ppowerfulowerful rrelationshipselationships/media/files/financial reports... · ·...

TRANSCRIPT

ANNUAL REPORT2009

PowerfulPowerfulRelationshipsRelationships

PowerfulRelationships

=PowerfulResults

HighlightsHighlights20092009

Earnings before interest, tax, depreciation, amortisation and

fair value movements of fi nancial instruments grew 25 per cent

to $260 million.

Underlying earnings after tax grew 28 per cent to $118.8 million.

Successful completion of Stage I – comprising 98.7 MW – of Snowtown Wind Farm project in South Australia, the Company’s

fi rst offshore project.

Resilient trading result despite very challenging conditions

experienced through winter 2008.

Strategic FocusStrategic Focus20102010

Complete successful resource consenting outcomes for the Wairau

and Arnold hydro projects.

Implementation of new customer care and billing system.

Protect and grow TrustPower’s premium retail brand.

Development of Australian business strategy including progressing

feasibility of new wind development opportunities in South Australia, Victoria and New South Wales.

Contents

Successful First Project Across the Tasman . . . . . . . . . . 02Directors’ Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 04Chief Executive’s Report . . . . . . . . . . . . . . . . . . . . . . . . . . . 08Deep Stream, Win-Win for Otago . . . . . . . . . . . . . . . . . . . 12Board of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14Management Team . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15About this Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Sustainability Outlook . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17Celebrating Volunteers in our Community . . . . . . . . . . . 20Preferred Partner for Top Energy . . . . . . . . . . . . . . . . . . . . 22Our Customers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Relationships Count . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26Environmental Performance . . . . . . . . . . . . . . . . . . . . . . . . 28Sustainable Economic Performance . . . . . . . . . . . . . . . . 31Corporate Governance Statement . . . . . . . . . . . . . . . . . . 34Financial Statements 2009 . . . . . . . . . . . . . . . . . . . . . . . . . 37Auditors’ Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38Statutory Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69Security Holder Information . . . . . . . . . . . . . . . . . . . . . . . . 72Sustainability GRI Index . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74Directory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77Financial Calendar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

TrustPower / Annual Report 2009 / 01

At TrustPower we believe it’s the quality and At TrustPower we believe it’s the quality and strength of our relationships that set us apart.strength of our relationships that set us apart.

We don’t stop at just what is expected but alwaysWe don’t stop at just what is expected but alwayslook further. What are the extra little things that look further. What are the extra little things that

make a difference? We believe it’s this singlemake a difference? We believe it’s this singleminded commitment that gives us a strategic minded commitment that gives us a strategic

advantage and will continue to deliveradvantage and will continue to deliverpowerful ongoing results.powerful ongoing results.

customers

peoplecommunities

stakeholders

environment

02

BBByyy ttttaaakkkkkiinngg aaannnn oooouuuuttccccooommmmeee ffffooccuusseeedddd aaaannnddd pppprrraaaaggggmmmmmmaaattttiiicccc aaaapppppppprrrrooooaaaacccchhhh ttooo tthhheeee ccoonnsssttttrrrruuctionnn oofff tthhhee Snoowtowwn WWWWiiinnnndddd FFFFaaaarrrrmmmm,,,, oouuurrrr fifififi rrrssstttt eeennnnttttrrrryyyy iinnttoo Ausssttrrrraaaalliiaa, wwee wweere able tto dddeeelliiivveeeer tthee pppprrrroooojjjjeeeecccctttt aaaahhhheeeaadddd oooff aaaalllllll exxppeeeccccttaatiions. NNooww sseeccuurreellyy iinn ooopppeeraaattiioonnnnaaaalll pppphhhhaaaasssseeee,,, tttthhhheeee wwwwiiiinnnndddd ffaarrmmmm iiss ppeerrffoorrmminngg bbrriillliiaannttllyy.POPOWEWWEEERRFFULUL RELELATATIOIONSNSHIHIPSPS == PPOWOWERERERERRRRRFUFUFF L L RERESUSUSUUSUSS LTLLTLTSSSS

Successful First Project Across the Tasman

TrustPower / Annual Report 2009 / 03

Adapt and Deliver Adapt and Deliver in a New Countryin a New CountryBuilding new relationships was a key focus prior to and during construction of the Snowtown Wind Farm. A key relationship was, naturally, with turbine supplier, Suzlon Energy Australia Pty Ltd, which had a “turnkey” contract to supply, install, and commission the entire project. Our relationship with Suzlon, meant both parties could maintain an open, fair and trustworthy approach, ensuring everybody focused on results rather than getting sidelined as inevitable issues and challenges arose. The relationship was such that Suzlon happily allowed TrustPower direct contact with project sub-suppliers, giving us a signifi cant network of people and expertise to call on for future Australian projects.

alialaliialililiiiiiliiiiiaaa aa aaa aa aaaaaaaaaaaa EstEstEstEEstEstEstEsEsEstEsEststablaablblablablablablablbablblablllaabababbbbbb ishishishishishishhshhiishshishishsshiiingingingingingingingngingngingnginginggggnginggg an an an a annnnnnnnananana as asas as asasasasssa setsetsetsetetettsetsesetsesssss inininininninininininnnin inn inn innin AuAuAuAuAuAuAuAuAuAuAuAuAuAu Au Au AuAuA strstrstrstrstrstrststrstrttststrtstrstss alialalialialalialialiaalia aaweweweweweweeeweww r r wr wr wr wwr wr wwr wwwwwithithithithhhhhhhithhithithithithithhth a a a aa aaaaa a nonotnotnototnotnotnotnotnonotnotnotnonnottt ononononon onnnnnn onoo ly ly lyly lyyyly ly lylyylyyy proproproprproproooproooppppppropropprooovidvidvidvidvidvidividvidvidvididdvididvv es es es es es sses eses eeeeeseeese TruTruTruTruTruTruTTruTruTruTruTTruTTT stPstPstPststPstPstPtPstPstPPs oweoweowwoweweweoweoweeowowwowwwwwww

t alalal alaalaal alalalalalalalalllllsoso sososo oo sossosssooso soo oo addaddaddaddaddaddaddadadddaadaddaddadda ddadddaa ss ts ts tss ts ttttttts ts ts o o ooo oo oooooooplaplaplalplaplaplaplaplaplaplappppplaplaplaplaplap tfotfotfotfotfotfotfotfoofoootfotfotfofoffofoorm rmrmrm rm rm m rmrm rrrmrmm forforforforforforforoforforofoorrfoffff r g g gr g grgrgrgr grg g ggrgg grggg grgrowtowtowtowtowtwtowtowtowwtowowwowwwow h, hh, hhhh, hh, h,hh,h, butbutbutbutbutbutbututbutbubutbbubuuuubututu alaa amememememememememeememeemememmememmemem d dididdidi didi didididi ddi di di verveveverveerverererrrvervvvevevvv rerrveveeereverrrrverrv revee sitsitsitsitsitsitiisittitsitsissitsititiittsitsitttsitssitsss ts y wy w wy wy wwy wy wy wy wwy wwy wwwwwwwwwwy wy wy wyyyyy eeee e e e eeee ee eeeeeeeethethethethethethethethehethehthetththethhh ge ge ge geegege ge ge gegegenenernernnerernernerrenerrrnernenernnenennere atiatiatitatiatiatiatiatiatitaaatiatiaatiatiatitiatitiatiatiaatiataa oooooonononononooooooonoononon onoon oonoononon n incincincincncccncncncnncnnincnnininciiii omomomomommmomomoooommmoo

nnnn Ne Ne NeNNeNeNNeNeNeNeNeNe NNee NeNNNN NeNNNNNew Zw Zw Zw Zw ZZ Zw ZZZZZZZw Zw Zw Zw Zw Zw ZZw ZZw Zw Zw Zw Zw Zww Zw ZZZw Zw Zw ZZZZZZw eealealealealealealllealealaalaealalaeeeaeallalalealalaaaeaae andandandandandandanddanddanddandanddandandandandandandndandandanda ddddandaaandandaanaandd BBBBBBBBBBB. BBBBBBBBB. B. B. BBBBB. BB. B. BBBB. BBBBB. . BBBB yyyy yy yyy yy yyyyy y yyyyyyyyycurcccurcurcurcurcurccccurcurcuuuuu renrererenrenennnnrennnrenrenrennr tlytlytlytlytlytlytlytlytlytlyltlytlytlytlyltlltlyy en enenenene en enenenn ee joyjoyoyjoyjoyjoyjoyojojoyjoyjoyjoyyjj in in inin in inin innnnnin N NNNNNNbb eeeeeeeeeeeee ooofofoo of of ofof of of ofofof ofofofooffof of th ththth thth th th thth thth thththtththththht thhhh thtt the be bee be be be be be be be bee beeeeee bee bbe b be bbestesteseseststesttteste testestesestestessttesteestestessts wwi www wi wi wiwiwiw wiii wiwwwiwwwwiwiwwiwiwiwww wiwww ndndndndndnddndnddndnd dnd ndndnndnd nddnnnnnd nnndndndnnnnddnnnnd farfarfarfarfarfarffarffarfarfararfffaffaf m m mmmm mm mmmmbuibuibuibuibuibuiuibuiuibubububuiiiuiuiuibuuibuu ldldildildildildildildlldildll nng ngng ngngng ngnnngng ng ng oonon onon onononoonononnono oneoneoneononeoneoneneonneneonennsitsisitssitsitsitsitsitsisitsitsittsitsss tts e aaaaraaaaaraaarralialialiailialialialialialiaiaaliaiaaaaiaiaiiai , w, ww, w, w, ww, wwwwwwww, wwww, w, www, e he he he he hhe hee he he he he hhe hhhhe hee he he he hhaaveaveaveaveaveaveaveaveaveaveaaveeavavevveveaveaveavevaveavavvavve es eseses eses eseseseseses eseesssseesssesesee tabtabtabtabtabababbbbabtabbtabtatabbtabtabtaabtaabtabtatattata lislislislislisiiislisilislislilislislislisslisisislislisislisisssssssshedhedhedheddddhedhedheddhedhedhedhhhedhhedhedhhehhhehedheeededde itittttiittes es eseeesesesses eseses ssssesssssesses inin nininininininininnn nnnnnnn AusAusAusussAusAuususAAAAAAAAAuuusAuAuuusAuAuAuuuussuuuAuuAAAustrtratrtratratratttrarttrra sa sa sa sa sa sssa sa a sa sa sa sa sa ssaa saaaa ssssssa sa seeeeeeeeeeeeeeeee ccncncnccncncnccccccccccccccccccccccccomeomeomeomeomeomeomeomeomemeeemememeomeomomemeomeomomemomomeomemomememomoo eoo ee ststsstsstststststst st sststststtt s st s stst ststssstsststststtstsss reareareaereareareaeeareeareareareaeaeaaeaareareareaeareaee m cm cm cm cm cm cm cm cm cm cm cm cm cm ccm cm compompompompompompompompomomommompompompompompompomompompommmpompo pomppmo letletetletletletletetletetetetetetetletetleletelettteeeteeteee elyelyelylelyelyyelyyelyelyyelyelyelylyelyelyelyelelylyyeleelylyyellylelyelyyyyye yy ecuecuecuecuececueccecuuuucucuccucure rere rerere re reerere rre rerrree inincncncinncincinciininncnnnncncnnnnnnnnnnnnnnnnnnnnnnncnniniindindindndndnddddnddinddddindindindinndndindindndddinindininndeeepepepepepepepepeppepepppepepepepepepepeeeeeppeep eeeeeeeeeeeeeeeeeent ntntnt ntnt nt ntnt nntnnnnntnnnnnntnt ofofofofofofofofof offoooof ofooof ofofoffof of ooo NewNewNNNNewNNewNewNewNewNewNewNewNewNewNewNewwNewNewNewNewNewNewNewNewNewNewewNewNewNeeweNewNewNewNewwwewwNeNeewwNNewewwNNN wwwwwww Ze ZeZe ZeZeZeZZeZeZe ZeZeZZee ZeZZeZeeZeeZeZeZZZ ZZZ ZZ Z lllllalalalaalaalaalaalaalalaalaalalalaalaalalaaalaaalaalaalaalaalaalaalaalaalaalaalaalaalaaaalaalaalaalaalaalaalaaalaalalaaaaaaalaaalaaaaaaaaaaaalalaalaaaaaaaaalaaalaaaaaa nndnd nd ndd ndndndnndddndndndnnndnnnddnnndnddnnnndndnndnnnnnnnndndndndndnnnddn weaweaweaweaweaweaweaweaweaeweaweaweawewwweweawweaweeweaewweaeweaweewwewewwwwwww awwwwww thetheththhthethethethhthehtheheththethehhethethethethethethhehethethettttheheerrrrrrr rrrrrrrrrrr rrrrrrrpepepepepepepepepeepepepepeeeeeeependendendendedndendendendedndedndeddddnddandandandandandandnandandnandanddandndandandandandandnddandddnddda dddddaa m mmm mmmmm mmmmmm mmmmmmmm kekekekekekekekekeeekekekekekekekekeeeeeeeeeeekeeeeekeekek t ct ct ct ct ccct ct ct ct cttt ct ct ct ct ctt t ctttttttt ccttt ctt cttt cccondondondondondondondonondondondnddondondondondondonddonndondondnondndondondondonnonnndnddddondo itiitiititiitiitiitiitiitiitiitttiitittititititititttttionsonsonsonononsonsooonsonsnnononsnnnnsssssssssssnsonsooononnsssssssnsonsonsonsnonsssssssnsnssssonnnnsssonsnnssonssnnonsnnsonsnonsonssnnssonsons.....mamammaamaamaamaaaaaaarkrkrkrkkrkrrkrkrkkk

