%

8 Unibep Group 20 925 16 211 4 713 29%

9 Mostostal Zabrze Group 19 134 7 648 11 486 150%

10 Mirbud Group 17 583 16 601 982 6%

11 Mostostal Warszawa Group -8 738 -314 380 305 642 97%

12 PBG Group* -80 799 207 512 -288 311 -139%

13 Polimex-Mostostal Group* -153 226 -260 889 107 663 41%

14 Skanska Group no data no data no data no data

15 PORR (Polska) S.A. no data no data no data no data

Average 25 836 11 643

Average net margin (%) 1.50% 0.73%

1.3. Ranking of the largest construction companies by 2014 net profit The net profit is a material indicator reflecting the overall condition of construction companies. The median net profit of the key 13 companies that disclosed their data for 2014 was positive and totalled PLN 26 million, i.e. a growth in excess of PLN 14 million compared with PLN 12 million in 2013.

The Budimex Capital Group earned the highest net profit of PLN 194 million which represents a 36% year-on-year decrease. However, the profit for 2013 included a gain from selling shares in the subsidiary Budimex Danwood. Following elimination of the transaction balance, the net profit of the Budimex Group for 2014 improved by approx. 34%. The Strabag Capital Group came second with a net profit of PLN 148 million, and the Trakcja Capital Group was third with a net profit

of PLN 50 million. Performance of Warbud S.A. was similar with a net profit of PLN 48 million. The Polimex-Mostostal Group generated a loss of PLN 153 million and closed the ranking.

As many as ten ranked companies that disclosed their data earned a net profit, whereas three incurred a loss. In the previous year, ten entities had generated a net profit, but the average net profit of all ranked companies had been lower. Additionally, please note that ten companies earned a net profit both in 2013 and 2014.

Polish construction companies 2015: Key players, growth factors and industry development prospects 11

4.73% 4.61%3.92%

3.23% 3.15% 2.44% 2.22% 1.94% 1.81% 1.65%

-0.58%

-5.28%

-7.29%

b.d. b.d.

1.50%2.25%

2.90%

6.34%

1.15% 2.35% 1.94% 1.33% 1.76% 1.77% 1.48%

-19.25%

16.90%

-11.04%

0.73%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%Ave

rage

Strab

ag G

roup

**

Budim

ex G

roup

Torp

ol Gro

up

Trakc

ja Gro

up*

Elektr

obud

owa G

roup

Mos

tosta

l War

szawa G

roup

Polim

ex-M

osto

stal G

roup

*

PBG G

roup

*

Erbud

Gro

up

Mirb

ud G

roup

Unibep

Gro

up

Mos

tosta

l Zab

rze G

roup

Skan

ska G

roup

2014 2013

Source: Financial statements for the years 2014-2013

The average net profit expressed as a percentage in 2014 was slightly higher than in the previous year and amounted to 1.5%. The Strabag Group and Warbud S.A. were nearly equal and came first with net profitability of 4.7% and 4.6%, respectively. The Budimex Group came third with a net profitability of 3.9%.

The aforementioned data shows that, similarly to the sales result, net profitability of most ranked companies has improved. Thus, events not directly related with their core business and performance on financial operations have positively affected the overall performance (net profitability doubled year-on-year, while the gross margin growth rate was slightly lower).

Chart 1.3: Net margin of the largest construction companies (in percent)

12

78.43%

b.d.

b.d.

0.49

0.58

0.70

0.58

0.66

0.73

0.66

0.75

0.83

0.88

0.87

0.83

1.22

78.48%

0.51

0.53

0.63

0.63

0.70

0.70

0.73

0.75

0.80

0.84

0.86

0.86

1.31

0.00 0.25 0.50 0.75 1.00 1.25 1.50

Average

Warbud S.A.*

Mostostal Warszawa Group

PORR (Polska) S.A.

Skanska Group

Unibep Group

Strabag Group**

Erbud Group

Elektrobudowa Group

Polimex-Mostostal Group*

Trakcja Group*

Mirbud Group

Torpol Group

Mostostal Zabrze Group

PBG Group*

Budimex Group

2014 2013

Chart 1.4: Debt/equity ratio in 2013 - 2014

Source: Financial statements for the years 2014-2013

1.4. Debt of 15 biggest construction companies in 2014Analysis of the debt ratios shows that the biggest construction companies’ debt was relatively high in 2014 (similar to 2013). In 2014, the average debt (weighted by revenue) remained flat and amounted to 78%. In the aforementioned period, six companies increased and six reduced the percentage of debt in their financing structure.

Similarly to 2013, six entities used debt capital to the extent corresponding to at least 75% of their assets.

In 2014, as in 2013, the PBG Group has the highest percentage debt with the total debt constituting 131% of its total assets (i.e. it exceeded the value of the company’s assets by 31%) and has increased by 9% compared to 2013. Following the loss of liquidity in 2012, the company had been put into liquidation with an arrangement option, which was voted for by its creditors in 2015. Among the remaining companies, Erbud had the largest debt increase, from 66% at the end of 2013 to 73% at the end of 2014. The growth in the debt of the other companies did not exceed 5 p.p. in 2014.

Polish construction companies 2015: Key players, growth factors and industry development prospects 13

No. Company nameCapital

expenditure 2014Capital

expenditure 2013Change expressed

in PLNChange expressed

in %

1 Budimex Group 48 401 17 724 30 677 173%

2 Polimex-Mostostal Group* 26 869 29 533 -2 664 -9%

3 Trakcja Group* 25 674 18 238 7 436 41%

4 Strabag Group** 24 464 44 580 -20 116 -45%

5 Warbud S.A.* 19 187 11 085 8 102 73%

6 Mostostal Zabrze Group 19 011 10 554 8 457 80%

7 Mirbud Group 17 212 3 158 14 054 445%

8 PBG Group* 17 125 179 970 -162 845 -90%

9 Erbud Group 16 077 12 007 4 070 34%

10 Torpol Group 15 046 7 026 8 020 114%

11 Elektrobudowa Group 11 489 17 399 -5 910 -34%

12 Mostostal Warszawa Group 8 279 12 684 -4 405 -35%

13 Unibep Group 3 191 11 734 -8 543 -73%

14 Skanska Group no data no data no data no data

15 PORR (Polska) S.A. no data no data no data no data

Total 252 025 375 692 -123 667 -33%

Average 19 387 28 899 -9 513 -33%

Source: Financial statements for the years 2014-2013

Table 1.5: Capital expenditure of the largest companies in nominal terms (PLN’000)

Among the ranked companies, the Mostostal Zabrze Group and Trakcja Group had the lowest debt/equity ratio of 51% and 53%, respectively.

At the end of 2014, the average debt/equity ratio of the biggest construction companies remained unchanged compared to the previous year. The real picture is distorted by the PBG Group, which has both the highest debt/equity ratio and saw the biggest growth among all analysed companies.

1.5. Capital expenditure to sales ratio of the largest companies in 2014 The capital expenditure (expenditure on property, plant and equipment and intangible assets) to sales ratio of companies in the construction industry is usually relatively low due to high sales volume and relatively low capital expenditure necessary to provide construction services. In 2014, the total capital expenditure of the biggest companies was PLN 252 million, i.e. nearly 33% lower year-on-year. It is also worth noting that only six construction companies reduced their capital expenditure compared with the previous year.

14

1.82%

b.d.

b.d.

1.27%

0.78%

1.35%

0.98%

0.37%

1.92%

14.66%

1.25%

1.43%

0.34%

0.99%

1.69%

1.84%

1.13%

0.30%

0.55%

0.78%

0.95%

0.98%

1.04%

1.12%

1.28%

1.60%

1.77%

1.83%

1.94%

2.20%

0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 14.00% 16.00%

Average

PORR (Polska) S.A.

Skanska Group

Unibep Group

Mostostal Warszawa Group

Strabag Group**

Erbud Group

Budimex Group

Elektrobudowa Group

PBG Group*

Polimex-Mostostal Group*

Trakcja Group*

Mirbud Group

Warbud S.A.*

Torpol Group

Mostostal Zabrze Group

Chart 1.5: Capital expenditure to sales ratio (data for 2014 and 2013)

Source: Financial statements for the years 2014-2013

2014 2013

As regards nominal capital expenditure, the Budimex Group was the leader in 2014 with the total of PLN 48 million (i.e. a 173% increase compared to 2013). The Polimex-Mostostal Group with a total expenditure of PLN 27 million (a 9% drop year-on-year) and the Trakcja Group with the total expenditure of PLN 26 million (a 41% increase year-on-year) came second and third, respectively.

