are you ready for jorc 2012?. outline timepresentation 13:00welcome (graham jeffress, aig wa)...

TRANSCRIPT

Are you Ready for Are you Ready for JORC 2012?JORC 2012?

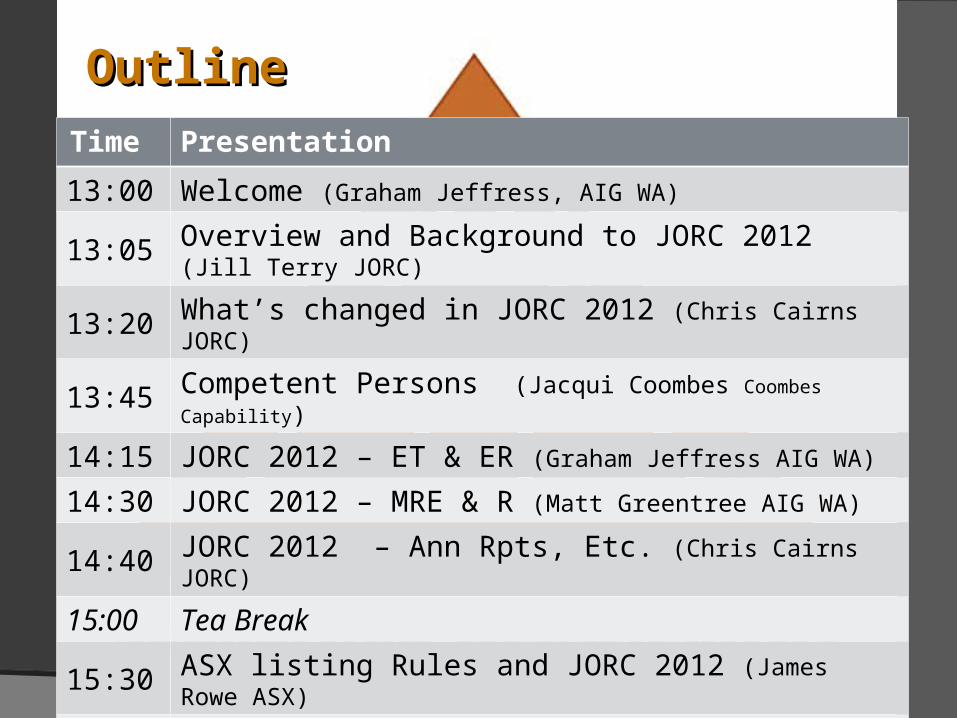

OutlineOutlineTime Presentation

13:00 Welcome (Graham Jeffress, AIG WA)

13:05 Overview and Background to JORC 2012 (Jill Terry JORC)

13:20 What’s changed in JORC 2012 (Chris Cairns JORC)

13:45 Competent Persons (Jacqui Coombes Coombes Capability)

14:15 JORC 2012 – ET & ER (Graham Jeffress AIG WA)

14:30 JORC 2012 – MRE & R (Matt Greentree AIG WA)

14:40 JORC 2012 – Ann Rpts, Etc. (Chris Cairns JORC)

15:00 Tea Break

15:30 ASX listing Rules and JORC 2012 (James Rowe ASX)

16:00 Moderated Panel Session and Question time (Rick Rogerson)

17:15 Sundowner & Informal discussions

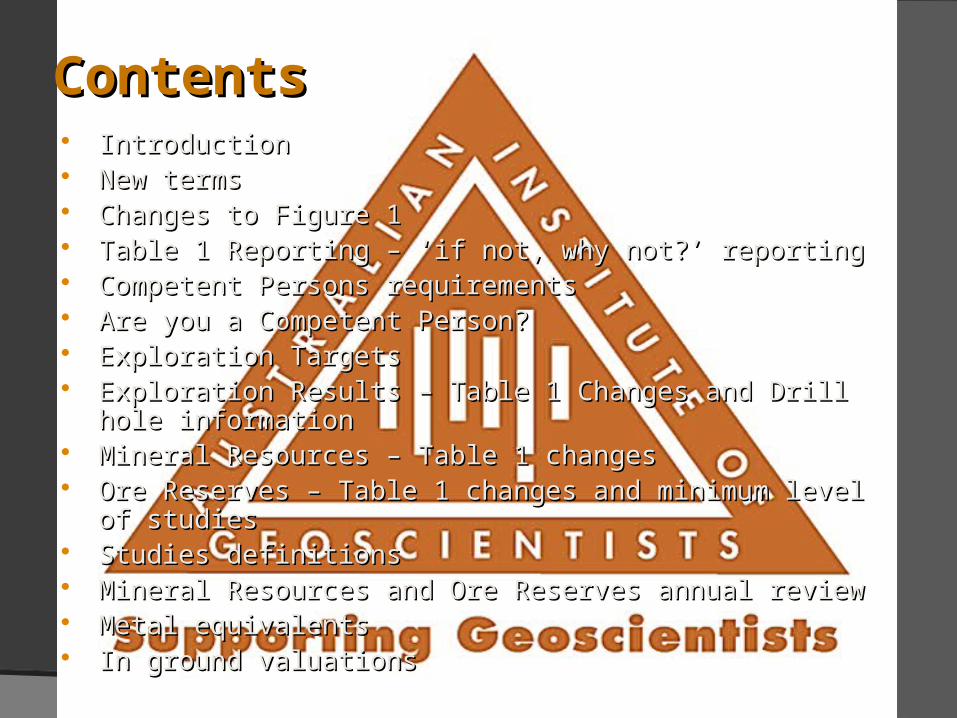

ContentsContents IntroductionIntroduction New termsNew terms Changes to Figure 1Changes to Figure 1 Table 1 Reporting – ‘if not, why not?’ reportingTable 1 Reporting – ‘if not, why not?’ reporting Competent Persons requirementsCompetent Persons requirements Are you a Competent Person?Are you a Competent Person? Exploration TargetsExploration Targets Exploration Results – Table 1 Changes and Drill hole informationExploration Results – Table 1 Changes and Drill hole information Mineral Resources – Table 1 changesMineral Resources – Table 1 changes Ore Reserves – Table 1 changes and minimum level of studiesOre Reserves – Table 1 changes and minimum level of studies Studies definitionsStudies definitions Mineral Resources and Ore Reserves annual reviewMineral Resources and Ore Reserves annual review Metal equivalentsMetal equivalents In ground valuations In ground valuations

OverviewOverviewJillian Terry

Why were the JORC Code and ASX Why were the JORC Code and ASX Listing Rules updated?Listing Rules updated?

