roland berger trend compendium · compiled by roland berger institute (rbi), the think ... 78.3...

TRANSCRIPT

February 2018

Roland Berger Trend Compendium 2030 Megatrends 1-7 Compact version

2 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

About the Roland Berger Trend Compendium 2030

What is it?

> The Roland Berger Trend Compendium 2030 is a

global trend study compiled by Roland Berger Institute (RBI), the think tank of Roland Berger

> It describes the

most important megatrends that will shape the world between now and 2030

> The megatrends have a broad impact on the environment of companies, strongly influencing

challenges and opportunities of their business

Our approach

> We first screened relevant trend, scenario and future

studies worldwide

> Then we verified, analyzed and

consolidated the results, using them to

define the megatrends

> Next, we broke down the megatrends into

subtrends, looking at each from a global

perspective and the viewpoints of

industrialized and developing countries

3 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

It covers seven megatrends that shape the future development of our world

Demographic dynamics

Globalization & future markets

Scarcity of resources

Climate change & ecosystem at risk

Dynamic technology & innovation

Global knowledge society

Sustainability & global responsibility

Megatrends

1 2 3 4 5 6 7

Megatrend 1 Demographic dynamics

Roland Berger Trend Compendium 2030

5 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Demographic dynamics are a global game changer for all economies and societies – There are four key subtrends

T1 Demographic dynamics: Subtrends

Growth – Global population on the rise

Young vs. old countries – A world full of contrasts

Migration – A world on the move

Urbanization – Megacities vs. wasteland

Subtrends of megatrend "Demographic dynamics"

6 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

The global population will grow by almost 1.2 billion between 2015 and 2030 – But the speed of growth is slowing down

T1.1 Growth – Global population on the rise

Developing countries

Developed countries

World population1) 2015-2030 [bn]

6.1

15.8%

2030

8.6

1.3

7.3

2015

7.4

1.3

World

14

18

16

12

8

6

4

2

0

10

2100 2050 2000 1950 1900 1850 1800

1927: 2

2024: 8

1999: 6

World population 1800-2100 [bn]

+18.5%

1974: 4 2017: 7.6

2100: 11

Medium fertility variant High/Low fertility variant

Source: United Nations World Population Prospects: The 2017 Revision, HYDE

+2.9%

1) 2030 data: medium fertility variant

7 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Average population growth p.a. [m]1)

2.00 – 2.99 1.00 – 1.99 0.00 – 0.99 < 0.00 > 3.00

Nearly 30% of total global population growth between now and 2030 will take place in just three countries: India, Nigeria and Pakistan

T1.1 Growth – Global population on the rise

Key countries in terms of average population growth/decline 2015-2030 [m]

Source: United Nations World Population Prospects: The 2017 Revision

1) Medium fertility variant

8 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

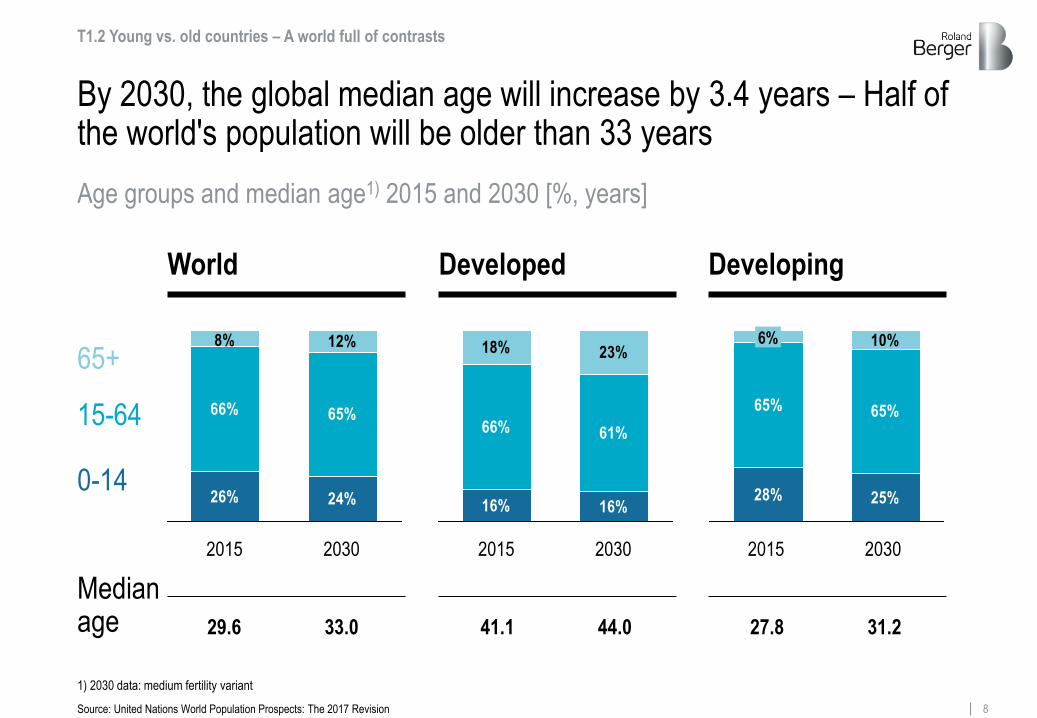

By 2030, the global median age will increase by 3.4 years – Half of the world's population will be older than 33 years

2015 2030

26% 24%

8% 12%

65%66%

29.6 33.0

World

16% 16%

18% 23%

61%66%

Developed

28% 25%

65%65%

10%6%

Developing

2015 2030 2015 2030

27.8 31.2 41.1 44.0

65+

0-14

15-64

Median age

T1.2 Young vs. old countries – A world full of contrasts

Age groups and median age1) 2015 and 2030 [%, years]

Source: United Nations World Population Prospects: The 2017 Revision

1) 2030 data: medium fertility variant

9 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

25,000

45,000

35,000

15,000

5,000

0

The upside of demographics: In developed countries, the elderly save less and spend more

World High-income countries Low and middle income countries

Annual flows per capita

Age

CONSUMPTION

LABOR INCOME

0 10 20 30 40 50 60 70 80 90

Per capita consumption and labor income by age1) [PPP 2010 USD, years]

> Labor income and consumption levels change during a person's lifetime

> In high-income countries consumption has a high plateau between 60 and 80 and increases markedly from the age of 80

> In low and middle income countries spending slightly decreases in old age

T1.2 Young vs. old countries – A world full of contrasts

Source: National Transfer Accounts

1) Aggregating most recent country data ranging from 2005 to 2015

10 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

International migration flows remain but are expected to decrease towards 2030

T1.3 Migration – A world on the move

Africa

Oceania

Asia

Europe Northern America

Latin America and the Caribbean

2000-2015 2015-2030

-22.8 -23.4

21.4

14.1

-6.9 -8.7

17.5 18.1

-4.4 -10.0

2.4 2.5

Source: United Nations World Population Prospects: The 2017 Revision

Selected net migration 2000-2015 vs. 2015-20301) [m]

1) 2030 data: medium fertility variant

11 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Since 2000, the number of international migrants has strongly increased – Only a minority of them are refugees

Development of international migrants1) and refugees2) 2000-2015 [m]

Migrants

1) According to the UN definition, an international migrant is any person who changes his or her country of usual residence for a period of at least three months 2) According to the UN definition, refugees are people owing to a well-founded fear of being persecuted for reasons of race, religion, nationality, membership of a particular social group or political opinion and being outside the country of their nationality. 3.8 million (2000) and 5.3 million (2015) of the refugees were Palestinians (incl. Palestinian population in the Gaza Strip and West Bank)

Refugees

2000 172.7 Million

2015 243.7 Million

15.9 Million 20.7 Million

+ 41.1%

T1.3 Migration – A world on the move

Source: UNESA, UNRWA, UNHCR

12 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

81.5 78.3 74.2

The number of people living in urban areas continues to increase, especially in developing regions

Development of the share of people living in urban areas, 2000-20301) [%]

46.6

+6.0 pps

60.0 54.0

2015 2030 2000 2015 2030 2000 2015 2030 2000

World Developed Developing

+7.2 pps

49.0 56.2

39.9

1) Data of 2030 according to the medium fertility variant of UN's forecast. The definition of urban areas follows the definitions that are used in each country. These definitions can vary widely. The criteria for classifying an area as urban may be based on one or a combination of characteristics, such as: a minimum population threshold, population density, proportion employed in non-agricultural sectors, the presence of infrastructure such as paved roads, electricity, piped water or sewers, and the presence of education or health services

+7.4 pps +9.1 pps

+3.2 pps +4.1 pps

T1.4 Urbanization – Megacities vs. wasteland

Source: UN World Urbanization Prospects: The 2014 Revision

13 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

By 2030, more than half of the 15 biggest urban agglomerations will be located in Asia, with Tokyo still being the largest megacity of all

Population development of the 15 biggest urban agglomerations 2015-20301) [m]

T1.4 Urbanization – Megacities vs. wasteland

Dhaka 2015: 17.6 2030: 27.4

Mexico City 2015: 21.0 2030: 23.9

New York City 2015: 18.6 2030: 19.9

São Paulo 2015: 21.1 2030: 23.4

Karachi 2015: 16.6 2030: 24.8

Lagos 2015: 13.1 2030: 24.2

Kolkata 2015: 14.9 2030: 19.1

Mumbai 2015: 21.0 2030: 27.8

Delhi 2015: 25.7 2030: 36.1

Cairo 2015: 18.8 2030: 24.5

Beijing 2015: 20.4 2030: 27.7

Kinshasa 2015: 11.6 2030: 20.0

Tokyo 2015: 38.0 2030: 37.2

Osaka 2015: 20.2 2030: 20.0

Shanghai 2015: 23.7 2030: 30.8

= 2015 = 2030

1) 15 biggest urban agglomerations in 2030 in descending order: Tokyo, Delhi, Shanghai, Mumbai (Bombay), Beijing, Dhaka, Karachi, Cairo, Lagos, Mexico City, São Paulo, Kinshasa, Osaka, New York City and Kolkata

