presentation 2q15

TRANSCRIPT

Earnings Results 2Q15 August, 2015

2

Disclaimer

This presentation may contain certain forward-looking projections and trends that neither

represent realized financial results nor historical information.

These forward-looking projections and trends are subject to risk and uncertainty, and

future results may differ materially from the projections. Many of these risks and

uncertainties are related to factors that are beyond CCR’s ability to control or to estimate,

such as market conditions, currency swings, the behavior of other market participants, the

actions of regulatory agencies, the ability of the company to continue to obtain financing,

changes in the political and social context in which CCR operates or economic trends or

conditions, including changes in the rate of inflation and changes in consumer confidence

on a global, national or regional scale.

Readers are advised not to fully trust these projections and trends. CCR is not obliged to

publish any revision of these projections and trends that should reflect new events or

circumstances after the realization of this presentation.

3

Agenda

Highlights

Results Analysis

Perspectives

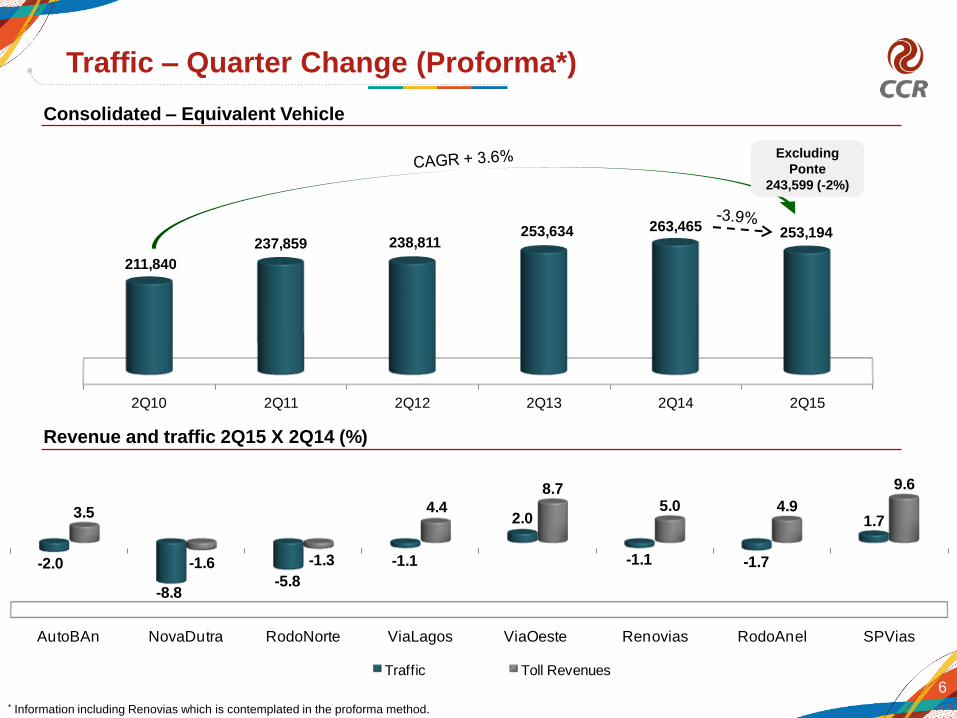

TRAFFIC:

Proforma consolidated traffic1 excluding Ponte fell by 2.0% in 2Q15.

TOLLS COLLECTED BY ELECTRONIC MEANS:

The number of STP users increased by 10.6% over June 2014, reaching 5,005,000

active tags.

