raleigh finlayson : managing director€¦ · raleigh finlayson : managing director asx gold...

TRANSCRIPT

RALEIGH FINLAYSON : MANAGING DIRECTOR ASX GOLD PRODUCER Euroz Rottnest Conference March 2015

Qualification

2

This presentation has been prepared by Saracen Mineral Holdings Limited (Saracen or the Company) based on information from its own and third party sources and is not a disclosure document. No party other than the Company has authorised or caused the issue, lodgement, submission, despatch or provision of this presentation, or takes any responsibility for, or makes or purports to make any statements, representations or undertakings in this presentation. You should be aware that as an Australian company with securities listed on the ASX, the Company is required to report reserves and resources in Australia in accordance with the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves (The JORC Code 2012 Edition ) ("JORC Code"). You should note that while the Company's reserve and resource estimates comply with the JORC Code, they may not comply with the relevant guidelines in other countries. This is a presentation about geology, geoscientific interpretation, geoscientific speculation, gold deposits, gold potential, engineering, infrastructure, potential values, costs, risks, and related matters pertinent to Saracen’s present and future activities as a publicly listed mineral exploration and production company. It includes forecasts, predictions, targets and estimates of future expenditures which may vary over time. It is uncertain if further exploration will result in the determination of a Resource or Reserve. Where exploration, evaluation, operational and feasibility study expenditure estimates and budgets amounts are presented herein, ongoing prioritisation and scaling of expenditures will be subject to results and, where applicable, scheduling changes. Targeted production and other outcomes are subject to change, and may not eventuate, depending on the results of ongoing performance and assessment of data. All Reserves and Resources as referred to herein are in accordance with the JORC Code. Refer to last slide of this presentation for the relevant Competent Person statements. Resources are inclusive of Reserves. Certain statements contained in the Presentation Materials, including information as to the future financial or operating performance of the Company and its projects, are forward looking statements. Such forward looking statements: a) are necessarily based upon a number of estimates and assumptions that, while considered reasonable by the Company, are inherently subject to significant technical, business, economic, competitive, political and

social uncertainties and contingencies; b) involve known and unknown risks and uncertainties that could cause actual events or results to differ materially from estimated or anticipated events or results reflected in such forward looking statements; and c) may include, among other things, statements regarding estimates and assumptions in respect of prices, costs, results and capital expenditure, and are or may be based on assumptions and estimates related to future

technical, economic, market, political, social and other conditions. The Company disclaims any intent or obligation to publicly update any forward looking statements, whether as a result of new information, future events or results or otherwise. The words “believe”, “expect”, “anticipate”, “indicate”, “contemplate”, “target”, “plan”, “intends”, “continue”, “budget”, “estimate”, “may”, “will”, “schedule” and similar expressions identify forward looking statements. All forward looking statements contained in the Presentation Materials are qualified by the foregoing cautionary statements. Recipients are cautioned that forward looking statements are not guarantees of future performance and accordingly recipients are cautioned not to put undue reliance on forward looking statements due to the inherent uncertainty therein. The Presentation Materials do not purport to be all inclusive or to contain all information about the Company. This presentation is not a prospectus, disclosure document or other offering document under Australian law or under any other law. It is provided for information purposes and is not an invitation nor offer of shares for subscription, purchase or sale in any jurisdiction. Take care to question and carefully evaluate any judgments you might make, on the basis of the Presentation Materials, as to the value of Saracen and its securities. This presentation is not intended to provide the sole or principal basis of any investment or credit decision or any other risk evaluation and may not be considered as a recommendation by Saracen or its officers. Any investor reading the Presentation Materials should determine its interest in acquiring securities in Saracen on the basis of independent investigations that it considers necessary, prudent or desirable. Saracen and its officers do not accept any liability for any loss or damage suffered or incurred by any investor or any other person or entity however caused (including negligence) relating in any way to this presentation including, without limitation, the information contained in it, any errors or omissions however caused by any other person or entity placing any reliance on the Presentation Materials, its accuracy or reliability.