Source: UN World Urbanization Prospects: The 2014 Revision

14 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

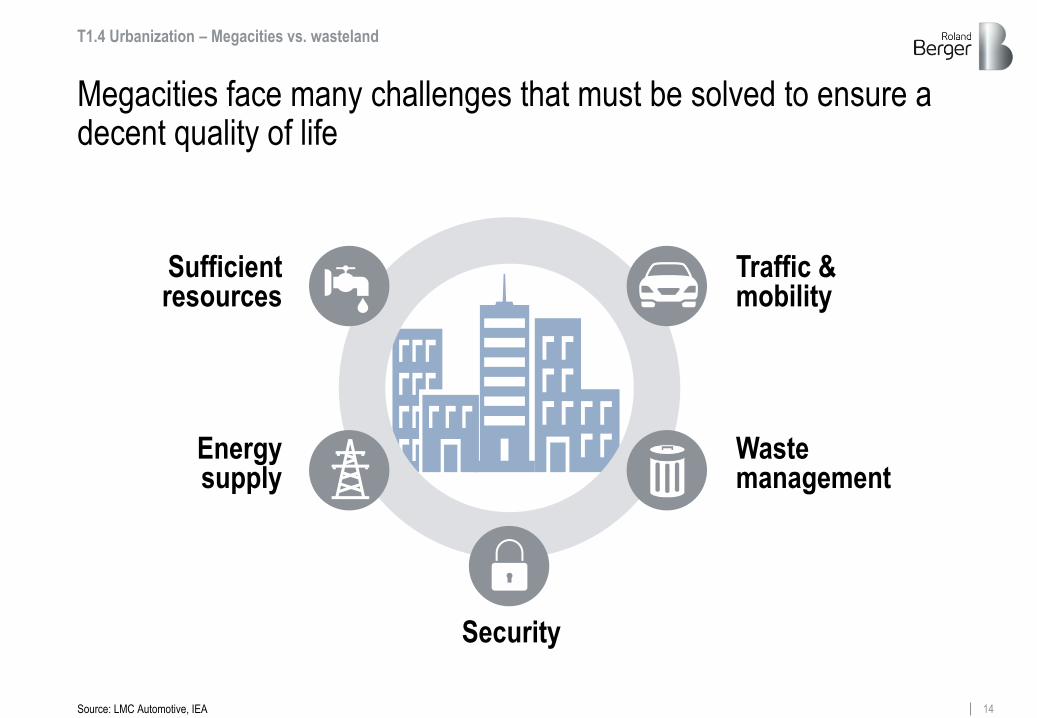

Megacities face many challenges that must be solved to ensure a decent quality of life

Traffic & mobility

Sufficient resources

Security

Energy supply

Waste management

T1.4 Urbanization – Megacities vs. wasteland

Source: LMC Automotive, IEA

Megatrend 2 Globalization & future markets

Roland Berger Trend Compendium 2030

16 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Globalization and the emergence of new markets will challenge countries, societies and economies – There are three key subtrends

T2 Globalization & future markets: Subtrends

Facets of globalization – Parameters are changing

Economic integration – Exports and FDIs are growing

BRICS and beyond – Future pathways are diverging

Subtrends of megatrend "Globalization & future markets"

17 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Globalization should be understood and analyzed in all its economic, political and social facets

> Imports and exports

> Trade agreements

> Cross-border investments

> Growth opportunities for developing countries

> Process of digitalization

> Globalized and connected society

> Linkage of governments

> Increasing reciprocity

> Trend of protectionism

T2.1 Facets of globalization – Parameters are changing

18 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

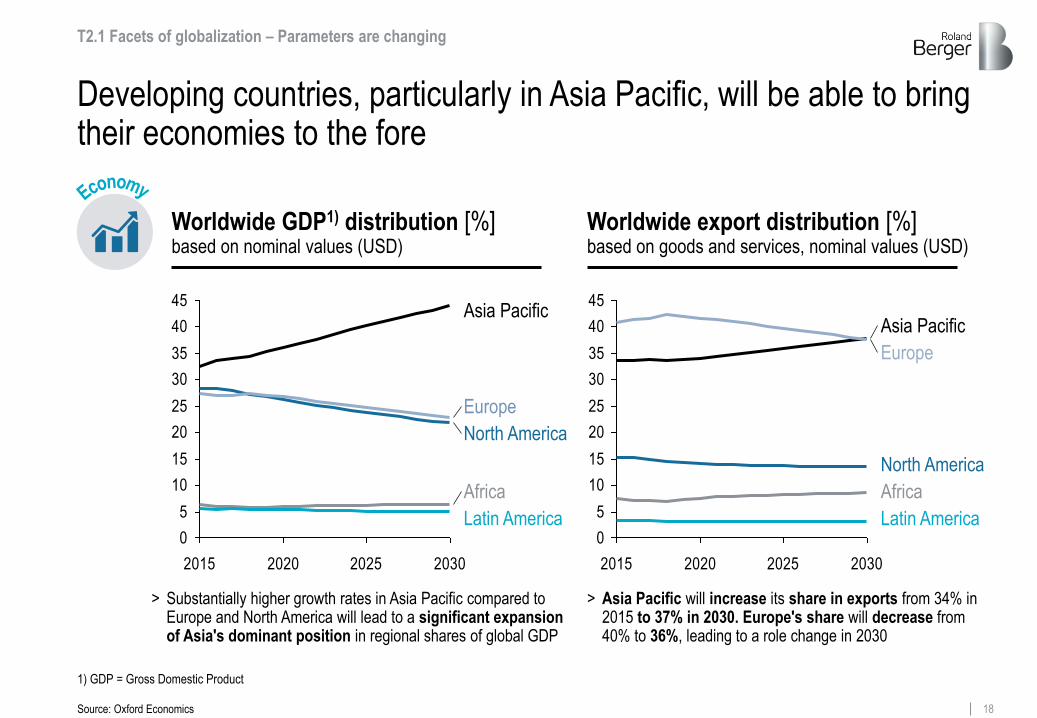

Developing countries, particularly in Asia Pacific, will be able to bring their economies to the fore

Worldwide GDP1) distribution [%] based on nominal values (USD)

Worldwide export distribution [%] based on goods and services, nominal values (USD)

> Substantially higher growth rates in Asia Pacific compared to Europe and North America will lead to a significant expansion of Asia's dominant position in regional shares of global GDP

> Asia Pacific will increase its share in exports from 34% in 2015 to 37% in 2030. Europe's share will decrease from 40% to 36%, leading to a role change in 2030

0

5

10

15

20

25

30

35

40

45

2015 2020 2025 2030

Europe

Asia Pacific

Latin America

North America

Africa

0

5

10

15

20

25

30

35

40

45

2015 2020 2025 2030

Africa

Europe

Asia Pacific

Latin America

North America

T2.1 Facets of globalization – Parameters are changing

Source: Oxford Economics

1) GDP = Gross Domestic Product

19 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Globalization triggers advocacy as well as opposing views taking on a geopolitical dimension in the context of global affairs

T2.1 Facets of globalization – Parameters are changing

Globalization proponents Globalization opponents

Source: The Washington Post

"Make our planet great again."

"America first."

"Our leaders chose globalization, which they wanted to be a happy thing. It turned out to be a horrible thing."

Emmanuel Macron, June 2017

Donald J. Trump, 2016

Marine Le Pen, February 2017

"If trade stops, war starts."

Jack Ma1), February 2017

"Many of the problems troubling the world are not caused by economic globalization."

Xi Jinping, 2017

20 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Finally, digitalization and growing global data traffic has the potential to change key parameters of globalization

49

35

24

17

117

4

CAGR +52%

2021 2020 2019 2018 2017 2016 2015

> Growing interconnection between countries

> Data flows form the basis of economic and social interaction

> Asia Pacific will take over largest portion of data traffic

> 71% of internet users already come from developing countries

T2.1 Facets of globalization – Parameters are changing

Global mobile data traffic [Exabytes per month]

Digitalization changes markets & societies

Note: CAGR = Compound annual growth rate

Source: Cisco, Euromonitor, ITU

21 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Global trade flows show strong inter- and intraregional relationships

Interregional and intraregional merchandise exports, 2016 [bn USD, %]

Source: WTO

T2.2 Economic integration – Exports and FDIs are growing

Russia/CIS Total: 421

Asia Pacific Total: 5,274

52%

18%

North America Total: 2,215

South and Central America Total: 512

Africa Total: 348

Europe Total: 5,948

Middle East Total: 776

50%

Interregional merchandise exports [USD bn] Bubble: size = total merchandise exports f.o.b., light blue section = intraregional share (exports between countries inside a specific region); dark blue section = interregional share (exports between regions) 100-300 300-800 >800

22% 20%

69%

11%

22 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

2015

22

Exports of goods and services as share of GDP are already at a high level – The global average will see little growth

Source: Oxford Economics

15.2% 18.7%

South/Central America

Europe Russia/

CIS

Africa

Middle East

Asia Pacific

North America 43.1% 51.1%

16.4% 17.5%

31.5% 32.3% 29.1%

25.6%

44.7% 53.1%

22.0% 25.6%

World

28.1% 29.8%

2030

Exports, goods and services as share of GDP (nominal) 2015 and 2030

T2.2 Economic integration – Exports and FDIs are growing

23 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

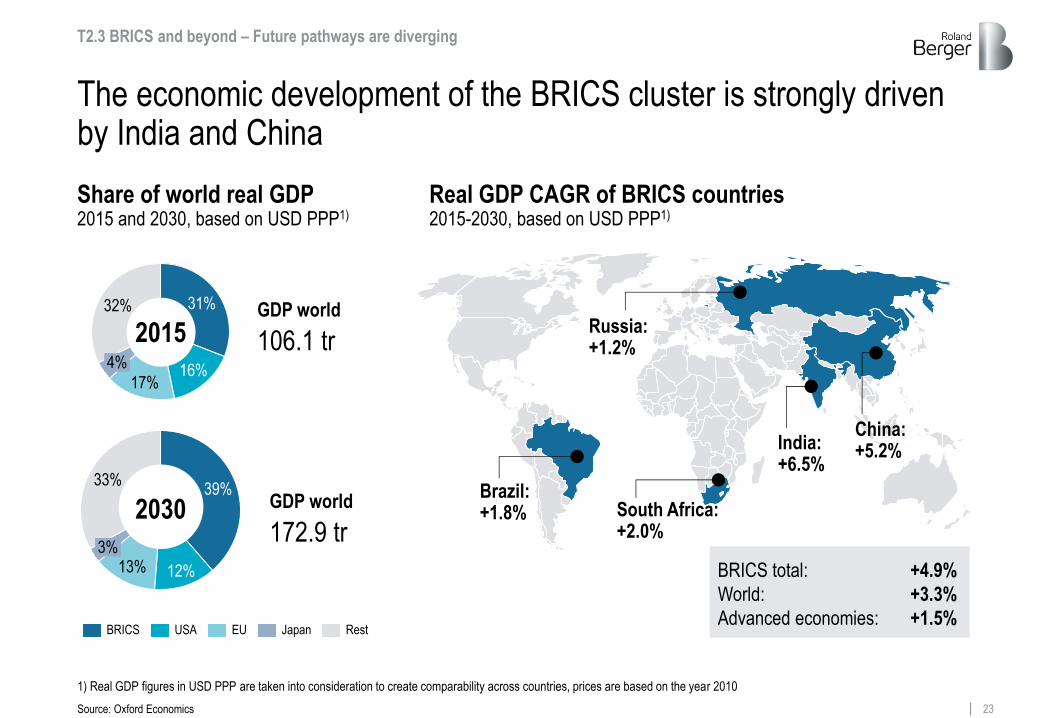

The economic development of the BRICS cluster is strongly driven by India and China

Real GDP CAGR of BRICS countries 2015-2030, based on USD PPP1)

Brazil: +1.8%

South Africa: +2.0%

Russia: +1.2%

India: +6.5%

China: +5.2%

Share of world real GDP 2015 and 2030, based on USD PPP1)