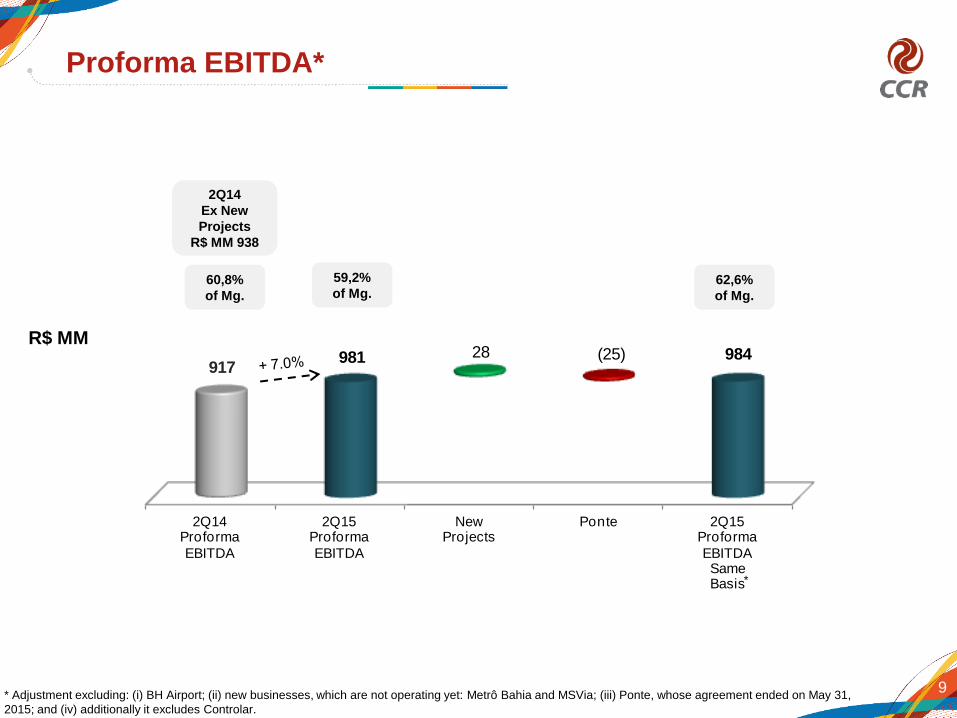

ADJUSTED EBITDA:

Same-basis2 adjusted proforma EBITDA increased by 4.9%, with an margin of 62.6%

(-1.1 p.p.).

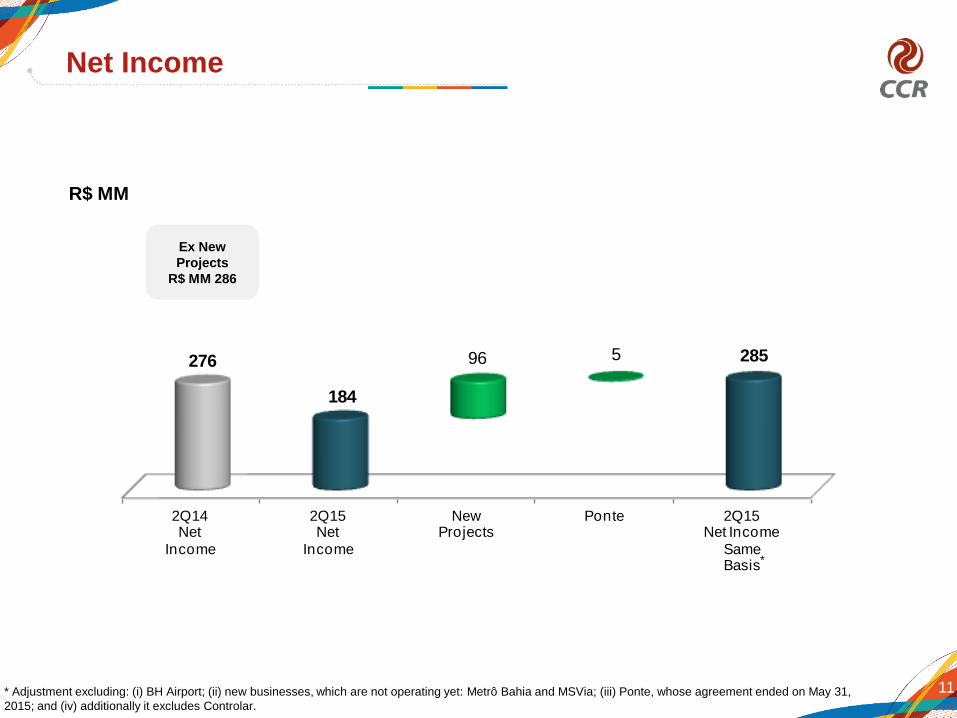

NET INCOME:

Same-basis2 net income totaled R$284.6 million, a 0.5% reduction in 2Q15.