Allowed for the inclusion of several Companies Updates since the Allowed for the inclusion of several Companies Updates since the adoption of the 2004 version of the JORC Code includingadoption of the 2004 version of the JORC Code including Metal Equivalents, sampling and Inferred Resource classificationMetal Equivalents, sampling and Inferred Resource classification In-situIn-situ values values Historical or foreign estimatesHistorical or foreign estimates

ASIC wanted a rule to govern Production Target announcementsASIC wanted a rule to govern Production Target announcements ASIC wanted annual review of Mineral Resources and Ore ReservesASIC wanted annual review of Mineral Resources and Ore Reserves Brought most terms into alignment with the international CRIRSCO Brought most terms into alignment with the international CRIRSCO

reporting guidelines (Committee for Mineral Reserves reporting guidelines (Committee for Mineral Reserves International Reporting Standards)International Reporting Standards)

Wanted to reinforce equal importance of JORC principles of Wanted to reinforce equal importance of JORC principles of Materiality, Transparency and CompetenceMateriality, Transparency and Competence

Why were the JORC Code and ASX Why were the JORC Code and ASX Listing Rules updated?Listing Rules updated?

Wanted to improve transparency for reporting of Exploration Wanted to improve transparency for reporting of Exploration TargetsTargets

Included a rule on extrapolation clarification for Inferred Included a rule on extrapolation clarification for Inferred ResourcesResources

Wanted to introduce requirements for minimum level of technical Wanted to introduce requirements for minimum level of technical studies to support Ore Reserve statementsstudies to support Ore Reserve statements

Wanted to change the emphasis of Table reporting from just Wanted to change the emphasis of Table reporting from just ‘material’ Table 1 criteria to all Table 1 criteria on an ‘if not, why ‘material’ Table 1 criteria to all Table 1 criteria on an ‘if not, why not?’ basis so investors cannot be mislead by a Public Report not?’ basis so investors cannot be mislead by a Public Report remaining silent on a material issueremaining silent on a material issue

Additional Definitions i.e. studies, material or significant projects, Additional Definitions i.e. studies, material or significant projects, material changematerial change

Consultation ProcessConsultation Process

Early 2012 review process commenced with request for feedback Early 2012 review process commenced with request for feedback on ASX Listing Rules and JORC Code exposure documentson ASX Listing Rules and JORC Code exposure documents

Public meetings by ASX, JORC, AIG, AusIMMPublic meetings by ASX, JORC, AIG, AusIMM Meetings with industry and MCAMeetings with industry and MCA 114 written JORC submissions received, 138 ASX written 114 written JORC submissions received, 138 ASX written

submissions received (two rounds)submissions received (two rounds) Co-operative liaison between JORC, ASX and ASIC to produce draft Co-operative liaison between JORC, ASX and ASIC to produce draft

JORC Code and draft ASX Listing Rules – released September 2012 JORC Code and draft ASX Listing Rules – released September 2012 for commentfor comment

81 written submission received for JORC Code, written 81 written submission received for JORC Code, written submissions received for ASX Listing Rulessubmissions received for ASX Listing Rules

Publishing and Transition PeriodPublishing and Transition Period

Submissions considered in final drafting of ASX Listing Rules and Submissions considered in final drafting of ASX Listing Rules and JORC CodeJORC Code

ASX Listing Rules released November 8ASX Listing Rules released November 8thth 2012 2012

JORC Code released December 20JORC Code released December 20thth 2012 2012

Mandatory from Dec 1Mandatory from Dec 1stst 2013 2013

Requirement for a Pre-Feasibility Study to support an Ore Reserve Requirement for a Pre-Feasibility Study to support an Ore Reserve mandatory from Dec 1mandatory from Dec 1stst 2014 2014

Benefits of High Quality ReportingBenefits of High Quality Reporting

Accepted and compatible national (and international) public reporting Accepted and compatible national (and international) public reporting standards will:standards will:

Provide greater confidence to investors and thereby facilitate capital Provide greater confidence to investors and thereby facilitate capital raising raising

encourage siphoning of scarce risk capital from non-mining sourcesencourage siphoning of scarce risk capital from non-mining sources

facilitate investment comparisons between different mineral deposits, facilitate investment comparisons between different mineral deposits, and reduce unnecessary effort and cost for debt/equity funding from and reduce unnecessary effort and cost for debt/equity funding from different sourcesdifferent sources

assist free flow of direct and portfolio investment and therefore assist free flow of direct and portfolio investment and therefore reduce cost of capitalreduce cost of capital

17/3/2013 Introduction to JORC 10

What has Changed?What has Changed?

What has changed in JORC 2012?What has changed in JORC 2012?

Table 1 reporting on an ‘if not, why not?’ basis – Clauses 2, 5, 19, Table 1 reporting on an ‘if not, why not?’ basis – Clauses 2, 5, 19, 27, 35 and the introduction of Table 1.27, 35 and the introduction of Table 1.

Competent Person Attributions – Clause 9Competent Person Attributions – Clause 9 Exploration Targets – Clause 17Exploration Targets – Clause 17 Pre-Feasibility required for Ore Reserves – Clause 29Pre-Feasibility required for Ore Reserves – Clause 29 Technical Studies definitions – Clause 37-40Technical Studies definitions – Clause 37-40 Annual Reporting – Clause 15Annual Reporting – Clause 15 Metal Equivalents – Clause 50Metal Equivalents – Clause 50 In situ In situ values – Clause 51values – Clause 51 Additional guidance on reporting in Table 1Additional guidance on reporting in Table 1

ASX Listing Rules have also changedASX Listing Rules have also changed

These changes include:These changes include:Annual Annual reporting of Ore Reservesreporting of Ore ReservesParallel requirementsParallel requirements with the JORC Code for the reporting of initial with the JORC Code for the reporting of initial or material changes to Exploration Results, Mineral Resources or Ore or material changes to Exploration Results, Mineral Resources or Ore ReservesReservesReporting of Reporting of Production TargetsProduction TargetsPre-Feasibility study required to report Ore Reserves – Clause 29Pre-Feasibility study required to report Ore Reserves – Clause 29Reporting of historical estimates and foreign estimatesReporting of historical estimates and foreign estimatesCompetent Person requirementsCompetent Person requirementsReporting Terms of Joint Venture agreementsReporting Terms of Joint Venture agreementsBe careful to check the related requirements of the relevant exchange Be careful to check the related requirements of the relevant exchange if reporting for a company listed on an exchange other than ASX!if reporting for a company listed on an exchange other than ASX!

Public Reporting of Exploration Results, Mineral Resources and Ore Public Reporting of Exploration Results, Mineral Resources and Ore

Reserves Reserves

mustmust be in compliance with the JORC Code be in compliance with the JORC Code

ANDAND

mustmust comply with comply with the rules of the relevant securities exchangethe rules of the relevant securities exchange

Ignorance is not a defence……Ignorance is not a defence……

Public Public Reporting Reporting that meets that meets

ALL ALL requirementsrequirements

New TermsNew Terms

New terms introduced into JORC 2012 New terms introduced into JORC 2012 CodeCode

Significant projectSignificant project““An exploration or mineral development project that has, or could have, a An exploration or mineral development project that has, or could have, a significant influence on the market value or operationssignificant influence on the market value or operations of the listed of the listed company, and/or has specific prominence in Public Reports and company, and/or has specific prominence in Public Reports and announcements.announcements.” ” (Appendix 1 Generic Terms and Equivalents)(Appendix 1 Generic Terms and Equivalents)

New terms introduced into JORC 2012 New terms introduced into JORC 2012 CodeCode

Material changeMaterial change““A material change could be a change in the estimated tonnage or grade or A material change could be a change in the estimated tonnage or grade or in the classification of the Mineral Resources or Ore Reserves. in the classification of the Mineral Resources or Ore Reserves.

