presented by: robert s. keebler, cpa, mst, aep baker tilly virchow krause, llp phone: (920) 739-3345...

TRANSCRIPT

PRESENTED BY:

Robert S. Keebler, CPA, MST, AEPBaker Tilly Virchow Krause, LLP

Phone: (920) 739-3345

Fax: (920) 733-6022

[email protected]© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved. 1

Strategies to Use Tax Carryforwards

> Capital loss carryforwards

> Passive activity loss carryforwards

> Charitable contribution carryforwards

> Investment interest expense carryforwards

> Foreign tax credit carryforwards

Strategies to Use Tax CarryforwardsOverview

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved. 2

Capital Loss Carryforwards

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved. 3

> In general, to the extent that a taxpayer has a capital loss (either short-term, long-term or both) in the current tax year, he/she may deduct the loss to the extent of any capital gain incurred in the current tax year.

> To the extent that the taxpayer has a net capital loss (after the offsetting against other capital gains), he/she may deduct up to an additional $3,000 of capital loss against other ordinary income in the current tax year.

> To the extent that there is a surplus capital loss (after taken into consideration the $3,000 “excess” deduction), the net capital loss carries forward to future tax years.

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Capital Loss CarryforwardsOverview

4

> The present value of the tax benefit associated with a capital loss carryforward is significantly diminished if it takes several tax years before the taxpayer can fully recognize the entire loss

> A capital loss carryforward ceases at death of the taxpayer

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Capital Loss CarryforwardsIssues

5

> Premium bond trade

> No-load mutual fund sale

> Deep-in-the-money calls

> Investment partnerships

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Capital Loss CarryforwardsCarryforward Utilization Strategies

6

> Objective> Convert ordinary income into capital gain income while utilizing

current capital loss carryforwards.

> Strategy> Sell an existing corporate bond (or U.S. Treasury bond) nearing its

maturity date, which is trading at a premium, followed by a repurchase of that same security (or a similar security).

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Capital Loss CarryforwardsStrategy #1 - Premium Bond Trade

7

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

On January 1, 2007, John purchased $1,000,000 worth of ABC Corp. bonds at par value. The bonds have a 5% stated interest rate (payable annually on December 31st) and mature on December 31, 2009. On January 2, 2009, the prevailing market rate of interest for similar bonds drops to 1.9417%, increasing the value of the ABC corporate bonds to 1.03 (i.e. $1,030,000).

Now let’s assume that John has a $250,000 capital loss carryforward from 2008 and decides to sell his ABC Corp. bond on January 2, 2009, for $1,030,000 (incurring a long-term capital gain of $30,000). On the next trading day, John repurchases the same bonds for $1,030,000, reflecting a $30,000 premium over their value on the maturity date. Under tax law, this $30,000 premium can be used to offset John’s interest income of $50,000 over the remaining life of the bond.

Given the assumptions above, and that John is in the 35% ordinary income tax bracket, the following slide summarizes the income tax results as of 12/31/2009:

Capital Loss CarryforwardsStrategy #1 - Premium Bond TradeExample

8

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Capital Loss CarryforwardsStrategy #1 - Premium Bond TradeExample (cont.)

No

Planning With

Planning Interest income ($1,000,000 x 5%) $50,000 $50,000 Less: Bond premium amortization - 0 - 30,000 Net interest income $50,000 $20,000 Long-term capital loss - $3,000 - $3,000 Taxable income $47,000 $17,000 Ordinary income tax @ 35% $16,450 $5,950 Capital gains tax @ 15% 0 0 Total income tax liability $16,450 $5,950 INCOME TAX SAVINGS (Proof: ($47,000 - $17,000) x 35%)

$10,500

9

> Objective> Convert potential ordinary income into capital gain income while

utilizing current capital loss carryforwards.

> Strategy> Sell existing mutual fund shares (or similar marketable securities),

which are nearing their ex-dividend date, at a premium followed by a repurchase of the same securities (or similar securities) at a lower price after the ex-dividend date.

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Capital Loss CarryforwardsStrategy #2 – No-Load Mutual Fund Sale

10

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

On January 1, 2008, Jackie purchased 10,000 shares of LMN Growth & Income Fund (“LMN”), a no-load mutual fund, at $50/share ($500,000 total investment). On July 1, 2009, LMN declared its annual ordinary dividend (0% qualified) of $3/share to be paid on August 14, 2009, to the shareholders of record as of July 31, 2009. On July 27, 2009, the day prior to going ex-dividend, LMN’s current trading price was $53/share. Two days later, LMN was trading ex-dividend at $50/share.

