r and rewards - soa

TRANSCRIPT

In This Issuepage

A 99-Year Prospective Test of anInterest-Rate Theoryby Daniel F. Case . . . . . . . . . . . 21

Actuarial Principles of Asset-Liability Management . . . . . . . . . . 2

Applying Insurance CompanyQuantitative Techniques forImproved Capital Budgetingby Tony Dardis and Andrew Berry 16

The Baby Boom, the Baby Bust, and Asset Marketsby Timothy Cogley and Heather Royer . . . . . . . . . . . . . 12

Call for Authors! . . . . . . . . . . . . . . . . 1

pageCapital Projects Working Party—

Recruitment Drive . . . . . . . . . . . 19Competing Education

by Zain Mohey-Deen . . . . . . . . . 31Fair Value Conference

by Shirley Hwei-Chung Shao . . . . 32It’s Time to Give More Focus to

Risk Controlby Patrick Reinkemeyer . . . . . . . . 20

October’s Market Demons: The ‘87Stock Market Crash andLikelihood of a Recurrenceby Vinod Chandrashekaran . . . . . . 3

pageReview of Financial Journals

Reviewed by Edwin A. Martin . . . 27Subjective Value at Risk

by Glyn Holton . . . . . . . . . . . . . 14Synthetic GIC and Guaranteed Separate

Account Model Regulationsby Victor Modugno . . . . . . . . . . . 1

Taking Stock: No Pain, No Gain, orWhat They Did Not Tell YouAbout Goldilocksby Nino Boezio . . . . . . . . . . . . . 11

What One Can Learn from the Bankof Canadaby Nino Boezio . . . . . . . . . . . . . 29

Synthetic GIC and Guaranteed Separate Account Model Regulations

RISKS and REWARDS

The Newsletter of the Investment Section of the Society of Actuaries NUMBER 31 OCTOBER 1998

Call for Authors! isks and Rewards needs yourRhelp. We have some ideas forfuture articles but are in dire needof authors. Some ideas we have

are:Review of Professor Richard Tha-ler’s speech (author of “The Win-ner’s Circle”) at the Investment Sec-tion breakfast at the Annual Meeting. If you are going to be at the break-fast, please volunteer.Financial Patents. There have beennew patents issued on financial top-ics, including one to an actuary andformer Section officer, MeyerMelnikoff. This article would dis-cuss financial patents in general andreview the specifics of one or morepatents. Richard Wendt, co-editor ofRisks and Rewards, has the patentdetails from the U.S. Patent Office. If you are interested in authoringsuch as an article, please contact Mr.Wendt at his Directory address.Review of Financial Economics, thenew text published by the ActuarialFoundation. Two articles would beappropriate to cover the breadth ofthis topic.If you would like to volunteer for one

of these topics, or have other ideas forarticles, please contact one of the co-edi-tors listed on page 2.

by Victor Modugno

wo new model regulations—one an accounting standard (SSAP 89),Tcovering synthetic GICs and the which governs accounting and reservingother guaranteed separate ac- for separate accounts. There is no ac-counts—are working their way counting standard for synthetics.

through the regulatory process. Both Industry groups developed initialwere on the agenda of the 1998 NAIC drafts of these model regulations based onsummer meeting held in Boston in June. existing separate account and syntheticA working group under the Life Insur- GIC regulations—New York Regulationance (A) Committee is developing the 128, California Insurance Code SectionsSynthetic GIC regulation. Action on 10506.4 and 10507, and Bulletins 95–8adapting a proposed model regulation was and 95–10. Reserves were based ondeferred until the fall meeting due to con- guaranteed values discounted at 1.05 oftroversy over several provisions in the treasury spot rates while market value oflatest draft. A working group under the assets were reduced by asset valuationAccounting Practices and Procedures reserve-based factors. The synthetic GIC(EX4) Task Force is developing the guar- regulation had several required contractanteed separate account regulation. A provisions, which seemed unusual be-revised model regulation was exposed for cause the purchasers of these contractscomment. Both regulations are available are large institutions that are representedon the NAIC web site (naic.org). The by attorneys and other experts. Mandatedweb site also has contact persons for com- contract provisions are not needed forments. consumer protection.

Most regulators in the working These drafts then went to the regula-groups and industry representatives of the tory task forces. There were several con-interested parties are the same for these ference calls and redrafts. Many of thetwo regulations. The main difference ideas developed by the synthetic groupbetween these two products is whether the were incorporated into the separate ac-assets subject to guarantees are held in a count regulation. The revised filing re-trust (synthetic GIC) or in an insurance quirements were of greatest concern tocompany separate account. The reason the industry group. In the for different working groups is that sepa-rate accounts are subject to continued on page 2, column 1

PAGE 2 RISKS AND REWARDS OCTOBER 1998

RISKS AND REWARDS

Issue Number 31 October 1998Published by the Investment Section of the Society of Actuaries

475 N. Martingale Road, Suite 800Schaumburg, IL 60173

Phone: 847–706–3500 Fax: 847–706–3599 World Wide Web: http://www.soa.orgThis newsletter is free to Section members. A subscription is $15.00 for nonmembers.

Current-year issues are available from the Communications Department.Back issues of Section newsletters have been placed in the Society library.

Photocopies of back issues may be requested for a nominal fee.Editor this issue:Nino J. BoezioMatheis Associates1099 Kingston RoadSuite 204Pickering, ON L1V 1B5CanadaPhone: 905–837–2600Fax: 905–837–2598Luke GirardLincoln Investment Mgmt. Phone: 219–455–4592Richard WendtTowers PerrinPhone: 215–246–6557Anthony DardisTillinghast-Towers PerrinPhone: 972–701–2739

Associate Editors:William Babcock, Finance and Investment JournalsEdwin Martin, Finance and Investment JournalsJoseph Koltisko, Insurance Company Finance and Investment TopicsGustave Lescouflair, Pension Plan Finance and Investment TopicsVic Modugno, Insurance Company Finance and Investment Topics

Investment Council:Joseph H. Tan, ChairpersonJosephine Elisabeth Marks, Vice-ChairChristian-Marc Panneton, TreasurerKlaus O. Shigley, SecretaryCouncil Members:Judy L. StrachanFrederick W. JacksonDavid X. LiFrancis P. SabatiniPeter D. Tilley

Expressions of opinion stated herein are, unless expressly stated to the contrary, not the opinion orposition of the Society of Actuaries, its Sections, its Committees, or the employers of the authors.The Society assumes no responsibility for statements made or opinions expressed in the articles,

criticisms, and discussions contained in this publication.

Copyright 1998 Society of ActuariesAll rights reserved. Printed in the United States of America.

Synthetic GICcontinued from page 1

original draft, a company would need to deregulation trend for sophisticated pur- the contract must be large, double-Aget approval of plan of operation in its chasers. Another area of comment was rated, and have appropriate staff to passdomiciliary state. So long as that state competition with banks. Banks in the the GIC manager’s due-diligence. Issuershad requirements similar to the model synthetic business can negotiate contracts who are allowed to bid are concernedregulation, other states would accept this with clients without getting advance ap- about protecting their capital and preserv-determination. Previously approved con- proval. Bank regulators focus on internal ing their high ratings from Moody’s andtract forms would be grandfathered. In risk management and controls of these S&P, which are needed to remain in thisthe latest draft, approval of the plan of and other businesses of the bank using business. They also have a group of ex-operation would be required in each state sophisticated value-at-risk measurements. perts in this field, including attorneys,in which the insurer wants to issue con- Others commented that only the domicili- investment professionals, and underwrit-tracts and grandfathering of existing con- ary state had all the information needed to ing and product experts. The potentialtracts is limited. assess solvency. State insurance depart- abuse of this product by a small-unrated

The synthetic GIC regulation was ments should use their limited resources insurer or unsophisticated buyer could befurther along in development and elicited where they can add the most value—in controlled through the financial qualifica-the most comments from industry repre- monitoring overall solvency of domestic tion requirements to issue or purchasesentatives prior to the Boston meeting. insurers and protecting unsophisticated these contracts.Most letters expressed concern about the consumers from abuses. Because of objections raised duringfiling requirements and the actuarial opin- Consider the typical separate account the Boston meeting, action on adoptingion and memorandum. A letter from the or synthetic GIC sale. A GIC manager, the synthetic GIC model regulation wasStable Value Association opposing the who specializes in purchasing these con- deferred until the next meeting. Mean-filing requirements indicated that buyers tracts, requests proposals for a large while an industry group is trying to orga-prefer efficient and effective regulation. 401k-plan client or a pool of smaller cli- nize united opposition to some of theAccording to that comment letter, these ents. This manager has investment pro- more burdensome requirements of theregulations are out of line with the current fessionals, credit analysts, and attorneys proposed regulations.free market, with substantial experience in these ar-

rangements. The insurer or bank issuing Victor Modugno, FSA, is Vice Presidentat Transamerica Asset Management inLos Angeles, California.

Actuarial Principles of Asset-Liability Management

he ALM Principles Task Force ofTthe SOA, chaired by MikeHughes, has completed a seconddraft version of Actuarial Princi-

ples of Asset-Liability Management. Thetask force welcomes your comments andsuggestions. The draft document can bedownloaded from the SOA HomePage/Libraries/Finance and Invest-ments/ALM Principles. You may alsorequest a hard copy by contacting CherieHarrold at 847–706–3598.

Please provide any comments or editson the draft Actuarial Principles of Asset-Liability Management to Kevin Long viae-mail at [email protected] or fax at847–706–3599.