AsAs AsAs As As As AsAsAss s s As As AsAs As AAsAsAs AsAAAAAAAsAAAssAsAsAsA papapapapapapapapapapapapapapapapapapapppaapapppaaapppppapapapapapppparararararaararraarararararaaaaaraaa tt ot ot ot ot ooot ot oot ott oot oot oot ot of of of of of of of of off of off of of off of off of oooff oof off uururur ur ur ururuuuur uruur uuurr focfocfocfofocfococfocfococfocfocfocfocoocfocfocfoffoooo us usus usuussus uus susususus uususuus uuuuuu oon ononon on on n n oonnnon thethethethethethethethehethethethethethehthett e envenvenvenvenvenveenenvenvenvenvenvnvnvenvvvvenvenvnvenvenvenvenvenvnnvnvenvenvennnveneennenvene vve iiriiririiiiiiiiiiiroroiroroirorororooororooroooroorrorororirir nmenmenmnmemnmenmnmenmenmenmenmemnmnmnmeenmenmenmenmeemnmenmen nt,nntnt,nt,nt,tntntnt,nnt,tnt,nnttnnnnt,nt, w wew weweweweeweewe wewewwweewwewee wew es e es esesesesesesses essseesess tatabtabtabtabtababtabtababtabtabbtabtabtatabtabbbbabat blislislislisisssslissisisslisslissllisli hedhedhedhedhedhedheddedhedhhedhedhhedhhedhedeeheehhhheeed st st stst st stt stst st stsssssst stststronronronronronronronronronononronronronrononononoooorororrorr nno gg gggg gg g g ggggggggggggggggrelrelrelrelrelrerelrelelrelrelreeelrelrelrelreelrelreleeeereeelelllllr lelee aaaaaaaaaaaaaaaaaaaaaaaaaaaaaatiatatiatiatiatiattittititiitiittatt onsoonsonsonsonsononononsonsonsonononsnnsonsoonsononnonnsnnnonnnonononsonsoonsnsonssshiphiphipiphiphiphiphiphhipihipph piphiphhhiphiphihipips ws s ws ws ws ws wws wws wwwsssss ws ws wwws ithithithithhhithithhithhhhithithhhtttt ththththththththththththththhth the Ae Ae Ae Ae Ae AAAe AAe Ae AAe Ae Aeeeee boborborborborborborbororbboborborrrborrorbbobbbobooorigiigigigigiigiigiigiggiggigigiggigiigigiiigiii nalnannalnalnalnalnalnalnalnalnallnanaalnaallnalna peoppeopeopeopeopepeopepeoeopeopeopeopeoppeoepeopeopppeopeopepeeeopeoopppeeeopppppp oeooeoeoopeeopeooeoopepepeop opeopepeooooooooooooooooooplepplepleplepleplepleplepleplepleplepleplepplepleplepp eplepple iin in in ininin in inninnnnnnnnn th ththth ththhtht thth thththth ththhhhh eeee Se Se Se Se Se Se Se Se Se Se Se See Se Se SSSSSeee See Snonownownownownowowownowwwnownownoowwon won woo towtowtowtototowtowtowowowowwtowowowtowwtowowown rn rn rnnn rn rn rnn n r n rrrn rn rrrreegiegiegiegiegiegiegiegeggegiegiegegegiegiegieggiee on.on.on.onon.on.on.ooon.ononnon.onnon TheTheTheTheTheTheThhTheheTheeheeTheTheTheThhehehTheThhTheThehheheeTheTT eThTheTheheehhThThhhhhThhThThhhhehThheeeeeeeeeeeesesese se se se se seseseseseseesseeessee rerelrerelrelrelrelrelrelreleleleeelllee atiatatatiatiatatatiatiiatiiatiattattiatittititiata iaaattttiooononsonsonsonsonsonsnsnsnsoonssnsnsonssnsonsoooonoooo sssnssshiphiphiphiphhiphiphiphiphhiphiphiphiphiphhhipppps rss rs rs rs rrs rs rs rss rs rs resuesuesuesuesesuesuesususuesueesueesususueseee usultelteltelteteteltelteltettlteltelltetltttteeeed idd id id id id id idd i id idd iddd idddd ddd n tn tnnn tn ttn tn tn ttn tn tn n tnnnn tn tn ttn hehe hehe hehe hhe eheheheeheheelocloclococococlocloclococococococlococlocococl cocococloccoccoloool cloccaaaaaaaaaaaaaaaaaaaaalal alaal al aaalaal AAAboAboAboAboAboAbooAboAAAbooAboAAAAboAAboA oA oAAb iiirigrigrigrigrigrigriggriggrr grr grigrigriggginainainainnainainainainaanaiininaaininininanaall pl pl pl pl ppl pl pl pppl ppp pl plll ppl eopeopeopeopeoooeopeopeopeoppeopeopeopeopopeopeopeoeopoooooeeoo lelleele ele le eleleeeeeee e haphaphaphaphaphaphaphaphaphapaphaaphapaphaphapapahapaphhaphapphhh ppilpilpilpilpilpilpilpilppilpilpipilippipiiipilppp y y yyyyy yyyyyy yyyy yyyyyyyyyyyyyyyyyyyyyyyyyyyyyyatattattattatattattattattattattattattattattattatattattattattattaattattttattttatttttattttattattaattttttttttttttttttttttttttttttttttttatttttattttttttttatatttaaaaattaaaatttttattttaattttttaaaa eneneneneneneeeneeneeneneeeeeneneeeeeneeeeeeeenenndnddnddnddndndndndndndndndndnddnddndndddndingingingngngngngingginginginginginggingngngngingingnggggggg ththt thtth th thtthh ththtthht thtttttthtththttt e se se see se se se se see seeeee se ee e se iteiteiteiteiteiteiteteiteteteiteiteiteet as as asasaas asasass aaaasasasasaaaaaaaas a an anaan an an anan an ananananaanannaanand wd wd wd wd wd wd wd wd www w wd wd wwwd wwwd wd wwdd wd wwd wd wd wwdd wddd hehenhenhehehenhenhenenhenhenhenhenhehenheheennenennenehhhehehhhehh nnnh n reqrreqreqrereqreqeqeqeqeqreqreqqqreqqqreqeqeqqreqreqeqrererereqreererererereqereereqeeeeeeqequiruiruiruiruiruiuiruiiiiiuiriiiuiruiuiiiiiiuiruiruiruiriruiruiruiuiruiruuiruiruiruiruuuiuiuiruiuiuirruiruiruirruirrriirrruiruu eeeeeerrrrrrrrrrrreeed,ed,ed,eded,ed,ed,ed,ed,ed,ededed,ededed,ed,ed,ed,ed,ded,ed,ed,eded,edd,,,, as asaas as aaas as a asaaaa as sississississississisisissississsistintintintintinntintintintttininng tg tg tg ttg tgg tg tg ttg t g he he he hehe hehe he he eheheheee concococonconconconconcooconcocoooncoconc strstrstrstrststststrstrststrstrst uctuctuctuctuctucucuctctucttuctucctuctionionionionionioniononionionionononnoonnonnonoonnn ttteateateateateateateateateateateateateeateateetteateattteaeaaeeeeeaeaeeam tm tm tmm tm tm ttm ttm tm ttm tmmm ttm tmm tm ttm ttmm tooooo ooo o oooo oooooooo ooooooo ao ao ao ao ao aao ao aavoivoivoivoioivoiiiioivoioivoivoivoivovovvvvo d ad aad ad ad ad adddd ad ad ad ad ad ad dd ad addddd aareareaeareareareaeareareaarearrereee s os os os os os os os os os oooooooooss os f hf hf hf hf hf hf hf f hf hf hf hf hhhf hhf hffff hf hf hff hhhf iststististstististttististtististisiiiii oorioooriorioriioriooo cc c c cccccsigsigsigigigsigsigsigsigsigsigsigsigsigigsigssigsiggsiggsisiggsigiigs gnifinifinifinifinifinifinifinifinififinifinifinififinnifinifinninifinifiififinnifi caccaca ca ca cacacaa ca caca caaacacaaaaacaccaca cacc cancencencenncnncnncncncncencncenncccencceececececececeececee, a, a, a, a, a, a, aa, a, aaa, a, a, aa, , and ndndndndd nd ndndnd nd nnd nn ararearearearearearearearearearearearaaaa eas asasasasasasasasas asaasssasaaasass conconcconconcononconoconcononconconconco taitaitaiaiitataitaaaiatata ninninninninninninnninninn g g gg g ggggnatnatnatnatnatnatnatnatnatnatnatnatnatnatnanatnanatnananatnananatnatnatnnanatnatnnnnnnnnannatnatnatnnnannnnan iiveiveiveiveiveiveiveveiveiveviveivevvevveiveviveiveveiveveiviveiveveveveveveeeev ve veveve ve ve ve vevevev vve ve ve ve veeeveve vevvevvvvve vvvvvv v vegetgegetgetgegetgetgettgetgetgetgetgetgetgetgetgetgetegetgeteeeetggegeetgetgetgegeg atiatatiatatatiatatatiaatiatatiatitaataatitiiiatiatiatiatitiiatiatatitatitiion.on.on.on.on.oonon.on.non.n.on.on.on.on.non.non.on.n Fo Fo Fo FoFo Fooo FoFooFFoFF Fo FoFoooFooFoFoollllollollollolloollollollolloollollollloooll owinwinwinwinwinwinwinwiiiwiwinwinww nng g g gg gg g g gggggggcomcomcomcomcomomomomoocomomomcomcomcomomomcoocomomcoccccocomcco plepleplepleplepleppleepleeplepleplepleplpplepleeeplpppllepllelelpppp titiotiotiotiotiotiotiotiotioooitiotiotiiotiootiotiotitiotiot ot oooooot n on on on on on on on oon oooon on on on oon ooon on on oon nnnn ooon oooof tf tf tf tf tf tff ttf tf tf tf tf tf tf tf tff tf tff tf tttffff ttf tff the hehehehhhehehehehehehehe hhe ehheeheheheeee ppppppppp ood odod odddod ddddod dooddddodddheeeeeeee proproproproproproproproprpropproprorprorpprojecjecjecjecjecjecjecjecjececjececjjejecjececje t, t, t, t, t, t,t,t, ttttt,,, thethethethethethethethethethethethethethehethehe go gogg go go go gogg gog gooo googoggg od odododdododdododddodododdoooworworworworworwororworworworwworworworworworwwworwoorwororworworworrrworrorworw rrw kinkinkinkinkinkikinkinnkkinkinkinkinkinkinkinnkinkinkinkkkinkininnnnnnkinnnk nk g rg rg rg rgg rrg rrg rg rgg rg rgg rgg rgg rg rg rg rg g rgggg rgg g rg elaelaelaelaelaelaelaelaelaelaaaaelaaaelaelaelelaeelaelaelaaaaelae aelaae aelaelaeeleleelele tititiotioiotiotiotioiotiotiotiotiottiotiotiotiioioot oioioootitioi nshnshnshnshnshshnshshhshshshnshnshnshnshnshnshshnshnshnshnshnsshnnnshnnsnshshnsnshnnsshsnsnshnshnshns ip ipip ipip ipipippipiip iippip ip pppip ipip ccccc ss ananananananan ananannanananan anananananaannananannnananananaananandddddddddd dddddd dddd dd dddd pppppppp conconcoconconcononconconconconconoconnnoncc noncontintintintintintintinintininintinintttiniinintttii uesuesuesuesuesuesuesuesuesueueseueueueessssssssues a a aaaa awwe wwewe we we we wewwwe wwe wewe we wwwwwwwwwwwewewwwweeweewe areaaareareareareareareareearereareaareareeeareeeeeareeeea eaa eaaaa eeeaa eeeereeer alal al al aalal al alla alaalaallalllalaaalaa rearerererereareareeeareareaeareaerearrrereaearreearerearreareaeeaeaee dy dy dy dy dy dy dy dy dydydydydy dydy dy ydydydydy ydy dyydyyy iinvinvinvinvinvinvinvinvinvinvinvnvinvnvnvinvnvnvvinvnvi vvvnnviiinnnvn olvolvolvolvolvolvolvolvolvolvolvolvolvolvolvolvvolvolvoolvolvolvolvoolvolvolvooooo vvo vingingingngnginginginginginginginginngngningninnniii ggg gggggggggggggggggggggggggggggggggggrourourourourourourourourourourooourourourourourrorourourooorourouooorour p ip ipp iip ip ip ip ip ip p ip ip p ip ip ip p ip ip ip ipppppp nnn n nnn nnnnnn nnnnngngngngnggnggggggggggggg ththt th thh t thththththththtthe ge ge ge ge ge gee e ge e e e e gee ge ethethethethethethethethethethehethethethetheththetthethehhehehhthehhtheheeeheeeeheehehettt e pl pl pl pl pl plplplpl pl plpl pl p pl pl pl plplplpppll p ppll plplppppp annannannannannannannananannannannannannannannannaaannannaannannannannannannanna nnnananannnnannningingingingngngnggngngngngingngnggnginginggingingnggingiinginggngnginngggggg of ofof ofof ofofof of of ofooofof ofofofo of ofofoffffofoff ofo StStStSS StStSt StSt StSt StStSS StStStSSS StStSSttSSttttSt St StStStSStStageageageageageageageagegeagageageeaageageageageageaageagagageageaggeagaagegeagea eageag 2 2 2 22222 2 2 2222 22 2222 22 oooooooooooooo hethehththethehehethehthehehethethehethhehetheheheheheheheheheeheeehhheeheeeh of ofof of of foof ffofoof oooo thtthhtttttttttttSSnoSnoSnoSnoSnoSnoSnonoSnoSnoSnoSnoSnoSnonoSnoSnoSnoSnoSnonnonoSnoSnoSnonnnnooSnnSnnnnSnonoowtowtowtowtowtowtowtowtowtotwtowtowtotowtowtowtotwtowtototototootowtowtowtotoooowtowtowtwtowtoowtowwwwtw wwnwn wn wwn wnwn wn wn nnnnwnwn wnwnwnwnnnnnwnwnn wn wn nnnnnnnwn wnwnwwnnnnnnnwwnnnnnnw devdevdevdevdevdevdevdevdevdedevdevddevdevdevevdevdevevevdedeedevdeededdevdevedevd vdevede eloeloeloeloeloeeloeloeloeloeloeloeloeloeloeloeloeloeleloeloeloeloeloeloeelolloelololl pmepmepmepmepmpmpmepmpmepmepmepmepmepmepmemepmepmemepmepmmpmepmpmpmemepmeepmpmempmeepmepmempppmp nt.ntntnt.nt.nnt.nt.nt.nt.nt.ntnt.ntntntntnt.nt.nt.nt.t.ntntntntnt.n