Assuming Jackie has a $100,000 capital loss carryforward from 2008, let’s assume Jackie has two choices. The first choice is for Jackie to hold on to LMN and collect the $30,000 ordinary dividend (10,000 shares x $3/share dividend). The second choice would be for Jackie to sell LMN on the day before it goes ex-dividend at $53/share and then buy it back two days later when LMN’s current price drops to $50/share.

Given the assumptions above, and that Jackie is in the 35% ordinary income tax bracket, the following slide summarizes the income tax results as of 12/31/2009:

Capital Loss CarryforwardsStrategy #2 – No-Load Mutual Fund SaleExample

11

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

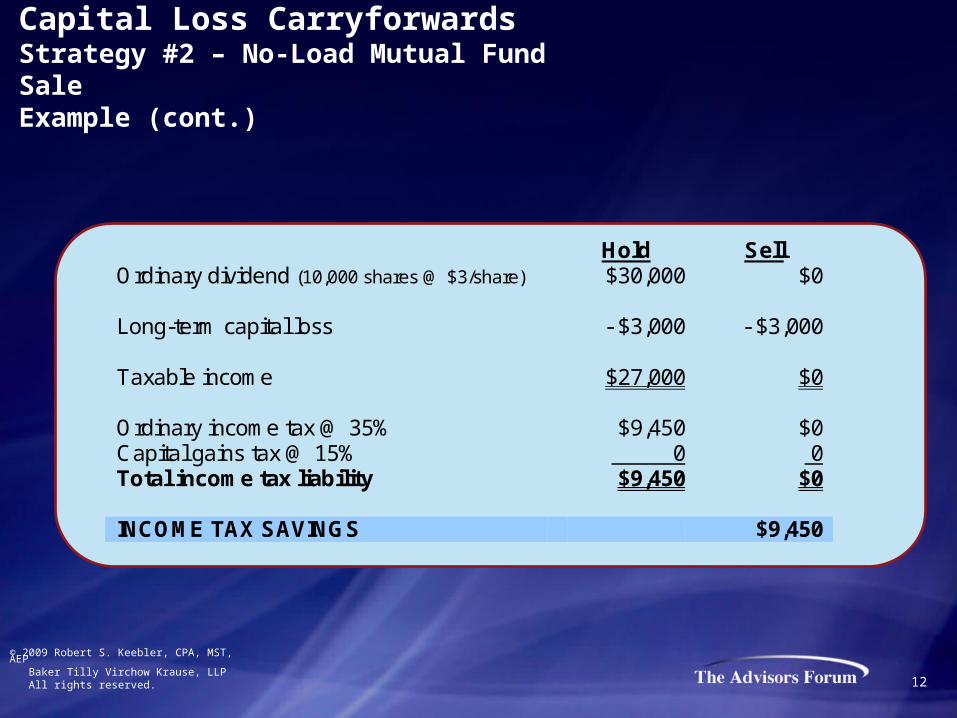

Hold Sell Ordinary dividend (10,000 shares @ $3/share) $30,000 $0 Long-term capital loss - $3,000 - $3,000 Taxable income $27,000 $0 Ordinary income tax @ 35% $9,450 $0 Capital gains tax @ 15% 0 0 Total income tax liability $9,450 $0 INCOME TAX SAVINGS $9,450

Capital Loss CarryforwardsStrategy #2 – No-Load Mutual Fund SaleExample (cont.)

12

> Objective> Utilize current capital loss carryforwards while making a modest

profit free of income tax.

> Strategy> Purchase a publicly-traded stock (or use an existing stock) followed

by the sale of a “deep-in-the-money” call option on that same stock. The premium received on the sale of the call option will subsidize a portion of the purchase price of the underlying stock.

> For purposes of this illustration, a “deep-in-the-money” call option is one in which the current value of the stock is significantly less than the option’s strike price (e.g. greater than 30%).

