preventing customer churn in the mobile telecommunication

TRANSCRIPT

Full Terms & Conditions of access and use can be found athttps://www.tandfonline.com/action/journalInformation?journalCode=wjab20

Journal of African Business

ISSN: 1522-8916 (Print) 1522-9076 (Online) Journal homepage: https://www.tandfonline.com/loi/wjab20

Preventing Customer Churn in the MobileTelecommunication Industry: Is Mobile MoneyUsage the Missing Link?

Eric Yeboah-Asiamah, Bedman Narteh & Mahmoud Abdulai Mahmoud

To cite this article: Eric Yeboah-Asiamah, Bedman Narteh & Mahmoud Abdulai Mahmoud (2018)Preventing Customer Churn in the Mobile Telecommunication Industry: Is Mobile Money Usage theMissing Link?, Journal of African Business, 19:2, 174-194, DOI: 10.1080/15228916.2018.1440462

To link to this article: https://doi.org/10.1080/15228916.2018.1440462

Published online: 26 Feb 2018.

Submit your article to this journal

Article views: 261

View Crossmark data

RESEARCH PAPER

Preventing Customer Churn in the Mobile TelecommunicationIndustry: Is Mobile Money Usage the Missing Link?Eric Yeboah-Asiamah , Bedman Narteh and Mahmoud Abdulai Mahmoud

Department of Marketing & Entrepreneurship, University of Ghana Business School, Accra, Ghana

ABSTRACTThe paper examines the influence of mobile money usage on custo-mer continuance intention (CCI). The study conveniently sampled507 mobile money users to test the research model using PLS-SEM.Satisfaction, trust and active usage of mobile money were found toinfluence CCI. Active usage of mobile money was also confirmed as amediator in the relationship between satisfaction and trust, on cus-tomer continuance. The study thus validated a theoretical model ofcustomer continuance intention as it relates to mobile money usage.It has also provided a new perspective on managing customer churnin an emerging market.

KEYWORDSMobile money; continuanceintention; satisfaction; trust;active usage; churn; mobiletelecommunication; third-party mediator

1. Introduction

The recent proliferation of mobile technology has resulted in easy access to mobilephones and has therefore reduced communication costs in many parts of the develop-ing world. The rapid growth pace, coupled with increased competition within thetelecommunications industry and the saturation of markets, come with the primechallenge of customer churn: losing customers, often to the competition (Hwang,Taesoo, & Euiiho, 2004). Essentially, all industries, irrespective of type and size, inone way or the other, experience voluntary churn – the decision by the customer toswitch to another company or service provider (Kuusik & Varblane, 2009). This isparticularly true for telecommunication companies where the average annual churn rateranges between 10% and 67% (Hughes, 2007).

In a developing country like Ghana, the mobile telecommunication industry thriveson the presence of mobile operators often referred to as “telecommunication compa-nies” or “TELCOs.” Mobile services from a particular operator are provided to thecustomer when a SIM card is inserted into the mobile device. Airtime can then bepurchased from agents and retailers for calls and data, which fuels social mediaapplications such as Whatsapp (www.web.whatsapp.com) and Facebook (www.facebook.com). Customers in Ghana often possess multiple SIM cards from one or moremobile operators, taking advantage of the promotional benefits offered by each. Arecent policy from the industry regulator, the National Communications Authority(NCA), has allowed customers to switch from one service provider to another (Nimako,

CONTACT Bedman Narteh [email protected]

JOURNAL OF AFRICAN BUSINESS, 2018VOL. 19, NO. 2, 174–194https://doi.org/10.1080/15228916.2018.1440462

© 2018 Informa UK Limited, trading as Taylor & Francis

Ntim, & Mensah, 2014) while retaining the same mobile number. This policy, referredto as mobile number portability, has thus worsened churn rates within the industry inGhana (ibid) as customers can change service providers without the perceived barrier oflosing their phone number (Shin & Kim, 2008).

Extant literature argues that customer churn leads to increased costs, which result notonly from the loss of revenue from current customers, but also from the additional cost ofacquiring new ones (Svendsen & Prebensen, 2013). In both cases, organizations are worseoff when customer churn occurs. Moreover, previous studies also argue that retaining 5%of customers could lead to about 60% increase in profit (Reichheld, 1996). This suggeststhat the key factor underpinning the long-term success of a business is its ability toincrease and retain loyal customers. Recent marketing emphasis is thus being shiftedfrom winning new customers to retaining existing ones (Kuusik & Varblane, 2009).

As mobile phone penetration increases, one key innovation in the Ghanaian tele-communication sector is the technology-enabled service which allows consumers to usemobile phones to perform financial transactions (Abor, Amidu, & Issahaku, 2018;Humbani& Wiese, 2017). Widely known as mobile money, the phenomenon consistsof a mobile operator acting as an e-money service provider (Lal & Sachdev, 2015;PricewaterhouseCoopers, 2016). Physical cash is given to an authorized mobile moneyagent who transfers the virtual equivalent into the customer’s phone wallet. This virtualcash can then be used to pay for products and services, be transferred to other users, oragain be extracted as physical cash from an agent. The mobile operator, on whoseplatform the system is run, receives a specified percentage of each transaction as fees.More than half a billion registered mobile money accounts globally were recorded as atend of 2016 (GSMA, 2017), and mobile money is now available in two-thirds of low andmiddle-income countries via 277 service providers (ibid).

Moreover, Sub-Saharan Africa continues to account for the majority of mobilemoney services (PwC, 2016), and Ghana – now one of the leading mobile moneymarkets in the world (GSMA, 2017) – has seen astronomical growth in mobile moneyusage since its introduction in 2009 (GhanaWeb, 2017). By the end of March 2017, atotal number of 20,500,470 customers were registered for mobile money services,representing 52.25% of the customer base of four mobile operators in the country,namely MTN, Tigo, Airtel and Vodafone (Bank of Ghana, 2017). Out of the registeredcustomers, 9,262,376 are active mobile money customers, meaning that they use theirmobile account frequently. The records for the total volume of transactions are equallyremarkable, with 198,236,640 transactions representing a 97% growth over the sameperiod in 2016. Total transaction value and balances on float stood at Ghc78,508.90bn($18,895.48bn) and Ghc1,257.40bn ($302.63m) respectively, with growth rates 121.5%and 129.47% in 2016(Bank of Ghana, 2017).

Despite the growing interest among academic and practitioner communities aroundthe world in the ways through which mobile money can be sustained and fullyharnessed (Bongomin, Ntayi, Munene, & Malinga, 2018; Gosavi, 2017), limited researchhas been devoted to investigating it. The scarce research on mobile money has focusedon behavioral intentions to adopt mobile money services (Humbani & Wiese, 2017;Narteh, Mahmoud, & Amoh, 2017), home economics of e-money (Mbiti & Weil, 2013),the mechanics and potential economic impact of M-pesa (Jack & Suri, 2010), the use ofmobile money to promote financial inclusion of the world’s poor (Abor et al., 2018),

JOURNAL OF AFRICAN BUSINESS 175

and the usage and impact of transformational mobile financial services (Morawczynski,2009). Although these lines of research have contributed vital knowledge toward ourunderstanding of the mobile money phenomenon, pertinent gaps still exist in theliterature. Notably limited in the prevailing literature is the critical role mobile moneycan play in influencing customers’ continuance intention toward a service provider inthe face of increasing competition across markets (Wamuyu, 2014).

Several scholars (Bhattacherjee, 2001; Bhattacherjee& Lin, 2014; Zhou, 2013)have emphasized the importance of continuance intention, stating that the essen-tial value of technology-enabled services, such as mobile money, is fully realized,not when it is adopted, but rather when there is continuous usage. Consequently,there exist numerous questions that remain unanswered, especially concerningmobile money’s ability to influence customer continuance. Furthermore, theimportance of factors like satisfaction and trust on the sustenance of servicerelationships has been underscored by various researchers (e.g., Morgan & Hunt,1994). Especially in technology-enabled environments where perceived risks arehigh (Zhou, 2013), consumers’ intention to continue patronage of a servicedepends largely upon their positive disconfirmations (Kuo, Wu, & Deng, 2009)and their assurance of the safety of their money. However, even high levels ofsatisfaction and trust may still be inadequate to encourage continuance in acustomer who is a relative stranger to the technological environment(Bhattacherjee, 2001; Roos & Gustafsson, 2011). Active usage of the service plat-form is therefore also an important factor to consider.