Figure 1: Distribution function of the minimum outcome from N draws from a normal distribution

0.0

0.2

0.4

0.6

0.8

1.0

1.2

N=1

N=10

N=100

N=1000

OCTOBER 1998 RISKS AND REWARDS PAGE 3

October’s Market Demons: The ‘87 Stock MarketCrash and Like-lihood of a Re-currence by Vinod Chandrashekaran

Editor’s Note: The following article originally appeared in the Winter 1998 issueof The BARRA Newsletter, Horizon, andis reprinted here with permission.

onday, October 27, 1997, wit-Mnessed a drop of 554 points inthe Dow Jones Industrial Av-erage, the largest one-day

point drop in the history of the market.Dramatic as it was, this drop was only thetwelfth-largest fall in percentage terms.The largest percentage drop in the historyof the stock market occurred on Monday,October 19, 1987, when the S&P 500Index declined by 20.5%. The recentsharp movements witnessed in globalmarkets raise an important question:What is the likelihood of market crashes? This article seeks to provide an answer tothis and related questions by focusingmainly on the crash of October 1987. Specifically, we shall seek answers tothree questions:1. Given the history of market returns,

was the crash of ‘87 unusual?2. How do conditional variance models

(such as GARCH) behave aroundperiods of extreme moves in the mar-ket?

3. What is the impact of the crash onbacktesting and performance evalua-tion?

I. Was the Crash of ‘87 Unusual?

The average daily return and the standarddeviation of the daily return on the S&P500 Index over the last two decades havebeen about 0.066% and 0.96%, respec-tively. On October 19, 1987, the indexhad a return of 20.5%, which is approx-imately a 20-sigma event. If we make thesimplifying assumption that daily returnsfollow a lognormal distribution, then theprobability of observing a 20-sigma eventis approximately equal to 2.75 × 10 . 89

Based on this analysis, we would con-

clude that the crash of ‘87 was a rare and pendent draws from a normal distributionunusual event. with mean zero and standard deviation 1. Effects of Repeated Draws Define a new random variable Y as fol-from One Distribution lows: Y=min (X , ..., X ). Figure 1

graphs the cumulative distribution func-We can learn a bit more about the likeli-hood of a crash by taking a slightly differ-ent perspective. The return of 20.5%does not represent a single draw from alognormal distribution. The history ofpublicly available daily returns on theU.S. stock market goes back over 100years, and the random return on October19, 1987, represents but one of the over25,000 daily returns that have been ob-served over the last century. A more ap-propriate question to ask is: Given that wehave observed 100 years of returns, whatis the probability that one of the observedreturns is 20.5%? Since the return onthe S&P 500 Index on October 19, 1987,is the lowest on record, we can ask thisquestion slightly differently as well: Given that we have observed 100 years ofreturns, what is the probability that theminimum daily return we will observe is

20.5%?To see how much difference this per-

spective makes, let us consider a simpleexample. Let X1, ..., X denote N inde-N

1 N

tion of Y for N=1, 10, 100, 1000. As wewould intuitively expect, the figure showsthat the distribution of Y shifts to the leftas the value of N increases. Table 1 liststhe probability that Y is less than 2 (a2-sigma

continued on page 4, column 1

TABLE 1Probability That the Minimum Outcome from N Draws Is a 2-Sigma or a 3-Sigma Event

N (Y< 2) (Y< 3)Prob Prob

1 0.023 0.00110 0.214 0.013

100 0.911 0.1261000 1.000 0.741

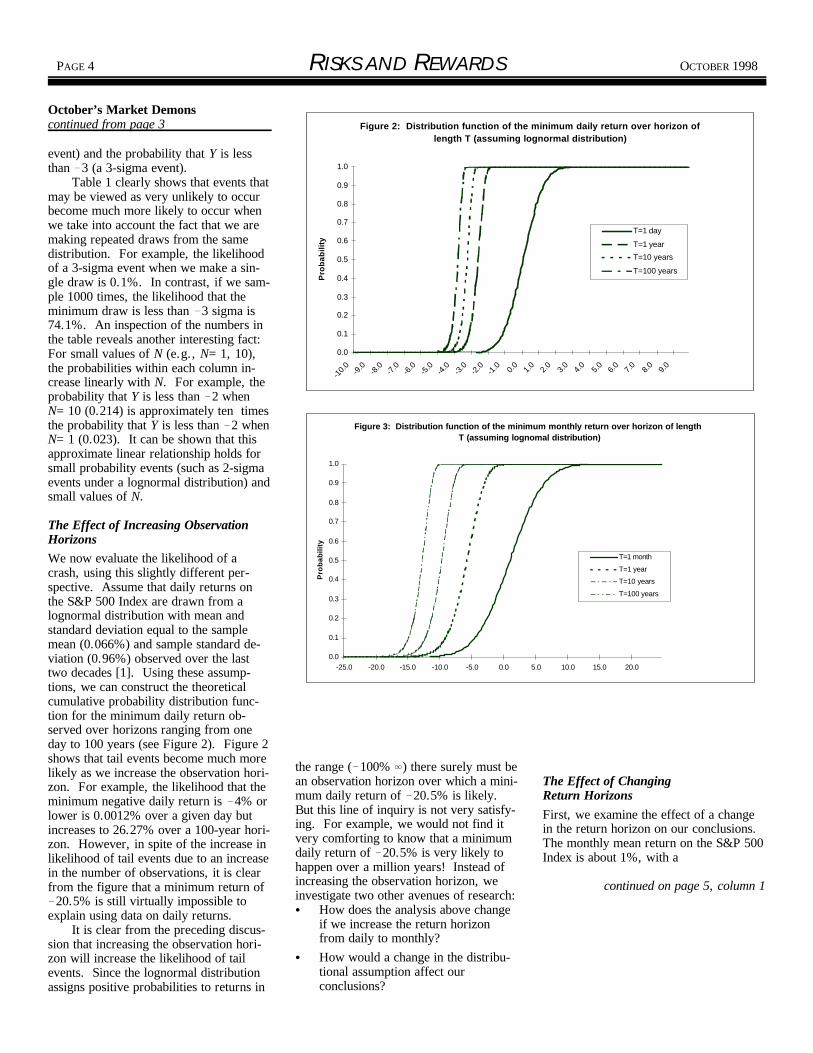

Figure 2: Distribution function of the minimum daily return over horizon of length T (assuming lognormal distribution)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-10.0 -9

.0-8

.0-7

.0-6

.0-5

.0-4

.0-3

.0-2

.0-1

.0 0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0 9.0

Pro

bab

ility

T=1 day

T=1 year

T=10 years

T=100 years

Figure 3: Distribution function of the minimum monthly return over horizon of length T (assuming lognomal distribution)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-25.0 -20.0 -15.0 -10.0 -5.0 0.0 5.0 10.0 15.0 20.0

Pro

bab

ility

T=1 month

T=1 year

T=10 years

T=100 years

PAGE 4 RISKS AND REWARDS OCTOBER 1998

October’s Market Demonscontinued from page 3

event) and the probability that Y is lessthan 3 (a 3-sigma event).

Table 1 clearly shows that events thatmay be viewed as very unlikely to occurbecome much more likely to occur whenwe take into account the fact that we aremaking repeated draws from the samedistribution. For example, the likelihoodof a 3-sigma event when we make a sin-gle draw is 0.1%. In contrast, if we sam-ple 1000 times, the likelihood that theminimum draw is less than 3 sigma is74.1%. An inspection of the numbers inthe table reveals another interesting fact:For small values of N (e.g., N=1, 10),the probabilities within each column in-crease linearly with N. For example, theprobability that Y is less than 2 whenN=10 (0.214) is approximately ten timesthe probability that Y is less than 2 whenN=1 (0.023). It can be shown that thisapproximate linear relationship holds forsmall probability events (such as 2-sigmaevents under a lognormal distribution) andsmall values of N.

The Effect of Increasing ObservationHorizonsWe now evaluate the likelihood of acrash, using this slightly different per-spective. Assume that daily returns onthe S&P 500 Index are drawn from alognormal distribution with mean andstandard deviation equal to the samplemean (0.066%) and sample standard de-viation (0.96%) observed over the lasttwo decades [1]. Using these assump-tions, we can construct the theoreticalcumulative probability distribution func-tion for the minimum daily return ob-served over horizons ranging from oneday to 100 years (see Figure 2). Figure 2shows that tail events become much morelikely as we increase the observation hori-zon. For example, the likelihood that theminimum negative daily return is 4% orlower is 0.0012% over a given day butincreases to 26.27% over a 100-year hori-zon. However, in spite of the increase inlikelihood of tail events due to an increasein the number of observations, it is clearfrom the figure that a minimum return of

20.5% is still virtually impossible toexplain using data on daily returns.

It is clear from the preceding discus-sion that increasing the observation hori-zon will increase the likelihood of tailevents. Since the lognormal distributionassigns positive probabilities to returns in

the range ( 100% ) there surely must bean observation horizon over which a mini- The Effect of Changing mum daily return of 20.5% is likely. Return HorizonsBut this line of inquiry is not very satisfy-ing. For example, we would not find itvery comforting to know that a minimumdaily return of 20.5% is very likely tohappen over a million years! Instead ofincreasing the observation horizon, weinvestigate two other avenues of research:

How does the analysis above changeif we increase the return horizonfrom daily to monthly?How would a change in the distribu-tional assumption affect ourconclusions?

First, we examine the effect of a changein the return horizon on our conclusions. The monthly mean return on the S&P 500Index is about 1%, with a

continued on page 5, column 1

Figure 4: Distribution function of the minimum daily return over horizon of length T (assuming t-distribution with 5 df)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-25.0 -20.0 -15.0 -10.0 -5.0 0.0 5.0 10.0 15.0 20.0

Pro

bab

ility T=1 day

T=1 year

T=10 years

T=100 years

Figure 5: Distribution function of the minimum daily return over horizon of length T (assuming t-distribution with 3 df)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-25.0 -20.0 -15.0 -10.0 -5.0 0.0 5.0 10.0 15.0 20.0

Pro

bab

ility T=1 day

T=1 year

T=10 years

T=100 years

vv 2

.

vv

v 2

½

vr

OCTOBER 1998 RISKS AND REWARDS PAGE 5

October’s Market Demonscontinued from page 4

standard deviation of about 4%. Usingthese statistics, Figure 3 graphs the cumu-lative probability distribution function forthe minimum monthly return over obser-vation horizons ranging from one monthto 100 years. The probability that theminimum monthly return over a 100-yearobservation period is less than 21.5%(which was the return on the S&P 500Index over the month of October 1987) isapproximately 0.0067%. These numberssuggest that even when we look atmonthly returns, the market crash repre-sents a very unlikely event.