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Capital Loss CarryforwardsStrategy #3 – Deep-in-the-Money Calls

13

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

On April 7, 2009, Jim purchases 1,000 shares of ABC Corp. stock at $20/share ($20,000 total purchase price). On that same day, Jim writes call options on the 1,000 shares with a strike price of $10/share and an exercise date of October 23, 2009. The total amount Jim received on the sale of the call options was $11,000 ($11/share x 1,000 shares).

Now, let’s assume that the stock price of ABC Corp. stock rises to $24/share on October 23, 2009. The purchaser of the call options will purchase the ABC Corp. stock at a significant discount while Jim will make a small profit on the overall transaction. This is illustrated on the following slide:

Capital Loss CarryforwardsStrategy #3 – Deep-in-the-Money CallsExample 1

14

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

NOTE: The value of the call option has two components, an intrinsic value (the difference between the strike price and the current value of the stock) and a time value reflecting the possibility that the spread could increase in the future. The net profit is limited to the time value component. Thus, the higher the time value of a call is as a percentage of a stock’s value, the higher the potential profit.

Stock Purchase Price (1,000 sh. @ $20/sh.) 20,000$ Less: Amount Received on Call Option Sale (1,000 sh. @ $11/sh.) (11,000) Net Cash Outlay 9,000$

Amount Received on Sale of Stock (1,000 sh. @ $10/sh.) 10,000$ Less: Net Cash Outlay (9,000) Net Profit/(Loss) 1,000$

Capital Loss CarryforwardsStrategy #3 – Deep-in-the-Money CallsExample 1 (cont.)

15

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

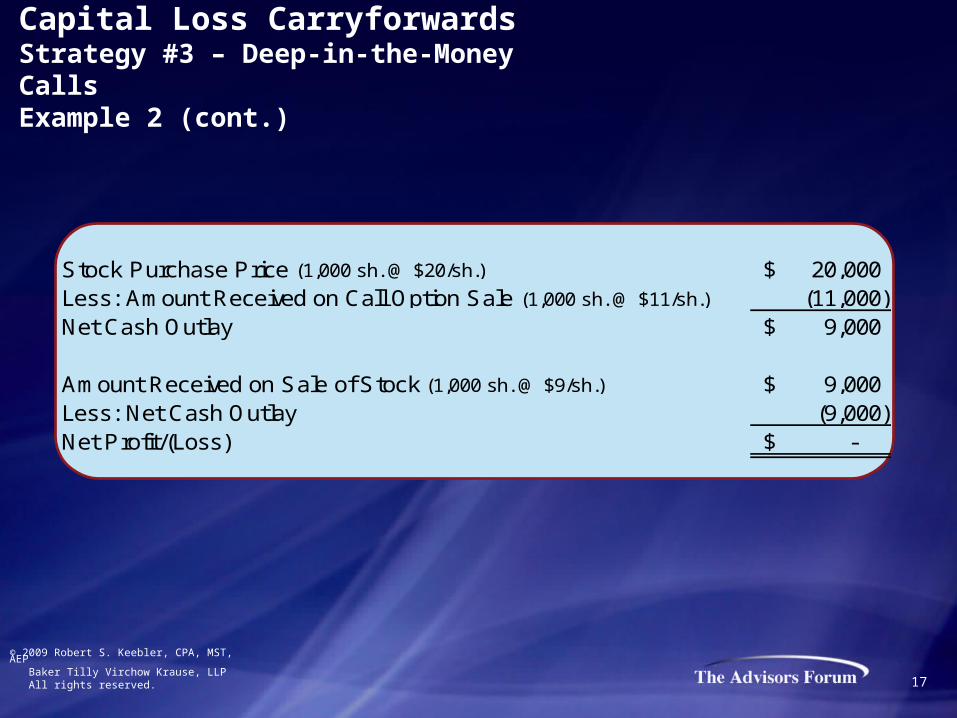

Assume the facts from Example 1, except that the stock price of ABC Corp. falls to $9/share on October 23, 2009. In this case, the purchaser of the call option would not exercise the option on October 23, 2009, in that the current price ($9) is less than the strike price ($10). Further, Jim will not make any profit on this transaction in that the price he receives for the stock ($9,000) is the same as his net cash outlay or, what amounts to the same thing, the total amount he receives ($9,000 sale proceeds + $11,000 option premium ) equals the $20,000 he paid for the stock.

