reliability of mnscu financial data - minnstate.edu

TRANSCRIPT

O F F I C E O F I N T E R N A L A U D I T I N G

M i n n e s o t a S t a t e C o l l e g e s a n d U n i v e r s i t i e s

FI

NA

L

RE

PO

RT

Reliability of MnSCU Financial Data

Public Release Date: May 19, 1999

Reliability of MnSCU Financial Data

For more information, additional copies or alternative formats, such as largeprint, Braille, or audio tape, call 651/296-3471.

MnSCU Office of Internal Auditing500 World Trade Center, 30 E. 7th Street, Saint Paul, MN 55101 • 651/296-3471

Public Copy Release Date: May 19, 1999

O F F I C E O F I N T E R N A L A U D I T I N G

500 Wor ld Trade Center • 30 East Seventh St reet • Sa int Pau l , MN 55101Phone 651-296-3471 • Fax 651-296-8488

Honorable Andrew Boss, ChairMnSCU Audit Committee

Members of the MnSCU Board of Trustees

Chancellor Morris Anderson

MnSCU Presidents

The MnSCU Board of Trustees have often expressed a strong interest in obtaining audited financial state-ments for the organization. Their interest has come amidst ongoing questions about the reliability of theunderlying data recorded in the MnSCU financial systems. In the first two years after the merger, financialaudits issued by the Office of the Legislative Auditor raised questions about college and university financialpractices and the integrity of MnSCU financial data. By fiscal year 1998, many observers believed, how-ever, that the quality of the financial data had improved significantly. Accordingly, in June 1998, the MnSCUAudit Committee directed my office to conduct this audit of the Reliability of MnSCU Financial Data.

We conducted the audit in compliance with the Institute of Internal Auditors: Standards for Profes-sional Practice of Internal Auditing and the Information Systems Audit and Control Association:Standards for Information Systems Auditing.

To prepare the report, we interviewed representatives from the 36 MnSCU colleges and universities andsystem office representatives responsible for finance, budgeting, and information technology services. Wealso conducted extensive detailed testing of financial transactions for fiscal year 1998 and reviewed thestatus of cash reconciliations as of December 1998.

Ms. Melissa Primus was responsible for the lead work on this project, including the design of interviewquestionnaires and testing. Other Internal Auditing employees, as identified on page i, have also contributedsignificantly to this project.

Sincerely,

/s/ John Asmusen

John Asmussen, CPA, CIA, CISAExecutive DirectorMnSCU Office of Internal Auditing

End of Fieldwork: April 9, 1999Public Release Date: May 19, 1999

Table of Contents

Report Section Pages

Audit Participation ................................................................................................................i

MnSCU Review & Response ...............................................................................................ii

Executive Summary...............................................................................................................iii

Chapter 1 – Introduction and Background ............................................................................1

Chapter 2 – System Design and Functionality .....................................................................5

Chapter 3 – Financial Data Integrity ....................................................................................15

Chapter 4 – Financial Data Consistency ...............................................................................25

Chapter 5 – Business Practices .............................................................................................29

Chapter 6 – Reporting ...........................................................................................................37

Appendix A: MnSCU Office of Internal Auditing Audit Project Proposal ..........................41

i

Audit Participation

The following representatives of the MnSCU Office of Internal Auditing contributedsignificantly to the completion of this project:

Executive Director: John Asmussen, CPA, CIA, CISA

Deputy Director: Beth Hammer Buse, CPA, CISA

Lead Auditor: Melissa Primus, CPARegional Audit CoordinatorCentral Minnesota

Tami Billing, CPARegional Audit CoordinatorNorthwest Minnesota

Marilyn Hansmann, CPA, CIARegional Audit CoordinatorSoutheast Minnesota

Janet Knox, CPA, CISARegional Audit CoordinatorMinneapolis Area

Kim McLaughlin, CPARegional Audit CoordinatorNortheast Minnesota

Paul Portz, CPA, MBA, CMARegional Audit CoordinatorSaint Paul Area

Eric Okpala, CPA, MBAPrincipal Auditor

Administrative Nancy HoglundSupport: Executive I

ii

MnSCU Review & Response

A draft of the executive summary, chapter conclusions, findings and recommendations wasreviewed and discussed with the following members of the system office onFriday, May 7, 1999.

Linda BaerSenior Vice Chancellor for Academic and Student Affairs

Laura KingVice Chancellor – Chief Financial Officer

Leslie MercerAssociate Vice Chancellor – Policy and Planning

Bill TschidaVice Chancellor – Human Resources

A complete draft was provided to the aforementioned persons on Tuesday, May 11, 1999.

Based on their review, the draft was modified to improve its clarity and accuracy. The finalconclusions and recommendations represent the professional judgement of the MnSCU Officeof Internal Auditing. The persons reviewing the draft indicated their general agreement with thereports overall conclusions and recommendations.

iii

Executive Summary May 1999

Overall Conclusion

The creation of the MnSCU financial systems consolidated several methods of accounting forfinancial activity into one common framework. The development of all-inclusive financialdatabases was a major accomplishment for the organization. Previously financial data wasmaintained on several different systems and maintained in a piecemeal fashion. The MnSCUsystems provide the foundation for analyzing system-wide financial data.

The MnSCU financial systems, though, are complicated and not well understood by users. Thesystems are not user friendly and have caused administrative inefficiencies. Because the coreaccounting and human resources systems have existed for nearly four years, users have beenable to adapt to their shortcomings and make them work for basic daily operational tasks. Thesystems produce reasonable results for supporting daily operational tasks, such as receipting anddisbursing. Additional efforts are needed, however, to produce complete information onfinancial condition.

The system office is aware of problems with the current financial systems. It has given a highpriority to solving critical operational concerns, such as reconciling bank accounts. It also hasestablished several study groups to ensure consistent data classifications in the future,particularly for use with the new allocation model.

There are additional areas where we recommend further improvements. Opportunities tosimplify the systems must be explored, user support must be improved, and training and up-to-date manuals need to be developed. Additional guidance and emphasis is needed to ensure thatcolleges and universities code occurrence dates properly, record transactions timely, andmaintain adequate supporting documentation for sensitive transactions. In order for the systemsto produce complete balance sheet information, additional routines and procedures must bedeveloped and implemented on a regular, disciplined basis.

Users often find standard system reports to be confusing and difficult to understand. As a result,many users produce their own reports off-line using spreadsheet applications. Rather thanconcentrate on improving the system’s reporting features, the system office has been trainingusers in database query tools.

To improve system efficiencies significantly and provide adequate reporting functionality forusers will be costly and time consuming. Therefore, the MnSCU information technologygovernance structure must explore other alternatives before making a major investment inpatching the current systems.

Executive Summary Continued May 1999

iv

This page left blank intentionally.

1

Chapter 1 – Introduction and Background May 1999

Scope and Objectives

The primary purpose of this report was toanalyze financial accounting data todetermine if it is complete, accurate, timely,and consistent.

Appendix A shows the full project proposalpresented to the Audit Committee onJune 17, 1998.

We completed our review by conductinginterviews with administrative staff at thesystem office and all 36 colleges anduniversities. In addition, we haddiscussions with information technologyservice (ITS) division staff on the input andprocessing controls within the primaryfinancial applications. We also completed acomprehensive review of the payrollprocess. Finally, we completed detailtransaction testing to analyze financialaccounting data primarily for fiscal year1998.

During March 1999, the Office of theLegislative Auditor (OLA) began theplanning stages of an application audit ofthe new Minnesota State Colleges andUniversities (MnSCU) Accounts Receivablesystem. We did not focus our review onthis system due to the work beingcompleted by the OLA. We anticipate areport from the OLA on the AccountsReceivable system in the fall of 1999.

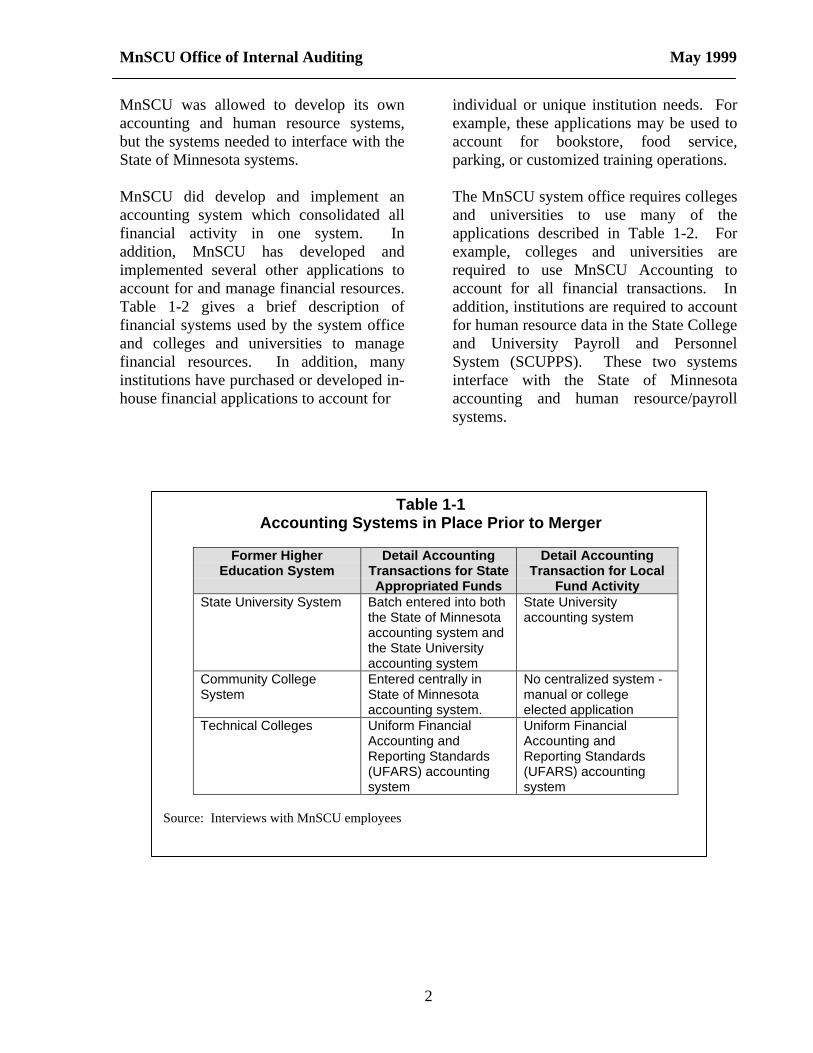

Financial System Background

Prior to the MnSCU merger, each highereducation system had a different method foraccounting for financial transactions.Table 1-1 documents where each systemaccounted for detailed accountingtransactions. The community colleges andstate universities directly entered detailtransactions in the State of Minnesotasystems for state funded activities.However, the technical colleges were notrequired to use the State of Minnesotasystems and accounted for all accountingtransactions on the Uniform FinancialAccounting and Reporting (UFARS)Standards system. This system is used toaccount for school district financial activityand is maintained by the MinnesotaDepartment of Children, Family, andLearning. Table 1-1 also shows that thecommunity college system did notconsolidate financial information foractivities outside the state treasury.

When planning for the merger, MnSCUadministration wanted a solution that wouldconsolidate the multiple systems describedin Table 1-1. MnSCU preferred to developfinancial systems that were independentfrom the State of Minnesota systems due tothe unique requirements of highereducation. On the other hand, the State ofMinnesota felt MnSCU should account forfinancial activity on the state’s centralizedsystems like other state agencies. Meetingswere held between MnSCU and stateagency heads to develop a solution. In theend, a compromise solution was made.

MnSCU Office of Internal Auditing May 1999

2

MnSCU was allowed to develop its ownaccounting and human resource systems,but the systems needed to interface with theState of Minnesota systems.

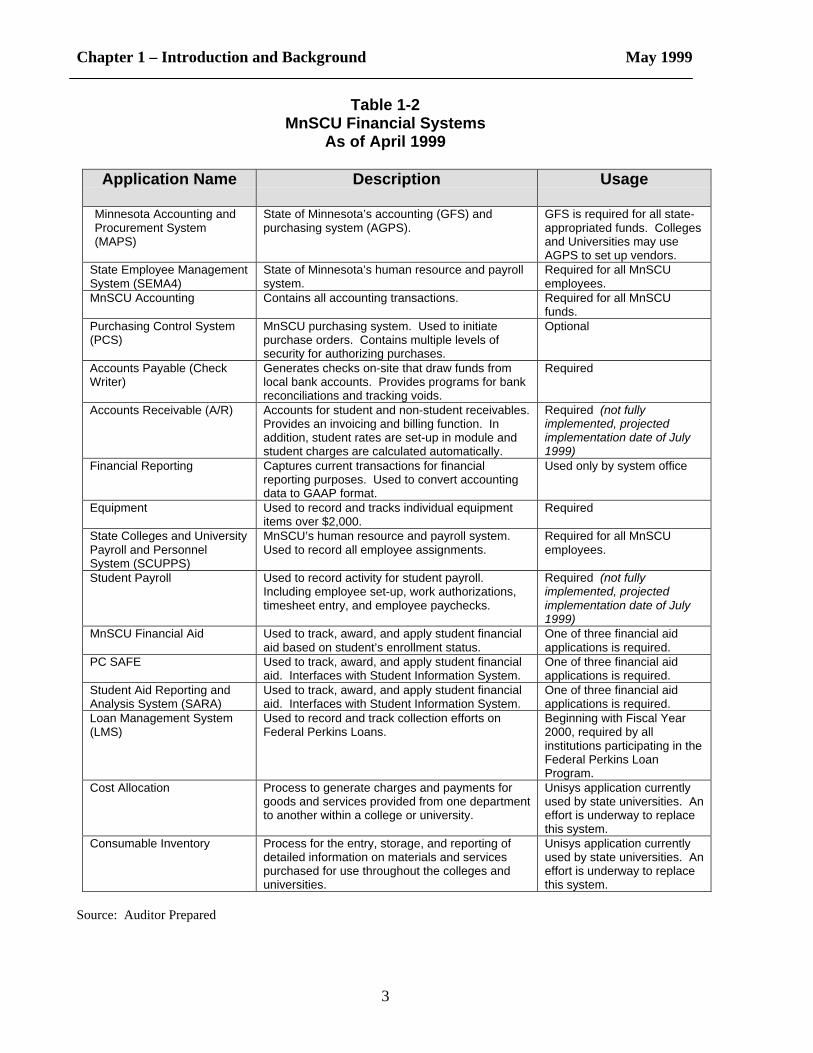

MnSCU did develop and implement anaccounting system which consolidated allfinancial activity in one system. Inaddition, MnSCU has developed andimplemented several other applications toaccount for and manage financial resources.Table 1-2 gives a brief description offinancial systems used by the system officeand colleges and universities to managefinancial resources. In addition, manyinstitutions have purchased or developed in-house financial applications to account for

individual or unique institution needs. Forexample, these applications may be used toaccount for bookstore, food service,parking, or customized training operations.