TheTheTheTheTheTheTheTheTheTheTTheTheeTTTheThTThee Sn Sn Sn SnSnSSnSnSnSnSn Sn SnnSnowtowtowtowtowtwtowtowwwowowtowtowtooow ooottttownownownownwnwnwnownowww cococ co co cocommummummumumummmmmmummumunitnitnitnitnitnitnitnity wy wy wy wy wy wyy wyyy wwy waas asas asaasas asheahehehheaheaheaheaheaheaheaheaheaheaheaeeaeeavilvilvililvilivivivvily iy iy iy iy iiiyy iy y iiy iyy iyy iy iy nnnnnnnnnnnvonvonvovonvonvonvonvonvoovv lvelvelvelvelvvlvelvevelveveved id iddd idd id id d id id innn tn tn tn tn tnnn tn tn thehehe he heheheheheh proproproproproproprooprppp jecjecjecjecjecjeccjeceeject, t, t, tt, t, t,t, incincincincinncincncncnccncncccciinccn lludludludludluddludl dlududududludludludluddddddiniinininiinininininningngngngngingnngingngn su sususu suusu susussus su susuupplpplpplpppplplpplppplpplpplpppppp yinyiyinyinyinyinyinyinyinnyiny nininny llg lg lg lg g lgg lg aboabobboaboabooaboaboababoaba oa ur ur uur ururuuuurruu andandandandandandddandandnaa accaccaccaccccaccaccacccaccaaccaccaaccaccacccccacccaccaccaccccccccacccomomomomooomomoomomooomomoommomomomooommmmmmmmmmmmmmmmmmmm odaododaodadaodaaodaaodaodaodaoododao tiotiotioitiotiotiotiootioottionnn. nnnn. nn.n. n. nnn TheThThTheheheThTheeThTheTT eTTheehe wiw wiiiwiw ww wiw wwiindddndndnd ndnd ndndddd ndnd ffffarfarrfarfaafarfara m m mmmmmm mmmopeopeopeopepeopopopeeeooo ep nnnnnnnninninninninnnininninng cg cg cg cg cg cg cg cg eereereereereereereeee monmonononmoonomonnmonm y, yyy, yyy helh lhelhehehelhelelhelhelhelhhh d od od oodd o oood oddd n tn tn tn tttn tn tttthhehhehhe hehe hehe e hehhhhh maimaimaimaimaimaiiinn n n nnssstststrstrstrstrstrststrstrs eeeeeeeeeeeeeeeteeteeteteteet of of of ofofofofo th thth thhhe te te e tte ttownownownownownowownownowwwnshishihshihshiishissh p ip ip ip iiipp pp n tn tn tn tn tttn tn ttnn tn the he he hhehe e e e fofoforfororforforfoforfo m om oom om om omm f ffffffa oa oa oa oa oa oa oa oaa oa oa oa oooa ooaa nnnnnnnne-nenene-nnne-ne-nenee dayddayddayddayyydadaydaydayy fefefe fefefe fefefestistististitstistististististivalvavalvalvalvalvalvavalvalvalv , ww, ww, w, ww, ww ww, w, wwaaaaaasas asas s ss ass aas s s plapplaplaplaplaplaplaplaplap nnennennenneeed wd wwd wd wd d ithithithiththithhhhhttththt thethethethethhehhthhethehethetheethethethee lo lololololl lololocalllcalcallcalcalcacal CoCoC CoC Co Co CoCo CoCommummummummummmumummummunitnitnitnitnitnitni y Myy My MMy MMy MMy Manaanaanaananananagemgemgemmgemgemmmg eeentenenentntentntnteentnteenttt AssAssAssAssAssAssssAssAssAsssssssssssssAssssA ssssssssociociiociocociocc atiatatiattatiaa on.on.onnoonon CeCeCeCCCe CeCeCe CeCeCeCeelebl bblebbleblebeblebeebblebe tttratttratrratraatr ingingngingininginginginnginggngg nonnonono no no no nonono n t ot ot oot ot oot oottt t ooot t nlnlynnlynlynlynlynlnnlylyyyy tththethetheeththeheethhethehhththeheee wiwiwiwiwwiwwiw nd nd nd nd nd nd nd nnd farfarfarfarfarfarfararfararara m, m,m,m, mm, m,m, m, mmm, butbutbutbutbutbutbutbutbuttb t al al aaala alal ala so so so soso osoooo thethethehethetheeht e wi wiw www derderderderderdededderde comcomomcommo i iiritttttt ititittititit attattattttattattattttatttraracraracracaccrracracacraccctedtedtedtedtedtedtedtedtedtedtedtedd an ananan an ananana mmmunmunu ityity sp spspiriirir t, t, it it it aestestesttestesestestimimiimi tttto ao ao aaoo aaaaao ao aa to tottototot tototo totoootownwnwnwnwwnwwnwnwnwnwnmamamatedtedted 2,2 2,00000000 pe pep oplople te to ao awitwitwwitittwitwwitwwith ah ahhh ah ah ah ah ah a aa po popop pulpulpulpulpu atiatiation oon of off jusjusst 4t 444400.0000.