The current study therefore aims primarily to investigate the question, “How much dosatisfaction, and trust influence customers’ intention to stay with their mobile operator?”Additionally, the study seeks to examine how (the) active usage of mobile money servicesmediates the relationships between satisfaction and customer’s continuance intention,and between trust and customers’ continuance intention.

The information system (IS) Post-Acceptance Model (PAM) developed byBhattacherjee (2001) was therefore adapted for the study, testing the effects ofsatisfaction, trust, and the active usage of mobile money services on customers’continuance intention. In the modified PAM, active usage of mobile money also actsas a mediator in the relationship between satisfaction and trust on the continuanceintention in the research model. Bhattacherjee (2001) first developed IS PAM forinvestigation into user continuance intention toward IS. The model was adaptedfrom Davis (1989) technology acceptance model (TAM) and Oliver’s (1980) expec-tation-confirmation theory (ECT), and has been validated in different settings(Chen, Chen, Lin, & Chen, 2011; Gao & Bai, 2014). The modified PAM modelwas suitable for the study because the dependent variable captures the fundamentalpurpose of the study, which is to determine customer continuance intentions towarda service provider as a result of active usage of mobile money.

The paper proceeds as follows. The theoretical background, research model, andresearch methodology are discussed. The next sections then present the results of thedata analysis and a discussion of the study’s findings, proceeded by the theoretical andmanagerial implications of the results. Finally, we discuss possible study limitations,and directions for future research.

176 E. YEBOAH-ASIAMAH ET AL.

2. Theoretical background

As indicated earlier, the theoretical basis for this research comes from the work ofBhattacherjee (2001) who adapted Davis (1989) technology acceptance model (TAM)and Oliver’s (1980) expectation-confirmation theory (ECT) to the field of post-accep-tance of computer technology, adapting the mixed pre/post consumption ECT model toa pure post-acceptance IS model. A core tenet of the continuance theory holds that auser’s continuance with a technology is contingent on a conscious decision to operate ina given way (Bhattacherjee& Lin, 2014). PAM asserts that once a user accepts and uses atechnology, he or she will form an initial opinion about the confirmation or disconfir-mation of their expectancies. In situations where the expectations are confirmed, theuser will form opinions about the benefits of the technology. Ultimately, both theconfirmation and the benefits will affect their satisfaction with the service and even-tually the satisfaction will impact their desire to continue to use the technology with thesame service provider (Bhattacherjee, 2001).

PAM advances our understanding of user continuance intention since it offers aconvincing case for an explicit distinction between the user’s preliminary acceptanceand durable use of a technology-enabled service, whilst presenting a baseline theoreticalmodel for assessing customers’ continuance with service providers. In the extant litera-ture, various factors are postulated to affect the user’s continuance with a technology-enabled service and service providers have been investigated. Notable among them aretrust (Gefen, Karahanna, & Straub, 2003; Qureshi et al., 2009), satisfaction (Bhattacherjee,2001; Limayem, Hirt, & Cheung, 2007), usage (Liao, Palvia, & Chen, 2009); and habit(Bhattacherjee & Lin, 2014; Limayem & Cheung, 2008).

Additionally, Ajzen and Fishbein’s (2000) theory of planned behavior (TPB)suggests that the frequent performance of a certain behavior (in this case activeusage) leads to the formation of habit, which influences subsequent behavior with-out conscious cognitive negotiation. By implication, an active customer is morelikely to remain in a relationship because such a customer has accumulated more(conscious) reasons for remaining in the relationship (Cioffi & Garner, 1996).Further, Roos and Gustafsson (2011) established that individual switching historiesare longer in case of passive customers, and that switching is less frequent whencustomers are more active (Roos & Gustafsson, 2011).Thus, to effectively enhancethe explanation of continuance usage behavior as far as staying with service provi-ders are concerned, trust and active usage of mobile money are added toBhattacherjee’s (2001) post-acceptance model of IS continuance in the currentpaper, as indicated in Figure 1.

3. Development of research model and hypotheses

Figure 1 illustrates the proposed relationships between satisfaction, trust, active mobilemoney usage, and customer continuance intention. This framework has two maincomponents. The initial objective is to analyze the influences of each of the twoindependent variables on customers’ continuance intention. Second, the study assessesthe mediation effect of active usage of mobile money services on the relationship

JOURNAL OF AFRICAN BUSINESS 177

between satisfaction and trust on a customer’s continuance intention toward a serviceprovider. Finally, hypotheses of the study are developed from the framework.

3.1. Customer satisfaction

In a consumer behavior context, customer satisfaction is considered the foundation toacquiring and maintaining a loyal base of stable customers (Oliver, 1993). In the case oftechnology-enabled services such as mobile money, Kuo et al. (2009) posited satisfac-tion as the reflection of positively aggregated feelings that are developed by/throughmultiple dealings with the service.

PAM, which is developed from the expectation confirmation theory (ECT), offers anexplanation on the generation of satisfaction in consumers (Bhattacherjee, 2001). Thetheory postulates that the relationship, between an individual’s initial expectations andthe results obtained by a service, largely determines the degree of satisfaction. By implica-tion, satisfaction is influenced by the difference between what a consumer wants and whathe/she attains. Further extension of this logic postulates that, should customers perceivesatisfaction from finding their wants fulfilled with/by the mobile money service, they arelikely to continue using the service to accomplishing the task. The opposite is also true,meaning that when a customer fails to achieve what he/she wants from a mobile moneyservice, the likelihood that the customer will discontinue to use the service is high, becausethe customer will have formed a negative attitude toward the service. The extant literaturehas adequately validated the assertion that satisfaction serves as an instrument to engenderuser continuance with a service (see e.g., Bhattacherjee, 2001; Bhattacherjee& Lin, 2014;Kuo et al., 2009; Liu, Guo, & Lee, 2011). Drawing on previous literature, we expectsatisfaction to affect continuance intention and active usage of mobile money services,because a contented user will continue to use the service for his or her target task(s) andremain satisfied with the service provider. (Liu et al., 2011; Zhou, 2013).

Hence we hypothesize that:

H1: Customer satisfaction positively influences customer continuance intention

H2: Satisfaction positively influences active usage of mobile money services

Satisfaction (SAT)

Trust (TRT)

Mobile Money Active Usage

(MMAU)

Customer Continuance

Intention (CCI)

H1

H2

H5

H3

H4

Figure 1. Conceptual Model for the Study (Modified PAM).

178 E. YEBOAH-ASIAMAH ET AL.

3.2. Customer trust

Based on Morgan and Hunt’s (1994) interpretation of the construct, we define trust inthis study as the “extent of confidence in the exchange partner’s reliability and integ-rity” (Morgan & Hunt, 1994, p. 23). For the purpose of this study, trust in a mobilemoney service signifies (a) trust in the brand itself, as one with which customers will becontented/satisfied to entrust their funds; (b) trust that the technology for servicetransmission will function as promised; (c) trust that agents will do what is requiredwith regards to customer funds and transactions; and (d) trust that individual activitiesand transactions will be fulfilled to expectation (Lal & Sachdev, 2015).

