promoting excellence in mission government statement …

TRANSCRIPT

1

UNDERSTANDING Y0UR FINANCIAL OVERSIGHT RESPONSIBILITIES

Martie Simpson, CPA ‐ Executive Director ‐ GFOAT

GFOAT Mission

Statement

Promoting Excellence in Government

Finance

2

2

GFOAT Virtual Fall Conference

3

UNDERSTANDING THE FINANCIAL PROCESS

4

3

What is Our Agenda Today?

• Fund Basics•Budgeting Basics•Capital Budget Basics• Tax Rates• Key Financial Policies• Financial Process• Funding Sources

5

Fund Basics: What are Funds?What are the types of Funds?

4

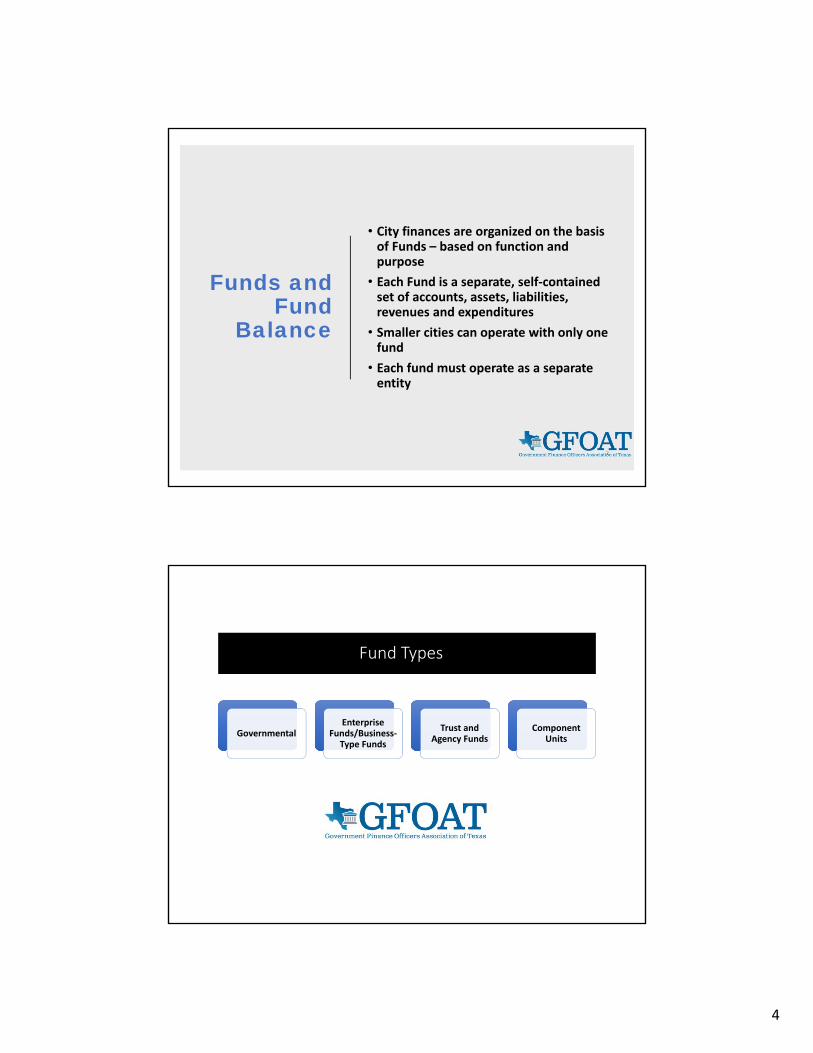

Funds and Fund

Balance

• City finances are organized on the basis of Funds – based on function and purpose

• Each Fund is a separate, self‐contained set of accounts, assets, liabilities, revenues and expenditures

• Smaller cities can operate with only one fund

• Each fund must operate as a separate entity

Fund Types

GovernmentalEnterprise

Funds/Business‐Type Funds

Trust and Agency Funds

Component Units

5

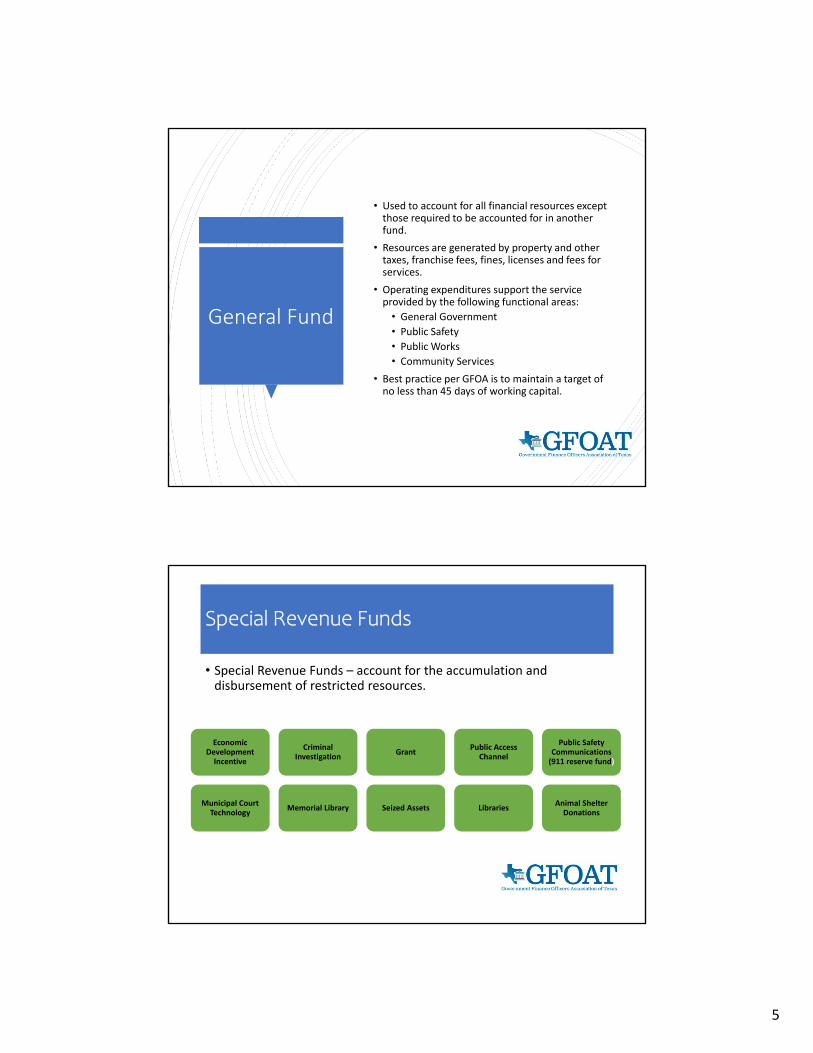

General Fund

• Used to account for all financial resources except those required to be accounted for in another fund.

