potash ridge april 2016

TRANSCRIPT

April2016

InvestorPresenta4on

Potash Ridge is a near term producer

of premium fertilizer with world class

development assets in Utah and

Quebec.

The Company is uniquely positioned to

take advantage of strong markets for

Sulphate of Potash

2

HIGHLIGHTS

3

SulphateofPotash(“SOP”)isapremium

potashwithasignificantsupplydeficit

§ Domes&csellingprice3xversusregularpotash(“MOP”)§ Globalconsump&onis~5milliontonnesperyear(“tpy”)§ Demandpoten&alis10milliontpy§ Exis&ngproducersunabletoexpandtomeetsupplydeficit

Strategy§ BecomethefirstSOPproducerusingMannheimprocessin

NorthAmericaand,longerterm,thelargestNorthAmericanSOPproducer

Valleyfield(Quebec)

§ 40,000tpyofSOP;CDN$48.8millioncapex§ 32.5%aUertaxIRR§ ProvenprocessusedthroughoutEuropeandAsia§ Produc&onscheduledtocommenceinQ42017§ Strategicloca&onnearby-producthydrochloricaciddemand§ Expansionpoten&alatsite§ Poten&alforover$13minaverageannualcashflows(Y1-Y5)

BlawnMountain(Utah)

§ Upto585,000tpyofSOP;poten&altophase-inproduc&ontoreducefrontendcapex

§ Prefeasibilitycomplete:20.5%aUertaxIRR§ Largesurfacemineraldeposit;over40-yearreservelife§ Majorpermitsandwaterrightssecured;infrastructurenearby§ Poten&alupsidefromaluminaresidueintailings§ Poten&alforoverUS$250Minaverageannualcashflow

SOP:SUPERIORPRODUCTWITHATTRACTIVEMARKET

4

SOP(K2SO4) MOP(KCI)

US$887/tonneinNorthAmerica US$238/tonneinNorthAmerica

Globalmarket5milliontpy,withpoten&almarketdemandof10milliontonnes(1)

Globalmarket55milliontpy

Fundamentalsupplydeficit–limitedabilitytosignificantlygrowproduc&onusingexis&ngproduc&onprocesses

Marketisinoversupply,withidlecapacityandmul&pleprojectsinpipeline

Lowchloride,highsulphur–providingbenefitstocropsnotavailablewithMOP

Containschloride–nonutrientvalue;inmanyinstancesdetrimentaltoplants

Improvesyield,taste,appearanceandshelflife;idealforsaltyorsandysoilsoraridclimates

Chloridecanleachintogroundwaterorbuild-upinaridsoilcondi&ons,impac&ngyieldsandcropquality

SignificantbenefitsoverMOPforfruits,vegetables,nuts,potatoes,tobacco–manyotherhighvaluecrops

