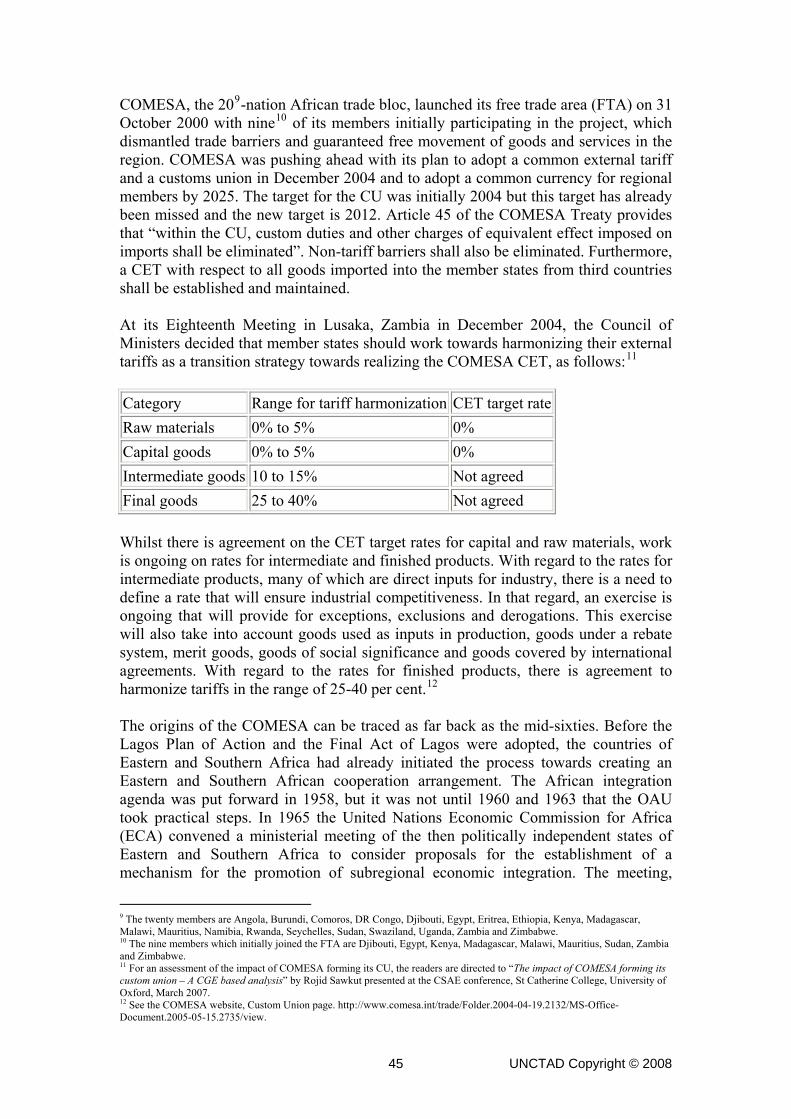

regional trade integrations: a comparative study

TRANSCRIPT

United Nations Conference on Trade and Development Virtual Institute Research Material

REGIONAL TRADE INTEGRATIONS: A COMPARATIVE STUDY THE CASES OF GAFTA, COMESA, AND SAPTA/SAFTA Authors Parts A and B (Comparative Analysis and GAFTA) Talib Awad, Professor of International Economics, Faculty of Business, University of Jordan([email protected]) Amir Bakir, Assistant Professor, Faculty of Business, University of Jordan([email protected]) Part C (COMESA) Rojid Sawkut, Lecturer, University of Mauritius ([email protected]) Sannassee Vinesh, Senior Lecturer, University of Mauritius ([email protected]) Seetanah Boopen, Lecturer, University of Technology of Mauritius ([email protected]) Fowdar Suraj, Lecturer, University of Mauritius ([email protected] ) Part D (SAPTA/SAFTA) Meeta Keswani Mehra, Associate Professor, CITD/SIS, Jawaharlal Nehru University, India Manoj Pant, Professor of Economics, CITD/SIS, Jawaharlal Nehru University, India

With research assistance from Saptarshi Basu Roy Choudhury, M.Phil. Scholar, CITD/SIS, Jawaharlal Nehru University, India Amit Sadhukhan, M.Phil. Scholar, CITD/SIS, Jawaharlal Nehru University, India

UNCTAD Copyright © 2008 1

TABLE OF CONTENT A. COMPARATIVE ANALYSIS............................................................ 6

I. Introduction .......................................................................... 6 II. Type and coverage of trade agreements ............................. 6 III. Intra-regional trade development and characteristics .......... 7

III.1 Intra-regional trade development ................................................ 7 III.2 Commodity structure.................................................................. 8 III.3 Trade direction .......................................................................... 8

IV. Impact of trade agreements on intra-regional trade ............. 9 IV.1 Revealed comparative advantage analysis .................................. 9 IV.2 Partial regression analysis ......................................................... 10

V. Intra trade obstacles ............................................................. 11 VI. Conclusion ........................................................................... 12

B. REGIONAL TRADE INTEGRATION: THE CASE OF GAFTA . 14 I. Introduction .......................................................................... 14 II. Overview: Theoretical background ....................................... 15

II.1 Economic analysis of regional economic integration............................... 15 II.2 Economic effects on member countries ................................................. 15

II.2.1 Trade creation and diversion ........................................................ 15 II.2.2 Scale and competition effects ....................................................... 18

II.3 Winners and losers .............................................................................. 19 III. Regional economic integration and the Great Arab Free Trade

Area ..................................................................................... 19 III.1 Previous economic integration efforts ......................................... 19 III.2 The Greater Arab Free Trade Area ...................................................... 20

IV. Trend and characteristics of intra-Arab trade ....................... 24 IV.1 Growth of intra-Arab trade .......................................................... 24 IV.2 Intra-Arab trade commodity structure .......................................... 25 IV.3 Intra-Arab trade destination ........................................................ 26

V. Measuring the effect of GAFTA on intra-Arab trade ............. 26 V.1 Revealed comparative advantage ............................................... 28 V.2 Partial regression analysis ......................................................... 29

VI. Intra-Arab trade problems and obstacles ............................. 31 VII. Conclusion and recommendations ....................................... 34

C. THE CASE FOR COMESA .............................................................. 38 I. Introduction .......................................................................... 38 II. Regional trade blocks in Africa ............................................. 38 III. Economic structure of some COMESA Members ................ 50 IV. Measuring the effect of COMESA on intra-COMESA trade: A

preliminary analysis ............................................................. 55 V. The role of COMESA exports in COMESA economic growth

............................................................................................. 56

UNCTAD Copyright © 2008 2

D. REGIONAL TRADE AGREEMENTS IN SOUTH ASIA: PROSPECTS FOR INTRA-REGIONAL TRADE COOPERATION............................................................................................................................................................. 65

I. Introduction and scope ......................................................... 65 II. Geo-political milieu of regional cooperation in South Asia ... 67 III. SAARC Preferential Trading Arrangement (SAPTA) ........... 68 IV. South Asia Free Trade Area (SAFTA) Agreement ............... 68 V. Bilateral initiatives................................................................. 70 VI. Multilateral initiatives outside the region............................... 72 VII. Broad economic and trade characteristics of South Asia ..... 74

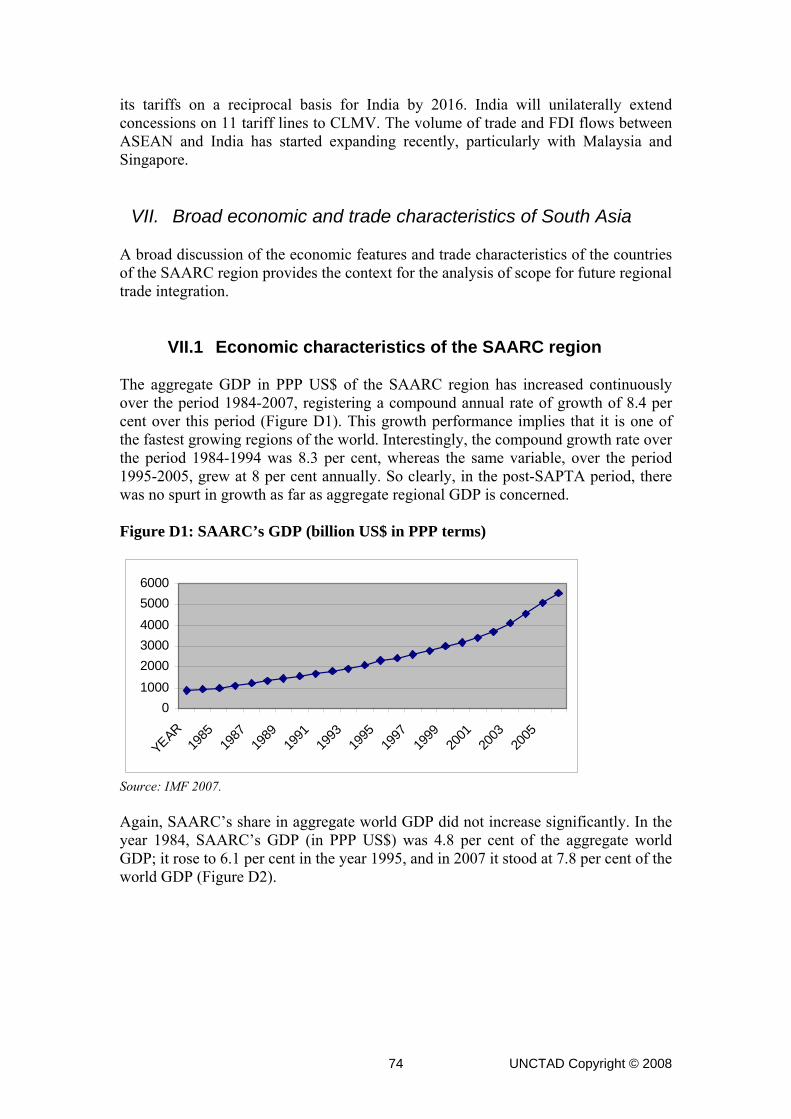

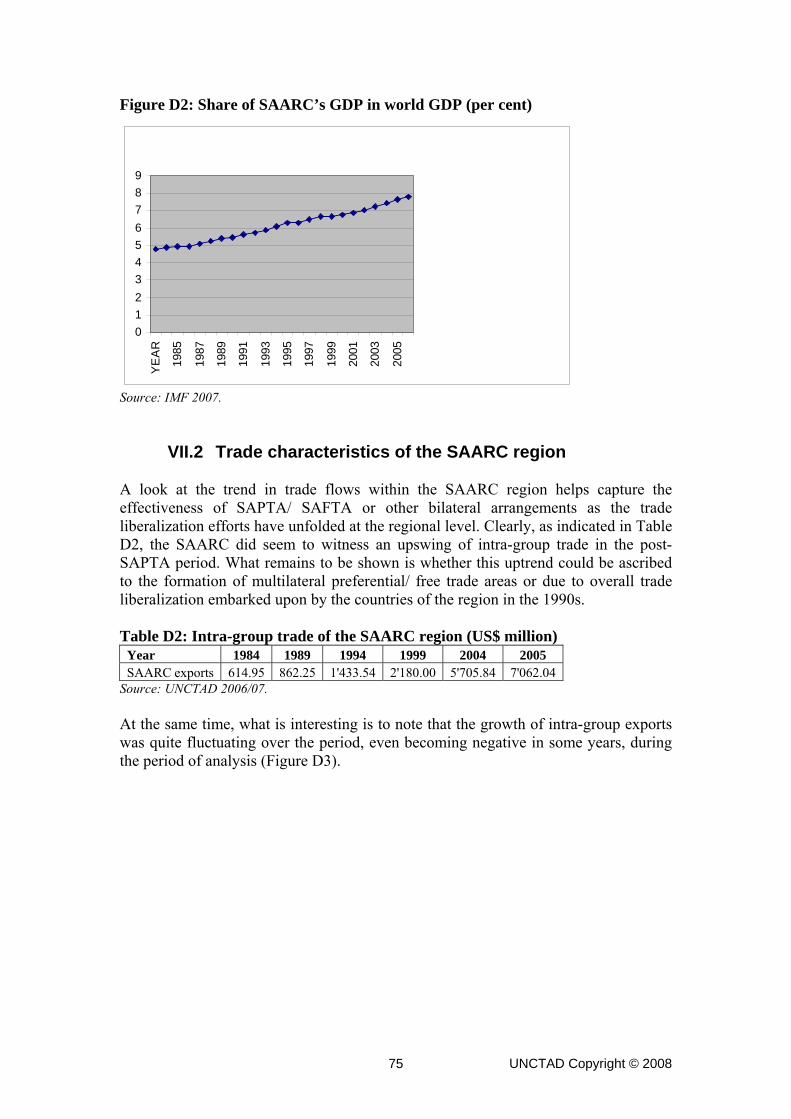

VII.1 Economic characteristics of the SAARC region............................ 74 VII.2 Trade characteristics of the SAARC region.................................. 75 VII.3 Assessing the scope for intra-regional trade ................................ 79

