rutger koopmans general manager ing wholesale banking netherlands 9 november 2005, brussels

Post on 22-Dec-2015

218 views

TRANSCRIPT

Rutger Koopmans

General Manager

ING Wholesale Banking Netherlands

9 November 2005, Brussels

2

Key message

• India is ‘hot’, but already well known to ING

• “India” hype may lead to losing sight of key issues

• The long term view could become ‘a fata morgana’: ‘the long and winding road’ (a steep learning curve)

• Embrace the cultural differences with knowledge

• Keep pace & manage expectations: things to do!!

3

ING’s perspective: ING in India

• India is a rapidly growing economy with one of the fastest growing financial services industries in the world

• India is the second fastest growing insurance market in Asia, second only to China

• ING has been in India since 1990 and is the only global player in banking, asset management & insurance with non-Indian management control

• ING Vysya Bank has the largest banking network amongst international players in India

• ING Vysya Life Insurance is one of the fastest growing private players in the Indian insurance market

4

ING Group in India – Key Milestones

ING Bank N.V.set up arepresentativeoffice in India

1991 1995 1997 1998 2000 2001 2002 20031990 1994 1996

Barings startedInvestment Bankingoperations in India

ING Bank N.V.representativeofficeconverted intofull-servicebranch

ING Groupacquired Barings

globally therebyacquiring thebusiness of Baringsin India as well

Bank BrusselsLambertacquired astrategic stakein Vysya Bank

ING Investment Trust(Asset Managementbusiness) incorporatedin India

ING Groupsets uprepresentativeoffice forInsurance inIndia MoUsigned withVysya Bank

ING Vysya LifeInsuranceCompanybeginsoperations

ING becamethe singlelargestshareholder inVysya Bankby increasingits stake to44%

Vysya Bank renamedas ING Vysya Bank

ING Vysya Bankacquired 26% stake inING InvestmentManagement (India)Private Limited

(this is the AssetManagementCompany whichmanages the INGVysya Mutual Fund)

ING set up joint venturewithVysya Bankand GMR groupfor the foray intoInsurance Sector in India

Barings PrivateEquity established inIndia

5

Universal banking franchise

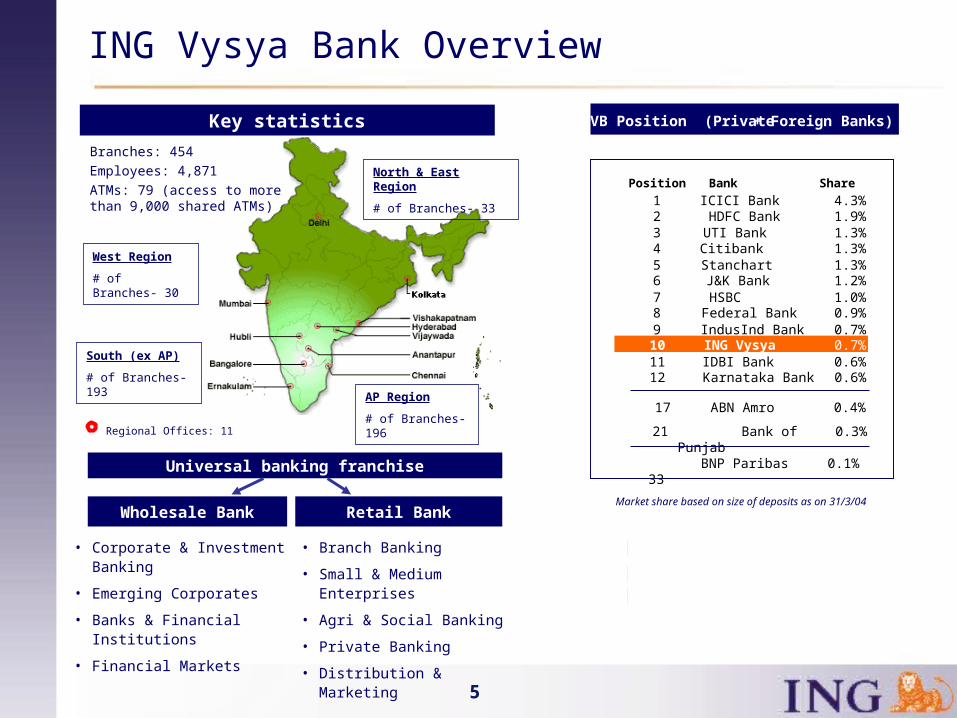

ING Vysya Bank Overview

Regional Offices: 11

Key statistics

North & East Region

# of Branches- 33

West Region

# of Branches- 30

AP Region

# of Branches-196

South (ex AP)

