positioning palm oil in vietnam market pots vietnam 1 … · -including pure sesame oil, peanut...

TRANSCRIPT

POSITIONING PALM OIL IN VIETNAM MARKET POTS VIETNAM

1 JULY 2013

2

CONTENT 1. GREAT POTENTIAL 2.TRENDS 3. PREFRRED VEGETABLE OIL 4. ORIGINS OF SUPPLY 5. LOCAL MARKET OVERVIEW 6. CHALLENGES 7. RECOMENDATION

3

With a population of 90 million, Vietnam is currently the 13th most populated country in the world and also the 13th largest importer of palm oil.

The country economy has grown rapidly within 10 years period 2001 – 2010, GDP increased by 7.2% per year on average; and still growing healthy at 6.5% and 5.0% during difficult period from 2011 - 2012.

Per capita GDP in 2012 is USD 1540/month, which is three times as much as 2002, and the Government has projected to increase this to USD 2500 in 2015 and subsequently around USD 4200 by 2020.

0 1 2 3 4 5 6 7 8 9

2007 2008 2009 2010 2011 2012 2013

GDP

GDP

%

0 500

1000 1500 2000 2500 3000 3500 4000 4500

2002 2004 2006 2008 2010 2012 2015 2020

Av GDP Per capita

USD

USD

1. GREAT MARKET POTENTIAL

4

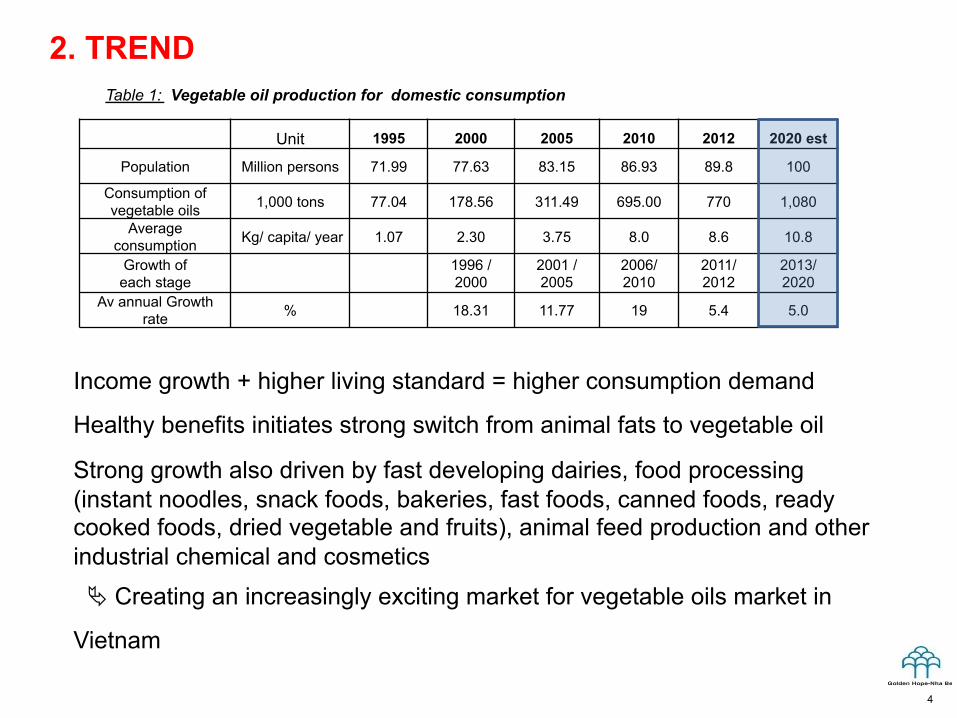

Income growth + higher living standard = higher consumption demand

Healthy benefits initiates strong switch from animal fats to vegetable oil

Strong growth also driven by fast developing dairies, food processing (instant noodles, snack foods, bakeries, fast foods, canned foods, ready cooked foods, dried vegetable and fruits), animal feed production and other industrial chemical and cosmetics