The general drop in year-on-year capital expenditure resulted mostly from a significant reduction in capital expenditure of the PBG Group, which used to be the ranking leader in this respect. Having eliminated the PBG Group from the ranking, the general level of capital expenditure among the largest construction companies increased by 20% compared to 2013.

In 2014, the capital expenditure to revenue ratio was 1.13% and was almost 0.7 p.p. lower than in 2013. The drop resulted from a significant reduction in capital expenditure in the PBG Group vs. 2013 on the one hand, and the general increase in revenue generated by construction companies on the other. The Mostostal Zabrze Group saw the highest capital expenditure to sales ratio.

In 2014, the Unibep Group had the lowest capital expenditure to sales ratio (0.3% in 2014 vs. 1.27% in 2013) with the Mostostal Warszawa Group coming second last (0.55% vs. 0.78% in 2013).

Polish construction companies 2015: Key players, growth factors and industry development prospects 15

No. Company nameExport sales

revenue2014

Export sales revenue

2013

Nominal change

Percentage change

1 Trakcja Group* 565 884 462 926 102 958 22%

2 Polimex-Mostostal Group* 383 978 588 481 -204 503 -35%

3 Unibep Group 319 497 255 636 63 861 25%

4 Mostostal Zabrze Group 254 503 235 578 18 925 8%

5 PBG Group* 226 268 230 512 -4 244 -2%

6 Budimex Group 195 632 550 574 -354 942 -64%

7 Erbud Group 195 373 209 736 -14 363 -7%

8 Mostostal Warszawa Group 144 453 414 262 -269 809 -65%

9 Elektrobudowa Group 67 336 229 269 -161 933 -71%

10 Torpol Group 28 507 13 927 14 580 105%

11 Strabag Group** 8 863 5 545 3 318 60%

12 Warbud S.A.* 0 0 0 0%

13 Mirbud Group 0 0 0 0%

14 Skanska Group No data No data No data No data

15 PORR (Polska) S.A. No data No data No data No data

Total 2 390 294 3 196 446 -806 152 -25%

Average 183 869 245 880 -62 012 -25%

Table 1.6.1: Export sales revenue of the largest construction companies in nominal terms (PLN’000)

Financial statements for the years 2014-2013

1.6. Revenue of the largest construction companies by geography and by type in 2014

1.6.1 Revenue by geography The largest construction companies operating in Poland operate also on foreign markets, but their export sales volume is relatively small. The median revenue generated by the biggest companies abroad amounted to PLN 184 million and was PLN 62 million lower than in 2013, marking a 25% year-on-year drop. The Trakcja Group generated the highest foreign revenue amounting to PLN 566 million, i.e. 22% higher than in 2013. The Group operates on the Lithuanian market. Polimex-Mostostal Group with a total revenue of PLN 384 million (a 35% drop year-on-year) was second

and the Trakcja Group with a total revenue of PLN 319 million (a 25% increase year-on-year) came third. Export operations of the Polish construction companies have focused on the neighbouring markets, mostly Eastern Europe, Scandinavia and Germany.

16

Chart 1.6.1: Percentage share of export sales in total sales of the largest companies in 2014

Source: Financial statements for the years 2014-2013

2014 2013

On average, export sales revenue amounted to 11% of total operating revenue (4 p.p. lower than in 2013). Export sales of three entities was in excess of 30% of total sales revenue (the Trakcja Group with 35%, the Unibep Group and the Mostostal Zabrze Group with 30% each).

Sales analysis by geography indicates that the number of entities in the construction sector that find their clients abroad has been increasing, as they search for new markets to diversify their operational risk. In light of the expected reduction in new investments once the EU funds for the 2014-2020 perspective are consumed, the trend may further increase.

35%

30% 30%

18%

15%

12%10%

6%4% 4%

0% 0% 0%

11%

36%

28%

41%

25%

19%17%

25% 25%

12%

3%0% 0% 0% b.d. b.d.

15%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Averag

e

Trakc

ja Gro

up*

Unibep

Gro

up

Mos

tosta

l Zab

rze G

roup

Polim

ex-M

osto

stal G

roup

*

PBG G

roup

*

Erbud

Gro

up

Mos

tosta

l War

szawa G

roup

Elektr

obud

owa G

roup

Budim

ex G

roup

Torp

ol Gro

up

Strab

ag G

roup

**

Mirb

ud G

roup

Skan

ska G

roup

Polish construction companies 2015: Key players, growth factors and industry development prospects 17

Skanska Group

Budimex Group

Strabag Group**

Polimex-Mostostal Group

Erbud Group

Trakcja Group

PBG Group

Mostostal Warszawa Group

Elektrobudowa Group

Unibep Group

Warbud S.A.

PORR (Polska) S.A.

Mirbud Group

Mostostal Zabrze Group

Torpol Group

MARKETS

DomesticWestern Europe

Eastern Europe

Scandinavian Asian OtherTOTAL

(2014, PLN’000)

5 081 675

4 949 939

3 133 492

2 102 197

1 692 055

1 601 674

1 530 248

1 509 524

1 108 316

1 079 703

1 049 886

1 045 019

971 603

862 650

775 399

28 493 380TOTAL:

4 754 307

3 124 629

1 718 219

1 496 682

1 035 790

1 365 071

760 206

971 603

608 147

no data

No information on the place of origin of the export revenue Export revenue value - 8 863

No information on the place of origin of the export revenue Export revenue value - 383 978

565 884

79 701

191 197 63 306

Chart 1.6.2: Sales of the largest companies by geography in 2014

Source: Financial statements for the years 2014-2013

no data

158 085 37 547

195 373

1 303 980 No information on the place of origin of the export revenue Export revenue value - 226 268

23 090 39 959 1 703

1 040 980 21 545 17 427 7 5929 806 10 966

173 964 123 323 5822 152

1 049 886

No information on the place of origin of the export revenue Export revenue value - 28 507746 892

18

Budimex Group

Skanska Group

Strabag Group**

Polimex-Mostostal Group*

Mostostal Warszawa Group

Trakcja Group*

PBG Group*

Erbud Group

Warbud S.A.*

PORR (Polska) S.A.

Mirbud Group

Unibep Group

Elektrobudowa Group

Mostostal Zabrze Group

Torpol Group

MARKETS

DomesticWestern Europe

Eastern Europe

Scandinavian Asian OtherTOTAL

(2013, PLN’000)

4 749 459

4 362 167

3 298 754

2 362 752

1 633 363

1 274 222

1 227 600

1 223 609

1 121 472

1 030 076

937 301

920 548

905 553

575 117

415 717

26 037 710TOTAL:

4 198 885

3 293 209

1 774 271

1 219 101

1 013 873

937 301

664 912

676 284

401 790

No information on the place of origin of the export revenue Export revenue value - 5 545

No information on the place of origin of the export revenue Export revenue value - 588 481

209 736

507 479 43 095

40 717

141 931 113 180 525

232 431 122 263 56 731 2 783 54

Chart 1.6.3: Sales of the largest companies by geography in 2013

50 668 90 607 19 600

Source: Financial statements for the years 2014-2013

no data

811 295 462 926

1 121 472

no data

27 597

339 539 203 128 32 450

No information on the place of origin of the export revenue Export revenue value - 13 927

No information on the place of origin of the export revenue Export revenue value - 230 512997 088

Polish construction companies 2015: Key players, growth factors and industry development prospects 19

The sales revenue structure by type shows that the largest construction companies have focused on road and railway construction projects. Construction projects for the power engineering sector have had an increasing share in revenue, too.

Skanska Group

Budimex Group

Strabag Group**

Polimex-Mostostal Group

Erbud Group

Trakcja Group

PBG Group

Mostostal Warszawa Group

Elektrobudowa Group

Unibep Group

Warbud S.A.

PORR (Polska) S.A.

