shining corporation ltd - finanznachrichten.de filehardware business, the sale of the shop unit, the...

TRANSCRIPT

CIRCULAR DATED 26 FEBRUARY 2008

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION.

If you are in any doubt as to the action you should take, you should consult your stockbroker, bank manager, solicitor,accountant or other professional adviser immediately.

If you have sold or transferred all your shares in the capital of Shining Corporation Ltd (the “Company”), you shouldimmediately forward this Circular, the Notice of Extraordinary General Meeting and the accompanying Proxy Form to thepurchaser or transferee or to the stockbroker, bank or agent through whom the sale or transfer was effected for onwardtransmission to the purchaser or transferee.

The Singapore Exchange Securities Trading Limited (“SGX-ST”) assumes no responsibility for the correctness of any of thestatements made, reports contained or opinions expressed in this Circular. Approval in-principle granted by the SGX-ST tothe Company for the listing and quotation of the Strategic Shares (as defined in this Circular) and the New Shares (asdefined in this Circular) on the official list of Catalist is not to be taken as an indication of the merits of the ProposedPlacement, the Strategic Shares, the New Shares, the Company, its subsidiaries and its securities.

SHINING CORPORATION LTD(Company Registration Number 199904729G)

(Incorporated in the Republic of Singapore)

CIRCULAR TO SHAREHOLDERS

in relation to

(1) THE PROPOSED ISSUE OF (A) 167,307,692 STRATEGIC SHARES IN THE CAPITAL OF THE COMPANY ATAN ISSUE PRICE OF S$0.13 FOR EACH STRATEGIC SHARE TOGETHER WITH THE ISSUE OF UP TO155,653,846 FREE WARRANTS EXERCISABLE AT S$0.13 PER WARRANT, ALL BY WAY OF PRIVATEPLACEMENT TO CITIPOINT ASIA REAL ESTATE CAPITAL LTD AND/OR ITS NOMINEE AND (B) THE NEWSHARES ARISING FROM THE EXERCISE OF THE WARRANTS PURSUANT TO THE STRATEGICPLACEMENT AGREEMENT.

(2) THE PROPOSED WHITEWASH RESOLUTION FOR THE WAIVER BY THE INDEPENDENT SHAREHOLDERSOF THEIR RIGHT TO RECEIVE A MANDATORY GENERAL OFFER FROM CITIPOINT ASIA REAL ESTATECAPITAL LTD (AND PARTIES ACTING IN CONCERT WITH IT) FOR ALL THE ISSUED AND PAID-UP SHARESOF THE COMPANY FOLLOWING COMPLETION OF THE PLACEMENT.

(3) THE PROPOSED CONDITIONAL SHINING IPT TRANSACTIONS RELATING TO THE SALE OF THEHARDWARE BUSINESS, THE SALE OF THE SHOP UNIT, THE USE OF THE NAME “SHINING” AND THENOVATION OR SUB-CONTRACT OF THE RETRO-FITTING CONTRACT.

(4) A MANDATE FOR THE COMPANY TO ENGAGE IN PROPERTY DEVELOPMENT IN SINGAPORE FOLLOWINGCOMPLETION OF THE PROPOSED TRANSACTIONS.

Financial Advisor to Shining Corporation Ltd

DMG & PARTNERS SECURITIES PTE. LTD.(Incorporated in the Republic of Singapore)

(Company Registration Number 198701140E)

Independent Financial Adviser to the Independent Directors of Shining Corporation Ltd

IMPORTANT DATES AND TIMES:

Last date and time for lodgement of Proxy Form : 16 March 2008 at 10.00 a.m.

Date and time of Extraordinary General Meeting : 18 March 2008 at 10.00 a.m.

Place of Extraordinary General Meeting : 11 Changi South Street 3, #04-01Singapore 486122

DMG & Partners

(Incorporated in the Republic of Singapore)(Company Registration Number 196100003D)

TABLE OF CONTENTS

Page

DEFINITIONS ...................................................................................................................................... 3

LETTER TO SHAREHOLDERS .......................................................................................................... 8

1. INTRODUCTION........................................................................................................................ 8

2. DETAILS OF THE PROPOSED PLACEMENT .......................................................................... 9

3. PROPOSED WHITEWASH RESOLUTION .............................................................................. 15

4. THE PROPOSED SHINING IPT TRANSACTIONS .................................................................. 18

5. MANDATE FOR THE COMPANY TO ENGAGE IN PROPERTY DEVELOPMENTIN SINGAPORE ........................................................................................................................ 23

6. APPOINTMENT OF PROPOSED NEW DIRECTORS .............................................................. 24

7. RATIONALE FOR THE PROPOSED TRANSACTIONS ............................................................ 25

8. FINANCIAL EFFECTS .............................................................................................................. 26

9. INTERESTS OF DIRECTORS AND SUBSTANTIAL SHAREHOLDERS .................................. 27

10. DIRECTORS’ AND SUBSTANTIAL SHAREHOLDERS’ INTERESTS IN THE COMPANY ...... 28

11. ADVICE OF HLF TO THE INDEPENDENT DIRECTORS IN RESPECT OF THE PROPOSED PLACEMENT AND THE PROPOSED WHITEWASH RESOLUTION.......... 28

12. ADVICE OF HLF TO THE INDEPENDENT DIRECTORS IN RESPECT OF THE PROPOSED SHINING IPT TRANSACTIONS .................................................................. 28

13. STATEMENT OF THE AUDIT COMMITTEE.............................................................................. 29

14. INDEPENDENT DIRECTORS’ RECOMMENDATIONS ............................................................ 29

15. EXTRAORDINARY GENERAL MEETING ................................................................................ 30

16. ABSTENTION FROM VOTING .................................................................................................. 30

17. ACTION TO BE TAKEN BY SHAREHOLDERS ........................................................................ 30

18. DIRECTORS’ RESPONSIBILITY STATEMENT ........................................................................ 31

19. CONSENTS .............................................................................................................................. 31

20. DOCUMENTS AVAILABLE FOR INSPECTION ........................................................................ 31

APPENDIX 1 ........................................................................................................................................ 32

APPENDIX 2 ........................................................................................................................................ 59

NOTICE OF EXTRAORDINARY GENERAL MEETING...................................................................... 60

PROXY FORM – EXTRAORDINARY GENERAL MEETING

2

DEFINITIONS

Except where the context otherwise requires, the following definitions apply throughout this Circular:-

Board : The board of Directors of the Company.

Builders Shop : Builders Shop Pte Ltd, a wholly-owned subsidiary of theCompany.

Business Transfer Agreement : A conditional agreement dated 10 September 2007 betweenBuilders Shop and Shining Holdings for the transfer of theHardware Business by Builders Shop to Shining Holdings on theterms and subject to the conditions therein.

Catalist : Formerly known as SGX-SESDAQ.

CDP : The Central Depository (Pte) Limited.

Circular : This circular dated 26 February 2008.

Completion : The completion of the Proposed Placement in accordance withthe terms and subject to the conditions of the Strategic PlacementAgreement.

Completion Date : The date notified in writing by the Company to the Subscriber asthe date for Completion, being a date no later than five (5) MarketDays after the satisfaction of the conditions precedents set out inthe Strategic Placement Agreement or such other date as theparties to the Strategic Placement Agreement may agree and allother conditions of the Strategic Placement Agreement beingsatisfied.

Code : The Singapore Code on Take-overs and Mergers.

Company : Shining Corporation Ltd.

Companies Act : The Companies Act, Chapter 50, of Singapore, as amended fromtime to time, and any enactment thereof.

Deed of Covenant : A conditional deed dated 10 September 2007 between theCompany, Shining Construction, Shining Holdings and Tan KayKiang.

Deed of Mutual Covenants : A conditional deed dated 10 September 2007 between theCompany, Shining Construction, Shining Holdings and ShiningDevelopment for the continued use of the name “Shining” by eachof the Shining Entities.

Deed Poll : The deed poll to be executed by the Company for the purpose ofconstituting the Warrants and containing, inter alia, provisions forthe protection of the rights and interests of the Warrantholders.

Director : A director of the Company as at the date of this Circular.

Effective Date : 1 January 2008

3

EGM : The extraordinary general meeting of the Company, notice ofwhich is set out on pages 60 to 62 of this Circular.

Executive Directors : Tan Kay Kiang, Tan Chin Hoon, Tan Kay Tho and Tan Kay Sing.

Exercise Period : The period during which Warrants may be exercised commencingon and including the date of issue of the Warrants and expiring at5.00 p.m. on the date immediately preceding the fifth anniversaryof the date of issue of the Warrants, subject to the conditions ofthe Deed Poll.

Exercise Price : $0.13, being the sum payable in respect of each New Share towhich the Warrantholder will be entitled to subscribe uponexercise of a Warrant, or such adjusted price subject to theconditions of the Deed Poll.

Existing Controlling : Tan Kay Kiang, Tan Chin Hoon, Tan Kay Tho, Tan Kay Sing Shareholders who are the Company’s Directors, their respective spouses, Alex

Tan Nan Choon, a Director of the Company, and Shining Holdingswho collectively are deemed interested in 29.72% of theCompany’s total issued shares.

FA : DMG & Partners Securities Pte. Ltd., being the financial adviser tothe Company.