VIII. Summary and conclusions ................................................... 90

FIGURES Figure B1: Intra Arab Trade, 1980-2005................................................... 24 Figure B2: Intra exports and exports with the rest of the world (US$

millions) .................................................................................................. 27 Figure B3: Intra imports and imports with ROW ($US million) ............. 28 Figure D1: SAARC’s GDP (billion US$ in PPP terms) ........................... 74 Figure D2: Share of SAARC’s GDP in world GDP (per cent) ............... 75 Figure D3: Year to year growth of intra-group exports of SAARC

(per cent)................................................................................................ 76 Figure D4: Proportion of SAARC’s intra-group trade to its aggregate

GDP (per cent) ...................................................................................... 76 Figure D5: Proportion of SAARC’s intra-regional exports to its

exports to ROW (per cent) .................................................................. 77 Figure D6: Proportion of SAARC’s intra-regional imports to its

imports from ROW (per cent) ............................................................. 77 Figure D7: Intra-group exports and SAARC’s exports to ROW

(current US$ million) ............................................................................ 82 Figure D8: Intra-group imports and SAARC’s imports from ROW

(current US$ million) ............................................................................ 82

UNCTAD Copyright © 2008 3

TABLES Table A1: Type and coverage of trade agreements ............................... 7 Table A2: Share of exports by main products, 1985-2005 .................... 8 Table A3: Regression results of intra exports for GAFTA, COMESA,

and SAPTA/ SAFTA............................................................................. 10 Table A4: Regression results of intra imports for GAFTA, COMESA,

and SAPTA ............................................................................................ 11 Table B1: Growth rates of intra trade during the period 1980-2004 .... 25 Table B2: Intra-Arab trade growth rates for selected countries (per

cent) ........................................................................................................ 25 Table B3: Relative importance of intra-Arab exports according to

commodity groups ................................................................................ 26 Table B4: RCA indices for GAFTA countries by broad commodity

groups (2003, 2004)............................................................................. 29 Table B5: Estimation results for intra exports and intra imports in

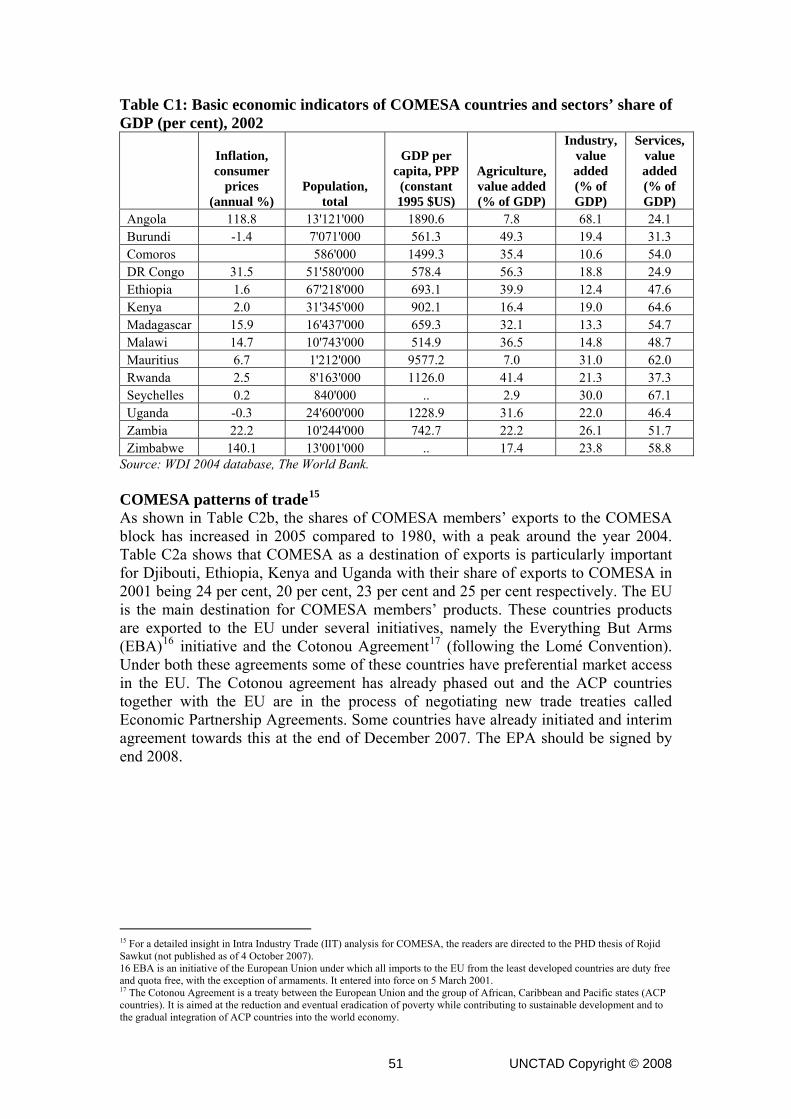

logarithm form ....................................................................................... 30 Table C1: Basic economic indicators of COMESA countries and

sectors’ share of GDP (per cent), 2002 ............................................ 51 Table C2a: Share of exports (per cent) .................................................... 52 Table C2b: Share of COMESA intra exports as a percentage of

COMESA total exports ........................................................................ 52 Table C2c: Average annual growth rate of exports and imports for

the COMESA region (per cent) .......................................................... 52 Table C3: Products exported as a percentage of COMESA total

intra exports ........................................................................................... 53 Table C4: GDP (PPP) yearly growth rate (per cent, 1995 prices) ....... 53 Table C5: GDP per capita yearly growth rate (per cent, 1995

prices) ..................................................................................................... 54 Table C6: OLS estimates in logarithm ...................................................... 56 Table C7: Cross section and random effects estimates ........................ 58 Table C8: Random effects panel estimates (COMESA exports to

COMESA and US and EU) ................................................................. 60 Table C-A: RCA for selected COMESA countries in 2000 at 2 digits

SITC ........................................................................................................ 61 Table D1: Preferences under SAPTA ....................................................... 68 Table D2: Intra-group trade of the SAARC region (US$ million) .......... 75 Table D3: Aggregate commodity composition of SAARC’s trade

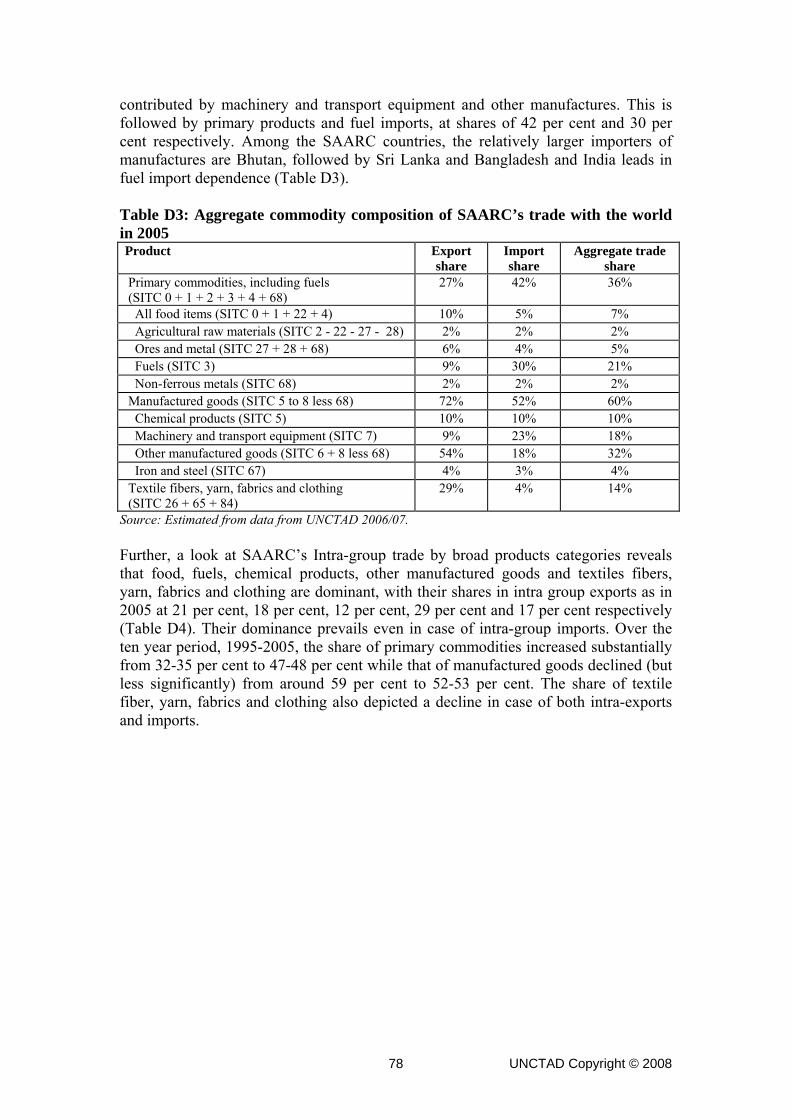

with the world in 2005 .......................................................................... 78 Table D4: Commodity composition of intra-group trade for the

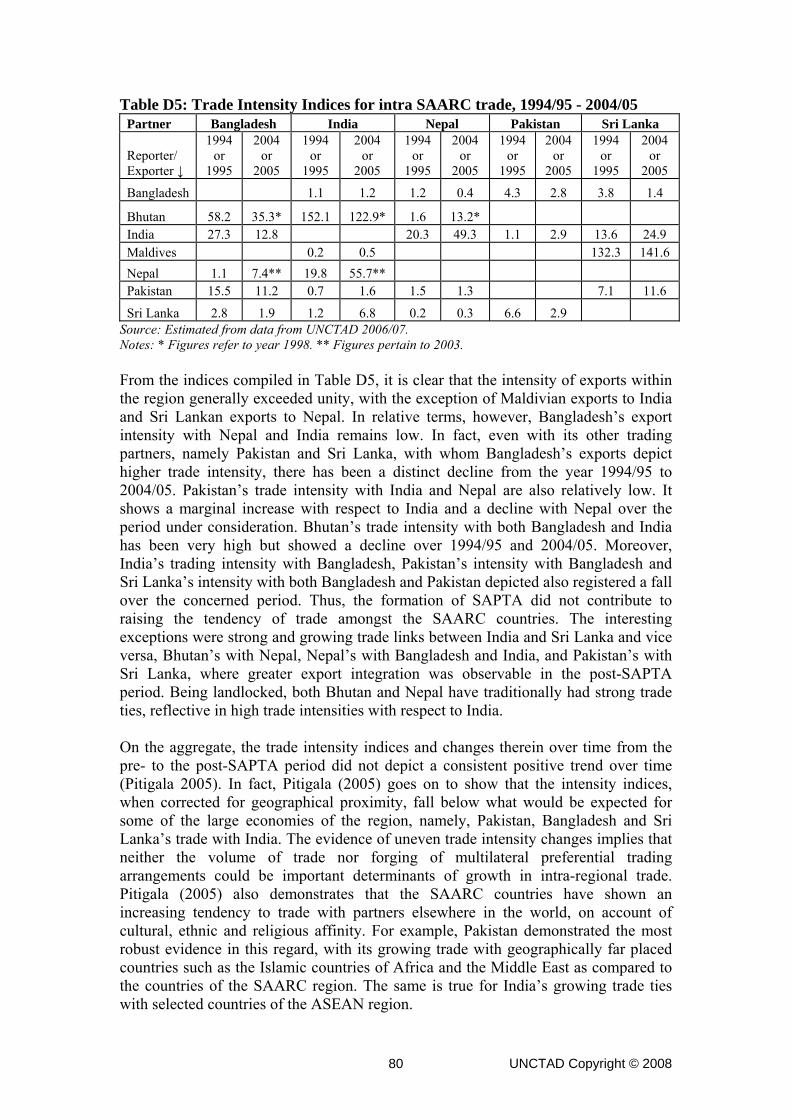

SAARC region in 2005 ........................................................................ 79 Table D5: Trade Intensity Indices for intra SAARC trade, 1994/95 -