Primarilyforcornandgraincropsthatcanwithstandchloride

(1)PerCRU

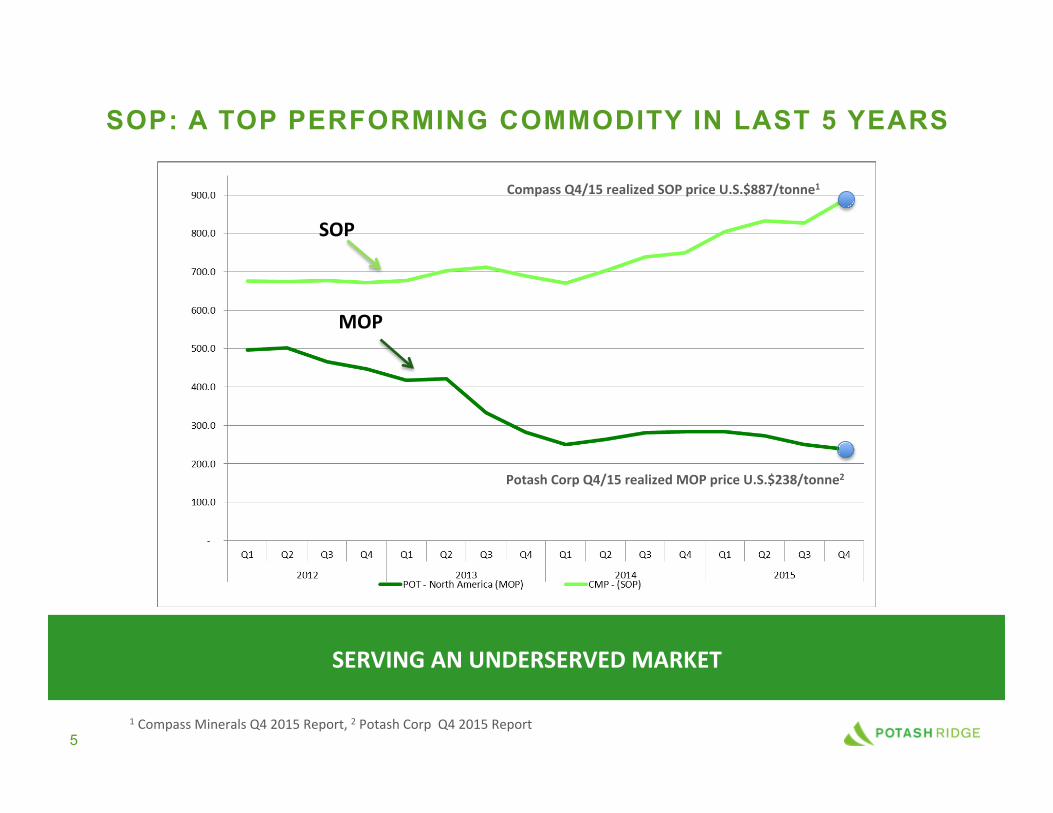

SOP: A TOP PERFORMING COMMODITY IN LAST 5 YEARS

5 1CompassMineralsQ42015Report,2PotashCorpQ42015Report

SERVINGANUNDERSERVEDMARKET

CompassQ4/15realizedSOPpriceU.S.$887/tonne1

PotashCorpQ4/15realizedMOPpriceU.S.$238/tonne2

SOP

MOP

DEVELOPMENTSTRATEGY

6

Valleyfield(Quebec) BlawnMountain(Utah)

Bringini&al40,000tpySOPintoproduc&oninQ42017

Poten&alforupto585,000tpySOPproduc&onEvaluatescalingdevelopment,withtargetedini&alproduc&oninlate2019