Capital Loss CarryforwardsStrategy #3 – Deep-in-the-Money CallsExample 2

16

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Stock Purchase Price (1,000 sh. @ $20/sh.) 20,000$ Less: Amount Received on Call Option Sale (1,000 sh. @ $11/sh.) (11,000) Net Cash Outlay 9,000$

Amount Received on Sale of Stock (1,000 sh. @ $9/sh.) 9,000$ Less: Net Cash Outlay (9,000) Net Profit/(Loss) -$

Capital Loss CarryforwardsStrategy #3 – Deep-in-the-Money CallsExample 2 (cont.)

17

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

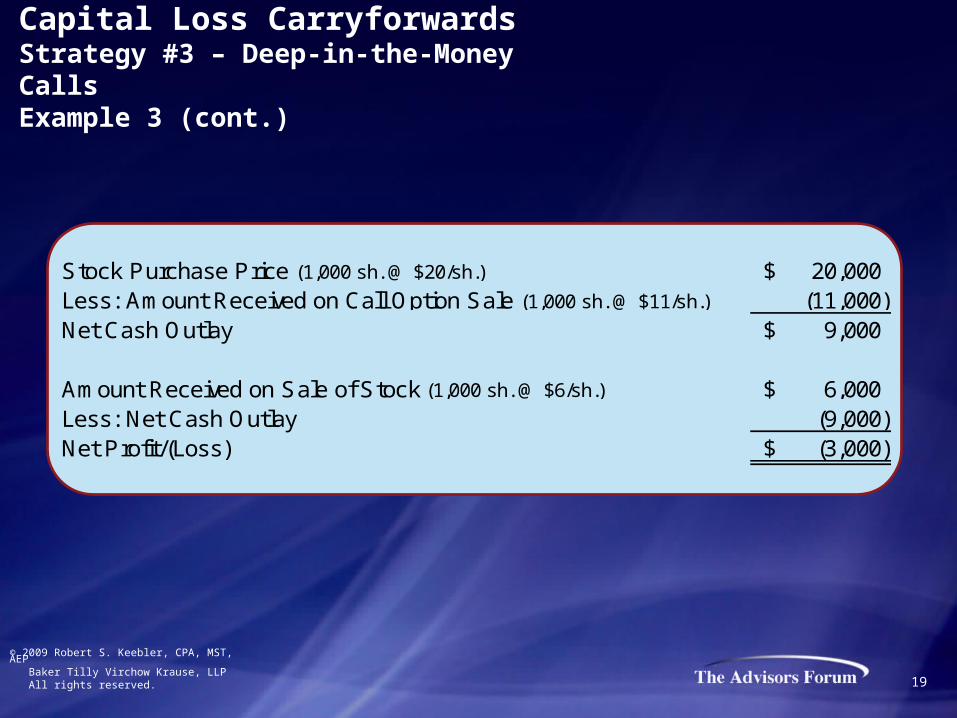

Assume the facts from Example 1, except that the current price of ABC Corp. falls to $6/share over the six month term of the call option. In this situation, Jim will suffer a loss because the total amount he receives ($6,000 + $11,000 = $17,000) is $3,000 less than the $20,000 he paid for the stock.

Capital Loss CarryforwardsStrategy #3 – Deep-in-the-Money CallsExample 3

18

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Stock Purchase Price (1,000 sh. @ $20/sh.) 20,000$ Less: Amount Received on Call Option Sale (1,000 sh. @ $11/sh.) (11,000) Net Cash Outlay 9,000$

Amount Received on Sale of Stock (1,000 sh. @ $6/sh.) 6,000$ Less: Net Cash Outlay (9,000) Net Profit/(Loss) (3,000)$

Capital Loss CarryforwardsStrategy #3 – Deep-in-the-Money CallsExample 3 (cont.)

19

> Objective> Convert ordinary income into capital gain income while utilizing

current capital loss carryforwards.

> Strategy> Purchase an interest in a limited partnership, such as a

commercial rental real estate partnership, where taxable income is low (due to depreciation), but partner distributions are high.