2004/05 .................................................................................................. 80

UNCTAD Copyright © 2008 4

Table D6: Results of multivariate regression for intra-regional exports.................................................................................................... 84

Table D7: Results of multivariate regression for intra-regional imports.................................................................................................... 84

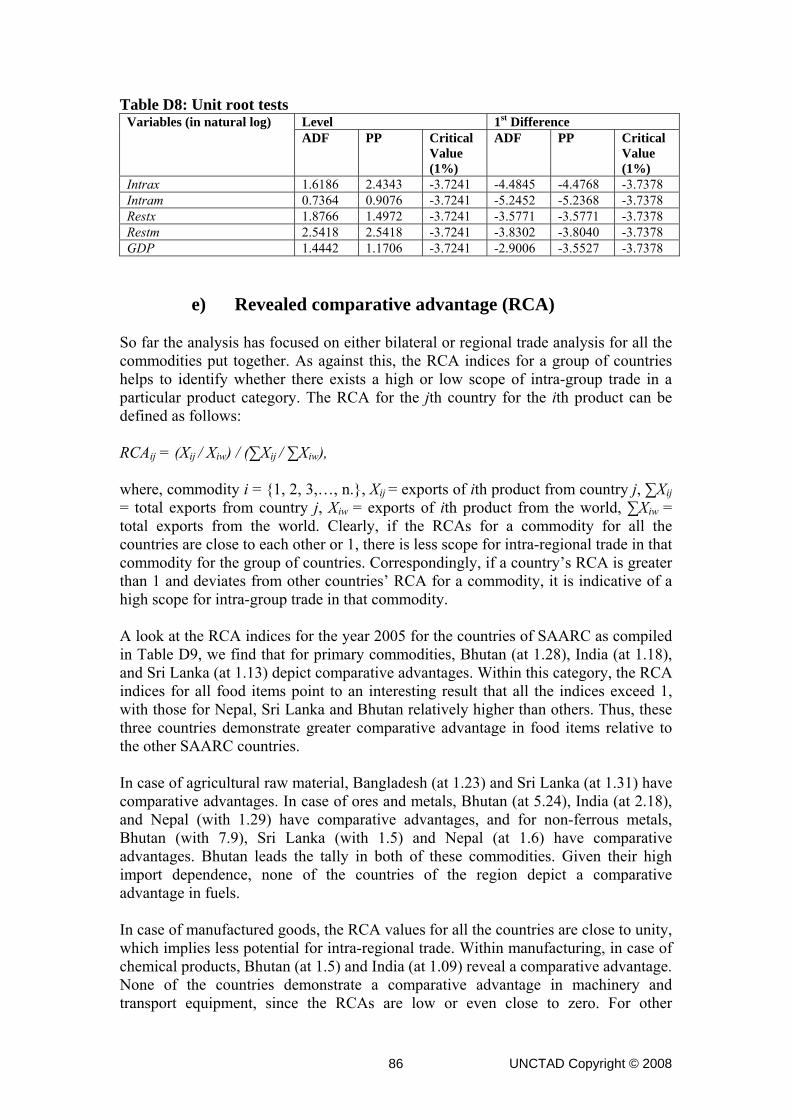

Table D8: Unit root tests.............................................................................. 86 Table D9: RCA indices for SAARC countries for broad commodity

groups in 2005 ...................................................................................... 87

UNCTAD Copyright © 2008 5

A. COMPARATIVE ANALYSIS By Talib Awad and Amir Bakir

I. Introduction Following the initiative by the UNCTAD Virtual Institute that was launched during the second annual meeting of the participating member universities, mutual interest in regional trade agreements was expressed by three research groups representing the University of Jordan, the University of Mauritius and the Jawaharlal Nehru University, India. The encouragement and coordination efforts of the Virtual Institute team played an important role in realizing this joint research project. This joint research covers three regional trade agreements in three different parts of the world, the Great Arab Free Trade Area (GAFTA) in the Arab region, the Common Market for Eastern and Southern Africa (COMESA) in the African region, and the South Asia Preferential Trade Agreement (SAPTA) (followed by the recently promulgated South Asia Free Trade Area) in the South Asian region. The comparative part of the study covers the following four dimensions: type and coverage of trade agreements, characteristics and development of intra trade, impact of trade agreements on intra trade, and problems associated with implementing the RTAs.

II. Type and coverage of trade agreements As shown in Table A1 trade integration is limited to the first stage of economic integration, as free trade area, for the GAFTA and COMESA groups, while it took the form of preferential trade agreement for the SAPTA group, which recently culminated in the ratification of SAFTA. The agreement coverage was extensive as it covered most of the countries in their respective regions; seventeen countries in the Arab group, twenty countries in South Asia and seven countries in South-East Africa. In terms of the application of the agreements, the GAFTA was the most effective and comprehensive. Its actual implementation started in 1998 with a clear objective of complete elimination of non-tariff restrictions and gradual cutting of applied tariff rates by an average of 10 per cent annually. In 2002 the zero-tariff goal was achieved among GAFTA members, and most non-tariff restrictions were eliminated in almost all goods. In the case of COMESA however, although the agreement calls for elimination of all trade barriers starting 2000, it is not clear whether this objective was actually implemented. Furthermore, SAPTA was a preferential trade agreement allowing members the freedom to choose the pace, the list of commodities and the mode of trade liberalization, resulting in limited actual tariff reductions and trade preferences among members. By comparison, SAFTA is more comprehensive as well as it specifies a phased reduction in tariffs for the member countries. However, the transition to SAFTA is of recent origin and its impact on regional trade integration remains to be seen.

UNCTAD Copyright © 2008 6

Table A1: Type and coverage of trade agreements

Title Arabic Group East-South African Group

South Asian Group

Main trade agreement

GAFTA COMESA SAPTA

Type of agreement

Free Trade Area Free Trade Area Preferential Trade Agreement

Coverage 17 countries: Algeria, Bahrain, Egypt, Iraq, Jordan, Kuwait, Lebanon, Morocco, Oman, Palestine, Qatar, Saudi Arabia, Sudan, Syria, Tunisia, UAE and Yemen.

20 countries: Djibouti, Egypt, Kenya, Madagascar, Malawi, Mauritius, Sudan, Zambia, Angola, Burundi Comoros, D.R. Congo, Eretria, Ethiopia, Namibia, Rwanda, Seychelles, Swaziland, Tanzania, Uganda and Zimbabwe.

7 countries: India, Pakistan, Sri Lanka, Bangladesh, Nepal, Bhutan and Maldives. Afghanistan slated to join SAFTA in January 2008.

Starting date of agreement

January 1998 October 2000 December 1995/ January 2006

Trade liberalization measures

Elimination of quotas and other quantitative restrictions. Reduction of tariff rates on traded goods by an average of 10 per cent annually. Preferential treatment is granted to Palestine and Sudan.

Elimination of quotas and other quantitative restrictions. Reduction of tariff rates on traded goods.

Gradual concession on tariff and non-tariff measures with provision for special treatment for least developed countries. Phased elimination of tariffs over 2006-16, with different rates for the least developed members. Elimination of quantitative restrictions.

Source: Based on the three regional studies in parts B-D of this document. In addition to these three major trade agreements, many bilateral and multilateral free trade agreements, either within the regions or with countries outside the region, were signed by individual countries in each region.

III. Intra-regional trade development and characteristics

III.1 Intra-regional trade development Intra-regional trade (from now on intra trade) showed a modest growing trend in all three regions. In the GAFTA group it grew at an average annual rate of 4.8 per cent during 1980-1997. However, annual average growth rates were much higher (more than 18 per cent) after 1998 as shown in Figure B2 of the GAFTA study. However, it must be noted that these growth rates are nominal and most likely due to the recent sharp increases in primary commodities especially fuel. Intra-regional exports (intra exports) of SAARC as percentage of rest of the world exports increased from around 4 per cent over the period 1984-1994, to 5 per cent over the period 1995-2005. Correspondingly, intra-regional imports (intra imports) grew from an average of 2.4 per cent to 4.1 per cent, respectively. The growth rate of SAARC’s intra trade

UNCTAD Copyright © 2008 7

increased from 8 per cent to 12 per cent, between the two time periods, respectively. As far as COMESA is concerned, intra exports as percentage of total exports increased from 4 per cent in 1980 to 4.8 per cent in 2005.

III.2 Commodity structure In the GAFTA region more than 57 per cent of intra trade in 2005 was fuel and raw materials, followed by food and beverages with a share of 17 per cent, chemicals (14 per cent), and manufactured goods (about 6 per cent). Trade patterns for GAFTA shifted in favor of food and manufactured goods at the expense of fuel and raw materials over the period of the study. In the COMESA region food and beverages share in intra trade exceeded one third, followed by manufactured goods & chemicals (31 per cent), and fuel and raw materials (22 per cent). The share of manufactured goods and food in intra trade increased at the expense of minerals and raw materials over the period of the study. In the SAARC region manufactured goods dominated intra exports with a share of over 52 per cent, followed by primary commodities including fuel (47 per cent). Over the period of the study, the share of primary commodities increased (from 34 per cent to 47 per cent) at the expense of manufactured goods (less significant decline from 59 per cent to 52per cent). Intra-group trade in textile fiber, yarn, fabrics and clothing registered a significant decline. Table A2: Share of exports by main products, 1985-2005

1985 2005 GAFTA* COMESA SAARC*** GAFTA COMESA** SAARC

Fuel and Raw Materials

96.0 43.1 34.0 57.7 21.9 47.5

Food and Beverages

0.9 17.9 - 17.2 35.2 -

Manufactured Goods & Chemicals

2.4 20.0 59.0 20.1 31.2 52.5

Source: Based on the three regional studies in parts B-D of this document. Notes: * For 1980; ** for 2000; *** for 1995. The above analysis shows that while intra trade in the GAFTA is dominated by fuel and raw materials, manufactured goods play more important roles in the intra trade of the other two regions. Over the study period GAFTA and COMESA region witnessed a shift in the pattern of intra trade toward manufactured goods while in the SAARC region the shift was towards primary products.

III.3 Trade direction In the three regions intra trade was characterized by a high level of geographical concentration and in most cases it was restricted between two or three neighboring countries. For example, in the GAFTA region, Oman exported 64 per cent of intra exports to United Arab Emirates, and Libya exported 69 per cent of its intra exports to Tunisia, and 57 per cent of Bahrain’s intra exports were destined to Saudi Arabia, and Iraq’s intra exports with Morocco and Jordan amounted to 47 per cent and 21 per cent

UNCTAD Copyright © 2008 8

respectively. Similarly, within the SAARC region, trade between Sri Lanka and Maldives was the most intensive in the region, followed by India and Bhutan. In the COMESA region, Djibouti, Ethiopia, Kenya and Uganda exported more than 90 per cent of total intra exports in 2001. The geographical concentration clearly indicates the importance of geographical proximity and political influence in determining the direction of intra trade.