BRICS total:

World:

Advanced economies:

+4.9%

+3.3%

+1.5%

T2.3 BRICS and beyond – Future pathways are diverging

Source: Oxford Economics

1) Real GDP figures in USD PPP are taken into consideration to create comparability across countries, prices are based on the year 2010

17%

4% 16%

31% 32%

12% 13% 3%

39% 33%

Japan USA EU BRICS Rest

GDP world

106.1 tr

GDP world

172.9 tr

2015

2030

24 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

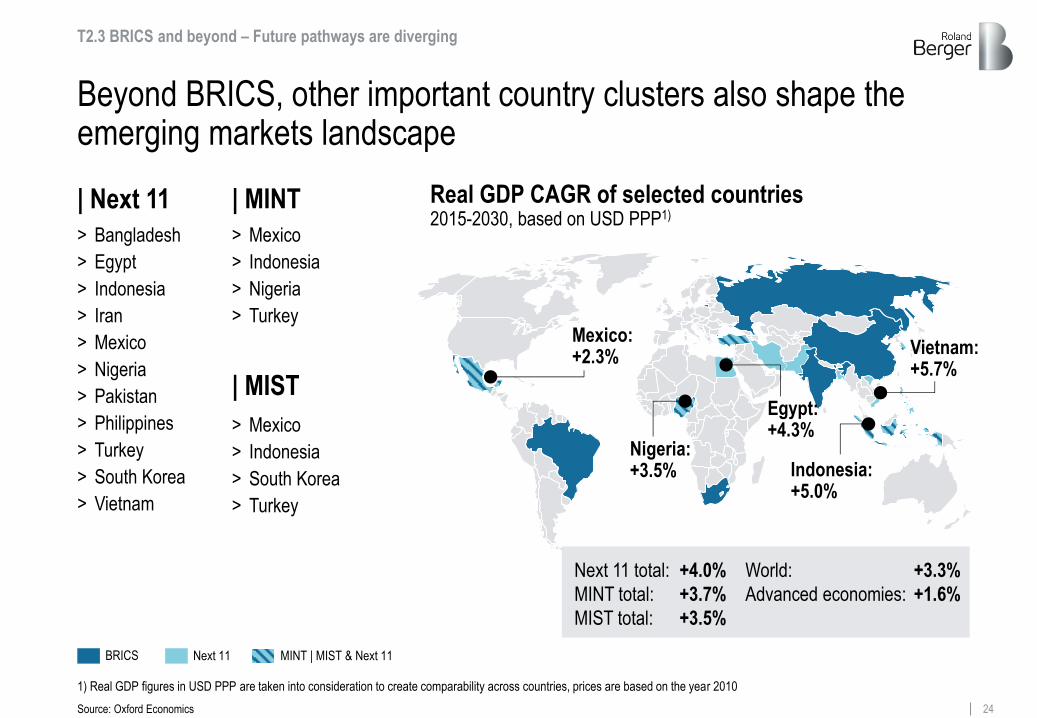

Beyond BRICS, other important country clusters also shape the emerging markets landscape

BRICS Next 11 MINT | MIST & Next 11

Real GDP CAGR of selected countries 2015-2030, based on USD PPP1)

Next 11 total:

MINT total:

MIST total:

+4.0%

+3.7%

+3.5%

Nigeria: +3.5%

Mexico: +2.3%

Egypt: +4.3%

Vietnam: +5.7%

Indonesia: +5.0%

T2.3 BRICS and beyond – Future pathways are diverging

Source: Oxford Economics

| Next 11

> Bangladesh

> Egypt

> Indonesia

> Iran

> Mexico

> Nigeria

> Pakistan

> Philippines

> Turkey

> South Korea

> Vietnam

> Mexico

> Indonesia

> Nigeria

> Turkey

> Mexico

> Indonesia

> South Korea

> Turkey

| MIST

| MINT

World:

Advanced economies:

+3.3%

+1.6%

1) Real GDP figures in USD PPP are taken into consideration to create comparability across countries, prices are based on the year 2010

Megatrend 3 Scarcity of resources

Roland Berger Trend Compendium 2030

26 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Scarcity of resources leads to global challenges – There are three key subtrends

T3 Scarcity of resources: Subtrends

Energy – GDP growth in emerging markets is fueling the demand for energy

Water and food – Satisfying the world's hunger and thirst with limited sources

Other commodities – Mastering regional imbalances

Subtrends of megatrend "Scarcity of resources"

27 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Global primary energy demand will increase by 17% to 2030 –predominantly driven by strong growth of demand in Asian countries

Evolution of primary energy demand 2015-2030 By sources [Gtoe1)] and by regions [Mtoe1)]

Fossil fuels Renewable & Others

+ 17%

14.2

16.7

79.1%

81.5%

14.3%

4.8%

13.7%

6.3%

2030

2015

GDP Growth

Population Growth

Urbanization

Expanding middle class

Energy efficiency gains

Sectoral Change

Drivers of Demand

T3.1 Energy – GDP growth in emerging markets is fueling the demand for energy

China

1,966 2,400

Asia/Pacific (excl. China, India)

2,990

3,744

India

1,309 883

2015 2030 Nuclear

1) Gtoe = Gigatonnes of oil equivalent, Mtoe = Megatonnes of oil equivalent

Source: ExxonMobil, Roland Berger

28 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

North America, CIS and Austral-Asia have the largest energy resources – Middle East with strong reserves, but small resources

Reserves1)

Resources2)

Cumulative production

191 124 36 52

192 77

2,385

4,658 410

110

57

181

40 32

298

230 87

4,743

46 22

192

T3.1 Energy – GDP growth in emerging markets is fueling the demand for energy

1) Reserves: Deposits which are known in detail and can be recovered economically using current technologies 2) Resources: Deposits which are either proved but are at present not economically recoverable, or which are not demonstrated, but can be expected for geological reasons

Source: BGR

Fossil energy production, reserves and resources, 2015 [Gtoe]

Resources: Reserves: Production 2015: Cumulative production until 2015:

12,906 918 12

451

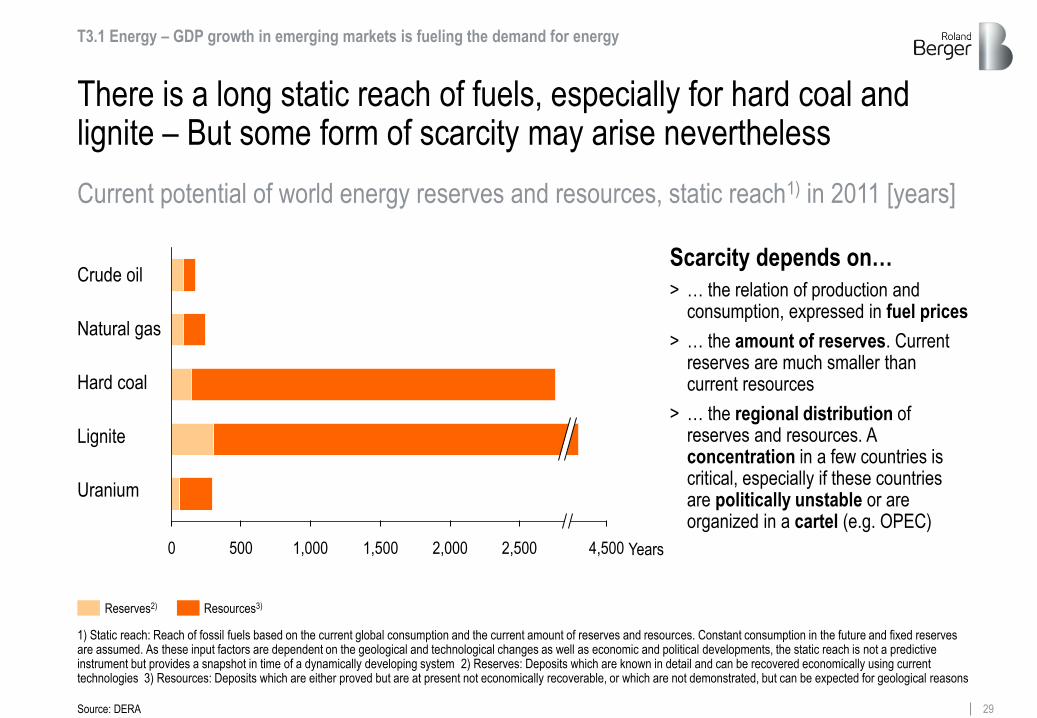

29 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

4,500 2,500 2,000 1,500 1,000 500 0

There is a long static reach of fuels, especially for hard coal and lignite – But some form of scarcity may arise nevertheless

Current potential of world energy reserves and resources, static reach1) in 2011 [years]

Scarcity depends on…

> … the relation of production and consumption, expressed in fuel prices

> … the amount of reserves. Current reserves are much smaller than current resources

> … the regional distribution of reserves and resources. A concentration in a few countries is critical, especially if these countries are politically unstable or are organized in a cartel (e.g. OPEC)

Hard coal

Lignite

Uranium

Crude oil

Natural gas

Years

T3.1 Energy – GDP growth in emerging markets is fueling the demand for energy

1) Static reach: Reach of fossil fuels based on the current global consumption and the current amount of reserves and resources. Constant consumption in the future and fixed reserves are assumed. As these input factors are dependent on the geological and technological changes as well as economic and political developments, the static reach is not a predictive instrument but provides a snapshot in time of a dynamically developing system 2) Reserves: Deposits which are known in detail and can be recovered economically using current technologies 3) Resources: Deposits which are either proved but are at present not economically recoverable, or which are not demonstrated, but can be expected for geological reasons

Reserves2) Resources3)

Source: DERA

30 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Global water demand will increase by 32% to 2050, driven heavily by the growing use for manufacturing and electricity

Global water demand 2015-20501) [km3]

Renewable internal freshwater resources 2014 [m3/inhabitant]

+ 32%

Irrigation & Livestock

No data < 500 500-1000 1000-1700 1700-5000 > 5000

56%

38%

20%

22%

13%

14%

Electricity Domestic Manufacturing

T3.2 Water and food – Satisfying the world's hunger and thirst with limited sources

5,467

4,135

12%

25%

2050

2015

GDP growth

Population growth

Growing food demand

Climate change

Efficiency gains

Drivers of demand

Source: OECD, FAO, Roland Berger

1) The values of 2015 are linearly extrapolated with the values of 2000 and 2050

31 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Future food price developments are difficult to predict – They are influenced by many factors and are subject to uncertainties

Demography Efficiency gains Population growth

Urbanization

Eating habits

Economic growth GDP growth emerging markets

Demand

Financial markets speculation

Trade policies

Geopolitical dynamics

Production

Wastage

Supply Prices Water and soil

Scarcity of resources

Climate change

Increasing temperature

Source: Barilla Centre, The European House-Ambrosetti, IPCC

Increase in calories

Changing consumer habits (more meat) ?