Whether there has been a material change in relation to a significant Whether there has been a material change in relation to a significant project must be considered by taking into account all of the relevant project must be considered by taking into account all of the relevant circumstances, including the style of mineralisation. circumstances, including the style of mineralisation.

This includes considering whether the change in estimates is likely to have a This includes considering whether the change in estimates is likely to have a material effect on the price or value of the company’s securmaterial effect on the price or value of the company’s securities.” ities.” (Guideline to Clause 5)(Guideline to Clause 5)

Is the project Material?Is the project Material?

What is the market capitalisation of the company? What is the market capitalisation of the company?

Will the disclosure of the information affect the price of the company’s Will the disclosure of the information affect the price of the company’s shares?shares?

Does the company spend a significant proportion on this project? Does the company spend a significant proportion on this project?

Does the company earn a significant amount from this project?Does the company earn a significant amount from this project?

Will the project be an asset in the medium to long term?Will the project be an asset in the medium to long term?

Has the company made specific announcements about this project?Has the company made specific announcements about this project?

How prominently does the company promote this project (website, How prominently does the company promote this project (website, quarterlies, annual reports, presentations, etc)?quarterlies, annual reports, presentations, etc)?

New terms introduced into JORC 2012 New terms introduced into JORC 2012 CodeCode

‘‘if not, why not?’if not, why not?’““means that each item listed in the relevant section of Table 1 must be means that each item listed in the relevant section of Table 1 must be discussed and if it is not discussed then the Competent Person must explain discussed and if it is not discussed then the Competent Person must explain why it has been omitted from the documentation.”why it has been omitted from the documentation.”

(Guideline to Clause 5)(Guideline to Clause 5)

Relationship between Exploration Relationship between Exploration Results, Mineral Resources, & Ore Results, Mineral Resources, & Ore Reserves, Figure 1 of the JORC Code Reserves, Figure 1 of the JORC Code

Clause 4 2012 Code — Additional Clause 4 2012 Code — Additional Explanation of PrinciplesExplanation of Principles

““Transparency and Materiality”Transparency and Materiality” are guiding principles of the Code, are guiding principles of the Code, and the Competent Person must provide explanatory comments on and the Competent Person must provide explanatory comments on material assumptions underlying the declaration of Exploration material assumptions underlying the declaration of Exploration Results, Mineral Resources or Ore Reserves Results, Mineral Resources or Ore Reserves

In particular, […] the benchmark of Materiality is that which In particular, […] the benchmark of Materiality is that which includes includes all aspects relating to the Exploration Results, Mineral Resources or all aspects relating to the Exploration Results, Mineral Resources or Ore ReservesOre Reserves that an investor (or their advisers) would reasonably that an investor (or their advisers) would reasonably expect to see explicit comment on from the Competent Person. expect to see explicit comment on from the Competent Person.

The Competent Person must not remain silent on any material aspect The Competent Person must not remain silent on any material aspect for which the presence or absence of comment could affect the for which the presence or absence of comment could affect the public perception or value of the mineral occurrence”public perception or value of the mineral occurrence”

This slide contains only This slide contains only extractsextracts from Clause 4, 2012 JORC Code from Clause 4, 2012 JORC Code

Table 1 ReportingTable 1 Reporting

Table 1 structureTable 1 structure

Section 1 Sampling Techniques and Data

Section 2 Reporting of Exploration Results

Section 3 Estimation and Reporting of Mineral Resources

Section 4 Estimation and Reporting of Ore Reserves

Section 5 Estimation and Reporting of Diamonds and Other Gemstones

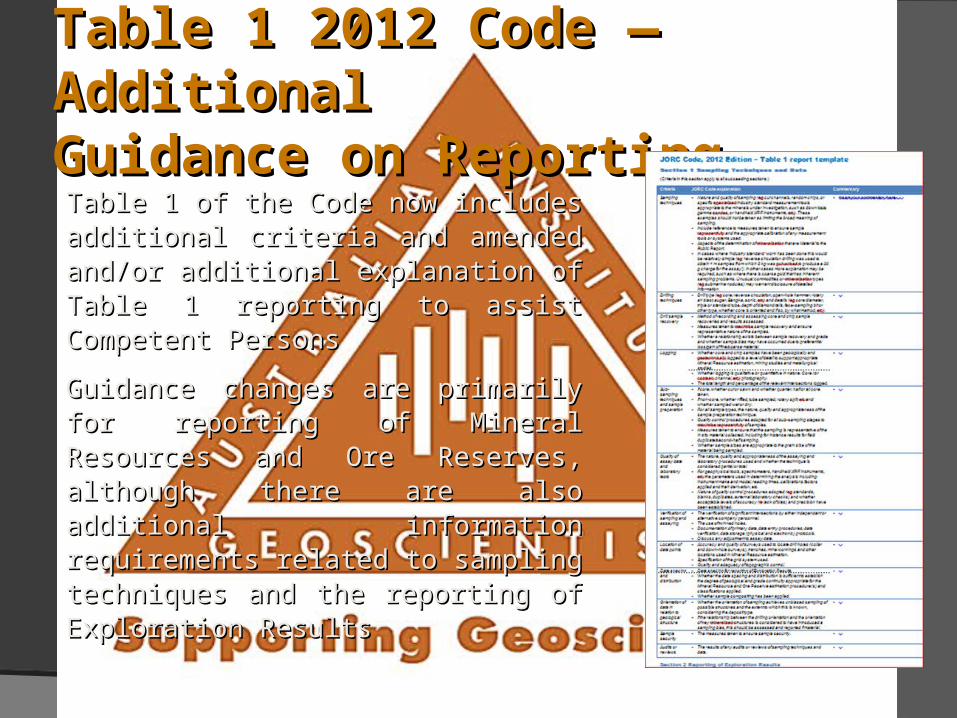

Table 1 2012 Code — Additional Table 1 2012 Code — Additional Guidance on ReportingGuidance on ReportingTable 1 of the Code now includes Table 1 of the Code now includes additional criteria and amended and/or additional criteria and amended and/or additional explanation of Table 1 reporting additional explanation of Table 1 reporting to assist Competent Persons to assist Competent Persons

Guidance changes are primarily for Guidance changes are primarily for reporting of Mineral Resources and Ore reporting of Mineral Resources and Ore Reserves, although there are also Reserves, although there are also additional information requirements additional information requirements related to sampling techniques and the related to sampling techniques and the reporting of Exploration Resultsreporting of Exploration Results