TheTTheTheTheTheTheTheTTheTThTheThTheee rerererereeeeee rer rere rereeeeeelatlatlatlatlattlatlatttllatlatlataattionioniononioniononionioniooioioooooo shishishihhshishishshhihhhs ps pspsps ps pspsss pspppssp betetbetetbbetbebebetbetbeetb weeweweeweeweeweeeeeeeeeweeweeweeeweewweeeewee n onnn on oonnn on on on on oon onn ooouur ururur ur ururur uuur r stastastatstastastastaastaafffffffff ff ffff ff f andandndandanandandaandddddandandnn coc co cocococo co cococcocontrntrntrntntrntrntrntrntrntrrntractactactactactactacttctctc orsorsorsorsssorsorsorsorsorsoro s wewerwerwwewerwerwerwereerwerwwererwere ee ee ee ee ee ee ee eee eextextextextextextextextexteextensinsinsinsinsisinsinsinsinsnnsnsnsnsnsnsnsns ve.ve.ve.ve.ve.ve.eeve.eevve A A A A A A AAA AA googoogoooogooggoogoogoogoogooggoo d ed ed eed ed ed ed eed d examxamxamxamxamamxamxamamxamxamxammmmpleplepleplplplepleplppplpleplepleeep of ofofof ofof of of of offofoff lilililili li liliaisaisiaisaisaisaisaisaisaisaisaisaaisaiaisa on on on oon on on oonoon ono wwiwwitwitwitwitwittwitwitw ttw twittwwitwitwittww hh h th th thh thhh hh th thhhh thh thhh thhhhehehhe hehe hhe hhe hehe hhehe locloclococlocllloclococloclocololoclocloclolooccccccccccc lalllalalalalalal al alaalcomcomcomcomcomomcomcococcomcommcomccomcomco munmumumunmmunmunmunmummunnmuunmunnnnunnnununmunnnnnnnnnnnu ityitytyititytityitytyityitityitityitytyityityitytyityityitytytyyyyyyyy ananananananannananananan anana an ana aand kd kd kkkkkkd kd kkddd kd kkkd d key eyeyeyey yyey eyeyey eyeyyeeyey eyyy stastastastastastastastastastttasstastaststasts kehkehkehkehkehkehhhkehkehhhkehkehehekehkehkehehkehhkee oldoldoldoldoldlddddooooldoldoldooldoldoldoo erserserseerrersrsrsserserssreerserseerserser oc ocococ ococ ocococococ oocococccurcurcurucucurcurcuucurcurcurcurcurcurucuc redredredreddddreddredddredredrededdedereded whwhwh whwhwhwh whwhwhwh wh wheeen en en en en nnnn en nennenne thethethehthethethethethhhehttheheee loclocloclocloclocoocococcococal al al al alal al aala bbusbusbusbusbusbbbusbusbusbubusb hhfi hfihfihfi hfi fi hfi fifihfi hfi hfi hfi firere re rerererreerrere fi gfifi gfi gfi gfi gfi gfifigfi gfigfi htihtihtihhhtihtihhtt ng ng ng gng ggg teateateateaeaeaeaaattetee m wm wm wm wm wm wmm wm wwwwwm asasassasasas as s sas shoshoshhhhhoshoshoshohoshoshoshohshohhshoshoshoshoshosh wnwn wnwnnwnwnwnwnwwwwwwwnnwn wn nwnwnwn aroaroaroaroaroaroarororoaroroaarooaroaroaaa undundundundundundundundundndnduuunduundundundundundunddddd th th ththh th ththththh t t t t e se se se se see iteiteiteettitettiteiteeeeettt , , , ,, ,,totottototo totototo tto to to toooto helhelhelelhelhhelhehehelhehehelhhee p tp tp tp tp tp tp tp tpp hemhemhemhemhememhhemhemhh ununnununununuuunnderdderderderdererdderdederderderd rrrstastattstattstastastastastasttaasttastssstsstss dndnd ddnd ddnd dndndndnndnnd worworworworwowoowowowowoworowoworo k ok ok okk ok ok ok ookkkkk n sn sn sn snn snn sn snn siteiteteteitetetiteiteiteee a ananananananana an anaaa d dd dd dd dd dd dd ddd dd dd dd ddd ddddeteeteeteeteeeteeteeteetete rmirmirmirmirmirmirmirmrmrr ne nene nenene neneneeoptoptoptptptoptptptpptooppop imaimamaimaimaimaimaimaiimimimmiimimammi l al al aaaal aaaal aaal accecceccecceccecccecceccecccccecec ss.ssssss.ss.ss.ssssssss.ss ThTh Th Th Th ThTThThThhTh T e ce ce ce ce ce cce cconsonsonsonsonsonsssoonsnnnonssnsstrutruttrutrutrutrutrutrutrutruurtructictictictictictictictictiction ononon on on ononoon teaeateateateateateaeateateaateteateeae m’sm’sm’sm’m’sm’sm’smm’smm ss re re ree re rereeer latlatlatatlattttlatattionionionionionionnshishishishishishhshsshssshh p p p pppwitwitwitwitwwitwwitwwitwiw th th th th tth th th th he he he he he hehehe hehe hehe firfi rfi rrfi rfi rfi fi rfi fi fi e fififie fifie fifie fie fie fie fie fie fieeee ghgh gh ghgh ghgh ghghghgggggg tertertererterterterteeree s ps ps ps ps ps ps ps pps rovrovrovroroovrovorovrovrovrovroroved ed ed ed ededed ededed eded tototo toto toto ttto to to be be bebe be be be bebe bebbeeeb a ba ba ba ba ba ba ba ba ba onuonuonuonuonuonuonuuonuuuonuuo us, s, sss,s, ss, , sss whewhewhewhewhehwhewhewhewhehwhewhehhewhewhewhwhewhehewhehew n tn tn tn tn tn tnn tt tn n heyheyheyheyheyheyheyheyheyheyhehehheyheheyywerwerwerwerwewewererwere ae ae ae ae aae abblebleblebleblebleblebleblee toto toto to toototoot sp sp sp sp sp sp spspppot ot ot otot ot ot otottoo a fia fia fia fia fia fia fia fia fia fia fi rere re rere re re rere ree in in in in in inininin innnnn a aa a a a a a aa fiefiefi efi efi efi efi efi efififi efi eeeld ld ldldldld ld dlld d sevsevsevsesesevsevsevsevseveveveraeraerareraeraeraeraeraraeral kl kl kl kl kl kl kl kkiloiloiloiloilooiloiloilometetmetmettmetmetmetmetmettmm resresresresresresresesesrresr awaawaawaawaawaawawawawawawaaawaawaawaaawaawaawaawaawwawwwwwawaaayyyyyy,yyy, y,y,y,yy, yyyy,y,y,y,yy andandandandndanndanannandandandndandandddddddddnaa al alalalalaalll ala al alaaaaaaalaaalalalerterterterterterterttteertertertertrtreeerrerere th thththththhththht th thtt e fie fie fie fie fie fie e fie fie fie fiee rere re re re re rere re se se se se sese sese sesservirvirvirvirvirvirvviviviviivivivicececececece ceeecee ece pripripripripriipriprpriprirpp or ororor oror rororoo tototo totoototootottoo thetheththethethethethehetheththethh fi fi fifi fi fifififi fifi fi re re reeeere reee re rere sprsprsprsprsprprspsprsprsprsprsprsprssprsprsprsppsprpssprspp eadeadeadeadeadeadeadeadeeaeaeadee ddingingingingingingingngggggg......

Local RelationshipsLocal Relationships

Community SpiritCommunity Spirit

Investment Investment Confi denceConfi dence

Caring for the Caring for the EnvironmentEnvironment

04

Financial PerformanceTrustPower’s consolidated underlying earnings after tax excluding fair value movements on fi nancial instruments, which are inherently volatile, and prior year adjustment for change in tax rate was $118.8 million for the year ended 31 March 2009. This represents an increase of 28 per cent compared with $92.6 million for the same period last year.

Earnings before interest, tax, depreciation, amortisation and fair value movements on fi nancial instruments (EBITDAF) grew by 25 per cent to $260.0 million from $208.0 million in the previous year.

Profi t after tax attributable to the shareholders of the Company was $105.1 million compared with $98.1 million for the prior year. This includes the impact of fair value movements on fi nancial instruments and prior year adjustment for change in tax rate.

Operating revenue of $785.4 million increased 15 per cent on the previous year as a result of higher energy prices charged to those customers paying spot market prices through the fi rst half of the year together with a $17.0 million revenue contribution from telecommunication services, $8.4 million from sale of carbon credits and $24.2 million from the Snowtown Wind Farm in South Australia.

Operating expenses including energy and line costs increased 11 per cent on the previous year, primarily driven by higher wholesale electricity costs during the fi rst half of the year.

Total electricity volume sold by the Company in New Zealand was 4,032 GWh compared with 4,540 GWh in the year to 31 March 2008 mainly due to the restructure and volume reduction of a large industrial contract. Customer numbers increased to 227,000 at 2009 year end from 222,000 a year earlier.

The New Zealand electricity market was volatile through the fi rst half of the 2009 fi nancial year with a combination of low wind production, low hydro infl ows and reduced HVDC transmission capacity causing signifi cant increases in wholesale prices. The major South Island hydro storage

lakes remained at lower than average levels through until September 2008 which elevated wholesale electricity prices for a number of months.

While TrustPower was negatively impacted through the fi rst quarter because of these market conditions, it was favourably impacted in the second quarter due to high infl ows into its own catchments which enabled the Company to run its hydro generation plant strongly during a period of high prices.

The second half of the fi nancial year has seen above average infl ows into key South Island hydro catchments and storage levels being quickly replenished and remaining at above average for the remainder of the fi nancial year. Consequently, wholesale electricity prices have fallen signifi cantly.

The Company’s New Zealand generation production of 2,127 GWh for the year was up 5 per cent on the previous year but around 190 GWh down on expected long term average. Total hydro production was up 96 GWh (7 per cent) on the previous year due to signifi cantly higher North Island hydro production (up 204 GWh or 37 per cent) off-set by a 107 GWh (12 per cent) decline in South Island hydro production. Wind production was up 2 per cent on the previous year but was down 11 per cent on expected long term average performance. Most of this shortfall occurred in the autumn months of the fi rst quarter.

Below average wind production during the third quarter from the Snowtown Wind Farm contributed to a 16 GWh (6 per cent) lower than expected output for the 2009 fi nancial year of 254 GWh. All 47 turbines have now passed fi nal acceptance testing under the turbine supply contract. TrustPower is pleased with the successful execution of the fi rst stage of this wind farm which is the Company’s fi rst project constructed outside of New Zealand.

Following the introduction of International Financial Reporting Standards (“IFRS”), the accounting standards require that certain changes in the fair value of fi nancial instruments be refl ected in the Income Statement.

Directors’Report

Bruce HarkerBE(Hons) ,

PhD (Elec. Eng) , MIPENZ

Chairman

TrustPower / Annual Report 2009 / 05

Deep StreamDeep StreamOtago

06

TrustPower utilises various fi nancial instruments to hedge electricity price risks, foreign currency risks and interest rate risks to which it is exposed. While the Company utilises valid economic risk management instruments to hedge these risks, these instruments must also meet the stringent criteria prescribed under IFRS in order to qualify for hedge accounting. For those instruments that do not qualify for hedge accounting, the change in fair value is recognised in the Income Statement.

The fi nancial instruments in TrustPower’s portfolio that do not qualify for hedge accounting are mostly interest rate swaps and Energy Hedge Market transactions. Due to the signifi cant drop in long term interest rates in both New Zealand and Australia over the second half of the fi nancial year there has been a signifi cant fair value reduction in the interest rate hedge portfolio.

Return on average equity, adjusted for fair value movements on fi nancial instruments but including the impact of the revaluation of generation assets was 8.8 per cent (last year 7.9 per cent).

Group operating cash fl ow was $214.2 million for the 2009 fi nancial year versus $161.0 million in the previous year.

Taking into account the shortfall in production from the Company’s own generation assets and volatile wholesale prices in the fi rst half of the fi nancial year, the result was good.

The governance of energy trading and oversight of risk management continues to be a focus. Inherently a company with 100 per cent hydro and wind generation assets will have some periods with below average generation and at times, this will occur with some correlation to when New Zealand’s major hydro catchments are also dry. TrustPower’s geographic diversity of asset location moderates this variability considerably but it does not eliminate it. TrustPower’s risk management policies aim to assess these inherent risks and ensure that fi xed priced contracted sales to customers are in line with the Company’s own generation capacity and externally contracted generation with only a manageable level of residual risk.

Financial PositionTrustPower’s balance sheet as at 31 March 2009 remains in good shape. Shareholders’ funds have increased to $1,430 million from $1,257 million.

TrustPower has a policy of independently reviewing the value of its generation assets at least every three years. The last valuation was completed as at 31 March 2007. However, IFRS require that key valuation inputs are re-examined annually and if there has been a material change then a revaluation must be undertaken.

TrustPower has determined that there have been material changes in forward electricity prices which warrant a revaluation being completed. Additionally, a number of generation projects were completed since the last revaluation namely, Tararua Stage III Wind Farm, Deep Stream hydro and the Snowtown Wind Farm. Consequently, Deloitte Corporate Finance has independently valued the Group’s generation assets as at 31 March 2009.

The fi nancial impact of the revaluation has been an uplift in generation asset values of $259.7 million. $204.1 million has been accounted through the revaluation reserve in equity with the balance of $55.6 million accounted as an increase to deferred tax liability.

Debt (including subordinated bonds) to debt plus equity was 33.9 per cent at year end, including the

impact of the revaluation of generation assets, versus 34.3 per cent in the previous year.

TrustPower continues to maintain high levels of committed credit facilities. Including subordinated bonds the Company currently has NZD equivalent of 1 billion of committed debt funding in place. As at 31 March 2009 Group net debt was $705 million. Given the ongoing uncertainty in fi nancial markets the Company has recently accepted refi nancing offers for $100 million of bank facilities due to mature in July 2009 together with a $20 million increase. These facilities have been extended to July 2011.

Capital StructureDuring the fi nancial year TrustPower successfully raised $100 million of seven year subordinated bonds from retail investors. TrustPower is one of only three corporate issuers that have successfully raised subordinated debt over the last two years and this achievement is testimony to the Company’s investment brand and conservative capital structure.

The Company purchased 236,312 shares on market at a weighted average price of $6.91 over the period October to December 2008 in accordance with the Share Buyback Programme approved by Shareholders at the last Annual Meeting.

Generation Development and Capital ExpenditureGood progress has been made on a range of growth options in New Zealand and Australia.

TrustPower currently has consents for 420MW of wind farm development in the South Island and is well advanced with a further 118 MW of South Island hydro consents at Arnold and Wairau.

In Australia, the TrustPower Group has planning consent for up to another 235 MW of capacity at the Snowtown Wind Farm and is awaiting approval for an extension to the 48 MW Myponga Wind Farm planning consent.

TrustPower is progressing negotiation with a small number of parties that have appealed the Arnold consent with the objective of avoiding another costly Environment Court process.

The Wairau consent appeal will inevitably go through an Environment Court process and a hearing has been scheduled for October 2009. The Company is undertaking further analysis in preparation for this process.

Good progress is being made in reaching agreement with landowners for potential wind farm developments at a number of New South Wales, Victoria and South Australia sites.