Oil and energy prices

Decline in nutritional value

Foreign exchange Fertilizer prices

T3.2 Water and food – Satisfying the world's hunger and thirst with limited sources

Influence factors on the development of food prices

32 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

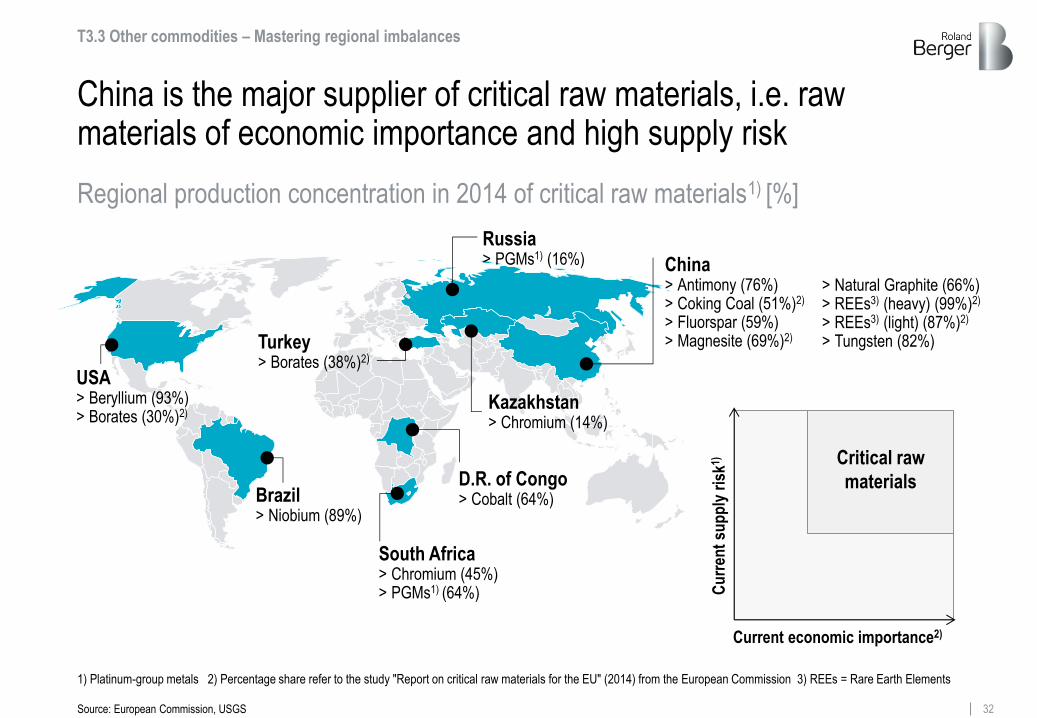

China is the major supplier of critical raw materials, i.e. raw materials of economic importance and high supply risk

T3.3 Other commodities – Mastering regional imbalances

China > Antimony (76%) > Coking Coal (51%)2) > Fluorspar (59%) > Magnesite (69%)2)

> Natural Graphite (66%) > REEs3) (heavy) (99%)2) > REEs3) (light) (87%)2) > Tungsten (82%)

USA > Beryllium (93%) > Borates (30%)2)

Brazil > Niobium (89%)

South Africa > Chromium (45%) > PGMs1) (64%)

D.R. of Congo > Cobalt (64%)

Turkey > Borates (38%)2)

Russia > PGMs1) (16%)

Kazakhstan > Chromium (14%)

Regional production concentration in 2014 of critical raw materials1) [%]

Current economic importance2)

Cu

rren

t su

pp

ly r

isk1)

Critical raw

materials

1) Platinum-group metals 2) Percentage share refer to the study "Report on critical raw materials for the EU" (2014) from the European Commission 3) REEs = Rare Earth Elements

Source: European Commission, USGS

Megatrend 4 Climate change & ecosystem at risk

Roland Berger Trend Compendium 2030

34 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Interdependencies of climate change and ecosystem trends require global answers and solutions – There are three key subtrends

Global warming – The core of climate change

Rising CO2 emissions – Non-OECD as accelerant

Ecosystem at risk – Threatened basis of life

T4 Climate change & ecosystem at risk: Subtrends

Subtrends of megatrend "Climate change & ecosystem at risk"

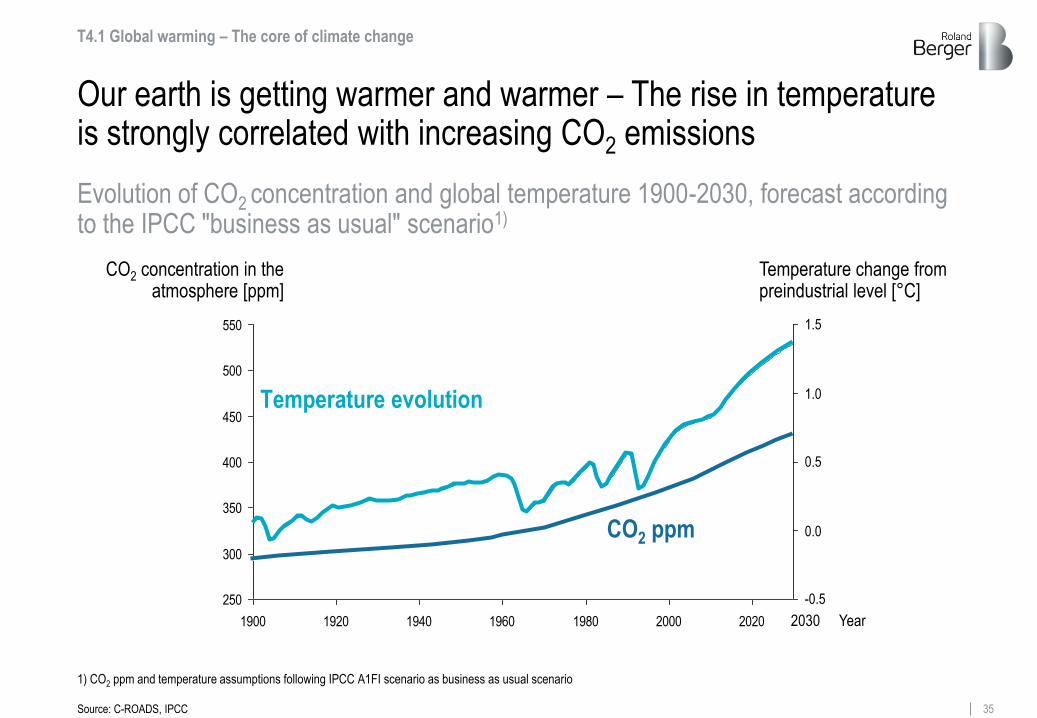

35 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

250

300

350

400

450

500

550

1900 1920 1940 1960 1980 2000 2020

1.0

0.5

0.0

-0.5

1.5

Our earth is getting warmer and warmer – The rise in temperature is strongly correlated with increasing CO2 emissions

Temperature change from preindustrial level [°C]

CO2 concentration in the atmosphere [ppm]

Year

T4.1 Global warming – The core of climate change

2030

Evolution of CO2 concentration and global temperature 1900-2030, forecast according to the IPCC "business as usual" scenario1)

CO2 ppm

Temperature evolution

Source: C-ROADS, IPCC

1) CO2 ppm and temperature assumptions following IPCC A1FI scenario as business as usual scenario

36 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Global warming has marked effects worldwide – yet regional impacts differ

Scarcity of fresh water Food scarcity Wildfire Extinction of species Flood damages Health problems (due to heat 6 diseases)

Loss of coastal infrastructure, settlements, natural habitats

North America

Central & South America

Europe

Africa

Small Islands (Maldives e.g.)

Asia

Australia/ Oceania

Oceans

Antarctica

Arctic

Natural disasters: Scarcity of resources: Impact on species: Impact on health:

Change of species appearance (concerning fishery e.g.)

Low crop yields

T4.1 Global warming – The core of climate change

Important impacts of climate change in different world regions

Source: IPCC, AFP, BZ

37 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

20

25

30

35

40

45

2000 2005 2010 2015 2020 2025 2030

Limiting global warming requires measures to reduce greenhouse gas emissions – CO2 being the most significant

T4.2 Rising CO2 emissions – Non-OECD as accelerant

Global CO2 emissions under different scenarios1) and composition of GHG emissions2)

1) CO2 emissions from fuel combustion and industrial processing. 6°C and 2°C scenarios according to IEA describing different global warming scenarios, referring to average global

temperature rise above pre-industrial levels by 2100 2) GHG = Green house gas, emissions' split refers to 2010 data of IPCC 2014 report 3) Gt = Gigatonnes 4) GtCO2e = Gigatonnes

CO2 equivalent

Source: IEA, EIA, IPCC

IEA 6°C Scenario "Business as usual"

IEA 2°C Scenario

> Higher energy efficiency

> CO2 capture and storage

> More renewables

> …

Global GHG emissions 2013: 54 GtCO2e4)

Others

8%

16%

Methane 76% CO2

Global CO2 emissions under different scenarios

Gt3)

Composition of GHG emissions

38 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx Source: IEA

Total CO2 emissions in selected regions 2013 and 2030 according to the 6°C and the 2°C IEA scenarios [Gt1)]

Asia and North America are key: Future CO2 emissions highly depend on actions being taken by China, India and the USA

USA China

South Africa

Brazil

India Mexico

Global

European Union

ASEAN

5.5

3.0

5.3

0.6 0.4

0.4

0.7 0.4

0.5

13.2

8.7

10.0

5.4

3.3 2.0

3.4

2.2

3.7

2.9

1.9 1.4

0.6 0.4

0.5

45.1

28.6

33.9

2013 2030, 6°C scenario – "Business as usual" 2030, 2°C scenario

1) Gt = Gigatonnes

T4.2 Rising CO2 emissions – Non-OECD as accelerant

39 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

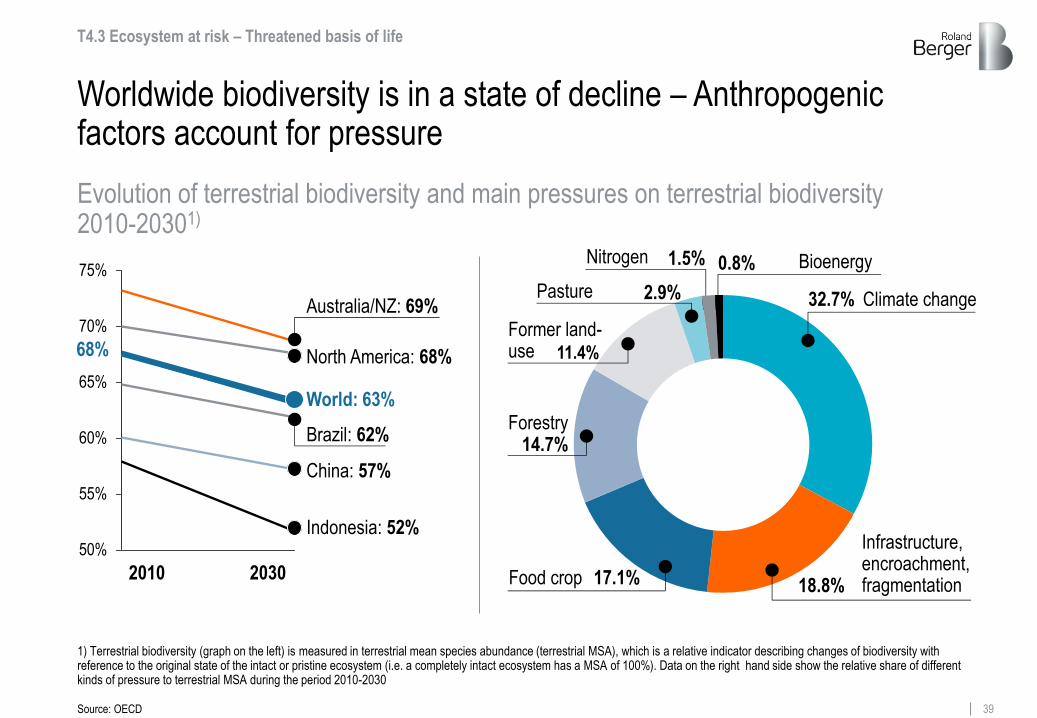

Worldwide biodiversity is in a state of decline – Anthropogenic factors account for pressure