‘‘if not, why not?’ if not, why not?’ reportingreporting

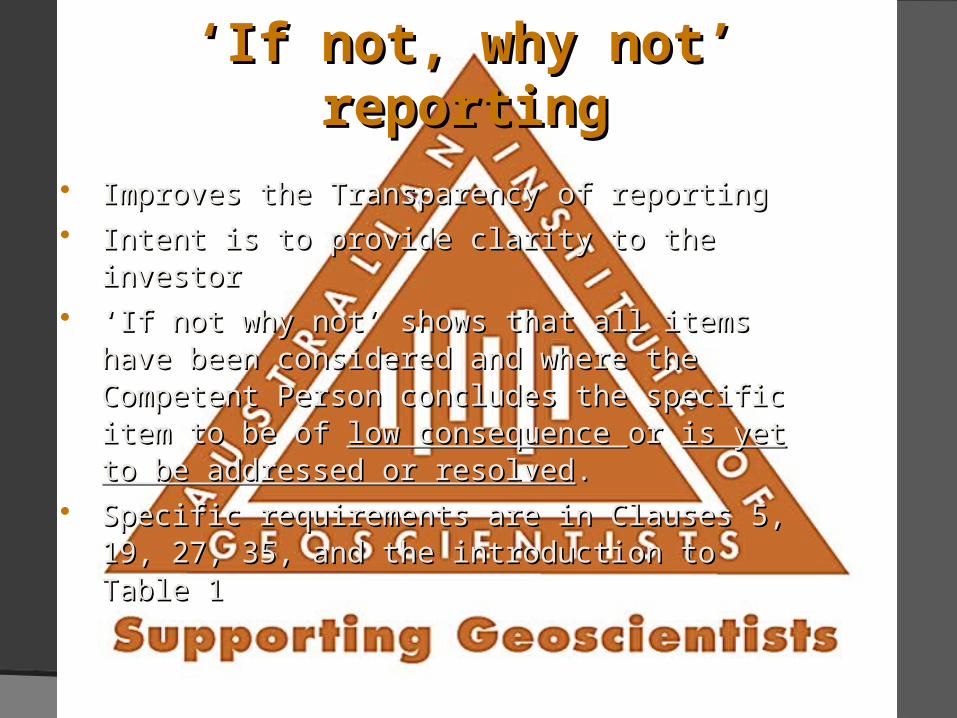

‘‘If not, why not’ reportingIf not, why not’ reporting

Improves the Transparency of reportingImproves the Transparency of reporting Intent is to provide clarity to the investor Intent is to provide clarity to the investor ‘‘If not why not’ shows that all items have been considered If not why not’ shows that all items have been considered

and where the Competent Person concludes the specific and where the Competent Person concludes the specific item to be of item to be of low consequence low consequence or or is yet to be addressed or is yet to be addressed or resolvedresolved..

Specific requirements are in Clauses Specific requirements are in Clauses 5, 19, 27, 35, and the 5, 19, 27, 35, and the introduction to Table 1introduction to Table 1

The introductory section of Table 1 is significantly expanded to reinforce The introductory section of Table 1 is significantly expanded to reinforce the 2012 Code’s requirements for how and when Table 1 and ‘if not, the 2012 Code’s requirements for how and when Table 1 and ‘if not, why not’ reporting are required.why not’ reporting are required.

““In the context of complying with the Principles of the Code, comment In the context of complying with the Principles of the Code, comment on the relevant sections of Table 1 should be provided on an ‘if not, why on the relevant sections of Table 1 should be provided on an ‘if not, why not’ basis within the Competent Person’s documentation and must be not’ basis within the Competent Person’s documentation and must be provided where required according to the specific requirements of provided where required according to the specific requirements of Clauses 19, 27 and 35 for significant projects in the Public Report. Clauses 19, 27 and 35 for significant projects in the Public Report.

This is to ensure that it is clear to the investor whether items have been This is to ensure that it is clear to the investor whether items have been considered and deemed of low consequence or have yet to be considered and deemed of low consequence or have yet to be addressed or resolved.”addressed or resolved.”

This slide contains only This slide contains only extractsextracts from the Introduction to Table 1, 2012 JORC Code from the Introduction to Table 1, 2012 JORC Code

““2. In this edition of the JORC Code, important terms and their 2. In this edition of the JORC Code, important terms and their definitions are highlighted in bold text. The guidelines are placed definitions are highlighted in bold text. The guidelines are placed after the respective Code clauses using indented italics. They are after the respective Code clauses using indented italics. They are intended to provide assistance and guidance to readers. They do intended to provide assistance and guidance to readers. They do not form part of the Code, but should be considered persuasive not form part of the Code, but should be considered persuasive when interpreting the Code. Indented italics are also used for when interpreting the Code. Indented italics are also used for Appendix 1 – ‘Generic Terms and Equivalents’ and Table 1 – ‘Check Appendix 1 – ‘Generic Terms and Equivalents’ and Table 1 – ‘Check List of Assessment and Reporting Criteria’ to make it clear that List of Assessment and Reporting Criteria’ to make it clear that they are also they are also part of the guidelines, and that the latter is not part of the guidelines, and that the latter is not mandatory for reporting purposesmandatory for reporting purposes.”.”

This statement (This statement (in green abovein green above), together with all of the examples ), together with all of the examples being negative, was taken by many Competent Persons as an being negative, was taken by many Competent Persons as an opportunity not to report all material information. opportunity not to report all material information.

““Table 1 provides a [reminder] of criteria to be considered by the Table 1 provides a [reminder] of criteria to be considered by the Competent Person in developing their documentation and in preparing a Competent Person in developing their documentation and in preparing a Public Report. Public Report.

In the context of complying with the principles of the Code, comments In the context of complying with the principles of the Code, comments relating to the items in the relevant sections of Table 1 should be relating to the items in the relevant sections of Table 1 should be provided on an ‘if not, why not’ basis within the Competent Person’s provided on an ‘if not, why not’ basis within the Competent Person’s documentation.”documentation.”

This slide contains extracts only of Clause 5, 2012 JORC Code.

““Additionally, comments related to the relevant sections of Table 1 must Additionally, comments related to the relevant sections of Table 1 must be complied with on an ‘if not, why not’ basis within Public Reporting for be complied with on an ‘if not, why not’ basis within Public Reporting for significant projects […] when reporting Exploration Results, Mineral significant projects […] when reporting Exploration Results, Mineral Resources or Ore Reserves for the Resources or Ore Reserves for the first timefirst time [or][…] where these items [or][…] where these items have have materially changedmaterially changed from when they were last Publicly Reported. from when they were last Publicly Reported.

Reporting on an ‘if not, why not’ basis is to ensure that it is clear to an Reporting on an ‘if not, why not’ basis is to ensure that it is clear to an investor whether items have been considered and deemed of low investor whether items have been considered and deemed of low consequence or are not yet addressed or resolved.”consequence or are not yet addressed or resolved.”