• Resources are generated by property and other taxes, franchise fees, fines, licenses and fees for services.

• Operating expenditures support the service provided by the following functional areas:

• General Government

• Public Safety

• Public Works

• Community Services

• Best practice per GFOA is to maintain a target of no less than 45 days of working capital.

Special Revenue Funds

• Special Revenue Funds – account for the accumulation and disbursement of restricted resources.

Economic Development Incentive

Criminal Investigation

GrantPublic Access

Channel

Public Safety Communications (911 reserve fund)

Municipal Court Technology

Memorial Library Seized Assets Libraries Animal Shelter Donations

6

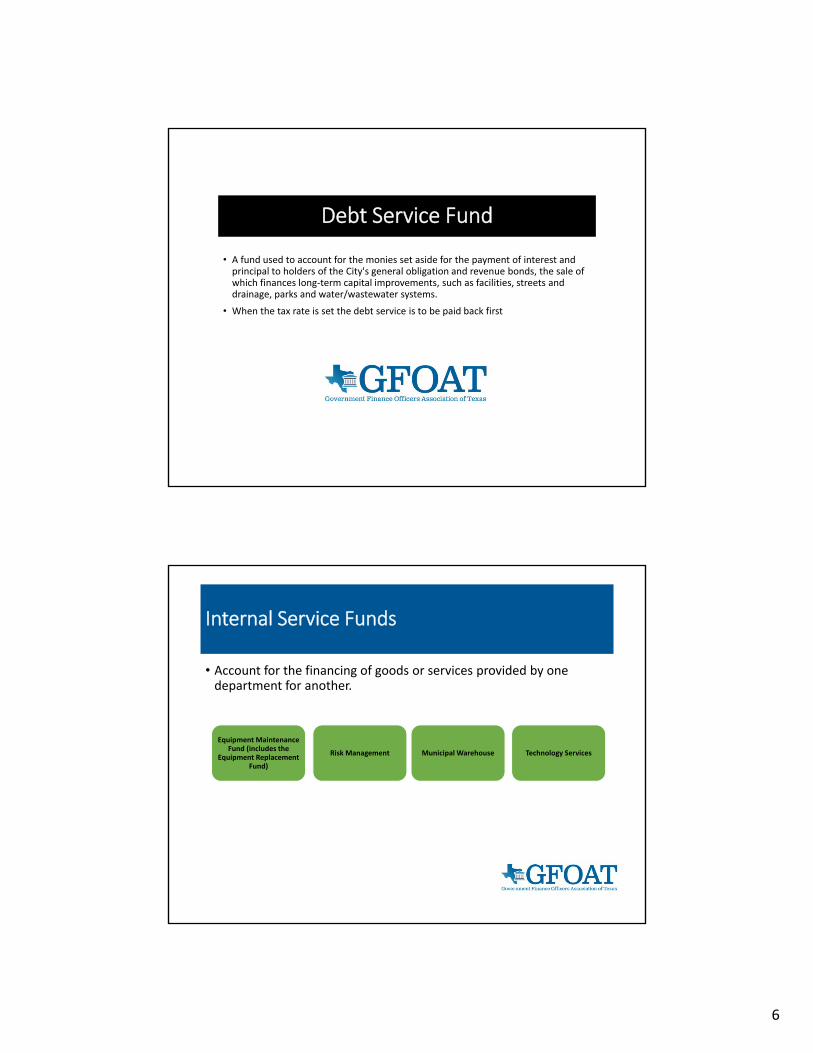

Debt Service Fund

• A fund used to account for the monies set aside for the payment of interest and principal to holders of the City's general obligation and revenue bonds, the sale of which finances long‐term capital improvements, such as facilities, streets and drainage, parks and water/wastewater systems.

• When the tax rate is set the debt service is to be paid back first

Internal Service Funds

• Account for the financing of goods or services provided by one department for another.

Equipment Maintenance Fund (includes the

Equipment Replacement Fund)