The Effect of Changing Distribution As-sumptionsNext we examine the effect of a change inthe distributional assumption on our re-sults. It is well-known that the uncondi-tional distribution of stock returns is char-acterized by the presence of fat tails. Adirect implication of this is that tail eventsare more likely than the lognormal distri-bution would predict. This line of inquiryhas a long history. Fama [2] concludedthat stock returns appeared to be drawnfrom a member of the stable Paretianfamily of distributions with infinite vari-ance. The normal distribution belongs tothe stable Paretian class and is the onlymember of this class with finite variance. Subsequent researchers have shown that ifthe time series of market returns is drawnfrom normal distributions withtime-varying variances, then the uncondi-tional distribution of market returnswould have fat tails.

One popular alternative to thelognormal assumption is to assume thatthe unconditional distribution of stockreturns is log-t. The log-t distributionarises when stock returns for each periodare lognormally distributed, with eachperiod’s variance being drawn from aninverted gamma distribution. If a randomvariable U has a log-t distribution with vdegrees of freedom, then log (U) t ,vwhere t follows a t-distribution with vvdegrees of freedom. The expected valueof log (U) is zero, and the variance of log(U) is equal to:

Let: .

Let r denote the log of 1 plus the rate of are infinite. (Note that in the latter casereturn on the market. The mean and the distribution has infinite kurtosis.)standard deviation of r are denoted by Figures 4 and 5 display the cumula-and respectively. tive probability distribution function for

In our study, we assume that: the minimum daily return for observation

.

follows a t-distribution with v degrees offreedom. We will present results for thecases v=5 and v=3. A point worth not-ing about t-distributions is that all evenmoments of orders equal to or greaterthan the v moment are infinite. So, forth

example, when v=5, even moments oforder 6 and above are infinite; and when

v=3, even moments of order 4 and above

horizons ranging from one day to 100years for v=5 and v=3, respectively. Anexamination of the graphs reveals that, asanticipated, tail events

continued on page 6, column 1

PAGE 6 RISKS AND REWARDS OCTOBER 1998

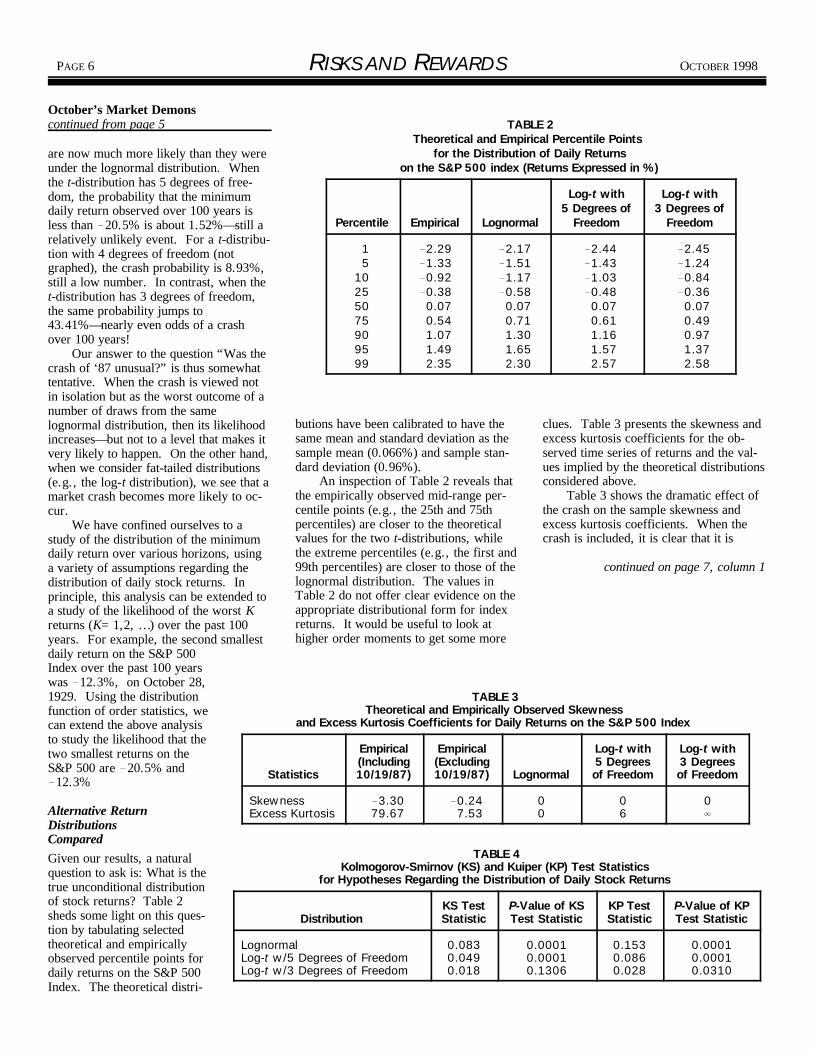

TABLE 2Theoretical and Empirical Percentile Points

for the Distribution of Daily Returnson the S&P 500 index (Returns Expressed in %)

Percentile Empirical Lognormal

Log-t with5 Degrees of

Freedom

Log-t with3 Degrees of

Freedom

15

10255075909599

2.291.330.920.380.070.541.071.492.35

2.171.511.170.580.070.711.301.652.30

2.441.431.030.480.070.611.161.572.57

2.451.240.840.360.070.490.971.372.58

TABLE 3Theoretical and Empirically Observed Skewness

and Excess Kurtosis Coefficients for Daily Returns on the S&P 500 Index

Statistics

Empirical(Including10/19/87)

Empirical(Excluding10/19/87) Lognormal

Log-t with5 Degreesof Freedom

Log-t with3 Degreesof Freedom

SkewnessExcess Kurtosis

3.3079.67

0.247.53

00

06

0

TABLE 4Kolmogorov-Smirnov (KS) and Kuiper (KP) Test Statistics

for Hypotheses Regarding the Distribution of Daily Stock Returns

DistributionKS TestStatistic

P-Value of KSTest Statistic

KP TestStatistic

P-Value of KPTest Statistic

LognormalLog-t w/5 Degrees of FreedomLog-t w/3 Degrees of Freedom

0.0830.0490.018

0.00010.00010.1306

0.1530.0860.028

0.00010.00010.0310

October’s Market Demonscontinued from page 5

are now much more likely than they wereunder the lognormal distribution. Whenthe t-distribution has 5 degrees of free-dom, the probability that the minimumdaily return observed over 100 years isless than 20.5% is about 1.52%—still arelatively unlikely event. For a t-distribu-tion with 4 degrees of freedom (notgraphed), the crash probability is 8.93%,still a low number. In contrast, when thet-distribution has 3 degrees of freedom,the same probability jumps to43.41%—nearly even odds of a crashover 100 years!

Our answer to the question “Was thecrash of ‘87 unusual?” is thus somewhattentative. When the crash is viewed notin isolation but as the worst outcome of anumber of draws from the samelognormal distribution, then its likelihoodincreases—but not to a level that makes itvery likely to happen. On the other hand,when we consider fat-tailed distributions(e.g., the log-t distribution), we see that amarket crash becomes more likely to oc-cur.

We have confined ourselves to astudy of the distribution of the minimumdaily return over various horizons, usinga variety of assumptions regarding thedistribution of daily stock returns. Inprinciple, this analysis can be extended toa study of the likelihood of the worst Kreturns (K=1,2, …) over the past 100years. For example, the second smallestdaily return on the S&P 500Index over the past 100 yearswas 12.3%, on October 28,1929. Using the distributionfunction of order statistics, wecan extend the above analysisto study the likelihood that thetwo smallest returns on theS&P 500 are 20.5% and

12.3%

Alternative Return Distributions ComparedGiven our results, a naturalquestion to ask is: What is thetrue unconditional distributionof stock returns? Table 2sheds some light on this ques-tion by tabulating selectedtheoretical and empiricallyobserved percentile points fordaily returns on the S&P 500Index. The theoretical distri-

butions have been calibrated to have the clues. Table 3 presents the skewness andsame mean and standard deviation as the excess kurtosis coefficients for the ob-sample mean (0.066%) and sample stan- served time series of returns and the val-dard deviation (0.96%). ues implied by the theoretical distributions

An inspection of Table 2 reveals that considered above.the empirically observed mid-range per- Table 3 shows the dramatic effect ofcentile points (e.g., the 25th and 75th the crash on the sample skewness andpercentiles) are closer to the theoretical excess kurtosis coefficients. When thevalues for the two t-distributions, while crash is included, it is clear that it is the extreme percentiles (e.g., the first and99th percentiles) are closer to those of the continued on page 7, column 1lognormal distribution. The values inTable 2 do not offer clear evidence on theappropriate distributional form for indexreturns. It would be useful to look athigher order moments to get some more

OCTOBER 1998 RISKS AND REWARDS PAGE 7

TABLE 5Daily GARCH-Forecast-Standardized Residuals

for the Days Surrounding the October 1987 Crash

Date

Return onS&P 500 Index

(%)

GARCH-PredictedStandard Deviation

(%)

GARCH-Forecast-Standardized

Residual

10/13/8710/14/8710/15/8710/16/8710/19/87

1.662.952.345.16

20.47

1.061.081.201.251.55

1.512.782.014.17

13.25

10/20/8710/21/8710/22/8710/23/8710/26/87

5.339.103.920.018.28

4.014.044.284.254.15

1.312.240.930.022.01

TABLE 6Monthly GARCH-Forecast-Standardized Residuals

for the Months Surrounding the Crash in October 1987

Month

Return onS&P 500 Index

(%)

GARCH-PredictedStandard Deviation

(%)

GARCH-Forecast-Standardized

Residual

September 1987October 1987November 1987December 1987

2.2021.528.167.35

4.364.347.416.93

0.755.201.250.91

October Market Demonscontinued from page 6

difficult to reconcile the sample higherorder moments with the theoretical mo-ments of any single distribution consid-ered above. On the other hand, when thecrash is excluded, the log-t distributionwith 5 degrees of freedom appears tohave predicted moments that match theempirically observed moments closely. However, since the crash did occur, it isdebatable whether it should be droppedfrom the analysis simply because it repre-sents an inconvenient data point!