# of Branches- 193

Branches: 454

Employees: 4,871

ATMs: 79 (access to more than 9,000 shared ATMs)

• Branch Banking

• Small & Medium Enterprises

• Agri & Social Banking

• Private Banking

• Distribution & Marketing

Wholesale Bank Retail Bank

• Corporate & Investment Banking

• Emerging Corporates

• Banks & Financial Institutions

• Financial Markets

IVB Position (Private

Position Bank Share

1 ICICI Bank 4.3%2 HDFC Bank 1.9%3 UTI Bank 1.3%4 Citibank 1.3%5 Stanchart 1.3%6 J&K Bank 1.2%7 HSBC 1.0%8 Federal Bank 0.9%9 IndusInd Bank 0.7%10 ING Vysya 0.7%11 IDBI Bank 0.6%12 Karnataka Bank 0.6%

17 ABN Amro 0.4%

21 Bank of Punjab 0.3%

33 BNP Paribas 0.1%

IVB Position (Private + Foreign Banks)

Market share based on size of deposits as on 31/3/04

6

ING Vysya Bank Capabilities

• Leverage unique position as the first “Indian International” bank

• Combines strengths of the erstwhile Vysya Bank and ING Group to create an integrated platform delivering a complete range of banking products to Indian and Global clients

Integrated approach allows ING Vysya Bank to follow a client centric approach and offer a range of products and services leveraging local and international strengths

• Strong Rupee Balance Sheet

• Broad based India presence

• Wide commercial banking suite

• Strong Rupee Balance Sheet

• Broad based India presence

• Wide commercial banking suite

• International Investment Banking Capabilities

• Strong Corporate Banking Franchise

• Global Network

• International Investment Banking Capabilities

• Strong Corporate Banking Franchise

• Global Network

7

11,000

12,000

13,000

14,000

15,000

16,000

17,000

2001/02 2002/03 2003/04 2004/05 2005/06F

(IN

R b

n)

Real GDP

GDP Growth (%age)

+4.0%+8.2%

+6.9%

+6.5%

Exports & Imports (USD bn)

4553

6370

78

5865

80

97109

-

20

40

60

80

100

120

2001/02 2002/03 2003/04 2004/05F 2005/06F

(US

D b

n)

Exports Imports

Source: Economic Survey, Reserve Bank of India, Forecasts - Brokerage Report

5171

103

135 150

0

20

40

60

80

100

120

140

160

2001/02 2002/03 2003/04 2004/05E 2005/06E

US

D b

n

FX Reserves

FX Reserves (USD bn)

167.00 176.60 188.70 204.55

020406080

100120140160180200220

2001/02 2002/03 2003/04 2004/05

Index of Industrial Production

Note: Index of Industrial Production, Base 1993-94 = 100

+6.9%+5.7%

India: Strong Macroeconomics Fundamentals

+8.3%

8

India: the challenges of a growing economy

• High fiscal deficit

• Inflationary pressure

• Increasing government debt burden

• A strong democracy, slow decision making process

• Weak infrastructure (roads, airports, water management)

• Maintaining pace of reform (upgrading public systems)

• Bureaucracy, corruption, complex/antiquated regulations

9

“India” beyond the opportunities

• Keep a close eye on these factors

• Do not get hung up in long-term scenario predictions

• Focus on how to realize the “India” challenge

10

Embrace the differences

• India has a unique cultural and religious heritage

• It takes time to understand the history, the social demography and the cultural values

11

Adopt and Adapt to the changes

• Indian businessmen in Europe have to adapt to a different European outlook on India

• Business relations have changed and will change, a new balance will occur

• Indian businessmen are part of ‘the Indian hype’ but: don’t overlook Europe’s potential

12

Keep pace & Manage expectations

• India is managing growth in a careful and diligent way; manage your expectations in the same way

• Looking ahead, the potential for economic and political stability in India is enormous, but we must be appreciate and respect that the road ahead inhibits a steep learning curve

• The outcome is clear, but there is a way to go!

13