This slide contains only extracts from Clause 5, 2012 JORC Code. Emphasis added.

Are You Competent?Are You Competent?

A common distortion of A common distortion of Principles from Clause 4, Principles from Clause 4, 2004 JORC Code 2004 JORC Code had resulted in:had resulted in:

Competence Based on work by Competent Person

JORCCompliant Reports?

2004 JORC Code Principles 2004 JORC Code Principles — — Competence Bias?Competence Bias?

Competent Person’s Consent Competent Person’s Consent

[For] Public reporting of Exploration Results, Mineral Resources and Ore [For] Public reporting of Exploration Results, Mineral Resources and Ore Reserves for significant projects for the first time or when there is a Reserves for significant projects for the first time or when there is a material change, the company must include the following: material change, the company must include the following: Competent Person’s Competent Person’s name and the name of their employername and the name of their employer Any possible Any possible conflicts of interest conflicts of interest for the Competent Persons? for the Competent Persons? Public report is based on documentation compiled by the Competent Public report is based on documentation compiled by the Competent

PersonPerson. The Competent Person(s) must have given prior written . The Competent Person(s) must have given prior written consent in regards to the “form and context” in which the public consent in regards to the “form and context” in which the public report appears; andreport appears; and

Competent Person’s Consent Competent Person’s Consent

Public reports also need …Public reports also need …

A statement of written consentA statement of written consent from the Competent Person from the Competent Person

A Competent Person Consent Form is available from the JORC A Competent Person Consent Form is available from the JORC website. website.

The onus is on the company to obtain approval, but the Competent The onus is on the company to obtain approval, but the Competent Person Person shouldshould encourage observation of this requirement encourage observation of this requirement

There are recent examples where this has not happened! Written There are recent examples where this has not happened! Written consent may be requested by ASX and placed on the Company consent may be requested by ASX and placed on the Company Announcements Platform. Announcements Platform.

JORC 2012 - Additional Provisions for JORC 2012 - Additional Provisions for Competent PersonsCompetent PersonsConflicts of interestConflicts of interest

•Identify and disclose potential conflicts of interest by the Competent Identify and disclose potential conflicts of interest by the Competent Person or a related party, such as: Person or a related party, such as:

• shares or options held in the Company, orshares or options held in the Company, or

• performance-related bonus payments linked to the reporting of performance-related bonus payments linked to the reporting of Exploration Results, Mineral Resources or Ore ReservesExploration Results, Mineral Resources or Ore Reserves

Previously Reported ResultsPreviously Reported ResultsWhere the Competent Person(s) has previously given consent [a] Where the Competent Person(s) has previously given consent [a] report can refer back to the original report. report can refer back to the original report.

However, the company However, the company must confirm must confirm that:that:

““It is not aware of any new information or data that materially It is not aware of any new information or data that materially affects the information included in the relevant market affects the information included in the relevant market announcement.”announcement.”

andand

““In the case of estimates of Mineral Resources or Ore Reserves, the In the case of estimates of Mineral Resources or Ore Reserves, the company confirms that all material assumptions and technical company confirms that all material assumptions and technical parameters underpinning the estimates in the relevant market parameters underpinning the estimates in the relevant market announcement continue to apply and have not materially changed.”announcement continue to apply and have not materially changed.”

Clause 9 of the JORC Code, 2012 EditionClause 9 of the JORC Code, 2012 Edition

What is a Competent Person? What is a Competent Person? (Clause 11)(Clause 11)

““A ‘Competent Person’ is a minerals industry professional who is a A ‘Competent Person’ is a minerals industry professional who is a Member or Fellow of AusIMM, or of AIG, or of a ‘Recognised Member or Fellow of AusIMM, or of AIG, or of a ‘Recognised Professional Organisation’ (RPO)Professional Organisation’ (RPO)

A Competent Person must have a A Competent Person must have a minimumminimum of 5 years of 5 years relevantrelevant experience in the style of mineralisation or type of deposit under experience in the style of mineralisation or type of deposit under consideration consideration andand in the activity which that person is undertaking. in the activity which that person is undertaking.

If the Competent Person is preparing documentation on Exploration If the Competent Person is preparing documentation on Exploration Results, the relevant experience must be in exploration. If the Results, the relevant experience must be in exploration. If the Competent Person is estimating, or supervising the estimation of Competent Person is estimating, or supervising the estimation of Mineral Resources, the relevant experience must be in the estimation, Mineral Resources, the relevant experience must be in the estimation, assessment and evaluation of Mineral Resources. If the Competent assessment and evaluation of Mineral Resources. If the Competent Person is estimating, or supervising the estimation of Ore Reserves, the Person is estimating, or supervising the estimation of Ore Reserves, the relevant experience must be in the estimation, assessment, evaluation relevant experience must be in the estimation, assessment, evaluation and economic extraction of Ore Reserves.”and economic extraction of Ore Reserves.”

Competent Person Self Test :Competent Person Self Test :1.1. Do I belong to an appropriate professional organisation?Do I belong to an appropriate professional organisation?

AusIMM, AIG, or a Recognised Professional Organisation (RPO)AusIMM, AIG, or a Recognised Professional Organisation (RPO)

2.2. Do I have the minimum relevant experience?Do I have the minimum relevant experience? 5 years experience relevant to the commodity & style of 5 years experience relevant to the commodity & style of

mineralisation & the activitymineralisation & the activity The key qualifier in the definition of a Competent Person is the The key qualifier in the definition of a Competent Person is the

word ‘relevant’. It is not always necessary for a person to have word ‘relevant’. It is not always necessary for a person to have five years experience in every type of deposit in order to act as a five years experience in every type of deposit in order to act as a Competent Person.Competent Person.

3.3. Am I satisfied that I could face my peers and demonstrate Am I satisfied that I could face my peers and demonstrate competence in the commodity, type of deposit, and situation competence in the commodity, type of deposit, and situation under consideration?under consideration?

If doubt exists, either seek an opinion from appropriately If doubt exists, either seek an opinion from appropriately experienced colleagues or decline to act as a Competent Personexperienced colleagues or decline to act as a Competent Person

Jacqui Coombes

Reporting of Reporting of Exploration TargetsExploration Targets

EExploration Target – now defined xploration Target – now defined ((Clause 17)Clause 17)

““An Exploration Target is a statement […] of the […] potential of a An Exploration Target is a statement […] of the […] potential of a mineral deposit in a defined geological setting where the statement or mineral deposit in a defined geological setting where the statement or estimate […] relates to mineralisation for which there has been estimate […] relates to mineralisation for which there has been insufficient exploration insufficient exploration to estimate a Mineral Resource.”to estimate a Mineral Resource.”

Clause 17 of the JORC Code, 2012 EditionClause 17 of the JORC Code, 2012 Edition

Exploration Target is defined in Clause 17 of the 2012 JORC Code which Exploration Target is defined in Clause 17 of the 2012 JORC Code which also explains how that terminology may be used within a Public Report.also explains how that terminology may be used within a Public Report.