We now turn to more formal tests ofthe distribution of daily stock re-turns—namely, the Kolmogorov- Smirnovtest and the Kuiper test. Table 4 presentsthe test statistics and the associated signif-icance levels.

The test statistics in Table 4 stronglyreject the null hypotheses that daily re-turns arise from a lognormal distributionor from a log-t distribution with 5 degreesof freedom. The null hypothesis of log-twith 3 degrees of freedom fails to be re-jected by both tests at the 1% level but isrejected by the Kuiper test at the 5%level. The results of the formal tests arethus consistent with our earlier findingsand strongly suggest that the uncondi-tional distribution of daily returns isfat-tailed with very large (possibly infi-nite) higher-order moments.

II. GARCH Forecasts AroundPeriods of Extreme MarketMovements

In Part I of this article we studied the un-conditional distribution of stock returnsover the last 100 years with special focuson the likelihood of a market crash. Ourconclusion was that a market crash hasnearly even odds of occurring over a pe-riod of 100 years if the unconditional dis-tribution of daily stock returns arisesfrom a fat-tailed distribution with verylarge (possibly infinite) higher-order mo-ments. It has been widely documentedthat such an unconditional distribution isconsistent with each period’s returns be-ing conditionally lognormally distributedwith time-varying conditional variances. In this section, we focus on a particularparameterization of the conditional vari-ance structure—namely, the GARCH(1,1) model—and study the behavior of

this model around periods of extreme had been about a week before themarket movements. crash.

GARCH Applied to October 1987To perform this study, we estimated sepa-rate GARCH(1,1) models using daily and ber 19, 1987, in contrast to themonthly returns on the S&P 500 Index. 20-sigma characterization of theThe daily model was estimated using re- crash using unconditional moments ofturns over the period March 1980 through the distribution of daily returns.September 1987 (1,906 days), and themonthly model used data from January1973 through September 1987 (177months). Table 5 presents theGARCH-forecast- standardized residuals and other numbersof interest for the days surrounding thecrash in October 1987. As the estimationperiod for the models excluded October1987, our reported results areout-of-sample.

Table 5 documents a number of in-teresting facts:

In response to sharp market moves inthe days immediately preceding thecrash, the GARCH forecast of thestandard deviation for October 19,1987, was about 50% higher than it

The crash return constitutes a13-sigma event relative to theGARCH forecast volatility for Octo-

After the crash, GARCH forecastvolatility rises to a level of over 4%per day, which causes many of thesharp post-crash market movementsto be classified as “normal” eventsthat are plausible even if daily returnsare conditionally lognormally distrib-uted.A look at the time series of GARCH

forecasts shows that the predicted volatil-ity continues to be very high for severalweeks after the crash. For example, thedaily GARCH forecast as of the end ofDecember 1987 (using data through De-cember 1987 to estimate

continued on page 8, column 1

Figure 6: S&P500 level and SPX-option-implied volatility over the last one year

13.0

14.0

15.0

16.0

17.0

18.0

19.0

20.0

21.0

22.0

7/1/96 8/1/96 9/1/96 10/1/96 11/1/96 12/1/96 1/1/97 2/1/97 3/1/97 4/1/97 5/1/97 6/1/97 7/1/97

Date

Imp

lied

vo

lati

lity

(SP

X o

pti

on

s)

600

650

700

750

800

850

900

S&

P50

0 le

vel

Implied volatility (SPX options)

S&P500 level

PAGE 8 RISKS AND REWARDS OCTOBER 1998

October Market Demonscontinued from page 7

the GARCH parameters) was 1.60%—anumber that is about 50% higher thanpre-crash forecasts. This is a manifesta-tion of the well-known high degree ofpersistence in daily GARCH forecasts. Table 6 shows GARCH-standardized re-siduals using the monthly GARCHmodel. The monthly GARCH forecastsalso rise sharply following the month ofthe crash and continue to remain high fora few months after the crash.

The fundamental intuition built intoGARCH models is the notion of volatilityclustering—i.e., periods of high volatilityare likely to be followed by more periodsof high volatility. If historical volatility islow, then GARCH models will continueto forecast low volatility. Although“outliers” are not ruled out even whenusing GARCH forecasts, the distinguish-ing feature of an accurate GARCH modelis that these outliers would be randomlydistributed in time, in contrast to the fore-casts of naïve models where outlierswould appear clustered together. Judgedby this metric, Tables 5 and 6 provideanecdotal evidence that, although thecrash itself appears as an outlier,GARCH models are at least partially suc-cessful in explaining the sharp movementsaround the period of the market crash.

Can We Predict an Abrupt Market Tran-sition?Since GARCH models use a weightedaverage of historical realized volatility topredict future volatility, in times of atransition from a low-volatility regime toa high-volatility regime the first few sharpmovements may appear as outliers thatare unanticipated by the GARCH model. An interesting question we might ask is:Are there other techniques that might beused to predict extreme market move-ments? This question is of clear interestin the current regime since popular debatein the weeks leading up to October 27,1997, centered on comparisons with Oc-tober 1987 and on the likelihood of an-other market crash.

One obvious answer is to look atS&P 500 Index option-implied volatilityforecasts. Figure 6 shows the time-seriesevolution of the S&P 500 Index level overthe past one year and the S&P 500 Index(SPX) option-implied volatility at the be-ginning of each month from July 1996through July 1997. The annualized aver-age implied volatility using near-term

(less than one month to maturity), In summary, our study of GARCH-near-the-money options has risen from standardized residuals around the periodapproximately 13.29% on July 1, 1996, of the crash of October 1987 shows that,to about 20.25% on July 1, 1997. Over while the crash itself was an outlier, mostthe same time period, the S&P 500 Index of the market volatility subsequent to thehas risen from 670 to 885. Somewhat crash can be fully accounted for usingsurprisingly, over a number of months GARCH forecasts. GARCH models use(e.g., May and June 1997) increases in the presence or absence of outliers to pre-the S&P 500 Index have been accompa- dict subsequent increases or decreases innied by increases in option-implied vola- volatility. Hence, while outliers may ex-tility, an observation which is at odds ist even when using GARCH forecasts,with the “leverage effect” (i.e., the usu- these outliers are likely to be randomlyally negative relationship between price dispersed through time. In the currentmovements and volatility). regime, we saw that option-implied vola-

One explanation for Figure 6 is that tility as of July 1, 1997, appeared to beoptions market participants expected the much higher than GARCH forecasts. S&P 500 Index to have higher short-term One explanation for this finding is thatvolatility in the coming weeks and options market participants expected tomonths. In contrast to the high implied see higher volatility in the comingvolatility forecasts, the conditional vari- weeks/months for the S&P 500 Index. ance prediction of GARCH models ranges Since the expected increase in volatilityfrom approximately 14.10% as of July 1, has been realized, we would expect that1996, to approximately 15.55% as of July GARCH forecasts will also respond.1, 1997. Since the sharp movements thatwere anticipated by options market partic-ipants were realized in October 1997, wewould expect that GARCH forecastswould have also risen subsequent to thefirst few sharp movements in the market.

Our study of option-implied volatilityover the past one year suggests that wecan incorporate “forward-looking” infor-mation in volatility forecasts by combin-ing option-implied volatility with GARCHforecasts. For example, we could esti-mate a GARCH model using op-tion-implied volatility as one of the vari-ables in the conditional variance equation. Studies by Day and Lewis [3] andLamoureux and Lastrapes [4] suggest thatthese two sources of information are com-plementary.

III. Impact of the Crash onBacktesting and PerformanceEvaluation

In the previous sections we have studiedissues relating to the likelihood of a crash(unconditional study) and the behavior ofGARCH forecasts of the S&P 500 Indexvolatility around the period of the crash(conditional study). In this section, weprovide some thoughts on

continued on page 9, column 1

Figure 7: Annualized Sharpe ratio for S&P500 index (over various horizons) including and excluding October 1987

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

01/1987-12/1987 01/1986-12/1990 01/1986-12/1995 01/1976-12/1995

Horizon

Annualized SR (including Oct 87)

Annualized SR (excluding Oct 87)

ˆ,B2,t

p,A,t

fB,t

2 BTˆ,B2,t

gB,t IC rB,t mB s 1 IC 2ut

OCTOBER 1998 RISKS AND REWARDS PAGE 9

October Market Demonscontinued from page 8

the influence of the crash on backtestinginvestment strategies and on performanceevaluation.

The Importance of Time Period ChoiceThe first point to note is that the time ho-rizon over which backtesting and/or per-formance evaluation are conducted willdetermine the extent to which excludingthe crash will affect the reported results. Figure 7 plots the ex-post Sharpe ratio onthe S&P 500 Index over horizons of 1, 5,10, and 20 years, including and excludingthe crash. As the horizon lengthens, wesee that the Sharpe ratio when the crash isincluded gradually approaches the Sharperatio excluding the crash. We shouldpoint out that because we need very largesample sizes to estimate mean returnsaccurately, the two sets of Sharpe ratiosare not statistically distinguishable fromone another (i.e., they are within twostandard errors of each other).

The second point is that excluding thecrash can have dramatic implications forthe profitability of certain types of strate-gies. For example, Sheikh [5] demon-strates that a strategy of buying the S&P500 Index plus writing out-of-the-moneyputs on the index was a profitable strategy(relative to buying the S&P 500 Index)over periods strictly before and strictlyafter the crash. The post-crash periodthat Sheikh studied was August 1988through February 1995. In contrast, asimilar strategy that was put in placestarting in September 1987 lagged thecumulative return on the S&P 500 Index,even after over seven years (as of Febru-ary 1995). In other words, the loss suf-fered in the month of the crash was morethan the gains made by the strategy overthe next seven years!

