slide title educating supporting representing nama debtor business plan version 2 nama forum...

TRANSCRIPT

EDUCATING

SUPPORTING

REPRESENTING

www.charteredaccountants.ie

NAMA Debtor Business PlanVersion 2

NAMA FORUM Michele Connolly

29th March 2011

Holiday Inn, Ormeau Avenue, Belfast

2

AGENDA

Business Plan Version 2

1. Overview and Guidance Note

2. Detailed discussion of the specific requirements within Sections 1 – 9 and consideration of:

• What information is required?

• Key issues to be addressed?

Taxation

Executive Summary

Asset Strategies

NAMA Debtor Business Plan

Creditors

Non-NAMA

Facilities

Uncumbered Cash / Assets

Assets Transferred

Funding / WC Requirements

3

Business Plan VERSION 2 – OVERVIEW

NAMA requests the completion and submission of the following documentation:

A.NAMA Information Pack

B.NAMA Cashflow Model

C.Business Plan VERSION 2 – TEMPLATE

4

Business Plan VERSION 2 – OVERVIEW

What is it?

• The BPV2 template is a Microsoft Word template document

• It must be populated in full

• Debtors are encouraged to include any other information which is significant with respect to any portion of their business

• It should be completed with utmost good faith as it will be relied upon

5

Business Plan VERSION 2 – OVERVIEW

The primary purpose of the Business Plan is to:

1.Present a complete account of the Debtor’s entire financial affairs and present an asset value maximisation strategy; and

2.Provide a debt reduction strategy detailing how the Debtor plans to reduce its debt to NAMA

“The NAMA Information Pack and Business Plan Version 2 (BPV2) are designed to capture information relating to all assets and facilities relating to the Debtor irrespective of whether NAMA debt is outstanding in relation to the assets.”

6

OVERVIEW

Section 1 Executive Summary

Section 2 Corporate Overview &

Section 2 Details of Management Team/Employees

Section 3 Individual Asset Strategies

Section 4 Debtor Funding/Working Capital Requirements

Section 5 Unencumbered Cash/Assets Availability to Support Borrowings

Section 5 Information on any Assets Transferred in the last 5 years

Section 6 Taxation & Other Financial Costs

Section 7 Creditors & Litigation

Section 8 Non-NAMA Facilities

Section 9 Statement of Affairs

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

Section 3 Individual Asset Strategies

Section 4 Debtor Funding/Working Capital Requirements

Section 5 Unencumbered Cash/Assets Availability to Support Borrowings

Section 5 Information on any Assets Transferred in the last 5 years

Section 6 Taxation & Other Financial Costs

Section 7 Creditors & Litigation

Section 8 Non-NAMA Facilities

Section 9 Statement of Affairs

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

Section 1 Executive Summary

7

Section 2 – Corporate Overview & Details of Management Team/Employees

2.1 Company Overview

Provide a company overview, including an overview of the company strategy and a description of all activities undertaken by the Debtor

• Opportunity to “tell the story” of the business• Activities undertaken• Company Strategy (past and present)• Portfolio Overview

8

Section 2 – Corporate Overview & Details of Management Team/Employees

2.2 Operational Structure/Chart

A detailed operational structure/chart indicating how the business is managed and monitored

Operational structure / chart should outline the lines of responsibility for activities undertaken, and should reflect the “Management Team” roles and responsibilities outlined in Section 2.4 below.

Narrative should outline how the business is managed and monitored on a day to day basis for example:

•Who has responsibilities for identified activities/duties? •How are risks/opportunities identified and managed? •Are there clear lines of reporting and active management?

9

Section 2 – Corporate Overview & Details of Management Team/Employees

2.3 A Schedule of all subsidiaries and partial holdings of the Debtor

The schedule should indicate;

• the percentage ownership by the Debtor;

• names and percentage ownership interests for each other shareholder(s);

• a description of the role of the other shareholder(s) in the management or development of the property;

• whether the other shareholder(s) is/are a related party; and

• details of any disputes between the Debtor and the other shareholders

Subsidiaries/HoldingsDebtor %

OwnershipOther

Shareholders

Other Shareholders

% Ownership

Role of Shareholder

Related Party Any Disputes

Entity 1 100 n/a n/a n/a n/a n/a

Entity 2 50 John Smyth 50Passive

ShareholdingNo No

Entity 3 100 n/a n/a n/a n/a n/a

10

Section 2 – Corporate Overview & Details of Management Team and Employees

2.4 A list of Management Team/Board of Directors / Investment Committee

A list of the Management Team and Board of Directors indicating roles and primary responsibilities for all members of the management team

2.5 Details of lending by Debtor to officers, directors or key employees

2.6 Details of borrowing by officers, directors or key employees secured against assets of the Debtor

These details should include any borrowings that are guaranteed by, or secured against assets of, the Debtor.

