presentation 1q11

TRANSCRIPT

1Q11 Results Presentation

1

DisclaimerDisclaimerThis presentation may contain references and statem ents representing future expectations, plans of growth and future strategies of BI&P.

These references and statements are based on the Ba nk’s assumptions and analysis and reflect the management’s beliefs, acco rding to their experience, to the economic environment and to predictable market conditions.

As there may be various factors out of the Bank’s c ontrol, there may be significant differences between the real results an d the expectations and declarations herewith eventually anticipated. Those risks and uncertainties include, but are not limited to, our ability to per ceive the dimension of the Brazilian and global economic aspect, banking devel opment, financial market conditions, competitive, government and technologic al aspects that may influence both the operations of BI&P, as the marke t and its products.

Therefore, we recommend the reading of the document s and financial statements available at the CVM website (www.cvm.go v.br) and at our Investor Relations page in the internet (www.indusval.com.br /ir) and the making of your own appraisal.

2

• Sustainable Growth: 4 to 5% GDP growth in the next 5 years

• Corporate Credit market projected growth of 20% p.a.

• Foreign Trade: from 18% to 25% of GDP in the next decade

• High concentration in the banking system

• Declining interest rates in the medium term and new regulatory framework will fuel the development of local high yield bond market

Opportunity for a Bank focused on Corporate Lending

& Fixed Income Debt Market

The Moment in Brazilian EconomyThe Moment in Brazilian Economy

New Stage in BI&P HistoryNew Stage in BI&P History

43 years History

• 1967 – Founded as a brokerage house

• 1991 – Became a Bank

• 2003 – Merged assets of Multistock

• 2006 – Opened the first 4 branches

• 2007 – IPO and opening of 6 new branches

• 2010 – Strategic review

• March 2011 – Banco Indusval & Partners

4

New Capital IncreaseNew Capital Increase

• On March 30, 2011 the Bank raised additional R$ 201 MM tier I equity, by private subscription of:

– R$ 150 MM by Warburg Pincus

– R$ 30 MM by controlling shareholders of Sertrading

– R$ 21 MM by controlling shareholders of BIM

5

New PartnersNew Partners

• Global leading private equity firm founded in 1966

• Invested more than $35 billion in equity in over 600 companies in more than 30 countries

• Current portfolio includes more than 110 companies and is diversified by status, sector and place

• Extensive expertise in the financial sector, having invested over US$ 7.5 billion in over 75 financial institutions

6

• Leading Brazilian import-export service company, exporting and importing for more than 90 countries

• Founded in 2001 by ex-controlling shareholders of CotiaTrading.

• In 2010, transacted a volume of R$ 1.7 billion – 45% annual growth for the past 5 years.

• 2010 Ebitda - R$ 30 MM

• 2010 Net Income - R$ 13 MM

• Branches in São Paulo, several Brazilian ports and China.

New PartnersNew Partners

7

Operating Agreement with Operating Agreement with SertradingSertrading• Capital infusion of R$ 25 MM in Sertrading in return for 18% of company’s capital.

• Entered a 5-year exclusive operational agreement

– Bank holds the right of first refusal for the acquisition of Trade Finance receivables generated by Sertrading with its customer base (~R$ 140MM in 2011)

– Sertrading never had a single default on its receivables in its 10-year history due to its operational knowledge of its client base.

• Option to purchase the balance of company’s capital over the next two years

• Acquisition of 100% of Serglobal Comércio de Cereais L tda and of Sertrading’sAgricultural Product Area for R$ 15MM

• Strategic Benefits

– Generation of high quality assets

– Relationship with Sertrading seeks to enhance the Bank’s operational knowledge of its client base

– Ability to offer financial products to Sertrading’s client base (cross selling)

8

New Partners New Partners –– JP MorganJP Morgan

• JP Morgan sold its import-export service Brazilian company, Vastera JPM Chase, to Sertrading.

• JP Morgan will grant a US$ 25 MM 2-year credit facility to the Bank. Other transactions are being discussed.

• JP Morgan has also agreed to purchase 5-year warrants for subscription of new non-voting shares(equity) of the Company corresponding to 2.5% of the Company’s corporate capital

9

New Management TeamNew Management TeamThe bank has attracted an experienced set of leader s in addition to its management team:

• Jair Ribeiro (Co-CEO and member of the controlling sh areholder group) – co-founder and former CEO of Banco Patrimônio (Salomon Brothers), former CEO of JP Morgan (Brazil).

• Francisco Cote Gil (VP Commercial Area) - former partner and MD at BBA and Itaú BBA (18 years); former MD Banco Crefisul/ Citibank.

• Gil Fawichow (VP Treasury) – former Treasurer of ING (Brazil); partner of Black River Asset Mgt (Cargill); co-founder and treasurer of Banco Rendimento.

• André Mesquita (VP Products & Corporate Finance) – former COO Cotia Trading (Argentina); co-founder of Sertrading; former CFO of CPM Braxis

10

NewNew Management TeamManagement TeamNew team will interact with existing senior managem ent of Banco Indusval:

• Manoel Cintra (Chairman of the Board) – former CEO of Banco Indusval, CEO of Banco Multiplic (Lloyds Brazil); former Chairman of BM&F.

• Luiz Masagão (Co-CEO) – former President of Banco Indusval; former Chairman of BM&F.

• Katia Moroni (VP Trade Finance and Funding) – former MD Banco Santander, Banco Multiplic and Barclays.

• Gilmar Melo de Azevedo (VP Special Credits) - former Regional Manager of Banco Real, former- Auditor of Banco Mercantil do Brasil, former-Executive Officer of Banco Sofisa and Banco Pine.