Group or Group Companies : The Company and its subsidiaries and Group Company meansany one of them.

HLF or IFA : Hong Leong Finance Limited, being the independent financialadviser to the Independent Directors in respect of the ProposedPlacement, the Proposed Whitewash Resolution and theProposed Shining IPT Transactions.

IFA Letter : The letter dated 26 February 2008 from HLF to the IndependentDirectors in respect of the Proposed Placement, the ProposedWhitewash Resolution and the Proposed Shining IPTTransactions, a copy of which is set out in Appendix 1 of thisCircular.

Hardware Business : The entirety of the business and goodwill carried on by BuildersShop as a going concern in hardware distribution and retailingand certain assets owned by or under the control or in thepossession of Builders Shop and used in the conduct of thisbusiness.

Independent Directors : The independent Directors as at the date of this Circular, namely,Lee Eng Kian and Gurdaib Singh s/o Pala Singh.

Independent Shareholders : Shareholders other than (i) the Subscriber and (ii) persons actingin concert with the Subscriber; and (iii) persons not independentof the persons mentioned in (i) and (ii) of this definition.

Issue Price : S$0.13 per Strategic Share.

Knight Frank : Knight Frank Pte Ltd.

4

Latest Practicable Date : 22 February 2008, being the latest practicable date prior to theprinting of this Circular.

Listing Manual : The listing manual of the SGX-ST, as amended from time to time.

Market Day : A day on which the SGX-ST is open for trading of securities inSingapore.

New Shares : New Shares in the capital of the Company to be issued from timeto time upon the exercise of the Warrants.

Nico Po : Nico Po Purnomo, an Indonesian citizen.

Open Market Value : The open market value of the Shop Unit.

Proposed Placement : The proposed placement of the Strategic Shares and theWarrants to the Subscriber under the Strategic PlacementAgreement.

Proposed Shining IPT : The respective transactions set out in the Business Transfer Transactions Agreement, the Deed of Covenant, the Deed of Mutual Covenants

and the Shop Unit Option Agreement.

Proposed Transactions : The Proposed Placement and the Proposed Shining IPTTransactions.

Proposed Whitewash : The resolution proposed as Ordinary Resolution Number 2 in the Resolution Notice of EGM appended to this Circular, for a waiver by the

Independent Shareholders of their rights to receive a mandatorytakeover offer from the Subscriber and its concert parties for theShares not already owned or controlled by the Subscriber and itsconcert parties.

Record Date : The date as at the close of business in relation to any dividend,right, allotment or other distributions on which members of theCompany must be registered in order to participate in suchdividend, right, allotment or other distributions.

Register of Members : The Register of Members of the Company.

Retro-Fitting Contract : The tender for retro-fitting addition and alteration work forapproximately $30 million submitted by Shining Construction toAFP Warehouse Pte Ltd.

Rights Issue : The renounceable non-underwritten rights issue of 48,000,000new Shares in the capital of the Company undertaken by theCompany pursuant to the offer information statement dated 16August 2007.

Securities Account : Securities account maintained by a Depositor with CDP but doesnot include a securities sub-account.

SFA : The Securities and Futures Act (Chapter 289) of Singapore andany statutory modification or re-enactment thereof.

5

Shareholder : Registered holders of Shares in the Register of Members of theCompany except that where the registered holder is CDP, theterm Shareholders shall, in relation to such Shares, mean thepersons to whose Securities Accounts maintained with CDP arecredited with the Shares.

Shares : Ordinary shares in the share capital of the Company.

Shining Entities : The Company, Shining Construction, Shining Holdings andShining Development.

SGX-ST or Exchange : Singapore Exchange Securities Trading Limited.

SGX-SESDAQ : SGX-ST Dealing and Automated Quotation System.

SIC : Securities Industry Council.

Shining Construction : Shining Construction Pte Ltd, a wholly-owned subsidiary of theCompany.

Shining Development : Shining Development Pte Ltd, a wholly-owned subsidiary ofShining Holdings.

Shining Holdings : Shining Holdings Pte Ltd, a company whose share capital iswholly held by the Executive Directors, Tan Siok Hwee and TanSeok Luan.

Shop IPT Sale : The proposed sale of the Shop Unit by Shining Construction toShining Holdings in accordance with the Shop Unit OptionAgreement.

Shop Unit : The shop unit at 29 Lorong 13 Geylang, Singapore 388672 ownedby Shining Construction.

Shop Unit Book Value : The book value of the Shop Unit as recorded in the books ofShining Construction as at 31 December 2006.

Shop Unit Option Agreement : The conditional option agreement dated 10 September 2007between Shining Construction and Shining Holdings for the sale,through an option, of the Shop Unit to Shining Holdings.

Strategic Placement : A conditional agreement dated 10 September 2007 between Agreement the Company and the Subscriber pursuant to which the

Subscriber will inter alia invest $21,750,000.00 in the Company bysubscribing for the Strategic Shares and the Warrants.

Strategic Shares : 167,307,692 new Shares in the capital of the Company with eachsuch new Share to be issued at $0.13 to the Subscriber.

Subscriber : Citipoint Asia Real Estate Capital Ltd, a corporation incorporatedin the British Virgin Islands and having its registered address atNerine Chambers, P.O. Box 905, Road Town, Tortola, British VirginIslands.

Substantial Shareholder : A substantial Shareholder as defined under Section 81 of theCompanies Act.

“S$”, “$” or “cents” : Singapore dollars and cents, respectively.

6

Valuation Certificate : The valuation certificate dated 12 December 2007 from KnightFrank in respect of the valuation of the Shop Unit.

Warrant Agent : The warrant agent to be appointed by the Company in connectionwith the Deed Poll.

Warrantholders : Registered holders of the Warrants, except where CDP is theregistered holder, the term Warrantholders shall, where thecontext so admits, mean the persons named as Depositors in theDepository Register into whose Securities Accounts are creditedwith such Warrants.

Warrants : Up to 155,653,846 warrants to be constituted under the Deed Poll,each warrant entitling the holder thereof to subscribe for one (1)new Share upon its exercise in accordance with the terms andsubject to the conditions of the Deed Poll.

“%” or “per cent” : Percentage or per centum.

The terms Depositor, Depository Agent and Depository Register shall have the meanings ascribed tothem, respectively, in Section 130A of the Companies Act.

The term subsidiary shall have the meaning ascribed to it by Section 5 of the Companies Act.

The term acting in concert shall have the meaning ascribed to it in the Code.

Words importing the singular shall, where applicable, include the plural and vice versa, and wordsimporting the masculine gender shall, where applicable, include the feminine and neuter genders andvice versa. References to persons shall include corporations.

Any reference in this Circular to any enactment is a reference to that enactment as for the time beingamended or re-enacted. Any word defined under the SFA, the Companies Act, the Listing Manual or theCode or any statutory modification thereof and used in this Circular shall, where applicable, have themeaning ascribed to it under the SFA, the Companies Act, the Listing Manual or the Code or anystatutory modification thereof, as the case may be.

Any reference to a time of day in this Circular shall be a reference to Singapore time unless otherwisestated.

All discrepancies in the tables included herein between the listed amounts and totals thereof are due torounding. Accordingly, figures shown as totals in certain tables may be an arithmetic aggregation of thefigures that precede them.

7

SHINING CORPORATION LTD (Company Registration Number 199904729G)

(Incorporated in the Republic of Singapore)

LETTER TO SHAREHOLDERS

Directors Registered Office

Tan Kay Kiang (Executive Chairman) 11 Changi South Street 3 #04-01Tan Chin Hoon (Group Managing Director) Singapore 486122Tan Kay Tho (Executive Director)Tan Kay Sing (Executive Director)Alex Tan Nan Choon (Non-Executive Director)Lee Eng Kian (Independent Director)Gurdaib Singh s/o Pala Singh (Independent Director)

26 February 2008

To: The Shareholders of Shining Corporation Ltd

Dear Sir / Madam

1. INTRODUCTION

On 10 September 2007, the Company announced that the Company had entered into theStrategic Placement Agreement for the proposed placement of new ordinary shares and certainfree warrants to the Subscriber.

The Subscriber is a special purpose corporation incorporated in the British Virgin Islands. Theentire share capital of the Subscriber is held by Nico Po.

Under the Strategic Placement Agreement, the Subscriber will invest S$21,750,000 in theCompany by subscribing for the Strategic Shares and the Warrants. Each Strategic Share will besubscribed for at the Issue Price. Each Warrant will be issued free to the Subscriber, on the termsand subject to the conditions of the Strategic Placement Agreement and the Deed Poll.

Nico Po has additionally undertaken that he shall ensure the performance by the Subscriber of itsobligations to subscribe for the Strategic Shares on the terms and subject to the conditions of theStrategic Placement Agreement. On 18 September 2007, the Company received writtenconfirmation from a bank in Singapore that Nico Po has sufficient financial resources to fulfil theobligations to subscribe for the Strategic Shares. The Company has accepted such writtenconfirmation of financial resources.

The Strategic Placement Agreement stipulates that as a condition to the placement of theStrategic Shares, the Group is to enter into the Proposed Shining IPT Transactions. Under theStrategic Placement Agreement, the performance of each of the placement of the Strategic Sharesand the Proposed Shining IPT Transactions by the respective parties thereto are inter-conditionalupon the performance of each of these transactions.