Completepermihngandbreakgroundin2016

CompletescalingstudyinQ3,2016

FinalizeSOPokakeandothercommercialarrangements

Leveragemanagementteams’strongprojectdevelopmentandfinancingexper&se

DevelopEPCorsimilarconstruc&onarrangementstominimizeexecu&onrisk

7

VALLEYFIELDPROJECT

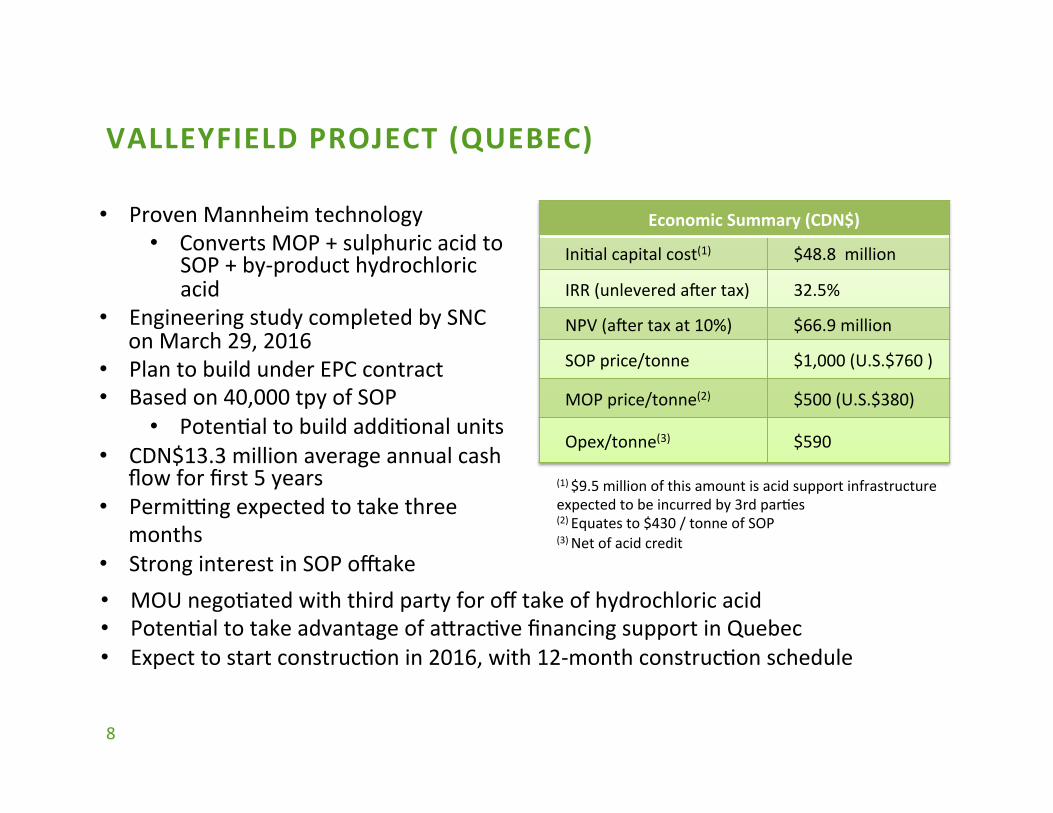

VALLEYFIELDPROJECT(QUEBEC)

8

• ProvenMannheimtechnology• ConvertsMOP+sulphuricacidto

SOP+by-producthydrochloricacid

• EngineeringstudycompletedbySNConMarch29,2016

• PlantobuildunderEPCcontract• Basedon40,000tpyofSOP

• Poten&altobuildaddi&onalunits• CDN$13.3millionaverageannualcash

flowforfirst5years• Permihngexpectedtotakethree

months• StronginterestinSOPokake

EconomicSummary(CDN$)

Ini&alcapitalcost(1) $48.8million

IRR(unleveredaUertax)

32.5%

NPV(aUertaxat10%) $66.9million

SOPprice/tonne $1,000(U.S.$760)

MOPprice/tonne(2) $500(U.S.$380)

Opex/tonne(3) $590

(1)$9.5millionofthisamountisacidsupportinfrastructureexpectedtobeincurredby3rdpar&es(2)Equatesto$430/tonneofSOP(3)Netofacidcredit

• MOUnego&atedwiththirdpartyforofftakeofhydrochloricacid• Poten&altotakeadvantageofaprac&vefinancingsupportinQuebec• Expecttostartconstruc&onin2016,with12-monthconstruc&onschedule

VALLEYFIELD:STRATEGICALLYLOCATED

• LocatednearMontreal,Quebec

• Propertysecured• Stronglocalsupport• Railaccessatsite• Portwithin2km,allowing

accessintokeyU.S.markets• Within2kmofsulphuric

acidsupplier–discussionsini&atedwithsuppliers

9

• Locatednearhydrochloricacidcustomers• MOUsignedforokakeofini&alproduc&on• Discussionsunderwayforsecondphaseofhydrochloricacidokake

PROVENMANNHEIMPROCESS

10

MannheimFurnace

PotassiumSulphate(“SOP”)

HydrochloricAcid(“HCL”)

PotassiumChloride(“MOP”)

SulphuricAcid

Energy

• ConvertsMOPtoSOP• Provenproduc&onprocess(over100yearhistory),withnumerousopera&ng

facili&esinEuropeandChina(about40%ofcurrentSOPproduc&onisfromMannheim)

• Highquality,consistentproduc&onprocess• Scaleallowsforconstruc&on&meof12-months