• Eliezer L. Ribeiro da Silva , (Middle Market Credit Officer)- former Sudameris and BMG, 17 years with Indusval.

11

Chief Executive Officers

ESTRUTURA ORGANIZACIONAL APÓS PARCERIA

ChairmanManoel Felix Cintra Neto

Investor Relations

Commercial Treasury

Products & Corporate Finance

Trade Finance

FundingSyndications

New Organizational StructureNew Organizational Structure

Jair Ribeiro

Credit

Information Technology

Accounting & Controlling

Operational Department

Legal Dept.

Compliance & Internal Controls

Risk Management

Luiz Masagão Ribeiro

Human Resources

12

New VisionNew Vision

To be an innovative bank, with excellence in corporate credit and deep understanding of our clients’ businesses.

Using our credit platform as a base, seek to become one of the leading players of the high-growth, domestic corporate bond market.

1Q11 1Q11 ResultsResults

Total Credit PortfolioTotal Credit Portfolio

717

9601,059

1,329

1,519

1,794

2,080

1,7941,736 1,728 1,684 1,699 1,719 1,763 1,769

1,940 1,967

691

4Q06 2Q07 4Q07 2Q08 4Q08 2Q09 4Q09 2Q10 4Q10

Local Currency Loans Trade Finance Letters of Guarantee and L/Cs

CAGR

+17.1% per quarte

r / +88.0% p.a.

CAGR: +6.3% per quarter / +27.7% p.a.

R$

mill

ion

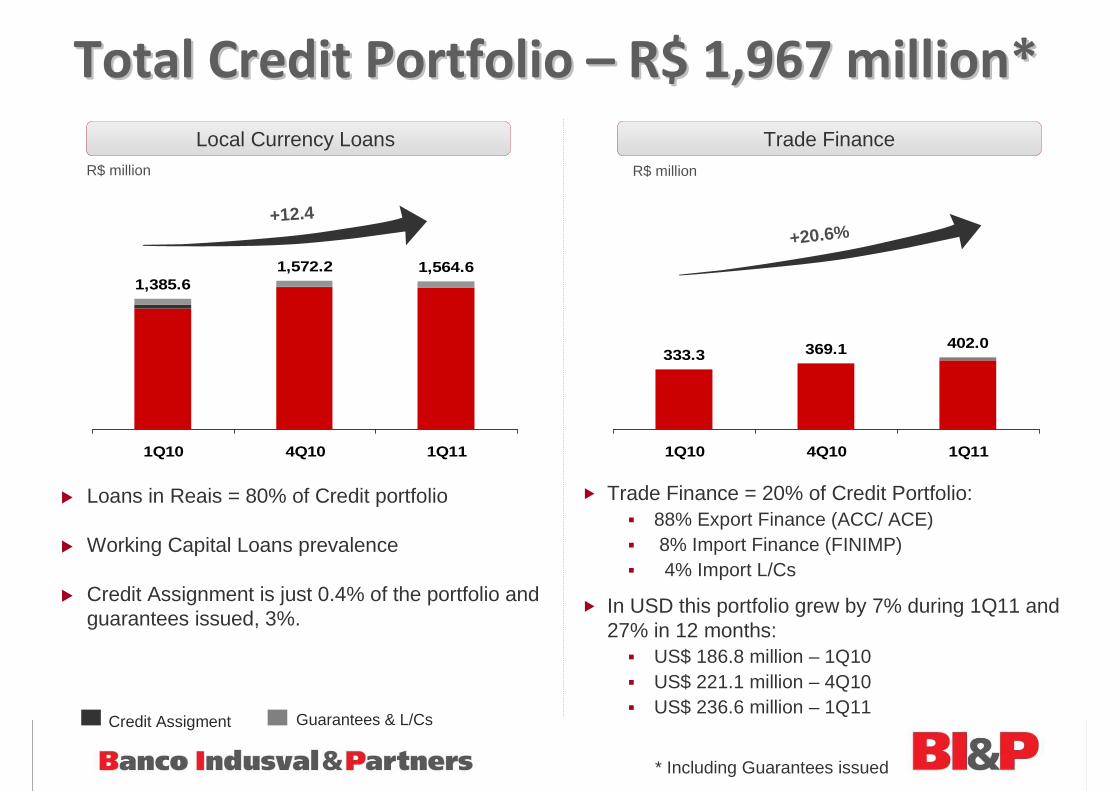

� Loans in Reais = 80% of Credit portfolio

� Working Capital Loans prevalence

� Credit Assignment is just 0.4% of the portfolio and guarantees issued, 3%.

� Trade Finance = 20% of Credit Portfolio:� 88% Export Finance (ACC/ ACE)� 8% Import Finance (FINIMP)� 4% Import L/Cs

� In USD this portfolio grew by 7% during 1Q11 and 27% in 12 months:

� US$ 186.8 million – 1Q10� US$ 221.1 million – 4Q10� US$ 236.6 million – 1Q11

Local Currency Loans Trade Finance

333.3 369.1 402.0

1Q10 4Q10 1Q11

R$ million

+20.6%

1,385.61,572.2 1,564.6

1Q10 4Q10 1Q11

+12.4

R$ million

* Including Guarantees issued

Credit Assigment Guarantees & L/Cs

Total Credit Portfolio Total Credit Portfolio –– R$ 1,967 million*R$ 1,967 million*