It is further the intention of Nico Po, who will be a controlling shareholder of the Company onCompletion, for the Group to enter into the new business of property development following thecompletion of the Proposed Placement. In line with the proposed new business, the ProposedShining IPT Transactions will allow the Company to divest itself of its current businesses that willno longer form its core business if the Proposed Transactions are approved.

A copy of the Company’s announcements made on 10 September 2007 and 18 September 2007are available on SGX-ST’s website at www.sgx.com.

8

The Directors are convening an EGM to seek Shareholders’ approval, by way of respectiveordinary resolutions, for (i) the issue of the Strategic Shares, (ii) the issue of the Warrants, (iii) theissue of New Shares upon the exercise of the Warrants, all of which are pursuant to the StrategicPlacement Agreement (and in the case of the issue of the Warrants and the New Shares,additionally pursuant to and on the terms of the Deed Poll), (iv) the Proposed Shining IPTTransactions and (v) the Group to be permitted to engage in property development in Singaporefollowing Completion, as set out in the notice of EGM on pages 60 to 62 of this Circular. Thepurpose of this Circular is to provide Shareholders with the relevant information relating to thesematters.

2. DETAILS OF THE PROPOSED PLACEMENT

2.1 The Strategic Placement Agreement

Pursuant to the Strategic Placement Agreement, the Company agreed to:-

(a) allot and issue the Strategic Shares to the Subscriber or its nominees at an issue price ofS$0.13 per Strategic Share; and

(b) issue up to 155,653,846 free Warrants to the Subscriber, each Warrant carrying the right tosubscribe for one (1) New Share at an exercise price of S$0.13 for each New Share,

upon the terms and subject to the conditions in the Strategic Placement Agreement.

The Strategic Shares and the New Shares when issued and fully paid will rank pari passu in allrespects with and carry all rights similar to the existing issued Shares except that they will not rankfor any dividend, right, allotment or other distributions, the Record Date for which falls on or beforethe Completion Date or the date of exercise of the relevant Warrants (as the case may be).

The Strategic Shares will represent approximately 53.7% of the enlarged issued share capital ofthe Company upon completion of the Proposed Placement. Accordingly, the Proposed Placementis subject to the prior approval of Shareholders pursuant to Rule 803 of the Listing Manual whichprovides that a company shall not issue securities to transfer a controlling interest without priorapproval of shareholders in general meeting.

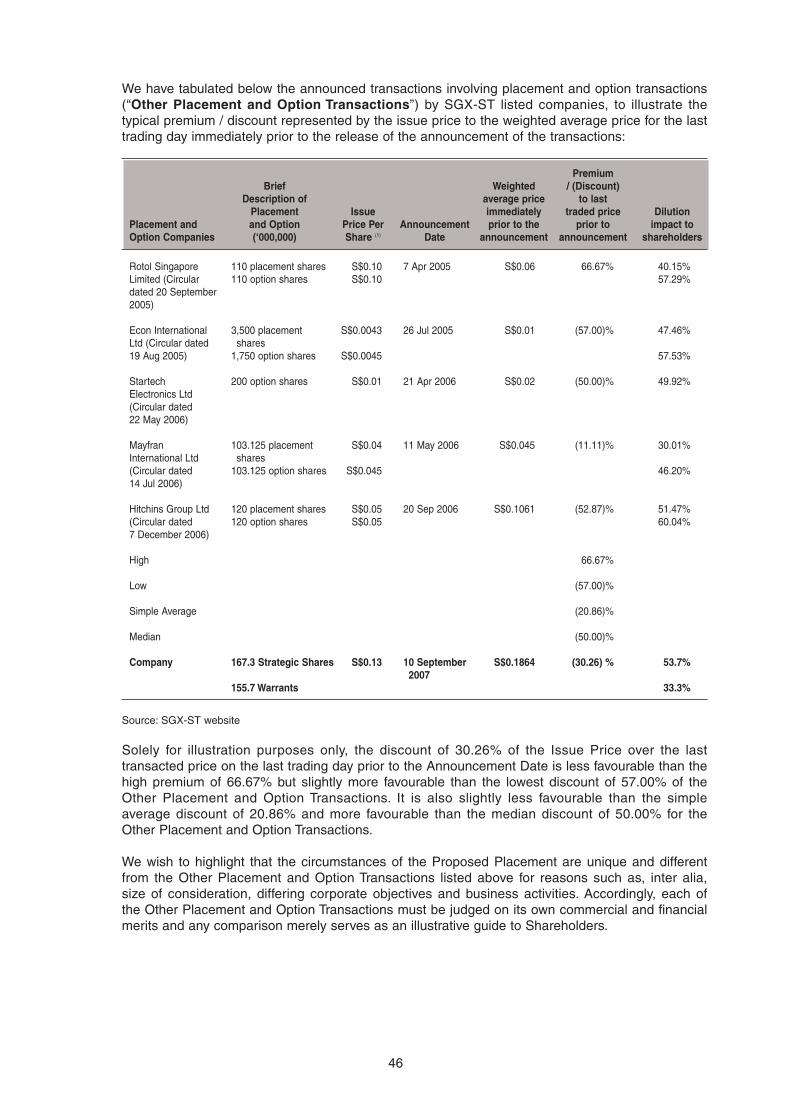

The Issue Price of S$0.13 for each of the Strategic Shares and the exercise price of S$0.13 foreach of the Warrants represents a discount of:-

(i) 24.3% to the weighted average price for trades done on the SGX-SESDAQ on 7 September2007, being the full market day prior to the signing of the Strategic Placement Agreement;and

(ii) 30.3% to the prevailing market price of the Shares on 7 September 2007 prior to the signingof the Strategic Placement Agreement.

The Issue Price was agreed based on arms’ length negotiations taking into account, inter alia, theexisting financial position of the Company, historical and prevailing Share prices and marketsentiments.

2.2 Principal Terms of the Warrants

The information contained in this section is a summary of the proposed terms of the Warrants tobe constituted under the Deed Poll.

Number of Warrants : Up to 155,653,846 free Warrants to be issued

Status of New Shares : The New Shares arising from the exercise of the Warrants will,upon, allotment and issue, rank pari passu in all respects with thethen existing Shares save for any dividend, right, allotment or otherdistribution that may be declared or paid, the Record Date forwhich falls before the relevant date of issue of the New Shares

9

Trading of the Warrants : Not applicable. Under Rule 826 of the Listing Manual, if anapplication is made for the listing of company warrants, the SGX-ST expects at least 100 warrantholders for a class of companywarrants in order to ensure a sufficient spread of holdings toprovide for an orderly market in the securities. As the Warrantsare proposed to be placed out only to the Subscriber, theWarrants will not be listed and traded on Catalist.

Form and subscription : The Warrants will be issued in registered form and will be rights constituted by the Deed Poll. Subject to the terms and conditions

of the Warrants to be set out in the Deed Poll, each Warrant shallentitle the Warrantholder, at any time during the Exercise Period,to subscribe for one (1) New Share at the Exercise Price.

Exercise Period : The Warrants may be exercised at any time from and including thedate of issue of the Warrants up to 5.00 p.m. (Singapore time) onthe date immediately preceding the fifth anniversary of the date ofissue of the Warrants unless such date is a date on which theRegister of Members is closed or is not a Market Day, in whichevent the Exercise Period shall expire on the date prior to theclosure of the Register of Members or the immediately precedingMarket Day, as the case may be, but excluding such period(s)during which the Register of Members may be closed, subject tothe terms and conditions of the Warrants to be set out in the DeedPoll. Warrants remaining unexercised at the expiry of the ExercisePeriod shall lapse and cease to be valid for any purpose.

Notice of expiry of the Warrants shall be given to allWarrantholders at least thirty (30) days before the expiry date, andthe Company shall announce the same on the SGX-ST.

Adjustments : The Exercise Price and the number of Warrants will, after theirissue, be subject to adjustments under certain circumstances asset out in the Deed Poll. Such circumstances include capitalisationissues, rights issues and certain capital distributions which will bemore particularly described in the Deed Poll.

Modification to terms of : The Company may, without the consent of the Warrantholders but Warrants and Deed Poll in accordance with the terms of the Deed Poll, effect any

modification to the terms of the Warrants or the Deed Poll which, inthe opinion of the Company, is not materially prejudicial to theinterests of the Warrantholders or which, in its opinion, is either (i)of a formal, technical or minor nature or to correct a manifest errorto comply with mandatory provisions of Singapore law or (ii) tovary or replace provisions relating to the transfer or exercise of theWarrants or meetings of the Warrantholders (in order to facilitatetrading in or the exercise of the Warrants or in connection with theimplementation and operation of the book-entry (scripless)settlement system in respect of the trades of the Company’ssecurities on Catalist). Any such modification shall be binding onall Warrantholders and all persons having an interest in theWarrants and shall be notified to them in accordance with theterms of the Deed Poll.

Any alteration in the terms of the Warrants to the advantage of theWarrantholders is subject to the approval of the Shareholdersexcept where the alterations are made pursuant to the terms of theDeed Poll.