Mirbud Group

Mostostal Zabrze Group

Torpol Group

MARKETS

General construction

Residental construction

Road and railway

construction

Construction engineering

Power construction

Other activities

TOTAL(2014, PLN’000)

5 081 675

4 949 939

3 133 492

2 102 197

1 692 055

1 601 674

1 530 248

1 509 524

1 108 316

1 079 703

1 049 886

1 045 019

971 603

862 650

775 399

28 493 380TOTAL:

4 566 628

no data

239 740

743 523

755 188

1 474 086

1 188 076

466 173

160 185

968 837

434 874

904 583

383 311

427 447

45 448

127 588

342 172

3 159

203 733

211 309

102 437

680 687

20 211

*** General construction and construction engineering

Source: Financial statements for the years 2014-2013

Chart 1.6.2.1: Sales of the largest construction companies by type in 2014

no data

no data

1 397 537 88 885

1 189 302317 063

124 871

1 038 747 11 139

434 292

181 963***

20

Budimex Group

Skanska Group

Strabag Group**

Polimex-Mostostal Group

Mostostal Warszawa Group

Trakcja Group*

PBG Group*

Erbud Group

Warbud S.A.*

PORR (Polska) S.A.

Mirbud Group

Unibep Group

Elektrobudowa Group

Mostostal Zabrze Group

Torpol Group

MARKETS

General construction

Residental construction

Road and railway

construction

Construction engineering

Power construction

Other activities

TOTAL(2013, PLN’000)

4 749 459

4 362 167

3 298 754

2 362 752

1 633 363

1 274 222

1 227 600

1 223 609

1 121 472

1 030 076

937 301

920 548

905 553

575 117

415 717

26 037 710TOTAL:

4 005 617

no data

367 243

998 102

343 006

623 640

126 008***

79 658

774 302

96 219

791 382

484 705

596 795

1 144 184

1 107 460

743 842

607 332

980

130 038

453 298

49 630

14 012

75 468

199 659

281 913

21 684

1 147 678

394 033

*** General construction and construction engineering

Source: Financial statements for the years 2014-2013

no data

no data

516 827

627 755 93 134

449 109

Chart 1.6.2.2: Sales of the largest construction companies by type in 2013

Polish construction companies 2015: Key players, growth factors and industry development prospects 21

17.45%

b.d.

b.d.

b.d.

0.06%

1.25%

5.22%

4.06%

15.66%

10.21%

8.05%

31.13%

21.69%

25.70%

36.93%

78.09%

13.30%

0.21%

1.06%

2.61%

2.69%

7.74%

7.97%

10.54%

18.38%

19.57%

20.33%

22.36%

78.91%

0.0% 25.0% 50.0% 75.0% 100.0%

Average

PORR (Polska) S.A.

Strabag Group**

Skanska Group

Mostostal Warszawa Group

Warbud S.A.*

Torpol Group

Erbud Group

Budimex Group

Trakcja Group*

Mirbud Group

Elektrobudowa Group

Unibep Group

Polimex-Mostostal Group*

PBG Group*

Mostostal Zabrze Group

Chart 1.6.2.3: Capital expenditure to sales revenue ratio (data for 2014 and 2013)

Source: Financial statements for the years 2014-2013

2014 2013

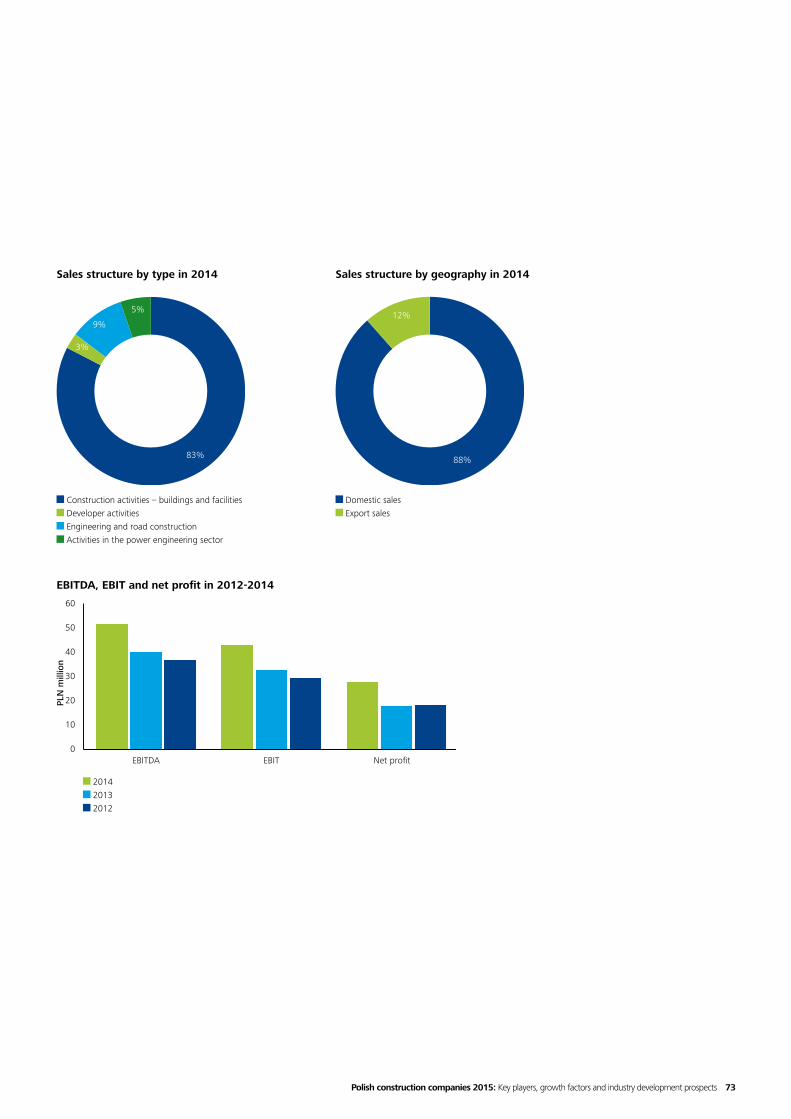

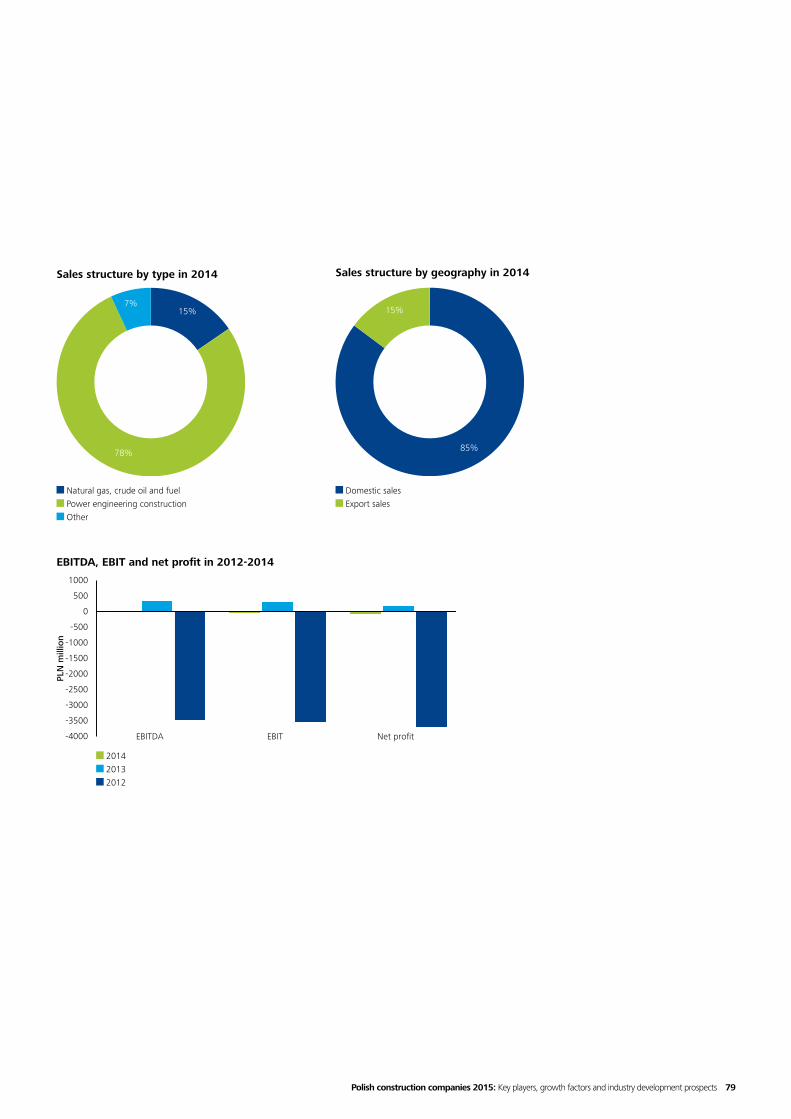

In nominal terms, the Mostostal Zabrze Group and Polimex-Mostostal Group had the largest share in other non-construction revenue in 2014 with PLN 681 million and PLN 427 million, respectively. As compared to 2013, the average weighted share of other operating revenue expressed as a percentage dropped from 17.5% to 13.3%. In 2014, in most cases, the share of construction and assembly services as a percentage of total revenue was in the range of 80-100%. The Mostostal Zabrze Group remains the entity with the most diversified operations (79%) including, along with construction, assembly and production.