Middle Market

82%

Upper Middle

14%

Other4%

10 largest20%

11 - 6032%

61 - 16024%

Other24%

Industry56%

Financial Cos3%

Other23%

Individual7%

Trade11%

Up to 90 days36%

91 to 18019%

181 to 360 15%

+360 days30%

Credit Portfolio BreakdownCredit Portfolio Breakdown

By Customer Concentration

By Economic Activity By Type of Customer

By Maturity

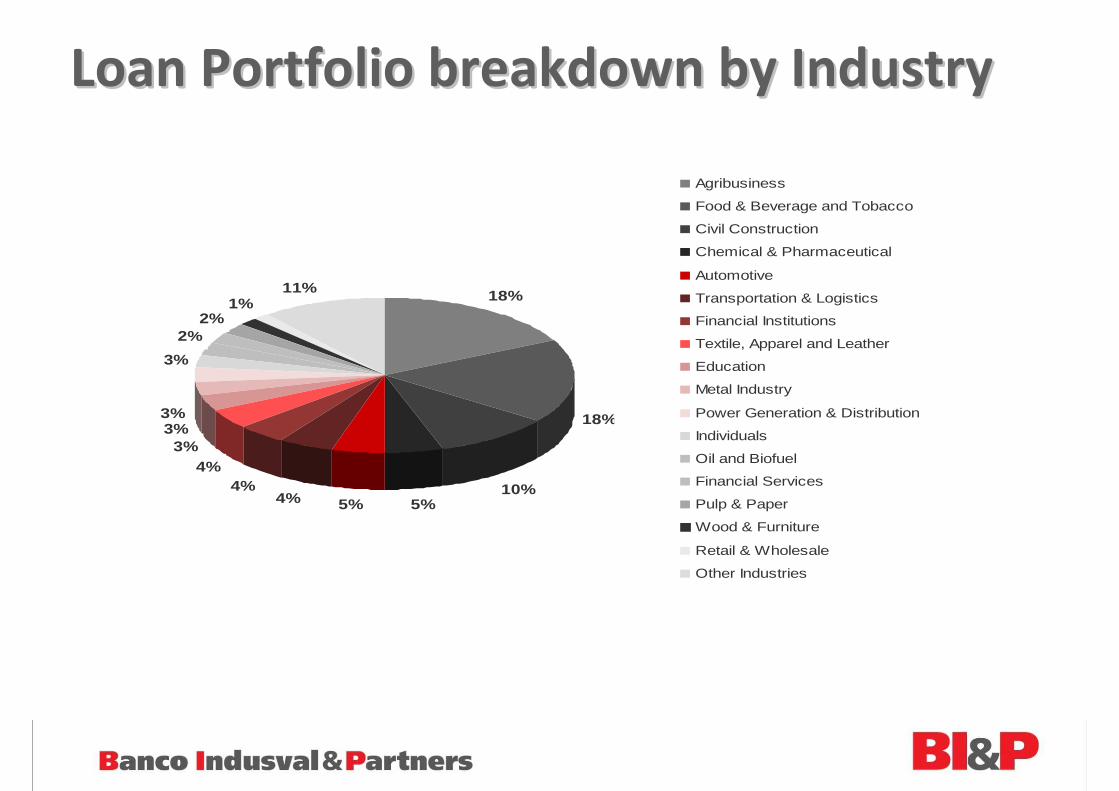

Loan Portfolio breakdown by Industry Loan Portfolio breakdown by Industry

18%

10%5%5%4%

4%

11%1%

2%2%

18%

3%

4%3%

3%3%

Agribusiness

Food & Beverage and Tobacco

Civil Construction

Chemical & Pharmaceutical

Automotive

Transportation & Logistics

Financial Institutions

Textile, Apparel and Leather

Education

Metal Industry

Power Generation & Distribution

Individuals

Oil and Biofuel

Financial Services

Pulp & Paper

Wood & Furniture

Retail & Wholesale

Other Industries