10

Transfer and transmission : A Warrant may only be transferred in the manner prescribed in theterms and conditions of the Warrants to be set out in the Deed Pollincluding, inter alia, the following:-

(i) a Warrantholder (“Transferor”) shall lodge, during normalbusiness hours on any Business Day (as defined in theDeed Poll) at the specified office of the Warrant Agent, theTransferor’s warrant certificate(s) together with a transferform as prescribed by the Company from time to time (the“Transfer Form”) duly completed and signed by or on behalfof the Transferor and the transferee and duly stamped inaccordance with any law for the time being in force relatingto stamp duty, provided that the Warrant Agent maydispense with requiring CDP to sign as transferee anyTransfer Form for the transfer of Warrants to CDP. ATransferor shall be deemed to remain a Warrantholder of theWarrants until the name of the transferee is entered in theRegister of Warrantholders by the Warrant Agent.

(ii) Deceased Warrantholder - the executors and administratorsof a deceased Warrantholder (not being one of several jointholders) and, in the case of one or more of several jointWarrantholders, the survivor or survivors of such jointWarrantholders, shall be the only persons recognised ashaving any title to Warrants registered in the name of adeceased Warrantholder. Such person(s) shall be entitled tobe registered as Warrantholders and/or to make suchtransfer(s) as the deceased Warrantholder is entitled tomake, upon the production by such persons to the Companyand the Warrant Agent of such evidence as may bereasonably required by the Company and the Warrant Agentto prove their title and on payment of the fees and expensesset out in the Deed Poll.

Winding-up : If a resolution is passed for a members’ voluntary winding-up ofthe Company then if such winding-up is for the purpose ofreconstruction or amalgamation pursuant to a scheme ofarrangement to which the Warrantholders, or some persondesignated by them for such purpose by a resolution, shall be aparty and shall have approved or assented to by way of such aresolution, the terms of such scheme of arrangement shall bebinding on all the Warrantholders and all persons having aninterest in the Warrants; and in any other case every Warrantholdershall be entitled upon and subject to the terms and conditions ofthe Deed Poll at any time within six (6) weeks after the passing ofsuch resolution for a members’ voluntary winding-up of theCompany, to elect to be treated as if he had immediately prior tothe commencement of such winding-up exercised the Warrants tothe extent specified in a notice to the Company and had on suchdate been the holder of the Shares to which he would havebecome entitled pursuant to such exercise and the liquidator of theCompany shall give effect to such election accordingly. TheCompany shall give notice to the Warrantholders in accordancewith the terms and conditions set out in the Deed Poll of thepassing of any such resolution within seven (7) Business Days (asdefined in the Deed Poll) after the passing thereof.

11

Subject to the foregoing, if the Company is wound up for any otherreason, all Warrants which have not been exercised at the date ofthe passing of such resolution for the winding-up of the Companyshall lapse and the Warrants shall cease to be valid for anypurpose.

Further issue of securities : Subject to the terms and conditions of the Warrants set out in theDeed Poll, the Company shall be at liberty to issue Shares toShareholders either for cash or as a bonus distribution and toissue further subscription rights, upon such terms and conditionsas the Company sees fit but the Warrantholders shall not have anyparticipating rights in such further issue(s) of Shares orsubscription rights unless otherwise resolved by the Company ingeneral meeting.

Governing Laws : Laws of the Republic of Singapore.

The 155,653,846 Warrants will be issued on the Completion Date.

2.3 Conditions Precedent for the Proposed Placement

The obligations of the Subscriber under the Strategic Placement Agreement to subscribe for theStrategic Shares and the Warrants, and the Company’s obligations to issue the Strategic Sharesand the Warrants, is conditional upon the performance by the Company and the Subscriber of theirrespective obligations under the Strategic Placement Agreement and also upon fulfilment of thefollowing:

(i) the Subscriber obtaining a whitewash waiver by the SIC of the requirement for theSubscriber and its concert parties to make a mandatory general offer for the Shares of theCompany not already owned by the Subscriber or its concert parties, and if granted subjectto conditions, such conditions being acceptable to the Subscriber (the “Whitewash WaiverRuling”);

(ii) the Company having obtained a whitewash waiver from the Company’s Shareholdersindependent of the Subscriber and its concert parties and fulfilment of other relevant termsand conditions (if any) of the Whitewash Waiver Ruling of the SIC;

(iii) approval in-principle for the listing and quotation of the Strategic Shares, the Warrants andthe New Shares to be issued upon the exercise of the Warrants on the SGX-ST (onconditions, if any, acceptable to the Company and the Subscriber) having been obtained andremaining in full force and effect and where such approval is given subject to conditionswhich must be fulfilled on or before the Completion Date, they are so fulfilled;

(iv) all corporate and Shareholders’ approvals having been obtained by the Company on termssatisfactory to the Company and the Subscriber in respect of the allotment, issue andsubscription of the Strategic Shares, the issue of the Warrants and all the transactionsancillary to or contemplated thereto and such approvals remaining in full force and effect onCompletion and, if such approvals are subject to any conditions which are required to befulfilled on or prior to Completion, such conditions are fulfilled;

(v) the allotment, issue and subscription of the Strategic Shares and the allotment and issue ofthe Warrants and the New Shares arising from the exercise of the Warrants not beingprohibited by any statute, order, rule, regulation or directive promulgated or issued after thedate of the Strategic Placement Agreement by any legislative, executive or regulatory bodyor authority of Singapore which is applicable to the Company or the Subscriber;

(vi) on the Completion Date, the representations and warranties of the Company and theSubscriber under the Strategic Placement Agreement being true, accurate and correct in allmaterial respects as if made on the Completion Date, with reference to the then existingcircumstances and the Company and the Subscriber having performed in all materialrespects all of their obligations under the Strategic Placement Agreement to be performedon or before the Completion Date;

12

(vii) all approvals and Shareholders’ approvals for the Proposed Shining IPT Transactions havingbeen obtained by the Company on terms satisfactory to the Company and the ExistingControlling Shareholders;

(viii) the Subscriber being satisfied that the audited consolidated net tangible assets of theCompany and its subsidiaries as a group not being less than S$12 million for the financialyear ended 31 December 2007, based on the same accounting policies and standardsadopted in the Company’s financial audited statements (“NTA”), however, in the eventCompletion occurs at any time before 31 December 2007, the NTA, as reviewed by theSubscriber’s appointed auditors in consultation with the auditors of the Company, in respectof the financial period ending as at the end of the month immediately prior to the month inwhich Completion occurs shall not be less than S$12,000,000 (for avoidance of doubt, allprofessional costs and related expenses up to an amount no more than S$550,000 inconnection with securing the requisite approvals for the Proposed Transactions andbrokerage fees payable shall not be computed as reducing the NTA);

(ix) the Shares of the Company have not been suspended for more than three (3) market days;and

(x) the Shares of the Company have not been delisted.

The Company and the Subscriber further agreed that they shall respectively use their bestendeavours to secure the satisfaction of the conditions precedent above on or before 31 March2008 or such other date as they may agree in writing (the “Cut-Off Date”).

The Subscriber may, upon such terms as it thinks fit, waive compliance with any of the conditionsprecedent above (other than the conditions contained in (i), (ii), (iii), (iv), (v), (vii) and (x)) and anycondition so waived shall be deemed to have been satisfied.

If any of the conditions precedent are not satisfied or waived, in accordance with the terms of theStrategic Placement Agreement, on or before the Cut-Off Date or such other date as the Companyand the Subscriber may agree, the Strategic Placement Agreement shall ipso facto cease anddetermine thereafter and neither the Company nor the Subscriber shall have any claim against theother for costs, expenses, damages, losses, compensation or otherwise.

2.4 Moratorium in respect of the Strategic Shares

The Subscriber has undertaken, that during the period of six (6) months commencing from thedate of issue of the Strategic Shares and ending on the date falling six (6) months from the date ofthe issue of the Strategic Shares, it shall not directly or indirectly dispose of any interest, direct orindirect, in the said Strategic Shares.

2.5 In-principle Approval from the SGX-ST

In-principle approval was obtained from the SGX-ST on 22 February 2008 for the dealing in, listingof and quotation for the Strategic Shares and the New Shares on Catalist, subject to:-

(a) compliance with the SGX-ST’s listing requirements;

(b) Shareholders’ approval for the Proposed Placement at the EGM;

(c) submission of an undertaking from the Company to:-

(i) provide a status report on the use of the proceeds from the Proposed Placement in itsannual report; and

(ii) announce any adjustment to the Warrants made pursuant to Rule 829(1) of the SGX-ST Listing Manual.

13

The SGX-ST has highlighted that in the event the Company acquires any asset from theSubscriber, Nico Po and/or their related parties, the SGX-ST reserves the right to aggregatethe acquisitions and the Proposed Placement, and deem the subsequent asset injections asa very substantial acquisition or reverse takeover under Rule 1015 of the Listing Manual.

The in-principle approval granted by the SGX-ST is not to be taken as an indication of the meritsof the Proposed Placement, the Company, its subsidiaries, the Shares, the Strategic Shares, theWarrants and the New Shares.

The Warrants will not be listed and traded on Catalist as the Warrants are proposed to be placedout only to the Subscriber.