IV. Impact of trade agreements on intra-regional trade To evaluate the impact of regional trade agreements two analytical tools are employed: revealed comparative advantage (RCA) indices and multiple regression models. The RCA index will help identify the possibilities of intra trade expansion, a higher than one value will indicate a revealed comparative advantage in that particular sector. However if revealed comparative advantages are similar among countries of the particular region then there will be limited potential for expanding intra trade within that region. The regression approach is intended to measure the partial impact of the agreement on the regional intra trade. Since the three regional agreements were signed recently (after 1995), the sample under consideration does not permit to divide the sample into two: one before and one after the signing of agreement due to lack of degrees of freedom. An alternative simple approach would be the use of a dummy variable that takes the value of zero in the absence of the agreement, and of one when the agreement is effective. Two models were employed for this purpose: the first for modeling intra exports and the other for modeling intra imports. For the purpose of identifying the substitution effect between intra trade and trade with the rest of the word (ROW), exports to ROW was introduced as a an explanatory variable in the first model, and imports from ROW was introduced as an explanatory variable in the second model. These two variables can serve the purpose of capturing the effects of trade agreements other than intra trade agreements. In addition, total GDP was used as explanatory variable in each equation to capture the economic size effect in each region. Also time was introduced in the model with the purpose of capturing the growing trend in intra trade over time.

IV.1 Revealed comparative advantage analysis Based on the RCA analysis for the three regions, the GAFTA countries showed a high concentration in revealed comparative advantage in primary goods mainly fuel and ores & metals, with almost negligible advantages in other products. This implies a very limited potential for expanding intra trade in the region. COMESA members have comparative advantage in quite similar products which suggests that complementarities as a way to stimulate trade might be limited among some COMESA members. For the SAARC region, there is also a lack of complementarities as indicated by similar RCA indices. This points toward a high degree of competition in export structures, albeit at the aggregated commodity level.

UNCTAD Copyright © 2008 9

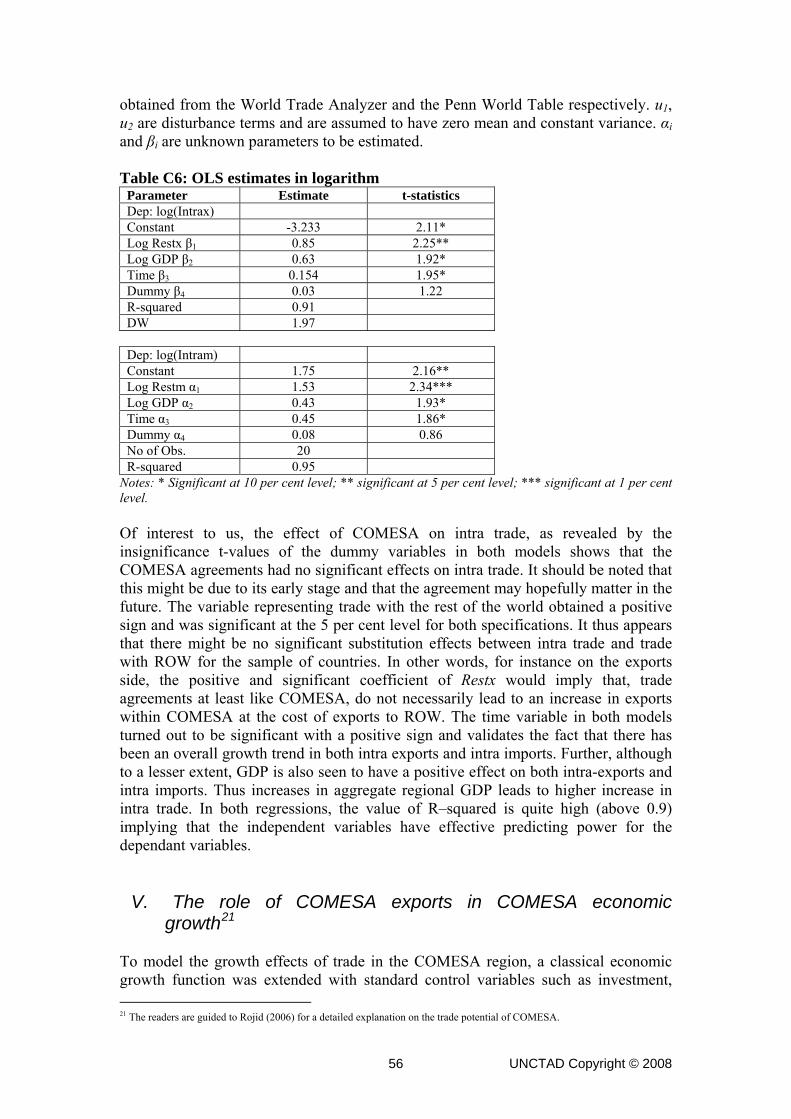

IV.2 Partial regression analysis The above specified regression model is used to explain the effects of the trade agreements on intra trade in the three regions. For the three regions a log linear specification was used. While the GAFTA and SAPTA's samples cover the period (1980-2005), the COMESA study used a slightly smaller sample covering the period (1985-2004). The results of applying the OLS for the three regions are summarized in Table A3: Table A3: Regression results of intra exports for GAFTA, COMESA, and SAPTA/ SAFTA

Variable GAFTA† COMESA SAPTA/ SAFTA

ROW exports 0.44 (4.3)**

0.85 (2.3)**

0.95 (5.3)***

Time 0.29 (5.4)**

0.15 (1.95)*

-0.22 (-3.8)***

GDP -0.007 (-0.27)

0.63 (1.92)*

0.54 (1.7)

Trade dummy -0.05 (-0.5)

0.3 (1.2)

0.06 (1.7)

R-square 0.83 0.91 0.99 Notes: † After correcting for first order autocorrelation. Figures in parenthesis are t-statistics. * Significant at 10 per cent level; ** significant at 5 per cent level; *** significant at 1 per cent level. The results of applying the OLS are satisfactory and consistent with economic theory in all three regions. The model fit is acceptable for the three regions as evident from the high R-squared values. As with regard to the substitution coefficient it turned out to be positive and statistically significant at least at the 5 per cent level. The positive sign indicates the absence of substitution effects between intra and ROW trade. The time trend variable coefficient was significant in all three regions (of varying degrees), indicating a positive trend in intra exports of the first two regions while it showed a decreasing trend in the SAPTA region over the period of study. The scale variable (GDP) was only significant (at 10 per cent level) for the COMESA region, which indicates toward a positive effect of economic size on intra exports in that region (This is also true for the SAARC region, although at a level of 11 per cent). Surprisingly, the trade dummy variable came out non-significant in all three regions indicating a negligible role of the trade agreements on intra exports of the three regions.

UNCTAD Copyright © 2008 10

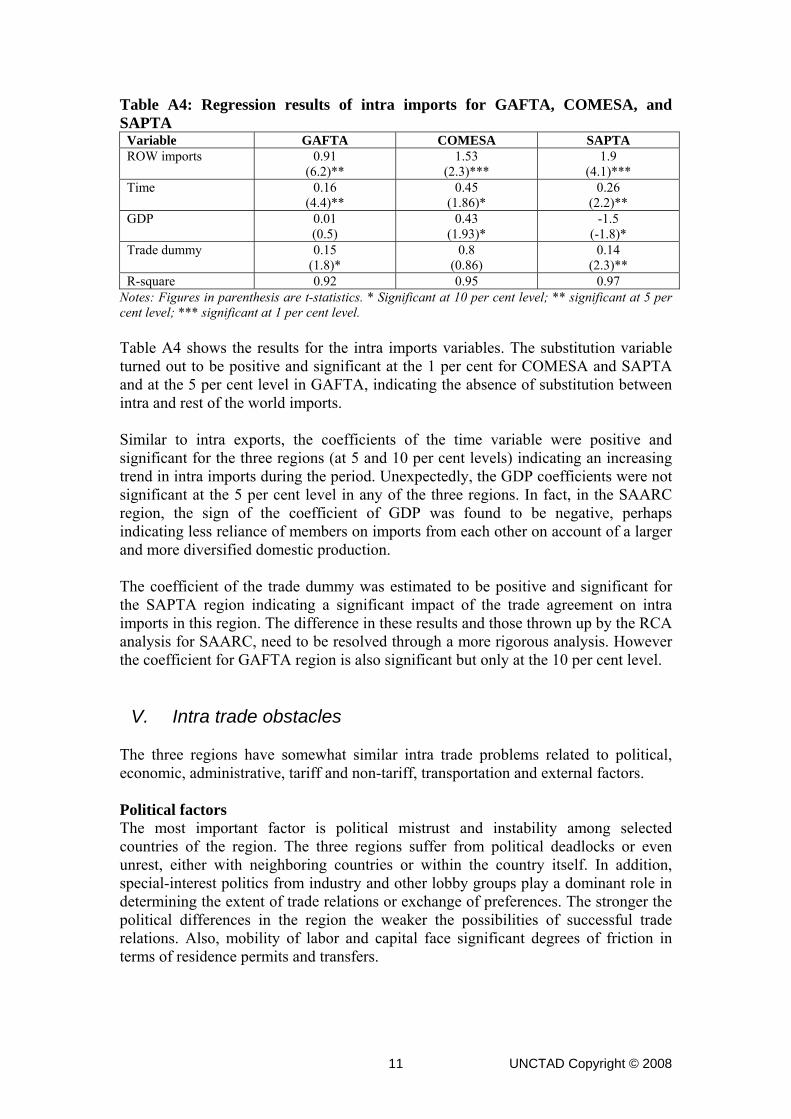

Table A4: Regression results of intra imports for GAFTA, COMESA, and SAPTA

Variable GAFTA COMESA SAPTA ROW imports 0.91

(6.2)** 1.53

(2.3)*** 1.9

(4.1)*** Time 0.16

(4.4)** 0.45

(1.86)* 0.26

(2.2)** GDP 0.01

(0.5) 0.43

(1.93)* -1.5

(-1.8)* Trade dummy 0.15

(1.8)* 0.8

(0.86) 0.14

(2.3)** R-square 0.92 0.95 0.97

Notes: Figures in parenthesis are t-statistics. * Significant at 10 per cent level; ** significant at 5 per cent level; *** significant at 1 per cent level. Table A4 shows the results for the intra imports variables. The substitution variable turned out to be positive and significant at the 1 per cent for COMESA and SAPTA and at the 5 per cent level in GAFTA, indicating the absence of substitution between intra and rest of the world imports. Similar to intra exports, the coefficients of the time variable were positive and significant for the three regions (at 5 and 10 per cent levels) indicating an increasing trend in intra imports during the period. Unexpectedly, the GDP coefficients were not significant at the 5 per cent level in any of the three regions. In fact, in the SAARC region, the sign of the coefficient of GDP was found to be negative, perhaps indicating less reliance of members on imports from each other on account of a larger and more diversified domestic production. The coefficient of the trade dummy was estimated to be positive and significant for the SAPTA region indicating a significant impact of the trade agreement on intra imports in this region. The difference in these results and those thrown up by the RCA analysis for SAARC, need to be resolved through a more rigorous analysis. However the coefficient for GAFTA region is also significant but only at the 10 per cent level.

V. Intra trade obstacles The three regions have somewhat similar intra trade problems related to political, economic, administrative, tariff and non-tariff, transportation and external factors. Political factors The most important factor is political mistrust and instability among selected countries of the region. The three regions suffer from political deadlocks or even unrest, either with neighboring countries or within the country itself. In addition, special-interest politics from industry and other lobby groups play a dominant role in determining the extent of trade relations or exchange of preferences. The stronger the political differences in the region the weaker the possibilities of successful trade relations. Also, mobility of labor and capital face significant degrees of friction in terms of residence permits and transfers.