The MnSCU system office requires collegesand universities to use many of theapplications described in Table 1-2. Forexample, colleges and universities arerequired to use MnSCU Accounting toaccount for all financial transactions. Inaddition, institutions are required to accountfor human resource data in the State Collegeand University Payroll and PersonnelSystem (SCUPPS). These two systemsinterface with the State of Minnesotaaccounting and human resource/payrollsystems.

Table 1-1Accounting Systems in Place Prior to Merger

Former HigherEducation System

Detail AccountingTransactions for StateAppropriated Funds

Detail AccountingTransaction for Local

Fund ActivityState University System Batch entered into both

the State of Minnesotaaccounting system andthe State Universityaccounting system

State Universityaccounting system

Community CollegeSystem

Entered centrally inState of Minnesotaaccounting system.

No centralized system -manual or collegeelected application

Technical Colleges Uniform FinancialAccounting andReporting Standards(UFARS) accountingsystem

Uniform FinancialAccounting andReporting Standards(UFARS) accountingsystem

Source: Interviews with MnSCU employees

Chapter 1 – Introduction and Background May 1999

3

Table 1-2MnSCU Financial Systems

As of April 1999

Application Name Description Usage

Minnesota Accounting andProcurement System(MAPS)

State of Minnesota’s accounting (GFS) andpurchasing system (AGPS).

GFS is required for all state-appropriated funds. Collegesand Universities may useAGPS to set up vendors.

State Employee ManagementSystem (SEMA4)

State of Minnesota’s human resource and payrollsystem.

Required for all MnSCUemployees.

MnSCU Accounting Contains all accounting transactions. Required for all MnSCUfunds.

Purchasing Control System(PCS)

MnSCU purchasing system. Used to initiatepurchase orders. Contains multiple levels ofsecurity for authorizing purchases.

Optional

Accounts Payable (CheckWriter)

Generates checks on-site that draw funds fromlocal bank accounts. Provides programs for bankreconciliations and tracking voids.

Required

Accounts Receivable (A/R) Accounts for student and non-student receivables.Provides an invoicing and billing function. Inaddition, student rates are set-up in module andstudent charges are calculated automatically.

Required (not fullyimplemented, projectedimplementation date of July1999)

Financial Reporting Captures current transactions for financialreporting purposes. Used to convert accountingdata to GAAP format.

Used only by system office

Equipment Used to record and tracks individual equipmentitems over $2,000.

Required

State Colleges and UniversityPayroll and PersonnelSystem (SCUPPS)

MnSCU’s human resource and payroll system.Used to record all employee assignments.

Required for all MnSCUemployees.

Student Payroll Used to record activity for student payroll.Including employee set-up, work authorizations,timesheet entry, and employee paychecks.

Required (not fullyimplemented, projectedimplementation date of July1999)

MnSCU Financial Aid Used to track, award, and apply student financialaid based on student’s enrollment status.

One of three financial aidapplications is required.

PC SAFE Used to track, award, and apply student financialaid. Interfaces with Student Information System.

One of three financial aidapplications is required.

Student Aid Reporting andAnalysis System (SARA)

Used to track, award, and apply student financialaid. Interfaces with Student Information System.

One of three financial aidapplications is required.

Loan Management System(LMS)

Used to record and track collection efforts onFederal Perkins Loans.

Beginning with Fiscal Year2000, required by allinstitutions participating in theFederal Perkins LoanProgram.

Cost Allocation Process to generate charges and payments forgoods and services provided from one departmentto another within a college or university.

Unisys application currentlyused by state universities. Aneffort is underway to replacethis system.

Consumable Inventory Process for the entry, storage, and reporting ofdetailed information on materials and servicespurchased for use throughout the colleges anduniversities.

Unisys application currentlyused by state universities. Aneffort is underway to replacethis system.

Source: Auditor Prepared

MnSCU Office of Internal Auditing May 1999

4

This page left blank intentionally.

5

Chapter 2 – System Design and Functionality May 1999

Chapter Conclusion

The creation of the MnSCU financial systems consolidated several methods of accounting forfinancial activity into one common framework. The development of all-inclusive financialdatabases was a major accomplishment for the organization. These systems, however, areexceedingly complex and difficult for users to understand. The MnSCU informationtechnology governance structure must evaluate options for long-term solutions to meet theorganization’s financial information needs. In the meantime, steps must be taken to addbasic user support, eliminate undue complexity, and incorporate the use of projectmanagement and quality assurance techniques for controlling system enhancements.

MnSCU created the InformationTechnology Services (ITS) division inJuly 1998. This division is responsible fordeveloping and maintaining the centralizedadministrative systems. The division isheaded by a chief information officer (CIO),who reports to the Vice Chancellor forFinance-CFO. Prior to the formation of theITS division, system development andmaintenance was primarily completed bycollege and university employees as timepermitted.

Our original intent was to address thefollowing question on the design andfunctionality of financial systems.

§ Does MnSCU Accounting haveeffective input and processing controls?

When we began to look at the input andprocessing controls over the financialsystems we determined there were broaderissues that needed to be reviewed. In thischapter, we focus our review on the design,functionality and support of the financialsystems. We completed our review byinterviewing ITS division employees. In

addition, we completed a detailed analysisof the payroll process. Finally, weinterviewed employees at colleges anduniversities on their overall understandingof financial systems.

1. MnSCU has not completed acomprehensive evaluation of the bestlong-term solution for meetingfinancial information and reportingneeds.

The financial systems introduced inChapter 1 were implemented without aformal system development methodology.In addition, the fundamental financialsystems (MnSCU Accounting andSCUPPS) were developed and implementedwithin an extremely short timeframe prior tothe merger. The January 1999 InternalAuditing report on the Student InformationSystem states “The organization was simplyill-equipped to develop its own software in-house. Insufficient resources were investedin testing the quality of software modules,developing training programs, anddocumenting system design andprocesses.”1

1 Student Information System Report, MnSCU Office of Internal Auditing – January 1999

MnSCU Office of Internal Auditing May 1999

6

These same issues contributed to many ofthe financial system issues cited in thisreport.

Beginning with calendar year 1999, aformal process was established forprioritizing system development work. Aspart of the process, MnSCU began steps toestablish an information technologygovernance structure. At this point, thegovernance structure is in the process ofbeing finalized. Once in place, thisstructure needs to set a foundation forsystem development decisions.

Currently, the process for prioritizingfunctionality and enhancement requests isthe responsibility of user groups. Usergroups are made up of representatives fromcolleges and universities within differentfunctional areas. There are several usergroups including accounting and humanresources that meet on a regular basis. ITSdivision architects facilitate these meetings

and record minutes. As priorities are set,the architects are responsible for developingdetailed specifications for use by developersand quality assurance employees.

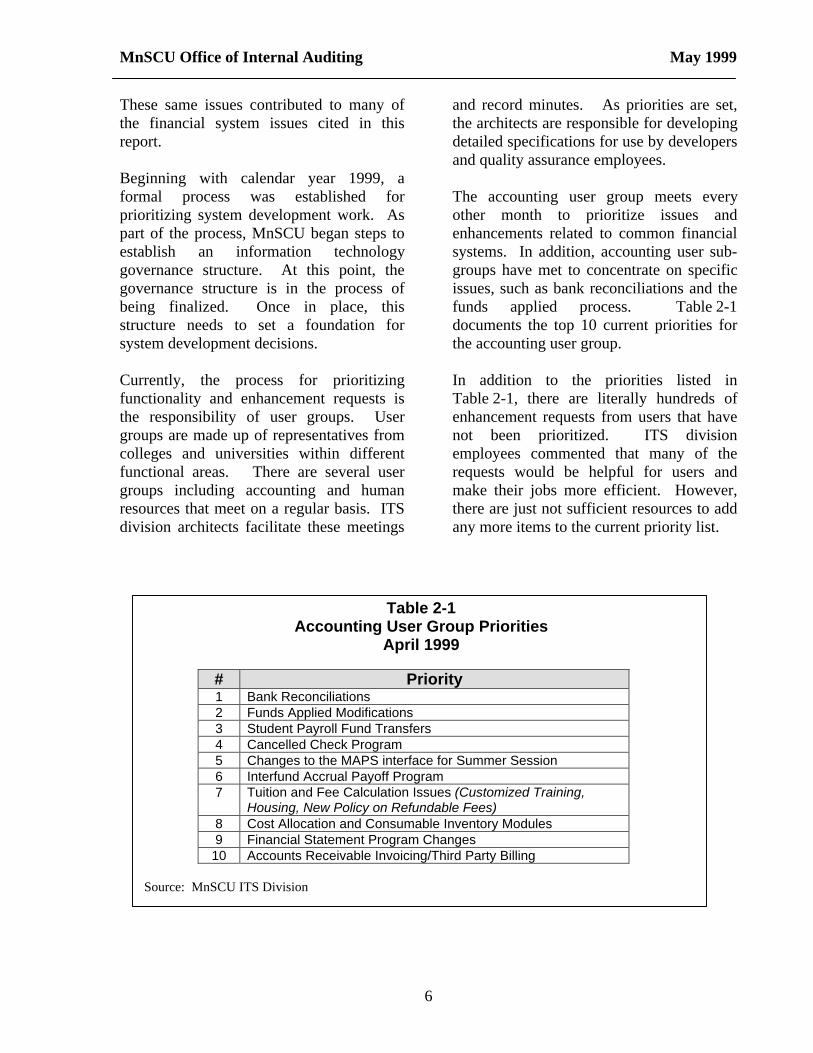

The accounting user group meets everyother month to prioritize issues andenhancements related to common financialsystems. In addition, accounting user sub-groups have met to concentrate on specificissues, such as bank reconciliations and thefunds applied process. Table 2-1documents the top 10 current priorities forthe accounting user group.

In addition to the priorities listed inTable 2-1, there are literally hundreds ofenhancement requests from users that havenot been prioritized. ITS divisionemployees commented that many of therequests would be helpful for users andmake their jobs more efficient. However,there are just not sufficient resources to addany more items to the current priority list.

Table 2-1Accounting User Group Priorities

April 1999

# Priority1 Bank Reconciliations2 Funds Applied Modifications3 Student Payroll Fund Transfers4 Cancelled Check Program5 Changes to the MAPS interface for Summer Session6 Interfund Accrual Payoff Program7 Tuition and Fee Calculation Issues (Customized Training,

Housing, New Policy on Refundable Fees)8 Cost Allocation and Consumable Inventory Modules9 Financial Statement Program Changes10 Accounts Receivable Invoicing/Third Party Billing

Source: MnSCU ITS Division

Chapter 2 - System Design and Functionality May 1999

7

The user groups are a good solution foranalysis and prioritization of day to dayfunctionality issues and questions.However, the organization needs to take astep back and evaluate the best long-termsolution for accounting for financialactivities and reporting. The user groupscannot resolve many questions and issuesrelated to system development, for example:

§ Will MnSCU Accounting be able toefficiently provide the data needed toproduce financial statements? TheBoard of Trustees has expressed interestin obtaining audited financialstatements.

§ Are MnSCU’s reasons for initiallyrequiring its own unique systems stillvalid? The State of Minnesota hascompleted upgrades to MAPS andSEMA4 in recent years. Will these newupgraded systems meet MnSCU’sneeds?

§ What financial systems have otherhigher education institutionsimplemented? Will these systems moreeconomically meet our needs?

§ With limited development resources,how do new initiatives receivepriorities?

§ Payroll processing gets lost betweenhuman resources and accounting. Howdo issues get resolved when they arise inthis critical area?

The existing financial systems were notdeveloped under ideal circumstances.However, these systems survived thedifficulties of the merger transition.

Furthermore, these systems enabled theorganization to combine financialaccounting data. These systems may not,however, be most suitable for theorganization in the future. As indicated inFinding 3, the systems have createdadministrative inefficiencies and, asdiscussed in Chapter 6, they haveinsufficient reporting capability. BeforeMnSCU invests significant resources intomodifying and enhancing existing systems,it needs to look at future needs anddetermine the best solution for the nextmillennium.

Recommendations

ü The MnSCU information technologygovernance structure must explorealternatives for providing theorganization with effective futuresolutions for meeting its financialinformation needs. Long-term solutionsmust take into account the personneldemands imposed by existing andproposed systems.