2.6 Approval from the SGX-ST for Waiver of Rule 825 of the Listing Manual

Rule 825 of the Listing Manual provides that the number of new shares arising from theexercise/conversion of outstanding company warrants or other convertible securities must inaggregate not exceed 50% of the issued share capital.

The number of New Shares arising from the full exercise of the Warrants would exceed 50% of theCompany’s existing issued share capital (which comprises 144,000,000 Shares). In thisconnection, the SGX-ST has indicated on 22 February 2008 that it has no objections to the waiverof Rule 825 of the Listing Manual, subject to:-

(a) the Company making an announcement of the waiver granted via SGXNET pursuant to Rule107 of the Listing Manual;

(b) the Proposed Placement is approved by Shareholders at the EGM;

(c) an unqualified opinion from a financial adviser that the Proposed Placement is notprejudicial to the interests of the Company and its minority shareholders;

(d) an unanimous approval from all the Company’s non-executive independent directors for theProposed Placement after having satisfied themselves that the Proposed Placement is notprejudicial to the interests of the Company and its minority shareholders.

In fulfilment of condition (a) above, the Company has made an announcement of the waiver ofRule 825 of the Listing Manual on 25 February 2008.

In fulfilment of condition (c) above, the Company has appointed HLF as its financial adviser.In the IFA Letter dated 26 February 2008 addressed to the Independent Directors, the IFAhas stated that given the factors and circumstances considered, as set out in the IFA Letter,the Proposed Placement is not prejudicial to the interests of the Company and itsShareholders. Hence, the IFA recommends that the Directors advise Shareholders to vote infavour of the Proposed Placement. The IFA Letter is set out in Appendix 1 of this Circular.

In fulfilment of condition (d) above, all the independent non-executive directors of the Companyhave also confirmed that having considered the IFA Letter dated 26 February 2008, they are of theview that the Proposed Placement is not prejudicial to the interests of the Company and itsminority Shareholders.

2.7 Proposed Use of Proceeds from the Proposed Placement and the Exercise of the Warrants

The Company intends to use the net proceeds from the Proposed Placement and the exercise ofthe Warrants as follows:-

(a) to undertake activities relating to high-end residential development of properties inSingapore; and

(b) for general working capital purposes.

14

3. PROPOSED WHITEWASH RESOLUTION

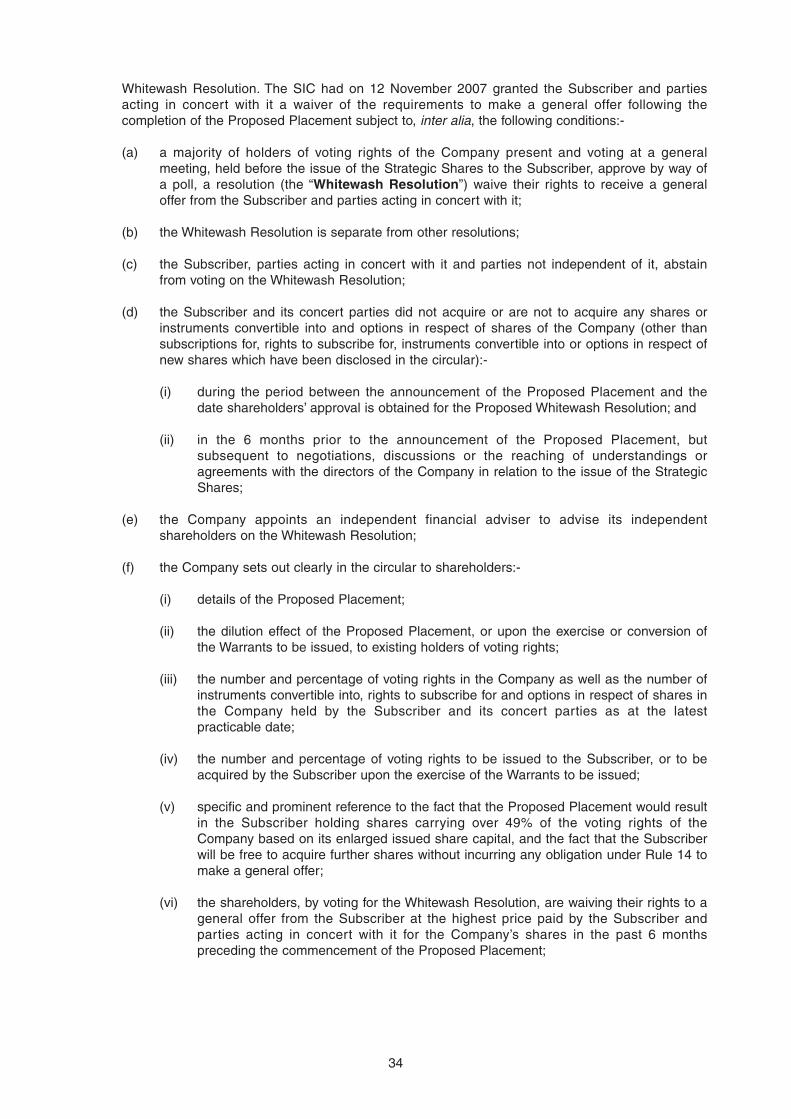

3.1 As at the Latest Practicable Date, the Subscriber and its concert parties do not hold any Shares orinstruments convertible into the rights to subscribe for and options in respect of Shares. Oncompletion of the Proposed Placement, the Subscriber and/or its nominees will hold 167,307,692Shares, representing approximately 53.7% of the enlarged Share capital of the Company. Pursuantto Rule 14.1(a) of the Code and Section 139 of the SFA, the Subscriber and parties acting inconcert with it would be required to make a general offer for the remaining Shares not owned oragreed to be acquired by the Subscriber and parties acting in concert with it at the highest pricepaid or agreed to be paid by the Subscriber and parties acting in concert with it for the Shares inthe past 6 months. The Subscriber has sought a waiver from the SIC of its obligation to make ageneral offer under Rule 14.1(a) of the Code and for SIC to permit it to propose the ProposedWhitewash Resolution. The SIC had on 12 November 2007 granted the Subscriber a waiver of therequirements to make a general offer following the completion of the Proposed Placement subjectto, inter alia, the following conditions:-

(a) a majority of holders of voting rights of the Company present and voting at a generalmeeting, held before the issue of the Strategic Shares to the Subscriber, approve by way ofa poll, a resolution (the “Whitewash Resolution”) to waive their rights to receive a generaloffer from the Subscriber and parties acting in concert with it;

(b) the Whitewash Resolution is separate from other resolutions;

(c) the Subscriber, parties acting in concert with it and parties not independent of it, abstainfrom voting on the Whitewash Resolution;

(d) the Subscriber and its concert parties did not acquire or are not to acquire any shares orinstruments convertible into and options in respect of shares of the Company (other thansubscriptions for, rights to subscribe for, instruments convertible into or options in respect ofnew shares which have been disclosed in the circular):-

(i) during the period between the announcement of the Proposed Placement and thedate shareholders’ approval is obtained for the Whitewash Resolution; and

(ii) in the 6 months prior to the announcement of the Proposed Placement, butsubsequent to negotiations, discussions or the reaching of understandings oragreements with the directors of the Company in relation to the issue of the StrategicShares;

(e) the Company appoints an independent financial adviser to advise its independentshareholders on the Whitewash Resolution;

(f) the Company sets out clearly in the circular to shareholders:-

(i) details of the Proposed Placement;

(ii) the dilution effect of the Proposed Placement, or upon the exercise or conversion ofthe Warrants to be issued, to existing holders of voting rights;

(iii) the number and percentage of voting rights in the Company as well as the number ofinstruments convertible into, rights to subscribe for and options in respect of shares inthe Company held by the Subscriber and its concert parties as at the latestpracticable date;

(iv) the number and percentage of voting rights to be issued to the Subscriber, or to beacquired by the Subscriber upon the exercise of the Warrants to be issued;

15

(v) specific and prominent reference to the fact that the Proposed Placement would resultin the Subscriber holding shares carrying over 49% of the voting rights of theCompany based on its enlarged issued share capital, and the fact that the Subscriberwill be free to acquire further shares without incurring any obligation under Rule 14 tomake a general offer;

(iv) the shareholders, by voting for the Whitewash Resolution, are waiving their rights to ageneral offer from the Subscriber at the highest price paid by the Subscriber andparties acting in concert with it for the Company’s shares in the past 6 monthspreceding the commencement of the Proposed Placement;

(g) the circular by the Company to its shareholders states that the waiver granted by the SIC tothe Subscriber and parties acting in concert with it from the requirement to make a generaloffer under Rule 14 is subject to the conditions stated at 3.1(a) to (f) above;

(h) the Subscriber obtains SIC’s approval in advance for those parts of the circular that refer tothe Whitewash Resolution; and

(i) to rely on the Whitewash Resolution, the acquisition of the Strategic Shares by theSubscriber pursuant to the Proposed Placement must be completed within 3 months of theapproval of the Whitewash Resolution.

3.2 The Independent Shareholders are therefore asked to vote on a poll on the Proposed WhitewashResolution set out as an ordinary resolution in the Notice of EGM on page 61 of this Circular.

3.3 Shareholders should note that the passing of the ordinary resolution relating to the ProposedPlacement is conditional upon the Proposed Whitewash Resolution being approved byIndependent Shareholders as the Proposed Whitewash Resolution is a condition precedent in theStrategic Placement Agreement.