DIVIDENDS:

CCR’s Management proposed to the Board of Directors the distribution of interim

dividends in the approximate amount of R$ 0,76 per share, subject to approval of said

body.

4

2Q15 Highlights

1 Including the proportional results of jointly-owned subsidiaries. 2 “Same-basis” amounts exclude: (i) BH Airport; (ii) new businesses, which are not operating yet: Metrô Bahia and MSVia; (iii) Ponte, whose agreement ended

on May 31, 2015; and (iv) in profit and pro-forma comparisons, it excludes Controlar, ViaRio and VLT.

1- Net revenue excludes construction revenue.

2- Same-basis” amounts exclude: (i) BH Airport; (ii) new businesses, which are not operating yet: Metrô Bahia and MSVia; (iii) Ponte, whose agreement ended on

May 31, 2015; and (iv) in profit and pro-forma comparisons, it excludes Controlar, ViaRio and VLT.

3- Calculated by adding net revenue, construction revenue, costs of services and administrative expenses

4- The adjusted EBIT and EBITDA margins were calculated by dividing EBIT and EBITDA by net revenue, excluding construction revenue, as required by IFRS,

whose counter-entry of the same amount impacts total costs.

5- Calculated excluding non-cash expenses: depreciation and amortization, the provision for maintenance and the recognition of prepaid concession expenses.

5

Financial Highlights – 2Q15

Net Revenues1 1,317.7 1,424.4 8.1% 1,507.2 1,657.3 10.0%

Adjusted Net Revenues on the same basis2 1,282.5 1,342.4 4.7% 1,472.1 1,573.1 6.9%

Adjusted EBIT3 563.0 583.0 3.6% 653.4 682.1 4.4%

Adjusted EBIT Mg.4 42.7% 40.9% -1.8 p.p. 43.4% 41.2% -2.2 p.p.

EBIT on the same basis2 589.7 594.8 0.9% 682.9 694.2 1.7%

EBIT Mg. on the same basis2 46.0% 44.3% -1.7 p.p. 46.4% 44.1% -2.3 p.p.

Adjusted EBITDA5 797.5 845.2 6.0% 916.9 980.9 7.0%

Adjusted EBITDA Mg.4 60.5% 59.3% -1.2 p.p. 60.8% 59.2% -1.6 p.p.

Adjusted EBITDA on the same basis2 815.6 848.1 4.0% 937.8 984.0 4.9%

Adjusted EBITDA Mg. on the same basis2 63.6% 63.2% -0.4 p.p. 63.7% 62.6% -1.1 p.p.

Net Income 275.8 183.7 -33.4% 275.8 183.7 -33.4%

Net Income on the same basis2 286.1 284.6 -0.5% 286.1 284.6 -0.5%

2Q14 2Q15 Chg %Financial Indicators (R$ MM) 2Q14 2Q15 Chg %

IFRS Proforma

2Q10 2Q11 2Q12 2Q13 2Q14 2Q15

253,194

211,840

237,859 238,811 253,634 263,465

6

Traffic – Quarter Change (Proforma*)

Consolidated – Equivalent Vehicle

Revenue and traffic 2Q15 X 2Q14 (%)

* Information including Renovias which is contemplated in the proforma method.