2.7 Personal tax refunds, personal income and other gains to the UBO or related parties

11

OVERVIEW

Section 1 Executive Summary

Section 2 Corporate Overview

Section 2 Details of Management Team/Employees

Section 3 Individual Asset Strategies

Section 4 Debtor Funding/Working Capital Requirements

Section 5 Unencumbered Cash/Assets Availability to Support Borrowings

Section 5 Information on any Assets Transferred in the last 5 years

Section 6 Taxation & Other Financial Costs

Section 7 Creditors & Litigation

Section 8 Non-NAMA Facilities

Section 9 Statement of Affairs

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

Section 2 Corporate Overview

Section 2 Details of Management Team/Employees

Section 4 Debtor Funding/Working Capital Requirements

Section 5 Unencumbered Cash/Assets Availability to Support Borrowings

Section 5 Information on any Assets Transferred in the last 5 years

Section 6 Taxation & Other Financial Costs

Section 7 Creditors & Litigation

Section 8 Non-NAMA Facilities

Section 9 Statement of Affairs

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

Section 1 Executive Summary

12

Section 3 – Individual assets Strategies

• Provide summary information for all assets pledged as security for loans transferred to NAMA

NAMA has provided a preferred template for summary information

13

Section 3 – Individual assets Strategies

Individual Asset Strategy Sheet

Asset name / Address

Proposed Date of Disposal / Refinance:

Estimated Current Asset Value: Asset Reference:

1. Asset Description

2. Proposed Capital / Operational Expenditure Information

3. Value Maximising Strategy

4. Any Current Issues / Current Status

• Asset type‒ Residential / Commercial Property (Retail / Office / Warehouse/Mixed use)‒ Development Site (Residential / Offices / Retail / Mixed / Warehouse)• Size (sq ft / sq m)• For Development Asset – Planning status / Works to date / Requirements and timescale to completion)• For Investment Asset – Occupied? / Leases / Tenants / Tenure• Any other relevant information

• What is the value maximising strategy for the asset?‒ Built-out?‒ Refurbishment?‒ Hold?‒ Sell?• What is the rationale for this strategy?• Timescale to exit• Projected realisation at exit

• Catch all!‒ Any issues?‒ Any risks?‒ Current status?

• Development Assets – Include any development finance required (if any)‒ Built-out?• Investment Assets – Include any Redevelopment finance required and ongoing operational expenditure (if any) such as:‒ Refurbishment‒ Salaries‒ Fees (e.g. Agents)‒ Other overheads

14

OVERVIEW

Section 1 Executive Summary

Section 2 Corporate Overview

Section 2 Details of Management Team/Employees

Section 3 Individual Asset Strategies

Section 4 Debtor Funding/Working Capital Requirements

Section 5 Unencumbered Cash/Assets Availability to Support Borrowings

Section 5 Information on any Assets Transferred in the last 5 years

Section 6 Taxation & Other Financial Costs

Section 7 Creditors & Litigation

Section 8 Non-NAMA Facilities

Section 9 Statement of Affairs

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

Section 2 Corporate Overview

Section 2 Details of Management Team/Employees

Section 3 Individual Asset Strategies

Section 5 Unencumbered Cash/Assets Availability to Support Borrowings

Section 5 Information on any Assets Transferred in the last 5 years

Section 6 Taxation & Other Financial Costs

Section 7 Creditors & Litigation

Section 8 Non-NAMA Facilities

Section 9 Statement of Affairs

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

Section 1 Executive Summary

15

Section 4 – Debtor Funding/Working Capital Requirements

Detail all funding lines that will be required to implement the proper debt requirement strategy, identifying:

•Self funding and money recycling opportunities within the Group

4.1 Company / Group annual overhead requirements

•Provide rationale or justification for specific overheads if deemed necessary

Table 1 - Debtor Organisational Overhead Cash Flow Table

Group Overhead Costs 31-Dec-11 31-Dec-12 31-Dec-13 31-Dec-14 31-Dec-15 31-Dec-16 31-Dec-17 31-Dec-18 31-Dec-19 31-Dec-20 Total

Employees Costs (2,000) (2,060) (2,122) (2,185) (2,251) (2,319) (2,388) (2,460) - - (17,785)Directors Cost (3,000) (3,090) (3,183) (3,278) (3,377) (3,478) (3,582) (3,690) - - (26,677)Rent Office/Cost - - - - - - - - - - -Ground Rents - - - - - - - - - - -Other Fees (3,000) (3,090) (3,183) (3,278) (3,377) (3,478) (3,582) (3,690) - - (26,677)Total Group Overhead Costs (8,000) (8,240) (8,487) (8,742) (9,004) (9,274) (9,552) (9,839) - - (71,139)

Group Other Costs 31-Dec-11 31-Dec-12 31-Dec-13 31-Dec-14 31-Dec-15 31-Dec-16 31-Dec-17 31-Dec-18 31-Dec-19 31-Dec-20 Total

Property Maintenance Cost (4,000) (4,120) (4,244) (4,371) (4,502) (4,637) (4,776) (4,919) - - (35,569)Maintenance Capex (5,000) (5,150) (5,305) (5,464) (5,628) (5,796) (5,970) (6,149) - - (44,462)Insurance Not Recovered Though Service Charge(6,000) (6,180) (6,365) (6,556) (6,753) (6,956) (7,164) (7,379) - - (53,354)Miscellaneous Cost (7,000) (7,210) (7,426) (7,649) (7,879) (8,115) (8,358) (8,609) - - (62,246)JV Funding Requirements Cost (8,000) (8,240) (8,487) (8,742) (9,004) (9,274) (9,552) (9,839) - - (71,139)Travel Costs (9,000) (9,270) (9,548) (9,835) (10,130) (10,433) (10,746) (11,069) - - (80,031)Other Costs (13,000) (13,390) (13,792) (14,205) (14,632) (15,071) (15,523) (15,988) - - (115,600)Total Group Other Costs (52,000) (53,560) (55,167) (56,822) (58,526) (60,282) (62,091) (63,953) - - (462,401)