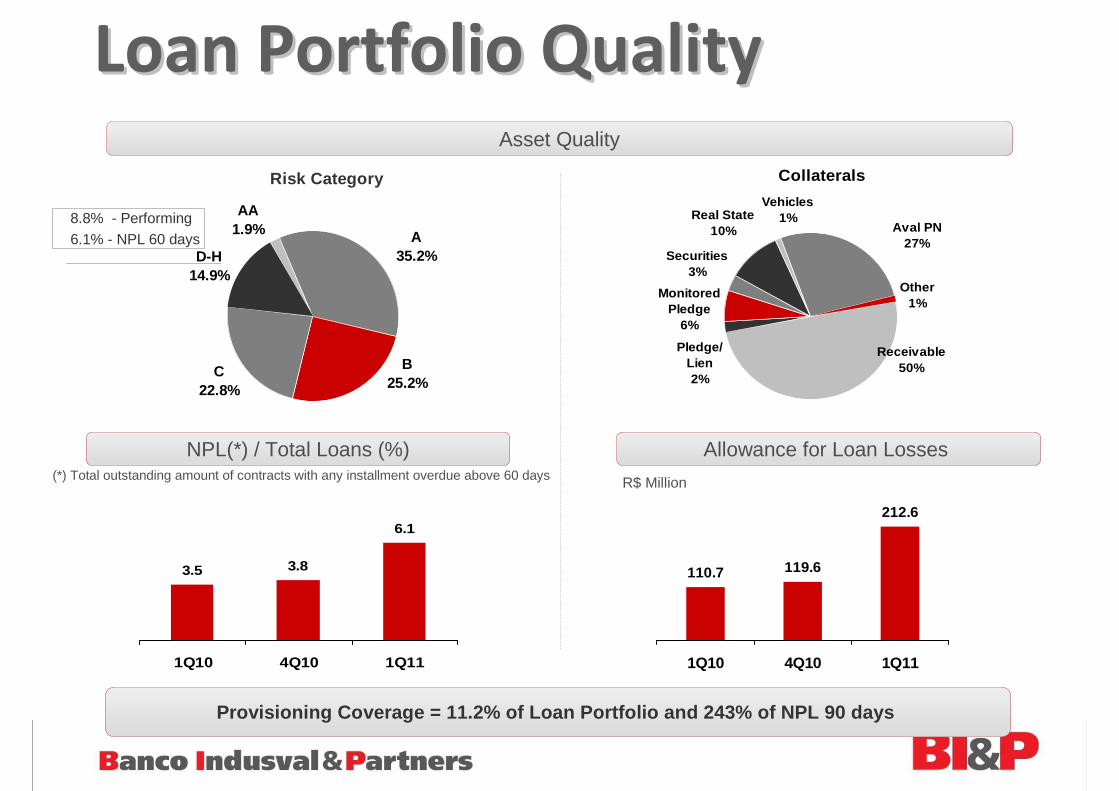

Loan Portfolio QualityLoan Portfolio Quality

Allowance for Loan Losses NPL(*) / Total Loans (%)

Asset Quality

Provisioning Coverage = 11.2% of Loan Portfolio and 243% of NPL 90 days

3.5 3.8

6.1

1Q10 4Q10 1Q11

Collaterals

Other1%

Securities3%

Real State10% Aval PN

27%

Monitored Pledge

6%

Vehicles1%

Pledge/ Lien2%

Receivable50%

Risk Category

AA1.9%

C22.8%

D-H14.9%

A35.2%

B25.2%

110.7 119.6

212.6

1Q10 4Q10 1Q11

8.8% - Performing6.1% - NPL 60 days

R$ Million(*) Total outstanding amount of contracts with any installment overdue above 60 days

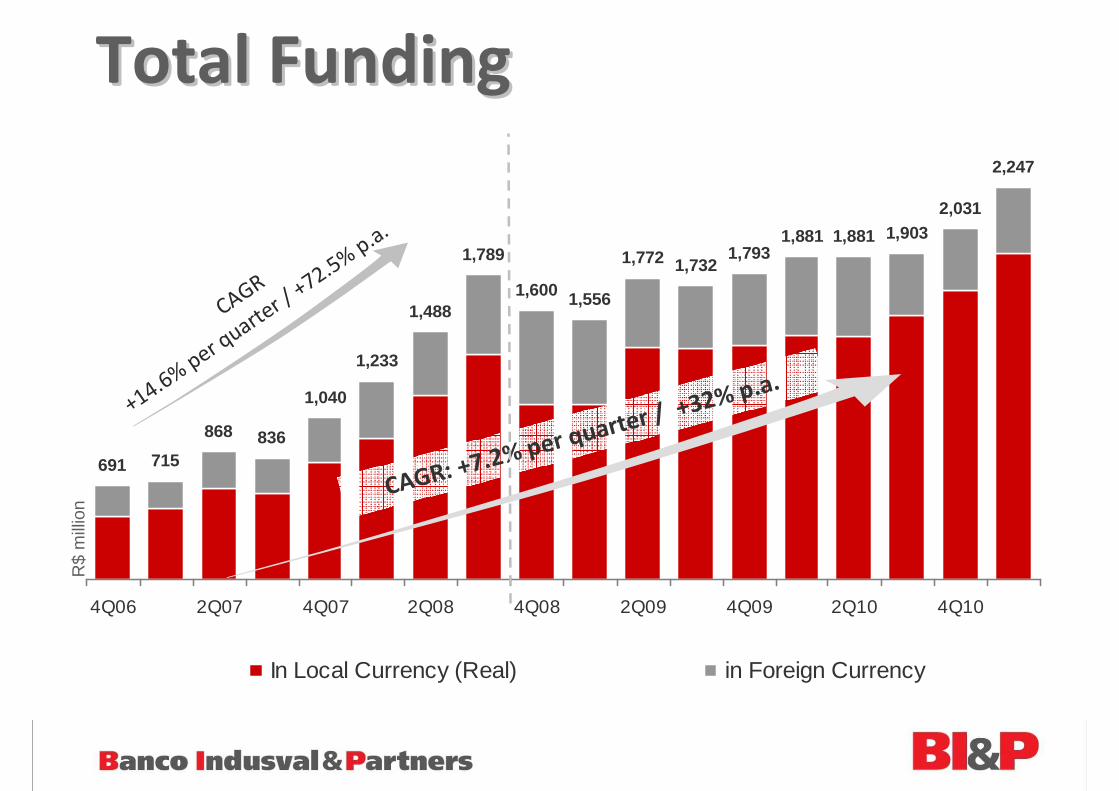

715

868 836

1,040

1,233

1,488

1,789

1,600 1,556

1,772 1,7321,793

1,881 1,881 1,9032,031

2,247

691

4Q06 2Q07 4Q07 2Q08 4Q08 2Q09 4Q09 2Q10 4Q10

In Local Currency (Real) in Foreign Currency

CAGR

+14.6% per quarte

r / +72.5% p.a.

CAGR: +7.2% per quarter / +32% p.a.