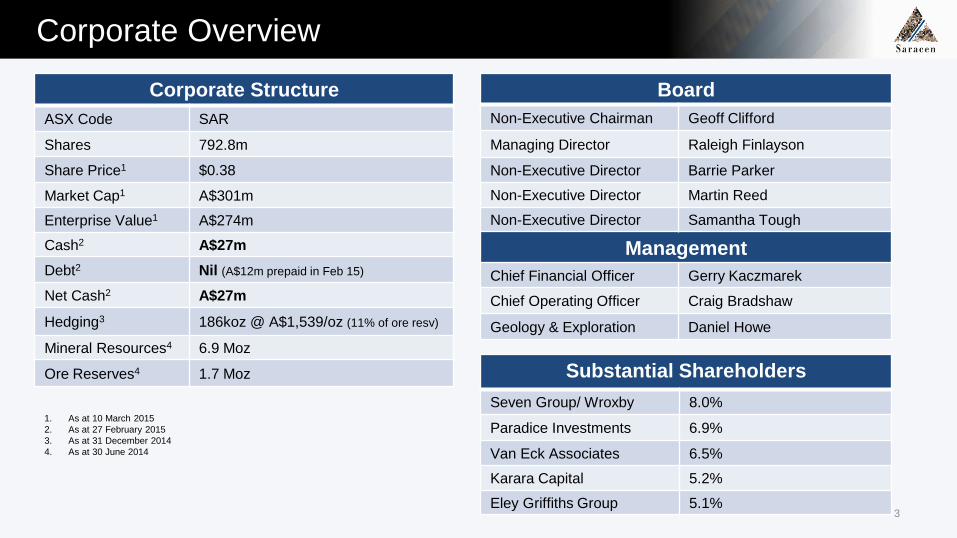

Corporate Overview

Corporate Structure ASX Code SAR

Shares 792.8m

Share Price1 $0.38

Market Cap1 A$301m

Enterprise Value1 A$274m

Cash2 A$27m Debt2 Nil (A$12m prepaid in Feb 15)

Net Cash2 A$27m

Hedging3 186koz @ A$1,539/oz (11% of ore resv)

Mineral Resources4 6.9 Moz

Ore Reserves4 1.7 Moz

Board Non-Executive Chairman Geoff Clifford

Managing Director Raleigh Finlayson

Non-Executive Director Barrie Parker

Non-Executive Director Martin Reed

Non-Executive Director Samantha Tough

Management Chief Financial Officer Gerry Kaczmarek

Chief Operating Officer Craig Bradshaw

Geology & Exploration Daniel Howe

Substantial Shareholders Seven Group/ Wroxby 8.0%

Paradice Investments 6.9%

Van Eck Associates 6.5%

Karara Capital 5.2%

Eley Griffiths Group 5.1%

1. As at 10 March 2015 2. As at 27 February 2015 3. As at 31 December 2014 4. As at 30 June 2014

3

4

Key Assets Thunderbox Operations: • DFS Due March 2015 • 2.5Mtpa CIL plant • Operational 2002 – 2007 • Produced 805koz @ US$290/oz Cash Costs • 2.8Moz Mineral Resources • 783koz Ore Reserves • 5 year mine life already in ore reserve

Carosue Dam Operations: • Developing a 5 year plan • 2.4Mtpa CIL Plant • Whirling Dervish OP +++ cashflow generation • Red October – record gold production • Karari Exploration Decline future upside catalyst

Combined Assets: • Vision + 300koz Producer • Vision < A$1,075/oz AISC • Vision + 5 years LOMP • Vision - 100% from organic growth • Vision - funded from internal cashflows • 6.9Moz Mineral Resources • 1.7Moz Ore Reserves

Carosue Dam Operations (CDO)

5

Red October: • 60koz delivered in FY2014 @ 6.4g/t • 60koz guidance in FY2015 @ 6.9g/t • Total UG production – 560kt @ 7.06g/t for 127koz • Record 21,511oz @ 8.43g/t delivered in Dec-14 Qtr • Recent High Grade drilling results:

• 3.1m @ 94.9g/t • 0.3m @ 337g/t • 3.7m @ 120.8g/t • 4.9m @ 104.7g/t

Carosue Dam: • 2.4mtpa CIL Plant • Record gold production of 42.8koz in Dec-14 • Record operational cashflow of A$16.4m in Dec-14 • Whirling Dervish OP - Strip Ratio <2.0:1 (w:o) • Whirling Dervish OP - Grade 1.6g/t rising to +2.0g/t • Karari - 28,000 metre exploration drilling program started • Karari - targeting +4 year UG ore reserve

6

Red

Oct

ober

Exp

lora

tion

7

Red

Oct

ober

Exp

lora

tion

Carosue Dam Operations – Whirling Dervish & Karari

8

KARARI WHIRLING DERVISH

PROCESSING PLANT

9

Whi

rling

Der

vish

Cro

ss S

ectio

n FY2013

FY2014

FY2015

10

Whi

rling

Der

vish

Gra

de &

Stri

p R

atio

s

11

Whi

rling

Der

vish

Pro

duct

ion

STO

CK

PILE

ORE STOCKPILE 1.67mt @ 1.05g/t

for 56,400 oz (as at 31 Dec 14)