16

Section 4 – Debtor Funding/Working Capital Requirements

4.2 Project specific working capital requirements

4.3 Any other capital requirements

• Outline funding requirements by asset over timeTable 8A - Debtor Proposed Capital Expenditure Cash Flow by Asset

Anon Limited 31-Dec-11 31-Dec-12 31-Dec-13 31-Dec-14 31-Dec-15 31-Dec-16 31-Dec-17 31-Dec-18 31-Dec-19 31-Dec-20 Total

Total CAPEX Costs F 1 A 1 Principe Vergara Residential - - - - - - - - - - -Total CAPEX Costs F 1 A 2 Volador Helicopter - - - - - - - - - - -Total CAPEX Costs F 1 A 3 Alcala Shopping Centre (50,000) (50,000) (1,000,000) (5,000,000) (1,500,000) - - - - - (7,600,000)Total CAPEX Costs F 1 A 4 Aruto Soria Hotel - - - - - - - - - - -Total CAPEX Costs F 1 A 5 Castellana Office Block - - - - - - - - - - -

TOTAL CAPEX COSTS Facility 1 ANG 04615 (50,000) (50,000) (1,000,000) (5,000,000) (1,500,000) - - - - - (7,600,000)

Total CAPEX Costs F 2 A 1 Salamanca Hotel - - - - - - - - - - -TOTAL CAPEX COSTS Facility 2 JOS 04625 - - - - - - - - - - -

Total CAPEX Costs F 3 A 1 La Latina Gate - - - - - - - - - - -Total CAPEX Costs F 3 A 2 Turbo Executive Plane - - - - - - - - - - -Total CAPEX Costs F 3 A 3 Serrano Shopping Centre (50,000) (50,000) (1,000,000) (5,000,000) (1,500,000) - - - - - (7,600,000)Total CAPEX Costs F 3 A 4 Berlin Hotel - - - - - - - - - - -Total CAPEX Costs F 3 A 5 Segovia Office Block - - - - - - - - - - -

TOTAL CAPEX COSTS Facility 3 JOS 04625 (50,000) (50,000) (1,000,000) (5,000,000) (1,500,000) - - - - - (7,600,000)

TOTAL CAPEX COSTS (100,000) (100,000) (2,000,000) (10,000,000) (3,000,000) - - - - - (15,200,000)

Table 8B - Debtor Proposed Operational Expenditure Cash Flow by Asset

Anon Limited 31-Dec-11 31-Dec-12 31-Dec-13 31-Dec-14 31-Dec-15 31-Dec-16 31-Dec-17 31-Dec-18 31-Dec-19 31-Dec-20 Total

Total Operational Costs F 1 A 1 Principe Vergara Residential (351,000) (358,020) (365,180) (372,484) (879,934) - - - - - (2,326,618)Total Operational Costs F 1 A 2 Volador Helicopter (16,050) (16,600) (17,000) (17,400) (17,800) - - - - - (84,850)Total Operational Costs F 1 A 3 Alcala Shopping Centre - - - - (700,000) - - - - - (700,000)Total Operational Costs F 1 A 4 Aruto Soria Hotel (103,400) (108,600) (113,800) (119,000) (124,200) - - - - - (569,000)Total Operational Costs F 1 A 5 Castellana Office Block (410,700) (418,714) (426,868) (435,166) (543,609) - - - - - (2,235,057)

TOTAL OPERATIONAL COSTS Facility 1 ANG 04615 (881,150) (901,934) (922,849) (944,050) (2,265,543) - - - - - (5,915,525)

Total Operational Costs F 2 A 1 Salamanca Hotel (634,000) (648,000) (662,240) (676,725) (691,459) (706,448) (721,697) - - - (4,740,570)TOTAL OPERATIONAL COSTS Facility 2 JOS 04625 (634,000) (648,000) (662,240) (676,725) (691,459) (706,448) (721,697) - - - (4,740,570)

Total Operational Costs F 3 A 1 La Latina Gate (988,000) (1,007,740) (1,027,875) (1,048,412) (1,069,361) (1,090,728) (1,112,522) (1,334,753) - - (8,679,390)Total Operational Costs F 3 A 2 Turbo Executive Plane (182,500) (186,150) (189,873) (193,670) (397,544) - - - - - (1,149,737)Total Operational Costs F 3 A 3 Serrano Shopping Centre - - - - (700,000) - - - - - (700,000)Total Operational Costs F 3 A 4 Berlin Hotel (103,400) (108,600) (113,800) (119,000) (124,200) (129,400) (134,600) - - - (833,000)Total Operational Costs F 3 A 5 Segovia Office Block (410,700) (418,714) (426,868) (435,166) (543,609) (452,201) (460,945) - - - (3,148,203)

TOTAL OPERATIONAL COSTS Facility 3 JOS 04625 (1,684,600) (1,721,204) (1,758,416) (1,796,248) (2,834,713) (1,672,329) (1,708,067) (1,334,753) - - (14,510,331)

TOTAL OPERATIONAL COSTS (3,199,750) (3,271,138) (3,343,505) (3,417,023) (5,791,715) (2,378,777) (2,429,765) (1,334,753) - - (25,166,426)

17

Section 4 – Debtor Funding/Working Capital Requirements

• Provide justification for funding requirements (be specific)

• Is it essential for enhancing the value of the project/business?