If Independent Shareholders do not vote in favour of the Proposed Whitewash Resolution, theProposed Placement will not take place. As completion of the Proposed Shining IPT Transactionsis also conditional upon the completion of the Proposed Placement taking place simultaneously,the Proposed Shining IPT Transactions will also not take place.

3.4 Independent Shareholders should note that the Proposed Placement would result in theSubscriber holding Shares carrying over 49% of the voting rights of the Company based onits enlarged issued share capital.

3.5 Independent Shareholders should also note that by voting for the Proposed WhitewashResolution:-

(a) the Subscriber will be free to acquire further Shares without incurring any obligationunder Rule 14 of the Code to make a general offer; and

(b) the Independent Shareholders will be waiving their rights to a general offer from theSubscriber at the highest price paid by the Subscriber and parties acting in concertwith it for the Company’s Shares in the past 6 months preceding the commencementof the Proposed Placement.

16

3.6 Shareholding Effects

Assuming that the Proposed Whitewash Resolution is approved by Shareholders, the illustrativeeffects of the allotment and issue of the Strategic Shares and the New Shares on the shareholdingstructure of the Company (based on the shareholding information available to the Company as atthe Latest Practicable Date) are set out below:-

After the Allotment Before the Allotment After the Allotment and Issue of the

and Issue of the and Issue of the Strategic Shares and Strategic Shares(7) Strategic Shares(8) the New Shares(9)

Total Interest Total Interest Total InterestDirectors No. of Shares % No. of Shares % No. of Shares %

Tan Kay Kiang(1) 20,500,320 14.24 20,500,320 6.59 20,500,320 4.39Tan Chin Hoon(2) 16,265,310 11.30 16,265,310 5.22 16,265,310 3.48Tan Kay Tho(3) 19,925,310 13.83 19,925,310 6.40 19,925,310 4.27Tan Kay Sing(4) 25,525,420 17.73 25,525,420 8.20 25,525,420 5.47Tan Nan Choon 2,425,020 1.68 2,425,020 0.78 2,425,020 0.52Lee Eng Kian – – – – – –Gurdaib Singh s/o Pala Singh – – – – – –

Substantial Shareholders

Shining Holdings 13,950,420 9.69 13,950,420 4.48 13,950,420 2.99Citipoint Asia Real Estate Capital Ltd(5) – – 167,307,692 53.74 322,961,538(6) 69.16(6)

Other Shareholders(10) 101,209,880 70.28 101,209,880 32.51 101,209,880 21.67

Public Shareholders(11) 84,544,380 58.71 84,544,380 27.16 84,544,380 18.11

Notes:-

(1) As at the Latest Practicable Date, Tan Kay Kiang has a direct interest in 1,549,920 Shares. He is deemed to beinterested in the 13,950,420 Shares held by Shining Holdings Pte Ltd and the 4,999,980 Shares held by his wife, TaySwee Leng, by virtue of section 7 of the Companies Act.

(2) As at the Latest Practicable Date, Tan Chin Hoon has a direct interest in 314,910 Shares. He is deemed to beinterested in the 13,950,420 Shares held by Shining Holdings Pte Ltd and the 1,999,980 Shares held by his wife,Tjioe A Lan, by virtue of section 7 of the Companies Act.

(3) As at the Latest Practicable Date, Tan Kay Tho has a direct interest in 1,474,890 Shares. He is deemed to beinterested in the 13,950,420 Shares held by Shining Holdings Pte Ltd and the 4,500,000 Shares held by his wife,Yeong Yoon Ying, by virtue of section 7 of the Companies Act.

(4) As at the Latest Practicable Date, Tan Kay Sing has a direct interest in 11,025,000 Shares. He is deemed to beinterested in the 13,950,420 Shares held by Shining Holdings Pte Ltd and the 550,000 Shares held by his wife, SimMong Lan, by virtue of section 7 of the Companies Act.

(5) Citipoint Asia Real Estate Capital Ltd, which is the Subscriber under the Strategic Placement Agreement, is wholly-owned by Mr Nico Po Purnomo. Mr Nico Po Purnomo is therefore deemed to be interested in such number ofStrategic Shares and New Shares as may be held by the Subscriber by virtue of section 7 of the Companies Act.

(6) All the Warrants will be placed out to the Subscriber (or its nominee) on the terms and conditions of the Deed Pollafter Shareholders’ approval has been obtained at the EGM.

(7) The issued share capital of the Company before the allotment and issue of the Strategic Shares comprises144,000,000 Shares.

(8) Assuming that 167,307,692 Strategic Shares are allotted and issued, the issued share capital of the Company willcomprise 311,307,692 Shares.

(9) Assuming that 167,307,692 Strategic Shares and 155,653,846 New Shares are allotted and issued, the issued sharecapital of the Company will comprise 466,961,538 Shares.

(10) Refers to persons other than Directors, their respective spouses and Substantial Shareholders.

(11) Refers to persons other than Directors, Substantial Shareholders and their respective associates.

17

3.7 HLF has been appointed the IFA to the Independent Directors in relation to the ProposedWhitewash Resolution. The letter from HLF to the Independent Directors containing their advice isset out in Appendix 1 of this Circular.

4. THE PROPOSED SHINING IPT TRANSACTIONS

4.1 Details of the Proposed Shining IPT Transactions

(a) The Proposed Shining IPT Transactions are set out in the following agreements:

(i) the Business Transfer Agreement;

(ii) the Shop Unit Option Agreement;

(iii) the Deed of Mutual Covenants; and

(iv) the Deed of Covenant.

Under Chapter 9 of the Listing Manual, where a listed company proposes to enter into atransaction with its director, CEO or Controlling Shareholder (or any of their “associates”, asthat term is defined in the Listing Manual), Shareholders’ approval and/or an immediateannouncement is required in respect of that transaction if its value is equal to or exceedscertain financial thresholds. In particular, Shareholders’ approval is required where the valueof such transaction with any such persons is equal to or more than:

(A) 5% of the listed company’s latest audited NTA; or

(B) 5% of the listed company’s latest audited NTA, when aggregated with the value of allother transactions entered into with the same Interested Person during the samefinancial year.

As at the Latest Practicable Date, Shining Holdings and Shining Development areassociates of the Executive Directors. The shareholders of Shining Holdings are theExecutive Directors (each of whom owns approximately 21.8% of the issued share capital ofShining Holdings), Ms Tan Seok Luan and Ms Tan Siok Hwee (each of whom ownsapproximately 6.4% of the issued share capital of Shining Holdings).

Accordingly, the Proposed Shining IPT Transactions constitute interested persontransactions within the meaning of Chapter 9 of the Listing Manual.

Pursuant to Chapter 9 of the Listing Manual, HLF has been appointed as independentfinancial adviser to the Independent Directors to advise them on whether the ProposedShining IPT Transactions are on normal terms and whether the transactions are prejudicialto the interests of the Company and the minority Shareholders. The letter from HLF to theIndependent Directors in relation to the Proposed Shining IPT Transactions is set out inAppendix 1 of this Circular.

(b) The proposed divestment of the Hardware Business – Business Transfer Agreement:

The Company’s wholly-owned subsidiary, Builders Shop, carries on the Hardware Businessat six shop units in Singapore including at the Shop Unit.

Builders Shop has entered into the Business Transfer Agreement to sell the HardwareBusiness to Shining Holdings. Shining Holdings is controlled by the Executive Directors.

Accordingly, the proposed divestment of the Hardware Business is an interested persontransaction within the scope of Chapter 9 of the SGX-ST Listing Manual.

18

The Hardware Business comprises the distribution and retailing of hardware by the Groupas carried out by Builders Shop. After the divestment of the Hardware Business, it is theintention of the Subscriber that Builders Shop will continue to be involved in the import andagency for stones, tiles and marbles.

As the Subscriber does not presently intend to modify the scope of the other ongoingbusinesses carried on by the Group, the Group will also continue to engage in the followingactivities after the divestment of the Hardware Business:-

(a) construction;

(b) retailing and trading of furniture and home lifestyle products and design; and

(c) manufacture of furniture.

Major Transaction – Chapter 10 Of The Listing Manual

Pursuant to Chapter 10 of the Listing Manual (“Chapter 10”), if a listed company proposesto enter into a transaction where any of the relative figures computed on the bases set out inRule 1006 of Chapter 10 exceeds 20%, the transaction is classified as a major transactionthat requires approval by the shareholders of the listed company in general meeting. Thebases set out in the said Rule 1006 are as follows:-

(a) The net asset value of the assets to be disposed of, compared with the group’s netasset value. This basis is not applicable to an acquisition of assets.

(b) The net profits attributable to the assets acquired or disposed of, compared with thegroup’s net profits.

(c) The aggregate value of the consideration given or received, compared with theissuer’s market capitalisation.

(d) The number of equity securities issued by the issuer as consideration for anacquisition, compared with the number of equity securities previously in issue.