Given the recent relational orientation emerging in marketing activities, trust hasbecome a key variable in the development of an enduring desire to maintain arelationship in the long term (Morgan & Hunt, 1994; Yeboah-Asiamah, Nimako,Quaye, & Buame, 2016). Trust was added to the original IS PAM because theliterature has established that in certain circumstances, service providers may notbe able to retain even those customers who are satisfied (e.g., Heskett, Jones,Loveman, Sasser, & Schlesinger, 1994; Ranaweera & Prabhu, 2003; Schneider &Bowen, 1999), suggesting that satisfaction alone is not enough to ensure long-termcustomer continuance and commitment. Looking beyond satisfaction to identifyother variables that develop and strengthen commitment in order to ensure eco-nomically viable, long-term relationships is often the right approach (Hart &Johnson, 1999; Morgan & Hunt, 1994), especially with mobile technology-enabledservices such as mobile money which are built on a significant level of uncertaintyand risk (Zhou, 2013). Trust affects active usage and influences positive intentionstoward mobile money service, because a user’s confidence in a service will foster acontinued relationship of frequent usage and an eventual delay in leaving the serviceprovider (Benamati, Fuller, Serva, & Baroudi, 2010; Luo, Li, Zhang, & Shim, 2010).Hence we hypothesize that:

H3: Trust positively influences customer continuance intention

H4: Trust positively influences active usage of mobile money services

3.3. Continuance intention and active usage of mobile money

The continued usage of technology-enabled services such as mobile money, ratherthan just the early acceptance, is what determines its success or otherwise.Bhattacherjee and Lin (2014) suggest that a technology-enabled service is notsuccessful if its application is not reinforced by the persons who seek to benefitfrom its offerings. By implication, the ability of a telecommunication service provi-der to maintain its existing customers in the long-term is reliant on knowledge ofthe factors that foster or constrain users’ continuance intentions toward the service(Akter et al., 2011). For the purpose of this study, customer continuance is definedas a customer’s self-reported determination to remain with his/her (the) currenttelecommunication mobile money service provider and use their technology-enabledservices over similar available services.

JOURNAL OF AFRICAN BUSINESS 179

The industry’s benchmark for active users of mobile money refers to the number ofcustomers who transacted or performed any activity on amobile money account at least oncewithin the 90 days prior to selection of targeted respondents (Bank of Ghana, 2017). Activeusage was added to the original IS PAM because several scholars have suggested thatcustomers who regularly use a service and enjoy the benefits of the service offerings/servicesoffered will more likely stay with the service provider (Bhattacherjee, 2001; Bhattacherjee&Lin, 2014; Limayem et al., 2007). According to Roos and Gustafsson (2007), the likelihood ofa passive customer switching to a competitor is greater than that of an active customerswitching. Furthermore, Roos and Gustafsson (2011) posit that switching is less frequentwhen customers are more active. In other words, user continuance is somehow guaranteedwhen the user is more active. Hence we posit that:

H5: Active usage of mobile money services is positively related to customer continuanceintention

3.4. Mediating effects of active usage of mobile money on satisfaction and trust

According to Hart and Johnson (1999), the condition beyond satisfaction that guaran-tees true customer loyalty is total trust. If firms are unable to retain satisfied customerspartially due to dearth of trust, then trust may act as a complement to satisfaction inunderpinning customer continuance (Hart & Johnson, 1999). This inference is consis-tent with other works on relationship contexts (Morgan & Hunt, 1994; Ranaweera &Prabhu, 2003). Ranaweera and Prabhu (2003) state that the customers most likely tocontinue with a service provider are those with high levels of both satisfaction and trustin the provider. Furthermore, Zhou (2013) notes that trust and satisfaction are the keyfactors that affect users’ continuance intention of mobile payment services such asmobile money.

Interestingly, active usage of mobile money services is one of the key metrics of interestto telecommunication operators, because the success of a technology-enabled service suchas mobile money is dependent on continued use rather than initial acceptance(Bhattacherjee, 2001; Limayem et al., 2007). Because former studies (Roos & Gustafsson,2011, 2007), have established that user continuance will be achieved once a user becomesmore active, we test the potential mediating effect of the active usage of mobile money inthe research model. Liu et al. (2011) and Zhou (2013) both conclude that satisfactioninduces active usage of mobile money services because a delighted user will continue to usethe service for his or her target task(s) (Liu et al., 2011; Zhou, 2013). Moreover, trust hasbeen found to (have an) impact (on) active usage of mobile money service because a user’sassurance in a service will foster a continued relationship for frequent use of service(Benamati et al., 2010; Luo et al., 2010) hence we state the sixth and seventh hypotheses as:

H6: Active usage of mobile money services significantly mediates the relationshipbetween satisfaction and customer continuance intention

H7: Active usage of mobile money service significantly mediates the relationshipbetween trust and customer continuance intention

180 E. YEBOAH-ASIAMAH ET AL.

4. Methodology

4.1 Sample population and data collection

Individual customers (subscribers) of four telecom firms operating mobile moneyservices in Ghana made up the population for the study. A sample of 700 registeredmobile money subscribers were (conveniently) selected from five of Ghana’s 10 regions(Greater Accra, Eastern, Volta, Central and Western Regions) in December 2016. Toenable the researcher (to) collect quality data that echo customers’ opinion and enhancethe sample representation, a survey methodology was employed for data collection fromcustomers. We inspected all questionnaires (700) and dropped 193 responses that hadtoo many missing values. Accordingly, 507 valid responses were obtained, producing aresponse rate of 72.4%. Both the sample size guidelines as recommended by Hair, Hult,Ringle, and Sarstedt (2013) stating that at least 59 observations are necessary toaccomplish a statistical power of 80% for detecting R-square values of at least 0.25(that is, 10 × 3 structural paths = 30 customers), and the “10 times rule” (Thompson,Barclay, & Higgins, 1995) are satisfied in this study. For a Partial Least Squares (PLS)model, the “10 times rule” proposes that the sample size should at least equal “10 timesthe maximum number of structural paths pointing at a latent variable anywhere in thePLS path” (Thompson et al., 1995).

This being a cross-sectional study, self-administered questionnaires were used to collectdata according to a seven-point Likert scale ranging from one, “strongly disagree”, to seven,“strongly agree.” All measurement items for the constructs were based on extant literatureand adapted for Ghana’s mobile telecommunication industry. Demographic variables suchas gender, age, qualification, etc., as well as categorical questions were used to collect data.To check for the suitability, structure and design of the instrument, questionnaires werepilot-tested with 20 mobile money users. This helped to restructure the wording of items inthe questionnaire. After the pilot, questionnaires were administered to the customers offour telecom operators at their various customer service centers. Subscribers who hadregistered for mobile money services and have actually used the service within the past90 days were selected, and the questionnaires were administered within a six-week periodby four hired and trained research assistants.

4.2. Data analysis

Partial Least Squares Structural Equation Modeling (PLS-SEM), available in SmartPLS3.2.6 (Ringle, Wende, & Becker, 2016) and SPSS 23.0, were used for the data anddescriptive analysis respectively in the study. The use of the PLS-SEM was to enable theresearcher(s) to evaluate the adequacy of the measurement model in relation to the primeconstructs and also to examine the hypothesized relationships (Figure 1) and the extra-polative significance of the conceptual model (Ringle et al., 2016). Since the ultimateobjective of the study was to test the ability of the respective antecedents to forecast theirinfluence on customers’ intention to stay with mobile money service provider, PLS-SEM isthe most suitable tool for the study. Furthermore, PLS-SEM is ideal for the purpose of thestudy due to its distribution-free assumption (Gye-Soo, 2016).

JOURNAL OF AFRICAN BUSINESS 181

5. Results of the study

5.1. Demographic analysis of respondents

The descriptive statistics showed that males comprised 60.4% of respondents, whilst femaleswere 39.6%. There were two dominant age groups: below 25 years (42%) and between 26 and35 years (42.6%). Respondents between 35 and 46 years were 11.2%, and those between 46and 55 years and above 55 years recorded 3.6% and 0.6% respectively. In terms of qualifica-tion, nearly half of the respondents (47.4%) had Diploma/HND education, with 21.9% and12.8% having Senior High School (WASSCE/SSCE) and Technical/Vocational trainingrespectively. Last but not least, respondents with a Bachelor’s and Master’s level of educationwere 14.5% and 3.4% respectively. About 30.6% of the respondents did not earn any incomebecause they were students, whilst 31.2% earn a monthly income below GH¢200 (US$ 45).Also 20.3% earned amonthly income betweenGH¢200 andGH¢500 (US$ 111), 8.8%of themearned between GH¢500 and GH¢1000 (US$ 222) and about 9.1% earned above GH¢1000.This is considered quite high in an economy where the average monthly income is GH ¢899(US$ 200) (Ghana Statistical Service, 2016).