• Is funding available under any committed facilities?

• Cost benefit analysis?

18

OVERVIEW

Section 1 Executive Summary

Section 2 Corporate Overview

Section 2 Details of Management Team/Employees

Section 3 Individual Asset Strategies

Section 4 Debtor Funding/Working Capital Requirements

Section 5 Unencumbered Cash/Assets Availability to Support Borrowings

Section 5 Information on any Assets Transferred in the last 5 years

Section 6 Taxation & Other Financial Costs

Section 7 Creditors & Litigation

Section 8 Non-NAMA Facilities

Section 9 Statement of Affairs

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

Section 2 Corporate Overview

Section 2 Details of Management Team/Employees

Section 3 Individual Asset Strategies

Section 4 Debtor Funding/Working Capital Requirements

Section 6 Taxation & Other Financial Costs

Section 7 Creditors & Litigation

Section 8 Non-NAMA Facilities

Section 9 Statement of Affairs

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

Section 1 Executive Summary

19

Section 5 – Unencumbered Cash/Assets Available to Support Borrowings and Information on any Assets Transferred in the last 5 years

With reference to the Unencumbered Assets if any listed in the Statement of Affairs in Section 9, please outline in this section how it is proposed to use these assets in support of current and proposed NAMA borrowings.

5.1 Details of all asset transfers

Details of all asset transfers (including sale) of group assets out of the Group entities that were undertaken during the past five years to the benefit of the UBO or their related parties

20

Section 5 – Unencumbered Cash/Assets Available to Support Borrowings and Information on any Assets Transferred in the last 5 years

5.2 Details of personal tax refunds, personal income and other gains

Details of any personal tax refunds, personal income and other gains applicable to the UBO, including his/her family and close associates.

5.3 Details of pension funds

Details of pension funds owned by or managed for the Debtor, the UBO (Ultimate Beneficial Owner), including his/her family and close associates.

5.4 Details of any tax refunds

Include tax refunds of any nature due or potentially due to the Debtor/Sponsor and expected receipt dates.

21

OVERVIEW

Section 1 Executive Summary

Section 2 Corporate Overview

Section 2 Details of Management Team/Employees

Section 3 Individual Asset Strategies

Section 4 Debtor Funding/Working Capital Requirements

Section 5 Unencumbered Cash/Assets Availability to Support Borrowings

Section 5 Information on any Assets Transferred in the last 5 years

Section 6 Taxation & Other Financial Costs

Section 7 Creditors & Litigation

Section 8 Non-NAMA Facilities

Section 9 Statement of Affairs

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

Section 2 Corporate Overview

Section 2 Details of Management Team/Employees

Section 3 Individual Asset Strategies

Section 4 Debtor Funding/Working Capital Requirements

Section 5 Unencumbered Cash/Assets Availability to Support Borrowings

Section 5 Information on any Assets Transferred in the last 5 years

Section 7 Creditors & Litigation

Section 8 Non-NAMA Facilities

Section 9 Statement of Affairs

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

Section 1 Executive Summary

22

Section 6 – Taxation & Other Financial Costs

In this section Debtors are required to detail any taxation/accountancy and other financial issues that should be factored into the individual property cashflows or the organisational cashflows within the NAMA Information Pack. This section outlines some suggested items that need to be considered and may need to be expanded upon depending on Debtor specific structures and issues.

6.1 Tax liabilities which currently exist and may potentially exist

Details of any tax liabilities particularly following the implementation of any asset value maximisation strategy. This asset value maximisation strategy is the strategy proposed for each asset as outlined by the Debtor in section 3.

6.2 Details of audits / investigations or disputes with the tax authorities

Details should be included of any of the above in the Republic of Ireland or any other jurisdiction and a high-level quantification of potential exposures. This should include any areas of possible dispute/investigation where the Revenue authorities of which the Debtor is aware but which has not yet commenced as well as a high-level quantification of the potential risk involved.

23

Section 6 – Taxation & Other Financial Costs

6.3 Details of the tax assumptions used in the preparation of the projections

Details should include the use of losses or particular reliefs which reduce the projected tax liability

6.4 Details of any properties “resting on contract”/CGT/SPV’s

Details should include impending stamp duty liabilities, inherent or rolled up CGT liabilities, SPVs, off-shore vehicles or other structuring arrangements entered into that could impact on saleability of individual properties or on ultimate sales proceeds that would be realisable on a change of ownership

6.5 All information regarding hedging in relation to any loans

These include swaps, options or any other derivatives. If hedging is used, present a proposed strategy to deal with these