R$

mill

ion

Total FundingTotal Funding

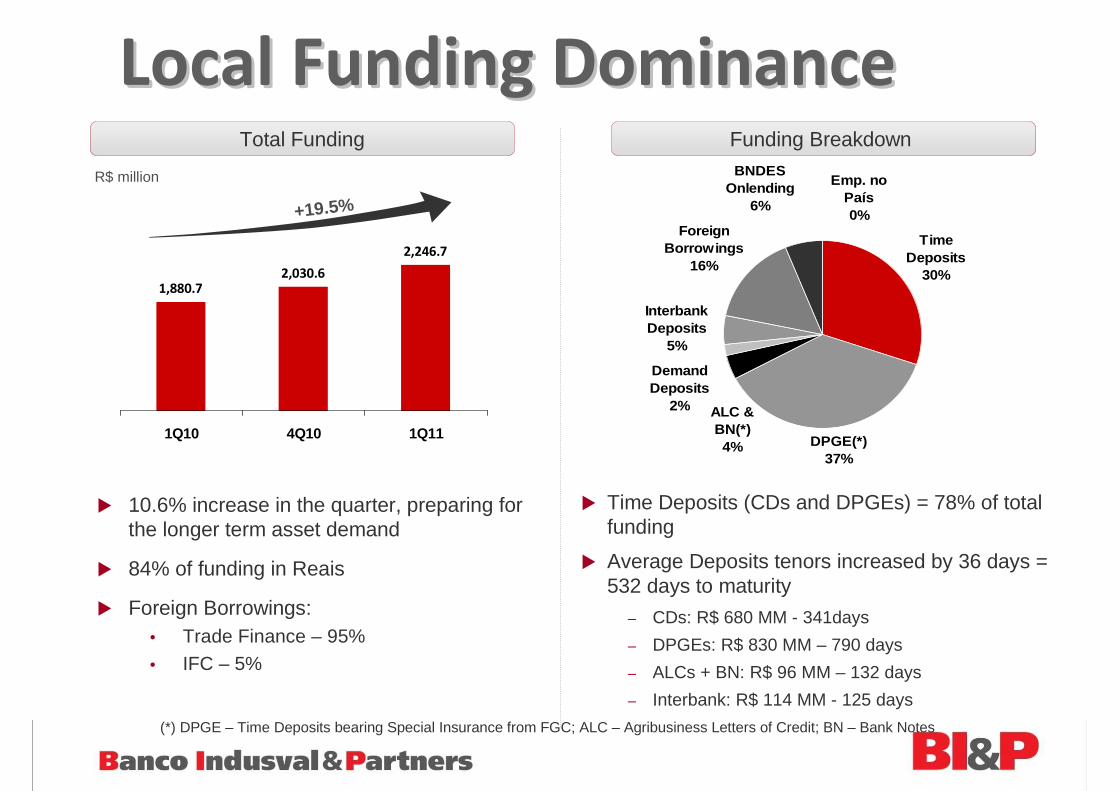

Time Deposits

30%

DPGE(*)37%

Interbank Deposits

5%

Foreign Borrowings

16%

BNDES Onlending

6%

Emp. no País0%

ALC & BN(*)4%

Demand Deposits

2%

Local Funding DominanceLocal Funding Dominance

R$ million

� 10.6% increase in the quarter, preparing for the longer term asset demand

� 84% of funding in Reais

� Foreign Borrowings:• Trade Finance – 95%

• IFC – 5%

Total Funding Funding Breakdown

1,880.72,030.6

2,246.7

1Q10 4Q10 1Q11

+19.5%

� Time Deposits (CDs and DPGEs) = 78% of total funding

� Average Deposits tenors increased by 36 days = 532 days to maturity

– CDs: R$ 680 MM - 341days

– DPGEs: R$ 830 MM – 790 days

– ALCs + BN: R$ 96 MM – 132 days

– Interbank: R$ 114 MM - 125 days

(*) DPGE – Time Deposits bearing Special Insurance from FGC; ALC – Agribusiness Letters of Credit; BN – Bank Notes

Good Liquidity with Longer TenorsGood Liquidity with Longer Tenors

707 734

1,027

1Q10 4Q10 1Q11

Free CashR$ Million

Free Cash = (Cash + Liquid Fin. Assets + Securities + Derivatives) (-) (Open Market Funds + Derivatives) equivalent to:

� 58% of Total Deposits

� 182% of Shareholder Equity

R$ 197.7 million cash deposited at the Central Bank of Brazil related to the capital increase paid on March 30, 2011 submitted to its approval:

• Warburg Pincus: R$ 150 million

• Sertrading Controlling Group: R$ 26.7 million (+R$ 3.3 million in May/11)