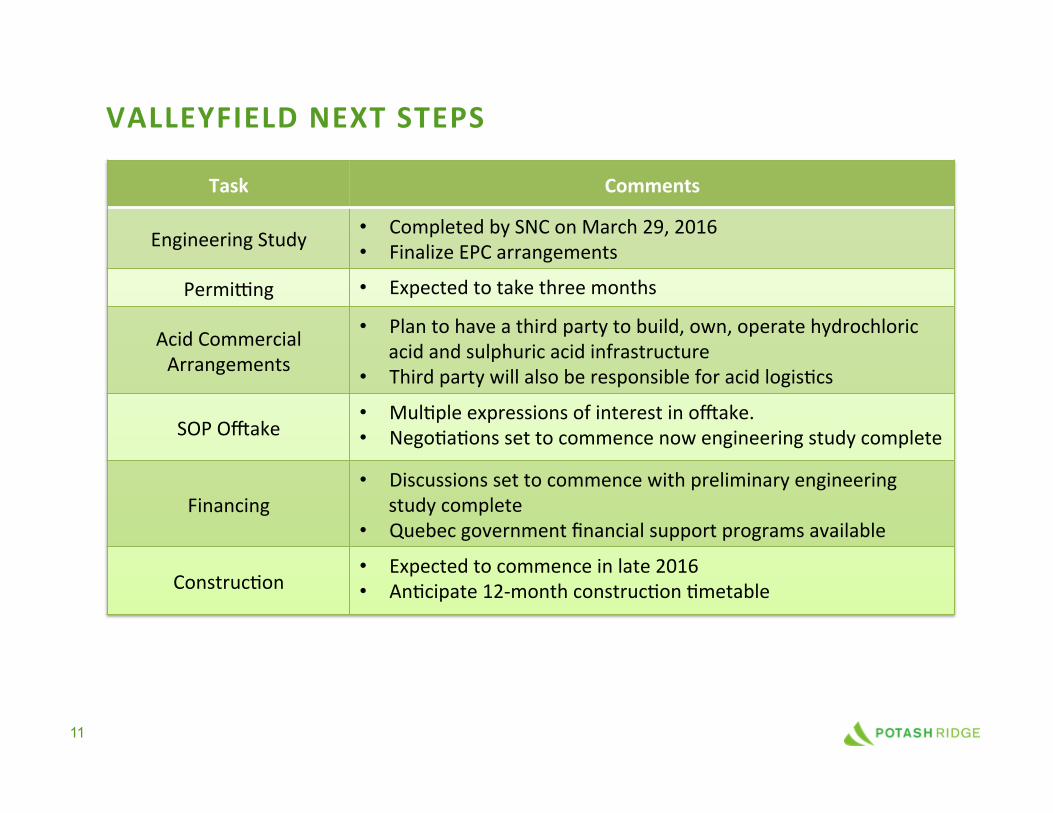

VALLEYFIELDNEXTSTEPS

11

Task Comments

EngineeringStudy • CompletedbySNConMarch29,2016• FinalizeEPCarrangements

Permihng • Expectedtotakethreemonths

AcidCommercialArrangements

• Plantohaveathirdpartytobuild,own,operatehydrochloricacidandsulphuricacidinfrastructure

• Thirdpartywillalsoberesponsibleforacidlogis&cs

SOPOkake• Mul&pleexpressionsofinterestinokake.• Nego&a&onssettocommencenowengineeringstudycomplete

Financing• Discussionssettocommencewithpreliminaryengineering

studycomplete• Quebecgovernmentfinancialsupportprogramsavailable

Construc&on• Expectedtocommenceinlate2016• An&cipate12-monthconstruc&on&metable

BLAWNMOUNTAINPROJECT

12

BLAWNMOUNTAINPROJECT(UTAH)

• Surfaceminingwithadjacentprocessingfacility

• KnownprocesstoconvertaluniteoreintoSOP,by-productsulphuricacidandanalumina-richmaterial

• PrefeasibilityStudycompletedbyNorwestinDecember2013

• P+Preservessupport40yearminelife,• Poten&altoincreaselifeof

opera&onsthroughaddi&onalexplora&on

• Projectpermiped;waterrightssecured

13

PFSEconomicSummary(US$)

Ini&alcapitalcost

$1,124million

IRR(unleveredaUertax)

20.5%

NPV(aUertax,at10%) $1.0billion

SOPprice/ton $649

Opex/ton(1) $173

(1)Netofacidcreditandexcludingroyal&es.

• MOUnego&atedwiththirdpartyforokakeofsulphuricacid• Currentlyassessingthepoten&altophaseproject(withphase1poten&allyaround200,000

tpy)tosignificantlyreduceupfrontcapex• Poten&altofasttracknextstageofdevelopment

UTAH–ANATTRACTIVEPLACEFORMINING

14

• Majorresourceproducingstate• Over100yearsofpotashproduc&on• Beststateforbusinessandtopquar&leminingjurisdic&on(1)• 100%state-ownedland• Strongstategovernmentandlocalsupport• Allnecessaryinfrastructurenearby