The clause emphasises the importance of ensuring that a reported The clause emphasises the importance of ensuring that a reported Exploration Target cannot be misconstrued or misrepresented as a Exploration Target cannot be misconstrued or misrepresented as a Mineral Resource or Ore Reserve, and that all disclosures of an Mineral Resource or Ore Reserve, and that all disclosures of an Exploration Target must clarify whether the target is based on actual Exploration Target must clarify whether the target is based on actual results or a proposed exploration programme.results or a proposed exploration programme.

EExploration Target – now defined xploration Target – now defined ((Clause 17)Clause 17)

Clause 17 of the 2012 JORC Code is a significant expansion and further Clause 17 of the 2012 JORC Code is a significant expansion and further development of Clause 18 of the 2004 JORC Code. development of Clause 18 of the 2004 JORC Code.

The 2012 Clause 17 definition of Exploration Target is identical to the The 2012 Clause 17 definition of Exploration Target is identical to the CRIRSCO definition. CRIRSCO definition.

Clause 17 also includes additional further explanation of how Clause 17 also includes additional further explanation of how Exploration Targets should be reported in Public ReportsExploration Targets should be reported in Public Reports.

EExploration Target – now defined xploration Target – now defined ((Clause 17)Clause 17)

Key points to remember:Key points to remember:

Must only report target tonnes and grade (quality) as RANGESMust only report target tonnes and grade (quality) as RANGES

Must report whether the target is based on actual results or on proposed Must report whether the target is based on actual results or on proposed [work][work]

Report Report all exploration all exploration conducted to dateconducted to date

Must include the warning statement within the same paragraph as the Must include the warning statement within the same paragraph as the first reference to the Exploration Targetfirst reference to the Exploration Target

EExploration Target – now defined xploration Target – now defined ((Clause 17)Clause 17)

Key points to remember (con’t):Key points to remember (con’t):

Exploration Targets Exploration Targets cannot cannot be used in a ‘headline’ or highlights sectionbe used in a ‘headline’ or highlights section

Must include details of [work] designed to test the validity of the Must include details of [work] designed to test the validity of the Exploration Target and a timeframe within which those activities are Exploration Target and a timeframe within which those activities are expected to be completedexpected to be completed

Maps, cross-sections or graphs must be accompanied with explanatory Maps, cross-sections or graphs must be accompanied with explanatory texttext

The Public Report including an Exploration Target must be accompanied The Public Report including an Exploration Target must be accompanied by a Competent Person’s statement taking responsibility for the form and by a Competent Person’s statement taking responsibility for the form and context in which the Exploration Target appears.context in which the Exploration Target appears.

EExploration Target – now defined xploration Target – now defined ((Clause 17)Clause 17)

Reporting of Reporting of Exploration ResultsExploration Results

Exploration Results Exploration Results ((Clause 19)Clause 19)

““Clear diagrams and maps designed to represent the geological Clear diagrams and maps designed to represent the geological context must be included in the report. These must include, but not be context must be included in the report. These must include, but not be limited to a plan view of drill hole collar locations and appropriate limited to a plan view of drill hole collar locations and appropriate sectional views.”sectional views.”

This slide contains only extracts from Clause 19, 2012 JORC Code

Exploration Results Exploration Results ((Clause 19)Clause 19)

““As required under Clause 4 and 5, the Competent Person must not As required under Clause 4 and 5, the Competent Person must not ‘remain silent on any issue for which the presence or absence of ‘remain silent on any issue for which the presence or absence of comment could impact the public perception or value of the mineral comment could impact the public perception or value of the mineral occurrence’. occurrence’.

For significant projects the reporting of all criteria in sections 1 and 2 of For significant projects the reporting of all criteria in sections 1 and 2 of Table 1 on an ‘if not, why not basis’ is required, preferably as an Table 1 on an ‘if not, why not basis’ is required, preferably as an appendix to the Public Report. appendix to the Public Report.

Additional disclosure is particularly important where inadequate or Additional disclosure is particularly important where inadequate or uncertain data affect the reliability of, or confidence in, a statement of uncertain data affect the reliability of, or confidence in, a statement of Exploration Results; for example, poor sample recovery, poor Exploration Results; for example, poor sample recovery, poor repeatability of assay or laboratory results, etc.”repeatability of assay or laboratory results, etc.”

This slide contains only extracts from Clause 19, 2012 JORC Code

EExploration Results xploration Results (ASX (ASX Listing Rule 5 and Guidance Note 31)Listing Rule 5 and Guidance Note 31)

ASX Listing Rule 5.7ASX Listing Rule 5.7

An entity publicly reporting in relation to a material mining project, An entity publicly reporting in relation to a material mining project, either: either:

(a) exploration results for the first time; or (a) exploration results for the first time; or

(b) any new exploration results, (b) any new exploration results,

must include all of the following information in a market must include all of the following information in a market announcement and give it to ASX for release to the market. announcement and give it to ASX for release to the market.

This slide contains extracts only of the ASX Listing Rules and Guidance Note 31

EExploration Results xploration Results (ASX (ASX Listing Rule 5 and Guidance Note 31 – cont’d)Listing Rule 5 and Guidance Note 31 – cont’d)

5.7.1 As an appendix to the market announcement, a separate report providing all information that is material to understanding the exploration results, in relation to each of the criteria in section 1 (sampling techniques and data) and section 2 (reporting of exploration results) of Table 1 in Appendix 5A (JORC Code).

An entity that determines that one or more of those criteria is not material for this purpose must identify each such criterion and explain why it has determined that it is not material to understanding the exploration results.

This slide contains extracts only of the ASX Listing Rules and Guidance Note 31

EExploration Results xploration Results (ASX (ASX Listing Rule 5 and Listing Rule 5 and Guidance Note 31 – con’t)Guidance Note 31 – con’t)

5.7.2 As an appendix to the market announcement, a separate table setting out the following information for material drill-holes unless the entity determines that the information is not material:

• easting and northing of the drill-hole collar

• elevation or RL of the drill-hole collar

• dip and azimuth of the hole

• down hole width and depth

• end of hole

This slide contains extracts only of Rule 5.5 of the ASX Listing Rules Guidance Note 31

Reporting of Reporting of Minerals ResourcesMinerals Resources

Additional Requirements for Reporting Additional Requirements for Reporting Mineral Resources Mineral Resources (Clause 27)(Clause 27)

When reporting a Mineral Resource for a significant project for When reporting a Mineral Resource for a significant project for the first time, or when those estimates have materially changed the first time, or when those estimates have materially changed from when they were last reported, the following must be from when they were last reported, the following must be included:included:

A brief summary of the information in relevant sections of A brief summary of the information in relevant sections of Table 1 must be provided, or, Table 1 must be provided, or,

if a particular criterion is not relevant or material, a disclosure if a particular criterion is not relevant or material, a disclosure that it is not relevant or material and a brief explanation of why that it is not relevant or material and a brief explanation of why this is the case must be provided.this is the case must be provided.