Forecast capital expenditure in the 2010 fi nancial year is expected to be around $38 million which includes generation expenditure undertaken as part of the Company’s 10 year asset management plan, small hydro enhancement projects and implementation of the Company’s new customer care and billing system.

Generation development costs to be expensed in the 2010 fi nancial year are projected to be around $7 million continuing the high level of investment in growing the Company’s portfolio of investment options. TrustPower is working to ensure that it is in a position to progress renewable projects should the Company conclude that shareholder value is likely to be created.

TrustPower / Annual Report 2009 / 07

SustainabilityTrustPower is fi rmly committed to sustainability principles and progress in relation to achieving its sustainability goals is provided in this annual report.

TrustPower takes its environmental obligations very seriously and has detailed systems and focussed resource in place to help manage compliance with its ever increasing level of consent conditions.

Pleasingly, TrustPower continues to report only a very small number of minor non-compliance events and none of these events have resulted in any signifi cant adverse environmental consequences.

TrustPower continues to invest heavily in its Community Awards Programme. This year the National Awards were held in Palmerston North and once again there were a number of outstanding examples of voluntary work being undertaken in communities throughout New Zealand.

In addition to the Community Awards Programme, TrustPower has a portfolio of other sponsorship initiatives regionally targeted at assisting education, the arts and wider communities through support of school music festivals, youth orchestras, photographic competitions, the Bay of Plenty rescue helicopter in association with the Tauranga Energy Consumer Trust and signifi cant regional events that are of benefi t to the wider community.

Regulatory IssuesThe Government is undertaking a review of the climate change legislation. A government select committee is due to report to Parliament shortly and the Government has advised that it intends to have an amended Emissions Trading Scheme (“ETS”) enacted by September 2009. However, the Government has also indicated that it would like to see harmonisation, where possible, with the proposed Climate Pollution Reduction Scheme (“CPRS”) that the Australian Government was targeting to introduce by July 2010. The Australian Government recently announced that the introduction of the CPRS will be delayed to mid 2011. It is likely that the CPRS will not be approved by the Australian Senate without the support of minor parties. This could cause further delays in fi nalising an amended ETS in New Zealand.

The Australian Government has announced that it will increase the Mandatory Renewable Energy Target (“MRET”) from 9,500 GWh per annum to 45,000 GWh by 2020 and for the scheme to remain in place through to 2030. The extension of this scheme will support new renewable energy development in Australia, in particular wind development which is currently viewed as the most economic renewable generation option. Legislation is expected to be passed to extend the scheme by July 2009.

On 1 April 2009, the Minister of Energy and Resources announced that there will be a ministerial review of the electricity market. The stated objective of the review is to improve the performance of the electricity market and its institutions and governance arrangements. The review will consider the fi ndings of a number of recent or upcoming reviews and investigations including the recently released Commerce Commission report on wholesale market competition. A Technical Advisory Group of six experts has been appointed to support the review process and advise the Minister. A discussion paper is expected to be provided to Cabinet in June and released for public consultation in July. Any legislative change arising from the review is expected to be enacted by June 2010.

DirectorsIn accordance with the Company’s Constitution, Mr Michael Cooney, Mr Geoffrey Swier and Sir Ron Carter will retire at the 2009 Annual Meeting and being eligible offer themselves for re-election.

In January 2009 Mr Lloyd Morrison took leave of absence from the Board due to health reasons. The thoughts and best wishes of the Board and the team at TrustPower are with Lloyd and his family as he takes the time to focus on his health. Mr Marko Bogoievski, Chief Executive of Infratil, has been appointed as an Alternate Director during Mr Morrison’s leave of absence.

AuditorsPricewaterhouseCoopers has indicated its willingness to continue in offi ce.

DividendThe Directors are pleased to announce a fi nal dividend of 17 cents per share, partially imputed to 9 cents per share, payable 8 June 2009 (record date of 29 May 2009). This together with an interim dividend of 16 cents per share provides a total payout of 33 cents per share for the 2009 fi nancial year compared with 30 cents per share for the 2008 fi nancial year, representing dividend growth of 10 per cent. The Company anticipates ongoing growth of normal dividends.

The Company also paid a 10 cent unimputed special dividend in December 2008. The Directors have approved a further unimputed special dividend of 10 cents per share with the same record and payment dates as the fi nal dividend. The Company believes that following the payment of the fi nal and special dividends it is positioned to pursue growth opportunities.

OutlookNew Zealand hydro storage is currently well above average for this time of year and TrustPower’s hydro storage lakes are also at above average levels. The current New Zealand hydro storage position should ensure a comfortable level of electricity supply to meet demand over the 2009 winter.

TrustPower believes that New Zealand’s signifi cant wholesale and retail price rises, driven initially by the end of the era of cheap gas and more recently to cover costs of moving to a renewable generation future, will moderate somewhat but price rises above infl ation are still likely for a period, especially as New Zealand dollar weakness will refl ect into the costs of new projects. While modest demand reduction may occur due to current recessionary conditions and new generation may be deferred due to recent capacity increase providing a suffi cient supply buffer, we expect this situation to be of short duration.

While it is too early to make predictions about the 2010 fi nancial year, it is worth noting that the Company is well positioned to meet its customers’ needs and to pursue further development of electricity generation assets when it is economically justifi able.

BJ HarkerChairman

08

Financial PerformanceThe Directors’ report sets out the detailed fi nancial results, but of particular note is the increase in EDITDAF of 25 per cent, the like-for-like adjusted net earnings increase of 28 per cent, and the Group operating cash fl ows increasing by 33 per cent to $ 214.2 million compared to last year.

The year has been especially challenging, with winter 2008 being one of the worst in recorded New Zealand hydro history. Our geographically diverse generation portfolio certainly assisted us to manage our exposure to high wholesale prices, but with both the North Island and South Island hydro catchments drying up at the same time, we suffered earnings losses in the fi rst quarter of the year. The second quarter saw our hydro lakes begin to replenish while the big lower South Island lakes remained comparatively dry. This allowed our fi rst quarter losses to be recouped plus some, setting the Company up for a good result. A full year of the Tararua Wind Farm Stage III, the progressive commissioning of both the Snowtown Wind Farm in South Australia and the Deep Stream hydro scheme in Otago contributed to the year’s earnings growth.

Our CustomersDuring the year, the opportunity arose to secure additional residential customers, particularly in the Dunedin and Southland markets, when a competitor announced signifi cant power price increases coupled with a proposed increase in fees to Directors. We also secured the electricity output contract for the Ngawha

geothermal power stations in Northland, allowing us to secure nearly 5,000 new customers in the local area.

There was strong competition for customers across most of our markets during the year with 11.5 per cent of customers nationally changing suppliers. Our customer losses were 21,073 customers or 9.6 per cent of our total customer base, pleasingly less than the national average.

Customer service standards were enhanced during the year with average Call Centre grade of service increasing from 62 per cent to 78 per cent (target 80 per cent), and our Company was again acknowledged as the top customer service performer in independent service research surveys of electricity retailers.

During the year a large industrial customer chose to purchase their electricity directly from the wholesale market instead of through our Company, which reduced industrial market sales by 587 GWh. Sales to residential and commercial customers increased by 78 GWh or 2.6 per cent.

Additionally, during the early winter of 2008, the electricity industry proactively and collectively called on consumers to save power resulting in our sales volume being reduced by about 5 per cent over that two-month period.

Our Kinect telecommunications brand has continued to grow during the year, with total sales topping $17 million. The Kinect brand not only allows us to offer our electricity customers an alternative service on their one monthly bill, but it also provides a great sales team resource which can swap from selling telecommunications product to winning new electricity customers at a moments notice when opportunities arise.

Chief Executive’s Report

The global economic crisis is placing signifi cant stress on the New Zealand economy, businesses and individuals. Our strong balance sheet, service oriented retail brand, investor confi dence and electricity sector focus places our Company in a good position to weather this economic downturn.

Keith TempestBBS

Chief Executive

TrustPower / Annual Report 2009 / 09

Tararua Wind FarmTararua Wind FarmStage III

10

Generation DevelopmentDuring the year the 99 MW Snowtown Wind Farm Stage I in South Australia was progressively commissioned, and offi cially opened by the South Australian Premier in November 2008. This project was the culmination of several years of investigation and research into the Australian electricity industry. The Australian electricity industry and regulatory environment is quite different to New Zealand, and we wanted to adopt a cautious and risk averse approach to this ‘beach head’ into Australia. A ten year power purchase arrangement with a large Australian electricity retailer secures the sale of 90 per cent of the Snowtown Wind Farm’s current 99 MW output. The site has future capacity for a further 235 MW of wind generation. Another consented site south of Adelaide is capable of hosting a 48 MW wind farm, and we have signed land access agreements on a number of potential sites in New South Wales, South Australia, and Victoria.

We commissioned the 6 MW Deep Stream (Otago) hydro scheme during the year, after a number of minor teething problems during commissioning. This scheme is very innovative in terms of its design and construction, with almost all components being New Zealand made, including the turbines and buried fi breglass penstocks. The scheme required the creation of a large lake behind a 19 metre high earth dam, and all the disturbed areas have been replanted using local native tussock.

The proposed Mahinerangi Wind Farm (Otago, 200 MW) and Kaiwera Wind Farm (Southland, 240 MW) are now fully consented. The Arnold (West Coast) and Wairau (Marlborough) hydro developments are both consented at Council level but subject to the Environment Court appeal process.

Looking forward to when New Zealand has a large number of wind farms, wholesale electricity prices may become more volatile - especially on windless days. We have identifi ed over 50 enhancement opportunities involving our existing hydro schemes, which have the potential to either increase lake storage, increase plant capacity or both. Most of our hydro schemes were built to provide ‘peaking capacity’, in that they have high output capacity relative to the stored water available, as a consequence they are ideally suited to a volatile wholesale electricity priced market.

We are also investigating opportunities for combining electricity generation with rural land irrigation, especially in areas where water storage is available and where the soils are dry but fertile. We have identifi ed Canterbury as having signifi cant potential as an ideal location for a large-scale electricity generation / irrigation project.

Existing Generation PortfolioThe 2008/9 year was particularly dry, and not particularly windy, resulting in our overall production being 190 GWh below long term averages, although 5 per cent above last year through the addition of new capacity.

During this last year New Zealand also faced a number of signifi cant and often quite long duration transmission fault outages, which shut down large parts of major metropolitan areas seriously inconveniencing businesses, transport, communications and households. At the same time, National Grid owner/operator Transpower and the Electricity Commission have been working hard to establish a far-reaching investment programme to improve the reliability and capacity of the national grid.

We are also very mindful of the necessity to maintain our own generation plant and electrical infrastructure to minimise the likelihood of failures. A comprehensive ten year asset management plan was implemented several years ago, and is updated on an annual basis. The Plan monitors and identifi es in advance plant and equipment that will require refurbishment or replacement. One of the measures we have used to monitor the outcomes from the Plan is failed start statistics. Failed starts measure the number of times our hydro generators don’t work when we require them to. In 2000, our hydro machines failed to start on average one time in every 133 attempts. In 2009 that fi gure has reduced to just one time in every 564 attempts, equating to 37 failures out of 20,873 machine starts. Back in 2000 most machine starts were performed manually by staff at the station, but now they are all controlled electronically from our control centre at Mount Maunganui.

Government Strategy and RegulationIt is interesting to note that TrustPower has continued to grow and prosper regardless of the continual uncertainty around successive Governments’ energy sector strategies and regulations. Each year in our Annual Report we explain the pending changes in Government Policy and proposed regulatory reforms, but to date they have had little impact on our business. What they do impact on however is the timing of new investments and the diffi culties and costs of bringing new investments to fruition.

The Resource Management Act has posed a signifi cant and costly hurdle, especially to our hydro development projects. Despite this, we have successfully negotiated those hurdles with 100 per cent success to date.

The existing Government Policy Statement and Energy Strategy have been amended or ignored by the recent incoming Government, and a review panel has been established to again look at the electricity sector. The Emission Trading Scheme legislation has been put on hold while a review is undertaken. The Electricity Commission’s roles and responsibilities are being reconsidered, and the Commerce Commission’s review, following a lengthy investigation, has recently been made public.

We consider that while continuing to have maximum exposure and input into Government strategy and regulation, we are best to focus on enhancing the long-term value of our company, and delivering improved returns to our stakeholders.