(1)ForbesMagazine,2015RankingandFraserIns&tute,April,2013

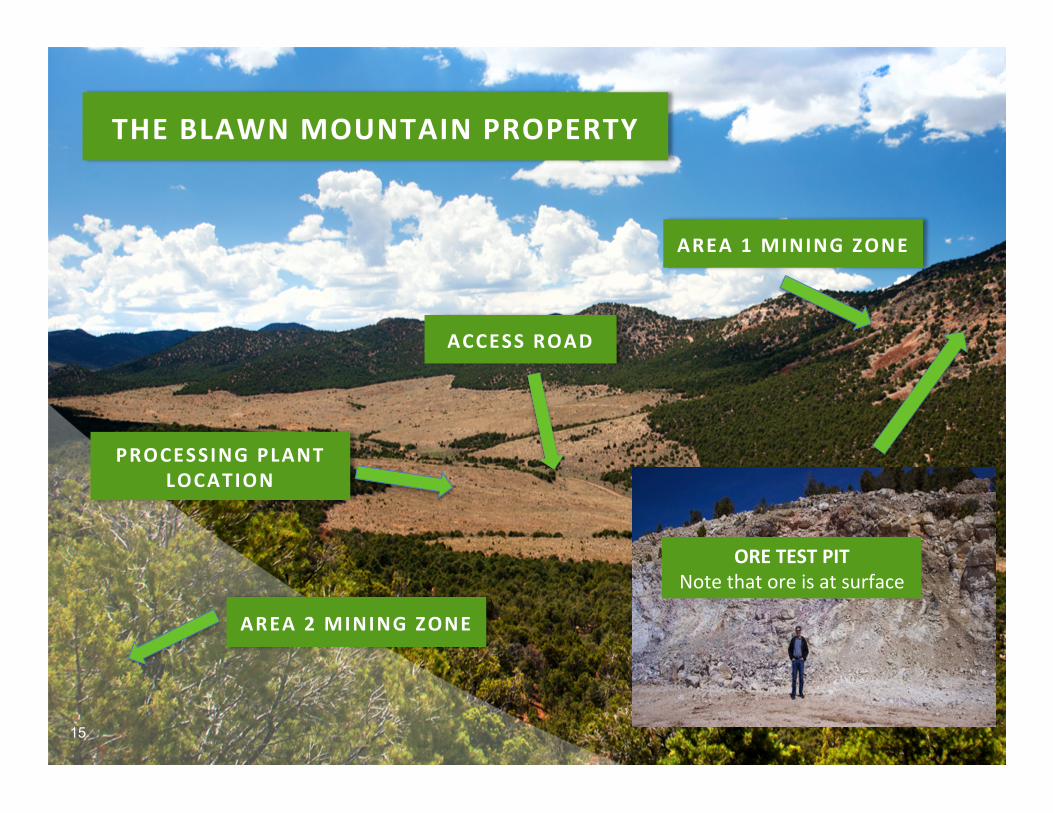

THEBLAWNMOUNTAINPROPERTY

15

AREA1MININGZONE

PROCESSINGPLANTLOCATION

AREA2MININGZONE

ACCESSROAD

ORETESTPITNotethatoreisatsurface

RESERVESANDMINELIFE

Drillingworktodatehasestablished40yearsofreserves–calculatedbyindependentengineer(Norwest)

Drillingtodatehasfocusedonlyontwoofthefourareaswithinthe15,400acrelandposi&on

16

ReserveCategory

TotalProven

('000tons)Probable('000tons)

AluniteOre(ROMtons) 136,254 289,540 425,794

Ore(averageK2O(%)grade) 3.56 3.49 3.51

Ore(averageK2SO4(%)grade) 6.59 6.46 6.49

SOP(tons) 8,457 17,970 26,427

SulphuricAcid(tons)@98%Purity 18,888 40,136 59,024

MineralReservesbyCategoryNovember6,2013

DRILLED

NOTYET DRILLED

17

PERMITTINGESSENTIALLYCOMPLETED

Thefollowingtableiden&fiesthemajorpermitsandapprovalsthattheCorpora&onhasors&llneedstoobtainpriortoconstruc&on:

Permit/Approval IssuingAgency Completed

Explora&onPermit UtahDivisionofOil,GasandMining October,2011

USArmyCorpsofEngineersJurisdic&onalWatersConcurrence USArmyCorpsofEngineers March,2014

GroundwaterPermits UtahDivisionofWaterQuality July,2014

LargeMineOpera&onApproval UtahDivisionofOil,GasandMining August,2014

AirQualityEmissionStandard UtahDivisionofAirQuality

AirQualityEmissionStandardrequirestheengineeringtobepar&allycompletedbeforetheapplica&onisfiled.Itistechnicallynotapermit,butmoreanagreeduponemissiontargetthattheProjectmustbedesignedtomeet.