“For a significant project, when Mineral Resource estimates are first Publicly Reported or when a material change occurs (including classification changes), there is an increased need for transparent discussion of the basis for the new Mineral Resource estimate in order that investors are appropriately informed of the basis for the changes.

As noted in Clauses 4 and 5 the benchmark of Materiality is that which an investor or their advisors would reasonably expect to see explicit comment on from the Competent Person, thus the reporting of all relevant criteria in Table 1 on an ‘if not, why not’ basis is required.”

“The Technical summary based against Table 1 criteria should be presented as an appendix to the Public Report.”

Note: This guidance relates directly to ASX Listing Rule requirements.

Additional Requirements for Reporting Additional Requirements for Reporting Mineral Resources Mineral Resources (Clause 27 – cont’d)(Clause 27 – cont’d)

Reporting of Ore Reporting of Ore ReservesReserves

Minimum of Pre-Feasibility Study for Minimum of Pre-Feasibility Study for Reporting Ore Reserves Reporting Ore Reserves (Clause 29 & 37)(Clause 29 & 37)

““An ‘Ore Reserve’ is the economically mineable part of a Measured An ‘Ore Reserve’ is the economically mineable part of a Measured and / or Indicated Mineral Resource. It includes diluting materials and and / or Indicated Mineral Resource. It includes diluting materials and allowances for losses, which may occur when the material is mined or allowances for losses, which may occur when the material is mined or extracted and is defined by studies at Pre-Feasibility or Feasibility level extracted and is defined by studies at Pre-Feasibility or Feasibility level as appropriate that include application of Modifying Factors” Clause 29as appropriate that include application of Modifying Factors” Clause 29

““However attention is drawn to the requirement for a Pre-Feasibility However attention is drawn to the requirement for a Pre-Feasibility Study or a Feasibility Study to have been completed for the Public Study or a Feasibility Study to have been completed for the Public Reporting of an Ore Reserve in Clause 29. An Ore Reserve must not be Reporting of an Ore Reserve in Clause 29. An Ore Reserve must not be reported based on the completion of a Scoping Study.” Clause 37reported based on the completion of a Scoping Study.” Clause 37

This slide contains extracts only of Clauses 29 and 37, 2012 JORC Code

Additional Requirements for Additional Requirements for Reporting Ore Reserves Reporting Ore Reserves (Clause 35)(Clause 35)

““In a Public Report of an Ore Reserve estimate for a significant project In a Public Report of an Ore Reserve estimate for a significant project for the first time, or when those estimates have materially changed for the first time, or when those estimates have materially changed from when they were last reported, a brief summary of the information from when they were last reported, a brief summary of the information in relevant sections of in relevant sections of Table 1 must be provided or, if a particular Table 1 must be provided or, if a particular criterion is not relevant or material, a disclosure that it is not relevant criterion is not relevant or material, a disclosure that it is not relevant or material and a brief explanation of why this is the case must be or material and a brief explanation of why this is the case must be provided. provided.

For a significant project, when Ore Reserve estimates are first Publicly For a significant project, when Ore Reserve estimates are first Publicly Reported Reported or when a material change occurs (including classification or when a material change occurs (including classification changes), there is an increased need for transparent discussion of the changes), there is an increased need for transparent discussion of the basis for the new Ore Reserve estimate in order that investors are basis for the new Ore Reserve estimate in order that investors are appropriately informed of the basis for the changes.”appropriately informed of the basis for the changes.”

This slide contains extracts only of Clause 35, 2012 JORC Code

Additional Requirements for Reporting Additional Requirements for Reporting Ore Reserves Ore Reserves (Clause 35 – cont’d)(Clause 35 – cont’d)

““As noted in Clauses 4 and 5 the benchmark of Materiality is that which As noted in Clauses 4 and 5 the benchmark of Materiality is that which an investor or their advisers would reasonably expect to see explicit an investor or their advisers would reasonably expect to see explicit comment on from the Competent Person, thus the reporting of all comment on from the Competent Person, thus the reporting of all criteria in Table 1 on an ‘if not, why not’ basis is required.” criteria in Table 1 on an ‘if not, why not’ basis is required.”

““The Technical summary based against Table 1 criteria should be The Technical summary based against Table 1 criteria should be presented as an appendix to the Public Report. presented as an appendix to the Public Report.

Where there are as yet unresolved issues potentially impacting the Where there are as yet unresolved issues potentially impacting the reliability of, or confidence in, a statement of Ore Reserves (for example, reliability of, or confidence in, a statement of Ore Reserves (for example, limited geotechnical information, complex orebody metallurgy, limited geotechnical information, complex orebody metallurgy, uncertainty in the permitting process, etc.) those unresolved issues uncertainty in the permitting process, etc.) those unresolved issues should also be reported.”should also be reported.”

This slide contains extracts only of Clause 35, 2012 JORC Code

Additional Requirements for Reporting Additional Requirements for Reporting Ore Reserves Ore Reserves (Clause 35 – cont’d)(Clause 35 – cont’d)

““If there is doubt about what should be reported, it is better to err on the If there is doubt about what should be reported, it is better to err on the side of providing too much information rather than too little. side of providing too much information rather than too little.

Uncertainties in any of the criteria listed in Table 1 that could lead to Uncertainties in any of the criteria listed in Table 1 that could lead to under-or over- statement of Ore Reserves should be disclosed.” under-or over- statement of Ore Reserves should be disclosed.”

This slide contains extracts only of Clause 35, 2012 JORC Code

Technical Studies Definitions in Technical Studies Definitions in 2012 Code2012 Code (Clauses 37 to 40) (Clauses 37 to 40)

Clause 37 describes what technical and economic studies are, and their Clause 37 describes what technical and economic studies are, and their application under the JORC Code.application under the JORC Code.

Scoping Study – Clause 38Scoping Study – Clause 38

Pre-Feasibility Study – Clause 39Pre-Feasibility Study – Clause 39

Feasibility Study – Clause 40Feasibility Study – Clause 40

This was in response to the requirement for a Pre-Feasibility Study to be This was in response to the requirement for a Pre-Feasibility Study to be conducted as part of estimating an Ore Reserve for inclusion in a Public conducted as part of estimating an Ore Reserve for inclusion in a Public Report.Report.

These definitions are identical to those in the CRIRSCO standard These definitions are identical to those in the CRIRSCO standard definitions, and will eventually be included in all the CRIRSCO standards definitions, and will eventually be included in all the CRIRSCO standards and codes.and codes.