Municipal Warehouse Technology ServicesRisk Management

7

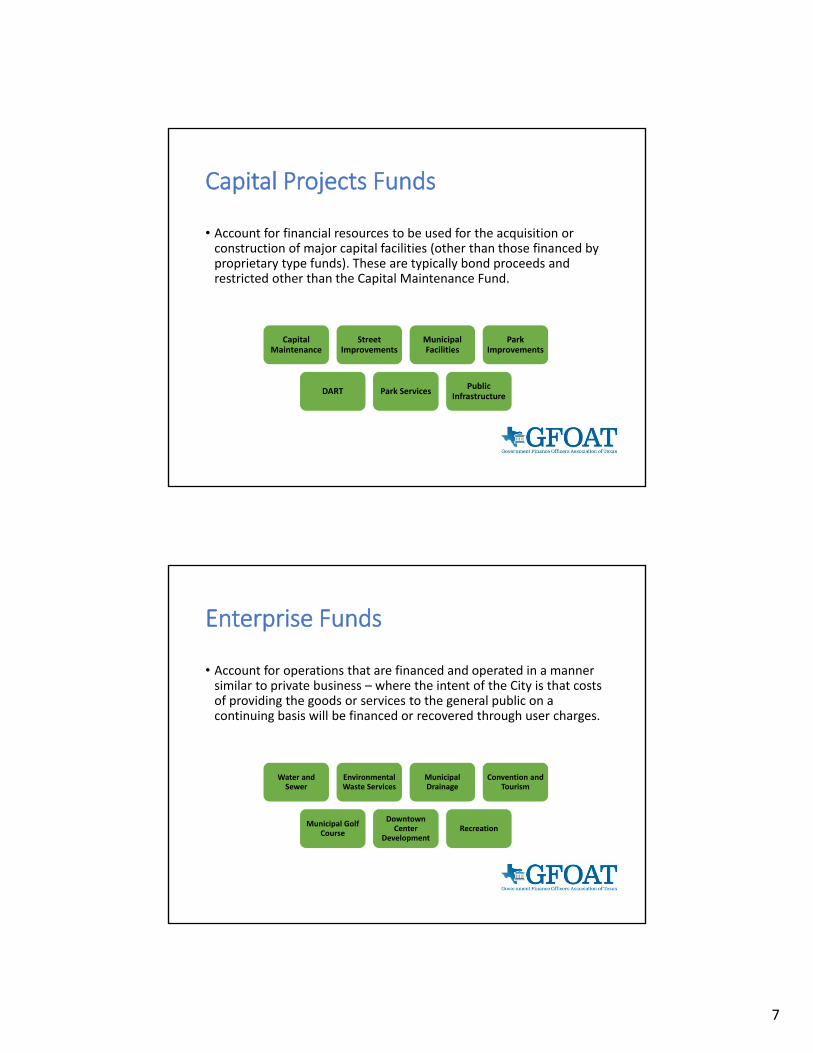

Capital Projects Funds

• Account for financial resources to be used for the acquisition or construction of major capital facilities (other than those financed by proprietary type funds). These are typically bond proceeds and restricted other than the Capital Maintenance Fund.

Capital Maintenance

Street Improvements

Municipal Facilities

Park Improvements

DART Park ServicesPublic

Infrastructure

Enterprise Funds

• Account for operations that are financed and operated in a manner similar to private business – where the intent of the City is that costs of providing the goods or services to the general public on a continuing basis will be financed or recovered through user charges.

Water and Sewer

Environmental Waste Services

Municipal Drainage

Convention and Tourism

Municipal Golf Course

Downtown Center

DevelopmentRecreation

8

Trust & Agency Funds

• Agency funds are restricted in how funds can be expended.

• Developers escrow is monies received from developers that must be returned to them once a project is completed.

• Unclaimed property must be held for the rightful owners.

• Trust funds are held in trust for the benefit of employees.

• Other Post‐Employment Benefits

• Retirement Security Plan

Component Units

Consideration to be classified as a component unit• Organization is legally separate

• City appoints a voting majority of the organizations board

• City is able to impose its will

• Organization has the potential to impose a financial burden on the City

• There is a fiscal dependency by the organization on the city

9

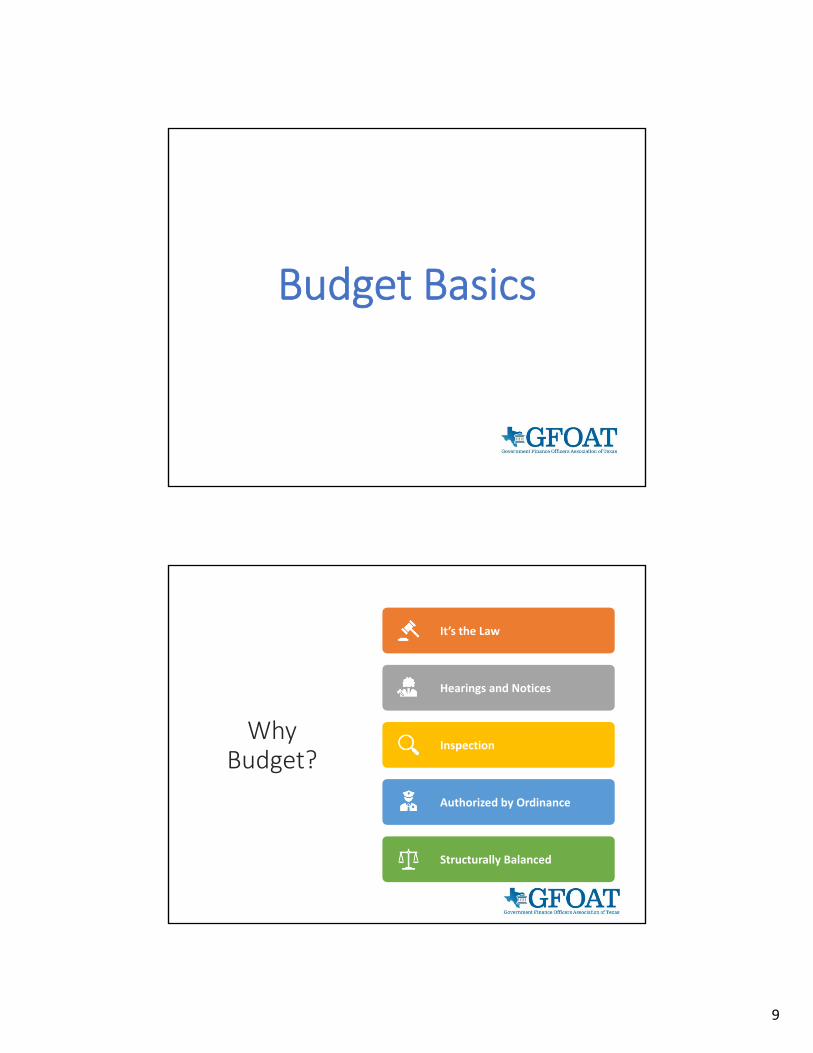

Budget Basics

Why Budget?

It’s the Law

Hearings and Notices

Inspection

Authorized by Ordinance

Structurally Balanced

10

Best Practices

• Government Finance Officers Association (GFOA) – www.gfoa.org

• 172 Best Practices covering 9 topic areas

• Distinguished Budget Award Program

• Certificate of Achievement for Excellence in Financial Reporting Program

• Elected Officials Guide Series

• National Advisory Council on State and Local Budgeting (NACSLB) ‐www.gfoa.org/services/nacslb.org

• Report issued in 1998

• Four principles and 58 recommendations

• Joint effort by 8 public sector associations

What is a Balanced Budget?

• Balanced Budget

Beginning Balance + Revenues

>= Expenditures

‐ Required by charter or state law

• Structurally Balanced Budget

Revenues = Expenditures• No use of fund balance to pay for expenses

20

11

Results of Good Budgeting Practices

•Good budgeting results in a number of positive financial outcomes •Balanced Budgets•Positive Budget Variances•Positive Fund Balances• Improved Bond Ratings•Avoidance of Enterprise Fund Subsidies/Transfers•Stable Finances

21

Phases of the

Budget Cycle

Establish Budget Focus

Three‐Year Financial Forecast

Revenue Estimates

Develop Proposed Budget

Budget Preparation: January ‐June

City Manager Recommended Budget submitted to Council

City Council reviews and approves budget & tax rate

•Adoption of the Budget & CIP first

•Tax Rate second

Budget Approval:

July ‐September

Periodic reporting and monitoring

Publish and submit Budget & CIP

Execution & Implementa

tion:October

The purpose of the audit is to ensure that the financial statements present fairly, in all material respects, the financial position of the City and have been prepared in accordance with U.S. generally accepted accounting principles and governmental accounting standards.