In 2014, of the twelve companies analysed above that generated revenue on other operations, just three managed to increase the percentage share of revenue from non-construction operations as a percentage of total revenue, compared to 2013. The main reason was a growth in revenue generated by the largest construction companies on construction and assembly in 2014.

22

Chart 1.7: Changes in WIG and WIG-Budownictwo indexes in 2005-2014

Source: Deloitte analysis based on data available on the WSE website.

1.7. Market capitalisation of the largest construction companies listed on the Warsaw Stock Exchange as at 31 December 2014The improving investor sentiment regarding companies indexed with WIG-Budownictwo (WIG BUD) has slightly slowed down in 2014.

In 2014, the WIG Budownictwo index decreased by 5% compared to 2013, while the main WIG index was close to the previous year’s level at the end of 2014.

Out of the 15 biggest construction companies, as many as 11 were listed on the Warsaw Stock Exchange in 2014, and we used them as our basis for the capitalisation ranking. At the end of 2014, the combined market value of the eleven construction companies listed on the Warsaw Stock Exchange was PLN 6.1 billion, i.e. PLN 0.2 billion higher than the combined market value of these companies at the end of 2013. Expressed as a percentage, the total capitalisation increased by 4%.

WIG WIG BUDOW

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

2005

-01-

0720

05-0

3-16

2005

-05-

3020

05-0

8-04

2005

-10-

1220

05-1

2-21

2006

-02-

2820

06-0

5-11

2006

-07-

1920

06-0

9-26

2006

-12-

0420

07-0

2-13

2007

-04-

2420

07-0

7-04

2007

-09-

1120

07-1

1-19

2008

-01-

3120

08-0

4-10

2008

-06-

2020

08-0

8-28

2008

-11-

0420

09-0

1-19

2009

-03-

2620

09-0

6-05

2009

-08-

1320

09-1

0-20

2009

-12-

3020

10-0

3-09

2010

-05-

1920

10-0

7-27

2010

-10-

0120

10-1

2-10

2011

-02-

1820

11-0

4-29

2011

-07-

0820

11-0

9-15

2011

-11-

2420

12-0

2-02

2012

-04-

1220

12-0

6-22

2012

-08-

3120

12-1

1-08

2013

-01-

2220

13-0

4-02

2013

-06-

1320

13-0

8-21

2013

-10-

2820

14-0

1-14

2014

-03-

2120

14-0

6-02

2014

-08-

0820

14-1

0-16

2014

-12-

29

Polish construction companies 2015: Key players, growth factors and industry development prospects 23

59.37%

6.42%

5.76%

5.44%

5.33%

4.98%

4.74%3.76%

1.97%1.84%

0.39%

No. Company nameMarket

capitalisation 31.12.2014

Market capitalisation 31.12.2013

Change expressed in PLN

Change expressed in %

1 Budimex S.A. 3 612 509 3 369 973 242 536 7%

2 Trakcja PRKiI S.A. 390 637 530 443 -139 807 -26%

3 Elektrobudowa S.A. 350 373 522 237 -171 863 -33%

4 Mostostal Zabrze S.A. 331 070 292 296 38 774 13%

5 Erbud S.A. 324 153 432 167 -108 015 -25%

6 Polimex-Mostostal S.A. 303 166 190 758 112 408 59%

7 Unibep S.A. 288 281 275 361 12 919 5%

8 Torpol S.A. 229 011 IPO on 8 July 2014

9 Mostostal Warszawa S.A. 120 000 89 800 30 200 34%

10 Mirbud S.A. 112 190 117 000 -4 810 -4%

11 PBG S.A. 23 444 31 592 -8 148 -26%

Total 6 084 833 5 851 628 233 205 4%

Table 1.7: Capitalisation of the largest construction companies listed on Warsaw Stock Exchange as at 31 December 2014

Budimex S.A. Trakcja PRKiI S.A. Elektrobudowa S.A. Mostostal Zabrze S.A. Erbud S.A. Polimex-Mostostal S.A. Unibep S.A. Torpol S.A. Mostostal Warszawa S.A. Mirbud S.A. PBG S.A.

Source: Deloitte analysis based on data available on the WSE website.

Chart 1.7.1: Share of the largest companies listed on the Warsaw Stock Exchange in total capitalisation as at 31 December 2014

Five of the eleven companies analysed experienced a drop in market value. Elektrobudowa S.A. saw the biggest drop: in 2014, its market value decreased by 33%. Budimex S.A. has remained the market value leader since 2011, with a capitalisation of PLN 3,613 million (a 7% increase compared to 2013). Trakcja PRKiI S.A. was second, and Elektrobudowa S.A. third with capitalisation of PLN 391 million and PLN 350 million, respectively. At the end of 2014, capitalisation of Budimex S.A. constituted over 59% of the total capitalisation of the eleven largest companies in our ranking listed on Warsaw Stock Exchange (a 2 p.p. drop vs. 2013).

In summary, please note that market capitalisation of the largest construction companies increased by 4% at the end of 2014 year-on-year. The trend agrees with a growth in the construction manufacturing ratio by 0.4% in 2014 and a 9% increase in revenue of the companies included in our ranking compared to 2013.

Source: Deloitte analysis based on data available on the WSE website.

* The financial data for 2013 was reconciled to the financial statements for 2014 following adjustments of the opening balance.

** Due to absence of consolidated financial statements, the financial data of the Strabag Group include (for simplification purposes) the total revenue of Strabag Sp. z o.o. and StrabagInfrastrukturaPołudnie Sp. zo.o.

The financial data of Strabag for 2013 was reconciled to the financial statements for 2014 following adjustments of the opening balance.

24

Chapter 2. Prospects for development of construction companies in Poland

Polish construction companies 2015: Key players, growth factors and industry development prospects 27

Construction Total economy

In the years to come, the construction engineering market shall grow the fastest, mostly thanks to an inflow of funds from the EU. The growth in this segment should peak in the years 2016-2018. The market of building construction shall increase too, in the coming years, although the growth will be slower. We assume the increase shall include the office, housing and warehousing segments.

Krzysztof Andrulewicz, CEO of Skanska S.A.

28

2.1 IntroductionThe second part of the report begins with an analysis of the key factors shaping the construction sector and a presentation of the changes taking place in the sector as seen through statistics on bankruptcies and employment in construction companies. Further herein we will discuss the characteristics and current conditions of each segment in the construction sector and analyse planned expenditures in the short- and medium-term perspective. This part of the report is concluded with a summary of the present condition and key growth factors for the sector from the viewpoint of representatives of the largest construction companies in Poland.

Following a period of slowdown in 2012-2013 resulting from the completion of large capital projects included in the previous EU perspective and organisation of the EURO 2012 tournament, the construction industry in Poland has been recovering.

Despite its growth in 2014 being very small (0.4%), the prospects are positive and the growth should accelerate in the coming years.

A number of signals from the market indicate an improvement in the standing of the construction sector. Since 2014, a significant decrease in the number of bankruptcies announced by construction companies has been observed. Additionally, in the initial months of 2015, a slow increase in employment has been observed, accompanied with further projections of employment growth.1 In the years to come, following the expected commencement of infrastructural investments, an increased labour demand is predicted, in particular in relation to road construction, which may even result in a labour shortage. The economic climate indicator as examined by the Main Statistical Office has confirmed the reversal of the negative trend in the construction sector. Since the beginning of 2013, the indicator for the sector has been growing, having outgrown the indicator for the entire economy in mid-2014.