• Indusval Controlling Shareholders: R$ 21 million

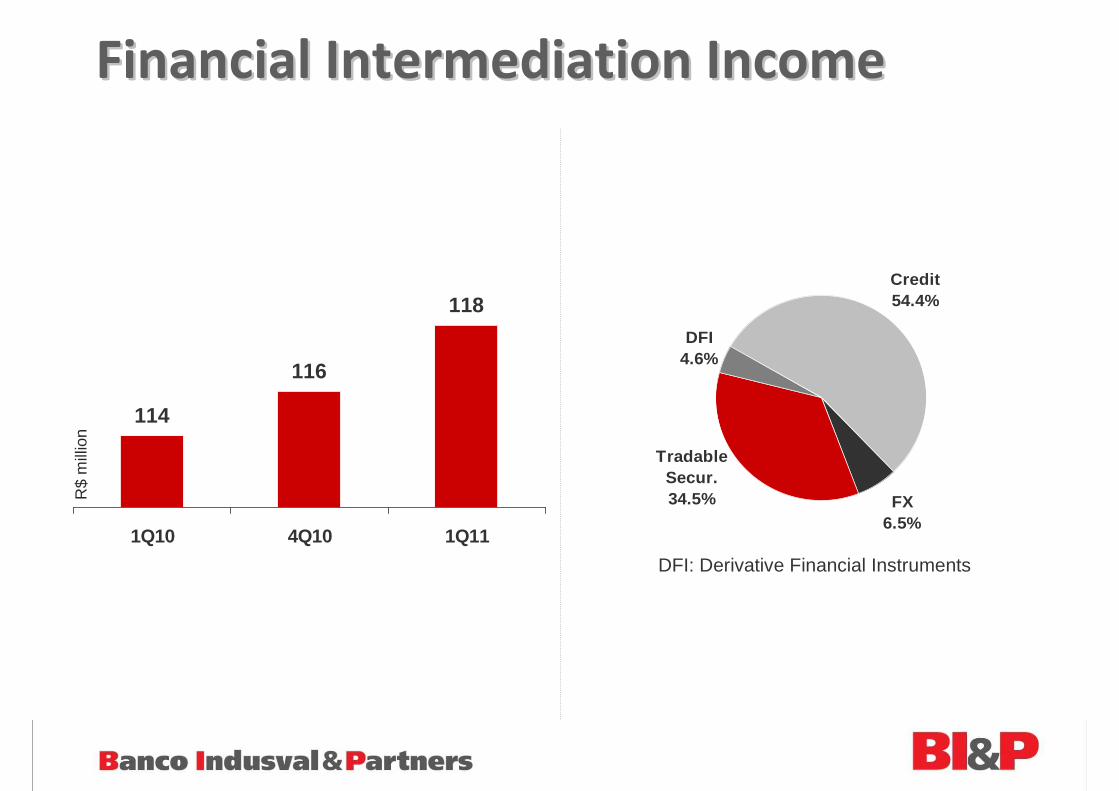

114

116

118

1Q10 4Q10 1Q11

Financial Intermediation IncomeFinancial Intermediation Income

Credit54.4%

Tradable Secur.34.5% FX

6.5%

DFI4.6%

R$

mill

ion

DFI: Derivative Financial Instruments

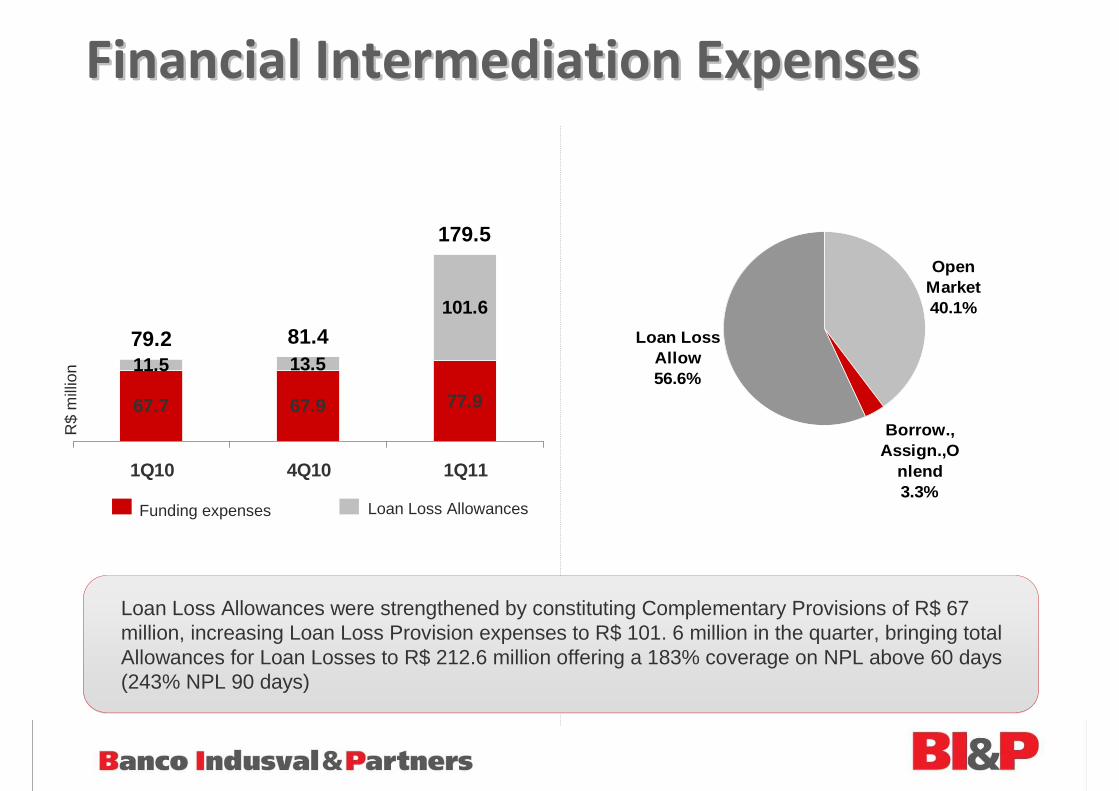

67.7 67.9 77.9

11.5 13.5

101.6

79.2 81.4

179.5

1Q10 4Q10 1Q11

Financial Intermediation ExpensesFinancial Intermediation Expenses

Open Market40.1%

Borrow., Assign.,O

nlend3.3%

Loan Loss Allow56.6%

R$

mill

ion

Funding expenses Loan Loss Allowances

Loan Loss Allowances were strengthened by constituting Complementary Provisions of R$ 67 million, increasing Loan Loss Provision expenses to R$ 101. 6 million in the quarter, bringing total Allowances for Loan Losses to R$ 212.6 million offering a 183% coverage on NPL above 60 days (243% NPL 90 days)