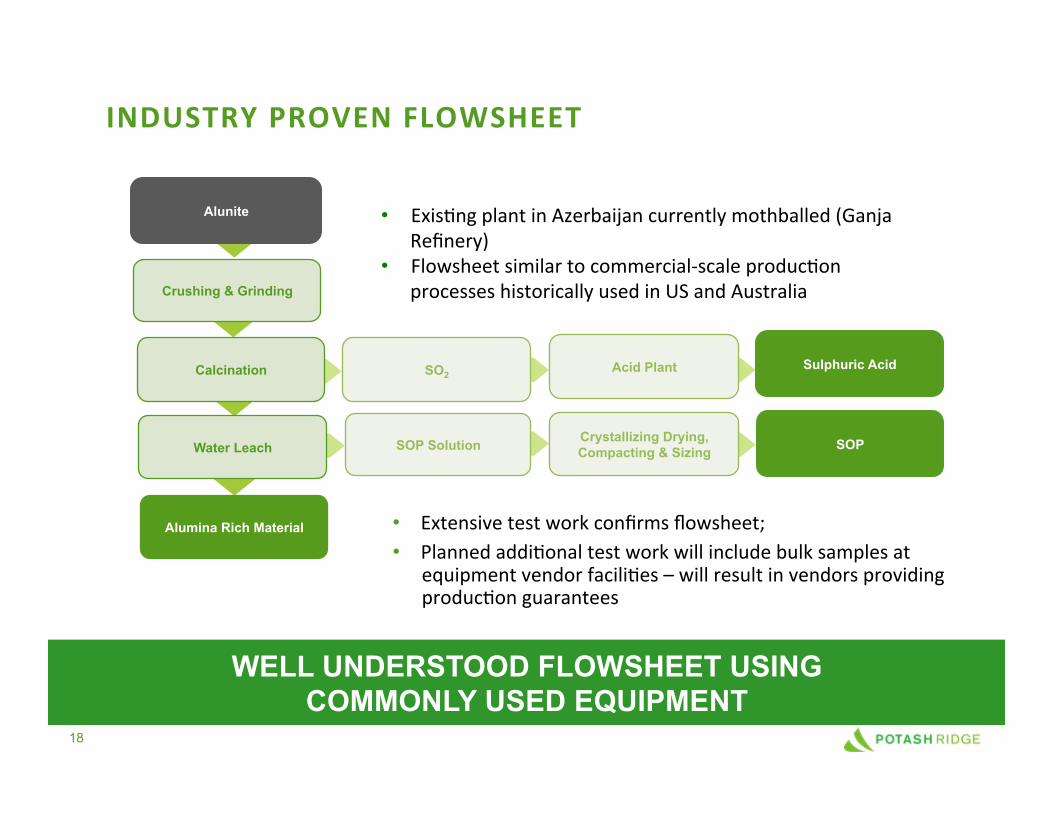

INDUSTRYPROVENFLOWSHEET

Alunite

Calcination

Water Leach

Alumina Rich Material

SOP Solution Crystallizing Drying, Compacting & Sizing SOP

SO2 Acid Plant Sulphuric Acid

18

WELL UNDERSTOOD FLOWSHEET USING COMMONLY USED EQUIPMENT

• Extensivetestworkconfirmsflowsheet;• Plannedaddi&onaltestworkwillincludebulksamplesat

equipmentvendorfacili&es–willresultinvendorsprovidingproduc&onguarantees

Crushing & Grinding

• Exis&ngplantinAzerbaijancurrentlymothballed(GanjaRefinery)

• Flowsheetsimilartocommercial-scaleproduc&onprocesseshistoricallyusedinUSandAustralia