Out of 507 respondents, 78.5% used bank accounts while 21.5% did not have traditionalbank accounts. Interestingly, 57.2% averred that mobile money services alone could meettheir banking needs, though 42.8% still believed that they couldn’t do without a bank account.Finally, with regards to the number of years they had been registered for the mobile moneyservice with their current service provider, 29.6% of respondents had spent less than one year.Almost 34.7% had spent between 1 and 2 years, while 26.8% had spent between 2 and 4 yearsand 8.9% had spent more than 5 years with their current service provider. This suggests thatmore than half (64.3%) of the respondents had registered formobilemoney service within theprevious two years.

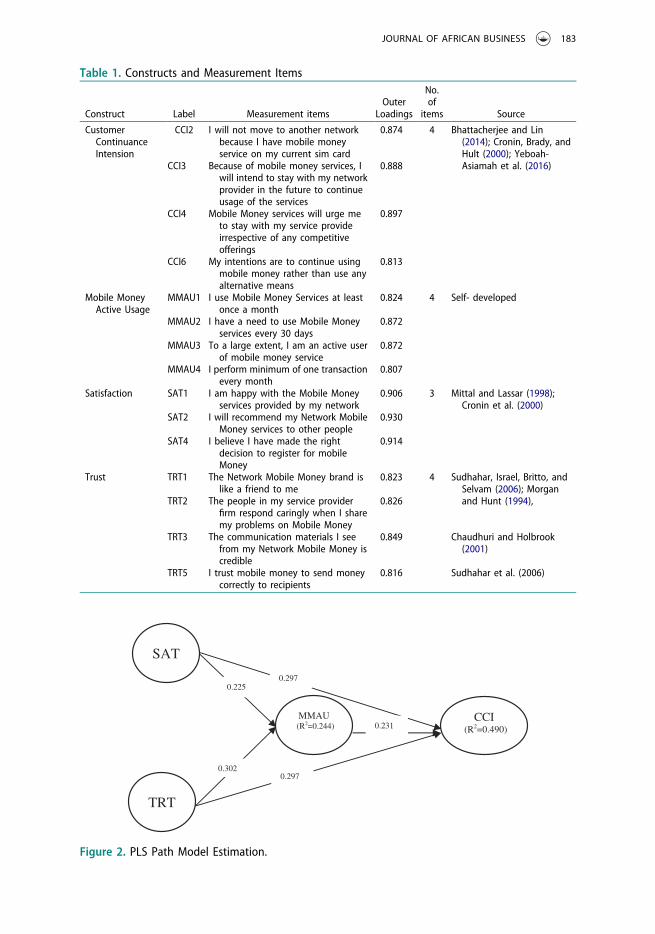

5.2. Constructs and measurement items

The measurement items used to assess the various constructs and their respective outerloadings are presented in Table 1, while the PLS path estimation model is presented inFigure 2. Indicator reliability, internal consistency reliability, discriminant validity, andconvergent validity of the reflective measurement model were assessed before a path coeffi-cient analysis to ensure the reliability of the data and the model (Wong, 2013). Four items(CCI1, CCI5, SAT3, TRT4) which did not meet the required thresholds were removed fromthe model. The remaining items used for analysis are indicated in the charts below.

5.3. The measurement/outer model

Internal consistency was assessed using composite reliability (CR), which, according toCevdet Altunel and Erkut (2015), should be valued above 0.70. From the measurementmodel, CRs of the constructs ranged from 0.897 to 0.940, establishing adequate reliabilityof the measures: CCI (0.925); MMAU (0.908); Satisfaction (0.940); and Trust (0.897).

Furthermore, to examine construct validity, convergent and discriminant validities wereestimated. Hair, Black, et al. (2014) postulate that the establishment of convergent validityrequires a factor loading of at least 0.50 and an average variance extracted (AVE) above 0.50to signify that more than half of the variance of the indicators of the latent variables are

182 E. YEBOAH-ASIAMAH ET AL.

Table 1. Constructs and Measurement Items

Construct Label Measurement itemsOuter

Loadings

No.of

items Source

CustomerContinuanceIntension

CCI2 I will not move to another networkbecause I have mobile moneyservice on my current sim card

0.874 4 Bhattacherjee and Lin(2014); Cronin, Brady, andHult (2000); Yeboah-Asiamah et al. (2016)CCI3 Because of mobile money services, I

will intend to stay with my networkprovider in the future to continueusage of the services

0.888

CCI4 Mobile Money services will urge meto stay with my service provideirrespective of any competitiveofferings

0.897

CCI6 My intentions are to continue usingmobile money rather than use anyalternative means

0.813

Mobile MoneyActive Usage

MMAU1 I use Mobile Money Services at leastonce a month

0.824 4 Self- developed

MMAU2 I have a need to use Mobile Moneyservices every 30 days

0.872

MMAU3 To a large extent, I am an active userof mobile money service

0.872

MMAU4 I perform minimum of one transactionevery month

0.807

Satisfaction SAT1 I am happy with the Mobile Moneyservices provided by my network

0.906 3 Mittal and Lassar (1998);Cronin et al. (2000)

SAT2 I will recommend my Network MobileMoney services to other people

0.930

SAT4 I believe I have made the rightdecision to register for mobileMoney

0.914

Trust TRT1 The Network Mobile Money brand islike a friend to me

0.823 4 Sudhahar, Israel, Britto, andSelvam (2006); Morganand Hunt (1994),TRT2 The people in my service provider

firm respond caringly when I sharemy problems on Mobile Money

0.826

TRT3 The communication materials I seefrom my Network Mobile Money iscredible

0.849 Chaudhuri and Holbrook(2001)

TRT5 I trust mobile money to send moneycorrectly to recipients

0.816 Sudhahar et al. (2006)

SAT

TRT

MMAU (R2=0.244)

CCI (R2=0.490)

0.2970.302

0.2250.297

0.231

Figure 2. PLS Path Model Estimation.

JOURNAL OF AFRICAN BUSINESS 183

explained. From Table 2, all the factor loadings of the items were above the minimum 0.50threshold. Again, the AVEs and the CRs all indicate appropriate internal consistency.Moreover, discriminant validity was assessed by analyzing the correlation among themeasures to identify any potentially overlapping constructs (Fornell & Larcker, 1981).Hair, Hult, et al. (2014) instruct that the square root of the AVE should be higher thanthe variance shared between the construct and other constructs in order to establishdiscriminant validity. Table 2 indicates that all the correlations and the square roots ofthe AVE’s indicate adequate discriminant validity.

5.4. Evaluation of the structural model in PLS-SEM: collinearity assessment

The structural model, just like the measurement model, has to be properly evaluatedbefore arriving at any logical conclusions. According to Hair, Ringle, and Sarstedt(2011), one of the potential problems in the structural model is collinearity, typicallyindicated by a variance inflation factor (VIF) value of 5 or above (Hair et al., 2011;Wong, 2013). In this study, the IBM SPSS 23.0 was utilized to generate VIF values.

From the summary of collinearity results in Table 3, it is clear that all the VIF values arelower than five, indicating that there is a low possibility of collinearity between each set ofpredictor variables.

5.5. Coefficient of determination (R2)

The assessment of the coefficient of determination (R2) is another key part in theevaluation of the structural model. In this study, customer continuance intention(CCI) is the major construct of interest, and from the PLS Path model estimationand from Table 6, the overall R2 is found to be relatively moderate. Threshold values of0.25, 0.50 and 0.70 to define weak, moderate and strong coefficients of determinationare recommended (Hair et al., 2013; Wong, 2013). The R2value for this study is 0.490,which suggests that the three constructs of SAT, TRT and MMAU jointly explain 49%

of the variance of the endogenous construct CCI. Last, the model estimation reveals

Table 2. Discriminant Validity

Latent Variable Correlations (LVC)

Discriminant Validitymet?