UNCTAD Copyright © 2008 11

Economic factors The economic factors that impede intra trade in the three regions include economic structure and policies. The countries of the respective region may or may not have similar economic structures, but evidently, limited differences in product-wise comparative advantage and absence of complementarities. The products that are similar are mainly primary including fuels and fuel products, agricultural products and raw materials, and to some extent manufactured products. Also, with the exception of some countries such as India, most of the countries are characterized by a small market and insignificant demand levels compared to the world market. Many of the countries, except those oil-producing ones, suffer from heavy foreign debt burden, poverty, low productivity, unemployment, inflation and non-competitiveness. The economic policies that impede intra trade include monetary restrictions, exchange rate controls and financial restrictions on across-the-border goods in the form of fees, stamps, etc. Administrative and technical constraints The administrative restrictions include all forms of procedures that are attached to the border crossing of goods such as customs documents and verifications, transit facilities, handling and inspection. The technical constraints include the applications of standards and specifications, health and environmental conditions, certificate of origin and value added verification. Transportation The transportation of goods depends heavily on land transport which is characterized by high costs since it relies on heavy vehicles. Conflict resolution and information The degree of trade conflict resolution and availability of information varies across the regions but it is in any case not well developed.

VI. Conclusion Intra trade in the three regions covered by this study was of relatively small importance in comparison to total trade of the regions. It did not exceed 10 per cent during the study period. Intra trade showed a modestly growing trend in the three regions over the period under study. Trade patterns within each region showed a great degree of similarity as indicated by the revealed comparative advantage analysis. Intra trade is dominated by primary products in GAFTA and COMESA while manufactured goods were more prominent in SAPTA. Fuel is more prominent than other products in GAFTA compared to the other two regions. Manufactured goods' share in intra trade increased over the period of the study in GAFTA and COMESA. In all regions intra trade was characterized by a high level of geographical concentration, mainly among neighboring countries.

UNCTAD Copyright © 2008 12

The commodity and geographical concentration of intra trade in the regions was reflected in very similar RCAs. This suggests a very limited potential for expanding intra trade in the three regions. The results of the partial econometric analysis supported the above conclusion as the coefficient measures of the trade agreement effect turned out to be statistically insignificant in all three regions. Furthermore, the results showed absence of crowding-out effects between intra and total trade for all regions.

UNCTAD Copyright © 2008 13

B. REGIONAL TRADE INTEGRATION: THE CASE OF GAFTA

By Talib Awad and Amir Bakir

I. Introduction During the last five decades most nations of the world moved toward trade liberalization under the umbrella of the General Agreement on Trade and Tariffs (GATT) and its later successor the World Trade Organization (WTO). WTO's membership has been ever expanding, and now covers more than 188 countries of the world. During the 1960s and 1970s there were a number of countries (mainly developing countries) who adopted an inward-looking import substitution strategy which were largely unsuccessful. By the 1980s and 1990s, most nations shifted toward a strategy of outward-looking export-led growth and dismantled all forms of trade barriers. These trade liberalizing trends were also accompanied by movements of most nations toward engaging in some form of regional economic integration. Regional integration agreements, although partial and discriminatory in nature, were seen as a first step towards more general and comprehensive trade liberalization, and hence were encouraged by GATT/WTO. An exemption from the principle of most favored nation (MFN) was granted to any group of countries that got involved in any form of regional integration agreement (RIA). Since the mid-1980s there has been a dramatic increase in regional integration activity. Of the 194 RIAs notified to GATT/WTO at the beginning of 1999, 87 were notifications since 1990. Now almost all countries are members of at least one RIA, and more than one third of world trade takes place within such agreements. New developments include the expansion and deepening of the EU; the construction of new and more open RIAs between developing countries; and the advent of RIAs in which both high-income and developing countries are equal partners. The latter development is lead by the North American Free Trade Area (NAFTA) which, in 1994, extended the Canadian-USA free trade agreement to Mexico. The following section provides a brief theoretical economic background of RIAs. The rest of the chapter is divided as follows: section two provides a theoretical background for regional economic integration, section three covers previous regional trade integration efforts among Arab countries as well as the most recent agreement namely, the Great Arab Free Trade Area (GAFTA) , section four is devoted to the analysis of intra Arab trade, section five attempts to evaluate the impact of GAFTA on intra Arab trade, section six highlights obstacles to intra Arab trade, and conclusions and recommendations are presented in the last section.

UNCTAD Copyright © 2008 14

II. Overview: Theoretical background

II.1 Economic analysis of regional economic integration Regional integration agreements are groupings of countries formed with the objective of reducing barriers to trade between members. In theory, there are several types of regional economic integration schemes. The simplest is a free trade area (FTA) that eliminates tariffs on goods among the member countries, while leaving national tariffs against non-member countries unchanged. Beyond this there is a wide range of policy options open to countries considering integration, many of which turn on the `depth' of integration sought by member countries ranging from modest trade liberalization, through full economic integration, to the formation of shared institutions. In comparison to a free trade area, a customs union, in which a common external tariff is set, involves greater sharing of sovereignty and requires establishing procedures for revenue sharing, but in return can yield much greater market integration. In a free trade area where countries set different external tariffs the free internal circulation of goods is impossible; border formalities have to be maintained to ensure that external imports do not all enter through the member with the lowest external tariff, for re-export to other member countries. Since these imports include intermediate goods that are further processed in member countries, in practice this involves enforcing complicated `rules of origin' governing trade flows within the RIA. It is increasingly recognized that tariffs and quotas alone may be just a small part of the overall barriers to trade created by an international border. Rules of origin create restrictions, and so do measures such as anti-dumping rules, duplicative customs procedures, differing national product standards, and simple border red tape.

II.2 Economic effects on member countries When analyzing the economic effects of such agreements, economists usually distinguish between effects on member countries and on the world trading system. Effects on member countries include the benefits and costs of trade creation and trade diversion, as well as gains from increased scale and competition. `Deeper' integration can be pursued by going beyond abolition of import tariffs and quotas, to further measures to remove market segmentation and promote integration. Effects on the world trading system are not clear-cut. There is little evidence that regionalism has retarded multilateral liberalization, but neither is there support for the view that continuing expansion of regional agreements will obviate the need for multilateral liberalization efforts. Our analysis will focus on the first group of effects.

II.2.1 Trade creation and diversion The modern analysis of RIAs is mainly based on Viner's (1950) distinction between trade-creating and trade-diverting effects of RIAs. The classical source of gains from trade is that global free trade allows consumers and firms to purchase from the cheapest source of supply, hence ensuring that production is located according to comparative advantage. In contrast, trade barriers discriminate against foreign supply,

UNCTAD Copyright © 2008 15

inducing domestic import competing producers to expand even though they have higher costs than imports. This in turn starves domestic export sectors of resources and causes them to be smaller than they otherwise would be. Since a RIA liberalizes trade, reducing at least some of the barriers, doesn't it follow that it too will generate gains from trade? Viner's contribution was to show that the answer is "not necessarily". The gains-from-trade argument applies if all trade barriers are reduced, but need not apply to a partial and discriminatory reduction in barriers, as in a RIA. This is because discrimination between sources of supply is not eliminated, it is just shifted. If partner country production displaces higher cost domestic production then there will be gains from trade creation. But it is possible that partner country production may displace lower cost imports from the rest of the world, and this is welfare reducing trade diversion. The analysis of trade creation and trade diversion constitutes one of the first formal analyses of the more general problem of 'second-best welfare economics'. Given that distortions remain in place in some activities in the economy, it is not necessarily the case that removing just some of the distortions (e.g. eliminating trade barriers on partner countries and leaving them in place on external countries) is welfare enhancing. In the literature on regional integration the response to the fundamental ambiguity created by the second-best took three main forms. First, authors established circumstances under which there is no interaction between formation of the RIA and external trade flows, so no possibility of trade diversion. Meade (1955) pointed out that if trade barriers with non-members take the form of fixed quantitative restrictions, then a RIA must raise the total welfare of member countries since there is no possibility that imports from the rest of the world are displaced. Ohyama (1972) and Kemp and Wan (1976) showed how, when external trade barriers take the form of tariffs, it is possible to adjust these to hold external trade volumes constant, so preventing trade diversion from occurring. Second, researchers identified conditions, in terms of changes in endogenous variables, for welfare gain. For example, welfare increases if the initial tariff-weighted change in trade volume is positive (Meade 1955). If internal tariffs are close to zero, then reducing them to zero raises welfare if it increases tariff revenues earned on external trade (Ethier and Horn 1984). The third approach is to identify features of economies (in terms of their underlying exogenous characteristics) under which they are more or less likely to gain or lose from RIA membership. Lipsey (1957) argued that joining with countries that are already one's largest trading partners is unlikely to lead to diversion, since the fact that the countries were originally the largest trading partners suggests that they are the lowest cost source of supply. Similar reasoning, including transport costs in the costs of supply, leads to the 'natural trading bloc' argument (Wonnacott and Lutz 1989, Summers 1991). Venables (2000) shows that those members of an RIA with comparative advantage most different from the world average are most likely to lose from trade diversion, as their trade is diverted to partner countries with comparative costs between theirs and the world average.

UNCTAD Copyright © 2008 16

Empirical work on trade creation and trade diversion has taken two main forms; econometric studies of changes in trade flows, and simulation studies of the full general equilibrium effects of RIA membership. Econometric studies seek to quantify the changes in trade flows attributable to membership of a RIA, and thereby identify trade creation and diversion. A variety of different econometric models have been developed, the most common being based on the gravity model which estimates bilateral trade between countries as a function of their GDPs, populations, the distance between them, and physical factors such as sharing a land border, and being landlocked or an island. Dummy variables capture whether or not countries are in a particular RIA, their estimated effect indicating whether countries in a RIA trade more or less than would otherwise be expected. Using this technique, Bayoumi and Eichengreen (1997) found that the formation of the European Economic Community EEC reduced the annual growth of member trade with other industrial countries by 1.7 percentage points, with the major attenuation occurring over 1959-61, just as trade preferences were phased in. Soloaga and Winters (2001) looked at a wide range of RIAs, producing a mixed picture with little evidence of widespread trade diversion. Overall, there appears to be weak evidence that external trade is smaller than it otherwise might have been in at least some of the blocs that have been researched, but the picture is sufficiently mixed that it is not possible to conclude that trade diversion has been a major problem. Furthermore, it cannot be inferred that trade diversion has been economically damaging without information on relative costs and tariff structures, variables that are not revealed in this sort of aggregate exercise. The second empirical approach is based on computable equilibrium modeling. This involves construction of a full computer model of the economies under study which simulates the effects of the policy changes associated with the RIA. Such a model typically contains a great deal of microeconomic detail, so it can be used to predict changes in production in each sector, and changes in factor prices and real incomes. In models that assume a perfectly competitive environment, the combined effects of trade diversion and trade creation typically give very small welfare gains – just a fraction of 1 per cent of GDP (see Baldwin and Venables 1997 for a survey). The strength of these models is that they have sufficient microeconomic structure for the effects of a policy change to be traced out in detail, and its real income effects to be calculated. They are also often used for prediction to estimate the likely effects of a policy change before it is implemented. But they have the major weakness that they are not usually fitted to data as carefully, or subject to the same statistical testing, as econometric models. The cost of the microeconomic detail is a complexity that makes rigorous econometric estimation impossible. Although the focus of the trade creation and diversion literature has been on the changes in trade flows induced by regional integration, two consequent effects are important. The first is that changes in trade flows may change world prices, possibly improving the terms of trade of member countries, although this gain arises at the expense of outside countries. For example, if trade diversion occurs then RIA imports from outside countries are reduced, and any reduction in import prices that this causes is a terms of trade gain. Empirical work on this issue by Winters and Chang (2000) shows that Brazil's membership in Mercosur has been accompanied by a significant decline in the relative prices of imports from non-member countries.

UNCTAD Copyright © 2008 17

The second is that changes in tariffs and trade volumes will lead to loss of government tariff revenue. This can occur directly (as intra-RIA tariffs are cut) and as a consequence of trade diversion (as imports are diverted away from external, tariff inclusive, sources of supply). Its cost depends on the social cost of raising funds by alternative means, and can be severe in some developing countries. For example Cambodia derived 56 per cent of its total tax revenues from customs duties prior to its entry into the Association of South East Asian Nations (ASEAN), and Fukase and Martin (1999) argue that entry into ASEAN provided a powerful stimulus for the introduction of a value added tax. Finally, it is generally accepted that RIAs have a better chance of being net trade-creating if they meet certain basic criteria, including the following; (i) relatively high initial tariff barriers among potential members; (ii) geographic contiguity; (iii) broadly similar stages of overall economic development; but (iv) varied national production structures. According to these criteria, the Arab countries of the Middle East and North Africa should be good candidates for the formation of an effective RIA. In practice, this has not yet happened, despite a plethora of multilateral and bilateral agreements designed to reduce trade barriers.