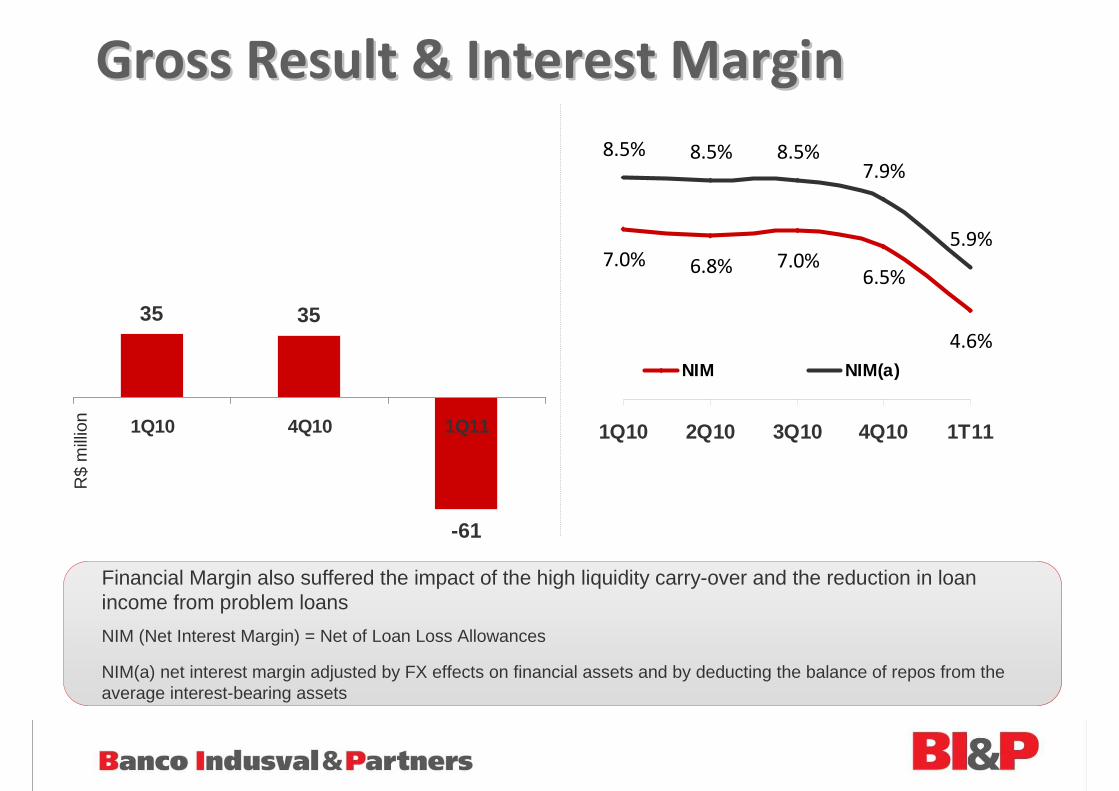

7.0% 6.8% 7.0%6.5%

4.6%

8.5% 8.5% 8.5%7.9%

5.9%

1Q10 2Q10 3Q10 4Q10 1T11

NIM NIM(a)

35 35

-61

1Q10 4Q10 1Q11

Gross Result & Interest MarginGross Result & Interest MarginR

$ m

illio

n

Financial Margin also suffered the impact of the high liquidity carry-over and the reduction in loan income from problem loans

NIM (Net Interest Margin) = Net of Loan Loss Allowances

NIM(a) net interest margin adjusted by FX effects on financial assets and by deducting the balance of repos from the average interest-bearing assets