1 More information provided in the section “Employment in the construction sector”

Economic climate indicator

Source: Main Statistical Office

70

80

90

100

110

120

130

I.08

IV.0

8V

II.08

X.0

8I.0

9IV

.09

VII.

09X

.09

I.10

IV.1

0V

II.10

X.1

0I.1

1IV

.11

VII.

11X

.11

I.12

IV.1

2V

II.12

X.1

2I.1

3IV

.13

VII.

13X

.13

I.14

IV.1

4V

II.14

X.1

4I.1

5IV

.15

VII.

15

Drawing the right conclusions from the previous EU financial perspective is of key importance. We must avoid another accumulation of projects that would generate cyclical speculation on the labour market, to include costs of labour and materials, and finally the costs of projects.

Paulo Silva, Management Board Member, Mota-Engil Central Europe S.A.

Polish construction companies 2015: Key players, growth factors and industry development prospects 29

The inflow of new EU funds shall be the strongest incentive improving the condition of the infrastructural construction segment in the coming years. Under the new 2014-2020 financial perspective, Poland shall receive a record amount of funds EUR 120.1 billion. The amount mostly includes funds under the Cohesion Policy (EUR 82.5 billion), Common Agricultural Policy (EUR 32.1 billion) and European Maritime and Fisheries Fund (EUR 0.5 billion). The construction sector shall mostly use funds under the Cohesion Policy. Significant portion of EU funding will be spend on infrastructural construction projects.

Representatives of the biggest construction companies see new opportunities offered under the new EU financial perspective. In order to avoid the accumulation of projects already experienced with investments carried out for EURO 2012, the General Directorate for National Roads and Motorways has already accepted tenders for PLN 30 billion out of the total of PLN 107 billion planned for investments to be carried out in the years 2014-2025 (as at 11 September 2015).

The attitude of PKP PLK, which, by the end of August, failed to call for any tenders under the new perspective, gives rise to concerns. In order to counteract the anxiety, PKP PLK has announced the Great Railway Investment Campaign, which includes initiatives aimed at improving cooperation with contractors and accelerating the tender procedures. The introduction of a two-stage procedure, additional tender evaluation criteria (along with the price) and advance payments for contracts, payments for materials stored at the construction site or partial payments for the performed work will be the measures adopted to achieve the improvement.

A strong growth in demand observed since 2014 has been the factor of crucial importance for positive prospects of the construction sector. The current macro-economic standing accompanied with access to government subsidies provides grounds for stabilisation in the housing segment in the nearest future.

This has been supported by the record area of office space constructed (622,000 sq. m.). Based on the analysed number of continued and planned investments in the portfolios of construction companies, the coming quarters should support the current positive trend.

In the coming years, some construction companies are planning to further diversify their business through expanding their construction services onto new construction market sectors or developing new non-construction business.

Additionally, certain companies see their potential in geographical diversification, and are planning investments in countries such as the Czech Republic, Slovakia, Romania or Hungary, as well as in Western Europe and Scandinavia.

All of the aforementioned factors are very promising for the Polish construction industry which is entering a new period marked by great opportunities for development.In the next section, we will try to summarise the current opportunities and describe planned directions for market development.

30

2.2. Key factors in the development of the construction market in PolandIn the coming years, the condition of the construction sector shall be determined by both the economic growth in Poland and infrastructural investments co-financed with EU funds under the new 2014-2020 financial perspective, as well as with domestic funds.

Economic growthIn 2014, following an increase in domestic demand, the Polish economy saw a growth of approx. 3.5% after a GDP growth slowdown seen in the years 2012-2013. According to the Economist Intelligence Unit, in 2015-2018 the average annual GDP growth will reach 3.15%. The future increase in GDP shall be supported by large investments related to the new EU perspective, a growth in net exports, private consumption, the improved standing of the labour market and low interest rates. In a longer run, the level of economic growth in Poland shall get closer to that observed in Western European countries, which will determine further GDP increase. The process is expected to be slow, though, in light of the current condition of the global economy and absence of rapid reforms that could materially increase employee productivity.

Public debtAbility to co-fund infrastructural projects from the national and local budgets depends significantly on the public debt level. At the end of 2014, the public debt to GDP ratio was 47.7%. According to the public debt management strategy for 2015-2018 proposed by the Minister of Finance in 2015, the public debt to GDP ratio shall remain at 48% and further decrease to 44.5% in 2018.

EU fundsThe inflow of EU funds under the 2014-2020 financial perspective is a major factor underlying the development of the Polish construction market. The funds allocated to Poland under the cohesion policy amount to EUR 82.5 billion and include EUR 45.6 billion to be used for subsidies under National Operational Programmes.

Public debt as a GDP percentage

Source: Ministry of Finance „Strategia zarządzania długiem sektora finansów publicznych w latach 2015-2018”, September 2014

GDP growth in Poland

Source: EUI “Country Forecast Poland - August 2015 update”

5.0%

1.6%

3.7%

4.8%

1.9%1.7%

3.5%3.3%

3.0% 2.9%

3.4%

0%

1%

2%

3%

4%

5%

6%

2008

2009

2010

2011

2012

2013

2014

2015

P

2016

P

2017

P

2018

P

53.4%52.6%

53.9%

47.7% 48.0%46.9%

46.0%

44.5%

40%

42%

44%

46%

48%

50%

52%

54%

56%

58%

60%

2011 2012 2013 2014 2015P 2016P 2017P 2018P

Technical assistance (EUR 0.7 bn) Eastern Poland (EUR 2 bn) Digital Poland (EUR 2.2 bn) Knowledge Education Development (EUR 4.7bn) Intelligent Development (EUR 8.6 bn) Infrastructure and Environment (EUR 27.4 bn)

Development of TEN-T road network and multimodal transport

Road infrastructure for cities Development of railway transport in Poland Development of low-emission public transport Other priorities

Rural Areas Development Programme Regional Operational Programmes National Operational Programmes

Source: Ministry of Infrastructure and Development

Polish construction companies 2015: Key players, growth factors and industry development prospects 31

Allocation of EU funds under National Operational Programmes under 2014-2020 financial perspective

Source: Ministry of Infrastructure and Development

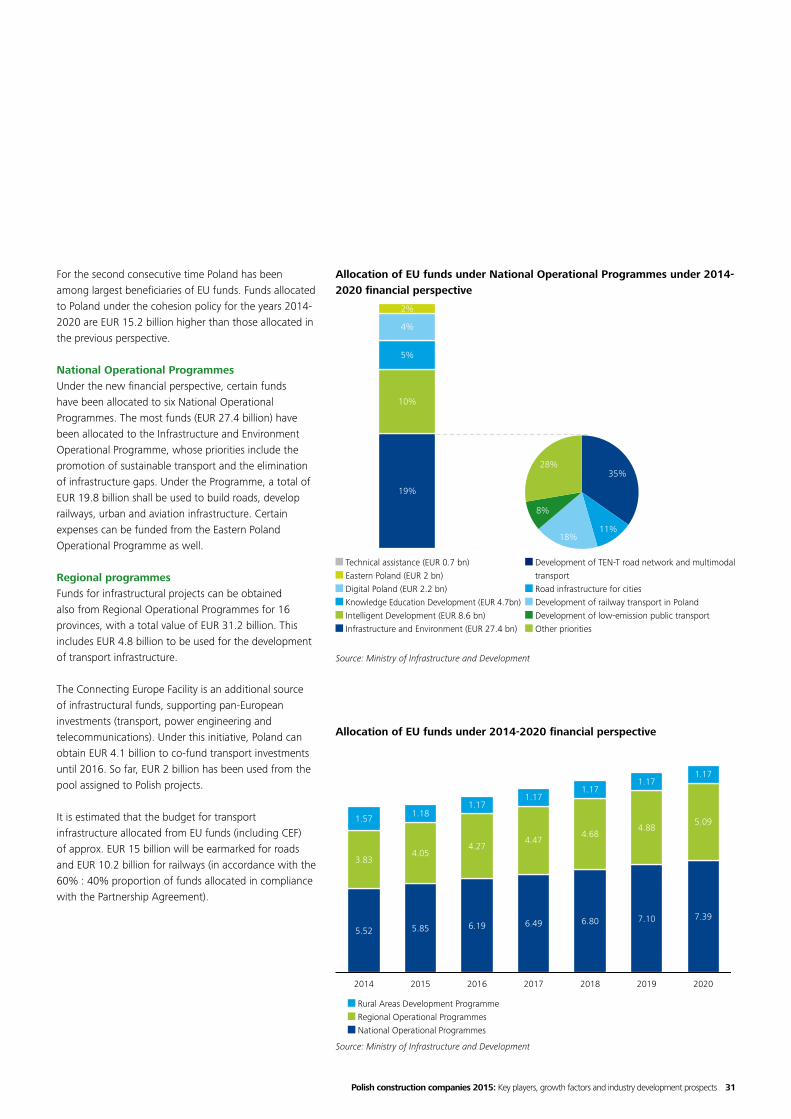

For the second consecutive time Poland has been among largest beneficiaries of EU funds. Funds allocated to Poland under the cohesion policy for the years 2014-2020 are EUR 15.2 billion higher than those allocated in the previous perspective.