The third point is that it is a goodidea to run backtests over historical peri-ods that represent different regimes—e.g., bull and bear markets, periods oflow volatility and high volatility, etc. Figure 8 shows the cumulative return onthe S&P 500 Index over the 10-year pe-riod January 1987 through December1996. It is evident from the figure thatthere have not been too many badmonths, especially over the past fiveyears. The crash represents a useful ob-servation precisely because it was a par-ticularly bad month. Including this obser-vation in backtests serves as a check onthe robustness of proposed investment

strategies.

Should the Crash Be Included in Performance Studies?Finally, we consider performance evalua-tion in the presence of the crash. As theabove analysis of the Sharpe ratio sug-gests, the total risk/return picture, espe-cially over smaller horizons, differs sig-nificantly depending on whether or not thecrash is included in the sample. For anactive manager who is usually fully in-vested in equities, including the crashdoes not bias performance results sincethe active manager is evaluated based onhis or her active risk/return profile (i.e.,risk and return net of the market).

Let us consider the more difficultquestion of an active manager who aimsto achieve superior returns by forecastingthe returns on the S&P 500 Index (that is,by timing the market). Let r be theB,texcess return on the S&P 500 Index inperiod t and let denote the per-periodlong-run expected excess return on theindex. Each period, the market timer hasa forecast of the excess return on the in-dex over its long-run average. In sym-bols, for each period the market timer hasa forecast f of the value of r . LetB B,t B

denote the risk aversion coefficient ofBTthe investor for benchmark timing and let be the investor’s forecast of thevariance on the index over period t. Then, the optimal active beta position forthe investor is given by:

Grinold and Kahn [6] discuss the appro-priate objective function for an activemanager and derive the optimal activebeta policy stated above. We conducted asimulation study using the actual historyof realized market returns over the periodJanuary 1987 through December 1996. The market timer is assumed to makemonthly forecasts of the index return. Each month, the market timer receives asignal g as follows:B,t

IC = the information coefficient of themanager

m = the average excess return on theBindex over the 10-year sampleperiod

s = the sample standard deviation ofthe excess return on the index,and

u = a random number drawn from atdistribution with zero mean andunit standard deviation.

continued on page 10, column 1

Figure 8: Cumulative return on the S&P500 index since January 1st, 1987

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Jan-87

Jul-87

Jan-88

Jul-88

Jan-89

Jul-89

Jan-90

Jul-90

Jan-91

Jul-91

Jan-92

Jul-92

Jan-93

Jul-93

Jan-94

Jul-94

Jan-95

Jul-95

Jan-96

Jul-96

Cumulative return on S&P500 index

ˆ,B2,t

fB,t E rB,t B gB,t (IC)gB,t

PAGE 10 RISKS AND REWARDS OCTOBER 1998

TABLE 7Ex-post Information Ratios (IR) for Market Timing

Over the Period January 1987 through December 1996(Average over 100 Simulations)

InformationCoefficient

Average Ex-post IR(including October 1987)

Average Ex-post IR(excluding October 1987)

0.050.100.15

0.1910.3960.467

0.1950.3770.448

October Market Demonscontinued from page 9

r = is set equal to the observed ex-B,tcess return on the S&P 500 In-dex in month t.

Given this signal, the manager con-structs an optimal forecast of the excessreturn on the index as follows:

For simplicity, we assume that theinvestor’s forecast of the variance of the

index return in month t, is equal tos for all months. For a given sequence2

of signal realizations, we can derive thecorresponding time series of active betapositions. Using the actual history ofmarket returns, we can then compute theex-post information ratio for the investor. We considered three different IC levels;0.05, 0.10, and 0.15. For each IC, weran 100 simulations of the entire 10-yearhistory from January 1987 through De-cember 1996. Table 7 reports the aver-age ex-post information ratios acrossthese simulations.

Table 7 shows that there are no sig-nificant differences between the two col-umns of information ratios. In otherwords, including the crash does not ap-pear to make a difference for the perfor-mance evaluation of a market timer.

SummaryIn this article, we have presented someperspectives on the crash of October1987. We found that the likelihood of amarket crash increases dramatically if theunconditional distribution of stock returnsis fat-tailed with very large (possibly infi-nite) higher-order moments. Our studyof GARCH forecasts showed that, withthe exception of the crash itself, theseforecasts were at least partially successfulin capturing sharp movements around theperiod of the crash. We found that op-

tion-implied volatility has increased dra- Index Options,” Journal of Econo-matically over the past one year, suggest- metrics, v.52, 1992, pp.267–287.ing that the market expects higher volatil-ity in the weeks/months ahead. Finally,we offered some thoughts on the impactof the crash on backtesting and perfor-mance evaluation. We showed via a sim-ulation study that including the month ofthe crash does not have a significant ef-fect on the ex-post information ratios of amarket timer.

End Notes1. Throughout this section, we assume

that the time series of daily returnsiid (independent and identically dis-tributed) draws from the specifiedunconditional distribution. In Part IIof this article we will explore thebehavior of conditional variancesaround the period of the crash.

2. Fama, Eugene F., “The Behavior ofStock Market Prices,” Journal ofBusiness, no. 38, 1995, pp.34–105.

3. Day, Theodore E. and Craig M.Lewis, “;Stock Market Volatility andthe Information Content of Stock

4. Lamoureux, Christopher and WilliamLastrapes, “Forecasting Stock ReturnVariance: Towards an Understandingof Stochastic Implied Volatility,” TheReview of Financial Studies, no. 6,1993, pp.293–326.

5. Sheikh, Aamir, “Portfolio Construc-tion with Derivatives,” BARRA’s19th Annual Equity Research Semi-nar, Pebble Beach, CA, June 11–14,1995.

6. Grinold, Richard C. and Ronald N.Kahn, Active Portfolio Management,Probus Publishing, Chicago, IL,1995.

Vinod Chandrashekaran is a Senior Con-sultant in the Research Group at BARRAInc. in Berkeley, California.

OCTOBER 1998 RISKS AND REWARDS PAGE 11

“The downfall of the Soviet Union in 1989 leadingto only one superpower, peace in the Middle East,positive demographics, and global capitalism mayhave lulled Joe and Lucy Public into believing thatnothing can go wrong.”

Taking Stock: No Pain No Gain, or What They Did Not Tell You about Goldilocks by Nino Boezio

f you haven’t heard it already, it’s When Goldilocks later awoke and saw the own destiny. For the latter, wealth gen-Itime that someone finally told you the first bear, she did not pay any attention to eration became the equivalent to investingcomplete story about Goldilocks and it. She was still hungry and thus went as much as one could in the stock market.the Three Bear Markets. back to eating soup, for now some of the The stock market, as it became in theGoldilocks is a soup connoisseur and hot ones cooled off (a buying opportu- 1920s (Japan in the 1980s), was increas-

loves to try various soups. The amount nity), not realizing that the circumstances ingly seen as the “no pain always gain”and variety of soups (equities) Goldilocks had now changed (Phase I of a bear mar- approach to increase one’s financial(today’s equity investors) eats depends on ket—denial). When the second bear ap- health. It would grant a person ultimatehow the temperature (the economy) of the pears (Phase II of a bear mar- financial independence (“deliverancesoup is—too hot, too cold, or just right. ket—realization), she may realize that from serfdom”) and allow one to retireThe soups overall were not much to her eating more soup in the presence of the early to a life of luxury. The downfall ofliking in the early 1990s because the tem- bears will put her in danger and her trepi- the Soviet Union in 1989 leading to onlyperature was “too cold” (recession), “too dation may result in her hunger being re- one superpower, peace in the Middlehot” in 1994 (economic overheating), but placed by hesitation and concern. She East, positive demographics, and global“just right“ in the last few years (hence will stop eating and the hot soups (equi- capitalism may have lulled Joe and Lucythe name Goldilocks economy). ties) will get even cooler (cheaper). Public into believing that nothing can go

While is search for soups, Goldilocks When the third bear appears (Phase III of wrong. Initially it was a good bet, untilhappened to enter into the lair of the bears a bear market— capitulation), she may too many began to believe it and drove

(overvaluation) but was not too concerned have not already done her harm, then they economy which potentially can suck upabout where she arrived. She had never probably will not do so and she should the excess supply of goods, the actions ofseen bears before and only heard rumors probably heat up the soups and start eat- this or that politician or leader, emergingof past rampages in foregone times. She ing once again. However, by then she Western Europe, or sometimes just sim-was told that bears these days are kept probably has run out and missed out on ply the use of money from one group toaway in zoos (the new era), and if one the soupfest (Phase I of a bull market) pay for the misgivings or “irrational exu-ever were to escape, the zookeepers that could ultimately ensue if she had only berance” of another group. As was(Alan Greenspan, the Fed, the stuck around longer. Or perhaps the pointed out in my article “It’s DifferentBundesbank, the International Monetary bears’ stove is broken (a depression) and This Time” in the March 1998 issue ofFund etc.) would quickly go after the bear she will not get a chance to eat more soup Risks and Rewards, traditional solutionsand put it back into captivity. Hence for a very long time. may not work this time, and the problemsthere was nothing to fear. She did not are substantially different than they ini-know that there were still bears running tially appear on the surface. It is nowfree. said that about 50% of the global econ-

The bears were not at home (lost all omy is in or on the verge of entering acredibility) when Goldilocks finally recession because of falling world de-showed up. Goldilocks, having tried the mand from the international financial cri-various soups, liked the ones that in her sis.opinion were not too hot or too cold, and It is sad to see a person’s hopesgorged herself. Needless to say, all that dashed or rattled as a result of any eating made her sleepy and she did nothear the rumblings outside (Asia, Russia, continued on page 28, column 1South America), sounds made by the re-turning bears. She went to sleep.