24

OVERVIEW

Section 1 Executive Summary

Section 2 Corporate Overview

Section 2 Details of Management Team/Employees

Section 3 Individual Asset Strategies

Section 4 Debtor Funding/Working Capital Requirements

Section 5 Unencumbered Cash/Assets Availability to Support Borrowings

Section 5 Information on any Assets Transferred in the last 5 years

Section 6 Taxation & Other Financial Costs

Section 7 Creditors & Litigation

Section 8 Non-NAMA Facilities

Section 9 Statement of Affairs

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

Section 2 Corporate Overview

Section 2 Details of Management Team/Employees

Section 3 Individual Asset Strategies

Section 4 Debtor Funding/Working Capital Requirements

Section 5 Unencumbered Cash/Assets Availability to Support Borrowings

Section 5 Information on any Assets Transferred in the last 5 years

Section 6 Taxation & Other Financial Costs

Section 8 Non-NAMA Facilities

Section 9 Statement of Affairs

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

Section 1 Executive Summary

25

Section 7 – Creditors & Litigation

7.1 Details of the extent of current creditor pressure

This should include a schedule of all the outstanding creditors (aged creditor listing) and commentary on relationship and position/difficulties with each one.

Creditors

Counterparty DescriptionStandard

credit terms

Age of invoiceTotal

<30 days 31-60 days 61-90 days 90 days +

Total

26

Section 7 – Creditors & Litigation

7.2 Details of any insolvency or similar proceedings

Details should be included of any insolvency or similar proceeding that have already commenced or are expected to commence or have been threatened against the Debtor or the UBO and/or any group entities/assets, including any advice that has been given or details of any advice sought

7.3 Details of any court judgements that have been obtained against the UBO and/or any entity of the group

27

OVERVIEW

Section 1 Executive Summary

Section 2 Corporate Overview

Section 2 Details of Management Team/Employees

Section 3 Individual Asset Strategies

Section 4 Debtor Funding/Working Capital Requirements

Section 5 Unencumbered Cash/Assets Availability to Support Borrowings

Section 5 Information on any Assets Transferred in the last 5 years

Section 6 Taxation & Other Financial Costs

Section 7 Creditors & Litigation

Section 8 Non-NAMA Facilities

Section 9 Statement of Affairs

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

Section 2 Corporate Overview

Section 2 Details of Management Team/Employees

Section 3 Individual Asset Strategies

Section 4 Debtor Funding/Working Capital Requirements

Section 5 Unencumbered Cash/Assets Availability to Support Borrowings

Section 5 Information on any Assets Transferred in the last 5 years

Section 6 Taxation & Other Financial Costs

Section 7 Creditors & Litigation

Section 9 Statement of Affairs

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

Section 1 Executive Summary

28

Section 8 – Non-NAMA Facilities

8.1 A detailed summary of all facilities which have not transferred to NAMA

8.2 An outline of the strategy for the repayment of the non-NAMA facilities as laid out in 8.1

Facility IDFacility Name

Lending Institution

Total Facility

Opening Balance €

GuarantorPersonal

Guarantee Amount €

Total - -

29

Section 8 – Non-NAMA Facilities

8.3 Details of any cross-collateralisation between assets secured to NAMA and non-NAMA facilities

8.4 Details of all personal guarantees provided in relation to non-NAMA facilities

8.5 Details on any non-NAMA facilities that are in default

8.6 Details of any non-NAMA loan restructuring that is ongoing or has taken place in the last 2 years and details of revised terms negotiated