The Community and the EnvironmentWe continue to place a signifi cant focus on both our customers’ communities, and the natural environment surrounding our generation assets.

Our fl agship TrustPower National Community Awards programme touches tens of thousands of people each year in the 23 regions where the programme is run.

A full year of the Tararua Wind Farm Stage III, the progressive commissioning of both the Snowtown Wind Farm in South Australia and the Deep Stream hydro scheme in Otago contributed to the year’s earnings growth.

TrustPower / Annual Report 2009 / 11

The programme recognises volunteers and the vast array of activities in which they are involved. In addition, we also support a wide range of community activities where we can assist local organisations maximise the contribution from their own initiatives to their local community.

We work closely with Government and local environmental agencies to ensure the fl ora and fauna in the regions hosting our generation assets are protected and enhanced.

With over 3,000 Resource Consent conditions to monitor and comply with, many being part of the daily generation dispatch decision processes, it was pleasing this year to record just fi ve breaches, all minor in nature. This number is half of those recorded in the previous year and less than one quarter of prior history. Previously I mentioned the vastly improved asset maintenance programme and reduced incidences of failed starts. Breaches of consent conditions often result from plant failure with water being either released or not released as a direct consequence of that failure. Our focus on reduced plant failure has effectively been a win-win, resulting in enhanced fi nancial outcomes while at the same time reducing incidents that result in breaches of resource consents and the potential for adverse environmental impacts.

Looking AheadHistory has shown that a combination of our strategic, yet risk averse, approach to development, our unique geographical spread of well maintained and managed generating assets, our careful development and nurturing of key internal and external relationships and our competent, well trained and well engaged people have together given TrustPower the ability to consistently outperform our competitors.

In a diffi cult international fi nancial environment, where there is the added challenge of potential regulatory and market environment changes, we are confi dent that our Company’s strengths leave us well placed to continue to deliver the outcomes and results that all of our stakeholders, including shareholders, have come to expect from us. Indeed, the culture of our Company is such that we look ahead with confi dence and excitement about our future.

Keith TempestChief Executive

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Call Centre Grade of Service

Grade Achieved

Target

Apr 08 May 08 Jun 08 Jul 08 Aug 08 Sep 08 Oct 08 Nov 08 Dec 08 Jan 09 Feb 09 Mar 09

Trend

Failed Starts

2004 2005 2006 2007 2008 20090.00%

0.25%

0.50%

0.75%

1.00%

% of attempted starts that fail

12

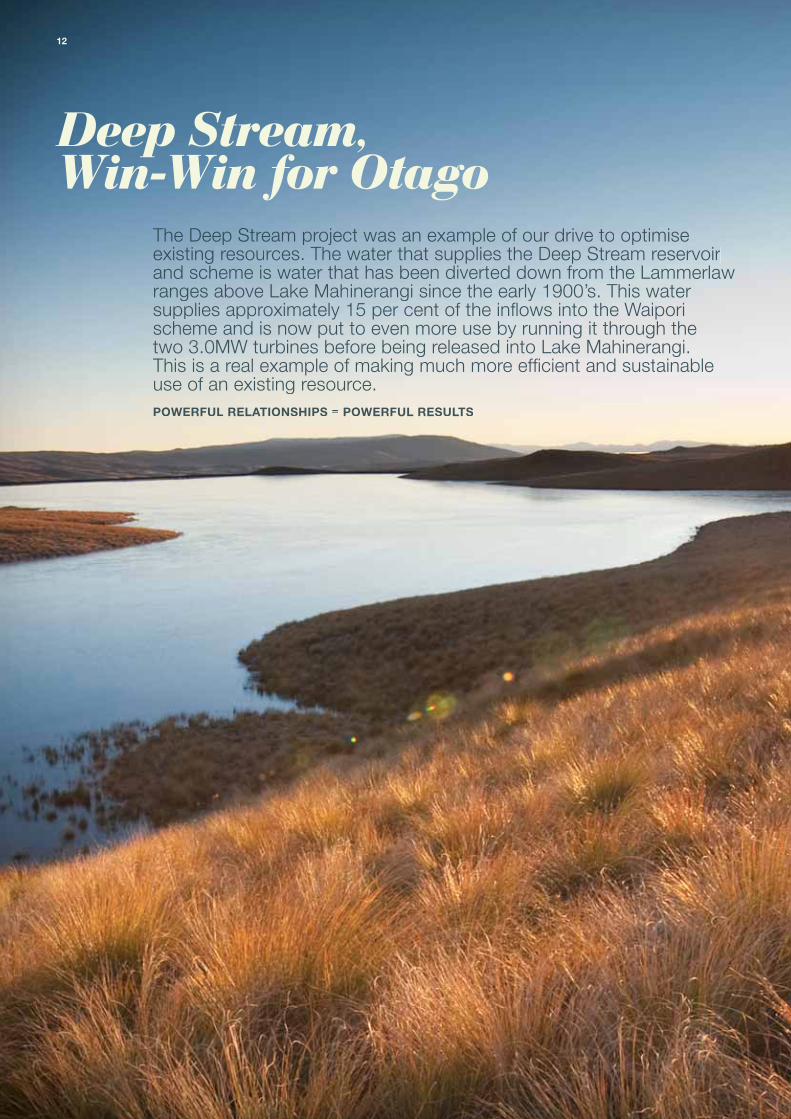

The Deep Stream pprroojjeecctt wwaas an example of our drive too ooppttiimmiissee existingg rreessoouurrccees. The water that suppliess tthhee DDeeeepp SSttream reservoir aanndd scheme is water that hass bbeeeenn ddiivveertted down from the Lammerlawranges above Lakkee MMaahhiinneerangi since the early 1900’s. This water supppplliieess aapppproximately 15 per cent of the infl ows into the Waiporischeme and is now put to even more use by running it through the two 3.0MW turbines before being released into Lake Mahinerangi.This is a real example of making much more effi cient and ssuussttaaiinnaabbllee use of an existing resource.POPOWEWERFUL RELATIONSHIPS = POWERFUL RESULTS

Deep Stream, Win-Win for Otago

TrustPower / Annual Report 2009 / 13

Powering Dunedin

Successful AgreementsSuccessful Agreementsnd accessThoThoughugh ou our rr relaelatiotionshnshipip appapproaroach c we successfully reached lad lans ts to optimise agragreemee ents with Landcorp and City Forests, allowing all partiesese DeDepartmenttheir use of the land whilst protecting the existing environment. The oughohout theof Conservation and Historic Places Trust were also involved thro

he Blaack plaplanninning ng stastagesges to to en ensursure te thathat co consenservarvatiotion an nd preservation of thceived the d theRock Scientifi c Reserve and Historical and ArA hchaeollogiogiggggggg calc sites recneeenenenen dindindindin Ci Ci CC ty yCithihhihighighighighighighihighighighigighighighigghiggghighighighigghighhighighighighighighighh hhhhhhhhhhhhhhhhheshheshhheshhheshesheshhhhhesheshhhehesttttt pt pt pt p iiiiriorio ititrittrityy. ThrThThrThrougougougoughouhouh t ct ccononsonsonstrutrut ctic on on extextextenennnsensnsenen iveiveveveee lilili li lililiiaaaiaiaisaissaaissisonnn nnon o witwititwwitwitwitwitwitth Dh DDh Dh Dhh h hhh uuurerereeeeeeeeereererrrrrrr dd ddddCouCCouncicil, l, CluCluthathaa Di Di Distrstrstrstrictictictct C Co Co Councu cu il il andaandandan OtOOt O agoagoagoagoogo R R ReReReeeR gigigiogioigiog onalnalalalalnalan CoCoCoCoCCoCoooouncuncuncncuncuuncncuuu ill eensensnssensssnsuurururururuuu

comcomcomplipliancance we wwithithithh rururururulesleslesleses an an aand td td td td hehe hhe raprapidid id id rrresreressessoluoluoluoluoo ttiotiootiotionnn n on on oof iff if if if iissssussussussusssss ues.es.ses.eseses

Made in Made in New ZealandNew ZealandThe Deep Stream project was built using a 100 per cent New Zealand labour force, with a total of 15 contracts over the construction period resulting in the employment of between 40 and 70 people at any one time in environmental, engineering and construction disciplines. During construction and commissioning periods there was a high use of people from within the greater Dunedin and Clutha districts, providing employment and revenue directly to the area. A highlight for TrustPower was our ability to purchase high effi ciency turbines from two Christchurch fi rms, HydroWorks and Mace Engineering. These units were designed and customised to TrustPower’s specifi c operating requirements, and constructed to a very high standard.

CCCCCiCiititttttCittCiCitittCC ttCCiCitCCCCiCiCitittCCCiitCCiiitC tCiCitty Cy CCCy Cy Cy CCy Cy y Cy CCCCCy Cy CCCCCCCyyyyyyyy ooounoounununnoounnoounoununooounounoooouoouoouununnounoounno ccilcilcilcilcilccilcililcilcilicilc ( ((D(D(D(D ((D((D((D(D ((D(D ((D(DD(D((DD(DD(((( CCCCCCCC)CC)CC)CC)CC)CCC)CCCCCCCCCCCCCCC)CCCCCCCCCC )))))))) w w weeeewe weweewewew we weweewewe ThrThrThrThrThrThrTThrThrThrThrThrThThThrThTh ouoououougougougougouougougouoo gugugugougoouououguggo gh oh h oh oh ooh oh h h oh h oh oh ooooooouuuur urururuur ur uruuuu relrelelrerelrelrelrelelrrelellatiatiatatiatiatiatiatiatiatiatiiat onsonssssononsonsonsonsonsonson hiphiphiphiphhhipppphhhiph pppp wi wiwi wi wiwiwiwiithththththth th ththhthhh thethehehethehethethethththethet DuDuDu Du Du DuuDuDDDDDD neneneeddededneennneneneednnneedededinnnnininin ninn Cbbbbbbbbbbbblllllle llllele e le lelelelelee aarrarrarrarrarrrrrararrarrarrarrarrrarrarraaananangggggggangangngngangangngngngganaananngaanannnnngangeeemeeememememeemeeeemeemeemeemeemememeemeemeee tttttnttnt tntnttnt ntnnt nntntnt t n fffffffforforforforfforforfofofofoforrfoforrf ttthhhttthhththtth hhtththh ththhthth t ttht lle lle lle le lee lle le leaeaseaseaasasssasssseeaeasassaseasasssssee see eeeee ee e e e eeeee werwerwerwereree ae ae ae ae bleblebleblebleb tot too cocococome mem to to oo a mma mmutututuutuuttualallally ay aayy grgrgregregrererregrgrreeabeabeababbbbbbeabbeabblllllll

dadad d ddadaaadadaddaammmmmsmmms,ms,ms,mms,ms,ms,s,s,ms,mm ,mm la lalala la laa la la laake kke kkke e kekekkkk andandandnanddddndananandanandandnnandn ssosoo sossooosoooomememe mme me me memem cancancancancancacacacancancancanccacancancancan lalsalsalsalsalsalsalsalslalsalsalsalsalsa sa ofof fofff thethethethethee lalala lalaland ndnd nnnd on onnonon on on no whiwhiwhiwhiwhiwhiwwhiichchch ch ch ch chc thethethethethethetheheeeeeee DeDeDeDe DeDeDeDD DDD ep epep ep ppppep ep p StrStrStrSStrStrtrStrtrStrreeeeameamamamamamee maaameamm d d ddddddnnnnnnnnnn th t t tthhhhthhh tthhtttheee e e e DDDDDDDDee DDDDe e e CCCC CC CCCCCCCC CCCCCCCCCCCC domdomdomdodomdododododdd mod estestesteststesttsteststttsttsstse ic icic ic cc c icicicccciciccicicc watwatwatwatwwatwatwwawatwatwwawatwawatwatwatawatawwaawwaa er er ererreeer eeeer ee supsupsupssusupupupupsupssususussuppppplyplyplyplyplyplyplyplyplyplyplypplyylyylyplylyplyyy wwerwerw rwerwere be be be be be be be bbuiluuuiluiiuiluiluiliu tt. t. . TheThTThTheTheTheThee la lalala lake keke keke ee isis is is sitsitsitssituatuatuatuatated ed ed ededed wiwitwitwitwitwiww ttttttw hinhinhinhinhinhinhinh n