Since Goldilocks had never seen livebears, she did not know what to fear.

finally acknowledge valuations skyward all over the world.her plight and run for No one in the world communitycover (and will even wants to suffer pain, even though theirstart vomiting what behavior may at times create pain for oth-she has already ers and ultimately themselves. When theeaten), and all the pain comes, there is often a mad scramblesoups will become to find a “cure” rather than to accept thefreezingly cold. In hurt, learn from it, take the lumps, andthis latter phase, she move on. The cure in the economicshould probably real- world has become known as the Interna-ize that if the bears tional Monetary Fund, a strong U.S.

No Pain, No Gain: Understanding GoldilocksHumanity has been searching for the HolyGrail for thousands of years—in modern-day terminology this is called the “freelunch” (or should we call it the “freesoup”).

There has always been a quest by theaverage person to find the ultimate happi-ness in personal life, the perfect balancebetween recreation and work (for somethat would mean no work), and for suffi-cient wealth so that one may guide his

PAGE 12 RISKS AND REWARDS OCTOBER 1998

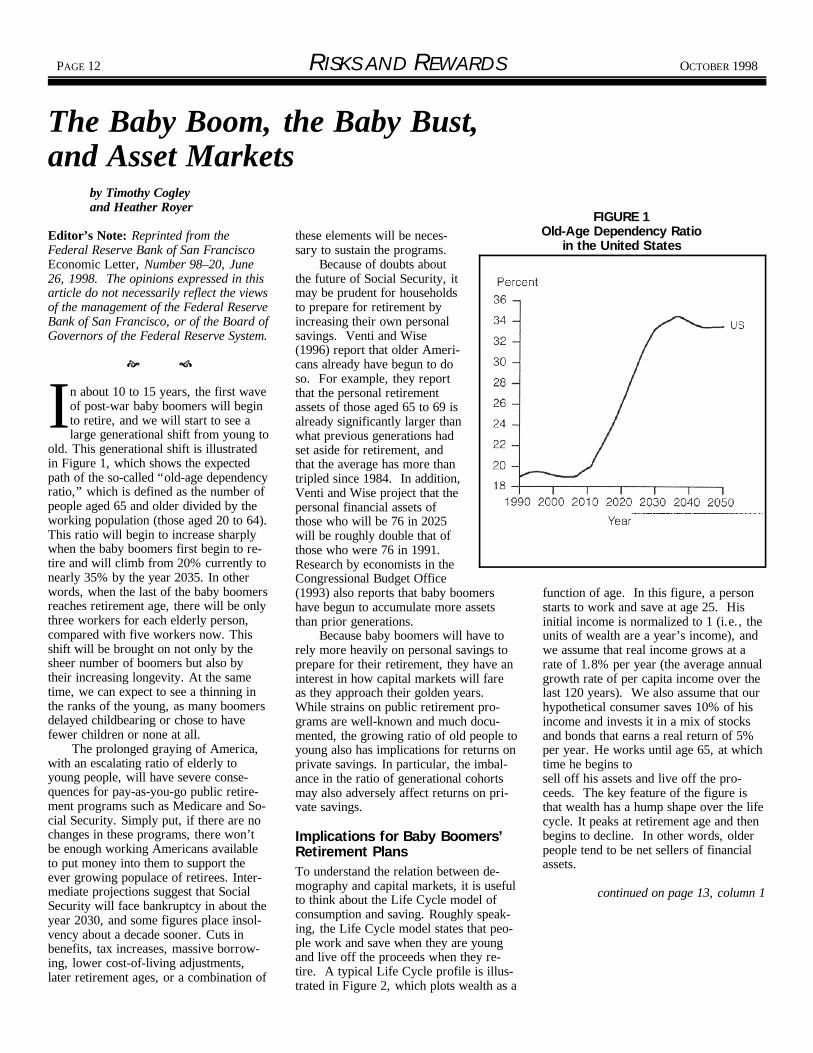

FIGURE 1Old-Age Dependency Ratio

in the United States

The Baby Boom, the Baby Bust, and Asset Markets by Timothy Cogley and Heather Royer

Editor’s Note: Reprinted from the these elements will be neces-Federal Reserve Bank of San Francisco sary to sustain the programs. Economic Letter, Number 98–20, June Because of doubts about26, 1998. The opinions expressed in this the future of Social Security, itarticle do not necessarily reflect the views may be prudent for householdsof the management of the Federal Reserve to prepare for retirement byBank of San Francisco, or of the Board of increasing their own personalGovernors of the Federal Reserve System. savings. Venti and Wise

n about 10 to 15 years, the first waveIof post-war baby boomers will beginto retire, and we will start to see alarge generational shift from young to

old. This generational shift is illustratedin Figure 1, which shows the expectedpath of the so-called “old-age dependencyratio,” which is defined as the number ofpeople aged 65 and older divided by theworking population (those aged 20 to 64). This ratio will begin to increase sharplywhen the baby boomers first begin to re-tire and will climb from 20% currently tonearly 35% by the year 2035. In otherwords, when the last of the baby boomersreaches retirement age, there will be onlythree workers for each elderly person,compared with five workers now. Thisshift will be brought on not only by thesheer number of boomers but also bytheir increasing longevity. At the sametime, we can expect to see a thinning inthe ranks of the young, as many boomersdelayed childbearing or chose to havefewer children or none at all.

The prolonged graying of America,with an escalating ratio of elderly toyoung people, will have severe conse-quences for pay-as-you-go public retire-ment programs such as Medicare and So-cial Security. Simply put, if there are nochanges in these programs, there won’tbe enough working Americans availableto put money into them to support theever growing populace of retirees. Inter-mediate projections suggest that SocialSecurity will face bankruptcy in about theyear 2030, and some figures place insol-vency about a decade sooner. Cuts inbenefits, tax increases, massive borrow-ing, lower cost-of-living adjustments,later retirement ages, or a combination of

(1996) report that older Ameri-cans already have begun to doso. For example, they reportthat the personal retirementassets of those aged 65 to 69 isalready significantly larger thanwhat previous generations hadset aside for retirement, andthat the average has more thantripled since 1984. In addition,Venti and Wise project that thepersonal financial assets ofthose who will be 76 in 2025will be roughly double that ofthose who were 76 in 1991. Research by economists in theCongressional Budget Office(1993) also reports that baby boomers function of age. In this figure, a personhave begun to accumulate more assets starts to work and save at age 25. Histhan prior generations. initial income is normalized to 1 (i.e., the

Because baby boomers will have to units of wealth are a year’s income), andrely more heavily on personal savings to we assume that real income grows at aprepare for their retirement, they have an rate of 1.8% per year (the average annualinterest in how capital markets will fare growth rate of per capita income over theas they approach their golden years. last 120 years). We also assume that ourWhile strains on public retirement pro- hypothetical consumer saves 10% of hisgrams are well-known and much docu- income and invests it in a mix of stocksmented, the growing ratio of old people to and bonds that earns a real return of 5%young also has implications for returns on per year. He works until age 65, at whichprivate savings. In particular, the imbal- time he begins toance in the ratio of generational cohorts sell off his assets and live off the pro-may also adversely affect returns on pri- ceeds. The key feature of the figure isvate savings. that wealth has a hump shape over the life

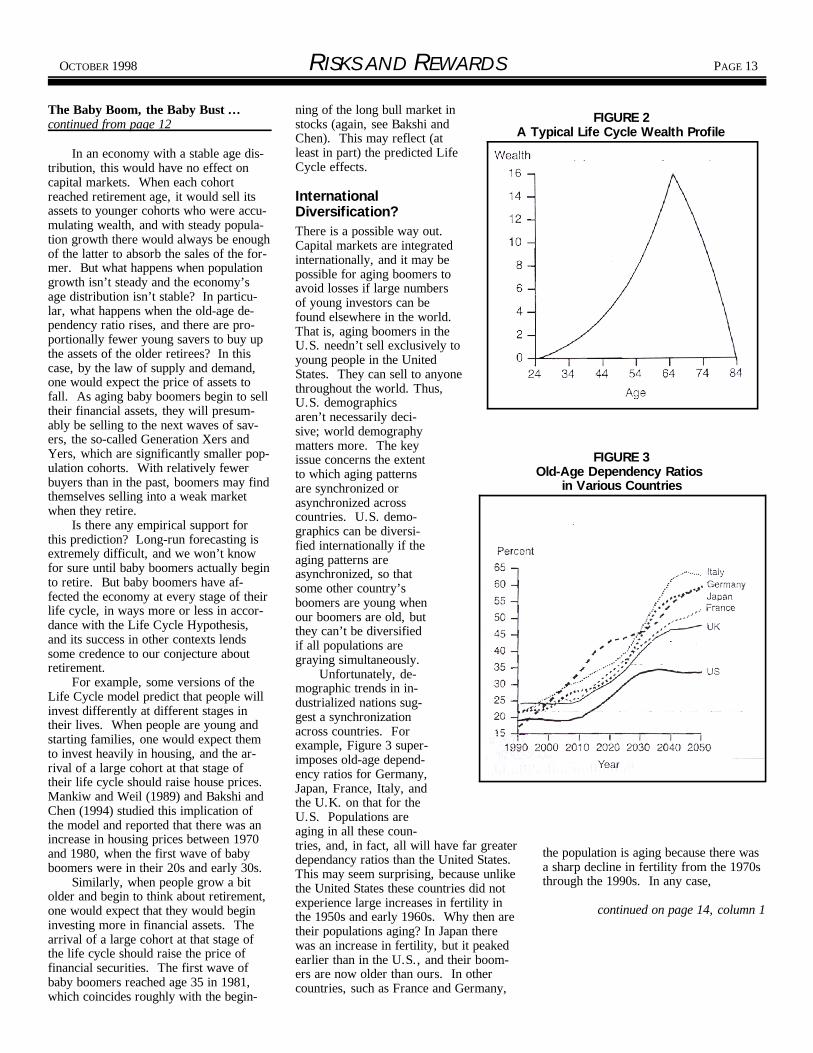

Implications for Baby Boomers’Retirement PlansTo understand the relation between de-mography and capital markets, it is usefulto think about the Life Cycle model ofconsumption and saving. Roughly speak-ing, the Life Cycle model states that peo-ple work and save when they are youngand live off the proceeds when they re-tire. A typical Life Cycle profile is illus-trated in Figure 2, which plots wealth as a

cycle. It peaks at retirement age and thenbegins to decline. In other words, olderpeople tend to be net sellers of financialassets.