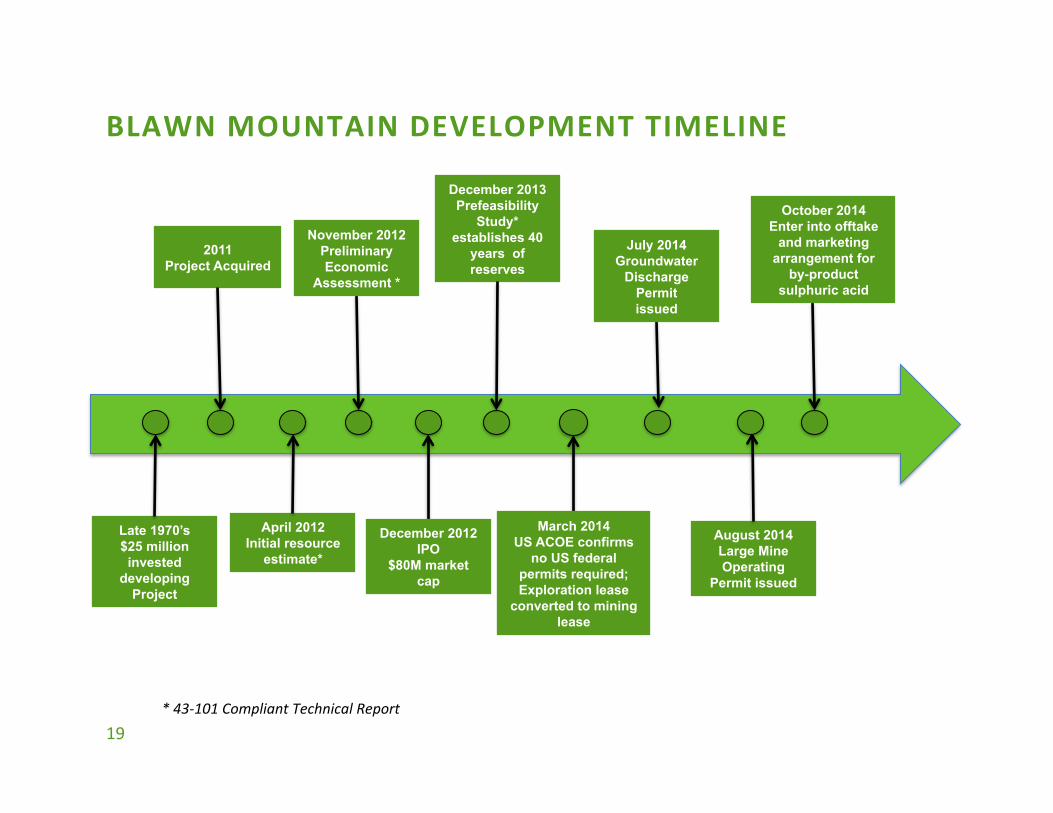

BLAWNMOUNTAINDEVELOPMENTTIMELINE

19

Late 1970’s $25 million invested

developing Project

2011 Project Acquired

April 2012 Initial resource

estimate*

November 2012 Preliminary Economic

Assessment *

December 2013 Prefeasibility

Study* establishes 40

years of reserves

*43-101CompliantTechnicalReport

December 2012 IPO

$80M market cap

August 2014 Large Mine Operating

Permit issued

March 2014 US ACOE confirms

no US federal permits required; Exploration lease

converted to mining lease

July 2014 Groundwater

Discharge Permit issued

October 2014 Enter into offtake

and marketing arrangement for

by-product sulphuric acid

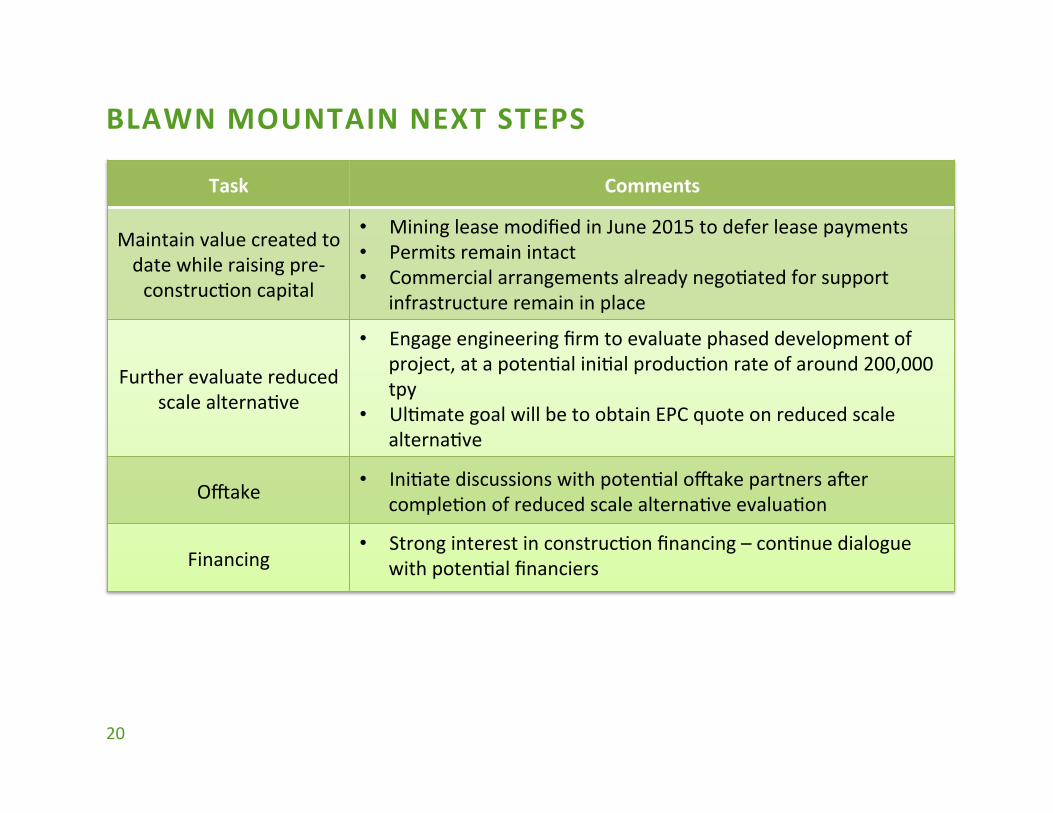

BLAWNMOUNTAINNEXTSTEPS

20

Task Comments

Maintainvaluecreatedtodatewhileraisingpre-construc&oncapital

• MiningleasemodifiedinJune2015todeferleasepayments• Permitsremainintact• Commercialarrangementsalreadynego&atedforsupport

infrastructureremaininplace

Furtherevaluatereducedscalealterna&ve

• Engageengineeringfirmtoevaluatephaseddevelopmentofproject,atapoten&alini&alproduc&onrateofaround200,000tpy

• Ul&mategoalwillbetoobtainEPCquoteonreducedscalealterna&ve

Okake • Ini&atediscussionswithpoten&alokakepartnersaUercomple&onofreducedscalealterna&veevalua&on

Financing• Stronginterestinconstruc&onfinancing–con&nuedialogue