National Operational ProgrammesUnder the new financial perspective, certain funds have been allocated to six National Operational Programmes. The most funds (EUR 27.4 billion) have been allocated to the Infrastructure and Environment Operational Programme, whose priorities include the promotion of sustainable transport and the elimination of infrastructure gaps. Under the Programme, a total of EUR 19.8 billion shall be used to build roads, develop railways, urban and aviation infrastructure. Certain expenses can be funded from the Eastern Poland Operational Programme as well.

Regional programmesFunds for infrastructural projects can be obtained also from Regional Operational Programmes for 16 provinces, with a total value of EUR 31.2 billion. This includes EUR 4.8 billion to be used for the development of transport infrastructure.

The Connecting Europe Facility is an additional source of infrastructural funds, supporting pan-European investments (transport, power engineering and telecommunications). Under this initiative, Poland can obtain EUR 4.1 billion to co-fund transport investments until 2016. So far, EUR 2 billion has been used from the pool assigned to Polish projects.

It is estimated that the budget for transport infrastructure allocated from EU funds (including CEF) of approx. EUR 15 billion will be earmarked for roads and EUR 10.2 billion for railways (in accordance with the 60% : 40% proportion of funds allocated in compliance with the Partnership Agreement).

Allocation of EU funds under 2014-2020 financial perspective

19%

10%

5%

4%

2%

35%

11%18%

8%

28%

5.52 5.85 6.19 6.49 6.80 7.10 7.39

3.834.05

4.274.47

4.684.88

5.091.57 1.181.17

1.171.17

1.171.17

2014 2015 2016 2017 2018 2019 2020

Market suffers from the shortage of talents, in particular with regard to railways, electrics, telecoms, utilities or hydro engineering specialists. Qualified production staff is also in high demand. Firms in need of new hires must remember that the Polish labour market has been turning into employee’s market and adjust their HR policies accordingly, bearing in mind not only the need to hire, but also to retain these talents.

Krzysztof Andrulewicz, CEO of Skanska S.A.

32

Number of bankruptcies among contractors in the construction sector in the period from 2011 to Q1 2015

Source: Euler Hermes

Share of construction firm bankruptcies in the number of all announcements

2.3. Bankruptcies in the construction sectorStatistics regarding bankruptcies are a good reflection of the current market condition.2 In the first half of 2015, the balance of bankruptcies decreased by one-third year-on-year and the share of the sector in the total number of bankruptcies dropped by 6 p.p. to 17%.

According to data derived from Euler Hermes reports, in the years 2012-2014, the number of bankruptcies announced for construction contractors decreased every year. During this period, the accumulated annual drop ratio reached 17.9%. The overall condition has improved, but the number of bankruptcies of construction companies compared to other industries was still high in 2014 and accounted for 22.4% of all bankruptcies announced.

Low margins in the construction and assembly sector are still a problem for construction firms. The reasons include pricing competition during tenders, where price is often the key selection criterion. According to the Main Statistical Office, in the years 2012-2014 the combined price decrease index in the sector amounted to 3.0%. Despite the index dropping again in 2014, the number of bankruptcies did not increase, which may be explained by the fact that due to a high number of bankruptcies in the previous year3 only the strongest market players, less sensitive to changes in raw material costs, are still in business.

2 Please note that they do not present the full scale of enterprises facing difficulties. Bankruptcy data does not include liquidated and suspended businesses, which in certain cases results in actual windup.

3 Since 2012, a wave of bankruptcies has gone through the sector. The organisation of the EURO 2012 tournament in Poland resulted in the significant development of infrastructure at the expense of the performance of many construction companies who participated in these investments due to very strong competition and the subsequent “pricing war” that caused a significant reduction of prices in the related tenders. Additionally, the commenced infrastructural projects made the prices of key materials increase, which affected the performance of construction companies. Consequently, in 2012 the number of bankruptcies in the construction industry increased the most in the last decade (according to a report by Arcata Partners). Large companies, such as PBG, Hydrobudowa Polska or DSS, were declared bankrupt, and so were hundreds of their subcontractors. Since then, a reduction in the sales of construction companies declaring bankruptcy has been observed, which confirms that the deterioration in the overall standing has been a problem mostly for subcontractors, not for general contractors, as in 2012.

146

273253

184

9866

0

50

100

150

200

250

300

2011 2012 2013 2014 1H2014 1H2015

17.9%

29% 27% 22% 23% 17%20%

Average gross pay (PLN) Average employment in the year (‘000)

The effect of road construction investment accumulation may occur in 2017-2019 when the majority of funds under the new National Road Construction Programme for 2014-2023 will be spent. This may result in an increase in subcontractor’s costs. A possible increase in material prices poses another risk.

Marcin Węgłowski, Management Board Member, Head of Economic and Finance Function, Budimex S.A.

Polish construction companies 2015: Key players, growth factors and industry development prospects 33

Price index in the construction and assembly-related production sector (previous year = 100)

Source: Main Statistical Office

Average employment and gross remuneration in the construction industry from 2008 to Q1 2015

Source: Main Statistical Office

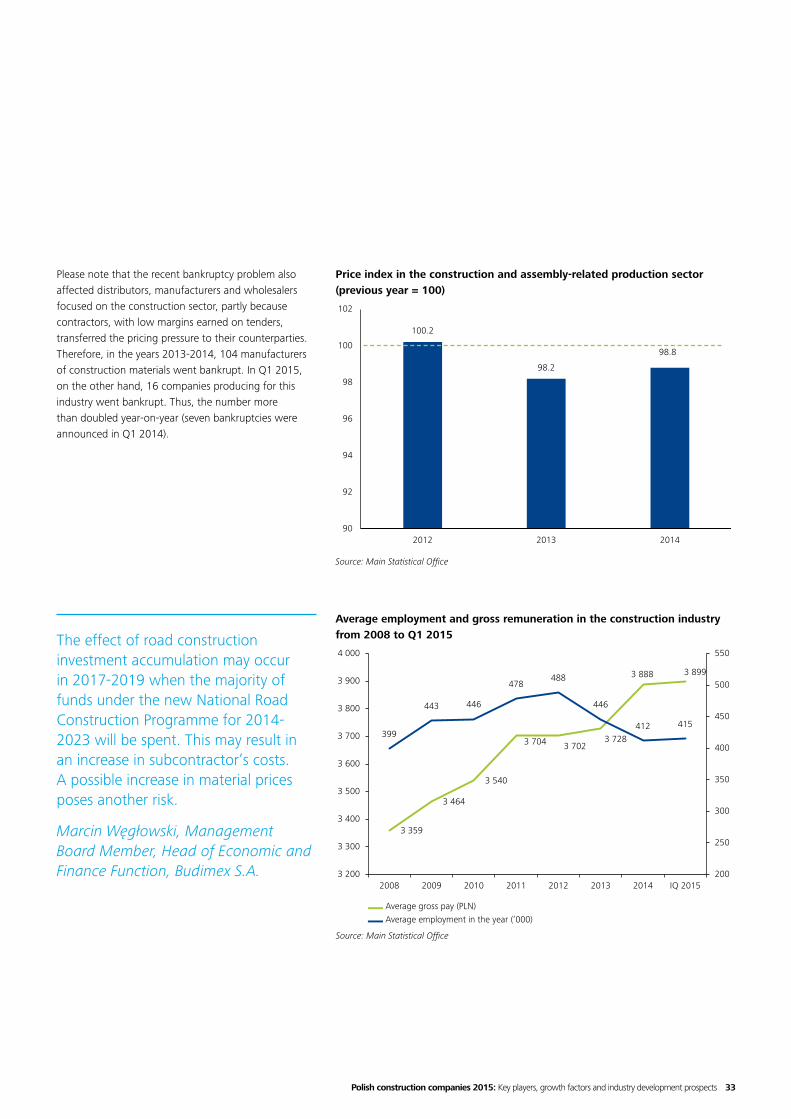

Please note that the recent bankruptcy problem also affected distributors, manufacturers and wholesalers focused on the construction sector, partly because contractors, with low margins earned on tenders, transferred the pricing pressure to their counterparties. Therefore, in the years 2013-2014, 104 manufacturers of construction materials went bankrupt. In Q1 2015, on the other hand, 16 companies producing for this industry went bankrupt. Thus, the number more than doubled year-on-year (seven bankruptcies were announced in Q1 2014).