Ä Creating an increasingly exciting market for vegetable oils market in

Vietnam

2. TREND Table 1: Vegetable oil production for domestic consumption

Unit 1995 2000 2005 2010 2012 2020 est

Population Million persons 71.99 77.63 83.15 86.93 89.8 100

Consumption of vegetable oils 1,000 tons 77.04 178.56 311.49 695.00 770 1,080

Average consumption Kg/ capita/ year 1.07 2.30 3.75 8.0 8.6 10.8

Growth of each stage

1996 / 2000

2001 / 2005

2006/ 2010

2011/ 2012

2013/ 2020

Av annual Growth rate % 18.31 11.77 19 5.4 5.0

5

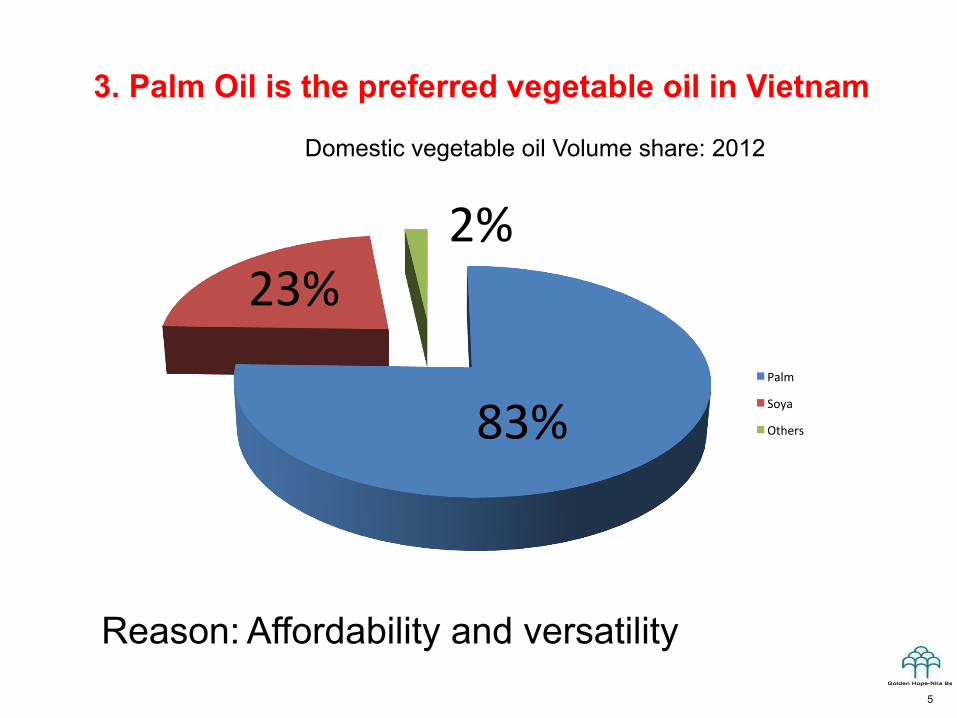

3. Palm Oil is the preferred vegetable oil in Vietnam

Palm

Soya

Others 83%

23% 2%

Reason: Affordability and versatility

Domestic vegetable oil Volume share: 2012

4. Origins of supply 100% of Palm Oil and Plam oil Products are imported Major import is from Malaysia (75%), followed by Indonesia (25%)