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Capital Loss CarryforwardsStrategy #4 – Investment Partnerships

20

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

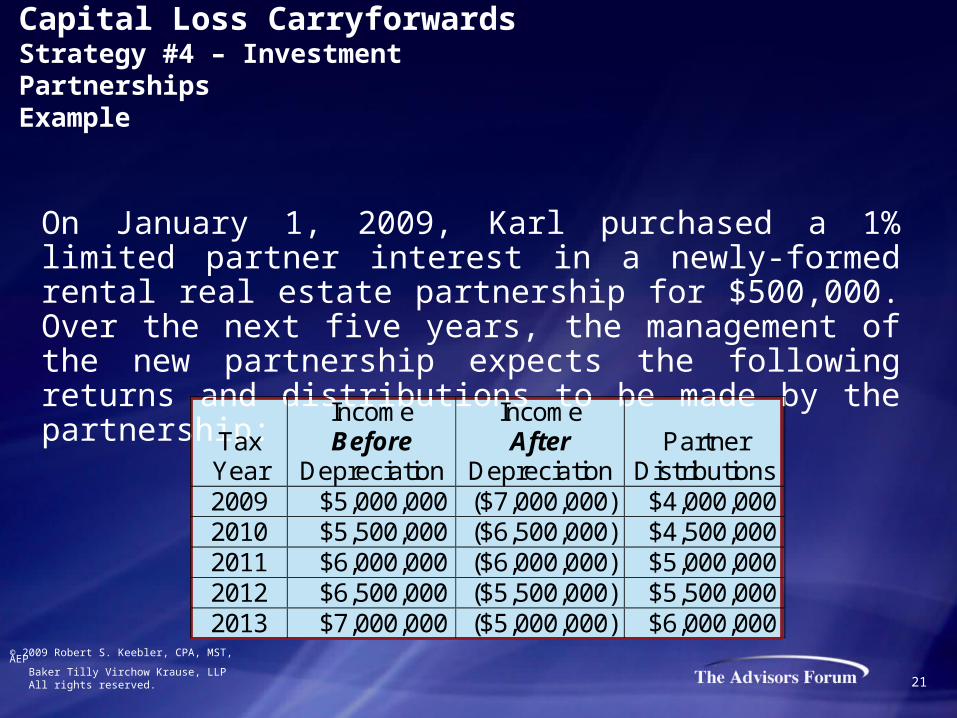

On January 1, 2009, Karl purchased a 1% limited partner interest in a newly-formed rental real estate partnership for $500,000. Over the next five years, the management of the new partnership expects the following returns and distributions to be made by the partnership:

Tax Year

Income Before

Depreciation

Income After

Depreciation Partner

Distributions 2009 $5,000,000 ($7,000,000) $4,000,000 2010 $5,500,000 ($6,500,000) $4,500,000 2011 $6,000,000 ($6,000,000) $5,000,000 2012 $6,500,000 ($5,500,000) $5,500,000 2013 $7,000,000 ($5,000,000) $6,000,000

Capital Loss CarryforwardsStrategy #4 – Investment PartnershipsExample

21

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

*NOTE: No loss would be recognized under the passive activity rules in that Karl held a limited partner interest and he did not materially participate in the management of the partnership. Therefore, Karl could only deduct losses from the rental real estate partnership only to the extent he has other passive income or disposes of his partnership interest.

Tax Year

Ordinary Income* Capital Gain

Partnership Cost Basis

2009 $0 ($3,000) $390,000 2010 $0 ($3,000) $280,000 2011 $0 ($3,000) $170,000 2012 $0 ($3,000) $60,000 2013 $0 ($3,000) $0

Using the facts from the previous slide and that Karl has an $80,000 capital loss carryforward, below is a summary of the taxable income Karl would report and his cost basis in the partnership each year:

Capital Loss CarryforwardsStrategy #4 – Investment PartnershipsExample (cont.)

22

Passive Activity Loss Carryforwards

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved. 23

> Generally, to the extent that a taxpayer has a loss from a “passive activity”, the taxpayer may recognize this loss to the extent that the taxpayer has “passive income” from another source.

> In addition, a taxpayer may recognize a current year loss, along with all prior year suspended losses, on a “passive activity” in the tax year in which the activity is fully disposed of and/or liquidated.

> Further, a special rule applies to rental real estate activities where there is “active participation”.

> In this case, a taxpayer may deduct up to a $25,000 loss each year (provided the taxpayer’s modified AGI is less than $100,000).

> To the extent a taxpayer cannot use a “passive activity” loss in the current tax year, this loss may be carried forward indefinitely to future tax years.