terererererterterererrerterermmm m aaaaam aammm m ammm amm aam aam aaaaccccccccccccccecceccccccecceccceeecceccecceccec ss,ss,ss,ss,ssss,ss,ssssssssss,sssssssss,ss,ss,s,,,s, TTT Tr TrTr Tr Tr Tr TrTrTTTTTTTTTTTTTTT ustustustustuustustustustuu ttttPowPowPoPowowwowPowPoPowowwP wP weereerer er er ererrrrrrr maimaimaimaimaimaimmmaima ntntntntantantatatataanntanntatanttataaaatn aaattnt insininsnsinsininsinsinsnssssssnsnnnnnnnns catcatcatcatcatcc ttc chmchmchmchmchhmchmhmchc mmmmmententeenententtntntntntn an an annn anananaaaaa d id id id id d n rn rn rn rretetuetuetuetut rnrnrn rn forforforforfororfooooo lo lo lo lo lololololoong nng g gng ngg g ngngngng teteteteesusuupupupupupsuuppupupuppppppplyplyplplypppplyplyplyplyplyplylyyyy fo fofofofofofofoffff fo fofffoff rr r tttttr tr ttttr rr tr ttr hhe he he he hehe he heheeheh DCCDCCDCCDCCDCCDCCCDCCDCCDCCDDDDD . . B. B BBBBBB. B. . othothothothothothhththtot pa pa ppapapapappapapaaartirtirtirttitititititirties es eeees eeeeeeeees s ss hhavhavhahahaavhavavavvvhavavhavvhahaavhhahaaaahhh ee ee ee ee eee eanaaanan an aanaaaan on on on onon nnn ccccalcalcalcalcalccalcalccccall el el el eeeemermermermermmermermmm gengegengengengengengeengenegennncycccy ccy cy ccy cy watwatwatwatwattatwatwatwawwawa eeeeer er er eee ssssupssususuuususuu

e e ccrecrecrrererecrererecreeecrcrrrerrerreccr atiaaatatiaatiatiatiatiiia iit on ononon on on on oooon onooonoooono of of of of ofof of of of of of foooooooooooooooo wwwwwwwatwaatwatwatwatwatwatwwwaaawww ter er er erreeeeeerer stostostostoststostostostotostotostostostostotostotttttttttttorrragragragragragragragragragragrrrragragge fe fe fe fe fe ffe fe fe fe e fe fee e ffe orororororoor oroorror r botbobotbotbotbotbootbotbotbottttttth gh gh gh gh gh gh gh gh gh gh gh gh gh gh gh h ghhhh h hhh ghhhhh gh gh ggggeneeenennneeneeneeeeee eeeneeee ennnnnnn ratratrararatratratatatratttrarrr tr tra iiioniononionionnonniononioi nionoo benbenbebenbenbenbeenbennebebebenennnnnnne efi efi efifiefi efi eeeee dtedtedtededtededddddeeededed gr gr gr grgrrrg eateateateateateateaatattatatttly ly ly lylyy frofrofrorom tm tm tttttm ttmm hhehehe he he hehehehhhe cccccccceeeeeeeeencyncyncyncyncyncyncyncycycyncncyyncyccc w wawa wawwawawwawawawaaawa waaaawwwawawaattttetereerrterertertererereereerrerrteterrr sss s susususususuussususuuuusu sssusuuuussuuss ppppppppppppppplpplppplppppppppppppp yy, y, y, y, y, y, y, y, y, yyy, at atatatttat at nononono nono ooonooonoooooooo coscoscososcosscosccoscososcososcoscoscosc st tt tt tt tt tt tt tt tttt ttt tt tttto to to to to tooooo to to to toooo ttthhe he he ee ehehehheehhehhee ratratraratrattratatratattratratrra epaepaepepaepaepaepaepaepaaeepeepaeeepaepppp yeryeryeryeryerereerryyerrryerryeryeryyyyy s.ss.s.s.s.s.ssssssss.aanandandnndndndandandandndndndnndddand th th th th ththththththhhe Ce Ce Ce CCe Ce Ceeeee Ce Ce Cityityityity’s ’s ’s’s ’s’ss emeemeemeememeemeemeemeee eem rgergergergergergegegeeeeeeennnnnnn

Protecting our Protecting our EnvironmentEnvironmentThroughout building and commissioning the Deep Stream hydro project our total focus on protecting the existing natural and historical environment, and ensuring any effects of the project were minimised. This ensured the scheme integrated well into the existing pastoral environment, and with the establishment of the new lake and waterways, new birdlife is now fl ocking to the area.

Benefi ts for Local Rate PayersBenefi ts for Local Rate Payers

DeeDeeDeeDeeDeeDe p Sp Sp Sp Sp Stretretrttrream has been buibu lt tosupupsupsupsupplelepp mmemenmennment tt tt thehe he exiexistitisting ng WaiWaiWaiporpopo i iHydH ddHyy roooo Electric Powwwer e SchS hhemee , whiwhwhiwhiwhichchchcchch proprovidvides es eleelectrct icicity ty dirdirectectly ly intntinti o oo o o D Duneunedindin Ci City.ty. It It de delivliversersrse addddaddditiitionanal el eleclectritricitcityy eequiquivalvalentententent toto to tosupsupsupupppppplyplypp iningngnngngngng ap ap ap apapppproproprop ximximximateatetetet lylyly y 3,03 03,03 00000 00 aveveveveeeeeeeragragragragge e Ne Ne New wew ZeaZeaZeaZealanlanlanland d hdd housousehoeholds, proproproproovvvvvvvidvivvidvidvidinginginging ad addditditditi ioniononalallal al aa secsecses uriur ty ty of osupsupsupppppplyplyplyply to to DuDuD dnedinin CitCitCCity wy wy hilhilst st

timmising the he useuse of waterer th that at hasasoptimmisbeeenen availablee to to t the mainalways s bee

eme.Waipori s schem

14

Board of Directors

Bruce HarkerBE( Hons) , PhD ( Elec. Eng ) ,

MIPENZ

Chairman

Michael CooneyLLB

Director

Sir Ron Carter KNZMBE( Hons) , ME,

DistFIPENZ, D.E ( Hons)

Director

Geoff SwierMCom ( Econ ) , MAICD

Director

Marko BogoievskiBCA, CA , MBA ( Harvard )

Alternate Director

Sam KnowlesMSc ( Hons)

Director

TrustPower / Annual Report 2009 / 15

Management Team

Keith TempestBBS

Chief Executive

Mike KedianBSc ( MechEng ) ,MSc ( Eng ) , MBA

Generation Manager

Karen BoyteBBS, MBS ( Hons) , MHRINZ

Human ResourceManager

Robert FarronBBS, CA , CFIPNZ

Chief FinancialOffi cer & Company

Secretary

Peter CalderwoodBE( Hons) , ME, MIPENZ

Strategic BusinessDevelopment

Manager

Therese ThornBE( Hons)

Trading & RiskManager

Chris O’HaraBAgrSc, Dip. Bus

Energy SalesManager

Nelson N TkatchBSc, BCom, ISP, HISP

Chief InformationOffi cer

16

About thisReport

The Reason for this ReportAt TrustPower we believe that producing an annual sustainability report is an essential part of being a good corporate citizen. This report provides a means of communicating with a range of stakeholders on the full range of our activities. Consistent with previous years we report on sustainability in conjunction with our annual report.

MaterialityTo determine which issues are of material importance, we considered issues that might impact our operations, the environment, the communities in which we operate, or substantially impact our individual customers and stakeholders.

Material measures are those identifi ed from stakeholder interaction (page 18) and key risks (page 17). By choosing these measures we have produced a report aimed at all stakeholders.

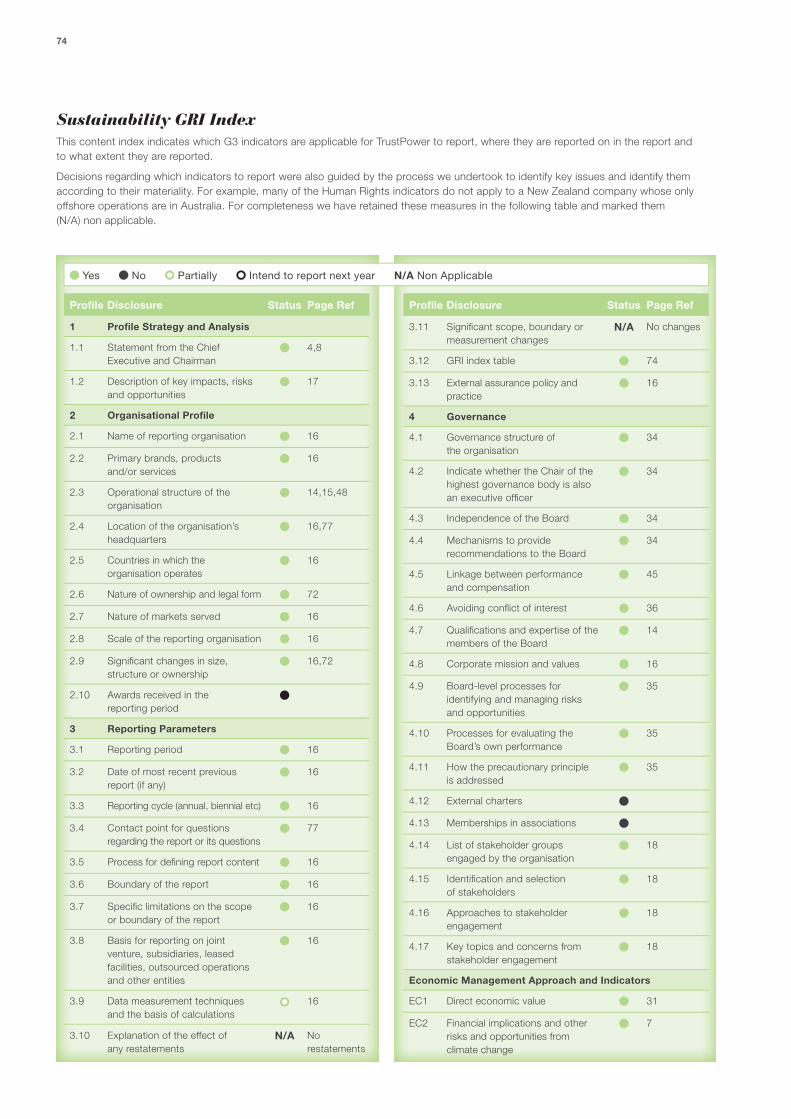

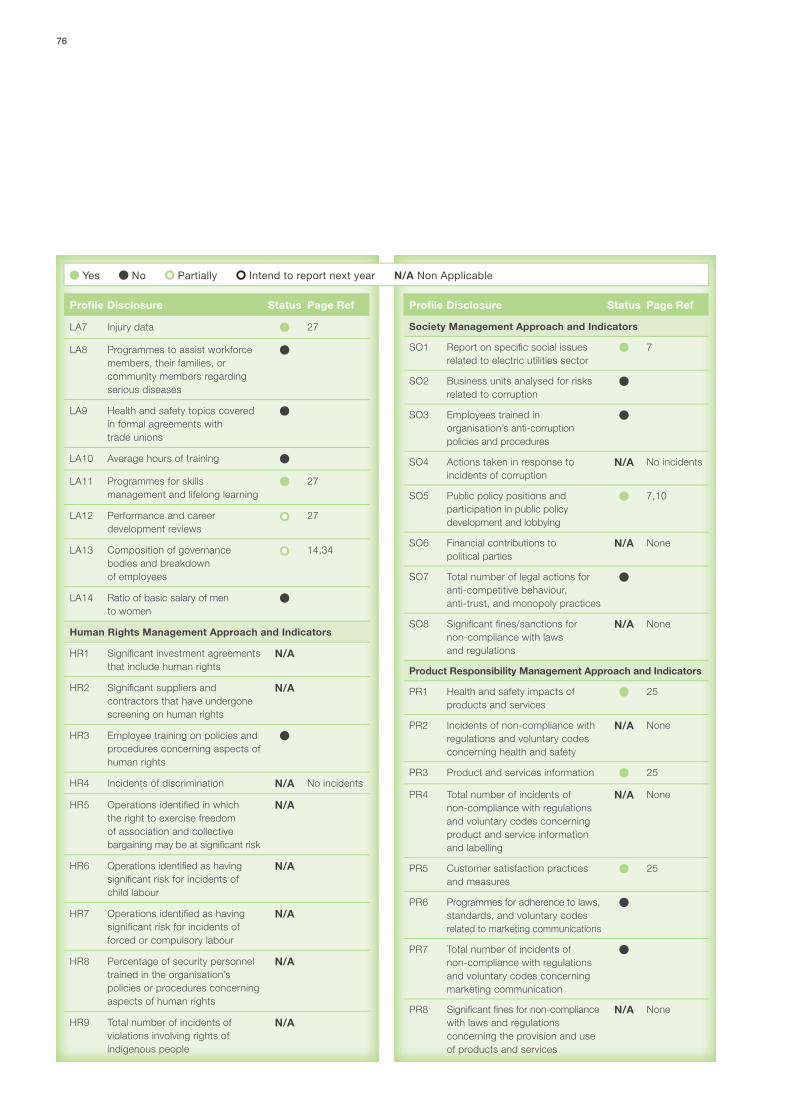

Sustainability Reporting GuidelinesThis Annual Report is available on our website, www.trustpower.co.nz and is compiled with reference to the Global Reporting Initiative (“GRI”) Sustainability Reporting Guidelines Version 3.0 (“G3”). We have assessed our compliance with the reporting guidelines at the Application Level (B).