Annual Audit:January

12

Budget Management• Budget management is a continual process

• If we are not preparing a budget we are monitoring and reporting on the current budget

• Monthly reporting on finances

• Summarize key revenues and monitor expenditures

• Allows for early identification of potential issues

• Important to assess budget proposal on a long range forecast

• Decisions made this year impact every future year

• Budget needs to be sustainable

Why Develop a CIP?

“If You Fail to Plan, You Plan to Fail”

Benjamin Franklin

13

Capital Improvements Overview

What is a CIP?

Why Develop a Capital Plan

Community Input

The Budget Connection

What is a CIP?

• Capital Improvement Project: Construction, Major Maintenance and Improvement Projects. Includes Infrastructure Upgrades and Replacement

• Capital Improvement Plan: A 5 to 10 Year Plan

• Update Annually – Not “One and Done”

• Approved by Council

• Future Capital Improvement Projects

14

Why Develop a Capital Plan

Inform Your Citizens of what Projects are Planned

Inform Your Citizens of what Projects are Planned

Provides Certainty for the Future

Provides Certainty for the Future

Aides in Outreach and Construction Coordination

Aides in Outreach and Construction Coordination

Prioritizes Capital Construction & Maintenance

Prioritizes Capital Construction & Maintenance

Helps Forecast /Coordinate Long‐

term Needs

Helps Forecast /Coordinate Long‐

term Needs

Ensures Infrastructure is Maintained & Upgraded

Ensures Infrastructure is Maintained & Upgraded

Provides a Plan for Funding

Provides a Plan for Funding

Maintain High Bond RatingsMaintain High Bond Ratings

Allows Time to Plan for Large

Projects

Allows Time to Plan for Large

Projects

Killeen‐Fort Hood Regional Airport

15

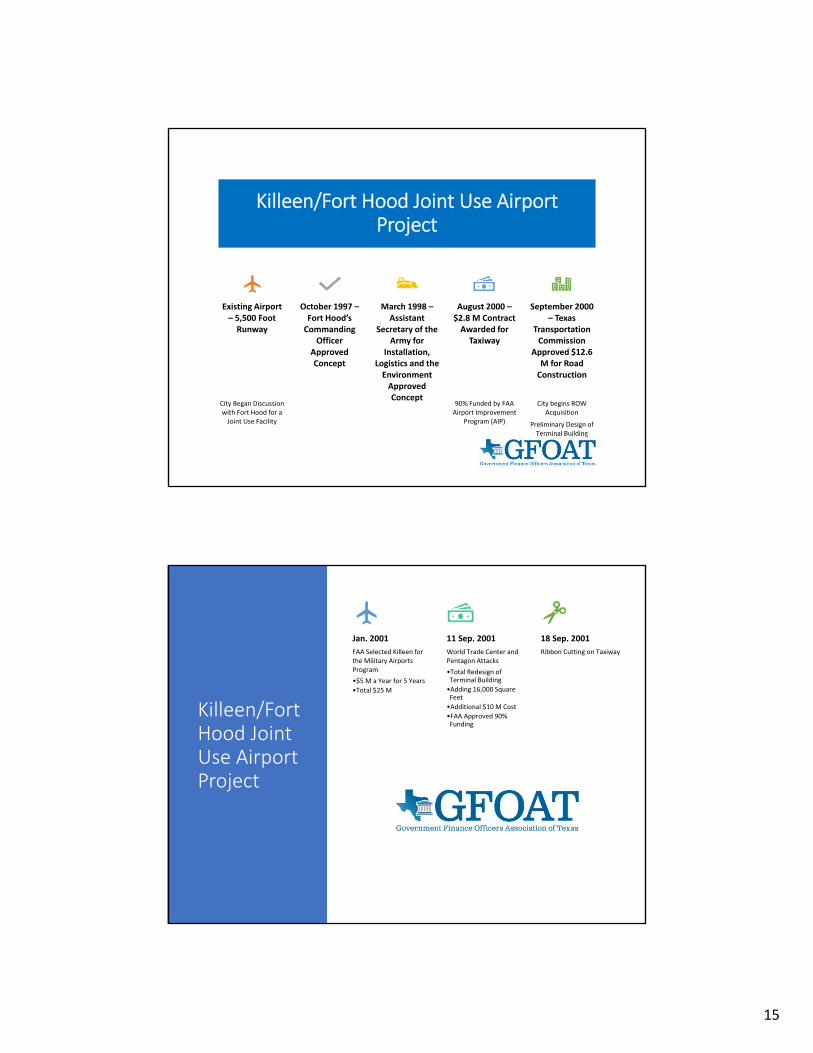

Killeen/Fort Hood Joint Use Airport Project

Existing Airport – 5,500 Foot Runway

City Began Discussion with Fort Hood for a Joint Use Facility

October 1997 –Fort Hood’s Commanding

Officer Approved Concept

March 1998 –Assistant

Secretary of the Army for

Installation, Logistics and the Environment Approved Concept

August 2000 –$2.8 M Contract Awarded for Taxiway

90% Funded by FAA Airport Improvement

Program (AIP)