Excluding

Ponte

243,599 (-2%)

AutoBAn NovaDutra RodoNorte ViaLagos ViaOeste Renovias RodoAnel SPVias

-2.0

-8.8-5.8

-1.1

2.0

-1.1 -1.7

1.73.5

-1.6 -1.3

4.4

8.75.0 4.9

9.6

Traffic Toll Revenues

2Q12 2Q13 2Q14 2Q15

90% 84% 84% 78%

10% 16% 16% 22%

Toll Others

2Q12 2Q13 2Q14 2Q15

67% 69% 70% 70%

33% 31% 30% 30%

Electronic Cash

AutoBAn26.6%

NovaDutra15.0%

ViaOeste13.4%

RodoNorte8.8%

Airports8.5%

SPVias7.9%

STP4.1%

ViaQuatro3.3%

RodoAnel3.1%

Renovias2.2%

Barcas2.2%

Ponte1.5%

ViaLagos1.3%

Others2.1%

7

Revenue Analysis (Proforma*)

Payment Means

Gross Operating Revenues Gross Revenue Breakdown

* Including the proportional results of jointly-owned subsidiaries.

2Q14 Depreciationand

Amortization

Third-partyServices

GrantingPower andAdvanced

Expenses

PersonnelCosts

ConstructionCosts

MaintenanceProvision

OtherCosts

2Q15 NewProjects

Ponte 2Q15SameBasis

1,229

1,476

883

3534 7 17

160 (7) 2 (589)

(4)

8

IFRS Costs Evolution (2Q15 X 2Q14)

Total Costs (R$ MM)

Construction of Service Roads, Duplication, New Projects and

Ponte

New Projects, Direct Costs and Ponte

New Projects, Wage Increase

and Ponte

Performed Work and

New Projects

Same-basis

Cash Cost:

+5.6%

Reduction in the Provision on RodoNorte

New Projects and Ponte

20% 9%

34% 20%

21%

(15)% 2%

8%

2Q14Proforma

EBITDA

2Q15Proforma

EBITDA

NewProjects

Ponte 2Q15Proforma

EBITDASameBasis

917981 (25) 98428

9

Proforma EBITDA*

60,8%

of Mg.

59,2%

of Mg. 62,6%

of Mg.

* Adjustment excluding: (i) BH Airport; (ii) new businesses, which are not operating yet: Metrô Bahia and MSVia; (iii) Ponte, whose agreement ended on May 31,

2015; and (iv) additionally it excludes Controlar.