ü Opportunities to eliminate multiple andduplicative financial systems must beexplored.

ü The governance structure must allocateappropriate personnel and financialresources to this project, whilebalancing the demands of non-financialsystems.

ü The governance structure must sort outresponsibilities for managing systemsthat have overlapping jurisdictionalconsiderations, such as payroll/humanresources.

MnSCU Office of Internal Auditing May 1999

8

Figure 2-1Simplified MnSCU Personnel/Payroll Process

SEMA4Pay to $PayrollWarrant

TimesheetEntry

Post PayrollExpenditures MAPS

SCUPPSSCUPPSMnSCU

AccountingMnSCU

Accounting

HRInformation

Reconcile

HRInformation

Interface

Post PayrollExpenditures

ElectronicFile of Payroll

Transactions

37 applicationcopies

LocallyFunded

EmployeeReimbursement

PayrollEncumbrances

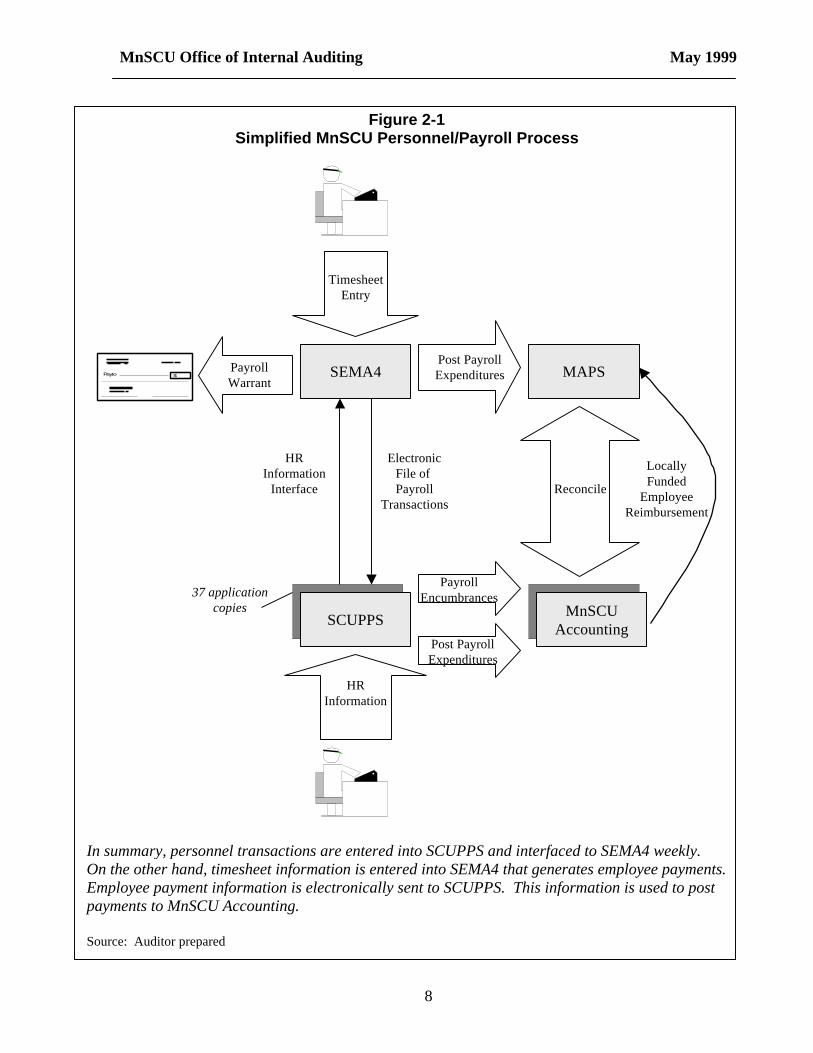

In summary, personnel transactions are entered into SCUPPS and interfaced to SEMA4 weekly.On the other hand, timesheet information is entered into SEMA4 that generates employee payments.Employee payment information is electronically sent to SCUPPS. This information is used to postpayments to MnSCU Accounting.

Source: Auditor prepared

Chapter 2 - System Design and Functionality May 1999

9

Figure 2-2Simplified MnSCU Equipment Purchasing Process

MAPSPay to $ Vendor

Warrant

PCSPCS MnSCUAccounting

MnSCUAccounting

InitiatePurchase

Order

37 applicationcopies

EquipmentEncumbrances

EquipmentEquipmentCheck WriterCheck Writer

StateTreasury

Funds

LocalFunds

Enter VendorPayment

Pay to $

VendorCheck

RecordEquipment

Reconcile

Reconcile

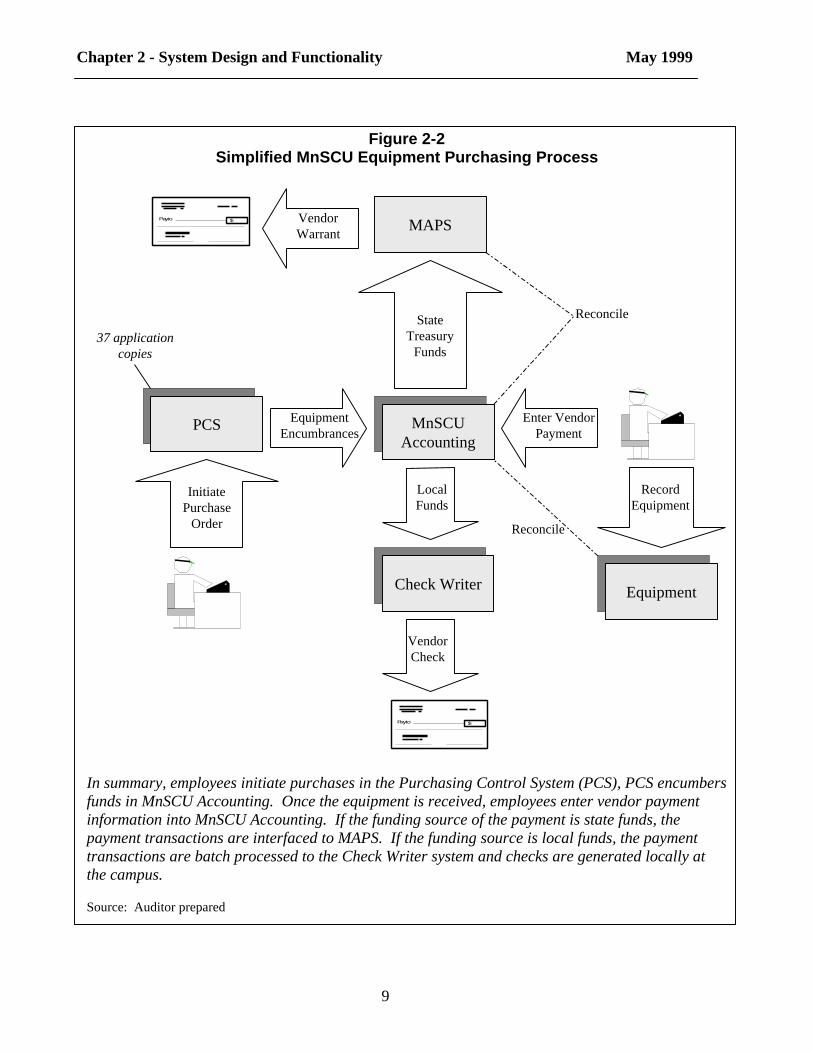

In summary, employees initiate purchases in the Purchasing Control System (PCS), PCS encumbersfunds in MnSCU Accounting. Once the equipment is received, employees enter vendor paymentinformation into MnSCU Accounting. If the funding source of the payment is state funds, thepayment transactions are interfaced to MAPS. If the funding source is local funds, the paymenttransactions are batch processed to the Check Writer system and checks are generated locally atthe campus.

Source: Auditor prepared

MnSCU Office of Internal Auditing May 1999

10

2. MnSCU has not provided basic usersupport for the financial systems.

College and university employees talkedabout the difficulties of implementing bothMnSCU Accounting and SCUPPS. Bothsystems were placed into production aroundthe time of the merger. At that time, userswere given minimal training anddocumentation on the new systems.Employees were forced to learn the systemsby trial and error. Improvements have beenmade for supporting users since that time.However, several issues still exist,including:

§ Documentation was developed forMnSCU Accounting after the systemwas implemented. However, themanual has not been updated for severalyears. In addition, some college anduniversity users did not know it existed.

§ No formal training has been developedfor MnSCU Accounting. Colleges anduniversities complete in-house trainingfor new employees. Many institutionswould like to see more formalizedtraining. In addition, employees wouldlike to have specialized training.

§ At the time of our review, nodocumentation existed on the processfor posting business expenses toMnSCU Accounting.

§ Recently, a financial system help deskwas established for users. However,users expressed concern that help deskemployees were not fullyknowledgeable on the financial systems.

§ Users expressed concerns that the on-line help features within the system arenot sufficient.

§ No technical documentation exists onthe process for posting payroll toMnSCU Accounting.

MnSCU needs to evaluate and improvesupport offered to users.

Recommendations

ü It is essential that an up-to-dateaccounting manual be developed forusers. The manual must provide afoundation for ensuring that users havecurrent guidance available to them on atimely basis and serve as an effectivereference tool.

ü Basic training courses for initiating newusers to the accounting system areneeded.

ü Priorities for adding other user-friendlyfeatures, such as on-line help, should bedependent on the decision of the MnSCUinformation technology governancestructure for future solutions.

3. The financial systems contain unduecomplexity and require excessiveadministrative maintenance.

To effectively manage financial resources,college and university employees need tohave a good working knowledge of howapplications process data. In addition,employees need to understand the differentrelationships or interfaces between theapplications. For example, Figures 2-1 and2-2 depict simplified versions of the numberof systems and interfaces needed to pay aMnSCU employee and complete anequipment purchase. As the figures depict,the processes are extremely complex. Inorder to complete these basic transactions,both the State of Minnesota and MnSCUsystems are used.

Chapter 2 - System Design and Functionality May 1999

11

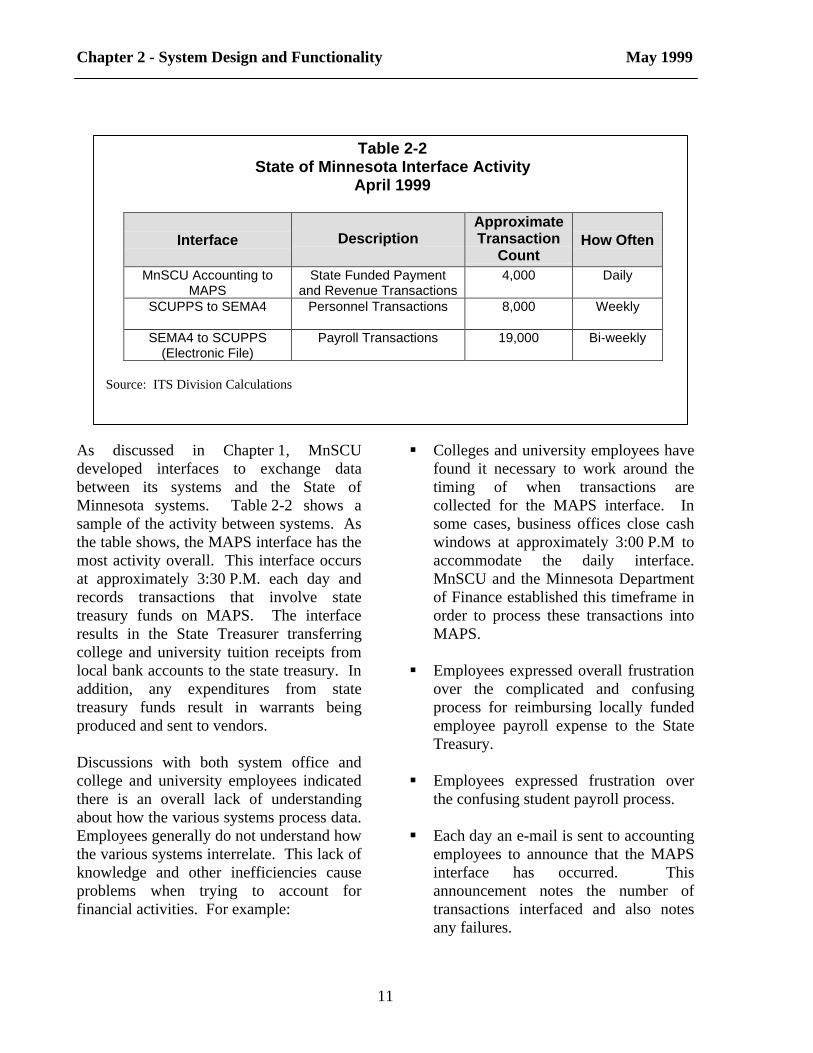

As discussed in Chapter 1, MnSCUdeveloped interfaces to exchange databetween its systems and the State ofMinnesota systems. Table 2-2 shows asample of the activity between systems. Asthe table shows, the MAPS interface has themost activity overall. This interface occursat approximately 3:30 P.M. each day andrecords transactions that involve statetreasury funds on MAPS. The interfaceresults in the State Treasurer transferringcollege and university tuition receipts fromlocal bank accounts to the state treasury. Inaddition, any expenditures from statetreasury funds result in warrants beingproduced and sent to vendors.