100.2

98.2

98.8

90

92

94

96

98

100

102

2012 2013 2014

3 359

3 464

3 540

3 704 3 7023 728

3 888 3 899

399

443 446

478488

446

412 415

200

250

300

350

400

450

500

550

3 200

3 300

3 400

3 500

3 600

3 700

3 800

3 900

4 000

2008 2009 2010 2011 2012 2013 2014 IQ 2015

Average pay per segment Average pay in the construction sector

In the years to come, a continued stable increase of the housing market is expected since the number of flats per 1,000 inhabitants ratio is still low compared to other EU countries and the existing housing resources are of low quality due to a high share of flats in so-called “concrete panel” buildings.

Marcin Węgłowski, Management Board Member, Head of Economic and Finance Function, Budimex S.A.

34

2.4. Employment in the construction sector In 2014, the average employment in the construction sector decreased by 7.7% year-to-year and amounted to 411,500 people. Therefore, the decreasing trend observed since 2012 was still visible. Since January 2015, the negative trend has slowed down. According to data published by the Main Statistical Office, the average employment in Q1 2015 increased by 1.5% year-on-year, and remains low.

In Q1 2015, salaries and wages in the construction sector increased by 5.2% year-on-year.4

The highest average pay level in the construction sector regarded civil and water engineering services, while the lowest occurred in construction of buildings.

4 Please note that due to the seasonal nature of its operations, wages and salaries in the construction sector are usually the lowest in Q1.

Average gross pay in Q1 2015 per construction industry segment

Source: Main Statistical Office

3 617

4 170

3 949

3 899

3 300

3 400

3 500

3 600

3 700

3 800

3 900

4 000

4 100

4 200

4 300

Constructionof buildings

Works related to constructionof civil and water engineering

structures

Specialised construction works

AUG 2013

AUG 2014

AUG 2015

Labour shortage is a hindrance for companies operating in the construction market. As a result, recruitment has focused on immigrants from the East, who, among other things, require additional training with regard to safety standards.

Joanna Makowiecka - Gaca, Chairman of the Management Board, Polimex-Mostostal S.A.

Polish construction companies 2015: Key players, growth factors and industry development prospects 35

Hindrances faced by enterprisesAccording to a survey carried out by the Main Statistical Office among construction companies, since the beginning of 2013, the shortage of qualified staff has been a growing problem. In July 2015, 22% of enterprises considered it a hindrance in their business operation. This fact is confirmed by a report published by pracuj.pl, according to which the number of job offers in this sector, in particular for specialists, has grown substantially. Please note that 62% of employers in the construction sector indicate labour costs as a hindrance in their business operations. This is the largest financial burden for companies in this sector.

Employment projectionsThe newest report entitled Barometr Manpower Perspektyw Zatrudnienia presents employment in the Polish economy projected for Q4 2015. Information presented in the report is based on individual interviews with a selected group of Polish employers and indicate the presence of positive sentiments in the construction sector. The year-on-year employment growth projected for Q4 2015 is 11%. Due to a significant number of projects to be performed in the next six or seven years thanks to availability of EU subsidies under the 2014-2020 financial perspective, an employment growth in the infrastructural construction sector may be expected in a longer time horizon. According to projections by Hays, the increase will focus on the road infrastructure segment with the average employment ratio in the railway infrastructure segment remaining flat. Demand for specialists in heavy construction and power engineering will increase as well.

0%

10%

20%

30%

40%

50%

60%

70%

Employment costs Insufficient demand Costs of materials Shortageof qualified staff

Specialised construction works

Construction of civil and water engineering structures

Construction of buildings

Specialised construction works

Construction of civil and water engineering structures

Construction of buildings

33.5% 33.8%

26.0% 25.8%

40.6% 40.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013 2014

36

Structure of the construction market in Poland in 2014

Source: Main Statistical Office

Polish construction market value by segment in 2010-2014 (PLN bn)

* CAGR - Compound Annual Growth Rate in a given period

Source: Main Statistical Office

2.5. Development outlook for construction segments in Poland

2.5.1. General description and outlookIn 2014 specialist construction services accounted for 40% of the construction market value, construction of buildings – 34% and civil and water engineering services making up the remaining 26%)5. The share of construction of buildings increased slightly year-on-year at the expense of the other segments.

In 2014, following a two-year recession, a symbolic growth of 0.4% in the construction market value occurred, compared to 2013.6 In light of higher economic growth projected for the coming years compared to the period 2012-2013 and planned infrastructural investments, the increase in the value of the construction market should accelerate.

The drop in construction related production in the years 2011-2014 resulted from a number of factors: GDP decrease from 4.8% in 2011 to 1.8% in 2012-2013, the completion of infrastructural investments prepared for EURO 2012, reduced trust and outflow of investors from the real property segment and a general decrease in investments made in other sectors of economy. The significant deterioration observed from 2011 was reflected by the WIG Budownictwo index, which has demonstrated a growing trend since the beginning of 2015.

5 The construction of civil and water engineering structures includes road and railway construction, as well as environmental and energy investment projects (pipelines, telecommunication lines, power lines, etc.). The construction of buildings comprises the construction of residential, office, commercial, industrial and warehouse buildings and structures. The specialist construction consists of demolition work, site preparation, electrical installations, water and sewage systems, painting and finishing.

6 Following the intense growth before 2011, the value of the construction market in Poland amounted to PLN 182.2 billion (+13.2% vs. 2010). During the two subsequent years, a significant decrease in construction-related production was observed in Poland (by 6.3% in 2012 and by 7.4% in 2013 year-on-year).

71.8 64.2 63.1 52.9 53.7

37.7 48.9 47.0

41.0 40.9

51.469.1

60.6

64.1 64.1

2010 2011 2012 2013 2014

CAGR*-4.5%

WIG Budownictwo WIG 20

Investments in expressways and motorways included in the National Roads Construction Programme for the years 2014-2023 (with projections until 2025)

Diversification, which should support margin growth on the highly competitive Polish market, seems to be unavoidable.

Paulo Silva, Management Board Member, Mota-Engil Central Europe S.A.

Polish construction companies 2015: Key players, growth factors and industry development prospects 37

An accelerated market growth in the coming years will be possible thanks to the inflow of EU funds under the 2014-2020 perspective and the expected 3.15% annual average GDP growth between 2015-20187. The projected market acceleration has been confirmed by market analysts who predict the average annual growth of the entire construction market of 4.6%8, in the years 2015-2017, with differences in the growth level in each market segment. According to analysts, the increase in general construction segments in Poland shall reach 2.6% in 2015, while the construction engineering segment will grow by 6.7%.

2.5.2. Road constructionIn 2014, the road construction segment continued projects commenced under the 2007-2013 perspective. The planning of investments for the new 2014-2020 perspective has commenced.

In the previous years, the National Roads Programme for the years 2011-2015 was the key document determining the development directions of the road construction segment.

Only in 2014, 331.7 km of national roads were commissioned (four sections of motorways, six expressways and two ring roads). In 2014 the total cost to the National Roads Fund and State Treasury in this respect was almost PLN 9.6 billion. Investments co-funded by the EU under the 2014-2020 perspective shall be based on the National Roads Construction Programme for the years 2014-2023 (with projections until 2025) developed by the Ministry of Infrastructure and Development (henceforth: ”NRCP”) being a follow-up of the previous Programme.