*

R$ MM

2Q14

Ex New

Projects

R$ MM 938

10

IFRS Financial Results

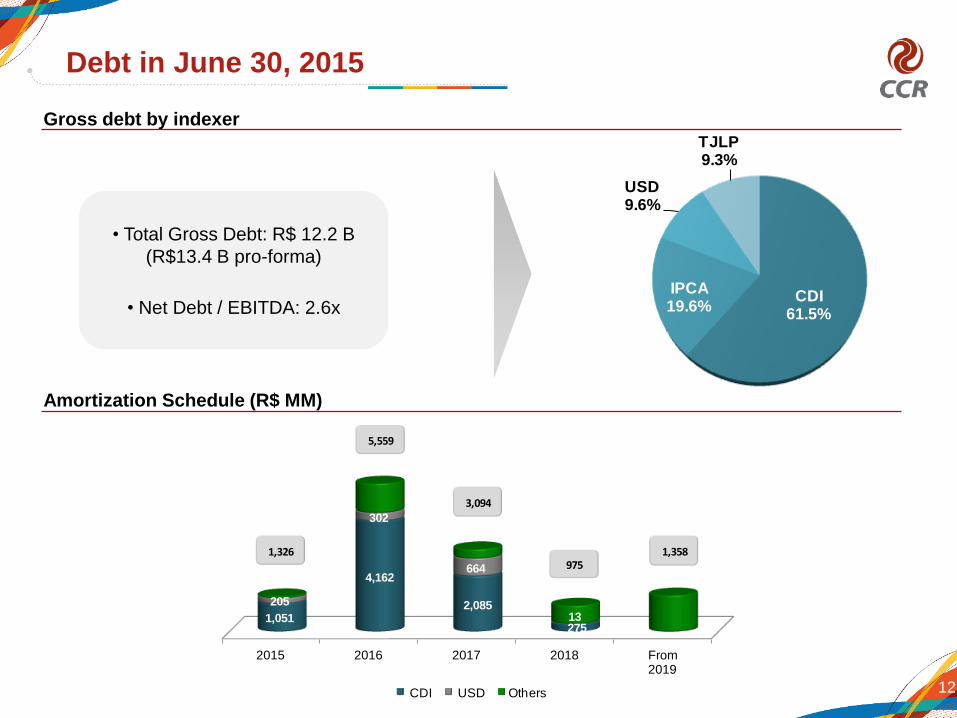

• Chg. of average CDI 2Q15 X 2Q14 = +2.3 p.p.

• Gross Debt = R$ 12.2 B (+37.5%)

R$ MM

Change on

the Proforma

Same-basis:

32%

92%

2Q14 NetFinancial Result

Income fromHedge Operation

Monetary variation on loans, financing

and debentures

Monetary Variation on Liabilities related

to the Granting Power

Exchange Rate Variation on Loans,

Financing and Debentures

Present Value Adjustment of

Maintenance Provision and

Liabilities related to the Granting Power

Interest on Loans, Financing and

Debentures

Investment Income and Other Income

Fair Value ofHedge Operation

Others 2Q15 NetFinancial Result

(202.9)

(13.4)(389.3)

(75.4)

(40.6)

(54.9) 29.3(11.6)

(78.1) 29.3

29.0

11

Net Income

R$ MM

Ex New

Projects

R$ MM 286

* Adjustment excluding: (i) BH Airport; (ii) new businesses, which are not operating yet: Metrô Bahia and MSVia; (iii) Ponte, whose agreement ended on May 31,

2015; and (iv) additionally it excludes Controlar.