Annual Reporting Annual Reporting of Mineral of Mineral

Resources and Ore Resources and Ore ReservesReserves

Annual Reporting of Mineral Annual Reporting of Mineral Resources and Ore Reserves Resources and Ore Reserves (Clause 15)(Clause 15)

““Companies must review and publically report their Mineral Resources Companies must review and publically report their Mineral Resources and Ore Reserves at least annually.” Clause 14 - 2004 JORC Codeand Ore Reserves at least annually.” Clause 14 - 2004 JORC Code

““Companies must review and publically report their Mineral Resources Companies must review and publically report their Mineral Resources and Ore Reserves annually. The annual review date must be nominated and Ore Reserves annually. The annual review date must be nominated by the Company in its Public Reports of Mineral Resources and Ore by the Company in its Public Reports of Mineral Resources and Ore Reserves and the effective date of each Mineral Resources and Ore Reserves and the effective date of each Mineral Resources and Ore Reserves statement must be shown. The Company must discuss any Reserves statement must be shown. The Company must discuss any material changes to previously reported Mineral Resources and Ore material changes to previously reported Mineral Resources and Ore Reserves at the time of publishing updated Mineral Resources and Ore Reserves at the time of publishing updated Mineral Resources and Ore Reserves.” Clause 15 – JORC Code 2012Reserves.” Clause 15 – JORC Code 2012

Annual Reporting of Mineral Resources Annual Reporting of Mineral Resources and Ore Reserves and Ore Reserves (Clause 15 – cont’d)(Clause 15 – cont’d)

What does it all mean for reporting Mineral Resources and Ore What does it all mean for reporting Mineral Resources and Ore Reserves?Reserves?

Companies must nominate their Companies must nominate their date of reviewdate of review

Does not need to be June 30 or January 1 but must be an annual Does not need to be June 30 or January 1 but must be an annual review date review date – don’t even think about February 29– don’t even think about February 29thth!!!!

Each reference in a Public Report must state the ‘effective date’Each reference in a Public Report must state the ‘effective date’

The annual review must discuss any material changes from the The annual review must discuss any material changes from the previously reported Mineral Resources and / or Ore Reservespreviously reported Mineral Resources and / or Ore Reserves

Other Code Other Code changes —changes —

Metal Equivalents Metal Equivalents & & In SituIn Situ Values Values

Reporting Metal Equivalents Reporting Metal Equivalents (Clause 50)(Clause 50)

New requirements for Public Reporting of Exploration Results, Mineral New requirements for Public Reporting of Exploration Results, Mineral Resources or Ore Reserves in terms of metal equivalents. Resources or Ore Reserves in terms of metal equivalents.

If a single equivalent grade for one major metal is reported, the details If a single equivalent grade for one major metal is reported, the details for for all material factors all material factors contributing to the net value [are needed]contributing to the net value [are needed]

Reporting Metal Equivalents Reporting Metal Equivalents (Clause 50)(Clause 50)

All material factors include:All material factors include:Individual grades for all metals Individual grades for all metals Assumed commodity prices for all metals (where the actual prices Assumed commodity prices for all metals (where the actual prices used are commercially sensitive, the company must disclose sufficient used are commercially sensitive, the company must disclose sufficient information, [though] perhaps in narrative rather than numerical form)information, [though] perhaps in narrative rather than numerical form)Assumed metallurgical recoveries for all metals and discussion of the Assumed metallurgical recoveries for all metals and discussion of the basis on which the assumed recoveries are derived (metallurgical test basis on which the assumed recoveries are derived (metallurgical test work, detailed mineralogy, similar deposits, etc.)work, detailed mineralogy, similar deposits, etc.)A clear statement that all the elements included in the metal A clear statement that all the elements included in the metal equivalents calculation have a reasonable potential to be recovered equivalents calculation have a reasonable potential to be recovered and soldand soldCalculation formula usedCalculation formula used

Reporting of Reporting of In Situ In Situ or ‘In Ground’ or ‘In Ground’ Values Values (Clause 51) (Clause 51)

Prohibition on the publication of Prohibition on the publication of in situ in situ or ‘in ground’ financial or ‘in ground’ financial values in a Public Report. values in a Public Report.

Such values are inconsistent with the requirements of the Code, Such values are inconsistent with the requirements of the Code, as they do not take account of the Modifying Factors and are as they do not take account of the Modifying Factors and are incompatible with the Code’s reporting terminology (as set out in incompatible with the Code’s reporting terminology (as set out in Figure 1, and throughout the Code). Figure 1, and throughout the Code).

The use of such financial values has little or no relationship to The use of such financial values has little or no relationship to economic viability, value or potential returns to investors. economic viability, value or potential returns to investors.

This new clause is based on information previously included in This new clause is based on information previously included in ASX Companies Update 03/08, previously prepared jointly by ASX ASX Companies Update 03/08, previously prepared jointly by ASX and JORC.and JORC.

Tea BreakTea Break

Are you Ready for Are you Ready for JORC 2012?JORC 2012?

ASX Listing Rules ASX Listing Rules and and

Guidance Note 31Guidance Note 31

ASX Listing Rules linkageASX Listing Rules linkage

17/3/2013 Introduction to JORC 72

ASX PresentationJames RoweState ManagerASX Listings Compliance (Perth)

Panel discussionPanel discussionRick Rogerson – ModeratorRick Rogerson – Moderator

Panel Panel Deborah Lord, SRK Consulting Deborah Lord, SRK Consulting Jason Harris, Cube Jason Harris, Cube Jeff Elliott, CSA GlobalJeff Elliott, CSA GlobalRichard Sulway, SnowdenRichard Sulway, SnowdenJohn Hearne , CoffeyJohn Hearne , CoffeyDean Carville , AMCDean Carville , AMC

Some Questions ?Some Questions ? Where can CPs find examples and advice about best practice and who Where can CPs find examples and advice about best practice and who

can CPs call for advice?can CPs call for advice? How do we deal with 2004 MRE in a 2012 world?How do we deal with 2004 MRE in a 2012 world? What is the difference between an aspiration & an Exploration Target? What is the difference between an aspiration & an Exploration Target?

Does at ET have an implication of being eventually economic? Must Does at ET have an implication of being eventually economic? Must there be on ground work done to define an ET?there be on ground work done to define an ET?

How do people deal with reporting preliminary economic information How do people deal with reporting preliminary economic information on ET or Inferred Res? Isn’t there a catch-22 between the Continuous on ET or Inferred Res? Isn’t there a catch-22 between the Continuous Disclosure provisions and the prohibition on reporting economic Disclosure provisions and the prohibition on reporting economic modelling based on Inferred Resources or Exploration Targets?modelling based on Inferred Resources or Exploration Targets?

How does VALMIN and JORC coexist?How does VALMIN and JORC coexist? How can we improve the ‘policing’ of the JORC code, will 2012 help?How can we improve the ‘policing’ of the JORC code, will 2012 help?

Thank YouThank YouRemember to visit the JORC website www.jorc.org for: Copies of the 2012 JORC CodeCopies of the 2012 JORC CodeDownloadable Table 1 templateDownloadable Table 1 templateLinks to ASX Listing Rules, FAQs, & Links to ASX Listing Rules, FAQs, & Guidance Note 31Guidance Note 31Other guidance materialOther guidance material