continued on page 13, column 1

OCTOBER 1998 RISKS AND REWARDS PAGE 13

FIGURE 2A Typical Life Cycle Wealth Profile

FIGURE 3Old-Age Dependency Ratios

in Various Countries

The Baby Boom, the Baby Bust ... ning of the long bull market incontinued from page 12 stocks (again, see Bakshi and

In an economy with a stable age dis-tribution, this would have no effect oncapital markets. When each cohortreached retirement age, it would sell itsassets to younger cohorts who were accu-mulating wealth, and with steady popula-tion growth there would always be enoughof the latter to absorb the sales of the for-mer. But what happens when populationgrowth isn’t steady and the economy’sage distribution isn’t stable? In particu-lar, what happens when the old-age de-pendency ratio rises, and there are pro-portionally fewer young savers to buy upthe assets of the older retirees? In thiscase, by the law of supply and demand,one would expect the price of assets tofall. As aging baby boomers begin to selltheir financial assets, they will presum-ably be selling to the next waves of sav-ers, the so-called Generation Xers andYers, which are significantly smaller pop-ulation cohorts. With relatively fewerbuyers than in the past, boomers may findthemselves selling into a weak marketwhen they retire.

Is there any empirical support forthis prediction? Long-run forecasting isextremely difficult, and we won’t knowfor sure until baby boomers actually beginto retire. But baby boomers have af-fected the economy at every stage of theirlife cycle, in ways more or less in accor-dance with the Life Cycle Hypothesis,and its success in other contexts lendssome credence to our conjecture aboutretirement.

For example, some versions of theLife Cycle model predict that people willinvest differently at different stages intheir lives. When people are young andstarting families, one would expect themto invest heavily in housing, and the ar-rival of a large cohort at that stage oftheir life cycle should raise house prices.Mankiw and Weil (1989) and Bakshi andChen (1994) studied this implication ofthe model and reported that there was anincrease in housing prices between 1970and 1980, when the first wave of babyboomers were in their 20s and early 30s.

Similarly, when people grow a bitolder and begin to think about retirement,one would expect that they would begininvesting more in financial assets. Thearrival of a large cohort at that stage ofthe life cycle should raise the price offinancial securities. The first wave ofbaby boomers reached age 35 in 1981,which coincides roughly with the begin-

Chen). This may reflect (atleast in part) the predicted LifeCycle effects.

International Diversification?There is a possible way out.Capital markets are integratedinternationally, and it may bepossible for aging boomers toavoid losses if large numbersof young investors can befound elsewhere in the world. That is, aging boomers in theU.S. needn’t sell exclusively toyoung people in the UnitedStates. They can sell to anyonethroughout the world. Thus,U.S. demographicsaren’t necessarily deci-sive; world demographymatters more. The keyissue concerns the extentto which aging patternsare synchronized orasynchronized acrosscountries. U.S. demo-graphics can be diversi-fied internationally if theaging patterns areasynchronized, so thatsome other country’sboomers are young whenour boomers are old, butthey can’t be diversifiedif all populations aregraying simultaneously.

Unfortunately, de-mographic trends in in-dustrialized nations sug-gest a synchronizationacross countries. Forexample, Figure 3 super-imposes old-age depend-ency ratios for Germany,Japan, France, Italy, andthe U.K. on that for theU.S. Populations areaging in all these coun-tries, and, in fact, all will have far greaterdependancy ratios than the United States. This may seem surprising, because unlikethe United States these countries did notexperience large increases in fertility inthe 1950s and early 1960s. Why then aretheir populations aging? In Japan therewas an increase in fertility, but it peakedearlier than in the U.S., and their boom-ers are now older than ours. In othercountries, such as France and Germany,

the population is aging because there wasa sharp decline in fertility from the 1970sthrough the 1990s. In any case,

continued on page 14, column 1

PAGE 14 RISKS AND REWARDS OCTOBER 1998

The Baby Boom, the Baby Bust ...continued from page 13

because the demographic profiles are syn- well, in ways we are just beginning tochronized, it seems unlikely that investors explore.in these countries will be net buyers ofcapital when aging Americans begin to Timothy Cogley, Senior Economistsell. If anything, this figure suggests that Heather Royer, Research Associateinternational linkages among developedcountries are likely to amplify life cycleeffects in the United States.

What about developing countries? Demographers project that their old-agedependency ratios will also rise, but ex-pect the increase to occur roughly 50years later than in the industrializedworld. Since their demographic profilesdiffer from the developed world’s, per-haps aging boomers in the latter can sellto younger boomers in the former. Butwill they have the means to buy? Capitaltends to be scarce in developing coun-tries, and unless they can grow rich in thenext 25 years, it seems unlikely that theywill be in a position to become net lendersto the developed world.

Other ConsiderationsThe looming crunch might be slightlyeased under several scenarios. For exam-ple, educated baby boomers may chooseto stay in their careers longer, workingpast the traditional age of retirement; theyneed not sell their assets if they earn steady paychecks. In addition, the periodover which the Baby Boom generation is 1994. “Baby Boom, Population Ag-expected to retire spans about 30 years. ing, and Capital Markets.” JournalCapital markets might have time to adjust of Business 67, pp. 165–202.to the gradual decline in supply of fundsfor capital investment. For example, ifGen-Xers, Yers, and Zers were to antici-pate further cuts in Social Security bene-fits, they might save a higher fraction oftheir incomes, and this would compensatefor the fact that there are relatively few ofthem. Despite such possibilities, thesurging old-age dependency ratio remainsa significant generational challenge, notjust for Social Security, but perhaps forprivate retirement plans as

REFERENCES

Bakshi, Gurdip S., and Zhiwu Chen.

Congressional Budget Office. 1993.“Baby Boomers in Retirement: AnEarly Perspective.”

Mankiw, N. Gregory, and David Weil.1989. “The Baby Boom, the BabyBust, and the Housing Market.” Re-gional Science and Urban Economics19, pp. 235–258.

Venti, Steven F., and David A. Wise.1996. “The Wealth of Cohorts: Re-tirement Saving and the ChangingAssets of Older Americans.” NBERWorking Paper No. 5609.

Subjective Value at Risk by Glyn Holton

Editor’s Note: The following article orig- If the VaR revolution is to succeed, it hind the screen, the man sees the result ofinally appeared in the August 1997 issue must be tempered by such concerns. Af- the die toss, but you have not yet seen it. of Financial Engineering News and is ter all, VaR is only a tool. All tools have In this example, the outcome is certain. reprinted with permission. limitations. For example, a hammer can It has already been determined. Uncer-

alue-at-Risk (VaR) is becomingVsomewhat of a revolution. Around the globe, organizationsare racing to implement the new

technology. Pundits propose extendingVaR to other risks, including credit riskand operational risk [1]. Some even sup-pose that all the risks of an organizationshould be summarized with a single riskmeasure [2].

It is the nature of revolutions thatthere be a backlash. One has begun. Critics suggest that VaR may be ineffec-tive for assessing risks other than marketrisks [3]—or that it fails even with marketrisk [4]. Others have noted disturbinginconsistencies between risk estimatesproduced by different implementations ofVaR [5].

drive nails, but it cannot drive screws. tainty exists only in your head—but theSaying that the hammer is limited is dif- risk is real until you see the die.ferent from saying it is flawed. Let’s try to quantify your risk in this

To understand the limits of VaR, we example. To characterize the risk, weneed to explore what it means to “quan- need to describe the uncertainty as well astify” risk. Let’s start by defining risk. your exposure to that uncertainty. Obvi-Risk is exposure to uncertainty. Accord- ously, your exposure is $100. That is theingly, risk has two components: (1) un- amount you stand to lose. But what iscertainty; and (2) exposure to that uncer- your uncertainty— what is the probabilitytainty. that you will lose $100?

A synonym for uncertainty is igno- If you say it is one chance in six, Irance. We face risk because we are igno- am sorry. You are wrong. I forgot torant about the future—after all, if we mention that the die is 10-sided. Thiswere omniscient, there would be no risk. illustrates an important point. WheneverBecause ignorance is a personal experi- we try to quantify risk, we are describingence, risk is necessarily subjective. our own understanding of a situation. When we put a number on risk, that num- Often, there will be aspects ber says as much about us—how little weknow—as it says about the world around continued on page 15, column 1us.