2010 2030

50%

55%

60%

65%

70%

75%

Australia/NZ: 69%

North America: 68%

World: 63%

Brazil: 62%

China: 57%

Indonesia: 52%

Evolution of terrestrial biodiversity and main pressures on terrestrial biodiversity 2010-20301)

11.4%

14.7%

17.1%

Infrastructure, encroachment, fragmentation Food crop

Forestry

Former land-use

Bioenergy

Pasture

Nitrogen

1) Terrestrial biodiversity (graph on the left) is measured in terrestrial mean species abundance (terrestrial MSA), which is a relative indicator describing changes of biodiversity with reference to the original state of the intact or pristine ecosystem (i.e. a completely intact ecosystem has a MSA of 100%). Data on the right hand side show the relative share of different kinds of pressure to terrestrial MSA during the period 2010-2030

68%

Climate change 32.7%

0.8% 1.5%

2.9%

18.8%

T4.3 Ecosystem at risk – Threatened basis of life

Source: OECD

40 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Over 60% of the earth's biocapacity is held by only ten countries, most suffer from heavy land and forest degradation

Shares of global biocapacity Shares of global forest degradation

Brazil

China

D.R. Congo

Others

Argentina

Indonesia

USA

Russia

Canada

India

Australia

14.8

10.6

9.8

8.1

4.7

4.6

3.0 2.5

2.4

1.6

38.1 Brazil 14.2

China 0.5

USA 6.1

Russia 20.4

Canada 21.4

Australia 3.3

Indonesia 3.7

2.6 D.R. Congo

Others 27.8

National shares of global biocapacity and forest degradation1) in 2013 [%]

T4.3 Ecosystem at risk – Threatened basis of life

1) Measured as degradation of intact forest landscape (IFL): IFL is an unbroken expanse of natural ecosystems within the zone of current forest extent, showing no signs of significant human activity, and large enough that all native biodiversity could be maintained. Biocapacity is the ecosystems’ capacity to produce useful biological materials and to absorb waste

Source: Global Footprint Network, Intact Forest Landscapes

Megatrend 5 Dynamic technology & innovation

Roland Berger Trend Compendium 2030

42 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Dynamic technology & innovation are major, central forces in today's business environment – There are three key subtrends

T5 Dynamic technology & innovation: Subtrends

Power of innovation – Driver of economic prosperity

Life Sciences – Addressing major challenges of humanity

Digital Transformation – The digital economy is here

Subtrends of megatrend "Dynamic technology & innovation"

43 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Today we still face major challenges, yet many promising fields of innovation are poised to overcome these challenges by 2030

> Provide enough water, food and healthcare

> Use resources more efficiently

> Cope with increasing energy and transportation demand

> Reduce waste and pollution

> Fight climate change

> …

> Life Sciences

> Digital Transformation

> Materials science

> New mobility

> Environmental science

> …

Major challenges for humanity

Fields of innovation

2030

Selected major challenges and fields of innovation towards 2030

T5.1 Power of innovation – Driver of economic prosperity

44 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

0 50 100 150 200 250 300 350 400 450

80,000

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0

90,000

South Africa

Singapore Sweden

Spain

Russia

Netherlands

South Korea

Japan

Italy

India

Israel UK France

Germany

China

Switzerland

Brazil

Belgium Austria

USA

Developed countries BRICS

Innovation drives wealth – BRICS countries have to catch up, although two Chinese corporations among largest PCT applicants

Largest corporate PCT applicants 2015

GDP per capita and PCT1) applications relative to population in 2016

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

Huawei (3,898; CN)

Qualcomm(2,442; US)

ZTE (2,155; CN)

Samsung (1,683; KR)

Mitsubishi (1,593; JP)

Ericsson (1,481; SE)

LG (1,457; KR)

Sony (1,381; JP)

Philips (1,378; NL)

HP (1,310; US)

Patent applications per 1 mio inhabitants

GDP per capita [USD]

T5.1 Power of innovation – Driver of economic prosperity

Source: IMF, Wipo, WEForum

1) Patent Cooperation Treaty: Intellectual property rights enforced in 148 countries worldwide

45 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

The powerful network of biology, chemistry and pharmaceuticals in Life Sciences provides answers to future challenges of humanity

T5.2 Life Sciences – Addressing major challenges of humanity

Medical devices

Ecology

Genetics

Neurosciences

Marine biology

Pharmaceutical sciences

Biophysics

Health sciences Biochemistry

Environ-mental pollution

Marine pollution

Chronic & age-related diseases

Growing demand for food & water

Contagious diseases

Source: PwC, Deloitte, Roland Berger

Selected fields of Life Sciences & important challenges associated with Life Sciences

46 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

In terms of patent publications by origin of applicant, Asian countries are catching up – the US and Europe are loosing out

1) PCT (Patent Cooperation Treaty): Intellectual property rights enforced in 148 countries worldwide) applications here refer to analysis of biological materials, medical technology, biotechnology, pharmaceuticals, food chemistry, environmental technology

Selected PCT Life Sciences1) publications by origin of applicant [% of global total]

T5.2 Life Sciences – Addressing major challenges of humanity

2016 2006

8.9 Japan 12.5

China 1.5

South Korea 2.1

Other countries 8.6 Japan 14.2

China 6.9

South Korea 5.6

USA 36.6 Europe 28.1 USA 43.2 Europe 31.9

Other countries

28,199 34,736

Source: Wipo

47 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

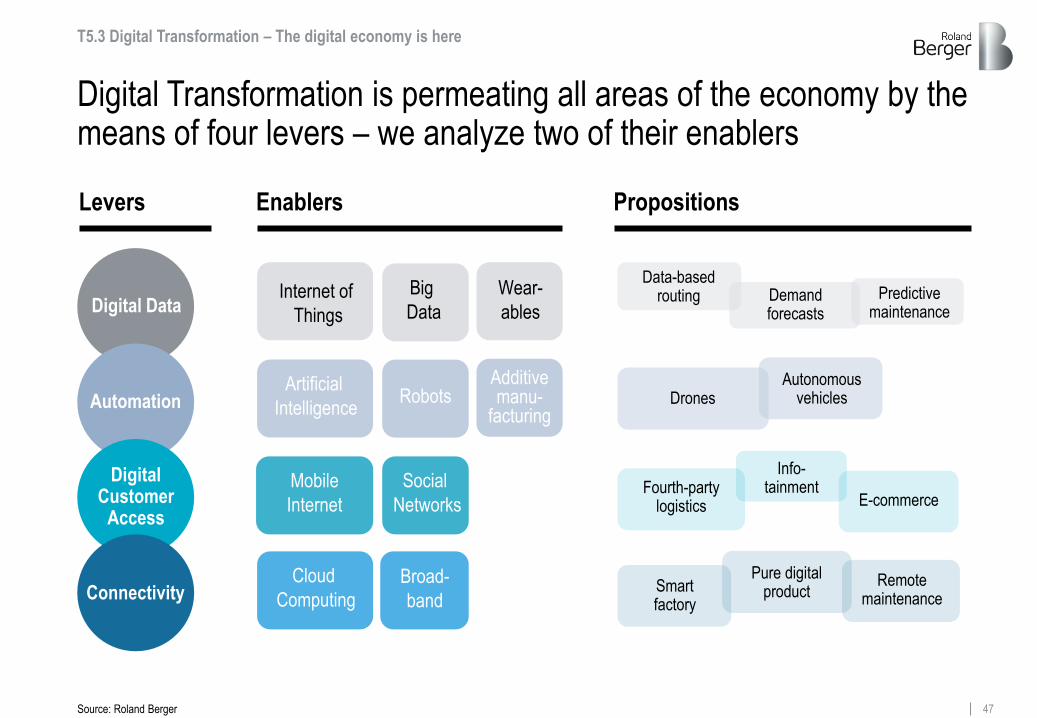

T5.3 Digital Transformation – The digital economy is here

Digital Transformation is permeating all areas of the economy by the means of four levers – we analyze two of their enablers

Source: Roland Berger

Automation

Connectivity

Digital Customer

Access

Artificial

Intelligence

Internet of

Things

Levers Enablers

Additive manu-

facturing

Social

Networks

Mobile

Internet

Cloud

Computing

Big

Data

Robots

Wear-

ables

Broad-

band

Propositions

Digital Data

Pure digital product Smart

factory

Remote maintenance

Info- tainment Fourth-party

logistics E-commerce

Drones Autonomous

vehicles

Demand forecasts

Data-based routing Predictive

maintenance

48 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

The Internet of Things is an important enabler of Digital Transformation and its growth is accelerating

Source: Ericsson, Roland Berger

Development of connected devices 2015-2021 [bn]