6

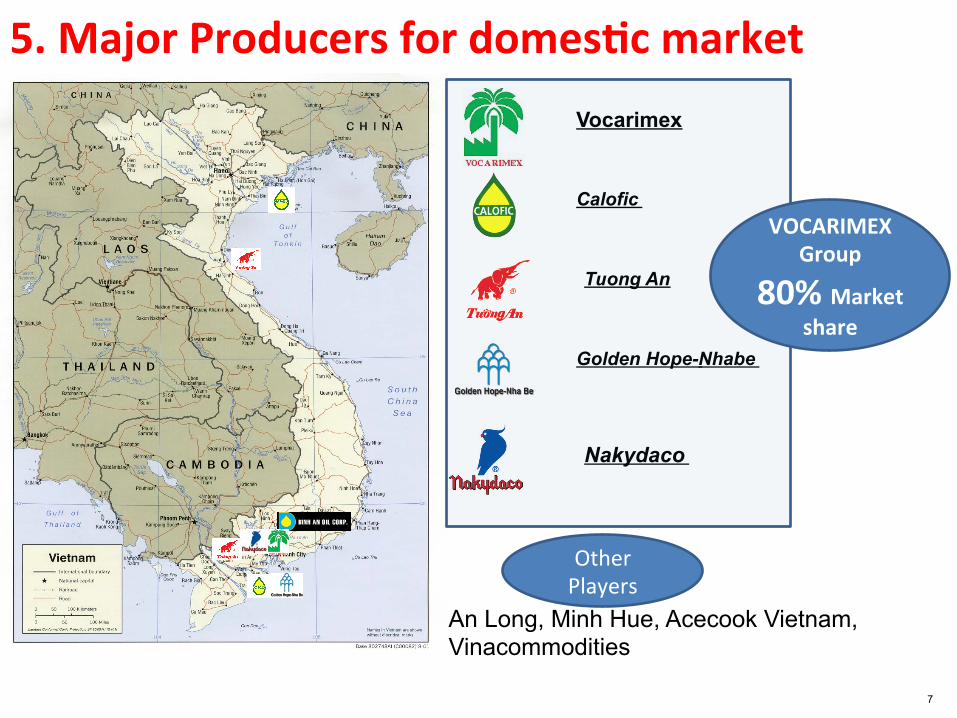

5. Major Producers for domes8c market

Calofic

Golden Hope-Nhabe

Tuong An

Nakydaco

Vocarimex

An Long, Minh Hue, Acecook Vietnam, Vinacommodities

VOCARIMEX Group

80% Market share

Other Players

7

8

Vegetable oil products in Vietnam comes in PET bottles, jerry can, BIB, in various pack sizes to suite food safety regulations and consumer demand

9

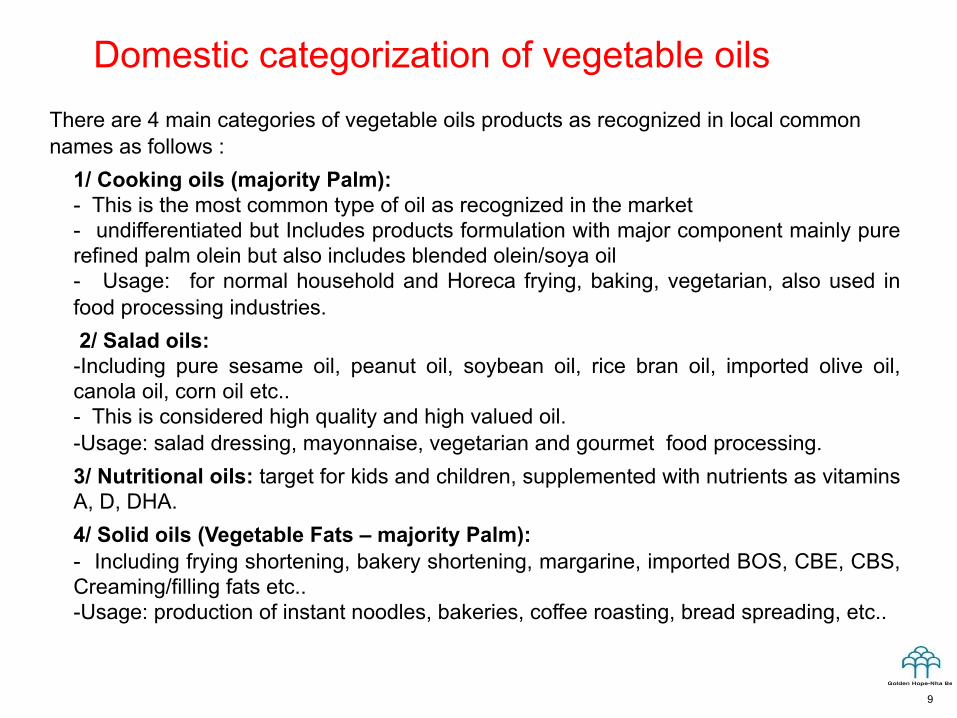

Domestic categorization of vegetable oils

There are 4 main categories of vegetable oils products as recognized in local common names as follows :

1/ Cooking oils (majority Palm): - This is the most common type of oil as recognized in the market - undifferentiated but Includes products formulation with major component mainly pure refined palm olein but also includes blended olein/soya oil - Usage: for normal household and Horeca frying, baking, vegetarian, also used in food processing industries. 2/ Salad oils: - Including pure sesame oil, peanut oil, soybean oil, rice bran oil, imported olive oil, canola oil, corn oil etc.. - This is considered high quality and high valued oil. - Usage: salad dressing, mayonnaise, vegetarian and gourmet food processing. 3/ Nutritional oils: target for kids and children, supplemented with nutrients as vitamins A, D, DHA. 4/ Solid oils (Vegetable Fats – majority Palm): - Including frying shortening, bakery shortening, margarine, imported BOS, CBE, CBS, Creaming/filling fats etc.. - Usage: production of instant noodles, bakeries, coffee roasting, bread spreading, etc..