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Passive Activity Loss CarryforwardsOverview

24

> The present value of the tax benefit associated with a “passive activity” loss carryforward is significantly diminished if it takes several tax years before the taxpayer can fully recognize the entire loss

> The “passive activity” loss carryforward ceases at death of the taxpayer

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Passive Activity Loss CarryforwardsIssues

25

Charitable Contribution Carryforwards

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved. 26

> Contributions of property - Basic rule> Deduction is the fair market value of the property

> Exceptions> Non-Capital Gain Property

> Tangible Property/Unrelated Use

> Private Foundation Donee

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Charitable Contribution CarryforwardsOverview

27

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Charitable Contribution CarryforwardsOverview (cont.)

Method Used to Determine

Tax Deduction AGI Limitation

Method Used to Determine

Tax Deduction AGI Limitation

Method Used to Determine

Tax Deduction AGI LimitationCash FMV 50% FMV 50% FMV 30%Appreciated Property (Publicly-Traded Stock, Land, etc…) FMV 30% FMV 30% FMV 20%Appreciated Property (Closely-Held Stock) FMV 30% FMV 30% Basis 20%

Public Charity Supporting Organization Private Foundation

28

> To the extent that the taxpayer has insufficient AGI to utilize all of his/her current year’s charitable deductions, he/she may carryforward the current year’s excess up to five years.

> The ordering of the deduction allowance is as follows:> Current year (2009) deductions

> 5th previous year (2004) deductions

> 4th previous year (2005) deductions

> 3rd previous year (2006) deductions

> 2nd previous year (2007) deductions

> Prior year (2008) deductions

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Charitable Contribution CarryforwardsOverview (cont.)

29

> The present value of the tax benefit associated with charitable contribution carryforward is significantly diminished if it takes a few tax years before the taxpayer can fully recognize the entire loss

> The charitable contribution carryforward lapses after the five-year statutory period

> The charitable contribution carryforward ceases at death of the taxpayer

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Charitable Contribution CarryforwardsIssues

30

Investment Interest Expense Carryforwards

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved. 31

> Typically, to the extent that a taxpayer has an interest expense associated with debt used to acquire investment assets (e.g. stock), he/she may deduct this expense (as an itemized deduction) to the extent he/she has “net investment income” (e.g. interest, non-qualified dividends, rents, royalties, short-term capital gains, etc).

> To the extent a taxpayer cannot utilize his/her entire investment interest expense in the current tax year, he/she may carryforward the excess expense indefinitely to future tax years when there is “net investment income”.

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Investment Interest Expense CarryforwardsOverview

32

> The present value of the tax benefit associated with an investment interest expense carryforward is significantly diminished if it takes several tax years before the taxpayer can fully recognize the entire expense

> The investment interest expense carryforward ceases at death of the taxpayer

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Investment Interest Expense CarryforwardsIssues

33

Foreign Tax Credit Carryforwards

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved. 34

> In general, to the extent that a U.S. taxpayer must pay an income tax both to a foreign country and the U.S. on a specific source of income, a taxpayer is allowed a tax credit, on his/her U.S. income tax return, on the foreign taxes paid or accrued (provided such foreign-sourced income is included on the taxpayer’s U.S. income tax return)

> There are special limitations on the amount of the available tax credit based on the type of income (e.g. passive, general, lump-sum distribution, etc) and the percentage of the foreign-sourced income compared to U.S-sourced income

> The foreign tax credit may be carried back one year and carried forward ten years

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Foreign Tax Credit CarryforwardsOverview

35

> The present value of the foreign tax credit carryforward is significantly diminished if it takes several tax years before the taxpayer can fully recognize the entire credit

> The foreign tax credit lapses after the ten-year carryforward period

> The foreign tax credit carryforward ceases at death of the taxpayer

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved.

Foreign Tax Credit CarryforwardsIssues

36

THANK YOU

FOR EDUCATIONAL PURPOSES ONLY.

Although effort was taken to ensure the accuracy of these materials Robert S. Keebler and Baker Tilly Virchow Krause, LLP assume no responsibility or liability for an individual’s reliance on these materials.

© 2009 Robert S. Keebler, CPA, MST, AEP Baker Tilly Virchow Krause, LLP All rights reserved. 37