Existing Deferred Free Cashflow of

~A$35.5m @ <A$900/oz AISC

Stockpile will

continue to grow to > 2.4mt & 100koz by the end of FY2015

@ < A$800/oz AISC = ~A$72m

Deferred FCF S/

PILE

Carosue Dam Operations - Guidance

12

FY2015 (Jul-14 to Jun-15) • Guidance of 145,000 to 155,000 ounces (set at start of FY2015) • 79,419 ounces delivered in 1st half… circa 160,000 ounce pa run rate • On track to comfortably exceed full year guidance:

• Grade increases from Whirling Dervish OP • Guidance being exceeded from Red October UG due to higher grades

FY2016 (Jul-15 to Jun-16) • Guidance to be advised in 2H FY2015 • Mill Feed from:

• Red October UG (guidance to be provided 2H FY2015) • Karari UG (guidance to be provided 2H FY2015) • Whirling Dervish Stockpile Ore (approx’ 100koz available for milling)

• Likely similar or better mill production as FY2015 • Lower AISC due to available Ore Stockpile (100koz @ <A$800/oz)

Carosue Dam Operations – Whirling Dervish & Karari

13

KARARI WHIRLING DERVISH

PROCESSING PLANT

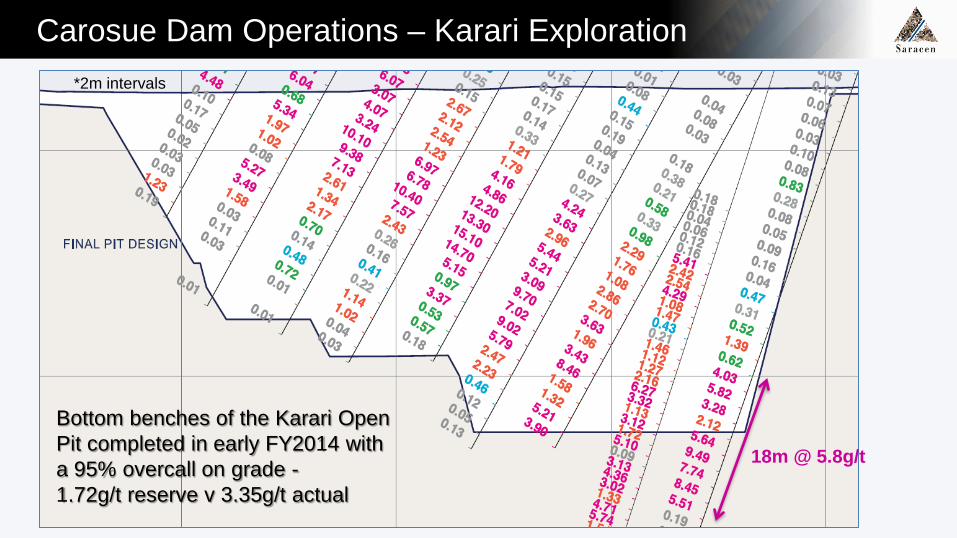

Carosue Dam Operations – Karari Exploration *2m intervals

18m @ 5.8g/t

Bottom benches of the Karari Open Pit completed in early FY2014 with a 95% overcall on grade - 1.72g/t reserve v 3.35g/t actual