30

OVERVIEW

Section 1 Executive Summary

Section 2 Corporate Overview

Section 2 Details of Management Team/Employees

Section 3 Individual Asset Strategies

Section 4 Debtor Funding/Working Capital Requirements

Section 5 Unencumbered Cash/Assets Availability to Support Borrowings

Section 5 Information on any Assets Transferred in the last 5 years

Section 6 Taxation & Other Financial Costs

Section 7 Creditors & Litigation

Section 8 Non-NAMA Facilities

Section 9 Statement of Affairs

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

Section 2 Corporate Overview

Section 2 Details of Management Team/Employees

Section 3 Individual Asset Strategies

Section 4 Debtor Funding/Working Capital Requirements

Section 5 Unencumbered Cash/Assets Availability to Support Borrowings

Section 5 Information on any Assets Transferred in the last 5 years

Section 6 Taxation & Other Financial Costs

Section 7 Creditors & Litigation

Section 8 Non-NAMA Facilities

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

Section 1 Executive Summary

31

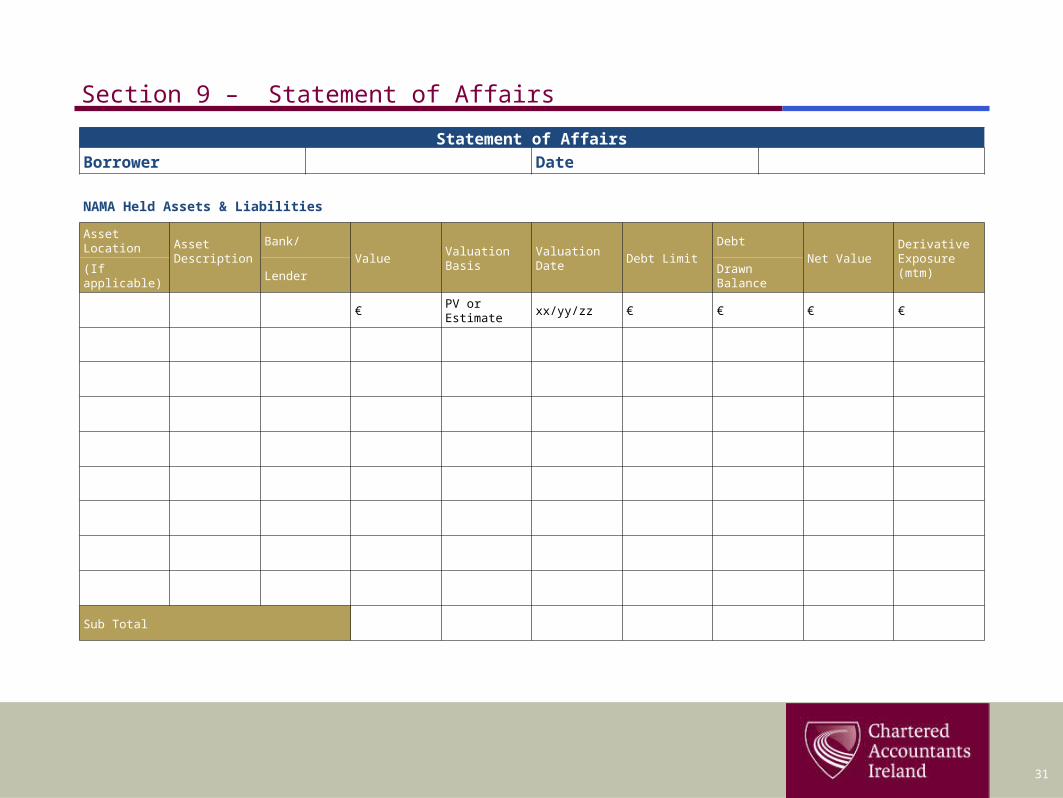

Section 9 – Statement of Affairs

NAMA Held Assets & Liabilities

Asset LocationAsset Description

Bank/

ValueValuation Basis

Valuation Date Debt Limit

Debt

Net ValueDerivative Exposure (mtm)(If applicable) Lender Drawn Balance

€ PV or Estimate xx/yy/zz € € € €

Sub Total

Statement of Affairs

Borrower Date

32

Section 9 – Statement of Affairs

NAMA Held Assets & Liabilities

Asset Location Asset

Description

Bank/Annual Income

Annual Debt ServicingProperty Costs

Surplus Cash

Debt Service Agreement

Debt Expiry Date

Derivative Expiry Date

OwnershipBorrower % Ownership(If

applicable) Lender InterestCapital Repayment

Total Commitment

€ € € € € €IRU / IO / C&I

Name of Legal Entity

%

Sub Total

33

Section 9 – Statement of Affairs

Other Bank/Lender Held Assets & Liabilities

Asset Location Asset

Description

Bank/Value

Valuation Basis

Valuation Date

Debt LimitDebt

Net ValueDerivative Exposure (mtm)(If applicable) Lender

Drawn Balance

€PV or Estimate

xx/yy/zz € € € €

Sub Total

Any Other Assets (& Liabilities) in Which Borrower (or related entity) Has Legal or Beneficial Interest

Asset Location Asset

Description

Bank/Value

Valuation Basis

Valuation Date

Debt LimitDebt

Net ValueDerivative Exposure (mtm)(If applicable) Lender

Drawn Balance

€PV or Estimate

xx/yy/zz € € € €

Sub Total

34

Section 9 – Statement of Affairs

Other Bank/Lender Held Assets & Liabilities

Asset Location Asset

Description

Bank/Annual Income

Annual Debt ServicingProperty Costs

Surplus Cash

Debt Service Agreement

Debt Expiry Date

Derivative Expiry Date

OwnershipBorrower % Ownership(If

applicable) Lender InterestCapital Repayment

Total Commitment

€ € € € € €IRU / IO / C&I

Name of Legal Entity

%

Sub Total

Any Other Assets (& Liabilities) in Which Borrower (or related entity) Has Legal or Beneficial Interest

Asset Location Asset

Description

Bank/Annual Income

Annual Debt ServicingProperty Costs

Surplus Cash

Debt Service Agreement

Debt Expiry Date

Derivative Expiry Date

OwnershipBorrower % Ownership(If

applicable) Lender InterestCapital Repayment

Total Commitment

€ € € € € €IRU / IO / C&I

Name of Legal Entity

%

Sub Total

35

Section 9 – Statement of Affairs

Unencumbered Assets, Including Pension Funds [see note 2 below]

Asset Location Asset

Description Value

Valuation Basis

Valuation Date

Annual Income

Property Costs

Surplus Cash OwnershipBorrower % Ownership

(If applicable) (If applicable)

€PV or Estimate

xx/yy/zz € € €Name of Legal Entity

%

Sub Total

36

Section 9 – Statement of Affairs

Other Income [All Other Income not Identified in Tables Above]

Income Source Income Amount Costs [If Any] Surplus Cash Income Duration Ownership

€ € € € €

Overall Connection Net Worth and Liquidity Position

Total Value Total Liability Net Value Total Income Total Repayment Total Property Costs Surplus Cash

€ € € € € € €

Contingent Liabilities (incl personal/corporate guarantees)

Nature of Contingent Liability

From To Amount Due DateExpiry Date

Status(if any)