(Square root ofAVE>LVC?)

Customer ContinuanceIntention

MM ActiveUsage Satisfaction Trust

Customer ContinuanceIntention

0.869 Yes

MM Active User 0.506 0.844 YesSatisfaction 0.626 0.453 0.917 YesTrust 0.631 0.472 0.755 0.829 Yes

Note: The square root of AVE values is shown on the diagonal and printed in bold; non-diagonal elements are the latentvariable correlations (LVC).

184 E. YEBOAH-ASIAMAH ET AL.

that the R2for the other latent constructs, SAT and TRT, are found to jointly explain(the) 24% of MMAU’s variances in this PLS-SEM model.

5.6. Path coefficient and hypothesis testing

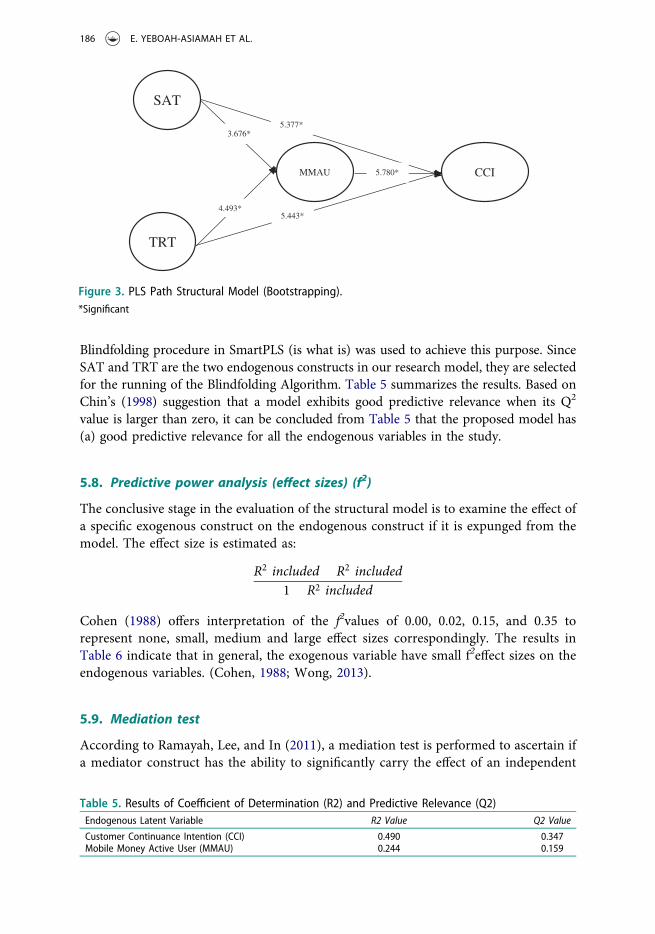

To assess the relationship between constructs in PLS-SEM, the path coefficient and therelated t-statistics through the bootstrapping procedure has to be examined (Wong,2013). Standardized path coefficients (b), significance levels (t-statistic), and R2 esti-mates were utilized to estimate the structural model as shown in Table 4.

The results from Table 4 indicate that all the hypotheses for the study weresupported. H1 predicted that active usage of mobile money services will have significantand positive effect on customers’ continuance intention toward service provider, andwith t-value = 5.780, and p < 0.001, hypothesis 1 is accepted. Satisfaction has significantpositive effect on customers’ continuance intention toward the service provider as wellas on active usage of mobile money service (t = 5.377, p < 0.001; and t = 3.676,p < 0.001 respectively), providing support for hypothesis H2 and H3. Hypotheses 4and 5 predicted that Trust will have significant positive influence on customers’continuance intention towards the service provider and on active usage of mobilemoney service. The results from Table 4 provide support for these hypotheses witht = 5.443, p < 0.001; and t = 4.493, p < 0.001 respectively. Figure 3 also indicates thepath structural model using the bootstrapping procedure.

5.7. Predictive relevance (Q2)

In PLS-SEM, the Stone-Geisser’s predictive relevance (Q2) assessment is essential becauseit helps the researcher confirm if the data points of indicators in the reflective measure-ment model of the endogenous construct can be accurately predicted (Wong, 2013). The

Table 3. Collinearity AssessmentFirst Set Second Set

Constructs

CollinearityStatistics Collinearity Problem?

(VIF>5?) Constructs

CollinearityStatistics Collinearity Problem?

(VIF>5?)Tolerance VIF Tolerance VIF

MMAU 0.756 1.323 No TRT 0.43 2.325 NoSAT 0.418 2.391 No SAT 0.43 2.325 NoTRT 0.409 2.446 No

Dependent variable: CCI Dependent variable: MMAU

Table 4. Significance Testing Results of the Structural Model Path Coefficients

Hypothesis Path:Path

Coefficients t Valuesp

Values Hypothesis

H1 MM Active Usage -> Customer ContinuanceIntention

0.231 5.780 0.001 Supported

H2 Satisfaction -> Customer Continuance Intention 0.297 5.377 0.001 SupportedH3 Satisfaction -> MM Active Usage 0.225 3.676 0.001 SupportedH4 Trust -> Customer Continuance Intention 0.297 5.443 0.001 SupportedH5 Trust -> MM Active Usage 0.302 4.493 0.001 Supported

JOURNAL OF AFRICAN BUSINESS 185

Blindfolding procedure in SmartPLS (is what is) was used to achieve this purpose. SinceSAT and TRT are the two endogenous constructs in our research model, they are selectedfor the running of the Blindfolding Algorithm. Table 5 summarizes the results. Based onChin’s (1998) suggestion that a model exhibits good predictive relevance when its Q2

value is larger than zero, it can be concluded from Table 5 that the proposed model has(a) good predictive relevance for all the endogenous variables in the study.

5.8. Predictive power analysis (effect sizes) (f2)

The conclusive stage in the evaluation of the structural model is to examine the effect ofa specific exogenous construct on the endogenous construct if it is expunged from themodel. The effect size is estimated as:

R2 included � R2 included1� R2 included

Cohen (1988) offers interpretation of the f2values of 0.00, 0.02, 0.15, and 0.35 torepresent none, small, medium and large effect sizes correspondingly. The results inTable 6 indicate that in general, the exogenous variable have small f2effect sizes on theendogenous variables. (Cohen, 1988; Wong, 2013).

5.9. Mediation test

According to Ramayah, Lee, and In (2011), a mediation test is performed to ascertain ifa mediator construct has the ability to significantly carry the effect of an independent

Table 5. Results of Coefficient of Determination (R2) and Predictive Relevance (Q2)Endogenous Latent Variable R2 Value Q2 Value

Customer Continuance Intention (CCI) 0.490 0.347Mobile Money Active User (MMAU) 0.244 0.159

SAT

TRT

MMAU CCI

5.443*4.493*

3.676*5.377*

5.780*

Figure 3. PLS Path Structural Model (Bootstrapping).*Significant

186 E. YEBOAH-ASIAMAH ET AL.

variable to a dependent variable (Ramayah et al., 2011). The causal steps approach(Baron & Kenny, 1986) was adopted to discover the indirect effect of the independentvariable on the dependent variable through a mediator variable. To assess whetheractive usage of mobile money functions as the mediator for satisfaction (H6) and trust(H7), three conditions should be met: (1) an independent construct should significantlyinfluence the dependent construct, (2) an independent construct should significantlyinfluence the mediator construct, and (3) both the independent construct and themediator should together predict the dependent construct (Baron & Kenny, 1986).