Discussions with both system office andcollege and university employees indicatedthere is an overall lack of understandingabout how the various systems process data.Employees generally do not understand howthe various systems interrelate. This lack ofknowledge and other inefficiencies causeproblems when trying to account forfinancial activities. For example:

§ Colleges and university employees havefound it necessary to work around thetiming of when transactions arecollected for the MAPS interface. Insome cases, business offices close cashwindows at approximately 3:00 P.M toaccommodate the daily interface.MnSCU and the Minnesota Departmentof Finance established this timeframe inorder to process these transactions intoMAPS.

§ Employees expressed overall frustrationover the complicated and confusingprocess for reimbursing locally fundedemployee payroll expense to the StateTreasury.

§ Employees expressed frustration overthe confusing student payroll process.

§ Each day an e-mail is sent to accountingemployees to announce that the MAPSinterface has occurred. Thisannouncement notes the number oftransactions interfaced and also notesany failures.

Table 2-2State of Minnesota Interface Activity

April 1999

Interface DescriptionApproximateTransaction

CountHow Often

MnSCU Accounting toMAPS

State Funded Paymentand Revenue Transactions

4,000 Daily

SCUPPS to SEMA4 Personnel Transactions 8,000 Weekly

SEMA4 to SCUPPS(Electronic File)

Payroll Transactions 19,000 Bi-weekly

Source: ITS Division Calculations

MnSCU Office of Internal Auditing May 1999

12

§ Some colleges and universities arerequired to reconcile MAPS to MnSCUeach month. The system officecompletes this reconciliation for somecommunity colleges. Discussions withemployees and review of documentationshowed that many institutions did notunderstand the importance of thisreconciliation. In addition, manyinstitutions did not understand or did notmake an effort to investigate thedifferences noted in thesereconciliations.

§ Our review of fiscal year 1998 payrolland business expenses generally showedthe process is working. However, wedid note several examples that resultedin approximately $60,000 not beingposted to MnSCU Accounting. A dailydiagnostic report sent to colleges anduniversities alerts the institutions whenposting errors occur. However, thisreport is not exception based andcontains too much detail. This maycause employees to ignore the reportand allow exceptions to go undetected.

Colleges and universities have notexperienced the same level of success withthe financial systems. Some institutionshave been able to overcome the hurdles andare making the systems work for them. Forthe most part, we observed that theseinstitutions have employees with a moreextensive accounting background.

Recommendations

ü Simplify the daily diagnostic report andmake it an exception report.

ü Eliminate daily batch processingmessages and report only exceptions.

ü Review the timing of the process forcollecting transactions for the dailyMAPS interface. For example,transactions could be collectedovernight and sent through the MAPSinterface the following day.

ü Develop standard routines andprocedures to ensure that accountingdata recorded on MAPS is accurate, sothat colleges and universities canconcentrate on MnSCU Accounting astheir exclusive accounting system.

4. System enhancements and problemresolutions are not managed withconventional quality assurance andproject management techniques.

The lack of a comprehensive qualityassurance process has resulted in significantfinancial system functionality issues. Forexample, the funds applied functionality putinto production in January 1999 resulted inseveral institutions being unable toreconcile MnSCU Accounting to bankaccounts. If a comprehensive qualityassurance process would have been in place,the reconciliation problem may have beenavoided.

Testing of any financial systemfunctionality should include acomprehensive testing plan. The testingplan should include steps for completingreconciliations for critical timeframes (i.e.month and year-ends). In addition, thetesting plan should include user acceptanceof any critical functionality. The newlyformed ITS division includes a qualityassurance unit. However, this unit is not yetfamiliar with quality assurance businesspractices and lacks expertise in the financialsystem applications.

Chapter 2 - System Design and Functionality May 1999

13

MnSCU needs to make a commitment touse project management tools. Userscontinually express frustration over missedtimeframes or incomplete functionality.The use of project management tools willbegin to eliminate these frustrations. Forexample, MnSCU needs to use detailedproject plans that include schedules andmilestones. Schedules should includerealistic timeframes for completingdevelopment and testing. In addition, theseplans should identify employees responsiblefor completing milestones.

Recommendations

ü Develop comprehensive testing plans forfinancial system modifications. Whencash transactions are included, theseplans should require a month-end cycleand test the completion of a bankreconciliation.

ü Projects must be managed withconventional project management tools.Estimated development resources andexpected delivery dates must becommunicated to users to enhanceaccountability.

MnSCU Office of Internal Auditing May 1999

14

This page left blank intentionally.

15

Chapter 3 – Financial Data Integrity May 1999

Chapter Conclusion

MnSCU financial systems produce reasonable results for supporting daily operations, such asreceipting and disbursing funds. Our testing showed that coding for attributes such as funds,program codes, and object codes was reliable. A critical operational issue that still must beresolved is the reconciliation of cash to bank balances. Additional operational issues thatneed improvement include the accuracy of occurrence date coding, the timeliness ofrecording data, and the support for sensitive transactions, such as journal entries. Finally,accounting operations lack the discipline of regularly recording the necessary information toproduce complete balance sheets and income statements.

We addressed the following question aboutfinancial data integrity:

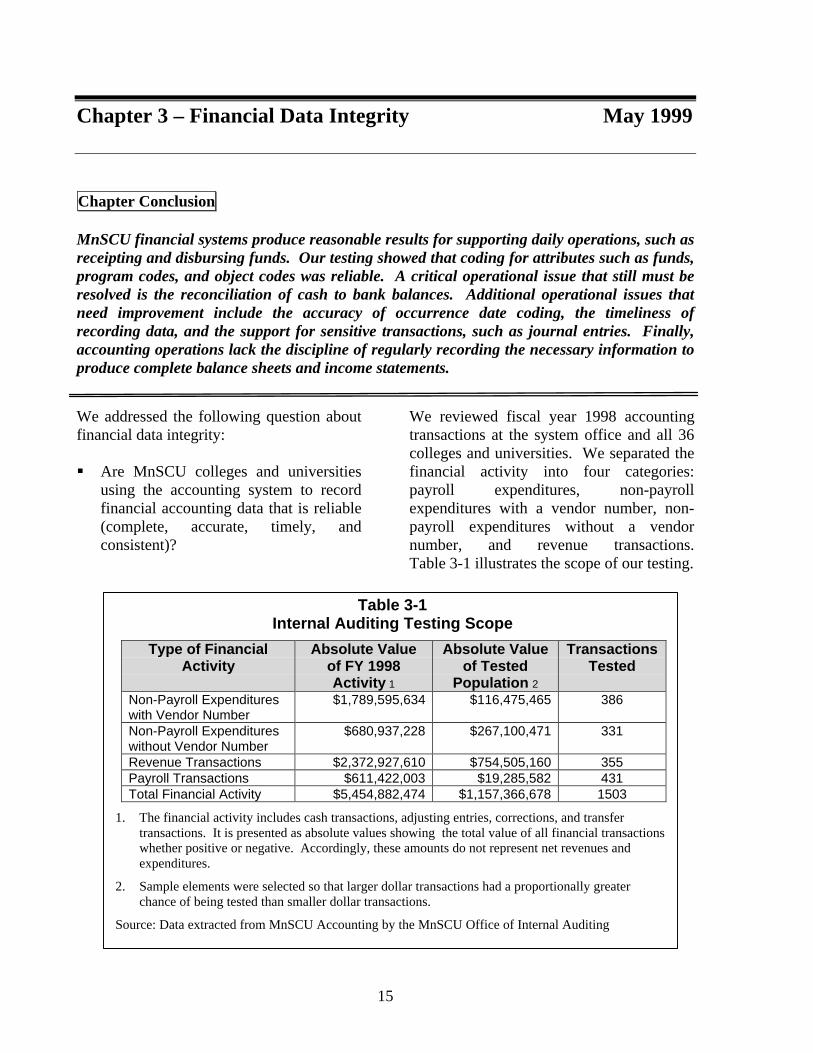

§ Are MnSCU colleges and universitiesusing the accounting system to recordfinancial accounting data that is reliable(complete, accurate, timely, andconsistent)?

We reviewed fiscal year 1998 accountingtransactions at the system office and all 36colleges and universities. We separated thefinancial activity into four categories:payroll expenditures, non-payrollexpenditures with a vendor number, non-payroll expenditures without a vendornumber, and revenue transactions.Table 3-1 illustrates the scope of our testing.

Table 3-1Internal Auditing Testing Scope

Type of FinancialActivity

Absolute Valueof FY 1998Activity 1

Absolute Valueof Tested

Population 2

TransactionsTested

Non-Payroll Expenditureswith Vendor Number

$1,789,595,634 $116,475,465 386

Non-Payroll Expenditureswithout Vendor Number

$680,937,228 $267,100,471 331

Revenue Transactions $2,372,927,610 $754,505,160 355Payroll Transactions $611,422,003 $19,285,582 431Total Financial Activity $5,454,882,474 $1,157,366,678 1503

1. The financial activity includes cash transactions, adjusting entries, corrections, and transfertransactions. It is presented as absolute values showing the total value of all financial transactionswhether positive or negative. Accordingly, these amounts do not represent net revenues andexpenditures.

2. Sample elements were selected so that larger dollar transactions had a proportionally greaterchance of being tested than smaller dollar transactions.

Source: Data extracted from MnSCU Accounting by the MnSCU Office of Internal Auditing

MnSCU Office of Internal Auditing May 1999

16

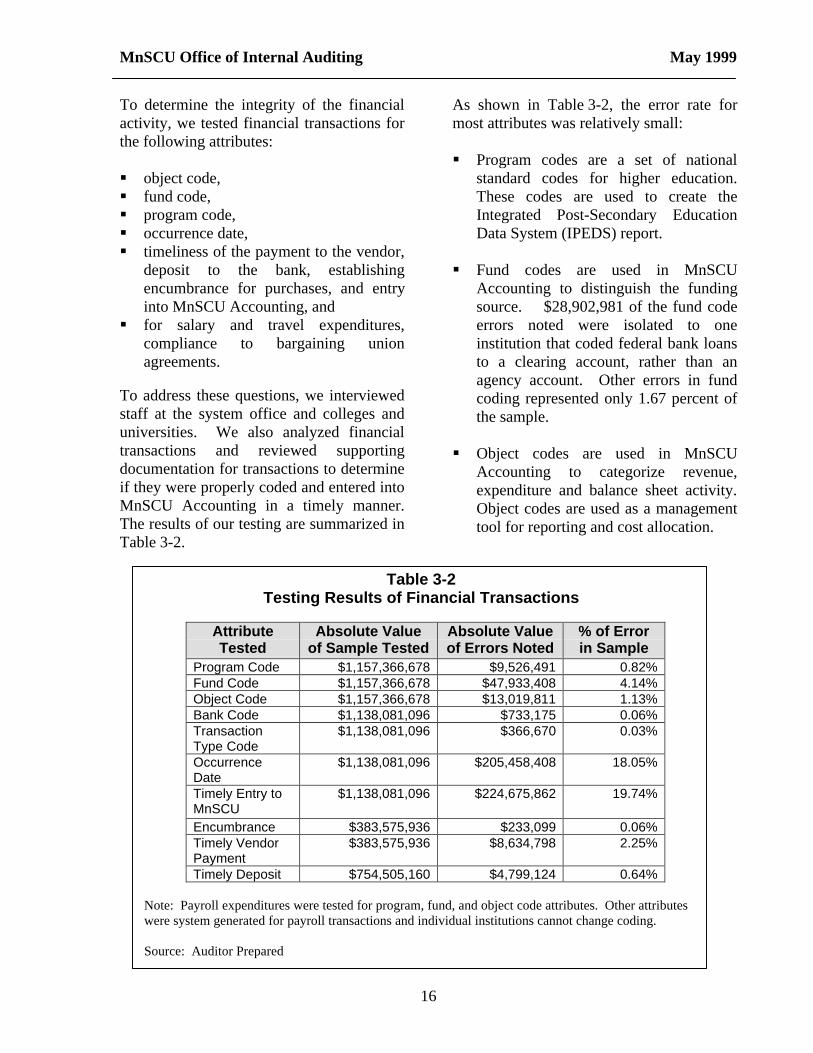

To determine the integrity of the financialactivity, we tested financial transactions forthe following attributes:

§ object code,§ fund code,§ program code,§ occurrence date,§ timeliness of the payment to the vendor,

deposit to the bank, establishingencumbrance for purchases, and entryinto MnSCU Accounting, and

§ for salary and travel expenditures,compliance to bargaining unionagreements.

To address these questions, we interviewedstaff at the system office and colleges anduniversities. We also analyzed financialtransactions and reviewed supportingdocumentation for transactions to determineif they were properly coded and entered intoMnSCU Accounting in a timely manner.The results of our testing are summarized inTable 3-2.

As shown in Table 3-2, the error rate formost attributes was relatively small:

§ Program codes are a set of nationalstandard codes for higher education.These codes are used to create theIntegrated Post-Secondary EducationData System (IPEDS) report.

§ Fund codes are used in MnSCUAccounting to distinguish the fundingsource. $28,902,981 of the fund codeerrors noted were isolated to oneinstitution that coded federal bank loansto a clearing account, rather than anagency account. Other errors in fundcoding represented only 1.67 percent ofthe sample.

§ Object codes are used in MnSCUAccounting to categorize revenue,expenditure and balance sheet activity.Object codes are used as a managementtool for reporting and cost allocation.