State legal entity State Legal Entity € xx/yy/zz

37

Section 9 – Statement of Affairs

Other Liabilities

Nature of Other Liability From To AmountDue Date

(if any)

Tax State legal entity State Legal Entity € xx/yy/zz

Creditor State legal entity State legal entity € xx/yy/zz

Other (if other, please specify below)

Asset Transfers (To Third Parties, Other Than Arm’s Length Transactions in Good Faith to Independent, Unconnected Third Parties for Valuable Consideration at Full Open Market Value, in Past Five Years, including all Transfers to Family and/or Related Parties)

Asset LocationAsset Description

From To Value of AssetConsideration for Transfer

Date of Reason for TransferTransfer

Property, cash, shares in private cos etc

State legal entity State Legal Entity € xx/yy/zz

38

OVERVIEW

Section 1 Executive Summary

Section 2 Corporate Overview

Section 2 Details of Management Team/Employees

Section 3 Individual Asset Strategies

Section 4 Debtor Funding/Working Capital Requirements

Section 5 Unencumbered Cash/Assets Availability to Support Borrowings

Section 5 Information on any Assets Transferred in the last 5 years

Section 6 Taxation & Other Financial Costs

Section 7 Creditors & Litigation

Section 8 Non-NAMA Facilities

Section 9 Statement of Affairs

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

Section 2 Corporate Overview

Section 2 Details of Management Team/Employees

Section 3 Individual Asset Strategies

Section 4 Debtor Funding/Working Capital Requirements

Section 5 Unencumbered Cash/Assets Availability to Support Borrowings

Section 5 Information on any Assets Transferred in the last 5 years

Section 6 Taxation & Other Financial Costs

Section 7 Creditors & Litigation

Section 8 Non-NAMA Facilities

Section 9 Statement of Affairs

Section 10 Legal Considerations

Section 11 Reference Documentation

Appendix A Business Plan Version 2 – Guidance Note

39

EXECUTIVE SUMMARY

• Similar information requested by NAMA as in Version 1:

Loan facilities overview

Portfolio overview

Debt reduction plan

Proposed funding requirements

• Version 2 provides generic templates for presenting this information (to be extracted from NAMA Cashflow Model)

• Version 2 is more user friendly and easier for Debtors to respond to specific requirements

• Keep to NAMA structure but do include any other relevant information that is deemed pertinent to the overall Business Plan

40

EXECUTIVE SUMMARY

1.1 Introduction to the Debtor

1.1.1 General introduction to the history of the Debtor

1.1.2 Corporate overview / structure

• Opportunity to “tell the story” of the Debtor• Company history (including timeline)• Achievements to date, for example:

– Growth of the business– Successful developments and sales– Health and safety record

• Detail the reasons why the Debtor is best placed to manage and add value to the portfolio going forward

• Provide a summary of Sections 2.1 and 2.2 including:– Activities undertaken– Portfolio overview– Company strategy– Corporate structure– Strength of management team

41

EXECUTIVE SUMMARY

1.1.3 Number of employees (including Organisational Chart)

1.1.4 Details of annual business running costs

• Summary organisational chart showing management team and employees (based on section 2.2)

• Summarise roles and responsibilities, i.e. outline how the business is managed and monitored

• Debtor Organisational Overhead Cashflow Table

42

EXECUTIVE SUMMARY

1.2 Introduction to Debtor Loan Facilities (NAMA and non-NAMA)

Table 2 - Debtor NAMA Facility Groups

Facility IDFacility Name

Lending Institution

Sum of Total Facility

Opening Balance €

Value of Non-NAMA Debt Where

Syndicated €

Value of NAMA Debt Excl. Syndicated Non

NAMA Debt €Guarantor

Sum of Personal Guarantee Amount €

Facility 1 ANG 04615 ANGLO 15,000,000 7,500,000 7,500,000 0 -Facility 2 JOS 04625 BOI 15,000,000 - 15,000,000 0 -Facility 3 JOS 04625 AIB 15,000,000 - 15,000,000 0 -Total 45,000,000 7,500,000 37,500,000 -

Table 3 - Debtor Non NAMA Facility Groups

Facility IDFacility Name

Lending Institution

Total Facility Opening

Balance €Guarantor

Personal Guarantee Amount €

Total - -

43

EXECUTIVE SUMMARY

1.3 Portfolio Overview

This section should explain the geographic location and sector split of the Debtor’s facilities

Geographic

25,650,00057%

5,000,00011%

14,500,00032%

Pie Chart 1.1 - Global Portfolio Breakdown by Debtor Asset Value

Ireland

United Kingdom

Europe Excl. UK and Ireland 19,150,000

75%

6,500,00025%

Pie Chart 1.2 - Irish Portfolio Breakdown by Debtor Asset Value

Dublin

Limerick

5,000,00026%

14,500,00074%

Pie Chart 1.3 - International Portfolio Breakdown by Debtor Asset Value

United Kingdom

Europe Excl. UK and Ireland

44

EXECUTIVE SUMMARY

1.4 Consolidated Cashflow Section

This section should explain the Debtor's debt reduction strategy over the cashflow life.