5.10. Magnitude of mediation

The strength of the mediator can be assessed through the use of total effect andvariance accounted for (VAF), after the significance of the indirect effect isascertained. Table 7 presents the results of the mediation analysis. It can be saidthat 20.2% of satisfaction’s effect on the customer’s continuance intention isexplained via the active usage of a mobile money mediator, and 20.1% of thetrust effect on customer continuance intention was also explained via the activeusage of mobile money as the mediator. Thus, the active usage of mobile moneyincreases the effect of trust and satisfaction on the customer’s continuance inten-tion. According to Hair et al. (2013), partial mediation is demonstrated when VAFexceeds the 0.2 threshold level and full mediation is demonstrated when it exceeds0.8. Since the VAF values for both hypotheses H6 and H7 were more than 20%,but smaller than 80%, it can be concluded that active usage of mobile moneypartially mediates the influences of satisfaction and trust on the continuanceintention towards the mobile money service provider. These findings lead us to

Table 6. Results of F2 Effect Sizes AnalysisCustomer Continuance Intention (CCI) Mobile Money Active User (MMAU)

VariablePath

CoefficientR2

IncludedR2

Excluded f2 RemarksPath

Coefficient R2IncludedR2

Excluded f2 Remarks

SAT 0.297 0.490 0.453 0.0725 SmallEffect

0.225 0.246 0.223 0.0305 SmallEffect

TRT 0.297 0.490 0.454 0.0706 SmallEffect

0.302 0.246 0.208 0.0504 SmallEffect

MMAU 0.231 0.490 0.451 0.0765 SmallEffect

N/A

Note: Target constructs appear in the first row, whereas the predecessor constructs are in the first column.

Table 7. Mediation Effect Analysis

Hypothesis IV M DV

Coefficient in regression

Totaleffect’ssize

Mediating Hypothesis

IV – >DV

IV – >M

M – >DV

Indirect effect’s Size

VAF StrengthIV – > M xM – > DV

t-value

H6 SAT MMAU CCI 0.500*** 0.453*** 0.280*** 0.127*** 10.974 0.627 0.202 Partial AcceptedH7 TRT MMAU CCI 0.504*** 0.472*** 0.268*** 0.126*** 10.581 0.630 0.201 Partial Accepted

Note: IV = Independent variable; M: mediator; DV: dependent variable; VAF: variance accounted for. *** P < 0.01.

JOURNAL OF AFRICAN BUSINESS 187

accept hypothesis H6 and H7 about MMAU’s mediator role. The results presentsome interesting results for discussion.

6. Discussion

This study explored how the use of mobile money services can deter (in deterring)customer churn. The relationship between customers’ continuance intentions and usageof mobile money services has not been studied to a significant extent in the mobiletelecommunications industry. The mediating role of active usage of mobile moneyservices in the link between satisfaction and trust in relation to customers’ continuanceintention has also seldom been studied. This study therefore filled these voids byexamining the mediation effect of active usage of mobile money service on the relation-ship between satisfaction and trust on customer continuance intention.

The results of the study indicate that satisfaction has a substantial positive effect on bothactive usage of mobile money as well as customers’ continuance intention. Previous researchhas established that satisfaction is a strong determinant of continuance behavior (Kim, Hong,Min, & Lee, 2011; Kuo et al., 2009; Liu et al., 2011), hence satisfaction should be the maininstrument through which telecommunication service providers seek to build active usageand loyalty to prevent churn. A contented user is likely to continue to use mobile moneyservices due to positive feelings about the service. On the contrary, if users are not satisfiedwith mobile money services they may discontinue their usage and subsequently have anegative attitude toward the service. In effect, satisfaction acts as a mechanism to stimulateactive usage and customer intention to stay with the service provider, as illustrated in theresearch model. In the extant literature, this assertion has been well supported and validatedin different settings (e.g., Bhattacherjee& Lin, 2014; Kim et al., 2011; Liu et al., 2011).

Trust has a positive and significant relationship with both active usage of mobile moneyand customers’ continuance intention toward service providers. This supports Liu et al.’s(2011) assertion that increasing user trust is key to the advancement of mobile technology-enabled services. According to Blau (1964), trust is the key element in the preservation ofexchange relations, and is hence the reason why customers would be willing to deposit theirmoney with agents (strangers) who are authorized by the service providers. The implicationis that, when amobile money user is persuaded that the service is worthy of accomplishing atask to an agreed standard, there is a high possibility that the user will continue patronage.On the other hand, a mobile money user is not likely to be an active user and remain withthe service provider unless the service provider is able to build trust to ease the customer’sperception of risk and uncertainty.

7. Implications of the research

This study provides both theoretical and practical implications. First, it is of theoreticalimportance, as it is among the first studies, to examine the effect of mobile money oncustomer churn prevention in the telecommunication industry from a theoreticalperspective. This study has also provided empirical support for the involvement oftrust and satisfaction in preventing customer churn, and has investigated the mediatingrole of active usage of mobile money, which is a key indicator of level of acceptance forservice providers. Furthermore, the study has validated a theoretical model of customer

188 E. YEBOAH-ASIAMAH ET AL.

continuance intention in the context of mobile money. This extends the purview of therelatively scarce literature on mobile money, and also provides a new perspective onmanaging customer churn in an emerging market.

The results of this research have additionally provided several practical insights intoensuring customers’ continuance in emerging markets as far as mobile money is concerned.In the first place, customer continuance intention towards the service provider is influencedby their satisfaction with the service and their trust in the provider. Managers must thereforefocus resources on creating positive and pleasant experiences for customers whenever theymake use of mobile money platforms, so that they can enjoy the usage, and recommend it toothers. Mobile operators must also strive to build trust, by strengthening their securityprocesses and training their staff to show empathy toward the customer size and adequatelyrespond when service failures occur. These will strengthen consumers’ intention to remainwith the operator. The results also make it clear that active usage of mobile money serviceshas a strong influence on continuance intention when combined with satisfaction and trust.This suggests that managers in the telecommunications industry must make engendering theactive usage of mobile money a priority in their strategic plans. Relevant and innovativeservices on the platform should be developed to attract and stimulate regular usage, as thiswill lead to customer retention. Regular users of mobile money services should also bespecifically targeted with interventions to increase trust and customer satisfaction as theywill yield a higher response in terms of CCI than less frequent users of the service.

It is again evident that trust and satisfaction significantly influence active usage ofmobile money. Thus, managers, as a strategy to influence resistance to churn, shouldseek to ensure that customers continue to use mobile money by working to alleviateuser perceptions of uncertainty and risk (Luo et al., 2010; Zhou, 2013), while ensuringthat technology-enabled services create customer satisfaction (Kuo et al., 2009).

8. Limitations and further research directions

This study has made a modest contribution to understanding CCI by defining a modelfor customer continuance intention in the context of mobile money. However, thestudy has limitations which offer opportunities for future research. In the first place, theuse of a cross-sectional study to assess a relationship which is present over a relativelylong period of time can be problematic (Davis-Sramek, Droge, Mentzer, & Myers,2009). Second, the use of the telecommunication industry as the context of this studyreduces the extent of generalization of the findings.

As recommendation for future research, similar studies based on longitudinal datawould help to compare the behavior of both active and passive mobile money users’continuance intention towards service providers. In addition, this study can be replicatedin different service sectors and markets to compare results and validate the findings of thisstudy. Lastly, a qualitative or case study method approach with a relatively larger samplecan be employed to validate the inferences and suppositions of this study.

Conclusion

The objective of the study was to examine the critical role of mobile money in ensuringcustomer continuance intention, which is a major issue for firms in very competitive

JOURNAL OF AFRICAN BUSINESS 189

markets. Overall, there has been considerable support for the study’s conceptual model,hence this study makes contribution to knowledge by establishing that customers’continuance intention towards service providers in the telecommunication firms canbe instigated by engendering satisfaction, trust and, more significantly, active usage ofmobile money services. The results further indicate that active usage of mobile moneyservices mediates the link between satisfaction and trust on customers’ continuanceintention.