Table 3-2Testing Results of Financial Transactions

AttributeTested

Absolute Valueof Sample Tested

Absolute Valueof Errors Noted

% of Errorin Sample

Program Code $1,157,366,678 $9,526,491 0.82%Fund Code $1,157,366,678 $47,933,408 4.14%Object Code $1,157,366,678 $13,019,811 1.13%Bank Code $1,138,081,096 $733,175 0.06%TransactionType Code

$1,138,081,096 $366,670 0.03%

OccurrenceDate

$1,138,081,096 $205,458,408 18.05%

Timely Entry toMnSCU

$1,138,081,096 $224,675,862 19.74%

Encumbrance $383,575,936 $233,099 0.06%Timely VendorPayment

$383,575,936 $8,634,798 2.25%

Timely Deposit $754,505,160 $4,799,124 0.64%

Note: Payroll expenditures were tested for program, fund, and object code attributes. Other attributeswere system generated for payroll transactions and individual institutions cannot change coding.

Source: Auditor Prepared

Chapter 3 – Financial Data Integrity May 1999

17

§ Bank codes are used by the institutionsto separate local activity from treasuryactivity. Institutions must have specificstatutory authority to maintain funds in alocal bank account.

§ Transaction type codes are used bycolleges and universities to performaccounting functions, such as paymenttransactions or journal entries.

§ A few purchased goods or services didnot have a proper encumbrance.Colleges and universities are required toencumber funds prior to incurring afinancial obligation.

§ Some receipts were not depositedtimely. Minnesota Statute requirescolleges and universities to depositreceipts over $250 on a daily basis.

We did, however, note that colleges anduniversities and the system office routinelyused improper occurrence dates. We alsonoted payments to vendors were not alwayscompleted timely. Several colleges anduniversities did not maintain adequatedocumentation for sensitive transactions,such as journal entries. MnSCUAccounting does not contain informationcomplete enough to produce balance sheetinformation or to measure auxiliaryenterprise net income. Finally, as discussedin Finding 10 in Chapter 5, problems withreconciling accounts continues to result inquestionable cash amounts on MnSCUAccounting.

5. Occurrence dates have not beenrecorded properly, resulting ininaccurate accounts payablecalculations.

The occurrence date is important fordetermining accounts payable for financialstatements prepared by both MnSCU and

the Minnesota Department of Finance.MnSCU Accounting allows the user to enteran occurrence date for each transaction.The occurrence date is supposed to be thedate that the financial event occurred. Forexpenditures, the occurrence date is the dategoods were received or last date serviceswere rendered. As illustrated in Table 3-2,occurrence dates errors represented 18.05percent of the sample tested.

In conversations with college and universitystaff, we found that most institutions payclose attention to occurrence dates only atthe end of the fiscal year. Many institutionsindicated that either they did not closelymonitor or did not know they shouldmonitor occurrence dates during theremainder of the fiscal year.

We noted several instances where collegesand universities did not monitor the date thegoods were received or the date the eventoccurred. Instead, these institutions let theoccurrence date default to the date of entry.Other institutions chose to use the invoicedate for the occurrence date. Occurrencedates were also not reliable for summaryentries originating from the MinnesotaStudent Information System (MSIS),College Information System (CIS) or legacystate university system.

In addition, we also noted severaltransactions that were coded with anoccurrence date after June 30, 1998,although they were fiscal year 1998transactions. For example, each fiscal yearthe system office incurs expenditures onbehalf of the colleges and universities. Atthe end of the fiscal year, the system officewill charge those expenditures back to thecolleges and universities. We noted thatsystem office employees routinely used anoccurrence date after the fiscal year end tocharge the expenditures to the colleges anduniversities. Colleges and universities often

MnSCU Office of Internal Auditing May 1999

18

followed the example of the system officeand did not change the occurrence date ofthe adjusting transactions. We also notedinstances of internal reclassification ofexpenditures by the colleges anduniversities with occurrence dates after thefiscal year end. Transactions posted with anoccurrence date past the fiscal year end arenot recognized in the determination of theState of Minnesota financial statementaccruals.

Recommendation

ü The importance of accurate occurrencedate coding must be emphasized.

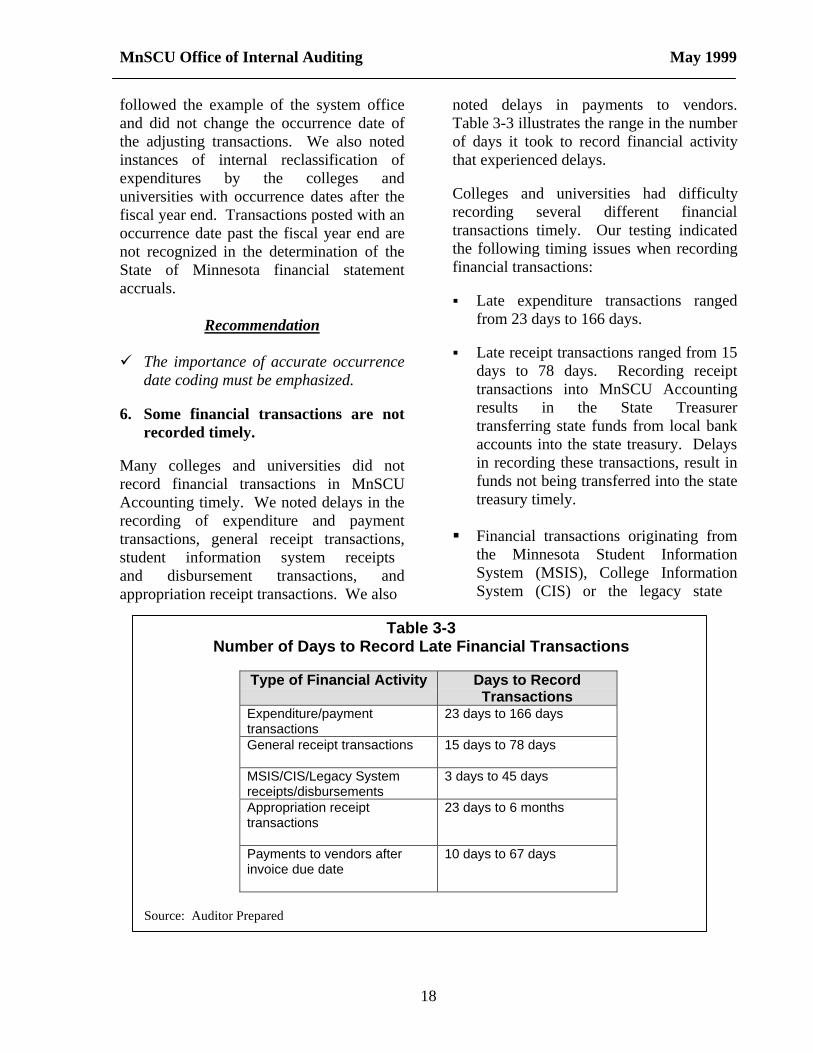

6. Some financial transactions are notrecorded timely.

Many colleges and universities did notrecord financial transactions in MnSCUAccounting timely. We noted delays in therecording of expenditure and paymenttransactions, general receipt transactions,student information system receiptsand disbursement transactions, andappropriation receipt transactions. We also

noted delays in payments to vendors.Table 3-3 illustrates the range in the numberof days it took to record financial activitythat experienced delays.

Colleges and universities had difficultyrecording several different financialtransactions timely. Our testing indicatedthe following timing issues when recordingfinancial transactions:

§ Late expenditure transactions rangedfrom 23 days to 166 days.

§ Late receipt transactions ranged from 15days to 78 days. Recording receipttransactions into MnSCU Accountingresults in the State Treasurertransferring state funds from local bankaccounts into the state treasury. Delaysin recording these transactions, result infunds not being transferred into the statetreasury timely.

§ Financial transactions originating fromthe Minnesota Student InformationSystem (MSIS), College InformationSystem (CIS) or the legacy state

Table 3-3Number of Days to Record Late Financial Transactions

Type of Financial Activity Days to RecordTransactions

Expenditure/paymenttransactions

23 days to 166 days

General receipt transactions 15 days to 78 days

MSIS/CIS/Legacy Systemreceipts/disbursements

3 days to 45 days

Appropriation receipttransactions

23 days to 6 months

Payments to vendors afterinvoice due date

10 days to 67 days

Source: Auditor Prepared

Chapter 3 – Financial Data Integrity May 1999

19

university system were not recordeddaily. During fiscal year 1998, mostcolleges and universities were usingMSIS, CIS or the legacy state universitysystem to register students for classes,record tuition payments and disbursefinancial aid. Some institutions posteddisbursements and revenue in summaryfor the previous week or month, ratherthan posting daily activity. Beginningin fiscal year 2000, all colleges anduniversities should be using the newstudent information system, whichshould eliminate this issue.

§ Delays in recording appropriationrevenue ranged from 23 days to sixmonths. Ideally, colleges anduniversities should post appropriationreceipts when the system office transfersthe funds. Delays in recordingappropriation revenues affect budgetreports and the ability to monitorfinancial operations. In addition,colleges and universities mayexperience difficulties reconcilingMAPS to MnSCU.

§ We noted several payments to vendorsthat were not timely. State law suggeststhat vendors should be paid by thevendor invoice date or within 30 days ofreceipt of invoice for services renderedor goods received. However, we notedseveral instances where payment wasmade after the invoice due date or afterthe 30 day timeframe. Delays rangedfrom 10 days to 67 days past the vendordue date. Untimely payments couldcreate a negative impact to theinstitution’s ability to monitor financialoperations. In addition, colleges anduniversities could fall out of goodstanding with vendors for consistentlylate payments. Finally, institutions mayincur finance charges for late payments.

As shown in Table 3-2, 19.74 percent ofrevenue and expenditure transactions testedwere not recorded timely. This can createproblems for reconciling MnSCUAccounting to bank accounts. In addition,reports to management or the Board ofTrustees do not reflect up-to-date financialactivity.

Recommendation

ü Standards must be developed andperformance monitored to ensure thatfinancial transactions are recorded on atimely basis.

7. Supporting documentation for sometransactions was incomplete.

Many colleges and universities did not haveappropriate supporting documentation forsome sensitive transactions, such as journalentries. Often, colleges and universitiespresented computer screen prints of thefinancial transaction as supportingdocumentation. MnSCU Accounting wasnot designed to be a paperless system.Therefore, the system does not have theability to provide detailed transactiondescriptions or transaction authorizations.The screen prints did not serve as sufficientdocumentation.

Journal entries are particularly sensitivesince they normally are used to adjusttransactions. Therefore, it is important tomaintain sufficient documentation to justifythe purpose and authorization of thetransaction, as well as how the amount wasdetermined. For example, we noted journalentries that were created to move fundsfrom one cost center or general ledger toanother. These transactions often did notinclude supporting documentation as to howthe amount of the transaction wasdetermined or show authorization for thetransaction.

MnSCU Office of Internal Auditing May 1999

20

A process should be developed to ensureappropriate documentation is available forall journal voucher transactions. Forexample, a best practice would be use of aform that includes the followinginformation: purpose of the transaction, dateof transaction, name of the originator,signature indicating independent review andapproval of transaction, and the amount ofthe transaction. Supporting documentationshould be attached to the journal voucherform. The forms should be filed forreference purposes.

Another area where a few colleges hadinsufficient supporting documentation waswith employee appointments. Personneland payroll information is maintained inSCUPPS for all employees. Humanresources employees enter appointmentinformation into SCUPPS. Theappointment record shows the salary detailsfor the employee such as bargaining union,step in the bargaining union contract, rate ofpay, and length of the appointment. A fewcolleges and did not keep additionaldocumentation regarding employeeappointments, such as appointment letters.

As with MnSCU Accounting, SCUPPS wasnot designed to be a paperless system.Therefore, maintaining appointmentinformation solely in SCUPPS does notprovide adequate documentation. Forexample, changes can be made to anemployee appointment during a currentfiscal year. The appointment change willoverride and erase the existing appointmentwithout storing the changes. Humanresource employees can enter electronicnotes when an appointment change is made,however, electronic notes are not required.Consequently, it is possible forunauthorized appointment changes to bemade. Colleges and universities riskinappropriate appointment increases when

additional documentation, such asappointment letters, are not maintained.

Recommendation

ü Adequate supporting documentationmust be developed to supporttransactions, particularly sensitivetransactions.

8. Accounting operations lack thediscipline of regularly recording thenecessary information to producecomplete information on financialcondition, e.g. balance sheet accounts,or to measure net income fromauxiliary enterprises.

MnSCU Accounting was designed to focusprimarily on daily operations such asrecording receipt and expendituretransactions. Regular procedures have notbeen developed to generate completebalance sheet information for accounts suchas investments, equipment, land andbuildings, compensated absences, creditmemos or fund balances.

§ Investment Balances: Colleges anduniversities generally do not rely onMnSCU Accounting to track investmentbalances. Institutions have developedinternal spreadsheets to trackinvestments on a daily or monthly basisand enter irregular updates to MnSCUAccounting. As a result, accountingreports do not accurately reflectinvestment activity on an interim basis.

§ Equipment Balances: TechnicalColleges have found it difficult toprovide proper equipment balances. Inthe transition of Technical Colleges intoState Government audit report (August1996), the Office of the LegislativeAuditor cited 19 technical colleges andconsolidated institutions as unable to

Chapter 3 – Financial Data Integrity May 1999

21

provide adequate accountability overequipment. As of the end ofMarch 1999, four of these colleges havestill not recorded all inventory balancesin the equipment system. In addition,seven colleges have not completedrecent physical inventories to verify thatinventory of equipment is accurate.Therefore, equipment accounts recordedon MnSCU Accounting are incomplete.

§ Land and Building Balances: Thesystem office maintains the land andbuilding account balances centrally.MnSCU Accounting has balance sheetcodes to record land and building.However, these codes are not used at thecollege and university level to track landand building balances. Some collegesand universities use manualspreadsheets to track land and buildingbalances.