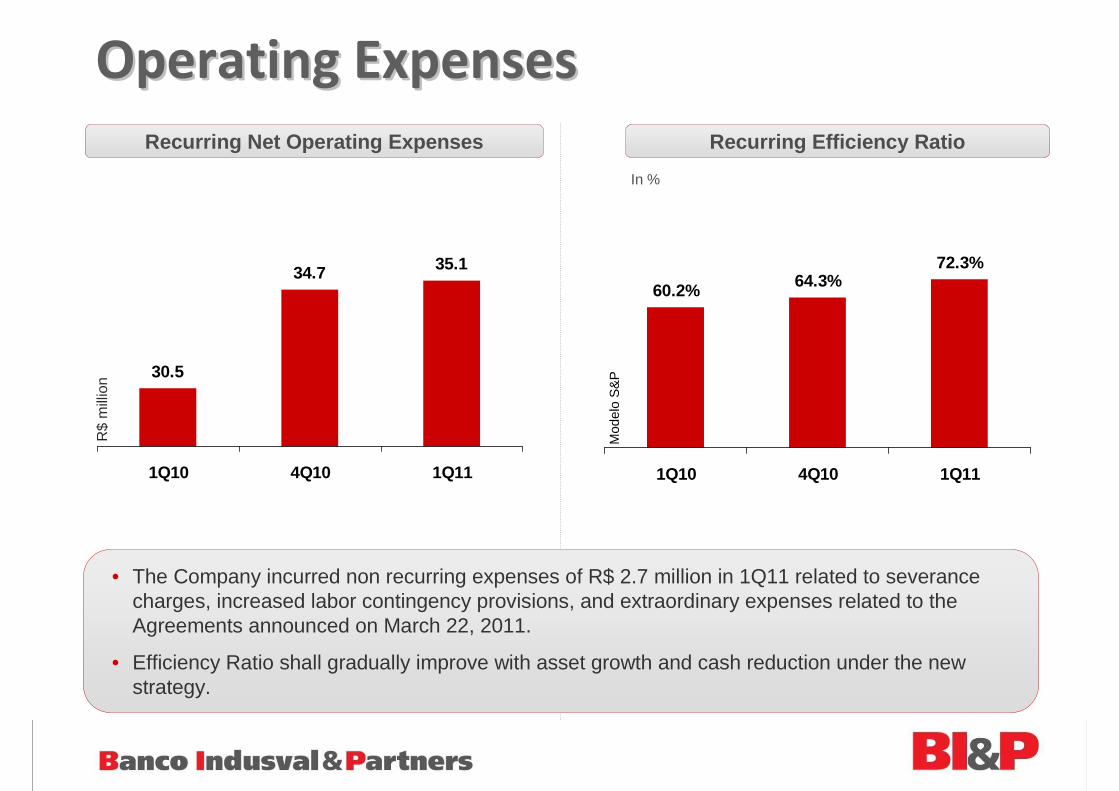

Recurring Efficiency Ratio

30.5

34.7 35.1

1Q10 4Q10 1Q11

In %

Recurring Net Operating Expenses

Operating ExpensesOperating ExpensesR

$ m

illio

n

60.2% 64.3%72.3%

1Q10 4Q10 1Q11

Mod

elo

S&

P

• The Company incurred non recurring expenses of R$ 2.7 million in 1Q11 related to severance charges, increased labor contingency provisions, and extraordinary expenses related to the Agreements announced on March 22, 2011.

• Efficiency Ratio shall gradually improve with asset growth and cash reduction under the new strategy.

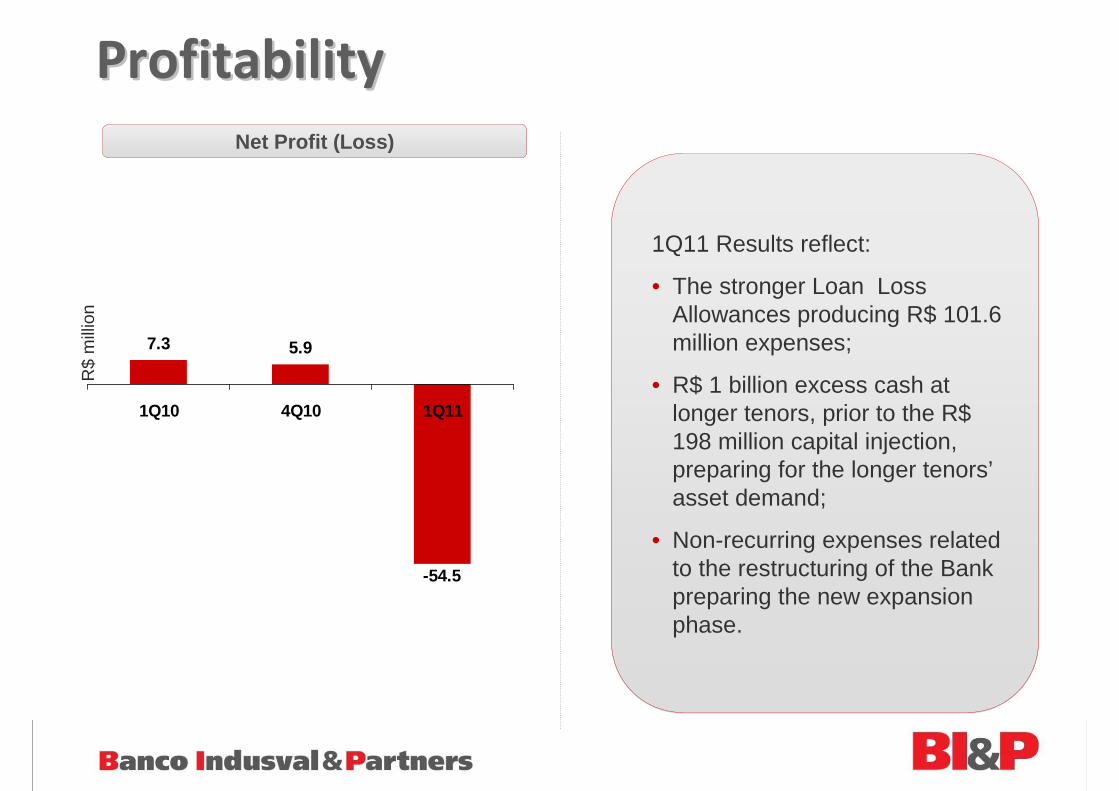

Net Profit (Loss)

ProfitabilityProfitability

7.3 5.9

-54.5

1Q10 4Q10 1Q11

R$

mill

ion

1Q11 Results reflect:

• The stronger Loan Loss Allowances producing R$ 101.6 million expenses;

• R$ 1 billion excess cash at longer tenors, prior to the R$ 198 million capital injection, preparing for the longer tenors’asset demand;

• Non-recurring expenses related to the restructuring of the Bank preparing the new expansion phase.

� 1Q11 Results reflect the Company’s restructuring to foster growth under new strategy

� Corporate lending business focus maintained, but pursuing innovation and excellence, with deep understanding of our clients’ businesses; and, using our credit platform as a base, seek to become one of the leading players of the domestic corporate bond market.

� Stronger capital base with the R$ 201 million capital injection raises Basel Index to circa 25%, and allows solid asset growth

� Operating Agreement with Sertrading accelerates growth and adds customer operating activities know-how

� New Partners and New Management bring expertise, entrepreneurship, global relationships and international experience

� We are in a position to develop a new growth pace under the new strategy designed together with the new partners

In a NutshellIn a Nutshell

IR Contact InformationIR Contact Information

Katia MoroniIROPhone: (55 11) 3315-6923E-mail: [email protected]

Maria Angela R. ValenteIR HeadPhone: (55 11) 3315-6821E-mail: [email protected]

Banco Indusval S/ARua Boa Vista, 356 – 7º andar01014-000- São Paulo – SPBrasil

IR Website: www.indusval.com.br/ir