The paper has demonstrated that active usage of mobile money services is crucial inlocking in customers, thus making them more resistant to churn. In specific terms, mobileoperators may prevent customer churn by pursuing combined strategies aimed at intro-ducing mobile money products/services that are relevant to the everyday lives and needs oftheir customers, thereby ensuring that they become active users of mobile money.

Disclosure statement

No potential conflict of interest was reported by the authors.

ORCID

Eric Yeboah-Asiamah http://orcid.org/0000-0002-2903-5907

References

Abor, J. Y., Amidu, M., & Issahaku, H. (2018). Mobile telephony, financial inclusion andinclusive growth. Journal of African Business, 1–24. doi:10.1080/15228916.2017.1419332

Ajzen, I., & Fishbein, M. (2000). Attitudes and the attitude-behavior relation: Reasoned andautomatic processes. European Review of Social Psychology, 11(1), 1–33. doi:10.1080/14792779943000116

Akter, S., D’Ambra, J., & Ray, P. (2011). Trustworthiness in mHealth information services: Anassessment of a hierarchical model with mediating and moderating effects using partial leastsquares (PLS). Journal of the American Society for Information Science and Technology, 62(1),100–116. doi:10.1002/asi.21442

Bank of Ghana. (2017). Payment systems statistics report. Retrieved 17 June, 2017, fromhttps://www.bog.gov.gh/privatecontent/Payment%20Systems/PAYMENT%20SYSTEM%20STATISTICS_%20First%20Quarter%202017%20.pdf

Baron, R. M., & Kenny, D. A. (1986). Moderator-mediator variable distinction in social psycho-logical research: Conceptual, strategic and statistical considerations. Journal of Personality andSocial Psychology, 51(6), 1173–1182. doi:10.1037/0022-3514.51.6.1173

Benamati, J. S., Fuller, M. A., Serva, M. A., & Baroudi, J. A. (2010). Clarifying the integration oftrust and TAM in e-commerce environments: Implications for systems design and manage-ment. IEEE Transactions on Engineering Management, 57(3), 380–393. doi:10.1109/TEM.2009.2023111

Bhattacherjee, A. (2001). Understanding information systems continuance: An expectation-con-firmation model. MIS Quarterly, 25, 351–370. doi:10.2307/3250921

Bhattacherjee, A., & Lin, C. P. (2014). A unified model of IT continuance: Three complementaryperspectives and crossover effects. European Journal of Information Systems, 24(4), 364–373.doi:10.1057/ejis.2013.36

Blau, P. M. (1964). Exchange and power in social life. New York: John Wiley.

190 E. YEBOAH-ASIAMAH ET AL.

Bongomin, G. O. C., Ntayi, J. M., Munene, J. C., & Malinga, C. A. (2018). Mobile money andfinancial inclusion in Sub-Saharan Africa: The moderating role of social networks. Journal ofAfrican Business, 1–24. doi:10.1080/15228916.2017.1416214

Cevdet Altunel, M., & Erkut, B. (2015). Cultural tourism in Istanbul: The mediation effect oftourist experience and satisfaction on the relationship between involvement and recommen-dation intention. Journal of Destination Marketing Management., 4(4), 213–221. doi:10.1016/j.jdmm.2015.06.003

Chaudhuri, A., & Holbrook, M. B. (2001). The chain of effects from brand trust and brand affectto brand performance: The role of brand loyalty. Journal of Marketing, 65(2), 81-93.doi:10.1509/jmkg.65.2.81.18255

Chen, S.-C., Chen, -H.-H., Lin, M.-T., & Chen, Y.-B. (2011). A conceptual model to understandthe effects of perception on the continuance intention in facebook. Australian Journal ofBusiness and Management Research, 1(8), 29–34.

Chin, W. W. (1998). The partial least squares approach for structural equation modeling. In G.A.Marcoulides (Ed.), Modern methods for business research. Mahwah, NJ: Lawrence ErlbaumAssociates.

Cioffi, D., & Garner, R. (1996). On doing the decision: Effects of active versus passive choice oncommitment and self-perception. Personality and Social Psychology Bulletin, 22(2), 133–147.doi:10.1177/0146167296222003

Cohen, J. (1988). Statistical power analysis for behavioral sciences (2nd ed.). Hillsdale, NJ: L.Erlbaum.

Cronin, J. J., Brady, M. K., & Hult, G. T. M. (2000). Assessing the effects of quality, value, andcustomer satisfaction on consumer behavioral intentions in service environments. Journal ofRetailing, 76(2), 193–218. doi:10.1016/S0022-4359(00)00028-2

Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of informa-tion technology. MIS Quarterly, 13(3), 319–340. doi:10.2307/249008

Davis-Sramek, B., Droge, C., Mentzer, J. T., & Myers, M. B. (2009). Creating commitmentand loyalty behaviour among retailers: What are the roles of service quality and satisfac-tion?Journal of the Academy of Marketing Science, 37(4), 440–454. doi:10.1007/s11747-009-0148-y

Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservablevariables and measurement error. Journal of Marketing Research, 18(1), 39–50. doi:10.2307/3151312

Gao, L., & Bai, X. (2014). An empirical study on continuance intention of mobile socialnetworking services. Asia Pacific Journal of Marketing and Logistics, 26(2), 168–189.doi:10.1108/APJML-07-2013-0086

Gefen, D., Karahanna, E., & Straub, D. W. (2003). Trust and TAM in online shopping: Anintegrated model. MIS Quarterly, 27(1), 51–90. doi:10.2307/30036519

Ghana Statistical Service. (2016, December). 2015 Labour force report. Retrieved 8 January, 2018,fromhttp://www.statsghana.gov.gh/docfiles/publications/Labour_Force/LFS%20REPORT_fianl_21-3-17.pdf.

GhanaWeb. (2017, October 20). Mobile money transactions shoot up 737%. Retrieved 18 January,2018, fromhttps://www.ghanaweb.com/GhanaHomePage/business/Mobile-money-transactions-shoot-up-737-592496

Gosavi, A. (2017). Can mobile money help firms mitigate the problem of access to finance inEastern sub-Saharan Africa? Journal of African Business, 1–18. doi:10.1080/15228916.2017.1396791

GSMA. (2017). State of the industry report on mobile money – decade edition: 2006 – 2016.Retrieved 18 January, 2018, from https://www.gsma.com/mobilefordevelopment/wp-content/uploads/2017/03/GSMA_State-of-the-Industry-Report-on-Mobile-Money_2016.pdf.

Gye-Soo, K. (2016). Partial least squares structural equation modeling(PLS-SEM): An applicationin customer satisfaction research. International Journal of U-And e-Service, Science andTechnology, 9(4), 61–68. doi:10.14257/ijunesst.2016.9.4.07

JOURNAL OF AFRICAN BUSINESS 191

Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2014). Multivariate data analysis (7thed.). Edinburgh Gate, Harlow: Pearson Education Limited.

Hair, J. F., Hult, G. T. M., Ringle, C., & Sarstedt, M. A. (2014). A primer on partial least squaresstructural equation modeling (PLS-SEM) (1st ed.). Thousand Oaks, CA, USA: SagePublications.

Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2013). A primer on partial least squaresstructural equation modeling (PLS-SEM). Thousand Oaks: Sage.

Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal ofMarketing Theory and Practice, 19(2), 139–151. doi:10.2753/MTP1069-6679190202

Hart, C., &Johnson, M. (1999). Growing the trust relationship. Journal of MarketingManagement, 8(1), 8–19.

Heskett, J. L., Jones, T. O., Loveman, G. W., Sasser, W. E., & Schlesinger, L. A. (1994, March/April). Putting the service-profit chain to work. Harvard Business Review, 77(2), 164–174.

Hughes, A. M. (2007). Churn reduction in the telecom industry. Retrieved 2 March, 2017,fromwww.telecommarketing.com/index.php?q.node/29.