September 2000 – Texas

Transportation Commission

Approved $12.6 M for Road Construction

City begins ROW Acquisition

Preliminary Design of Terminal Building

Killeen/Fort Hood Joint Use Airport Project

Jan. 2001

FAA Selected Killeen for the Military Airports Program

•$5 M a Year for 5 Years

•Total $25 M

11 Sep. 2001

World Trade Center and Pentagon Attacks

•Total Redesign of Terminal Building

•Adding 16,000 Square Feet

•Additional $10 M Cost

•FAA Approved 90% Funding

18 Sep. 2001

Ribbon Cutting on Taxiway

16

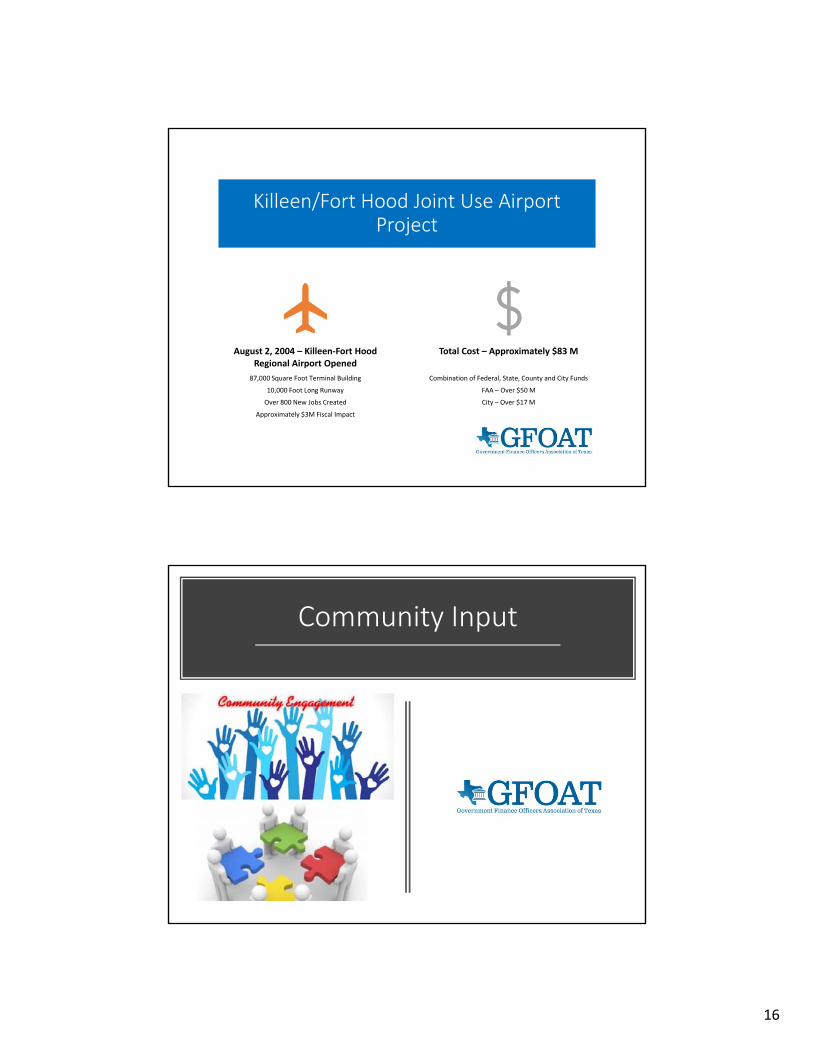

Killeen/Fort Hood Joint Use Airport Project

August 2, 2004 – Killeen‐Fort Hood Regional Airport Opened

87,000 Square Foot Terminal Building

10,000 Foot Long Runway

Over 800 New Jobs Created

Approximately $3M Fiscal Impact

Total Cost – Approximately $83 M

Combination of Federal, State, County and City Funds

FAA – Over $50 M

City – Over $17 M

Community Input

17

The Budget Connection

The Budget Connection –

How do These

Projects Fit

Funds Identified for Initial Construction

Annual Budgets Must Include Operating and Maintenance Costs

Inflation Should be Factored in to the Equation

Set Aside Contingency Funds

Internal Service Funds Used to Set Aside Funds for Future Purchases

SCBA

I Information Technology

Long Term Forecasting Included in the Annual Budget Process

18

Capital Maintenance Program

• Deferred Maintenance Increases Future Capital Costs

• On‐going Capital Maintenance is Included in Operating Budget

• Internal Service Funds ‐ “Lease” Equipment to Departments

• Lease Fees Fund Capital Repairs and Replacement

35

ALL TAXING UNITS

MUST PROPOSE A

TAX RATE

Tax Rate

19

Property Tax Rates Have Two Components:

Interest & Sinking (I&S)/Debt Service Tax Rate – Debt Service Fund

Maintenance & Operations (M&O) Tax Rate – General Fund

Tax Rate

Texas Constitution

Makes Taxpayers Aware of Rate Proposals

Can Limit Tax Increases

What is Truth‐in‐Taxation

20

Tax Code

Education Code

Water Code

Special District Local Laws Code

Where Do You Find TNT

What is Truth‐In‐ Taxation

Also Known as TNT

21

Appraisal District Provides Value

Governing Body Drafts Budgets

Tax Assessor Calculates Rates, May Publish Notices

Governing Body Proposes Rate/Holds Hearings

Governing Body Adopts Tax Rate

Tax Assessor Mails Bills

A Brief Review of the Process

Keep Last Year’s Revenue Using Current Year’s

Taxable Values

Truth‐In‐Taxation

22

Truth‐In‐Taxation

Old Terms

• Effective Tax Rate

• Rollback Tax Rate

New Terms

• No‐New‐Revenue Tax Rate

• Voter‐Approval Tax Rate

• De Minimis Rate

• Unused Increment Rate

2019 Truth‐In‐Taxation

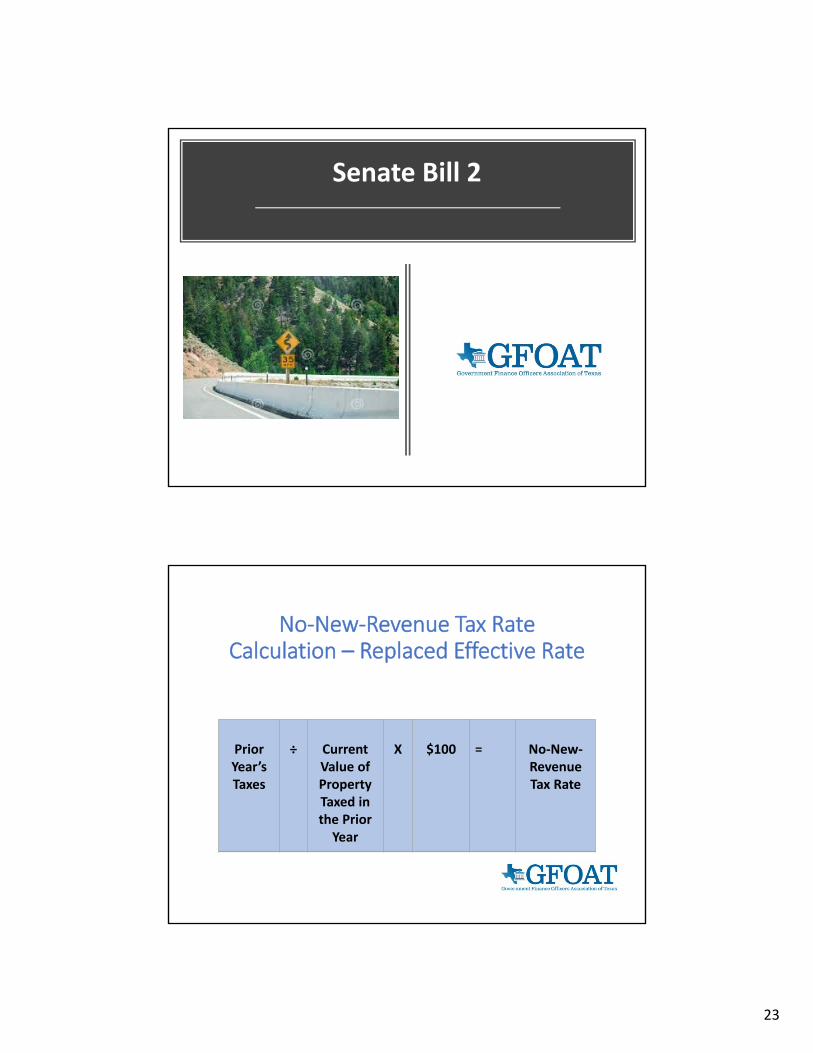

23

Senate Bill 2

No‐New‐Revenue Tax Rate Calculation – Replaced Effective Rate

PriorYear’s Taxes

÷ Current Value of Property Taxed in the Prior Year

X $100 = No‐New‐Revenue Tax Rate

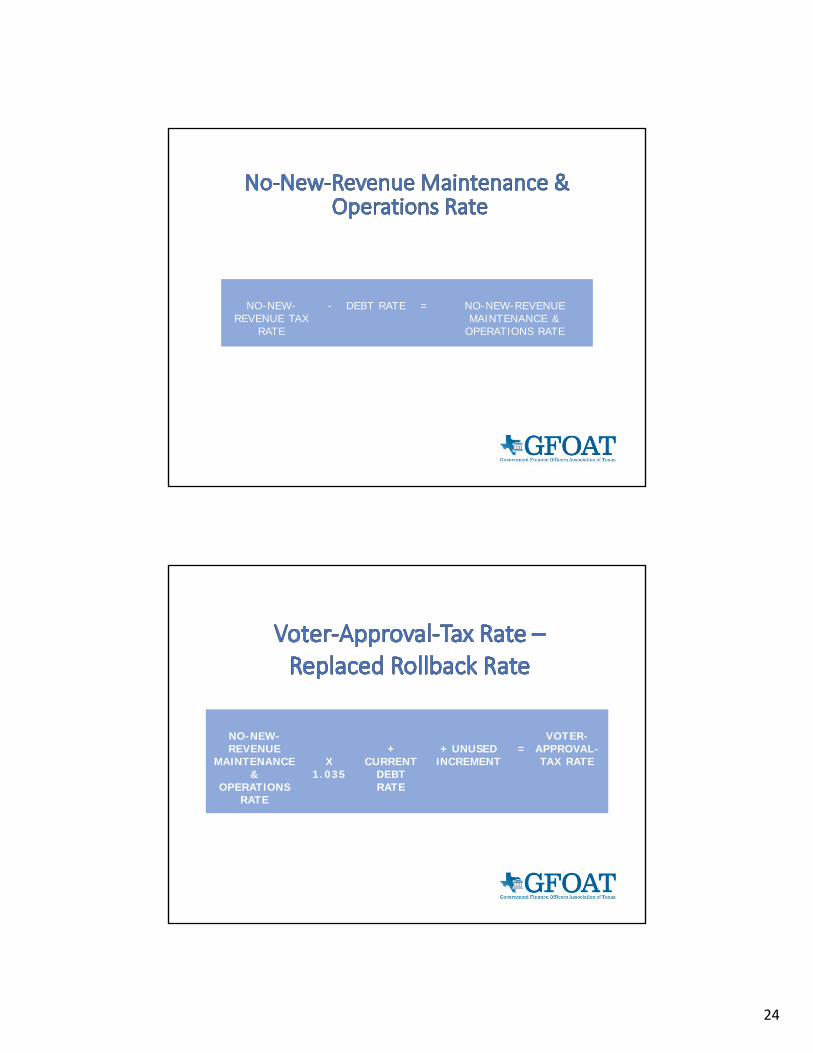

24

NO-NEW-REVENUE TAX

RATE

- DEBT RATE = NO-NEW-REVENUE MAINTENANCE &

OPERATIONS RATE

NO-NEW-REVENUE

MAINTENANCE &

OPERATIONS RATE

X 1.035

+ CURRENT

DEBT RATE

+ UNUSED INCREMENT

=VOTER-

APPROVAL-TAX RATE

25

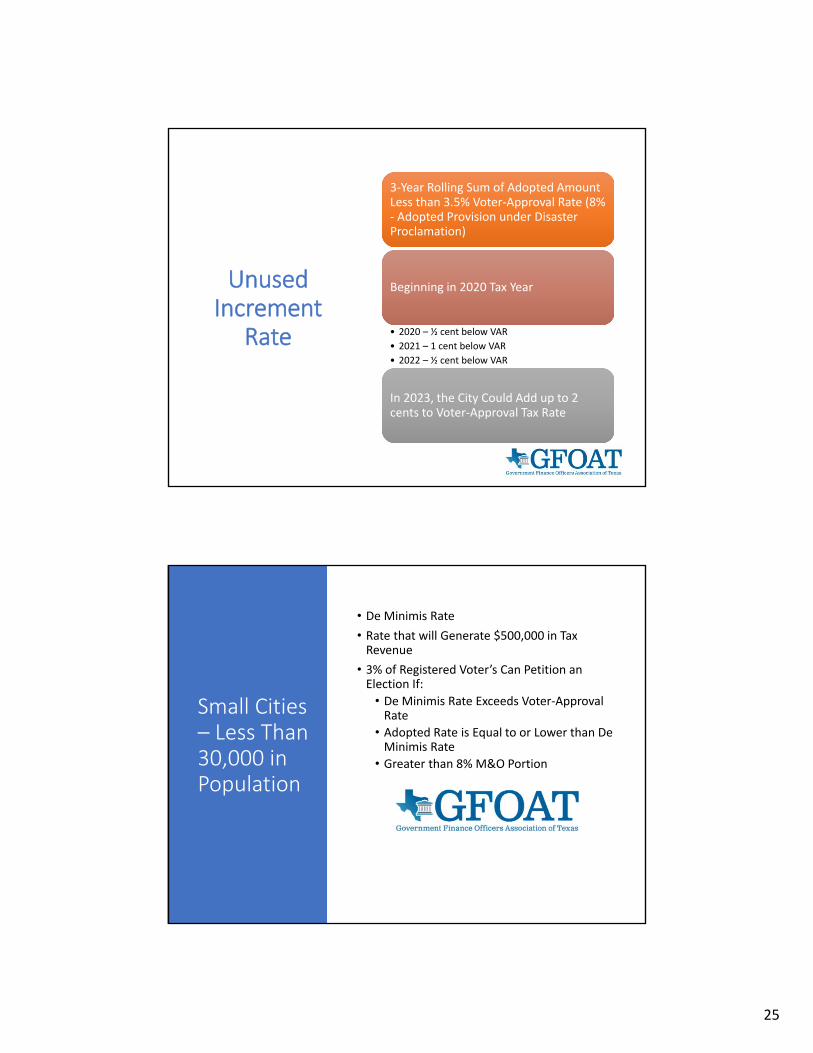