Applying the abovementioned bases of computation, the disposal of the Hardware Businessconstitutes a major transaction within the meaning of Chapter 10, thereby requiring theapproval of the Shareholders at the EGM. The computations are set forth below:-

Rule Bases Relative Figure

1006(a) The attributable net tangible assets of the Hardware Business 4.2 %is approximately $0.52 million as at 30 June 2007. The Group’s consolidated net tangible assets for the same period is approximately $12.4 million (taking into account the recently completed Rights Issue)

1006(b) For the half year ended 30 June 2007, the net profits attributable 48.7 %to the Hardware Business is $52,147. The Group’s net profits forthe same period is $107,000.

1006(c) The Consideration payable for the Hardware Business is the 1.9 %underlying net book value of approximately $0.52 million as at 30 June 2007. The Company’s market capitalisation as at 7 September 2007, being the market day prior to the signing ofthe Business Transfer Agreement is $28.1 million.

1006(d) The Consideration is payable in cash. Not Applicable

19

(c) Divestment details

Pursuant to the Business Transfer Agreement, Builders Shop shall sell, transfer and assignthe Hardware Business to Shining Holdings all rights, title and interests of Builders Shop inthe Hardware Business as a going concern and the assets owned by or under the control orin the possession of Builders Shop and used in the conduct of the Hardware Business.

All liabilities of Builders Shop in respect of the Hardware Business (including but not limitedto trade payables, other payables, finance leases and the obligations in respect of certainpremises leases) whether current, long term or contingent of Builders Shop as at 1 January2008 together with (but subject to completion) all such liabilities of Builders Shop from 1January 2008 down to the completion date shall be assumed by Shining Holdings.

Subject to completion of the Business Transfer Agreement, property in and title to theHardware Business and its assets to be transferred under the Business Transfer Agreementshall pass to Shining Holdings on 1 January 2008.

(d) Consideration payable for the Hardware Business

The consideration (“Consideration”) payable by Shining Holdings for the sale and transferof the Hardware Business and its assets is effectively the net tangible assets of the saidHardware Business as at 1 January 2008. Such net tangible assets shall be the sum that isequal to the net book values of the assets as recorded in the audited books of BuildersShop less the liabilities at their net book values being assumed by Shining Holdings.

The Consideration shall be satisfied by Shining Holdings paying at completion in cash toBuilders Shop according to the following schedule:-

(i) 20% of the Consideration on completion;

(ii) four equal payments of 20% of the Consideration at the end of each consecutivemonth in the four-month period following completion,

provided that the Consideration shall be based on the net book value set out in thecompletion accounts and in the event of dispute, the determination of the auditors of theCompany as expert shall be binding. In preparing the completion accounts, the auditors ofthe Company shall apply the same accounting policies and principles as that of prior years.

(e) Conditions Precedent

The completion of the proposed divestment of the Hardware Business is conditional upon:-

(i) all resolutions as may be necessary or incidental in relation to Builders Shop’s saleand transfer of the Hardware Business, having been passed at the general meeting ofshareholders of the Company or any adjournment thereof;

(ii) all necessary approvals being given and not having been withdrawn by the SGX-STfor the admission to the official list of the SGX-ST and the dealing and quotation ofthe Strategic Shares being issued pursuant to the Strategic Placement Agreement;

(iii) the simultaneous completion of the Strategic Placement Agreement, the proposeddivestment of the Hardware Business and the exercise of the purchase of the ShopUnit; and

(iv) all necessary consents or approvals of third parties, bankers, financial institutions orgovernmental or regulatory authorities having jurisdiction over the sale and transfer ofthe Hardware Business having been obtained.

20

If any one of the conditions precedent to the Business Transfer Agreement described aboveis not fulfilled or waived on or before the Cut-Off Date (or such later date as the Companyand the Subscriber may agree in writing), the Business Transfer Agreement shall de factocease and determine provided that any extension of time under the Strategic PlacementAgreement shall be deemed an extension made to the timeline under the Business TransferAgreement.

(f) Other salient terms

(i) Indemnity: Shining Holdings has agreed and undertaken to Builders Shop that it willindemnify Builders Shop against, and save it harmless from, all costs, proceedings,claims, demands and expenses (including legal fees on an indemnity basis) whichmay be incurred, made or threatened against Builders Shop and/or any loss ordamage suffered by Builders Shop as a result of or in connection with any act,neglect, default or omission on the part of Shining Holdings in respect of any of theassets or the business or the liabilities which Shining Holdings shall assume underthe Business Transfer Agreement or any breach by Shining Holdings of any of itsundertakings in the Business Transfer Agreement.

(ii) Premises Transfer: As part of the sale of the Hardware Business to ShiningHoldings, Shining Construction will by way of the Shop Unit Option Agreement selland convey the Shop Unit to Shining Holdings. With respect to the other premisesbeing leased by Builders Shop to carry on the Hardware Business, Builders Shop willeither procure for the novation, assignment or a sub-tenancy of these leasedpremises on the same terms and conditions to Shining Holdings for the remainingtenancy periods.

(iii) Employees: Upon completion of the Business Transfer Agreement, with effect fromthe Effective Date, Shining Holdings shall assume and be responsible for all debts,obligations and liabilities of Builders Shop pertaining to the employment of theemployees of the Hardware Business whether or not the employees shall haveaccepted employment with Shining Holdings including, without limitation, payment ofsalaries and wages, any taxes, accrued holiday pay, accrued bonus, Central ProvidentFund payments, contributions to retirement benefit schemes and all other costs andexpenses related to their employment as from and after the close of business on theEffective Date.

4.2 Divestment of Shop Unit and other tenancy arrangements – Shop Unit Option Agreement

(a) In connection with the sale of the Hardware Business, another integral transaction is thesale of the Shop Unit by Shining Construction (which is a sister subsidiary of Builders Shop)to Shining Holdings at the book value of the Shop Unit as recorded in the books of ShiningConstruction as at 31 December 2006.

(b) In respect of the lease over the Shop Unit, Shining Construction will by way of an optionexercisable by Shining Holdings (“Shop Unit Call Option”) within 3 months from theCompletion Date sell and convey the Shop Unit at its book value to Shining Holdings or asShining Holdings may nominate. Upon such conveyance and completion of the sale of theShop Unit, the lease over the Shop Unit with Builders Shop shall end.

(c) The consideration, which is the underlying net book value of the Shop Unit of $213,887 asat 31 December 2006, is 0.76% of the Company’s market capitalisation of $28.1 million asat 7 September 2007. The net book value of the Shop Unit is S$212,827 as at 30 June2007.

(d) In respect of the other tenancy arrangements which are between Builders Shop and othermembers of the Group for the Hardware Business, Builders Shop shall procure the novationand/or assignment of such other tenancy arrangements on the same terms and conditionsto Shining Holdings for the balance of the tenancy period.

21

(e) In addition, the Hardware Business requires the tenancy over 11 Changi South Street 3,#01-01, Singapore 486122 (the “Required Unit”) (in respect of which Builders Shop is themaster tenant). Builders Shop shall procure a sub-tenancy agreement over the RequiredUnit to be entered into in favour of Shining Holdings for a period of 3 years from completionof the Shop Unit Option Agreement and at the same rent.

(f) In respect of third party tenancy agreements, which are between Builders Shop and thirdparties, Builders Shop shall procure for the novation and/or assignment of the other tenancyagreements on the same terms and conditions to Shining Holdings for the remainder of thetenancy period.

(g) The Company has obtained a valuation on the Shop Unit from Knight Frank, who has valuedthe Shop Unit at S$800,000. A copy of the Valuation Certificate is attached as Appendix 2 tothis Circular.

4.3 Continued use of the name “Shining” by the Shining Entities – Deed of Mutual Covenants

(a) The Company and its subsidiary, Shining Construction (the ““A” Covenantors”) and ShiningHoldings and Shining Development which is also controlled by the Executive Directors (the““B” Covenantors”) have each been using the name “Shining” as part of its respectivename and/or for its respective business for a number of years and such use was in their ownrespective business and not confusing to the public or their customers.

(b) In contemplation of the Completion of the Strategic Placement Agreement whereupon thefuture businesses of the Company and the Group may change and as a result, possibleconfusion may happen, each of the covenantors has acknowledged that each can continueto use the name “Shining” in the same manner as they have done so previously except thatin the case of:

(i) the Company, the use shall be for a period of at most one (1) year after theCompletion of the Strategic Placement Agreement after which the Company shallchange its name and not use the name “Shining”;

(ii) Shining Construction, for an indefinite period after the completion of the StrategicPlacement Agreement provided that the name “Shining” is used in conjunction withanother name.

(c) In the event that the Company sells its present subsidiaries (the “Transfer”) or the Companydecides that the present subsidiaries shall cease, sells and liquidate their currentbusinesses and return their capital to the Company and thereby become dormant shells (the“Cessation”) then the Company shall do the following:

(i) in the case of the Transfer, the Company shall procure and offer for assignment by thesubsidiaries for a sum of S$10,000 in aggregate the names “Cream Homestore” and“Builders Shop” (as corporate names or other usages) to Shining Holdings or itsnominees;

(ii) in the case of the Cessation, the Company shall procure and offer for sale for a sumof S$10,000 in aggregate the subsidiaries Cream Homestore Pte Ltd and BuildersShop to Shining Holdings or its nominees on the basis that such subsidiaries areclean shells with no assets or liabilities save for their ownership of such names andtheir uses.