2015 2021

T5.3 Digital Transformation – The digital economy is here

1.3

4.6

+83.1%

2.4

15.4

1.4

28.2

2.8

8.7

15.3

7.1

PC, labtop, tablet

M2M and consumer electronics Mobile phones

Fixed phones

Levers Enablers

Internet of

Things

Automation

Connectivity

Digital Customer

Access

Digital Data

49 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

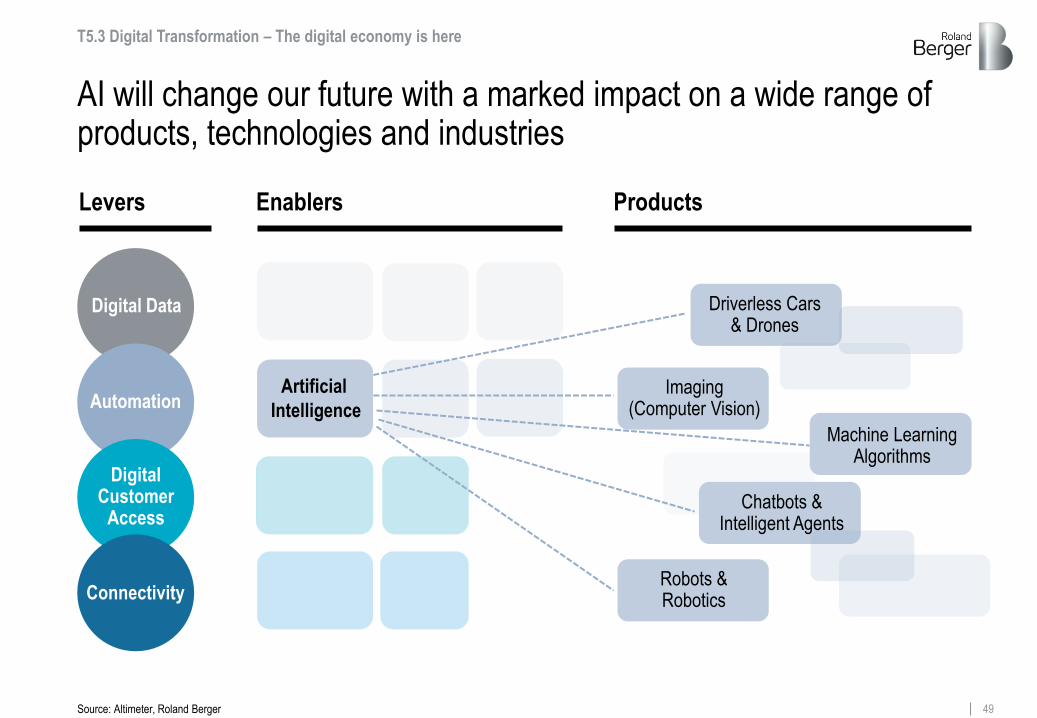

AI will change our future with a marked impact on a wide range of products, technologies and industries

Driverless Cars & Drones

Chatbots & Intelligent Agents

Machine Learning Algorithms

Imaging (Computer Vision)

Robots & Robotics

T5.3 Digital Transformation – The digital economy is here

Levers Enablers Products

Artificial

Intelligence

Source: Altimeter, Roland Berger

Automation

Connectivity

Digital Customer

Access

Digital Data

50 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

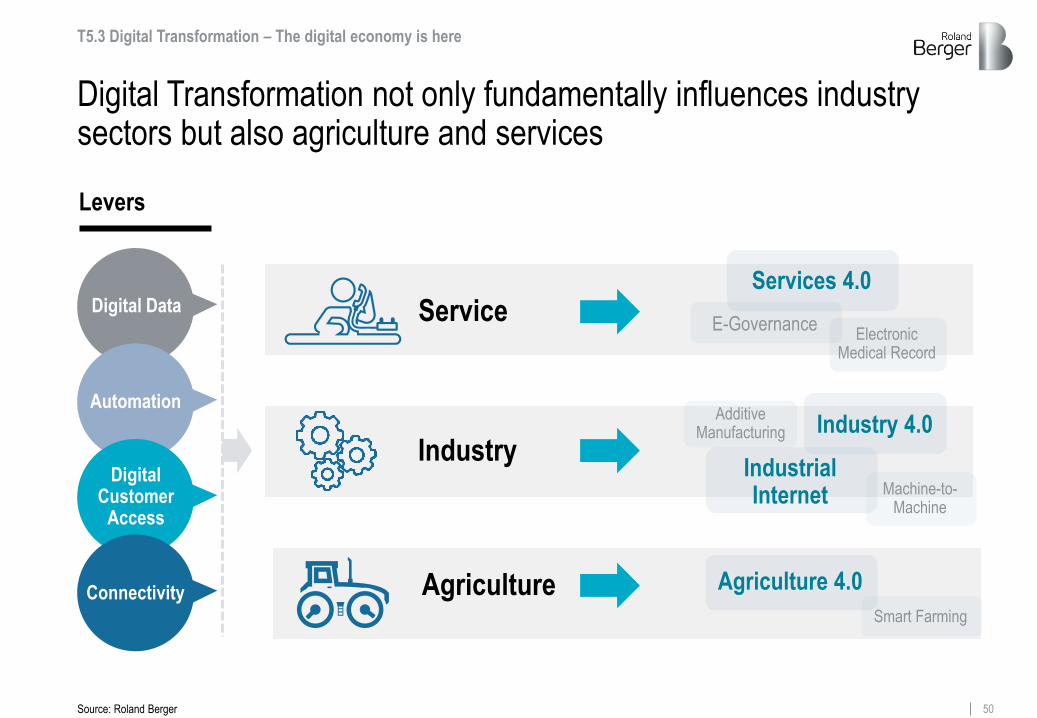

Digital Transformation not only fundamentally influences industry sectors but also agriculture and services

Industry

Agriculture

Service

T5.3 Digital Transformation – The digital economy is here

Levers

E-Governance

Services 4.0

Additive Manufacturing Industry 4.0

Industrial Internet

Electronic Medical Record

Machine-to-Machine

Agriculture 4.0

Smart Farming

Source: Roland Berger

Automation

Connectivity

Digital Customer

Access

Digital Data

51 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

The digital economy requires platform thinking as the basis for new value creation – Leveraging network effects is key to success

Platform-driven business models

Source: Roland Berger, Yahoo Finance

Traditional thinking Platform thinking

Consumer Marketing Distribution Production

Platform Ecosystem

vs.

Revenues 8.2 bn 4.7 bn

Market Cap. 80 bn 74 bn (Time Warner Inc.)

Unique users >1 bn 140 mn

T5.3 Digital Transformation – The digital economy is here

Megatrend 6 Global knowledge society

Roland Berger Trend Compendium 2030

53 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Knowledge is becoming increasingly multidisciplinary, the war for talent will intensify and gender gaps will narrow

T6 Global knowledge society: Subtrends

Know-how base – Increasing knowledge diffusion

Gender gap – Bridging the distance

War for talent – Rising skills shortage as a key challenge

Subtrends of megatrend "Global knowledge society"

54 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

5 6 7 8 9 10 11 12 13 14

60,000

50,000

40,000

30,000

10,000

0

20,000

United States

United Kingdom

Turkey Russia

Korea Japan Italy

Indonesia

India

Germany

France

China Brazil

Australia

Years spent in education – prerequisite and benchmark of a strong know-how base – clearly pay off in terms of financial prosperity

Years of education

GDP per capita PPP

Source: IMF, University of Denver

Average number of years of education completed in 2015 related to GDP per capita PPP in 20161) [years, USD]

1) Number of years of education completed by people aged 25 years and older; PPP stands for purchasing power parity. They are taken into consideration to create comparability across countries. Here measured in current international dollar

T6.1 Know-how base – Increasing knowledge diffusion

55 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

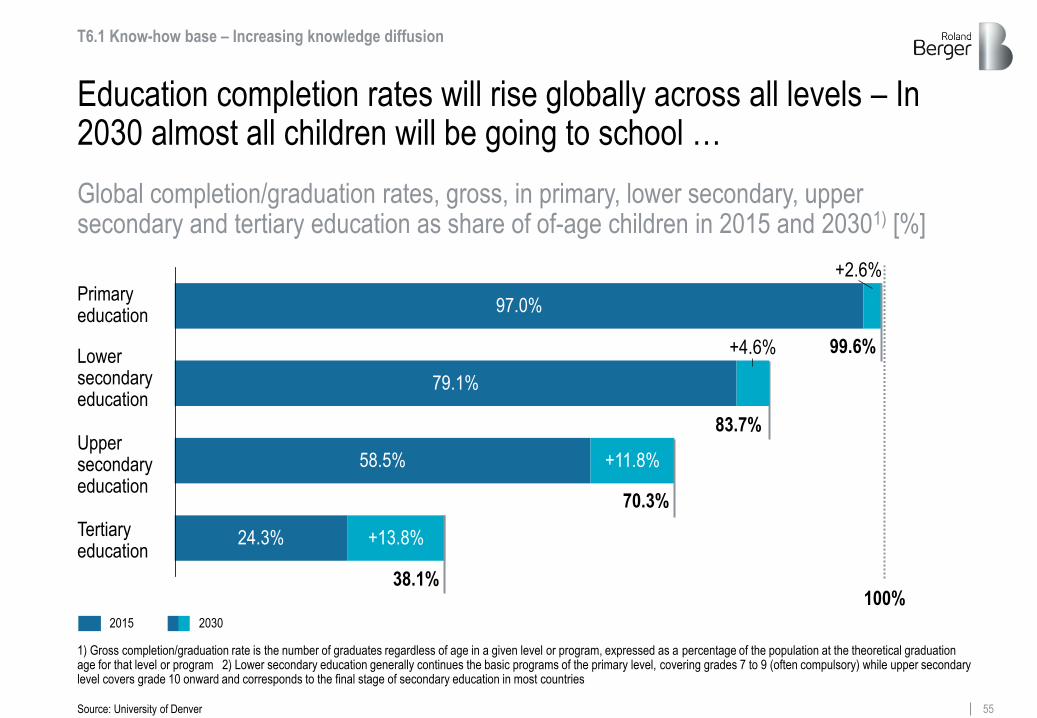

Education completion rates will rise globally across all levels – In 2030 almost all children will be going to school …

Global completion/graduation rates, gross, in primary, lower secondary, upper secondary and tertiary education as share of of-age children in 2015 and 20301) [%]

Tertiary education

Upper secondary education

Lower secondary education

Primary education

+2.6%

97.0%

24.3%

79.1%

58.5%

+4.6%

+11.8%

+13.8%

2015

100% 38.1%

70.3%

83.7%

99.6%

2030

T6.1 Know-how base – Increasing knowledge diffusion

1) Gross completion/graduation rate is the number of graduates regardless of age in a given level or program, expressed as a percentage of the population at the theoretical graduation age for that level or program 2) Lower secondary education generally continues the basic programs of the primary level, covering grades 7 to 9 (often compulsory) while upper secondary level covers grade 10 onward and corresponds to the final stage of secondary education in most countries

Source: University of Denver

56 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

2015 2030

… having a vital impact on fundamental skills: Regarding literacy rates, Asia and Africa will strongly catch up in the next decades

Africa

81% 66%

Asia-Pacific

91% 84%

T6.1 Know-how base – Increasing knowledge diffusion

World

Niger

57% 19%

India

Nigeria

80% 60%

Afghanistan

70% 38%

84% 72%

91% 85%

Average literacy rates 2015 and 2030 [% of population aged 15+]

Source: University of Denver

57 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Developed countries with a declining population will feel talent shortages most acutely – bar some exceptions

Projected change in working age population 2015-20301) [%]

2.9

14.0

-4.8

2.3

Turkey

-10.2

Russia Japan

-10.5 -11.1 -9.7

-8.8

Germany Netherlands South Korea Italy UK USA

1) Based on medium fertility variant of UN population forecasts. Working age population is defined as those aged 15 to 64