At fiscal year end, the system officesends each college and university areport requesting the accounting staff toreview and verify the balances for thepreparation of financial statements.Because land and building assetbalances are not recorded at theinstitution level, colleges anduniversities are unable to provideaccurate balances for interim financialstatements.

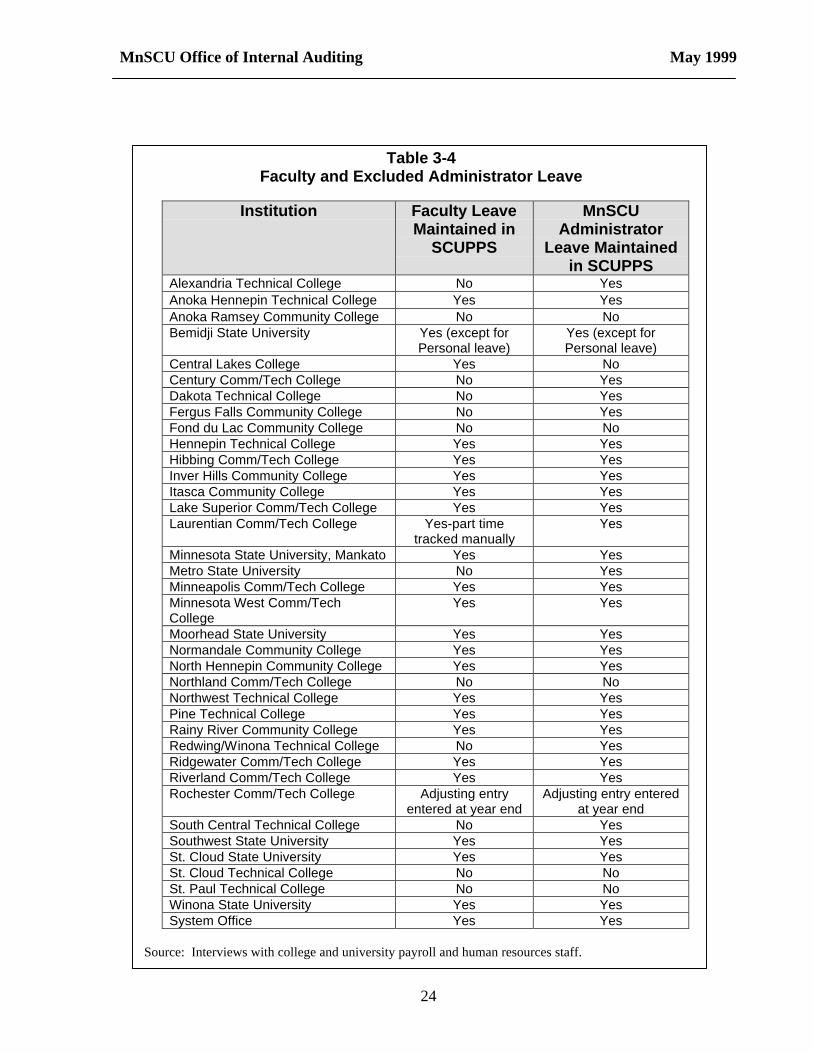

§ Compensated Absence Balances: Wenoted problems encountered by collegesand universities in recording accuratebalances for compensated absences.MnSCU requires the use of SCUPPS tomaintain leave balances. However,some of the colleges and universities donot use SCUPPS to maintain faculty andMnSCU administrator leave. Instead,these colleges and universities trackleave in manual spreadsheets and postyear-end balances into SCUPPS. A

manual system is more susceptible toclerical errors. Table 3-4 shows asummary of the colleges anduniversities that use SCUPPS tomaintain faculty and MnSCUadministrator leave balances.

Colleges and universities use manualspreadsheets to calculate leave forvarious reasons. For example, personalleave for faculty and MnSCUadministrators creates a negativebalance as the leave is used. At the endof the fiscal year, the colleges anduniversities need to zero out thenegative balances for used personalleave. Also, some colleges anduniversities have had problems usingSCUPPS to track adjunct faculty leave.

For financial statements, compensatedbalances are obtained from the leaveaccrual balances in SCUPPS onJune 30th of each year. For theinstitutions that do not use SCUPPS totrack faculty and administrator leave, amanual entry is required to update leavebalance records. If the SCUPPS systemis not used to track faculty andadministrator leave, the liability forcompensated absences is not easilycalculated during the fiscal year.

In addition, the financial statements donot properly reflect the liability for post-retirement employee benefits. Collegesand universities can budget for post-retirement employee benefits, such asinsurance, in the current fiscal year.However, the payments are onlyreflected as expenditures in the incomestatement. The system office does notobtain post-retirement employee benefitliabilities from the colleges anduniversities. Therefore, this information

MnSCU Office of Internal Auditing May 1999

22

is not included as a liability in thebalance sheet.

§ Credit Memos: Colleges anduniversities have the ability to entercredit memos into MnSCU Accounting.The credit memo entry will create theappropriate balance sheet receivable.As the credit memos are used, thecheck-writer system will reduce theamount of the check written by thecredit memos.

Some colleges and universities do notuse the credit memo process forbookstore activity. Instead, theseinstitutions track credit memos in amanual ledger or spreadsheet. At fiscalyear end, the college or universitymakes an entry into the accountingsystem for the year end balance of creditmemos. Therefore, the balance sheetaccounts do not reflect accurate activitythroughout the fiscal year. In addition, amanual system of tracking credit memosis more susceptible to error and mayresult in credit memos being unused.

§ Fund Balances: College and universityfund balances cannot be relied uponbecause they are not updated on aregular basis. Current fiscal year fundbalances are not accurate until priorfiscal years have been closed and fundbalances changes are recorded in thenew fiscal year. The system office isresponsible for closing the fiscal yearand rolling forward the changes in fundbalance.

The system office did not close outfiscal year 1996 until approximatelyOctober 1998. In addition, fiscal years1997 and 1998 have not beencompletely closed (although collegesand universities cannot make accounting

entries to those fiscal years). Therefore,colleges and universities are unable torun reports that provide accurate fundbalance information.

Also, accounting for enterprise fundactivities is incomplete on the financialsystems.

MnSCU Accounting does not adequatelymeasure financial results for enterprise fundactivities. Colleges and universities areforced to prepare manual profit and lossstatements for the enterprise fund activitiessince MnSCU Accounting is unable toaccount for the activity and provide anadequate report. A few colleges anduniversities have not prepared manual profitand loss statements and have been cited inOLA audit reports for not producing incomestatements for enterprise activity,determining if the markup is reasonable,and reviewing profits and fund balances.

For those institutions that do preparemanual income statements, the institutionsmust manually calculate the cost of goodssold. In addition, MnSCU Accountingdoes not calculate depreciation or update thegeneral ledger for gain or loss on sale ofequipment in the enterprise fund. Manualadjustments are required to recorddepreciation or gain/loss on sale ofequipment.

Also, MnSCU Accounting does not updatethe balance sheet object codes for inventorypurchases or reductions. Instead, the systemrequires the balance sheet to be manuallyadjusted to reflect changes in inventory.Although the institutions may prepare theadjusting entries at any time, they aregenerally performed only at fiscal year end.This entry increases the balance sheetinventory account and reduces the costcenter expenditures for resale activity.

Chapter 3 – Financial Data Integrity May 1999

23

Recommendations

ü Compensated absence liabilities andpost-retirement employment benefitsmust be measured and recorded on theaccounting system periodically.

ü Fixed assets, such as plant andequipment, must be recorded on theaccounting system.

ü Credit memos for bookstores must berecorded as assets on the accountingsystem.

ü Prior fiscal years need to be closed in amore timely manner so that fundbalances are presented accurately.

ü The capacity to calculate and recordbusiness type expenses, such as cost ofgoods sold and depreciation expensemust be developed.

MnSCU Office of Internal Auditing May 1999

24

Table 3-4Faculty and Excluded Administrator Leave

Institution Faculty LeaveMaintained in

SCUPPS

MnSCUAdministrator

Leave Maintainedin SCUPPS

Alexandria Technical College No YesAnoka Hennepin Technical College Yes YesAnoka Ramsey Community College No NoBemidji State University Yes (except for

Personal leave)Yes (except forPersonal leave)

Central Lakes College Yes NoCentury Comm/Tech College No YesDakota Technical College No YesFergus Falls Community College No YesFond du Lac Community College No NoHennepin Technical College Yes YesHibbing Comm/Tech College Yes YesInver Hills Community College Yes YesItasca Community College Yes YesLake Superior Comm/Tech College Yes YesLaurentian Comm/Tech College Yes-part time

tracked manuallyYes

Minnesota State University, Mankato Yes YesMetro State University No YesMinneapolis Comm/Tech College Yes YesMinnesota West Comm/TechCollege

Yes Yes

Moorhead State University Yes YesNormandale Community College Yes YesNorth Hennepin Community College Yes YesNorthland Comm/Tech College No NoNorthwest Technical College Yes YesPine Technical College Yes YesRainy River Community College Yes YesRedwing/Winona Technical College No YesRidgewater Comm/Tech College Yes YesRiverland Comm/Tech College Yes YesRochester Comm/Tech College Adjusting entry

entered at year endAdjusting entry entered

at year endSouth Central Technical College No YesSouthwest State University Yes YesSt. Cloud State University Yes YesSt. Cloud Technical College No NoSt. Paul Technical College No NoWinona State University Yes YesSystem Office Yes Yes

Source: Interviews with college and university payroll and human resources staff.

25

Chapter 4: Financial Data Consistency May 1999

Chapter Conclusion

Colleges and universities did not record data in a consistent manner, hamperingthe ability to produce reliable comparative data. Data consistency is a majorconcern for the new budget allocation model. The system office has established aseries of study groups to address the data inconsistencies and provide improvedguidance. A formal structure must be established, however, to ensure thatguidance is developed, communicated, and implemented effectively.

Financial data that is classified andsummarized in a similar manner will allowdecision-makers to compare the financialactivities between colleges and universities.The Board of Trustees, system office,legislature and others are interested incomparative financial data on the collegesand universities. The system office, whichhas access to all institutions’ financial data,prepares various reports for both internaland external users. These reports may be aconsolidation of all system-wideinformation or an aggregation based on oneor more of the data elements. The MnSCUallocation model must have consistentfinancial data in order to distribute funds asintended. The system office must also beable to respond to information requests fromtrustees and legislators on spendingquestions on areas such as technology,counseling, remedial education, and manyother areas.

We addressed the following question aboutfinancial data consistency:

§ Is the financial accounting dataclassified and organized in a mannerthat will allow for meaningfulsummaries and comparisons?

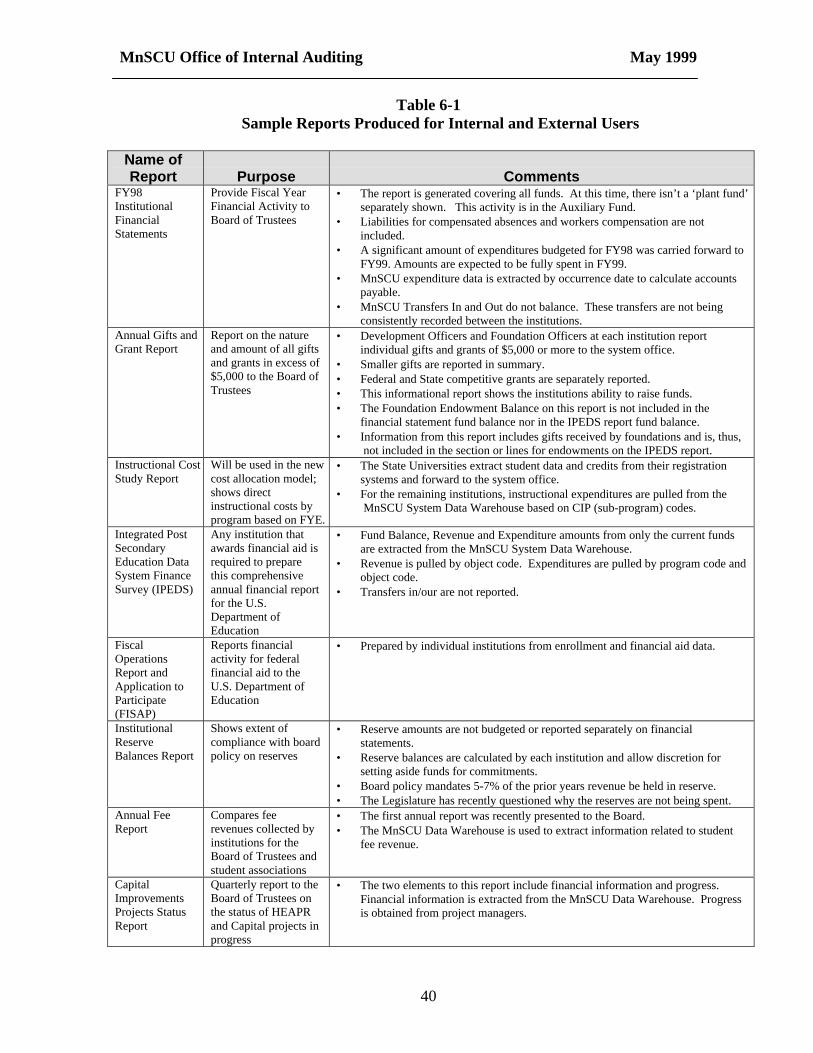

We interviewed the accounting staffs ateach institution to determine how certaintypes of transactions were recorded on theaccounting system.