7 According to projections of the Economist Intelligence Unit. 8 Based on the report “Construction Market in Poland 2015- 2019”

prepared by TechNavio.

WIG Budownictwo and WIG20 index in the period from 31 July 2008 to 18 September 2015

Source: National Roads Construction Programme for the years 2014-2023 (with projections until 2025)

Completed or pending investments New investments included in NRCP 2014-2023 New investments included in the funding system beyond the state budget

0

500

1000

1500

2000

2500

3000

3500

2014-12-30 2015-06-30

EU funds

National Road Fund

State budget

38

As in the preceding period, in 2014-2023, investments within the National Road Construction Programme will be financed from the National Road Fund, contributed to from a variety of sources9, including, among others, through EU funding. State budget funds will be used to maintain technical standards of the existing road network, prepare tasks to be performed in the future and carry out management roles. Expenditure on national roads to be incurred in 2014-2025 are estimated at PLN 168.4 billion, out of which PLN 14.5 billion shall be used to continue the tasks under the National Roads Construction Programme 2011-2015 and PLN 107.1 billion to finance investments under the 2014-2020 EU perspective. Out of this amount, PLN 97.5 billion shall be used to build motorways and expressways, and PLN 9.6 billion for ring roads. The list of tasks includes two motorway sections, 49 expressway sections and 57 ring road sections of trunk roads.

Following public consultation, the NRCP has been extended for two additional years (2024 and 2025) and the pool of the National Roads Fund assigned to tasks performed under the 2014-2020 perspective has been increased by PLN 14.4 billion10. The objective of the NRCP is to complete the target motor- and expressway network in Poland as defined in the Transport Development Strategy until 2020 (with projections until 2030)11. The completion of the task shall depend also on the value of savings on investment projects. The amount of the savings may be substantial, as confirmed by an analysis of tenders already closed under the new EU perspective. The average price of winning tenders in projects included in our analysis (the total value of which constitutes nearly 30% of the accepted tenders amounting to PLN 30 billion) constituted 70% of the investment value as estimated by the General Directorate for National Roads and Motorways.

9 Defined in the Act on toll roads and National Road Fund of 27 October 1994 (Journal of Laws of 2012 item 931 as amended).

10 Ministry of Finance and the Council of Ministers approved the increase of the investment pool.

11 Transport Development Strategy defines the target motor- and expressway network in accordance with the Ordinance of the Council of Ministers of 20 October 2009 amending the ordinance on the network of motor- and expressways.

Funding sources for railway infrastructure investments in 2014-2025 (PLN bn)

Source: National Roads Construction Programme for the years 2014 – 2023 (with projections until 2025)

Length ratio of expressways and motorways (km / 1,000 sq. km of national territory)

Source: General Directorate forNational Roads and Motorways, Eurostat, Deloitte analysis.

2.9 2.9 3.15.1 5.2 5.3 5.4 5.5 5.6 5.7

1.6

6.2

10.5

12.5 11.59.6

10.97.9

1.71.15.2

2.7

5.4

8.5 10.5

10.35.3

0.2

0.0

5.0

10.0

15.0

20.0

25.0

30.0

2014 2015 2016 2017 2018 2019 2020 2021 2022 years2023-25

9.7

36.2

32.8

20.8 20.5

15.7 15.1 14.5

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

PolandRepublic

Germany Spain France Austria CzechRepublic

UK Ireland

Investments under 2014-2020 EU perspective

Continued investments

Maintenance and management expenses (financed from the state budget)

Polish construction companies 2015: Key players, growth factors and industry development prospects 39

The network of trunk roads, accounting for 4.7% of the total length of public roads in Poland, supports over 60% of traffic. This confirms the necessity to carry out broad-scale investment projects concerning these roads especially that Poland lags behind other EU countries in terms of the density of its expressway and motorway network. For example, expressways and motorways account only for 9.7 km per 1000 sq. km of land in Poland compared with 36.2 km in Germany. The objective determined in the NRCP is to achieve the density ratio of 22.7 km / 1,000 sq. km.

The poor technical condition of roads, which deteriorated in 2014 despite significant investments, has remained a problem in Poland. At the end of 2014, 13.2% of the roads were considered ‘in poor condition’ (compared with 12.5% at the end of 2013) and 25.1% were deemed ‘unsatisfactory’ (compared with 21.4% in 2013).

According to the Report on the Technical Condition of Trunk Roads at the end of 2014 prepared by the General Directorate for National Roads and Motorways, the deterioration in the technical condition of these roads has resulted from the reduced length of road sections commissioned and refurbished in 2014 compared to 2012 and 2013 (mainly resulting from a reduction of funds assigned to the Directorate, unfavourable climate conditions and the growing number of trucks). The General Directorate for National Roads and Motorways (GDNRM) assumes that financial needs related to the improvement of roads assessed as in poor or unsatisfactory condition shall amount to PLN 6.6. billion in 2015.

Expenditure on trunk roads in the years 2014-2025 (PLN bn)

Source: National Roads Construction Programme for the years 2014 – 2023 (with projections until 2025)

Condition of surface of trunk roads per province (at the end of 2014)

Source: Report on the Technical Condition of Trunk Roads at the end of 2014, GDNRM

Performing most works with the use of own resources allows effective control of projects and keeping the deadlines.

Paulo Silva, Management Board Member, Mota-Engil Central Europe S.A.

2.9 2.9 3.15.1 5.2 5.3 5.4 5.5 5.6 5.7

6.13.8 3.1

1.2 0.3

0.65.2

12.8

19.8 21.620.0

16.2

8.11.7 1.1

0.0

5.0

10.0

15.0

20.0

25.0

30.0

2014 2015 2016 2017 2018 2019 2020 2021 2022 years2023-25

Good condition

Unsatisfactory condition

Poor condition

Legend

40

Network of provincial, municipal and county roadsApart from trunk roads (to include motor- and expressways), the Polish network of public roads includes also those maintained by local governments: provincial, county and municipal.

The Ministry of Infrastructure and Development supports the financing of investments in provincial, county and municipal roads under the general subsidy provision and the National Programme for Local Roads Redevelopment (henceforth: NPLRR) valid until the end of 201512.

In September 2015 the Council of Ministers passed the Programme for Development of Municipal and County Road Infrastructure for 2016-2020, being a follow-up of NPLRR. Subsidies available under the programme in the years 2016-2020 total to PLN 4 billion13. which will allow construction, redevelopment and renewal of approx. 2,200 km of county and municipal roads each year.

12 National Programme of Local Roads Redevelopment has been carried out since 2008 and expires at the end of 2015. In the period 2008-2014 local self-government entities carried out over 4,900 investments and renewals totalling to nearly PLN 9.3 billion under the programme. The amount of PLN 4.4 billion was assigned to these tasks from the state budget. The programme has resulted in improvement and extension of the local roads network with the total length of 12,200 km.

13 PLN 800 million, PLN 1 billion, PLN 1.1 billion and PLN 1.1 billion in subsequent years.

According to the Supreme Control Chamber (NIK), 25% of county and municipal roads are in poor condition, with a mere 29% being in good and satisfactory condition14. The poor condition of these roads and no funds earmarked for the co-financing of local road infrastructure investments15 under the new EU perspective require the provision of financial support from the state budget.

14 As in March 2014 including the effects of NPLRR implementation. 15 Investments in provincial roads may be funded under Regional

Operational Programmes.

Classes of public roads in Poland

Road class Length [km] Share [%] Managing body* Owner

Trunk roads 19 296 4,7% GDNRM State Treasury

Provincial roads 28 480 6,8% Province authorities Provincial self-government

County roads 125 274 30,1% County authorities County self-government

Municipal roads 242 923 58,4% Mayor Municipal self-government

Total 415 973 100% - -

*In the territory of cities classified as counties, the city president is the managing body of all public roads except of motor- and expressways.

Source: National Roads Construction Programme for the years 2014-2023 (with projections until 2025), Deloitte analysis

The legal system discouraging investments, all the way from the public procurement law to the local zoning plans, hinders the development of the railway market in Poland. Additionally, the price remains the key criterion in tenders and risks are not equally distributed between contract parties.

Jarosław Tomaszewski, Chairman of the Management Board, TRAKCJA PRKiI S.A.

Performance

Estimates