II.2.2 Scale and competition effects A second mechanism through which member countries are affected by RIA membership derives from the fact that countries may be too small to support, separately, activities that are subject to large economies of scale. Regional cooperation offers a route to overcome the disadvantages of smallness, by pooling resources or combining markets. These scale benefits can arise in public projects (see World Bank 2000) and also at the level of the private firm, which typically interact in imperfectly competitive market structures. These considerations are absent from the trade creation and trade diversion approach outlined above, which is based on the perfect competition and constant returns to scale paradigm of traditional trade theory. It was only in the 1970s and 1980s that formal analysis of the interaction between trade, economies of scale and imperfect competition began with the 'new trade theory', and these techniques have now been applied extensively to regional integration. The basic argument is that there is a trade-off between the extent to which firms can achieve economies of scale, and the intensity of competition in the market. For a given size market, larger firms means fewer firms and hence more monopolistic outcomes. If regional integration combines markets, then it shifts this trade-off, potentially allowing firms to be bigger and markets to be more competitive (Smith and Venables 1988). For example, there might be an initial situation in which two economies each have two firms in a particular industry, and these firms exploit their 'duopoly' power, setting prices well above marginal cost. After formation of the RIA this becomes four firms in one combined RIA market. This increases the intensity of competition, and possibly induces merger (or bankruptcy), perhaps leaving only the three most efficient firms. The net effect is increased competition, increased firm scale, and lower costs. Oligopoly competition is likely to be more intense than the original duopolies, and surviving firms are larger and more efficient, so they can better exploit economies of

UNCTAD Copyright © 2008 18

scale. A further source of gains comes from possible reductions in internal inefficiencies that firms are induced to make. If the RIA increases the intensity of competition, it may induce firms to eliminate internal inefficiencies (X-inefficiency) and raise productivity. Since competition raises the probability of bankruptcy and hence layoffs, it also generates stronger incentives for workers to improve productivity, and increases labor turnover across firms within sectors.

II.3 Winners and losers Another concern accompany RIAs is about the distribution of its costs and benefits between member countries. Do central regions gain at the expense of peripheral ones, and do poor countries tend to catch up or get left behind? The evidence is, broadly speaking, that RIAs composed of developed countries tend to show convergence (for example the narrowing of per capita income differentials observed in the EU, see Ben- David 1993). However, the picture for RIAs composed of developing countries is more mixed, with some examples of divergent performance (World Bank 2000). The analytical literature on these questions is quite sparse, but provides several clues why this might occur. First, as mentioned above, trade diversion is more likely for countries with 'extreme' comparative advantage, suggesting that in a RIA amongst developing countries it might be the lowest income countries that experience diversion. For example, their imports of manufactures might be diverted from non-member countries to a partner that has a comparative advantage in manufactures within the RIA, but not relative to the world at large. Second, industries might tend to cluster in locations that have relatively good market access, or that are well supplied with business services or provision of other intermediate goods. This is more likely to occur in developing countries than in developed ones, partly because of their sparser provision of business infrastructure, and partly because the small size of their manufacturing sectors means that clustering is less likely to run into congestion and other sources of diminishing returns. The clustering may lead to wages being bid up in one member country at the expense of others.

III. Regional economic integration and the Great Arab Free Trade Area

III.1 Previous economic integration efforts

Soon after most Arab countries obtained their independence from British and French colonialism, efforts were initiated at the formal level to move toward both economic and political integration in the Arab region. As early as 1950, a Treaty for Joint Defense and Economic Cooperation was signed by Egypt, Jordan, Lebanon, Saudi Arabia, Syria and Yemen at the meeting of the Arab League's Economic Council. Its main economic objectives were tariff reduction and liberalization of capital and labor flows. It was followed up in 1953 by the Convention for Facilitating Trade and Regulating Transit, which aimed at eliminating barriers to trade in agricultural goods and minerals. Efforts to lower tariffs on manufactures were largely thwarted by Iraq, Saudi Arabia and Yemen, which relied heavily for revenue on import duties (Awad 1995).

UNCTAD Copyright © 2008 19

The next move towards integration, involving efforts to create an Arab Common Market, began in the late 1950s, when Egypt, Jordan, Morocco, Syria and Kuwait agreed in principle to unify economic policies and legislation. The five states ratified this proposal in 1964, but the intention of effectively abolishing duties and quantitative restrictions over a 10-year period was undermined by four rounds of negotiations on exemptions. Attempts to establish a common external tariff were finally abandoned in 1971. Another attempt to promote regional integration was the 1981 Arab League-sponsored Agreement for the Facilitation and Promotion of intra-Arab Trade. The agreement represented a declaration of intent to negotiate full exemption from tariffs and non-tariff restrictions for manufactured and semi-manufactured goods. As with previous agreements, the 1981 effort had little effect on formal trade liberalization or actual trade. It lacked binding commitment to its terms and a timetable for implementation, and featured a "positive list" approach, whereby specific products for liberalization must be listed (as opposed to the "negative list" approach, whereby liberalization covers all items other than those specifically listed for continuing protection). Meanwhile, subregional arrangements, such as the 1981 Gulf Cooperation Council - arguably the only effective Arab trade agreement to date, with its successful promotion of trade liberalization and free movement of capital and labor among member states - and the abortive 1989 Arab-Maghreb Union, along with a proliferation of strictly bilateral arrangements between trade partners have become a feature of the Arab scene. Bilateral treaties are now estimated to number more than 45. They typically comprise limited preferential arrangements, mostly confined to varying degrees of tariff exemptions for specific categories of agricultural goods and raw materials; their partial nature has had the net effect of hindering rather than stimulating wider inter-Arab trade (Hoekman 1995). While noble political aspirations helped to initiate successive integration efforts, less noble political frictions equally often helped subsequently to vitiate them. Lack of a forceful time table for practical implementation of such agreements, together with lack of coordination with the private sector, poor infrastructures, partiality in the nature of the agreements, differences in economic and political systems, spread of corruptions and red tape, and regional political instability were among the main factors behind the poor achievements of these early formal attempts.

III.2 The Greater Arab Free Trade Area In February 1997, the Arab League launched a free trade programme, known as the Greater Arab Free Trade Area, or GAFTA, in which member states were asked to come up with specific commitments regarding elimination of tariffs, non-tariff measures and rules of origin. The so called Executive Program was an effort to revive the 1981 Agreement for Facilitation and Promotion of Trade among the members. All the 22 member states of the Arab League, except Algeria, Djibouti, the Comoros Islands and Mauritania have endorsed the Agreement and have committed to the Executive Program.

UNCTAD Copyright © 2008 20

The programme calls for tariff reductions over a ten year period at a rate of 10 per cent per year, meaning that tariffs would be reduced to zero by 2007. In addition, the members agreed to bind their national tariff schedules as of December 31, 1997. By September 1999, 14 countries had applied tariff reduction schemes and fulfilled the tariff commitments. For the rest of the members who did not ratify the agreement, the bound tariffs will be applied at the time they notify the Arab League of their endorsement of the programme. Regarding liberalization of industrial products, members are allowed to draw up a list of exceptions from tariff reductions during the first years of the programme. The exceptions are intended to enable local industry to restructure and improve its competitiveness before having to face competition from other GAFTA countries' imports. In the area of agriculture, the programme offers members the opportunity to suspend tariff reductions on some produce during the peak harvest seasons. Each GAFTA country is allowed to submit ten produce items for suspension, with a total exemption for all the items of 45 months. So far, 10 GAFTA countries have submitted a list of 30 fruits and vegetables. Non-tariff barriers Although the programme calls for a schedule to reduce non-tariff barriers, at this point the GAFTA countries have not tackled these barriers. A committee on non-tariff barriers has agreed on a list of goods whose imports are prohibited for religious, health, environment and national security reasons, and the list is to be reviewed on a yearly basis. The committee is also supposed to sort out other goods submitted by members and start negotiations for their elimination. The programme calls for the application of international rules regarding subsidies, countervailing measures, safeguards and anti-dumping measures. This should be possible under WTO agreements. However the programme does not explicitly refer to the WTO agreements since some Arab countries are still seeking membership. GAFTA rules of origin The programme offers rules of origin for duty-free treatment. The GAFTA value added requirement is set at 40 per cent, and there are two methods for calculating origin. The first is based on the local value added approach. The other is the net cost approach, which subtracts specified imported expenses from the transaction price to determine the base for calculating the ratio of foreign to domestic content. An important feature of the programme is the ongoing scheme for the elaboration of detailed preferential rules of origin for GAFTA-made products. This scheme adopted rules for full commutation of origin among the GAFTA countries. This means that materials obtained from, for example, Jordan, and incorporated into a product made in Egypt, may be considered as if they were obtained in Egypt. Finally, the programme also calls for the need for harmonization of preferential rules of origin to comply with the Euro-Mediterranean free trade agreements underway.

UNCTAD Copyright © 2008 21

Monitoring GAFTA implementation GAFTA is managed by the Council of Ministers of Member Countries and by a permanent executive body. So far, GAFTA has a functioning Secretariat that comes under the Economics Department of the Arab League Secretariat. The programme also calls for the chambers of industry and commerce in Arab countries to monitor implementation. The involvement of the private sector is expected to enhance the transparency of the members' trade practices. GAFTA achievements prospective The GAFTA programme calls for across-the-board tariff reduction offering the advantage of transparency and ensuring that high tariffs are reduced faster than lower tariffs. However, the extent to which this approach will boost intra-regional trade flows depends on the magnitude of tariff dispersion as well as the effective rate of protection across industries in various countries. Tariff structures among the members are uneven. Low-tariff countries, namely the Gulf countries (Bahrain, Kuwait, Qatar, Oman, Saudi Arabia and the United Arab Emirates) have simple average tariffs of four to 12 per cent, while countries such Egypt, Jordan, Morocco, Syria and Tunisia have tariffs of 40 to 100 per cent. Tariffs reach 235 per cent in Syria. In addition, tariff escalation exists in many countries, particularly in textiles, clothing, leather and basic metal industries where average tariffs on finished products are multiples of the lower tariff levels on raw materials. An across-the-board tariff reduction could have a significant effect on trade creation. However, the most serious shortcomings of the programme are loopholes allowing the exclusion of certain industrial agricultural products from tariff reduction. The list of exceptions already submitted includes consumer goods competing with domestic production (e.g. textiles, clothing and leather articles). Moreover, the transition period for the excluded industrial products would allow for pressures from interest groups to resist market opening at all. The exclusion of certain agricultural products during the crop/harvest seasons for the full transitory period of ten years would also substantially limit the trade creation effect. The use of quotas has been declining in GAFTA countries partly as a result of unilateral trade reforms implemented by countries such as Morocco, Tunisia, Egypt and Jordan. In these countries, non-tariff barriers take the form of import licensing for safety and health standards. In the Gulf Cooperation Council (GCC) countries, non-tariff barriers are relatively low. However, Syria still imposes an import license requirement on virtually all imports. Customs and administrative procedures associated with importing are still important trade barriers within the region. The programme calls for some harmonization related to customs clearance procedures, but it does not address harmonization of other major regulations regarding product standards, testing and certification procedures, and environmental standards. Transportation is also a problem. The members signed an earlier agreement to simplify the transit of goods and persons, but there has been no legal enforcement for the implementation of this agreement, and there are periodic reports citing barriers to cross-border trade such as closure of roads, delays and cumbersome cross-border regulations such as no driving on weekends or the refusal of visas professional drivers of certain nationalities.