9. Financial data was not recorded in aconsistent manner between collegesand universities.

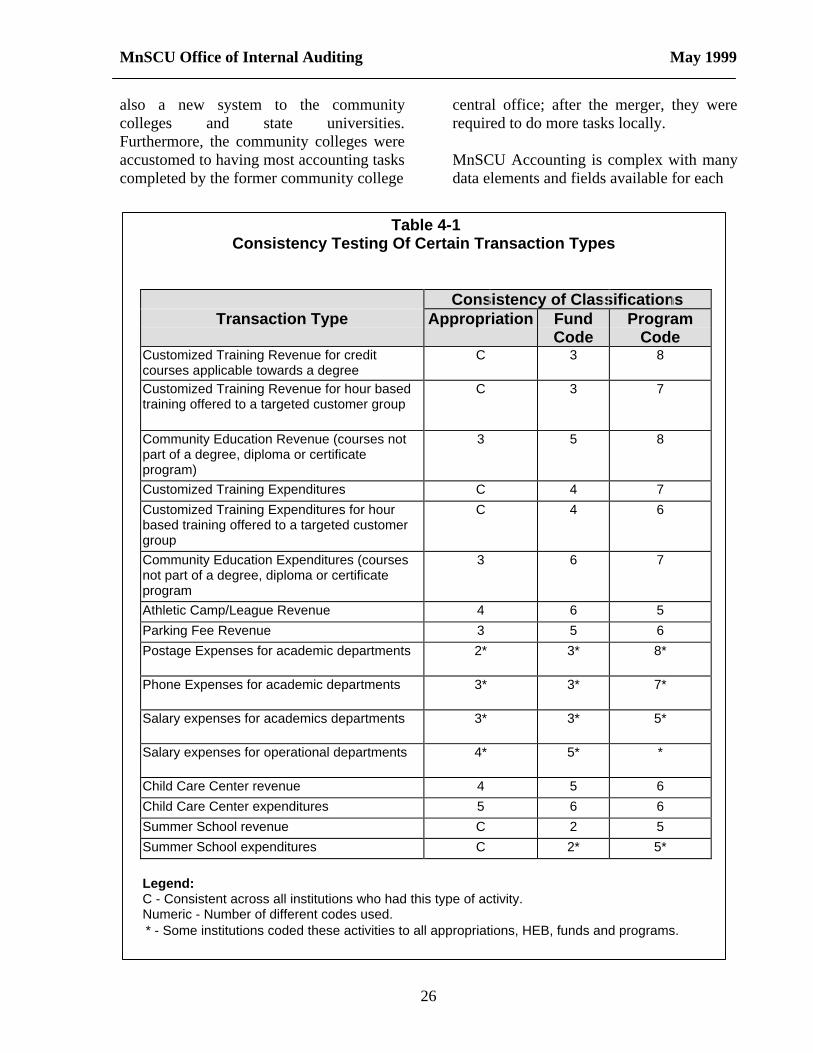

Table 4-1 shows significant codinginconsistencies between colleges anduniversities. We also found otherfundamental differences in recordingtransactions. For example, universitiesgenerally distribute administrativeexpenditures such as telephone costs toseparate departments, however, most two-year colleges charge such costs to onecommon cost center.

When MnSCU Accounting wasimplemented in July 1995, colleges anduniversities were given limited guidelineson how to record transactions. Training onusing the accounting system concentratedon implementing basic daily operations.The significance and use of each particulardata element was not well understood. Thetechnical colleges faced a particularlydifficult challenge because they had justbecome part of state government. It was

MnSCU Office of Internal Auditing May 1999

26

also a new system to the communitycolleges and state universities.Furthermore, the community colleges wereaccustomed to having most accounting taskscompleted by the former community college

central office; after the merger, they wererequired to do more tasks locally.

MnSCU Accounting is complex with manydata elements and fields available for each

Table 4-1 Consistency Testing Of Certain Transaction Types

Consistency of ClassificationsTransaction Type Appropriation Fund

CodeProgram

CodeCustomized Training Revenue for creditcourses applicable towards a degree

C 3 8

Customized Training Revenue for hour basedtraining offered to a targeted customer group

C 3 7

Community Education Revenue (courses notpart of a degree, diploma or certificateprogram)

3 5 8

Customized Training Expenditures C 4 7

Customized Training Expenditures for hourbased training offered to a targeted customergroup

C 4 6

Community Education Expenditures (coursesnot part of a degree, diploma or certificateprogram

3 6 7

Athletic Camp/League Revenue 4 6 5

Parking Fee Revenue 3 5 6

Postage Expenses for academic departments 2* 3* 8*

Phone Expenses for academic departments 3* 3* 7*

Salary expenses for academics departments 3* 3* 5*

Salary expenses for operational departments 4* 5* *

Child Care Center revenue 4 5 6

Child Care Center expenditures 5 6 6

Summer School revenue C 2 5

Summer School expenditures C 2* 5*

Legend:C - Consistent across all institutions who had this type of activity.Numeric - Number of different codes used.

* - Some institutions coded these activities to all appropriations, HEB, funds and programs.

Chapter 4: Financial Data Consistency May 1999

27

transaction – cost centers, bank accounts,activity codes, appropriation codes, fundcodes, grant/projects records, object codes,organization codes, program codes,subprogram codes, tax indicator codes anduser fields. The complexity of theaccounting systems resulted in colleges anduniversities developing disparate solutionsfor coding financial transactions.

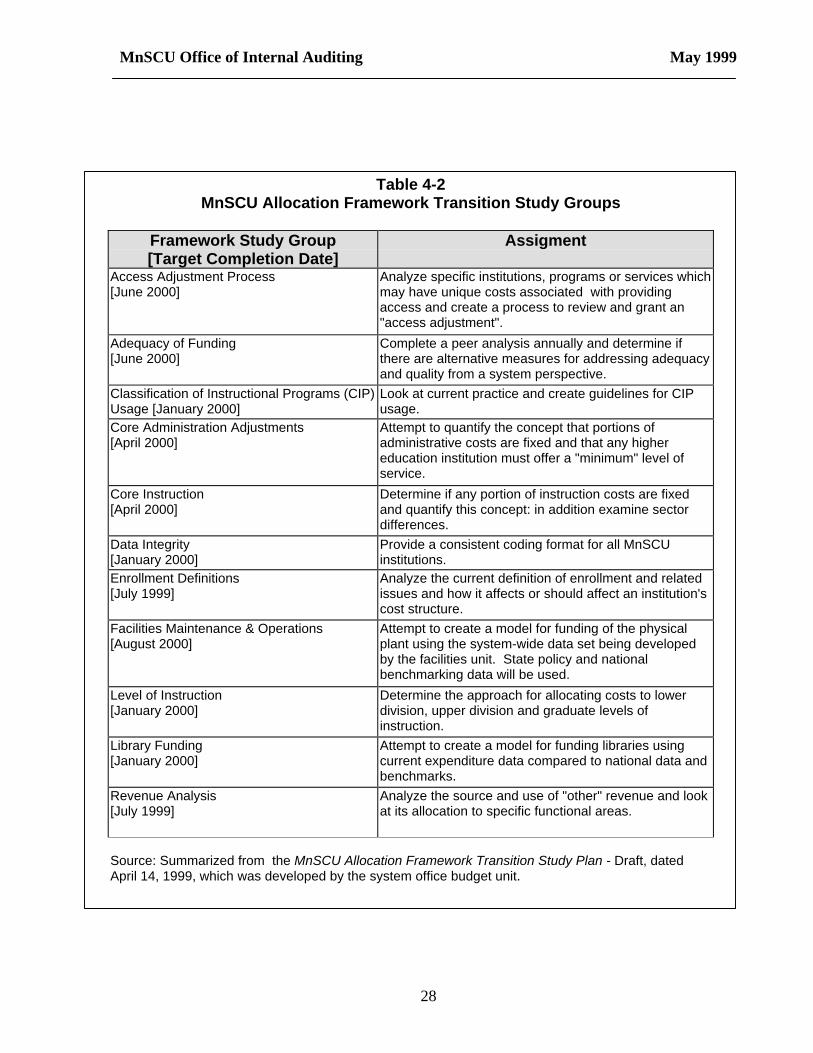

Recognizing the importance of consistentdata standards, the system office hasdeveloped the MnSCU AllocationFramework Transition Study Plan. It isintended to obtain input from theinstitutions and develop standards system-wide. This study plan involves eleven studygroups with system-wide representation tolook at various aspects of the allocationmodel. These study groups were eitheridentified by the Allocation ImplementationCommittee or are a result of issues raised atpublic hearings held throughout the state.Table 4-2 shows the study groups, theirrespective assignments, and timelines.

The Allocation Framework Study Plananticipates that the AllocationImplementation Committee, the PresidentialAllocation Review Committee, theChancellor, and finally the Board ofTrustees will review draft standards. TheData Integrity Group has recently finishednew definitions for program codes.Because this group had already been formedprior to the Allocation FrameworkTransition Study Plan its review andapproval process was slightly different. The

new program definitions were distributed ina memorandum signed by the ViceChancellor for Finance.The development of clear, acceptedstandards is a precursor to establishingconsistent financial data. To ensure generalacceptance of these standards, thedevelopment process must provide a wideexposure of its proposals. All colleges anduniversities must be given the opportunityand ample time to comment on proposedstandards. Finally, a systematic method forcommunicating final standards is needed.The standards will serve as an importantreference tool that must be readilyaccessible when the institutions are makingdecisions about how to code theiraccounting transactions.

Recommendations

ü MnSCU must continue the efforts of thestudy groups and ensure that theirefforts are completed timely.

ü To ensure that guidelines are generallyaccepted, MnSCU must establish andmaintain an appropriate due process fordeveloping, reviewing, and approvingdata standards.

ü A structure must be established andmaintained to ensure that the guidancedeveloped by the study groups arecommunicated and implementedeffectively.

MnSCU Office of Internal Auditing May 1999

28

Table 4-2MnSCU Allocation Framework Transition Study Groups

Framework Study Group[Target Completion Date]

Assigment

Access Adjustment Process[June 2000]

Analyze specific institutions, programs or services whichmay have unique costs associated with providingaccess and create a process to review and grant an"access adjustment".

Adequacy of Funding[June 2000]

Complete a peer analysis annually and determine ifthere are alternative measures for addressing adequacyand quality from a system perspective.

Classification of Instructional Programs (CIP)Usage [January 2000]

Look at current practice and create guidelines for CIPusage.

Core Administration Adjustments[April 2000]

Attempt to quantify the concept that portions ofadministrative costs are fixed and that any highereducation institution must offer a "minimum" level ofservice.

Core Instruction[April 2000]

Determine if any portion of instruction costs are fixedand quantify this concept: in addition examine sectordifferences.

Data Integrity[January 2000]

Provide a consistent coding format for all MnSCUinstitutions.

Enrollment Definitions[July 1999]

Analyze the current definition of enrollment and relatedissues and how it affects or should affect an institution'scost structure.

Facilities Maintenance & Operations[August 2000]

Attempt to create a model for funding of the physicalplant using the system-wide data set being developedby the facilities unit. State policy and nationalbenchmarking data will be used.

Level of Instruction[January 2000]

Determine the approach for allocating costs to lowerdivision, upper division and graduate levels ofinstruction.

Library Funding[January 2000]

Attempt to create a model for funding libraries usingcurrent expenditure data compared to national data andbenchmarks.

Revenue Analysis[July 1999]

Analyze the source and use of "other" revenue and lookat its allocation to specific functional areas.

Source: Summarized from the MnSCU Allocation Framework Transition Study Plan - Draft, datedApril 14, 1999, which was developed by the system office budget unit.

29

Chapter 5: Business Practices May 1999

Chapter Conclusions

Colleges and universities have struggled to maintain effective and efficient businesspractices, partly due to the administrative demands of the financial systems. As aresult, internal controls have not received the necessary attention.

Reliable financial data is the product of adisciplined accounting operation that hasmaintained effective internal controls. Asinternal controls deteriorate, the possibilityof accounting errors increases. Although, itwas not a primary objective of this study,we felt it was vital to consider the followingquestion:

§ Are colleges and universitiesexperiencing any common problems orchallenges in recording accountingfinancial data, e.g. reconciliations?

To address this question, we relied on ourobservation while testing the accountingdata and analyzed prior Office of theLegislative Auditor (OLA) reports. Sincethe merger and through January 1999, theOLA has issued 32 financial audit reports.Since fiscal year 1996, MnSCU has had acontract with the OLA to conductcomprehensive financial audits of itscolleges and universities.