Unused Increment

Rate

3‐Year Rolling Sum of Adopted Amount Less than 3.5% Voter‐Approval Rate (8% ‐ Adopted Provision under Disaster Proclamation)

Beginning in 2020 Tax Year

• 2020 – ½ cent below VAR

• 2021 – 1 cent below VAR

• 2022 – ½ cent below VAR

In 2023, the City Could Add up to 2 cents to Voter‐Approval Tax Rate

Small Cities – Less Than 30,000 in Population

• De Minimis Rate

• Rate that will Generate $500,000 in Tax Revenue

• 3% of Registered Voter’s Can Petition an Election If:

• De Minimis Rate Exceeds Voter‐Approval Rate

• Adopted Rate is Equal to or Lower than De Minimis Rate

• Greater than 8% M&O Portion

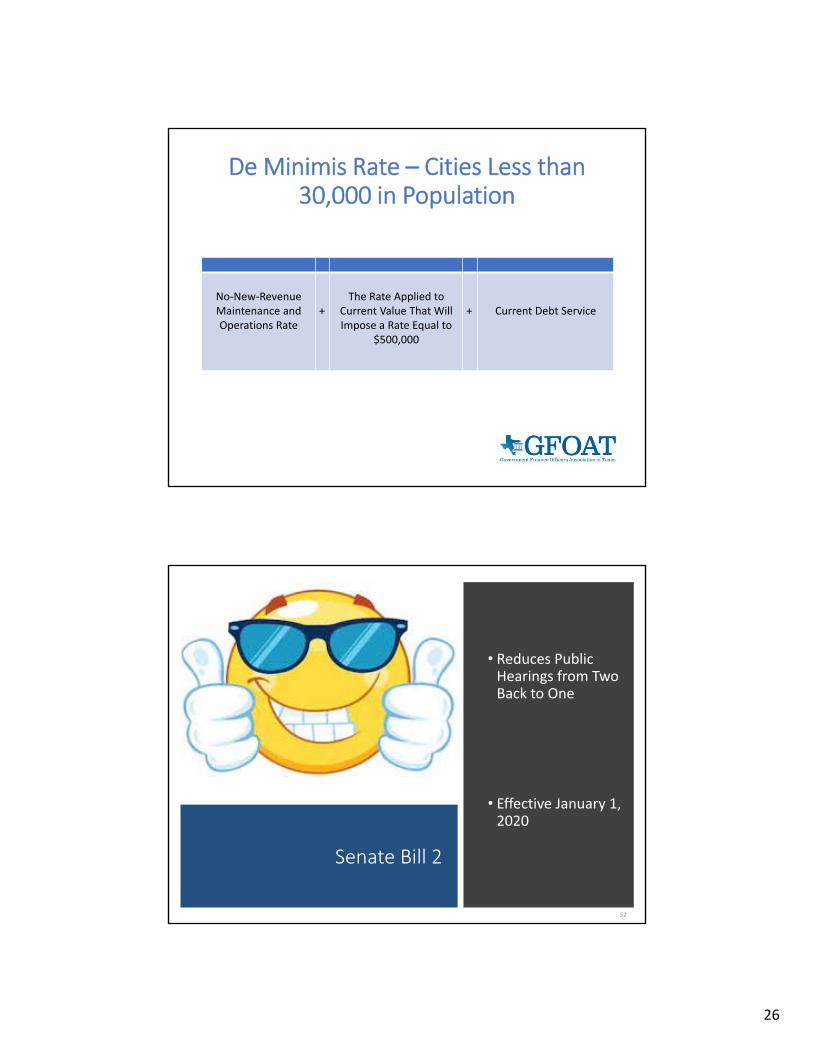

26

De Minimis Rate – Cities Less than 30,000 in Population

No‐New‐Revenue Maintenance and Operations Rate

+The Rate Applied to

Current Value That Will Impose a Rate Equal to

$500,000

+ Current Debt Service

Senate Bill 2

• Reduces Public Hearings from Two Back to One

• Effective January 1, 2020

52

27

What Are the Most Common Policies?

•Budget•Revenues/Expenditures• Fund Balance/Reserves•Accounting, Auditing and Financial Reporting

• Internal Control•Asset Management

53

OtherPolicies

• Capital Improvements and Maintenance

• Debt Management

• Investment

• Grants

• Economic Development

• Risk Management

• COVID 19

• Remote Work

• Safety Protocol

• Opening up City Offices

54

28

Financial Reporting Policies: What Governs Financial Reporting?