The Deed of Mutual Covenants is inter-conditional upon the performance of each of theProposed Transactions.

22

4.4 Novation or sub-contract of the Retro-Fitting Contract to Shining Holdings – Deed ofCovenant

(a) The Company through its subsidiary, Shining Construction, has submitted a tender for acontract value of approximately $30 million for the refurbishment of an industrial warehouse.The tender is currently pending award by the owner, AFP Warehouse Pte Ltd.

(b) In the event that the Proposed Transactions are completed, the Deed of Covenant providesthat the Retro-Fitting Contract shall be novated or sub-contracted in its entirety to ShiningHoldings or its nominees on the basis as if Shining Construction has not entered into theRetro-Fitting Contract. Both the economic benefit and losses in respect of the Contract shallbe transferred and belong to Shining Holdings.

4.5 Rationale for the Proposed Shining IPT Transactions

The Proposed Shining IPT Transactions are proposed to be entered into by Builders Shop andShining Construction in connection with the completion of the Strategic Placement Agreement.

As the Hardware Business would not be in line with the proposed future business direction of theCompany (which is to engage in property development in Singapore), the Company is proposing todispose of the Hardware Business through the Proposed Shining IPT Transactions.

5. MANDATE FOR THE COMPANY TO ENGAGE IN PROPERTY DEVELOPMENT IN SINGAPORE

5.1 The Company has been engaged in the supply of building materials to the construction relatedsector for a long time. The Company has a relatively small market capitalisation and a modestbalance sheet compared to larger construction-related companies.

5.2 It is the intention of Nico Po, who will be a controlling shareholder of the Company on Completion,for the Group to enter into the new business of high-end residential property development followingthe completion of the Proposed Placement.

It is believed that despite current uncertainties arising from the sub-prime concerns in the UnitedStates of America, prospects for high-end residential properties still remain attractive.GoldenFlowerGroup Real Estate had recently completed the en-bloc acquisition of residential landat 55 Devonshire Road. In order to position the Group with entry into the business of developmentof high-end residential apartments, injection of its residential land at 55 Devonshire Road into theCompany in future may be considered. Any asset injection will be subject to approval of theCompany’s Board and will be carried out in compliance with the applicable provisions of the ListingManual, including the requirements relating to interested person transactions.

5.3 In support of this future business direction, Nico Po intends to transfer experienced real-estateprofessionals based in Singapore from his private operations in Singapore to become seniormanagement of the Company. In addition, Po Sun Kok, who is the father of Nico Po and thechairman of GoldenFlowerGroup, the general name for a group of privately and separately ownedcorporations in Indonesia with over 10,000 employees, is proposed to be appointed as a non-executive chairman of the Company whilst Nico Po will be appointed as the managing director ofthe Company.

5.4 GoldenFlowerGroup Real Estate is currently developing an integrated development, Paragon City,in Semarang, Central Java, which would have a 1,000,000 square feet retail mall, a 250-room four-star hotel and convention facilities. The hotel and convention facilities will be managed by the Inter-Continental Hotel Group. The group also has land banks in Jakarta for offices, apartments and asix-star hotel. In Singapore, the group’s investment holdings includes MacDonald House, an officebuilding along Orchard Road, 51 apartment units at Suite@Central in the Orchard Road area. Onerecent successful project was the purchase, refurbishing and divestment of 135 Cecil Street(previously known as the LKN Building). A recent en-bloc acquisition of residential land at 55Devonshire Road positions the group with an entry into development of high-end residentialapartments.

23

5.5 In line with the future business direction, the Company is now seeking Shareholders’ approval toengage in property development in Singapore. For the further reasons discussed in Section 7below, it is anticipated that the Company’s participation in the property development sector withcash injection from the Subscriber will enhance the market capitalisation of the Company. TheCompany and the Group is not intending to engage in property investment holding.

5.6 GoldenFlowerGroup, with the benefit of its experience in real estate, will continue to seekopportunities for property development, both in Singapore and elsewhere, to raise the profile ofthe Group and enhance the intrinsic value of the Group. Upon the Shareholders’ mandate forproperty development being approved, Nico Po intends to engage primarily in residential propertydevelopment in Singapore exclusively through the Group.

6. APPOINTMENT OF PROPOSED NEW DIRECTORS

6.1 Pursuant to the terms of the Strategic Placement Agreement, the Subscriber proposes to nominateadditional directors to form a majority of the Board whose appointment is intended to take effectupon Completion. Nominees of the Subscriber will be appointed by the Board pursuant to theArticles of Association of the Company upon Completion of the Strategic Placement Agreement.

6.2 The current members of the Board (save for one Director who is representing the ExistingControlling Shareholders) will resign on Completion of the Strategic Placement Agreement. TheSubscriber and the current Board members will take the necessary steps to ensure that thecomposition of the Board meets the relevant best practices of corporate governance uponCompletion of the Strategic Placement Agreement.

6.3 The particulars of the new directors proposed to be nominated by the Subscriber as members ofthe Board are set out below.

Name Age Address Proposed Position

Nico Po Purnomo 26 9 Ardmore Park #11-01 Managing DirectorSingapore 259955

Po Sun Kok 59 Dr. Cipto 182 Semaran ChairmanCentral Java Indonesia

6.4 The Subscriber is a special purpose corporation incorporated in the British Virgin Islands on 1December 2006 which is wholly owned by Nico Po. Since the incorporation of the Subscriber todate, it has not entered into any transactions and thus has no substantial assets or liabilities todate.

Nico Po, aged 26, has been the Chief Executive Officer of GoldenFlowerGroup Real Estate sinceJanuary 2003 and has been involved in the property development projects undertaken andacquisition of investment properties by GoldenFlowerGroup Real Estate during the last 4 years.Nico Po holds a Bachelor’s Degree in Computing from the National University of Singapore.

6.5 Since founding the GoldenFlowerGroup in August 1981, Mr Po Sun Kok has helmed theGoldenFlowerGroup as Chairman and Chief Executive Officer. As GoldenFlowerGroup’s Chairman,he sets the GoldenFlowerGroup’s strategic direction and determines its financial and investmentdecisions. Mr Po Sun Kok has led the GoldenFlowerGroup through several pivotal chapters of itshistory including the GoldenFlowerGroup’s diversification into 3 main industries (apparelmanufacturing, banking and finance and real estate) and the international expansion of its realestate business.

24

7. RATIONALE FOR THE PROPOSED TRANSACTIONS

The Company has made an announcement on 30 July 2007 with regards to its future corporatedirection. Certain relevant extracts of the announcement are set out below:-

“Future Corporate Direction

The Directors further wish to make the following announcement regarding the future corporatedirection of the Company.

The Directors noted that although the Company has been in the building materials andconstruction related sector for a long time, the Company has a relatively small marketcapitalisation and a modest balance sheet when compared to larger construction-relatedcompanies. This would remain the case even after the proposed rights issue which is for a grossamount of S$2.88 million. Increasingly, with the bullish property market and the growing scale ofbuilding projects in Singapore, competitors with larger market capitalization and financial resourceswould have relative comparative advantages.

The Directors have reviewed and considered strategic ways to grow the market capitalization andthe balance sheet and resources of the Company. The Directors wish to announce that for theforeseeable future, the Company intends to pursue the following corporate possibilities:-

(i) to explore acquisition opportunities of substantial and viable property, construction orbuilding materials related businesses (such acquisitions would complement or leverage onthe existing business of the Group);

(ii) in the event that acquisition opportunities in such related areas are not possible or notavailable, to explore acquisition opportunities in other viable businesses; and

(iii) in connection with (i) or (ii) above, to issue as payment for such acquisition new shares ofthe Company.

…………………..It must be noted that a pursuit of such acquisition opportunities may result in avery major transaction or a reverse takeover under Chapter 10 of the Listing Manual.”

The Directors had prioritized, amongst others, property business in its 30th July 2007announcement because the Group’s current building material and construction businesses arecomplementary and supportive to property development activities. The Directors believe that theGroup has expertise in the construction of high-end or luxury apartment projects for third-partydevelopers. For example, it was reported in The Straits Times on 5 September 2007 that one ofthe condominiums built by the Group, namely One Moulmein Rise, was among the 9 winners ofthe 2007 Aga Khan Award for Architecture. In addition, the Group has an established andextensive capability in the sourcing of natural stones and tiles that are of quality and appealingdesigns that has recently seen growing demand from the high-end developers. For example, theGroup has supplied products to high-end residential projects such as St Regis Residences (by CityDevelopments Limited), the BLVD and The Marq (both by SC Global Developments Ltd).

The Directors believe that the resources and experience of Nico Po and of GoldenFlowerGroup,taking into account their experiences in real-estate in Indonesia, and their growing participation inthe Singapore real-estate market would benefit the Group in its future direction of residentialproperty development.

The overall outcome of the Proposed Placement and the proposed shareholders’ mandate forresidential property development would enable the Company to transform itself beyond merely asupporting and facilitating supplier and contractor to the property market to becoming a real estatedeveloper in its own right. The entry of Nico Po as a new controlling shareholder through theProposed Placement would increase the market capitalisation of the Company, and with thepotential of further increases in its financial resources in the future through possible exercise of theWarrants will enable the Company to better compete in the property development industry.

25

8. FINANCIAL EFFECTS