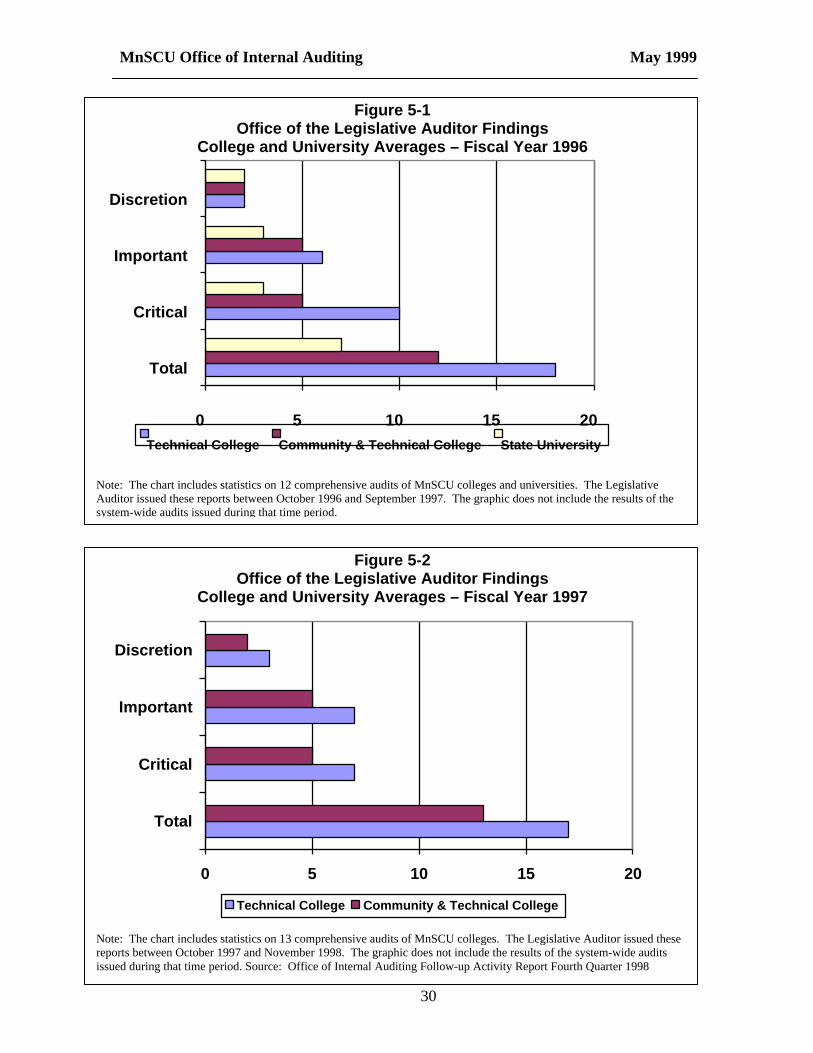

Figures 5-1 and 5-2 compare the averagenumber of audit findings by type ofinstitution for audits covering both fiscalyear 1996 and 1997, the first two years ofthe contract. It is somewhat surprising that

the average number of audit findings hasremained constant by type of institution.The OLA is currently in the process ofcompleting audits of the remaining collegesand universities.

As the organization becomes more stableand colleges and universities gainexperience with the new business systemsone would expect to see the average numberof audit findings decline. Since the merger,however, the MnSCU information systemshave experienced continual change. Asbusiness offices have struggled to learn andimplement constant system changes,attention is diverted from the maintenanceof basic internal controls.

Furthermore, all institutions have notexperienced the same level of success withthe financial systems. Colleges anduniversities operating with the most successgenerally have employees with moreextensive accounting and informationsystem educational backgrounds and largerstaff sizes. The system office is currentlystudying the administrative structure andstaff sizes of business offices. It hopes toidentify a model for maintaining effectivefinancial management practices.

MnSCU Office of Internal Auditing May 1999

30

Figure 5-1Office of the Legislative Auditor Findings

College and University Averages – Fiscal Year 1996

0 5 10 15 20

Total

Critical

Important

Discretion

Technical College Community & Technical College State University

Note: The chart includes statistics on 12 comprehensive audits of MnSCU colleges and universities. The LegislativeAuditor issued these reports between October 1996 and September 1997. The graphic does not include the results of thesystem-wide audits issued during that time period.

Figure 5-2Office of the Legislative Auditor Findings

College and University Averages – Fiscal Year 1997

0 5 10 15 20

Total

Critical

Important

Discretion

Technical College Community & Technical College

Note: The chart includes statistics on 13 comprehensive audits of MnSCU colleges. The Legislative Auditor issued thesereports between October 1997 and November 1998. The graphic does not include the results of the system-wide auditsissued during that time period. Source: Office of Internal Auditing Follow-up Activity Report Fourth Quarter 1998

Chapter 5 - Business Practices May 1999

31

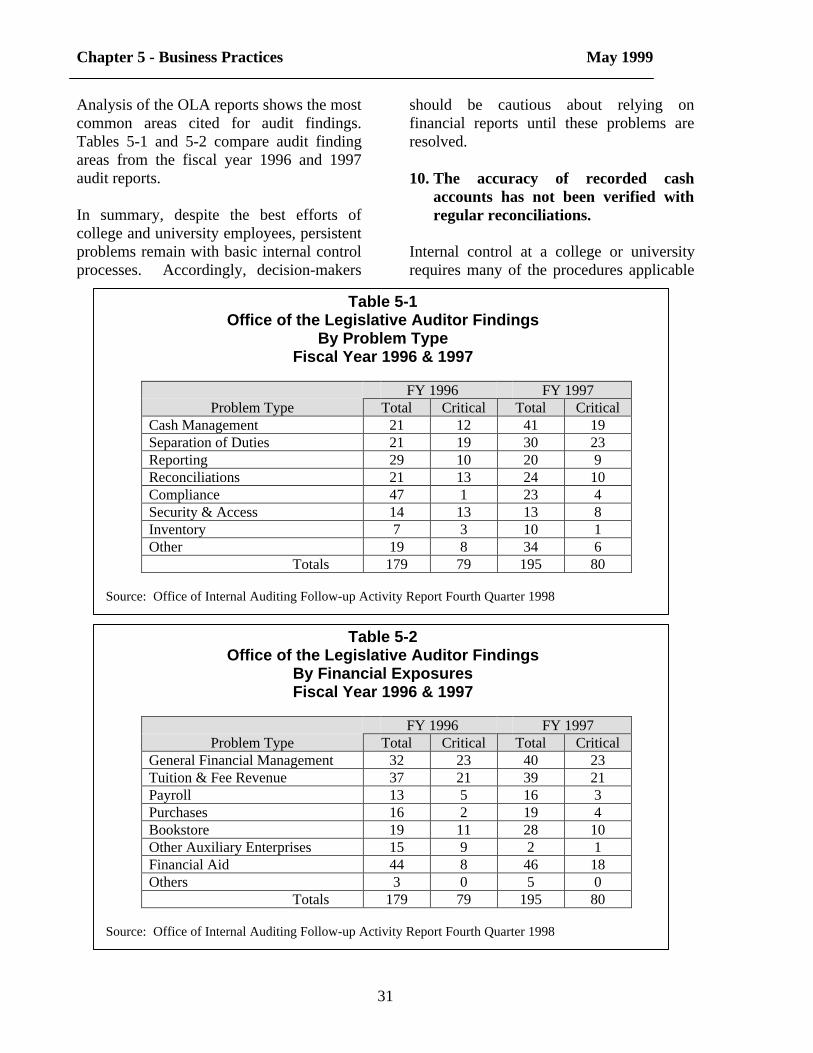

Analysis of the OLA reports shows the mostcommon areas cited for audit findings.Tables 5-1 and 5-2 compare audit findingareas from the fiscal year 1996 and 1997audit reports.

In summary, despite the best efforts ofcollege and university employees, persistentproblems remain with basic internal controlprocesses. Accordingly, decision-makers

should be cautious about relying onfinancial reports until these problems areresolved.

10. The accuracy of recorded cashaccounts has not been verified withregular reconciliations.

Internal control at a college or universityrequires many of the procedures applicable

Table 5-1Office of the Legislative Auditor Findings

By Problem TypeFiscal Year 1996 & 1997

FY 1996 FY 1997Problem Type Total Critical Total Critical

Cash Management 21 12 41 19Separation of Duties 21 19 30 23Reporting 29 10 20 9Reconciliations 21 13 24 10Compliance 47 1 23 4Security & Access 14 13 13 8Inventory 7 3 10 1Other 19 8 34 6

Totals 179 79 195 80

Source: Office of Internal Auditing Follow-up Activity Report Fourth Quarter 1998

Table 5-2Office of the Legislative Auditor Findings

By Financial ExposuresFiscal Year 1996 & 1997

FY 1996 FY 1997Problem Type Total Critical Total Critical

General Financial Management 32 23 40 23Tuition & Fee Revenue 37 21 39 21Payroll 13 5 16 3Purchases 16 2 19 4Bookstore 19 11 28 10Other Auxiliary Enterprises 15 9 2 1Financial Aid 44 8 46 18Others 3 0 5 0

Totals 179 79 195 80

Source: Office of Internal Auditing Follow-up Activity Report Fourth Quarter 1998

MnSCU Office of Internal Auditing May 1999

32

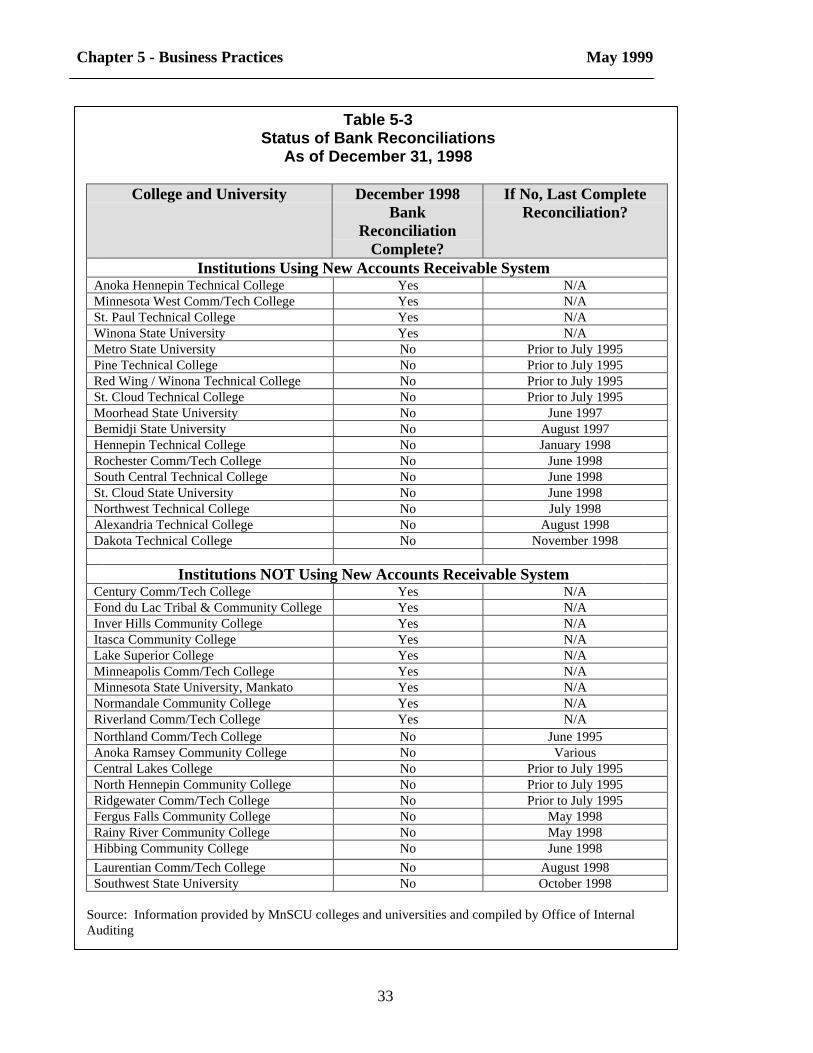

to commercial entities. This includes, but isnot limited to, a sound bank reconciliationprocess. Table 5-1 summarizes the bankreconciliation status as ofDecember 31, 1998 by college anduniversity.

§ Overall, 64% of MnSCU colleges anduniversities (23 of 36) had notsuccessfully reconciled their local bankaccount statement to MnSCUAccounting.

§ 76% of MnSCU colleges anduniversities (13 of 17) who were usingthe new Accounts Receivable systemdid not successfully reconcile their localbank account statement to MnSCUAccounting.

§ 53% of the MnSCU colleges anduniversities (10 of 19) who were notusing the Accounts Receivable systemdid not successfully reconcile their localbank statement to MnSCU Accounting.

Although not limited to the reconciliation ofcash accounts, of the 48 critical OLA auditfindings that were unresolved atMarch 31, 1999, 15 (31.3%) fell into thereconciliation category. As of March 31 1999 the average age of the criticalunresolved reconciliation audit findings was359 days.

Untimely and incomplete bankreconciliations make an organization morevulnerable to losses from fraud. Anorganization may be responsible for anylosses attributable to check fraud if itreasonably should have been discoveredthrough the bank reconciliation process andthe review of cancelled checks. UnderUniform Commercial Code, MinnesotaStatutes Section 336.4-406, customers mustreconcile their bank statements within a

reasonable time to detect unauthorizedchecks. A reasonable time is typicallydefined as not more than 30 days ofreceiving the bank statement.

College and university officials commonlycited the following as barriers preventingthem from successfully reconciling theirlocal bank account statements to MnSCUAccounting in a timely and efficientmanner:

§ Consolidation of local bank accounts,§ Use of the recently implemented

Accounts Receivable system,§ Time constraints and staffing shortages,§ Inability to generate outstanding check

reports as of a specific date,§ Outstanding check reports do not

include check dates,§ Need to generate a second, stand alone,

outstanding check list for institutions,processing disbursements using asecond system (e.g., CIS system),

§ Inconsistency when the State Treasurerremoves state funds from local bankaccounts,

§ Discrepancies in the cash disbursementand the payment amount denoted on thestandard reports, and

§ Transactions posted within theaccounting period with occurrencedates, outside of the accounting periodcannot be easily identified.

As a result, colleges and universities oftendeveloped creative, but operationallyinefficient, workarounds in an attempt toreconcile their bank accounts. Despite thebest efforts of business offices, the endproduct was frequently a bankreconciliation that contained unidentifiedreconciling items.

The system office staff believes that thedifficulties currently encountered by

Chapter 5 - Business Practices May 1999

33

Table 5-3Status of Bank Reconciliations

As of December 31, 1998

College and University December 1998Bank

ReconciliationComplete?

If No, Last CompleteReconciliation?