10

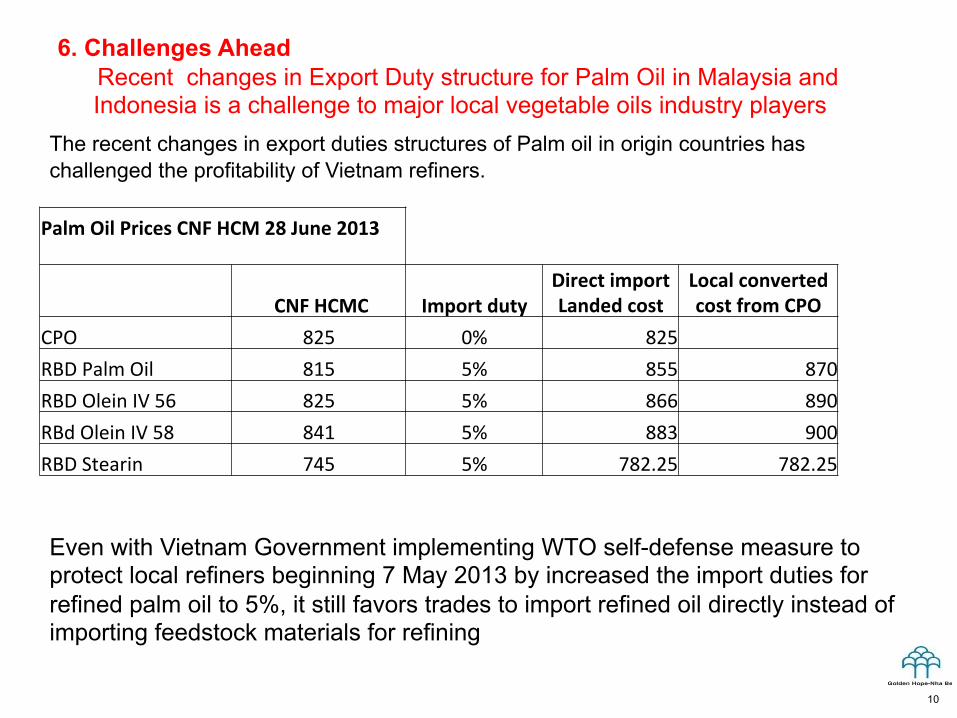

6. Challenges Ahead Recent changes in Export Duty structure for Palm Oil in Malaysia and

Indonesia is a challenge to major local vegetable oils industry players

The recent changes in export duties structures of Palm oil in origin countries has challenged the profitability of Vietnam refiners. Palm Oil Prices CNF HCM 28 June 2013

CNF HCMC Import duty Direct import Landed cost

Local converted cost from CPO

CPO 825 0% 825 RBD Palm Oil 815 5% 855 870 RBD Olein IV 56 825 5% 866 890 RBd Olein IV 58 841 5% 883 900 RBD Stearin 745 5% 782.25 782.25

Even with Vietnam Government implementing WTO self-defense measure to protect local refiners beginning 7 May 2013 by increased the import duties for refined palm oil to 5%, it still favors trades to import refined oil directly instead of importing feedstock materials for refining

11

Challenges to local Palm Oil refining Industries

• Low profitability discourage further investment and development in vegetable oil industries in general.

• There will be further implication to greater social economic consequences such as employment, supporting industries and trades etc.

• Current duties structures favors trades to import, sell and directly consume commodity grades refined oil in Vietnam. This may be risky to consumer heath in term of food safety control.

12

7. RECOMMENDATION FOR CONSIDEARTION TO PROMOTE MALYSIAN PALM OIL TO VIETNAM

TO MPOC Malaysia may give special consideration to provide export duty exemption for CPO export to Vietnam refiners

TO VIETNAM AUTHORITIES From the local refiners point of view, we may want to propose to the Government to extend and/or further increase the self-defense duties rates for refined oils. We may also want to propose to the Government to impose more technical barriers and food safety control for direct consumption of commodity grades refined oils.

The key factor to promote growth of Malaysian Palm Oil usage in Vietnam is that the refiners interests need to be taken care of.

Thank You

The above presentation represent only personal view of the speaker