Suppose you are in a casino. A manrolls a die behind a screen. If the resultis a 6, you are going to lose $100. Be-

OCTOBER 1998 RISKS AND REWARDS PAGE 15

Subjective Value at Riskcontinued from page 14

of a situation that we are simply unaware her risk limit. She knows the markets would reduce the risk manager to being,of. It is one thing to not know the answer and is aware of a combination of market in effect, just another trader.to a question. It is another matter to not factors—perhaps central banks are inter- Instead, we implement an objectiveeven know the question exists. vening in the markets—that are going to benchmark for risk in the form of a VaR

Returning to our casino example, we drive the yen up in the short-term. She model. It may assume that market vari-still don’t know your probability of losing considers the position appropriate. ables are normally distributed despite$100. It is not one in ten. After all, the Her risk manager disagrees. He some observers preferring the lognormalman throwing the die may be cheating. doesn’t know about central bank inter- assumption. It may not capture marketWe are aware of the possibility, but it is vention—and he doesn’t care. All he leptokurtosis. It probably won’t under-difficult to place a number on that risk. knows is that the trader has exceeded her stand “sticky” volatilities. This is not

Would it help if I told you the man is limit, and he calls her on it. important.unshaven and smells of whiskey? Maybe Reviewing the VaR number that indi- If we have a perfect model, it wouldyour opinion would change if I told you cates her limit violation, the trader re- know everything there was to know aboutinstead that he is a kindly grandfather torts: “The model is wrong. I know the the markets. It would eliminate the needwearing a boy scout cap. Changing the markets. I know what the central banks for traders. We could trade the portfoliodescription may sway some peoples’ are doing. I’m on the phone with FX based upon the model—and we would beopinions. It may not sway others’. Risk professionals all day long. This VaR foolish not to.is subjective. model is just a bunch of formulas. It A VaR model, however, is limited

So what does this mean if we want to doesn’t know the yen is going up, but I because it is objective whereas risk takingmeasure the financial risks of an organi- do. There is zero risk in my long posi- is subjective. If we deny that subjectiv-zation? To find out, let’s look at how tion because any other market position, ity, we deny a role for human judgment. risks are quantified. It is a four-step pro- under these circumstances, would be ri- Rather than trade portfolios based upon acess: diculous.” model, we rely upon traders because we

Who is right, and who is wrong? believe they understand things the modelDefine the risk to be measuredAgree on a model for that riskSpecify a risk measure that is com-patible with that modelEstimate the value of that measureimplied by the model.For example, the process might be as

follows:Risk: market risk of a specified port-folioRisk model: market variables areassumed to be jointly normally dis-tributed with specified volatilities andcorrelationsRisk measure: one-day 90% VaRRisk estimate: achieved with MonteCarol simulation using 5,000 quasi-randomly generated scenarios.It is the second step of the process

that is pivotal. It is at this point that wetake the subjective notion risk and de-scribe it in an objective manner. How-ever, a group of individuals may agree ona model, but retain their own subjectiveopinions about the risk. In this sense, themodel does not make risk an objectivenotion, it merely makes the measure ofrisk an objective notion.

Let’s continue with the example ofmarket risk. Suppose a trading operationhas implemented the above VaR system. One day a trader takes on a sizable longposition in the Japanese yen, exceeding

The trader knows the markets. It’s her cannot.job. By the same token, what is the point This leaves us with two—potentiallyin having a risk manager who is going to inconsistent—market views: that of thebe overruled by every trader with a mar- model; and that of the traders.ket view? The question is: How can we use the

Some might perceive that the answer objective VaR model to manage the risk-is to build a better VaR model— one that taking process, but not place arbitrary—orsomehow captures the trader’s intuitive even dangerous—restrictions upon theunderstanding of central bank interven- activities of traders?tion. Others may cling to the existing The answer is risk limits. TheseVaR model, claiming that efficient mar- represent explicit authority for traders tokets and no-arbitrage conditions ensure its take positions that differ from the model’sultimate validity. perception of the markets. Risk limits

In fact, neither approach can possibly enable an organization to manage risk bywork. They both make a supposition that limiting traders to taking positions withinthere is a “right” model—if only we can a specified range. The role of the VaRidentify it. Markets, however, are too model is to objectively define what thatcomplex and ever-changing for any model range is. The trader’s role is to select theto fully describe. Selecting a model is a optimal position within the range.subjective process. In this context, VaR is just a tool for

Our FX trader and risk manager have delimiting a set of acceptable portfolios. a legitimate difference of opinion. To We can call it a “risk measure” if weresolve such a situation, we have to get like, but we don’t have to.beyond the simplistic notion that one is Like any tool, VaR has limitations. right and the other is wrong. I so doing, It will be useful for performing somewe must challenge the idea that every risk tasks, but not others. For example, otherhas a number—that there is a “right” possible applications of VaR model that will find that number, andother models are “wrong.” We must continued on page 16, column 1embrace the notion that risk is subjective.

We cannot manage market risk byhaving a risk manager forming—and thenenforcing—his own subjective opinionsabout the riskiness of a trader’s position. This would be unfair to the trader, and it

PAGE 16 RISKS AND REWARDS OCTOBER 1998

Applying Insurance CompanyQuantitative Techniques for Improved Capital Budgeting

Subjective Value at Riskcontinued from page 15

include determining capital requirements,capital allocation, or performance-basedcompensation.

Each process entails risk assessment. Accordingly, each is subjective. If wewish to apply the objective tool VaR toany of these, we must first ask what roleVaR is to play. In each case, somemechanism must be found that will enableVaR to support subjective human judg-ment—without replacing it. For marketrisk management, the answer was risklimits. For other possible applications,the question remains open.

Glyn Holton is an independent consultantbased in Boston and a frequent speaker atSOA meetings. He maintains an extensiveweb site at:http://www.contingencyanalysis.com

END NOTES

1. See the J.P. Morgan CreditMetricsTechnical Document and “VaR inOperation” by Duncan Wilson, Risk,December 1995.

2. See “CIBC Gets Commercial,” Risk,August 1996.

3. See “Modeling of Operations Risk,”by M. Yone, et al., in the FinancialRisk Management Discussion Group(March 1997).

4. See “The World According toNassim Taleb,” Derivatives Strategy,December/January 1997.

5. See “Value at Risk: Implementing aRisk Management Standard,” byChris Marshall and Michael Siegel,Journal of Derivatives, Spring 1997.

Financial Engineering News is a bi-monthly trade newspaper covering thediscipline of financial engineeringgenerally. Complimentary subscriptionsare available to qualified persons and maybe obtained from the publisher at 7843289th Place SE., Issaquah, WA 98027,USA or on-line athttp:\\www.fenews.com/subscriptions.

by Tony Dardisand Andrew Berry

he insurance industry has always • Starting a new business producingTused sophisticated quantitative goods or services, or a new producttechniques for appraising capital line in an existing businessinvestment. The same, however,

cannot always be said of other industries. In a 1994 study, the Confederation ofBritish Industry found that only about onequarter of manufacturing companies usequantitative methods to assess projectrisk, with the majority relying on subjec-tive judgment. It is generally thought thatmanufacturers in the United States havesimilarly been slow to adopt quantitativetechniques in appraising projects. So,could some of these insurance industrytechniques be applied to help organiza-tions in other fields? In particular, shouldconsideration be given to the use of thesetechniques for appraisals of capital pro-jects?

This article recognizes and acknowl-edges the work of both the U.K. Instituteof Actuaries and the Society of Actuariesin this area, in particular the importantpaper authored by a working party set upby the U.K. Institute entitled “CapitalProjects,” published in the British Actuar-ial Journal (Volume 1, Part II, 1995,pages 155–300). Many of the definitionsused in the introductory sections of whatfollows are taken directly from the Insti-tute paper. We take the discussion some-what further, however, in looking at someof the more state-of-the-art techniquescurrently in use today within the insur-ance industry. A similar SOA workingparty is in its formative stages in theUnited States.

We have defined a capital project inthe same fashion as the Institute workingparty, that is, “any project where the in-vestment has significant physical, social,or organizational consequences and is notmerely to secure a transfer of ownershipof an existing asset [such as portfolioinvestment].” This definition thereforeincludes such schemes as:• Physical construction, such as build-

ing a factory, bridge, or road

• Taking over and modernizing an ex-isting business or physical asset

• Developing a new asset for an exist-ing business

• Repairing or renewing an existingasset.

Current Capital Budgeting TechniquesCapital projects are most commonly eval-uated using pay-back period, net presentvalue, or internal rate of return. Again,using the Institute paper definitions:• Pay-back Period Technique: A pro-

ject is accepted if the number ofyears of projected cash flow requiredto return the initial investment is lessthan a pre-set maximum cut-off pe-riod (no account taken of the timevalue of money).

• Internal Rate of Return: Find theinterest rate (IRR) that equates thepresent value of expected future cashflows with initial costs and accept theproject if the IRR exceeds the oppor-tunity cost of capital.

• Net Present Value: Find the presentvalue (NPV) of the expected futurecash flows of a project discounted atthe opportunity cost of capital andaccept the project if the NPV isgreater than zero.IRR and NPV incorporate the time

value of money through discounting topresent values and try to incorporate thenotion of risk through the use of the rele-vant discount rate. Risk in this contextmeans that actual returns from the project(revenues less costs) may be

continued on page 17, column 1

OCTOBER 1998 RISKS AND REWARDS PAGE 17

“Where DFA is especially useful is in allowing theuser to build a sophisticated model thatincorporates the interrelationship betweenvariables.”

Quantitative Techniquescontinued from page 16

different than expected. This volatility of a risk profile similar to the industry competitor beats it to market. Similarly,returns will be different between different as a whole? an economic downturn could increaseprojects. financing costs in construction of a new

The relative riskiness of the project is sports stadium and reduce demand forincorporated into the discount rate by add- tickets. Other variables may be independ-ing a risk premium to the “risk-free” in- ent or act as natural hedges.terest rate as reflected by a Treasury bill. With faster computer run times, sim-This risk premium is necessary to com- ulation of potential net returns should bepensate investors for the risk they are easier. These techniques are being usedtaking by providing higher returns. The in insurance settings by actuaries andkey questions are how large should the could be adapted to capital budgeting. risk premium be and how do we calculate These simulation techniques makeit? The answer to these questions re- bottom-up risk profiling possible and rec-quires an assessment of the risks in the ognize the volatility of individual risk fac-project. In most cases this assessment is tors, their impact on returns, and the de-arbitrary. gree to which they are interrelated.

Rather than try to estimate the risk Covariance is not the only consider-costs inherent in a capital project, organi- ation in developing a project risk profile:zations will use their cost of capital (that investment decisions are not static. Inis, the rate at which they can raise capital) many cases, management has some op-as the discount rate. The reason for this tions over the future direction of the in-is that this is the rate of return that the vestment. It can abandon the project,financial markets require to compensate increase its investment, or have an optionthem for taking the risk of investing in the to revise the project at a later date. This