15

Kar

ari E

xplo

ratio

n - L

ongs

ectio

n

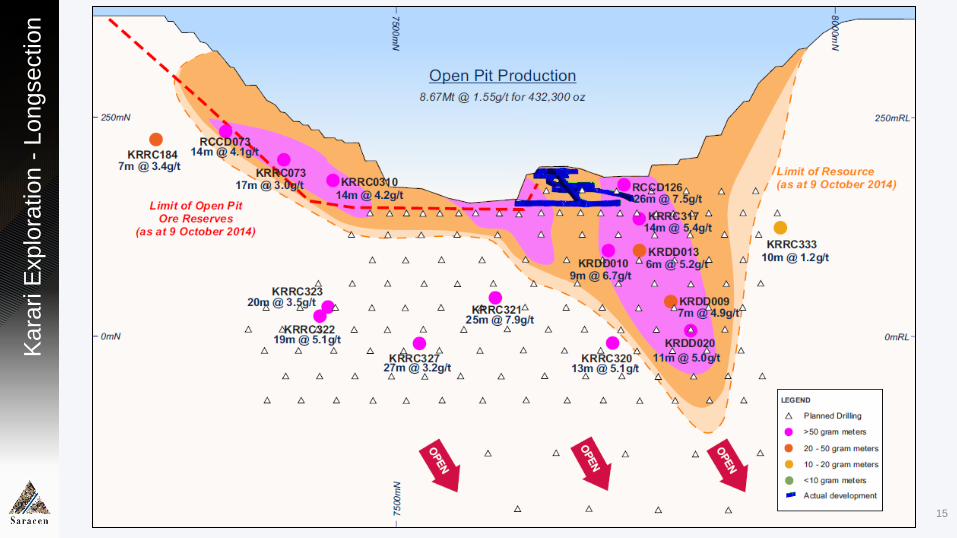

Carosue Dam Operations – Karari Exploration

16

17

Thun

derb

ox O

pera

tions

Acquisition (21/01/2014): • A$20m cash on Settlement; • A$3m cash upon the sooner of

commencement of commercial production, or if, after a period of 24 months following settlement, the prevailing gold price has exceeded A$1,550/oz for a calendar month;

• 1.5% NSR Royalty on the Thunderbox Operations - capped at A$17 million.

Equates to an acquisition cost of: • A$11 per Resource ounce • A$32 per Reserve ounce • Includes 2.5mtpa mill & facilities

Thunderbox 2.5mtpa CIL Plant

18

2.5mtpa gold processing facility. Similar size plant and scope of refurbishment as Saracen’s Carosue Dam 2.4mtpa plant

Thunderbox Open Pit

19 805,000 ounces yielded from the Thunderbox Open Pit @ US$290/oz Cash Costs

20

Thun

derb

ox –

His

toric

al P

rodu

ctio

n

805koz produced over 4.75 years (170kozpa) during early-mid 2000’s 100% from Thunderbox open pit @ 2.4g/t average grade Grade reconciliation performance excellent – within 1% of resource Excellent Mill Recoveries of 95.1% over life of project Very low Cash Costs of US$290/oz over life of project Remained in Care & Maintenance whilst owned by the World’s largest

Nickel Producer (Norilsk) during the gold bull run (ie) no depletion!

21

Thun

derb

ox L

ongs

ectio

n

<500m Below Surface

Thunderbox Operations Development Plans

22

Acquisition Case Development Plans (Jan-14): • US$45 - $55m Capex • 100% open pit mill feed • 728,000 ounces (431,000 ounces - Thunderbox OP; 297,000 ounces – Bannockburn OP) • Approx’ 140,000 ounces per annum • Approx’ A$1,100/oz AISC

Feasibility Study Development Plans (as at Feb-15): • Final Feasibility study outcomes due to be released in March 2015 • Phase 1 Open Pit Development from Thunderbox – years 1 to 4 • Phase 2 Underground Development from Thunderbox (subject to drilling) – year 3+ • Phase 3 Open Pit Development from Bannockburn, Mangilla, Rainbow & North Well

(subject to feasibility study) – year 5+

Thunderbox Development Timeline

23

Settlement

Approvals

Feasibility Study

Thunderbox Extension Drilling

Thunderbox Drilling Results

Bannockburn Infill Drilling

Bannockburn Drilling Results

Development Decision*

Plant Refurbishment

Development

Commissioning

Production

* Subject to positive feasib ility results

Jun QThunderbox Operations FY2016Dec Q Mar Q Jun Q Sep Q Dec Q Mar Q

FY2015

On track

On track

Assays Pending

Assays Pending

Decision Pending

On track to double Saracen’s production to ~300kozpa

On track

On track

News Flow!

24

March 2015 Qtr: • ½ Year Accounts • Red October Drilling Results • Karari Exploration Update • Thunderbox Drilling Results • Bannockburn Drilling Results • Thunderbox Feasibility Study

June 2015 Qtr: • Karari Drilling Results • Blue Manna Drilling Results • Red October Ore Reserve Update • Red October Drilling Results • FY2016 Guidance

September 2015 Qtr: • Full Year Accounts • Ore Reserves Update • Whirling Dervish UG Feasibility • Deep South UG Feasibility • Red October Drilling Results • Karari Drilling Results

December 2015 Qtr: • 2015 Annual Report • 2015 Annual General Meeting • Karari Drilling Results • Red October Drilling Results • Guidance Update >FY2017

Vision – Join the Mid Tier Ranks

25

Mid Tier Juniors

Join the Mid Tier Ranks – How? • > 300 koz pa • < A$1,075/oz AISC • + 5 years combined LOMP • 100% from organic growth • Funded from cashflows

Source: Macquarie Capital

27

Gro

up M

iner

al R

esou

rces

- G

old

28

Gro

up M

iner

al R

esou

rces

- N

icke

l

29

Gro

up O

re R

eser

ves