UNCTAD Copyright © 2008 22

At first, the commutating of rules of origin for products made in GAFTA countries may help create backward and forward linkages between the member countries and increase the potential for trade. However the further extension of commutation of the Euro-Mediterranean Agreements and the GAFTA countries would be even more beneficial to Member Countries and would also help reduce the emerging hub-and-spoke nature of the Euro-Mediterranean Agreements. Deepening integration of GAFTA So far, GAFTA has been limited to regional liberalization of merchandise trade. This effort at regional integration alone is not sufficient to ensure a more credible path for further domestic market efficiency allowing GAFTA member countries to face greater competitiveness from world exporters. There is a need to extend regional liberalization to the areas of trade in services and labor. Linking GAFTA with the Euro-Mediterranean trade areas through incorporation of binding rules and various policy harmonization that are included in the Euro-Mediterranean Agreements would enhance market efficiency, allowing GAFTA countries to face greater competition from emerging world exporters in Asia and Eastern Europe. The absence of provisions for free movement of services and the right of establishment in GAFTA reduces the benefits of the agreement, given that services trade is generally complementary to merchandise trade. Barriers to trade in services in GAFTA countries are clearly important. A regional agreement which allows free entry into services activities should help domestic services companies to expand to regional markets before venturing into the more competitive world markets. Liberalization of transportation services should lie at the heart of intra-regional efforts to facilitate merchandise trade. Maritime transport remains by far the principal means of intra-regional transport of goods and a regional agreement on common shipping policy principles is needed. Land transportation services are an important cross-border mode of passenger and freight transport in the GAFTA countries. However, the regulatory regime for road transport is highly restrictive in the GAFTA countries. For instance, cross border freight transport returning with cargo is not allowed by most of the GAFTA countries. Internal coasting trade is also not allowed in virtually all the GAFTA countries. A regional agreement regarding land transport is needed. Financial services There is also the need to harmonization some of the banking and insurance regulations as well as a provide for the right of establishment with countries in the region. There is relatively little integration among the financial institutions in the GAFTA countries, although it is more significant in banking activities. Egypt, being the most advanced in liberalizing the financial sector among the reforming MENA (Middle East and North Africa) countries, has discretionary procedures for allowing new entry in this sector. Since domestic financial institutions in most of the GAFTA countries have comparable high operating costs and comparable technology, the real efficiency gains would come from integrating domestic financial markets into the world financial markets in order to facilitate capital and technological flows into the region. For many GAFTA countries, labor services are the mainstay of their service exports. From the viewpoint of efficiency, free movement of skilled labor enhances the

UNCTAD Copyright © 2008 23

efficiency of production. Cooperation among GAFTA countries to promote professional/technical labor mobility is desirable. Some important measures for freer mobility of professional and skilled labor in the context of GAFTA include recognition of professional certification standards, visa and work permit practices and measures allowing the temporary movement of corporate personnel, engineers, architects, accountants, lawyers and computer programmers. Political and economic considerations dictate that integration at the bilateral, regional, inter-regional and multilateral levels needs to proceed in a systematic way on parallel tracks. Hopefully, building closer commercial ties in the region can play a role in supporting political initiatives to reactivate the peace process. Economically, the emergence of an integrated market in the region may yield advantages that substantially exceed the current dimension of intra-regional trade. This paper's final objective is to provide an objective evaluation of the potential success of GAFTA in expanding intra-Arab trade (IAT). But first it is necessary to review the trend and main characteristics of Arab countries' trade.

IV. Trend and characteristics of intra-Arab trade

IV.1 Growth of intra-Arab trade Trade in the region has witnessed reasonable growth during the period 1980-2005; it grew at an annual rate of 2 per cent. The growth rates of total exports and imports reached 1.8 per cent and 2.3 per cent, respectively. Similarly but more outstandingly, IAT grew by 5.9 per cent. However, the percentage of IAT in total trade did not exceed 10 per cent. The percentage of intra exports in total exports has been rising over the period while the percentage of intra imports in total imports has been declining since 1990 to reach 8 per cent in 2005, as shown in Figure B1. Figure B1: Intra Arab Trade, 1980-2005

0%

2%

4%

6%

8%

10%

12%

14%

1980 1985 1990 1995 2000 2005

Exports

Imports

Source: Calculated based on data taken from the Arab Monetary Fund website (www.amf.org.ae). It is interesting to note that intra trade growth rates are higher during the period 1998-2004 compared to the period 1980-1997. This might suggest that the GAFTA

UNCTAD Copyright © 2008 24

agreement had a significant role in enhancing intra trade, as shown in Table B1 below. Table B1: Growth rates of intra trade during the period 1980-2004

1980-1997 1998-2004 1980-2004 Intra exports 3.5 14.7 5.7 Intra imports 3.5 12.6 6.0 Intra trade 3.5 13.7 5.9

Source: Calculated using exponential growth formula based on data taken from the Arab Monetary Fund website (www.amf.org.ae). Indeed, as shown in Table B2 individual countries trade growth rates vary significantly among themselves. For example, Syrian and Egyptian intra exports grew by 10.2 per cent and 9.7 per cent respectively, while the corresponding growth rates for Morocco and Jordan did not exceed 4 per cent. Similarly, Egyptian intra imports grew by 9.6 per cent while that of Saudi Arabia was less than 2 per cent, as shown in Table B2. Table B2: Intra-Arab trade growth rates for selected countries (per cent)

Country Intra exports Intra imports Jordan 4 5.1 Syria 10.2 2.6 Egypt 9.7 9.6 Morocco 2.9 6.2 Saudi Arabia 7.2 1.3 United Arab Emirates 8.7 8.1

Source: Calculated by the researchers using the exponential growth formula for the period 1980-2004. Data are taken from the Arab Monetary Fund, Annual Statistical Book, several issues.

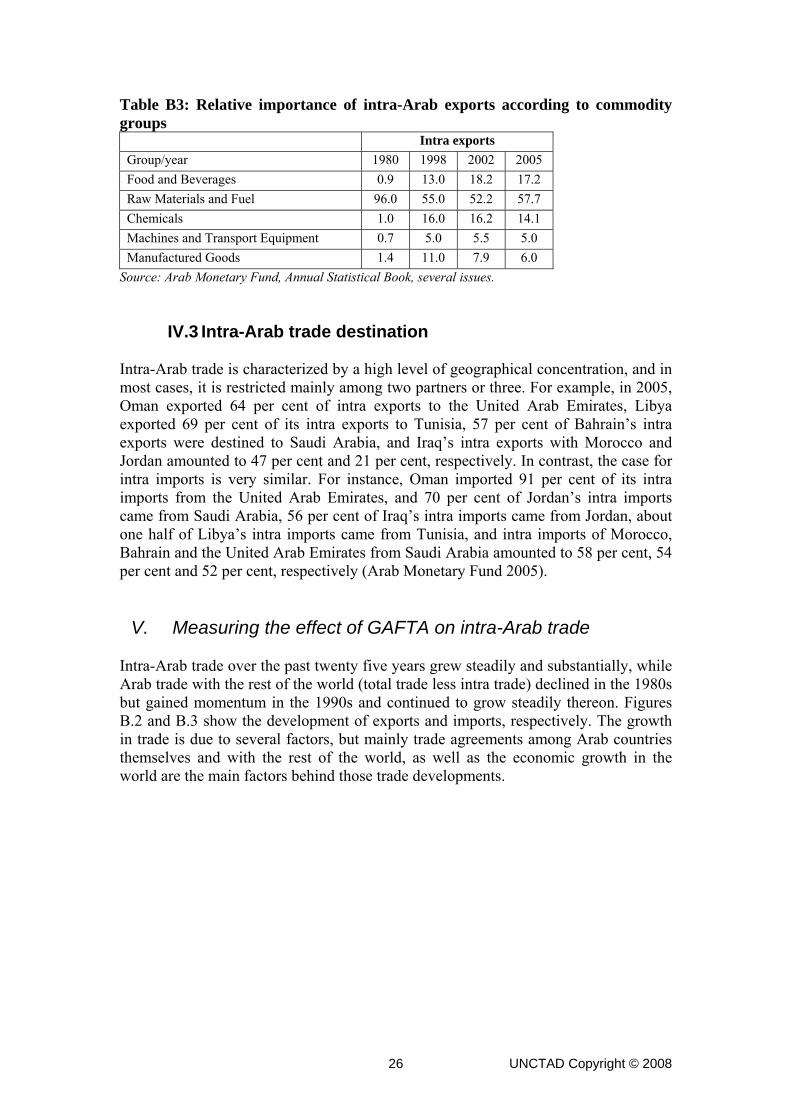

IV.2 Intra-Arab trade commodity structure The analysis of commodity groups uses the SITC classification and for this purpose the following commodity groups were chosen: Food and Beverages, Raw Materials and Fuel, Chemicals, Machines and Transport Equipment, and Manufactured Goods (Table B3). Fuel and raw materials share in intra trade exceeds 50 per cent, followed by food and beverages with a share of 17 per cent, then chemicals with a share of 14 per cent-15 per cent, followed by manufactured goods with a share of 8 per cent-9 per cent, and finally machines and transport equipment with a share of 5 per cent-6 per cent. Over the period under investigation in this study, the development of the relative importance of the above mentioned commodity groups, as shown in Table B3, reveals that food and beverages and manufactured goods have realized a dramatic gain in relative importance on the expense of raw materials and fuel.

UNCTAD Copyright © 2008 25

Table B3: Relative importance of intra-Arab exports according to commodity groups

Intra exports Group/year 1980 1998 2002 2005 Food and Beverages 0.9 13.0 18.2 17.2 Raw Materials and Fuel 96.0 55.0 52.2 57.7 Chemicals 1.0 16.0 16.2 14.1 Machines and Transport Equipment 0.7 5.0 5.5 5.0 Manufactured Goods 1.4 11.0 7.9 6.0

Source: Arab Monetary Fund, Annual Statistical Book, several issues.

IV.3 Intra-Arab trade destination Intra-Arab trade is characterized by a high level of geographical concentration, and in most cases, it is restricted mainly among two partners or three. For example, in 2005, Oman exported 64 per cent of intra exports to the United Arab Emirates, Libya exported 69 per cent of its intra exports to Tunisia, 57 per cent of Bahrain’s intra exports were destined to Saudi Arabia, and Iraq’s intra exports with Morocco and Jordan amounted to 47 per cent and 21 per cent, respectively. In contrast, the case for intra imports is very similar. For instance, Oman imported 91 per cent of its intra imports from the United Arab Emirates, and 70 per cent of Jordan’s intra imports came from Saudi Arabia, 56 per cent of Iraq’s intra imports came from Jordan, about one half of Libya’s intra imports came from Tunisia, and intra imports of Morocco, Bahrain and the United Arab Emirates from Saudi Arabia amounted to 58 per cent, 54 per cent and 52 per cent, respectively (Arab Monetary Fund 2005).