• Connection consolidated Cashflow

• Asset Disposal / Refinancing Timetable Cashflow

• Asset Rental & Other Income Cashflow

45

EXECUTIVE SUMMARY

1.4.1 Debtor to provide a general summary of the projected debt repayment outcome proposed

• Provide a summary of proposed debt repayment plan, i.e.:

What is the strategy for debt repayment

– Sale of assets?– Development and sale of completed units?– Capital and interest repayment from income over time (cash sweep)?– Refinancing of existing liabilities?

• Narrative should outline:– Why the Debtor has chosen this proposed strategy– How it meets NAMA primary objective of debt reduction (i.e.

cummulative debt reduction @ years 3,5,7 etc)

Refer to section 1.5

46

EXECUTIVE SUMMARY

1.4.2 Debtor to identify any key issues / risks associated with achieving their proposed debt repayment targets

• For example:– Availability of finance (for proposed developments/re-developments)– Interest rate risk– Planning risk– etc.

47

EXECUTIVE SUMMARY

1.5 High level description of debt reduction projections

Debtor Debt Reduction Targets over 10 year period

Table 7 - Debtor Debt Reduction Targets over 10 year period

Total NAMA Debt 68,614,316

YearNet Debt (€

'000k)

Debtor Target Debt

Repayment %

2011 46,038,183 0.0%2012 47,202,099 0.0%2013 50,602,419 0.0%2014 62,408,767 0.0%2015 68,614,316 0.0%2016 38,787,738 43.5%2017 38,377,743 44.1%2018 8,816,736 87.2%2019 - 100.0%2020 - 100.0%

48

EXECUTIVE SUMMARY

1.6 Summary of all further proposed funding required for the implementation of the Debtor debt repayment strategy

Debtor in this section to Summarise all capital and operational expenditure required per asset as per information input into the NAMA Information Pack

• Debtor Proposed Capital / Operational Expenditure Cashflow by Asset

1.6.1 Provide a high level description of where capital is required for the implementation of the debt repayment strategy

1.6.2 Provide a summary of the Debtor’s current cash position and what capital is available to support capital and operational expenditure requirements

49

KEY CHANGES FROM ORIGINAL DEBTOR BUSINESS PLAN (VERSION 1)

• Templates provided are simplified and more “user-friendly”

• Revised report template allows for a more fluent presentation of the Debtor’s strategy and supporting information

• Reduced asset commentary required (particularly with respect to “non-NAMA” assets)

• No historic financial information is required

• Debtor is required to complete and certify a NAMA Statement of Affairs as part of their Business Plan

• Requirements relating to “Market Analysis” have been removed

• Majority of information required for the Executive Summary is automatically generated in the Cashflow Model

50

1. Debtor’s loans transferred to NAMA

2. NAMA issue a letter to Debtor, detailing: - NAMA Case officer assigned to Debtor - NAMA ID - Proposed deadline for receipt of Business Plan (usually

30 days)

3. Debtor Business Plan submitted to NAMA

4. Debtor Business Plan reviewed by NAMA and advisors (“Independent Reviewer”)

5. Proposal submitted to NAMA Credit Committee or Board for approval

Outcome of approval process will form the basis of the proposed asset(s) / funding strategy

6. NAMA issue a Memorandum of Understanding to Debtors which includes NAMA’s Proposed strategy for assets (including sales targets) and future funding presented to Debtors

Remaining TranchesTiming

?

?

Tranche 1-2Timing

30-50Days

2-4Months

7. Strategy agreed by both parties and then implemented

DEBTOR BUSINESS PLAN – NAMA PROCESS

? ?

?

?

2 – 4 Months

51

DEBTOR BUSINESS PLAN – KEY ISSUES

• Comprehensive Business Plan

• Address all requirements in full

• Start early, don’t underestimate the work involved

• Sell the Debtor to NAMA

• Assume no prior knowledge

• Attitude

52

DEBTOR BUSINESS PLAN – KEY ISSUES

• Identify the UBO(s)

• How many Business Plans?

• Identify all loans relating to UBO(s)

• Identify all assets relating to UBO(s)

• Develop outline strategy

• Submit queries / questions to NAMA

53

• Information and Communications

Borrowers are getting limited information on loan transfer process from their banks (i.e: which loans, when etc.); and

NAMA are also unwilling or unable to provide regular updates to borrowers until loans have actually transferred

• NAMA teams have significantly improved their responsiveness to Debtor specific Business Plan queries and questions

• NAMA will manage loans of top borrowers. Remainder will be managed on NAMA’s behalf by NAMA units in banks

DEBTOR BUSINESS PLAN – KEY ISSUES

54

Post NAMA’s Debtor Business Plan Review

•NAMA issue MOU

•Key elements of NAMA’s proposals likely to include a focus on:

Taking additional unpledged assets as security;

Taking unpledged cashflow streams as security;

Requiring spousal transfers to be reversed;

Requiring personal assets to be sold; and

Requiring investment properties to be disposed of.

•NAMA willingness to / ability to negotiate commercial deals?

DEBTOR BUSINESS PLAN – KEY ISSUES

55

CONCLUSION

• Submit a comprehensive Business Plan as required

• Demonstrate a willingness/appetite to fully engage with NAMA early

• Debtor Business Plan should propose and present a debt repayment schedule that assumes 100% par value of debt as starting position