*

2Q14Net

Income

2Q15Net

Income

NewProjects

Ponte 2Q15Net Income

SameBasis

276

184

96 5 285

2015 2016 2017 2018 From2019

1,051

4,162

2,08513

205

302

664

275

CDI USD Others

1,358975

3,094

5,559

1,326

CDI61.5%

IPCA19.6%

USD9.6%

TJLP9.3%

12

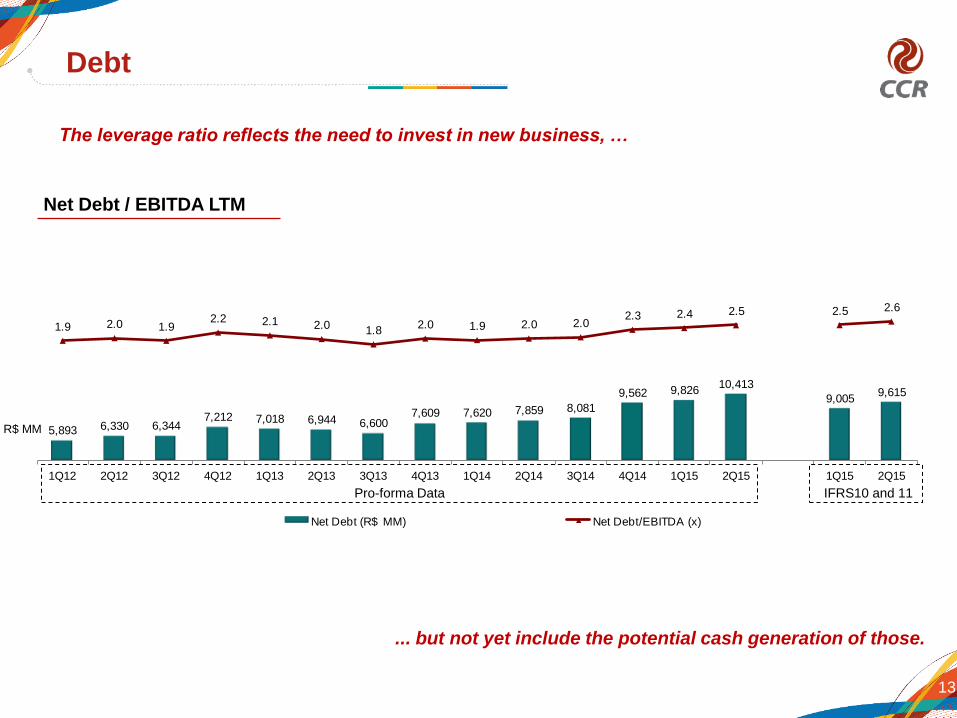

Debt in June 30, 2015

Gross debt by indexer

Amortization Schedule (R$ MM)

• Total Gross Debt: R$ 12.2 B

(R$13.4 B pro-forma)

• Net Debt / EBITDA: 2.6x

5,893 6,330 6,3447,212 7,018 6,944 6,600

7,609 7,620 7,859 8,081

9,562 9,82610,413

9,0059,615

1.9 2.0 1.92.2 2.1 2.0 1.8

2.0 1.9 2.0 2.02.3 2.4 2.5 2.5 2.6

-2.5

-1.5

-0.5

0.5

1.5

2.5

3.5

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 1Q15 2Q15

Net Debt (R$ MM) Net Debt/EBITDA (x)

13

Debt

Net Debt / EBITDA LTM

IFRS10 and 11

Pro-forma Data

R$ MM

The leverage ratio reflects the need to invest in new business, …

... but not yet include the potential cash generation of those.

14

Realized Investments and Maintenance

1- The investments made by the Company, which will be reimbursed by the granting authority as monetary consideration or contribution, compose the financial

assets.

2- For 100% of the project, the total investment was R$297.9 million, of which R$88.9 million is related to the portion of the Concessionaire and R$209.0 million

to the Granting Authority.

3- Includes CCR, MTH, CPC, SPCP and eliminations.

2Q15 2Q15 2Q15 2Q15

AutoBAn 21.8 3.4 25.2 2.5 0.0

NovaDutra 24.3 3.7 28.0 19.1 0.0

ViaOeste 14.4 1.7 16.2 4.5 0.0

RodoNorte (100%) 29.2 1.2 30.4 6.3 0.0

Ponte 0.0 0.1 0.1 0.1 0.0

ViaLagos 10.7 2.0 12.8 2.3 0.0

SPVias 15.0 1.4 16.4 8.7 0.0

ViaQuatro (58%) 17.7 0.9 18.6 0.0 3.4

Renovias (40%) 0.3 0.2 0.6 1.0 0.0

RodoAnel (100%) 0.5 0.6 1.0 0.0 0.0

SAMM 0.1 6.8 6.8 0.0 0.0

ViaRio2 (33.33%) 29.3 0.0 29.3 0.0 0.0

Quito 8.5 0.6 9.1 0.0 0.0

San José 9.4 0.1 9.5 0.0 0.0

Curaçao 3.7 0.0 3.7 0.0 0.0

Barcas 1.4 0.1 1.4 0.0 0.0

VLT (24.88%) 13.0 2.3 15.3 0.0 13.6

Metrô Bahia 309.0 1.0 310.0 0.0 42.5

BH Airport 26.5 2.0 28.5 0.0 0.0

MSVia 155.8 26.8 182.7 0.0 0.0

STP (34.24%) 2.8 23.9 26.7 0.0 0.0

Other3 0.3 4.2 4.5 0.0 0.0

Consolidated 693.9 82.8 776.7 44.4 59.4

R$ MM

Intangible AssetsPerformed

maintenance

ImprovementsEquipments and

OthersTotal Maintenance Cost

2Q15

Proforma Financial

Asset1