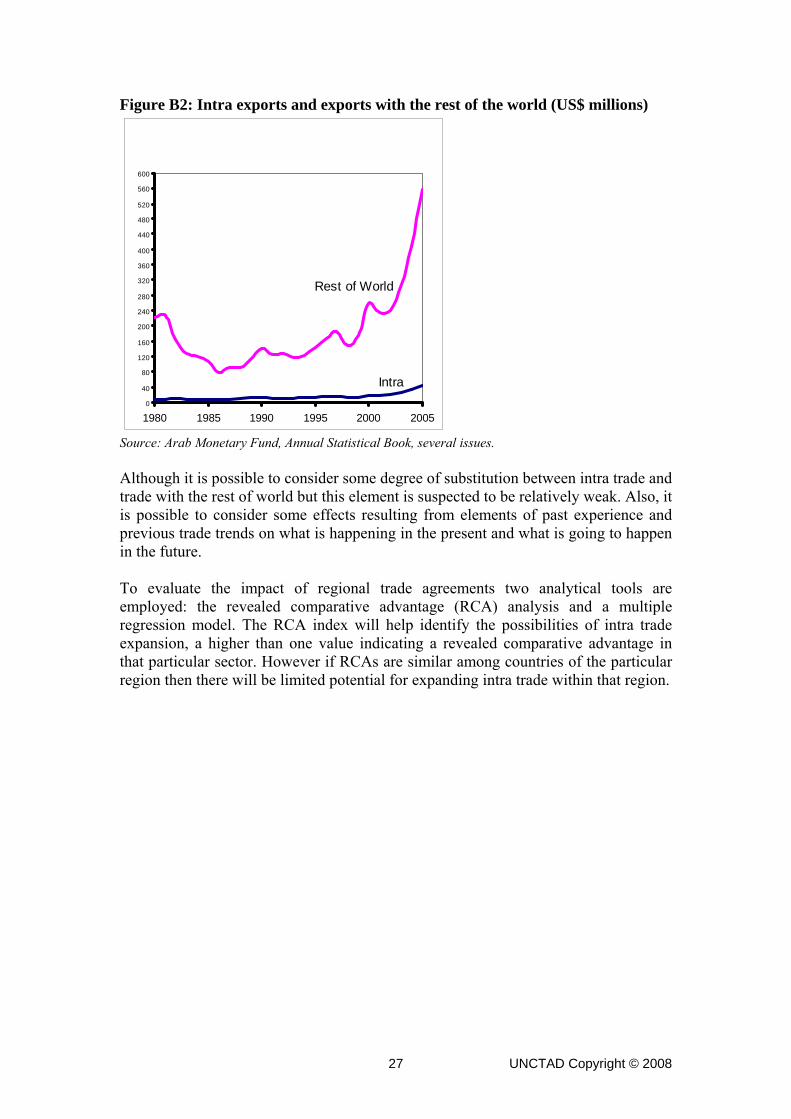

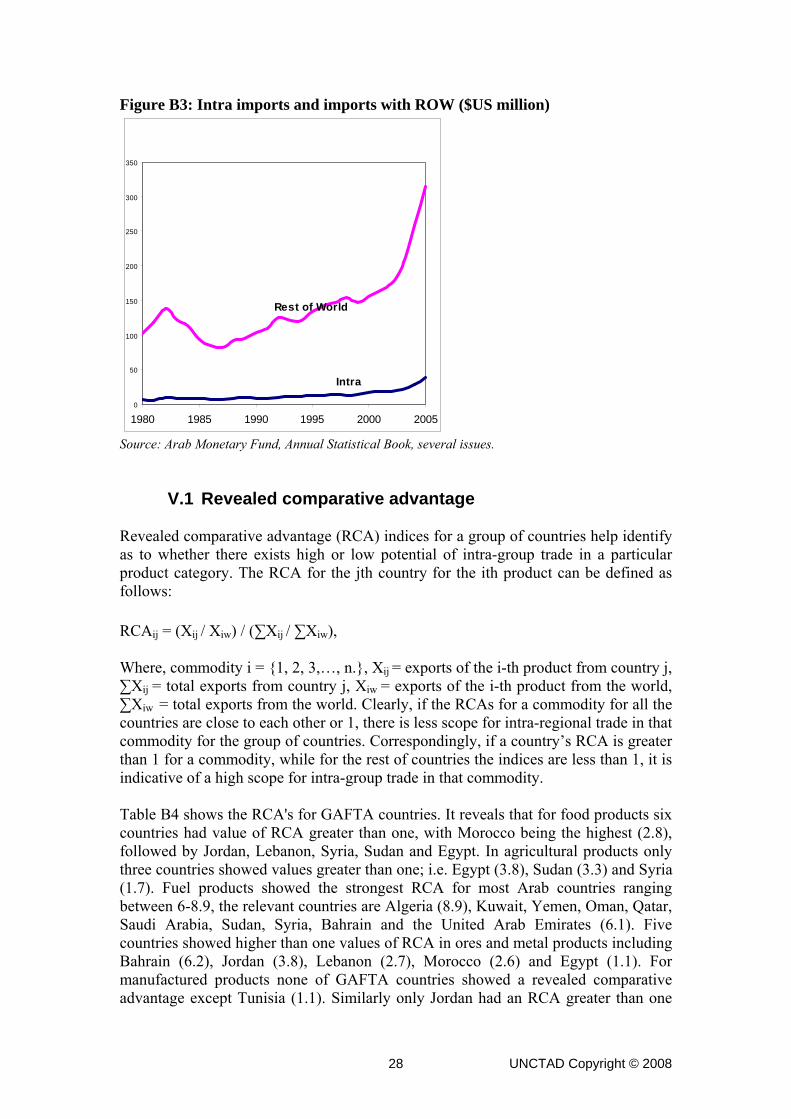

V. Measuring the effect of GAFTA on intra-Arab trade Intra-Arab trade over the past twenty five years grew steadily and substantially, while Arab trade with the rest of the world (total trade less intra trade) declined in the 1980s but gained momentum in the 1990s and continued to grow steadily thereon. Figures B.2 and B.3 show the development of exports and imports, respectively. The growth in trade is due to several factors, but mainly trade agreements among Arab countries themselves and with the rest of the world, as well as the economic growth in the world are the main factors behind those trade developments.

UNCTAD Copyright © 2008 26

Figure B2: Intra exports and exports with the rest of the world (US$ millions)

0

40

80

120

160

200

240

280

320

360

400

440

480

520

560

600

1980 1985 1990 1995 2000 2005

Intra

Rest of World

Source: Arab Monetary Fund, Annual Statistical Book, several issues. Although it is possible to consider some degree of substitution between intra trade and trade with the rest of world but this element is suspected to be relatively weak. Also, it is possible to consider some effects resulting from elements of past experience and previous trade trends on what is happening in the present and what is going to happen in the future. To evaluate the impact of regional trade agreements two analytical tools are employed: the revealed comparative advantage (RCA) analysis and a multiple regression model. The RCA index will help identify the possibilities of intra trade expansion, a higher than one value indicating a revealed comparative advantage in that particular sector. However if RCAs are similar among countries of the particular region then there will be limited potential for expanding intra trade within that region.

UNCTAD Copyright © 2008 27

Figure B3: Intra imports and imports with ROW ($US million)

0

50

100

150

200

250

300

350

1980 1985 1990 1995 2000 2005

Rest of World

Intra

Source: Arab Monetary Fund, Annual Statistical Book, several issues.

V.1 Revealed comparative advantage Revealed comparative advantage (RCA) indices for a group of countries help identify as to whether there exists high or low potential of intra-group trade in a particular product category. The RCA for the jth country for the ith product can be defined as follows: RCAij = (Xij / Xiw) / (∑Xij / ∑Xiw), Where, commodity i = {1, 2, 3,…, n.}, Xij = exports of the i-th product from country j, ∑Xij = total exports from country j, Xiw = exports of the i-th product from the world, ∑Xiw = total exports from the world. Clearly, if the RCAs for a commodity for all the countries are close to each other or 1, there is less scope for intra-regional trade in that commodity for the group of countries. Correspondingly, if a country’s RCA is greater than 1 for a commodity, while for the rest of countries the indices are less than 1, it is indicative of a high scope for intra-group trade in that commodity. Table B4 shows the RCA's for GAFTA countries. It reveals that for food products six countries had value of RCA greater than one, with Morocco being the highest (2.8), followed by Jordan, Lebanon, Syria, Sudan and Egypt. In agricultural products only three countries showed values greater than one; i.e. Egypt (3.8), Sudan (3.3) and Syria (1.7). Fuel products showed the strongest RCA for most Arab countries ranging between 6-8.9, the relevant countries are Algeria (8.9), Kuwait, Yemen, Oman, Qatar, Saudi Arabia, Sudan, Syria, Bahrain and the United Arab Emirates (6.1). Five countries showed higher than one values of RCA in ores and metal products including Bahrain (6.2), Jordan (3.8), Lebanon (2.7), Morocco (2.6) and Egypt (1.1). For manufactured products none of GAFTA countries showed a revealed comparative advantage except Tunisia (1.1). Similarly only Jordan had an RCA greater than one

UNCTAD Copyright © 2008 28

(1.8) for chemicals. For machinery and transport products no country in the region showed a relative comparative advantage. Based on the above RCA analysis it can be concluded that the GAFTA countries showed a high concentration in revealed comparative advantage in primary goods, mainly fuel and ores and metals, with almost negligible advantages in the other products. This implies a very limited potential for expanding intra trade in the region. Table B4: RCA indices for GAFTA countries by broad commodity groups (2003, 2004)

Country Total Food Agriculture Fuel

Ores &

Metal Manufactured

Goods Chemical

Machinery &

Transport Algeria 0.0 0.0 8.9 0.1 0.0 0.1 0.0 Bahrain 0.1 0.1 7.1 6.2 0.2 0.3 0.1 Egypt 1.2 3.8 4.3 1.1 0.4 0.7 0.0 Jordan 2.1 0.2 0.1 3.8 1.0 1.8 0.3 Lebanon 2.0 0.8 0.0 2.7 0.7 0.8 0.3 Morocco 2.8 1.0 0.3 2.6 0.9 1.0 0.4 Oman 0.7 0.0 8.0 0.3 0.2 0.1 0.2 Qatar 0.0 0.0 7.9 0.0 0.2 0.9 0.0 Saudi Arabia 0.1 0.1 8.0 0.1 0.2 0.9 0.0 Sudan 1.4 3.3 7.9 0.1 0.0 0.0 0.0 Syria 1.9 1.7 7.1 0.3 0.1 0.1 0.0 Tunisia 1.0 0.5 0.9 0.6 1.1 0.9 0.4 UAE 0.5 0.1 6.1 1.0 0.4 0.3 0.0 Yemen 0.7 0.2 8.4 0.1 0.0 0.0 0.0 Kuwait 0.0 0.1 8.5 0.2 0.1 0.4 0.0

Source: Calculated based on data from UNCTAD Handbook of Statistics 2005. Calculations are based on either 2003 or 2004 depending upon data availability.

V.2 Partial regression analysis As GAFTA became effective starting 1 January 1998 and data on intra trade at the time of writing is only available up to 2004, it is not possible to perform a subset regression analysis for the two periods: before and after the agreement. Hence, a multiple regression model is fitted for the whole sample. The effect of GAFTA on intra trade is simply introduced using a “Dummy” variable that takes the value of zero in the absence of the effect of the agreement, and one when the agreement was effective (1998-2004). Two models were fitted: the first represents intra exports and the latter represents intra imports. For the purpose of identifying the substitution effect between intra trade and trade with the rest of the world (ROW), exports with ROW was introduced as a an explanatory variable in the first model, and imports from ROW was introduced as an explanatory variable in the second model. These two variables can serve the purpose of capturing the effects of trade agreements other than intra trade agreements. GDP was introduced as an extra explanatory variable to capture the economic size effect of the region. In addition, a time trend was introduced with the purpose of capturing the growth trend in intra trade that may be attributed to other than GAFTA factors. Hence the two models to be estimated take the following form:

UNCTAD Copyright © 2008 29

143210 uGaftadBTimeBGDPBNetxBBIntrax +++++= (1)

243210 uGaftadCTimeCGDPCNetmCCIntram +++++= (2)

Where: Intrax = intra exports, Netx = exports with the rest of the world, GDP = Gross domestic product, Gaftad = Dummy variable takes the value one for the period 1998-2004, and zero otherwise, Time is a simple time trend, Intram is intra imports, Netm refers to imports with the rest of the world, and u1 and u2 are white disturbance terms. BBi and Ci are unknown parameters to be estimated. For the purpose of data stationarity and to obtain the long run elasticity directly the log-linear form is chosen. The results of applying ordinary least squares (OLS) on the available sample (1980-2004) are shown in Table B5. Table B5: Estimation results for intra exports and intra imports in logarithm form

Parameters Estimate t-statistics constant 3.5 1.25 lnetx 0.44 4.3** lgdp -0.007 -.27 ltime 0.29 5.35** gaftad -0.04 -0.48 R-square 0.84 constant -1.77 -1.02 lnetm 0.91 6.2** lgdp 0.01 0.5 ltime 0.16 4.4** gaftad 0.15 1.82*** R-square 0.92