T6.2 War for talent – Rising skills shortage as a key challenge

Source: UN World Population Prospects: The 2017 Revision, Roland Berger

58 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Even countries with growing populations such as Turkey, USA and UK already face difficulties in filling job vacancies

T6.2 War for talent – Rising skills shortage as a key challenge

86%

49%

Japan

Germany

India

France

USA

23%

China

UK

Switzerland

Turkey 66%

48% 46%

18% 20%

10%

Percentage of companies in having difficulties filling jobs 2016

Top 10 jobs employers are having difficulty in filling 2016

Skilled trade workers

Sales re-presentatives

Engineers Technicians

Accounting & finance staff

Management/ Executives

Office support staff

Production/ Machine operations

IT Staff

Drivers

1 3 4 2

7 6 10 9 8

5

Brazil 43%

Talent shortages in leading economies and top 10 jobs with shortages 2016

Sources: Manpower Group

59 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Globally speaking, the increasing number of graduates provides a chance to mitigate the intense war for talent

137m

2013 2030

Others 16% China 17%

Mexico 3%

UK 3%

Indonesia 4%

Brazil 4%

Korea 4%

Japan 6%

Russia 10% US 14%

India

14%

Others 18%

Japan 3%

Saudi Arabia 3%

Russia 4%

Indonesia 5%

Brazil 5%

US 8%

China 27%

India

23%

300m

Share of 25-34 year-olds with a tertiary degree across OECD and G20 countries

Developed countries Developing countries

Source: OECD

T6.2 War for talent – Rising skills shortage as a key challenge

60 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

The war for talent calls for efforts to narrow the gender gap – In terms of education, labor force participation and disposable income

Years of education

Labor force participation

T6.3 Gender gap – Bridging the distance

Disposable income

> America & Europe enjoy gender parity in terms of years spent in education

> In Africa & Asia the gap is narrowing towards 2035

> Regarding labor participation, Scandinavian countries are the benchmark

> Forecasts show stagnation of current indicators

> Women earn significantly less than men

> The future will only bring slight improvements

Three factors that are important regarding the gender gap

Source: University of Denver, ILO, UN, Euromonitor

Megatrend 7 Sustainability & global responsibility

Roland Berger Trend Compendium 2030

62 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

1

2

3

4

5

6

Sustainability comprises three actionable areas of responsibility, influenced by six megatrends and shaped by three stakeholders

STAKEHOLDER State

T7 Sustainability & global responsibility

Demographic

Dynamics

Globalization &

future markets

Scarcity of

resources

Climate change &

ecosystem at risk

Dynamic technology

& innovation

Global know-

ledge society

"Sustainability is the responsible development that meets the needs of the present without compromising the ability of future generations to meet their own needs."

(World Commission on Environment and Development – Brundtland Commission)

Sustainability

STAKEHOLDER Society

STAKEHOLDER Businesses

Source: Adams "The future of sustainability", Roland Berger, World Commission on Environment and Development

63 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

We focus on what the three key stakeholders can do to foster a globally sustainable level of development

State – Cooperation or conflict

Society – Citizens and NGOs change the world

Businesses – Corporate citizens on duty

T7 Sustainability & global responsibility: Subtrends

Subtrends of megatrend "Sustainability & global responsibility"

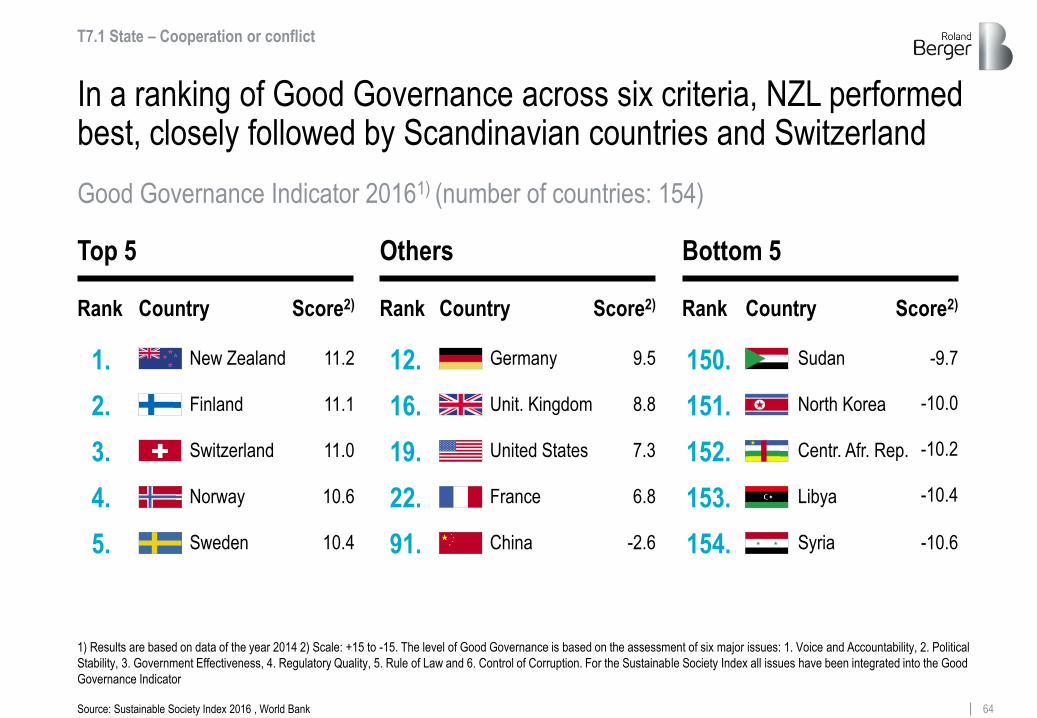

64 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Good Governance Indicator 20161) (number of countries: 154)

In a ranking of Good Governance across six criteria, NZL performed best, closely followed by Scandinavian countries and Switzerland

Source: Sustainable Society Index 2016 , World Bank

T7.1 State – Cooperation or conflict

Top 5

1.

2.

3.

4.

5.

Bottom 5 Others

Rank

New Zealand

Finland

Switzerland

Norway

Sweden

Country Score2)

11.2

11.1

11.0

10.6

10.4

12.

16.

19.

22.

91.

Rank

Germany

Unit. Kingdom

United States

France

China

Country Score2)

9.5

8.8

7.3

6.8

-2.6

150.

151.

152.

153.

154.

Rank

Sudan

North Korea

Centr. Afr. Rep.

Libya

Syria

Country Score2)

-9.7

-10.0

-10.2

-10.4

-10.6

1) Results are based on data of the year 2014 2) Scale: +15 to -15. The level of Good Governance is based on the assessment of six major issues: 1. Voice and Accountability, 2. Political

Stability, 3. Government Effectiveness, 4. Regulatory Quality, 5. Rule of Law and 6. Control of Corruption. For the Sustainable Society Index all issues have been integrated into the Good

Governance Indicator

65 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

When it comes to the future of governmental sustainability there are both promising as well as worrying signs

Select examples of recent sustainable and non-sustainable governmental actions

Source: Roland Berger, Oxford Economics

> Many violent conflicts that threaten sustainable actions (e.g. Syria/Middle East)

> Closed-border policies towards refugees in many countries

> Failure of TTIP trade deal

> US withdrawal from the Paris Agreement

> Tensions between USA and North Korea

T7.1 State – Cooperation or conflict

> Strong efforts of many countries to reduce their fiscal deficit and government debt

> "Historic understanding" (Obama) with Iran about its nuclear program

> Intense international cooperation to manage the Greek crisis

> Strong efforts in many countries to foster a "green economy"

> Negotiation and signing of the Paris (Climate) Agreement

Sustainable government actions Non-sustainable government actions

66 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Official development assistance of many donor countries does not reach UN target, including some of the most developed ones

T7.1 State – Cooperation or conflict

0.08 0.07

0.12

UN target: 0.70% Three least assisting countries

Three most assisting countries

Sweden

0.70

0.70 0.38

0.26

0.26

0.20

0.18

1.11

1.00

0.94 Luxembourg

Norway

Other selected OECD countries

Israel

Japan

United States

Italy

Canada

France

United Kingdom

Germany

Latvia

Slovak Republic

Official development assistance of selected OECD countries 2016 [% of national GNI]

Source: OECD

67 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

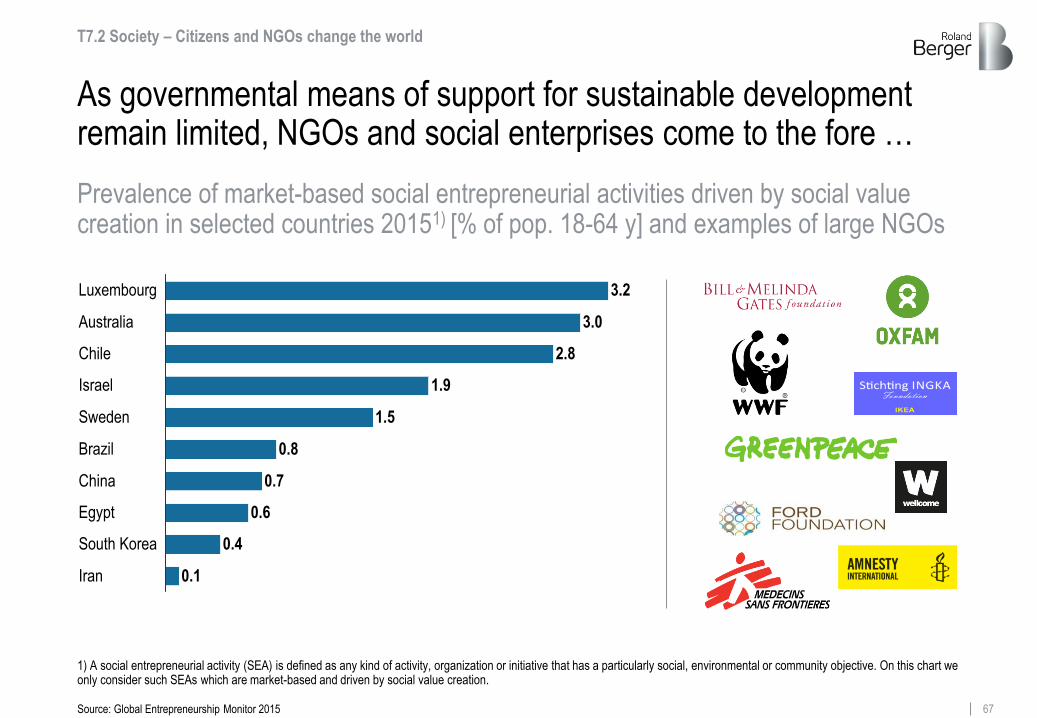

As governmental means of support for sustainable development remain limited, NGOs and social enterprises come to the fore …

0.6 Egypt

China 0.7

Brazil 0.8

Sweden 1.5

Israel 1.9

Chile 2.8

Australia 3.0

Luxembourg 3.2

0.1

South Korea

Iran

0.4

Prevalence of market-based social entrepreneurial activities driven by social value creation in selected countries 20151) [% of pop. 18-64 y] and examples of large NGOs

1) A social entrepreneurial activity (SEA) is defined as any kind of activity, organization or initiative that has a particularly social, environmental or community objective. On this chart we only consider such SEAs which are market-based and driven by social value creation.