withpoten&alfinanciers

CORPORATEINFORMATION

21

EXPERIENCEDANDPROVENMANAGEMENT

OVER 70 YEARS COMBINED EXPERIENCE 22

GuyBen4nckPresidentandChiefExecu4veOfficer

CharteredProfessionalAccountant20yearsmining/resourceexperienceSherripCFOandSVPCapitalProjects

RossPhillipsChiefOpera4ngOfficerandChiefFinancialOfficer

MA(Econ)/MBA/CFA/CPA10yearsexperienceinlargeresourceandenergysectorprojectsSherrip,CapitalPower

JayHusseyVPCorporateFinanceandPresident,ValleyfieldFer4lizer

20yearscapitalmarketsconsul&ng9yearsSOPexperiencewithMigaoCorpora&on

PaulHamptonProjectManager

GeologistandMetallurgicalEngineer30yearsindesign,construc&onandmanagementofmineralprocessingfacili&esSNC,WashingtonGroup,Outotec

CAPITALRAISESANDCAPITALIZEDCOSTS

23

Date/Price Price Proceeds$mm

February2011 $0.05 $1.1

August2011 $0.25 5.4

November2011 $0.25 1.5

December2011 $0.25 0.5

December2011 $0.75 10.5

December2012 $1.00 20.0

November2015 $0.03 0.6

Total $39.6

Ac4vity $mm

Variousengineeringstudies $10.4

Drilling 6.8

Employeecosts 6.3

Engineeringandpermihngconsul&ngcosts 5.4

Mineralleases 2.5

Other 1.2

Total $32.6

CapitalRaises CapitalizedCosts

CAPITAL STRUCTURE

24

Millions

Total Common Shares Outstanding 106.9

Warrants – $ 0.08 (exp. Nov 2017) 11.3

Stock options 9.4

Total Fully Diluted Shares 127.6

As at February 29, 2016

April2016