The GRI guidelines provide a voluntary reporting framework used by organisations around the world as the basis for sustainability reporting. The GRI is the generally accepted framework for ‘measuring, disclosing, and being held accountable to internal and external stakeholders for organisation performance toward the goal of sustainable development’.

The GRI consists of a framework and guiding principles as well as a range of ‘indicators’ that reporting organisations can report against. Indicators are chosen on the basis of materiality or signifi cance to the business and / or stakeholders. Not all indicators are reported on in this report.

Pages 74-76 show the full list of G3 indicators, where they are reported on in the report and to what extent they are reported.

Reporting PrinciplesWe have reviewed GRI’s G3 Reporting Principles in an effort to provide a balanced and reasonable representation of our sustainability performance.

We have applied the key principles of materiality, completeness, context, comparability, accuracy, timeliness, clarity, reliability and boundary setting.

Reporting Period, Accuracy and CompletenessThis report is based on the performance and information for the fi nancial year to the end of March 2009. We use in-house reporting systems to collect data for the GRI process.

Boundary of the ReportThis report covers the operations of TrustPower and all of its subsidiaries. Outside the scope of this report are outsourced customer services and a variety of fi eld services contractors.

External AssuranceThe fi nancial statements have been audited by PricewaterhouseCoopers. Independent review of the Company’s impact on green house gases ‘carbon footprint’ has been completed by Landcare.

The remainder of the report has not been subjected to independent review. We are considering a full independent review of next year’s report.

Who We AreWe own 594MW of hydro and wind generation spread throughout New Zealand from the Kaimai scheme in the Bay of Plenty to Waipori in Otago. These assets produce an average of 2,320 GWh per year. During the year we also completed the construction and commissioning of a 98.7MW wind farm in South Australia which is expected to produce around 390 GWh per year.

We supply electricity to around 227,000 customers and provide 30,000 telecommunications services to 20,000 customers throughout New Zealand. We have 394 employees working throughout New Zealand and two employees in Adelaide, South Australia. Around 69 per cent of New Zealand employees are based in our Tauranga head offi ce.

Our ValuesOur PRIIDE values are

PassionRespectIntegrityInnovationDeliveryEmpower

Our vision is to be the leading renewable energy company in Australasia.

TrustPower / Annual Report 2009 / 17

Sustainability Outlook

Our performance this year was strong across the fi ve areas we report on.

Area Measure 2008 Actual 2009 Actual 2009 Target 2010 Target

Economic EBITDAF Growth 6% 25% 8-12% 8-12%

Staff 1 Staff Survey 4.9 4.9 >5.15 >5.15

Environmental Resource Consent Breaches

8 5 0 0

Customer 2 Customer Satisfaction 97% 95% >85% >95%

Community Stakeholder Consultation

Completed Completed Complete detailed stakeholder consultation

Complete detailed stakeholder consultation

1 Scale ranges from 0 (worst) to 7 (best)2 Customers rating good or excellent

A more detailed analysis can be found in pages 21-33.

All businesses face risks and challenges. Our key risks and challenges are summarised in the table below.

Category Key Risks / Challenges Approach Targets Progress

Economic Unable to meet future demand for electricity

Shareholder value growth

Develop a pipeline of opportunities for new investment

Maintain strong focus on effi ciency of operation

Invest in economic growth projects

Focus on long term sustainable pricing

Costs benchmarked at below industry average

New projects all economically viable

New projects completed on time and to budget

Prices set at levels so customer base maintained

1

Environmental Need to minimise environmental impact of generation schemes

Overall impact on carbon emissions

Work closely with special interest groups and the local community to minimise impact of new generation

Comply with resource consents

Maintain carbon neutrality

Zero signifi cant resource consent breaches

Certifi ed carbon neutral

Our People Need to retain and develop a team to produce ongoing performance

Extensive training and development programme

Succession planning and internal promotion

75% of management roles fi lled by internal promotion

Continuous improvement in staff survey results

Staff survey exceeds international benchmark

Community Relationships with and an understanding of local communities is required to effectively operate the business

Community engagement including sponsorship and community awards

Consultation around resource issues

Maintain a strong corporate profi le in all areas in which we operate and build relationships within those communities

No resource consents turned down due to lack of consultation

Customer Dissatisfi ed customers prevent sustainable economic performance

Competitive pricing

Excellent customer service

Information and advice

Carbon neutrality

Net customer churn <2%

>85% satisfaction in survey

Certifi ed carbon neutral

Green = Achieved Amber = Partially achieved Red = Not achieved

1 Deep Stream delayed with some budget overruns

At TrustPower we believe that sustainability means building a long term business through relationships with everyone we interact with. In order to report on our progress in this regard we report economic, staff, environmental, customer and community related measures.

18

Sustainability Outlook

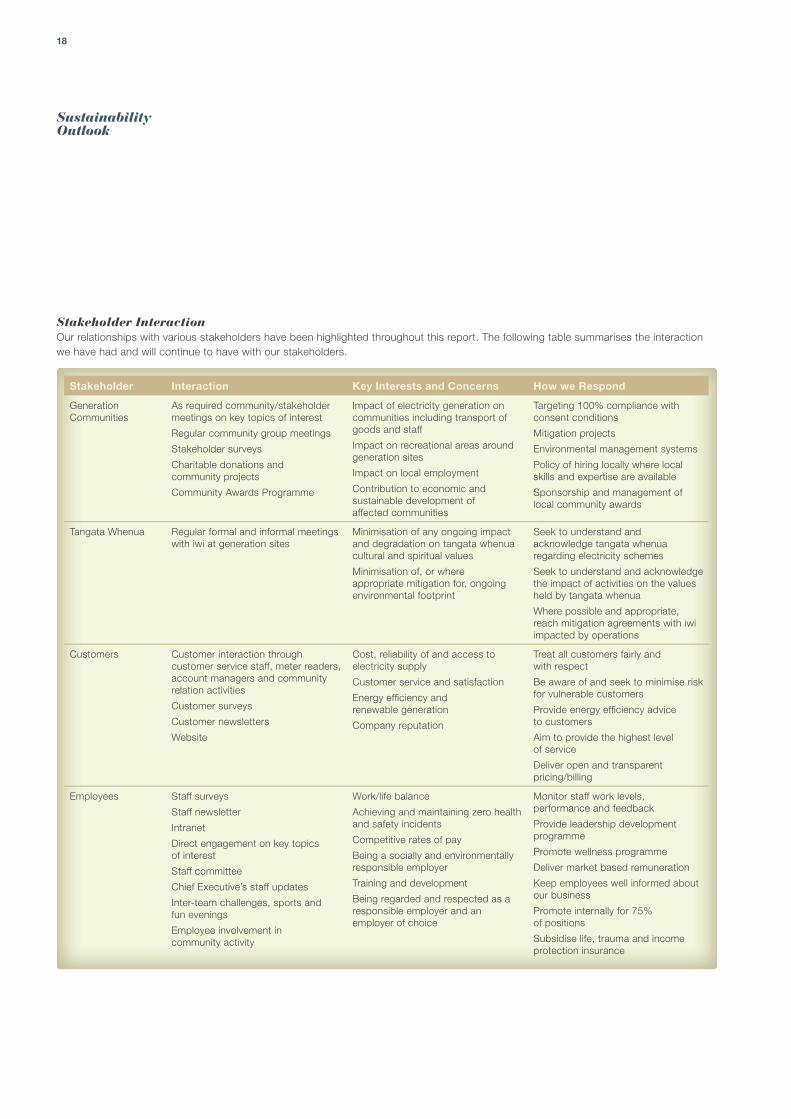

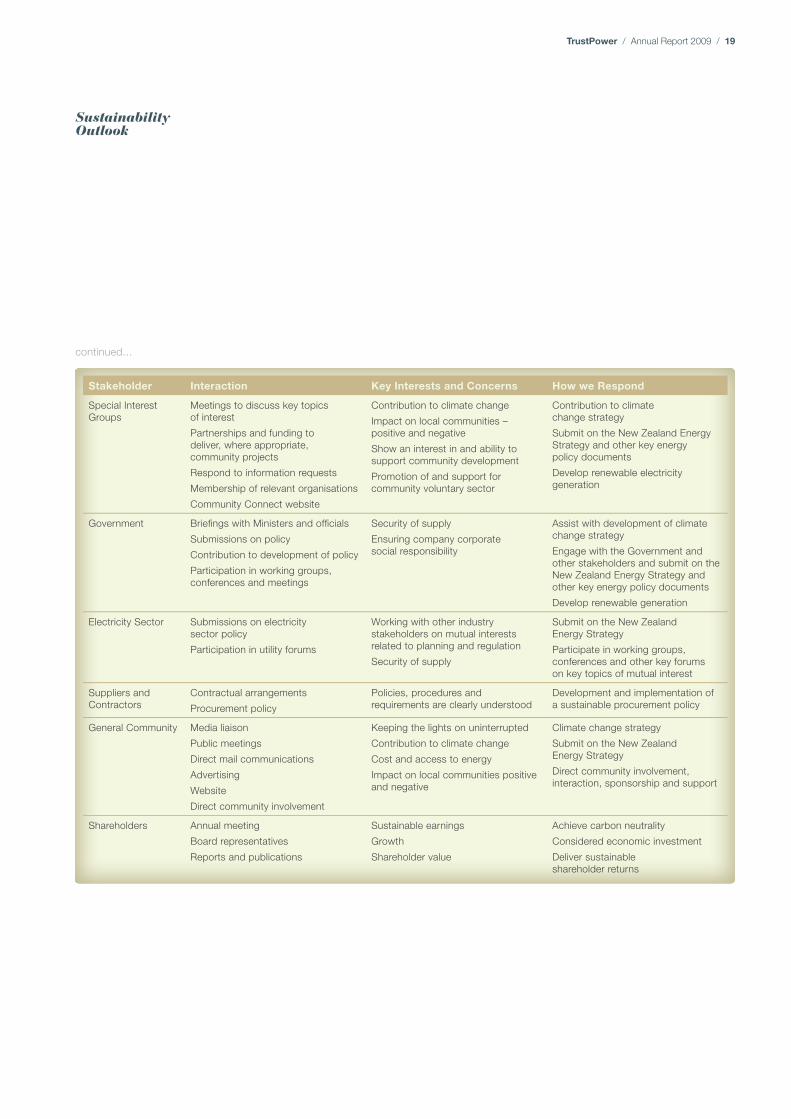

Stakeholder InteractionOur relationships with various stakeholders have been highlighted throughout this report. The following table summarises the interaction we have had and will continue to have with our stakeholders.

Stakeholder Interaction Key Interests and Concerns How we Respond

Generation Communities

As required community/stakeholder meetings on key topics of interest

Regular community group meetings

Stakeholder surveys

Charitable donations and community projects

Community Awards Programme