T7.2 Society – Citizens and NGOs change the world

Source: Global Entrepreneurship Monitor 2015

68 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

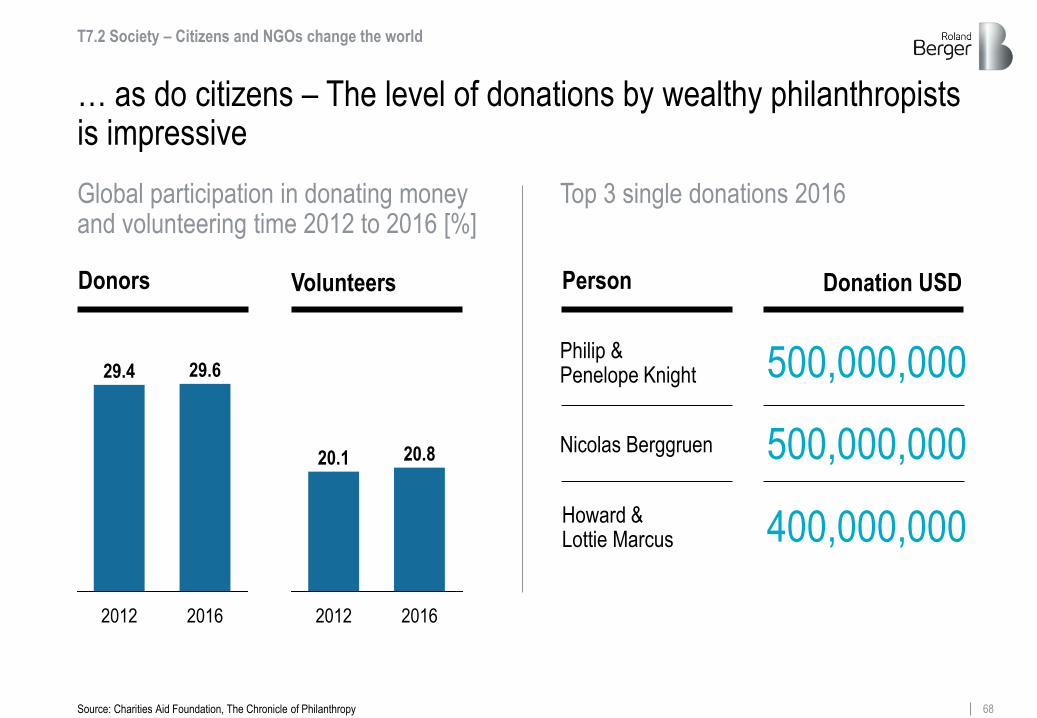

… as do citizens – The level of donations by wealthy philanthropists is impressive

Donors Volunteers

Global participation in donating money and volunteering time 2012 to 2016 [%]

Top 3 single donations 2016

Person Donation USD

T7.2 Society – Citizens and NGOs change the world

Source: Charities Aid Foundation, The Chronicle of Philanthropy

Philip & Penelope Knight

Nicolas Berggruen

Howard & Lottie Marcus

500,000,000

500,000,000

400,000,000

2012

29.4

2016

29.6

2016

20.8

2012

20.1

69 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Customer demands and pressure from other stakeholder groups drive companies to act as good corporate citizens

Corporate Citizen

Customers Employees

Suppliers

Shareholders

Society & local

communities

Government

Media

T7.3 Businesses – Corporate citizens on duty

Corporate citizens stand up for:

Relevant stakeholders of companies acting as corporate citizens

> A respectful relationships with their employees

> A trust-based and sustainable cooperation with suppliers

> A 'green' supply chain

> Enhanced corporate value due to sustainable growth for their shareholders

> Environmental preservation & social contribution

> A "client first, quality first" strategy

Source: Toyota, Roland Berger

70 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

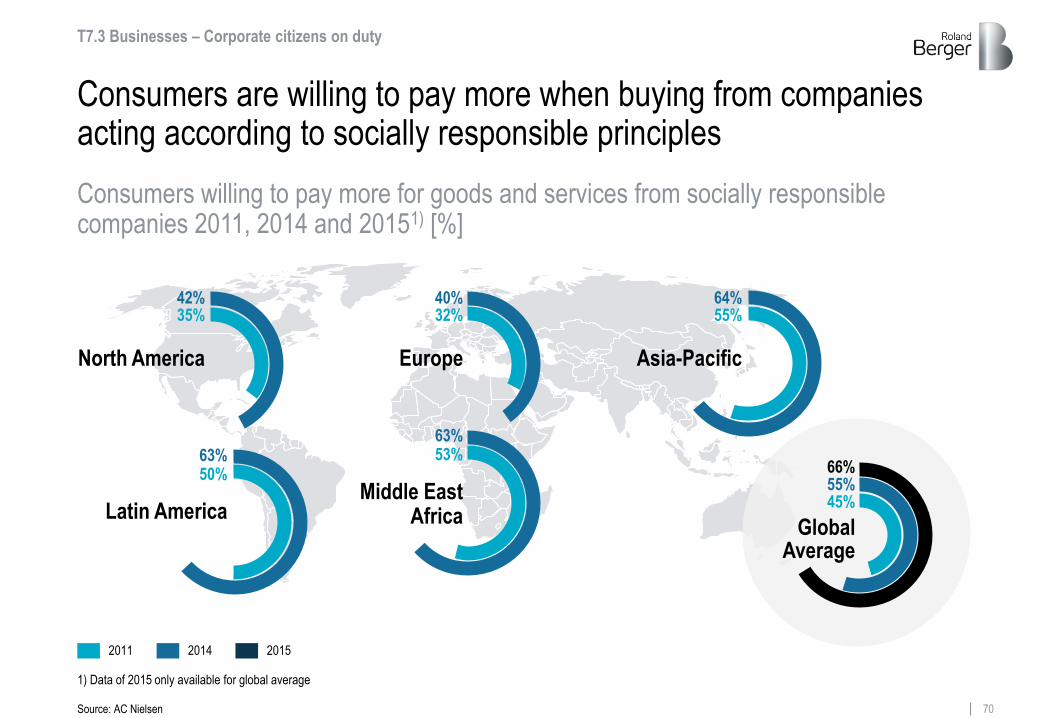

Asia-Pacific

64% 55%

Latin America

63% 50%

Middle East Africa

63% 53%

North America

42% 35%

Europe

40% 32%

Global Average

55% 45%

2011 2014

Consumers are willing to pay more when buying from companies acting according to socially responsible principles

Consumers willing to pay more for goods and services from socially responsible companies 2011, 2014 and 20151) [%]

2015

66%

Source: AC Nielsen

1) Data of 2015 only available for global average

T7.3 Businesses – Corporate citizens on duty

71 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

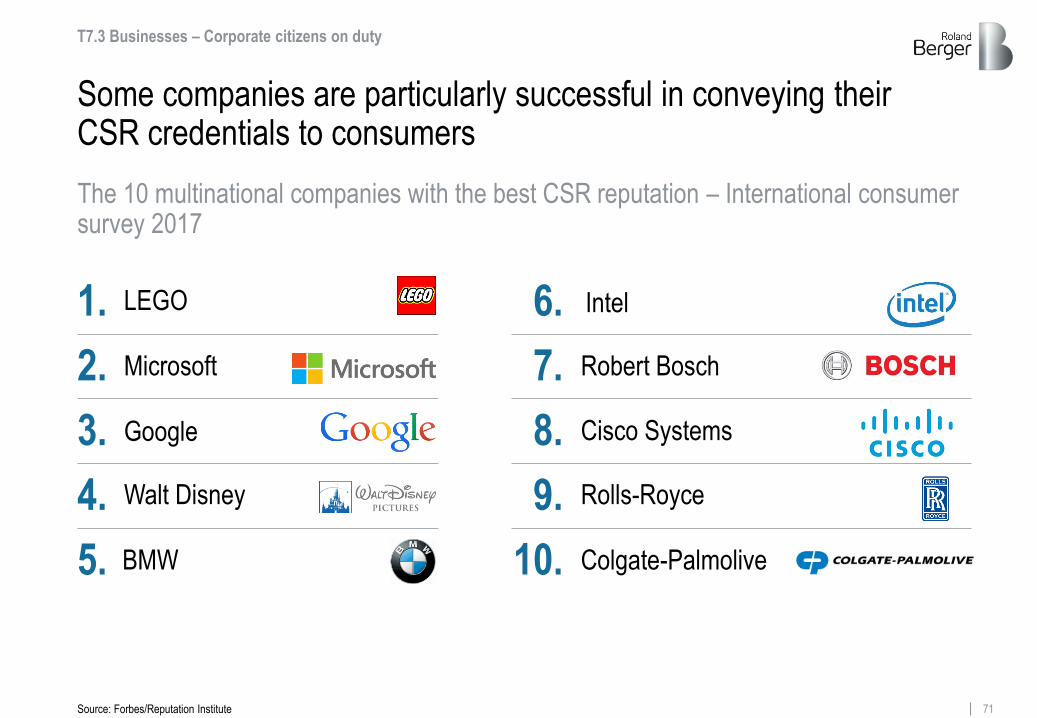

Some companies are particularly successful in conveying their CSR credentials to consumers

Microsoft

Walt Disney

BMW

LEGO

Rolls-Royce

Intel 1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

Robert Bosch

Cisco Systems

Colgate-Palmolive

Source: Forbes/Reputation Institute

The 10 multinational companies with the best CSR reputation – International consumer survey 2017

T7.3 Businesses – Corporate citizens on duty

72 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

Conclusion: Megatrends shape our societies, our economies and our natural environment

Demographic dynamics: World population is growing, aging, migrating and increasingly living in big cities

Globalization & future markets: Ongoing globalization caught between opponents and proponents, power shift to emerging markets

Scarcity of resources: Scarcity of energy resources nuanced, water stress increasing, China holds quasi-monopoly on critical raw materials

Climate change & ecosystem at risk: CO2 emissions and average global temperature increasing, biodiversity decreasing

1

3

4

5

6

7

Dynamic technology & innovation: Innovation drives prosperity, Life Sciences and digital transformation constitute two key fields of innovation

Global knowledge society: Improving educational provision in developing countries, global talent pool increasing, gender gap narrowing only in part

Sustainability & global responsibility: Sustainability is key for governments, citizens and businesses, consumers reward corporate social responsibility

2

73 Roland Berger Trend Compendium 2030 - Trends 1-7 Compact version.pptx

73

We are looking forward to your comments or questions – The full report, Trend Compendium 2030, can be accessed below

Klaus Fuest

The bigger picture for a better strategy

Dr. Christian Krys

Tel.: +49 211-4389-2231 [email protected]

Tel.: +49 211-4389-2917

Trend Compendium

https://www.rolandberger.com/en/Dossiers/Trend-Compendium.html