•State Law (TML Resources)

• Local Charter•Federal Agencies (SEC/MSRB)

• Industry Standards (GASB)•Management Policies

Asset Management

• Investment Policy

• Reviewed Annually by Council

• Confirms to Legal Requirements

• Governed by PFIA

• Required Training

• Adopted Policies

• Regular Reporting ‐ Quarterly

• Fixed Assets

• Capitalization Criteria ‐ $5,000

• GASB 34 Requirements

56

29

Debt Management

• Use of Debt Financing

• Future Use Against Future Payment

• Long‐Life Capital Assets

• Affordability Targets

• Debt Per Capita

• Debt as a Percent of Taxable Value

• Debt Service Payments as % of CurrentRevenues

• Debt Tax Rates as Percent of Total Tax Rate

• Sale Process

• Competitive vs. Negotiated

• Full and Continuing Disclosure

57

Types of Debt

• General Obligation

• Tax Supported and Voter Approved

• Certificates of Obligation

• Tax Supported

• Issued by Council after Notice Process

• Revenue Bonds

• Repaid through Rates

• Self‐Supporting Debt

• Tax Debt PAID FROM OTHER SOURCES

• Internal Borrowings

• Between Funds Within the City

58

30

Other Funding Alternatives

• Provides Guidelines on Alternative Funding for New Projects

• Grants• Documents Grant Funding Process

with Council• Use of Reserve Funds

• Used for Debt Management Purposes

• Developer Contributions• Links to Development Regulations

• Leases• Impact Fees• CARES Act

59

Accounting & Financial Reporting

• Provide Quarterly/Monthly Reports to Council

• Outside Audit Annually of all City Accounts

• Accountable Directly to City Council

• Prepare (CAFR)

• Follow GFOA Standards and Best Practices

60

31

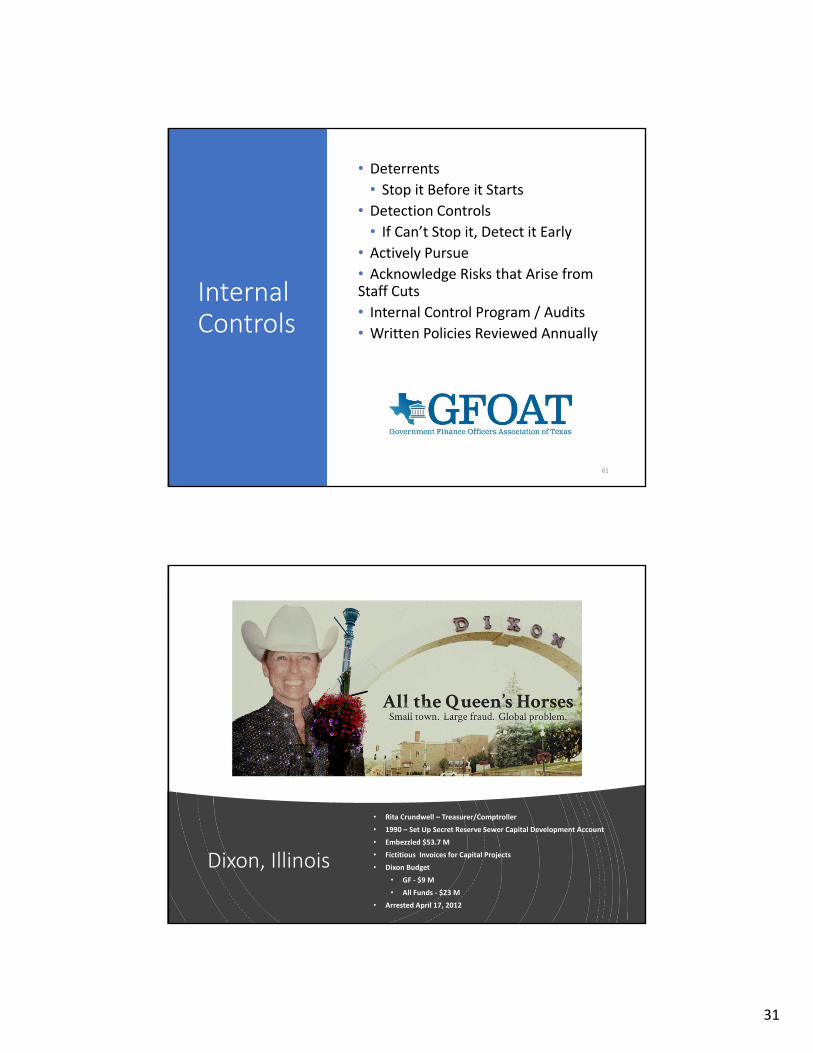

Internal Controls

• Deterrents

• Stop it Before it Starts

• Detection Controls

• If Can’t Stop it, Detect it Early

• Actively Pursue

• Acknowledge Risks that Arise from Staff Cuts

• Internal Control Program / Audits

• Written Policies Reviewed Annually

61

Dixon, Illinois

• Rita Crundwell – Treasurer/Comptroller

• 1990 – Set Up Secret Reserve Sewer Capital Development Account

• Embezzled $53.7 M

• Fictitious Invoices for Capital Projects

• Dixon Budget

• GF ‐ $9 M

• All Funds ‐ $23 M

• Arrested April 17, 2012

32

Financial Reserves

• Fund Balance Policy – 25‐30%

• Rainy Day Fund for Unexpected Emergency

• 90 Day Reserve in General Fund

• 30 Days = “Emergency” Funds

• Offset Sudden Tax Increase

• Replenished Next Budget Cycle

• 60 Days = Long‐term Reserves

63

Revenue ProjectionsWhere does the money come from?

33

Forms of Revenue (General Fund)

Ad Valorem Sales Tax

Franchise Fees

Fines and Forfeitures

Permits

Forms of Revenue (Non‐General Fund)

Water & Sewer Fund

Solid Waste Fund

Municipal Drainage Fund

Convention and Tourism Fund

Recreation Fund

Golf Course

34

Policy Review & Benchmarking

•Review financial policies annually during the budget process

•Clarify areas that may be confusing

• Look for new ways to improve the policy•Example: Addition of a “revenue shortfall contingency plan”

Conclusion

Allow policies to guide City’s financial operations

1

Adhere to the guidelines addressed in the policies

2

Benchmark to ensure policies are reasonable and achieve desired goals

3

Communicate policies and guidelines to citizens and employees

4

35

Technical Resources

GFOA –www.gfoa.org

Best Practices

Elected Officials Guide Series

TML Series – www.tml.org

GFOAT ‐www.gfoat.org

Finance Forum

National Council on State and Local Budgeting (NACSLB) Publications

Contact info:Martie Simpson,

Executive Director GFOAT