Humbani, M., & Wiese, M. (2017). A cashless society for all: Determining consumers’ readinessto adopt mobile payment services. Journal of African Business, 1–21. doi:10.1080/15228916.2017.1396792

Hwang, H., Taesoo, J., & Euiiho, S. (2004). An Ltv model and customer segmentation based oncustomer value: A case study on the wireless telecommunications industry. Expert Systemswith Applications, 26(2), 181–188. doi:10.1016/S0957-4174(03)00133-7

Jack, W., &Suri, T. (2010). The economics of M-PESA: An update. Unpublished research paper,Georgetown University.

Kim, J., Hong, S., Min, J., & Lee, H. (2011). Antecedents of application service continuance: Asynthesis of satisfaction and trust. Expert Systems with Applications, 38(8), 9530–9542.doi:10.1016/j.eswa.2011.01.142

Kuo, Y. F., Wu, C. M., & Deng, W. J. (2009). The relationships among service quality, perceivedvalue, customer satisfaction, and post-purchase intention in mobile value-added services.Computers in Human Behavior, 25(4), 887–896. doi:10.1016/j.chb.2009.03.003

Kuusik, A., & Varblane, U. (2009). How to avoid customers leaving: The case of the Estoniantelecommunication industry. Baltic Journal of Management, 4(1), 66–79. doi:10.1108/17465260910930458

Lal, R., & Sachdev, I. (2015). Mobile money services–Design and development for financialinclusion. Harvard Business School. Working Paper 15-083.

Liao, C., Palvia, P., & Chen, J. L. (2009). Information technology adoption behavior life cycle:Toward a Technology Continuance Theory (TCT). International Journal of InformationManagement, 29(4), 309–320. doi:10.1016/j.ijinfomgt.2009.03.004

Limayem, M., & Cheung, C. M. (2008). Understanding information systems continuance: Thecase of internet-based learning technologies. Information & Management, 45(4), 227–232.doi:10.1016/j.im.2008.02.005

Limayem, M., Hirt, S. G., & Cheung, C. M. (2007). How habit limits the predictive power ofintention: The case of information systems continuance. MIS Quarterly, 31(4), 705–737.doi:10.2307/25148817

Liu, C. T., Guo, Y. M., & Lee, C. H. (2011). The effects of relationship quality and switchingbarriers on customer loyalty. International Journal of Information Management, 31(1), 71–79.doi:10.1016/j.ijinfomgt.2010.05.008

Luo, X., Li, H., Zhang, J., & Shim, J. P. (2010). Examining multi-dimensional trust and multi-faceted risk in initial acceptance of emerging technologies: An empirical study of mobilebanking services. Decision Support Systems, 49(2), 222–234. doi:10.1016/j.dss.2010.02.008

Mittal, B., & Lassar, W. M. (1998). Why do customers switch? The dynamics of satisfactionversus loyalty. Journal of Services Marketing 12(3), 177–194.

Mbiti, I., & Weil, D. N. (2013). The home economics of e-money: Velocity, cash management,and discount rates of m-pesa users. The American Economic Review, 103(3), 369. doi:10.1257/aer.103.3.369

192 E. YEBOAH-ASIAMAH ET AL.

Morawczynski, O. (2009). Exploring the usage and impact of “transformational” mobile financialservices: The case of M-PESA in Kenya. Journal of Eastern African Studies, 3(3), 509–525.doi:10.1080/17531050903273768

Morgan, R. M., & Hunt, S. D. (1994). The commitment-trust theory of relationship marketing.Journal of Marketing, 58(3), 20–23. doi:10.2307/1252308

Narteh, B., Mahmoud, M. A., & Amoh, S. (2017). Customer behavioural intentions towardsmobile money services adoption in Ghana. The Service Industries Journal, 37(7/8), 1–22.doi:10.1080/02642069.2017.1331435

Nimako, S. G., Ntim, B. A., & Mensah, A. F. (2014). Effect of mobile number portability adoptionon consumer switching intention. International Journal of Marketing Studies, 6(2), 117.doi:10.5539/ijms.v6n2p117

Oliver, R. L. (1980). A cognitive model of the antecedents and consequences of satisfactiondecisions. Journal of Marketing Research, 17(4), 460–469. doi:10.2307/3150499

Oliver, R. L. (1993). Cognitive, affective, and attribute bases of the satisfaction response. Journalof Consumer Research, 20(3), 418–430. doi:10.1086/jcr.1993.20.issue-3

PricewaterhouseCoopers (2016). 2016 Ghana banking survey: How to win in an era of mobilemoney. Retrieved 17 January, 2018 from https://www.pwc.com/gh/en/assets/pdf/2016-banking-survey-report.pdf

Qureshi, I., Fang, Y., Ramsey, E., McCole, P., Ibbotson, P., & Compeau, D. (2009).Understanding online customer repurchasing intention and the mediating role of trust - anempirical investigation in two developed countries. European Journal of Information Systems,18(3), 205. doi:10.1057/ejis.2009.15

Ramayah, T., Lee, J. W. C., & In, J. B. C. (2011). Network collaboration and Performance in thetourism sector. Service Business, 5(4), 411–428. doi:10.1007/s11628-011-0120-z

Ranaweera, C., & Prabhu, J. (2003). The influence of satisfaction, trust and switching barriers oncustomer retention in a continuous purchase setting. International Journal of Service IndustryManagement, 14(4), 374–395. doi:10.1108/09564230310489231

Reichheld, F. F. (1996). Learning from customer defections. Harvard Business Review, 74(2), 56–69.Ringle, C. M., Wende, S., & Becker, J.-M. (2016). SmartPLS 3. Bönningstedt: SmartPLS GmbH.Roos, I., &Gustafsson, A. (2007). Understanding frequent switching patterns – A crucial element

in managing customer relationships. Journal of Service Research, 10(1), 93–108. doi:10.1177/1094670507303232

Roos, I., & Gustafsson, A. (2011). The influence of active and passive customer behavior onswitching in customer relationships. Managing Service Quality: An International Journal, 21(5), 448–464. doi:10.1108/09604521111159771

Schneider, B., & Bowen, D. (1999). Understanding customer delight and outrage. SloanManagement Review, 41(1), 35–45.

Shin, D. H., & Kim, W. Y. (2008). Forecasting customer switching intention in mobile service:An exploratory study of predictive factors in mobile number portability. TechnologicalForecasting and Social Change, 75(6), 854–874. doi:10.1016/j.techfore.2007.05.001

Sudhahar, J. C., Israel, D., Britto, A. P., & Selvam, M. (2006). Service loyalty measurement scale:A reliability assessment. American Journal of Applied Sciences, 3(4), 1814-1818. doi:10.3844/ajassp.2006.1814.1818

Svendsen, G. B., & Prebensen, N. K. (2013). The effect of brand on churn in the telecommunica-tions sector. European Journal of Marketing, 47(8), 1177–1189. doi:10.1108/03090561311324273

Thompson, R., Barclay, D. W., & Higgins, C. A. (1995). The partial least squares approach tocausal modeling: Personal computer adoption and use as an illustration. Technology Studies:Special Issue on Research Methodology, 2(2), 284–324.

Wamuyu, P. K. (2014). The role of contextual factors in the uptake and continuance of mobilemoney usage in Kenya. The Electronic Journal of Information Systems in Developing Countries,64(1), 1–19. doi:10.1002/(ISSN)1681-4835

Wong, K. K. (2013). Partial least squares structural equation modeling (PLS-SEM) techniquesusing SmartPLS. Marketing Bulletin, 24, Technical Note 1, 1–32.

JOURNAL OF AFRICAN BUSINESS 193

Yeboah-Asiamah, E., Nimako, S. G., Quaye, D. M., & Buame, S. (2016). Implicit and explicitloyalty: The role of satisfaction, trust and brand image in mobile telecommunication industry.International Journal of Business and Emerging Markets, 8(1), 94–115. doi:10.1504/IJBEM.2016.073402

Zhou, T. (2013). An empirical examination of continuance intention of mobile payment services.Decision Support Systems, 54(2), 1085–1091. doi:10.1016/j.dss.2012.10.034

194 E. YEBOAH-ASIAMAH ET AL.